Abstract

Selling the family firm to financial investors is a financially attractive exit option for family firm owners, especially those lacking a capable and willing family-internal successor. Building on the socio-emotional wealth (SEW) perspective, we investigate the factors that affect a family firm owner’s preference to sell to an activist private equity investor focused on financial goal maximisation, versus a steward private equity investor focused on upholding family firm values and business stability. We also study the potential moderating effect of portfolio ownership as the literature suggests that exit decisions and SEW considerations depend on family firm portfolio status. Based on our vignette scenario study with 200 responses from family firm owner-managers, we find that greater importance of non-financial considerations, such as family prominence and strong firm financial performance, reduces the preference to sell to an activist private equity investor compared to a steward private equity investor. Moreover, we show that portfolio ownership weakens the proposed positive relationship between an innovation focus and the preference to sell to an activist versus a steward private equity investor. Our findings have consequences for both family firm succession research and SEW research.

Introduction

Selling the family firm is an increasingly important topic in studies of succession (DeTienne and Chirico, 2013; Widz and Kammerlander, 2022). In particular, there is growing interest in studying family firms – those with a majority of shareholders belonging to one family (Croce and Martí, 2016) – in which the owning family exits by selling their shares to a financial investor due to the absence of a suitable internal succession candidate (Schickinger et al., 2018). Studying this phenomenon has practical relevance given its salience, as well as theoretical relevance because such sales can mark the end of family involvement in the business (DeTienne, 2010). Investors can resolve succession-related issues and provide attractive financial opportunities to the owning family and their firm through an attractive purchase price, hence benefitting the family and invest in the firm post-acquisition and so benefitting the firm. There is, however, a potential goal conflict between family firms and financial investors (Schickinger et al., 2018); this arises from the tension between the goal of upholding family firm values and maintaining longstanding business practices and culture in former family firms, and that of profit maximisation for the owning family. While empirical evidence suggests a growing trend among family firms to engage in exit strategies involving financial investors, 1 financial investors are clearly not homogeneous (Tao-Schuchardt et al., 2022). Conceptual work by DeTienne and Chirico (2013) differentiated between two types of financial investors. The first are generally more intrusive into the family firm, affecting business models and ways of working as they aim to quickly generate high returns. Typically, such investors offer higher premiums and are known as activist private equity investors (APEIs; Schickinger et al., 2018). The other type of investor offers more opportunities for continued family involvement and firm stability as a quasi-family firm where the values, culture and business practices are preserved, but such investors generally offer lower prices per share; these are described as steward private equity investors (SPEIs) (DeTienne and Chirico, 2013). SPEIs typically offer a lower price per share than APEIs given their less intrusive approach towards the acquired firms as they rely less on debt and restructuring intentions and, thus, generate lower returns (DeTienne and Chirico, 2013; Tao-Schuchardt et al., 2022). The choice between these options might involve a trade-off for exiting family firm owners as they are confronted with the dilemma of maximising their own financial payout versus safeguarding family business stability (DeTienne and Chirico, 2013; Tao-Schuchardt et al., 2022). However, the family firm-related drivers that affect how family firm owners resolve this dilemma are still largely unknown.

Research on succession has generated important knowledge on which exit options exist for family firms (DeTienne and Chirico, 2013). Moreover, prior research illustrates that in addition to financial considerations, non-financial considerations such as the desire to maintain socio-emotional wealth (SEW) 2 not only influence day-to-day family firm decisions (Berrone et al., 2012; Gómez-Mejía et al., 2007), but also extend to the family firm owner’s exit route preferences (Akhter et al., 2016; Palm et al., 2024). However, research on exit routes has not yet fully embraced contemporary advancements in SEW research, including the distinction between extended and restricted SEW (Miller and Le Breton-Miller, 2014). Thus, we still lack a theoretical and empirical understanding of how considerations relating to financial aspects and to extended and restricted SEW jointly influence how family firm owners resolve the dilemma of choosing a specific type of financial investor. The extant evidence (Debicki et al., 2016; Slavec et al., 2017), indicates the importance of family prominence - that is, the family’s reputation within the community - referred to as restricted SEW, and the innovation focus of the family firm owner - referred to as extended SEW – as non-financial drivers. The performance of the family firm is also a potential financial driver influencing how the owners might address the aforementioned exit dilemma (DeTienne and Chirico, 2013; Gómez-Mejía et al., 2011; Symeonidou et al., 2022). Furthermore, extant research also indicates that family firm exits can depend on structural aspects such as whether the firm is a sole family firm or part of a portfolio (Akhter et al., 2016; DeTienne, 2010; DeTienne and Chirico, 2013). It is assumed that in the absence of a portfolio, all financial and non-financial considerations are concentrated in a single firm. This, in turn, leads to the complete loss of SEW if the firm is sold, whereas divesting one firm in a portfolio might have a smaller impact on both non-financial and financial considerations (Palm et al., 2023; Sieger et al., 2011). Thus, we explore the following research questions:

1. How do non-financial considerations related to restricted and extended SEW (family prominence and innovation focus) and financial considerations (financial performance) affect the family firm owner-manager’s preference to exit via an APEI versus an SPEI where there is no suitable internal successor?

2. How do these relationships depend on the family firm’s structure in terms of whether it is part of a portfolio?

We anchor our research in the family firm succession literature (Chirico et al., 2020) as well as that upon SEW (Berrone et al., 2012). We used a vignette scenario study design (Aguinis and Bradley, 2014; Mathias and Williams, 2017) to empirically test our hypotheses. Specifically, we presented family firm owners with an exit scenario in which they had to sell their business when they retired due to a lack of an internal successor asking if they would choose to sell all of the family’s shares to either an SPEI or an APEI. Our findings support our hypotheses that family prominence and financial performance decreased the family firm owner’s preference to sell to an APEI. However, we could not detect any significant effect of the family firm owner’s innovation focus on their exit preference. Yet, in line with our theorising, we find that the existence of a family firm portfolio has a significant moderating effect on the relationship between the family firm owner’s innovation focus and their propensity to sell to an APEI versus an SPEI.

Our study contributes to the external succession literature on family firms (Chirico et al., 2020), particularly the sub-stream focusing on financial investors (Ahlers et al., 2018), and to the literature on SEW (Berrone et al., 2012). The extant family firm succession literature has, so far, largely focused on the determinants of family-internal succession whereas we focus on family-external succession. We contribute to such work by researching a family firm owner’s preference to sell to a certain type of investor, thereby acknowledging that in practice, an increasing share of family businesses are being sold to financial investors (Invest Europe, 2021). Our research advances knowledge regarding the relationship between family firms and private equity investors by shifting the focus from the buyer’s perspective explored, for instance, by Kammerlander et al. (2024) and Tao-Schuchardt et al. (2022) to that of the family firm seller’s perspective, shedding light on their preferences and the drivers of external succession decisions. We draw attention to the heterogeneity of financial investors and the important implications of this for future research on external succession in family firms. From a theoretical stance, we also advance the SEW perspective by analysing how both restricted and extended SEW (Miller and Le Breton-Miller, 2014) influence exit route preferences and how these relationships depend upon structural aspects of family firms. Our empirical results reveal that restricted SEW significantly affects exit route preferences regardless of the structure of the family firm. However, our results also illustrate that extended SEW considerations are only statistically relevant when considering the structure of the family firm. Specifically, while extended SEW does not have a major role when the family firm is part of a portfolio, it does so when exiting a sole family firm.

In the following sections, we first provide an overview of existing literature on family-external succession and current knowledge regarding investors who purchase family firms. Subsequently, we develop a set of three main hypotheses and three moderating hypotheses, building on arguments from the SEW perspective. We then explain our research design and the analyses performed followed by our results along with additional tests. In the following discussion section, we briefly summarise our results and discuss contributions to research and practice. We then outline limitations and directions for future research and finally, conclude.

Theoretical background

For families who own and manage businesses, the absence of a family-internal successor is critical given that exiting the firm commonly signifies the end of their involvement with the firm (DeTienne, 2010; DeTienne and Wennberg, 2016). There are several exit routes that can be pursued in such a scenario (Chirico et al., 2020), such as liquidation, management buy-in/-out, an initial public offering, or a trade sale (Chirico et al., 2020; DeTienne, 2010). The dominant purchasers of privately held firms, of which many are family-owned (Berrone et al., 2012), are financial investors (Ahlers et al., 2018; Ljungqvist, 2024). Research focusing on the perspective of firm buyers (Kammerlander et al., 2024; Kurta and Kammerlander, 2022; Tao-Schuchardt et al., 2022) has noted that family firms are generally attractive investment targets; thus, using financial investors as an exit strategy has gained increased attention in the scholarly literature on family firms (Schickinger et al., 2018) for two key reasons. First, exiting through selling to financial investors is deemed an attractive option for sellers, as it allows for the firm’s continuation and offers a financial reward to the family (Achleitner et al., 2010). Second, the goals of family firm owners and investors often diverge, and family firm owners may, therefore, be concerned about the firm losing its values and shared identity (Marti et al., 2013; Neckebrouck et al., 2017). One root cause for such divergence is the financial investor’s goal to ultimately divest the acquired firm for a profitable return after a short investment period (Schickinger et al., 2018). This particular strategy encourages private equity investors to focus mainly on majority takeovers (Dawson and Barrédy, 2018) giving them operating and decision making control in the acquired firm.

To date, most studies have examined sales to financial investors as a homogeneous exit route without distinguishing between investor types (Gompers et al., 2020; Hernandez, 2012). However, not all financial investors are similar (Molly et al., 2018); there are two archetypes of financial investors relevant for family firm exits: those that adopt an activist approach and those that take a stewardship approach. An APEI aims to maximise financial returns by introducing measures that are likely to differ from the family firm’s current business model, business practices and overall values 3 (Acharya et al., 2013; Marti et al., 2013); this optimises their returns upon the future sale of the firm. APEIs also enhance a family firm’s financial evaluation by taking seats on the board and providing strategic advice (Bruining et al., 2013). This active, more intrusive approach typically allows the investor to offer a higher purchase price to the family firm owner. Although SPEIs 4 also aim to achieve high levels of financial return (Haslem, 2013; Manigart and Wright, 2013; Wong, 2010), they draw more upon stewardship-based strategies, such as aligning their approach with family firm values, focusing on longevity and taking account of stakeholder needs (DeTienne and Chirico, 2013). Consequently, SPEIs are unlikely to offer comparable purchase prices to those of APEIs given their lower financial value-enhancing activities during the intended holding period (Hernandez, 2012; McNulty and Nordberg, 2016).

From a family firm owner’s perspective, choosing a financial investor might pose a dilemma. On the one hand, family firm owners can follow economic principles aiming to maximise their financial reward when selling their life’s work. On the other hand, they may prioritise maintaining at least some elements of their SEW (Berrone et al., 2012) and protecting embedded values (Zellweger et al., 2012). The SEW perspective encompasses several different dimensions (Berrone et al., 2012), including the desire for transgenerational succession (Berrone et al., 2012; Zellweger et al., 2012); identification with the firm, for example, by using the family name in the firm name (Berrone et al., 2010; Kammerlander et al., 2015) and social status enhancement through association with the firm (Deephouse and Jaskiewicz, 2013; Miller and Le Breton-Miller, 2014). These dimensions comprise of non-financial considerations that owners derive from the family firm. Although selling a family firm to an external investor leads to the potential loss of accumulated SEW, Kammerlander (2016) argues that family firm owners still care about the future of the firm after their exit because of the above-mentioned non-financial considerations. The prioritisation of non-financial considerations over financial considerations has been confirmed in many family firm contexts, including nepotism or reluctance to accept external capital injection (Martin et al., 2019), or the acceptance of lower financial returns (Gómez-Mejía et al., 2007, 2022). Preserving SEW often comes at a cost for family firms when strategic and financial decisions are primarily driven by a non-economic rationale (Zellweger et al., 2012) that prioritises the needs of the family above those of the firm (Kellermanns et al., 2012). Researchers have begun to differentiate between restricted SEW – referring to non-financial goals focusing on family benefits – and extended SEW – referring to non-financial goals going beyond family benefits to consider other stakeholders (Li and Daspit, 2016; Miller and Le Breton-Miller, 2014). Restricted SEW focuses on the immediate non-financial benefits for the nuclear family such as job security for family members, or the current reputation of the family. Extended SEW, in contrast, refers to long-term benefits for the family, the firm and its stakeholders (Li and Daspit, 2016; Miller and Le Breton-Miller, 2014).

As noted below, when exiting the family firm by selling to a financial investor, owners are often confronted with the dilemma of either choosing a deal that maximises their financial returns at the cost of harming their SEW when selling to an APEI, or forgoing some returns to minimise the loss of SEW endowments when selling to an SPEI. In the next section, we will discuss important considerations that affect exit preferences.

Hypotheses development

We now hypothesise, based on the SEW literature, how two important non-financial considerations, that is, family prominence and innovation focus, and one important financial consideration, that is, firm performance, affect a family firm owner’s propensity to sell their firm to an APEI versus an SPEI. We also propose that the firm’s structure, that is, the presence or absence of a family firm portfolio, has a moderating effect on the exit preference.

Family prominence and investor type preference

The SEW perspective proposes that non-financial considerations divert the focus of family firm owners away from financial returns (Cennamo et al., 2012). So, for example, some family firms have a key role as local stakeholders; they tend to be deeply embedded in the local community and value the family’s reputation within the community (Reay et al., 2015). Furthermore, some family firm owners place a high value on being perceived as responsible people (Cruz et al., 2014) who care about stakeholder interests (Cennamo et al., 2012). While part of this behaviour is value-driven, it is also motivated by reputation protection and visibility within the community. We argue that an owner’s family prominence, defined as: ‘the importance of the family’s image and reputation associated with the firm’ (Chrisman et al., 2024: 706), will reduce their propensity to sell the firm shares to an APEI versus an SPEI. APEIs are often perceived as profit-driven and ruthless in their transformation activities with strategies involving cost-cutting, redundancies, reduction of financial support for local initiatives or other actions detrimental to the local community or stakeholders (Achleitner et al., 2010; Olsson and Tåg, 2017). Hence, choosing an APEI might contradict or indeed, damage family firm values and reputation in the community. Moreover, family firm owners might anticipate changes or damage to aspects of the business to which they are emotionally attached (König et al., 2013), such as established routines, products or cultural aspects. An SPEI, conversely, is more likely to maintain the status quo and act according to the family firm’s existing values. They are more likely to support responsible business practices and long-term community relationships that align with firm values and the community’s perception of the family as responsible business owners (Vincent et al., 2018).

We hypothesise that when owners exit their family firms and face competing investor offers, prioritising family prominence reduces the attractiveness of an APEI offer relative to an SPEI. Family firm owners who emphasise the importance of non-financial considerations, such as family prominence, are more likely to be reluctant to exit their firm through selling to an APEI, reflecting prior research on SEW (Berrone et al., 2012). Conversely, focusing on non-financial goals aligns with the typical SPEI’s intentions and shifts the dilemma towards accepting a lower financial pay-off in order to preserve SEW. Thus, our first hypothesis is as follows:

Hypothesis 1: Higher importance afforded to family prominence is negatively related to the propensity to sell the family firm to an APEI versus an SPEI.

Innovation focus and investor type preference

Family prominence is a non-financial consideration that primarily focuses on the family itself, and specifically its emotions and values and how the family is perceived within the community. While family prominence is, thus, a facet of restricted SEW, we next examine innovation focus as representation of a family firm owner’s extended SEW.

A family firm owner’s innovation focus refers to their willingness to enable a firm culture that fosters innovative, long-term projects (Gal, 2019; Naranjo-Valencia et al., 2016). Innovation focus typically comes along with a high degree of openness to new, or changed, situations (Glińska-Neweś et al., 2017) and the frequent incorporation of innovative solutions (Tsai and Yang, 2013). Reflecting extant research (Makó et al., 2018; Martínez-Alonso et al., 2018), we argue that family firm owners with a high degree of innovation focus are more likely to follow an extended SEW approach as innovation supports long-term value creation and fosters mutual benefits for the firm and its stakeholders. Not only do family firm owners with an extended SEW focus consider the exit consequences for the nuclear family, but they also the potential benefits for other stakeholders, such as employees, customers and suppliers (Kellermanns et al., 2012; Miller and Le Breton-Miller, 2014).Family firm owners who exhibit a high degree of innovation focus generally value transparency and business expansion by creating innovative goods, services or business methods (Slavec et al., 2017; Xia et al., 2023). These values and activities are typically ascribed to APEIs, which have been found to spur innovation in acquired firms (Amess et al., 2016). Specifically, APEIs are known to provide former family firms with directions, ideas and management styles that foster innovation (Achleitner et al., 2010; Gómez-Mejía et al., 2014). They also enable and accelerate innovation activities by providing the necessary funds and skills (Link et al., 2014). Innovative firms appear to be more attractive to employees (Futurestep, 2013) with professionalised structures that allow career progression through performance evaluations (Bish, 2021; Jia-Jun and Hua-Ming, 2022).

As noted, APEIs, in contrast to SPEIs, have been found to impose major changes in acquired family firms that create more challenging working environments (Ashwini and Prasanna, 2016). They also focus on reducing operational inefficiencies and increasing productivity and profitability (Croce and Martí, 2016; Davis et al., 2014), thereby contributing to an overall more effective and efficient business, which might also benefit stakeholders for instance through more generous annual bonuses. Innovative solutions are also beneficial for the suppliers and customers of former family firms, as well as for the community as a whole (Basco, 2015) and, thus, align well with the extended SEW approach. As such, we theorise that a high degree of innovation focus would lead family firm owners to prefer selling to an APEI who are more likely to introduce changes to benefit the firm and its stakeholders over time. Family firm owners with fewer extended SEW concerns and a lower innovation focus, however, might prefer the preservation of the status quo (Makó et al., 2018), associated with the SPEI approach. Thus, we hypothesise:

Hypothesis 2: A higher innovation focus by family firm owners is positively related to the propensity to sell the family firm to an APEI versus an SPEI.

Family firm performance and investor type preference

Next, we theorise that, due to both SEW and financial considerations, financial performance would reduce the family firm owner’s preference to sell to an APEI versus an SPEI, highlighting an interplay between financial and non-financial considerations. 5 Better financial performance by the family firm generates additional monetary resources for the owners they can subsequently use to build further SEW endowments. For instance, they can invest the financial resources created through firm profitability into new production plants, employee-related welfare programmes or events targeted at community and family members. This can increase both restricted and extended SEW (Miller and Le-Breton-Miller, 2014); it directly benefits the family by enhancing its reputation and also fosters long-term value creation and supports the community. Therefore, better financial performance by the family firm is related to higher levels of SEW endowments. In contrast, family firms facing financial constraints often struggle to pursue SEW-enhancing activities as survival takes precedence over long-term socio-emotional goals. In line with this reasoning, prior research has also argued that better family firm performance increases a family member’s identification with the firm (Cabrera-Suárez et al., 2014). While SPEIs are known for maintaining the status quo within acquired businesses, APEIs typically take a disruptive restructuring approach (Dawson and Barrédy, 2018; Schickinger et al., 2018) regardless of profitability that is likely to negatively affect firm culture and diminishes SEW endowments. As such, owners of family firms exhibiting strong financial performance have much to lose when selling to an APEI, including their identification with the firm, their emotional attachment to certain products or routines and their reputation. This arises as investors commonly engage in margin-optimising cost-cutting measures (Davis et al., 2014; Marti et al., 2003), in conflict to the sustainable value creation approach typically found in family firms with strong financial performance (Flammer and Bansal, 2017). SPEIs, however, are likely to take a more cautious approach, maintaining many of the assets that the family has accrued during its tenure and so also maintaining a positive association with the former owners.

A strong performance profile typically evokes a high level of identification with the firm (Cabrera-Suárez et al., 2014) and low level of internal family conflict. In such cases, family members have also typically been able to accumulate substantial personal wealth, for example, through consistent dividend payments (Isakov and Weisskopf, 2015). Such financial advantages enable family firm owners to base their selling decisions less on financial considerations. As SPEIs typically maintain an acquired family firm’s values, culture and business practices, it is more likely that owners of family firms with strong financial performance would prefer such investors given their priority on non-financial considerations, and a desire to leave the business in good hands (Kammerlander, 2016). Such a pattern might not necessarily be evident for owners of family firms with poorer financial performance; they might prefer a path that yields higher monetary returns upon exit by selling to an APEI, even if they had focused on SEW preservation during their ownership tenure. This would especially be the case if the owners needed cash resources to finance their lifestyle after exit; thus, selling to an APEI might seem an attractive choice to enhance economic well-being (Bacon et al., 2013). Family firm owners in challenging financial situations might, therefore, prioritise short-term financial gains making an APEI’s offer more appealing. Furthermore, APEIs often have superior access to substantial financial resources, as compared to SPEIs, and a network of industry experts (Fuchs et al., 2021). They can provide larger capital infusion and greater operational support to improve the firm’s potential by implementing the necessary improvements (Hotchkiss et al., 2021). Thus, we propose the following hypothesis:

Hypothesis 3: Better financial firm performance is negatively related to the propensity to sell the family firm to an APEI versus an SPEI.

The moderating effect of portfolio structures

Finally, we argue that structural elements in the form of family firm portfolios (Sieger et al., 2011) – that is, the existence of multiple firms owned by one family – moderate the aforementioned hypotheses. While the extant literature often assumes a ‘one family, one firm’ relationship, prior research suggests portfolio ownership is a common phenomenon (Michael-Tsabari, 2023; Sieger et al., 2011). Such portfolios might affect the chosen exit strategy as owners may attribute SEW to each venture (DeTienne and Chirico, 2013), affecting the above theorised relationships between SEW and selling preferences. While family firm exit in the case of a sole family firm leads to the owner’s complete loss of SEW, this loss – when selling a portfolio firm – is limited (Chirico et al., 2020). Moreover, prior research has found that family firm owners do distinguish between firm-level and portfolio-level SEW (Palm et al., 2023) and might sacrifice firm-level SEW to safeguard portfolio-level SEW. We theorise that the existence of a family firm portfolio would alter the owner’s SEW considerations and, thus, their preference to sell to one type of investor. Specifically, we expect that family firm portfolios weaken the proposed effects as the potential loss of SEW from selling one part of the portfolio can be offset by the activities of the remaining firms (Zellweger et al., 2012).

Family firm portfolio and family prominence

In H1, we hypothesised that family prominence is negatively related to the likelihood of selling to an APEI because of the expected negative effect of this exit route on the family’s reputation. We argue that this effect is likely to be weaker in the case of selling a portfolio firm, and stronger in the case of selling a sole family firm. In other words, we expect family firm portfolios to have a moderating effect on the primary relationship between the importance of family prominence and the propensity to sell to an APEI versus an SPEI, due to overall portfolio SEW considerations. The underlying reason being that the family’s presence in the community is less affected in the case of selling one firm from a portfolio as the owner can continue to view and present themselves as a business family. As such, they maintain high levels of SEW at the portfolio level (Akhter et al., 2016; Sieger et al., 2011), bolstering their values, emotions and reputation. Additionally, the substantial financial returns generated by selling one firm in a portfolio to an APEI can be reinvested in the remaining firms to further increase the family’s SEW endowments (Palm et al., 2023). Because the family is still engaged in firm-related activities, they continue to pursue and receive SEW benefits. Moreover, having more firms in the portfolio could lead to the owners having a lower emotional attachment to one particular firm (Akhter et al., 2016); therefore, they may be more inclined to sell to an APEI as SEW-related barriers are lower. In such cases, the family firm owner’s primary concern might be maximising the portfolio’s overall financial and non-financial value (Palm et al., 2023; 2024), which aligns with selling to an activist investor. Thus, we hypothesise:

Hypothesis 4a: Family firm portfolios weaken the negative effect of family prominence on the propensity to sell the family firm to an APEI versus an SPEI.

Family firm portfolio and innovation focus

In H2, we hypothesised that a family firm owner’s innovation focus is positively related to their propensity to sell to an APEI given extended SEW considerations. We argue that the positive relationship between the family firm owner’s innovation focus and their propensity to sell to an APEI, versus an SPEI, is weakened in the case of family firm portfolio ownership. One of our main arguments here being that APEIs are seen as investors that introduce change – for example, through restructuring, operational improvements and expansion (Acharya et al., 2013; Schickinger et al., 2018) – and will hence, foster growth and so benefit the overall community. In the case of selling a sole family firm in the absence of an internal successor, an APEI can act as an extension of the family firm owner’s pursuit of change following their exit (Slavec et al., 2017). However, when a family firm is part of a portfolio, the owner has alternative means of pursuing innovation through the remaining businesses. This reduces the need to rely on an APEI to fulfil innovation-related SEW considerations (Miller and Le Breton-Miller, 2014). Thus, portfolio ownership allows the family firm owner to address their innovation focus independently, leveraging the other businesses in the portfolio to achieve their broader goals (Palm et al., 2023). As a result, the presence of a portfolio diminishes the necessity of choosing an APEI to satisfy these considerations. As such, we propose:

Hypothesis 4b: Family firm portfolios weaken the positive effect of innovation focus on the propensity to sell the family firm to an APEI versus an SPEI.

Family firm portfolio and financial performance

In H3, we hypothesised that in the case of strong financial performance, owners are less inclined to sell to an APEI due to both financial and non-financial considerations. We conclude our theorising by proposing that this relationship is also weakened in the case of a family firm portfolio. Extant evidence (DeTienne and Chirico, 2013; Iacobucci and Rosa, 2010; Palm et al., 2023) suggests that not all firms in family firm portfolios generate the same SEW benefits and, likewise, they do not all generate the same financial benefits. As such, the financial performance of the firm is less relevant when making exit decisions as SEW, identification and family conflicts are likely to be influenced by the portfolio’s overall performance, not by the performance of an individual firm. Hence, the relationship proposed in H3 becomes less relevant in the case of portfolio firms. We also argue that owning a firm with a strong financial performance is likely to enable the family owners to further develop SEW through sound investments. Further to this, we propose that family firm portfolios allow owners to invest the returns generated by selling one firm into building up further SEW in others. For instance, they can build further SEW by opening new plants or investing in employee or community programmes. As such, the higher share prices offered by APEIs become more attractive as the returns generated can contribute to building further SEW in the remaining portfolio firms (Cruz and Justo, 2017). We conclude that family firm portfolios substantially alter both the financial and non-financial considerations of exiting family firm owners. Our final hypothesis is therefore:

Hypothesis 4c: Family firm portfolios weaken the negative effect of financial performance on the propensity to sell the family firm to an APEI versus an SPEI.

Methods

We used a vignette scenario study design to test our hypotheses. The vignettes we presented to family firm owners can be regarded as policy capturing, as they provide hypothetical but realistic scenarios (Connelly et al., 2016; Priem et al., 2011) that combine experimental and survey elements (Beham et al., 2015). The vignette part of our study consisted of two scenarios that only differed regarding the information provided about the existence of a family firm portfolio. Using vignette scenarios in various studies across different disciplines has yielded promising results, mainly when complex decision-making processes exist (Kim et al., 2024; Richards et al., 2019), such as selling the family firm to an external party. We gathered data from survey respondents in Germany, specifically targeting family firm owner-managers. We collected contacts using an initial data sample of 10,000 family firms located in the family firm portal Die Deutsche Wirtschaft, which has been used in prior research (Kurta et al., 2022; Querbachet al., 2020b). The portal defines family firms as private companies where at least 50% of the shares are in the control of the owning family or public companies where at least 25% of the shares are in the control of the owning family (Querbach et al., 2020b). We asked respondents whether they consider their firm a family firm, and only included their responses if they answered ‘yes’ to this question. We physically mailed the invitations to participate in our survey on 25 March 2021. Approximately 20% of the addresses in the dataset were outdated or had been changed, thus reducing the number of potential participants who received an invitation. The postal mailing date also coincided with lockdown and work-from-home regulations due to the COVID-19 pandemic; during the pandemic, approximately 38% of the total workforce were working from home during our data collection period (see IGES Institut, 2021), which further decreased the number of participants who received the invitation to participate in our survey. In week 4 of our data collection process, we contacted a random subsample of the potential respondents via e-mail or social media with a reminder note. We collected the data over 12 weeks between March and June 2021 and ultimately received responses from 306 firms; this gave a 6.2% response rate out of a presumed 4960 potential participants in our survey, which reflects prior research (Richards et al., 2019).

Before starting our analyses, we excluded responses that met any of the following criteria: (1) the firm was not considered a family firm, (2) more than 25% of the overall data was missing or there was missing information on the dependent variable or (3) the respondent was not a family owner or manager. After accounting for these criteria, our final sample consisted of 100 responses. Due to the within-person nested data structure of the two scenarios, the final multilevel regression contains 200 responses.

Design

Each respondent answered two scenarios (see the Appendix). In the first vignette scenario, we assumed the existence of a family firm portfolio, that is, the respondents were asked to decide about the sale of one family firm out of a portfolio of family firms. The second vignette scenario was identical to the first, with the exception that the family firm was presented as a sole family firm, that is, the scenario stated that the family did not have other firm holdings besides the family firm to be sold. We worked with two vignette scenarios instead of inquiring about the actual existence of a family firm portfolio, since the chosen approach allows us to capture the effect of a portfolio in isolation without interference factors (Aguinis and Bradley, 2014). Thus, the respondents assessed two identical short scenarios where only the existence (or non-existence) of a family firm portfolio was changed. The respondents then had to rate the following two offers that were in line with bids observed in the real world: (1) an APEI (Private Equity Investor A) offering 15% above the expected purchase price but that intends to comprehensively restructure the firm and (2) an SPEI (Private Equity Investor B) offering 15% below the expected purchase price but that is in alignment with the existing family firm values. In addition to the vignette scenarios, respondents filled out survey questions to capture additional information about themselves and their firms (see section “Measures”). We pilot-tested the questions with seven researchers and eight professionals to ensure that the descriptions were both realistic and comprehensive; the pilot test led to minor wording changes.

Measures

Dependent variable: Propensity to sell to the APEI versus the SPEI

Each respondent indicated their propensity to sell to each of the two investors. The respondents answered the question ‘What is the likelihood that you will consider the offer of the A/SPEI?’ on a five-point scale for each of the two offers (with ‘1’ indicating a very low likelihood and ‘5’ indicating a very high likelihood). The mean likelihood of selling to the APEI is 3.26 (standard deviation (SD) = 1.33), and the mean likelihood of selling to the SPEI is 2.97 (SD = 1.17), showing a general preference to sell to the activist investor. The resulting values for the offer made by the APEI served as our dependent variable in the multilevel regression analysis. As shown in the section on Post-hoc and Robustness tests, we used the responses for the SPEI in a robustness test.

Independent and moderator variables

To capture the importance of non-financial considerations, we assessed family prominence. According to Debicki et al. (2016), family prominence can be measured with three items (‘recognition of the family in the domestic community for generous actions of the firm’, ‘accumulation and conservation of social capital’ and ‘maintenance of family reputation through the business’) on a five-point scale ranging from ‘1 – not important’ to ‘5 – very important’. When we averaged the three items, we found that the mean value of family prominence is 3.13 (SD = 0.79). The items have a Cronbach’s alpha of 0.67.

Based on a scale by Tsai and Yang (2013), we used five items to measure innovation focus. We asked respondents to indicate whether they agreed or disagreed with the following statements based on a five-point scale ranging from ‘1 – fully disagree’ to ‘5 – fully agree’: ‘Innovation based on research results is readily accepted in our company’; ‘Management actively seeks innovative ideas’; ‘Innovation is readily accepted in management’; ‘Our company encourages and supports innovative activities’ and ‘New ideas are quickly accepted in our company’. These items indicate the acceptance of new ideas or the active pursuit of innovation by the family firm owner and by extension the importance of this in their firm (Tsai and Yang, 2013). The mean value of the five items is 3.86 (SD = 0.68), and they have a Cronbach’s alpha of 0.87.

We measured financial performance as a self-reported variable (Cheng et al., 2014; Zhang and Walton, 2017) by asking respondents to assess four items (‘return on assets’, ‘sales growth’, ‘market share growth’ and ‘overall firm performance’) on a five-point scale ranging from ‘1 – very unsuccessful’ to ‘5 – very successful’, and we calculated their average. We followed prior research by Tsai and Yang (2013) to capture business performance in a self-reported manner because we had no objective data on the performance of our sampled family firms (Cheng et al., 2014; Zhang and Walton, 2017). The mean value of financial performance is 3.74 (SD = 0.60). The items achieve a Cronbach’s alpha of 0.79.

The scenarios included the dummy variable family firm portfolio (DeTienne and Chirico, 2013). This variable indicates the existence of a family firm portfolio versus the existence of a sole family firm and is changed in the two vignette scenarios that the respondents answered.

Control variables

We controlled for additional factors that might influence a respondent’s preference for each of the two types of investors. We included the percentage of the firm owned by the family as a control variable, since a family firm with a shareholder structure that already has external participation might differ in its governance guidelines and capital preferences (Martin et al., 2017). We also controlled for the generation in charge of the family firm. Later-stage generations might have a different manifestation of SEW due to the family firm’s longevity, which could also shift external investor preferences (Berrone et al., 2012). We measured generation on a scale ranging from ‘1’ to ‘7 and above’.

We determined that controlling for the size of the family firm was particularly important, given that larger family firms are more likely to have experience with outside investors (Seet et al., 2010). In addition, those firms with a larger number of employees might be more professionally managed, for instance through non-family managers and thus, might prioritise financial rewards above non-economic goals (Dawson, 2011; Granata and Gazzola, 2010; Stewart and Hitt, 2012). We included size, based on the number of employees, as a control variable. We also controlled for whether eponymy was in place using a dummy variable, where ‘1’ indicated eponymy and ‘0’ indicated no eponymy. A firm name related to the family name (eponymy) leads to higher identification of stakeholders and shareholders with the firm and is related to the non-economic benefits of SEW (Berrone et al., 2012).

In order to understand the respondent’s educational level, we asked for their highest completed level of education, ranging from ‘0 – no high school degree’ to ‘6 – PhD or higher’. This is because prior family firm research has shown that education influences exit preferences (Richards et al., 2019). Finally, we asked for the industry, which we grouped into ‘production’, ‘services’ and ‘other’.

Results

Descriptive analysis and tests for data quality

Table 1 shows the correlation matrix and descriptive statistics for the variables included in our analysis. As the correlation matrix reveals, there are primarily low to moderate correlations between the variables in the model. On average, the family firms in our sample were in the third generation, and most of the shares were held by family members (97.58%). The average firm size based on the workforce was 1097 employees. The respondents were, on average, 51 years old and, therefore, according to prior research (Leach, 2016), should have already seriously considered succession options. Respondents had primarily finished a master’s degree or equivalent diploma. Forty-nine percent of family firms in our sample were from the production sector, 35% were in services, and the remaining 16% were active in other sectors. Fifty-three percent of firms had a name connected to that of the family. Fourteen percent of respondents were female, while the majority (86%) of the respondents were male. On average, they had been with the family firm for 18 years, with nine years of experience outside the firm.

Descriptive statistics.

APEI: activist private equity investor; SD: standard deviation; SPEI: steward private equity investor.

Number of employees has been standardised by log-transformation.

p < 0.05.

Common method bias

We applied several measures to avoid common method bias. Due to the nature of our study and in line with our research questions, we collected data on the variables from single respondents in one survey. This can result in common method bias; however, we argue that this is less likely in our case. To pre-emptively reduce the occurrence of common method bias, we phrased the survey questions simply and tested them by involving family firm owner-managers in a pilot study (Podsakoff et al., 2024). Furthermore, as Podsakoff et al. (2024) suggested, we avoided complexly worded questions, peculiar scientific phrasing and double-barrelled questions. As the vignette scenarios were part of a more extensive data collection, we ordered the questions in a way that did not allow respondents to predict which correlations we were interested in exploring. This step helped prevent respondents from answering in a way that they assumed the researchers expected them to reply (Podsakoff et al., 2024). Further, we pledged total anonymity and confidentiality, which has been found to improve honesty and reduce social desirability bias (Podsakoff et al., 2024).

In addition to our pre-emptive efforts to reduce common method bias, we completed two retrospective tests to check for common method bias. First, we conducted a single-factor test based on Harman (1976; see also Fuller et al., 2016 for a review): We identified seven factors where the Eigenvalues exceeded 1. In total, these factors accounted for 73.69% of the variance, with the first factor only explaining 21.69% of the variance. This result indicates that common method bias is likely not a major concern in our analysis because a single factor does not explain most of the variance. Therefore, we can assume that the existing data structure is not an artefact of the measurement process (Fuller et al., 2016). Additionally, we performed the marker variable test (Lindell and Whitney, 2001), which investigates the correlation between our dependent and marker variables (Homburg et al., 2010; Querbach et al., 2020a). To conduct the marker variable test, we assessed the correlation between the perceived probability of finding a family internal successor (marker variable) and the propensity to sell to an APEI (r = −0.04). A correlation of over 0.30 between any of the latent variables and our marker variable would indicate that common method bias is an issue (Tehseen et al., 2017). We concluded that common method bias was not an issue because the correlations between the latent variables and the marker variable were below 0.30 (e.g. correlation with family prominence: 0.1058 non-significant (ns); correlation with financial performance: 0.0121, ns; correlation with innovation focus: 0.0234, ns). The significance of these correlations does not change substantially after correction of the correlation tables, providing additional evidence for the absence of common method bias (Simmering et al., 2015).

Representativeness and non-response bias

We conducted representativeness and non-response bias checks of our data. We compared our sample’s primary attributes – such as the number of employees, the age of the firm and the industry – with information on family firms in Germany to verify our sample’s representativeness. These data were taken from a major database on family firms. Regarding firm size, the firms in our sample were slightly smaller than average, with a median of 350 employees, compared with 380 employees in our peer group database. The firms in our sample were also slightly older than the peer group average, with an average firm age of 90 years versus 85 years in the peer group. Regarding industry type, the share of firms in our sample that were in the production sector was slightly lower than the peer group, at 49.0% versus 58.5%. The remaining 51.0% of our sample (and 41.5% of the peer group) were in either the service sector or other sectors. Finally, we discovered no significant difference between the average age of our sample respondents, at 51 years, and the average age of 49 years for family firm owner-managers reported in the literature (Glowka et al., 2021). We ran a Welch t-test for unequal variances and sample sizes and found no statistically significant differences (t = −1.62; p = 0.11).

Attention checks

We used factual checks to verify whether our study participants diligently read and correctly understood the scenarios, as Kane and Barabas (2019) suggested. One example of these checks was as follows: ‘Based on the previous description, the activist private equity investor . . .’ with only one right answer, ‘pays more than the steward investor’. The selection of any of the four other answer choices (e.g. ‘pays less than the steward investor’) would indicate that the participant failed the attention check. We excluded 14 participants who answered both scenarios but failed the attention checks.

Regression results

Due to the within-person nested data structure, we tested our hypotheses by performing a multilevel regression analysis with the propensity to select the APEI as our dependent variable. Using an empty null model, we estimated the intraclass correlation coefficient (ICC), which is used to quantify the degree of similarity among values within a group. Between-subject variances were responsible for 74.08% of the outcome variability, indicating that much of the variation in the outcome can be explained by the differences between the groups (family portfolio status). This suggests that the differences between groups significantly influenced the observed outcomes. An ICC of over 0.05 indicates that hierarchical linear regression modelling is recommended (McNeish, 2014; Raudenbush and Bryk, 2012). Table 2 depicts the results of the multilevel regression with three models. Model 1 only includes the control variables. Model 2 subsequently adds the independent variables of family prominence, innovation focus and financial performance, as well as the moderator variable of family firm portfolio. Model 3 includes the interactions between the independent and moderator variables, and hence the full model.

Regression model.

APEI: activist private equity investor; ICC: intraclass correlation coefficient.

p < 0.05. **p < 0.01.

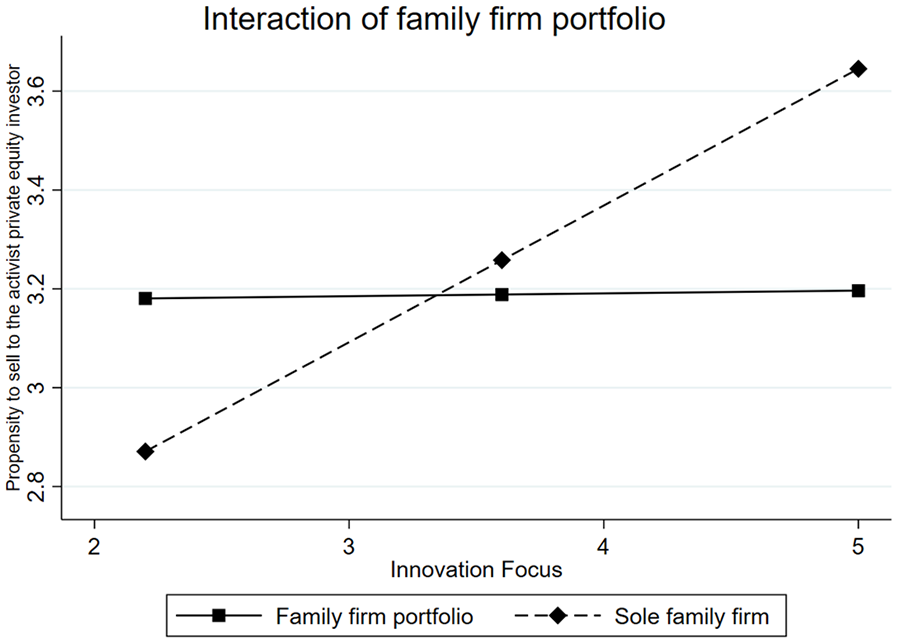

Model 1 indicates a significant negative effect of the control variable eponymy on the preference to sell to an APEI (β = −0.665; p < 0.05). Model 2 indicates a significant negative effect of family prominence (β = −0.395; p < 0.01) and financial performance (β = −0.545; p < 0.01) on propensity to sell to an APEI, in line with our hypotheses, while the effect of innovation focus on propensity to sell to an APEI was not significant (β = 0.094; ns). The results of Model 3 provide support for H1 (β = −0.424; p < 0.01) and H3 (β = −0.552; p < 0.01), but not for H2 (β = 0.224; ns). H4 suggests that family firm portfolios moderate the theorised relationships. Only the interaction effect between innovation focus and family firm portfolio (β = −0.260; p < 0.05) is significant in our analysis; thus, our results partially confirm H4. Figure 1 shows the interaction plot of the moderation of family firm portfolio and innovation focus.

Interaction plot showing the interaction of family firm portfolios and innovation focus of the family firm owner.

Post hoc and robustness tests

As a post hoc test, we probed how the independent variables in our model affect a family firm owner’s propensity to accept the offer of the SPEI. We performed a multilevel regression analysis where the propensity to sell to the SPEI was the dependent variable. The results were in line with our main results: H1 (β = 0.332; p < 0.05), H2 (β = −0.138; ns) and H3 (β = 0.480; p < 0.01). We argue that the SPEI does not harm but rather respects the SEW goals of the family and is, thus, favoured when family prominence and firm performance are higher. For H4, the interaction between innovation focus and family firm portfolios is positive and marginally significant (β = 0.223; p < 0.1). Table 3 shows this full post hoc test.

Regression model robustness test I.

ICC: intraclass correlation coefficient; SPEI: steward private equity investor.

p < 0.05. **p < 0.01. +p < 0.1.

As we targeted individuals both owning and managing the family firm, we ran an additional robustness test where we excluded all participants for whom we could not guarantee this status (n = 15) because they did not answer that question in the survey. We ran the models again, excluding these respondents. This robustness test indicates no significant difference from the results of our main analysis; detailed results for this test are shown in Table 4. We also conducted additional regression analyses with control variables, capturing: (1) the existing intent to sell to a financial investor and (2) previous experience with financial investors. The results remain stable and can be obtained from the authors upon request.

Regression model robustness test II.

APEI: activist private equity investor; ICC: intraclass correlation coefficient.

p < 0.05. **p < 0.01. +p < 0.1.

Discussion

Selling to an investor is an important exit option for family firm owners, particularly in cases where there is no internal succession candidate. Availing of this option ensures that owners are compensated for their life work (Von Bonsdorff et al., 2019) while ensuring future firm prosperity after their exit. However, investors are not homogeneous; their diversity affects the preferred sales route of family firm owners (Molly et al., 2018). APEIs are financially focused, and their priorities have the potential to undermine the SEW-generating, but perhaps less financially focused activities of the family owners (Gómez-Mejía et al., 2007). SPEIs, conversely, might perpetuate these activities for the family’s sake; however, their potential financial gain from their purchase might be constrained leading to a lower offer price than that from an APEI. Our research examined what might influence the family firm owner’s preference to sell to either of these two financial investor types. We drew on arguments embedded in the SEW perspective (Berrone et al., 2012) and considered how the preservation of family prominence, innovation focus and firm performance affect such propensity whilst examining how this preference was moderated by family firm portfolio status. We found that valuing family prominence and strong financial performance decreases the propensity to sell to an APEI and so increases the propensity to sell to an SPEI. Family firm portfolio status is crucial as it moderates the effect of the family firm owner’s innovation focus on the propensity to sell to an APEI (see Figure 1).

Contribution to family firm succession literature

Our research contributes to the family firm external succession and exit literature (Chirico et al., 2020; DeTienne and Chirico, 2013). We explore factors that influence the sale preferences of family firm owners with regard to investor types (Neckebrouck et al., 2017; Seet et al., 2010) noting that on a global basis, external succession is becoming increasingly common for family businesses. Existing research has investigated the impact of private equity investments on family firms (Achleitner et al., 2010) and considered the buyer side, and their interest in acquiring family firms (Dawson, 2011). The seller side, that is the family firm perspective, has been under-studied. We contribute to this debate by investigating the family firm-specific drivers that influence the preference to sell to different investor types. This is important as knowledge regarding why family firm owners might prefer an APEI, rather than an SPEI – or vice versa – is an important step towards understanding the repercussion this might have on negotiations and relationships (Michelet al., 2020; Scholes et al., 2010). Our insights, moreover, are relevant to the family firm succession and exit literature as the preference for, and subsequent choice of, a specific investor type might have substantial consequences for the future of the firm, its stakeholders and potentially the community and region as a whole. Thus, a better understanding of the antecedents of such preferences is required. As such, our research advances family firm succession knowledge by acknowledging that private equity investors are not homogeneous, and by providing theoretical and empirical evidence that future succession and exit research need to distinguish between different types of investors. Advancing the conceptual work of DeTienne and Chirico (2013), we empirically study and provide initial insights into a family firm owner’s preference for APEIs over SPEIs, or vice versa. Extant research (Richards et al., 2019) has explored family-internal succession dilemmas, such as considering the importance of competence versus motivation. We, however, extend such arguments to external family firm succession dilemmas, such as analysing the family firm owner’s own financial benefits versus continuing the quasi-family firm.

Our theoretical and empirical findings illustrate that both financial and non-financial considerations affect a family firm owner’s preference for an investor type. While, overall, the descriptive results of our study reveal that exiting family firm owners prefer to sell to the highest bidder, our data also reveal substantial heterogeneity, highlighting the importance of non-financial considerations in selecting an investor type. The evidence also shows that these considerations are related to family prominence and prior firm financial performance. Accordingly, our hypotheses that family firm owners who have sufficient financial resources due to strong firm financial performance, who possess substantial SEW endowments within their firms and/or who care about family reputation and family firm values will forgo personal wealth maximisation. Our results support the argument proposed by Martin et al. (2019) that owners care about their former firm and how the new decision-makers will sustain, or revoke, their former decisions.

Interestingly, our hypothesis regarding the influence of innovation focus, referring to extended SEW, was not empirically supported. We proposed that the assumed effect of APEIs on stakeholders, such as employees, might be more complex than initially expected. While an innovative and professional firm will benefit employees, as we argued in the section on “Innovation Focus and Investor Type Preferences”, family firm owners might be influenced by the generally negative public perception of APEIs (Bacon et al., 2013; Goergen et al., 2014). This may evoke some reluctance to consider the positive effects that selling to an APEI has on their extended SEW. This effect might be particularly strong in the context of family firms in Germany, where, in 2005, a high-profile politician generated an intense societal debate about APEIs, comparing their prevalence to a locust infestation. As such, our study contributes to this debate by revealing a need for further research on the effect of different types of private equity investors on the employees, and other stakeholders, of former family firms.

This study also contributes to family firm exit research (DeTienne, 2010; Widz and Kammerlander, 2022) by illustrating the effect of family firm portfolios on exit route preferences (Sieger et al., 2011). Although Palm et al. (2023) emphasised the importance of portfolios as a structural determinant of family firm restructuring decisions, our results are mixed. We do see that the existence of a family firm portfolio moderates the effect of an innovation focus on investor type preference. As shown in Figure 1, the proposed effect of a greater innovation focus being positively related to the propensity to sell to an APEI exists for sole family firms; yet, it disappears in the case of a family firm portfolio. Contrary to our hypotheses, we did not identify any of the proposed interactions between a portfolio structure and family prominence or financial performance. One potential explanation being that family prominence is of such social significance for family firm owners that it remains unaffected by portfolio status. Selling one portfolio firm to an APEI could financially benefit the whole portfolio; however, it might still diminish the family’s standing within the community, thus leading the family to reject selling to an APEI unless considered as a ‘last resort’ (Henn and Lutz, 2017: 9). A similar reason might explain the non-significant effect tested in H4c. This hypothesis followed the argument that the sale of one firm from the portfolio might benefit the others, thereby enhancing overall portfolio SEW. While this theorising aligns with extant research (Palm et al., 2023), the non-significant effects in our analysis might indicate that in these cases, firm-level SEW considerations were stronger than overall portfolio-level SEW considerations; once again, this calls for further research.

Contribution to research on the SEW perspective

Our theoretical and empirical findings also advance research on SEW (Berrone et al., 2012; Gómez-Mejía et al., 2007). Specifically, our study builds on and extends prior work on the importance of SEW considerations for family firm exit route preferences (Ahlers et al., 2018). With our study, we propose that SEW considerations are not only relevant for family firm owners during their period of firm ownership, but also that these considerations influence exit preferences, thereby extending the application of the SEW perspective beyond the family’s ownership tenure. Although one could assume that selling the family firm would result in a total loss of the accumulated SEW, we propose that the phenomenon is more nuanced: while the SEW endowments within the firm are not accessible to former family firm owners after their exit, SEW considerations still affect the related decision-making. For instance, we argue that the reputation of the family – an important SEW dimension (Berrone et al., 2012) – might depend on the future of the family firm and is, therefore, affected by the specific investor type chosen. It is also possible that family firm owners might find pleasure in the idea that certain values and established routines will continue to exist in the firm (Kammerlander, 2016). Hence, as SEW considerations continue following the family’s exit from the firm, our findings supported our hypothesis that family firm owners who prioritised family prominence would prefer SPEIs who claimed they would safeguard business stability, rather than implementing more severe restructuring efforts (Gómez-Mejía et al., 2007; Vincent et al., 2018). As such, our research encourages future studies to debunk the assumption that firm sale equals a total loss of SEW and to consider non-financial aspects after the exit.

This study also notes the distinction between extended and restricted SEW (Miller and Le Breton-Miller, 2014). Our theorising includes the concept of family prominence, which focuses on the immediate benefits for the family – specifically its reputation – and, as such, is closely related to restricted SEW. 6 Our results reveal that restricted SEW considerations substantially influence exit preferences (DeTienne and Wennberg, 2016) independent of the family firm structure. Our results can be seen as a confirmation of the strong influence of restricted SEW on major family firm decisions. Innovation focus (Tsai and Yang, 2013), however, is not centred on immediate benefits or benefits for the family, but rather relates to the family-external stakeholders and the long-term prosperity of the firm. As such, innovation focus, as we argued in the section on innovation focus and investor type preferences, is closely related to extended SEW (Makó et al., 2018; Martínez-Alonso et al., 2018). Our results show that innovation focus only affects exit preferences in cases of sole family firm structures, and not in cases where family firm portfolios exist. Therefore, the effect of extended SEW is strongly dependent on family firm structure. Thus, our research advances the literature by providing preliminary evidence that not only might extended and restricted SEW differ in their focus, time perspective and consequences, but also that their importance differs depending on context. Finally, from a methodological point of view, we add to an emerging research stream that uses experimental approaches to gain insights into family firm behaviours and SEW implications using a policy capture approach (Richards et al., 2019). We combine a vignette scenario design with SEW theorising to offer insights into a complex real-world phenomenon (Berrone et al., 2012; Debicki et al., 2016), focusing on realistic, situational vignettes (Aguinis and Bradley, 2014; Mathias and Williams, 2017) that allow for the study of individual sensemaking processes.

Contributions to practice

Besides its theoretical implications, our study also offers insights for practice. Specifically, this research can help family firm owners to better understand their succession options related to selling to a financial investor. Based on our theorising, family firm owners and their advisors can obtain a clearer perspective about the SEW consequences of a sale to an APEI versus an SPEI. We highlight that financial investors are not homogeneous in their offering, or their impact on a family’s SEW endowments. Having several offers at the time of firm exit, however, can lead to conflicts for decision-makers; a thorough understanding of the consequences of each option might help family firm owners and their advisors take the best decision for their situation. As our research shows, there is no universal best option; each investor type has both advantages and disadvantages of the family and the firm which require diligent assessment. Being aware of the influence of family prominence, innovation focus, firm performance and portfolio structures can reveal the underlying reasons why some family firm owners might prefer a certain type of buyer when several investor offers are available. Such knowledge also helps advisors to engage in meaningful conversations when supporting family firm owners with the succession process. We would argue that the complexity of deciding upon which of the different sales options is most appropriate should encourage family firm owners to devise an exit strategy in a timely fashion to anticipate unforeseen circumstances leading to hasty decisions. In addition, family firm owners need to be aware of the asymmetrical situation in the case of firm sales: Whereas this is often a ‘once-in-a-lifetime’ event for family firm owners, private equity investors are experienced in such negotiations and, therefore, have greater power. As such, it is highly recommended that family firm owners work together with specialised lawyers and other experts if considering selling to such investors. The evidence from this study can also inform those seeking to invest in family firms. We highlight that family firm owners have divergent preferences regarding the potential buyers of their firms; many value the importance of SEW endowments even beyond their exit. As such, they may forego a higher valuation of the firm at the time of exit in order to safeguard those SEW endowments. An awareness of such preferences can avoid potential conflicts between investors and family firm owners.

Limitations and avenues for further research

Like all research projects, our study has limitations. Some scholars may criticise that we analysed hypothetical exit intentions rather than actual firm exits. We argue that this research design offers significant advantages by examining a family firm owner’s preferences in isolation, segregating them from external considerations such as the negotiation process or the influence of other stakeholders on the exit process (DeTienne et al., 2015; Schickinger et al., 2018). Through our vignette scenarios, we can study the direct implications of our independent variables. Still, further research should scrutinise when and under what circumstances these preferences also translate into real family firm exits. Also, we did not investigate whether the respondents had already contemplated succession options before participating in our study and we, therefore, encourage future research to examine the temporal sequence of how preferences for certain types of buyers develop.

We do acknowledge that in the vignette scenarios, we focused on one specific exit type, namely the complete sale of the firm to a financial investor due to the family firm owner nearing retirement and the absence of an internal successor. While such situations are common (Schickinger et al., 2018), other exit options also exist. We encourage the conduct of future studies to deepen our understanding of other reasons for selling family firms such as exploiting growth potential, as well as other types of sales such as the sale of minority shares, and how these might affect the type of investor chosen. For such studies, alternative theoretical approaches, such as pecking order theory (Tappeiner et al., 2012), might be appropriate. Moreover, it would be interesting for future research to not only focus on financial investors, but also to include strategic buyers and, using a qualitative research design, scrutinise how the family business seller and the investor that buys the firm interact with each other and how the negotiation process develops over time.

Finally, firm exit, especially when financial investors are involved, is a particular and complex family firm succession scenario (Di Toma and Montanari, 2017). Despite the limitations of a single study, we highlighted some factors related to SEW that affect the propensity to sell to one of two types of external investors. Future research could replicate our study in other geographical settings, include further explanatory variables such as family size or family cohesion and study additional implications such as non-financial considerations, for example, employment security. Furthermore, future research should focus on the type of portfolio firm being sold – that is, selling a core versus satellite firm – as it has been noted that there are differences in SEW inclinations of family firm owners regarding such firms which could affect exit preferences (Akhter et al., 2016).

Conclusion

This article examined an understudied, yet increasingly important, external succession route for family firms – selling to a financial investor. We commenced the analysis with the assumption that financial investors are not a homogeneous group but differ in their financial and non-financial implications for both the family and the firm. Integrating existing literature on family firm succession, SEW and family firm portfolios, we developed a set of four hypotheses which we subsequently tested based on responses of family firm owners to vignette scenarios. We hypothesised and empirically demonstrated a negative effect of family prominence and financial performance on a family firm owner’s preference to sell to an APEI versus an SPEI. Additionally, we demonstrated that the existence of a family firm portfolio plays a moderating role by weakening the effect of innovation focus on the propensity to sell to an APEI. Our study, therefore, illustrates how restricted SEW directly affects succession preferences, whereas extended SEW considerations might only play a role in the case of sole family firm exit and not in the case of a family firm portfolio. In so doing, we advance understanding of family firm succession as well as SEW and provide relevant insights for practitioners.

Footnotes

Appendix

Author’s note

An earlier version of this paper was presented at the Academy of Management Annual Meeting 2022, IFERA conference 2022 and EURAM 2022 as well as at several doctoral seminars at WHU – Otto Beisheim School of Management, Germany.

Author contributions

The first author was involved in all parts of the research project, providing guidance regarding the research design, data collection and analysis and conducted a literature review. Moreover, she was responsible for carrying out the revisions. The first author was responsible for data collection, data analysis and for writing the first draft.

Data availability

As noted in the manuscript, the paper is based on a more extensive data collection, out of which one paper has already been published (Kurta et al., 2022). Both studies differ in the dependent variables, most independent variables (except family prominence), moderator variables and sample size. There is overlap in the control variables, though.

Declaration of conflicting interests

The authors declare that they have no conflict of interest and adhered to the ethical standards of the institution, WHU – Otto Beisheim School of Management, that they are affiliated with.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: The author disclosed receipt of the financial support of the law firm Poellath & Partners, Munich, to collect survey data. The funder exerted no influence on the design of the questionnaire and/or data analysis and interpretation.