Abstract

The digital transformation of the FinTech industry has revealed a plethora of significant challenges for industry decision makers and wider stakeholder groups as organisations contend with the onset of new regulatory frameworks, legacy systems, flexible business models and alignment with corporate social responsibility practice. The reshaping of organisations and drive to greater levels of decentralisation and employee centric practice, presents a cultural shift for the sector, with implications for the success and resulting benefits of change across the industry. This study aims to develop novel insight to the ‘lived in’ impact of digital transformation within the FinTech industry from a factor interdependency perspective. This research adopts a mixed methods approach incorporating Interpretive Structural Modelling, Analytical Hierarchy Process and interviews with expert participants, to offer a unique perspective on the challenges and unintended consequences of industry level technological change. The findings highlight the high levels of interdependency and priority for challenges related to the investment in products and infrastructure for new markets, criticality of stakeholder support and development of a digital mindset for the adoption of new technologies.

Keywords

Introduction

The process of digitalisation has revolutionised the finance industry, engendering significant levels of disruption and disintermediation of existing business models and practice. The established dominance of the banking sector by the traditional ‘bricks and mortar’ service providers has been challenged via the transformative adoption of technology, new channels of customer interaction and innovative financial products offered by new entrants to the sector (Agarwal and Zhang, 2020; Mărăcine et al., 2020). This digital-led change by challenger banks such as Monzo, Startling, Metro, etc. has been driven by the increasing use of big data and development of interactive mobile centric products, that have directly appealed to younger demographics unconcerned by the ‘online-only’ focus of operations (Agarwal and Zhang, 2020; Alt et al., 2018).

As new entrants continue to expand market share via data and customer-centric business models, innovative use of automation and technology adoption, incumbent banks have faced an urgent need to modernise existing systems to remain competitive. This process of modernisation via digital transformation has significantly disrupted established banks that have experienced high costs of branch-based models, changing consumer behaviours and mandatory adherence to stringent regulatory requirements (Breidbach et al., 2020). Many traditional banks have been slow to adapt to the digital age, constrained by the established silo-based corporate structures and reliance on dynamically complex legacy proprietary Information Systems (IS) and technical architecture (Hoffmann, 2017; Lauterbach et al., 2020). The changes in customer behaviour and impact from the COVID pandemic, has forced many traditional banks to significantly invest in new technology and adapted processes, to offer the range of digital financial services, adoption of contactless payments and mobile interaction as demanded by consumers. This has presented significant and complex challenges for established banking and financial services organisations (Al Nawayseh, 2020; Fu and Mishra, 2020). The pace of transition to an integrated digital infrastructure has been somewhat constrained by a disparate complex legacy technical architecture, silo-like working process and burdensome mandated regulatory compliance that does not exist in the same form for challenger banks (Alt et al., 2018; Dapp, 2017; Vasiljeva and Lukanova, 2016).

Unconstrained by the legacy issue of the traditional banks, new markets entrants to financial services have established market share by embracing agility, developing new innovative interactive financial products, and alignment with a strategy geared toward online-only, business models (OECD, 2020). The increasing levels of adoption of online-only banking services has significantly increased between 2019 and 2022 with one quarter of UK adults operating an account by 2022 with banks that offer internet only services, compared to just nine percent in 2019 (Statista, 2022). Challenger banks have succeeded in developing a set of innovative digital products and data-driven streamlined business models, that have transformed the payments sector and automated many previously entrenched and inherently inefficient processes with a focus on mobile centric interaction and low fees (Khrais and Shidwan, 2020; Rahi et al., 2019).

Although existing banks have suffered from significant disruption from the increased levels of competition, different regulatory framework and transition to digitalisation (Dapp, 2017, 2015), their historical dominance within the sector does present some advantages that can be used in the development of new products and services. The typical younger demographic customers of the challenger banks do not have the long-term finance history of established traditional banking customers, thereby operating on a different set of trade-offs and risk reward model (Broby, 2021). This offers established banks the opportunity to develop deeper data insights on their established customer base and deliver a wider and personalised set of products and services (Johnson, 2021). Although many challenger banks operate within a different – less burdensome regulatory framework, established banks can offer a much greater protection via the Financial Services Compensation Scheme (FSCS) for their products and services (Agarwal and Zhang, 2020; Goh and Arenas, 2020).

Whilst aspects of the literature have explored some of the underlying complexities within the banking industry and the impact of the significant levels of innovative change driven by new entrants (Agarwal and Zhang, 2020; Broby, 2021; Chanias et al., 2019; Dapp, 2017; Khrais and Shidwan, 2020; Vasiljeva and Lukanova, 2016), researchers have omitted to assess these challenges from the interdependency and hierarchical perspective. This gap in the existing research highlights a lack of meaningful insight to the underlying driving and dependence characteristics directly related to the challenges from digital transformation. In the light of these aspects, we propose the following research questions: (1) (2)

We explore these research questions and perspectives through an interpretive and hierarchical lens, utilising the views and expertise of expert participants from the financial technology industry, to gain valuable insight on this topic and its impact on the financial sector. Methodologically, this study utilises a mixed methods approach. This incorporates Interpretive Structural Modelling (ISM) to assess the interdependencies between the factors and the application of the Analytical Hierarchy Process (AHP) to develop the hierarchical structure of the key factors. This approach is supported by interviews with expert participants to gain a detailed insight to the many challenges and complexities facing decision makers.

We organise the paper as follows. In the literature review we identify key factors directly related to the digital transformation of the financial sector. In the research methodology section, we discuss the approach utilised within this research. Our results are presented in the following section and are then discussed. Our theoretical contributions are next presented, and the paper concludes where we outline the limitations of the research and develop future research directions.

Literature review and challenge identification

Literature review process

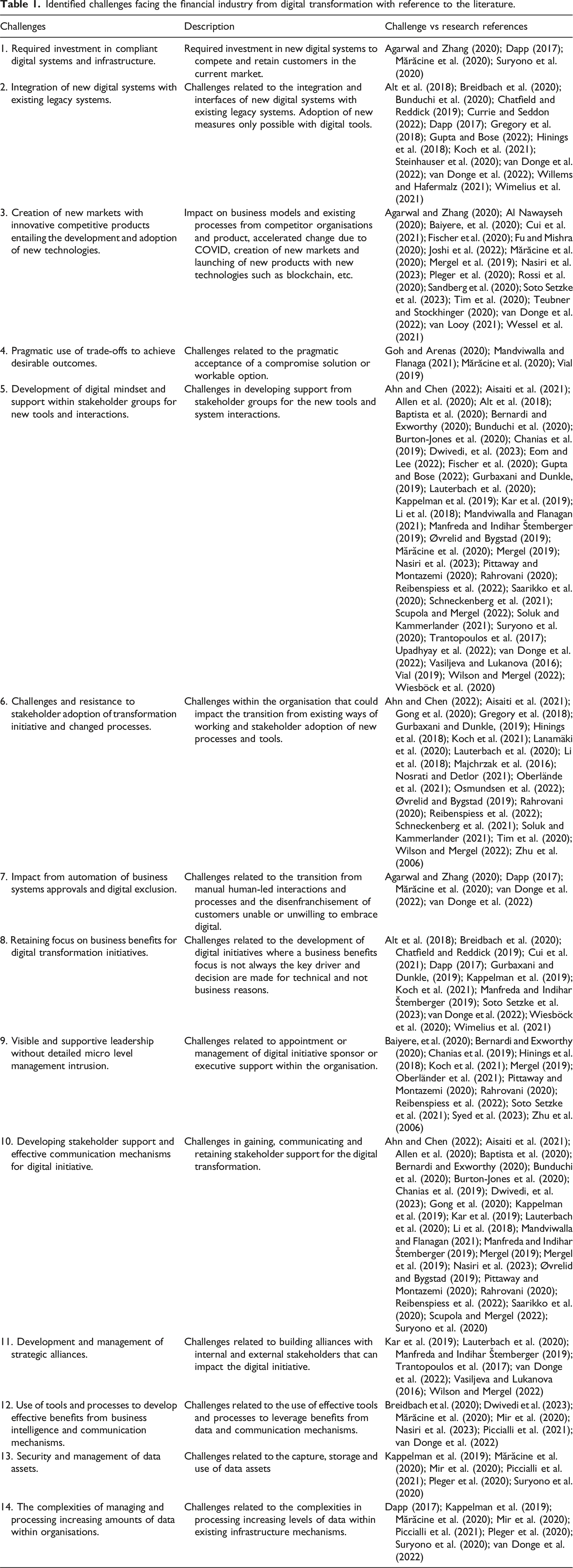

Identified challenges facing the financial industry from digital transformation with reference to the literature.

Digital transformation challenges

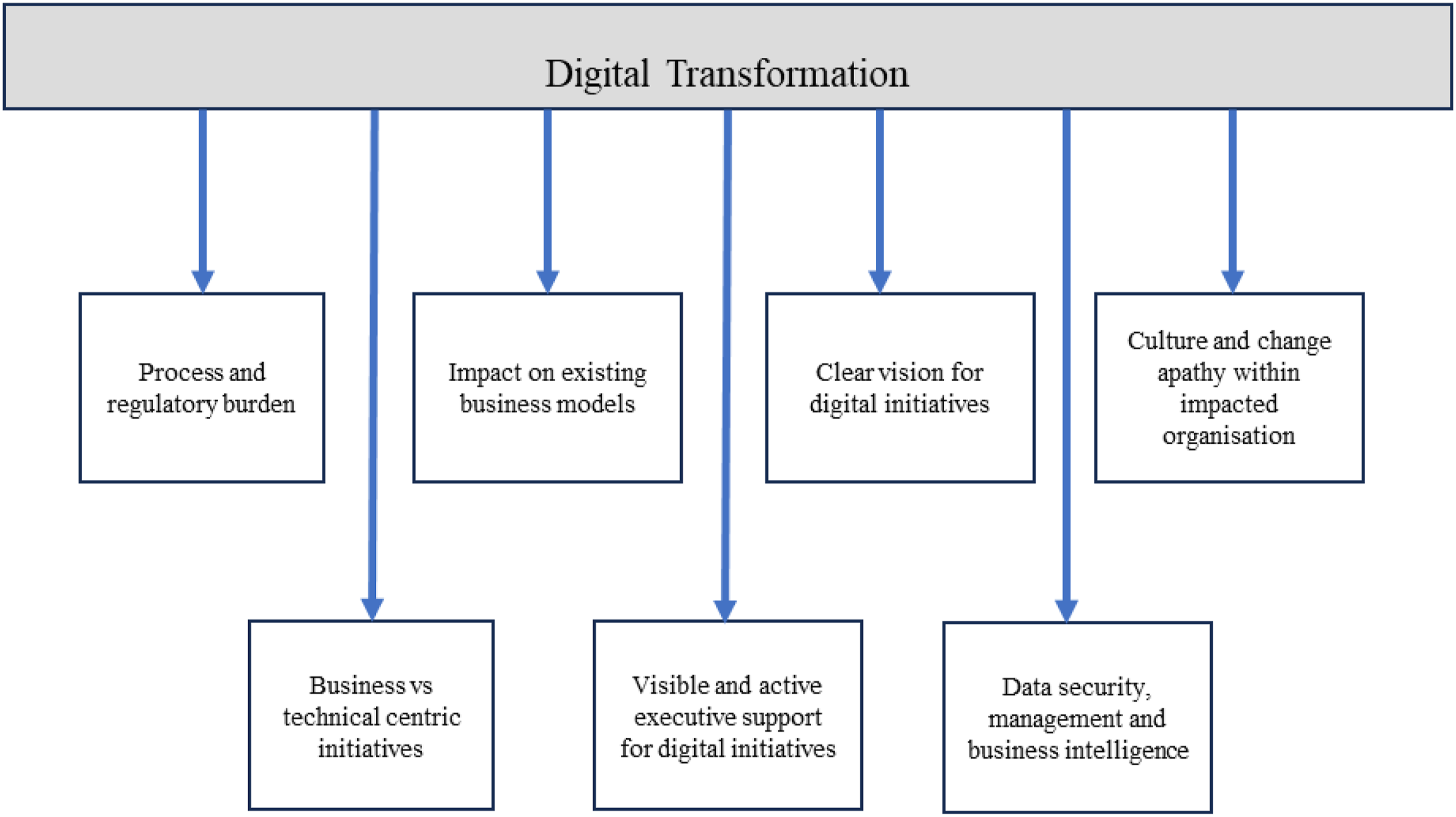

The literature has articulated the concept of digital transformation primarily relating it to the resulting impact from the adoption and interaction with new technologies and the migration away from legacy-based tools and processes (Brunetti et al., 2020). Advances in digital technologies such as cloud computing, big data analytics, artificial intelligence together with the transition to mobile-based commerce and interaction, have heralded a new era within IS, where few businesses, industry, organisation or human activity is not impacted from its effects (Curran, 2018; Hess et al., 2016). Studies have highlighted that many organisations are viewing their internally focussed, efficiency-driven transformations as a pathway to future growth opportunities, helping to define new and agile ways of working, delivering significant benefits and operational effectiveness (Schroeck et al., 2019). Researchers have analysed the wide-ranging impact from digital transformation initiatives across many genres of industry, focussing on the disruption of business models from a challenge perspective, categorising the core elements affecting organisations as they strive to adapt to the resulting changing operational landscape (Vial, 2019). As outlined in Figure 1, this challenge-based perspective within the literature follows a number of overarching themes of research that focus on the varied and often interconnected factors, directly associated with digital transformation. Themes linked to digital transformation.

Themes: process and regulatory burden, impact on existing business models

These themes are generally associated with the complexity surrounding the transition from traditional bricks and mortar, and in-person based business models – to one more reliant on a digital infrastructure (Mărăcine et al., 2020; Steinhauser et al., 2020; Willems and Hafermalz, 2021). This particular aspect has been linked to the decline in the traditional banking industry due to increasing levels of regulatory burden and the emergence of digital only providers, better able to leverage the benefits of digital-based products and services (Agarwal and Zhang, 2020). The stringent compliance regulations applied to the established financial industry have required existing operational systems to shape and adapt to a changing legal and fiscal environment subject to institutional policy changes and initiatives (Currie and Seddon, 2022). Studies have highlighted the issues relating to existing regulatory frameworks that have posed significant challenges to the banking sector, constrained by the imposition of ‘Chinese walls’ that have severely limited communication mechanisms and data processing (Dapp, 2017; Gregory et al., 2018). The research by van Donge et al. (2022) analyses the impact on the traditional banking industry, highlighting the reality of a sector, in catch-up mode struggling to compete within a regulatory environment that favours new entrants, unconstrained by the usual rules and regulations. The transition to digital within existing regulatory environments, has impacted the pace of digital initiatives and existing business models, often requiring the pragmatic use of trade-offs to absorb the required level of change (Breidbach et al., 2020; Gupta and Bose, 2022; Mandviwalla and Flanagan, 2021). Incumbent organisations have needed to maintain and enhance existing systems, often within a cultural context, tending to focus on designing systems and infrastructure, rather than focussing on the institutional perspective, customer interaction, information exchange, value co-creation and business benefits (Alt et al., 2018; Goh and Arenas, 2020; Hinings et al., 2018; Joshi et al., 2022; Wimelius et al., 2021). The key challenges that emerged from the literature aligned to this theme are as follows: (1) Required investment in compliant digital systems and infrastructure; (2) Integration of new digital systems with existing legacy systems; (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies; (4) Pragmatic use of trade-offs to achieve desirable outcomes. These challenges highlight the complexities within organisations to invest in the necessary digital infrastructure and products, ensuring effective integration with legacy systems, whilst maintaining compliance with regulatory constraints and commitments to deliver successful outcomes.

Themes: Clear vision for digital initiatives; culture and change apathy within impacted organisation; business versus technical centric initiatives; visible and active executive support for digital initiatives

Researchers have identified the association between successful digital transformation initiatives and the ‘buy-in’ from participative stakeholders that exhibit strong organisational identity (Ahn and Chen, 2022; Aisaiti et al., 2021; Allen et al., 2020). Studies by Gurbaxani and Dunkle (2019) analysed many of the key dimensions of digital transformation that can be associated with successful outcomes, highlighting the organisations strategic vision and a digital innovation focussed culture amongst the prerequisites. The cultural context is discussed in a number of studies where researchers have elaborated on the complexities relating to employee ability to adapt to disruptive change, and development of a culture based on innovation (Aisaiti et al., 2021; Baptista et al., 2020; Gurbaxani and Dunkle, 2019). Researchers have examined the dynamics between the traditional IT management, Chief Information Officer (CIO) decision maker roles, versus the business centric – Chief Story Telling Officer (CSTO) type roles, in the context of digital product innovation and contribution to strategy (Chatfield and Reddick, 2019; Cui et al., 2021; Koch et al., 2021). The key challenge in this area, is the need to focus on the business benefits of digital transformation (Burton-Jones et al., 2020) and the alignment of resources to focus on strategic aims, rather than a knee jerk change in strategy to attempt to keep up with the competition (Cui et al., 2021; Dapp, 2017). The criticality of visible and active sponsorship for digital initiatives, has been widely cited within the literature, with studies articulating the significant challenges facing delivery teams where executive support is lacking or insufficient to drive the initiative forward (Bernardi and Exworthy, 2020; Bunduchi et al., 2020; Dwivedi et al., 2023; Nasiri et al., 2023). The key challenges that can be associated with these themes are as follows: (5) Development of digital mindset and support within stakeholder groups for new tools and interactions; (6) Challenges and resistance to stakeholder adoption of transformation initiative and changed processes; (7) Impact from automation of business systems approvals and digital exclusion; (8) Retaining focus on business benefits for digital transformation initiatives; (9) Visible and supportive leadership without detailed micro level management intrusion; (10) Developing stakeholder support and effective communication mechanisms for digital initiative; (11) Development and management of strategic alliances.

Theme: Data security, management and business intelligence

Researchers have outlined the many challenges related to data security, data analytics and business intelligence and their role in the delivery of business benefits from digital transformation (Breidbach et al., 2020; Kappelman et al., 2019). Technologies such as biometric identification and device authentication are now ubiquitous as many service providers have adopted these security and privacy mechanisms for system access (Mir et al., 2020). However, the onset of mobile device access to services, poses significant challenges for organisations as they weigh up the trade-off between ease of system interaction and secure management of data assets. Studies have assessed the role of AI as an integral component of digital transformation and the criticality of access to structured and non-biased data for effective decision-making (Piccialli et al., 2021). The effective use of advanced analytical tools and processes is essential to support and automate customer assessment processes, allowing decision makers to focus on tasks that require human engagement (Mărăcine et al., 2020). The research by Pleger et al. (2020) highlights the expectations amongst stakeholders for high levels of data security with digital systems in connection with the digital transformation of the public sector. Key complexities exist in protecting consumer data and increasing the digital literacy of users to protect all stakeholders (Suryono et al., 2020). The key challenges emerging from this theme are as follows: (12) Use of tools and processes to develop effective benefits from business intelligence and communication mechanisms; (13) Security and management of data assets; (14) The complexities of managing and processing increasing amounts of data within organisations.

Research methodology

To deliver the requisite aims of this study and develop the necessary insight to the key interdependencies and hierarchical structure of the underlying factors surrounding digital transformation within the financial sector, a mixed methods approach was selected. Pairwise methods offer a number of distinct advantages to researchers in the assessment of the relationships between the relevant underlying factors: (i) systematic and repeatability of process, (ii) graphical representation of outputs, (iii) no requirement for expert participants to have knowledge of the underlying pairwise comparison process, ability to translate real life complexity to participant driven cognitive models (Donne et al., 2021). Pairwise comparison methods require the evaluation of multiple options or factors by comparing each factor with all other factors in turn to gain perspective on the extent of interdependency and hierarchy within the pairwise model (Hughes et al., 2020). Pairwise comparison methods have featured extensively within the extant IS related literature where researchers have sought to develop greater insight via the use of subject-matter experts to develop the interrelationships between sets of factors, utilising factor comparison approaches (Lee, 1993; Luthra et al., 2023; Rana et al., 2019).

This study incorporates the ISM and AHP methods that rely on the views of expert participants to facilitate a pairwise comparison and the development of a model of the relationships and representative hierarchy of the factors. ISM is a structured pairwise method, initially proposed by Warfield (1974) and subsequently adapted by Sage (1977), that stems from discrete and finite mathematics. The method offers a visual representation of complexity via a systematic process of structural modelling using interconnected matrices. The ISM method can illustrate and develop a hierarchical model (digraph) to depict the interrelationships between each of the factors (Kar et al., 2019). In alignment with many applications of ISM within the literature (Hughes et al., 2020; Kapse et al., 2018; Yadav and Desai, 2017), this study incorporates the Matrice d’Impacts Croisés Multiplication Appliquée á un Classment (MICMAC) modelling approach to visually demonstrate the factor relationships in the context of their driving and dependent powers (Rana et al., 2019; Saxena and Vrat, 1990). The AHP method (Saaty, 1977) is used within this research to develop the necessary factor hierarchy and ranking based on the pairwise comparison of the factors related to digital transformation within the financial sector. The factor ranking aspect is somewhat limited within the ISM process, as it’s an attribute of the interdependency modelling process, rather than a pairwise choice made by the experts themselves. Hence, many studies that incorporate pairwise comparison methods utilise a mixed method approach (ISM and AHP) to expand on the factor ranking aspect of the pairwise approach (Donne et al., 2021; Hughes et al., 2020). To provide additional insight and contribution on some of the qualitative aspects of the underlying factors relevant to digital transformation of the financial industry, this research conducted interviews with members of the expert participant group. The process and implementation steps in applying the selected methodological approach are as follows:

Interpretive structural modelling process

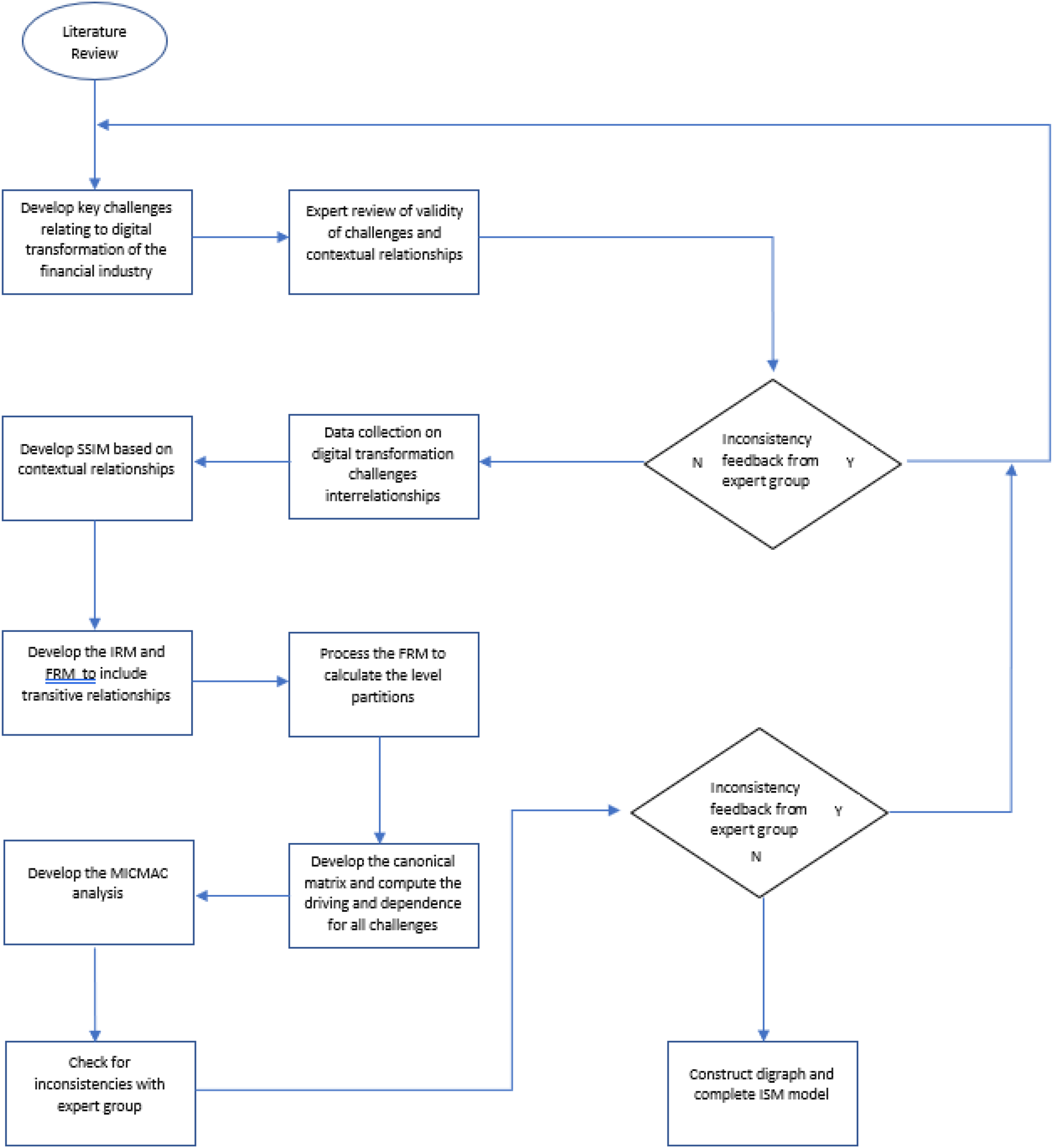

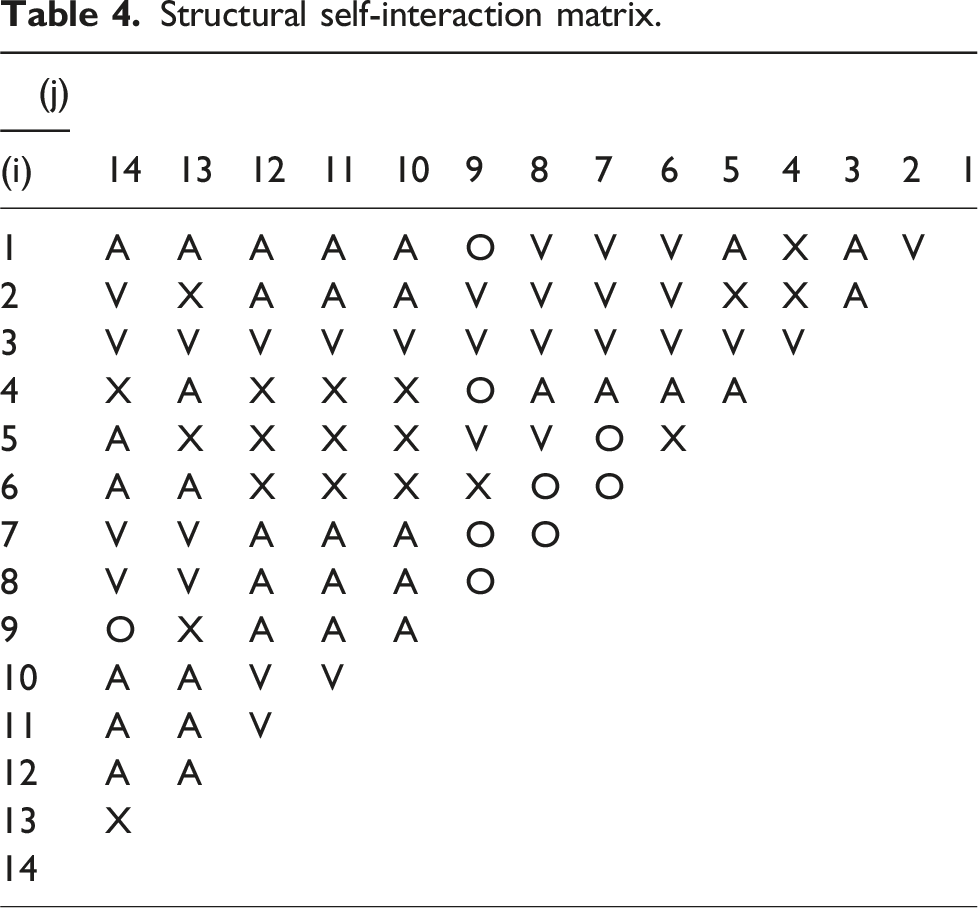

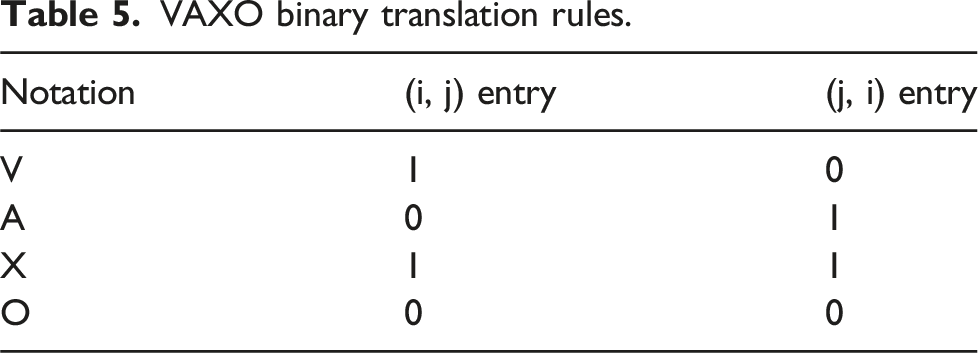

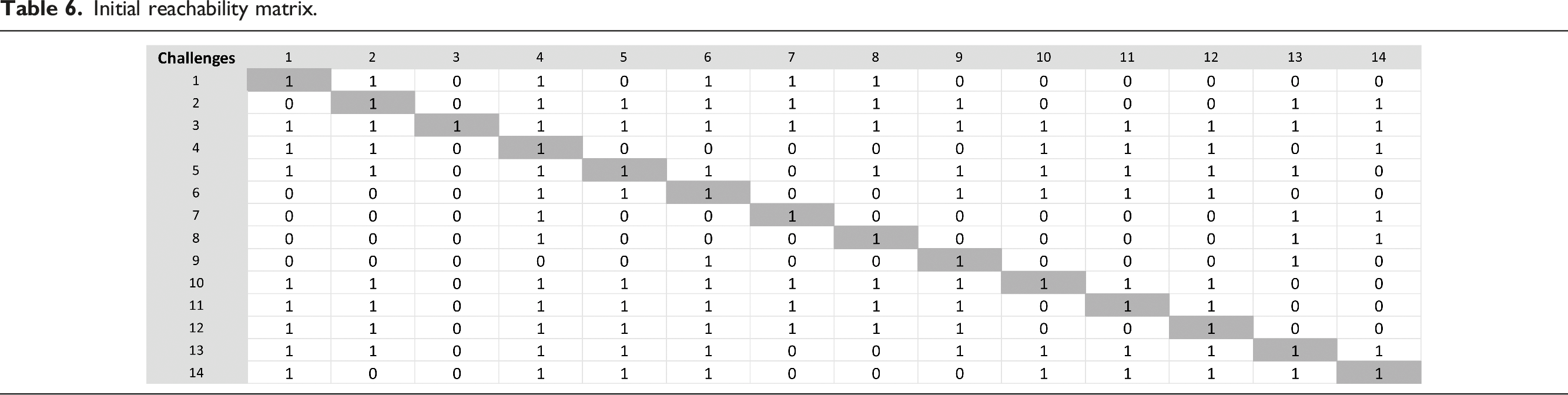

The ISM process as set out in Warfield (1974) and Sage (1977), is described in Figure 2. The method entails a number of distinct steps that are required to identify and process the key factors and their interdependencies: • Step 1: Identify the key factors from the literature review of the key challenges related to the digital transformation of the financial sector. • Step 2: Validate the set of factors for consistency with the expert participant group. • Step 3: Collect the data for identifying the interrelationships between the key challenges from the expert group based on the pairwise comparisons. • Step 4: Develop the Structural Self-Interaction Matrix (SSIM) based on the extent of the contextual relationships between the factors. • Step 5: Translate the SSIM to the Initial Reachability Matrix (IRM) and Final Reachability Matrix (FRM) incorporating the rules of transitivity, for example, if A is connected to B (A → B) and B is connected to C (B → C) then a transitive relationship exists between A and C (A → C). • Step 6: Develop the level partitions for all the factors where the reachability, antecedent and intersection sets are calculated. The reachability set is developed from the challenge itself and all other challenges influenced by it. The antecedent set comprises of the challenge and other challenges that influence it. The intersection set is developed by calculating the common points of the reachability and antecedent sets for each of the challenges. • Step 7: Create the canonical form matrix to compute the driving and dependence power figures by summing the binary values for each factor against each axis. • Step 8: Conduct MICMAC analysis and visually represent the distribution of the challenges from the canonical form within a matrix structure to represent the measures of influence within a spectrum of driving and dependence power interdependencies. • Step 9: Check for inconsistencies with the expert group. • Step 10: Construct the ISM digraph and complete the model. ISM process.

Analytical hierarchy process

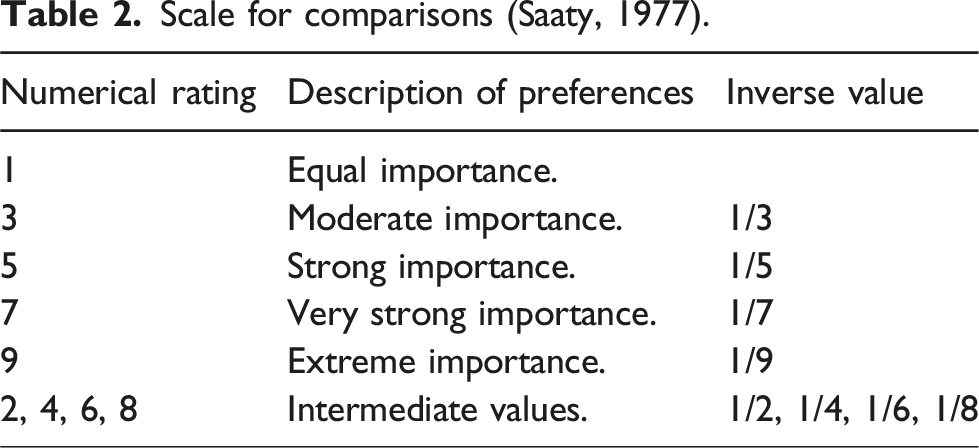

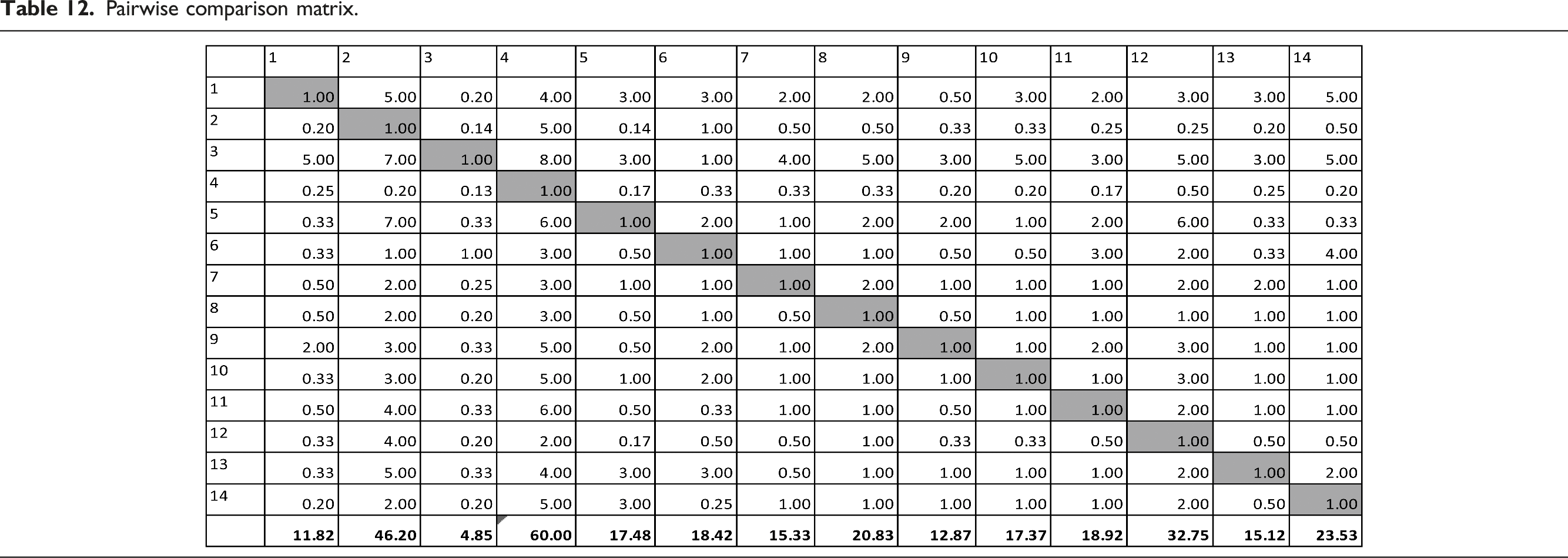

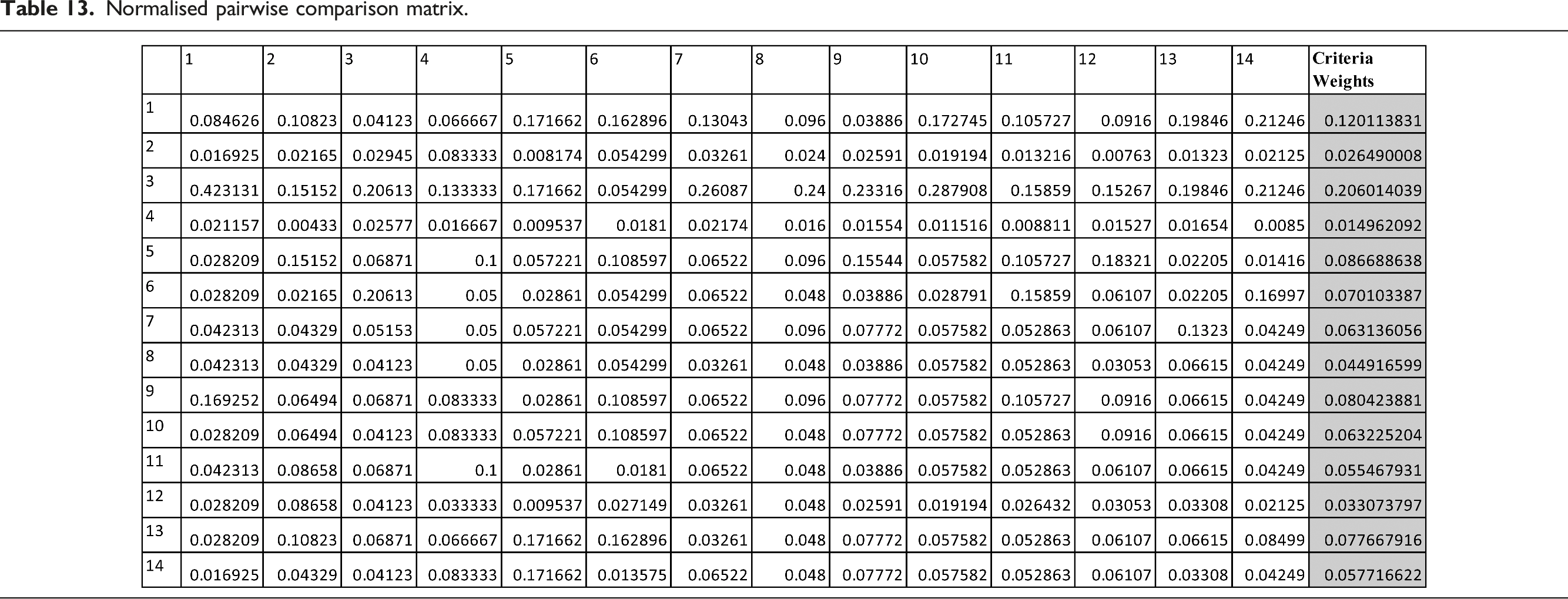

The AHP method utilises a pairwise approach to develop a comparison matrix and subsequent weighted hierarchy of ranked factors (Saaty, 1977, 1980). The AHP analysis utilised the same list of factors from the ISM process, but in this stage of the factor processing, the expert participants were tasked with assessing the pairwise comparison in the context of the relative importance between each of the individual challenges. The required steps to develop the AHP outputs are as follows: • Step 1: Develop the data collection instrument to enable the documenting of each instance of pairwise comparison between the factors. • Step 2: The experts generate the pairwise comparison matrix of the relative importance between the factors, based on the scale of 1–9 as presented in Table 2. If factor B was deemed more important than factor A, then the reciprocal value of the scale (denoted by 1/n) was used. • Step 3: Develop the normalised pairwise comparison matrix and calculated criteria weights. • Step 4: Check for consistency using the consistency ratio (CR) of less than 0.10. This is used to assess the judgement consistency when making pairwise comparisons. A CR of greater than 0.1 indicates that the pairwise comparison judgements are not consistent. • Step 5: Compute the criteria weights and ranking hierarchy. Scale for comparisons (Saaty, 1977).

In alignment with the AHP literature (Donne et al., 2021; Lee, 1993), we adopted a AHP 9-point scale for Pairwise Comparison. Scores 2, 4, 6 and 8 are used as intermediate values. The computed outputs of the AHP process are the set of weighted ranked factors.

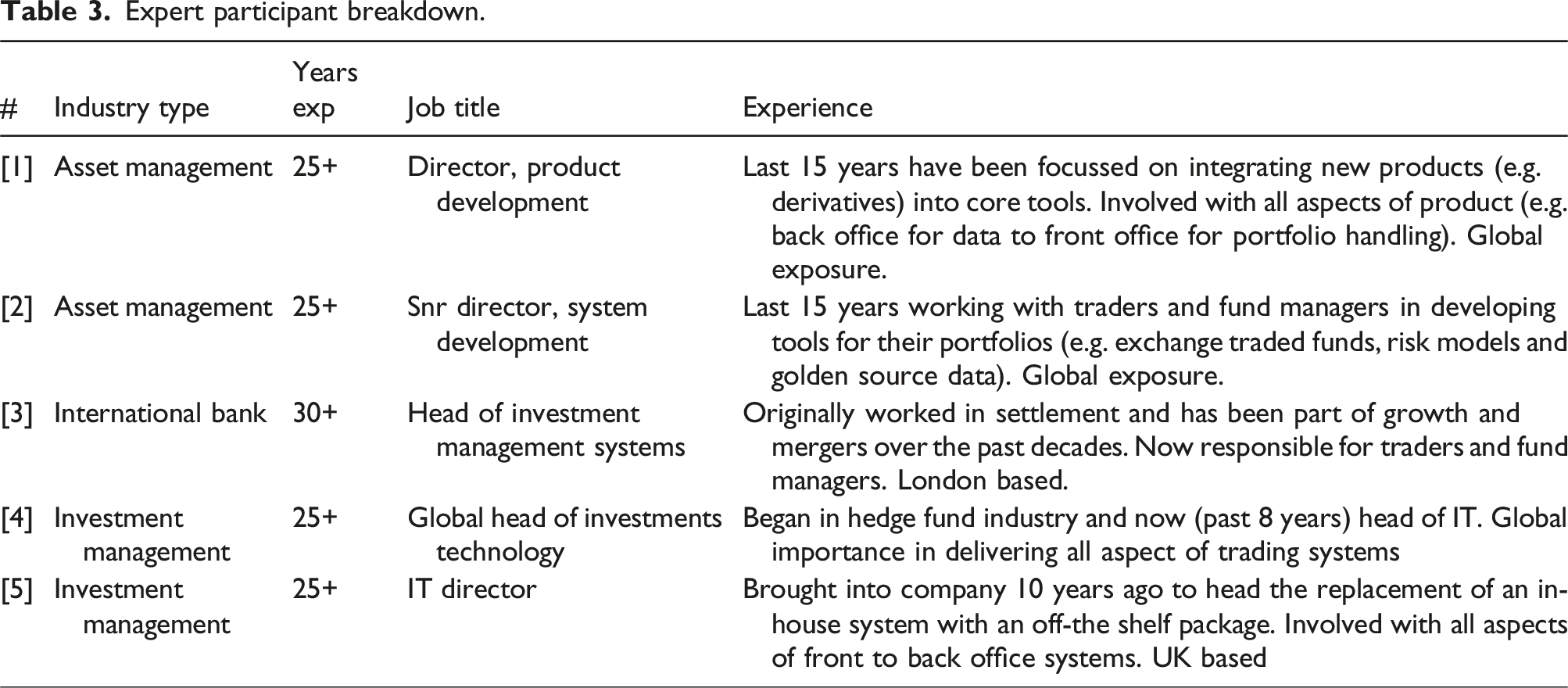

Interviews with expert participants

Expert participant breakdown.

The interviews followed an unstructured format and were conducted after the completion of the pairwise comparison exercise. Interviews were recorded and transcribed to extract the key observations and expert perspectives specific to the views on the resulting impacts of the pairwise comparisons.

Results

Due to the high levels of cognitive load experienced by participants within previous studies (Hughes et al., 2020), this research conducted separate data collection rounds for the ISM and AHP elements, with follow-up consistency analysis and interrelationship validation with expert participants. The interviews with the expert participants, were captured within the ISM sessions to ensure the views and implications on the identified interrelationships, retained their validity and relevance for the identified challenges related to digital transformation. The key extracts from the interviews are contextualised within the Discussion section.

The review of the literature identified 14 separate challenges that form the basis of the factors used within the pairwise comparison process – listed in Table 1. The matrices developed for the ISM and AHP exercises were structured around these challenges, to process the data collection and develop the pairwise comparison results. The listed challenges were assessed by the expert participants to check for inconsistencies and to ensure validity. The review identified a number of minor changes and clarifications to the naming and scope, for three of the challenges. These were then revised and used to populate the subsequent pairwise matrices.

The appendix includes a detailed explanation of the underlying process and workings of the ISM and AHP methods.

Interpretive structural modelling results

Structural self-interaction matrix.

VAXO binary translation rules.

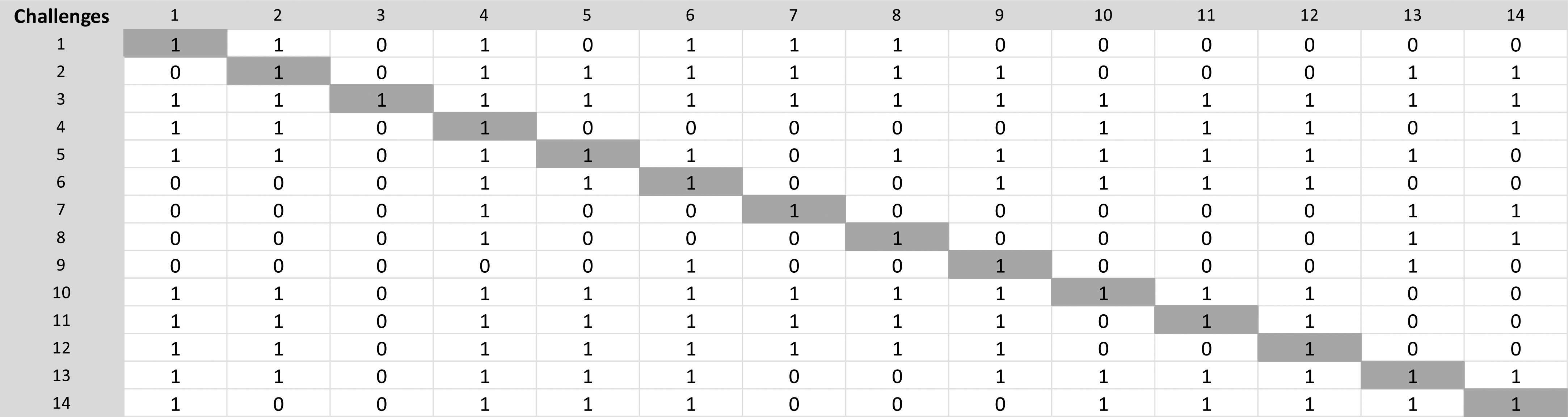

Initial reachability matrix.

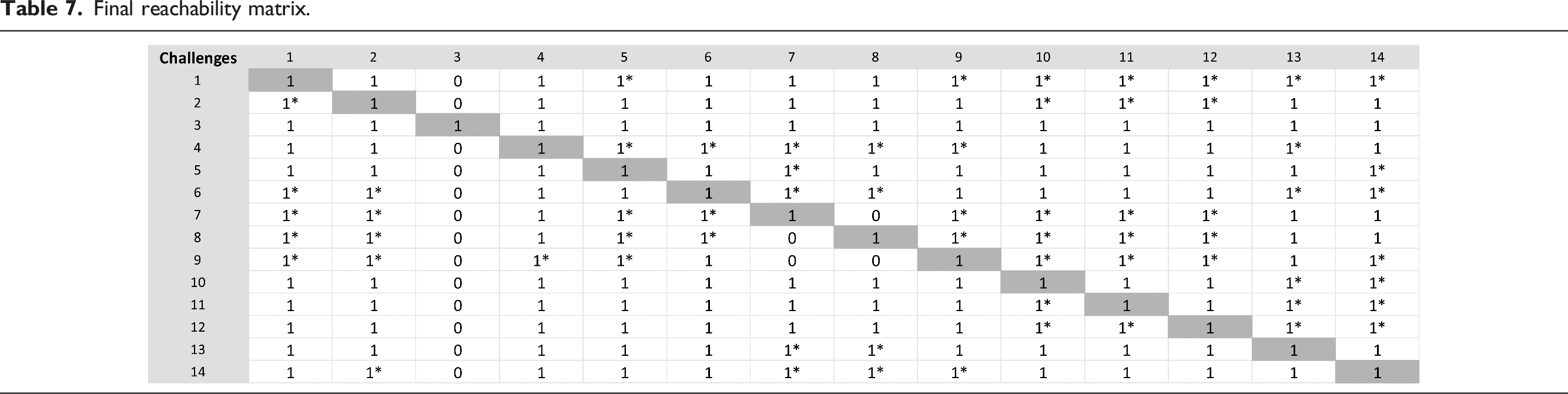

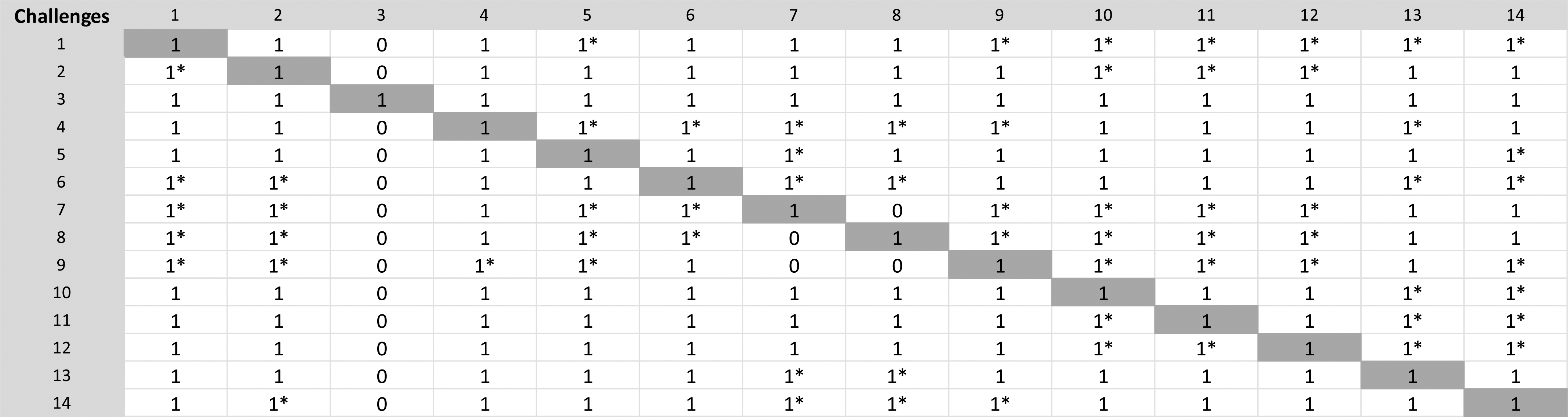

Final reachability matrix.

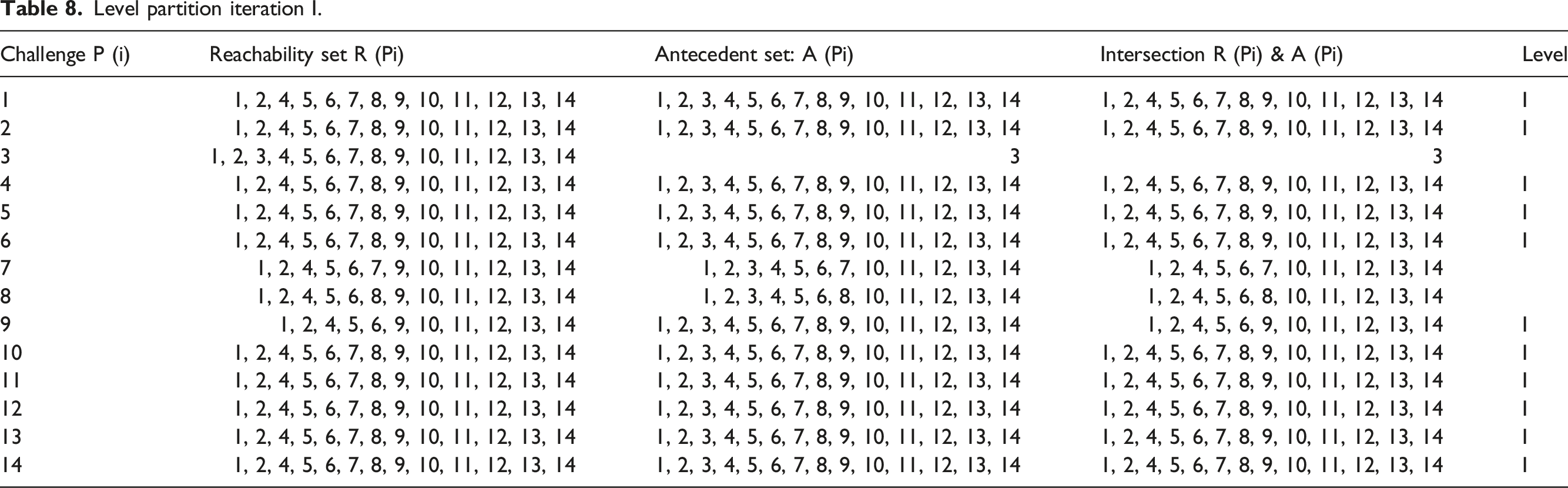

Level partition iteration I.

Level partition iteration II.

Level partition iteration III.

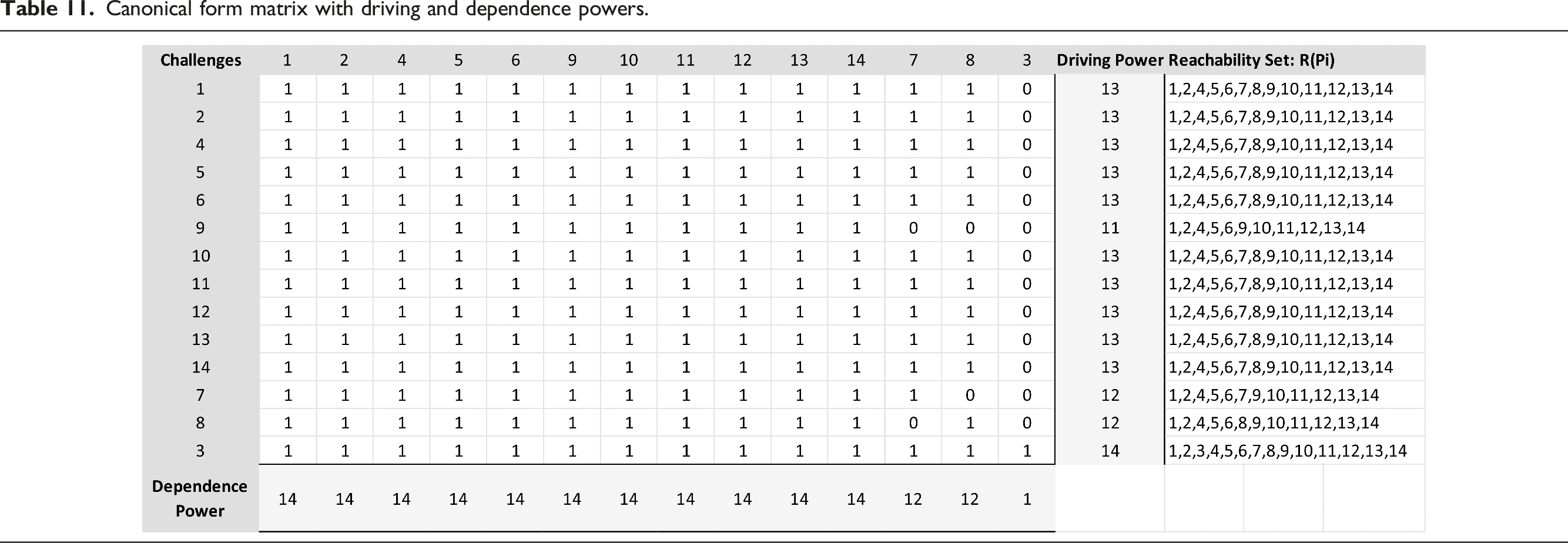

Canonical form matrix with driving and dependence powers.

The canonical form matrix is structured to reflect the level partition results based on the R (Pi) definitions. The canonical form represents the instances of ‘1’ for each (i, j) element within the matrix. The driving power figures are calculated from summing the (j, i) values across the x axis and the dependence power values are calculated from the sum of the (i, j) elements along the y axis. The matrix is then organised based on the driving and dependence power hierarchy. The canonical form results indicate the high degree of individual challenges that are clustered at the higher range of the driving power and dependence power range.

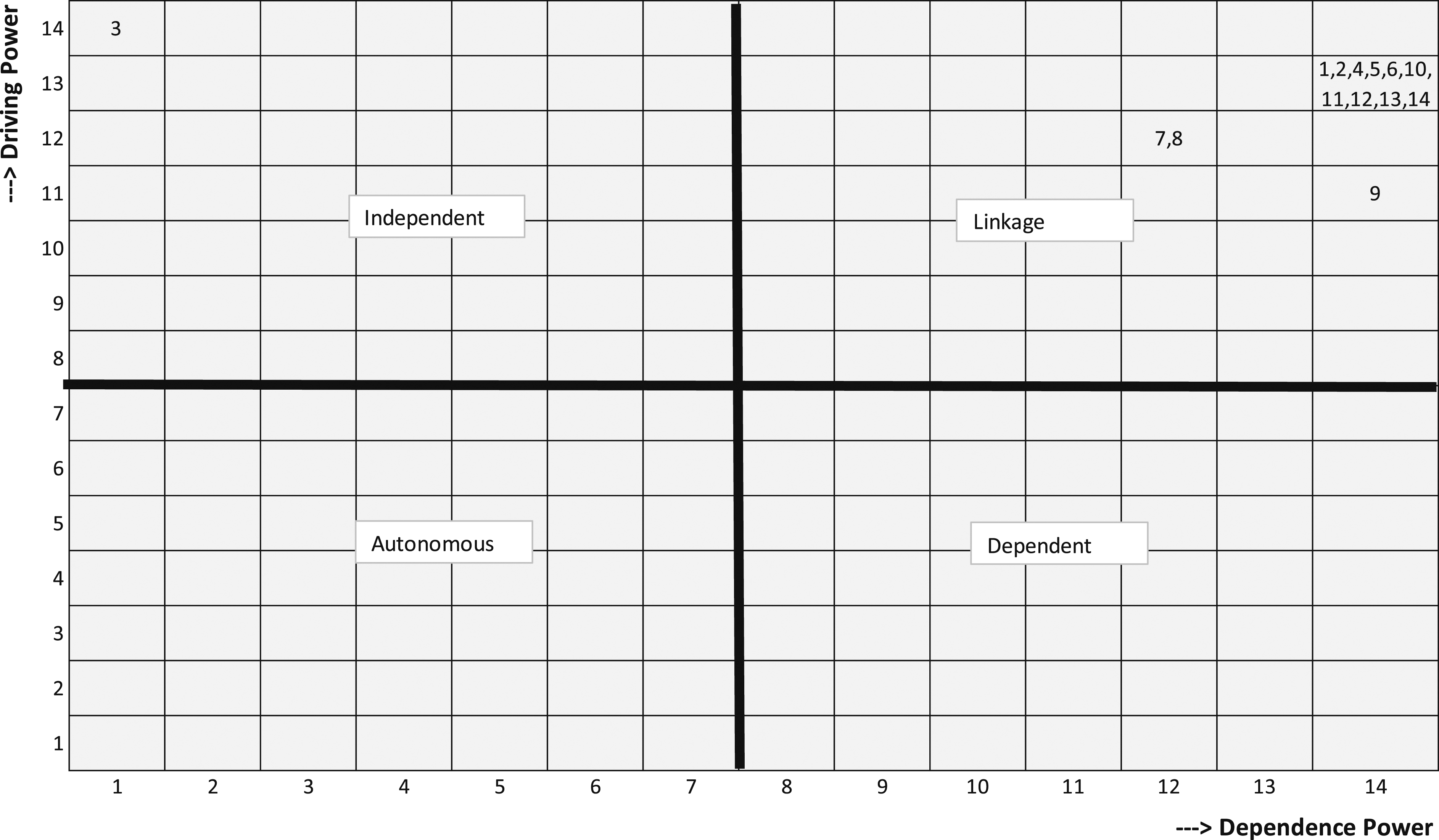

The MICMAC step in the process visually represents the distribution of the challenges from the canonical form within a quadrant-based structure to represent the measures of influence within a spectrum of driving and dependence power interdependencies. The MICMAC diagram has four distinct quadrants: • Independent – this identifies variables that have weak dependency power but strong driving power. • Linkage – this identifies variables that exhibit strong driving power and strong dependence power. Variables located in this quadrant are categorised as unstable, as any action on these variables will have a consequential effect on other variables and feedback on themselves. • Dependent – this identifies the variables that have strong dependence power but at the same time exhibit weak driving power. • Autonomous – variables exhibit low levels of interdependency and are relatively disconnected from the system. As such, they have weak driving power and weak dependence power, therefore, low impact on the overall ISM model.

The MICMAC diagram presented in Figure 3 highlights the large number of individual challenges that are positioned within the linkage quadrant. This indicates the high degree of interdependency between many of the variables highlighting how instances of these challenges may have wider and more consequential impact for the organisation. The challenges (7) Impact from automation of business systems approvals and digital exclusion and (8) Retaining focus on business benefits for digital transformation initiatives although listed within the linkage quadrant, exhibit lower levels of both driving and dependence power when compared to the majority of the challenges. The challenge (9) Visible and supportive leadership without detailed micro level management intrusion, is also positioned in the linkage quadrant but possesses maximum dependence power with relatively lower levels of driving power than the other factors in the linkage quadrant. This highlights how this specific challenge is viewed by the expert group as exhibiting less influence than the other challenges in this quadrant. MICMAC diagram.

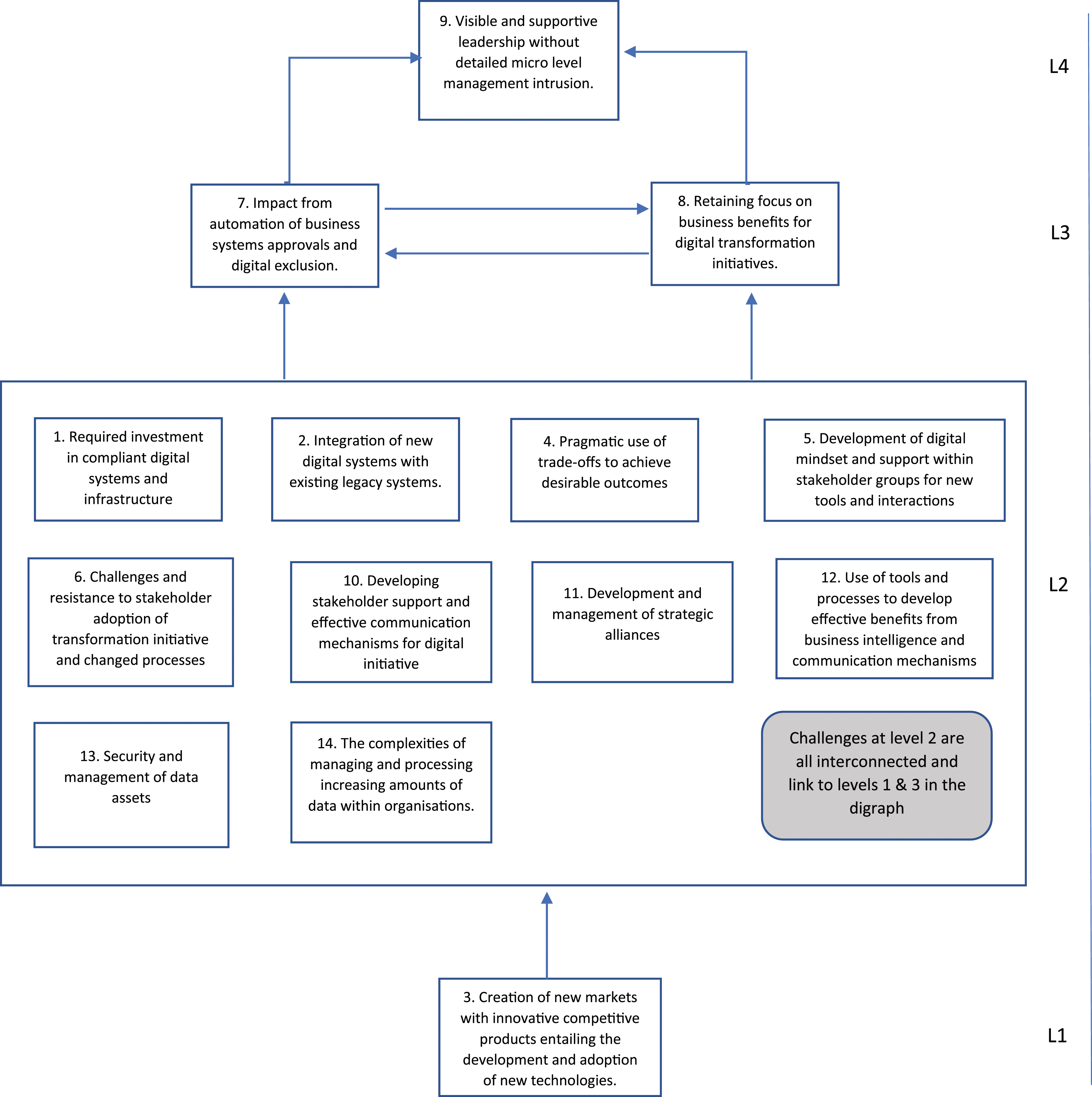

The challenge (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies, is listed within the independent quadrant. This indicates that although this challenge possesses maximum levels of driving power, exhibits minimal levels of dependence, and therefore, reliance on other challenges within the model. The final step in the ISM process is the development of the digraph and is presented in Figure 4. The digraph models the ISM hierarchy based on the assigned interdependencies and influence that the challenges exhibit within the model. ISM digraph.

The ISM digraph details the hierarchical structure of the ISM model where each of the challenges are represented based on their influence and reliance on other factors in the structure. The digraph is developed from the canonical form step in the ISM process. The digraph highlights the perceived driving power and influence of the challenge (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies, due to its position at the base of the model. The challenge (9) Visible and supportive leadership without detailed micro level management intrusion is positioned at the very top of the model at level 4, denoting this challenge as the one that possesses the highest levels of dependence power on other factors in the model. The challenges (7) Impact from automation of business systems approvals and digital exclusion and (8) Retaining focus on business benefits for digital transformation initiatives are position at level 3 in the model denoting the relatively high levels of dependence power and also high levels of interdependency with the high number of challenges clustered at level 2.

Analytical hierarchy processing results

Pairwise comparison matrix.

Normalised pairwise comparison matrix.

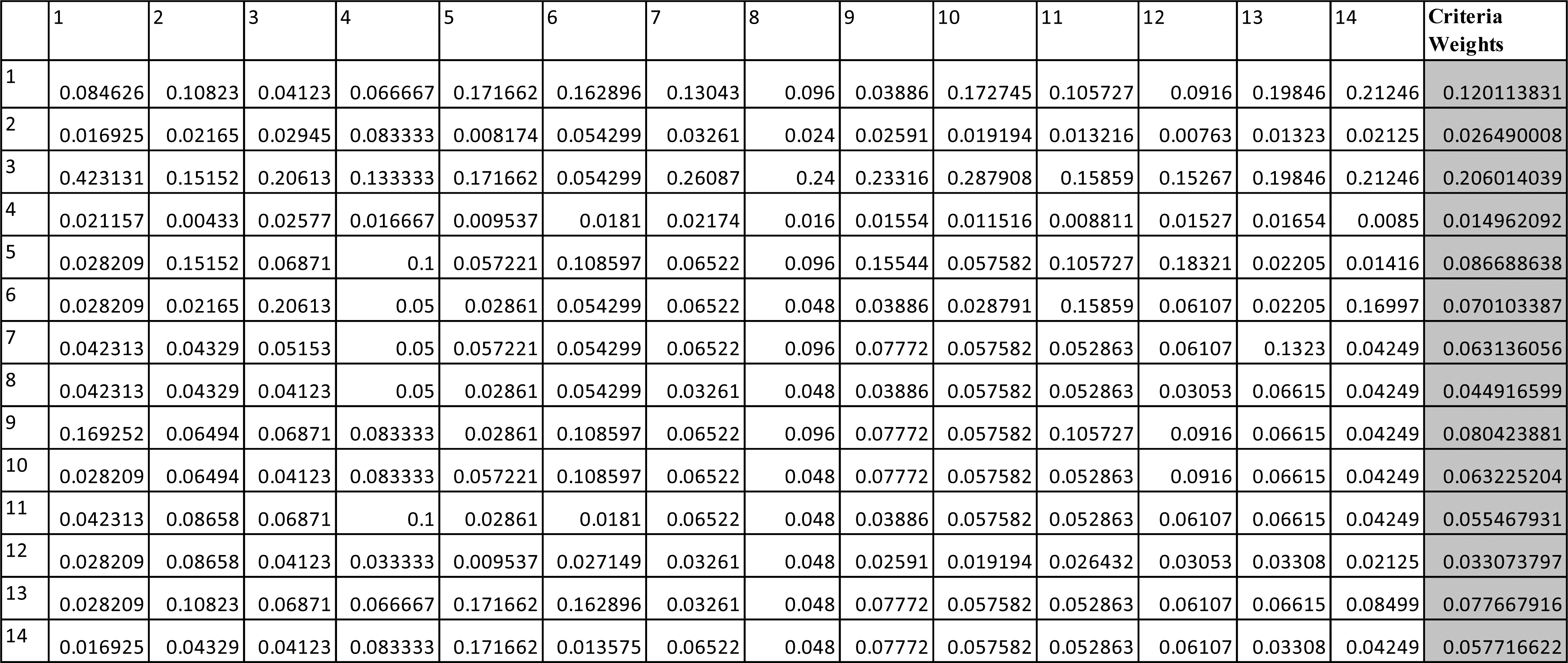

To ensure the pairwise judgements are acceptable, we calculate the consistency ratio (CR) based on the table of random indexes (RI) in Saaty (1977) using a value of 1.57 for n = 14. If the CR is <0.10 then the matrix is deemed to be consistent (Saaty 1977). The figure - λmax (lambda max) is calculated by averaging the weighted values in the normalised pairwise comparison matrix in Table 13. This gives us a λmax figure of 15.93. This is then used to calculate the Consistency Index (CI), where n = the number of challenges:

The CR is calculated as

By calculating the CR using the formulae in (1) and (2), we have a CR of 0.0945 which is within the acceptable consistency criteria of <0.10 based on the Saaty (1977) consistency criteria.

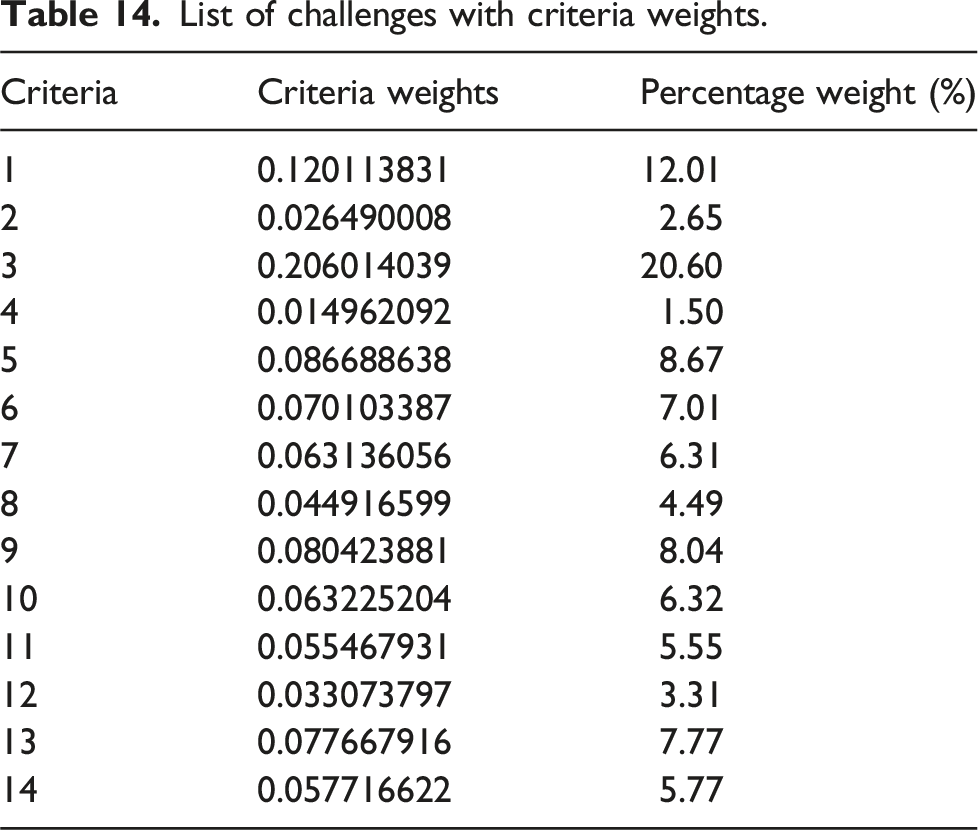

List of challenges with criteria weights.

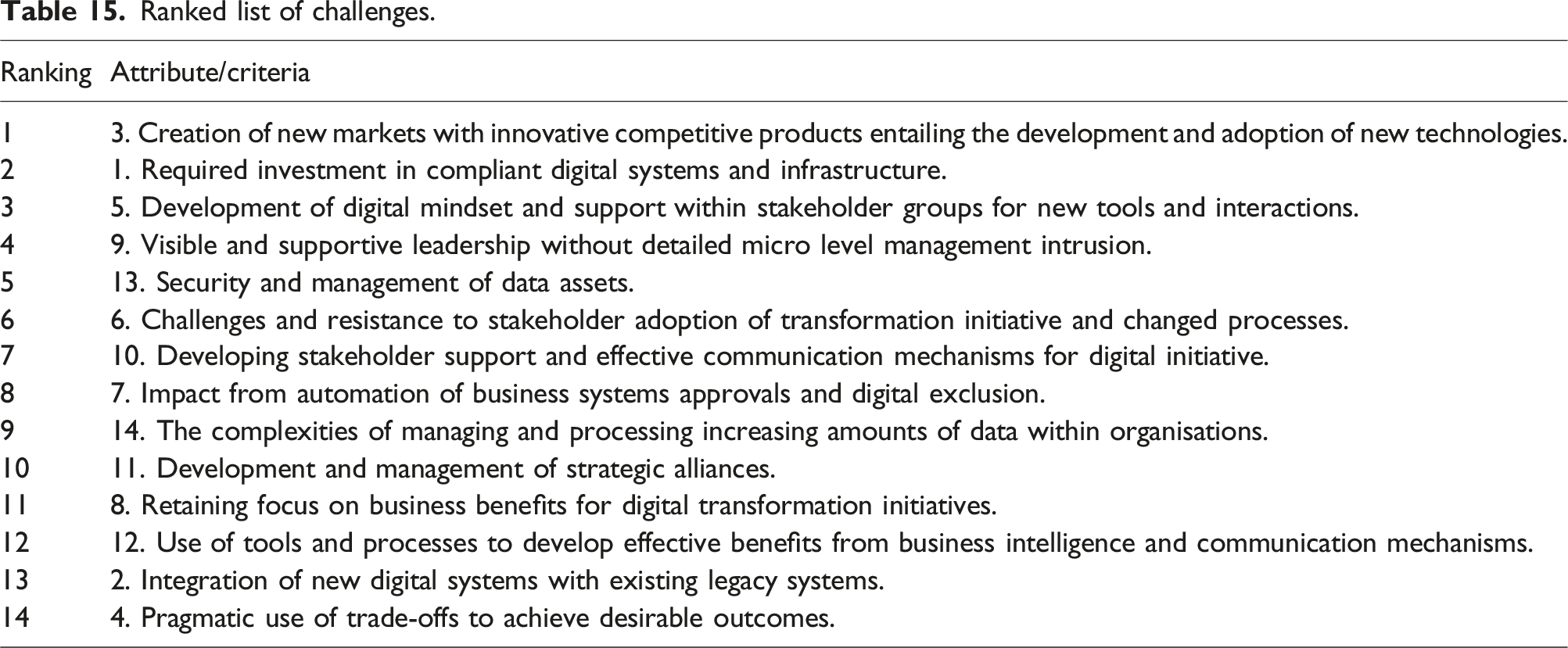

Ranked list of challenges.

Discussion

The key objective of this research is to develop further insight to the underlying interdependencies between the key challenges related to digital transformation within the finance industry. As described in previous sections, the key challenges were sourced from a review of the literature focussing on the key factors relating to digital transformation within the financial sector. The financial sector has experienced a period of tremendous disruptive change with many traditional banking and financial services organisations developing their digital capabilities to compete with new market entrants (Breidbach et al., 2020). Financial organisations have faced significant challenges in their need to align their strategic direction with digital transformation initiatives whilst maintaining vital legacy systems, within an environment where customers expect to interact within a digital ecosystem on the device of their choosing (Dapp, 2017).

The ISM and AHP findings reveal a number of key associations between the challenges that were exposed during the pairwise comparison exercises carried out with the expert participant group. The ISM results and MICMAC analysis revealed a high level of interconnectivity between the challenges where a number of them exhibited high levels of driving and dependence powers. The clustering of the challenges: (1) Required investment in compliant digital systems and infrastructure; (2) Integration of new digital systems with existing legacy systems; (4) Pragmatic use of trade-offs to achieve desirable outcomes;) (5) Development of digital mindset and support within stakeholder groups for new tools and interactions; (6) Challenges and resistance to stakeholder adoption of transformation initiative and changed processes; (10) Developing stakeholder support and effective communication mechanisms for digital initiative; (11) Development and management of strategic alliances; (12) Use of tools and processes to develop effective benefits from business intelligence and communication mechanisms; (14) The complexities of managing and processing increasing amounts of data within organisations, within the linkage quadrant of the MICMAC analysis, highlights the significant levels of interdependency between these variables that exhibit strong driving power and also strong dependence power. Variables located within the linkage quadrant are categorised as unstable, as any action on these variables will have a consequential effect on other variables and feedback on themselves. This finding means that due to the interconnectivity between these challenges, in instances where an organisation had identified that: (6) Challenges and resistance to stakeholder adoption of transformation initiative and changed processes, was a key factor within a digital initiative, then due to the interrelation between this cluster of factors, decision makers should review the interconnected list of challenges to identify key areas of risks to the organisation and highlight potential problem areas. These challenges are critical to successful outcomes particularly within the context of institutional resistance to change and importance of adopting a digital mindset (Alt et al., 2018; Zhu et al., 2006).

The expert interviews discussed the underlying issues surrounding the challenge: (1) Required investment in compliant digital systems and infrastructure, and its interrelationship with (14) The complexities of managing and processing increasing amounts of data within organisations, highlighting the complexities in developing Markets in Financial Instruments Directive (MiFID) compliant systems and the high degree of linkage between these challenges:

“As compliance keeps changing its driving the complexity higher” [1].

“You need to spend money to get a MiFID compliant system. Requirements to meet regulation drives the complexity up. Regulation comes first and you need to invest in digital systems. Prior to MiFID none of the data was stored, and so this drove its capture” [2].

“You need to be able to specify the required investment with the increasing amounts of data” [3].

“You need to know what the challenges are before you can justify or define your required investment” [4].

The interview extracts above show how the experts elaborated on the reality of investment choices and the impact of MiFID in the context of increasing data storage requirements and additional levels of complexity resulting from this. These observations highlight the interdependencies between these two challenges and the implications for the remaining challenges within the same cluster in the linkage quadrant of the MICMAC analysis. The investment in infrastructure and data complexity aspects of digital transformation, are discussed extensively within the literature, where studies have highlighted the impact of these factors on existing business models (Lauterbach et al., 2020; Mărăcine et al., 2020).

The ISM digraph in Figure 4 displays the three-layer hierarchy of challenges and their influence in the context of driving and dependence powers on other factors in the model. The position at the base of the digraph hierarchy for the challenge: (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies, indicates the high levels of driving power and low levels of dependency power for this specific challenge. This highlights the significant influence that (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies has on other factors in the model and the importance of focussing on any risks that could emerge from this specific challenge due to its interconnectivity and position in the digraph. The expert interview extracts below further illustrate the power of this specific challenge and its influence within the model, indicating how decision makers need to frame any potential migration to new markets with existing or new products and services.

“You don’t create processes and complexities of data without the creation of new markets, so it’s the driver” [1].

“A new market drives everything” [2].

“Types of data can have an influence on new markets. If you are trying to create a new market because that is what your competitor is doing, and doing something new, they you are going to be creating new types of data you haven’t necessarily used before, so the two things are interlinked, but just because you have complex data doesn’t mean you go off and create a new market!” [3].

The challenges (7) Impact from automation of business systems approvals and digital exclusion and (8) Retaining focus on business benefits for digital transformation initiatives are positioned within the 2nd tier of the ISM digraph, demonstrating the significant influence on the other interconnected factors higher up within the model. These two challenges exhibit significant driving and dependence power and possess equal ratings for both of these attributes within the model, highlighting the impact alignment of these factors and importance of alignment of strategic transformative initiatives (Breidbach et al., 2020; Chanias et al., 2019). “The impact from automation impacts complexities of managing and processing increasing amounts of data” [4]. “You can do a lot of things with digital connections, and this will create resistance from end users… ‘why are we not doing this,’ ‘why are you doing that automatically,’ ‘why are you looking at this’” [1]. “This is the sales process because you have to have gone through the process before the change is resisted” [4]. “You want to migrate existing customers to a new platform and increase new users. Thinking about client on-boarding. More clients with more data requirements. You have a challenge trying to get people off their manual ways. But then you have got a desire to automate client on-boarding, which leads to challenges related to all the complexities of data because you have got to automate” [3].

The expert interview extracts above highlight some of the complexities related to these two challenges and how they interact with the challenges related to stakeholder resistance in the context of process automation and implementation of new processes as decision makers align change with delivery of business benefits.

The AHP pairwise comparison element of the data collection and processing, yields additional insight to the importance and ranking of the various challenges based on the views of the expert participants, and offers another valuable perspective on the key challenges related to digital transformation within the finance industry. The AHP results in Table 15, position the challenge: (4) Pragmatic use of trade-offs to achieve desirable outcomes at the base of the ranking at no. 14, indicating that the experts view this specific challenge as exhibiting low level of importance when compared to the other challenges in the list. This can be interpreted as the presence and use of trade-offs in the context of digital transformation (Goh and Arenas, 2020), is either not a key factor when compared to other challenges, or that trade-offs are a necessary agent of compromise and are not seen as a challenge, but more of a natural consequence of change. “Data doesn’t have a compromise – the solution has. Humans have compromises. If you don’t have the relevant data you can’t create an outcome” [2]. “The complexities in managing increasing amounts of data could actually lead to a trade-off, but sometimes the data can influence the trade-off” [4]. “All throughout the process you can have conversations around the whys and wherefores of trade-offs, and then go out to external stakeholders who say “we can only accept ‘y’ and you want to do ‘x,’” so we need to have a trade-off. Those conversations can go both ways” [4]. “Trade-off by definition is ‘compromise’” [5].

The interview extracts above highlight the references to trade-offs and the ‘on the ground’ realities of compromise within digital initiatives. Another interesting aspect of these extracts are the links between data and trade-offs, and the criticality of intelligent data analysis (van Donge et al., 2022).

The AHP results in Table 15 position the challenges: (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies, (1) Required investment in compliant digital systems and infrastructure and 5) Development of digital mindset and support within stakeholder groups for new tools and interactions, within the top three of the ranked list of challenges. These results highlight the criticality of investment in digital systems and infrastructure and how high-level stakeholder support and mindset for digital change initiatives, is key for successful outcomes (Hughes et al., 2020). “We build out a platform for a sustainable fund just for one client and this does not justify the costs, but the idea is once they are on the platform, we will get more clients. It’s a loss leader but it’s still business led” [1]. “If you were doing a technology led project, as opposed to a business led project, you’d still need to have the digital mindset in order to do it” [4]. “The digital mindset is developed at the executive level following the report done for them by a consultancy firm. They don’t know the detail but are sold the concept of, say, blockchain and the benefits to their strategy” [5]. “We developed a dealing platform, four months into it before we realised that legally in the US we couldn’t trade because we had not involved the lawyers on the movement of the data that was to be traded. We had to involve stakeholders on the initiative” [1]. “You have got new securities and data assets but you need to educate in terms of what this actually is and what issues are associated” [1]. “Trying to make the most of your data you encourage a digital mindset and vice versa” [3].

The interview extracts above highlight the importance of strategic investment in digital systems and the implications of failings in stakeholder identification and communication. The experts articulated the importance of focussing on the stakeholder aspect within the early stage of digital initiatives. The experts also identify the benefits of developing the digital mindset at the executive level and for this to be linked to the realisation of potential benefits aligned with the strategic direction of the organisation. The implications of the expert views and AHP ranking of these challenges, is that decision makers need to commit to the investment and adoption of innovative digital systems, prioritise the involvement of stakeholders at an early stage and ensure that the development of a digital mindset is focussed at the senior stakeholder level to engender awareness of the strategic benefits to aligning with changing customer requirements (Alt et al., 2018; Dapp, 2017; Mergel et al., 2019).

Theoretical contributions

A number of researchers have analysed the impact of digital transformation within the finance industry, highlighting many of the key complexities facing organisations as they extend their digital capability in terms of products and services (Agarwal and Zhang, 2020; Mărăcine et al., 2020). • Although studies have discussed the numerous challenges facing organisations that are developing their digital initiatives and the impact on business models from the attempts to compete with new market entrants that are less restricted by legacy applications and regulatory commitments (Breidbach et al., 2020; Dapp, 2017; Suryono et al., 2020), to our knowledge, no studies have analysed the challenges through a combined interpretive and hierarchical and qualitative lens. • Furthermore, the application of a pairwise analysis approach via the use of ISM and AHP offers further unique contribution and extends existing knowledge in a new direction, delivering valuable insight to the interrelationships between the identified challenges. • The contribution of this research is further extended with the addition of the expert interviews that provide insightful visibility of the pairwise decision-making process and ‘practice-based’ rational to the pairwise process. • To our knowledge this study is the first to utilise this mixed methods combination of ISM, AHP with expert interviews approach to the research the underlying challenges within the finance industry. Researchers can utilise this approach as a framework and theoretical foundation for future studies that can further the understanding of this key topic.

Contributions for management and practice

The results have identified a number of aspects that can contribute to a more informed understanding of how the key challenges relating to digital transformation initiatives are prioritised and interconnected. • The ISM results highlight a high degree of interconnectivity between the challenges, meaning that in instances where one or more of these challenges were to be identified as significant threat to the success of the digital initiatives, the impact could be wide ranging in scope requiring careful management and mitigation. • The identification of the ISM-based power and influence of the interconnected challenges (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies; (7) Impact from automation of business systems approvals and digital exclusion; (8) Retaining focus on business benefits for digital transformation initiatives, highlights the criticality of these aspects of digital transformation. Decision makers would be advised to retain focus on these challenges in the context of risk assessment and management, and to understand the implication for other connected challenges if these areas prove to be problematic within digital initiatives. • The ranking of the factors (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies, (1) Required investment in compliant digital systems and infrastructure and (5) Development of digital mindset and support within stakeholder groups for new tools and interactions, indicates the criticality of these aspects and how decision makers should prioritise investment within project planning and risk management, to increase the chance of successful outcomes. The discussion points within the expert interviews highlight the importance of business-led strategic investment, stakeholder alignment and the development of a digital mindset at the highest levels of the organisation. These areas need to be prioritised to help deliver benefits from the digital transformation initiative. • The position at the base of the ISM digraph in Figure 4 and highest AHP-based ranking in Table 15. For the challenge: (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies, thereby aligning the ISM and AHP influence of this critical factor, further demonstrates the importance of digital innovation and its strategic alignment with business benefits.

Conclusions, limitations and future research

This research contributes to the current discourse on digital transformation within the IS literature, that has focussed on the challenges within the finance industry (Agarwal and Zhang, 2020; Alt et al., 2018; Breidbach et al., 2020; Duperrin and Godet, 1973). This sector that has faced significant change within the digital era as organisations have struggled to develop their technology infrastructure whilst retaining existing legacy systems and complying with stringent regulatory requirements. This study has investigated the interdependencies and ranking of the key underlying digital transformation challenges faced by the finance industry. Via the use of expert participants, each with substantial IS experience within the finance industry, this research utilised an interpretive and hierarchical mixed methods process, incorporating the ISM and AHP approaches, supported by interviews with the participants to gain a deeper understanding of the pairwise interpretations. Both the ISM and AHP results highlight the significant influence and ranking of the challenge (3) Creation of new markets with innovative competitive products entailing the development and adoption of new technologies, and the importance of focussing on any risks that could emerge from this specific challenge due to its interconnectivity and influence in both models. The results highlight the criticality of investment in digital systems and associated infrastructure, and importance of a digital mindset as well as high-level stakeholder support are key for successful outcomes. The expert interviews contribute to the understanding and underlying rational of the identified interrelationships and how the interdependencies impact other challenges in the model.

This research to our knowledge is the first to utilise a mixed methods, interpretive and hierarchical focussed methodology utilising a combination of ISM, AHP and expert interviews to gain valuable insight to the key challenges facing decision makers within digital transformation initiatives. This offers valuable contribution in extending the use of these methods within new subject genres using a mixed methods approach. The expert interviews contribute to a greater understanding of some of the practice-based complexities and the ‘on the ground’ realities of decision-making within complex environments. The research is somewhat limited by the focus on the interrelationships between the challenges from the perspective of the experts who are key decision makers within digital transformation initiatives. Further insight could be gained from a greater understanding from the wider stakeholder perspective, to analyse the change implications and how this may impact productivity and adoption of new systems and processes.

Supplemental Material

Supplemental Material - Disruptive change within financial technology: A methodological analysis of digital transformation challenges

Supplemental Material for Disruptive change within financial technology: A methodological analysis of digital transformation challenges by Laurie Hughes, Jonathan JJM Seddon and Yogesh K Dwivedi in Journal of Information Technology.

Footnotes

Acknowledgements

The authors would like to thank Professor Nripendra P. Rana for his insights on the pairwise analysis conducted within this study. Furthermore, the authors would like to express their gratitude to the guest editors and reviewers for their constructive feedback and valuable contributions in helping to develop this paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.