Abstract

Crowdlending offers entrepreneurs and lenders a low-barrier alternative to traditional finance but operates under high uncertainty and limited firm-level information, requiring reliance on observable cues. One crucial cue arises when entrepreneurs disclose and explain prior failure. Drawing on attribution theory, we examine how crowd lenders respond to different failure attributions and how this shapes willingness to invest. Using a metric-conjoint experiment in Germany (N = 78; 2496 observations) and analysing results with linear mixed-effects models, we find that lenders react more positively to internal, controllable, and unstable attributions compared to external, stable, and uncontrollable causes. Moreover, gender differences emerged, with female lenders responding differently from men. By shifting the focus from the self-responses by entrepreneurs to lender evaluations, we extend attribution theory to the crowdlending context and demonstrate how gender shapes the interpretation of failure signals. These insights advance understanding of decision-making in alternative entrepreneurial finance, informing entrepreneurs, lenders, and platform design.

Introduction

Failure is an inherent aspect of entrepreneurship, with approximately two-thirds of businesses ceasing operations within their first five years (Czakon et al., 2024; Jenkins and McKelvie, 2016; Roccapriore et al., 2021). Typically, it is defined as the termination of a venture that has fallen short of its economic goals due to an inability to sustain operations or generate sufficient returns (Ucbasaran et al., 2013). Despite the prevalence of failure, however, many entrepreneurs persist in launching new ventures and seeking funding (Al-alawi et al., 2025; Plehn-Dujowich, 2010; van Praag, 2003). In these instances, their track record of failure becomes a critical cue for potential investors. While failure occurs across all forms of entrepreneurial finance, it is particularly pronounced in crowdlending, where default rates remain a significant concern (Dorfleitner et al., 2023). Crowdlending enables entrepreneurs to raise funds from many individual lenders by offering repayment with interest, typically via online platforms that facilitate borrower–lender matching (Escudero et al., 2025). Examples of these platforms include bettervest.com and LendingClub. Estimates suggest that by 2025, the global crowdlending market will grow to US$33.70 billion, which is an increase of 4.30% from the previous year (Statista, 2024). By removing institutional intermediaries, crowdlending lowers barriers to capital but also reduces formal screening, leaving lenders with limited borrower information (Cumming and Sewaid, 2024). Consequently, lenders must rely on surface-level cues provided on the platform to assess entrepreneurial credibility and competence (Cumming and Hornuf, 2022; Hoegen et al., 2018; Shafi, 2019). Among these cues, an entrepreneur’s experience, especially a history of failure, can be crucial in shaping lender perceptions (McSweeney et al., 2025).

Previous research shows that prior entrepreneurial failure can be perceived both positively and negatively by crowd lenders (Bai and Gao, 2023; McSweeney et al., 2025). For example, Roccapriore et al. (2021) find that prior failure leads to negative perceptions of entrepreneurs (e.g. lower perceived competence and trustworthiness), to the extent that entrepreneurs with prior failure are viewed more negatively compared to entrepreneurs without any entrepreneurial experience. This, in turn, can negatively affect investor willingness to invest (Zunino et al., 2022). At the same time, existing evidence suggests that prior failure can be reframed as a learning experience that increases resilience and skill, thereby enhancing entrepreneurial credibility when presented effectively (Cumming and Hornuf, 2022; Ucbasaran et al., 2013). However, this positive interpretation is highly contingent on contextual factors, such as an entrepreneur’s narrative framing (Anglin et al., 2018; Shepherd and Patzelt, 2015). Crowd lenders tend to be a more heterogeneous group and less experienced than traditional investors, and, hence, they may be particularly sensitive to such framing (Burtch et al., 2016).

The underlying mechanisms driving the positive or negative reactions of crowd funders remain insufficiently understood. Accordingly, we introduce attribution theory (Weiner, 1985), which suggests that observer reactions depend on how they attribute the causes of an outcome based on the dimensions of locus of causality (internal vs. external), stability (stable vs. unstable), and controllability (controllable vs. uncontrollable). Applying attribution theory helps explain why some crowd lenders react to failure negatively, for example, when it is attributed to external, stable causes, while others interpret failure more positively, for instance, when attributed to internal or unstable causes. It is important for crowd lenders to investigate these mechanisms, as they are often unaware of the underlying rationale driving their decisions, which may lead to suboptimal investment outcomes. For example, they could choose to fund an entrepreneur who has not failed before, rather than one who has, because they see prior failure as a negative cue. However, in reality, the latter may actually lead to a better return on investment. The impact of boundary conditions on lender perceptions of previously failed entrepreneurs is scattered and ambiguous (Anglin et al., 2018). In particular, the gender of the crowd lender seems to be important, but underdeveloped (Wang and Prokop, 2025). Crowd lenders are highly diverse, coming from various backgrounds and experiences, which shape their investment behaviours (Burtch et al., 2014; Cumming and Hornuf, 2022; Dushnitsky et al., 2016). Although approximately 70% of crowd lenders are men, the share of women lenders is steadily increasing (Shneor et al., 2024).

Previous research on equity crowdfunding, an investment model closely related to crowdlending, suggests that gender differences influence investment preferences. For instance, inexperienced female crowd investors are more likely to support women entrepreneurs (Bapna and Ganco, 2021; Harrison et al., 2020). Furthermore, women who join women-only networks invest more frequently and are more open to other investor opinions compared to women in mixed networks (Harrison et al., 2020). As entrepreneurial failure is perceived either positively or negatively in crowdlending (Bai and Gao, 2023), how a lender’s gender influences failure attributions in either direction remains unclear (Mohammadi and Shafi, 2018). Given that failure is a high-risk signal, and risk tolerance varies by gender (Hervé et al., 2019; Ren et al., 2025), it is critical to investigate whether male and female crowd lenders interpret failure attributions differently. This is important as it can help crowd lenders become more aware of their own potential biases. For instance, male lenders are more willing to support previously failed entrepreneurs, that is, due to the higher risks associated with such entrepreneurs, while female lenders are more cautious, which may lead to an unequal gender distribution of support and limit the diversity of perspectives in investment decisions. This may reduce long-term success for both lenders and ventures, as diverse funding teams have shown to improve the success of ventures (Greenberg and Mollick, 2017).

In this regard, we aim to answer the following research questions: How do crowd lenders react to distinct failure attributions of entrepreneurs? How does the gender of crowd lenders influence their reactions to an entrepreneur’s attribution of failure? To answer these two research questions, we employ a metric-conjoint experiment (N = 78, 2496 observations), a method that enables scholars to evaluate how individuals make complex, multidimensional decisions by presenting them with systematically varied profiles and quantifying their preferences (Green and Srinivasan, 1978). We chose this method because it mirrors the real-world decision environment of crowd lenders, who must simultaneously consider multiple pieces of information when making funding decisions.

This study offers three important contributions. First, while prior research primarily focuses on the entrepreneur’s internal response to failure (Anglin et al., 2025; Berchicci and Boons, 2025; Sewaid et al., 2025), we shift attention to third-party reactions (Bai and Gao, 2023; Roccapriore et al., 2021; Souakri et al., 2023), highlighting the relevance of failure attributions as an observable cue in early-stage funding decisions. Second, we investigate these third-party reactions in the context of crowdlending, where lenders lack access to detailed firm-level data and face high uncertainty, by showing that entrepreneurial failure substitutes for formal evaluation mechanisms (Bai and Gao, 2023; Bort et al., 2024; Cumming and Sewaid, 2024; Zunino et al., 2022). Third, we contribute to gender research in entrepreneurial finance by examining whether male and female crowd lenders interpret failure attributions differently (Bapna and Ganco, 2021; Mohammadi and Shafi, 2018), thereby offering new insights into how lender reactions shape inequality dynamics in alternative finance. In this way, we directly respond to the call by Roccapriore et al. (2021).

Theoretical background and hypotheses development

Attribution theory

Attribution theory (Heider, 1958; Weiner, 1985) provides a suitable framework for examining how crowd lenders respond to causes of failure (Kibler et al., 2017; Mandl et al., 2016). Heider (1958) describes individuals as intuitive psychologists striving to understand the world. According to attribution theory, individuals seek causal explanations for success or failure along three dimensions: locus of causality, controllability, and stability (Weiner, 1985). While this framework has been applied extensively to understand social and organisational judgements, its application to investment decision-making, particularly in the context of entrepreneurial failure, remains underexplored (Kibler et al., 2017; Mandl et al., 2016; Sewaid et al., 2025). The locus of causality identifies whether the cause of an event is internal, such as personal traits or actions, or external, meaning arising from situational factors (Harvey et al., 2014). Controllability refers to whether the factors are under an individual’s control (Weiner, 1985), and stability reflects whether the causes persist over time (Harvey et al., 2014). These dimensions influence psychological responses, including affective reactions and expectations for future success, which inform subsequent actions (Weiner, 1985). These mechanisms are particularly relevant in negative events, such as entrepreneurial failure, where the need to find explanations for potential causes is heightened (Gendolla and Koller, 2001; Sewaid et al., 2025). Research on entrepreneurial failure has shown that the entrepreneur’s descriptions of failure align with configurations of attribution dimensions (Mandl et al., 2016). In the context of crowdlending, entrepreneurs can explain their failures to potential lenders along these dimensions to influence affective responses, expectations of success and investment decisions.

Failure in crowdlending

Crowdfunding allows entrepreneurs to raise capital from a large pool of funders via online platforms, encompassing donation-based, reward-based, equity-based and lending-based models (Escudero et al., 2025; Rejeb et al., 2024). Unlike donation-based models, which rely on voluntary contributions with no financial return, or reward-based approaches, where funders receive non-monetary incentives, crowdlending involves debt financing, requiring entrepreneurs to repay loans with interest (Cumming and Sewaid, 2024; Escudero et al., 2025). In contrast to equity crowdfunding, where funders receive company shares, crowd lenders act as lenders rather than co-owners (Escudero et al., 2025).

Crowdlending operates in a high-uncertainty, information-asymmetric environment, where entrepreneurs have insights about their skills and venture risks that lenders cannot directly observe (Cumming and Hornuf, 2022; Cumming and Sewaid, 2024; Hoegen et al., 2018). Other than traditional financial institutions, crowd lenders lack access to extensive due diligence and rely on heuristic cues, such as prior experience, to assess credibility and risk (Davies and Giovannetti, 2022). Accurate assessments are vital for minimising risk and maximising returns (Hoegen et al., 2018; Slimane and Rousseau, 2020), as unsecured crowdlending loans can have default rates as high as 27% (Dorfleitner et al., 2023; Kgoroeadira et al., 2019; Vanacker et al., 2019).

Due to limited verifiable information, the characteristics of entrepreneurs and impressions derived from them play a key role in crowdlending decision-making (Hoegen et al., 2018). The prior experience of entrepreneurs, for instance, constitutes critical information for crowd lenders that can affect financing success (Chila et al., 2025; Huang et al., 2022). Previous research thus far, has examined the impact of prior entrepreneurial or crowdfunding experience on financing outcomes (Davies and Giovannetti, 2022; Huang et al., 2022). Entrepreneurial experience, is highlighted as a key criterion for investment decisions in early-stage ventures (Escudero et al., 2025). In particular, an entrepreneur’s experience reflects their prior activities and may influence crowdfunding success (Zunino et al., 2022). However, researchers emphasise the importance of distinguishing between previous successes and failures. Given the high failure rates of start-ups and the tendency of many individuals to re-enter entrepreneurship despite past failures (Al-alawi et al., 2025; Plehn-Dujowich, 2010), understanding the implications of past failures is crucial. Many entrepreneurs seeking crowdfunding have likely experienced entrepreneurial failure (McSweeney et al., 2025), which poses challenges in securing financial resources (Lindlar et al., 2025). Initial evidence suggests that crowd lenders react both positively and negatively to entrepreneurs with prior failures (Bai and Gao, 2023; Zunino et al., 2022). This pattern is consistent with attribution theory, which posits that in the absence of complete information, external evaluators rely on observable cues to infer underlying characteristics. Thus, in the context of crowdlending, an entrepreneur’s history of success or failure provides such cues, shaping lender attributions regarding the entrepreneur’s competence, trustworthiness and potential (Cardon et al., 2011; Zunino et al., 2022).

Formulation of hypotheses

Locus of causality and investment willingness among crowd lenders

According to attribution theory, individuals infer the causes of others’ actions by assigning responsibility either to internal dispositions or external circumstances (Weiner, 1985). In the context of crowdlending, the explanations of entrepreneurs for past failures, whether framed as internally or externally caused, serve as an observable cue that shapes how crowd lenders assess their credibility and investment potential. However, the favourability of these attributions remains debated due to mixed implications for investment and credibility. While external attributions may help entrepreneurs distance themselves from failure by framing it as circumstantial, for example, market conditions or team issues (Sewaid et al., 2025), the relevance of these attributions for crowd lenders remains contested. For lenders, such explanations can mitigate concerns about emotional instability or poor leadership continuity (Kibler et al., 2017; Walsh and Cunningham, 2017). Therefore, crowd lenders may view external attributions with suspicion. Due to the fundamental attribution error, observers tend to overemphasise personal responsibility and underemphasise situational factors when evaluating the failures of other (Pronin et al., 2004). Thus, crowd lenders may perceive external attributions as evasive or self-serving, which could potentially undermine trust in an entrepreneur’s integrity and competence.

Conversely, internal attribution, which means to take responsibility for failure, can signal credibility and responsibility (Jenkins et al., 2024) and positively influence entrepreneur behaviours (Lee et al., 2024), which in turn fosters lender trust. When entrepreneurs acknowledge personal responsibility, it aligns with expectations regarding the cause of failure (Kibler et al., 2017). Consistent with this view, Lee and Tiedens (2001) found that individuals in high entrepreneurial positions who adopt internal attributions are perceived as more credible after negative events. Credibility serves as a crucial cue for entrepreneurs to secure investments in crowdfunding (Courtney et al., 2017; Huang et al., 2022). Furthermore, Dinh et al. (2024) suggest that crowd lenders are not solely driven by financial returns but also by social and altruistic motivations. Thus, entrepreneurs demonstrating accountability for their failures may resonate with the crowd lender’s desire to support responsible, resilient and socially conscious ventures. Beyond credibility, internal attribution signals self-reflection and learning potential (Lee et al., 2024), as entrepreneurs who recognise their own role in failure are more likely to develop corrective strategies and improve future performance (Cope, 2011; Lee and Chiravuri, 2019). In addition, it may also promote counterfactual thinking, whereby entrepreneurs actively analyse what they could have done differently to develop effective strategies for the future, which also benefits the crowd lender who invests in the business (Baron, 2008). Internal attribution can thus facilitate learning from failure, fostering the development of entrepreneurial knowledge, skills and personal growth (Espinoza-Benavides and Díaz, 2019; Walsh and Cunningham, 2017; Yamakawa et al., 2010).

If entrepreneurs perceive the learning effects as insufficient relative to the failure costs, they may be less inclined to pursue entrepreneurship again (Ucbasaran et al., 2013). As prior entrepreneurial success strongly increases the likelihood of subsequent success, while prior failure does not, the framing of past failures emerges as an especially important cue for crowd lenders (Gompers et al., 2010). A subsequent venture, combined with internal attribution, could signal to lenders that an entrepreneur is resilient, has addressed necessary personal adjustments, has experienced learning effects and is capable of bearing the costs of failure (Mantere et al., 2013; Ucbasaran et al., 2013). Conversely, external attribution may demonstrate that entrepreneurs are unlikely to change their behaviour in the future, even though lenders may regard such behaviour as the cause of failure due to the fundamental attribution error (Harvey et al., 2014; Ross, 1977).

Overall, while external attributions may reduce personal blame, they can also appear as an avoidance of responsibility, weakening lender confidence. In contrast, internal attribution enhances credibility, signals learning and aligns with lender expectations, possibly rendering it a more favourable strategy in crowdlending decisions. Therefore, we hypothesise the following:

Controllability and investment willingness among crowd lenders

Controllability refers to the extent to which entrepreneurs control the causes of failure. Luck and task difficulty are considered uncontrollable, whereas effort and ability are controllable (Harvey et al., 2014; Weiner, 1985). Attribution theory suggests that failures attributed to uncontrollable causes tend to elicit sympathy, while those stemming from controllable mistakes provoke frustration or blame (Graham, 1991). Kibler et al. (2017) found that entrepreneurs who attribute failure to uncontrollable factors are perceived as more legitimate by the general public. However, different stakeholders may exhibit varying reactions to attributions depending on their relationship with the failed entrepreneur (Kibler et al., 2017). Unlike passive observers, investors engage in financial risk-taking and expect entrepreneurs to exert control over key business outcomes (Frydrych et al., 2014). Entrepreneurs play central roles in determining a venture’s success or failure (Müller et al., 2023), making their attributions to uncontrollable factors potentially concerning for investors (Lee and Tiedens, 2001). While an entrepreneur may genuinely lack control over external circumstances, acknowledging this lack of control may signal an inability to secure critical resources, adapt to challenges or make necessary adjustments (Lee and Robinson, 2000; Marshall et al., 2020).

Conversely, attributing failure to controllable factors signals self-awareness and a proactive attitude towards improvement. Entrepreneurs who take responsibility for failure demonstrate a capacity for learning and adjustment, thereby reducing lender concerns about repeated mistakes (Amankwah-Amoah et al., 2022; Harvey et al., 2014). Since crowd lenders have limited means to verify an entrepreneur’s capabilities (Hoegen et al., 2018), controllable attributions may be important heuristic cues that suggest learning potential and resilience (Roccapriore et al., 2021). Additionally, entrepreneurs who acknowledge and learn from controllable mistakes are more likely to receive support. Attribution theory suggests that individuals who recognise their role in failure and actively address it are perceived as more competent and capable of future success (Ucbasaran et al., 2013). However, attributing failure to uncontrollable factors may raise doubts among lenders about an entrepreneur’s ability to make necessary corrections or their ability to gain control over critical resources in the future, thereby increasing the likelihood of repeated failures (Harvey et al., 2014; Lee and Robinson, 2000).

Thus, while uncontrollable attributions might elicit sympathy, they can also signal passivity and raise doubts about an entrepreneur’s ability to adapt. In contrast, controllable attributions suggest learning, self-improvement and reduced likelihood of future failure, making them a stronger signal of investment potential. Hence, we hypothesise the following:

Stability and investment willingness among crowd lenders

Stability refers to the persistence of the factors that lead to success or failure (Harvey et al., 2014) and is associated with expectations about whether these factors will recur in the future and whether they will lead to repeated (mis)success. The link between stability and expectations can also evoke feelings of hope or hopelessness (Weiner, 1985). Attribution to non-recurring, unstable factors could foster hope for the future, potentially enhancing the perceived legitimacy of entrepreneurs after failure, which may positively influence investment decisions in crowdlending (Huang et al., 2022; Kibler et al., 2017; Weiner, 1985). Conversely, attribution to stable factors may lead lenders to expect future failures, creating a sense of hopelessness regarding the venture’s prospects (Kibler et al., 2017; Weiner, 1985). If the attribution conveys the impression that the failure factors will persist, lender confidence in the entrepreneur’s ability to achieve future success may be undermined (Kibler et al., 2017). Attribution to unstable factors, on the other hand, could reinforce expectations that future failures will not recur, potentially signalling a lower risk of failure compared to stable attributions (Weiner, 2018). This would positively affect investment willingness, as crowdlending investors carefully weigh risk and return (Hoegen et al., 2018; Slimane and Rousseau, 2020). Thus, we posit the following:

The moderating role of stability

While the dimensions of attribution theory are conceptually distinct, the literature has also explored their interrelationships (Kibler et al., 2017; Walsh and Cunningham, 2017; Yamakawa et al., 2010). Existing research indicates that the stability of failure factors can influence reactions to attributions regarding the locus of causality and controllability (Homsma et al., 2007; Kibler et al., 2017). To prevent repeated failures, it is expected that entrepreneurs learn from their failures and leverage the knowledge gained in future entrepreneurial endeavours (Eggers and Song, 2015; Ucbasaran et al., 2013). When failure is attributed to internal and controllable factors, it is typically seen as unstable, meaning entrepreneurs can adapt and avoid the same mistakes (Harvey et al., 2014; Schwarzer and Weiner, 1991; Walsh and Cunningham, 2017; Yamakawa et al., 2010). In contrast, stable attributions suggest that failure is likely to recur, contradicting lender expectations that internal and controllable factors should lead to learning and improvement (Kibler et al., 2017; Weiner, 2018). This contradicts the implicit assumption of lenders that internal and controllable factors will not lead to repeated failures (Harvey et al., 2014). If entrepreneurs claim to have learned from failure, stable attributions may undermine this perception (Eggers and Song, 2015; Ucbasaran et al., 2013), whereas unstable attributions reassure lenders that past mistakes will not be repeated, increasing confidence in future success. Such stable characteristics can also include individual-level traits such as emotion regulation, which represents a relatively persistent ability to manage affective responses (Fang He et al., 2018). Therefore, we hypothesise the following:

The moderating role of the crowd lender’s gender

Crowd lenders, gender and causality

Nearly three decades ago, research identified gender as a crucial determinant of investment behaviour (Bajtelsmit and Bernasek, 1997). This influence may be partly explained by psychological and cognitive differences between men and women, which shape financial decision-making (Vismara et al., 2016). These differences become particularly significant in failure situations, as failure acts as a substantial risk signal, and risk tolerance varies by gender (Hervé et al., 2019). Extensive research suggests that women are more risk-averse than men (Deo and Sundar, 2015; Holden and Tilahun, 2022; Marinelli et al., 2017). This risk aversion becomes even more pronounced in investment-based crowdfunding, such as equity and lending, where uncertainty is particularly high (Hervé et al., 2019; Mohammadi and Shafi, 2018). While women tend to be more optimistic overall (Holden and Tilahun, 2022), they exhibit a lower tolerance for uncertainty when making investment decisions (Deo and Sundar, 2015; Ren et al., 2025).

Recent research provides a more nuanced understanding of this gender difference in risk perceptions. Ren et al. (2025) demonstrate that women exhibit distinct patterns of brain activity that are associated with a stronger future-oriented and emotionally controlled approach to financial decision-making. As such, they may prefer external attributions of failure in entrepreneurs, as these suggest that setbacks were due to situational factors and may not influence the new venture creation. In contrast, men, who tend to be less risk-averse (Ren et al., 2025), may interpret internal attributions as a sign of accountability and responsibility, aligning with their preference for structured, performance-based evaluations (Huang and Kisgen, 2013). Although internal attributions can be emotionally disruptive, they can also enhance learning and future success (Shepherd et al., 2016), which men may view as a positive indicator of an entrepreneur’s resilience and potential.

Furthermore, depending on their own gender, lenders themselves bring personal experiences into their decision-making. On the one hand, prior research indicates that women themselves are more likely to attribute their own failures to internal factors, such as a lack of ability (Bandura, 1997; Rakowska and Rupert, 2024; Uebbing et al., 2025) and success to external factors, for example, luck, whereas men tend to do the opposite (Laguía et al., 2019; Ryckman and Peckham, 1987). Therefore, we believe that female crowd lenders are also aware of the potential consequences of this mindset. Conversly, female lenders themselves are more aware of potential external barriers and therefore do not perceive them as excuses, but rather as realistic factors that can cause failure. Hence, we hypothesise the following:

Crowd lenders, gender and controllability

Gender-based differences in emotional engagement and decision-making styles also shape investment decisions. Previous research indicates that women exhibit greater sympathy and relational considerations when evaluating investment opportunities (Eagly and Carli, 2003), while men tend to rely on more rational, non-emotional decision-making processes (Croson and Gneezy, 2009). As a result, women lenders may be particularly willing to support entrepreneurs who attribute failure to uncontrollable factors, perceiving them as victims of circumstance rather than fundamentally incompetent. In contrast, male lenders, prioritising rational assessment over emotional considerations, may prefer entrepreneurs who acknowledge personal responsibility for failure, which signals control and accountability. However, previous research has indicated that women entrepreneurs are generally more likely to attribute failure to controllable factors, for example, ‘I did not work hard enough’ or ‘I made the wrong decision’ (Barrett and Bliss-Moreau, 2009), whereas men tend to attribute failure to uncontrollable factors, such as market conditions, external forces.

While homophily suggests that lenders may be drawn to entrepreneurs with similar attribution styles (Butticè et al., 2023; Chen et al., 2023; Khurana and Lee, 2023; Wang and Prokop, 2025), heterophily in attributional reasoning may also shape investment decisions (Bellucci et al., 2025; Hao et al., 2024; Howell and Nanda, 2024). Lenders may prefer explanations of failure that challenge their attribution tendencies, offering alternative perspectives that appear more insightful or strategic (Martinko et al., 2007). Other reasons could be the demonstration of their legitimacy (Xu et al., 2024) or females evaluating females more critically than their male counterparts (Voitkane et al., 2019). Female lenders, who typically attribute failure to internal and controllable causes, may find uncontrollable attributions particularly compelling, as these provide a less self-critical perspective and align with structural explanations of failure. Conversely, male lenders, who tend to externalise their failure, viewing it as driven by uncontrollable circumstances, may perceive controllable attributions as a sign of accountability and resilience. Additionally, male crowd lenders may be less influenced by whether entrepreneurs see their failure as controllable. Therefore, we hypothesise the following:

Crowd lenders, gender and stability

Men and women utilise distinct information-processing strategies when making decisions (Thaler, 2021), influencing their investment behaviour (Mittal and Vyas, 2009). Research suggests that, because lenders have limited information about the business, they have to rely on behavioural heuristics (Tomlinson, 2020). Importantly, reliance on such heuristics is not uniform across individuals: men are more likely to adopt heuristic-based, simplified decision-making approaches, focusing on singular, salient cues to guide their choices (Meyers-Levy and Maheswaran, 1991). In contrast, women process information more comprehensively, integrating explicit and subtle cues (Graham et al., 2002). Additionally, women tend to allocate more time to decision-making and seek more detailed information before making financial choices (Jamil and Khan, 2016). This becomes evident in Khurana and Lee’s (2023) study, which concludes that although male lenders express positive evaluations of women entrepreneurs, they are ultimately less likely to reach a final deal with teams that include women. In contrast, female lenders do not display such a pattern. This suggests that male lenders tend to rely more heavily on a single evaluative cue, whereas female lenders may be less immediately convinced and instead seek additional information before making a final investment decision. Beyond cognitive processing differences, gender also influences confidence levels in investment behaviour. Male investors typically exhibit higher overconfidence, leading to more aggressive financial decision-making, whereas women investors tend to be more cautious and deliberate (Huang and Kisgen, 2013). These differences suggest that men may prefer stable causes of failure, as they offer predictability and align with heuristic-based decision-making, allowing for quick assessments of risk and return. In contrast, women’s preference for detailed evaluations and adaptability may lead them to favour unstable causes, as these allow for change, learning and future improvement. Thus, we posit the following:

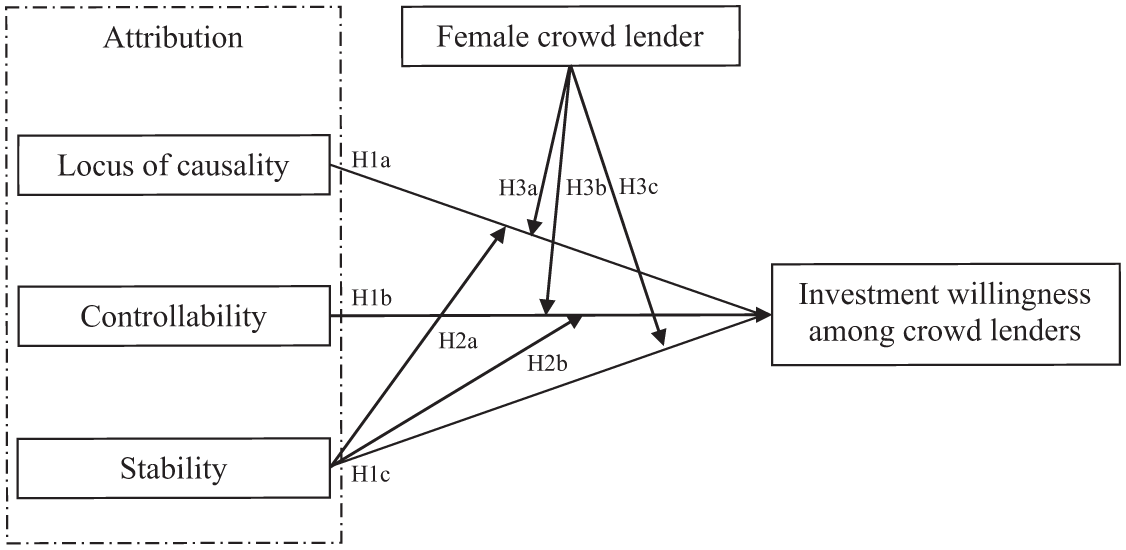

Figure 1 shows our conceptual model and all hypothesised relationships.

Conceptual model.

Method

Research design

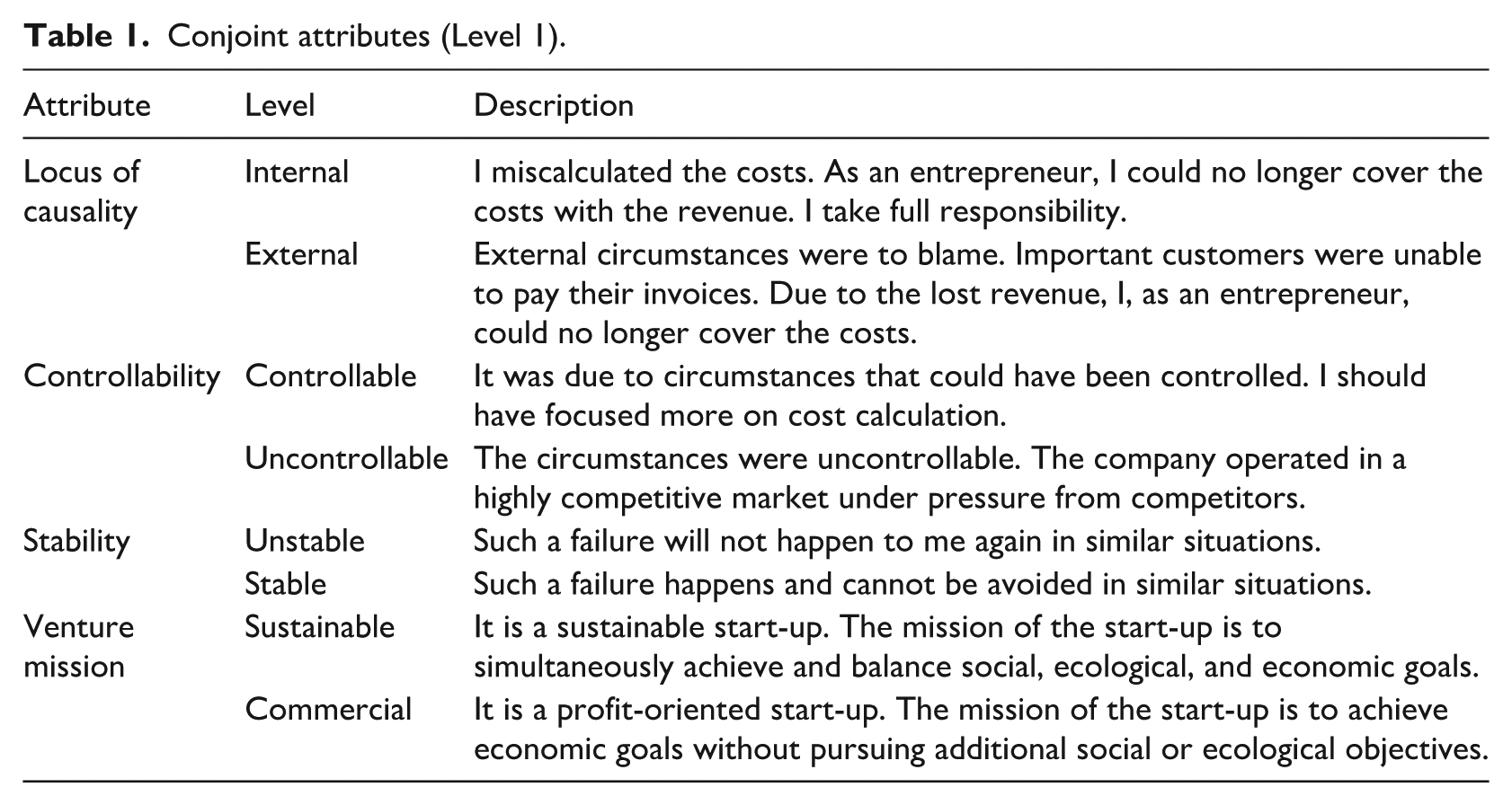

This study employs a metric-conjoint experiment to investigate how crowd lenders respond to failure attributions, precisely the dimensions of causality, controllability and stability. In metric-conjoint experiments, participants make a series of decisions regarding different investment options (Warnick et al., 2018). This within-subject approach is suitable for our study because it enables us to explore investment choices depending on different profiles (Lohrke et al., 2010). In this regard, a metric-conjoint experiment mirrors the real-world decision environment of crowd lenders, who must simultaneously consider multiple pieces of information when making investment decisions. Hence, it is particularly well suited to our study because it isolates the specific attributes of failure attributions, allowing us to assess how each dimension independently influences investment decisions. By systematically varying only the attribution-related factors while holding other contextual factors constant, we can draw more precise conclusions about which attributions of failure affect lender willingness to fund ventures. The profiles used in this study are based on consistent decision attributes but differ in the combination of values assigned to these attributes (Shepherd and Zacharakis, 2018). Moreover, this approach manipulates decision attributes while keeping contextual factors constant (Schüler et al., 2024). To test our hypotheses, participants made investment decisions regarding different start-up profiles. These profiles varied in terms of the three dimensions of attribution theory used to describe prior failure and the venture’s mission (i.e. sustainable vs. commercial). We considered the venture’s mission to account for potential differences in failure attributions, but it was not a central focus of our analysis.

At the beginning of the experiment, participants received general information about the study’s duration, procedure and data protection policies. Providing consent to the data protection agreement was a prerequisite for further participation. Participants were then asked to imagine that they had saved money, which they now intended to invest in start-ups via a crowdlending platform. Before presenting the various investment options, the principle of crowdlending was explained to the participants to ensure they understood the opportunities and risks associated with this financing model. They were also informed that all the options presented featured promising business ideas and plans, operating in industries with high market growth and profit margins. Furthermore, as they were in the crowdlending context, they were told that all start-ups promised a return of 7% over 6 years (Dinh and Wehner, 2022). Importantly, participants were informed that all entrepreneurs had previously started a failed business and had to cease operations. The introduction text of the study emphasised that the start-ups differed only in terms of their description of the previous failure and their venture mission. Participants were instructed to carefully read the investment profiles and assess the likelihood of investing in each start-up separately.

Participants were presented with an excerpt from a fictional start-up profile on a crowdlending platform for each investment option. These profiles clearly outlined the venture’s mission and included a question-and-answer section with the entrepreneurs regarding their previous failures (Zunino et al., 2022). Table 1 summarises the attributes and their descriptions. Appendix A shows an example of the Q&A format presented in the experiment. Responses from the entrepreneurs illustrated how they attributed the causes of their failure along the three dimensions of attribution theory. To prevent response biases due to the order of the investment profiles, their sequence was randomised for each participant (Schüler et al., 2024). Afterwards, participants answered additional demographic questions to capture control variables that could influence their decision-making.

Conjoint attributes (Level 1).

The investment options were presented based on four criteria, each with two different levels. This resulted in a full factorial design with 2⁴ = 16 possible profiles. Following the recommendations of prior research (Schüler et al., 2023; Warnick et al., 2018), a practice profile was included to help participants acclimate to the task. Additionally, all profiles were replicated to ensure the reliability and stability of response behaviour (Schüler et al., 2024; Shepherd and Zacharakis, 2018). Consequently, each participant made 33 decisions, with 32 being relevant for our analysis.

Implementation and manipulation checks

Several measures were implemented before and during the study to minimise potential biases in the research design and ensure high data quality (Podsakoff et al., 2012). First, to enhance the validity of failure attributions in the investment profiles, we developed them based on prior research (Küsshauer and Baum, 2020). Furthermore, using a question-and-answer format to present attributions is a common feature of crowdfunding platforms (Zunino et al., 2022) and may help participants immerse themselves in the investment scenario.

Before the main study, a pre-test was conducted with eight participants to evaluate the clarity of the experiment. Based on the feedback, adjustments were made to the study’s description of the context to better immerse participants in the investment scenario. The pre-test was also conducted to assess the study’s length (Karren and Barringer, 2002). Complex conjoint studies can lead to participant fatigue, declining motivation and inattentive responses (Aiman-Smith et al., 2002; Huang et al., 2012). Thirty-two investment decisions (+ one practice profile) per participant is considered appropriate in research (Schüler et al., 2024); this number was found to be manageable.

An attention-check item was also included in the questionnaire to identify inattentive respondents: ‘Please select “strongly agree”’ (Barber et al., 2013). Incorrect responses to this item led to the exclusion of the participant’s data during cleaning. A realism check was also conducted (Maute and Dubés, 1999). Using two items on a 7-point Likert scale, participants were asked to rate how realistic they perceived the described situation to be (1: not at all realistic to 7: very realistic) and how well they could imagine themselves in that situation (1: not at all to 7: very well). Furthermore, another item on a 7-point Likert scale assessed how thoroughly participants had read the investment options (1: not at all to 7: very thoroughly). The mean scores indicate that participants found the situation to be reasonably realistic (M = 4.67, SD = 1.31), were able to imagine themselves in it relatively well (M = 4.60, SD = 1.41), and read the investment options with a fair degree of attention (M = 5.03, SD = 0.98). These findings suggest that participants could relate the experimental decisions to real-life decisions, a critical criterion for conjoint experiments (Shepherd and Zacharakis, 2018).

Sample

The data were collected during a two-week period at the beginning of July 2024. A total of 84 German participants started the survey, whom we recruited through social media platforms, including LinkedIn, Instagram, Facebook and WhatsApp (i.e. a messenger app). The data cleaning process revealed that three participants failed the attention check. Additionally, a visual inspection of the data identified a response pattern in one participant’s answers. Moreover, only participants who were at least 18 years old and legally competent to invest in stocks and similar asset classes at the start of the study were included in the data analysis. Consequently, six participants were excluded. After excluding incomplete responses, 78 valid cases remained, resulting in a response rate of 92.9%. Our final sample consisted of 78 German participants, each of whom evaluated 32 investment profiles (following one practice profile), resulting in 2496 individual decisions (78 × 32). While the number of participants may appear modest compared to survey-based research, this sample size is in line with established standards in metric-conjoint analysis. According to a systematic review of conjoint studies in entrepreneurship, sample sizes of 50 or more are considered acceptable (Schüler et al., 2024). Thus, our study adheres to widely accepted methodological norms in this research domain.

Our sample included 50% women, resulting in a balanced gender distribution. The average age was 31.99 years (SD = 7.28), and participants reported an average of 9.23 years of work experience. Over half of the sample (55.13%) had prior nonprofessional investment experience, averaging 4.27 years. Five participants indicated that they had previously invested in crowdfunding projects, and 30.77% of the respondents reported having personal or professional relationships with individuals who had experienced entrepreneurial failure.

Measures

The dependent, independent and control variables were operationalised as follows.

Independent variables

The variables were manipulated across four attributes based on the dimensions of attribution theory and the venture’s mission. The failure attributions were adapted from validated descriptions developed by Küsshauer and Baum (2020). The dimension of causality is distinguished between internal explanations: ‘I miscalculated costs and take full responsibility’ and external explanations: ‘Key clients failed to pay their invoices’. Controllability refers to whether the failure was presented as controllable: ‘I could have better managed costs or, they were uncontrollable: ‘The venture faced strong market competition’. Stability is differentiated between unstable attributions: ‘This failure will not happen again’ and stable attributions: ‘This failure is unavoidable in similar situations’. Finally, the venture mission was described as either sustainable, emphasising ecological, social and economic or commercial goals, focusing exclusively on financial objectives.

Dependent variable

The willingness to invest was measured using a single-item scale. Participants rated their likelihood of investing in each start-up profile on a 7-point Likert scale, following established measures in prior research on investment decisions (Warnick et al., 2018).

Moderation variable

To identify patterns among women and men crowd lenders, we used the demographic variable of gender, which was coded with 1 for women and 0 for men.

Control variables

Several control variables were included to account for individual factors that might influence investment decisions. Investment experience was measured in years following previous research on investor behaviour in crowdfunding contexts (Penz et al., 2022). Willingness to take risks was measured with two items using a 7-point Likert scale, such as ‘Are you generally a risk-tolerant person?’, based on validated scales (Menkhoff and Sakha, 2016), with a Cronbach’s α of 0.81. Perspective taking, or the ability to adopt another person’s psychological viewpoint, was measured using four items adapted from Davis (1980), demonstrating strong internal consistency (Cronbach’s α = 0.87). One example item included the following: ‘Before criticising somebody, I try to imagine how I would feel if I were in their place’. Lastly, familiarity with entrepreneurial failure was measured dichotomously, asking whether participants had personal or professional relationships with someone who had experienced business failure (Kibler et al., 2017). Please see Appendix B for an overview of the relevant measures for the study.

Analytical approach

The data included 2496 observations, as each of the 78 participants evaluated 32 investment profiles and completed one practice profile (78 × 32). A multilevel modelling approach, specifically hierarchical linear modelling, was employed to analyse the data, accounting for the nested structure, in which multiple investment decisions (Level 1) are nested within participants (Level 2). This method estimates within-participant and between-participant effects while controlling for individual differences (Lohrke et al., 2010). Before the analysis, the data were cleaned to ensure consistency. Multicollinearity among the independent variables was examined using variance inflation factors (VIFs), all of which were well below the threshold of 2 (Cohen et al., 2002). Reliability was assessed using intra-class correlation coefficients (ICCs), which averaged 0.76 across replicated profiles, indicating stable responses (Schüler et al., 2024). The ICC represents the proportion of variance in the dependent variable attributable to the grouping structure of the data (Hox, 2002).

The analysis was conducted stepwise. First, a null model was estimated to verify whether there was a significant variance in investment likelihood across participants. Second, the independent variables were included as fixed effects at Level 1. Interaction terms were added to test the moderating effect of stability. Finally, control variables, including investment experience, risk tolerance, perspective taking, and familiarity with entrepreneurial failure, were added at Level 2. Cluster-robust standard errors were used to account for correlations between responses among participants. 1 Moreover, we conducted an additional analysis that incorporated the venture’s mission, which, although not the primary focus of our study, was considered a relevant attribute. To examine ventures mission potential influence, we conducted an additional analysis to test its effects and explore its moderating role in the relationship between the independent variables.

Results

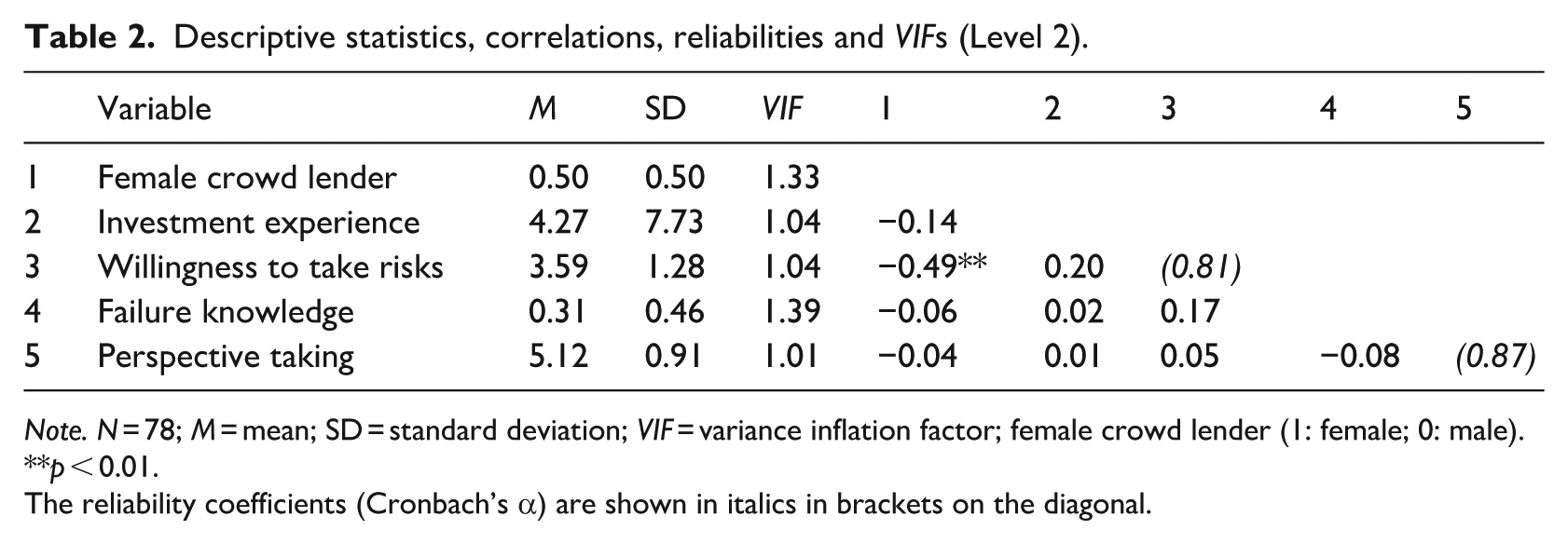

Table 2 presents the descriptive statistics, correlations, VIFs, and Cronbach’s α for the Level-2 variables. Due to the orthogonal study design, the correlations between Level-1 variables as well as their correlations with Level-2 variables are zero and, therefore, not reported.

Descriptive statistics, correlations, reliabilities and VIFs (Level 2).

Note. N = 78; M = mean; SD = standard deviation; VIF = variance inflation factor; female crowd lender (1: female; 0: male).

**p < 0.01.

The reliability coefficients (Cronbach’s α) are shown in italics in brackets on the diagonal.

Primary results

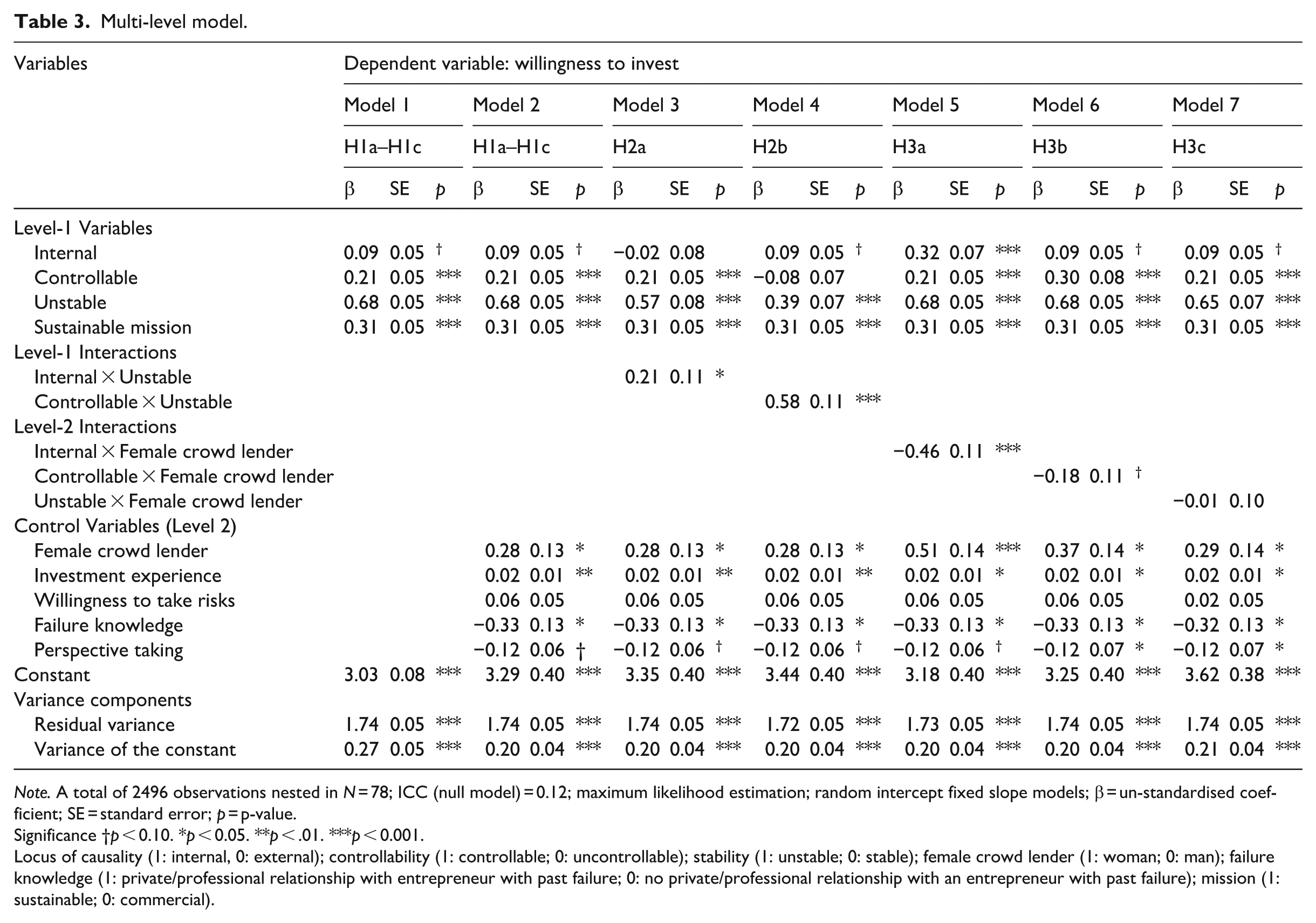

The multilevel analysis began with the specification of a null model (Aguinis et al., 2013), which included a random intercept for participants. An ICC of 0.12 indicates that individual differences among participants explain 12% of the variance in investment willingness. This finding justifies the use of multi-level analysis to model the relationships and test the hypotheses (Hayes, 2006). Building on the null model, Level-1 variables were added as fixed effects in Model 1. The multilevel models are summarised in Table 3. The χ2 test indicates that adding these variables significantly improves the explained variance of the dependent variable compared to the null model (χ2 = 210.03, p < 0.001). The marginal pseudo-R2 is 7.07%, demonstrating that the manipulated Level-1 variables contribute to explaining investment willingness.

Multi-level model.

Note. A total of 2496 observations nested in N = 78; ICC (null model) = 0.12; maximum likelihood estimation; random intercept fixed slope models; β = un-standardised coefficient; SE = standard error; p = p-value.

Significance †p < 0.10. * p < 0.05. **p < .01. ***p < 0.001.

Locus of causality (1: internal, 0: external); controllability (1: controllable; 0: uncontrollable); stability (1: unstable; 0: stable); female crowd lender (1: woman; 0: man); failure knowledge (1: private/professional relationship with entrepreneur with past failure; 0: no private/professional relationship with an entrepreneur with past failure); mission (1: sustainable; 0: commercial).

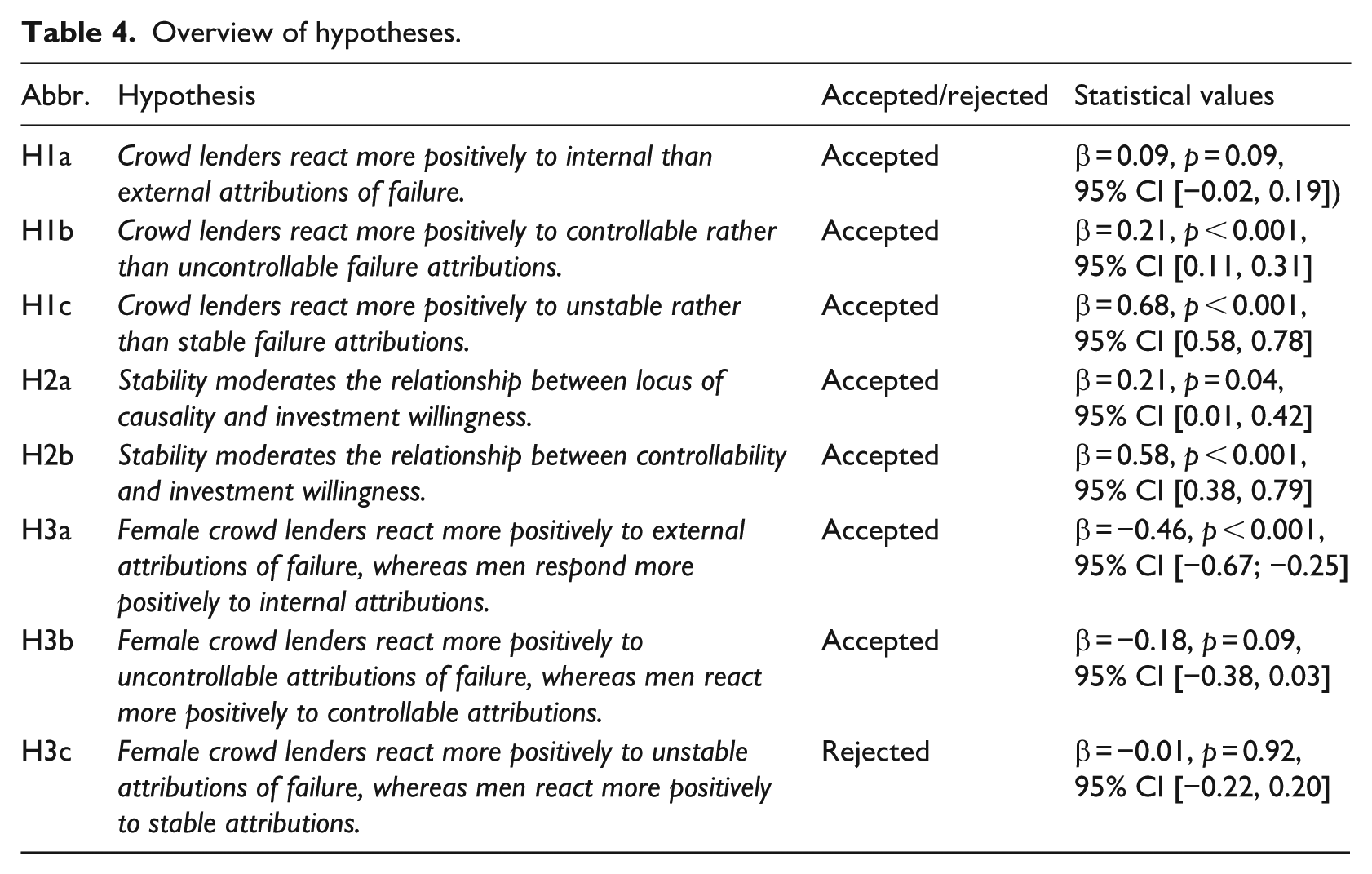

Models 1 and 2 test hypotheses H1a, H1b and H1c. The results show that internal attributions, compared to external ones, have a weakly significant positive effect on investment willingness (β = 0.09, p = 0.09, 95% CI [−0.02, 0.19]), confirming Hypothesis 1a. Furthermore, crowd lenders react more positively, indicated by their higher investment willingness, when entrepreneurs attribute failure to controllable rather than uncontrollable factors (β = 0.21, p < 0.001, 95% CI [0.11, 0.31]), confirming Hypothesis 1b. Hypothesis 1c is also supported, as attributing failure to unstable rather than stable factors has a significant positive effect (β = 0.68, p < 0.001, 95% CI [0.58, 0.78]).

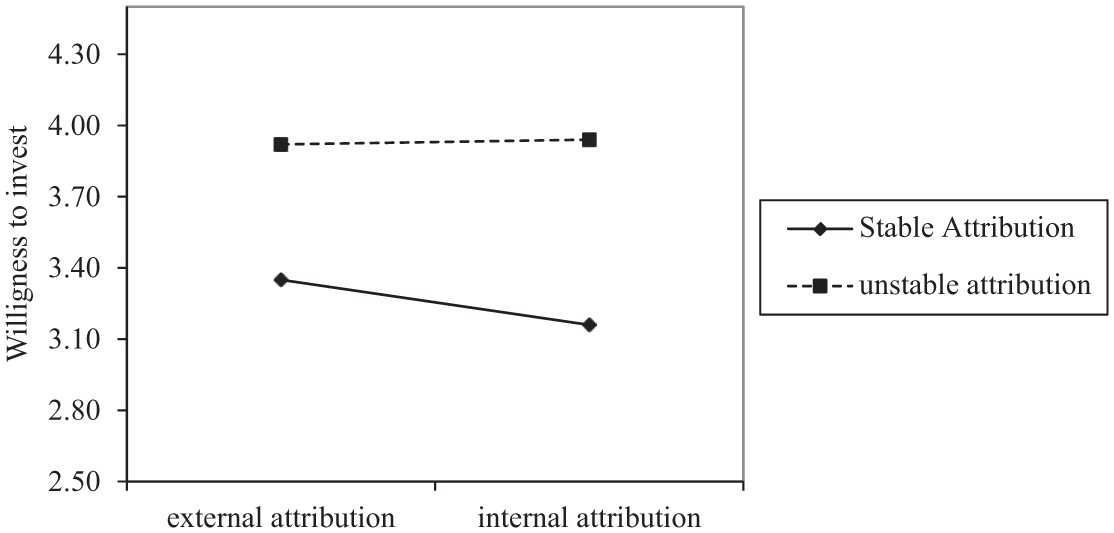

Five models were specified to test Hypotheses 2a, 2b, 3a, 3b, and 3c, building on Model 2 by including the relevant interaction terms. The interaction of Model 3 between causality and stability is significant and positive (β = 0.21, p = 0.04, 95% CI [0.01, 0.42]). The visual representation in Figure 2 illustrates that the relationship between causality and investment willingness is influenced by attribution stability; therefore, Hypothesis 2a is confirmed.

Moderation – locus of causality × stability.

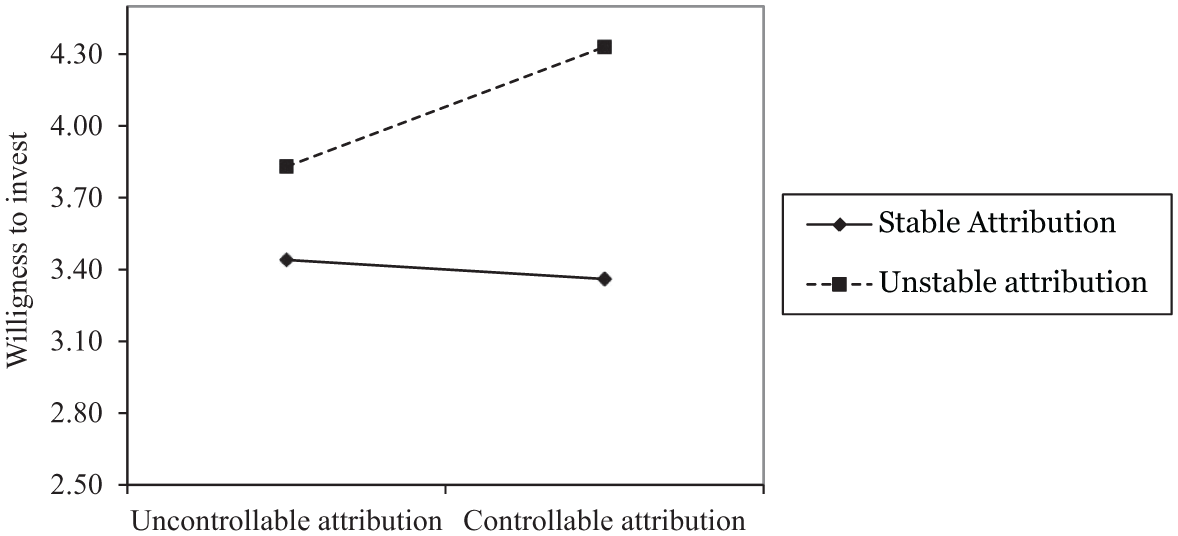

Model 4 tests Hypothesis 2b and reveals a significant positive interaction effect (β = 0.58, p < 0.001, 95% CI [0.38, 0.79]) between stability and controllability. Figure 3 shows that the relationship between controllability and investment willingness is more positive when failure is attributed to unstable rather than stable factors. An unstable attribution leads to a positive relationship, whereas a stable attribution reverses the effect to a negative relationship; thus, Hypothesis 2b is supported.

Moderation – controllability × stability.

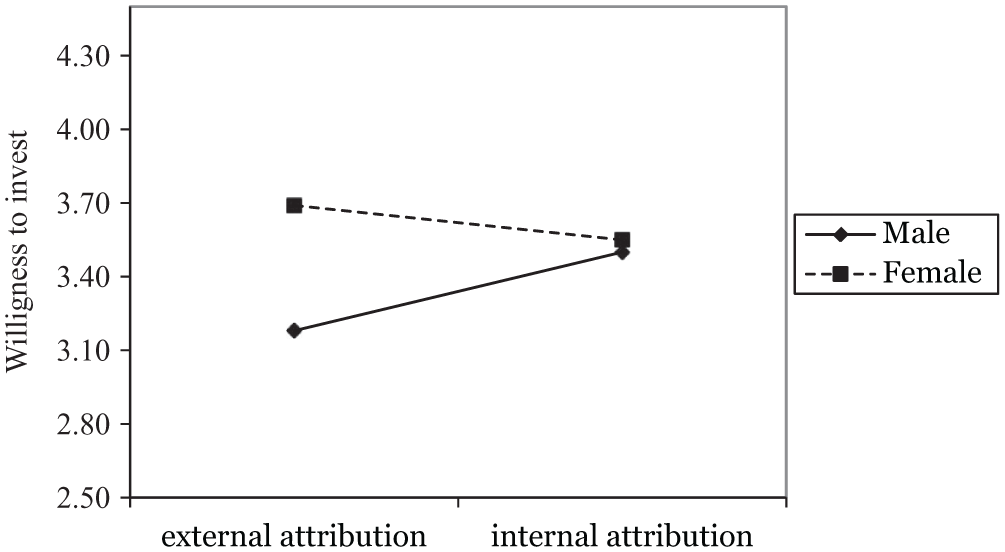

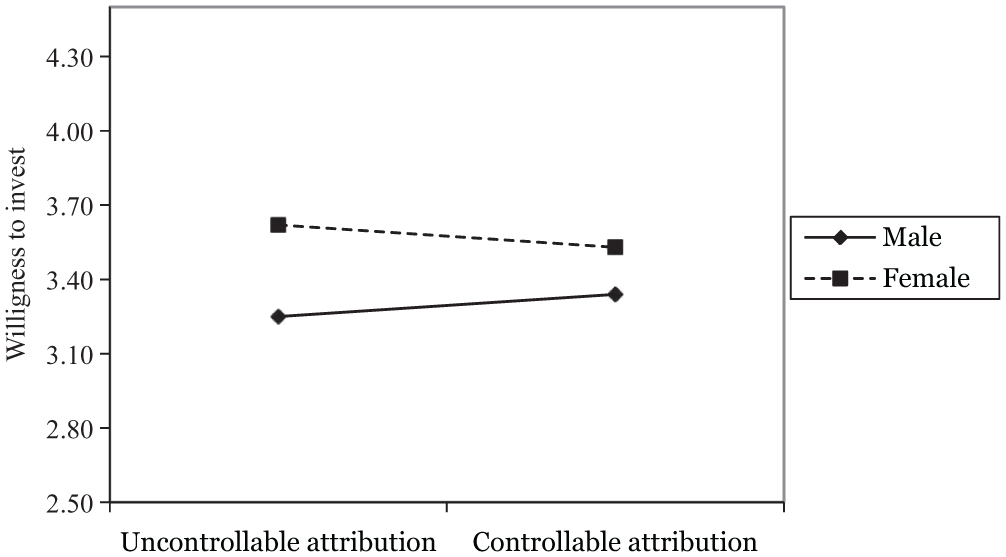

Models 5 to 7 test the moderation hypotheses regarding the gender of crowd lenders. Therefore, we interact with Level-1 and Level-2 variables, revealing significant results for the interaction between the gender of the crowd lender and attributions. The analysis showed a significant interaction between attribution type causality (internal vs. external) and lender gender (β = −0.46, p < 0.001, 95% CI [−0.67, −0.25]), supporting Hypothesis 3a. Specifically, women lenders evaluated internal attributions of failure less favourably than their male counterparts. The negative coefficient suggests that while internal attributions might generally increase willingness to invest, this effect is moderated by investor gender, with women lenders showing a more critical response (Figure 4). Regarding the attribution type controllability (controllable vs. uncontrollable), we find a weak yet significant effect (β = −0.18, p = 0.09, 95% CI [−0.38, 0.03]), which supports Hypothesis 3b (Figure 5). In contrast, no significant interaction was found between lender gender and stability (β = −0.01, p = 0.92, 95% CI [−0.22, 0.20]), leading to the rejection of H3c. Table 4 provides an overview of all hypotheses.

Moderation – locus of causality × female crowd lender.

Moderation – controllability × female crowd lender.

Overview of hypotheses.

Additional results

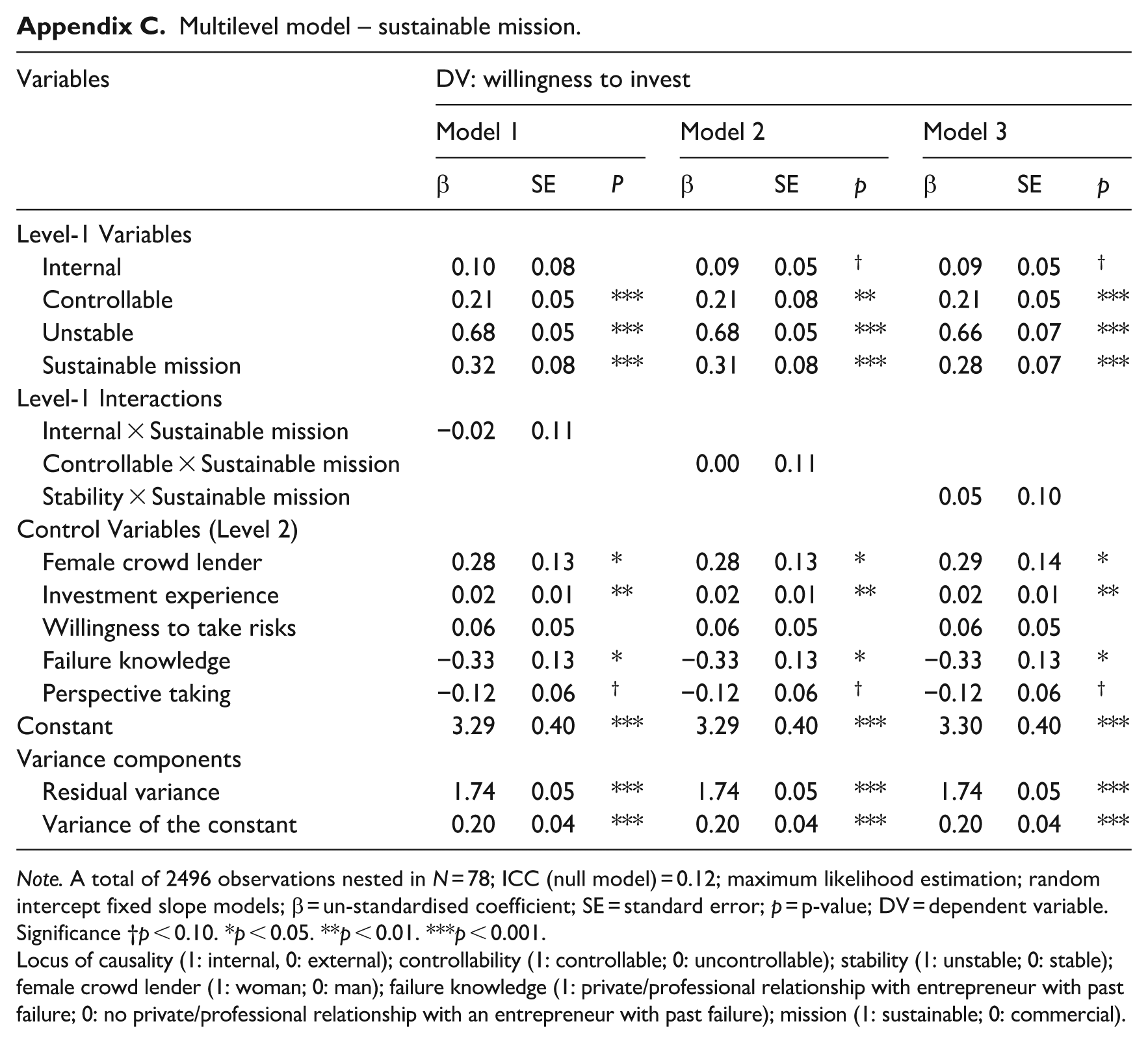

We conducted additional analyses on the attribution interactions, focusing on the venture mission and its moderating influence on the relationship between causality, controllability, stability and investment willingness. First, our results indicate a positive effect of a sustainable mission on investment willingness (β = 0.32, p < 0.001, 95% CI [0.21, 0.42]). Second, our moderating results concerning the attributions of failures and a sustainable mission show no significant interaction effects for either relationship (causality: β = −0.02, p = 0.87, 95% CI [−0.23, 0.19]; controllability: β = 0.00, p = 0.99, 95% CI [−0.21, 0.21]; stability: β = 0.05, p = 0.66, 95% CI [−0.16, 0.25]; see Appendix C).

Discussion

This study aimed to answer the following two research questions: How do crowd lenders react to distinct failure attributions of entrepreneurs? How does the gender of crowd lenders influence their reactions to an entrepreneur’s attribution of failure? Our results demonstrate that failure attributions significantly influence crowd lender decision-making and investment willingness. Specifically, attributions to internal rather than external factors, controllable rather than uncontrollable factors, and unstable rather than stable factors each have a positive effect on crowd lender investment willingness. Additionally, we found that attributions to internal or controllable factors are more positively associated with investment willingness when the causes are framed as unstable rather than stable. A positive relationship exists between internal or controllable attributions and investment willingness in cases where explanations are unstable, whereas the relationship becomes negative when causes are attributed to stable factors. By identifying boundary conditions, such as stability and the gender of the crowd lender, we were also able to highlight distinct patterns in failure attribution particularly relevant for women female crowd lenders, primarily reflecting their responses to external and uncontrollable failure attributions.

Third-party reactions to failure attributions

With this, our study advances the literature on entrepreneurial finance (Cope, 2011; Roccapriore et al., 2021; Souakri et al., 2023) and, more specifically, the crowdlending literature focusing on failure (Lindlar et al., 2025; Zunino et al., 2022), by shifting the analytical focus towards third-party reactions (Bai and Gao, 2023; Roccapriore et al., 2021; Souakri et al., 2023) and emphasising the relevance of failure attributions as an observable cue in early-stage funding decisions. Building on prior work that has established the ambivalent nature of failure perceptions among crowd lenders, we present the mechanisms through which responses to failure may elicit positive investor behaviour (Bai and Gao, 2023; McSweeney et al., 2025). Our findings show that attributional framing significantly influences lender willingness to invest, thereby extending existing evidence (Kibler et al., 2021; Roccapriore et al., 2021) that failure narratives can shape future resource acquisition. Specifically, our results reveal that crowd lenders favour internal over external attributions, thereby adding to the findings of Zunino et al. (2022), who highlight the importance of demonstrating learning competencies to positively influence investor reactions. We align with this view by showing that internal attributions are often interpreted as indicators of learning and accountability, which in turn enhance perceived credibility and positively affect investment intentions.

Our results also demonstrate that both internal and controllable attributions, signals of responsibility acceptance (Kibler et al., 2017; Tsiros et al., 2004), positively affect willingness to invest. This supports arguments in the literature that the denial of responsibility can lead to unfavourable evaluations of entrepreneurs (Cardon et al., 2011; Kibler et al., 2021). At the same time, our findings initially appear to contradict those of Kibler et al. (2017), which suggest that external and uncontrollable attributions may be strategically beneficial for preserving professional legitimacy. This apparent contradiction underscores the importance of attributional framing as a nuanced signal, particularly in the context of crowdlending, where investor interpretation may differ from traditional investor settings. Furthermore, the moderating effect of stability on the relationship between locus of causality or controllability and willingness to invest supports prior findings in both failure and attribution research (Homsma et al., 2007; Kibler et al., 2017). Specifically, the positive impact of internal or controllable attributions on investment intentions is amplified when these attributions are unstable, but it is attenuated, or even reversed, when they are stable. While internal and controllable causes are generally perceived as modifiable and thus, unstable (Harvey et al., 2014; Walsh and Cunningham, 2017; Yamakawa and Cardon, 2015), attributing failure to stable factors may signal persistent deficiencies, raising concerns about repeated failure and undermining lender confidence (Harvey et al., 2014; Hochberg et al., 2014; Zunino et al., 2022).

Gendered reactions to failure attributions

Our research contributes to the entrepreneurship literature on gender and investment behaviour (Bapna and Ganco, 2021; Harrison et al., 2020), which has shown that ‘gender differences stem from a complex combination of mechanisms’ (Koziol et al., 2025: 231). We identify failure attribution as one such mechanism that shapes lender evaluations of entrepreneurs. Specifically, our findings show that female lenders respond more positively when prior entrepreneurial failure is attributed to external factors, whereas male lenders react more favourably when the failure is attributed to internal factors.

This pattern can be understood through the lens of risk perception. External attributions frame the failure as the result of temporary, situational factors, such as adverse market conditions, rather than persistent weaknesses of the entrepreneur. For female lenders, who have been shown to exhibit lower risk tolerance, particularly in uncertain contexts like investment-based crowdfunding (Hervé et al., 2019; Mohammadi and Shafi, 2018), external attributions reduce the perceived downside risk of investing. In contrast, male lenders appear to interpret internal attributions, where entrepreneurs take responsibility for past failures, as a sign of accountability and learning (Shepherd et al., 2016). This signals to them that the entrepreneur has grown from the experience and is therefore, better equipped to succeed in the future. By identifying these gender-specific reactions, our study offers a more nuanced explanation for the well-documented finding that women lenders tend to be more risk-averse than their male counterparts (Deo and Sundar, 2015; Holden and Tilahun, 2022; Marinelli et al., 2017; Ren et al., 2025). More specifically, our results suggest that part of this difference may stem from women’s preference for external attributions, which present investment opportunities as less inherently risky. This insight extends existing research by highlighting how subtle framing cues, such as how failure is explained, can differentially influence the decisions of male and female lenders. Female lenders also responded more favourably to uncontrollable attributions of failure, while male lenders reacted more positively to controllable attributions. Although modest in size, this result adds nuance to prior evidence on gendered decision-making and attributional reasoning in entrepreneurial finance. Women’s preference for uncontrollable attributions aligns with research showing that they tend to engage more relationally and empathetically in decision-making (Eagly and Carli, 2003), sympathising with entrepreneurs who are portrayed as victims of circumstance rather than inherently flawed. In contrast, men’s preference for controllable attributions reflects a rational, performance-based perspective (Croson and Gneezy, 2009), where accountability and evidence of learning signal resilience and future success (Shepherd et al., 2016).

These results challenge traditional homophily explanations (Greenberg and Mollick, 2017), which predict alignment with one’s own attribution style (Butticè et al., 2023; Chen et al., 2023; Wang and Prokop, 2025). Instead, our findings point towards heterophily, suggesting that lenders may value perspectives that complement rather than mirror their own (Martinko et al., 2007) – aligning with more recent studies (Bellucci et al., 2025; Hao et al., 2024; Howell and Nanda, 2024; Xu et al., 2024). Female lenders, who often internalise controllable causes for failure (Barrett and Bliss-Moreau, 2009), may perceive uncontrollable attributions as offering a more balanced and less self-critical narrative. Conversely, male lenders, who tend to externalise their own failures, may interpret controllable attributions as a rare but credible signal of accountability and legitimacy. Instead, our findings align more closely with attribution theory, which suggests that failures attributed to uncontrollable causes elicit sympathy, while those attributed to controllable factors provoke frustration or blame (Graham, 1991). Given that women tend to exhibit higher levels of empathy and emotional engagement in investment decisions (Eagly and Carli, 2003), their preference for entrepreneurs who attribute failure to uncontrollable causes may stem from a greater propensity to perceive such individuals as victims of circumstance rather than as fundamentally incompetent. Contrary to our expectations, we found no significant interaction between the stability of failure attribution and lender gender, which suggests that, unlike causality and controllability, the stability dimension of attribution may be less influential in shaping the investment willingness of lenders in terms of gender moderation. One possible explanation is that stability cues are less salient for investors in the context of crowdlending, where decision-making often occurs with limited information (Tomlinson, 2020). Whereas women tend to process information more comprehensively (Graham et al., 2002) and men rely more on heuristic cues (Meyers-Levy and Maheswaran, 1991), these differences may not have been triggered strongly enough by the stability framing in our scenarios.

Theoretical implications

Overall, our findings contribute to attribution theory (Weiner, 1985) by extending its application into the domain of entrepreneurial finance, specifically within the context of crowdlending. More specifically, our findings demonstrate that the core dimensions of attribution in salient and influential high-uncertainty investment environments are characterised by minimal information and high heterogeneity among decision-makers. By showing that internal, unstable and controllable attributions elicit more favourable responses from crowd lenders, we offer empirical validation of attributional reasoning in a novel context where attributions serve as strategic signals. Building on this foundation, our study advances attribution theory in the following ways.

First, we extend attribution theory by shifting the focus from the actor’s self-explanations to third-party observers in financial decision-making contexts and by conceptualising attribution as a two-sided process (Geiger, 2024). Failure attribution by entrepreneurs acts as an investment signal that directly shapes crowd lender resource allocation decisions, thereby broadening the scope of attribution theory into entrepreneurial finance. Second, our findings illustrate the boundary role of stability. While locus of causality and controllability are generally associated with positive evaluations, we show that these effects hold only when causes are framed as unstable. Attributing failure to stable internal or controllable factors instead reduces investment willingness, as it signals enduring incompetence. This highlights the critical role of stability in high-risk decision contexts. Third, we reveal that attributional effects are not uniformly interpreted but are moderated by the gender of the observer, thereby contributing to a more nuanced understanding of attribution theory by integrating gender as a boundary condition. This nuanced extension underscores that attribution processes are shaped not only by the characteristics of the actor (entrepreneur) but also by the cognitive and demographic traits of the observer (lender), thereby expanding the scope of attribution theory in entrepreneurial decision-making contexts.

Practical implications

Beyond its theoretical contributions, this study provides several implications for entrepreneurs, investors, managers, policymakers and crowdlending platforms. Entrepreneurs seeking funding on crowdlending platforms should recognise that explanations of past failures serve as a critical investment signal. While internal, controllable, and unstable attributions generally increase investment willingness, this effect is not uniform across all lenders. Women lenders are more critical of internal attributions, whereas men lenders respond more favourably to them. Accordingly, entrepreneurs may consider tailoring their narratives to the likely composition of their potential lender base. For female audiences, entrepreneurs could emphasise uncontrollable external factors alongside resilience and learning; for male audiences, they could transparently acknowledge controllable shortcomings and corrective actions. However, such tailoring must remain authentic and consistent, as mismatches between words and actions may damage trust (Wang et al., 2022). Entrepreneurs should also present concrete evidence of post-failure learning, such as process improvements, team strengthening or strategic pivots, to reinforce the signal value of their attribution (Walsh and Cunningham, 2017).

For crowd lenders, understanding the systematic influence of attribution framing can enhance decision quality. Being aware of potential biases, such as discounting viable ventures based on attribution style, may help lenders avoid missed investment opportunities. Lenders could adopt structured decision-making approaches, including pre-defined evaluation criteria or checklists that weigh attribution content alongside other venture fundamentals, such as repayment capacity or sector trends. This can help mitigate overreliance on heuristic judgements triggered by attribution framing. Furthermore, recognising gender-related tendencies in one’s own judgements can reduce the risk of systematically favouring or disfavouring particular entrepreneur profiles.

At the organisational level, our findings suggest that attribution framing is not only relevant in external investor–entrepreneur interactions but also within founding teams and established organisations. Team members may interpret the same attribution of failure differently, depending on their cognitive and gender-related tendencies. By acknowledging these differences, teams can create an environment where diverse interpretations are openly discussed, thereby reducing the risk of biased judgements. Such awareness can ultimately strengthen organisational resilience by ensuring that failures are constructively analysed and that learning is shared across heterogeneous teams. Nevertheless, whether these differences in attribution processing translate into effects within organisational teams requires further empirical investigation.

For policymakers and platform designers, our results highlight that failure explanations matter. Therefore, platforms could introduce standardised sections for failure explanations, encourage transparent narratives of corrective actions or guide effective framing strategies. Platforms can leverage these insights to diversify their investor base, attract more female lenders and build trust by normalising diverse approaches to risk evaluation. At the policy level, recognising women’s strengths in financial decision-making supports initiatives that promote gender diversity in investment ecosystems and leadership positions, ultimately fostering more balanced and resilient funding environments.

Limitations and future research

Despite its important theoretical and practical contributions, this study has limitations that should be addressed in future research. First, we employed a conjoint experiment using hypothetical investment scenarios to isolate and test the effects of specific attributional cues on investment decisions. While this method enhances internal validity and allows for controlled hypothesis testing (Aiman-Smith et al., 2002; Huang et al., 2012), it does not fully replicate the complexity of real-world crowdlending decisions, where lenders typically have access to a broader set of information (Messeni Petruzzelli et al., 2019). Although prior research suggests that decisions in hypothetical scenarios often mirror those in actual contexts (Kühberger et al., 2002), future studies should aim to validate our findings, considering additional criteria relevant for lender decisions and using behavioural data from real crowdlending platforms to enhance external validity. Our experiment also assessed preferences for attributional frames, but did not measure the actual investment amounts participants would allocate. Investigating how attributional framing affects both investment likelihood and the financial volume of support would offer valuable insights (Khurana and Lee, 2023). Additionally, although a pre-test was conducted to refine the materials and ensure clarity, the small sample size (n = 8) limits the confidence with which we can generalise its outcomes, pointing to the need for more extensive pilot testing in future studies.

Second, we potentially face the limitation of the generalisability of our results due to using a German sample. Perceptions of failure as well as attitudes towards entrepreneurial failure and failed entrepreneurs may vary across regions and cultures (Cardon et al., 2011; Kuckertz et al., 2020; Lewis et al., 2010). Research using German samples is considered representative of Western countries with low entrepreneurial activity (Kuckertz et al., 2020) and serves as a reference point for crowdlending research in other European countries (Dinh and Wehner, 2022; Hörisch and Tenner, 2020). Nevertheless, integrating more diverse national and regional contexts into future research offers the potential to gain a more nuanced understanding of these relationships across cultures and regions. We also built upon previous research by focusing on participants with general prior investment experience (Dinh and Wehner, 2022; Penz et al., 2022). However, recent studies suggest behavioural differences exist among individuals with prior crowdfunding experience (Bapna and Ganco, 2021; Lindlar et al., 2025). Therefore, future research should validate our findings using a sample of experienced crowd lenders.

Third, our study focuses on crowdfunding, especially crowdlending. Prior research has shown that responses to entrepreneurial failure may vary depending on the financing context (Oo et al., 2025; Roccapriore et al., 2021; Souakri et al., 2023; Zunino et al., 2022). Hence, future studies could explore reactions to failure attributions in the context of other crowdfunding types or alternative financing options to build a comprehensive view of how entrepreneurs should communicate their prior failures to supporters.

Fourth, our study examined the role of a sustainable mission in failure attribution, but we found no significant differences between commercial and sustainable ventures. We encourage future research to explore this intersection further, as deeper factors may be at play. This is particularly relevant given that previous research identified differing reactions to failure in sustainable ventures compared to commercial ones (Hornuf et al., 2021; Lindlar et al., 2025).

Fifth, as one of few first studies to examine crowd lender preferences for failure attributions based on gender, our work opens several avenues for future research. For example, we did not find a significant effect for Hypothesis 3c, which proposed that women respond more positively to stable attributions. This suggests that stability may be less salient in our context. Future studies could replicate our design in different settings to test whether alternative contexts yield different results.

Conclusion

This article examined how crowd lenders react to distinct entrepreneurial failure attributions and how the gender of the lender shaped these reactions. In response to our research question, the results demonstrate that internal, controllable, and unstable attributions significantly increase willingness to invest. However, the effectiveness of these attribution types is shaped by key interactions among the attribution dimensions. Importantly, gender differences emerged: Women lenders were generally less receptive to internal and, to a lesser extent, controllable attributions. These findings illustrate the need to account for both the content of failure explanations and the observer characteristics when examining lender reactions in the context of failure. By applying attribution theory to the domain of crowdlending, our study shifts attention from the self-responses made by entrepreneurs to stakeholder evaluations, offering a new perspective on how failure narratives influence decisions.

Footnotes

Appendix

Multilevel model – sustainable mission.

| Variables | DV: willingness to invest | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Model 1 | Model 2 | Model 3 | |||||||

| β | SE | P | β | SE | p | β | SE | p | |

| Level-1 Variables | |||||||||

| Internal | 0.10 | 0.08 | 0.09 | 0.05 | † | 0.09 | 0.05 | † | |

| Controllable | 0.21 | 0.05 | *** | 0.21 | 0.08 | ** | 0.21 | 0.05 | *** |

| Unstable | 0.68 | 0.05 | *** | 0.68 | 0.05 | *** | 0.66 | 0.07 | *** |

| Sustainable mission | 0.32 | 0.08 | *** | 0.31 | 0.08 | *** | 0.28 | 0.07 | *** |

| Level-1 Interactions | |||||||||

| Internal × Sustainable mission | −0.02 | 0.11 | |||||||

| Controllable × Sustainable mission | 0.00 | 0.11 | |||||||

| Stability × Sustainable mission | 0.05 | 0.10 | |||||||

| Control Variables (Level 2) | |||||||||

| Female crowd lender | 0.28 | 0.13 | * | 0.28 | 0.13 | * | 0.29 | 0.14 | * |

| Investment experience | 0.02 | 0.01 | ** | 0.02 | 0.01 | ** | 0.02 | 0.01 | ** |

| Willingness to take risks | 0.06 | 0.05 | 0.06 | 0.05 | 0.06 | 0.05 | |||

| Failure knowledge | −0.33 | 0.13 | * | −0.33 | 0.13 | * | −0.33 | 0.13 | * |

| Perspective taking | −0.12 | 0.06 | † | −0.12 | 0.06 | † | −0.12 | 0.06 | † |

| Constant | 3.29 | 0.40 | *** | 3.29 | 0.40 | *** | 3.30 | 0.40 | *** |

| Variance components | |||||||||

| Residual variance | 1.74 | 0.05 | *** | 1.74 | 0.05 | *** | 1.74 | 0.05 | *** |

| Variance of the constant | 0.20 | 0.04 | *** | 0.20 | 0.04 | *** | 0.20 | 0.04 | *** |

Note. A total of 2496 observations nested in N = 78; ICC (null model) = 0.12; maximum likelihood estimation; random intercept fixed slope models; β = un-standardised coefficient; SE = standard error; p = p-value; DV = dependent variable.

Significance †p < 0.10.

p < 0.05. **p < 0.01. ***p < 0.001.

Locus of causality (1: internal, 0: external); controllability (1: controllable; 0: uncontrollable); stability (1: unstable; 0: stable); female crowd lender (1: woman; 0: man); failure knowledge (1: private/professional relationship with entrepreneur with past failure; 0: no private/professional relationship with an entrepreneur with past failure); mission (1: sustainable; 0: commercial).

‘Declaration of Generative AI and AI-assisted technologies in the writing process’.

During the preparation of this work, the author(s) used ChatGPT in order to improve readability and language. After using this tool/service, the author(s) reviewed and edited the content as needed and take(s) full responsibility for the content of the publication.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: We are grateful for the financial support provided by the scholarship award of the Manchot Graduate School at the Heinrich Heine University Düsseldorf (Germany).

Data availability statement

The data is available upon request.