Abstract

This article analyses the organisational and individual drivers and barriers to the implementation of circular business models (CBM) by incumbents and start-ups in the workwear industry. It is based on a qualitative study of 15 organisations in the Swedish workwear industry. Most incumbents are found to have either long-life models with hybrid elements, such as repair, or access models, while circular start-ups have a larger variety of CBMs, although the most common is gap exploiter. Internal organisational barriers mostly differ between the two groups; however, external organisational barriers are more significant and common, such as the low price of new workwear, a lack of demand and a lack of supporting policies, for example, public procurement. Several organisational drivers are identified, such as opportunities to deliver customer value, textile and digital innovations and environmental concerns. Drivers and barriers are influenced by both type of CBM and type of company. Individual drivers and barriers, which are often overlooked in literature, are found to be important to CBM implementation.

Keywords

Introduction

Today, the concept of circular economy is of growing interest for policymakers, investors, corporations and civil society to meet calls for sustainability (Blomsma and Brennan, 2017). A circular economy is an economic system that is envisioned to decouple economic growth from resource use and, as a consequence, also from environmental impacts by preserving the value of products, components and materials in the economy and using them more effectively and efficiently (Korhonen et al., 2018). This is achieved through activities such as repair, maintenance, reuse, redistribution, refurbishment, remanufacturing, recycling, cascading, repurposing and organic feedstock use (Lüdeke-Freund et al., 2019). The underlying premise is that resource extraction, and waste and pollution generation will be minimised without crippling economic growth, which is necessary for a growing global population (McCarthy et al., 2018; Murray et al., 2017). Firms are going to implement these activities while policymakers need to create the conditions to make implementation possible and profitable (Ghisellini et al., 2016; Lieder and Rashid, 2016).

In the ever-increasing body of both academic and grey literature, focusing on how firms can align their activities to circular economy principles of preserving the value of products in the economy, the concept of circular business models (CBM) has become central (Bocken et al., 2016; Ferasso et al., 2020). A business model describes how a firm creates, delivers and captures value (Osterwalder and Pigneur, 2010). CBMs allow firms to create, deliver and capture value, in such a way that the value of resources is kept in the economy and used more efficiently and effectively (Pieroni et al., 2019). Although the term ‘CBM’ itself is relatively new, different aspects of product life extension or intensification have been the focus of many streams of research such as remanufacturing (Östlin et al., 2009), material efficiency (Allwood et al., 2011) or product-service systems (Tukker and Tischner, 2006). Since various strands of CBM literature have a decades-long history (Whalen, 2020) and CBM publications are increasing fast, the majority of which are qualitative case studies (Ferasso et al., 2020), one might expect CBM implementation in firms to be high. Reports from various organisations, however, such as the Circularity Gap Report (2022), which gives a global score for circularity implementation or the progress report on the global commitment on circularity of plastics (Ellen MacArthur Foundation, 2022), both state that the circular economy is still a niche endeavour and that key targets are predicted to be missed. This indicates an implementation gap, and academics are in agreement: a shift is happening, but progress is slow (Urbinati et al., 2017).

One way of making sense of this implementation gap is by looking into the drivers and barriers faced by firms (Govindan and Hasanagic, 2018; Kirchherr et al., 2018). It is within this broader field that this research is placed. It is not the first work in this field; there have been a number of articles explicitly investigating drivers and barriers to a circular economy and CBMs (Tan et al., 2022) as well as empirical studies of CBM where drivers and barriers are taken up as part of a larger discussion around CBMs (Hina et al., 2022). In this research, we intend to add to this body of literature in four distinct ways.

First we research the drivers and barriers for both incumbents, that is, existing firms, including SMEs and large firms that already have a product or service on the market, and start-ups, that is, firms starting from scratch with the intention of growing beyond the founder. Current research both on CBMs and their drivers and barriers has focused almost exclusively on incumbents (Henry et al., 2020; Tan et al., 2022) or just combines incumbents and start-ups without distinguishing between them (Kirchherr et al., 2018). These two categories, however, face somewhat different sets of drivers and barriers both in general and in the circular economy context, and therefore it is necessary to research them as separate categories.

Second, apart from focusing only on the drivers and the barriers of the organisation, we explore the role of the individuals involved, that is, the entrepreneur in the case of a start-up or the intrapreneur in case of an incumbent. Hopkinson et al. (2018) stated that developing and maintaining successful CBMs requires the development of managerial competencies and capabilities. However, the individual’s role has been largely overlooked in the implementation of CBM (Ferasso et al., 2020).

Third, we do not just consider either incumbents or start-ups separately but compare these two groups and reflect upon their relationship to each other in the context of a specific industry. This helps us to understand how these two types of firms relate to each other in more general terms. The specific context we use in this study is that of the workwear industry. Using a specific context is necessary in making a meaningful comparison because both product characteristics (Böckin et al., 2020) and industry sector (Pieroni et al., 2021) influence what type of measures and CBMs can be implemented.

Fourth, we aim to contribute to sector-specific CBM knowledge, that is the workwear industry, a key part of the textile industry, which, according to a recent study, has a large environmental footprint but nevertheless has been mostly overlooked in both sustainability and circular economy research (Malinverno et al., 2023).

To sum up, the research question is: What are the organisational and individual drivers and barriers for start-ups compared to incumbents when implementing CBM?

We use a qualitative method to answer the research question by collecting data from 15 organisations operating in various stages of the workwear lifecycle in the Swedish workwear industry.

We find that incumbents offer either classic long-life models or access models while circular start-ups bring a larger variety of CBMs to the market, although the most common is gap exploiter. A variety of external drivers and barriers are identified on the organisational level, many are common to both groups of firms. The three main barriers are: the lack of supporting policies (e.g. public procurement), the low price of new workwear and the general lack of demand and incentives for reuse. Both incumbents and start-ups are driven by their customers’ environmental concerns and the upcoming extended producer responsibility regulation. Internal organisational drivers and barriers differ substantially, although some commonalities are observed relating to environmental concerns, opportunities to deliver customer value and textile and digital innovations. Apart from the organisational perspective, the individuals’ drivers and barriers are found to significantly influence CBM implementation. This article highlights opportunities for future research and examples of practical implementation.

This article is structured as follows: First, in sections ‘Introduction’ and ‘Frame of reference’ the article is positioned in relation to the key characteristics of the workwear industry in Sweden, the literature on CBMs and its drivers and barriers, as well as the role of start-ups, incumbents, entrepreneurs and intrapreneurs in a circular economy. This is followed by a description of the methodology and a presentation of the results and analysis where the research question is answered. This answer is then discussed in relation to the literature and managerial implications. We conclude with a discussion of our contribution and implications for further research.

Frame of reference

The workwear industry

Today the textile and clothing industry is one of the most polluting and resource-intensive industries in the world (European Environment Agency, 2019). Production and distribution of textiles require large amounts of energy, water and material resources, and contribute to air, water and land pollution as well as greenhouse gas emissions (ibid.). The texttile industry is characterised as having Another challenge is textile overconsumption, which is driven, amongst other reasons, by our need for novelty and numerous alternatives, a lack of awareness of the environmental impacts and a lack of infrastructure that supports repair, reuse, upcycling and so on. (Chen et al., 2021). The rule of thumb is that reducing our overall consumption is the best option from an environmental perspective followed by keeping a textile product as close to its original form through reuse, repair or upcycling, followed by recycling materials and finally, energy recovery (Braun et al., 2021).

A not-insignificant part of the textile and clothing industries is workwear. Workwear is required for many reasons, including health and safety, comfort and company branding and include suits, overalls, jackets, trousers, skirts, gloves, protective gear and so on. Using workwear can be mandated by regulations, for example, in the Swedish Work Environment Act (1977:1160, chapter 2:7), and therefore, there is a very important safety and ergonomic aspect of workwear where different industries set different requirements (Ke et al., 2015). For example, in the healthcare sector, the hygiene risk factor requires high temperature washing of workwear (Riley et al., 2015).

The market of workwear was globally valued at USD 16,773.3 million in 2021 and is expected to grow at an annual rate of 5.6 % from 2022 to 2030 (Grand View Research, 2022). This growth reflects the importance of company branding generally in the workplace, especially in manufacturing and corporate sectors as well as the increase in workplace accidents and fatalities globally that drives up the demand for protective workwear and footwear (ibid.). Research and government reports claim that the workwear industry also faces overconsumption and fast disposal challenges similar to the fashion industry (Malinverno et al., 2023). However, generally, the workwear industry, as opposed to the fashion industry, shows a relatively higher potential for reuse and recycling because workwear is often uniform, available in large quantities and of high quality, which makes it easy to develop economies of scale around CBMs (Malinverno et al., 2023).

On the demand side of the workwear industry, public organisations make up a large part of the market. Their procurement of workwear is often governed by public procurement regulations. There are also many large firms that procure workwear, for example, supermarket chains and construction firms. Both groups usually order customised clothes with company logos. Then there are also smaller firms and individuals who buy workwear to use for DIY projects. These two groups buy clothes from ready-made product ranges, possibly with the company logo sewn into it. On the supply side, production is similar to the textile industry, that is, via globalised complex supply chains. These include both large and small retailers, large distributors and resellers and many providers of upstream activities such as cotton, fibre and yarn production, spinning, dyeing, printing and manufacturing.

The workwear industry is far from being part of a circular economy (Ellen MacArthur Foundation, 2021) and CBMs based on recycling, upcycling, downcycling, reusing redesigning and remaking require a network of actors that take responsibility for collaboration and sustainability. Both on the demand and the supply side, there are some very large actors that have the power to change or resist change to the linear status quo (Huulgaard et al., 2022). For example, Huulgaard et al. (2022) and Rainville (2021) identified public procurers as having power to make change happen in the workwear industry. This difference in market power and actor sizes creates the context for implementing CBMs and identifying drivers and barriers in the workwear industry. It also shows that there are differences between the workwear industry and the fashion industry, which has more small-scale retailers and individual consumers, amongst others. Therefore, we draw upon literature from the fashion industry as well as broader circular economy literature in the following section.

Circular business models

The concept of a circular economy is not clearly defined, and the fast-paced growth of the literature using the concept, as well as the fact that this term has now become an umbrella term (Blomsma and Brennan, 2017), means that it will most likely remain unclear; thus, it remains more of a vision for our future. Despite the lack of an established definition, there is a basic common understanding that resources are used more efficiently and effectively within the economy to meet the needs of the growing global population and the need for more job opportunities (Murray et al., 2017).

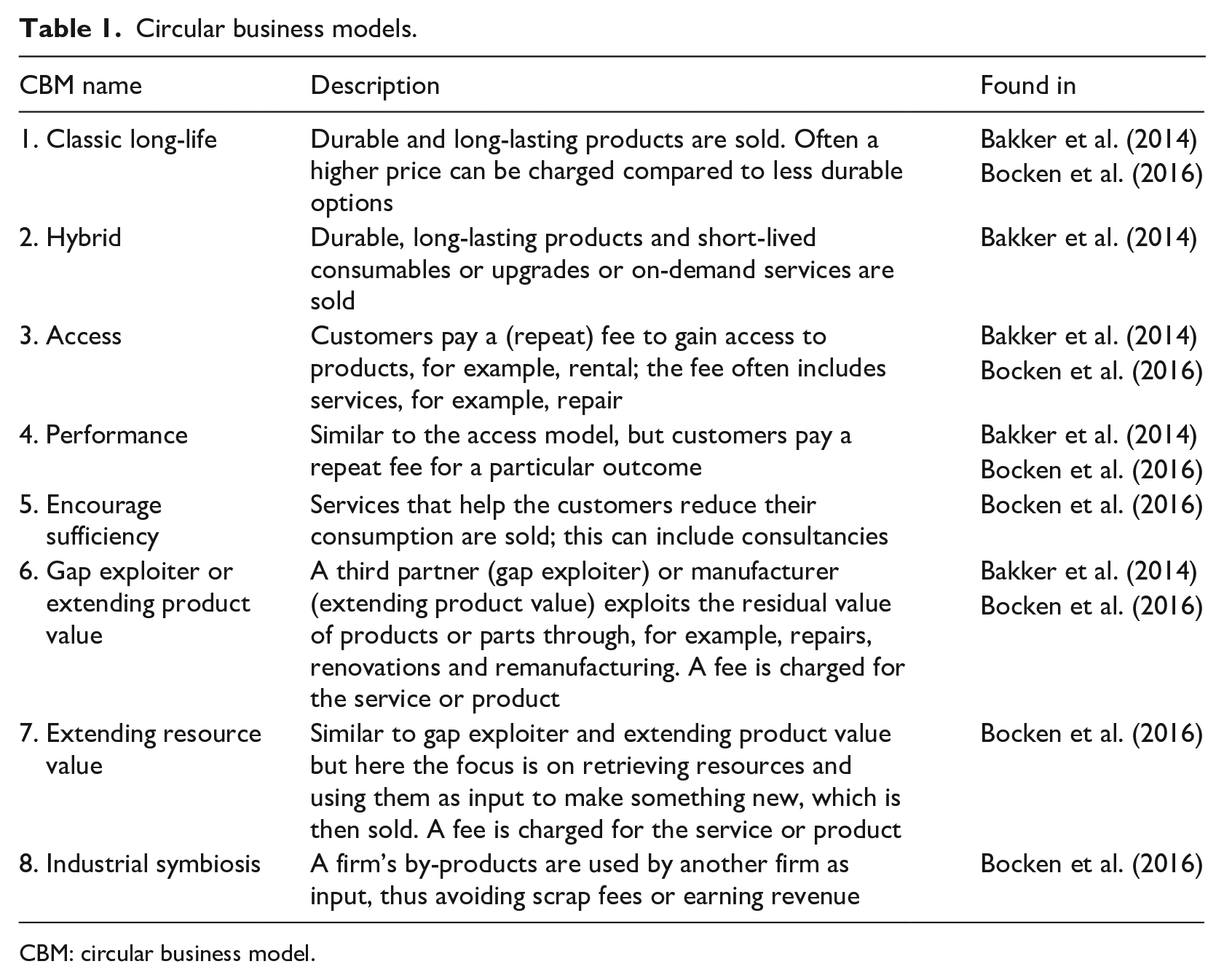

The focus of the expanding body of literature dealing with the implementation of a circular economy has fallen on individual firms as the driving force of economic activity because they design, manufacture, distribute, sell and deliver products and services (Lieder and Rashid, 2016). The concept of CBMs is new, first appearing in a single publication in 2006, then mentioned in 2012, before growing rapidly (Geissdoerfer et al., 2020). Here an adapted definition from Pieroni et al. (2019) is used, where CBMs allow firms to create, deliver and capture value in such a way that the value of resources is kept in the economy and used more efficiently and effectively. More central to our analysis, however, are the types of CBMs. Here the literature provides many typologies (Bocken et al., 2016; Lüdeke-Freund et al., 2019; Urbinati et al., 2017). The one employed here is an adaptation of two early versions; those by Bocken et al. (2016) and Bakker et al. (2014) presented in Table 1. These build upon the work of others; for instance, the access and performance models come from the product-service systems research field (Tukker and Tischner, 2006). They are chosen because they emphasise how firms actually generate income as opposed to, for example, Geissdoerfer et al.’s (2020) CBM typology of cycling, extending, intensifying and dematerialising, which focuses on resource flows, or Lüdeke-Freund et al.’s (2019) CBM patterns: repair, maintenance, reuse, redistribution, refurbishment, remanufacturing, recycling, cascading, repurposing and organic feedstock use, that emphasise measures implemented for products.

Circular business models.

CBM: circular business model.

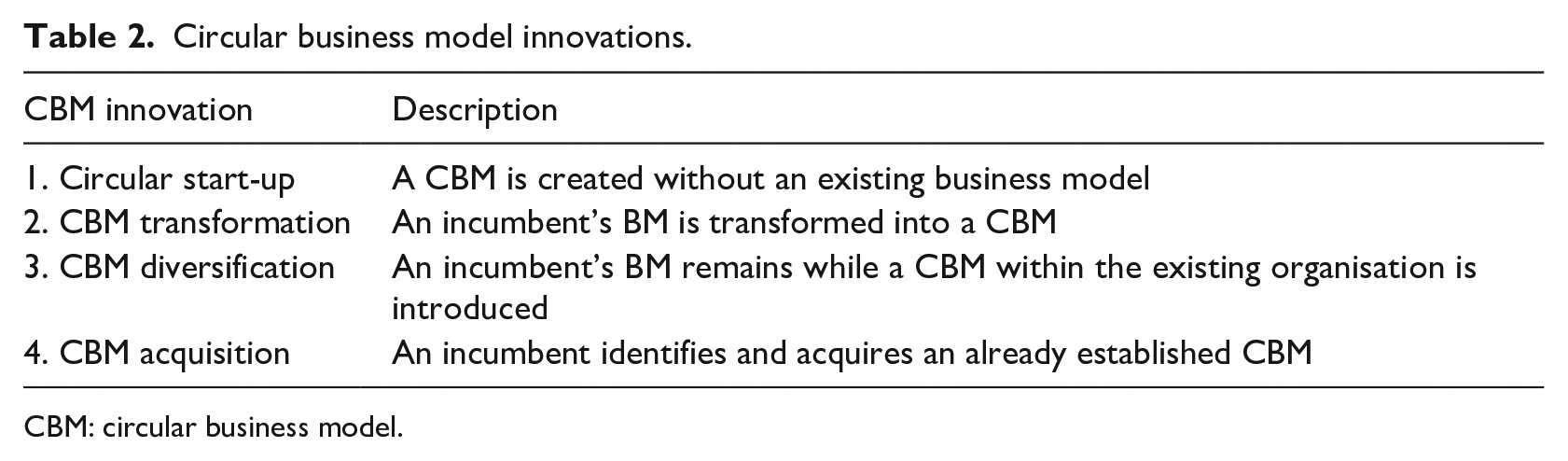

The process of conceptualising and implementing a CBM is referred to as CBM innovation (Geissdoerfer et al., 2020). There is less research on CBM innovation than for CBM, and thus, there are fewer typologies from which to choose. We use the most established one, a framework of four types of CBM innovations by Geissdoerfer et al. (2020) for the analysis, which is presented in Table 2. However, not all firms engage in CBM innovation. Consequently, when categorising the firms, there is also the possibility that some will continue with business as usual.

Circular business model innovations.

CBM: circular business model.

In this framework of CBM innovation types, there is a clear distinction between incumbents and start-ups. To achieve a more circular economy overall, existing firms engage in CBM innovation (Lieder and Rashid, 2016), although start-ups also have a crucial role to play (Henry et al., 2020). Literature beyond the circular economy field, that is, concerning entrepreneurship, innovation, business model development and so on has often stated that start-ups and incumbents have different preconditions and different success factors, drivers and barriers (Johnson and Lafley, 2010). For example, incumbents have existing investments, supply chains, business models and so on that are hard to change (Henderson and Clark, 1990; Hill and Rothaermel, 2003). Start-ups, however, are expected to have more freedom of action and adaptability (Christensen, 2013). They also run a lower risk of cannibalising the market share of their prior products or investments compared to established firms (Hockerts and Wüstenhagen, 2010). At the same time, however, they face their own set of challenges, including access to human, financial and resource capital and networks (van Gelderen et al., 2005). These issues concerning drivers and barriers are explored in the following section in the context of CBMs.

Organisational drivers and barriers for CBMs – start-ups versus incumbents

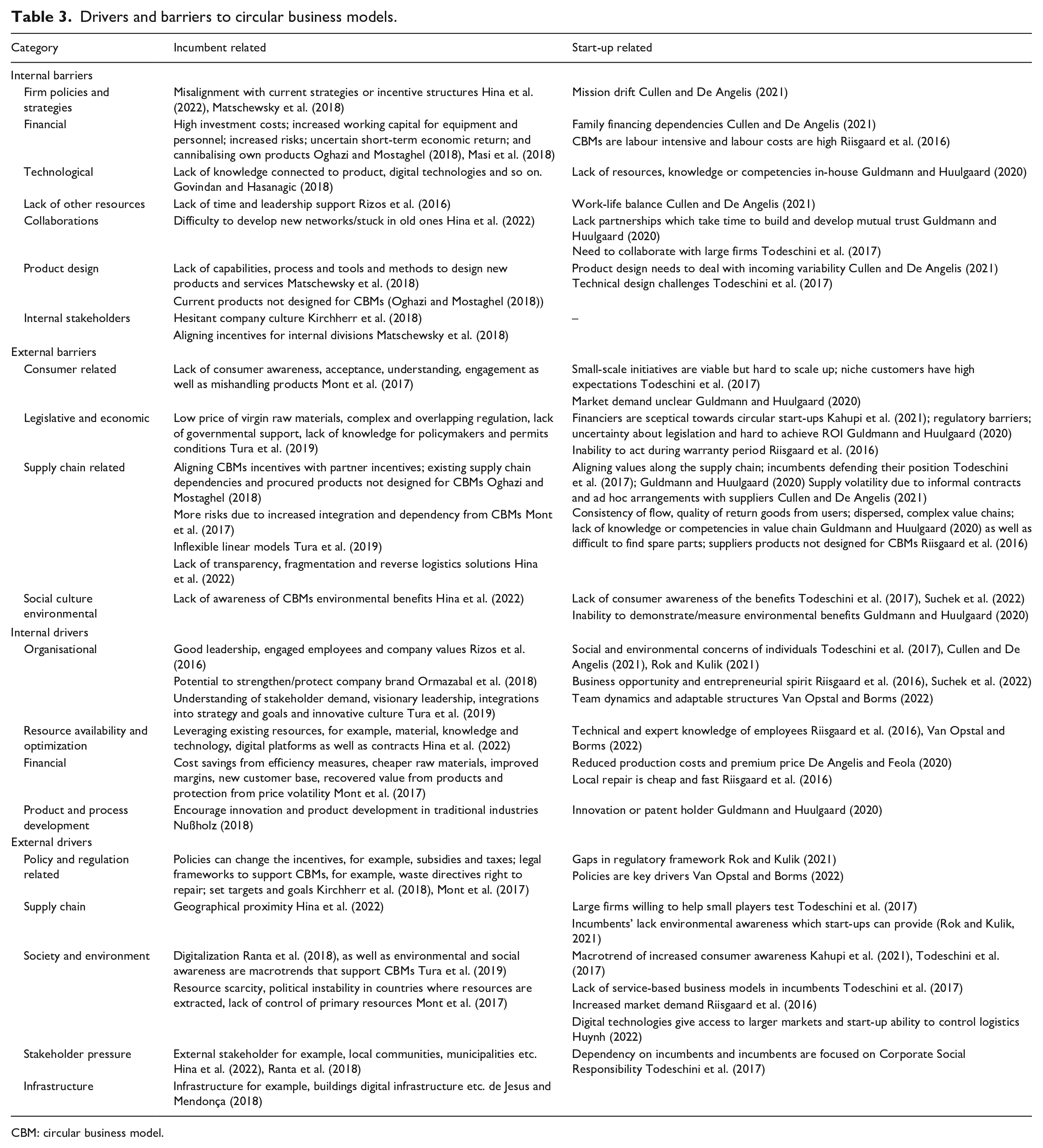

It is understood that firms implementing CBMs challenge current consumption patterns, established laws and policies for products, production and consumption and collective and individual mindsets (Kirchherr et al., 2018). Moreover, implementing them may require technologies not yet developed (Govindan and Hasanagic, 2018). Therefore, CBM implementation faces many barriers. However, there are also drivers such as environmentally minded employees, customer concerns about unsustainable consumption, increases in resource prices and difficulty of access to resources (Mont et al., 2017; Rizos et al., 2016). Many authors deal with firms implementing CBMs as a generic group, but research has shown that both drivers and barriers differ in relation to the type of business model (Mont et al., 2017), the size of the firm (Rizos et al., 2016), being an incumbent or a start-up (Henry et al., 2020), the institutional context of operation (Ranta et al., 2018) and the type of industry sector (Mehmood et al., 2021). Incumbents, and especially SMEs, have been the most researched (Tan et al., 2022) less is known about start-up drivers and barriers (Ferasso et al., 2020). There are many analyses of the drivers and barriers to a circular economy and to CBM, most of which are based on incumbents (Tan et al., 2022). To create a frame of reference for the analysis and discussion we use the categories of organisational drivers and barriers of CBMs from a recent review by Hina et al. (2022). The four categories are internal and external drivers and internal and external barriers, these are further divided into sub-categories, such as legislative, and are presented in Table 3. For each category some key points are raised both for incumbents and for start-ups.

CBM innovation is often challenging for incumbent firms. As can be seen in Table 3, they face more internal barriers and are to a large extent held back by their existing supply chains. In relation to this, Stewart and Niero (2018) found that incumbents do not change their business models but tend to extend their strategies to include, for example, recycling because it is easier to develop and commercialise new products and services within the existing model. Similarly, Antikainen and Valkokari (2016) find that it is start-ups rather than incumbents who are able to dismantle and re-design the value chains. They do not face the same risks of cannibalising their existing products or depreciating previous investments in manufacturing processes (Henry et al., 2020). This freedom that start-ups are envisioned to have is, nonetheless, constrained not only by limited resources such as networks, finance and knowledge (see organisational barriers in Table 3) but also by being dependent on incumbents that have more power and are interested in defending the existing system (De Clercq and Voronov, 2011).

Drivers and barriers to circular business models.

CBM: circular business model.

Individual drivers and barriers for CBMs – intrapreneur versus entrepreneur

Apart from covering the drivers and the barriers of the organisation, the role of the individuals involved such as, the intrapreneur in the case of an incumbent and the entrepreneur in the case of a start-up, is explored in terms of drivers and barriers. Hopkinson et al. (2018) stated that developing and maintaining successful CBMs requires the development of managerial competencies and capabilities. Bocken et al. (2018) concluded that individual business experimentation is an important capability that facilitates the transition to a CBM with limited risks and resources. Dynamic capabilities, in particular, can bridge and facilitate intrapreneurial capabilities (Klofsten et al. 2021). However, the individual’s role has been largely overlooked in the implementation of CBMs (Ferasso et al., 2020).

Entrepreneurs are central for solving complex and important sustainability problems that involve risk-taking and uncertainty because they can produce value from uncertainty (Hockerts and Wüstenhagen, 2010; Veleva and Bodkin, 2018). One of the main drivers for the circular entrepreneur is to transform a sector, system or market to improve the environmental performance by exploitation of business opportunities (Henry et al., 2021; Nhemachena and Murimbika, 2018). This can also be seen in the internal organisational drivers of start-ups in Table 3. Other drivers for an entrepreneur, noted in Table 3, are their entrepreneurial spirit, expert knowledge, and adaptability; they also face individual barriers such as mission drift, that is, drifting away from their original ideas or an inability to find a work-life balance (see Table 3). Although the extant claims that entrepreneurs are often driven by access to networks and partners who can secure funding (Light and Dana, 2013; Schoon and Duckworth, 2012), circular economy research found that these factors constitute barriers for circular entrepreneurs (Kahupi et al., 2021).

In comparison to the entrepreneur, the intrapreneur is defined as, ‘a person within a large corporation who takes direct responsibility for turning an idea into a profitable finished product through assertive risk-taking and innovation’ (American Heritage Dictionary, 2022). Intrapreneurs work with initiatives outside their working area and across the boundaries of organisational divisions (Pinchot, 1985). Therefore, an intrapreneur is basically introducing a new economic activity within the existing business model (Davidsson, 2004). Hopkinson et al. (2018) have emphasised that managerial competencies are crucial to successful CBMs but focused mainly on sustaining them. In general, little focus in the circular economy context has been on the intrapreneur with perhaps the exception of the industrial symbiosis field where a number of authors highlight the importance of industrial symbiosis champions (Walls and Paquin, 2015).

Entrepreneurs and intrapreneurs face different types of barriers, the former face barriers throughout the various stages of business development. In particular, challenges when it comes to securing financing (Wright and Stigliani, 2013) compared to intrapreneurs who have access to the established corporate resources. Conversely, intrapreneurs face organisational barriers, such as bureaucracy and rigid routines that hinder the formation of new ideas and opportunities (Engzell, 2023). Lastly, both have the fear of failure in common (Engzell, 2021; Shinnar et al., 2012). Although, individual drivers and barriers, just like organisational ones, could potentially also be further dived into internal and external ones, a framework was not found to support such a distinction which is somewhat expected since the individual’s role has been largely overlooked in circular economy (Ferasso et al., 2020).

Methodology

Research design

The focus of this research is on a contemporary real-life phenomenon, that is, CBM and drivers and barriers to CBM innovation. Therefore, exploring cases of this phenomenon is considered the best approach (Given, 2008). Moreover, information about this phenomenon is not documented, even though detailed descriptions and context are central to its understanding. Thus, a qualitative approach is preferred with data collected through interviews. Before initiating this research, the researchers gained a basic understanding of what the Swedish market for workwear looks like today, that is, actors and flows of materials. It became clear that the heterogeneity of actors on the market necessitated researching and comparing a variety of cases, as suggested by Eisenhardt (1989). The following sections describe how the data were collected and analysed.

Data collection

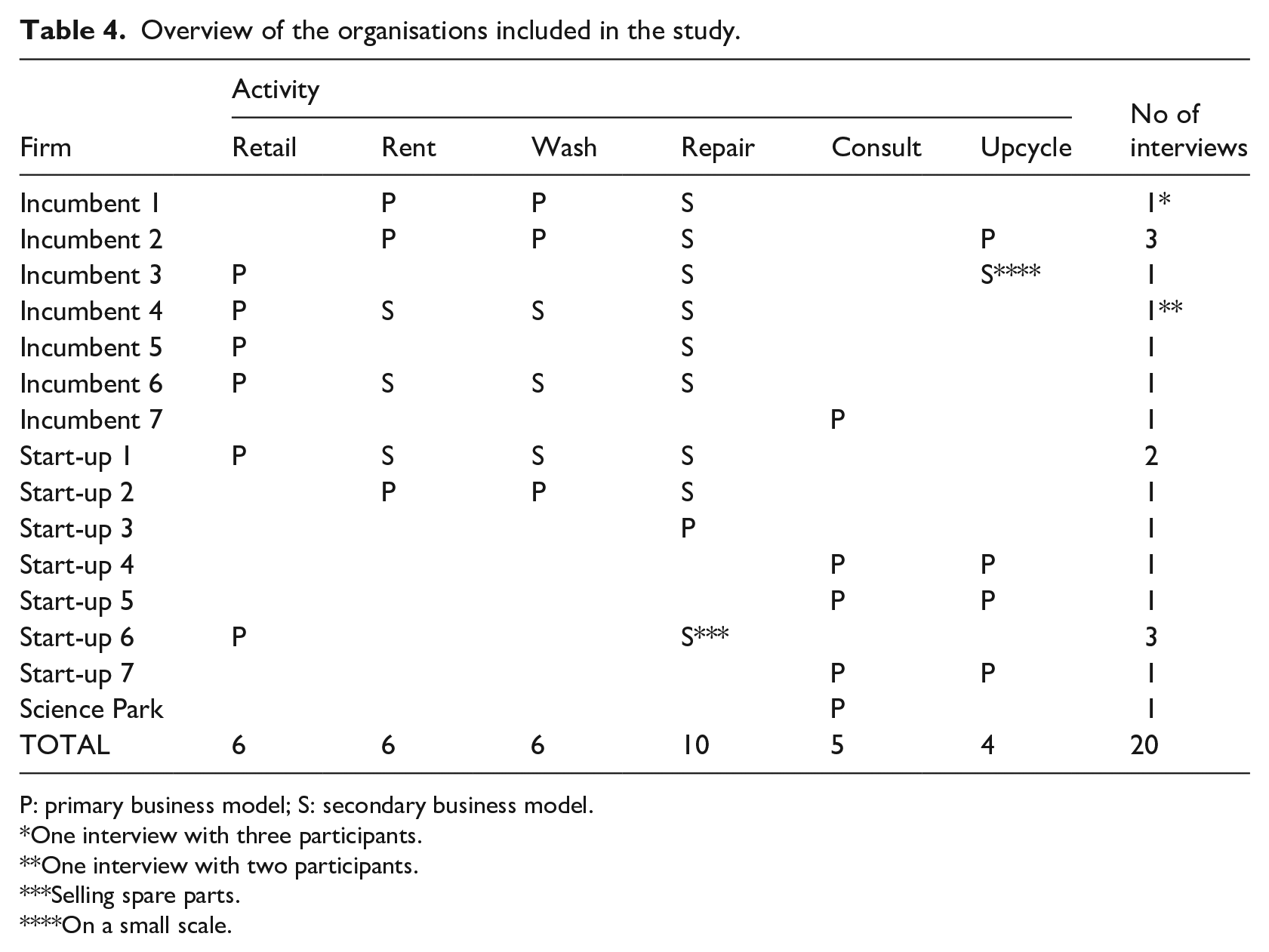

In total, 15 organisations representing different types of actors in the workwear industry in Sweden were studied. To select cases, a list of key incumbents on the Swedish market was compiled, including retailers, wash service providers and so on. This was achieved by searching the internet and commercial firm websites. A few firms from each type were approached and requested to provide an interview, with the aim of having an equal number of incumbent and start-up cases and a variety of types of incumbents. A different process for identifying circular start-ups had to be utilised because only one could be identified by searching the internet. Five were suggested by a Swedish Science Park which specialises in textile-related topics. Two more were added to the list by using the snowballing technique of asking respondents if they could suggest other start-ups. All the start-ups, except one, agreed to be interviewed making a sample of seven equal to that of the incumbents. One Science Park was included in the study, not as a case, but to add an overview perspective of the actors in the workwear industry. This is the previously mentioned Science Park; it was previously approached for an interview since it runs a project on increasing circular practices related to municipal workwear in Sweden. It also offers an innovative environment and meeting place for business, civil society, academia and public actors, which encourages co-creation and challenges established in business models and consumption patterns.

All the 14 case firms included in this study, as well as the Science Park, have pseudonyms since the firms are active on the same market and wanted to remain anonymous. However, an overview of their activities can be found in Table 4. In this table ‘Retail’ describes firms that design, brand and sell clothes and to some extent control the manufacture without necessarily performing it in-house. ‘Rental’ indicates firms that offer clothes on contract. ‘Wash’, ‘repair’ and ‘upcycle’ describes services that can be part of a contract or on-demand. ‘Consult’ indicates help to other organisations with design or procurement of workwear. The incumbents ranged from having several thousand employees to fewer than a hundred and the start-ups had one to three employees.

Overview of the organisations included in the study.

P: primary business model; S: secondary business model.

One interview with three participants.

One interview with two participants.

Selling spare parts.

On a small scale.

Interviews were requested from the start-up founder(s) and from the people involved in CBM development for the incumbents. For the incumbents, the sustainability department or front desk was sent the interview request, and they suggested relevant people to interview within the firm. At three interviews, more than one person participated, as indicated in Table 4, as there was more than one relevant respondent. Also, as indicated in Table 4, three people were interviewed more than once. A total of 20 semi-structured interviews were conducted during 2022, and 19 respondents participated from 14 firms and one Science Park.

Prior to the interviews, publicly available data were gathered to understand the key BM and offerings as well as sustainability and circular economy-related activities. An interview guide was developed with four parts. The first focused on understanding the interviewee’s role in the firm and his/her knowledge on circular economy. The second focused on understanding the current BM or CBM and the planned changes. The third focused on organisational drivers and barriers regarding the current BM or various activities or business models such as rental and repair. Finally, questions concerning the role of individuals in CBM were asked. The same interview guide was used with the Science Park respondents; they discussed drivers and barriers as third-party observers. Despite having an interview guide, the format was semi-structured to be able to react to whatever information the respondent provided to the initial question (Given, 2008: 470–472; Kvale, 1983). All the interviews were digital, using the software ‘Microsoft Teams’ for conducting, recording and transcribing, and the language was Swedish.

Data analysis

The authors followed a conventional stepwise approach to systematically analyse concepts and themes from the data (Miles and Huberman, 1994). The frame of reference was central to analysing the data. The first stage of the analysis was to categorise the various cases according to the different types of CBM and CBM innovation presented in Tables 1 and 2. This was done using both the publicly available information and interview data. Each author did this separately followed by a joint discussion to reach a final result. The second stage of analysis aimed at identifying organisational and individual drivers and barriers from the interview data. The frame of reference for this activity is provided in Table 3. As explained in the section ‘Frame of reference’, the top-level categories of drivers and barriers to CBM come from a recent review by Hina et al. (2022). Both the categories and the details of the drivers and barriers guided the researchers when reducing the interview data. The first author did the initial identification, and the second reviewed it; any misalignments were discussed, and then the data were revisited and agreed upon. The third stage was a comparative analysis between start-ups and incumbents to identify differences and similarities in business models and drivers and barriers to CBM on both the organisational and individual level. Finally, the authors tried to identify, using the frame of reference, which of these drivers and barriers characterise the workwear industry as a whole and which are generic to CBMs. The two final stages combined both independent and collective analysis by the researchers to strengthen the authenticity and trustworthiness of the study’s findings as suggested by Guba and Lincoln (1994).

Methodological limitations

The risk that qualitative research can have sample selection bias and respondents give desirable responses cannot be removed but can be reduced (Bergen and Labonté, 2020; Denzin and Lincoln, 2011). This can be especially true when discussing internal drivers and barriers that some respondents might consider sensitive. Moreover, researcher values can also influence the analysis (Given, 2008: 60). To mitigate these biases, we selected cases as representative as possible of both incumbents and start-ups. Moreover, when it was possible, several employees at the same organisation were interviewed to explore different aspects of their experienced barriers and drivers (Auerbach and Silverstein, 2003). When it was not possible to have multi-informants, we tried to select the most suitable representative. During the interviews, we asked direct and indirect follow-up questions about the drivers and barriers to nuance the answers and ensure the validity and reliability of the findings. Finally, both researchers were involved in the analysis to gain a plurality of perspectives. Despite these precautions, there may be more aspects of drivers and barriers in the workwear industry than explored in this article, not least because this study is limited to data collection in one country.

Results and analysis

The main results and analysis are presented in the following sections.

CBMs in the workwear industry

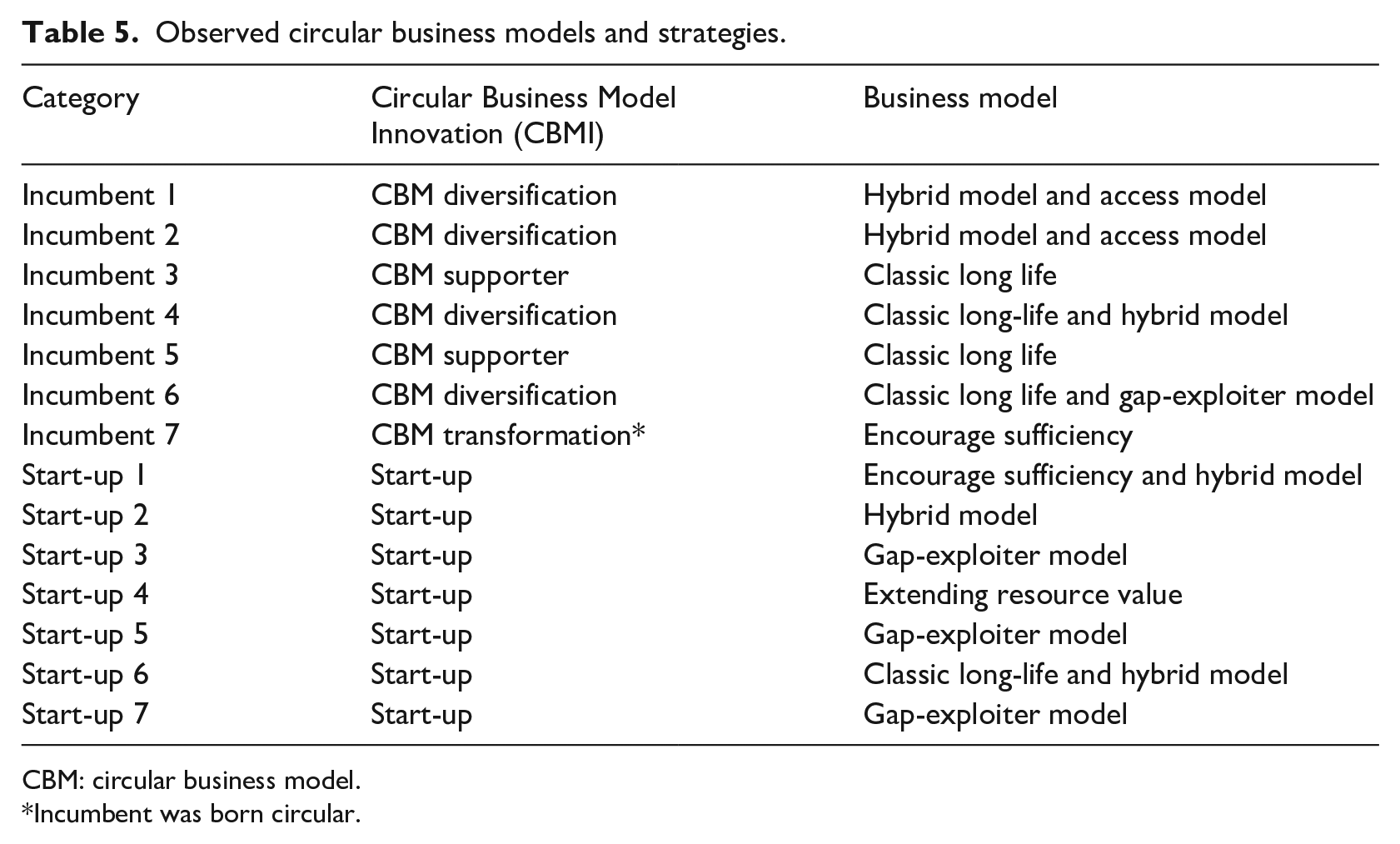

The results presented in Table 5 show the types of CBMs for incumbents and start-ups. All the organisations claimed that they contribute in some way to the circularity of workwear. However, the effort invested in circular activities varied greatly.

Observed circular business models and strategies.

CBM: circular business model.

Incumbent was born circular.

Incumbents 1 and 2 are large firms with CBM diversification, implementing hybrid or access models. They are suppliers of workwear rental and washing services for hotels, restaurants, healthcare providers, industries and so on, and are large players in the Swedish workwear market. Both engage in environmental and sustainability initiatives with set goals as well as implementation and monitoring routines, for instance, energy efficiency and sustainable fibres procurement. Principally, Incumbents 1, 2 and 4 stated that they actively work at all levels to reduce unnecessary production as well as to amplify waste management and textile recycling. Incumbents 3, 4, 5 and 6 are retailers or own brand manufacturers of professional clothing, shoes and gloves. All four stated that they produce durable clothes according to the classic long-life model and thus, contribute to a circular economy. It is important to note that without a standardised way of measuring durability, this becomes a matter of personal perception. Incumbents 3 and 5 also mentioned that they support the CBMs of other firms by providing durable clothing that withstands many washes and is used by Incumbents 1 and 2 in their access and hybrid models. The CBM typology presented in Table 1 does not cover this type of supporting role in the circular value chains that we identified. However, recent work by Kanda et al. (2021) has argued that the boundaries of a business model should be wider than the perspective of a single firm, and that circulating resources is usually made possible by a business ecosystem. Kaipainen et al. (2022) also emphasise the importance of circular supply chains. Thus, we categorise these firms as CBM supporters, which we define as a firm that does not implement a CBM but is part of an ecosystem that supports another firm implementing it.

Incumbent 4 offers small-scale washing services (hybrid). As one employee noted: ‘The laundry concept is a service and an alternative to the customers who want laundry and repair without being forced into a rental system. It is used by a very small proportion of our customers and is not something that the firm is heading towards’. This signifies their current intention not to scale up the CBM. Similarly, many incumbents offer small-scale repairs or have initiated pilot projects with upcycling and material recycling but have not yet made larger business model changes in this direction. Nevertheless, Incumbent 6 stated its intention to take a more serious step towards a gap-exploiter or resource value extension model. Incumbent 7 is different from the rest of the Incumbents as it is an SME and was born circular. It provides consultancy services and helps large firms in the procurement of workwear so that they can select durable and appropriate clothing, thus implementing an encourage sufficiency model.

Start-ups 1 and 2 are mainly resellers of the incumbent’s workwear and provide small-scale repair and washing services (hybrid model); they both encourage sufficiency, with Start-up 1 using it as a primary customer value in their business model by helping customers choose the correct size of clothing. Incorrect sizing increases wear and, therefore, reduces the lifespan of workwear. Start-up 3 is exclusively working with repair services, such as sewing, relining and so on, and has a pure gap-exploiter model. Start-up 4 offers consultancy, but the main vision is to commercialise a technology for separating textile fibre, that is, pre-processing for recycling and thus implementing the extending resource value model. Start-ups 5 and 7 are quite similar. They create new clothes from textile waste through upcycling and design (gap-exploiter model). Start-up 6 differs substantially from the other start-ups because it is not only a retailer, but also designs its own brand of durable modular workwear. This means it sells replacements for the workwear sections that get worn down fastest and has pockets that can be removed to facilitate washing (classic long-life and hybrid model).

In summary, large retailers and own brand manufacturers (Incumbents 3, 4, 5 and 6) are implementing pilot projects and small-scale diversification of the linear business model, for instance, repairs. They want to explore and test ideas that add value to their existing business model but that are not too risky or expensive to implement. One successful pilot project is mentioned by Incumbent 3 that collaborated with a local firm to take apart and reuse fibre for new workwear. Another example, described by Incumbent 6, is the redesigning of a chef’s jacket to become a skirt. There are many examples of successful pilot projects that have been considered and tested by incumbents, which lie beyond the scope of this study, but the majority have not been implemented on a larger scale. In relation to this, the Science Park stated that ‘it might be easier to improve the value chain than change it completely’, and that the incumbents have their existing logistics or digital systems, which are obstacles for implementing circular activities.

The washing service providers (Incumbents 1 and 2) implement access and performance models successfully, for which there is a growing demand. It is, however, unknown to what extent these CBMs reduce resource use as there is a lack of published research on this topic. Incumbent 7 is an interesting exception as it fulfils a different role on the market by helping large firms and public procurers who lack textile knowledge to procure appropriate clothing according to their needs. Yet, start-ups implement more ambitious initiatives, and most have some innovative elements. Four of the seven utilise gap-exploiter and resource value extension models to prolong the lifetime of workwear or the material it comprises. Two are more classic resellers with hybrid services, but both have textile knowledge to encourage sufficiency, similar to Incumbent 7. Finally, apart from Start-up 6 none of the start-ups make their own clothing but use that from large manufacturers. This shows that start-ups are more active later in the process. Start-up 6 produces its own clothes and focuses on durable modular products whose lifetime can be prolonged through spare parts. In general, both incumbents and start-ups state that they are aware of CBMs and are willing to make changes, but as the Science Park interviewee reflected ‘they might not always know what the right way is’.

Organisational drivers and barriers for CBMs in the workwear industry

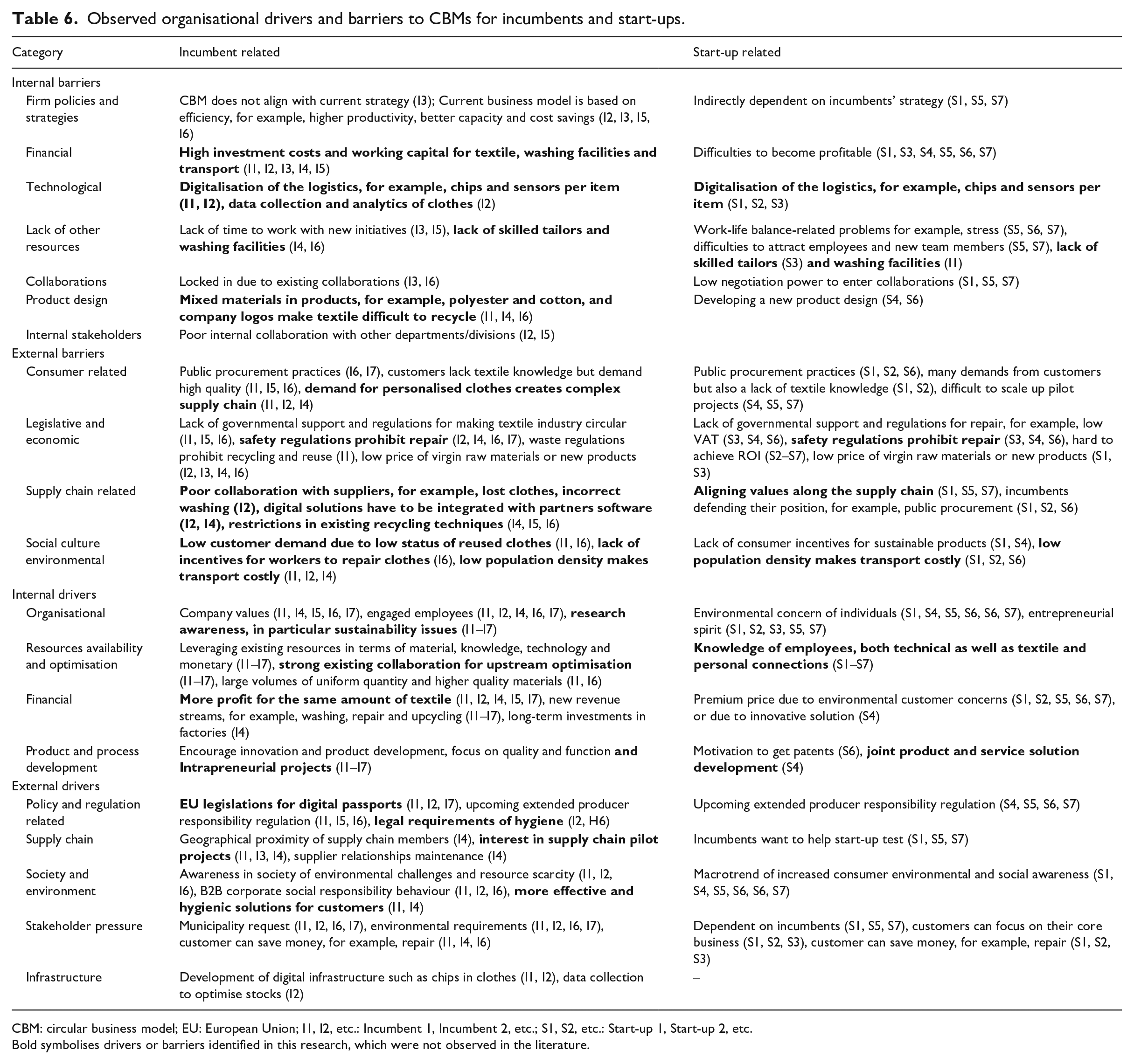

The results presented in Table 6 show the internal and external organisational drivers and barriers identified for the incumbents and start-ups, and some key points are further elaborated in this section.

Observed organisational drivers and barriers to CBMs for incumbents and start-ups.

CBM: circular business model; EU: European Union; I1, I2, etc.: Incumbent 1, Incumbent 2, etc.; S1, S2, etc.: Start-up 1, Start-up 2, etc.

Bold symbolises drivers or barriers identified in this research, which were not observed in the literature.

All the firms, regardless of their size, are driven by customer needs and demands. Following the overall trend in Sweden of assigning significant importance to environmental protection, customers are also increasingly interested in the environmental performance of their workwear. This is one of the main external drivers that all firms discussed. However, this increased awareness does not always translate into a demand for more circular solutions; this is because of the low cost of new clothes according to the case companies, but also for other reasons discussed below. There is also a lack of policies to nudge the whole workwear industry in that direction; however, upcoming European Union (EU) policies are expected to be influential. Some firms even mentioned that current regulations limit how actors can handle discarded textiles, classified as waste, even though there is potential for them to be used for longer.

Looking at the two groups separately, incumbents are traditionally driven by selling large volumes based on efficient process so they can provide a competitive price to quality ratio. This is because a main objective is to win public procurements, or large customer contracts. These typically last 3–4 years, are based on either sale or rental and potentially, include additional services such as washing and repair. These organisations have historically had a strong price focus and purchasing power because they form a large part of the market. However, the Science Park stated that ‘we are at the beginning of innovative procurement’, which shifts the focus from prioritising low cost alternatives to including other aspects such as repair, reuse and recycling. This is still at an early stage, as illustrated by several respondents, for instance, Incumbent 1 stated that: ‘Customers want the cheapest price most of the time but other perspectives such as the environment are coming in more and more’. Another driver for access and hybrid business models is the cost savings for customers; as Incumbent 1 said, ‘It is many times actually more cost-effective to rent clothes than to buy’. Others mentioned that repair could prolong the life and slightly reduce costs, although safety must not be compromised. Other drivers are also identified such as the incumbent’s sustainability-related values and goals. Incumbents also have many existing relationships, knowledge and infrastructure that they can leverage towards CBMs. One example is the technology development, such as chips put in clothes by Incumbents 1 and 2, which could analyse usage and match the workwear with the right customer. Another example is long-term customer relationships that generate opportunities for joint product development and customisation.

However, the existing systems also act as a key barrier for incumbents to implement CBMs by locking them in, for instance, to business models, investments, contracts and partnerships. Other barriers to meeting their circular economy ambitions are a lack of collaboration between departments, finding skilled workers like tailors and capabilities and knowledge connected to textile recycling and upcycling. One interviewee said: ‘The challenge is to coordinate people from different divisions and also to work cross functionally and interact’ (Incumbent 2). They mention the complexity of their product and service offerings, and that customers have high expectations on design, functionality and newness often coupled with little textile knowledge. For example, in the construction industry workers expect personalised workwear and do not accept a sharing solution, as in the health sector. This leads to an organisational challenge not only of creating a digital tracking system per item but also of ensuring that it integrates with all the local supply chain partner systems. Another example is that ‘second-hand’ or ‘repurposed’ clothes signify low-quality and low status to some users so, requiring efforts from the incumbents to educate and work against preconceptions. Furthermore, these actions must be profitable.

In contrast, start-ups are born circular. They share a strong drive to reduce environmental impacts. For example, Start-ups 5 and 7 are driven to reduce textile waste through upcycling and design. Start-up profitability is also a common driver. To achieve this profitability, some are charging premium prices, while others are targeting customer cost savings through, for example, repair. Some start-ups are also driven by creativity and a wish to challenge the status quo. For example, Start-up 4 founder said, ‘Everything works today in the workwear industry, should we be there to disrupt with a new system solution? – yes, we can supply a circular workwear system’. Another start-up has the desire to sell workwear through a new logistics channel (Start-up 1) and a third wants to sell innovative consultancy services, such as material expertise (Start-up 4). These activities are both business opportunities that incumbents have not acted upon, or activities in collaboration with incumbents, such as recycling pilot projects.

Start-ups, however, because face several internal and external barriers to implementing CBMs. A key barrier is the profitability aspect. Although one entrepreneur said: ‘I had starting capital myself since I sold partnership in a previous firm’ (Start-up 1), the rest had difficulty in accessing capital and making it over the breakeven threshold. They are faced with the challenge of developing a novel value proposition and putting a price on it. For example, the Start-up 4 stated that ‘Our challenge is finding a technical solution that works in practice. Then package and present it for customers and then also charge a price for this’. However, some barriers were company-specific, as indicated in the former quote, where only Start-up 4 faced technical challenges. Also, in a market dominated by large customers it is hard for start-ups to compete especially regarding public procurement. As written earlier, large incumbents have better preconditions because of their large volumes of clothing, established relationships, logistics solutions, and so on, while start-ups have small-scale production and need to build new relationships and find logistics partners. This results in start-ups that attract customers that are smaller and often located closer geographically, as well as having difficulty to scale up pilot projects. As the entrepreneur from Start-up 2 explained, the complexity of finding external partners to support growth, significantly contributed to his decision not to become a national supplier. Several start-ups mentioned the dependency on incumbents for their core business idea, for example, getting access to the incumbents’ products, materials and waste. Apart from external partners, start-ups also have challenges finding partners or employees; as one entrepreneur said, ‘When we become two in the firm, we can speed up at a new level’ (Start-up 5).

In general, both incumbents and start-ups in the workwear industry are facing the same changes of laws and policies aiming to reform the textile industry, because it is one of the most polluting and resource-intensive industries in the world. This generates a general debate in the industry for both incumbents and start-ups on how to adjust their businesses to the current and future requirements. As one start-up expressed, ‘The EU legislation will be important, but the industry does not know where to start. . .’ (Start-up 4). This illustrates the importance of policy and the complexity of implementing change.

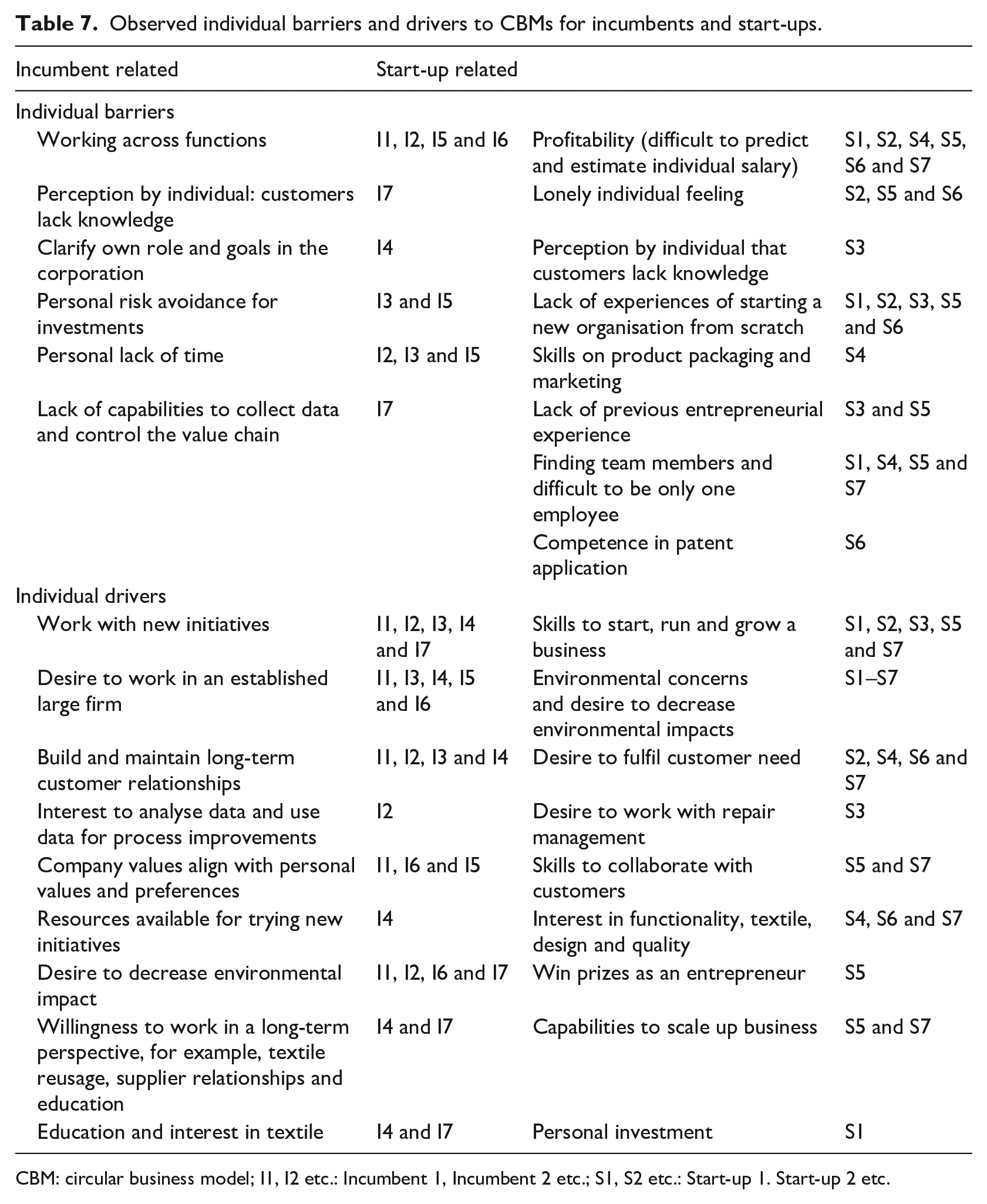

Individual drivers and barriers for CBMs in the workwear industry

The results presented in Table 7 show the drivers and barriers to implementing CBMs for the individuals involved, including, the intrapreneur in the case of an incumbent and the entrepreneur in the case of a start-up. In general, all respondents referred to their customer focus as a driver, noting fulfilling customer needs, customer co-design and close long-term relationships. Also, many referred to their personal environmental concerns as individual drivers. Many employees, as incumbents, expressed their interest in starting initiatives outside their current working area as well as in experimenting within the established company. However, not all employees who worked on a new initiative can be classified as intrapreneurs. According to the intrapreneur definition used in this article, we identified four intrapreneurs that had environmental incentives to start projects within or outside their current working area. The respondent at Incumbent 2 expressed the following personal driver towards starting a new project: ‘I want to find a clever way to figure it out and build something that’s quicker and faster and saves time for people’. This project targeted a new customer segment by combining existing tools, data and logistics in a new way. This person worked with this project outside his current working area and had to convince colleagues that it would be profitable. After implementation, it proved successful. Individuals mentioned a lack of time to work with new initiatives and the personal risk avoidance connected to investing effort into uncertain projects. Four individuals mentioned the challenge of working across departments due to somewhat rigid organisational structures. According to the employee in Incumbent 2: ‘the different functions work independently from each other without many interactions at the lower level’. This resulted in collaboration challenges in the project.

Observed individual barriers and drivers to CBMs for incumbents and start-ups.

CBM: circular business model; I1, I2 etc.: Incumbent 1, Incumbent 2 etc.; S1, S2 etc.: Start-up 1. Start-up 2 etc.

For start-ups, their main personal driver was to start, run and grow their own business. All founders directly or indirectly stated that they wanted to be ‘their own boss’. They also had a common interest in challenging the system, as well as environmental concerns such as, global warming and waste reduction. Previous experiences from working in the textile industry in combination with an interest in new product development and design, are driving them in their daily work to focus on customer needs and develop new solutions. In general, entrepreneurs want to design, develop and customise their products. Almost all entrepreneurs have a common desire to scale up and become profitable but struggle to predict their individual salary. Some of the respondents also raised the challenge of being alone and having to perform all the different functions as well as the difficulties of finding new team members with the desired skills and competencies. One start-up founder mentioned competence in patent applications as crucial. He wanted to bring the new solution as quickly as possible to the market and had to simultaneously develop the skills and competencies that are needed for a patent application.

Discussion

CBMs in the workwear industry

Most of the incumbents interviewed offer either classic long-life models with some hybrid features such as repair, or access models. They are suppliers of workwear through sale or rental for hotels, construction, restaurants, healthcare providers, industries and so on. Consequently, their CBMs centre around producing durable clothes, according to the classic long-life model, or diversifying their current BM by adding services such as repair and washing or offering the workwear as a service. All have in common the desire to contribute to a circular economy. Although large incumbents have the power to lead change to CBM in the workwear industry, our analysis suggests that they might not exercise it, but instead they find it is easier to develop and commercialise new products and services within the existing model rather than shifting towards implementing a CBM innovation. This is in line with recent findings by Guldmann and Huulgaard (2020).

A few of the incumbents that offer the classic long-life models can be defined as CBM supporters. These because they support other firms by providing long-lasting clothes but are not central to the CBM implementation. This highlights the importance of exploring constellations of actors that make CBMs possible (Kanda et al., 2021; Kaipainen et al., 2022) and calls for further research on issues of centrality, ecosystems and supporting roles in a circular economy. In general, we concluded that incumbents are more active upstream in relation to the customer, although they do have various upcycling and recycling projects. Overall, incumbents are making small-scale changes to their BMs compared to start-ups that do not yet have an established model. This finding confirms the extant literature that claims that when a business model is established it is difficult to change and a shift requires changes in the whole business logic (Henderson and Clark, 1990).

We also identified several circular start-ups bringing a larger variety of CBMs to the market, although the most common were gap-exploiter and hybrid models. As observed by Guldmann and Huulgaard (2020), start-ups are in general more ambitious in their implementation, offering consultancy services and other innovative elements. Their circular activities vary, from upcycling durable clothes produced by large manufacturers to designing and creating modular new clothes where sections can be replaced. None of the start-ups make their own clothes and some are, therefore, dependent on incumbents’ products. Similar to Todeschini et al. (2017), we find that this dependency creates certain preconditions to their offers, such as the quality and design in the workwear. The majority of the start-ups are more active downstream rather than upstream in relation to the customer. Many start-ups offer innovative consultancy and other customised services based on a deep knowledge of textile and workwear as a unique selling point.

Organisational drivers and barriers for CBMs in the workwear industry

This article adds to the existing body of literature on the drivers and barriers for both incumbents, for instance, existing firms, including SMEs and large firms that already have a product or service on the market, and new ventures.

A detailed description of the drivers and barriers is presented in section ‘Organisational drivers and barriers for CBMs in the workwear industry’ and Table 6. Three factors that affect the drivers and barriers of a firm when implementing CBM were be identified in this study. These are the type of industry, the type of firm, that is incumbent or start-up, and the type of business model. Some drivers and barriers are found to be common for all the firms in the industry. Key topics are current public procurement practices, customer environmental concerns, the upcoming extended producer responsibility regulation or the low cost for new workwear. However, even here some differentiation was obvious as, for example, incumbents spoke more about the EU legislation for digital passports than the start-ups. These common drivers and barriers for the whole industry were mainly external. By comparing these common drivers and barriers to the literature reviewed in Table 3, we see that these differ from other industries, for example, Mehmood et al. (2021) and Agyemang et al. (2019) do not identify public procurement as a key issue in the agri-food industry and automobile industry, respectively. Thus, we conclude that the type of industry influences the type of barriers and drivers that firms face. This also exemplifies the limitations in terms of generalisability of this study to other industries.

Incumbents and start-ups are also found to have their own set of common drivers and barriers. Incumbents have more internal barriers due to their existing process and structures compared to start-ups. On the other hand, start-ups face less internal barriers and more external ones, including difficulty in finding partners and accessing financing as well as low negotiating power. These findings are in line with other studies by Antikainen and Valkokari (2016) and Henry et al. (2020) that find that start-ups are not constrained by their existing structures. Worth mentioning is that a few start-ups collaborate with incumbents on projects that are often similar to their business ideas. This results in an indirect dependency on the incumbent’s strategy by selling their products, which creates a potential lock in effect for start-ups. Thus, the dependency on incumbents can be seen as an internal barrier for start-ups and has also been mentioned by Todeschini et al. (2017). This confirms the initial argument behind this research: that incumbents and start-ups face somewhat different drivers and barriers, and that more research on these two in the context of a circular economy as separate entities is needed. Finally, as noted (Mont et al., 2017; Vermunt et al., 2019), several drivers and barriers are related to the type of CBM. For example, logistics challenges and digitalisation were more relevant to firms providing hybrid and access models, whereas the difficulty of removing a company logo from the textile was more relevant to gap-exploiters.

These factors are not a comprehensive list of issues that can influence drivers and barriers; rather, they are those it was possible to observe in this study; further research is needed to confirm them and extend the list. The socio-economic context could potentially be an additional factor because, for example, the importance of public procurement can vary between different countries depending on the level of privatisation. Moreover, the identified drivers and barriers concern intended consequences and are limited by the perspective and knowledge of the respondents (Guzzo et al., 2023).

Individual drivers and barriers for CBMs in the workwear industry

This article has shown that the individuals involved in CBMS, such as the entrepreneur in the case of a start-up or the intrapreneur in the case of an incumbent, face their own barriers and drivers. The role of the individual has been somewhat overlooked in circular economy literature (Hopkinson et al., 2018) as has how individual factors interact with organisational culture to influence the adoption of CBMs (Tura et al., 2019), with the exception of the industrial symbiosis field (Walls and Paquin, 2015). However, our research demonstrates the importance of researching the individual’s perspective as they are key to CBM success. This is demonstrated by our finding that individuals were more forthcoming in the interviews when describing their drivers rather than their barriers. This could potentially be due to social desirability bias and therefore, using other data collection methods in future research such as surveys with forced choice items or randomised response technique is advisable (Nederhof, 1985).

A key finding is that individuals in incumbents, defined as intrapreneurs are driven by working within new initiatives, environmental concerns and have the support of a large firm. These initiatives are sometimes outside their working area and relate to improvements in existing business activities. If these intrapreneurs are not supported by the corporate culture and their managers and also not offered satisfying working conditions, they underperform or leave and commercialise their ideas themselves. This is confirmed by previous research (Engzell, 2021; Engzell, 2023) and exemplified by one respondent who left a large company and became an entrepreneur. Barriers raised by the individuals in incumbents were the lack of time to work with new circular initiatives but also risk avoidance in terms of investing resources into something uncertain. In this study, we identified four intrapreneurs. It was difficult to distinguish between the intrapreneurs who were self-driven and those who were assigned an intrapreneurial task from a manager. Therefore, there is no distinction in our study between the drivers and barriers for each of these two groups. Hence, further research is needed to better understand the differences between self-driven and designated intrapreneurs in the circular economy context.

Entrepreneurs are generally driven by starting their own business and working within their respective field of interest, that is, textile, design, quality or technical solutions. Some are also driven by establishing new collaborations, in some cases with incumbents, to scale up their businesses. All our circular entrepreneurs were driven by environmental concerns. Our findings confirm previous research, in that experimentation and eagerness to learn and adjust, as well as finding new collaborations, facilitate the transition to a CBM with limited risks and resources (Bocken et al., 2018). Almost all entrepreneurs talked about their desire to scale up and become profitable, but it was difficult on the individual level to predict and estimate the salary and find new team members with the right competencies for the development of the new organisation. Many of the barriers and drivers identified for the circular start-ups align with extant literature on generic start-ups, as presented in the frame of reference, and not unique to circular ones or the workwear industry specifically. Individual drivers and barriers for start-ups were mostly found to be the same as the organisational ones because the start-ups consist of the entrepreneur and possibly a limited number of other people, making the distinction difficult.

In summary, although the importance of the individual for successful CBM innovation is highlighted for both incumbents and start-ups in this research, this is an underexplored research topic requiring further attention from scholars from various disciplines. These may span, for example, management, innovation, organisational psychology, psychology and environmental management, and using various data collection and analysis methods. Moreover, studies in a variety of industries are needed.

Sector-specific CBMs knowledge for the workwear industry

When considering CBMs in our research, it is the variety in the workwear industry that is emphasised. There are different sizes and types of customers and providers, and different types of workwear, such as construction or healthcare clothes. There is also variety in ownership, for instance, with some workwear bought outright and owned and sometimes rented or leased by the customer. Also, workwear ranges from standardised to personalised clothes with chips or sensors. Thus, although some similarities exist in CBM drivers and barriers for firms in the workwear industry, there are also many differences. However, we also noted that the public procurement practices characterise the workwear industry with many public procurers with agreements that normally last over a long time, for example, 3–4 years. Therefore, we are in agreement with Huulgaard et al. (2022) and Rainville (2021) that influencing public procurement is central to driving demand for circular solutions in this industry.

The workwear industry has, however, an advantage over fast fashion because clothes are more expensive resulting in somewhat higher incentives to repair. Also, given the higher incidence of uniformity of materials used in workwear, large firms may be able to send large batches of workwear for repair, upcycle or recycle and thus minimise their transaction costs such as, transportation and administration and create economies of scale. However, the presence of mixed materials in workwear and logos on clothes can make various reuse and recycling processes difficult. Nor do these economies of scale easily apply to the many smaller firms, such as a small firm of electricians. Workwear in some industrial sectors still suffers from an individual’s priority to own, and many of our respondents were only positive towards rental, wash and repair if personalised clothes are guaranteed. This requires that firms closely monitor and digitalise their logistics chains, which is a key cost driver.

Concerning environmental benefits, incumbents cautioned against reaching the conclusion that CBMs reduce resource use. For example, in access models the number of changes of clothing per person and frequency of washing might significantly increase resource use (Incumbent 2). This challenge has been brought up multiple times by other authors in the context of access models in a circular economy (Kjaer et al., 2018; Zink and Geyer, 2017). Our conclusion is that the actors in the workwear industry must take a lifecycle perspective and consider both the production and distribution of textiles as well as overconsumption and recycling. As Braun et al. (2021) concluded, reducing our overall textile consumption is the best option from an environmental perspective. Moreover, a circular economy is not a substitute for the broader sustainable development goals that exist (Geissdoerfer et al., 2017) and therefore, both should be pursued. Firms and governments, therefore, need to ensure that access to CBM and benefits from a circular economy are distributed equitably.

Our findings from the workwear industry confirm the general trend that firms are implementing CBMs, but progress is slow (Urbinati et al., 2017). The workwear industry is still far from being an industry built on circular economy principles. It is characterised by the unsustainable consumption patterns of new textiles and the lack of incentives for reuse, but also the absence of supporting policies and regulations. There seems to be a large potential to further reduce resource consumption in the industry. The upcoming producer responsibility regulations in 2025 may lead to change. The absence of guidelines for sustainable materials in textiles also creates uncertainty in the industry. Our findings conclude that the industry needs dynamic and innovative agreements for procurement that take into consideration, for example, the quality of textile, reusage of workwear and recycling of waste and materials. Both incumbents and start-ups are capable of influencing and changing existing practice.

Managerial implications

For firms, this article suggests that the starting point of implementing CBM should be the analysis of customer needs and what value the firm can provide for the customer in relation to the existing business model. The awareness of environmental challenges is increasing in society providing new business opportunities for both incumbents and start-ups. This article shows many additional ways to provide customer value in the workwear industry, such as rental services, washing service and repair services. Providing consultancy services and supporting customers with textile knowledge were also shown to add value and at the same time reduce the amount of textile in the long term.

The profitability aspect of circular activities for start-ups is found to be a main barrier. Thus, start-ups are recommended to initially focus on securing funding, or collaborating, with those incumbents that have established revenue streams. More collaboration among actors in an ecosystem can also generate knowledge, competence and resource sharing opportunities which are especially important for start-ups. Our contribution confirms the research by Kanda et al., 2021 that there is a need to shift from our understanding of CBMs to circular ecosystems. Through collaboration, knowledge and resource sharing, incumbents and start-ups can take advantage of their drivers and overcome their barriers and work together in an ecosystem, where ensuring the positive impact on resource consumption is the main priority. There is also need for firms to move beyond small-scale changes to their existing BM.

Our findings indicate that a culture of encouraging intrapreneurial initiatives such as pilot projects introduced by Incumbents 2, 3 and 4, are desirable and beneficial for implementing CBM activities. Although such pilot projects may be desirable for innovation, they also pave the way for other employees and circular initiatives within the firm. Therefore, to effectively support intrapreneurial initiatives, supporting role models that drive such activities is important. Managers should consider supporting their intrapreneurial role models and provide them with resources and conditions to implement their initiatives. Finally, policymakers need to create conditions for the workwear industry to make the implementation of circular activities possible and profitable. They must facilitate funding opportunities for entrepreneurs to work with innovative and new circular solutions and create incentives for consumers to, for example, reuse or repair by reducing tax on repair services. This article hopefully provides inspiration for firms in the workwear industry on how to operationalise CBM processes and in the transition to a circular economy.

Limitations and further research

This research has a number of limitations that can form the basis for further research. First, the workwear industry in Sweden is relatively concentrated. Some incumbents have a very large market share, such as, the organisations identified in our sample, which influences our results. Smaller resellers and classic laundries were less prominent in our research and as an interview-based qualitative research study, this may have sample selection bias. Thus, further research could capture the workwear industry broadly using other more quantitative research methods, such as surveys, or qualitative methods in other national contexts to get other perspectives or conduct deeper case studies to capture more details. Second, some firms have specific characteristics and focus that is, manufacturing, rental and repair, therefore, further studies could seek to analyse the drivers and barriers for homogenous categories of organisations within the workwear sector. Third, a gap exists with regard to the relevance of the corporate culture and individual behaviour in the CBM implementation (Centobelli et al., 2020; Ferasso et al., 2020). Fourth, ways to influence the external barriers and especially demand from customers and users are important aspects to further research. Customers can mobilise and pressure the supply side actors to change their business models and overcome internal organisational barriers. Fifth, existing research on ownership and control over the supply chain in the workwear industry is rather unexplored (Saha et al., 2021). Finally, this research did not explore recycling activities, a crucial part of a circular economy, and more work on this topic is needed (Malinverno et al., 2023). In conclusion, workwear is a major part of the textile industry and there are many topics that need to be researched and acted upon if the textile industry is to become more sustainable and circular.

Conclusion

The aim of this article was to analyse the organisational and individual drivers and barriers for incumbents and start-ups to CMS specifically in the workwear industry and address calls for the need for more research on circular start-ups (Ferasso et al., 2020; Suchek et al., 2022). The study included seven incumbents in the workwear industry. All, except one, offer either classic long-life models with some hybrid features such as, repair or access models. The seventh encourages sufficiency through consulting services. The seven circular start-ups bring a larger variety of CBMs to the market, although the most common are gap-exploiter and hybrid models. Although both incumbents and start-ups in the workwear industry have several internal organisational drivers and barriers, the start-ups have more ambitious agendas and face fewer internal organisational barriers. In contrast, the incumbents tend to innovate within their existing structures. The external drivers and barriers are, however, more significant and to a large extent common between the two groups. Therefore, we conclude that there is a potential in the workwear industry to move faster towards CBMs if these are addressed. Three key external barriers are identified, in relation to the workwear industry: a lack of demand, a lack of supporting policies, such as public procurement, and the low price of new workwear. These barriers can be generalised to other related sectors within the textile and clothing industry but are not necessarily key to other industries. Increased collaboration among actors in the ecosystem can generate knowledge and competence and enhance resource sharing, especially for start-ups. Apart from providing a deeper understanding of the workwear industry, this study also contributes to theory. We suggest that the drivers and barriers for CBMs are both dependent on the industry, the size of the firm and on the type of business models. Moreover, we highlight the need to look into circular business ecosystems and supply chains and explore the different roles that firms take on, such as CBM supporters and CBM leaders. Finally, we emphasise the importance of the individuals in driving CBM innovation, that is, the entrepreneur or intrapreneur and suggest that considerable research is needed in this area.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the project ‘Circular workwear in construction and industry’ No.52057-1, which is part of the strategic innovation program RE: Source and funded by Energimyndigheten (The Swedish Energy Agency), Vinnova (Sweden’s Innovation Agency) and Formas (The Swedish Research Council for Environment, Agricultural Sciences and Spatial Planning).