Abstract

Tech media giants are no strangers to controversy in relation to the payment of corporate tax, such as the cases of Apple and Facebook (Meta) in Ireland, Alphabet (Google) in the UK and Amazon in Luxembourg. While the tech media giants are not the only global corporations that take advantage of international tax avoidance opportunities, this paper argues that their hypermobility and unprecedented cash assets place them especially well to take advantage of these practices. Moreover, the nature of some of the commodities, such as information, software or intellectual property that can be moved at the touch of a button; or even a simple re-conception of where the property resides can mean a state gaining or losing billions of dollars. This paper will explore how tech media giants are redefining property and commodity forms and how this allows for creative tax policies. Moreover, the conception of where immaterial commodities, such as pure information, is located (or not located) challenges tax collection strategies for the state. To explore these conceptions, this paper discusses the ideology surrounding the tech media industry, a particular brand of liberalism coined the ‘Californian Ideology’: An ideology that can sometimes be described as transgressive, but also one that may legitimise tax avoidance. The ideology gives a somewhat nebulous definition of what property is (and isn’t) and its location or non-location, thereby negating justification for taxation.

Introduction

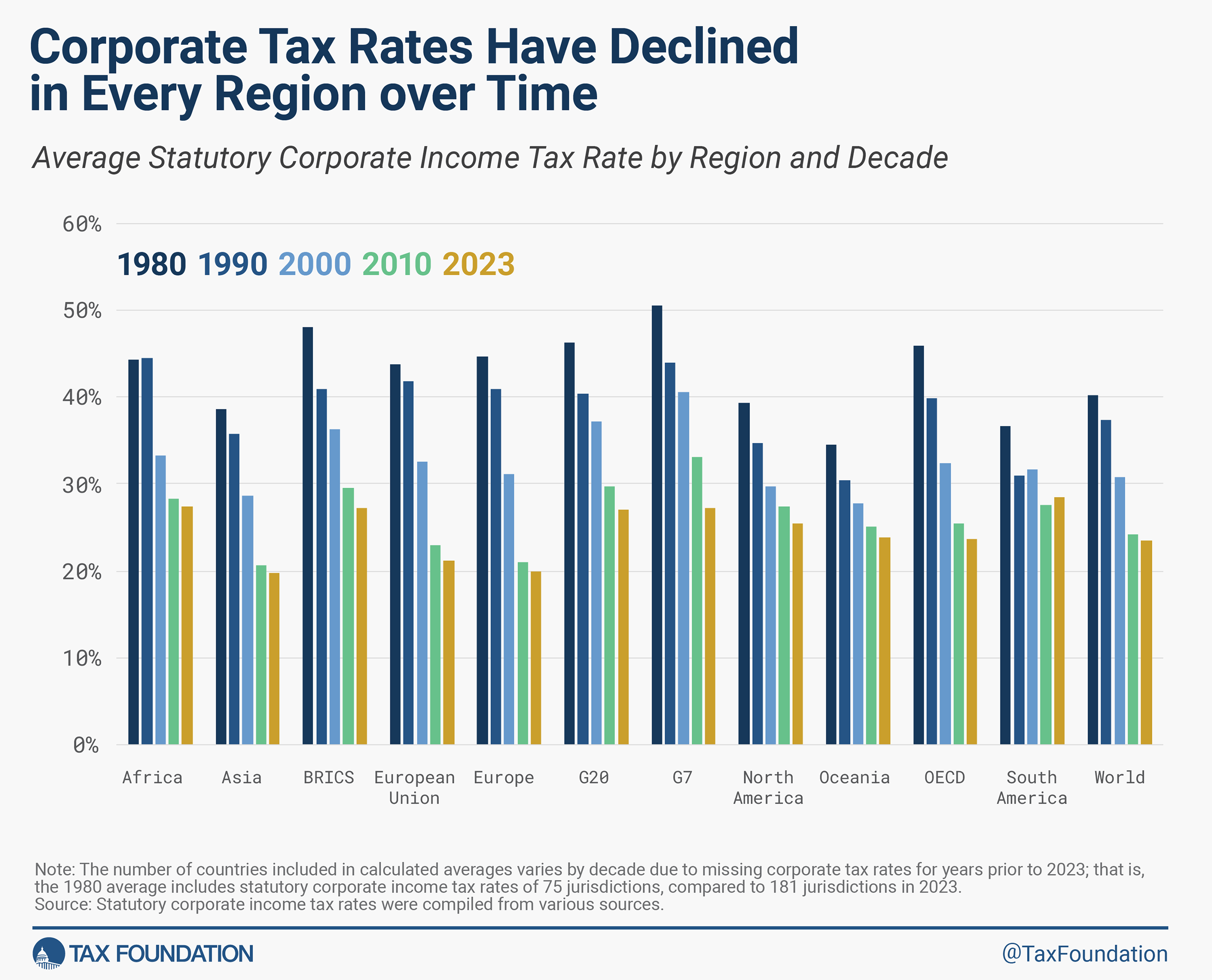

Conceptually, this paper attempts to tease out how contemporary society thinks about property and taxation. We rarely hear of the philosophical arguments regarding the uses of taxation, or the entitlement of state and/or jurisdictional authorities to levy them and exert allocative or redistributive control over them. Considered within the context of the intensifying corporate tax avoidance, the prescience of this issue is evident. In this context, we consider the question of whether taxation is collectively owned wealth improperly withheld by private entities or the opposite. The issue is further complicated by the prevalent construction of tax evasion by individuals as immoral, shameful and illegal (Carr et al., 2018; Tognato, 2015) while tax avoidance by corporations is constructed as a legitimate business strategy, the ‘fiduciary duty’ of accountants to shareholders. These issues are teased out ideologically and theoretically, and in the contemporary corporate tax environment which is increasingly hostile to its payment. Over the last four decades of what has come to be termed neoliberalism, there has been a steady and severe decline in corporate tax rates (see Figure 1).

Declining global corporate tax rates 1980–2020 (Tax Foundation 2021 in Asen 2022).

This paper focuses on tech media companies and their relationship and even conception of taxation, the state and property and discusses how their conception of such issues allows a justification of tax avoidance. If we think of one example, how information is stored on what is called ‘the cloud’, by very definition a non-space, is this information property and if this information is property should it be taxed? And if so where? The ‘cloud’ of course does not exist, but rather is a network of very real data centres; however, it remains nebulous – which data is stored where and under which jurisdiction? And likewise in a nebulous international taxation system, which jurisdiction is liable to collect any taxation that might be conceived of?

We focus on tech giants firstly due to their size and importance in the global economy; most industries operate using the tech giants’ technologies – in fact, it would be difficult to conceive of the contemporary capitalist market system operating without them. Secondly, due to the prestige held by such companies, their global reach and their role within broader media systems, they are very much part and parcel of the hegemonic system of contemporary capitalism and play an immense role in the idea of ‘common sense’ or ‘rule by consent’ as described by Antonio Gramsci (Gramsci and Gerratana, 1975).

To explore these conceptions the paper discusses the ideology surrounding the tech media industry, a particular brand of liberalism coined as the ‘Californian Ideology’ by Barbrook and Cameron (1996): an ideology that can sometimes be described as transgressive but also one that may legitimise tax evasion. The ideology allows for new definitions of what property is (and isn’t) and the location or non-location of a commodity or a property, thereby negating justification for taxation that was traditionally based on a material location in a nation-state. It is recalled that such companies benefit from the state, both directly via subsidy and protection of their intellectual property rights and indirectly by services and access to an educated workforce (Mazzucato, 2011).

Taxation and the state

As discussed, this paper is concerned with taxation from a conceptual perspective and considers the pervasive philosophical question of who actually owns the wealth that is taxed. This is particularly important in the context of international taxation and the challenges presented by jurisdictional boundaries – earlier conceptualizations of taxation placed it relatively firmly within state or city-state boundaries, allowing tithes to be placed by jurisdictional authorities over the economic activity in their region. However, the contemporary challenges brought about by global business activity and the concurrent mobility of corporations make the issue of taxation a much more complicated one. The very concept of property is not as in feudal times, always something tangible and in a single place, more readily seen, counted and taxed by the state. Contemporary commodities and property, especially in the tech industry may be the immaterial, pure information stored on servers anywhere on the planet, but retrievably immediately; likewise intellectual property rights, again something nebulous and immaterial, easily mobile and whose registered location can decide where and what taxation is paid (Griffith et al., 2014). Creative accounting has long used mechanisms such as moving intellectual property and transfer pricing (Sikka and Willmott, 2010) to move wealth around jurisdictions, making the nation-state seem like feudal lords chasing 21st-century technology.

Taxation has become a relative constant in the construction of the contemporary state, throughout history, (Winer et al., 2013) having existed in various forms for centuries. Taxation may be conceived of or framed as a form of collective property or belonging to the sovereign ruler. Early forms of taxation existed in mediaeval times, as well as the mercantile city states throughout Europe, recognised as a means of payment to the state, such as it existed in return for protection, security, services, access to basic markets, etc. Examining the history of the political economy of taxation, Kiser and Karceski suggest that contemporary conceptions of taxation began in earnest during the industrial revolution, the era representing a ‘turning point’ towards modern states, representing one of their main activities and a prerequisite of everything else states do (2017: 76). Sikka concurs, describing tax revenues as the ‘vital life blood of all democracies’ (2012: 15), without which states cannot alleviate poverty nor provide the social structures expected of a civilised society (2015). Winer et al. (2013) recognise in this statement that without taxing private entities, the body politic cannot ‘flex’ its own muscles. Therefore, taxation can be understood to have a central role in the administration of the state, without which state spending cannot be done. In other words, taxation can be described as a Hobbesian social contract not necessarily entered into voluntarily, but one which is depended on to allow the state to operate.

Taxation as we know it became more formalised during the industrial revolution: the employment of capital produced a much more reliable and accessible form of taxable economic activity. Its relative abundance therefore posed the question of ownership and use of taxation, although the key issue of taxing labour rather than taxing wealth is arguably even more contentious now than it was then. Marx contends that the ‘modern fiscal system, whose pivot is formed by taxes on the most necessary means of subsistence’ tends towards automatic progressions in which over-taxation of wage labourers follows (Marx, 1867: 921); in essence, Marx considered that wage labour bore the majority of the taxation burden and, acknowledging De Witt's maxim which recognised its inherent advantages for rendering those wage-labourers ‘submissive, frugal and industrious and overburdened with work’ (1867: 921).

During the Keynesian post-war period, Swank and Steinmo argue that the key policy role played by taxation was towards the achievement of social and economic policy objectives (2002). They point out that, post-World War II, tax policy became a ‘central instrument’ for achieving these goals (2002: 642). In fact, they suggest that the system of high marginal tax rates was a ‘centrepiece of the post-war compromise between capital and labour in all industrialised democracies’ (2002: 643), which was critical to the Keynesian welfare state (Martin, 1991: Steinmo, 1993; Swank, 1992). In this period, taxation can be described not only as allowing the state to operate but also as becoming part of the so-called ‘social safety net’ to protect citizens from sickness and job loss, and even furthermore to be considered a method of redistributing wealth from the top to bottom and keep social peace. This paper concurs with Castel's conception of ‘social property’ beyond private property and assets, which afforded a right of access to ‘collective goods and services which had a social purpose, ensuring the social security of members of a modern society, which reinforces their interdependence in a way that constitutes a society’ (2002: 319). Castel's conception has a clear application to taxation, which has come under significant challenge in the context of late-stage neoliberalism and the Californian ideology. In other words, we can conceive of taxation as a collective good to be used to improve the quality of life for the entire society, to act as a form of redistribution to lessen inequality and to be used to invest in the future development of various industries, social services and scientific progress. In certain ideological forms, taxation and indeed regulation are seen in the post-Keynesian ideological constructs as a barrier to the entrepreneurial zeal in developing industry and in turn wealth, which will ‘trickle down’ to the masses eventually. The ideological aspect of this is of huge importance at once to justify the taxation strategies of corporate actors but also in a hegemonic sense to gain consent from the wider polity and society to establish legal frameworks to allow such inequitable strategies. Finally to frame taxation as a negative theft from the rightful owners of wealth rather than as a public good, which sees a portion of the collective wealth created by a society returned.

Decline in corporate taxation rates

Rates of corporate taxation have been lowering consistently across the world for decades. Figure 1 shows how Corporate Income Tax (CIT) rates have fallen globally, from approximately 45% in 1980 to approximately 20% in 2020 (Tax Foundation, 2021). The UK case is indicative: in 1980, its corporate tax was at 52% but had fallen significantly to 19% by 2023 (Trading Economics, 2023). Key decisions made by the neoliberal Thatcher and Reagan administrations that involved changes in tax policy regulations, market liberalisation and deregulation, increasingly favoured international banking and finance and fundamentally altered the structure of western economies (Hutton, 2012; Davis and Walsh, 2016; Pianta, 2018; Berry, 2019). Moreover, the outdated system of bilateral tax treaties (Picciotto, 2013) already under pressure from substantially increased global trade, faced additional challenges from an increasingly substantial accounting sector, growing up around the issues of corporate tax compliance and avoidance (Braverman, 1974; Strange, 1988; Picciotto, 2013) which gradually formed into the formidable entity that Sikka terms the ‘tax avoidance industry’ (2015).

Corporate taxation is especially illuminating, representing as it arguably does a pinnacle of interaction between the relative, often conflicting, powers of business and society. As such, we can determine how the taxation of corporates, along with where, and at what rates they’re charged, essentially demonstrates the priorities and urgencies within contemporary political economies. Alstadsaeter et al. (2022) draw upon the key formative distinction between corporate tax avoidance and personal tax evasion. Corporations aided by the ‘tax avoidance industry’ (Sikka, 2015) apply conceptions of what represents a property and its location via mechanisms such as the location of intellectual property and transfer pricing, therefore leveraging their capital, assets and supply chains to legally minimise their tax burdens, upholding their ‘fiduciary duty’ to shareholders, while on the other hand, personal tax evasion is presented not only as a crime but a morally reprehensible, shameful act (Carr et al., 2018).

A question to be considered is to whether taxation (i.e., the surplus wealth being extracted by taxation) belongs to the state or belongs to the private entity that pays it. Is taxation theft or is the avoidance of taxation theft? For example, if we consider in Proudhon's terms that property itself constitutes theft (as it was created collectively by the working classes) is taxation (even within the capitalist state) a small element of redress of that theft? Does the ideology of tech media giants offer a justification for tax avoidance, and the following loss of funding for services supplied by the state.

Tech Media giants

This paper focuses on what we term ‘tech media giants’ due to their role not only as some of the wealthiest companies in the world but also due to their position in the cultural sphere, making them hegemonic leaders in the Gramscian sense. These companies are among the largest and most powerful in Silicon Valley and so therefore we will draw on Barbrook and Cameron's (1996) identification of the Californian Ideology to help explain how this ideology has redefined how these companies’ pay – or rather fail to pay – tax. We will begin by discussing and defining what we term tech media giants drawing from Manfred Knoche and others in the field of the political economy of communication before discussing the Californian Ideology and how this helps define the giants relationship with the state and taxation.

Firstly, we will discuss what we mean by ‘tech media giants’; here, we mean the major tech companies, for example, Apple, Alphabet (Google), Meta and Microsoft. We do this by recalling that ‘…the mass media are first and foremost industrial and commercial organisations which produce and distribute commodities’

How these companies and their various commodities are perceived is hugely important when it comes to taxation. The conception of immaterial commodities such as information and intellectual property, and how that property can be ‘moved’ across various locations has massive repercussions for how they are taxed, or not taxed. These conceptions matter in companies dealing with budgets and profits larger than the GDP of some countries. Moreover, we contend, due to the various roles of media giants, from infrastructure to media production, down to broadcasting and Social Media platforms these companies play a clear role in global hegemony, both via prestige as industrial giants and with their huge role in the cultural economy. The fact that tech giants have access to audiences 24 hours a day via smartphones, television and other devices such as ‘smart speakers’, is the kind of access that the most totalitarian regimes could only dream of. The fact that this is consensual underlines the Gramscian conception of hegemonic leadership.

The finance power that the sector holds is remarkable. Four of the ten wealthiest companies in the world are tech giants – Apple, Google, Amazon and Microsoft (McKinsey, 2021). The world's ten wealthiest companies now control over $10 trillion collectively – using market cap as a measure (Johnston, 2022) – of total world wealth of over $1500 trillion (McKinsey, 2021). This metric itself is indicative of a skew towards a financialised valuation of the economy. Given that the so-called ‘real economy’ is valued at $500 trillion, we get a sense of the vast capital resources that these companies, four of them tech giants, control – almost 7% of the total world wealth (McKinsey, 2021). Coupled with the propensity for capital to control rather than oversee production, combined with the vast tech-sector wealth (the big five are estimated at over $8 trillion collectively (Johnston, 2022), the financial power of the industry becomes clear. Beyond that, the companies’ knowledge-based data business interests, as indicated earlier, are so pervasive that arguably states have become beholden to them in terms of security provision: consider the FBI-Apple encryption ‘GovtOS’ dispute (Grossman, 2016) in which Apple flaunted its knowledge power over law enforcement; as well as a pointed yet omnipresent suggestions that, by handling nine out of ten internet searches perhaps Google, like its tech counterparts, has become ‘too big to fail’ (Wither and Jones, 2021).

While tech media tech giants are not the only industries that engage in various international strategies to avoid paying taxes, they are at the vanguard of these practices. Recently, it has been estimated that tech media companies avoided paying over £2bn Stg in the UK by Corporate Tax Advocacy Group, Taxwatch UK (The Guardian, 2023). Their importance both in terms of wealth creation and in terms of ideology make them an important area to study. Moreover, the nature of the commodities produced by their international mode of production, especially around information commodities, may act to conflate the idea of property and taxation.

Tech Media giants and the Californian ideology

Barbrook and Cameron's seminal work (1996) on the ideology surrounding the US tech sector, what they term the ‘Californian Ideology’, offers us an important insight into the information age and the philosophies underpinning it. Their depiction of a ‘bizarre fusion’ of West Coast cultural bohemianism with Silicon Valley's high-tech industries provides an irresistible cocktail that is readily picked up by the media: there are no tyrannic capitalist bogeymen in this story, only the ‘free-wheeling hippy spirit infused with the entrepreneurial zeal of the yuppies’ (1996: 1). The ideology is seen as somewhat transgressive, non-conformist or avant-garde; however, as discussed by Angela Nagle (2017), transgression can be utilised by an ideology to support current structures of class power and inequality and oppose challenges to such structures.

Barbrook and Cameron's work identifies an important strand in the development of capitalism, which imbues it with a new lease of life that makes it much more appealing to society than its stricter predecessors. It is also a much more alluring ideological sell for media industries. That the so-called tech counter-revolution has proven to have strengthened repressive power structures rather than upend them, further demonstrating the growing power in that industry (Tarnoff, 2023). Moreover, during that timeframe, the tech giants have become the biggest, most profitable and most powerful companies in the world. Ideology plays no insignificant part in their elevation. As Strange (2015: 13) notes, how can we, and to what extent can we avoid the pervasive dominance of the values purveyed by wealthy Western media? And to what extent can we avoid its impact on our socio-economic and political discourses, especially when media companies control not just the content, but the infrastructure of mediated communications.

This must also be considered within the context of neoliberalism. At its root, neoliberalism celebrates and seeks to insulate property-based power from political interferences and so further amplifies the material as well as ideological power of corporate and other concentrated capital forms. This issue is further amplified in the context of globalisation. For decades, state and supranational authorities have struggled to keep up with the activities of global firms and their accounting experts who seek to exploit variation in international tax systems. Efforts of the OECD to address this have failed to make any significant impact. The issue tends to be presented as one where the Multi-National Corporations are entitled to exploit any advantage available to them.

How the Californian ideology conceives of property

The Californian ideology began as what is described as a hybrid of leftist anti-statism opposed to militarism and oppression, and right-wing anti-statism opposed to state interference in the market. In the right-wing element of the Californian Ideology, which arguably has become dominant as the tech industry has grown, everyone is promised the opportunity to become a successful hi-tech entrepreneur. Information technologies will empower the individual, enhance personal freedom and radically reduce the power of the nation-state. Existing social, political and legal power structures will wither away to be replaced by unfettered interactions between autonomous individuals and their software. In place of counter-productive regulations, visionary engineers are inventing the tools needed to create a ‘free market’ within cyberspace, such as encryption, digital money and verification procedures. Indeed, attempts to interfere with the emergent properties of these technological and economic forces, particularly by the government, merely rebound on those who are foolish enough to defy the primary laws of nature. (Barbrook and Cameron, 1996: 7)

By way of example, we can cite Google's tax deal with the British State in the Diverted Profits Tax (DPT) controversy. This controversy began with the declaration that the Google UK subsidiary made no profits and therefore was not tax liable in. In spite of employing 2300 employees in 2016 and sales value of £3.8bn in the UK (BBC, 2016), Google argued to Her Majesty's Revenue and Customs (HMRC) that it had no permanent base in the UK economy, a defence that HMRC accepted. In addition to this, the channelling of profits by Google through The Netherlands and Bermuda has seen the company accused of exploiting tax shelters, leading to further investigations by the European Commission.

Likewise, Brennan et al. have examined the case of Apple (2017). Their work notes that the company's global operations have changed over recent decades and now maintains only a small in-house manufacturing component as part of their international investment model and has been gradually reducing their level of long-term investment in host economies. In fact, their Irish operation is the company's only self-operated manufacturing facility in the world (Irish Independent, 2017) outside of the USA. Like other tech companies, a significant part of their activity involves the offshoring of assets, in particular intellectual property assets (Burke-Kennedy, 2021). For example, instead of direct investment, Apple has turned to outsourcing of their manufacturing capabilities, primarily in China, using contracted supply chain partners to physically produce their goods (Brennan, 2017) often with poor employment conditions such as the notorious Foxconn operations. These practices, crucially, enable them to insulate themselves from the costs and complexities of operating in these regions; moreover, it prevents them from having to employ their own resources to make a profit. In essence, this means that companies like Apple can take advantage of their mobile assets and their footloose international operations. Apple exploits these dynamics globally, but also within the USA, taking advantage within US states, shifting its taxable operations from, somewhat ironically, from California to Nevada using its asset management subsidiary Braeburn Capital (Duhigg and Kocieniewski, 2012; Mazzucato, 2011).

This tech idealism conveniently ignores the state subsidies, over decades, needed to develop such industry, (Mazzucato, 2011) not to mention the hidden armies of workers needed both to work in these industries and to work in all the areas of society that supports the tech companies, including the armies of migrant workers that keep places like California afloat. It presupposes an almost feudal arrangement where tech elites have freedom, power and property whereas the labour force upholding the edifice live in ever-growing employment precarity as state provisions of housing and health are further cutback. It ignores the material reality of how commodities are created and conceives of them as immaterial property separated from the political economy at their base, allowing a justification for tax evasion policies as the immaterial commodity can be moved through creative accountancy.

This very much chimes with what can be described as the dominant ideology, or neoliberalism, a sometimes nebulous term that deserves discussion. Radical neoliberal discourse can often be anti-state or anti-political, this is from the point of view of the social democratic re-distributive state (or socialist appropriation) and state regulatory policies or programmes such as permanent employment or wage rates – where the state is seen to ‘interfere’ with the market. It is explicitly opposed to Keynesian demand interventionism. On the other hand, an interventionist state to either defend or create markets is deemed permissible (Amable, 2010: 12). The role of the state, therefore, is to keep the market competition from either collective interest of monopolisation, in that sense the neo-liberal state is regulatory; however, the state should not over-regulate and allow commerce to run freely as much as possible. This can lead to conflict within the state and between various capitalist actors, for example, a smaller business fearing competition from a perceived monopoly, or a large corporation fearing monopoly regulation, or state actors regulating to prevent monopolisation or ‘unfair’ advantages for companies.

It is important to note that alternative philosophical and redistributive arguments view taxation as a form of social contract (Rousseau, 2018) as the rightful property of states/government(s), to be used ideally for the benefit of all citizens. Or as discussed in a Keynesian sense part of the post-war social contract or even wealth redistribution. This may include the contradictions that arise surrounding taxation in the context of wealth redistribution within the capitalist state. Drawing from Castel's work on social property (2002), in the context of what is deemed public as opposed to private property (Van Dyk and Kip, 2023), taxation can therefore be considered a form of collective or social property coming from the collective efforts of a given society, to be used for the collective wellbeing of said society.

California dreaming: statelessness, mobility and tax havens

A key issue for the concept of property, commodities and taxation is the concept of location, where a property, a commodity or even a company is based. One of the dreams of the Californian ideology is the tech entrepreneur existing above the state and beyond its reach of regulation and arguably taxation, a pure ‘free market’ within cyberspace (Barbrook and Cameron 1996: 7), and this we argue is expressed in the concept of ‘statelessness’, which we will discuss below.

Traditionally states flex their power in a number of ways: their power is derived from several sources; from force, from wealth and from ideas (Strange, 2015: 26). This power gives states the capacity to do many things; to facilitate and regulate markets and to apply taxation. And markets do not and cannot exist without the state: the state provides the legislative framework that legitimises markets and enforces legal agreements between actors. Without the rigour of the law to support it, no entity could ever be certain they’d be paid for their exchange and confidence in markets’ capacity to deliver anything would evaporate (Nitzan and Bichler, 2000). While the contemporary state exists and coexists with powerful corporate actors and global structures and these institutions can exert power over the state, we must also remember that at the same time, the state uses its power to facilitate capitalist modes of production and repress its threats (Panitch and Henwood, 2011).

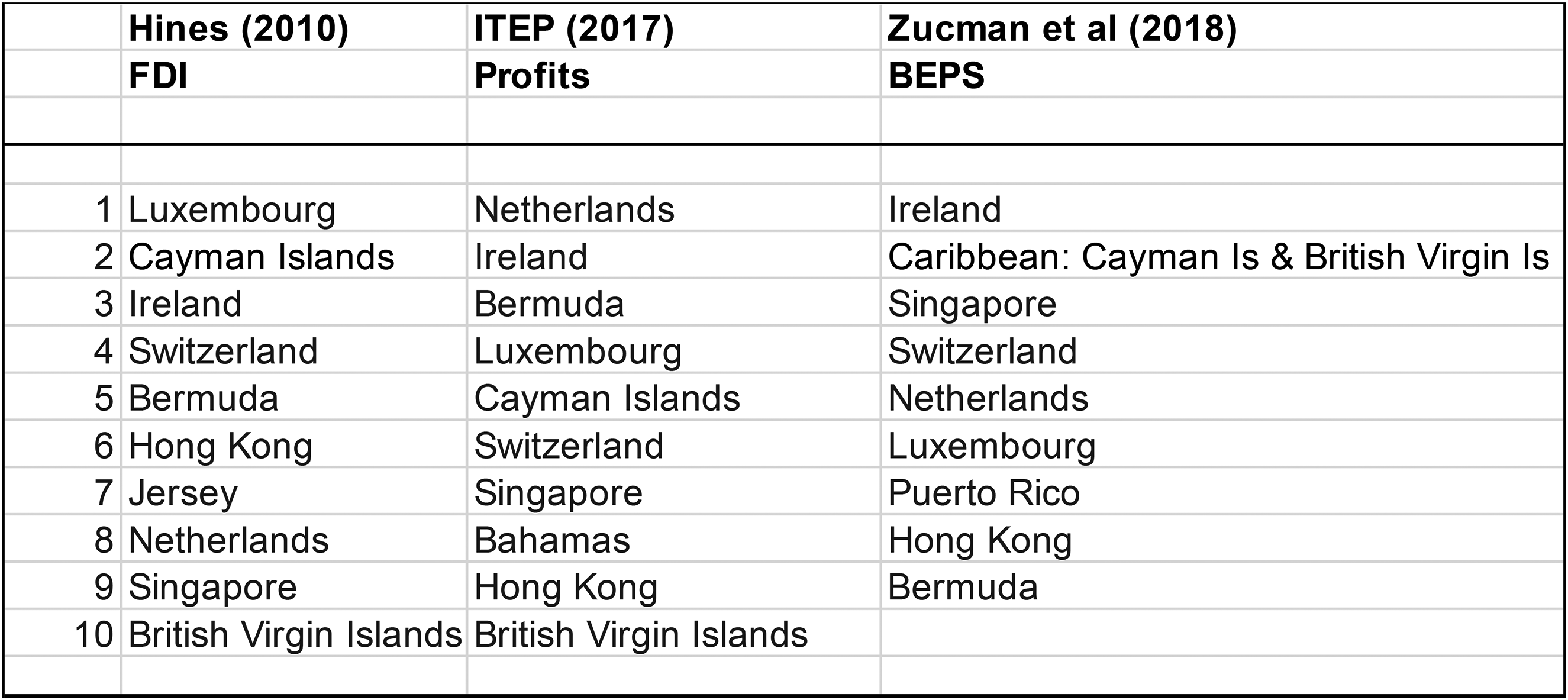

However, highly mobile companies have been able to utilise the relatively new concept of ‘statelessness’ (US Senate Report, 2013) as a corporate weapon to avoid taxation and regulation. This concept of statelessness means that companies can move between states in a tax-competitive global environment. Therefore, the location and non-location of companies, commodities and profits as imagined in the Californian Ideology has seen expression in the growth of so-called tax havens across the world economy. Companies are choosing to place either the commodity, the intellectual property or even claims of where surplus value (profits) are produced in countries with lower regulation and taxation across the world. It is no accident that much of the tech giants European and global headquarters are in Dublin, Ireland. Ireland has been singled out for its role in facilitating large-scale tax avoidance, most notably for Apple, the subject of the European Commission's ruling in 2016 (Graham and O’Rourke, 2023). While Ireland's administration persistently rejects the moniker (Paul, 2018), a number of important academic studies, using metrics of Foreign Direct Investment, profitability and Base Erosion and Profit Shifting, have identified Ireland as a tax haven (shown in Figure 2). Data produced by the US National Bureau of Economic Research found that in 2016, over half of all the foreign profits of US-owned multinationals were booked in tax havens, with Ireland topping the list, followed by Bermuda and the Caribbean, Switzerland, The Netherlands and Singapore (Wright and Zucman, 2018). In spite of the relative academic consensus on Ireland's status as a tax haven, following the publication of the Zucman and Torslov study which found that over $100 billion of corporate profits had been shifted to Ireland in 2015, Ireland's Department of Finance disputed its findings, rejecting them as ‘overly simplistic’ (Paul, 2018).

Top ten international tax havens (Hines, 2010; ITEP, 2017; Zucman and Wright, 2018).

Highlighting a report on taxation published by the European Parliament (2019), Stewart notes that the parliament also identifies Ireland and four other member states – Cyprus, Malta, Luxembourg and The Netherlands – as tax havens; moreover, that report calls on the European Commission to recognise them as such until ‘substantial tax reforms are implemented’ (2019). Stewart identifies further features of a tax regime consistent with tax havens: they tend to grant extremely generous depreciation allowances on assets, offer tax favoured financing (such as Section 100 loans) and tax concessions on intangible assets, such as Intellectual Property which replaced the ‘stateless income’ and ‘double Irish’ tax loopholes (2019); this was in spite of the Irish Minister for Finance's commitment in 2013 to eliminate statelessness (Kelleher, 2014). The European Parliament's (2019) report concurs with previous findings which identify some of the activities that are common to these states that ‘facilitate aggressive tax planning’. The European Parliament's report also cites two previous reports by Oxfam (2016, 2017), which identifies the same five states as tax havens. This report further condemns member states that potentially confiscate the tax base of other states, while at the same time allowing companies to artificially lower their tax payments, a practice that they consider to contradict EU solidarity while at the same time redistributes wealth to MNEs at the expense of European citizens (2019).

According to the OECD, the concept of a ‘tax haven’ does not have a specific technical meaning, but they do identify two key criteria that mark out potential tax havens: the first are countries which can finance their public services with none or nominal income taxes and offer this facility to non-residents who wish to avoid taxation in their own country of origin; second, those countries which do obtain significant revenue from income taxes but whose ‘tax system has features which constitute harmful tax competition’ (OECD, 1998: 20). Using different criteria, countries such as Ireland have been singled out based upon FDI (Hines, 2010), based upon profitability (ITEP, 2017) and BEPS data (Tørsløv et al., 2018) – these studies all find Ireland to be within the top three tax havens in the world. Added to the OECD's own definition, relating to ‘harmful tax competition’ almost certainly applies in the Irish case. Therefore, Ireland's role within global corporate tax avoidance is key. It has been subject to controversy nationally (Stewart, 2013) and internationally, largely through the use of a series of subsidiary companies including Apple Operations International (AOI) which it incorporated in Ireland in 1980. This type of subsidiary management was instrumental in what culminated in the European Commission's 2016 ruling on Apple's tax affairs (Jacobson, 2018).

Apple's overseas operations which was addressed in the US Senate Subcommittee’ investigation into its corporate practices (2013) found that the company considered itself, for the purposes of taxation, to be beyond the jurisdiction of any state – in other words, ‘stateless’. Similarly, while Google's productive output is less easily defined, it nonetheless has managed to outsource large parts of its economic activity beyond the reach of ‘Uncle Sam’, again despite its receipt of significant government investment (Mazzucato, 2011). This characterises the contemporary ‘intangible economy’ (Ciuriak and Akinyi, 2021) and the additional challenges it presents to the authority of the state.

Living the dream: evidence of tax evasion by tech Media giants

As discussed above many, of the tech media giants are no strangers to controversy in relation to the payment of corporate tax, such as the recent cases of Apple and Facebook (Meta) in Ireland, Alphabet (Google) in the UK and Amazon in Luxembourg (Graham and O’Rourke, 2021) While the tech media giants are not the only global corporations who take advantage of international tax avoidance opportunities, this paper argues that their hypermobility and unprecedented cash assets place them especially well to take advantage of these practices.

Moreover, the nature of some of the commodities, such as software or intellectual property that can be moved at the touch of a button, or even by a simple re-conception of where the property resides can mean a state gaining or losing billions of dollars. Moreover, this mystique attached to their technologies often renders the logistics of their operations impenetrable to oversight, such as in the case of Google and HMRC in the UK, when the latter accepted that in spite of employing thousands of people, the former did not actually operate a ‘permanent base’ in the UK. The ideological aspect of the tech media giants and their justification for tax avoidance of importance as a justification is needed to allow for such inequitable taxation strategies to be practised. Moreover, as discussed the tech media giants via their roles in the tech industry, their role as a major part of the wider industry and their role in the cultural industries act as hegemonic leaders to create political consent for what are severe inequalities. The Californian ideology itself a fusion of tech and cultural ideologies acts as a bedrock to this justification. Tax and regulation are not avoided for greed, but rather to release the entrepreneurial spirit of innovators to develop technology that will make all our lives better, innovative solutions to the state's attempts to tax and regulate the giants are avoided by non-conformist/transgressive entrepreneurs engaging in new ways of thinking about property.

For decades, authorities have struggled to regulate tech media organisations as they operate outside of traditional regulatory jurisdictions (European Commission vs Microsoft, 2007 & 2023; European Commission vs. Facebook, 2014; European Commission vs. Google, 2017; European Commission vs. Amazon, 2019; see Europa.eu for details, 2024); their technologies allowing them to stay a number of steps ahead of the governmental authorities. In other words, tech giants are using conceptions of property, commodities and location of intellectual property rights, commodities and profits to ‘move’ such conceptions to states with less regulation or taxation, or as discussed above tax and regulatory havens, living the Californian dream of unencumbered markets.

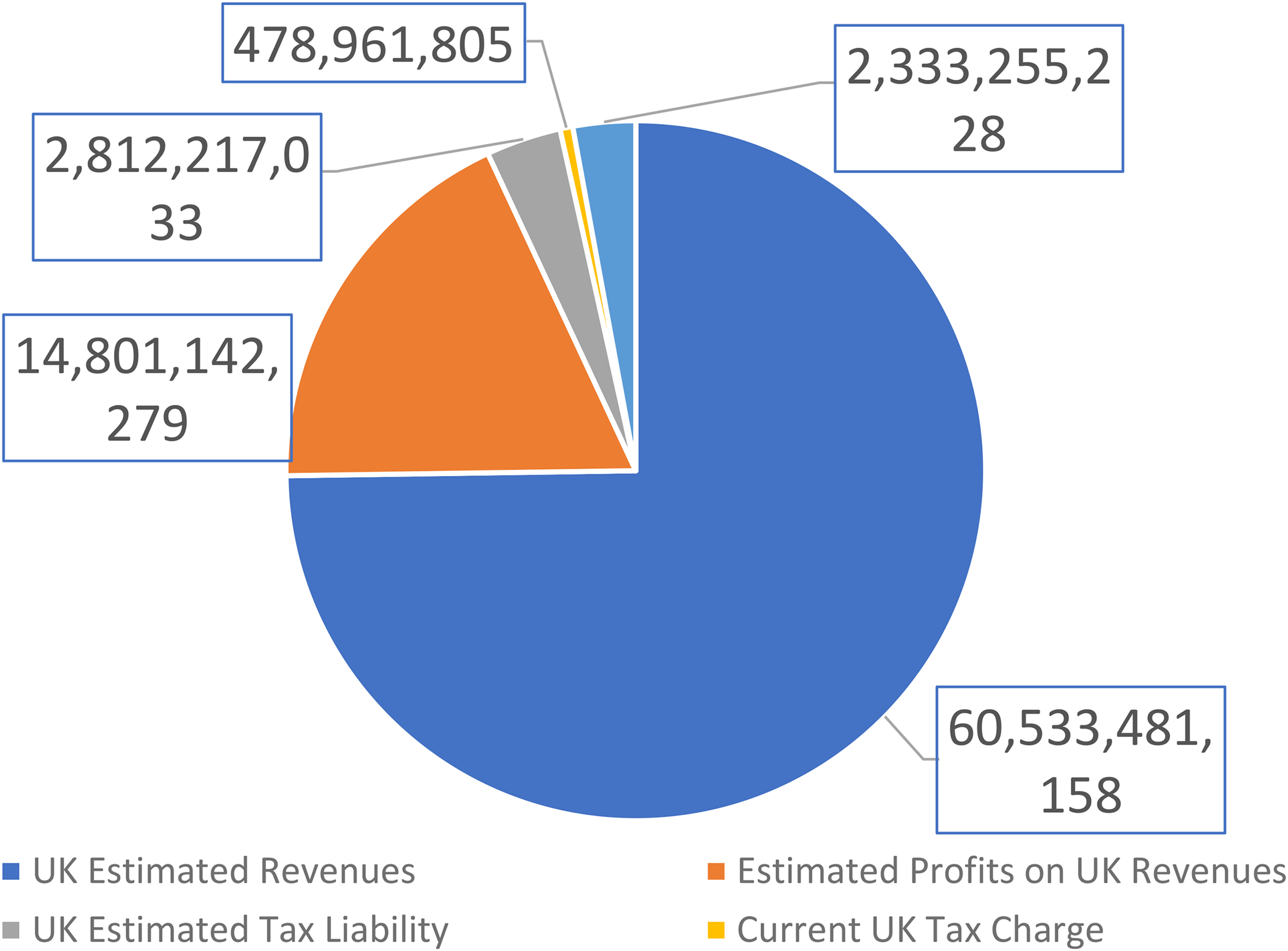

Owing to the murky nature of the tax avoidance industry and its mechanisms; we must necessarily be sceptical of the figures it reports. Typically, the corporate giants involved offer statements around paying ‘the required level of taxes under international rules’ as platitudes to those concerned by CTA. However, the UK experience of corporate tax avoidance, following the Parliamentary Public Accounts Inquiry in 2013, catapulted the issue into public consciousness (Figure 3).

Potential corporate tax returns, Taxwatch UK, 2023.

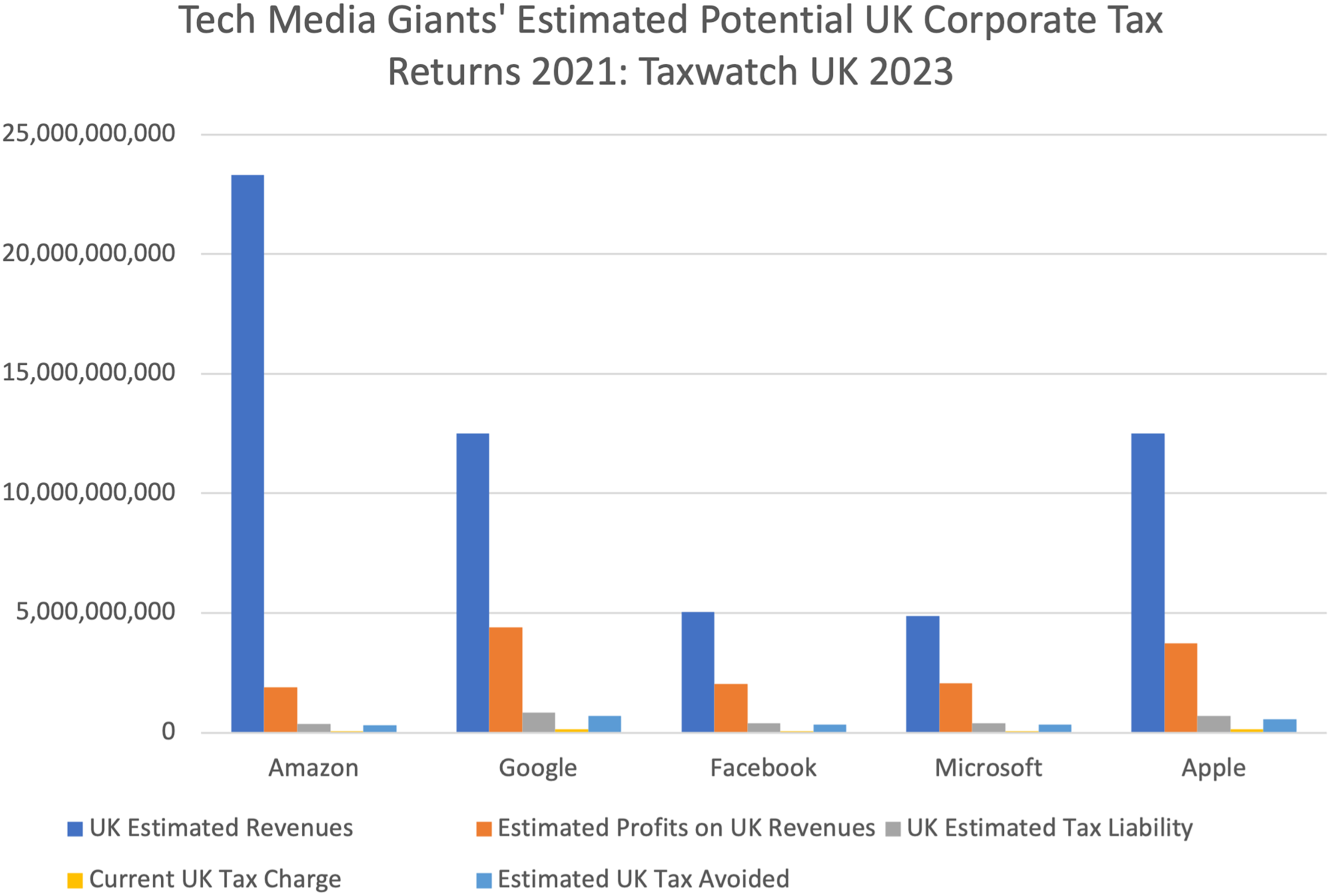

Controversial corporate tax practices have courted more public controversy in the UK than elsewhere over the past decade (Graham and O’Rourke, 2023), attributable in part to the strident activities of tax activist charities and NGOs (Ashour, 2021). Taxwatch UK has estimated substantial collective tax avoidance by some of the largest and most profitable global companies operating in the UK, and in particular single out the tech media giants for what they estimate is significant tax avoidance. Investigating beyond these companies’ complex tax-driven structures, Taxwatch assesses substantial underpayment of taxes by Amazon, Google, Facebook, Microsoft and Apple to the extent of £2bn Stg (Taxwatch, 2023). Figures 3 and 4 elaborate on this.

Taxwatch UK's estimated potential corporate tax loss.

As discussed, the rise of so-called tax competition (Picciotto, 2013), coinciding with the effects of globalisation, has meant tech media giants are increasingly mobile and able to take advantage of the ever-reducing tax rates on offer in different countries around the world (Brennan and Bakir, 2016) – their output being largely intangible, it is particularly suited to mobility; tech media giants like Apple were sufficiently mobile to operate key subsidiaries which had ‘no declared tax residency anywhere in the world’ (PSI, 2013: 4). In 1998, the OECD recognised the existence of what it termed ‘harmful tax competition’ and proposed the idea of collaborative initiatives to coordinate tax globally. Acting as conceived of by the Californian Ideology in a free market outside the regulatory arm of the state. Moreover, the establishment of tax havens, from the Caribbean to Switzerland to the Channel Islands, has placed further downward pressure on corporate tax rates (Jacobson, 2018). More worryingly, Zucman (2021) has quantified that these account for the equivalent of $7.6 trillion, which he contends represents a huge threat to the world economy. For these reasons, there have been increasing demands to attempt to provide a platform for the possible cooperation on tax policies with cross-jurisdictional effects (Bartelsman and Beetsma, 2003), which have culminated in the Base Erosion and Profit Sharing (BEPS) agreement (OECD, 2020). However, the OECD has struggled to garner full cooperation for this agreement, not least from Ireland itself, which has been very keen not to jeopardise its low corporate tax reputation internationally.

These examples demonstrate the enormous market, for and of itself, which the ‘Tax Avoidance Industry’ now constitutes. A number of authors draw attention to the practices used within that industry: under the guise of financial innovation, the international tax avoidance industry combines a strong national presence while marketing its international network (Raitasuo and Ylonen, 2022; Fichtner, 2016) and by exploiting loopholes in international tax treaties (Arel-Bundock and Blais, 2023). Moreover, the role that accounting plays, as powerful ‘agents of capital’ cannot be understated; as without that ‘industry's’ participation, it would be difficult to imagine how individual companies, even large ones, could possibly have instituted such expansive and coordinated international tax practices (Fichtner, 2016).

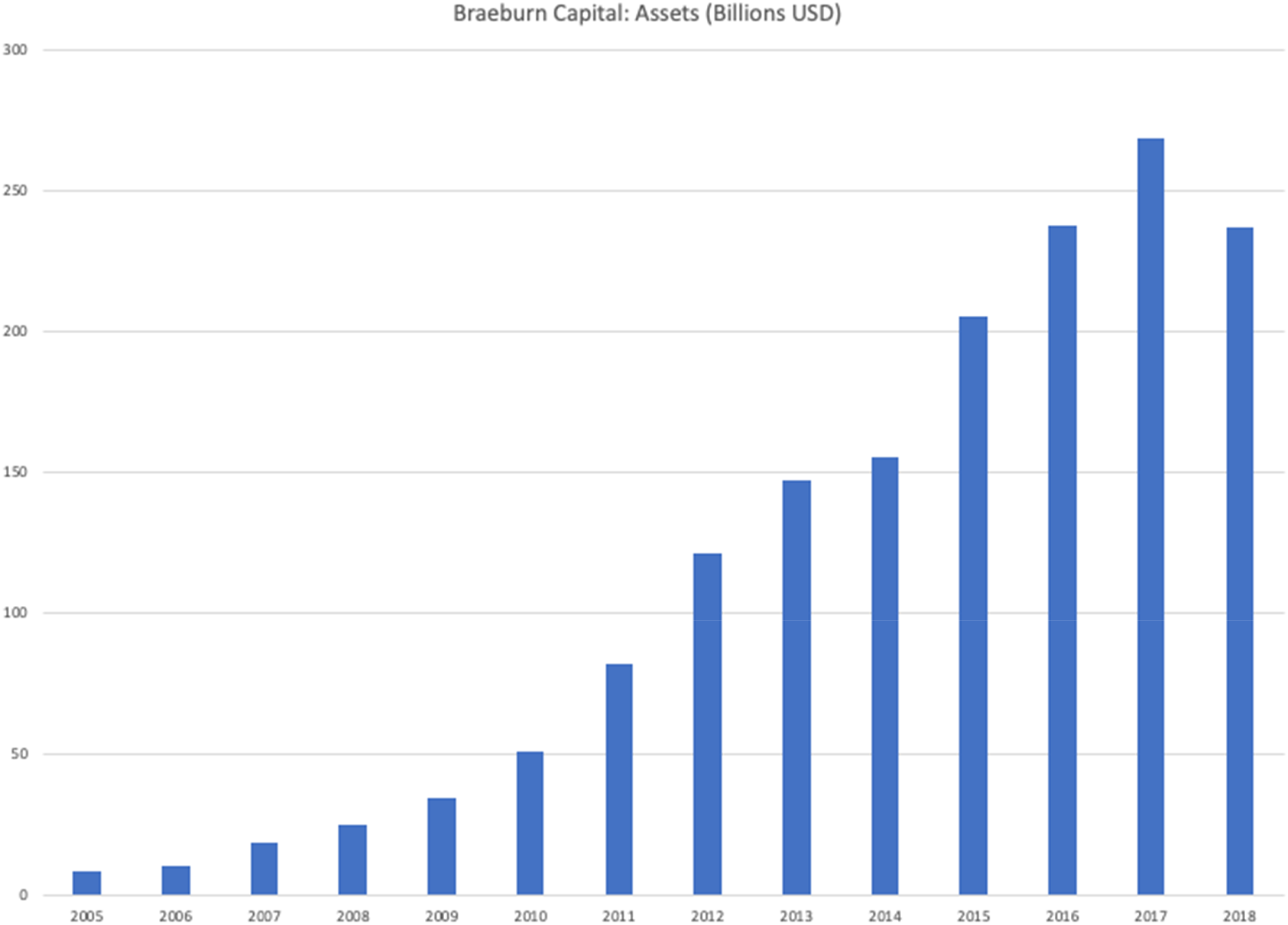

Although synonymous with the state of California, its long-time home, Apple ironically crossed its state border to Nevada in order to its home state's corporate income tax rate of 8.84% (Loughead, 2024), demonstrating what Marx termed the true mobility of capital. The company uses its wholly owned asset-management subsidiary, Braeburn Capital, to take advantage of Nevada's tax corporate tax status. The following graph shows the short, long and cash asset holdings of Apple Inc by its asset management subsidiary Braeburn Capital, which manages 70% of Apple's total book assets (Gilbert and Hrdlicka, 2018). They contend that the parent company behaves like a hedge fund, supporting their enormous portfolio with $115 billion worth of debt, facilitating large-scale tax avoidance as Braeburn is registered in Nevada, itself a US tax haven with no corporate income tax levy (Tax Foundation, 2024; Figure 5).

Braeburn's capital assets: 2005–2018 (Gilbert and Hrdlicka, 2018).

Conclusion

In this paper, we have discussed the changing nature of taxation and the state, going from early forms of taxation to the Keynesian concept of taxation ‘for the greater good’ to the reorganisation of the global economy and market over centuries until finally landing at the present state of highly mobile transnational corporations, using both creative tax strategies and leveraging their size and multi-national status to avoid paying tax in individual states. We discussed how this has been aided by developments in global communication technology and indeed by the tech media giants themselves, who we argue act as hegemonic leaders through their status as global industries and their status as cultural leaders. We argue that the so-called ‘Californian ideology’ born with these tech giants in their infancy, as a mix of transgressive politics, futuristic idealism and an anti-state ideology has infused to create a justification for these industries moving above and beyond state structures, being internationalist or global and avoiding what would be seen as meddlesome regulation and taxation. The ideology's conception and reality of immaterial commodities and intellectual property rights which can be anywhere, while also being nowhere has allowed the companies to avoid tax and regulation in their dream of a pure market in ‘cyberspace’ avoiding the clutches of the nation-state. It is a contradictory ideology as the tech industry itself could not exist without direct state subsidies, and indirect subsidies such as access to an educated workforce and most importantly the state acting to protect intellectual property rights. It is at the same time a form of liberalism, but one given new emphasis by a young and dynamic industry. However, the loss of this taxation, both to be used as a social safety net, to support necessary infrastructure in health, education, etc and even as a method of redistribution, negates the post-war social contract and leads to greater inequalities at local and global levels.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.