Abstract

Decentralized autonomous organizations (DAOs) leverage blockchain technology to facilitate collaboration and decentralize decision-making through rules encoded in smart contracts. DAOs challenge traditional governance theory by combining ownership and management using governance tokens. A governance token’s performance is traceable based on token price changes and subject to influencing factors. Understanding these factors is essential to ensure DAOs’ long-term viability as a new organizational form. However, insights into the drivers of token performance are still limited, leaving both DAO founders and potential token holders in the dark about which on-chain governance design choices to adopt to attract potential token holders. We apply signaling theory to elucidate how on-chain governance design choices influence token performance and use a unique dataset of 204 DAOs. We find that a minimum token quorum positively relates to token performance, while embedding voting incentives, such as non-fungible tokens or additional governance tokens, can negatively relate to token performance. Moreover, we identify founders’ stake as a contingent factor moderating these signals.

Introduction

Decentralized autonomous organizations (DAOs) are a unique blockchain-enabled organization form that challenges long-held assumptions in corporate governance theory. They question the traditional separation of ownership and management by shifting internal control from hierarchical command to democratic processes (Ding et al., 2022b; Saurabh et al., 2024; Wegner et al., 2024). DAOs leverage blockchain technology to enable new forms of collaboration and decentralized decision-making governed by rules and protocols encoded in smart contracts (Beck et al., 2018; Ellinger et al., 2024a; Lacity, 2022). They do so by issuing governance tokens that not only reflect the organization’s value in their token performance after a DAO listing (Wright, 2021) but also allow token holders to participate in the organization’s decision-making processes by voting for proposals from other token holders (Lumineau et al., 2021; Saurabh et al., 2024; Wiriyachaokit et al., 2022). Design choices that encourage broad participation attract more potential token holders, increase resource inflows, and ultimately boost a DAO’s growth and development, leading to positive token performance, defined as token price development. Such positive token performance is critical, given the novelty of DAOs as an organizational form whose early-stage challenges require strong financial backing to ensure long-term viability.

However, despite the criticality of token performance, knowledge on its drivers remains limited. While existing research has predominantly examined aspects such as tokenomics (Gan et al., 2023) and community engagement (Wright, 2021), the relationship between DAO on-chain governance mechanisms and token performance is still unclear. Potential token holders may have diverse motivations to participate in DAOs, ranging from active governance participation to purely speculative interests (Beck et al., 2018; Rikken et al., 2019; Wright, 2021). Nevertheless, we argue that potential token holders select DAOs that signal higher quality. We define quality as a DAO’s ability to fulfill its vision and purpose through democratic governance that allows broad participation. We argue that a higher quality attracts greater market interest, ultimately increasing token performance. Token holders participate in a DAO and its overarching vision and purpose, expecting that decentralized democratic decision-making with broad participation (Bellavitis and Momtaz, 2024) helps achieve these goals. Collective decision-making fosters transparency and reflects the interests of a diverse group of token holders. In this context, two key elements underlie quality: first, ensuring proper recognition of token holders’ votes in the governance process in the form of a minimum token quorum (MTQ); second, creating incentives to promote widespread engagement in voting. We examine these two essential on-chain governance design choices (i.e., MTQ and voting incentives) as signals to potential token holders.

An MTQ is defined as a technical on-chain design choice to have a minimum percentage of tokens participate in a vote for the proposal to be approved (Ding et al., 2022a; Rikken et al., 2019). An MTQ can signal a DAO’s commitment to token holders’ participation (O’Mahony and Karp, 2022; Schirrmacher et al., 2021), potentially enhancing market interest and token performance. However, if the MTQ is not met and the proposal fails despite strong support from the participating token holders, it can cause deadlocks and inefficiencies in DAO decision-making (Goldsby and Hanisch, 2022), leading to negative token performance.

Voting incentives are defined as stimuli meant to encourage broad participation among token holders and can include additional tokens or exclusive opportunities within the DAO (Gao and Leung, 2022). On the one hand, research indicates that voting incentives can serve as a positive participatory signal by bridging the gap between ownership and control (e.g., Halac, 2012; Mosley et al., 2022), ultimately increasing token performance by aligning token holders’ interests with the DAO’s decision-making processes. On the other hand, scholars suggest that voting incentives can encourage voting behavior primarily motivated to obtain financial rewards (Saadatmand et al., 2019; Yermack, 2017). For example, the Decentraland DAO rewards participants with non-fungible tokens (NFTs) for virtual land ownership, and the MakerDAO incentivizes active participants with additional MakerDAO tokens.

However, as the influence of these signals might be contingent upon contextual factors (Bafera and Kleinert, 2022), we also investigate how the founders’ stake influences the signaling effects of these two on-chain governance mechanisms. Founders’ stake refers to the percentage of ownership or tokens held by the founders of a DAO. Following prior research, we argue that founders can exert substantial control over decision-making when owning a significant stake (Nelson, 2003). Moreover, DAO founders have clear information advantages over outsiders such as potential governance token holders (Belitski and Boreiko, 2021) Thus, we argue that the founders’ stake can shape the signaling effects of the on-chain governance mechanisms MTQ and voting incentives, ultimately moderating their relationship to token performance.

We build an event-based general linear model (GLM) with 204 different DAOs in our unique sample to answer two research questions: (1) How do on-chain governance mechanisms set by the founders affect the token performance post listing? (2) How does the level of founders’ stake shape the effect of on-chain governance mechanisms on the token performance post listing?

Drawing on signaling theory (Spence 1973), we contribute to the intersection of information systems and DAO governance literature in three ways. First, we identify two effective but opposing signaling effects in the emerging field of DAOs. We show that having an MTQ is positively related to token performance, indicated by the percentage return based on the token price 30 days after its initial listing. Our study also finds that having voting incentives, such as NFTs or extra governance tokens, negatively affects token performance. We validate these on-chain governance mechanisms as distinct signals in the nascent domain of DAOs, differentiating them from those in other blockchain contexts (Colombo, 2021). Second, our research deepens the discussion on DAO governance (e.g., Beck et al., 2018; Santana and Albareda, 2022; Wright, 2021) by highlighting the contextual sensitivity of governance signals within DAOs, demonstrating that the contingent factor founders’ stake disparately moderates the interplay with other signals. Third, our study adds to signaling theory research that has primarily focused on positive signals. By showing that voting incentives act as a negative signal regarding token performance, we advance theory on how such signals shape investor decisions and, ultimately, token performance. In terms of practical contributions, our research underscores that DAO founders should consider the signals of their governance design choices to enhance token performance, while token holders can gain insights into the factors driving token performance.

Theoretical background

DAOs and their challenges

DAOs represent a new organizational form that leverages blockchain technology for governance purposes. Unlike traditional organizations or allocating control to an organizational elite (Cumming et al., 2025), DAOs operate without centralized leadership, relying instead on smart contracts to automate execution and decentralized decision-making processes to govern their operations (Colombo et al., 2022; Santana and Albareda, 2022).

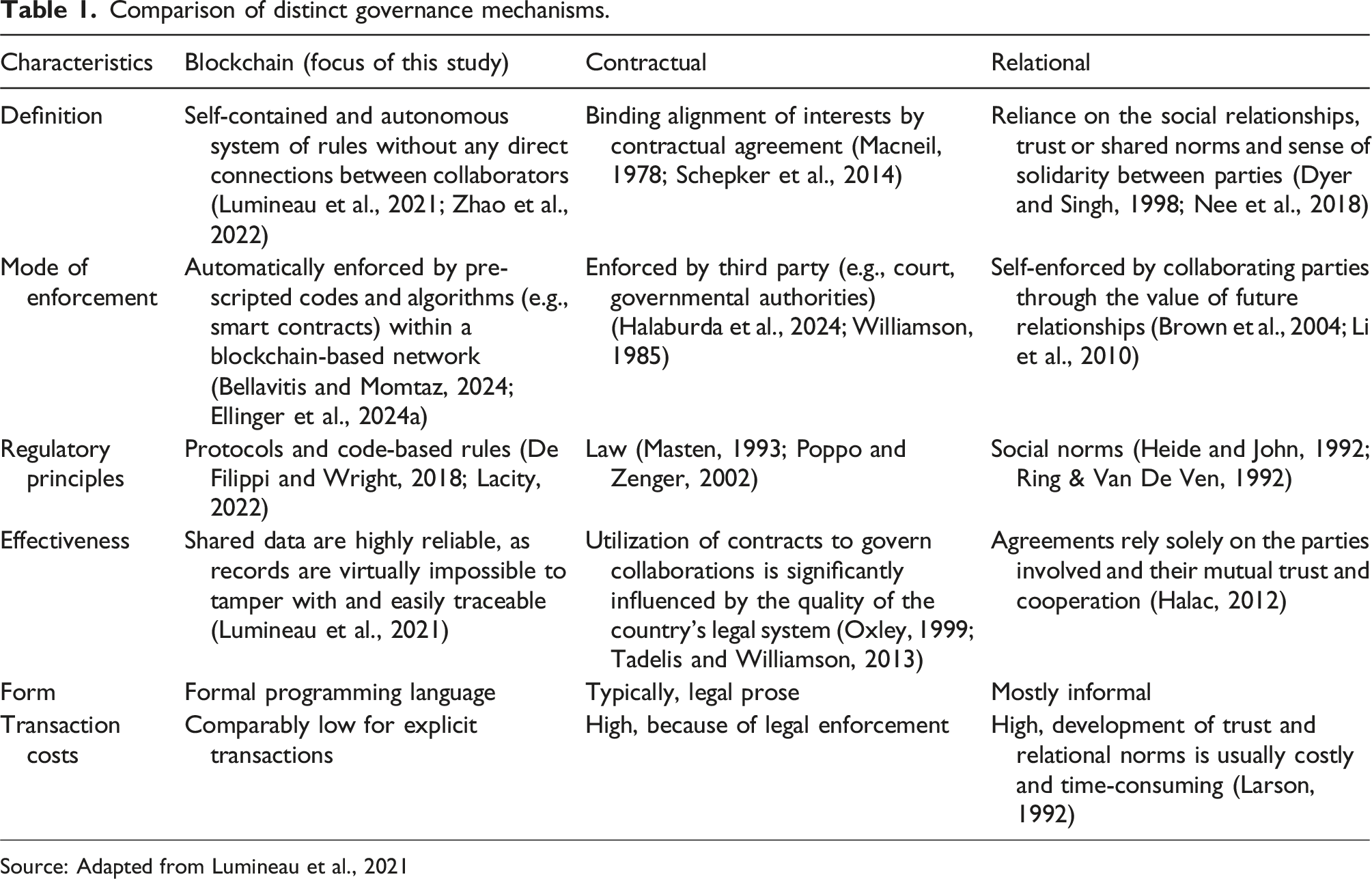

Comparison of distinct governance mechanisms.

Source: Adapted from Lumineau et al., 2021

Since our study focuses on DAOs, we concentrate on blockchain governance, which primarily manifests in two forms: on-chain, where actions are executed directly on the blockchain, and off-chain, where decisions are made externally and implemented subsequently on the blockchain (Lumineau et al., 2021). For example, MakerDAO’s forum discussions illustrate off-chain governance: Participants make decisions outside the blockchain, which are later manually implemented on-chain. Compound DAO, a DAO that allows users to borrow and lend cryptocurrencies without intermediaries, is a contrasting example of on-chain governance where decisions made through token holder votes are executed directly via smart contracts. Another illuminative example of on-chain governance relates to the mechanisms applied to process proposals in DAOs. In the case of VitaDAO, governance token holders initiate proposals that are discussed, transitioned to on-chain voting on longevity research proposals, and, if the vote succeeds, executed directly on the blockchain (Supplemental Appendix 2). While community discussions and consensus-building may occur via Discord, the final decision-making proceeds on the blockchain, ensuring transparency and immutability in the voting process. The on-chain mechanism provides a secure and verifiable method for members to support innovative research initiatives (VitaDAO | The Longevity DAO, n.d.). Hence, DAOs are unique as key governance processes are ultimately executed directly through blockchain technology (Wright, 2021). This automated approach not only differentiates them from traditional governance methods but also introduces built-in enforcement mechanisms. These on-chain mechanisms reduce non-compliance risks while increasing reliability and predictability (Lumineau et al., 2021).

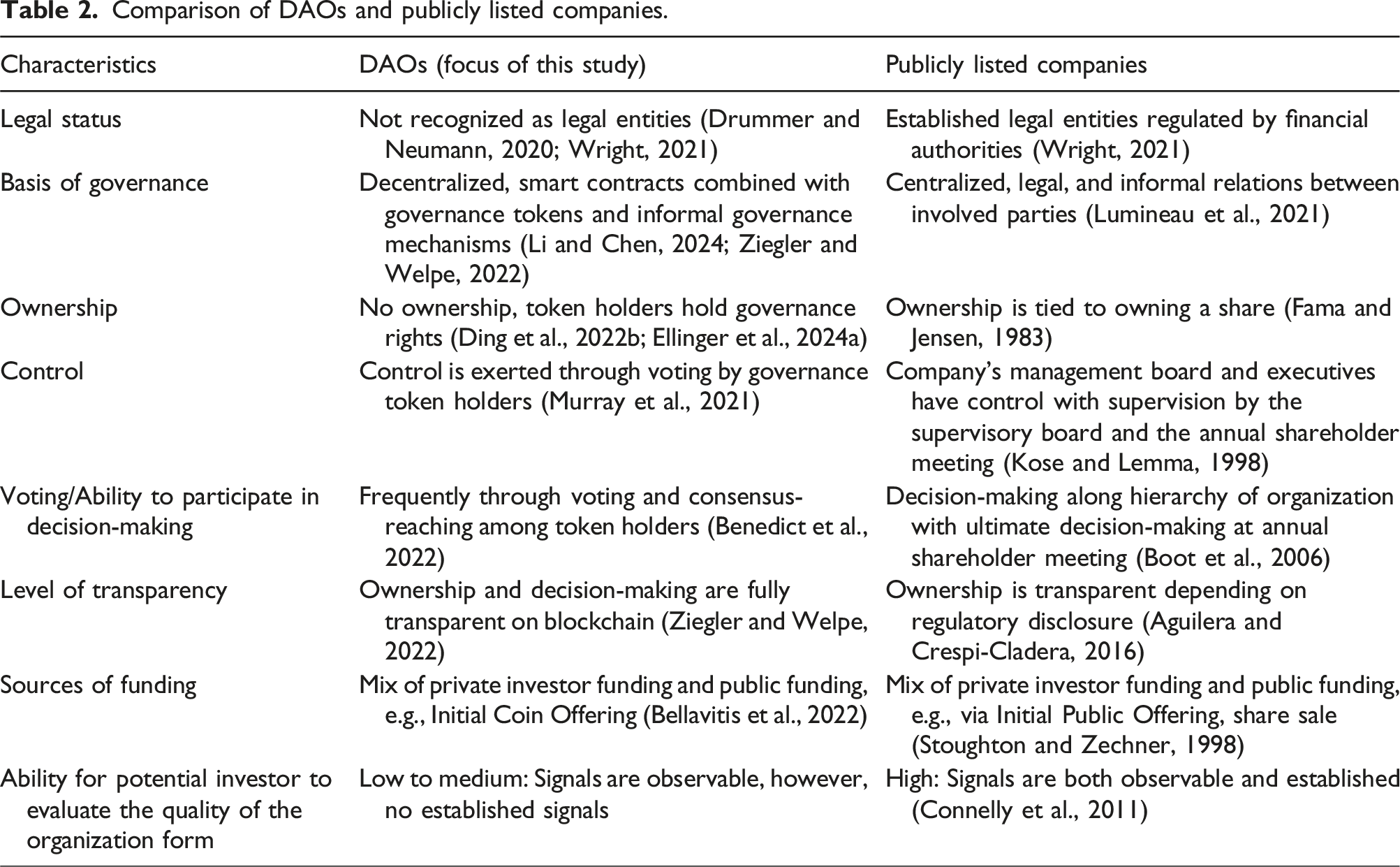

Comparison of DAOs and publicly listed companies.

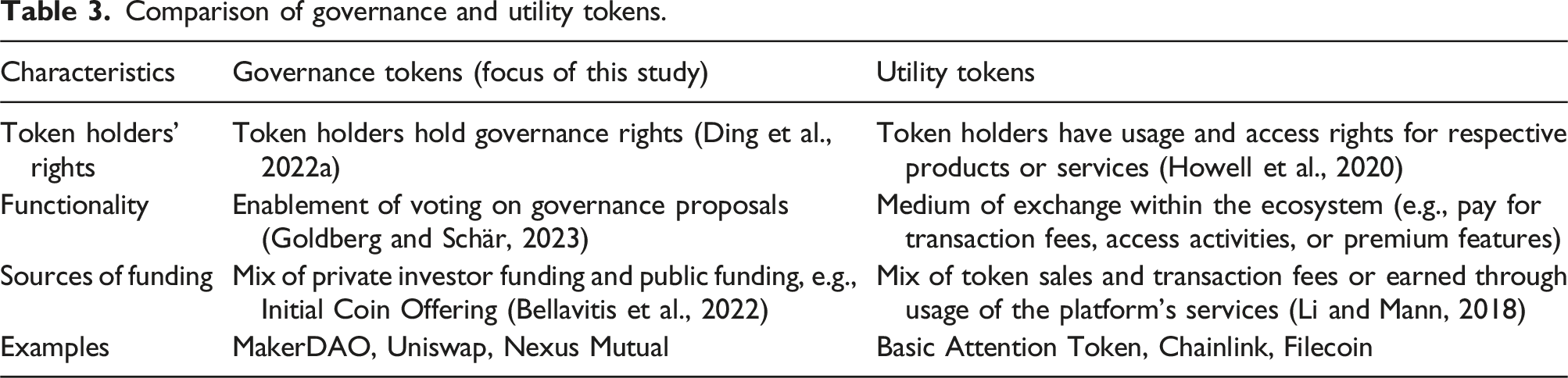

Comparison of governance and utility tokens.

However, a key challenge is that potential token holders face uncertainty regarding the quality of DAOs. Indeed, some DAO projects have failed in the past, notably “The DAO” in 2016, which was hacked because the founders had neglected to implement sufficient security measures in the smart contract code (Kaal, 2019). As investors struggle to assess which DAOs are most promising to participate in and finance, their investing behavior remains cautious. The prevalent uncertainty can lead to under-investment, resulting in diminished token performance and stunted growth, particularly given the novelty of DAOs as an organizational form. Here, token performance reflects not only the token price but also market interest in a DAO (Wright, 2021). By offering mechanisms that encourage active participation (Ellinger et al., 2024a), DAOs could attract more potential token holders, which in turn may enhance token performance. Therefore, DAO founders must find ways to ensure broad participation through their governance design choices, reducing uncertainty and signaling a DAO’s quality through active token holder participation.

Although the broad and diversified participation of their token holders distinguishes DAOs (Ding et al., 2022b), there is no universal definition of participation. It generally encompasses the motives and outcomes associated with members working together within an organization (Glew et al., 1995) and can yield benefits such as increased productivity and efficiency when fostered adequately (Dachler and Wilpert, 1978). Recent research in the crowdfunding domain illustrates that platform design choices can significantly influence investors’ willingness to participate (Ferrer et al., 2023). Both crowdfunding and DAOs operate in decentralized, noisy environments with competing signals and without traditional governance structures, where design choices can effectively motivate participation, democratize access to capital (Colombo et al., 2022), and enable ventures to send signals to investors (Steigenberger and Wilhelm, 2018). For example, Zhang et al. (2023) find that reliable institutional mechanisms (e.g., platform rules and regulations) and information transparency can boost investors’ perceived value of participation. Yet, Yasar et al. (2022) argue that design choices allowing inefficient use of investors’ funds (e.g., models where funders receive money even without goal achievement) may discourage investors from participating. These insights, however, are not seamlessly applicable to the context of DAOs, not least because of a DAO’s focus on participative governance. In the absence of a clear consensus on best practices for DAO governance designs (S. Li and Chen, 2024; Ziegler and Welpe, 2022), DAO founders seeking to maximize the potential of this new organizational form remain unclear about which governance mechanisms to implement and signal to attract potential token holders. While DAO founders know about the quality of their DAO, potential investors lack such knowledge, which creates an information asymmetry and the need for DAO founders to emit effective signals about their DAOs’ true quality. Against this backdrop, we draw on signaling theory.

Signaling theory and its effect on DAO governance

According to signaling theory, a signaler sends a message to a receiver who observes and interprets the signal before responding (e.g., Connelly et al., 2011; Spence, 1973). Signals can be categorized as either costly or costless, depending on the effort or resources required to send them (Colombo, 2021). A costly signal is defined as one where the signaler expends resources to convey the signal to the receiver (Colombo, 2021). In contrast, a costless signal, or so-called “cheap talk” (Almazan et al., 2008), requires minimal effort or resources (Connelly et al., 2011), such as the voluntary release of unverifiable information in white papers. DAO environments are particularly prone to information asymmetries due to their decentralized nature, anonymous participation, and reliance on complex technologies, making it difficult for potential token holders to assess a DAO’s merit due to limited access to key information. Recent literature on blockchain-based ventures confirms that information asymmetry is especially critical in the context of early-stage ventures and their blockchain token performance (Chod et al., 2022; Roosenboom et al., 2020).

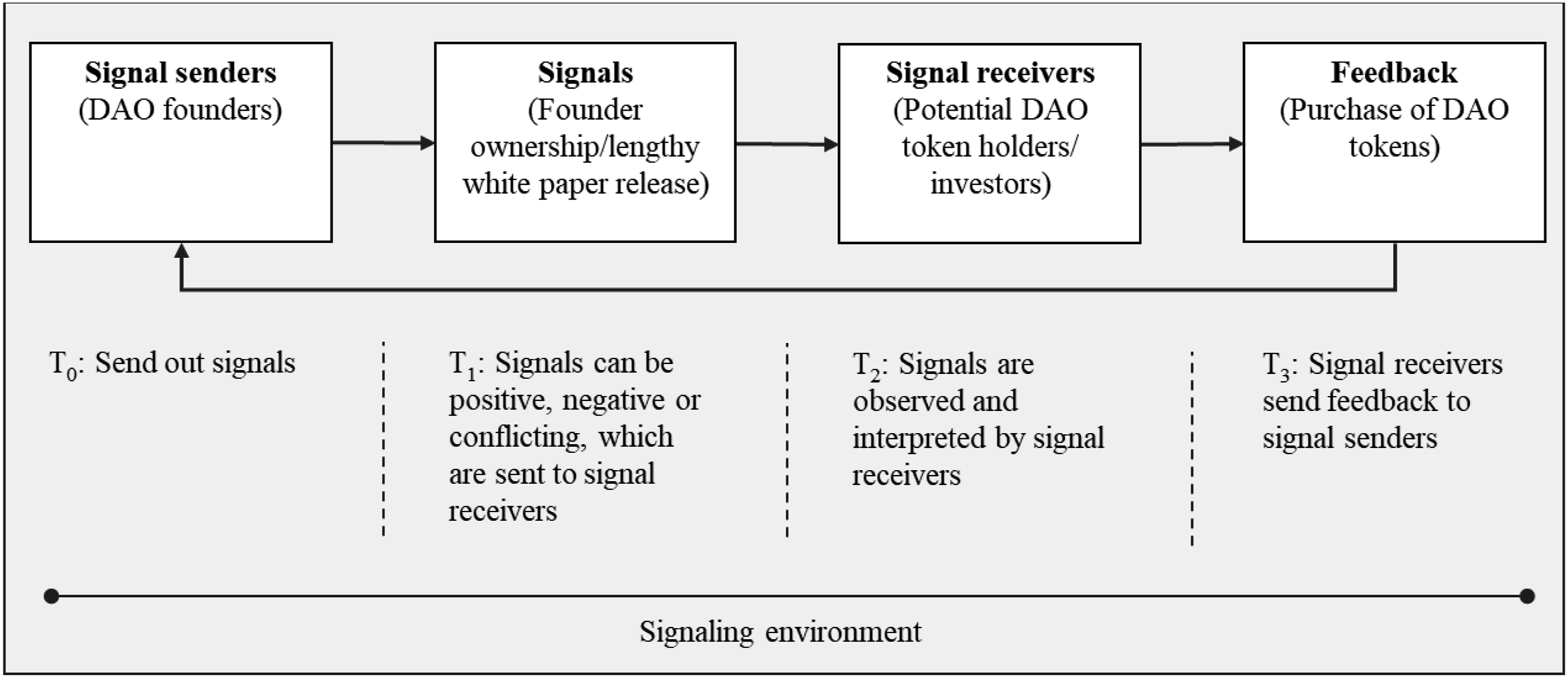

Figure 1 illustrates the signaling process in the context of a DAO. DAO founders are signal senders looking to attract investors during their initial coin offering (Campino et al., 2022). They send signals—such as establishing the DAO founders’ ownership or releasing white papers—to potential DAO token holders, who act as signal receivers and rely on the signaled information (Chod and Lyandres, 2021). Based on the quality and credibility of these signals, potential DAO token holders may provide positive feedback by purchasing DAO tokens, thereby validating the venture’s signals. Or they may furnish negative feedback by not purchasing DAO tokens. Thus, potential DAO token holders rely on costly and costless signals to offer feedback to the signaler by buying the token in noisy environments like the web-3 context (Momtaz, 2021). In this context, examples of costly signals encompass founders holding substantial token investments or participating in fundraising and token-locks to signal long-term commitment. Examples of costless signals in related fields include transparent communication on future roadmaps or FAQ sections to facilitate user interactions and foster trust within the online community. However, signals can also interact, requiring ventures to provide a wide range of information and understand their impact on the receiver (Anglin et al., 2018). Simplified overview of signaling process in DAO context. Source: Own illustration adapted from Connelly et al. (2011).

Thus, signaling theory emphasizes that insiders can strategically convey positive attributes by voluntarily sharing information, thereby enhancing funding success (Howell et al., 2020). However, a DAO’s founders may also send negative signals, casting doubts about their skills and abilities (Amit et al., 1990; Schaefer et al., 2021). Consequently, the governance mechanisms of DAOs have a signaling character toward investors (Howell et al., 2020).

In this study, on-chain governance design choices of DAO founders serve as costly signals to all market participants, whether they seek participative opportunities or are driven by speculative motives, as governance design choices indicate a DAO’s perceived value and future stability. Hence, as token holders focus on high-quality DAOs, which are expected to remain viable in the future, signals that matter to various interest groups, including those seeking decision rights, incentives, or speculative returns, are aligned in their emphasis on high-quality DAOs.

A high-quality DAO is defined by its ability to achieve its vision through democratic governance and broad participation. For investors, quality is thus closely tied to the extent of participation in the governance process, which is essential for realizing the DAO’s overarching vision. Participation ultimately leads to more informed decision-making that aligns with the interests of a diverse group of token holders (Wright, 2021). In this context, quality comprises two key aspects: first, ensuring proper recognition of token holders’ votes in the governance process; second, creating incentives to promote widespread engagement in voting. Against this backdrop, we analyze two particularly salient signals: the MTQ, which relates to the acknowledgment of votes by prescribing a minimum percentage of participating tokens required for proposal approval, and voting incentives intended to foster broad participation among token holders. We focus on these two on-chain governance mechanisms for the following reasons. The MTQ constitutes a costly signal since altering technical governance configurations on the blockchain is resource-intensive and complex (Ding et al., 2022b; Dixit et al., 2022). For example, if the MTQ equals 20% in a DAO, at least 20% of the distributed tokens need to participate in a vote. However, the MTQ also entails the risk of hampering effective governance by potentially requiring too broad participation (Goldsby and Hanisch, 2022). In a worst-case scenario, proposals cannot be passed due to insufficient token holder participation, resulting in a deadlock for the DAO—and ultimately sending a detrimental signal on its quality.

Voting incentives—such as NFTs or additional governance tokens—aim to incentivize token holders to participate in the DAO (Gao and Leung, 2022). For instance, the Decentraland DAO combines blockchain governance with virtual reality, rewarding participants with NFTs that grant virtual land ownership and exclusive items. MakerDAO maintains the stability of DAI, a stablecoin pegged to the US dollar, with decentralized governance mechanisms, incentivizing active participants with additional MakerDAO tokens. These incentives can be seen as a form of financial stimuli because the underlying assets—tokens or NFTs—are tradable (S. Wang et al., 2019), which makes them a costly signal.

Aligning incentives can be an important means to reduce the principal-agent dilemma (Coles et al., 2001). The existence of incentives can, on the one hand, act as a signal to foster participation by narrowing the gap between ownership and control (Halac, 2012); on the other hand, incentives may also signal reward-driven behavior (Saadatmand et al., 2019). Both motivations underscore the importance of evaluating voting incentives, as they can influence token performance by signaling active engagement among potential token holders. Thus, MTQ and voting incentives are DAO design choices that can signal quality and long-term viability, ensuring a DAO’s market competitiveness, thereby reinforcing investor trust and sustaining market interest. As the overall interest in a DAO increases, so likely does its token price.

Founder’s stake as contingent factor

The relationship of such governance design choices with token performance might, however, be contingent on context factors. Thus, another focal aspect of our study is to examine how the founders’ stake impacts the signaling effect of on-chain governance mechanisms, namely, MTQ and voting incentives. Founders with a higher stake in their ventures have substantial sway over the firm and can shape its governance more independently (Nelson, 2003), which can be an asset or a liability (He, 2008). Their psychological commitment can play a pivotal role in governance (Fama and Jensen, 1983), as it can reduce the drain on the organization’s resources and counter agency costs (Nelson, 2003). For example, studies show that having a larger founding and advisory team positively relates to funding success in initial coin offerings due to the higher reputational stake generated (Giudici and Adhami, 2019). Expanding prior research, we argue that we need to better understand the DAO founders’ stake as a contextual factor influencing on-chain governance mechanisms. DAOs have only recently become more prominent and widespread (Bellavitis et al., 2022) but are a different and new type of organization. Hence, it is essential to investigate their governance mechanisms and design choices to comprehend their implications in the evolving landscape of digital blockchain organizations. Beyond their inherent influence in a venture (He, 2008), founders with a larger amount of governance tokens gain more control over their DAOs’ governance by leveraging the voting power these tokens confer (Tsoukalas and Falk, 2020). Thus, absent a proven track record for crowd-involved projects within anonymous, decentralized DAO environments, investors may want to rely on observable traits, such as founder experience or stake, to reduce information asymmetry and foster trust (Courtney et al., 2017).

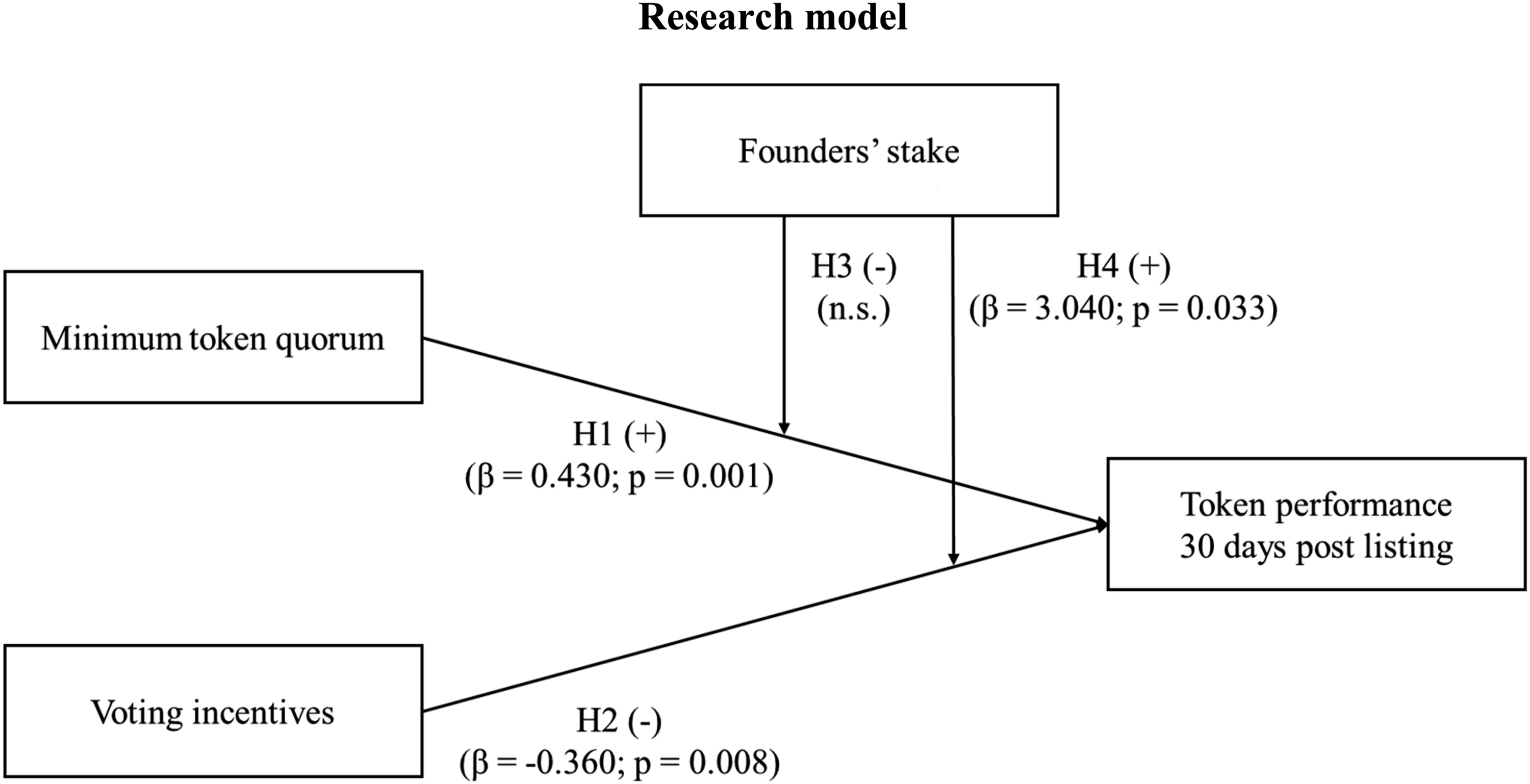

In sum, we argue that on-chain blockchain governance mechanisms, such as MTQ and voting incentives, act as vital signals to potential token holders and are contingent upon the founders’ stake in the DAO, influencing the token performance after a DAO’s listing. Figure 2 illustrates our research model. Research model Source: own illustration.

Hypotheses dsevelopment

Drawing on signaling theory, we examine the effectiveness of two on-chain governance mechanisms and argue that MTQ and voting incentives explain the variance in a DAO’s token performance. In addition, we investigate founders’ stake as a contingency factor that moderates the relationship of MTQ and voting incentives on token performance.

Minimum token quorum and token performance

We argue that DAOs with an MTQ will achieve a higher token performance—indicated through token price changes—than DAOs without an MTQ. Based on signaling theory, the first step in evaluating the effectiveness of signals is assessing whether a signal is costly or not. An MTQ is a technical on-chain feature constituting a costly signal to potential token holders because changing a technical governance design choice in the blockchain is complicated and requires significant resources (Ding et al., 2022b; Dixit et al., 2022). Compared to DAOs without an MTQ, the presence of an MTQ leads to a broader participation of DAO governance token holders, as it mandates achieving a certain threshold percentage of tokens actively involved in the voting process (O’Mahony and Karp, 2022; Schirrmacher et al., 2021). Such an active involvement signals a higher DAO quality, resulting in higher token performance. An MTQ also helps prevent the negative impact of malign proposals launched by bad-faith actors hoping for the inactivity of the other token holders. The mere existence of an MTQ can deter such behavior because fulfilling the quorum necessitates greater engagement from all token holders. Greater token holder engagement increases the likelihood that the collective wisdom of the crowd overrides any malign proposals (Tsoukalas and Falk, 2020). This upside, in turn, can heighten a DAO’s quality by improving its ability to achieve its overarching vision through democratic decision-making. An MTQ can thus result in broader participation and, ultimately, higher token performance.

At the same time, an MTQ reduces information asymmetry for potential token holders by making it transparent that the DAO fosters participation and collective decision-making. It signals founders’ commitment to promoting decentralization while potentially limiting their ability to enforce personal agendas (Dong et al., 2021), which positively affects token performance. Moreover, fraudulent DAOs cannot easily replicate an MTQ because it prohibits them from propelling their agendas by faking broad participation (Yermack, 2017). To summarize, an MTQ is a positive costly signal that encourages broad participation and helps fend off malign actors. Arguing that DAOs implementing an MTQ signal a higher quality of participation rights to potential token holders, we predict that an MTQ will positively relate to token performance.

The existence of a minimum token quorum is positively related to token performance, as indicated through price changes of the token.

Voting incentives and token performance

We argue that the existence of voting incentives is negatively related to token performance. As voting incentives are an on-chain governance feature that has to be written into the source code, their existence constitutes a costly signal analogously to an MTQ (Dixit et al., 2022). A common challenge with participation in DAOs is that token holders can enjoy the contributions of others without becoming active themselves (Goes et al., 2016). Some token holders may decide not to engage actively, simply holding their tokens and relying on others to participate and advance the DAO, which can ultimately affect DAO performance. On the one hand, having voting incentives may signal to potential token holders that the DAO’s founders encourage broad participation, which might constitute a positive signal (Z. Liu et al., 2022). On the other hand, voting incentives may foster participation driven by the pursuit of financial benefits rather than the interest to partake in votes to advance the DAO’s best interests (Yermack, 2017). Potential governance token holders can observe this incentive but cannot determine whether their fellow governance token holders’ motivation lies in the incentive’s financial benefit or a real commitment to advance the DAO; hence, information asymmetry increases, which negatively affects token performance.

Moreover, research on user-generated content, such as online reviews and communication in help forums, indicates that financial incentives are a double-edged sword: incentives can result in higher content volume but lower content quality (Burtch et al., 2018). The same applies to DAO participation. Governance token holders perceive an incentive to vote without properly considering the proposal because they only vote to receive the financial reward, which sends a negative signal to potential token holders. This negative signal indicates a DAO’s lower quality by undermining its core objective of achieving its vision through broad participation, as decisions no longer reflect genuine collective decision-making in the best interest of the DAO and, consequently, all token holders. Hence, token performance will decrease. In addition, distributing tokens and minting NFTs consumes DAO resources, resulting in fewer resources available to advance the technology or product (Cong et al., 2021; Kranz et al., 2019)—once more signaling lower DAO quality and decreasing token performance. In sum, the existence of a voting incentive governance mechanism is a costly signal that negatively affects token performance by incentivizing qualitative inferior participation, resulting in inferior token performance and a signal of lacking the resources necessary to realize the DAO’s purpose. Moreover, voting incentives increase uncertainty for potential governance token holders as information asymmetries increase. Thus, we hypothesize:

The existence of voting incentives is negatively related to token performance, as indicated through price changes of the token.

The moderating role of founders’ stake

Based on signaling theory, we propose that a higher founders’ stake will negatively moderate the positive relationship between an MTQ and token performance. We see two reasons for this: First, from a signaling perspective, a higher founders’ stake results in higher centralization and substantial decision-making power of founders, reducing broad participation opportunities for potential governance token holders (Belitski and Boreiko, 2021; Forte et al., 2009) and, consequently, weakening the MTQ-token performance relationship. Greater centralization thus lessens the influence of individual token holders, impeding the effectiveness of the signal of broad participation that an MTQ implies, ultimately decreasing token performance.

Second, an MTQ is an on-chain governance mechanism implemented to foster governance token holders’ broad participation (O’Mahony and Karp, 2022; Schirrmacher et al., 2021). The more tokens the founders possess, the easier it is for them to reach the MTQ without encouraging broad participation by other governance token holders, making the quorum obsolete. Therefore, a higher founders’ stake sends a conflicting signal to potential governance token holders because it contradicts and diminishes the participating nature of MTQs. Hence, we expect that a signal of a higher founders’ stake weakens the positive relationship between the existence of an MTQ and token performance. We hypothesize:

A higher founders’ stake weakens the positive association between the existence of a minimum token quorum and token performance, as indicated through price changes of the token. However, a higher founders’ stake can be a double-edged sword. As previously argued, the existence of voting incentives may emit the negative signal of a voting behavior where token holders vote primarily for the sake of financial benefits (Burtch et al., 2018; Y. Liu and Feng, 2021; Yermack, 2017). This scenario allows less engaged token holders to align their votes with the majority simply to gain incentives. However, as a higher founders’ stake centralizes power (Tsoukalas and Falk, 2020), it also positions the founders as role models within the organization (Fama and Jensen, 1983; He, 2008), which might induce the majority of token holders to vote in line with the founders (Nelson, 2003). Consequently, the influence of bad-faith token holders—who vote solely for the reward’s sake—diminishes (Nemeth, 1986). This is especially relevant in environments of high uncertainty, such as new ventures, where individuals can mitigate perceived voting stress by aligning with the majority. Such alignment provides the psychological assurance of going with the argument that there is strength in number and fosters a sense of social connection to the majority group (Baker and Petty, 1994; D. Zhang et al., 2007). Ultimately, this dynamic weakens the negative relationship between voting incentives and token performance, as the alignment of votes among token holders and founders can serve as a quality signal. A higher founders’ stake might also mitigate the influence of potential resource expenditures directed at voting incentives. Specifically, their higher stake indicates the founders’ extraordinary dedication to their project’s governance system and a deeply rooted alignment between ownership and proposal outcomes, potentially reducing the drain on organizational resources (Fama and Jensen, 1983). Hence, we argue that a higher founders’ stake moderates the relationship between the existence of on-chain voting incentives and token performance in that it weakens the negative effects of voting incentives.

A higher founders’ stake weakens the negative association between the existence of voting incentives and token performance, as indicated through price changes of the token.

Methodology

Sample

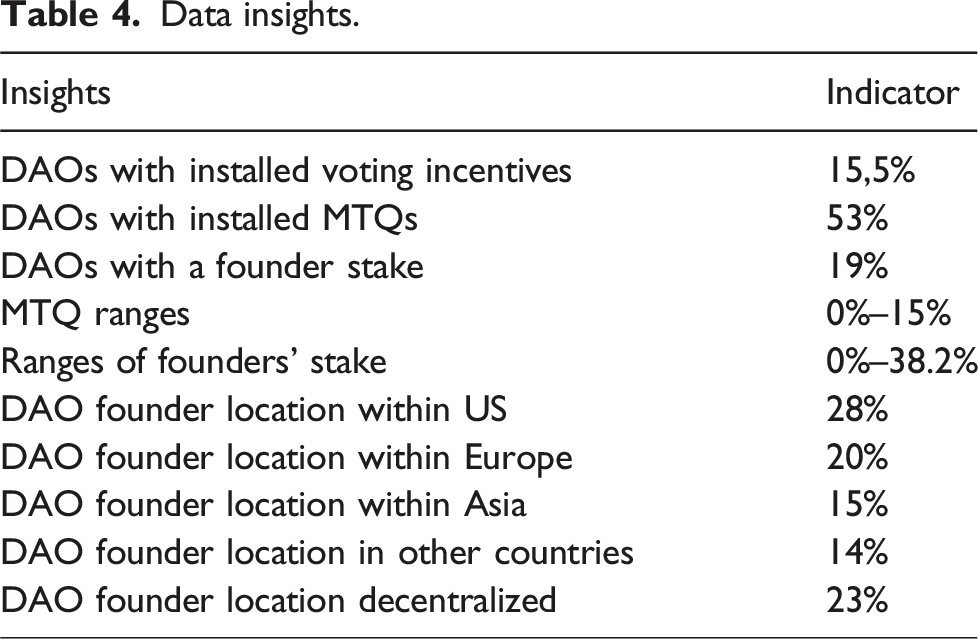

Data insights.

We checked whether our sample includes so-called scam tokens by comparing our sample to several websites tracking scam tokens (deadcoin.info, nomics.com, coinopsy.com, 99bitscoins.com, scamnewschannel.com on scam tokens). Our findings confirm that our dataset contains no scam tokens. Setting up a DAO entails establishing a complex smart contract infrastructure and implementing a voting process (Norta, 2015). Given this inherent complexity, it is not surprising that we find no scam tokens in our sample. Criminals trying to defraud potential token holders would rather take the easier way through an initial exchange offering or direct token sale, thereby perpetuating the issue of scams among ICOs (Boreiko and Vidusso, 2019).

Measures

Dependent variable

We measure our dependent variable token performance by calculating the percentage return based on a DAO’s token price 30 days after its initial listing on an exchange (Chod and Lyandres, 2021; Colombo et al., 2022; Lowery et al., 2010). This percentage return indicates how much a token’s price has increased or decreased over this period. Following prior research, we winsorized the returns at 5% on both ends (Fan et al., 2007; Fisch and Momtaz, 2020). The feedback of potential DAO token holders to purchase a token or not acts as a valuable proxy for the overall sentiment towards key governance features (Hsieh and Vergne, 2023). The time horizons were chosen to incorporate short-to-medium term token dissemination (Chod and Lyandres, 2021).

Independent variables

As the information on DAO governance is not standardized, we manually obtain our independent variable data from the planned on-chain governance descriptions in ventures’ published information before the initial token listing (Schaefer et al., 2021). Within the context of this study, on-chain governance information consists of two binary independent variables. The variable minimum token quorum (MTQ) relates to the existence of a minimum quorum of tokens needed to vote for a proposal and for the proposal to pass; for example, at least 10% of token holders must participate in the vote. The variable voting incentives refers to the existence of voting incentive schemes; for example, voters receive more tokens for participating in the governance process.

Moderating variable

We measure our moderating variable founders’ stake through the percentage of tokens held by the founders. This variable indirectly measures the decision-making power of DAO founders because tokens are used for voting (Axelsen et al., 2022; Wiriyachaokit et al., 2022).

Control variables

We follow adjacent research to control for factors on the firm, signal dissemination, technological, and industry level. Furthermore, we control for the influence of off-chain governance mechanisms on token performance (Coles et al., 2001; Hoetker and Mellewigt, 2009). On the firm level, we use team size to control for the founding team (Fisch and Momtaz, 2020; Giudici and Adhami, 2019). We control for the influence of social media with the number of social media channels a DAO uses (Grau and Bendig, 2019), with white paper existence (Florysiak and Schandlbauer, 2022; Howell et al., 2020), and the total number of tokens initially released. On the technological level, we control for the technology applied by checking whether the underlying usage of the Ethereum blockchain has an influence; we also control for the transparency of technology through the binary variable of an active GitHub account where the code is published (Fisch, 2019; Howell et al., 2020; Roosenboom et al., 2020). On the industry level, we control for the price development of the cryptocurrency market in the post-listing period (Schaefer et al., 2021). We do so by using the Crypto-Currency index (CCi30), an index containing the 30 most significant cryptocurrency positions (Livieris et al., 2022) and thus acting as a proxy for the volatility of the overall crypto token market (Aslan et al., 2021; Beinke et al., 2021). We included year dummies to capture the influence of specific events in the year of release.

Results

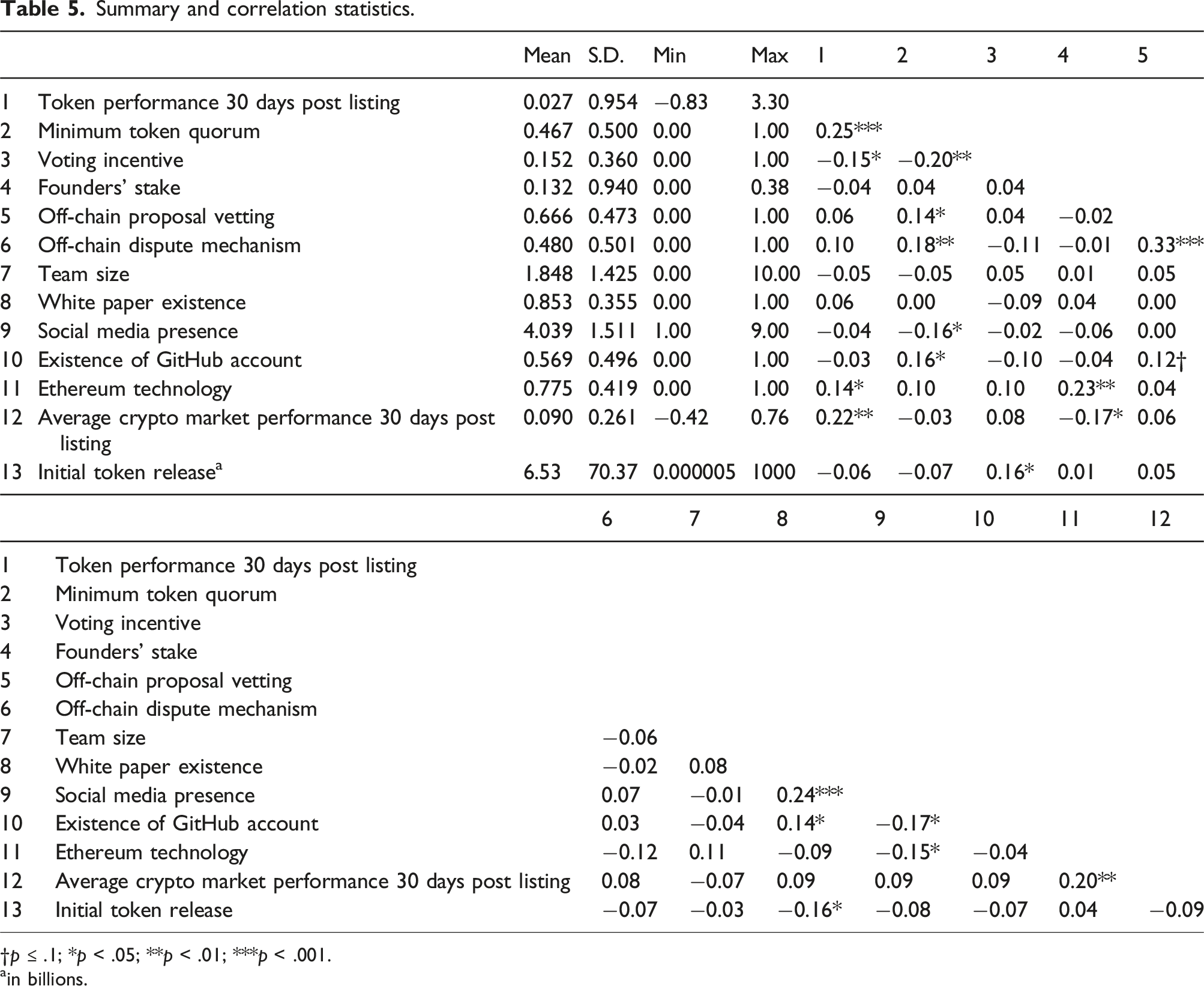

Summary and correlation statistics.

†p ≤ .1; *p < .05; **p < .01; ***p < .001.

ain billions.

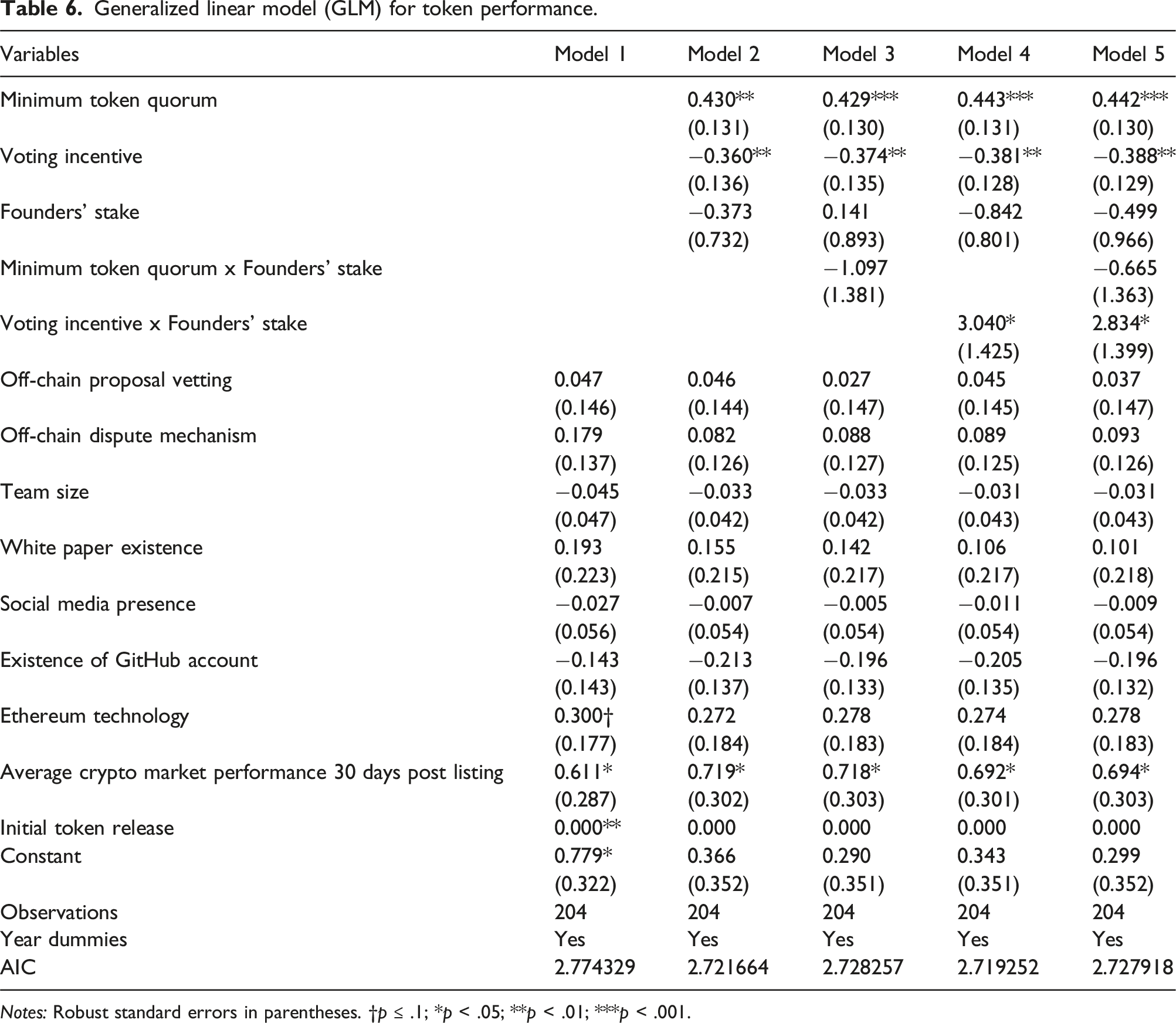

Generalized linear model (GLM) for token performance.

Notes: Robust standard errors in parentheses. †p ≤ .1; *p < .05; **p < .01; ***p < .001.

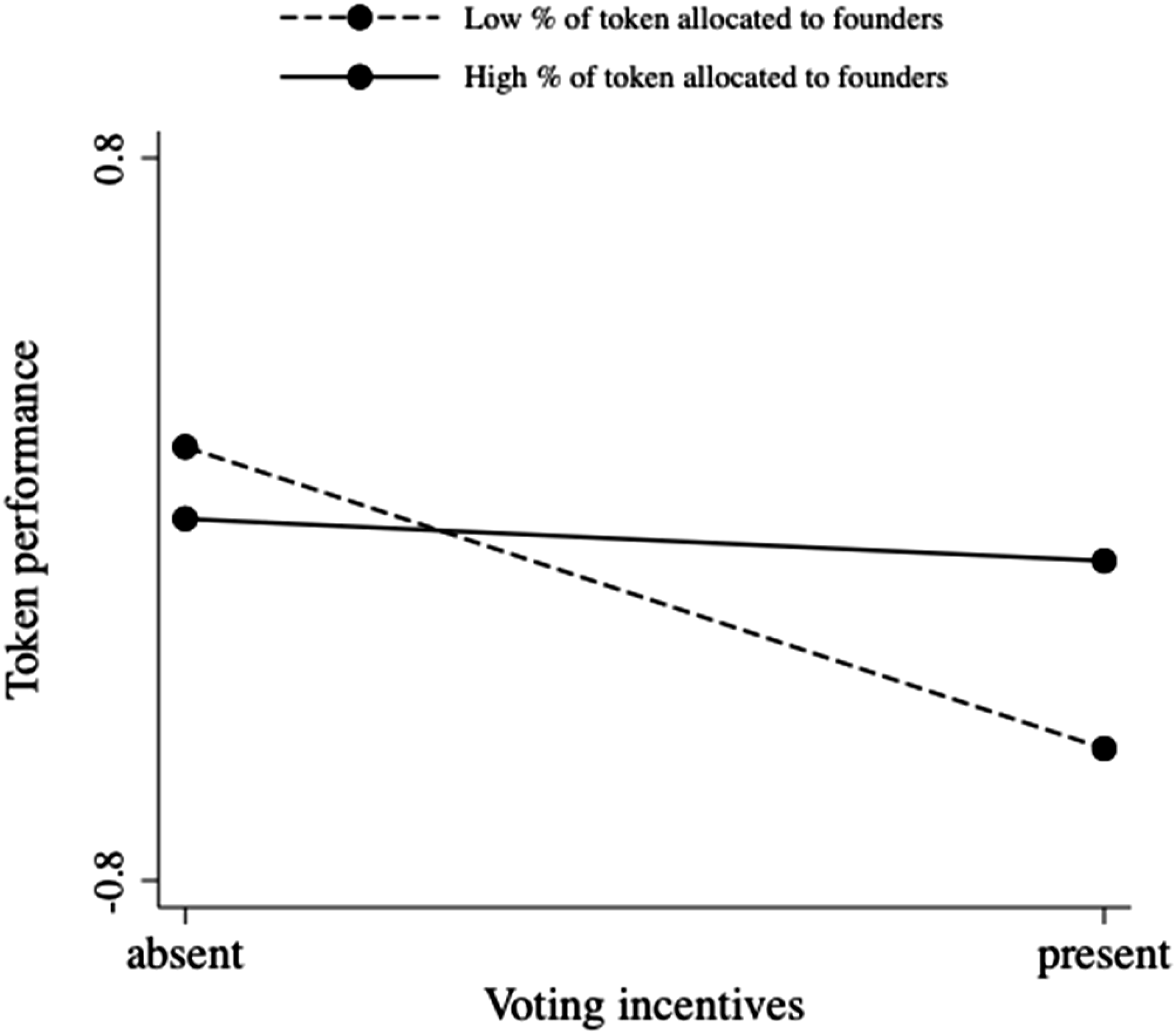

In hypothesis 1, we argue that the existence of an MTQ is positively related to token performance. Our results in model 2, as presented in Table 6, support this notion (β = 0.430; p = .001). Hypothesis 2 proposes that having a voting incentive is negatively related to token performance. Our estimation model finds evidence for this relation in model 2 (β = −0.360; p = .008). Hypothesis 3 argues a moderating effect of founders’ stake on the relationship between minimum token quorum and token performance. We introduce this moderating effect in model 3. Table 6 depicts that the results are not significant (p > .1). In hypothesis 4, we argue for the moderating effect of founders’ stake on the relationship between voting incentives and token performance. Table 6 illustrates this moderating effect in model 4, showing a significant, positive interaction term between voting incentives and founders’ stake (β = 3.040; p = .033). We interpret this result at low and high levels of founders’ stake (i.e., one standard deviation below and above the mean) by testing the slopes shown in Figure 3. The relationship between the existence of voting incentives and token performance moderated by founders’ stake. Source: Own illustration.

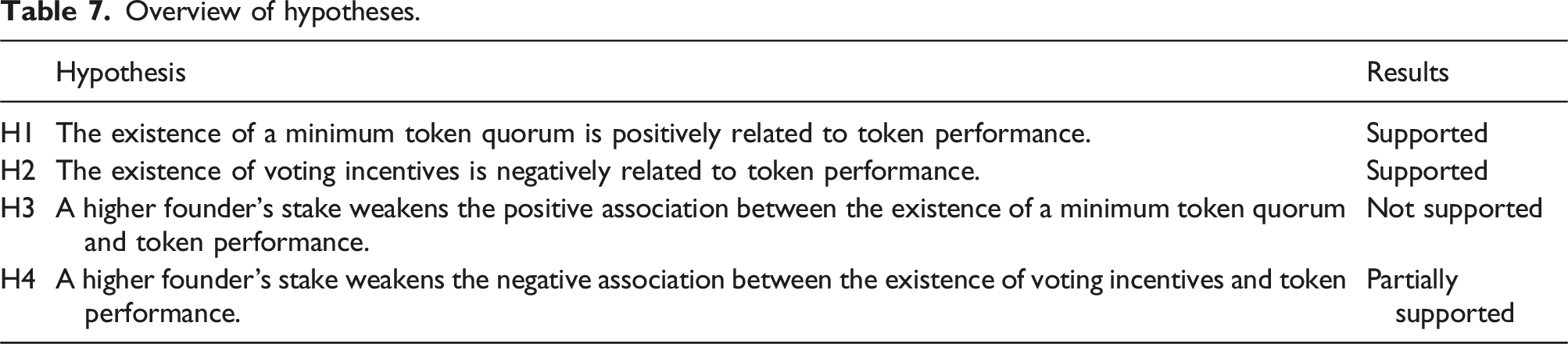

Overview of hypotheses.

Supplemental analyses

Sample selection

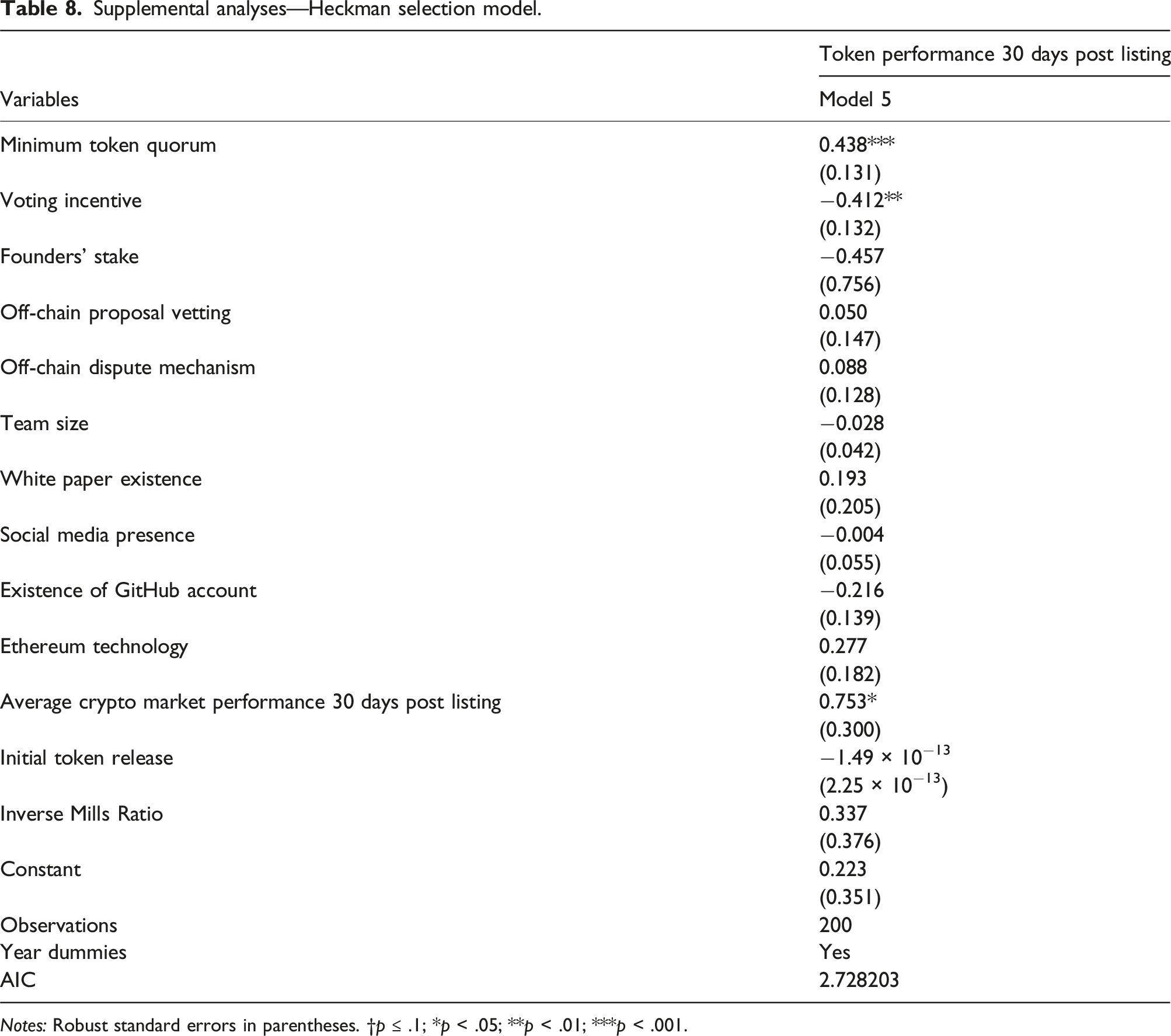

Supplemental analyses—Heckman selection model.

Notes: Robust standard errors in parentheses. †p ≤ .1; *p < .05; **p < .01; ***p < .001.

Omitted variables bias

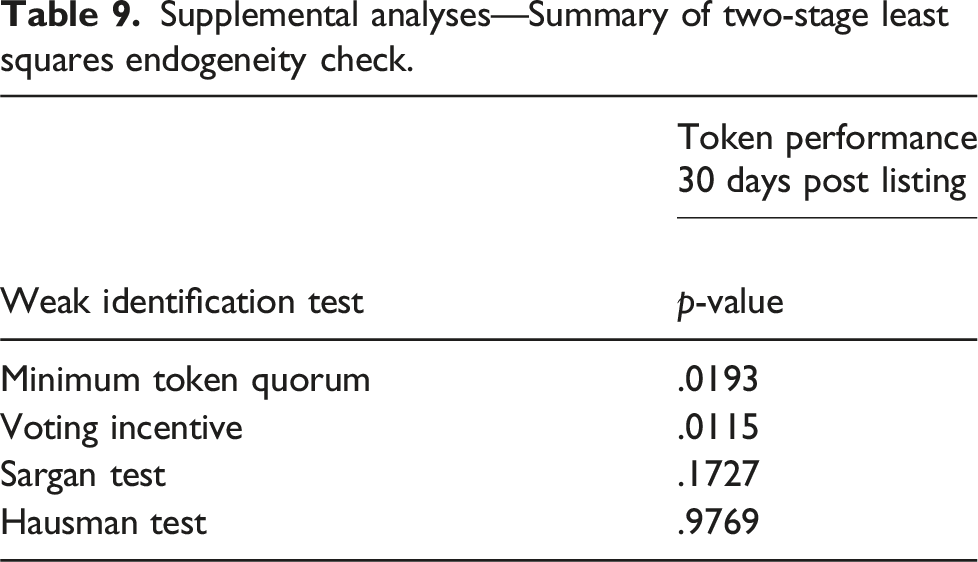

Supplemental analyses—Summary of two-stage least squares endogeneity check.

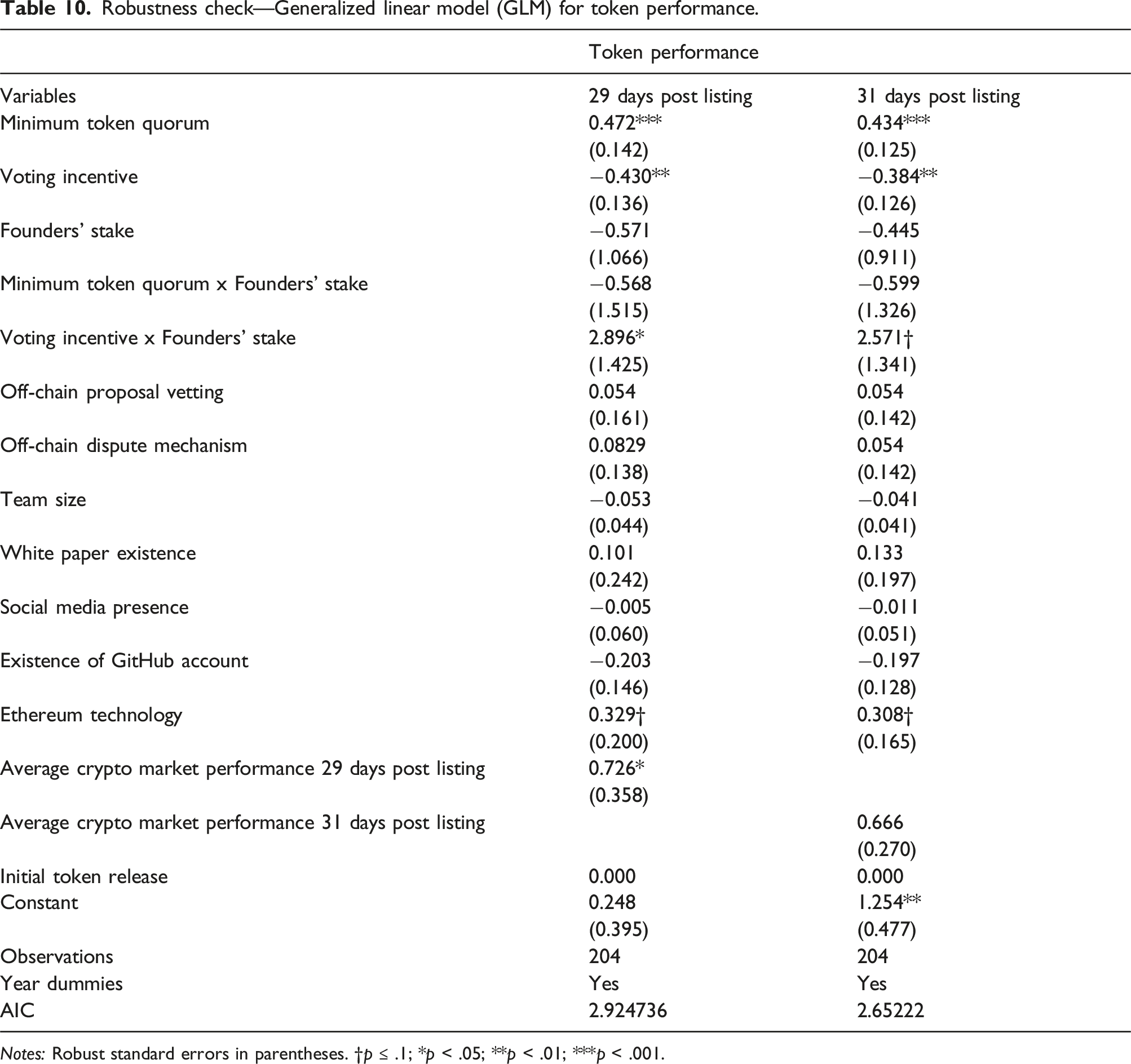

Robustness

Robustness check—Generalized linear model (GLM) for token performance.

Notes: Robust standard errors in parentheses. †p ≤ .1; *p < .05; **p < .01; ***p < .001.

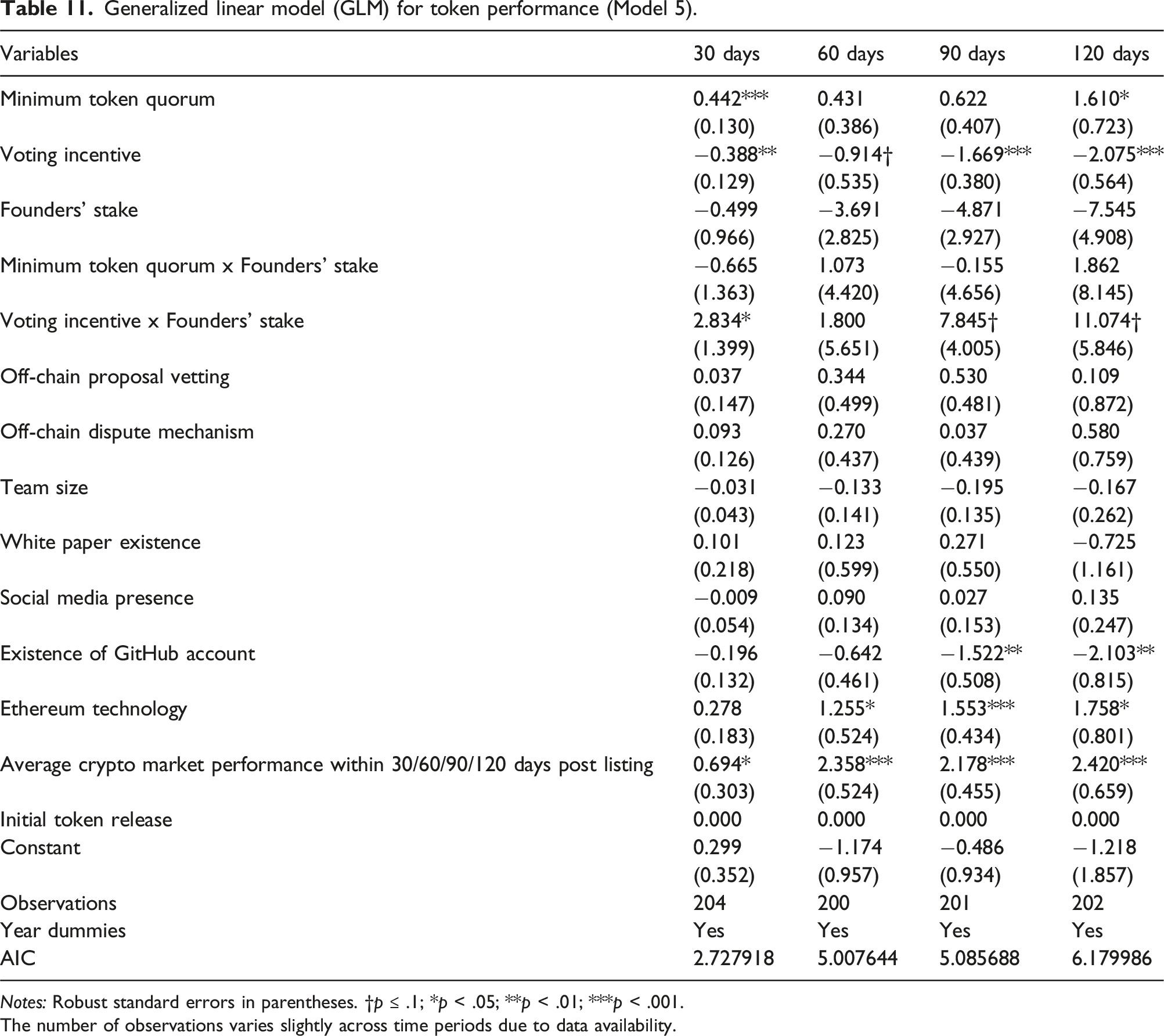

Generalized linear model (GLM) for token performance (Model 5).

Notes: Robust standard errors in parentheses. †p ≤ .1; *p < .05; **p < .01; ***p < .001.

The number of observations varies slightly across time periods due to data availability.

Moreover, to analyze further the non-significant interaction between MTQ and the moderating variable founders’ stake, we compute an additional variable by calculating the percentage difference between MTQ and founders’ stake (n = 149). We thus seek to explore how the relative difference between MTQ and founders’ stake affects token performance. However, the corresponding coefficient is not significant (p = .971), reaffirming the results of our main analysis.

Finally, we also examine whether the actual percentages of MTQ affect token performance. We do not find evidence for such a relationship. Table A1 in the Online Appendix shows these results in more detail.

Discussion

Theoretical implications

Our study makes three main contributions to the literature at the intersection of information systems and DAO governance. First, we identify effective signals in the emerging field of DAOs, which differ fundamentally from signals previously studied in blockchain contexts (Colombo, 2021). Specifically, we reveal two opposing signaling effects: the installation of an MTQ, which has a positive association with token performance, and of voting incentives, which show a negative relationship. While existing research has explored signals in blockchain-based platforms, such as how a founder’s past success and credibility can reduce information asymmetry (Courtney et al., 2017), these signals might not be equally effective in the context of DAOs. Particularly, the decentralized governance structure of DAOs shifts the focus from individual founder credibility to collective participation and consensus-building among token holders (Ding et al., 2022). As a result, signals that work in rather centralized settings may carry less weight in DAOs.

Prior research highlights the benefits of fostering participation as a distinct quality feature in DAOs (O’Mahony and Karp, 2022; Schirrmacher et al., 2021; Wiriyachaokit et al., 2022), finding that token incentives in decentralized DAO settings can significantly encourage user participation compared to curated platforms (Gao and Leung, 2022). Interestingly, our study challenges the assumed positive impact of voting incentives, presenting evidence that they negatively affect token performance, as they also signal fewer participatory opportunities and lower DAO quality. These findings support the notion that voting incentives can be a double-edged sword: Despite potentially increasing participation, they can also undermine the DAO’s democratic purpose by encouraging inferior participation and diverting resources. This is particularly relevant in light of recent research underlining the unique governance challenges of DAOs and their voting systems (Goldberg and Schär, 2023), the cost of on-chain voting (Bellavitis and Momtaz, 2024), and the tension between financial rewards and sustained contributions to the DAO (Ellinger et al., 2024b). We particularly add to research that calls for more empirical evidence on DAOs’ governance mechanisms (Goldberg and Schär, 2023; Lumineau et al., 2021) by examining how DAOs depart from so-far established notions of governance, such as incentives (Beck et al., 2018; Constantinides et al., 2018). Furthermore, although not hypothesized, our empirical results also show that off-chain governance control variables do not significantly affect token performance, underscoring the influence of on-chain governance mechanisms as signals. Two potential explanations support this view. First, on-chain governance mechanisms tend to be more resource-intensive, making them more costly signals compared to off-chain mechanisms (Dixit et al., 2022). Second, the anonymity of collaborating parties in blockchain environments enhances the effectiveness of on-chain governance (Beck et al., 2018), while off-chain governance relies on the identifiability of collaborators (Lumineau et al., 2021). We contribute to the DAO governance literature by theoretically and empirically demonstrating that on-chain governance mechanisms serve as costly signals through their rigorous enforcement, thereby shaping reliance and participation, which are essential for the effective functioning of DAOs as self-governing entities.

Second, our research enriches the discourse on DAO governance (e.g., Beck et al., 2018; Santana and Albareda, 2022; Wright, 2021) by offering nuanced implications of the interaction between governance signals and contextual factors. Specifically, our results help determine the context sensitivity of the analyzed signals, suggesting a disparate influence of the contextual factor founders’ stake (T. Wang and Song, 2016). In particular, and as hypothesized, voting incentives show context sensitivity regarding founders’ stake, as the negative relationship between voting incentives and token performance is especially pronounced when the founders’ stake in their DAO is lower. Put differently: When founders keep only a few of their DAO’s tokens, on-chain governance mechanisms giving more incentives to token holders to participate in voting are perceived as signaling lower quality, thereby decreasing token performance. Interestingly, when the founders’ stake is higher, the relationship between voting incentives and token performance becomes non-significant, speculatively suggesting that a high founder stake could offset the negative effect of voting incentives. With these findings, our research advances the understanding of how on-chain mechanisms are not universally effective but can instead also be sensitive to contextual factors (Lumineau et al., 2021), ultimately shaping DAO performance.

In addition, we find that the signaling effect of an MTQ remains unaffected by the moderating variable founders’ stake, meaning that the existence of an MTQ affects token performance independent of the founders’ stake in their DAO. Thus, an MTQ seems to unfold its impact on token performance in a more isolated manner. However, future research should explore additional context factors, thereby establishing whether an MTQ works in isolation.

Third, our study demonstrates the importance of negative signals in the DAO context, which existing literature on signaling theory has largely overlooked. Although current research indicates that negative signals, such as failed proposals, play a crucial role in shaping investor perceptions in other contexts, they have received less attention than positive signals (e.g., Bell et al., 2008; Fischer and Reuber, 2007; Taj, 2016). By examining how voting incentives as a negative signal impact token performance, we advance the understanding of how such signals influence investor decisions and thereby token performance. Our insights are valuable for research on signaling theory as “in the context of new ventures, a […] description of […] both positive and negative information may be more effective than an excessively positive presentation of the venture [which may] reduce the likelihood of unintended signals”. By showing the negative signaling impact of voting incentives, we address this gap and particularly expand knowledge regarding unintentional negative signals.

Practical implications

Our research has practical implications for both DAO founders and DAO token holders. First, DAO founders should carefully evaluate the signals their on-chain governance choices convey. Our study suggests that signals that positively invite broad participation relate to higher token performance. Therefore, founders should not only evaluate whether their chosen on-chain governance mechanism invites the participation of governance token holders but also what type of participation. Second, our findings indicate that retaining tokens as a founder can positively influence the signals of on-chain governance mechanisms. Consequently, founders should keep this in mind when considering reducing their stake to receive funding.

Our findings also benefit governance token holders in two ways: First, they provide a better understanding of the factors driving token performance, allowing them to decide whether to hold a specific DAO’s governance token. Second, our findings can help them better understand the underlying consequences of on-chain governance design choices and the ability to participate in the DAO’s decision-making.

Limitations, future research, and conclusion

Our study has several limitations that offer avenues for future research. Our study presents theory on the relationship between pre-listing signals and post-listing token performance. We chose specific salient on-chain blockchain signals for our analyses; however, an abundance of other on-chain and off-chain governance mechanisms and contextual factors and their respective signals warrant further inquiry. Future research could examine the impact of signals such as reputation and staking on DAO governance and investor trust as well as the interaction between on-chain and off-chain governance mechanisms and their respective importance. Furthermore, researchers could take a more direct approach to potential token holders and conduct experiments or surveys to shed further light on their motives and needs to better interpret different signals in the DAO context. Lastly, our selection of an event-based model was driven by the rather recent emergence of the DAO phenomenon. Future research could explore longitudinal data to examine the long-term signaling effects in this evolving field.

Supplemental Material

Supplemental Material - The power of governance: A study on the relationship between on-chain DAO governance and token performance

Supplemental Material for The power of governance: A study on the relationship between on-chain DAO governance and token performance by Julie Saesen, Bastian Kindermann, Darius Abel, and Steffen Strese in Journal of Information Technology

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.