Abstract

Companies grapple with the challenge of effectively managing the profound changes brought about by digital technologies. As companies seek to navigate these challenges, the role of chief digital officers (CDOs) has gained prominence, with increasing numbers appointed to lead digital initiatives. While extant literature has primarily explored CDOs’ roles and company-internal considerations, this study takes a market view, investigating the impact of CDO appointments on companies’ stock market value. Drawing on signaling theory and employing an event study with a comprehensive data sample of 307 CDO announcements and corresponding stock prices in the timeframe 2009-2020, this research delves into the conditions of CDO appointments influencing stock market reactions positively or negatively. The analysis considers the type of appointment and the power profile of CDOs, revealing nuanced insights into how these factors shape investors’ perceptions of a company’s future prospects. Furthermore, the study connects with the findings of chief information officer (CIO) research by systematically examining and contrasting reactions to CDO and CIO appointments across different timeframes. Overall, this study makes a significant contribution by disentangling competing and complementary signals CDO appointments may send regarding CDOs’ influence on organizations’ future prospects.

Keywords

Introduction 1

Existing Information Systems (IS) literature dealing with investors’ reactions to senior IS managers’ appointments has found that these are overwhelmingly perceived positively, as reflected by increased stock prices (Bandodkar and Grover, 2022; Chatterjee et al., 2001). Such appointments are argued to reflect changes in top management thinking and policy regarding the role of IT, and to communicate companies’ intentions to develop effective IT capabilities leading to a better competitive position, which in turn is valued by investors (Chatterjee et al., 2001). However, these findings from existing research are currently challenged in practice as well as research in IS and other research fields, such as management, for the following reasons.

First, the rich insights provided by existing research on central aspects of how and why changing a company’s top management landscape influences investors are based upon “presuppositions researchers make about a subject matter” (Rivard, 2014, p. vi). In recent years, these presuppositions have been challenged by the pervasiveness of digital technologies that are blurring the boundaries between previously separated functional entities such as business and IT departments and the respective senior managers responsible for them. Digital technologies have created unprecedented opportunities to transform how business is done in companies “in ways that go beyond the traditional capabilities of their IT” (Tumbas et al., 2018: p. 188). Thus, companies are forced to rapidly innovate, reconsider their business strategy and business models, and radically alter their internal structures (Hanelt et al., 2020; Vial, 2019), while facing direct competition from other industries or new ventures (Huang et al., 2017; Seo, 2017). This has created a need for new ways of managing the emerging opportunities and challenges in transforming organizations effectively (Lyytinen et al., 2016; Yoo et al., 2012).

Second, partly in response to the previous point, this fundamental shift in the role of IS has profound implications for the configuration of companies’ top management team and governance (Bharadwaj et al., 2013; Tumbas et al., 2018). These changes are reflected in an increasing number of companies appointing chief digital officers (CDOs) to take over the strategic responsibility for managing digital initiatives (Firk et al., 2021; Kunisch et al., 2022). Referring to existing research, appointing a CDO may be perceived as positive by investors. However, evidence from practice points to major challenges, too. Although introducing a CDO position is often accompanied by excitement and high expectations that may eventually drive the stock price, it also complicates the organizational chart, creates new interdependencies, is often expected to introduce quite large changes, leading to fierce resistance (Dhall and Kanungo, 2023), and ultimately dooms the CDO to failure making him or her a “Chief Depressed Officer” and eventually the “Chief Departed Officer” (World Economic Forum, 2020). Such development paths typically will not be perceived positively by investors.

Third, research in fields other than IS has identified several conditions under which investors’ reactions to senior management succession appointments are negative or insignificant, in contrast to IS studies that have identified positive reactions (Bandodkar and Grover, 2022; Chatterjee et al., 2001). Furthermore, unlike most IS studies that either examine new position appointments (Chatterjee et al., 2001) or do not distinguish between appointment types (Bandodkar and Grover, 2022), research in fields other than IS focuses on reactions to succession appointments (e.g., Brinkhuis and Scholtens, 2018; Gangloff et al., 2016). Succession appointments appear to behave quite differently than new position appointments, suggesting the need to distinguish between new position and succession appointments and highlighting the need to analyze both types of appointments.

We argue that the time is ripe to update our theoretical considerations on investors’ reactions to senior IS management appointments because the presuppositions of existing research increasingly constrain our ability to explain phenomena in the ongoing digitalization of reality. Therefore, we invite scholars to engage with our offer of an alternative way of thinking about how and why appointing CDOs in the burgeoning digital world will eventually lead to stock market reactions—in whatever direction.

In line with existing research, we consider CDO appointment announcements as strategic signals for investors (Zmud et al., 2010) that are used to assess the extent to which a company can effectively implement the goals of digital transformation and thus improve its future prospects. Going beyond existing research, we distinguish between signals based on mandatory information required by regulation (e.g., the US Securities Exchange Act of 1934) and those based on voluntary information. The basic idea is that companies have to issue appointment announcements that contain mandatory information, namely, the creation or retention of the position itself and the name of the appointed person. Companies also typically offer voluntary information to varying degrees, such as a CDO’s skills, experience, and organizational assertiveness. We argue that the stock market reactions, whether positive, neutral, or negative, to CDO appointments depend essentially on voluntary information. The collective judgment of investors is then reflected in the company’s market value, which is the company’s primary goal and the central measure of its financial health and reputation.

To structure the information provided by appointment announcements, we use three concepts of managerial power (Finkelstein, 1992). Information on structural power regarding a formal hierarchical position is often used in existing research to reflect the ability of managers to exert their will (Chen et al., 2010; Taylor and Vithayathil, 2018). Rarely used in existing research are expert power, characterized as a greater influence due to relevant knowledge and experience, and prestige power, denoting greater influence due to personal status. Namely, we argue that stock market reactions to CDO appointments are influenced by signals of CDOs’ prestige and expert power, which may play a prominent role and may be even more relevant than structural power due to the wide range of responsibilities for digital initiatives assigned to CDOs (Singh and Hess, 2017; Tumbas et al., 2018).

We therefore ask the following research question: What are the differential effects of structural, expert, and prestige power signaled by CDO new position and succession appointments on stock market reactions?

We draw on signaling theory (Spence, 1973) to explain how information disclosure regarding CDO appointments and CDOs’ power profile may reduce information asymmetries between companies and investors and send competing or complementary signals regarding companies’ future prospects. Competing signals (Connelly et al., 2011) convey incompatible information, creating incongruence and ambiguity (Paruchuri et al., 2021). In contrast, we define complementary signals as signals that reinforce each other by providing compatible, mutually confirming information, thus ensuring congruence (Paruchuri et al., 2021). Signals, which change the perception of a company’s future prospects among investors, then lead to imminent reactions on the stock market (Herbig and Milewicz, 1996; Moore and Chapman, 1992).

Using data from a comprehensive global sample of 307 press releases announcing unique CDO appointments and matching stock price data in the timeframe 2009 to 2020, our event study reveals conditions for positive and negative stock market reactions to CDO appointments, depending on the type of appointment and CDOs’ power profile. The event study method, an approach widely used in IS research (Bandodkar and Grover, 2022; Bose and Leung, 2013), allows us to isolate how strategically important organizational events, such as senior management appointments, affect investors’ expectations regarding company value and future cash flows in the short term.

In addition, to link and contrast our analyses with existing research that has mostly focused on the position of the chief information officer (CIO), rather than the CDO, we also collected data on CIO appointments for the timeframes (1) 1987-1998, the period also used by Chatterjee et al. (2001), and (2) 2011-2020, a period comparable to our sample of CDO appointments. The analyses reveal interesting shifts in how these roles are perceived by investors over time.

Overall, our study contributes to the literature on investors’ reaction to senior management appointments by examining CDOs’ appointment to new and existing positions and eliciting the conditions under which the appointment of a CDO can exert a positive as well as negative impact on the future prospects of the appointing company. For example, we show that the negative effect of succession appointments can turn positive for CDOs with company-external knowledge and an elite university degree. For new position appointments, we demonstrate that the overall positive stock market reaction effect can turn negative for CDOs with misaligned reporting lines and responsibilities, and CDOs possessing a too specialized education with a singular focus on either business or IT. Thus, we identify complementary and competing signals surrounding CDO appointments. We also reveal a distinct market perception of CDOs in comparison to CIOs in recent years, underscoring the diverging perception of both roles on the stock market.

In the following, we first present the theoretical foundation of signaling theory, introduce our research model, and derive the hypotheses. Next, we introduce the event study method by outlining the estimation method, summarizing the data and variables used, and discussing our method of analysis. Subsequently, we show our results by first depicting the overall stock market reaction to CDO new position and succession appointments and then presenting the results of the multivariate regression using different explanatory variables describing CDOs’ power profile to explain stock market reactions. We then discuss our main contributions. Finally, we present our study’s limitations, avenues for future research, and theoretical and practical implications.

Theoretical foundation and hypotheses development

In the following, we present the theoretical foundation of signaling theory. Subsequently, we give an overview of our research model and develop hypotheses to explore the link between CDO appointments and stock market reactions.

Signaling theory

Signaling theory argues that companies can use signals to diminish existing information asymmetries between two stakeholders (Spence, 1973, 2002). Originally derived from analyzing the labor market (Spence, 1973), signaling theory has been applied to the organizational context. Companies reduce information asymmetries by sending strategic signals that communicate previously unknown information to external stakeholders (Zmud et al., 2010). Signals, which change the perception of a company’s future prospects among external stakeholders, such as investors, lead to imminent reactions (Herbig and Milewicz, 1996; Moore and Chapman, 1992). Companies often rely on strategic signaling, which are actions that implicitly or explicitly indicate an organization’s motives, goals, and current situation, to influence the perception and behavior of stakeholders (Moore and Chapman, 1992). In this context, past research in the field of IS has studied the impact of IT investments on the market value of companies (Dehning et al., 2003; Dos Santos et al., 2012), or the appointment of senior managers (Chatterjee et al., 2001).

Using press releases, organizations signal intended actions to attract the attention of customers, discourage competitors, or signal future prospects to investors (Herbig and Milewicz, 1996; Zmud et al., 2010). In efficient financial markets, such as the stock market, investors respond to new information about a company by selling or buying shares in the company, depending on whether the new information elevates or lowers investors’ expectations about the company’s future (Fama, 1970; Herbig and Milewicz, 1996). The aggregate of investors’ reactions to a company’s announcement of new information influences the value of a company on the stock market.

Companies can credibly reduce information asymmetries if a signal is associated with costly strategic decisions so that no incentive exists to send dishonest signals (Connelly et al., 2011; Spence, 1973). Furthermore, credibility is only achieved if a signal is a reliable indicator of an underlying characteristic that affects the company’s ability to generate positive cash flow (Connelly et al., 2011). Credibility is also closely tied to expectations. If a signal contradicts stakeholders’ expectations, because the signaling company may not have the resources to meet those expectations, this will create uncertainty for stakeholders and reduce the company’s credibility (Gomulya and Mishina, 2017). Credibility is also affected when a company sends more than one signal to reduce information asymmetries. In that case, consistency across multiple signals is essential for effective stakeholder communication (Paruchuri et al., 2021).

Companies have often used the announcement of senior management appointments, such as CDOs in recent years, to reduce information asymmetries about their viability by disclosing the unobservable quality of their management team (Connelly et al., 2011). Consequently, signaling non-directly observable qualities of senior managers can include their education and prior work experience as indicators of their knowledge and skills that enable them to contribute positively to companies’ future prospects (Menz, 2012). For instance, for CIOs appointed to the board of directors, their recent work experience within a similar position signals the contribution they can bring to the appointing company (Bandodkar and Grover, 2022). Similarly, if a CDO appointment is expected to add value to companies and earn positive cash flows through effective management of and strategic focus on digital initiatives, the announcement of a CDO appointment is likely to attract the attention of a company’s shareholders and trigger stock market reactions. Such strategic signals are particularly likely to be closely followed by stakeholders if they are perceived to be credible (Connelly et al., 2011; Spence, 1973). As appointment announcements are costly due to the creation of a new position or the continuation of an existing position, and subject to close scrutiny due to the legal requirements involved, CDO appointment announcements can be assumed to be credible.

Research model

In the following, we first present an overview of our research model. We then derive six hypotheses about the relationship between CDO appointments and stock market reactions. To derive these hypotheses, we rely on signaling theory and build on C-level literature, which has focused on the CIO and, more recently, the CDO in the IS field.

Overview of research model

Our research model puts forth arguments based on signaling theory and uses concepts of managerial power to structure the information contained in appointment announcements that send strategic signals to investors. We distinguish between two types of signals that companies can send to reduce existing information asymmetries with external stakeholders: mandatory and voluntary signals. First, most financial market regulators require the ad hoc disclosure of senior management changes to stakeholders, which has led to the establishment of a norm for communicating all senior management changes, as these changes can affect the stock price of listed companies (Zmud et al., 2010). Consequently, ad hoc disclosure of senior management changes, that is, new position or succession announcements, represents a mandatory signal. For CDOs, we therefore first consider CDO appointments in general and differentiate between succession and new position appointments, as reflected in our research model.

Second, companies announcing a CDO appointment may choose to disclose additional information about the appointee's power profile to reduce information asymmetries between the company and outsiders (e.g., investors). Such information constitutes a voluntary signal to reveal the non-directly observable characteristics of the appointed manager, such as their professional competencies and hierarchical position, and sends a positive signal about their ability to generate positive cash flows. For instance, voluntarily disclosing appointees’ membership in the top management team (TMT) reveals their potential to influence organizational decision-making and strategy (Feng et al., 2021), thereby reducing information asymmetry between investors and companies.

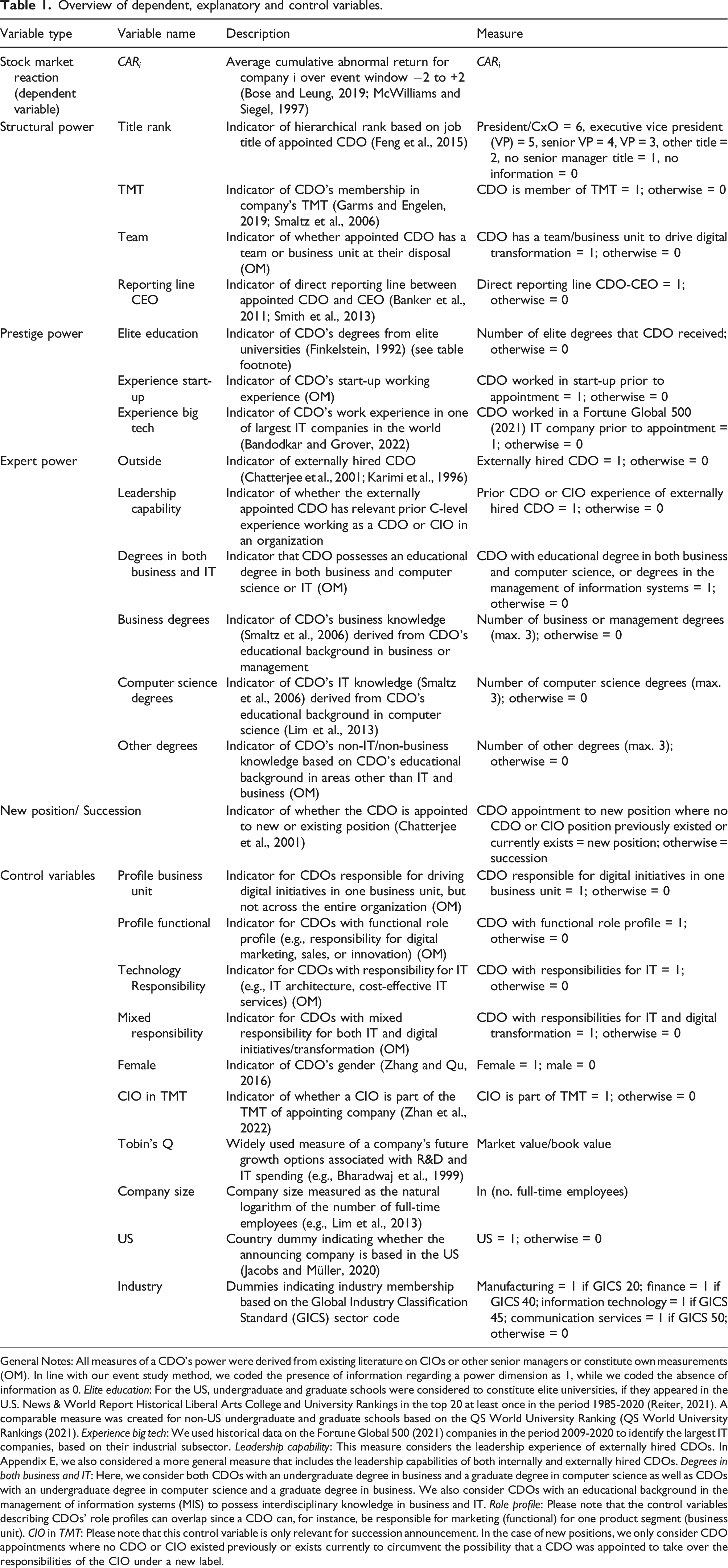

We use the conceptual lens of managerial power to study such voluntary signals contained in appointment announcements in a structured way and to analyze the link between CDOs’ profiles and stock market reactions (briefly referred to as market reactions). Managerial power is a prominent lens used in research (see Table A1 in Appendix A for a detailed overview). 2

Managerial power (also referred to as power) is defined as “the capacity of individuals to exert their will” (Finkelstein, 1992: p. 506), that is, the ability of managers to follow through with their plans. It is attained by senior managers who can deal with internal and external uncertainty, both due to their ability and position (Finkelstein, 1992; Thompson, 1967). Focusing on strategic decision-making power, Finkelstein (1992) differentiates between structural, prestige, and expert power, 3 for which he develops measurements and demonstrates their reliability and validity. These three concepts can serve as signals that are issued voluntarily in the context of signaling theory and are reflected in our research model accordingly. Structural power is defined as senior managers’ authority derived from their position within the organization’s formal structure or hierarchy (Finkelstein, 1992; Hambrick, 1981). Structural power can act as voluntarily disclosed information of a senior manager’s influence and decision-making authority. In appointment announcements, this includes, for instance, information regarding the appointee’s hierarchical position, which may reveal the weight of the appointee’s role within the company. Prestige power is the influence that results from senior managers’ prestige or status due to their high standing or personal relationships with influential people (Finkelstein, 1992). In appointment announcements, information on appointees’ relationship to renowned institutions or companies may reflect this power dimension. Companies may voluntarily reveal such information to heighten the external perception of appointees’ credibility and perceived competencies. Expert power is defined as senior managers’ ability to cope with environmental contingencies by drawing on their relevant knowledge and experience (Finkelstein, 1992; Hambrick, 1981). Information on appointees’ skills and experiences forms part of this concept. Signaling such information may reassure investors of the appointee’s capability in fulfilling their role successfully. Thus, we interpret the disclosure of structural, expert, and prestige power in appointment announcements as voluntary signals meant to lower information asymmetries by showcasing the appointee’s potential impact and alignment with strategic goals. Finally, we consider the stock market reaction as the dependent variable.

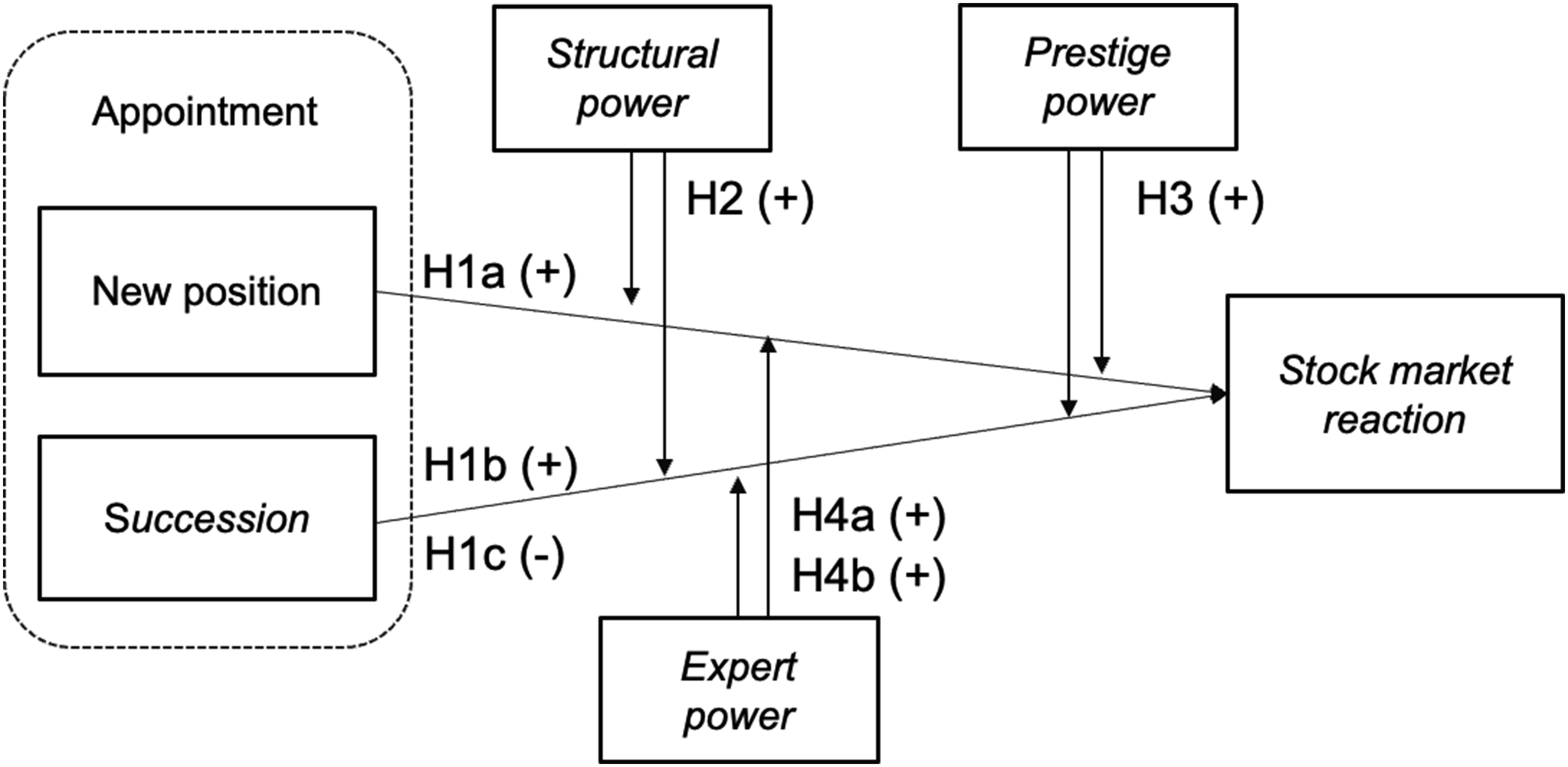

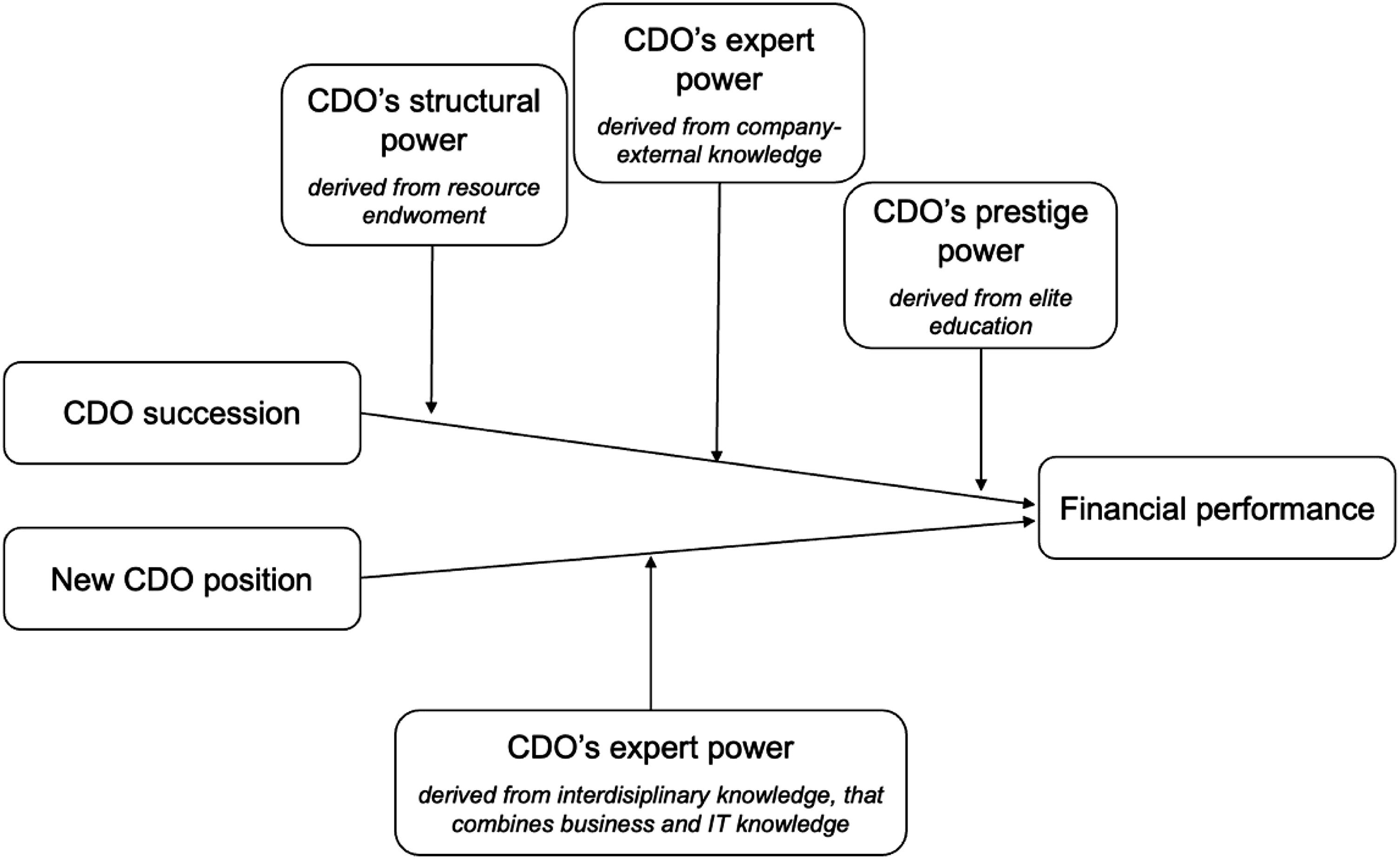

Figure 1 gives an overview of the hypotheses we derive below. Research model.

Hypotheses development: CDO appointments and stock market reactions

Generally, prior research agrees that announcements of senior management changes, especially newly created positions, are recognized as essential signals of change by investors (Chatterjee et al., 2001; Gangloff et al., 2016). As a result, they lead investors to buy or sell stock depending on their positive or negative perception of the senior management change, which results in rising or falling stock prices and aggregates in a market reaction. To develop hypotheses about the mandatory signals of CDO appointments, where companies are required by regulation to release ad hoc information about senior management changes to reduce information asymmetry with investors, we build on contrary empirical evidence regarding the market reaction to senior management appointments (e.g., Arora et al., 2020; Chatterjee et al., 2001). Below, we hypothesize the possible contrary signals that CDO appointments send and their different effects on market reactions, depending on whether CDOs are appointed to new or existing positions.

We turn first to the relationship between CDO appointments to newly created positions and market reactions as one mandatory signal that companies can send. Studies have shown that the market reacts positively to senior management changes when they are perceived as signals of change or strategic redirection (Gangloff et al., 2016; Huson et al., 2004). This is particularly true for CIO appointments to new positions, where the appointment can signal a strategic shift to make IT a strategic asset (Chatterjee et al., 2001). Similarly, concerning the appointment of CDOs to new positions, we argue that companies’ announcements send a costly, strategic signal to investors (Spence, 1973; Zmud et al., 2010) that these companies are promoting digital initiatives and transforming mindfully (Swanson and Ramiller, 2004; Tumbas et al., 2018). This signal conveys that CDOs play a key role in orchestrating and managing companies’ digital transformation by acting as entrepreneurs, digital evangelists, and coordinators, while typically not assuming functional IT responsibility (Singh and Hess, 2017). Thus, by appointing a CDO to a newly created position, companies signal that they are working towards implementing a viable digital business strategy and launching new digital initiatives (Singh et al., 2020; Tumbas et al., 2017). Accordingly, CDO new position appointments send a credible strategic signal (Zmud et al., 2010) of companies’ intention to focus on the challenges of digital transformation and to implement major changes to modernize their digital presence. This reflects companies’ future digital capabilities and improved future prospects, which will subsequently lead to a short-term stock market reaction. We thus hypothesize:

A signal conveying a CDO appointment to a newly created position is associated with a positive stock market reaction. We now turn to the link between CDO succession appointments and market reactions, as a second mandatory signal that companies can send. Existing studies find mixed evidence, including positive, negative, and insignificant effects of senior manager succession announcements on the stock market (e.g., Brinkhuis and Scholtens, 2018; Gangloff et al., 2016; Huson et al., 2004). This mixed effect can be attributed to two divergent signals contained in a succession announcement, namely, regarding (1) the position and (2) the appointee (Beatty and Zajac, 1987). First, regarding the position, a CDO succession appointment signals that a company has made the strategic decision to retain the CDO position and continue its efforts to drive digital transformation forward. Given that digital transformation has been characterized as a sustained, long-term process requiring significant organizational and technological change (Vial, 2019), a succession announcement may be perceived as a repeated signal of a company’s commitment to its strategic direction to drive and orchestrate digital initiatives. Such a repeated signal may be perceived favorably by investors, as it prominently reminds stakeholders of the company’s continued commitment to the ongoing digital transformation, which can be linked to positive expectations regarding future cash flows (Rindova et al., 2005; Worrell et al., 1993). Second, regarding the appointee, a succession announcement signals the appointment of a new senior manager to an existing position. Senior management changes are often perceived as disruptive events, since a new manager may implement a new strategic direction, make different decisions, and have diverging risk attitudes (Berns and Klarner, 2017). For example, Beatty and Zajac (1987) find that stock markets react negatively to CEO successions because they are perceived as disruptive events with potentially negative consequences. Recent research suggests that the disruptive signal of chief executive officer (CEO) and chief financial officer (CFO) successions may be exacerbated, resulting in more pronounced negative market reactions, when accompanied by a gender change due to differences in leadership styles between men and women (Zhang and Qu, 2016). Building on these findings, we argue that the announcement of a new appointee to the CDO position might introduce uncertainty and signal risk, leading to negative market reactions. Depending on whether investors perceive a stronger positive signal from the position, indicating the continuity in digital transformation efforts, or a stronger negative signal, because a new appointee is perceived as disruptive, the overall impact of a CDO succession announcement on the stock market may vary. Therefore, we derive the following alternative hypotheses:

A signal conveying a CDO appointment to an existing position (succession) is associated with a positive stock market reaction.

A signal conveying a CDO appointment to an existing position (succession) is associated with a negative stock market reaction.

Hypotheses development: CDOs’ power profile and stock market reactions

We now turn to the moderating effect of CDOs’ power profiles, which are conveyed through voluntary signals. With respect to the effectiveness of a senior manager appointed to a new or existing position, information asymmetry exists ex ante: The appointing company knows more than investors about the appointee’s power profile, which may indicate the appointee’s qualities (e.g., experience, education) and hierarchical position (Connelly et al., 2011; Spence, 1973). Companies may choose to strategically disclose information about an appointee’s power profile to reduce information asymmetries and voluntarily signal a manager's competencies relevant to the position, if they expect that investors will positively perceive this additional information (Connelly et al., 2011). 4 Looking at the stock market, we argue that investors’ reaction will depend on whether the signal is credible regarding their perception of the appointee’s ability to initiate or continue the company’s digital transformation efforts.

The voluntary signal of a CDO’s power profile is sent together with the mandatory signal of a senior management change (see previous subsection). We hypothesize that voluntary signals regarding an appointee’s qualities as a CDO, reflected in information about structural, expert, or prestige power, positively moderate the relationship between CDO appointments to new and existing positions and the market reaction, as depicted in Figure 1. According to Baron and Kenny (1986, p. 1174), a moderator is a “variable that affects the direction and/or strength of the relation between an independent or predictor variable and a dependent or criterion variable.” For new positions, a strong power profile, indicating structural, prestige, and expert power, may credibly signal the potential of the appointed CDO in initiating and driving digital transformation and contributing to the company’s financial success. Consequently, the positive effect of CDO new position appointments on the market reaction will be reinforced (H1a), since the strong power profile of the CDO amplifies the signal of change and strategic redirection, which is positively perceived by investors (Gangloff et al., 2016; Huson et al., 2004).

For successions, we previously hypothesized a positive or negative market reaction (see H1b/1c). On the one hand, a CDO succession appointment may be viewed positively by investors, if it signals the company’s continued commitment to digital transformation efforts (Rindova et al., 2005). Similar to our argument for new positions, a strong power profile could amplify this positive market reaction following a CDO succession appointment (H1b). Succession appointees with a strong power profile are likely to be perceived as capable of successfully driving the company’s ongoing digital transformation initiatives, for instance, due to their decision-making authority and influential network. On the other hand, the appointment of a CDO successor may be associated with a negative market reaction, if it is interpreted as a disruptive event, potentially signaling a change in direction or divergent risk attitudes introduced by the new appointee (Berns and Klarner, 2017). In this situation, a strong power profile may dampen or even reverse the negative market reaction following a CDO succession announcement (H1c). For example, an appointment that is perceived as disruptive may be viewed less negatively if the appointee demonstrates the expertise and knowledge necessary to successfully manage digital transformation.

CDOs’ Structural Power and Stock Market Reactions

Structural power, as a formal right to exert influence that stems from managers’ hierarchical position, allows senior managers to control their subordinates’ actions and gives them access to more resources (Finkelstein, 1992; Hambrick, 1981). When such power is disclosed in appointment announcements, it can function as a voluntary signal. This reduces information asymmetries between the company and external stakeholders, particularly investors. Specifically, it reveals that the appointee has the formal authority to enact strategic change and to influence companies’ fortunes (Finkelstein, 1992). As a result, the appointment of senior managers with structural power can reinforce positive perceptions of appointments that are viewed as companies’ persistent efforts to drive digital transformation or, alternatively, weaken or reverse negative perceptions of appointments that are viewed as disruptive managerial changes.

Existing literature on CIOs identifies structural power as an essential success factor for CIOs’ exploration of IT-enabled business opportunities, which contribute to strategic growth and company effectiveness (Chen et al., 2010). CIOs with structural power are well-positioned to build potent relationships with other TMT members and company stakeholders, providing them with opportunities to drive strategic activities (Carter et al., 2011). CIOs’ level of structural power has also been linked to IS strategic alignment (Preston and Karahanna, 2009), higher quality of IT governance (Bradley et al., 2012), and better long-term performance (Feng et al., 2021). Drawing on these studies, we argue that the appointment of a CDO positioned at a high hierarchical level and, therefore, equipped with the influence and resources required to drive digital transformation (Tumbas et al., 2018) will signal to stakeholders the appointee’s ability to orchestrate digital initiatives effectively. This is especially the case because the ensuing change in the management structure or the provision of resources is costly, making the signal credible (Spence, 1973). Consequently, the voluntary signal of a CDO’s structural power indicates better company prospects and positively influences investors’ perception of a CDO appointment. Therefore, we hypothesize:

Signals of an appointed CDO’s structural power positively moderate the relationship between a CDO appointment and the stock market reaction.

CDOs’ Prestige Power and Stock Market Reactions

Prestige power, that is, the influence resulting from senior managers’ status and association with respected institutions (Finkelstein, 1992), can serve as an important signal in appointment announcements. Senior managers with prestige power are often well-positioned to deal with uncertainty, as their influential network may grant them early access to critical information about environmental contingencies. By disclosing an appointee’s association with a highly respected institution (e.g., elite university) and the resulting powerful connections (Finkelstein, 1992; Rindova et al., 2005), companies can reduce information asymmetries between the company and investors about appointees’ qualities and future behavior (Connelly et al., 2011). Accordingly, managers with prestige power may reduce stakeholders’ perceived uncertainty about a company based on these managers’ ability to manage environmental contingencies, thereby dampening the potentially negative effect of disruptive appointments or enhancing the positive perception of appointments associated with ongoing transformation efforts.

In line with this, D'Aveni (1990) argues that stakeholders carefully monitor signals regarding TMT members’ prestige power, for instance, by considering whether they earned degrees from prestigious universities, since it may indicate managers’ ability to manage uncertain situations using their influential network. Additionally, prestigious TMT members have been shown to form relationships with influential external stakeholders more easily, which is linked to higher organizational performance (Higgins and Gulati, 2003; Stuart et al., 1999). Furthermore, managers with prestige power may be able to demand higher compensation, as the existing literature finds a wage premium for elite university education (Anelli, 2020). This makes appointing managers with prestige power more costly, and thus, the signal sent more credible. Based on these findings, we argue that appointing CDOs with prestige power sends a costly signal to investors that a CDO may be well positioned to manage the risk and uncertainty associated with organizational change related to digital transformation. We hypothesize:

Signals of an appointed CDO’s prestige power positively moderate the relationship between a CDO appointment and the stock market reaction.

CDOs’ Expert Power and Stock Market Reactions

Expert power, defined as senior managers’ ability to cope with environmental contingencies by drawing on deep knowledge and relevant experience (Finkelstein, 1992), can serve as a powerful, voluntary signal of appointees’ competencies. Senior managers with expert power are often influential in shaping strategic choices and thereby impact an organization’s external perception, since they are frequently sought out for advice, and their advice is more readily accepted (Finkelstein, 1992; Tushman and Scanlan, 1981). Given that digital transformation constitutes a complex process characterized by multiple contingencies and high uncertainty (Drechsler et al., 2020; Vial, 2019), expert power may be especially decisive for CDOs. By highlighting a CDO’s expert power across relevant domains, companies can voluntarily signal that the appointee is well equipped to lead the company’s transformation efforts. Consequently, companies can decrease investors’ perceived uncertainty about a company through the reduction of information asymmetries between investors and the company. Thereby, they can mitigate the potentially negative perception of a disruptive appointment or reinforce the positive effect of an appointment that is perceived as a continuation of a company’s long-term transformation efforts.

In summary, based on signaling theory, signals that convey CDOs’ expertise are perceived positively by investors. The literature suggests that we can further specify the source of expert power that moderates the relationship between CDO appointments and stock market reactions. Accordingly, we derive two specific hypotheses in the following paragraphs.

CDOs, acting as digital harmonizers or coordinators, must possess a broad understanding of a company’s business to align different business units and functions and weaken organizational silos to successfully implement digital initiatives (Singh and Hess, 2017; Tumbas et al., 2017). However, investors do not inherently possess knowledge about CDOs’ abilities to manage and integrate diverse knowledge or collaborate across functions. According to signaling theory (Connelly et al., 2011; Spence, 1973), the disclosure of information regarding the educational background of appointees can serve as a signal to investors. In the case of the CDO, it may reduce information asymmetries by indicating the CDO’s capability to share and integrate different types of knowledge and effectively collaborate across functions and business units.

In that regard, existing research on CIOs shows that an extensive IT background combined with a business orientation leads to a higher quality relationship between the CIO and the TMT (Preston et al., 2008). Additionally, companies pay significant compensation premiums for IT professionals with an MBA compared to other degrees (Mithas and Krishnan, 2008). Due to such compensation premiums, hiring a manager with an interdisciplinary educational background may be costly. Accordingly, we argue that appointing a CDO with an interdisciplinary educational background that combines business and IT knowledge may send a positive and credible signal to investors. Therefore, we hypothesize:

Signals of an appointed CDO’s expert power derived from knowledge in both business and IT positively moderate the relationship between a CDO appointment and the stock market reaction. Apart from knowledge in both business and IT, the disclosure of CDOs’ company-external knowledge might reduce information asymmetries and send a positive strategic signal to investors. CDOs appointed from the outside are equipped with another source of expert power because they have gained extensive knowledge and experience regarding digital transformation in other contexts. They may have demonstrated their ability to navigate complex organizational challenges and implement digital strategies successfully. This includes gaining experience in influential positions (e.g., C-level) in other companies, which plays a crucial role in developing leadership capabilities (McCall, 2004). Thus, appointees’ experience as senior managers may credibly signal leadership capability in driving digital transformation initiatives. Moreover, senior managers hired from the outside can judge the company’s current state more objectively than insiders with political and personal loyalties and agendas (Chatterjee et al., 2001; Hambrick and Finkelstein, 1987). Prior research also indicates that external hires may signal strategic change (Schepker et al., 2017), an essential aspect of digital transformation, where companies face changing competitive landscapes due to the disruptive nature of digital technology (Bharadwaj et al., 2013). Furthermore, since external hires earn a higher salary than internal hires (Bidwell, 2011), appointing a CDO from outside may be more costly and, thus, send a credible signal to investors. Accordingly, we put forth the following hypothesis:

Signals of an appointed CDO’s expert power derived from company-external knowledge positively moderate the relationship between a CDO appointment and the stock market reaction.

Event study method

To test our research model empirically, we adopted an event study method and measured the short-term impact of announcing a CDO appointment on a company’s equity on the stock market. The impact of CDOs on organizational performance is generally hard to isolate due to numerous other organizational and environmental factors that may impact this relationship. Applying an event study to measure the link between CDOs’ appointment and the market reaction can circumvent such problems. By conducting an event study, we can isolate and measure the effect of an unexpected event based on changes in the stock price (Fama, 1970; McWilliams and Siegel, 1997). The event study method has been widely used in IS literature and applied in various contexts, such as the adoption of identity theft countermeasures (Bose and Leung, 2019), the establishment of new CIO positions (Chatterjee et al., 2001), the appointment of CIOs with prior experience in a similar position to the board of directors (Bandodkar and Grover, 2022), IT failures (Bharadwaj et al., 2009), and transformational IT investments (Dehning et al., 2003). We closely followed the approach of these earlier event studies and took existing guidelines for conducting event studies into account (McWilliams and Siegel, 1997).

In conducting the event study, we undertook several steps: retrieving the events’ announcements, filtering announcements, collecting stock prices and other data, constructing the market model, estimating abnormal returns (our measure of the stock market reaction—see below), coding explanatory and control variables, testing the statistical significance of abnormal returns and conducting regression analyses (see Appendix B for details).

Estimation method

The underlying idea behind the event study method is a comparison between the observed, actual stock market return around an event and the estimated common return on the stock market for a hypothetical scenario without the event (MacKinlay, 1997). Thus, we compared a company’s stock return in the event of appointing a CDO (five-day event window) with a hypothetical, estimated case where the same company does not appoint a CDO (estimation window). The 5-day event window encompasses the day of the announcement (day 0), 2 days before (days −1 and −2), and 2 days after (days +1 and +2), following established guidelines for event studies (MacKinlay, 1997; McWilliams and Siegel, 1997). For the estimation window, we relied on stock price data of 255 trading days starting on t = −300 and ending on t = −45 before the event (t = 0) to ensure that the observed event cannot influence the market model estimates and following the lead of earlier studies in IS literature (Chatterjee et al., 2001; Dehning et al., 2003). We calculated the daily abnormal return by comparing the observed market return of the event window with the estimated return of the estimation window.

Data

We collected two types of data: financial data and press releases. First, we retrieved stock price data, prices of market indices, and company characteristics from Refinitiv Eikon. Second, we collected press releases of companies announcing a CDO appointment, either in addition to an already existing CIO or as the solely responsible senior IS manager. Since announcements of publicly listed companies are subject to public and legal scrutiny, which discourages companies from dishonest signaling (Zmud et al., 2010), only companies that expect the benefits of appointing a CDO to outweigh the costs associated with the role will make and communicate this strategic decision.

Announcements of CDO appointments from 2009 to 2020 5 were retrieved via LexisNexis, a database for periodical articles and press releases. Our comprehensive search used the keyword “chief digital officer” and alternative position titles, such as “vice president digital” or “head digital” as well as abbreviations, such as “CDO,” along with keywords, such as “appoint,” “create,” or “new” that indicate an appointment. In selecting our keywords, we followed the lead of other event studies that explored the announcement of managerial positions (e.g., Chatterjee et al., 2001). Our search covered the period January 1, 2009, to December 31, 2020, and resulted in 7014 announcements. A comprehensive filtering process and quality checks (see Appendix B) led to a sample of 334 CDO appointment announcements. Next, we coded the press releases to retrieve detailed information about CDOs’ characteristics (see the following subsection). For the principal analysis, all explanatory variables were derived exclusively from information provided in the press releases because these represent observable signals for investors.

We then matched all announcements with daily stock price data for the respective company. In this step, we filtered out 27 announcements of companies for which stock price data was missing. Our final sample contained 307 CDO appointment announcements.

To connect with existing research, we also collected data on CIO appointments for the timeframes (1) 1987-1998, the period also used by Chatterjee et al. (2001), and (2) 2011-2020, a period comparable to our sample of CDO appointments. We provide detailed information on the collected data and our findings in Appendix C.

Variables

Dependent variable

Cumulative abnormal return (CAR), a measure of the stock market reaction in the 5 days surrounding the event (day −2 through day +2), is our dependent variable. CAR denotes the difference between a company’s observed stock market return at the event and the expected return in the absence of the event, cumulated across the 5 days surrounding the event (see Appendix B).

Independent and control variables

Overview of dependent, explanatory and control variables.

General Notes: All measures of a CDO's power were derived from existing literature on CIOs or other senior managers or constitute own measurements (OM). In line with our event study method, we coded the presence of information regarding a power dimension as 1, while we coded the absence of information as 0. Elite education: For the US, undergraduate and graduate schools were considered to constitute elite universities, if they appeared in the U.S. News & World Report Historical Liberal Arts College and University Rankings in the top 20 at least once in the period 1985-2020 (Reiter, 2021). A comparable measure was created for non-US undergraduate and graduate schools based on the QS World University Ranking (QS World University Rankings (2021). Experience big tech: We used historical data on the Fortune Global 500 (2021) companies in the period 2009-2020 to identify the largest IT companies, based on their industrial subsector. Leadership capability: This measure considers the leadership experience of externally hired CDOs. In Appendix E, we also considered a more general measure that includes the leadership capabilities of both internally and externally hired CDOs. Degrees in both business and IT: Here, we consider both CDOs with an undergraduate degree in business and a graduate degree in computer science as well as CDOs with an undergraduate degree in computer science and a graduate degree in business. We also consider CDOs with an educational background in the management of information systems (MIS) to possess interdisciplinary knowledge in business and IT. Role profile: Please note that the control variables describing CDOs’ role profiles can overlap since a CDO can, for instance, be responsible for marketing (functional) for one product segment (business unit). CIO in TMT: Please note that this control variable is only relevant for succession announcement. In the case of new positions, we only consider CDO appointments where no CDO or CIO existed previously or exists currently to circumvent the possibility that a CDO was appointed to take over the responsibilities of the CIO under a new label.

Structural power

We used established measures of structural power in this study, such as the existence of a reporting line to the CEO, TMT membership, and title rank (e.g., Feng et al., 2021; Smaltz et al., 2006). Additionally, we included the resource endowment of CDOs with a team or business unit as an additional variable (team) to measure structural power because these resources facilitate exerting influence.

Prestige Power

Following Finkelstein (1992), we used elite education to measure a CDO’s prestige power. A degree from an elite university provides senior managers with a personal network with other people in powerful positions who attended the same elite institution with them (Finkelstein, 1992). More recent studies have also considered senior managers with work experience in large IT companies to carry prestige (Pollock et al., 2010), since they can be expected to have personal ties to stakeholders and access to valuable information about these companies (Burton et al., 2002). Start-up experience also carries prestige, signaling entrepreneurial spirit and more virtue than established companies (Gamez-Djokic et al., 2022).

Expert Power

Prior IS literature has emphasized the importance of interdisciplinary business and IT education and competencies for business and IT professionals (Bassellier et al., 2003; Mithas and Krishnan, 2008). Accordingly, we included a measure of an interdisciplinary educational background in both business and IT, measured as at least one degree in both business and IT, as a dimension of expert power. Earlier literature has also argued that externally hired senior managers introduce new perspectives and knowledge and challenge existing assumptions and beliefs (e.g., Chatterjee et al., 2001), leading us to consider external experience (outside) as a measure of expert power. Additionally, we include a measure of leadership capabilities, informed by existing literature emphasizing the role of experience for acquiring leadership skills (McCall, 2004).

New position and succession

We differentiate between two types of positions: new positions and succession. We considered CDO appointments to constitute a new position if no CDO or CIO existed in the company before or during the appointment. Moreover, we only coded appointments as new positions if this information was explicitly mentioned in the press release. By adopting this approach, we can eliminate the possibility that a CIO position was renamed to create a CDO position, without changing the appointed senior manager’s responsibilities. This approach also allows us to compare our results with Chatterjee et al. (2001), who only studied newly created positions during a timeframe when CIOs constituted novel senior managers. All CDO appointments in companies where a CDO or CIO existed previously or at the point of the announcement were considered successions. 6

Control variables

We included control variables in the regression analyses and robustness checks (see also Appendix E). Prior research has identified different role profiles for CDOs, ranging from role profiles with overarching responsibility for all digital initiatives to specialized role profiles with a focus on digital innovation or digital marketing only (Singh and Hess, 2017; Tumbas et al., 2017). At the same time, CDOs may not be responsible for driving digital initiatives across the entire organization but only for a specific business unit. Accordingly, we used control variables to identify CDOs with responsibility for one business unit, CDOs with a functional role profile (e.g., marketing, innovation), CDOs with mixed responsibility for IT and business, and CDOs with responsibility for IT infrastructure only. Additionally, we included controls on the individual, company, industry, and country levels. These and additional control variables used in the robustness tests are described in Table 1 and in Table E3 in Appendix E.

Testing abnormal returns and regression analyses

Our analysis is divided into two steps based on the approach of earlier event studies (Chatterjee et al., 2001; Yang et al., 2012). To test hypotheses 1a to 1c, we first evaluated the statistical significance of the overall market reaction to CDO appointments. Here, we used both parametric and non-parametric tests, as suggested by McWilliams and Siegel (1997), to control for the possibility of outliers or violations of the normality assumption. The described approach to evaluate the overall market reaction follows established guidelines in IS 7 and is described in detail in Appendix B.

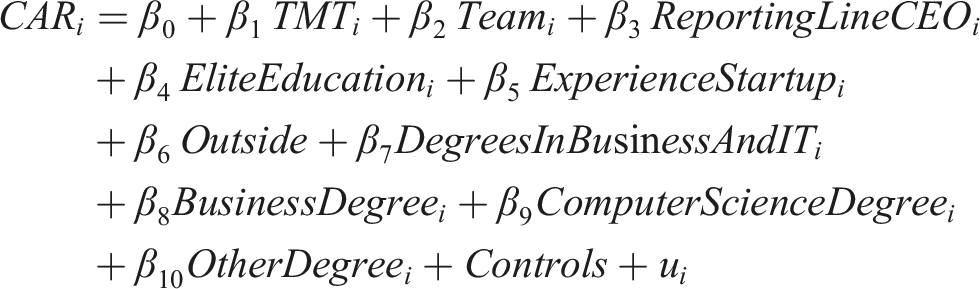

To test the remaining hypotheses, we then conducted multivariate OLS regressions, following earlier IS studies (Bose and Leung, 2019; Chatterjee et al., 2001). Here, we used the CAR over the event windows (day −2 to day +2) as the dependent variable and included explanatory variables indicating CDOs’ structural, prestige, and expert power. We conducted separate regression analyses for CDO appointments to new positions and successions and included numerous control variables. The following regression equation reflects the consolidated model with controls for CDO succession appointments (see Table 4, Models III-IV):

In addition to the regression analyses reported in the following sections, we also conducted several robustness checks using alternative event windows, different estimation windows, and additional control variables (see Appendix E).

Results

Stock market reactions to CDO appointments

In the following, we analyze the overall market reaction to mandatory signals conveying CDO appointments. We separately analyze CDO new position and succession appointments.

Signals conveying CDO appointments to newly created positions

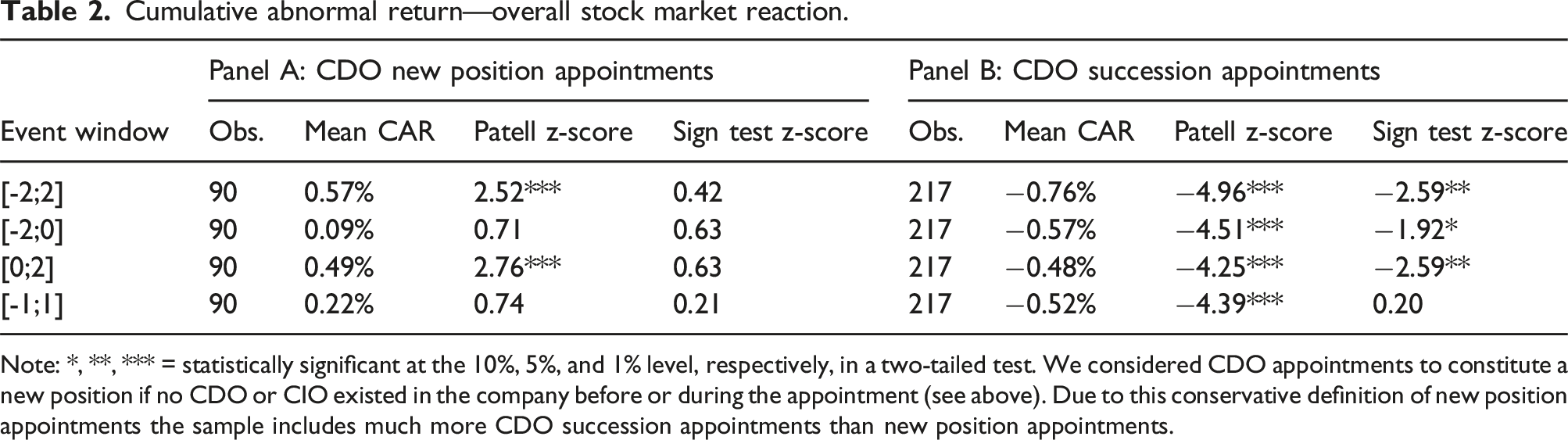

Cumulative abnormal return—overall stock market reaction.

Note: *, **, *** = statistically significant at the 10%, 5%, and 1% level, respectively, in a two-tailed test. We considered CDO appointments to constitute a new position if no CDO or CIO existed in the company before or during the appointment (see above). Due to this conservative definition of new position appointments the sample includes much more CDO succession appointments than new position appointments.

Considering the event window [−2; 2], the value of the stock increases by an average of 0.57% after a company’s announcement to appoint a CDO, which is a sizeable effect that is comparable to other event studies (Bose and Leung, 2019; Han and Chang, 2012). To illustrate the effect size, consider the average market capitalization of around US$20 billion across the sampled companies at the time of the CDO appointment. An increase of 0.57% against the market index would have resulted in a gain of approximately US$114 million in market capitalization in 5 days for a sampled company on average.

We also observe some heterogeneity in the market reaction. We identify a positive but statistically insignificant market reaction for the specific event windows [−2; 0] and [1; 1]. Such heterogeneity of effects across event days and windows is in line with earlier event studies that report different event windows (Han and Chang, 2012; Yang et al., 2012). The sign test indicates no statistical significance for all event windows. 8

Hypothesis 1a states that announcements of CDO appointments to new positions are associated with a positive market reaction. Overall, the results presented in Panel A of Table 2 show support for this hypothesis.

Signals Conveying CDO Succession Appointments

Panel B in Table 2 depicts the cumulative abnormal return for CDO succession appointments. We find a negative and statistically significant effect of announcing the appointment of a CDO succession on the cumulative abnormal return in all event windows according to both the Patell and sign tests, except for the event window [−1;1], where the non-parametric sign test could detect no statistical significance. For the event window [−2; 2], the value of the stock decreases by an average of 0.76% (p-value <.01) after a company’s announcement to appoint a succeeding CDO, an effect greater in size than the average positive market reaction to CDO appointments to new positions. Considering again the average market capitalization across companies in the sample, a decrease of 0.76% against the market index would have resulted in an average loss of approximately US$152 million in market capitalization in 5 days.

Hypothesis 1c states that announcing a CDO succession appointment is associated with a negative market reaction. As illustrated in Panel B of Table 2, our results strongly support this hypothesis (for comparison to CIO appointments, see post-hoc analysis). At the same time, hypothesis 1b, which states that announcing a CDO succession appointment is associated with a positive market reaction, is rejected.

Regression results for signals conveying CDOs’ managerial power

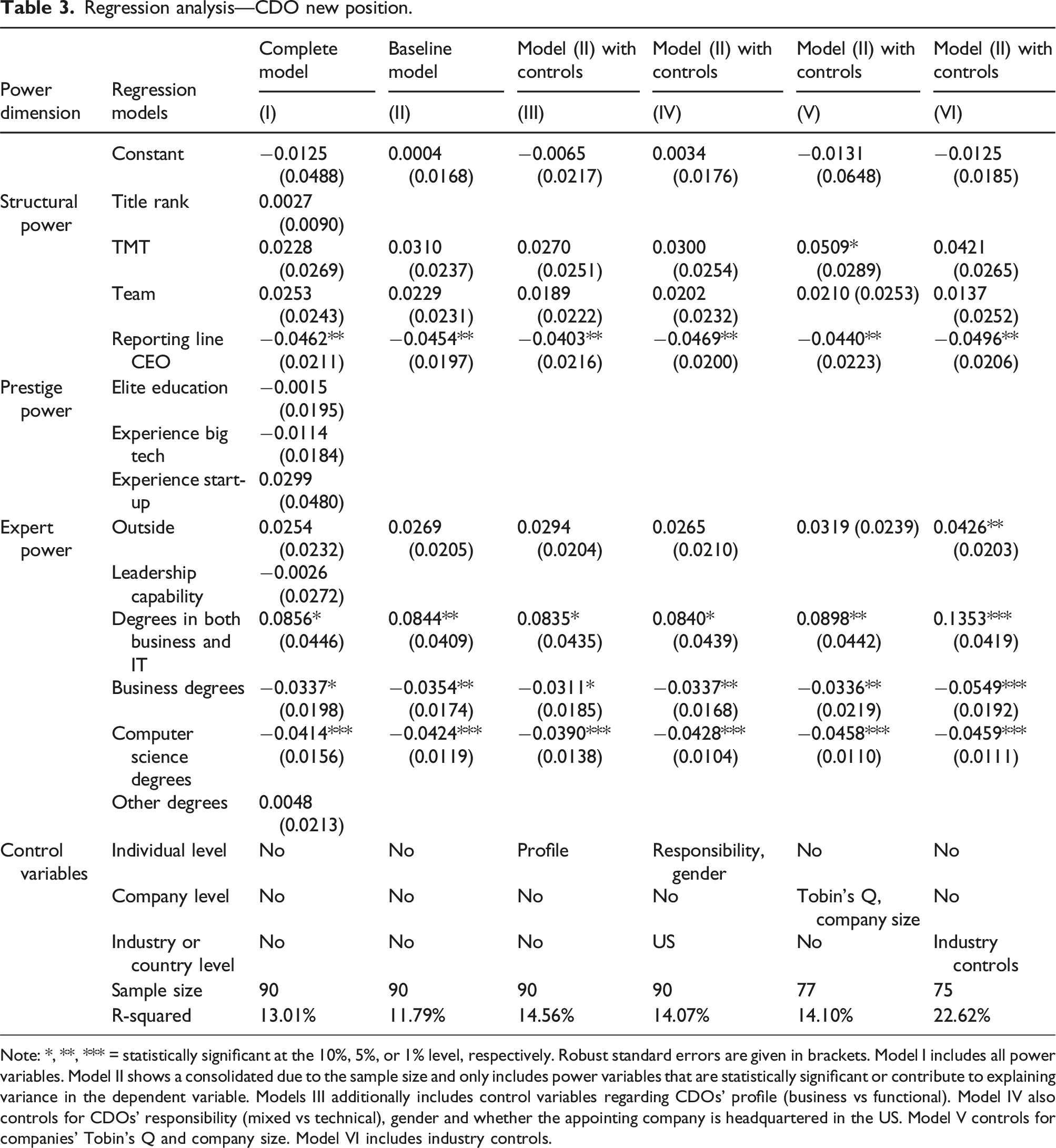

Regression analysis—CDO new position.

Note: *, **, *** = statistically significant at the 10%, 5%, or 1% level, respectively. Robust standard errors are given in brackets. Model I includes all power variables. Model II shows a consolidated due to the sample size and only includes power variables that are statistically significant or contribute to explaining variance in the dependent variable. Models III additionally includes control variables regarding CDOs’ profile (business vs functional). Model IV also controls for CDOs’ responsibility (mixed vs technical), gender and whether the appointing company is headquartered in the US. Model V controls for companies’ Tobin’s Q and company size. Model VI includes industry controls.

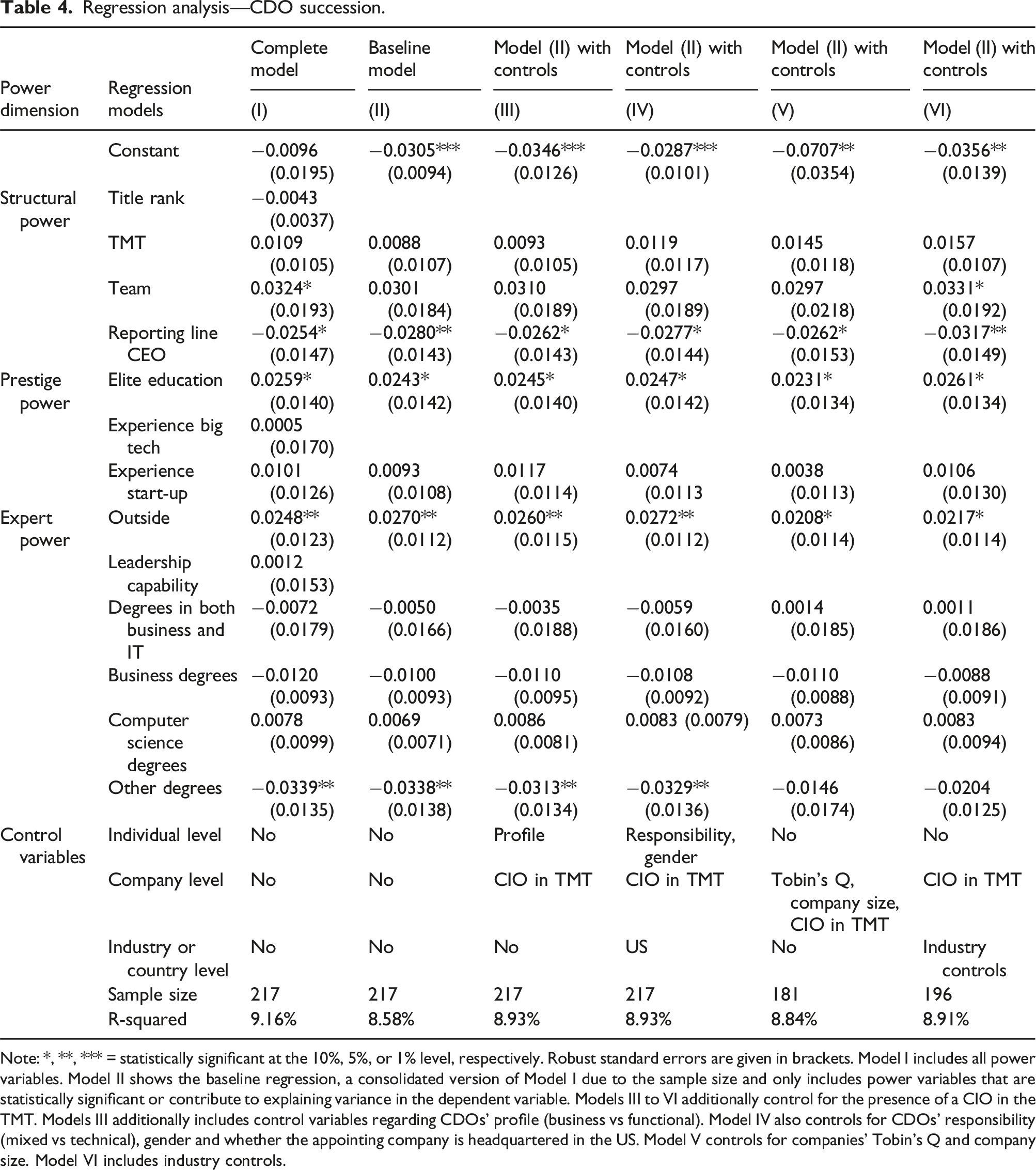

Regression analysis—CDO succession.

Note: *, **, *** = statistically significant at the 10%, 5%, or 1% level, respectively. Robust standard errors are given in brackets. Model I includes all power variables. Model II shows the baseline regression, a consolidated version of Model I due to the sample size and only includes power variables that are statistically significant or contribute to explaining variance in the dependent variable. Models III to VI additionally control for the presence of a CIO in the TMT. Models III additionally includes control variables regarding CDOs’ profile (business vs functional). Model IV also controls for CDOs’ responsibility (mixed vs technical), gender and whether the appointing company is headquartered in the US. Model V controls for companies’ Tobin’s Q and company size. Model VI includes industry controls.

Regression results for signals conveying CDOs’ structural power

Hypothesis 2 argues that the abnormal return following the appointment of a CDO is positively associated with the CDO’s structural power. For CDO appointments to new positions, Models I to VI in Table 3 illustrate that CDOs’ title rank, membership in the TMT, and endowment with a subordinate team do not influence the market reaction. An exception is Model V, where a positive and weakly statistically significant effect is observed for TMT membership. Regarding the reporting line between CDO and CEO, surprisingly, we find a statistically significant negative effect, which we explore in depth in a post-hoc analysis (see Appendix D). We find no statistically significant effect for other reporting structures (see Appendix E). Our results, therefore, indicate no support for hypothesis 2 for CDO appointments to new positions.

For CDO succession appointments, Models I to VI in Table 4 show that CDOs’ title rank and membership in the TMT do not influence the market reaction. Yet, announcements of CDO appointments with a subordinate team or business unit are perceived as positive by the stock market, with an average return of 3.24% (Model I). This effect is statistically significant at the 10% level for Model I and Model VI only. Surprisingly, we again find a statistically significant negative effect for a direct reporting line between CDO and CEO (p-value <.1; see Appendix D) across all models, but no statistically significant effect for other reporting structures (see Appendix E). Overall, our results for CDO succession appointments indicate weak support for hypothesis 2.

Regression results for signals conveying CDOs’ prestige power

Hypothesis 3 suggests that abnormal returns in response to CDO appointments are positively associated with CDOs’ prestige power. For CDO appointments to new positions, the regression analysis on the market reaction to CDOs’ prestige power, depicted in Model I in Table 3, indicates no statistically significant effects, although CDOs’ experience in a start-up has a positive and sizeable coefficient. The coefficients for CDOs’ elite education and big tech experience are also statistically insignificant. Thus, for newly created CDO positions, we find no support for hypothesis 3.

Next, we analyze the market reaction associated with CDOs’ prestige power for succession appointments, which is depicted in Table 4. All models show a statistically significant effect of CDOs’ elite education. On average, stocks rise by 2.43% (Model II, p-value <.1) if a CDO with a degree from an elite university is appointed to a CDO succession position. In contrast, experience in start-ups and big tech companies have no statistically significant effects on investors’ reactions. Overall, and in contrast to CDO appointments to new positions, we find support for hypothesis 3 for CDO succession appointments.

Regression results for signals conveying CDOs’ expert power

Hypothesis 4a suggests that abnormal returns in response to CDO appointments are positively associated with CDOs’ expert power derived from knowledge in both business and IT. The regression results in Table 3 show strong support for this hypothesis across all models (p-value <.1) for CDO new position appointments. This contrasts with the regression results for the number of degrees in either business or computer science, where a statistically significant negative effect exists. The combined effect for the appointment of a CDO with one degree in business or management and another degree in computer science leads, on average, to a stock price increase of 0.66% 10 (Model II). Thus, we find strong support for hypothesis 4a for new position appointments.

For CDO succession appointments, we find no statistically significant effect for CDOs’ expert power derived from knowledge in both business and IT across all models, as Table 4 illustrates. Therefore, hypothesis 4a is not supported for CDO succession appointments. Yet, our analysis in Table 4 shows that investors sanction the appointment of CDOs with degrees in either engineering or humanities (other degrees).

Hypothesis 4b argues that the abnormal return following a company’s announcement to appoint a CDO is positively associated with the CDO’s expert power derived from external knowledge. When analyzing the market reaction to CDO new position appointments, Table 3 shows that externally hired CDOs (outside) are perceived as positive by investors, but the coefficient is statistically insignificant for almost all models. Additionally, the coefficient for appointees’ leadership capability is close to zero and statistically insignificant. Thus, we find no support for hypothesis 4b.

When we turn to CDO succession appointments, Table 4 illustrates that CDOs hired externally are perceived as positive by investors. On average, a company announcing the appointment of a CDO from outside the company can expect a cumulative increase of 2.70% (Model II) of its stock, 11 an effect that is statistically significant at the 5% (10%) level in Models I to IV (V and VI) and robust to the inclusion of controls. In contrast, we observe no statistically significant link between appointees’ leadership capability and stock market reactions. Thus, we find support for hypothesis 4b for CDO succession appointments.

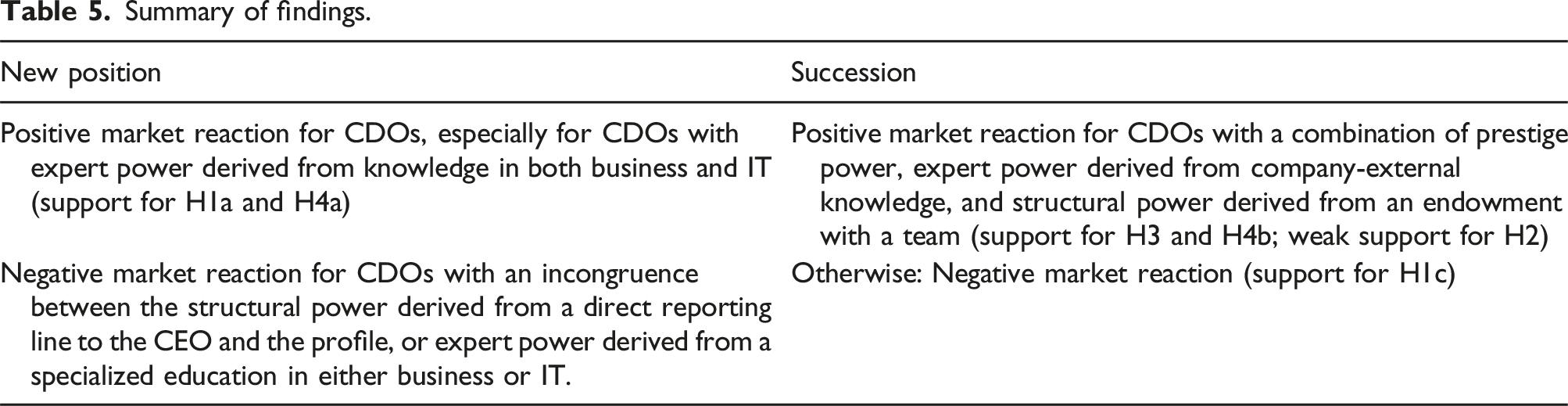

Summary of findings.

Post-hoc analysis: CDO versus CIO appointments

The mixed market reaction following CDO appointments contrasts with the observed positive market reaction to CIO appointments (Chatterjee et al., 2001). To understand this result better, we conducted a post-hoc analysis where we investigated market reactions to CIO appointments during two time periods. We study (1) earlier years (1987-1998) to connect with existing CIO literature (Chatterjee et al., 2001) and (2) recent years (2011-2020) to compare investors’ perceptions of signals regarding CDO and CIO appointments. The analysis of these two time periods not only allows us to ensure the consistency of our methodological approach with earlier event studies, but also to test the persistence of earlier findings by Chatterjee et al. (2001) until today. Our results in Tables C2 and C3 in Appendix C are twofold.

First, in alignment with Chatterjee et al. (2001), we find a positive market reaction for CIO appointments to newly created positions in the timeframe 1987-1998. This corresponds to our findings regarding CDO appointments to new positions in the timeframe 2011-2020. Second, we show that CIO appointments during the more recent period 2011-2020 elicited a negative market reaction for both new positions and succession. The observed negative effect is comparable in size to the market reaction to CDO succession appointments in our study and is highly statistically significant.

Additionally, we analyzed the role of CIOs’ power profile for market reactions in the recent period 2011-2020. Our analysis in Table C4 in Appendix C shows different results for investors’ reactions to CIOs’ power profiles following their appointments in the timeframe 2011-2020 compared to investors’ reactions to CDO appointments. For CIO appointments, only the positive effect of expert power derived from business knowledge is statistically significant and can dampen the overall negative market reaction. In contrast, structural power and other expert power variables exhibit no statistically significant association with the market reaction following CIO appointments.

Discussion

In the following, we discuss our main contributions. We first outline how this paper contributes to the existing literature on CDOs. We then discuss how complementary and competing signals contribute to investors’ reactions to CDO appointments and how we thereby extend existing literature on senior IS management appointments. Finally, we discuss the distinct nature of CDOs and CIOs, as revealed by our analysis.

The CDO and the stock market

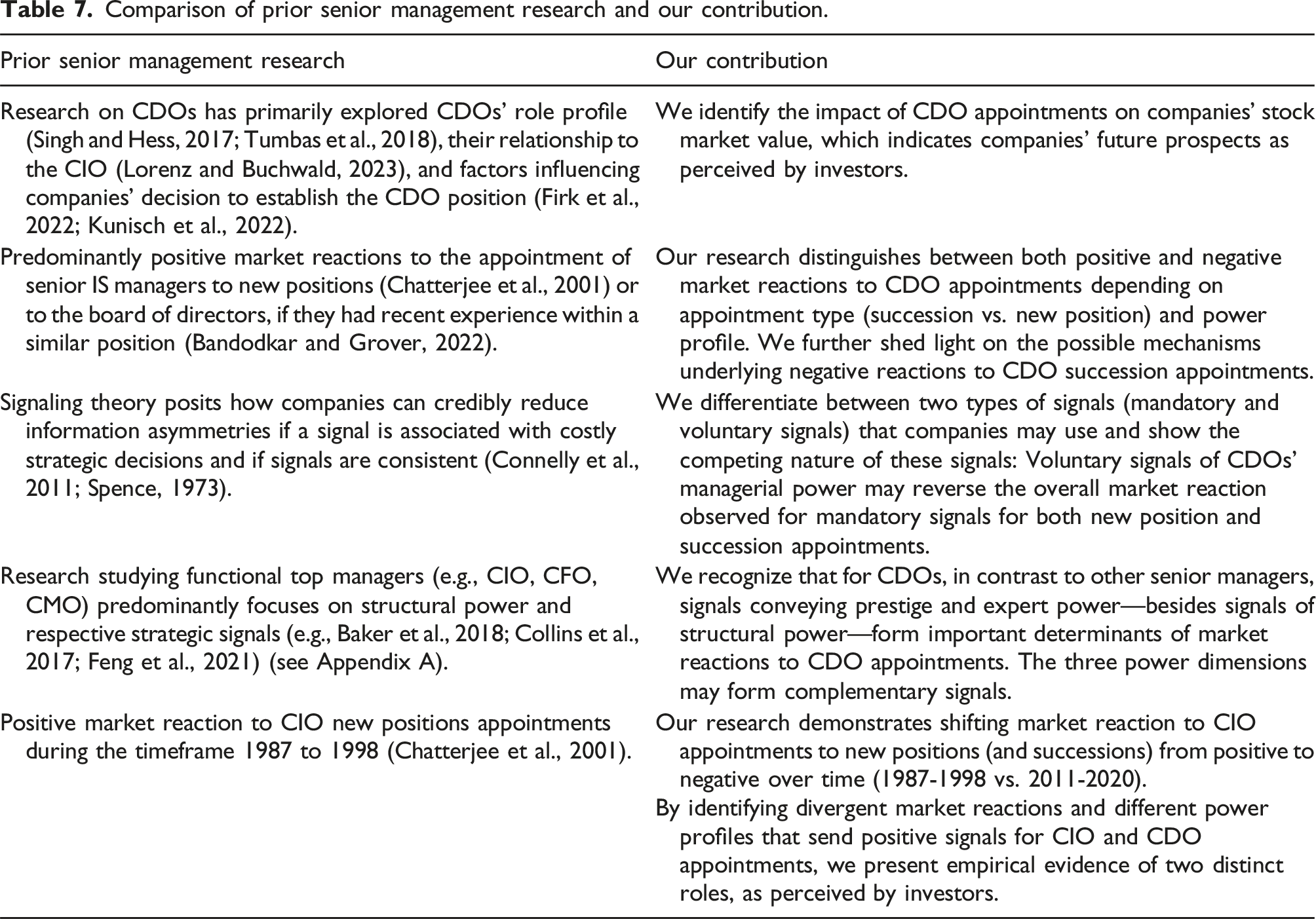

By studying the stock market reaction to CDO appointments, we contribute to the existing literature on CDOs’ important role for digital transformation by identifying the impact of CDO appointments on companies’ stock market value. Existing research studying CDOs has predominantly neglected the market perspective and focused on CDOs’ roles and company-internal considerations. Namely, research conceptualized CDOs’ role profiles (Singh and Hess, 2017; Tumbas et al., 2018), derived a universal CDO archetype (Culasso et al., 2023), studied the relationship to the CIO (Lorenz and Buchwald, 2023), and identified factors influencing companies’ decisions to establish the CDO position (Firk et al., 2022; Kunisch et al., 2022). Yet, we know little about how CDO appointments impact companies’ future prospects and success. Except for Zhan et al. (2022), our study is the first to take a market perspective and explore the signals that companies send to investors by appointing a CDO. However, Zhan et al. (2022) only focus on new positions and do not differentiate between chief digital and data officers or CDOs’ power profiles. We elicit the conditions under which a CDO appointment can positively impact the future prospects of the appointing company. Although our analysis primarily examines the short-term effects of CDO appointments on the stock market, the results may also indicate potential implications for companies’ overall performance. Previous research has demonstrated that favorable signals in the stock market can increase companies’ substantive value, including future financial success (Bandodkar and Grover, 2022).

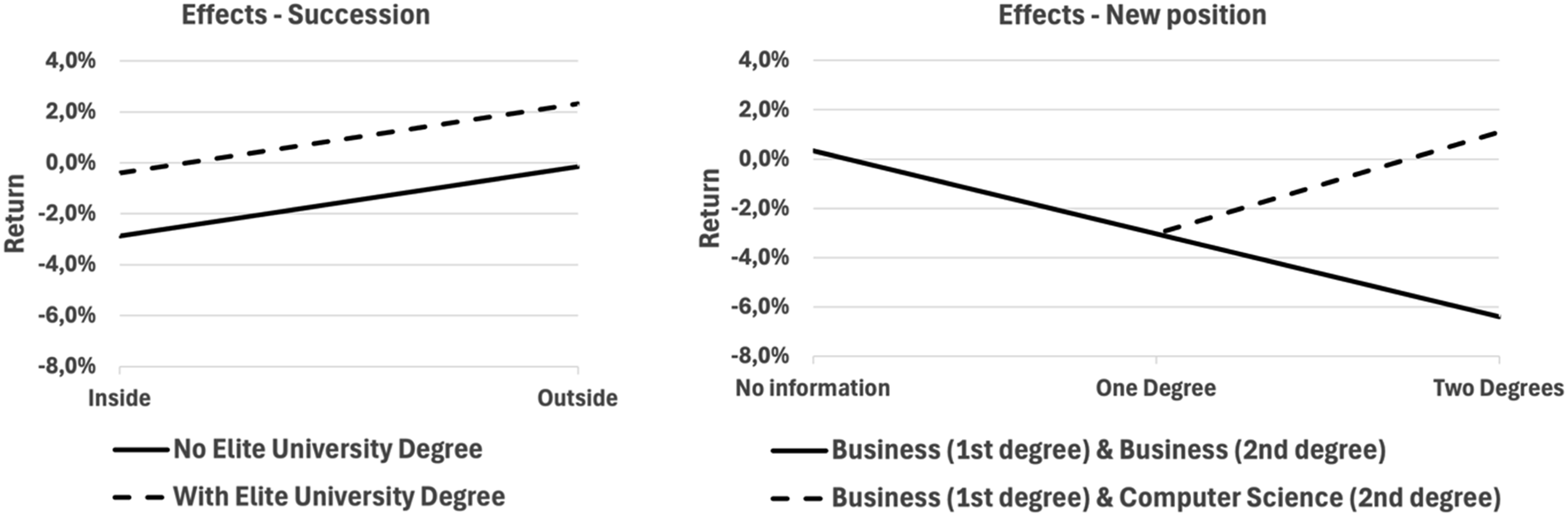

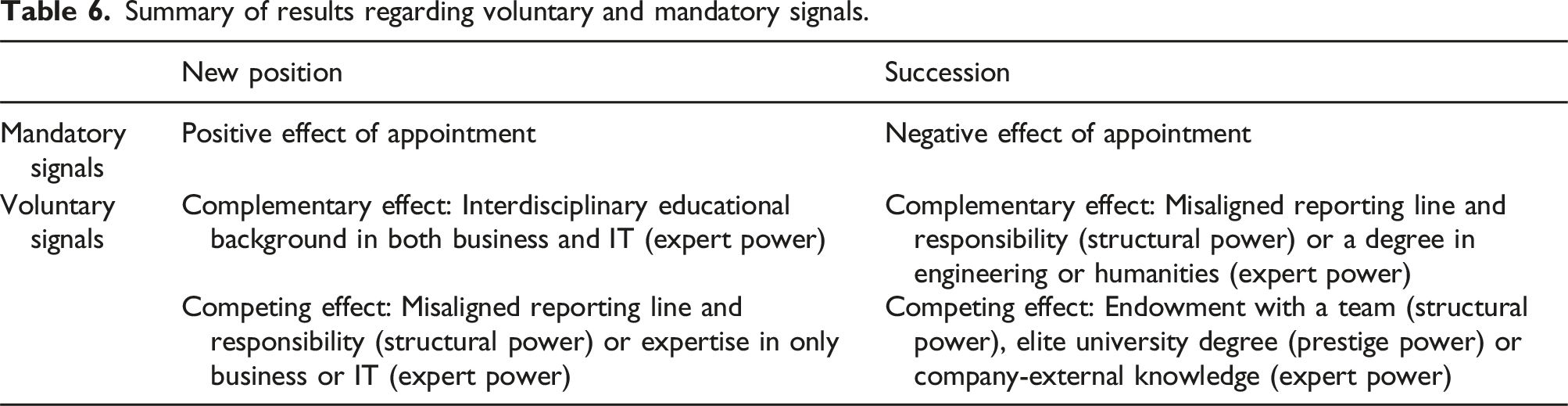

We also connect with and extend existing research on stock market reactions to senior IS managers in three ways. First, in line with existing studies (e.g., Chatterjee et al., 2001), we find that on average, and when only considering mandatory signals, stock markets react positively to CDO new position appointments. However, our findings reveal that this effect is conditional on the accompanying voluntary signals that convey information about the CDO’s power profile. Going beyond existing literature, we show that voluntary signals conveying CDOs’ power profile may form competing signals to the mandatory signals of new position appointments. Thus, voluntary signals can counteract the positive perception of CDO appointments. The overall positive market reaction for CDO new position appointments may turn negative for CDO appointments, signaling weak structural and expert power. For example, new position appointments of CDOs with misaligned reporting lines and responsibilities and CDOs possessing a specialized education with a singular focus on either business or IT, but no educational background in both business and IT (see Figure 2(b)), are associated with a negative market reaction. Thus, an appointment signaling a weak CDO may counteract the positive signal of digital transformation efforts in the company conveyed by a new position appointment. (a) and (b) Effect size and direction of competing signals.

Second, extending existing IS research, we explore succession appointments and find that CDO succession appointments are generally perceived as negative by investors. The reasoning used during hypotheses development provides a potential explanation for these findings. Appointing CDOs to new positions may send credible signals of companies’ intention for strategic change toward digital transformation. In contrast, succession appointments contain two contrarian signals. On the one hand, CDO succession appointments send positive strategic signals that companies continue their strategic efforts of digital transformation and reinforce existing positive perceptions toward the appointing companies (Rindova et al., 2005). On the other hand, succession appointments send a negative strategic signal, since the new appointee may disrupt existing processes and introduce a new leadership style (Berns and Klarner, 2017). The negative market reaction to CDO successions that we find in our analysis suggests that the second effect dominates.

As with new position appointments, we find that the overall effect due to signals based on mandatory information can reverse when considering signals based on voluntary information. For instance, we demonstrate that the overall negative market reaction to CDO succession appointments (see above) can turn positive if announcements for CDO succession appointments signal that the respective CDO strongly exhibits prestige and expert power. For instance, Figure 2(a) illustrates that succession appointments of CDOs with company-external knowledge and elite university degrees are, after all, perceived as positive by investors, while CDO appointments of insiders are perceived negatively, regardless of an elite university degree. This illustrates that while succession appointments may signal a failed digital transformation in a company overall, succeeding CDOs who, for example, introduce new knowledge from the outside or have influential relationships or leadership qualities due to their elite education can reverse investors’ perceptions. Thus, our analysis not only explores succession appointments of senior IS managers but also proposes the possible mechanisms.

Overall, these findings on the contrarian effect of mandatory and voluntary signals underscore the role of voluntary signals in reducing information asymmetries.

Third, we show that voluntary signals that convey different power dimensions and sources are relevant for the appointment of CDOs to new positions compared to existing ones. Whereas for CDO new position appointments, signals regarding structural power and expert power derived from knowledge in both business and IT impact market reactions, for CDO succession appointments, signals regarding structural and prestige power as well as expert power derived from company-external knowledge influence investors’ reactions. We argue that this finding may be attributed to the different situations and responsibilities of the appointed CDO. CDOs appointed to new positions may focus on analyzing the company’s current situation and creating a digital transformation roadmap. These are tasks where broad and interdisciplinary knowledge can be helpful. In contrast, CDOs appointed to succeed a CDO or CIO may predominantly need to focus on successfully implementing an already existing vision of digital transformation for the appointing company. Executing and leading such a vision, especially prestige and structural power can be beneficial because they allow for faster implementation due to the appointed CDO’s broader or more influential network of contacts (prestige power) or resource endowment with a team (structural power).

Competing and complementary signals of senior manager appointments

Summary of results regarding voluntary and mandatory signals.

Although signaling theory has traditionally addressed the strategic transmission of information to reduce information asymmetries between two parties (Spence, 1973, 2002), it has so far not differentiated between mandatory and voluntary signals systematically. In accounting and finance research, both types of signals have only been studied separately within the literature on information disclosure, though typically not through the lens of signaling theory. A notable exception is Hennig et al. (2025), who examine the role of signal credibility in the relationship between earnings call tone and investor reactions. Most research on the voluntary disclosure of information has focused on its antecedents, such as company size, liquidity, ownership structure, board characteristics, and executive compensation (e.g., Brockman et al., 2019; Laksmana, 2010; Zamil et al., 2021). Fewer studies investigate the effects of such disclosures, with almost all studies focusing on the disclosure of company-level information, such as companies’ choice of partners (Downes et al., 2022) and carbon emission information (Datt et al., 2019). Additionally, a key insight in existing literature on the effects of information disclosure is that more detailed and transparent disclosures often signal higher management quality or governance (e.g., Premuroso and Bhattacharya, 2008), thereby reducing information asymmetry between companies and external stakeholders.

Our study adds to this key insight by demonstrating another effect: voluntarily disclosed information about a CDO’s power profile signals that the appointee is well-suited to the role, thereby reducing uncertainty surrounding the appointment. Consequently, the voluntary disclosure of managerial power impacts companies’ financial performance.

Figure 2(a) and (b) illustrates the competing effects of mandatory and voluntary signals. Figure 2(a) shows how the negative market reaction to succession appointments (mandatory signal) turns positive for CDOs with an elite university degree and company-external experience (voluntary signals). Figure 2(b) demonstrates how the positive market reaction to new position appointments (mandatory signal) may turn negative for CDOs with one or two degrees in either business or IT, but not for CDOs with an interdisciplinary educational background in business and IT (voluntary signal).

By demonstrating these effects of competing mandatory and voluntary signals on companies’ future prospects, our study contributes to understanding the conditions under which CDO appointments may (not) prove beneficial for companies (Lorenz and Buchwald, 2023) and extends existing work on inconsistent signals sent by companies (Paruchuri et al., 2021).

We also demonstrate that signals conveying all three power dimensions of structural, expert, and prestige power have to be considered to explain market reactions, since the different power dimensions can send complementary or competing signals. Although our study is engaged with signals conveying power concepts, the insights gained might also be beneficial for studies in other domains using concepts from managerial power. Existing research, in that regard, predominantly has focused on structural power only or taken non-specific conceptual perspectives toward managerial power by using power-related concepts with other theoretical lenses (Baker et al., 2018; Bradley et al., 2012). Apart from Lim et al. (2013) and Schäper et al. (2024), who include expert and structural power in their studies on CIOs, the power dimensions of prestige and expert power—to our knowledge—have been largely overlooked by prior IS research.

Post-hoc analysis: The diverging nature of CDO and CIO appointments

To ensure the robustness of our methodological approach and in light of our findings regarding the impact of different sources of CDOs’ power on market reactions, we conducted a post-hoc analysis, where we explored the market reaction to CIO appointments. Our post-hoc analysis reveals differences in market reactions between CDO and CIO, as well as across time. We identify a positive market reaction for CIO new position appointments in the timeframe 1987-1998, in line with earlier findings by Chatterjee et al. (2001), and for CDO new position appointments in the timeframe 2009-2020 based on signals conveying mandatory information. However, studying CIO appointments in the later timeframe, we find that investors react negatively to companies appointing CIOs to both new and existing positions. That is, while in the early years CIO appointments to new positions led to positive market reactions, CIO appointments in recent years led to negative market reactions. In contrast, CDO appointments to new positions in recent years led to positive market reactions.