Abstract

Underpinning this instrumental case study is an effectuation lens. It investigates how a firm’s governance affects decision-making within international new ventures (INVs), which rapidly withdrew from markets abroad, regarding their re-internationalisation activities. Interviews with founding owners, exhibiting growth-oriented objectives, provide unique insights regarding a combination of effectuation and causation-oriented decision-making. In comparison to earlier studies that focus on the role and mind-set of the founding management team, findings suggest stakeholders like angel investors may exhibit an influence on certain INVs’ internationalisation decisions. Some decision-makers view risks/rewards against objectives in subjective ways like ‘loss of credibility’ and the ‘fear of missing out,’ rather than simply economic terms like growth. New light is shed on the importance of decision-makers validating internationalised business models and exhibiting an ability to pivot product-market strategies. Non-linear international scale-up behaviour may include a temporary domestic market focus and potentially re-internationalising to different countries targeted prior to de-internationalisation.

Introduction

Underpinned by an effectuation lens (Sarasvathy, 2001), the objective of this instrumental case study is to understand how a firm’s governance affects decision-making within international new ventures (INVs), which rapidly withdrew from markets abroad, regarding their re-internationalisation activities. This investigation involves interviews (and secondary data where possible) with INVs’ founding owners, who exhibited growth-oriented objectives. All owners perceived that to facilitate growth, there was a need to exhibit ‘scale-up’ behaviour influencing their initial rapid internationalisation. However, contextualising this study in relation to broader-based research on scale-up behaviour and high-growth firms is important. This is because although Jansen et al. (2023) note that interest has gained momentum, the existing body of knowledge remains largely fragmented and dispersed.

Therefore, context is likely to play a role in explaining the observation of Jansen et al. (2023), since scale-up behaviour may be contingent on various circumstances. This instrumental case study contributes to a relatively under-researched body of knowledge recognising that scale-up, growth-oriented behaviour that manifests in internationalisation is not always forward moving and may be non-linear (Benito and Welch, 1997; Bernini et al., 2016; Crick et al., 2020; Kafouros et al., 2022; Vissak and Francioni, 2013; Yayla et al., 2018). This focus is important due to a consideration raised by Kafouros et al. (2022). They suggest that identifying factors affecting re-internationalisation is important to gain an understanding of a firm’s internationalisation portfolios, in addition to their performance, growth and nature of competitive advantages. Nevertheless, the consideration raised by Kafouros et al. (2022) brings up the important question of who in a start-up’s governance structure is likely to make (re-)internationalisation decisions.

In addressing this question, this investigation provides a challenge to certain earlier work featuring governance considerations among internationalising firms. Specifically, although not exclusively, there is a tendency for some prior studies to focus on the role, experience and mind-set of the key decision-maker and/or members of the founding management team, as opposed to other stakeholders (Costa et al., 2023a; 2023b; Nummela et al., 2004; Reuber and Fischer, 1997; Torkkeli et al., 2018). Yet, various studies recognise that many small firms, and especially new ventures, are typically under-resourced; hence, they may struggle to facilitate survival or indeed growth (Blank, 2013; Fürst et al., 2023; Young et al., 2000). This instrumental case study illustrates certain owners needing to recruit angel investors as stakeholders to form part of their governance structures to facilitate re-internationalisation. Alternatively, other owners relied on the capabilities of their respective founding management team. Such governance considerations resulted in a varied combination of causation and effectuation-oriented decision-making (as per Sarasvathy, 2001). This also manifested in varying degrees of strategic flexibility and improvisation behaviour (following Evers and O’Gorman, 2011; Hughes et al., 2020; Pauwels and Matthyssens, 2004) in decision-makers’ speed, scale and scope of re-internationalisation. Consequently, the notion of ‘governance’ is pertinent. That is, respective INVs with differing governance structures are likely to vary in respect of their tangible resources (like financial capital) and intangible capabilities (such as knowledge and experience), which may affect growth-oriented decision-making (Barroso-Castro et al., 2022; Crick and Crick, 2014; Quas et al., 2022).

Given that terminology differs in existing studies, three key concepts are considered necessary to clarify regarding rapid internationalisation, forms of governance and scale-up behaviour to facilitate growth. First, rapidly internationalising firms are termed differently across existing studies such as ‘born globals’ (BGs) as well as the previously mentioned INVs (Andersson et al., 2020; Coviello, 2015; Gerschewski et al., 2015; Hashai, 2011; Jiang et al., 2020; Knight and Cavusgil, 2004; Oviatt and McDougall, 1994). It has been recognised that earlier literature varies in categorisations of firm speed, scale and scope of internationalisation (Crick and Crick, 2014). The firms in this study rapidly internationalised (within their first three years). However, prior to de-internationalising, their percentage of exports to total business and number of markets served, including geographic spread, were not especially high. The same was true following initial re-internationalisation. As such, the term ‘global’ (as per BGs) would be misleading; hence, they are termed INVs.

Second, the term ‘governance’ is viewed from narrow to broad terms in prior research. Bevir (2012) highlights that different stakeholders can exist depending on the context, ranging from government in a macro-level sense through to an individual firm from a micro-level perspective. From this latter firm-level perspective, research has outlined the importance of knowledge acquisition, learning and capability development (Felzensztein et al., 2022; Hilmersson and Johanson, 2020; Jones and Crick, 2004). In facilitating these important issues, earlier studies have often considered the importance of various stakeholders that may feature in a firm’s governance. These include the role of the management team (Reuber and Fischer, 1997) or a board of directors (Puthusserry et al., 2021) that may be diversified or narrowly defined. In fact, governance may be restricted among key members of the same family in some businesses (Chua et al., 1999), or influenced by other key stakeholders such as rival firms (Crick, 2019) and alliances more broadly (Zahoor and Lew, 2022).

Nevertheless, another form of stakeholder involves investors that may add to the governance structure and influence decision-making (Collewaert, 2012; Crick and Crick, 2018; Mason and Harrison, 1995; 1996; Mason and Stark, 2004; Mason et al., 2017; Maxwell et al., 2011; Yao and O’Neill, 2022). For example, the notion of ‘blitzscaling’ has become prevalent for funding typically disruptive technology to facilitate very fast growth, including prioritising speed over efficiency despite facing environmental uncertainty (Kuratko et al., 2020). For clarity, this study features angel investors as these were the only type of investor that owners utilised, as opposed to options like venture capital providers. However, support such as financing can extend to other sources like a government-backed approach (Aernoudt, 2017). This study investigates governance issues over key decisions within businesses employing an internationalised business model (Onetti et al., 2012). Specifically, after rapidly internationalising, all INVs temporarily de-internationalised. Subsequently, all INVs re-evaluated their governance structures, whereby, to help re-internationalise, some brought in angel investors and others did not want to relinquish a degree of control. In all INVs, a key owner nonetheless maintained majority equity control.

Third, the context features owners with growth objectives that required them to exhibit ‘scale-up’ behaviour (sometimes used inter-changeably with ‘scaling’ and ‘scalability’). This is an issue that has gained prominence in recent literature, making this investigation both timely and important (Huang et al., 2017; Jansen et al., 2023; Monteiro, 2019; Piaskowska et al., 2021; Reuber et al., 2021; Stallkamp et al., 2022; Tippmann et al., 2023a; 2023b). We purposefully use the term ‘scale-ups’ to contextualise an owner’s growth-oriented objectives consistent with Piaskowska et al. (2021, p. 1). These are ‘high-growth firms at an intermediate stage of organisational development (situated between the start-up and mature firm stage in the organisational life cycle), which pursue strategies that prioritise the attainment of economies of scale’. The quote is pertinent because this investigation features high-growth-oriented INVs at the post internationalisation stage (Gerschewski et al., 2018; Ibeh et al., 2018; Morgan-Thomas and Jones, 2009; Prashantham and Young, 2011). However, it explicitly does not feature those INVs at an adolescent/mature stage, and rather having passed their initial start-up and early internationalisation phases. Furthermore, decision-makers were looking to attain economies of scale by engaging in exporting rather than multinationalisation (Monaghan and Tippmann, 2018; Reuber et al., 2021; Tippmann et al., 2023b), where the latter may imply having income generating assets abroad.

This investigation builds on calls for more research involving internationalisation decision-making in particular contexts (see, Ahi et al., 2017; Yang and Gabrielsson, 2017). More specifically, it builds on the work of Reuber et al. (2017), highlighting three directions for opportunity-focused research addressing entrepreneurial internationalisation: ‘context’, ‘dynamics’ and ‘variety’. Using the broadly termed directions of Reuber et al. (2017), this study offers a contribution in respect of the role of governance regarding re-internationalisation activities and whose mind-set is important. This investigation follows recent calls for research (Gerschewski et al., 2018; Ibeh et al., 2018; Sadeghi et al., 2018), noting that a relatively limited number of studies has investigated rapidly internationalising firms’ post-overseas market entry strategies. Nevertheless, to re-iterate an earlier point for clarity, the research setting under investigation does not feature firms reaching their adolescent/mature phases and rather somewhat early-stage decision-making. Moreover, this study follows calls for more research involving de/re-internationalising firms (Kafouros et al., 2022; Sousa et al., 2021; Surdu et al., 2019; Vissak et al., 2020; Yayla et al., 2018). In short, to date, the role of governance and the influence on decision-making in respect of INV de-/re-internationalisation activities remains under-researched. Four specific contributions follow from this study.

The first contribution is to extend the current understanding of decision-makers’ experience regarding internationalisation activities (Reuber and Fischer, 1997; Nielsen and Nielsen, 2011). Irrespective of a founding owner’s prior and evolving international experience, unique insights build on earlier knowledge featuring the potential role of key stakeholders (Bell et al., 2004; Belhoste et al., 2019; Fischer and Reuber, 2003; Wiltbank et al., 2009). Specifically, new light is shed on the role of angel investors that may become part of an enhanced and experienced governance structure. This issue raises the question for researchers – who is making key (re-) internationalisation decisions across INVs with different governance structures?

Second, on a related point, this investigation extends the current understanding of the notion of decision-maker ‘global/international mind-set’, to some extent challenging certain prior research (Nummela et al., 2004; Torkkeli et al., 2018). New insights emerge concerning the question of whose mind-set is important in decision-making based on the governance of a particular firm, whereby, in some INVs, angel investors with a different mind-set to the founding owner may help shape (re-) internationalisation paths as opposed to growth via a focus on their domestic market. As such, knowledge acquisition regarding various phases of internationalisation may come from different sources (building on Agustí et al., 2022).

The third contribution arises from the underpinning effectuation lens (as per Sarasvathy, 2001). Prior research suggests a combination of causation and effectuation-oriented decision-making will sometimes occur in respect of exploration and exploitation activities (Evers and Andersson, 2021). Novel findings in respect of scale-up activities suggest that a growth-oriented end goal implies causation-related decision-making. However, the practices of different members of an INV’s governance structure (founding owners that may extend to angel investors) in addressing that goal suggests decisions are often effectuation-oriented. Unique findings extend literature featuring non-linear internationalisation activities (Bernini et al., 2016; Crick et al., 2020; Kafouros et al., 2022; Vissak and Francioni, 2013; Yayla et al., 2018). Moreover, new insights build on the notion of an ‘affordable loss’, suggesting this is viewed in both financial and non-financial terms, where the latter includes perceived credibility in a market and the fear of missing out on potential opportunities.

Fourth, supported by lean start-up principles (Blank, 2013; Ries, 2011), new findings highlight a need for members of a respective firm’s governance structures to exhibit ‘readiness’ for implementing strategically flexible and improvised decision-making (Evers and O’Gorman, 2011; Hughes et al., 2020; Pauwels and Matthyssens, 2004). Specifically, these insights demonstrate an ability to pivot business models, like a domestic or international market focus, in line with evolving validation and evaluation activities (Gassmann et al., 2014; Osterwalder and Pigneur, 2010). This may at times mean losing customers abroad with a temporary focus on the domestic market. Furthermore, practices may not necessarily result in re-internationalisation to the countries targeted prior to market withdrawal.

Literature review

To facilitate growth-oriented behaviour, prior research raises the question of how internationalisation begins and manifests in early stages after the start-up phase (Casillas et al., 2020; Crick and Crick, 2016). In helping to answer this question, existing studies suggest key indicators are often evident to signal international entrepreneurial activity, namely, how quickly a new venture enters foreign markets, its extent of internationalisation and the scope of markets or regions served (Acedo et al., 2021). A body of literature exists that suggests decisions to internationalise can arise from various reasons, not least, decision-makers identifying and exploiting opportunities as part of their growth-oriented objectives; also, in some circumstances, influenced by stakeholders in network relationships (Blank, 2014; Chandra et al., 2009; Karami and Tang, 2019; Kayiha, 2020; Leonidou et al., 1998; Yang and Gabrielsson, 2017). In fact, earlier studies highlight that various stimuli influence decision-makers in respect of their speed, scale and scope of internationalisation through to more specific issues like the mode of market entry (Ahi et al., 2017; Crick and Crick, 2014; Jones et al., 2011).

Nevertheless, irrespective of motives affecting growth-oriented activities via internationalisation, decision-makers face time and cost implications, alongside a degree of uncertainty. Indeed, decision-making may follow consideration of issues like different institutional conditions in foreign markets leading to a variety of perceived obstacles and risks existing in pursuit of opportunities (Kahiya, 2018; Liesch et al., 2011; Magnani and Zucchella, 2019; Sraha et al., 2020; Torkkeli et al., 2019). Risks associated with internationalisation are potentially compounded with the introduction of new technologies (Kriz and Welch, 2018); hence, the need for decision-makers to be mindful of information collection and validating facets of their business models (Crick and Crick, 2018; Ojala, 2016; Onetti et al., 2012; Spiegel et al., 2016; von Delft and Zhao, 2021).

Some decision-makers are quicker than others in forming an effective organisational architecture/infrastructure (Pedersen and Shaver, 2011) enabling them to implement an internationalised business model, for example, finding an appropriate value proposition(s) for respective customers (Bailetti et al., 2020). More specifically, to facilitate growth, such considerations help them transition from the start-up to scale-up phase (Picken, 2017). Such decisions are likely to vary depending on the objectives of key members of the governance structure as performance can be measured in different ways like profit, growth, etc. (Spence and Crick, 2006; Wach et al., 2016; Wheeler et al., 2008). It is therefore useful to link aspects of the earlier underpinning themes of this study in order to address the research objective. This commences with the central topic of decision-making to facilitate internationalisation and support growth-oriented activities, while noting the relatively under-researched theme of de- and re-internationalisation. That is, activities may not be as linear and forward moving as some earlier studies suggest. This leads to considerations in respect of facilitating strategic flexibility and improvised behaviour in business models. Subsequently, key issues associated with the theoretical lens employed follow.

Internationalisation and de-/re-internationalisation decision-making

Early seminal research featured internationalisation decision-making leading to an incremental process based on increasing knowledge. That is, key decision-makers commence foreign activities via a country having a close psychic distance to their domestic market and subsequently expand operations following learning via a progressive process (Johanson and Vahlne, 1977). Later studies recognise that although a gradual approach may occur, some firms internationalise more rapidly (Andersson et al., 2020; Jantunen et al., 2008; Jiang et al., 2020; Paul and Rosado-Serrano, 2019; Puthusserry et al., 2020). Various issues influence firms’ speed, scale and scope of internationalisation. These range from owner (and their management team) experience through to their respective mind-set towards exploiting foreign opportunities (Nielsen and Nielsen, 2011; Nummela et al., 2004; Reuber and Fischer, 1997; Torkkeli et al., 2018). Recently, the Internet and digital platforms have provided opportunities that facilitate internationalisation in ways not available to decision-makers in some earlier studies, for example, ranging from ease of information search through to reduced supply chains, such as selling direct to end users rather than via intermediaries (Monaghan et al., 2020; Ojala et al., 2018; Sahut et al., 2020; Samiee, 2020; Sigfusson and Chetty, 2013; Sinkovics and Sinkovics, 2020).

A tendency nonetheless exists for earlier research to report on forward moving internationalisation activities (Jones and Coviello, 2005; Jones et al., 2011; Leonidou and Katsikeas, 1996; Leonidou et al., 2010). In contrast, a comparatively under-researched body of knowledge highlights that internationalisation may be non-linear and evolutionary in nature (Bell et al., 2003; Santangelo and Meyer, 2017; Schweizer and Vahlne, 2022). Internationalisation can take a variety of forms with respective decision-makers entering and exiting product-markets (Benito and Welch, 1997; Hadjikhani, 1997; Javalgi et al., 2010; Kafouros et al., 2022; Yayla et al., 2018). In fact, cognitive, emotional and social triggers in addition to biases are likely to affect individual decision-making. Such considerations provide support for the non-predictive decision-making lens of effectuation theory (Sarasvathy, 2001; Sarasvathy et al., 2014), discussed in a later sub-section.

Certain decision-makers withdraw from foreign markets, while others sporadically enter and exit international markets; also, some temporarily withdraw from internationalisation activities and then later return to sales abroad (Bell et al., 2003; Bernini et al., 2016; Sousa et al., 2021; Surdu et al., 2019; Vissak et al., 2020). Moreover, recognition exists that in respect of decisions-makers withdrawing from markets abroad, it is important to re-evaluate strategies during a ‘time-out’ period, namely, between de-internationalisation and international market re-entry (Crick and Chaudhry, 2006; Welch and Welch, 2009). Indeed, Pauwels and Matthyssens (2004) note the importance of learning and flexibility in terms of shaping strategies, and so it is necessary to contextualise decision-making behaviour in respect of the impact on business models.

Strategic flexibility, improvisation and business model considerations

Effective decision-making leading to a viable business model is important, since many businesses ‘fail’ for various reasons (García-Quevedo et al., 2018); in particular, among start-up firms (Blank, 2013). Although perseverance in addressing difficulties to avoid failure is important (Lamine et al., 2014), clarification on the issue of ‘failure’ is necessary. It is possible to view this in different ways ranging from not meeting decision-makers’ objectives to a business closure. In this study featuring re-internationalisation strategies and governance considerations, the context follows the consideration of Welch and Wiedersheim-Paul (1980) who note that the decision to withdraw from foreign markets is not necessarily a market failure. Instead, consistent with the broader strategy literature, it is common practice for decision-makers to learn and exhibit strategic flexibility and improvisation behaviour to evolve business models (as per Gassmann et al., 2014; Osterwalder and Pigneur, 2010). Moreover, decision-making should reflect a strategic commitment rather than being ad hoc in nature (Kouropalatis et al., 2012), for example, in addressing a product-market fit (Hughes and Morgan, 2008). Consequently, understanding the role of governance in decision-making regarding re-internationalising is important, given that for firms in certain countries, remaining in their small domestic market would not sustain the business in the long term (Bell et al., 2004; Kahiya, 2020).

A body of literature exists that highlights the importance of being alert to opportunities to meet objectives, including via networking, like to achieve ‘first mover status’ (Blank, 2014; Crick et al., 2020; Lamine et al., 2015; Yang and Gabrielsson, 2017). In fact, opportunity recognition and exploitation may be enhanced by various network partners that range from different types of investors through to government support providers and even rivals (Bell et al., 2004; Crick and Crick, 2018; Fischer and Reuber, 2003; Ryan et al., 2019). It may therefore seem to some extent rather counterintuitive for start-up firms to internationalise rapidly, then, quickly withdraw from foreign markets. In contrast, decision-making associated with rapid market withdrawal is to some extent consistent with existing research involving ‘lean start-up’ principles; hence, it is not counterintuitive (Blank, 2013; Ries, 2011). That is, in accordance with effective governance, be this via owners, investors, etc., lean start-up principles indicate that if a business model is not viable, decision-makers need to fail quickly and inexpensively or pivot their approach taken. In the latter case, meaning decision-makers need to sometimes evolve business models rapidly for reasons like learning from validation, reacting to customer feedback and changing market conditions (Gassmann et al., 2014; Osterwalder and Pigneur, 2010).

Therefore, assuming decision-makers have the appropriate resources/capabilities (that may include enhancing their founding governance structures via new stakeholders like angel investors), the inter-related notions of ‘strategic flexibility’ and ‘improvisation’ are important factors (Evers and O’Gorman, 2011; Hughes et al., 2020; Pauwels and Matthyssens, 2004), and specifically in the decision to pivot business models. Such notions are contrary to earlier literature referring to certain decision-makers appearing to exhibit an ‘absence-of-strategy’ (Hauser et al., 2020), ‘muddling through’ (Schweizer, 2011) and/or exhibiting a lack of planning together with an inconsistency in strategising (Wang et al., 2007). In short, understanding how business models and associated strategies may change following the ‘time-out’ period after de-internationalisation links to the role of governance in decision-making and hence the focus of this cross-disciplinary study. Namely, since as Eggers et al. (2012, p. 203) point out: ‘strategies cannot come out of nowhere’. As such, consideration of the decision-making literature focusing on an effectuation lens follows.

Decision-making and an effectuation lens

Irrespective of an individual firm’s governance structures, research involving patterns of decision-making in a broader strategic sense has existed for some time (Mintzberg, 1978), including terms like ‘deliberate’ and ‘emergent’ (Mintzberg and Waters, 1985). This contrasts with the more recent rapid ‘build, measure, learn’ approach inherent in the lean start-up literature (Blank, 2013; Ries, 2011). However, Ahi et al. (2017) drawing on earlier studies (like Aharoni et al., 2011; Ji and Dimitratos, 2013) call for more research concerning the decision-making process in respect of internationalisation processes. For example, Ji and Dimitratos (2013) suggest that although decision-making processes of some kind appear to exist within internationalised firms, research explaining the process remains largely under-explored. Similar arguments are pertinent regarding de- and re-internationalisation decision-making to facilitate growth-oriented activities, namely, issues featuring in this investigation.

In terms of an appropriate underpinning theoretical lens and/or framework for this study, various approaches were possible and hence a brief consideration is useful. The broader literature includes decision-makers undertaking modes of market entry like foreign direct investments that are different to the exporting approach taken by all owners participating in this investigation. Therefore, terms like ‘multinationalisation’ (Reuber et al., 2021; Tippmann et al., 2023b) were not appropriate. Consequently, a lens like internalisation theory (Buckley and Casson, 1976) was outside of the scope of this investigation. Moreover, the focus involved decision-making and therefore a broader lens like resource-based theory (Westhead et al., 2001) outlining the resources/capabilities-performance relationship was not appropriate. Neither was a broader appreciation of the way in which decision-makers adapt to environmental issues associated with an institutional perspective (Torkkeli et al., 2019). Ahi et al. (2017) suggest that various lenses can apply to understanding decision-making ranging from real options (McGrath, 1999) through to an effectuation-oriented approach (Sarasvathy et al., 2014). Indeed, Hills and Hultman (2011) note that the development of effectuation theory assists the understanding of decision-making under conditions of risk/uncertainty, making this pertinent given the environmental circumstances faced by owners employing an internationalised business model (Liesch et al., 2011; Magnani and Zucchella, 2019).

Sarasvathy (2001) differentiates between effectuation and causation-based decision-making. An effectuation-based approach suggests the future is not predictable and decision-makers should work with what is within their control to co-create the future based on the realisation that various alternatives can end in different ways. In contrast, causation-based decision-making may begin with various alternatives, but leads to meeting an objective. Andersson (2011) draws attention to a causation-oriented approach as potentially more effective in predictable environments whereas effectuation-oriented decision-making is appropriate when the future is unpredictable. In terms of internationalisation, certain planning to meet growth-oriented objectives might seem important, suggesting a causation-based approach. Nevertheless, the uncertainty faced by decision-makers in unpredictable environmental circumstances (Liesch et al., 2011; Magnani and Zucchella, 2019) may imply utilising an effectuation-oriented approach. Indeed, an effectuation lens is consistent with a body of cross-disciplinary research related to internationalisation activities (Andersson, 2011; Chetty et al., 2015; Evers and Andersson, 2021; Gabrielsson and Gabrielsson, 2013; Galkina and Chetty, 2015; Kalinic et al., 2014; Prashantham et al., 2019; Yang and Gabrielsson, 2017). However, debate exists regarding the merits of this lens and the extent to which decision-making in respective contexts is causation or effectuation-based, and possibly a combination (Arend et al., 2015;; Galkina and Jack, 2022; Karami et al., 2023; Read et al., 2016; Reuber et al., 2016). This study follows the perspective of Nummela et al. (2014) and Hauser et al. (2020), noting that decision-makers can potentially switch between effectuation and causation approaches based on the context.

In terms of the aspects of the theoretical lens underpinning this investigation (Sarasvathy, 2001), there are five key facets that are also termed ‘principles’. Commencing with first ‘The Bird in Hand Principle’, this involves decision-makers recognising who they are, what they know and whom they know. It follows that respective decision-makers will have various resources/capabilities that extend to relevant network partners. In the context of internationalisation, particular decision-makers will have different degrees of experience and vary in the extent they know relevant stakeholders. The second facet involves ‘The Affordable Loss Principle’. Essentially, the underlying issue is that decision-makers should invest in what they can afford to lose. In doing so, they should not focus on the upside, like profits; rather, consider whether the downside is acceptable, such as minimising potential losses. This is important since internationalisation activities can prove costly to address growth-oriented objectives. Nevertheless, it is likely that decision-makers will need to develop further network partners; hence, third, ‘The Crazy Quilt Principle’ notes that decision-makers should develop a network of partners influencing future strategies. In an internationalisation context, this is likely to mean extending domestic networks to those abroad, including stakeholders like government support providers and types of investors that can facilitate access to international opportunities. Fourth, ‘The Lemonade Principle’ involves decision-makers looking at how to leverage contingencies, like whether they are flexible to surprises offering potential opportunities. Internationalisation activities expose decision-makers to varying institutional conditions; hence, adaptability to changing circumstances is important. Fifth, ‘The Pilot-in-the-Plane Principle’ places the previous four together; hence, via decision-maker actions, they co-create their future.

This previously mentioned body of literature is pertinent in this study, whereby, key notions are important to build on existing knowledge. These involve INVs’ rapid (de- re-) internationalisation decision-making; forms of governance, as well as, flexible/improvised scale-up behaviour to facilitate growth. It follows that different stakeholders making internationalisation decisions, like owners and angel investors, will have their own assets that include issues such as funds, experience, mind-sets and network partners (Crick and Crick, 2018; Reuber and Fischer, 1997; Torkkeli et al., 2018; Wiltbank et al., 2009). That said, however, irrespective of the approach taken and by whom in respect of decision-making, Hauser et al. (2020) note that a series of poor decisions consistent with a bad strategy may eventually end in a failure. As such, readiness to employ strategic flexibility and improvisation is likely to be important for decision-makers (Evers and O’Gorman, 2011; Hughes et al., 2020; Pauwels and Matthyssens, 2004). The next section discusses the methodology employed in this study in addressing the research objective mentioned earlier.

Methodology

Recognition exists of the potential value of qualitative research in particular domains like international business (Birkinshaw et al., 2011). Indeed, benefits of using a qualitative as opposed to a quantitative research design to address how/why ‘issues’ involving under-researched contexts are widely recognised; however, considerations associated with the robustness of certain approaches undertaken are also noted (Ji et al., 2019; Suddaby, 2006; Welch et al., 2011; 2022). The use of the term ‘issues’ follows from the perspective of Stake (1995) in this investigation, namely, to avoid quantitative terminology such as ‘variables’. An instrumental case study (Stake, 1995) was employed to investigate issues associated with this study’s research objective. More specifically, Grandy (2010, p. 474) notes that ‘an instrumental case study is the study of a case (person, specific group, occupation, department, organisation) to provide insight into a particular issue, redraw generalisations, or build theory’. The ‘specific group’ in this study refers to decision-makers in rapidly internationalising start-up firms that withdrew from markets abroad but re-internationalised (these represent ‘actors’ and selected characteristics follow in the next sub-section). By undertaking an instrumental case study, the approach allowed the researchers to move from what might simply be viewed as descriptive data, to provide insights into core ‘issue(s)’, involving re-internationalisation decision-making. It also allowed the researchers to redraw generalisations from prior literature and build theoretical arguments underpinned by an effectuation lens (Appendix 1 outlines the process undertaken following the framework of Styles and Hersch, 2005).

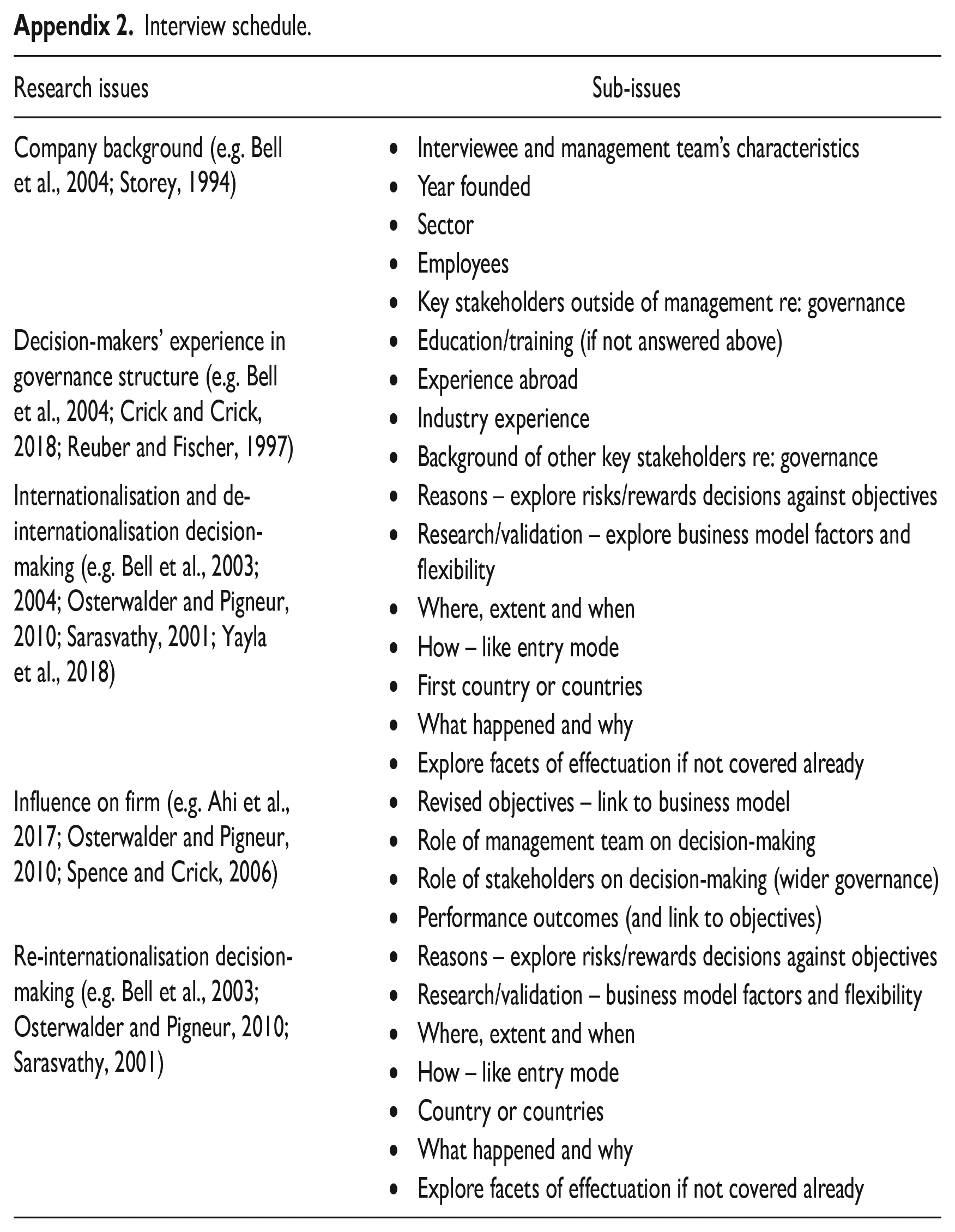

Appendix 2 provides the template for the semi-structured interviews lasting up to one and a half hours with the founding owner as the key decision-maker of rapidly internationalising start-up firms that had temporarily withdrawn from foreign markets and re-internationalised. Limited utilisation occurred of certain sources of secondary data like company reports because of perceived confidentiality; instead, the researchers used non-confidential and freely available information like websites. This offered a degree of triangulation and a thicker description of the data. As such, the procedures addressed the purpose of triangulation highlighted by Farquhar et al. (2020) involving convergence, complementarity and divergence within the data. More details regarding the approach taken to collect and analyse the data follow in later sub-sections. Questions were primarily drawn from the underpinning literature that enabled flexibility to probe for details addressing key issues associated with decision-making and the role of governance. Furthermore, there was flexibility to change the order of questions if required, namely, based on a respective interviewee’s response to the issues under investigation. Additionally, the approach undertaken allowed shared meanings between the interviewer and interviewee to take place and for understanding practitioner terminology. To illustrate, no interviewee used the word ‘effectuation’ to reflect the study’s underpinning lens but did use discourse like ‘risks’ and ‘rewards’ in decision-making integral to that lens.

Data collection

‘Boundary’ conditions featured in this investigation (as per Stake, 1995). It is important to recognise key characteristics of those actors participating in this instrumental case study, a consideration how representative they are to the population of interest, plus any potential bias. By way of background, Blank (2013) notes that start-up firms often have high failure rates. Hence, a challenge existed when identifying start-ups that had internationalised rapidly but had subsequently de-internationalised on a temporary basis and subsequently re-internationalised. No sampling frame was known to exist of firms exhibiting these characteristics and so no claim is possible in terms of how representative they are to the population of interest. That is, the total population of these types of businesses was unknown following informal communication with a variety of academics and practitioners. Nevertheless, this consideration adds further support for the utilisation of qualitative research via an instrumental case study in redrawing generalisations from existing studies. Consequently, a non-probability purposive sampling strategy was employed featuring 16 owners of start-ups, being existing contacts of a member of the research team. These contacts had been established through industry network relationships. All available contacts agreed to participate, and the researchers observed diminishing returns in collecting new and significant information, namely, suggesting reaching a point of theoretical saturation.

More specifically in terms of contextual respondent characteristics, each of the firms in this instrumental case study were less than 5 years old and de/re-internationalisation decision-making was recent; namely, within 18 months of making contact. Earlier research recognises that practices can differ across trade sectors (Andersson et al., 2014). Hence, consistent with Bell et al. (2004), the term ‘knowledge-intensive’ is used in this study to categorise INVs’ trade sectors, with a recognition that incumbent firms have a propensity to internationalise rapidly. Moreover, consistent with mixed criteria in review articles such as Jones et al. (2011), having ‘rapidly internationalised’ meant the INVs under investigation needed to have commenced serving foreign markets within three years of the start-up phase (with each de-internationalising soon after and subsequently re-internationalising in line with the nature of the research objective). These UK-based INVs met the broad criterion of ‘smaller-sized’ firms by employing less than 50 staff (Storey, 1994). All were on the lower end of this categorisation with each containing less than 10 people, more associated with the term ‘micro-businesses’ (Henley and Song, 2020). The size of the management team varied between a single founding owner to a maximum of three members. That is, other staff being of an administrative and/or operational nature with respect to their activities. Each firm had a majority shareholder, but participants were somewhat vague about the exact nature of this confidential data related to the capital structure, including the equity share of investors (where applicable).

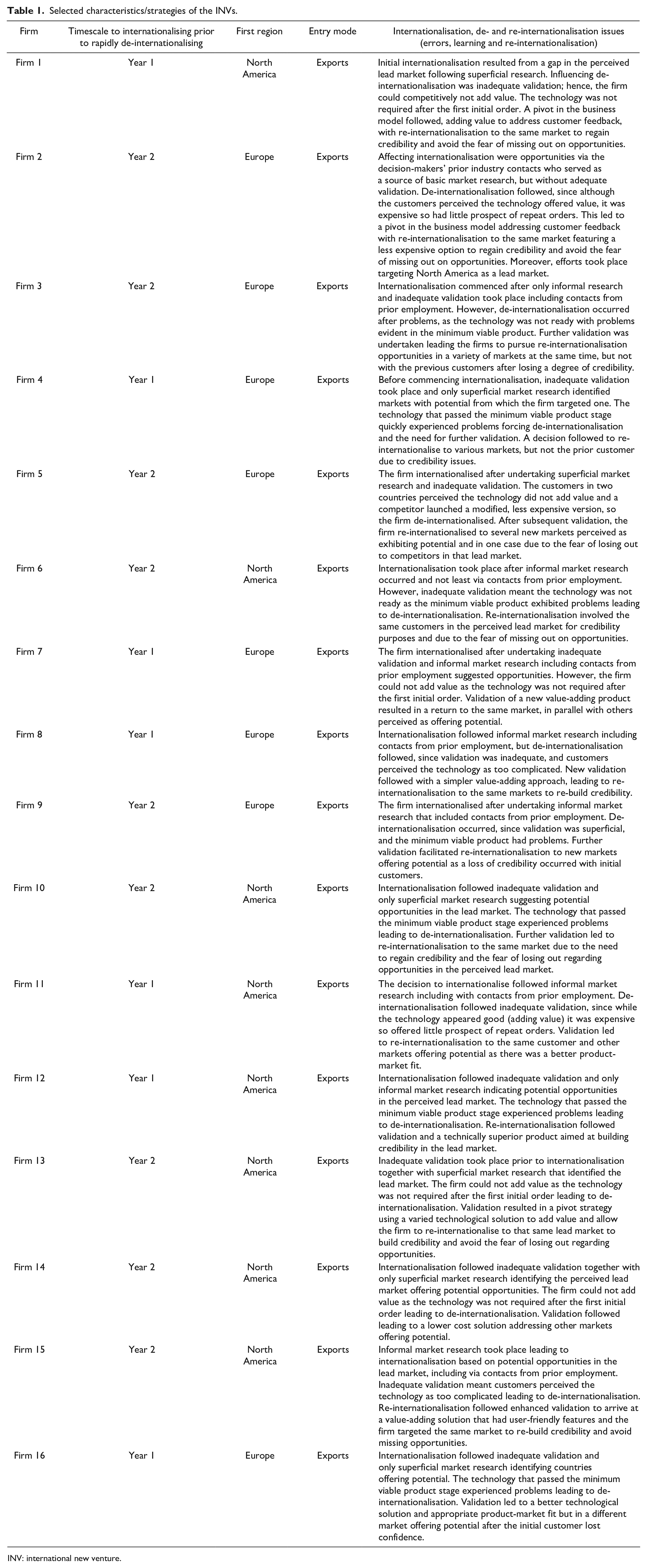

In terms of interviewees, following Kumar et al. (1993), utilising single informants is sometimes acceptable when researching activities in small firms, where one individual is most suitable to answer the issues under investigation. As previously mentioned, all businesses were small (of a ‘micro’ categorisation), with relatively flat organisational structures, and one person being the majority shareholder. Consequently, the respective founding owner (majority shareholder) appeared appropriate regarding being the interviewee, despite offering a key informant’s perspective within each INV. A judgement was made that other managers/employees in the participating firms would contribute relatively little. In every case, the interviewee identified themselves as the key decision-maker with regards to internationalisation decisions. In terms of potential retrospective bias, recognition existed that all interviewees responded with hindsight, but the questions minimised the extent to which this occurred via going between themes to triangulate answers. Table 1 provides a summary of selected activities of the firms in this investigation together with a brief narrative.

Selected characteristics/strategies of the INVs.

INV: international new venture.

Analysis

Certain investigations present the qualitative research analysis undertaken as indicating a seemingly linear process, whereas Sinkovics and Alfoldi (2012) suggest the actual process may be iterative in nature. In this investigation, certain ‘issues’ (Stake, 1995) arose via the practitioner discourse that resulted in the researchers revisiting the existing literature. This is not to suggest that a fully ‘abductive’ research design took place (Timmermans and Tavory, 2012), but rather iterations occurred in line with Sinkovics and Alfoldi (2012). To illustrate, an unanticipated subjective notion of the ‘fear of missing out’ on opportunities arose in the interviews as one reason to help explain re-internationalisation. However, this simply supplemented the identified broader notion of an ‘affordable loss’ (Sarasvathy, 2001) rather than change the direction of the research. Therefore, consistent with Stake (1995), analysis involved ‘particularisation’ taking place, since within the research design, the researchers accounted for issues like the context, narratives and personal engagement.

Furthermore, although Sinkovics and Alfoldi (2012) highlight potential benefits associated with using software to analyse data, in this study, manual coding enabled the researchers to get ‘close’ to the data to understand nuances. Specifically, the approach involved an ‘adapted’ version of the ‘Gioia methodology’ (Gioia et al., 2013) taking place. The term ‘adapted’ recognises that first, the approach undertaken is consistent with the iterative process noted by Sinkovics and Alfoldi (2012). Second, earlier studies present the ‘Gioia methodology’ in particular ways (e.g. Crick and Crick, 2018; Magnani and Zucchella, 2019) and not least depending on the extent to which the respective research is truly ‘inductive’ in nature. Consequently, Appendix 3 demonstrates examples of first and second order themes, together with the aggregate dimension. For clarity, the second order themes and aggregate dimension did not emerge from the empirical data in line with an inductive approach, but rather from the underpinning literature. This does not imply a deductive, but instead, an iterative approach regarding data analysis.

In this study, the notion of ‘trustworthiness’ of the data was important to reflect qualitative as opposed to quantitative terminology like validity and reliability (Lincoln and Guba, 2000; Morrow, 2005); hence, accounting for credibility, transferability, dependability and confirmability. An illustration to enhance credibility was to undertake the triangulation discussed earlier. Additionally, the previously mentioned ‘boundary’ was important given the recognition of context in respect of decision-making under investigation. This involved a very specific group of participants as owners of re-internationalising start-up firms that rapidly entered then temporarily withdrew from foreign markets. This recognition was important to reflect potential transferability of the data from this instrumental case study to other contexts; that is, given the total population was unknown. Discussions occurred among the researchers and that allowed them to agree the ‘issues’ of importance under investigation; whereby, sharing of those issues of importance from the analysis followed with interviewees to enhance dependability. Finally, confirmability took place by utilising a coding scheme that captured the views of informants featuring in this investigation together with the triangulation where possible (outlined earlier); hence, minimising potential bias from the researchers.

Findings

Underpinned by an effectuation lens as per the data analysis illustrated in Appendix 3, issues that help address the previously mentioned research objective follow in aggregate terms for the purposes of brevity. Nevertheless, ‘The Pilot-in-the-Plane Principle’ not shown in Appendix 3, to some extent draws together the other principles of effectuation theory. Hence, via respective decision-makers’ actions, they co-create their future as per the individual summaries in Table 1. More important in contributing to knowledge is to consider the other principles of effectuation theory in greater depth. However, before doing so, Table 1 suggests that to varying degrees, despite being growth-oriented, inadequate validation of their business models together with undertaking superficial market research influenced decision-makers in all the INVs participating in this study to internationalise too quickly. For example, issues involved failing technology, lack of competitiveness or an inadequate product-market fit. In effect, there was a failure by INVs’ decision-makers when identifying and exploiting customer needs, and especially adding value.

Thus, in taking control of actions to co-create their futures, decision-makers in all firms engaged in rapid de-internationalisation to facilitate a ‘turnaround strategy’; hence, to allow re-validation procedures to occur and enable a rapid pivot of their respective business models. Since all interviewees had the broad objective of growth (somewhat consistent with causation decision-making), all perceived that re-internationalisation was a necessary strategy to meet that goal. However, of more interest was that decision-making in respect of the implementation of their respective re-internationalisation strategy varied among interviewees based on the resources/capabilities among respective governance structures. For example, different resources/capabilities affected the speed, scale and scope of activities. Additionally, considerations varied depending on issues like greater networking and perceived risk/reward considerations (together, issues were consistent with effectuation decision-making). In some cases, this resulted in re-internationalisation to the same market(s) prior to temporary market withdrawal, while in others to different markets. Growth in the domestic market was also a key consideration. Illustrations of decision-making in respect of the facets of an effectuation lens follow in addressing the research objective.

The Bird in Hand Principle

This principle involves decision-makers recognising who they are, what they know and whom they know. Despite having previously temporarily withdrawn from foreign markets, it was evident that all interviewees perceived they had a risk-taking, growth-oriented mind-set; that is, having internationalised rapidly despite facing potential barriers associated with liabilities of the newness of the firm, technology and regarding institutional conditions in foreign countries. As the owner of firm 5 noted, ‘as a new firm we went overseas too quickly, you know, without undertaking the proper testing’. Nevertheless, each interviewee perceived that their respective firm’s resources and capabilities were initially constrained. Even with prior experience within their sector, each had relatively limited initial customer contacts because experience tended to be more of a technological nature even though certain foreign networks existed. As the owner of firm 10 explained, ‘we were great on the technical side but not on the business side. I had some contacts from my last job, but they were also on the technical side, and it was difficult getting in touch with those making the purchasing decisions’. None of the decision-makers had taken on any type of investor to enhance organisational governance during the very early stage in their firm’s start-up operations. They largely relied on their own experience together with personal savings and loans/lines of credit from financial institutions to varying degrees. As the owner of firm 15 mentioned, ‘we had to get the business up and running and that meant having something to demonstrate with our technology before investors would take us seriously’. In other words, governance was initially restricted to the founding owners until traction was achieved to make investors (specifically angel investors) interested.

However, things changed as the respective decision-makers took their businesses passed the early start-up stage; not least, networks had developed to varying degrees (see later under The Crazy Quilt Principle) and especially following de-internationalisation. The key issue involving a change of governance featured 10 owners taking on angel investor support during the time-out period (from foreign sales) to build on their limited resources/capabilities like funds, experience and networks. Nevertheless, in those INVs with angel investors, this difference in governance had changed the dynamics of the respective governance structures. Angel investors had a large role in decision-making, despite not being majority equity holders, and especially regarding their re-internationalisation mind-set (where, when, how and the extent of activities). To illustrate, as the owner of firm 11 mentioned, ‘It was a case of where best to take it [the new technological offering]. I was told quite simply [by the angel investor] that America was the key market and the firm needed to gain a presence there to lead to sales in other countries’.

Tensions existed between certain owners and angel investors within those governance structures and some founders looked to exit their firm. As the owner of firm 1 explained, ‘things have not turned out as I thought and if (investor’s name withheld) makes me a good enough offer I’m out of here’. In contrast, some other interviewees recognised the benefits of these stakeholders in the governance structure and as the owner of firm 16 explained (investor’s name withheld) ‘is like a breath of fresh air and has given us a new lease of life. I don’t just mean the money, but also the experience and people he knows in the industry’. That meant there was a need for founding owners to allow angel investors a degree of latitude regarding decision-making to help ensure they did not exit the firms and leave owners without the added resources and capabilities they brought to the enhanced governance structures. Those owners without angel investors nonetheless maintained 100% control in a governance role. However, their decision-making was constrained by their limited resources/capabilities. As the owner of firm 12 explained, ‘I wanted to maintain control and have realistic expectations of what the firm can achieve – you know, like growth and the pace we work at’. As such, those firms without angel investors had re-internationalised with less commitment compared to their counterparts in terms of the percentage of exports to total sales (export intensity) and they typically targeted fewer countries (export scope). Instead, they tried to facilitate growth by focusing on domestic operations with the intention of expanding re-internationalisation further when they had the means to do so.

The Affordable Loss Principle

This principle suggests that decision-makers should invest in what they can afford to lose; hence, not focus on the upside, like profits and rather whether the downside is acceptable, such as, minimising potential losses. An important consideration for all interviewees was the time-out period following de-internationalisation, enabling them to undertake re-validation and pivot their business models. This was especially in the case of firms without angel investors that would have enhanced their governance structure via new funds, experience and networks. That is, to avoid exhausting limited funds due to the ‘burn period’ of operating costs with reduced revenues. For example, certain owners had assets as collateral. Therefore, decision-making did not necessarily mean in a worst-case scenario that a firm would go bankrupt and rather this extended to financial institutions potentially seizing an interviewee’s assets if poor decisions took place. This led to a consideration of the notion of affordable losses in a financial sense. As the owner of firm 14 noted, ‘you get a different perspective if you re-mortgaged your house’. In contrast, the owner of firm 2 with an angel investor mentioned, ‘once (name withheld) arrived it changed our finances overnight. We were no longer relying on lines of credit and that affected the risks we all (owners and angel investor) were prepared to take’.

An issue across all interviewees related to perceived affordable losses in a non-financial sense. This involved not losing credibility in their technologically niche market, since word soon passed around networks; hence, potentially having a knock-on effect regarding growth-oriented activities undertaken and resulting revenues together with profits. As the owner of firm 4 noted in respect of inadequate validation, ‘we looked a bit stupid when our technology failed’. All decision-makers to some degree expressed a fear of missing out on opportunities. This fear ranged from not gaining a presence in a market exhibiting potential before competitors achieved first mover status, through to a fear of not having enough funds to network widely, such as events that may lead to opportunities, both in terms of markets and enhancing their technology. As the owner of firm 13 with an angel investor noted, ‘that is one reason why he (investor) came on board as (name withheld) had the networks to get us quickly into that market before the competitors. Actually, quicker than I would have wanted given we made mistakes before, but his attitude is to move quickly and grab opportunities before it is too late’. As such, emotional considerations supplemented economic issues as potential concerns regarding affordable losses.

The Crazy Quilt Principle

This principle notes that decision-makers should develop a network of partners influencing future strategies. Expanding on issues covered so far regarding networks and governance, each interviewee perceived foreign sales and in certain cases the sector’s lead market, acted as a reference point for potential customers. Moreover, by initially rapidly internationalising and having a presence in certain key markets, this sent a signal to potential stakeholders such as angel investors as an indication of gaining traction and growth. As the owner of firm 3 explained, ‘we needed to quickly demonstrate we were scalable. We needed to get the MVP [minimum viable product involving the new technology] to key [foreign] markets quickly’. For those interviewees that subsequently found angel investors to enhance their governance structures, they perceived these network partners helped facilitate a rapid turnaround strategy leading to a re-internationalised business model. Those without angel investors still re-internationalised, but decision-making was constrained by limited resources/capabilities among those in the governance structure. Nevertheless, it is worth re-iterating that angel investor relationships did not always work out as particular owners planned. Consequently, certain interviewees noted that finding an angel investor with a similar mind-set offered advantages in addition to funds, experience and networks. In contrast, others suggested the importance of undertaking due diligence, since angel investors may not be a good addition to their governance structure if they exhibit a different mind-set and try to take control of decision-making by moving the firm in a particular direction. As the owner of firm 13 mentioned, ‘it’s not just a case of finding someone [angel investor] who knows your industry, but you need to be able to work with that person. If they think differently to you there may be trouble.’

All interviewees, irrespective of whether they brought angel investors to their business, discussed other stakeholders, for example, trade advisers through to government assistance providers as network partners that they perceived as influencing decision-making to varying degrees, but who were not part of their governance structures. Examples of stakeholder support ranged from subsidised assistance such as providing advice on gaining access to certain markets through to technological support regarding their business models. As the owner of firm 6 noted, ‘at one stage I was so busy networking searching for government grants rather than running my business I let some major decisions slip. However, we needed the grants to get the technology off the ground’. However, a key point was that by networking widely, this opened opportunities. For example, networking extended to enhancing social media usage as part of the INVs’ wider stakeholder engagement activities that allowed interviewees to reach key people more easily and especially getting by administrative gatekeepers. Nevertheless, the owner of firm 8 mentioned, ‘you have to make sure that you get the balance right with the number of times you engage with partners to avoid ****ing them off!’

The Lemonade Principle

This principle involves decision-makers looking at how to leverage contingencies, like whether they are flexible to surprises offering potential opportunities. Therefore, linking with the issues associated with ‘The Crazy Quilt Principle’, it followed that decision-makers could potentially build network relationships that may present seemingly serendipitous or unplanned opportunities. An illustration involved attempts via the help of an angel investor (as part of an enhanced governance structure) to target a specific market and gain a positive reputation; in doing so, word may get around and lead to sales in other markets not specifically targeted. In effect, putting efforts into targeting a specific market(s) might enable a decision-maker to leverage contingencies to increase other opportunities. In varying practitioner discourse, this reflected in what various interviewees stated as ‘making your own luck’.

A consistent message across all interviewees using practitioner rather than academic discourse was that initial implementation of internationalisation strategies in the pursuit of growth was poor; otherwise, they would not have temporarily withdrawn from foreign markets after their initial rapid internationalisation. Nevertheless, apart from a recognition that an effective validation of their business model was required, of further importance was learning from experience so similar mistakes did not reoccur. A simple example in this respect involved the suggestion of the owner of firm 9 that ‘I basically screwed-up didn’t I. One thing’s for sure, I did my homework second time around [meaning learning and validation]’. As such, each owner recognised the beneficial nature of a commitment to implement effective validation of their business model, and if things go wrong, to pivot in line with lean start-up principles. In other words, linking with an effectuation lens, decision-makers were, to varying degrees, able to leverage contingencies (domestic and/or abroad) like being flexible to opportunities and improvising behaviour.

The analysis provided insights highlighting that from one perspective, decision-makers’ actions (internationalisation then de- and re-internationalisation) may appear as an absence-of-strategy and muddling through from one approach to another. From a different perspective, interviewees exhibited flexibility and improvisation in pivoting business models to arrive at viable solutions to their problems. As the owner of firm 7 summed it up, ‘I’m an engineer by training and the technology was good but too expensive for the customer. I really should have tested things out [to add value for the price charged]. After we brought in an experienced [angel] investor with a business background and lots of experience, we remained flexible if opportunities came the firm’s way, but this time got things right [added value] with the customer and not just the technology. We are back on track to meet goals [growth]’.

Theoretical contributions/implications, implications for practice, future research and conclusions

Theoretical contributions/implications

Unpinning this investigation, involving decision-making among INVs’ governance structures was an effectuation lens (Saravathy, 2001). This suggested that the future is not predictable, and decision-makers should work with what is within their control to co-create the future based on the realisation that various alternatives can end in different ways. However, the notion of what was within their control to support growth-oriented activities varied depending on whether resources/capabilities were enhanced by bringing-in stakeholders and especially angel investors as part of governance structures. The findings therefore raise doubt about the relative importance of the experience and international mind-set of certain founding owners in decision-making; also, whether other stakeholders play a more prominent role than some earlier literature suggests (Reuber and Fischer, 1997; Torkelli et al., 2018). Moreover, a combination of causation and effectuation decision-making was evident. All decision-makers of INVs (with or without angel investors as part of their governance structures) exhibited a growth-oriented objective that appeared causation-oriented. However, all INVs’ decision-makers undertook an iterative process (internationalising, de- and re- internationalising) to meet that objective, resembling an effectuation-oriented approach.

This investigation is important and timely, following several recent calls for more research. First, it follows the call by Ahi et al. (2017) for more research into decision-making within internationalising firms. More specifically, positioning of this investigation features the respective decision-maker’s growth-oriented goal to ‘scale-up’. This is a topic that has gained prominence in recent literature (Piaskowska et al., 2021; Reuber et al., 2021; Stallkamp et al., 2022; Tippmann et al., 2023a; 2023b). Second, the call by Ibeh et al. (2018) for more research involving the post market entry strategies of INVs (but it is again stressed firms had not reached their adolescent phase). Third, the call by Reuber et al. (2017) for more research into contextual issues; the specific context being de- and re-internationalised INVs in line with an under-researched area identified by Yayla et al. (2018). It therefore follows that gaining further insights into decision-making can offer a theoretical contribution that also provides implications for practice.

In building on existing literature, the findings support lean start-up principles whereby decision-makers should undertake quick but effective validation of their business models (Gassmann et al., 2014; Osterwalder and Pigneur, 2010); that is, leading to them not employing strategies that over-stretch limited resources/capabilities such as internationalising too early with the wrong product-market fit. However, owners that do internationalise too quickly and are forced to withdraw from foreign markets need to re-evaluate strategies during a brief ‘time-out’ period, namely, between de-internationalisation and international market re-entry (Crick and Chaudhry, 2006; Welch and Welch, 2009). This period illustrates the importance of knowledge acquisition and possibly from different sources (extending Agustí et al., 2022); hence, this enables decision-makers to balance risks/rewards when attempting to meet growth-oriented goals. It is likely that exhibiting strategic flexibility and improvisation behaviour can assist decision-makers (Evers and O’Gorman, 2011; Hughes et al., 2020; Pauwels and Matthyssens, 2004); not least, via undertaking further validation, liaising with key stakeholders like angel investors that can enhance their governance structures and pivoting business models. Unique insights lead to two research propositions arising from this study.

Building on the contributions in more detail, first, new insights demonstrate that rapidly evolving decision-making should not be confused with an ‘absence-of-strategy’ (Hauser et al., 2020), ‘muddling through’ (Schweizer, 2011) and/or a lack of planning together with an inconsistency in decision-making (Wang et al., 2007). However, in efforts to achieve a seemingly broad objective like growth-oriented activities, this may appear causation-oriented. In addressing that goal, decision-making may be largely iterative and effectuation-oriented (building on Sarasvathy, 2001). Specifically, because respective decision-makers in the governance structure manage risks/rewards by utilising the resources/capabilities available to them, these resources/capabilities will vary depending on what they have and whom they know. Decision-makers will accept mistakes and surprises to varying degrees, enabling them to identify and exploit new opportunities (Evers and Andersson, 2021), and not least via their network relationships. Sometimes decisions can mean losing certain international customers in pivoting business models.

Nevertheless, within these evolving strategies, the findings build upon Sarasvathy’s (2001) notion of ‘affordable losses’ as these are viewed by certain decision-makers in both financial and non-financial terms. Although profits and growth are objective and measurable, decision-making is likely to trade-off objective criteria with subjective criteria and over time. For example, where the latter include maintaining perceived credibility in a market and the fear of missing out on potential opportunities, such decision-making may not necessarily result in re-internationalisation to the countries targeted prior to market withdrawal. It may even mean focusing on their domestic market until the means are available to enhance re-internationalisation. Indeed, in a broader sense, performance can be measured in various ways (Wach et al., 2016; Wheeler et al., 2008). Researchers considering firm performance, therefore, need to understand decision-maker objectives (Spence and Crick, 2006) and/or those of an extended governance structure that potentially includes stakeholders like angel investors. To illustrate, this helps explain decision-making over time, such as trading off short-term reduced profits to facilitate longer-term gains, like growth into new markets (or even the domestic market) perceived as important. This leads to the first research proposition arising from this study.

P1: Decision-makers in re-internationalising INVs are likely to employ a combination of causation-related and effectuation-oriented behaviour.

Second, the findings shed new insights into the potential importance of the role of members of INVs’ governance structures to enable them to engage in strategically flexible and improvised behaviour. That is, in respect of their responsibility for (re-)internationalisation decision-making (irrespective of their experience as per Nielsen and Nielsen, 2011; Reuber and Fischer, 1997). ‘Experience’ is a broad notion whereby the findings suggest this can vary among decision-makers with some being more useful than others. For example, experience regarding commercialising new technology is likely to be supported by appropriate validation and can offer a greater value proposition to customers in some markets compared to others. As such, to overcome potential problems with limited ‘useful’ experience among founding owners (that may be technology and/or more widely business-oriented), this study highlights the importance of network partners including potential stakeholders like angel investors. Indeed, such network partners can help overcome founding owners of INVs’ typically limited resources/capabilities like funds, market experience and networks to facilitate being able to identify and exploit opportunities. Recruitment of appropriate stakeholders like investors can enhance governance structures and associated decision-making (Bell et al., 2004; Crick and Crick, 2018; Fischer and Reuber, 2003; Wiltbank et al., 2009).

This is not to say that all similar businesses will feature angel investors as some owners may want to maintain 100% control in governance and associated decision-making. However, this may result in their ability to exhibit strategic flexibility and improvisation in respect of re-internationalisation activities being affected, for example, if their growth-oriented activities are slowed by limited funds, experience and networks relationships. By maintaining control in terms of governance, those respective owners may utilise different stakeholders that range from business mentors through to government support providers. It nonetheless follows that within INVs, the unit of analysis regarding decision-making in studies within the cross-disciplinary domain potentially becomes the expanded governance structure, that is, depending on the influence stakeholders can exert.

On a related theme, the findings also provide new insights regarding the extent to which the notion of the owner’s global/international mind-set influences performance-enhancing decision-making (to some extent challenging Nummela et al., 2004; Torkkeli et al., 2018). Instead, building on the prior issue about the potential role of an expanded governance structure in INVs, it follows that researchers might question whose mind-set is important in decision-making. As previously alluded to, not all founding owners will relinquish control to angel investors but may still utilise stakeholders with a non-equity stake to support activities like via government support providers. In contrast, some owners probably need keeping angel investors content to avoid them exiting the business. Furthermore, the findings indicate that certain owners whose mind-sets are not in line with those of angel investors may themselves look to exit the business. In such circumstances, the importance and mind-set of the founding owners may become superseded by that of the new expanded governance structure, affecting their strategic flexibility and improvisation behaviour.

In short, roles and mind-sets of decision-makers may vary across INVs with different governance structures. While there is a potential need to manage tensions, irrespective of who is making key decisions (owner and/or investors), the likelihood is that there is need to exhibit behaviour reflecting strategic flexibility and improvisation (following Evers and O’Gorman, 2011; Hughes et al., 2020; Pauwels and Matthyssens, 2004). From one perspective, it may appear that iterative practices correspond with the notion of ‘unplanned’ strategies (Crick and Crick, 2014), when activities are often somewhat consistent with an effectuation-oriented approach (Sarasvathy, 2001). Nevertheless, from a different perspective and supported by lean start-up principles (Blank, 2013; Ries, 2011), to avoid or overcome problems, decision-makers may benefit from pivoting business models in line with validation activities (Gassmann et al., 2014; Osterwalder and Pigneur, 2010). For example, pivoting behaviour may manifest in issues like an effective use of resources, adding value, and an appropriate product-market fit (Hughes and Morgan, 2008). In doing so, a commitment to engaging in strategically flexible and improvised behaviour following validation activities should help avoid a seemingly ‘absence-of-strategy’ approach (Hauser et al., 2020), hence, not appear as ‘muddling through’ (Schweizer, 2011). Such considerations lead to the second research proposition arising from this investigation.

P2: Decision-makers in re-internationalising INVs are likely to benefit from exhibiting strategic flexibility and improvisation behaviour to enable them to address growth-oriented activities.

Implications for practice

First, although governance structures may differ, decision-makers in INVs attempting to achieve growth are likely to benefit from taking control of manageable issues to co-create their future. For example, this may result from recognising the extent of their performance-enhancing resources and capabilities, together with whom they know to help fill resource/capability gaps. Moreover, decision-makers are advised to consider what they are prepared (and can afford) to lose, that is, losses in broader emotional terms like losing credibility and missing opportunities in addition to economic measures such as growth. They are also likely to benefit from networking widely, so can respond to potential opportunities. Second, a strategically flexible and improvised approach to decision-making is likely to minimise decision-maker vulnerability to environmental circumstances, assuming commitment exists to undertake adequate validation in supporting the pivoting of facets of their business models. Sometimes decision-making may need to be rapid as opportunities are identified and exploited. In some cases, this may mean decision-makers lose customers across their product-market strategies on a temporary or permanent basis. However, that is by no means to suggest lots of time consuming and expensive planning are always necessary in pursuing evolving opportunities. In fact, the opposite is potentially useful in line with lean start-up principles. That is, if a business model is failing, then quick but effective validation should underpin a pivot strategy to facilitate a performance-enhancing product-market fit. For INVs, this may facilitate growth via a domestic and/or international market focus.

Third, by decision-makers recognising their limitations, the role of key network partners (that includes potential angel investors as part of an enhanced governance structure) should not be underestimated. For those owners engaging with angel investors, care is necessary to set expectations; otherwise tensions may result in key decision-makers looking to exit the business, not least, when a large equity stake is transferred to angel investors who (perhaps based on their experience and mind-set) may want to take a business in a different direction to that of the founding owners. However, not all owners will want angel investors, but those with limited resources/capabilities may have constraints imposed on their business models and the associated ability to pivot without the help of such stakeholders. Nonetheless, by networking widely, owners may retain control (equity and decision-making) by utilising partners other than angel investors like via business advisers and government assistance. As previously alluded to, decision-makers in INVs may benefit from not overlooking the possibility of temporarily losing customers to help their firm; that is, by withdrawing from foreign markets on a temporary basis. Such an approach may seem somewhat counterintuitive to much of the forward moving internationalisation literature. Nevertheless, on closer inspection, this appears rational to help avoid a loss of credibility and to have a brief ‘time-out’ period prior to pursuing opportunities abroad. Specifically, this is likely to be helped via exhibiting a validated and pivoted business model in respect of subsequent re-internationalisation.

Limitations and future research

This investigation had certain limitations that consequently lead to opportunities for future research. First, a possibility exists that influencing the results were institutional factors, since the study occurred in a single country. Second, as data collection took place with owners of a relatively limited number of smaller-sized INVs, resource and sectoral considerations may also feature in the study. As the Methodology section outlined, this recognition was important to reflect potential transferability to other contexts. Third, the investigation involved the perceptions of owners having the benefit of hindsight; hence, offering a potential degree of retrospective bias. These do not pose serious limitations and instead offer opportunities for future research. Opportunities include quantitative research for the purposes of generalisability, possibly involving different sectors and across countries. However, locating de- and re-internationalising INVs may pose a problem for data collection purposes; that is, finding a sampling frame and subsequently facilitating a response rate adequate for statistical analysis. If an adequate sample is obtained, research might involve a study of perceptual differences between respective stakeholders influencing INVs’ decision-making. Alternatively, subject to facilitating access, the opportunity exists for in-depth qualitative data utilising a case study approach and offering a longitudinal research design to investigate decision-making with a temporal perspective. Such studies may take a process-based approach to add insights involving decision-making across contextual timeframes like internationalisation, de- and re-internationalisation activities, together with the impact on business models and performance. In fact, different underpinning lenses may offer new insights regarding governance issues, like agency theory. Various contexts would add breadth to existing knowledge and help identify emergent and evolutionary processes among respective decision-makers.

Conclusions