Abstract

Market entry performance is critical during internationalisation; prevailing views suggest that firms need to carefully plan their entry before putting the plan into action. This article focuses on three attributes affecting the possibility and usefulness of making a pre-planned market entry: unpredictability, improvisation and business network commitment. We develop six hypotheses tested on a sample of 250 entries; our main finding is that improvisation plays a mediating role in relation to performance in unpredictable markets. The analysis reveals that the relationship between unpredictability and network commitment is not significant, while the effect of unpredictability on market entry performance is negative. These findings suggest implications for internationalisation and international entrepreneurship theory. For managers and entrepreneurs, we show that unpredictability weakens market entry performance, a negative effect that can be mitigated if the entrant firm improvises.

Keywords

Introduction

Existing research on small and medium-sized enterprise (SME) internationalisation offers a well-developed understanding of the critical mechanisms and key determinants of the internationalisation process. We know that learning and knowledge development are two of the most important explanatory constructs (Hilmersson and Johanson, 2020; Guo and Wang, 2020) as they reduce uncertainty and build confidence in managers to commit resources to foreign markets. These insights, however, build on an implicit assumption that markets are stable over time and that decisions about the future can be taken in the present with influence from the past (Figuiera-De-Lemos, Johanson, and Vahlne 2009). However, as Johanson and Johanson (2021) demonstrate, not only do foreign markets differ from home market but they are dynamic and can change in various ways. Reflecting such arguments, we argue that unpredictability has a temporal meaning as actors cannot foresee what will happen in the future.

Unpredictable changes, rather than stable market differences, have indeed characterised many international markets over the years. The fall of the Berlin Wall in 1989 and the opening up of previously closed markets in Eastern Europe are prime examples. When Gorbachev was appointed general secretary of the communist party of USSR in 1995, he launched the policies of Glasnost and Perestroika. This led to an extensive period of turbulence in the former Soviet Union (Johanson and Johanson, 2006), which spread to Central and Eastern Europe and resulted in a highly unpredictable period of transition from a planned economy to a market economy in most countries within the region. Not least, it led to civil war in the former Yugoslavia. Other prominent examples of market unpredictability are the bursting of the dot-com bubble in 2000 and the 2003 war in Iraq, preceded by the attack on the Twin Towers on 11 September 2001. The global economic recession began in 2008 and the Arab Spring took place in 2010 creating unpredictability in several markets in Africa and the Middle East. More recently, commencing in 2020, we witnessed challenges to humanity when COVID-19 (C19) developed into a pandemic. While the virus itself generated great uncertainty, the restrictions implemented to prevent the spread of the virus fundamentally changed markets (Cowling et al., 2020). Unforeseen and changing restrictions to prevent the spread of the virus resulted in uncertainty for entrepreneurs, and since we currently do not know how long restrictions will persist, markets remain highly unpredictable (Brown and Cowling, 2021). Considering the heterogeneity of the restrictions implemented in different countries, we assume that SMEs with international exposure face even greater unpredictability than their domestic counterparts (Nummela et al. 2020). In predictable situations, previous experience is useful for forward-looking decisions (Nemkova et al., 2015). However, such insights offer limited value and guidance for entrepreneurs and policy-makers facing unpredictable market developments (Hilmersson et al., 2015). With this background, it is important to contextualise research on international entrepreneurship (Reuber et al., 2017) and for managers to develop a strategy for how to act in unpredictable markets.

Inspired by recent developments in global markets, we question the assumption of market stability that implicitly exists in most internationalisation models. Even though past experiences may be quantifiable, structured and explicit, the future is often obscure, uncertain and difficult to predict (Clarke and Liesch, 2017). In light of an uncertain future, market changes will happen such that differing circumstances will emerge (McMullen and Shepherd, 2006). Such uncertainty, in which the unknown prevails (Knight, 1921), results in unpredictability and an awareness that knowledge is limited in terms of present facts and future possibilities (Black et al., 2012). Learning is likely to be difficult and past experiences less useful (Hilmersson et al., 2015). Knowledge about cultural and institutional distance is still critical, if this distance is stable, but when unexpected and extensive changes take place, the critical knowledge will be more how to act in markets characterised by turbulence. Consequently, alternative approaches to finding information and planning for the future will be needed (Miller, 2007; Clarke and Liesch, 2017).

In the entrepreneurship literature, we find two means of dealing with uncertain and unpredictable markets. The first is improvisation (Hmieleski and Corbett, 2008), a behaviour whereby the performer invents something new. The second is network commitment (Mäkelä and Maula, 2006; Hohenthal et al., 2014), whereby actors seek to build positions in networks by way of investments of financial and human resources in specific relationships and networks to gain long-term value, with the exclusion of alternative deployment of these resources. Yet, we contend that there are three essential research gaps that relate to these two means of unpredictability management.

First, although planning may be beneficial, previous findings are contradictory and contextual factors are likely to influence its value (Brinckmann et al., 2010). Specifically, case-based research demonstrates that when conditions are unpredictable, SMEs are likely to improvise (Hmieleski and Corbett, 2008); this has been described as an irrational (Chandra et al., 2012; Newark, 2018) and accidental behaviour (Hennart, 2014). Often, SMEs lack resources to develop formal planning and a forecasting strategy (Savioz and Blum, 2002); instead, they improvise (Fultz and Hmieleski, 2021), which may offer a competitive advantage within changing environments (Gray and Mabey, 2005). By improvising, SMEs adapt to the changing environment without the need to commit resources to forecasting or developing risk management tools (Evers and O’Gorman, 2011). Still, improvisation is mainly seen as a reactive behaviour to an unexpected interruption or to the change of activity in a market (Hadida et al., 2015). Apart from the insights of Nemkova et al. (2015), who concluded that improvisation lies behind many export decisions, and Souchon et al. (2016), who showed that spontaneity weakens in importance in dynamic markets, the extant knowledge is largely limited to case studies (Galkina and Chetty, 2015; Kalinic et al., 2014) with a lack of evidence using broader samples with greater variation.

Second, we know little about how improvisation is linked to the foreign market and the business network the firm is entering. There is knowledge on how cultural and institutional distance generates a liability of foreignness; however, as both are characterised by inertia and so, change slowly, we need more evidence about the effects of volatility on SME behaviour and performance (Hilmersson et al., 2015). Research suggests that networks are important in uncertain contexts (Engel et al., 2017) as they are stable and enable firms to foresee developments and develop plans (Bai et al., 2021). We thus, expect that network commitment is an important part of unpredictability management.

Third, although uncertainty is critical in internationalisation research, surprisingly few studies measure and empirically observe uncertainty (Bruneel et al., 2017; Hilmersson and Jansson, 2012). This is also the case with unpredictability. Accordingly, research not only needs to conceptualise how unexpected changes take place in international markets (Kalinic et al., 2014), but it also needs to develop measures so that it can link such changes to causes and outcomes. Addressing these gaps is essential for theory development as we lack knowledge about how firms may, or should act, in unpredictable markets with implications for informing entrepreneurs regarding future activities. To our knowledge, there is a dearth of evidence integrating findings from the improvisation literature with findings from the network perspective on internationalisation. With the aim of explaining how SMEs manage unpredictability in foreign market entry, we explore this gap by seeking to answer a two-part research question: What is the effect of business unpredictability on market entry performance and how is this relationship affected by network commitment and improvisation?

We make two contributions to the literature. First, by challenging the assumption of market stability, held in most internationalisation models, we show that markets are rarely stable; instead, they change and are often unpredictable weakening the market entry performance of SMEs. Second, we show that the negative performance effect caused by market unpredictability can be mitigated by improvisation by committing resources to the business network. We argue that these insights are important for entrepreneurs, managers and policy-makers seeking to navigate highly unpredictable business situations, such as those brought about by Covid19 and the restrictions implemented to reduce its spread.

In the following section, we present a conceptual framework. Next, we develop our hypotheses, present the method of our study and test the hypotheses. Then, the results of our study are discussed, followed by conceptual and managerial implications, the limitations of our findings, and suggestions for further research. Finally, we end the article with our conclusions.

Conceptual framework

Business unpredictability

The greater control a firm has upon extant contingencies, the more likely it will be able to predict the future. Business unpredictability reflects the dynamics of a market, that is, the perception of the extent and impact of drastic market change (Hilmersson and Jansson, 2012) - referred to as market turbulence (Buccieri et al., 2020). As most SMEs internationalise by exporting to foreign markets, changes in customer behaviour, and the extent to which the firm can predict these changes, will influence its activities when entering foreign markets (Santangelo and Meyer, 2011). Aside from customers and their behaviour, the market can also change in a general sense through environmental dynamism (Yu et al., 2019). Laws, and regulations and the market’s distribution system and technology can all shift and change; the more extensive and less expected these changes, the greater the business unpredictability. Foreign market predictability makes it easier for the firm to develop market entry strategies (Hilmersson and Jansson, 2012) providing a sense of security that makes firms less reluctant to enter the market and commit resources (Liesch et al., 2011). Clearly, earlier experience is useful under stable circumstances (Hilmersson et al., 2015). The firm’s course of action will depend on its ability to predict the general development of the foreign market, as well as its ability to predict more specific aspects, such as how its business relationships will develop with regard to, for instance, customer strategies and investments (Figueira-de-Lemos et al., 2011).

For most firms entering foreign markets, developing business relationships with customers and suppliers is critical (Tolstoy, 2012); taken together, these relationships form a business network – one benefit of such being that they tend to be stable and predictable (Johanson and Vahlne, 2009); however, if they are unpredictable, this benefit declines (Santangelo and Meyer, 2011). Unpredictable business networks are characterised by the establishment of new and unexpected business relationships as well as by the termination of existing ones. Business predictability does not necessarily exclude change and dynamics; however, when changes are unexpected, prediction become less meaningful. Thus, such contingencies will influence the strategic behaviour of the firm (Banalieva and Sarathy, 2011).

Commitment in business networks

Research has moved from the idea that firms commit resources to a foreign market (Sleuwaegen and Onkelinx, 2014) to the view that instead, they commit resources over time to specific networks (Kerr and Coviello, 2020). Who those in the firm know, and to what extent suppliers and customers are committed to the firm and its products, is important with regard to internationalisation (Johanson and Vahlne, 2009; Mejri and Umemoto, 2010). Interaction with stakeholders, rather than competitive analysis, promotes internationalisation (Hohenthal et al., 2014; Welter et al., 2016). This network perspective views the foreign market as a system of long-term business relationships between customers and suppliers (Anderson et al., 1994). Firms act to keep the system together and as they modify their operations, mutuality and interdependence emerge (Slotte-Kock and Coviello, 2010), improving the execution of the exchange in terms of production, distribution, storage, technology and payment (Håkansson, 1982) aims to reduce costs or increase sales (Liesch et al., 2011). However, modifications require resource sacrifices and commitment; the firm needs to exclude some alternatives and invest in others deemed likely to render the highest long-term value (Pollack et al., 2013). Business network commitment is thus, based on considerations of the needs, resources and capabilities of the firms involved.

Commitment may be a product of systematic planning (Hilmersson et al., 2021), but can also emerge from an urgent problem-solving process based on improvisation, most of which seems to be ad hoc or reactive (Baker et al., 2003). The flexibility shown when firms make commitments can be viewed as the ability to accept and respond to the changing needs of customers and suppliers, while network commitment can be viewed as the actual changes made in response to such needs. As such, business network commitment captures the firm’s willingness to make sacrifices in terms of financial and human resources in specific relationships and networks in order to gain long-term growth and value (Mäkelä and Maula, 2006). Commitment to a specific business network thereby implies the exclusion of an alternative deployment of resources (Pollack et al., 2013).

Improvisation

Contingency theory (Lawrence and Lorsch, 1967) has been applied in studies on the relationship between firm performance and context (Robertson and Chetty, 2000); it suggests there is no best way to organise a business given the diverse nature of the internal and external environment (Donaldson, 2001; Scott, 1992). The former relates to the firm’s product and process-related qualities; the latter relates to the industry and export market. Furthermore, while conditions vary between firms and markets, they also change over time; so for example, firms are affected by, for instance, changes in legislation (Banalieva and Sarathy, 2011) and, as experienced in 2020 and 2021, by measures to reduce the spread of Covid19. Improvisation deviates from models based on planning (Ansoff, 1979) or adaptation (Mintzberg and Waters, 1985) by assuming that firms can have agency over constraints and opportunities in the foreign market. As such, it has much in common with effectuation (Sarasvathy, 2001), it also resembles strategy as a process (Mintzberg and Waters, 1985; Santangelo and Meyer, 2011) or as a non-predictive strategy (Wiltbank et al., 2006). Firms pursue a non-predictive strategy under challenging conditions that do not necessarily have to be an outcome of an unpredictable market (Sarasvathy et al., 2014). Studies on effectuation and non-predictive strategy connected to internationalisation (Karami et al., 2020; Sarasvathy et al., 2014) contend that unexpected events can occur thereby, making it pointless either to predict the future or to view prediction and the execution of prediction as two distinct and sequential phases. Instead, improvisation integrates prediction and execution over time.

Firms are affected by the needs, wishes and demands of customers and suppliers; some of which will inevitably be predictable but others, unpredictable and urgent. To address the latter, the firm has to react quickly or proactively, often at short notice, to address problems or to take advantage of an opportunity. While insights on ‘strategic fit’ (Lawrence and Lorsch, 1967) signal a rather static solution, the best strategic fit with an unpredictable business environment is likely to be a flexible approach that allows for improvisation and while effectuation emphasises the control of contingencies, improvisation refers to the simultaneous integration of prediction and action. Improvisation ‘requires individuals to explore and work in the market (to be “shaped” by it)’ (Crossan et al., 1996: p. 31); this reflects arguments by Banalieva and Sarathy (2011) regarding multinational firms in emerging markets and those by Hilmersson and Papaioannou (2015) in their study of SMEs scouting for international opportunities. It also aligns with Hadida et al. (2015, p. 440), who suggest that improvisation is a strategy to meet unexpected or changing contextual developments by acting ‘extemporaneously, spontaneously, intuitively and ad hoc in an emergent manner’.

Conceptual models have been developed that contrast improvisation with more fixed behaviour such as routines (Hohenthal et al., 2003), systematic search or planning (Nemkova et al., 2015), or a view of the future as a continuation of the past that can be predicted and controlled (Dew et al., 2009; Wiltbank et al., 2006). Firms can improvise on the basis of plans or forecasts (Nemkova et al., 2015); however, the need to act quickly should unexpected events arise reveals the limitations of pre-existing plans and structures. The process of market entry is often characterised by surprises and by the need to react, rethink, restructure and recommit often necessitating reshaping plans and strategies. Although Johanson and Vahlne (1977) acknowledged the role of contingencies in internationalisation, improvisation has remained hidden in the concept of experiential learning. It did however, gain more recognition after the inclusion of effectuation theory (Sarasvathy, 2001) as effectuation logic, described as ‘entrepreneurial contingency’ (p. 243), contains important aspects of improvisation in the form of experimentation and flexibility (Chandler et al., 2011).

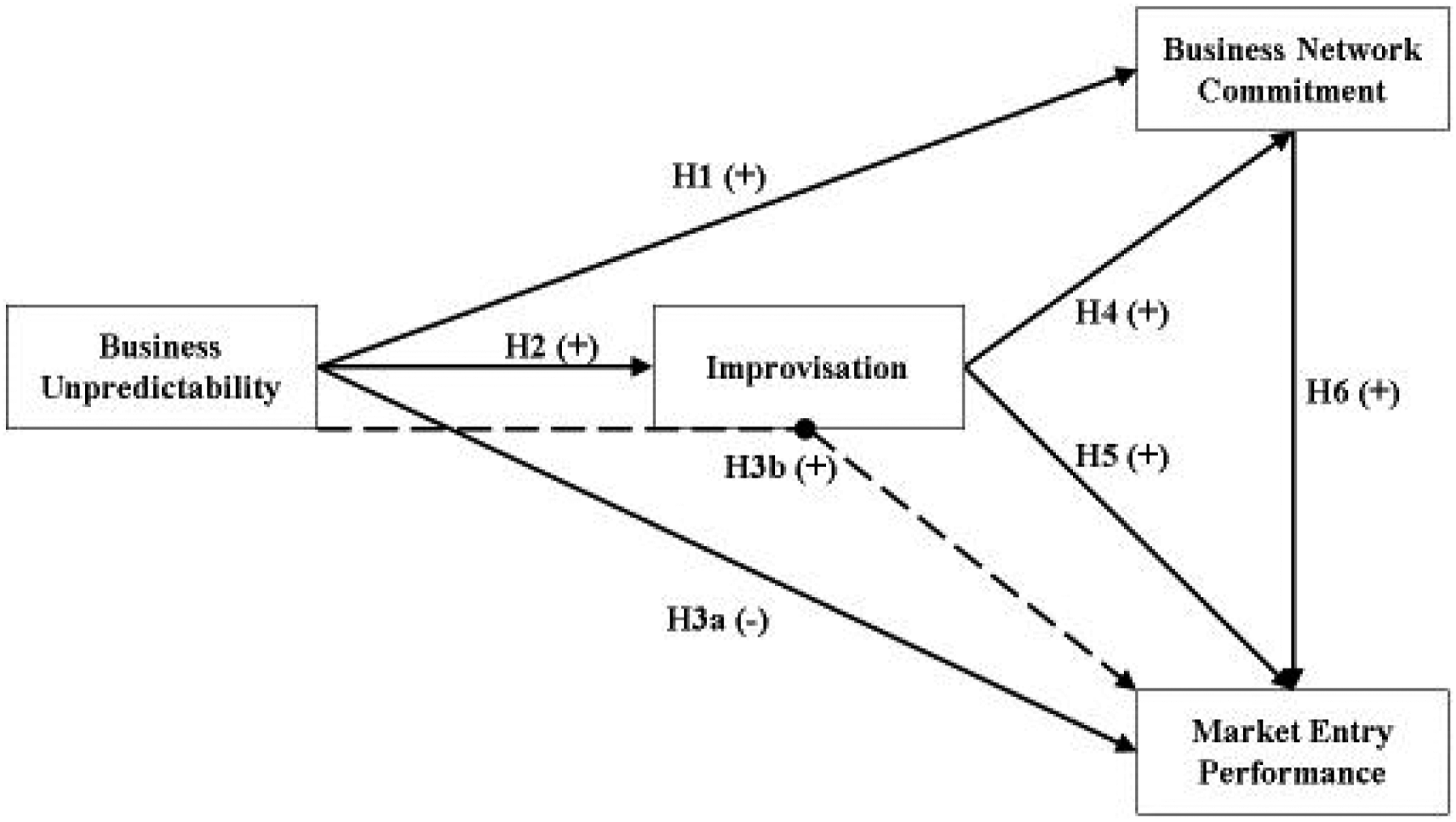

Analyses of international entrepreneurship tend not to consider the nature of the decision-making process (Perks and Hughes, 2008) and the way it is affected by uncertainties (Bylund and McCaffrey, 2017). Likewise, studies on export performance applying a contingency perspective generally focus on internal factors, such as resources and competence, and/or external factors such as market characteristics regarding demand and uncertainty in relation to export performance – without considering mediating variables such as strategies for planning versus improvisation (Safari and Saleh, 2020). Improvisation has mainly focused on case studies of internationalisation (Evers and Gorman, 2011; Johanson and Johanson, 2006). Its value is often unclear as it seems that improvisation is suitable when the firm is aware of its lack of market knowledge or market unpredictability. In such situations, it is difficult to make forecasts or to specify goals as their value may erode during the process (Johanson and Johanson, 2006). Improvisation may, in turn, be a consequence of network relationships (Evers and Gorman, 2011). Entering a foreign market implies interacting with potential customers and suppliers to overcome the liability of outsidership (Yamin and Kurt, 2018). Firms may then have to improvise by modifying products, production processes and/or routines to show their commitment to the relationship. In the next section, we develop the relationships between the constructs presented above (presented in Figure 1). Hypothesised model.

Hypotheses development

Business unpredictability and business network commitment

During market entry, the firm is likely to commit to various critical stakeholders, which in the case of SMEs tend to be customers and suppliers (Tolstoy, 2012). Relationship-specific investments can be made in the organisation, production processes, or technology (Street and Cameron, 2007). Making an additional commitment to a relationship tends to strengthen it as it signals an intention to continued cooperation with that counterpart (Johanson and Vahlne, 2003). In times of high uncertainty and goal ambiguity caused by unpredictability, the firm can commit to partners in a flexible network. Such a commitment constructs the platform for an intense interaction with other firms in a network likely to reduce uncertainty (Busch and Barkema, 2020). Foreign markets are unknown and thereby, uncertain (Chari et al., 2014; Clarke and Liesch, 2017); to varying degrees, they are dynamic and changing and thus, unpredictable (Figueira-de-Lemos et al., 2011). Unpredictability implies that it is even more difficult to calculate the return on investment so this discourages investment in foreign markets (Johanson and Vahlne, 2009; Santangelo and Meyer, 2011). Business networks characterised by trust and openness, however, promote the sharing of information and knowledge between firms (Zaheer and Venkatraman, 1995).

Relationships can be islands of relative stability (Håkansson and Snehota, 1989) within markets. When firms aim to exploit contingencies that arise from business unpredictability (Baker et al., 2003; Sarasvathy, 2001) they can utilise structures such as networks to find clarity, stability and not least, relative predictability. In order to deal with changes in the market and to exploit opportunities (Bai and Johanson, 2018; Johanson and Johanson, 2021), the firm makes business network commitments to improve its network position (Schweizer et al., 2010). In other words, when a firm finds it hard to predict the market, its business network becomes central to gaining control over the market (Bai et al., 2021). Consequently, firms can gain greater control over conditions of market entry by committing to a business network; thus, we hypothesise:

During market entry, market unpredictability will positively influence the SME’s degree of commitment to its business network.

Business unpredictability and improvisation

Whereas research has mainly addressed market instability or unpredictability in an emerging market context (Hilmersson and Jansson, 2012), since 2020 it has been evident that measures to control the spread of Covid19 have generated significant unpredictability on a global scale. In contrast, stable markets are characterised by resistance to change and smooth movements without surprises; the future seems to be path-dependent and past experience can be used as a compass for future direction (Delmar and Shane, 2003). When predictability prevails, planning is a key activity and well-specified goals and targets guide the firm’s actions; this is in accordance with the cause-effect relationship (Dess and Beard, 1984). While plans and strategies are formulated on the basis of prior experience and available information, reality happens in a different time dimension – in the here and now. In fast-changing markets, the past no longer resembles the present: circumstances change, reducing the value of predicting the future. Consequently, existing plans were based on changing and often, incorrect, assumptions. Previous studies have depicted spontaneity and creativity, combined with improvisation – or as Weick describes it (1995) a ‘just-in-time strategy’ – as the missing link between intention and realisation (Vera and Crossan, 2004). When a business, in terms of markets and business relationships, is difficult to predict, flexible strategies, goals, problems and solutions are assumed to be an advantage (Ford et al., 2008). The firm can then react to market changes and swiftly address both challenges and opportunities in the market by ‘thinking outside the box’ (Hmieleski and Corbett, 2006) or by improvising solutions to problems (Hmieleski and Corbett, 2008). Thus, we hypothesise:

During market entry, market unpredictability will positively influence the SME’s degree of improvisation in the market.

Business unpredictability and market entry performance

Risk is the probability of resource commitment failure due to business unpredictability (Figueira-de-Lemos et al., 2011); this has three key components: the general market, network development and customer behaviour. The more change there is in the foreign market, the lower is the value of knowledge and prior experience within the firm and so, the higher is business unpredictability (Hilmersson and Jansson, 2012). Unpredictability that stretches into the future has a strong negative impact on the firm’s strategic and long-term performance in the foreign market (Hult et al., 2008). It makes firms reluctant to invest in, and commit resources to, the market whilst the process of market entry is slower (Prashantham et al., 2018), as are growth possibilities. The strategic importance of having entered a specific market goes beyond the financial aspects given links between these market activities and those in other markets, as well as in relation to general performance. In order to sustain performance over the long-term, the firm needs to demonstrate a sound and sustainable financial return indicating that business operations are profitable. Thus, we hypothesise:

During market entry, market unpredictability will negatively influence the SME’s market-entry performance. When markets are stable and the firm has information that is valid and relevant for the future, business predictability will be high and planning and action, as two distinct but strongly interrelated sequences, will be meaningful (Delmar and Shane, 2003). However, when markets are unstable it is difficult for firms to predict future activity and so, planning and action are only weakly linked (Ford et al., 2008) suggesting a need for flexibility (Alpkan et al., 2007). Consequently, a non-predictive course of action (Wiltbank et al., 2006), such as improvisation, is more likely to be successful (Sarasvathy, 2001). We also know that firms facing exogenous shocks need to act swiftly, and at times in a way that radically deviates from how prior activity. Repeated experience of solving problems by making swift readjustments and improvising will strengthen their competitive position and their business network (Koka et al., 2006). When firms improvise, planning and action are not sequences; rather, they converge in time (Moorman and Miner, 1998; Weick, 1998). This temporal agility gives the firm room to be flexible to the dynamics of the market; this is likely to improve firm performance (Galbraith, 1990; Mintzberg, 1994). Thus, we hypothesise:

During market entry, improvisation positively mediates the relationship between business unpredictability and the SME’s market entry performance.

Improvisation and business network commitment

Entering a foreign market network is an act of entrepreneurship (Schweizer et al., 2010) in a new and therefore, uncertain context of contingencies (Bruneel et al., 2017). It implies facing customers and suppliers that have needs that differ from those of domestic market networks (Johanson and Vahlne, 1977). During the development of a new relationship, thinking and reacting quickly may be necessary, especially where things change quickly (Ford et al., 2008). Improvising implies thinking and acting differently or unconventionally, or from a new perspective, in response to the needs and dynamics of the foreign market’s network (Coviello, 2006). Existing goals and strategies are challenged, including how the firm established its business in other foreign market networks. The outcome of improvisation is likely to be new solutions to new problems (Hilmersson et al., 2021). Experienced firms emphasise the importance of stitching together networks of relationships (Dew et al., 2009). However, acting in an interconnected network implies that a firm is not in full control; therefore, the firm is often forced to improvise (Pavlovich, 2003). Firms improvise in response to requests for commitments from specific customers or suppliers in the network, but commitments may also originate within the firm as a consequence of, for instance, decisions related to a change in strategy. In commitment processes arising from internationalisation, the firm not only commits its products to the preferences of a specific market, but may also have to modify its technology as well as its organisation and production processes (Tolstoy, 2012; Håkansson, 1982). Thus, we hypothesise:

During market entry, the SME’s degree of improvisation positively influences its degree of commitment to specific customers and suppliers in the network.

Improvisation and entry performance

Internationalisation involves the identification and continuous exploitation of opportunities in the foreign market network (Schweizer et al., 2010). The opportunity value emerges when the firm acts upon an opportunity and a business relationship is established. While plans work relatively efficiently in well-known, stable and predictable markets (Delmar and Shane, 2003), the exploitation of opportunities in new foreign markets raises novel challenges that require rapid responses (Child and Hsieh, 2014) and flexibility (Tolstoy, 2012). Plans and possible scenarios need real-time adjustments to match the development of business networks as they cannot be governed by a single actor. In dynamic markets, planning flexibility positively influences a firm’s performance (Alpkan et al., 2007) whilst improvisation enables firms to be innovative and creative at the moment they face unknown and unexpected situations. Crossan’s (1998) and Mintzberg’s (1973, 1988) depictions of the strategy process as a blend of plans, emerging ideas and opportunities show that because plans and intentions are only part of the process, improvisation should be added to attain higher efficiency and performance (Bingham et al., 2007). We assume that improvisation influences performance positively in three ways. First, it contributes to learning (Chelariu et al., 2002; Vendelø, 2009); it represents an important competency that stimulates value development (Eisenhardt and Tabrizi, 1995; Moorman and Miner, 1998). Second, it implies flexible, fast and cheap problem-solving, which has a positive effect on outcomes (Akgün, Byrne, Lynn, and Keskin, 2007; Alpkan et al., 2007) and market performance (Autio et al., 2000; Hult et al., 2008). Third, because improvisation means doing things in new ways, using existing resources for new purposes and finding new solutions to old problems, the firm has to be creative and think ‘outside the box’. Novel experiences may then result in innovations that increase efficiency or that produce more value than previous solutions; it is, in other words, a resource generating type of behaviour (Williams et al., 2021). Thus, we hypothesise:

During market entry, the SME’s degree of improvisation positively influences its market entry performance.

Business network commitments and entry performance

Commitment to actors in the foreign market’s network reflects the intensity of the cooperation in the relationships between the firms (De Clercq and Sapienza, 2006) and signals long-term engagement and trust (Musteen et al., 2014). By making a commitment to the business network in a foreign market, the firm sacrifices short-term benefits to prioritise a long-term strategy (Johanson and Vahlne, 2009). Such changes may also improve coordination and communication between firms that are not each other’s customer or supplier but still part of the same network (Håkansson and Snehota, 1989). Commitments can arise from conditions within, or related to, a specific relationship (Schweizer et al., 2010). A firm can identify an opportunity to further develop a relationship - or a customer/supplier may demand a specific measure. There seems to be consensus that commitments are primarily beneficial to customers (Murfield and Esper, 2016) while commitment to the network has a positive influence on experiential learning (De Clercq and Sapienza, 2006; Jost, 2021; Street and Cameron, 2007). If customer benefits pave the way for sustained or increased sales, entry performance increases. It may be the case that the potential value of having established business relationships cannot be exploited if a commitment is not made. Business network commitments may, in other words, increase long-term competitiveness (Prashantham et al., 2018). There is, however, a negative aspect to this; commitments that are costly and hard to apply in other relationships may result in dependency on the other party and locked-in effects. Furthermore, as the sum of resources is limited in any organisation, making commitments in one network implies refraining from commitments in another. Commitment can lead to the development of long-lasting relationships (Johanson and Vahlne, 2006) and thereby, to a sustainable position in the network (Street and Cameron, 2007). It can also lead to specialisation as each partner develops skills and talents particular to that relationship; however, shifting commitments such as these can be difficult. Maintaining important customers and suppliers is a central feature of strong business relationships and is critical to long-term competitiveness in the business network (Sandberg, 2013). Thus, we hypothesise:

During market entry, the SME’s degree of commitment to specific customers and suppliers in the network positively influences its market entry performance.

Method

Sample characteristics

To test the hypotheses, we used an original dataset compiled from on-site personal interviews combined with a structured questionnaire. The selection of cases was made according to three main criteria. First, we selected SMEs based on the EU definition 1 in five Swedish counties (Jämtland, Gävleborg, Västernorrland, Västmanland and Halland). Second, we examined SMEs within the manufacturing sector, following the widely established distinction between manufacturing and service firms in an international context (Buckley and Ghauri, 1993). Third, we used a time-related variable to ensure that our retrospective data would not be seriously affected by recall biases. This is strongly dependent on the complexity of the questionnaire as well as the time in which responses are obtained (Rylander et al., 1995). To ensure high data reliability with reduced recall bias, we only included firms that had entered a new country market within the past seven years and respondents who took part in the market entry with sufficient recall to be able, with high validity, to inform us about the circumstances at the time of opportunity identification and development.

The sample identification procedure followed four steps. First, data on all exporting firms in the selected geographical areas were obtained from Statistics Sweden. Second, the list of firms was narrowed down to those fulfilling the study’s firm size and industry criteria. Third, a telephone interview of about 15 min was conducted with the firms to exclude those that did not meet the time cut-off limit and to ensure that the other criteria were met. Of the remaining 214 firms, 168 (78.5 percent) agreed to participate in the study: these we visited on-site to collect data. Some firms reported more than one new market entry opportunity in the past seven years, which gave us a total of 258 foreign entries. Of these entries, 31 percent took place in emerging country markets and the remaining 69 percent took place in mature country markets.

Data collection

Prior to the main study, a pilot study tested the questionnaire on 10 firms that were visited on-site. The main study was also performed on-site to maximise the overall quality of the data, improve the response rate, reduce personal bias (Holbrook et al., 2003; Cobanoglu and Cobanoglu, 2003), and so, reduce the risk of any potential selection bias. When designing the questionnaire, we followed the suggestions by Podsakoff et al. (2003) to reduce the risk of systematic biases related to single respondents. First, we tried to reduce the risk of respondents answering based on implicit theories by contextually and temporarily disconnecting the variables in our model. The indicators reflecting the constructs were presented to the respondents in three different sections; a general discussion was held between each section. Second, we reduced the risk of socially desirable answers by including reversed scales and diverse formulations for some of our statements. Third, the on-site data enabled the researcher to exclude certain unreliable or problematic answers or cases from the data analysis.

Our interviews took place in 2014 and 2015. Each visit lasted between one and two hours; the researcher took structured notes, and a closed-question questionnaire was completed by the respondent. In most cases, the CEO (68 percent) or the sales manager (24 percent) was interviewed, an approach applied in numerous studies using retrospective reports from strategic-level managers. Of the cases, 8.3 percent had missing values and were multiple amputated (Rubin, 1987) using the EM algorithm of LISREL software, which resulted in 258 analysed cases. The multiple amputation procedure secures the reliability of the results from non-random missing values. The results from the independent sample t-test comparing the means (2-tailed significance >0.05) of early respondents with late respondents excluded the presence of non-respondent bias.

Measures

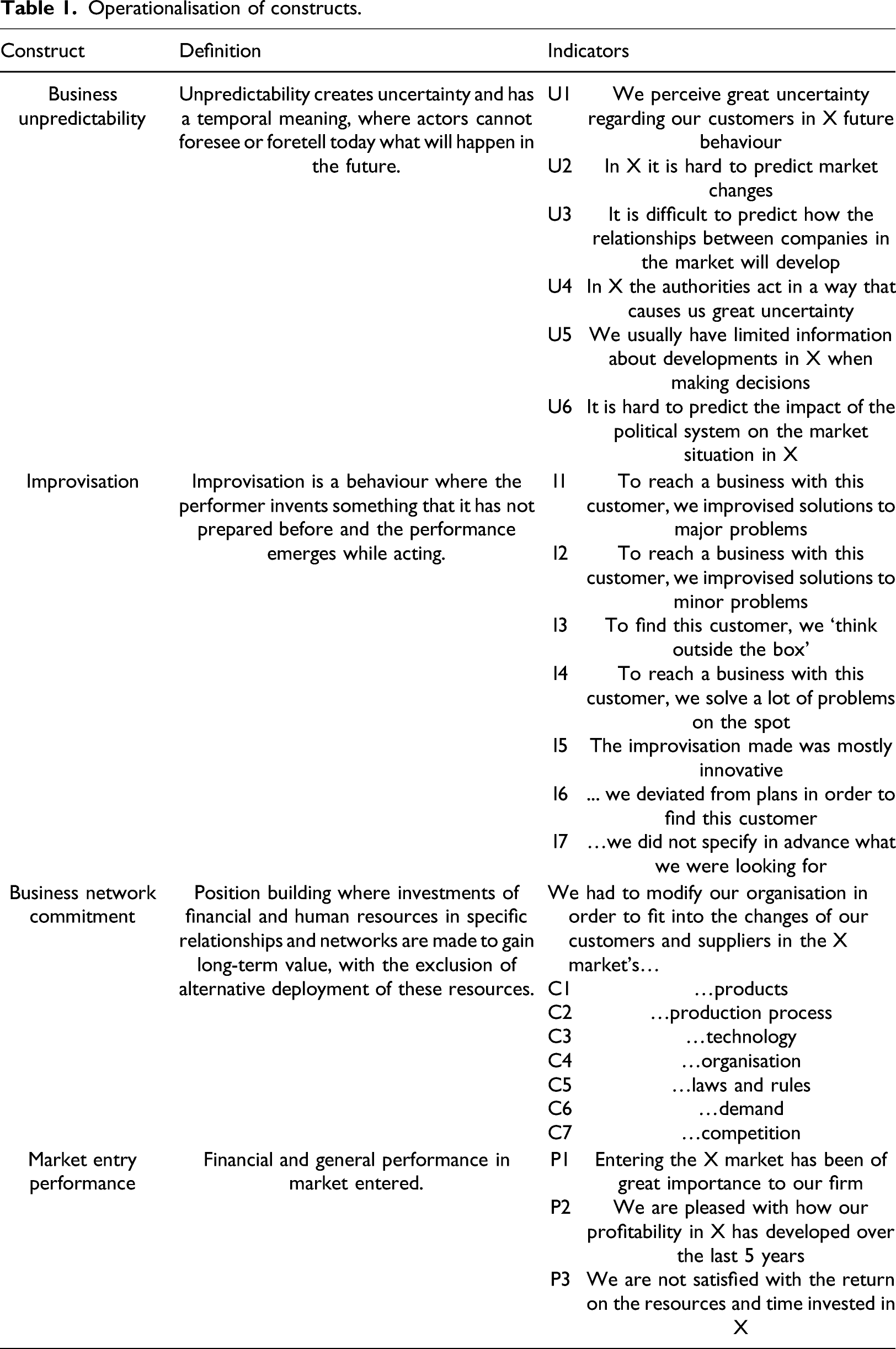

Operationalisation of constructs.

Exploratory factor analysis.

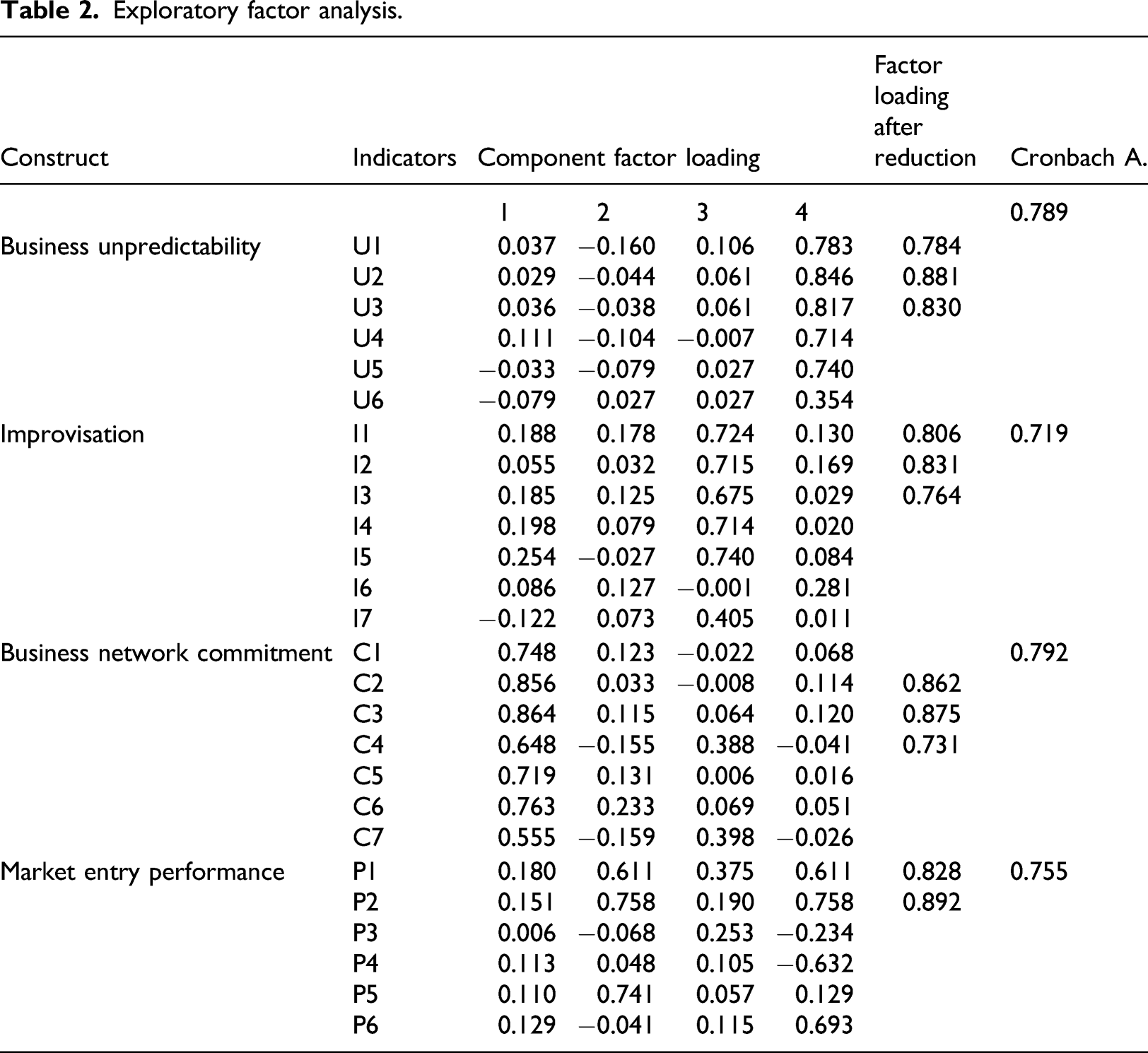

To establish the scales used to test the hypotheses, we imported the survey response into SPSS where we performed an exploratory factor analysis with varimax rotation. This allowed us to evaluate the scales based on eigenvalues, factor loadings and Cronbach alpha. We iteratively moved between construct definition and statistical values and could reduce the 11 indicators of our questionnaire into four valid and reliable factors. In this iteration, we followed established rules of thumb and considered a construct to be reliable and valid in statistical terms if the factor loadings were above 0.7, the cross-loadings below 0.3, the eigenvalues above 1 and the Cronbach alpha values above 0.7. The outcome of the exploratory factor analysis is provided in Table 2, where the final solution of the scale development is presented.

The measures evaluated as valid and reliable in the exploratory stage were next imported to LISREL, where a confirmatory analysis was performed. We evaluated model fit as well as the modification indices to ensure the construct validity and the reliability of the measures. The confirmatory analysis resulted in an RMSEA of 0.031 and a Goodness of Fit Index of 0.94. The non-existence of any modification indices between the latent constructs indicates construct validity and composite reliability. Consequently, we combined the exploratory and confirmatory technique to generate the most stable measures of our constructs and found that both the exploratory and confirmatory analyses generate a reliable and valid measurement model. The final scales used in LISREL for hypothesis testing are as follows:

Business Unpredictability: Based on the three components of our definition for business unpredictability, we use three items on a 7-point Likert scale (1: completely disagree, 4: neither agree nor disagree, 7: completely agree), capturing perceptions of dynamic changes in the customers’ behaviour, in the market in general, and in the network relationships. In the question put to the respondent, X represents the foreign market that the firm had entered within the last 7 years: a) We perceive great uncertainty regarding the future behaviour of our customers in X, b) In X it is hard to predict market changes, c) It is difficult to predict how the relationships between companies in the market will develop. The alpha values for the three items reached 0.789, and the lowest factor loading was 0.784 with AVE of 0.702, which exceeded the cut-off level of 0.5 (Fornell and Larcker, 1981).

Improvisation: Inspired by previous studies (Hmieleski and Corbett, 2006, 2008), we use three items on a 7-point Likert scale to assess the improvisational behaviour of the firm: a) To reach a business exchange with this customer, we improvised solutions to major problems, b) To reach a business exchange with this customer, we improvised solutions to minor problems, c) To find this customer, we had to think outside the box. The alpha values for the three items reached 0.719, and the lowest factor loading was 0.764. In the confirmatory analysis in LISREL, the items have an AVE of 0.694.

Business network commitment: To assess the business network commitment of the firm, we used three items evaluated on a 7-point Likert scale: We had to modify our organisation in order to fit with the changes of our customers and suppliers in the X market in terms of: a) The production process, b) The technology, c) The organisation. The alpha values for the three items reached 0.792, and the lowest factor loading was 0.731. In the confirmatory analysis in LISREL, the items have an AVE of 0.717.

Market entry performance: Market entry performance is assessed with two indicators that addressed strategic importance and profitability. Since there is no objectively available performance data on the foreign market level for SMEs, we needed to use perceptual items (Katsikeas et al., 2000). Attitudinal measurements of performance can be used as a reflective measure as earlier research states that respondents are equally inconsistent in their responses, but that responses have a central tendency and a variance (Zaller and Feldman, 1992), while the ‘true attitudes’ of respondents can be considered as fixed and stable over time. Thus, we assessed market entry performance with two indicators on a 7-point Likert scale: a) Entering the X market has been of great importance to our firm, b) We are pleased with how the profitability of our business in X has developed over the past five years. The alpha values for the two items reached 0.755, and the lowest factor loading was 0.828. In the confirmatory analysis in LISREL, the items have an AVE of 0.670.

Control variables: We included four control variables in the analysis. First, we controlled for the age of the firm since we expected older firms to have more well-developed and institutionalised routines (Autio et al., 2000). Second, we controlled for the size of the firm in terms of number of employees since we expected their available resources to influence the international behaviour. Third, we controlled for international experience with a variable based on the number of years since the firm’s first export sales, which we expected would indicate the international capabilities of the firm (Hilmersson and Johanson, 2020). Fourth, we included a variable separating family-owned firms from firms with alternative ownership, since previous research (Fernández and Nieto, 2006; George, et al., 2005) has indicated that ownership influences international behaviour and performance.

Marker variable: To check for the presence of common method variance biases and following the suggestions of Lindell and Whitney (2001), we included a marker variable that was theoretically unrelated to our other variables but part of the same database: ‘The contact with our bank’s domestic office(s) has been of high importance for our firm’s operations in our domestic markets’.

Data analysis and results

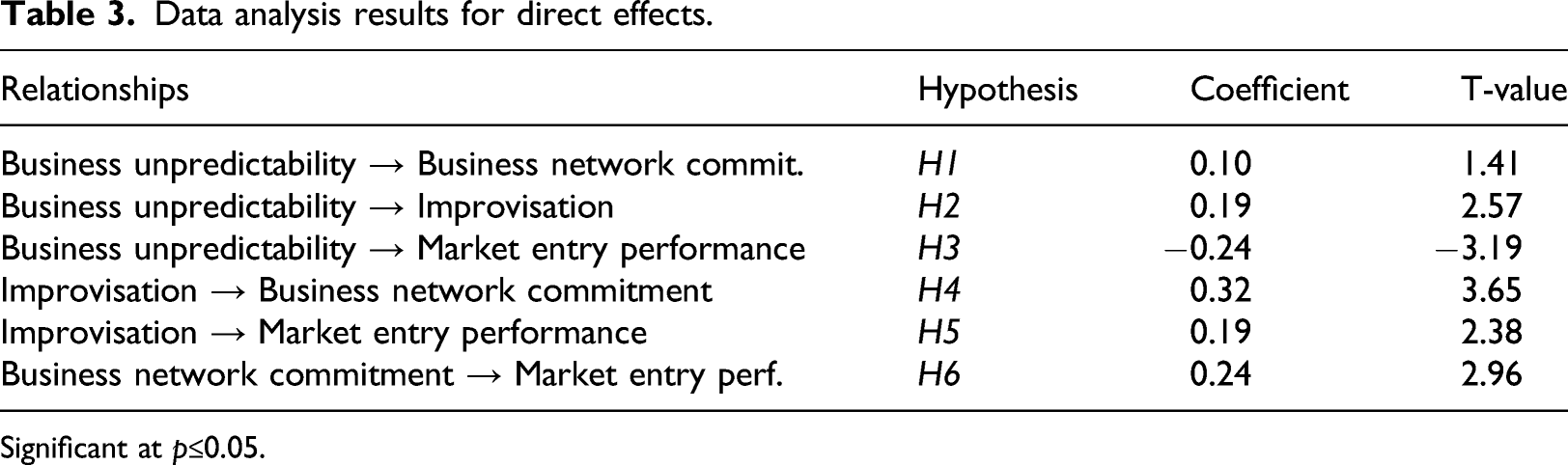

Data analysis results for direct effects.

Significant at p≤0.05.

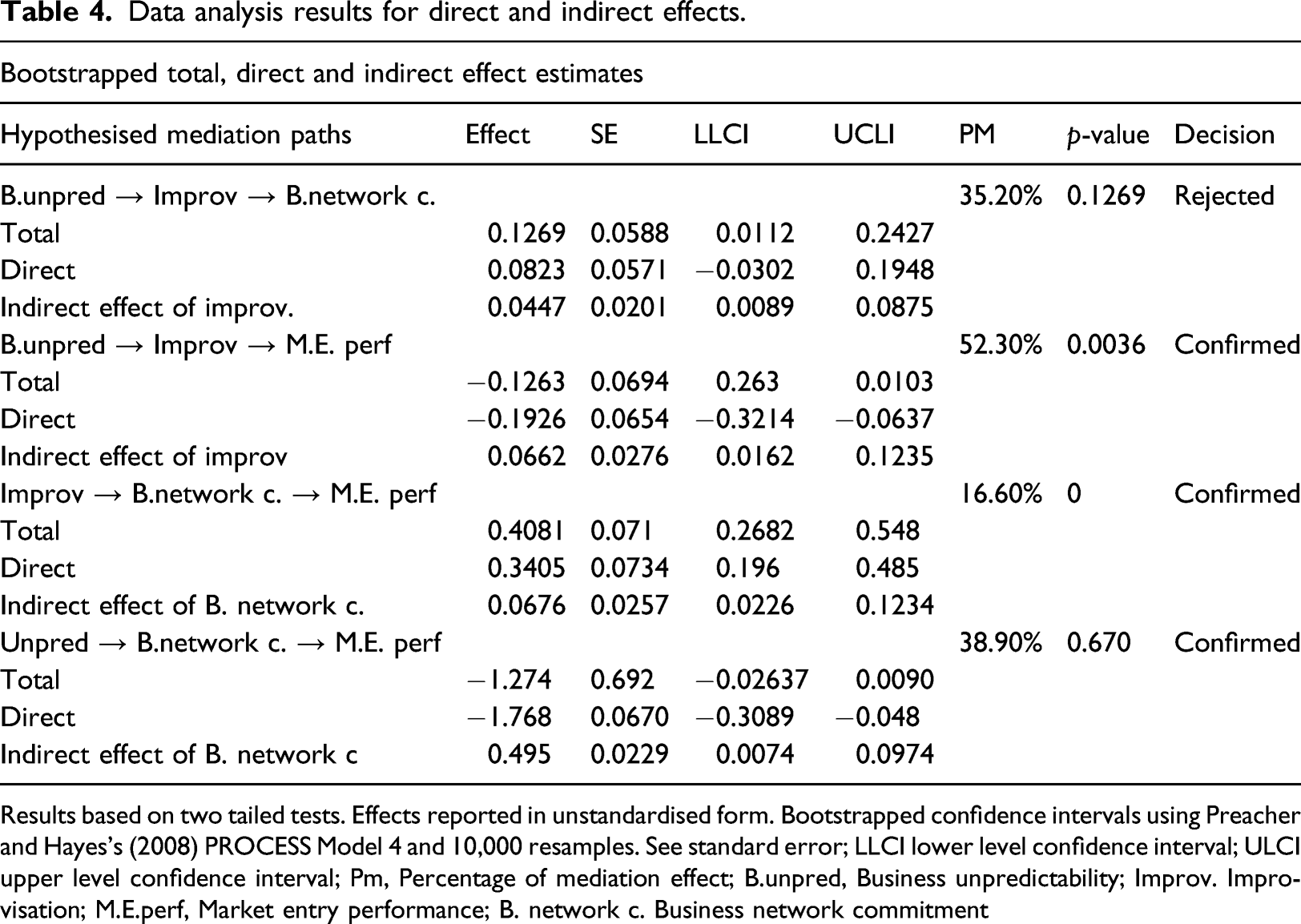

Data analysis results for direct and indirect effects.

Results based on two tailed tests. Effects reported in unstandardised form. Bootstrapped confidence intervals using Preacher and Hayes’s (2008) PROCESS Model 4 and 10,000 resamples. See standard error; LLCI lower level confidence interval; ULCI upper level confidence interval; Pm, Percentage of mediation effect; B.unpred, Business unpredictability; Improv. Improvisation; M.E.perf, Market entry performance; B. network c. Business network commitment

We used multiple methods to test our hypotheses. The direct effects, as well as the model structure, were examined using an SEM-based approach. In addition, we used Preacher and Hayes’s (2008) bootstrapping method to examine the statistical significance and the indirect effects of the hypothesised mediators (improvisation and business network commitment). Preacher and Hayes’s bootstrapping algorithm was used to produce 10,000 bootstrap resamples with a 95 percent bias-corrected confidence interval (MacKinnon et al., 2004; Preacher and Hayes, 2008). We chose the aforementioned technique to test for the significance of the mediation effect, because for the sample size of this study, bootstrapping does not rely on the assumption of a normal sampling distribution, which is only relevant to very large samples.

Additionally, this technique can constitute a remedy for potential endogeneity bias (Zaefarian et al., 2017). We examined the indirect effects of each mediator using Preacher and Hayes’s (2008) PROCESS macro in SPSS 24. The results (Table 3) were obtained using 10,000 bootstrap resamples and a 95 percent bias-correct confidence interval. Improvisation explained, in a statistically significant way (p>0.05), the relationship between business unpredictability and business network commitment, even though the confidence interval CI did not pass 0 (B = 0.0447, CI = 0.0089 to 0.0875). However, when testing for indirect effects to see if, and how, improvisation mediates the relationship between business unpredictability and market entry performance, we found the indirect effect to be positive, and statistically significant (B = 0.0662, CI = 0.0162 to 0.01235). The direct negative effect of business unpredictability on the market entry performance was reduced by 52.3 percent through improvisation, confirming hypothesis 3b. Finally, business network commitment was found to significantly explain the relationship between improvisation and market entry performance by 16.6 percent of the total effect (B=0.0676, CI = 0.0226 to 0.1234), confirming a mediating or indirect relationship in the model.

Discussion

Entering a foreign market with unpredictable conditions brings challenges and opportunities (Johanson and Vahlne, 1977). A quick, improvised response may, under such circumstances, give rise to first mover advantages (Lieberman and Montgomery, 1988) and improved performance. Research is limited on the causes and outcomes of improvisation in an internationalisation context (Nemkova et al., 2015; Arend et al., 2015). Addressing these gaps, this article takes an empirical approach to the relationship between business unpredictability, improvisation, business network commitments and market entry performance.

We did not find support for the first hypothesis (H1), where we expected business unpredictability to have a positive influence on business network commitment, which contradicts Bai et al. (2021). We expected that when the market is unpredictable, the firm turns to those customers and suppliers that are relatively predictable – the ones with which they have developed stable relationships and so, are deemed less risky. There could be several reasons why this hypothesis was not supported. As unpredictability increases, so does the reluctance to invest in any kind of business or business relationship in the foreign market (Santangelo and Meyer, 2011); SMEs prefer – at least to a certain point – to commit to the network when unpredictability increases, while not sacrificing or investing anything. It could also be assumed that when unpredictability is too great, SMEs prefer to withdraw resources from both their networks and indeed, from the market in general.

Unpredictability makes the market less attractive for investment even if the firm’s relationships may prosper at that moment in time. Changes in institutions as well as more general business characteristics, like distribution systems and banks, may moderate these relationships, something for which business relationships may not be able to compensate. We found support for our second hypothesis (H2), stating that market unpredictability will lead to improvisational behaviour. The argument that ambiguity, uncertainty and unpredictability drive improvisation is well-established in the management (Ciuchta, O'Toole, and Miner, 2021; Macpherson et al., 2021), innovation management (Magni et al., 2013; Vera et al., 2016) and the entrepreneurship literature (Balachandra, 2019).

Our third hypothesis (H3a) contended that business unpredictability has a negative impact on entry performance. Its confirmation reflects the idea that risk and uncertainty need specific management so as not to have a negative effect (Catanzaro and Teyssier, 2021). It should, however, be interpreted in light of the second hypothesis, confirming that firms facing unpredictable markets turn to improvisation. This indicates that the path to high performance, and further penetration in unpredictable business markets, should include improvisation.

The confirmation of hypothesis 3b, which proposes the mediating effect of improvisation between business unpredictability and market performance, supports the central role of improvisation in the internationalisation of firms. Here, our findings contradict earlier research. Hughes, Hodgkinson, Hughes, and Arshad (2018) did not find any support for this hypothesis in their study in the context of emerging markets. In our study, which is not limited to emerging markets, improvisation not only explains 52.3 percent of the total relationship between unpredictability and market performance, but also signifies a reduction in the negative direct effect between unpredictability and market performance. Thus, the inclusion of improvisation in the hypothesised model enables it to provide a more complete view of the mechanisms of internationalisation.

In the fourth hypothesis (H4), we posited a positive relationship between improvisation and business network commitment based on earlier research (Hilmersson et al., 2021; Dorra et al., 2021). To gain a position, the firm needs to commit to the network it enters as this network is likely to differ from other networks in which the firm operates. An improvised way of acting may, at times, be necessary so that solutions can be found to emerging problems and also, that opportunities within in the network can be pursued. These solutions may, in turn, lead to the identification of previously unknown opportunities during the market entry process – opportunities that, due to their novel nature, may create a need for further improvised solutions. Such improvised solutions represent investments in terms of business network commitments and may concern the firm’s production processes or technologies, or the way it organises its business. The confirmation of this hypothesis lends support to this reasoning, thereby indicating an important outcome of improvisation during market entry processes. We thereafter hypothesised that improvisation has a positive effect on market entry performance (H5); this was confirmed. This finding supports earlier research in the field (Adomako et al., 2018; Bingham, 2009). By breaking away from previous patterns, the firm is presented with novel opportunities. By thinking outside the box, the firm begins to act in new ways, which, despite maybe costing more, have the potential to generate higher value than would the repetition of previous actions.

In contrast to the claim that there is a causal relationship between market entry performance and business network commitment – that is, when firms enjoy something of value, they are willing to commit – the supported hypothesis H6 informs us about the opposite direction of this relationship, that making business network commitments may be a rewarding path to improved performance. By committing organisation, production and technologies to the business network, firms create conditions that may result in high performance (Prashantham et al., 2018). By committing to the network, firms can reap further value from their investment – but the main value and profit do not perhaps result from the general activities in such foreign markets, but rather from the activities performed in networks. Our analysis demonstrates that improvisation is critical in unpredictable markets. It fulfils a mediating function in the model; the path to entry performance is to be found through improvisation.

Conceptual implications

Our findings demonstrate that an improvised approach can be used to mitigate negative performance in unpredictable markets and that such negative performance can be further reduced by the business network commitments that improvisation tends to stimulate. These direct and indirect positive effects of improvisation on market entry performance provide empirical evidence of the central role that improvisation plays in internationalisation. Previous studies that interpreted improvisation as being an irrational strategy do not provide the whole picture (Chandra et al., 2012; Newark, 2018). Based on our findings, the concept of improvisation can be seen in a new light, namely, as a relevant strategy that firms can adopt when the market is unpredictable.

The extent to which a foreign market differs from the home market has been explored at length whereas business unpredictability tends to be a theoretical assumption so, is more rarely empirically studied. Furthermore, although knowledge is probably the factor that has attracted the most attention in internationalisation research, it has yet to be related to unpredictability and improvisation. Extant theory assumes international markets are different, yet stable and predictable (Hilmersson and Jansson, 2012). By relaxing this assumption, we have shown that unpredictable markets influence the strategic behaviour of the firm. Our findings support those of Hilmersson et al. (2015), who showed that former international experience has less value in changing markets, while Alpkan et al. (2007) show the need to be flexible in such environments. While the literature often treats improvisation as a random strategy, applied by the naïve and ignorant firm, we suggest that it can be a deliberate and relevant choice – indeed, at times even the best approach in unpredictable markets. As improvisation in such a case is based on experience, combined with thinking ‘outside the box’, and doing things in new ways, the role of experiential knowledge in unpredictable markets still needs to be analysed in more depth. The result of too much experiential knowledge may be that the firm sticks to its past strategies, even when a market requires an agile approach. Experiential knowledge gained from unpredictable markets may, on the other hand, reassure the firm that it would be naïve to rely too much on formal planning in unpredictable markets.

While decision-making based on formal strategies and plans prevails in theories explaining internationalisation, empirical studies indicate a great distance between this approach and real decision-making by entrepreneurs (Gilboa, 2009). Indeed, decision-makers have been repeatedly shown to make decisions in violation of objective and strategic thinking, deliberately applying biases because they acknowledge the uncertainty of the market in which they operate (Alvarez and Barney, 2007). Market turbulence might persuade decision-makers to improvise by convincing them they do not possess sufficient knowledge to thrive or that their knowledge will constantly become obsolete, making it impossible to devise plans that are valid over time. They might choose to reject their plans and instead act in a creative and flexible manner, a process that is often explained as a leadership style rather than as a rational thought process (Newark, 2018). In cases like this, improvisation could be a purposeful course of action, even if it is a consequence of ignorance rather than of knowledge. Our findings, thus, shed light on previously observed inconsistencies between empirical research on decision-making and internationalisation theories that overlook the intentional ‘unintentionality'.

This study does not, however, confirm the often implied assumption that unpredictability encourages firms to make commitments to customers and suppliers in their business network in order to reduce risk (Johanson and Vahlne, 2009). In unpredictable markets, where fast decision-making is essential, improvisation is important to attain higher performance; it is insufficient to simply follow Johanson and Vahlne’s (2009) suggestion that by committing to networks in the foreign market, a firm will be able to enter an unpredictable market. The entry must be characterised by agility and flexibility which, in turn, can clarify to which network actors the firm should commit. Thus, the main insight from our model is that there is no direct relationship between unpredictability and network commitment; instead, this relationship is mediated by improvisation. Entrepreneurial firms improvise and when doing so, they commit to specific network actors as a means to manage the unpredictability and to mitigate negative performance effects in unpredictable markets.

Interestingly, and a contribution in itself to previous calls for research on commitment benefits, our results demonstrate that successful entry is not only a matter of committing to the foreign market’s culture or institutions (Calof and Beamish, 1995) or to the market in general (Johanson and Vahlne, 1977). Rather, it is also about the firm committing its organisation, technology and production to specific actors in the network confirming suggestions by Sandberg (2013), who argues that attention should be shifted from entry modes, to the network entry node.

Managerial implications

There are certain situations and contexts, such as unpredictable markets, when planning may be a waste of both time and resources even guiding actions in a direction that becomes obsolete even before the plan has been executed. Improvisation may then be necessary. By learning from the resulting novel experiences, a greater value may be achieved over time as new capabilities emerge. Improvisation may lead to a variety of development paths, which calls for leadership that addresses integrative and coordinative issues. Improvisation is however, not inherently either positive or negative (Hadida et al., 2015; Baker et al., 2003). This study has indicated benefits resulting from improvisation, but unlimited improvisation may cause stress and psychological burnout, and result in a lack of focus and unwanted variation (Hatch, 1999). Improvisation can, in an unpredictable market, be a very deliberate and rational decision. However, this implies an awareness of the extent to which the foreign market is unpredictable. Otherwise, the discovery will come as a surprise. We advise entrepreneurs to prepare the organisation and to outline an improvisation strategy, which in turn will require autonomy and delegated authority within the organisation.

Limitations and suggestions for further research

This study comes with some limitations that must be considered. First, it only covers Swedish SMEs operating in the manufacturing sector. Second, studies are needed on the various forms of improvisation, their relationship with entry performance, and the way they either reinforce or counteract each other. Also, studies applying a qualitative method could provide increased understanding of the underlying mechanisms, and longitudinal data could also be a more sophisticated approach to understanding the degree of improvisation applied under various circumstances. Third, our performance measures are not based on register-data since such data are not publicly available. Future studies may seek to develop more sophisticated measures. Fourth, further research using longitudinal methods could reveal the processual nature of improvisation effects on internationalisation. Such studies could also build on a more holistic network view by identifying network actors (beyond customers and suppliers) who are important in the management of unpredictability. Finally, it would be valuable to analyse what concepts influence unpredictability and how these are related to experiential knowledge in the internationalisation process.

Conclusions

It is evident that markets are rarely stable; they change and are often unpredictable which can have a negative impact upon firm performance. Our results build on insights from the improvisation literature that are integrated with insights from a network perspective on internationalisation. We contribute to internationalisation theory and the international entrepreneurship literature by showing that improvisation mediates the negative relationship between market unpredictability and firm performance. Together with resources committed to the business network, improvisation is important in mitigating the negative performance consequence of unpredictability. These findings are important as they elucidate the rationality behind the seemingly irrational improvisational behaviour and point at important ways to improve firm performance in unpredictable internationalisation processes. Improvisation can furthermore, be prepared for and learned. It is, thus, a way of acting that needs to be acknowledged, rather than regarded as inferior to forecasting and planning.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.