Abstract

This article explores whether new firms managed by founder-chief executive officers (CEOs) are more likely to survive than those managed by successor-CEOs in times of crisis. Drawing on the concept of ‘resilience’ to adversity, we argue that founder-CEOs increase the likelihood of new firm survival, especially in times of crisis. Using a sample of Japanese firms founded during the 2003–2010 period, we examine the impact of founder-CEO succession on new firm survival. The analysis shows that new firms managed by founder-CEOs are less likely to liquidate than those managed by successor-CEOs, especially during the 2008–2009 financial crisis. This suggests that founder-CEOs are more resilient to crises than successor-CEOs. In contrast, new firms managed by successor-CEOs are more likely to exit via merger than those managed by founder-CEOs, regardless of macroeconomic conditions. These findings are robust after controlling for the endogeneity of CEO succession.

Introduction

A rich stream of research on entrepreneurship has emphasised the role of founders (or entrepreneurs) in a firm’s post-entry performance (Grilli et al., 2020; Karami and Tang, 2019; Kato and Honjo, 2015). Some are still managed by founders as chief executive officers (CEOs) after incorporation, and founder-CEOs play a critical role in initiating new ideas and setting initial conditions (Samuelsson et al., 2021; Wang et al., 2019). However, in other firms, founder-CEOs are replaced by successor-CEOs (i.e. non-founder-CEOs). CEO succession (synonymously, CEO turnover) clarifies significant differences between founder- and successor-CEOs (Wasserman, 2003; Willard et al., 1992). Indeed, scholars have focused on performance differences between firms managed by founder-CEOs and those managed by successor-CEOs (Fahlenbrach, 2009; Gao and Jain, 2012; Jain and Tabak, 2008). Some, moreover, have examined whether firms managed by founder-CEOs perform better in terms of investment and profitability (Gao and Jain, 2011; He, 2008). These studies have provided evidence on the role of founder-CEOs compared with successor-CEOs in firm performance.

However, despite the higher proportion of founder-CEOs in privately held firms, previous studies tend to focus on large established or publicly traded firms (Fahlenbrach, 2009; Jain and Tabak, 2008; Willard et al., 1992). The impact of CEO succession varies between large bureaucratic organisations and small, young ones, and founder-CEO succession differs considerably from later-stage succession (Wasserman, 2003). As the impact of CEO succession on firm performance, such as survival and exit, presumably depends on the firm’s life cycle, we should pay more attention to tracing CEO succession while considering firm age. Although the role of CEOs in small, young firms is more critical than that in large established firms, relatively little research on CEO succession has examined new firm performance. Critical issues remain unresolved regarding the impact of founder-CEO succession on new firm survival. While founder-CEO succession may significantly affect firm survival, very few studies have examined performance differences between new firms managed by founder-CEOs and those managed by successor-CEOs (Chen and Thompson, 2015; Wasserman, 2003). Focusing on new firms could fill a critical research gap on the role of founder-CEOs in firm performance after incorporation.

As expected, founder-CEOs possess intrinsic attributes incomparable to successor-CEOs, including professional CEOs (Gao and Jain, 2011; He, 2008). 1 Compared with professional CEOs, founder-CEOs do not necessarily have superior management knowledge and skills, which differ from entrepreneurial knowledge and skills, in business sustainability. Meanwhile, founder-CEOs have more advantages in organisation-specific skills, as they have shaped their organisations from inception (Fahlenbrach, 2009). In particular, founder-CEOs possess a strong psychological attachment and express commitment to their firms (He, 2008; Nelson, 2003). According to stewardship and agency theories, founder-CEOs tend to pursue organisational interests by acting more like organisational stewards (Wasserman, 2006). Drawing on the concept of ‘resilience’ to adversity, we emphasise that founder-CEOs increase the possibility of new firm survival, especially in times of crisis. Entrepreneurial resilience, which is the ability of founders to persist under difficult business circumstances (Santoro et al., 2020, 2021), is expected to play a pivotal role in promoting entrepreneurship in the face of adversity. In the literature, some studies have examined whether entrepreneurial resilience relates to entrepreneurial intention (Bullough and Renko, 2013; Bullough et al., 2014). Others have provided evidence on the relationship between entrepreneurial resilience and perceived success (Santoro et al., 2020, 2021). However, their findings were limited to evidence from subjective measures of entrepreneurial resilience obtained from questionnaire surveys, and exit cases could not be identified. There is a paucity of research on whether entrepreneurial resilience helps sustain businesses in times of crisis.

This study explores whether new firms managed by founder-CEOs are more likely to survive than those managed by successor-CEOs in times of crisis. Using a sample of Japanese firms founded during the 2003–2010 period, we examine the impact of founder-CEO succession on new firm survival. We identify founder-CEO succession using the COSMOS2 database compiled by Teikoku Data Bank (TDB), one of the major credit investigation companies in Japan, and construct a data set of new firms. Moreover, this study examines whether the impact of founder-CEO succession on new firm survival depends on the exit route. Indeed, previous studies have addressed the exit routes of new firms (Cefis and Marsili, 2011; Coad and Kato, 2020; Grilli, 2011; Kato and Honjo, 2015). In particular, exit via merger differs considerably from other exit routes, such as bankruptcy and voluntary liquidation. In other words, mergers may in part include successful exits, while bankruptcy can be regarded as an unsuccessful exit. Thus, we also discuss how new firms managed by founder-CEOs exit in times of crisis.

Using a discrete-time duration model, we demonstrate that new firms managed by founder-CEOs are less likely to liquidate than those managed by successor-CEOs. The results reveal that during the 2008–2009 financial crisis, the impact of founder-CEO succession on liquidation, including bankruptcy, is positive, indicating that new firms managed by founder-CEOs are less likely to liquidate than those managed by successor-CEOs, especially during a financial crisis. These findings suggest that founder-CEOs tend to exhibit resilience to adversity, which positively influences new firm survival. In addition, new firms managed by successor-CEOs are more likely to exit via merger than those managed by founder-CEOs.

The major contributions of this study are threefold. First, it provides empirical evidence on the impact of founder-CEO succession in new firms. To date, numerous scholars have examined the impact of CEO succession on the performance of large established firms, irrespective of the firm’s life cycle (Beatty and Zajac, 1987; Worrell and Davidson III, 1987). However, very few studies have examined the impact of founder-CEO succession among new firms (Chen and Thompson, 2015; Wasserman, 2003, 2017). 2 We present empirical evidence on how founder-CEO succession is associated with new firm survival, which could contribute to a better understanding of performance differences between new firms managed by founder-CEOs and those managed by successor-CEOs.

Second, this study provides new evidence on the impact of founder-CEO succession—that is, a founder’s exit—on the probabilities of liquidation, including bankruptcy, and exit via merger. 3 The results reveal that new firms managed by founder-CEOs are less likely to liquidate than those managed by successor-CEOs. In addition, new firms managed by successor-CEOs are more likely to exit via merger. These suggest that the role of founder-CEOs in new firm survival is associated with exit routes.

Third, we provide new insights into how the impact of founder-CEO succession on new firm survival differs according to macroeconomic conditions. Previous studies have discussed the emotional and psychological functioning of founders, through examining variables such as entrepreneurial self-efficacy and resilience, in the face of adversity (Bullough and Renko, 2013; Bullough et al., 2014). While CEOs with resilience, agility and flexibility should be appointed in the face of adversity, there is little evidence on how founder-CEO succession affects firm survival in an unexpected recession period. By examining founder-CEO succession in new firms, especially during the 2008–2009 financial crisis, we provide comprehensive evidence that founder-CEO succession has a significant impact on liquidation in times of crisis. Our evidence suggests that founder-CEOs tend to be more persistent under adverse conditions, as new firms managed by founder-CEOs are less likely to liquidate during the financial crisis. Such findings provide managerial implications for founder-CEO resilience to crises.

The remainder of this article is organised as follows. The next section introduces relevant literature and proposes hypotheses. In the Data and method section, we explain the variables used in the analyses. We then present the empirical results, including the managerial and policy implications of our findings. The Discussion and conclusions section provides a summary of the key contributions of our findings.

Literature review and hypothesis development

Role of founders in new firms

The management and economics literature has debated the role of CEOs on strategy and performance (Bandiera et al., 2020; Mackey, 2008; Weng and Lin, 2014). According to upper echelon theory (Hambrick, 2007; Hambrick and Mason, 1984), organisational actions and outcomes can be viewed as resulting from the idiosyncratic traits of individual executives or top management teams (Schuster et al., 2020). Among the top management team members, CEOs generally play a pivotal role in setting strategy and making decisions, such as investment, especially in shaping organisational architecture through their decisions, including incentives (Hambrick and Quigley, 2014).

New firms are endowed with knowledge and experience at birth through the human capital of founders (Dencker et al., 2009: 516). From the resource-based view of the firm, it is conceivable that the founder’s human capital is a valuable resource significantly associated with organisational outcomes (Ganotakis, 2012; Honjo et al., 2014; Krause et al., 2016). As discussed, founders play a critical role in initiating new ideas and setting initial conditions (Samuelsson et al., 2021; Wang et al., 2019). Founders require the ability to discover and exploit entrepreneurial opportunities for business start-ups (Corbett, 2007; Shane and Venkataraman, 2000). As new firms generally have limited resources, and lack a business history and track record, the founder’s role is more crucial, especially in the early stage of the growth process. Undoubtedly, founders must have management knowledge and skills to sustain businesses. In this context, founders play a key role in determining new firm survival.

Meanwhile, there are critical differences between starting businesses and managing successful firms (Boeker and Karichalil, 2002; Boeker and Wiltbank, 2005; He, 2008). Management styles and capabilities change as new firms evolve and grow, and the focus shifts to challenges associated with managing organisations (Gao and Jain, 2012; Jain and Tabak, 2008). Top managers need different management skill sets in various stages of a firm’s life cycle (Gounopoulos and Pham, 2018). Founder knowledge and skills relating to business creation may no longer be significant in the later stage. In addition, some founders may lack management knowledge and skills or have less incentive to enhance financial performance. New firms may require specific human capital suitable for management to survive after incorporation. It is plausible that founders do not always have the management knowledge and skills required in each stage. Under the premise of different knowledge and skills required in each stage, founders without the appropriate management knowledge and skills to sustain businesses should be replaced by successors.

Nevertheless, founders may devote considerable investment of time, energy, efforts and resources to ensure that their firms survive and grow, and they derive intrinsic benefits by virtue of firms that often represent their lifetime achievement (Gao and Jain, 2012). This propensity may lead to entrepreneurial resilience enabling persistence under critical business circumstances (Santoro et al., 2020, 2021). More importantly, founders may struggle to sustain businesses with ‘resilience’ when they face adverse conditions. Resilience is the ability to go on with life, or to continue living a purposeful life, after hardship or adversity (Bullough and Renko, 2013; Tedeschi and Calboun, 2004). It is conceivable that such psychological resources of founders, including resilience, are valuable for new firm survival.

Founder-CEOs versus successor-CEOs

The impact of founder-CEO succession on firm performance has been debated (Adams et al., 2009; Fahlenbrach, 2009; Gao and Jain, 2011, 2012; He, 2008). The transition from a founder-CEO-led start-up to a professionally managed firm entails a significant change in the firm’s organisation and strategy (Serra and Thiel, 2019). It is plausible that founder-CEO succession affects new firm performance because of the prominent role of CEOs in new firms.

Founder-CEOs have a number of advantages over successor-CEOs. First, founder-CEOs can accumulate specific knowledge about the firm because of their involvement in its creation and management (He, 2008). New firms managed by founder-CEOs can easily share strategic directions in organisations, which may be able to overcome challenges in the early stage. In addition, founder-CEOs often retain significant ownership in firms (Fahlenbrach, 2009; Nelson, 2003). Given this, founder-CEOs can reduce agency conflicts between ownership and management. Moreover, founder-CEOs make effort to ensure that their firms survive and grow, as they derive intrinsic benefits by virtue of firms that often represent their lifetime achievement (Gao and Jain, 2012). Stewardship theory is also likely to describe the behaviour of founder-CEOs (Davis et al., 1997; Gao and Jain, 2012). 4 As discussed, founder-CEOs tend to pursue organisational interests by acting more like organisational stewards (Wasserman, 2006). Moreover, several scholars have emphasised the important of founders’ psychological attributes, such as entrepreneurial self-efficacy and resilience (Bullough and Renko, 2013; Bullough et al., 2014; Corner et al., 2017). Founder-CEOs may be more intrinsically motivated by non-pecuniary benefits than successor-CEOs (Wasserman, 2006) and tend to have higher levels of intrinsic motivation and a long-term approach (Fahlenbrach, 2009). In particular, psychological attributes such as entrepreneurial resilience are vital for firm survival, especially in the face of adversity (Bullough and Renko, 2013; Corner et al., 2017; Santoro et al., 2020, 2021).

Conversely, founder-CEOs also have disadvantages over successor-CEOs. First, as the organisational life cycle theory suggests, management styles and capabilities change as firms evolve and grow (Gounopoulos and Pham, 2018; Jain and Tabak, 2008). Entrepreneurial skills in the start-up stage differ from managerial skills in the later stage. In this respect, it is more effective to replace founder-CEOs with successor-CEOs who possess professional management knowledge and skills, which may increase the probability of firm survival. In addition, although founder-CEOs can reduce agency conflicts between ownership and management, they may exhibit stronger entrenchment behaviour (Gao and Jain, 2011). Moreover, some founder-CEOs have less incentive to expand, as they start businesses for their own self-interest. In these respects, new firms managed by founder-CEOs may underperform those managed by successor-CEOs. Furthermore, founder-CEOs may lose flexibility when market and economic conditions change after starting businesses if they have a propensity to cling to their initial ideas. Firms often require flexibility to respond to unforeseen and unanticipated changes (Zander, 2007). Particularly when new firms face adverse conditions, they may require entrepreneurial mobility, broadly defined as the entrepreneurial activity that involves the movement of an entrepreneur from the current context to another (Wright, 2011; Wright et al., 2012). From the perspective of entrepreneurial mobility, successor-CEOs may be able to alter the inherited strategic orientation by introducing new management resources and strategies that differ from those of founder-CEOs.

Comparing founder-CEOs with successor-CEOs can enhance our understanding of the effect of top management on firm performance. Indeed, previous studies have examined the impact of founder control, including founder turnover (i.e. founder-CEO succession), on firm performance, such as valuation and survival (Chen and Thompson, 2015; Wasserman, 2017). These studies indicate pronounced performance differences between firms managed by founder-CEOs and those managed by others.

Role of CEOs in times of crisis

The extant literature recognises that entry and exit depend on market and economic conditions (Geroski et al., 2010; Mata, 1996; Parker et al., 2012; Santarelli and Vivarelli, 2007). Given that potential founders avoid unfavourable conditions, it is likely that founders launch new firms at favourable times. In this respect, founders tend to start their businesses while expecting favourable conditions. Conversely, in an unexpected recession, founders face difficulties sustaining their businesses. They must overcome risk and adversity and adapt to market and economic conditions. Such an unexpected recession may bring about a necessary change in the role of CEOs, including management styles. As noted, management styles and capabilities change as new firms evolve and grow, and the top management needs different skill sets during various stages of growth (Gounopoulos and Pham, 2018; Jain and Tabak, 2008). In addition, macroeconomic conditions, such as booms and recessions, are associated with adaptive management styles formed by potential CEO career experiences. It is likely that CEOs have more conservative management styles during a recession period (Schoar and Zuo, 2017); moreover, a powerful CEO can be beneficial during a financial crisis but not so under normal circumstances (Dowell et al., 2011). The more appropriate management style depends on market and economic conditions. In other words, CEOs must be able to adapt to environmental changes useful in sustaining new businesses.

As financial and labour markets are subject to market and economic conditions, the impact of founder-CEO succession on firm performance depends on these conditions. The supply of external finance lessens during a recession (Cowling et al., 2012); thus, new firms face difficulties accessing financing from capital markets during such times significantly affecting survival. It may also be difficult to find potential successors with appropriate management knowledge and skills in CEO labour markets. Accordingly, new firms may face difficulties conducting founder-CEO succession, depending on market and economic conditions, even if they require founder-CEO succession.

It has been argued that a founder’s human capital affects firm survival (Santarelli and Vivarelli, 2007; Unger et al., 2011); thus, firms managed by founders with a higher level of human capital are more likely to persist (Grilli, 2011; Kato and Honjo, 2015). In contrast however, founders with a higher level of human capital may decide to discontinue operations as more attractive options are available to them (Bates, 2005). Moreover, founder networks are associated with the successful outcomes of new firms (Witt, 2004). Most, but not all, founders seek external resources, such as financial capital, when starting their businesses. Founder networks are often useful in acquiring external financing because investors use private information about the founders (Shane and Cable, 2002).

Importantly, appreciating psychological and situational factors are indispensable for a better understanding of founder or CEO behaviour, depending on market and economic conditions. Founder-CEOs exhibit a greater propensity to take risks while proactively responding to environmental opportunities (Kumar et al., 2020). In particular, small firms must be more resilient and flexible in coping with the disequilibrium caused by economic recession (Cowling et al., 2015). Indeed, the literature has highlighted entrepreneurial resilience (Corner et al., 2017; Santoro et al., 2020, 2021), and some studies, although limited to evidence from subjective measures of entrepreneurial resilience obtained from questionnaire surveys, have identified whether entrepreneurial resilience is related to entrepreneurial intention and perceived success (Bullough and Renko, 2013; Bullough et al., 2014; Santoro et al.,2020, 2021). However, there is little evidence on how founder-CEO succession is associated with new firm survival in times of crisis. From the entrepreneurial resilience perspective, we pay more attention to the impact of founder-CEO succession on new firm survival over time, including in a recession period. An investigation using the case of founder- and successor-CEOs would provide a more comprehensive understanding of the role of CEOs in new firm survival.

Hypotheses development

There are several reasons why new firm survival differs between firms managed by founder-CEOs and those managed by successor-CEOs. Founder-CEOs can accumulate specific knowledge about firms because of involvement in their creation and management (He, 2008). However, some founder-CEOs may have less incentive to expand, as they start businesses for their own self-interest. Given that successor-CEOs with professional management knowledge and skills increase the probability of firm survival, it is more effective to replace founder-CEOs. From the perspective of psychological functioning, however, founder-CEOs have a higher level of intrinsic motivation and may exert more effort to sustain businesses. Founder-CEOs are more likely to possess strong psychological attachment and express commitment to their firms (He, 2008; Nelson, 2003). According to stewardship and agency theories, founder-CEOs may intrinsically have advantages over successor-CEOs (Wasserman, 2006). New firms managed by founder-CEOs are less likely to face agency conflicts between ownership and management (Gao and Jain, 2012). Founder-CEOs act less like self-interested agents and more like organisational stewards (Wasserman, 2006). Founder-CEOs may struggle to sustain their businesses, as they derive intrinsic benefits by virtue of firms that often represent their lifetime achievement (Gao and Jain, 2012). Therefore, new firms managed by founder-CEOs have more incentive to survive than those managed by successor-CEOs. To identify whether founder-CEOs have advantages in terms of firm survival, we examine the following hypotheses:

New firms managed by founder-CEOs are less likely to liquidate than those managed by successor-CEOs. With this hypothesis, we provide empirical evidence that founder-CEOs sustain their businesses, which is consistent with arguments on the behaviour and performance of founder-CEOs based on stewardship and agency theories (Gao and Jain, 2012; Wasserman, 2006). As noted, previous studies have addressed the exit routes of new firms, including merger (Cefis and Marsili, 2011; Coad and Kato, 2020; Grilli, 2011; Kato and Honjo, 2015). Essentially, exit via merger differs from other exit routes, such as bankruptcy and voluntary liquidation. Meanwhile, founder- and professional CEOs have different motivations for adopting takeover resistance strategies. Founder-CEOs have more incentive to sustain their businesses rather than to liquidate their firms, including exit via merger, as they possess strong psychological attachment and express commitment to their firms (He, 2008; Nelson, 2003). Such attachment of founder-CEOs to their businesses may make them less likely to sell their firms. In addition, potential bidders may find it more difficult to overcome founder-CEO resistance strategies (Gao and Jain, 2012). Conversely, firms that have already been transferred for management to successor-CEOs are more attractive to acquisition. Moreover, given that firms are transferred for management to successor-CEOs with a larger professional network, founder-CEO succession may encourage firms to engage in mergers because their personal networks affect the likelihood of mergers and the performance of merged entities (El-Khatib et al., 2015). Specifically, serial entrepreneurs have an incentive to sell their firms to partners seeking business expansion (Westhead and Wright, 1998). Thus, the likelihood of a merger may be associated with CEO turnover. It is plausible that new firms that successor-CEOs have already managed tend to be transferred to other firms. Therefore, founder-CEOs are less likely to exit via merger than successor-CEOs. To investigate the differences between founder- and successor-CEOs, according to exit routes, such as mergers, we consider the following hypothesis:

New firms managed by founder-CEOs are less likely to exit via merger than those managed by successor-CEOs. By identifying the differences between liquidation and exit via merger, we show the different roles of CEOs in firm survival and exit. In addition, we emphasise the importance of exit routes regarding founder-CEO succession. The role of CEOs varies according to market and economic conditions. Although CEOs struggle to sustain their businesses in a recession, a financial crisis significantly influences the role of CEOs in firm survival. Successor-CEOs with more appropriate management knowledge and skills in times of crisis, such as the 2008–2009 financial crisis, may be more advantageous in terms of firm survival than founder-CEOs. If successor-CEOs need not persist in an inherited strategic culture, founder-CEO succession may be effective in responding promptly to changing market and economic conditions. Conversely, from the entrepreneurial resilience perspective, founder-CEOs are more likely to struggle with sustaining their businesses and persisting under adverse conditions. As discussed, founder-CEOs may be more intrinsically motivated than successor-CEOs (Fahlenbrach, 2009; Wasserman, 2006). Indeed, some have found a positive relationship between entrepreneurial resilience and business success (Ayala and Manzano, 2014; Santoro et al., 2020, 2021). In addition, founder-CEOs who maintain strong control of firms are more able to respond promptly to changing market and economic conditions, presumably because firms experience few agency conflicts. Therefore, we hypothesise that new firms managed by founder-CEOs are more likely to avoid liquidation than those managed by successor-CEOs. We test the following hypothesis:

New firms managed by founder-CEOs are less likely to liquidate than those managed by successor-CEOs, especially during the financial crisis. By testing this hypothesis, we highlight whether founder-CEOs are more resilient during the financial crisis than successor-CEOs. Furthermore, exit via merger may differ from liquidation or bankruptcy from the entrepreneurial resilience perspective, mainly because founder-CEOs are more likely to persist under adverse conditions than successor-CEOs. As discussed, potential bidders find it more difficult to overcome founder-CEO resistance strategies (Gao and Jain, 2012). Therefore, founder-CEOs have more incentive to persist independently and prevent their firms from exiting via merger. In contrast to founder-CEOs, successor-CEOs have less incentive to persist independently under adverse conditions and may be able to sell their firms to partners. In particular, individuals with highly specific experiences alleviate crisis effects by finding appropriate partners to merge with their firms (Grilli, 2011). Professional CEOs may have advantages over founder-CEOs in terms of merger partner networks. Such CEOs seek merger to avoid liquidation under adverse conditions. Therefore, we test the following hypothesis:

New firms managed by founder-CEOs are less likely to exit via merger than those managed by successor-CEOs, especially during the financial crisis. While previous studies have examined the impact of entrepreneurial resilience on firm performance (Bullough and Renko, 2013; Corner et al., 2017; Santoro et al., 2020, 2021), there is a paucity of research on its impact on new firm survival according to exit routes and macroeconomic conditions. Focusing on the role of CEOs in times of crisis can improve our understanding of new firm survival under adverse conditions and the role of CEOs in a firm’s growth process.

Data and method

Data

We constructed a data set of new Japanese firms using COSMOS2 compiled by the TDB. 5 We focused on joint-stock companies employing up to 50 employees and excluded sole proprietorships and partnerships because joint-stock companies are more appropriate for research on CEO succession than sole proprietorships and partnerships. COSMOS2 covers exiting and surviving firms. Moreover, COSMOS2 includes information on not only whether a firm exits but also how and when the firm exits.

We obtained information on CEOs from COSMOS2. We identify whether CEOs are replaced by successor-CEOs, based on CEO names (both kana and kanji notations) and other information (i.e. address, and date and place of birth of CEOs). As there were spelling inconsistencies in CEO names, we manually checked whether CEO succession occurred. Furthermore, CEO- (educational background, gender, and age), firm- (sales and year of incorporation) and sector-specific characteristics (industry classification) were obtained from COSMOS2.

The information in COSMOS2 is normally updated annually. Therefore, firm exit and CEO succession are observed by year. Moreover, the original sample included only a few large firms. From the sample, we excluded firms with more than 50 employees in the first year of observation. As a result, our final sample covers small-sized firms in the manufacturing, information services, postal and telecommunication services, and other services sectors that were incorporated during the 2003–2010 period. The observation window for firm exit is 2003–2013. The sample contains 7842 firms and 38,371 firm-year observations.

Method

We measure firm performance by firm survival and exit. To identify differences in the probabilities of survival and exit between new firms managed by founder-CEOs and those managed by successor-CEOs, we construct a panel data set of new firms. As we discuss later, the dependent variables for firm survival and exit are binary, which indicates whether the firm continues or exits during the observation window. To examine the duration of firm survival, while some empirical studies have used the continuous-time model (Buehler et al., 2006; Esteve-Pérez et al., 2010), others have used the discrete-time duration model (Cefis and Marsili, 2011, 2012; Fontana and Nesta, 2009; Kato and Honjo, 2015). As the timing of survival and exit is observable only at the year level, we use the discrete-time duration model, following previous studies. By estimating the regression model, we describe which firms managed by founder- or successor-CEOs are more likely to exit – in other words, the estimation results indicate which types of firms are less likely to survive.

For the dependent variable, we identify firm survival and exit using a binary indicator. We classify ‘pooled exit’ (all types of exits) into (i) liquidation (bankruptcy and voluntary liquidation) and (ii) exit via merger. Regarding the major independent variable, we focus on the effect of the variable that captures founder-CEO succession using a binary indicator. We also measure the financial crisis period using a binary indicator and, importantly, use an interaction term between founder-CEO succession and crisis dummies. Using this interaction term, we identify whether the impact of founder-CEO succession on new firm survival is greater especially during the financial crisis.

We estimate the determinants of founder-CEO succession using a random-effects logit model to account for unobserved firm-specific heterogeneity. For the variable for founder-CEO succession, we take a 1-year lag from the dependent variables to avoid reverse causality.

Dependent variables

Non-survival can be disaggregated into various exit routes (Cefis and Marsili, 2011; Coad and Kato, 2020; Grilli, 2011; Kato and Honjo, 2015). Moving beyond a binary distinction between survival versus failure to a richer recognition of heterogeneous exit routes is essential for a better understanding of firm exit. In this study, we not only use a variable for firm survival versus exit (pooled exit), but also distinguish between liquidation and exit via merger. Coad (2014) emphasised that ‘business death’ includes both involuntary and voluntary death. In this study, liquidation, which indicates business death, includes both bankruptcy and voluntary liquidation. In other words, liquidation is referred to as failure due to bankruptcy or the firm’s disappearance due to voluntary liquidation and other reasons besides a merger. Exit via merger is referred to as the firm’s disappearance due to a merger with another firm. In the sample, we classify the types of firm exit into liquidation (bankruptcy and voluntary liquidation) and exit via merger.

‘Pooled exit’ is a dummy variable equal to one if the firm goes bankrupt, voluntarily liquidates or exits via merger between years t and t + 1, and zero otherwise. ‘Liquidation’ is a dummy variable equal to one if the firm goes bankrupt or voluntarily liquidates between years t and t + 1, and zero otherwise. ‘Merger’ is a dummy variable taking a value of one if the firm exits via merger between years t and t + 1, and zero otherwise. It is important to note that these variables (pooled exit, liquidation and exit via merger) are censored in the year of exit during the observation window.

Major independent variables

CEO succession

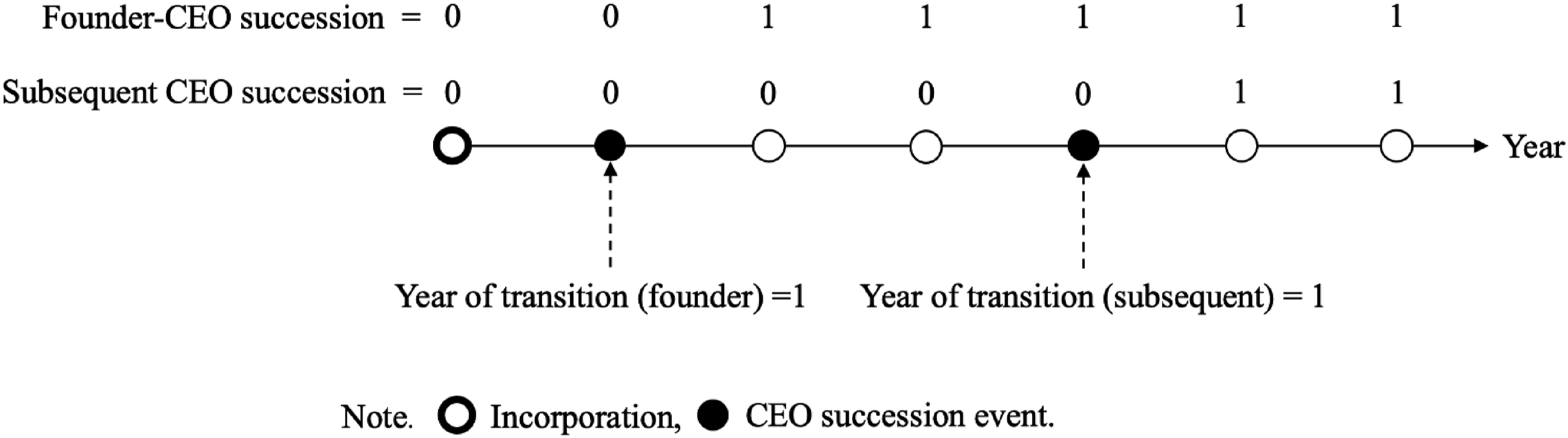

We classify the management of new firms into those managed by founder-CEOs and those managed by successor-CEOs. Figure 1 illustrates the definitions of these variables. As described in Figure 1, ‘founder-CEO succession’ represents a dummy variable equal to one if the firm experiences founder-CEO succession before year t, and zero otherwise. In addition, as described in Figure 1, the year of CEO transition, which includes both pre- and post-CEO succession periods, is differentiated from other periods, following previous studies (Bach and Serrano-Velarde, 2015; Bennedsen et al., 2007; Biggerstaff et al., 2015). ‘Year of transition (founder)’ represents a dummy variable equal to one if founder-CEO succession occurs in that year, and zero otherwise. Definitions of founder-CEO and subsequent CEO successions and the year of transition.

Moreover, to clarify whether founder-CEO succession is a distinctive event compared with other CEO successions, we compare the impact of subsequent CEO successions on new firm survival with the impact of founder-CEO succession. As presented in Figure 1, therefore, we also estimate the model by including a variable ‘subsequent CEO succession’. Similarly, we add the dummy variable ‘year of transition (subsequent)’ to control for the year of CEO transition.

Crisis

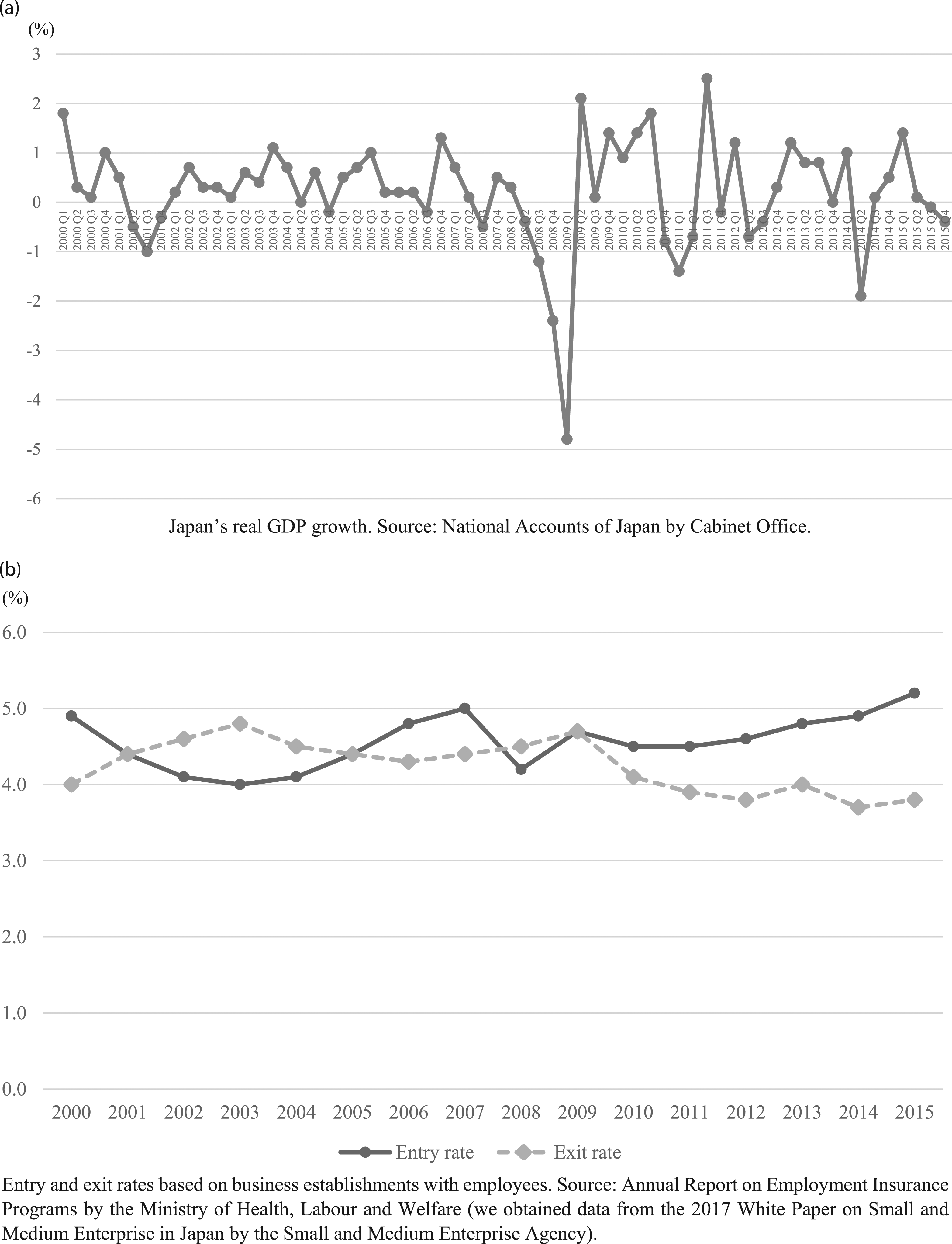

We focus on the financial crisis as a crisis event in Japan. According to Hoshi (2011: 120), the financial crisis that originally started in the market for assets derived from subprime loans in the US developed into a global crisis and a near meltdown of the entire global financial system, especially after the failure of Lehman Brothers in September 2008. Figure 2 depicts (a) real gross domestic product (GDP) growth and (b) entry and exit rates, based on establishments with employees, in Japan. Figure 2(a) shows that real GDP growth slowed sharply in the second quarter of 2008, continuing until the second quarter of 2009. Figure 2(b) shows that the exit rate increased slightly and was larger than the entry rate in 2008. While some studies regard 2007 and 2008 as the crisis period (Brown and Lee, 2019; Cefis and Marsili, 2019), we take 2008 and 2009 as the financial crisis period in Japan following others (Cowling et al., 2018; Harrison and Baldock, 2015). ‘Crisis’ represents a dummy variable equal to one if the year is 2008 or 2009, and zero otherwise. Real GDP growth and entry–exit rates in Japan (2000–2015). (a) Japan’s real GDP growth. Source: National Accounts of Japan by Cabinet Office. (b) Entry and exit rates based on business establishments with employees. Source: Annual Report on Employment Insurance Programs by the Ministry of Health, Labour and Welfare (we obtained data from the 2017 White Paper on Small and Medium Enterprise in Japan by the Small and Medium Enterprise Agency).

CEO succession – crisis interaction term

To examine the impact of founder-CEO succession on new firm survival, depending on the financial crisis, we use the interaction term of the founder-CEO succession and crisis dummies. Furthermore, we include the interaction term of the subsequent CEO succession and crisis dummies when using the subsequent CEO succession dummy.

Control variables

We include firm-specific variables as the control variables. ‘Current sales’ and ‘initial sales’ represent current and initial firm sizes, respectively. It has long been debated whether firm size affects survival (Audretsch et al., 1999; Levinthal, 1991; Mata et al., 1995). Firm size is crucial for new firms. The standard model of firm dynamics indicates that although firms start with no prior knowledge about their efficiency, they gradually learn about it (Jovanovic, 1982). While current firm size at any given moment incorporates all of the firm history and nothing further is required to predict survival, the fact that firms adjust gradually toward their desired size makes it relevant to know their departing point as well as their current position (Geroski et al., 2010: 512). In addition, firm age is known to affect survival because young firms face various ‘liabilities of newness’ (Stinchcombe, 1965).

Definition of variables.

Descriptive statistics

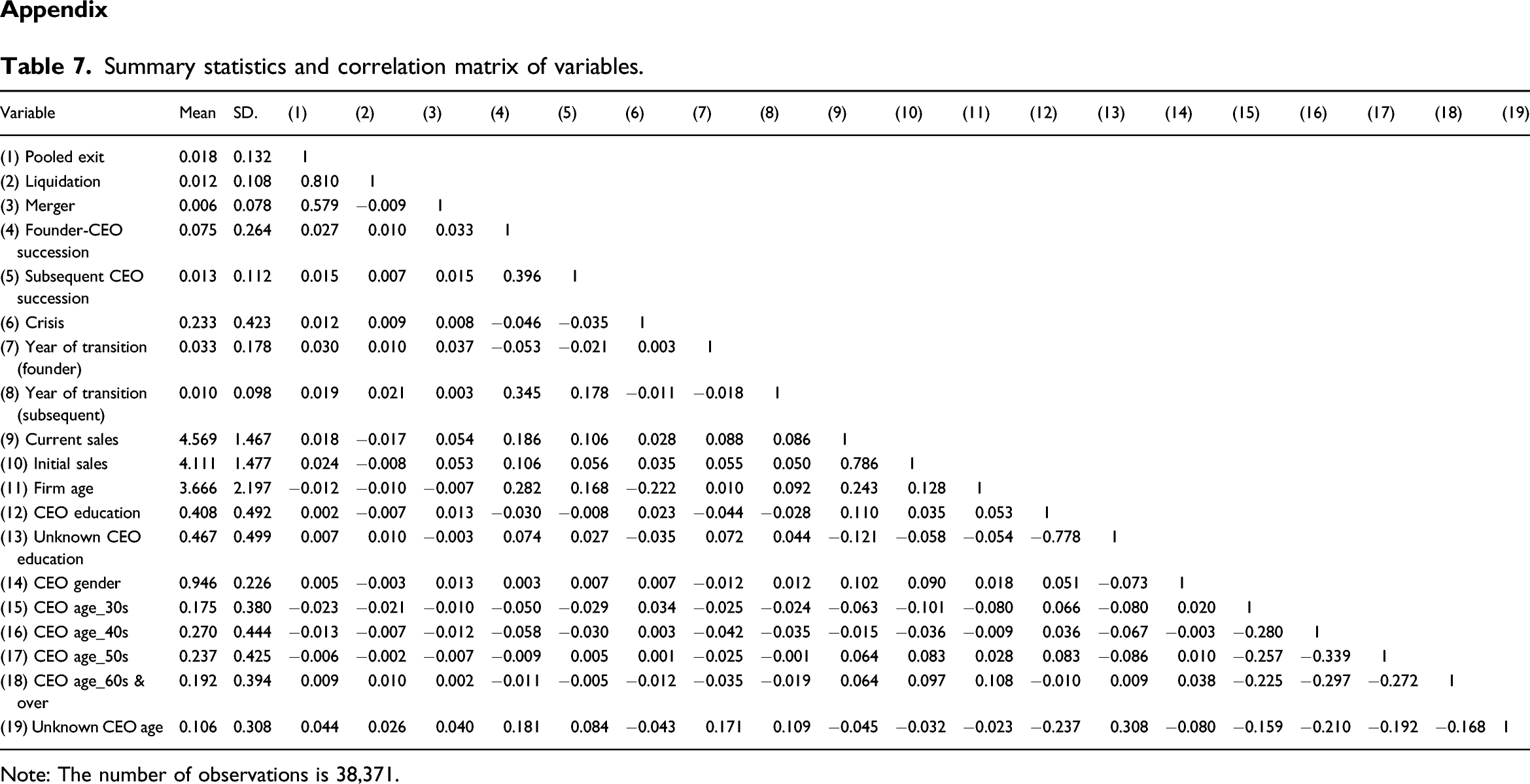

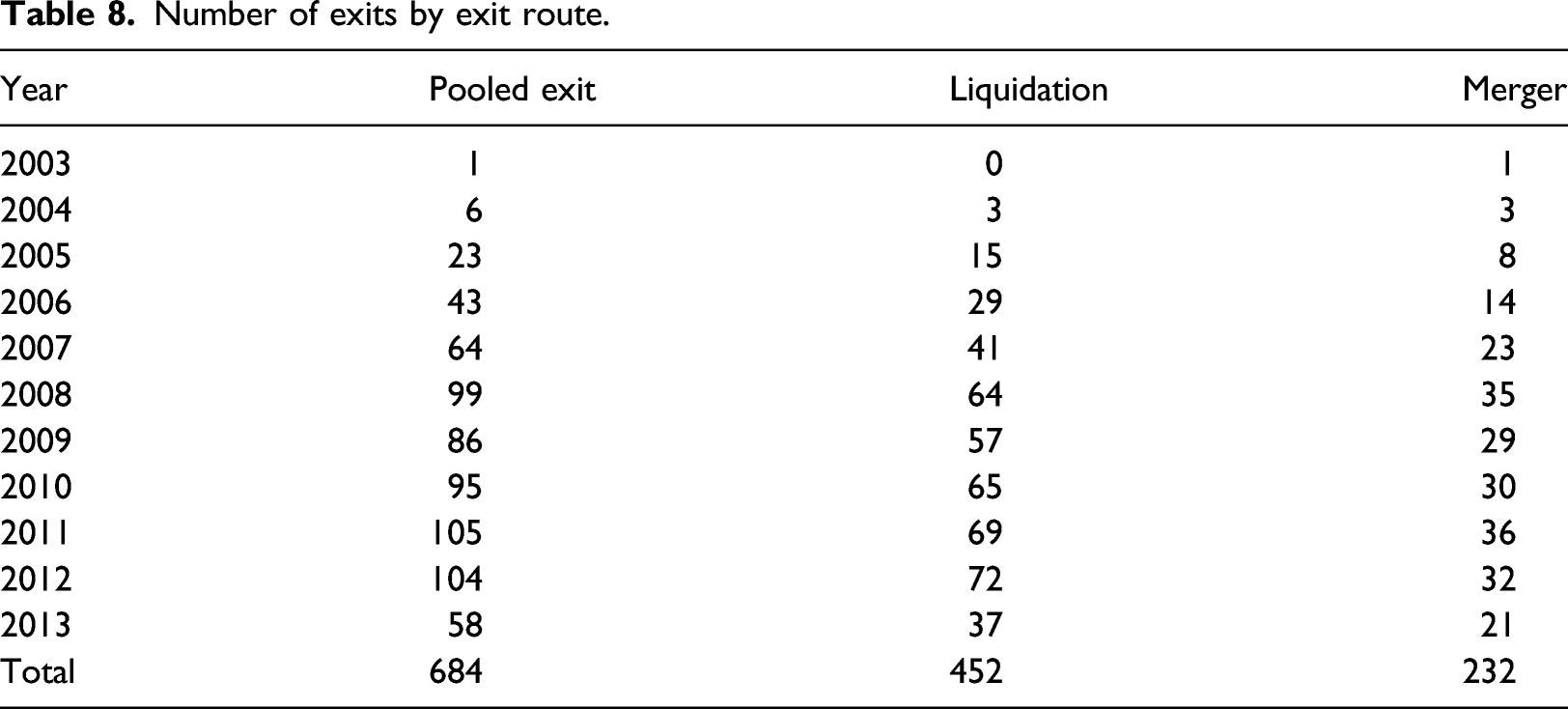

Among the 7842 firms in the sample, 684 exited up to the end of 2013. More importantly, 452 firms went bankrupt or were voluntarily liquidated, while 232 firms exited via merger. The annual number of exits by route during the observation window is shown in Table 7 in the Appendix.

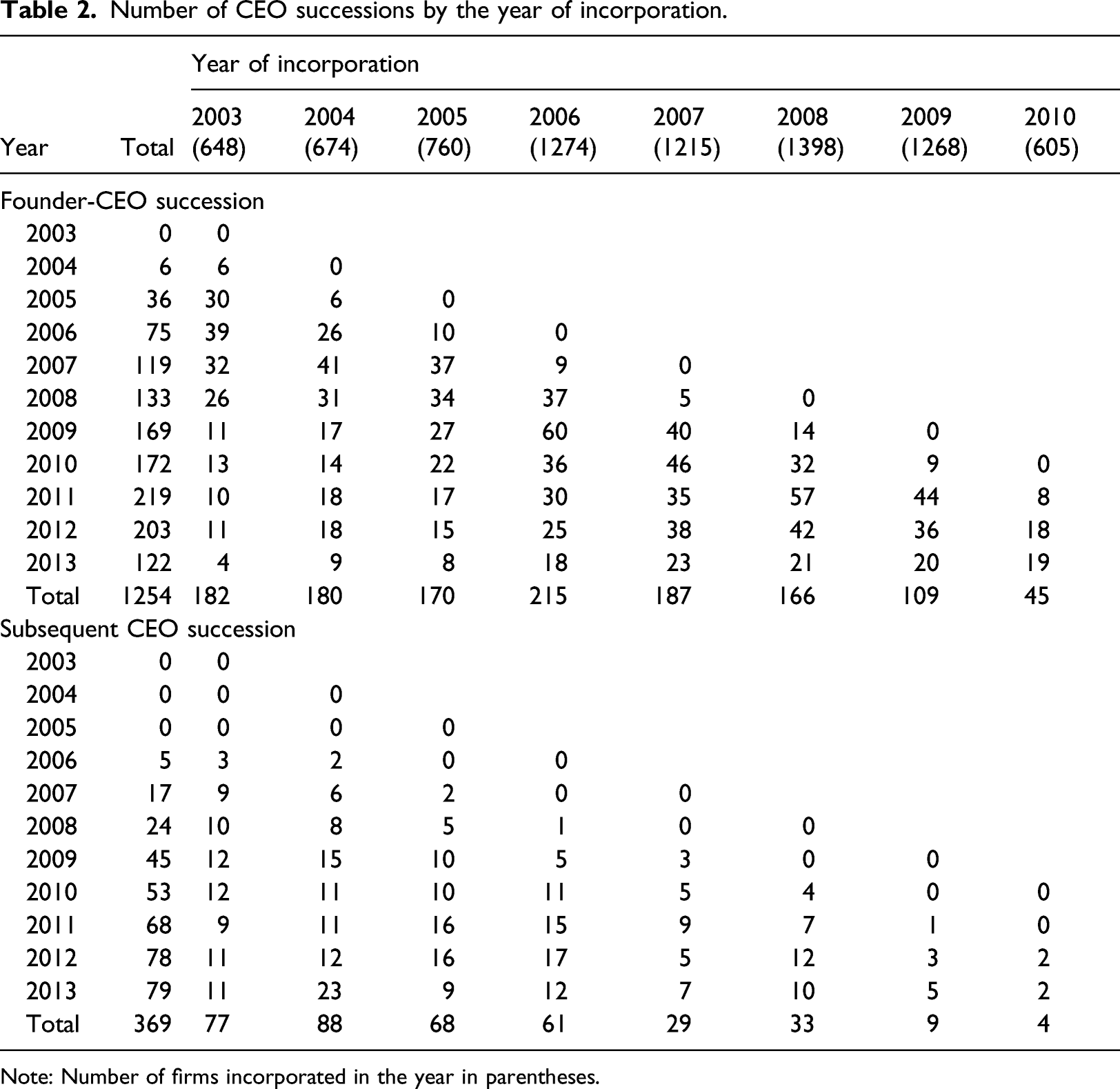

Number of CEO successions by the year of incorporation.

Note: Number of firms incorporated in the year in parentheses.

The summary statistics and correlation matrix of the variables are presented in Table 8 in the Appendix.

Results

Estimation results

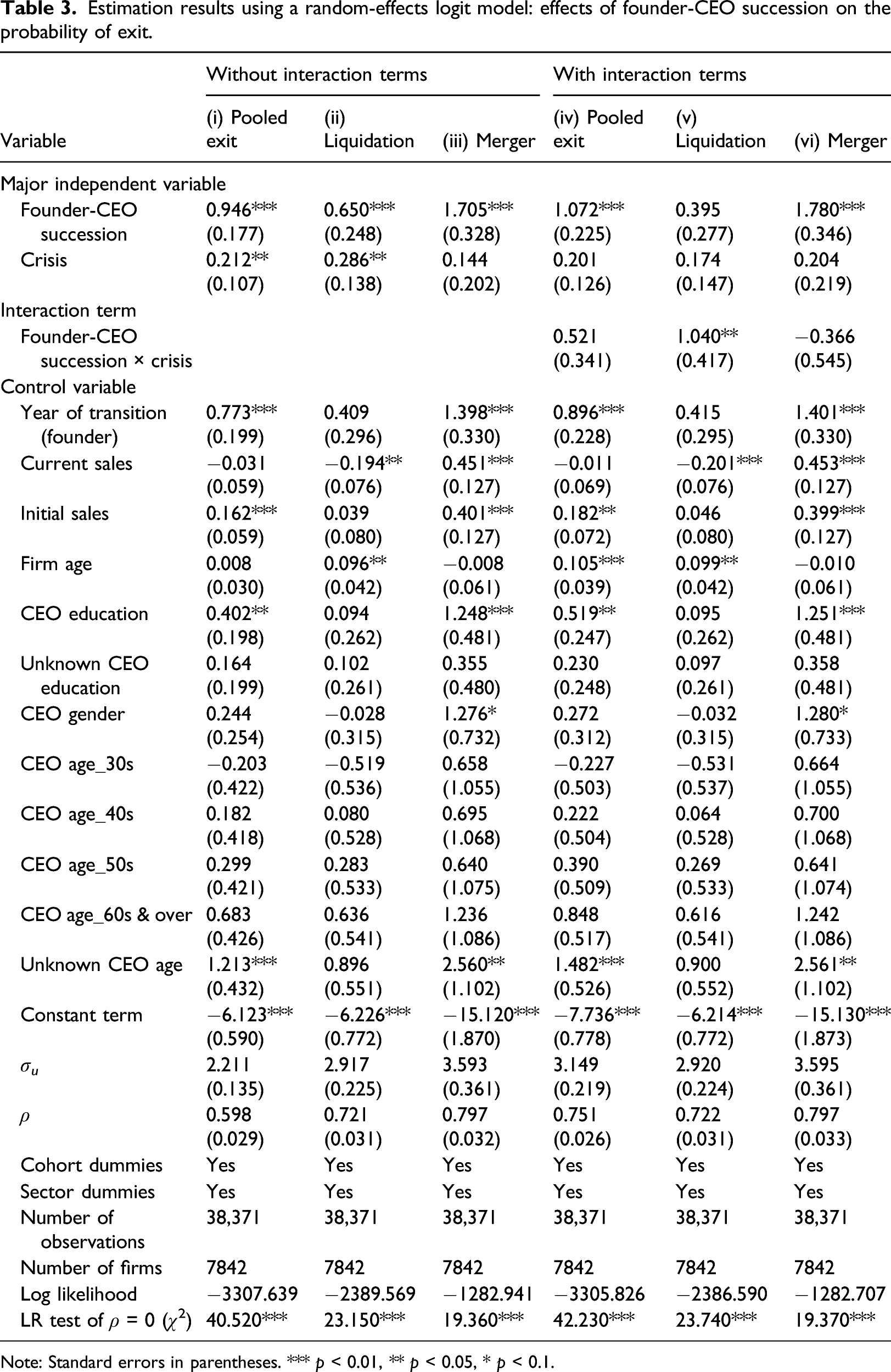

Estimation results using a random-effects logit model: effects of founder-CEO succession on the probability of exit.

Note: Standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

In column (i) of Table 3, founder-CEO succession has a positive and significant effect on pooled exit, indicating that the probability of pooled exit increases with founder-CEO succession. The results suggest that new firms managed by founder-CEOs are less likely to exit than those managed by successor-CEOs. In addition, the crisis dummy has a positive and significant effect on pooled exit in column (i), indicating that the probability of pooled exit among new firms tends to increase in times of crisis. Regarding the results by exit route, column (ii) shows that the effect of founder-CEO succession on liquidation is positive and significant. This indicates that the probability of liquidation increases with founder-CEO succession and that new firms managed by founder-CEOs are less likely to liquidate their businesses than those managed by successor-CEOs. Therefore, Hypothesis 1 is supported. The crisis dummy also has a positive and significant effect on liquidation in column (ii), indicating that the probability of liquidation increases in times of crisis.

Column (iii) shows that the probability of exit via merger increases with founder-CEO succession, indicating that new firms managed by founder-CEOs are less likely to exit via merger than those managed by successor-CEOs. This supports Hypothesis 2. However, the effect of the crisis dummy is positive, but not statistically significant, indicating that the probability of exit via merger is not associated with the 2008–2009 financial crisis.

Turning to the results with interaction terms, the interaction term of the founder-CEO succession and crisis dummies has no significant effect on the pooled exit in column (iv) of Table 3, while the effect of founder-CEO succession is still positive and statistically significant. By contrast, column (v) shows that the interaction term of the founder-CEO succession and crisis dummies has a positive and statistically significant effect on liquidation, while the founder-CEO succession and crisis dummies are insignificant. The findings indicate that the probability of liquidation increases with founder-CEO succession during the 2008–2009 financial crisis. This suggests that the transition from founder-CEOs to successor-CEOs is detrimental to firm survival, especially in times of crisis. In other words, founder-CEOs are more resilient than successor-CEOs in surviving a crisis. Therefore, Hypothesis 3 is supported.

Column (vi) in Table 3 moreover shows that while founder-CEO succession still has a positive and significant effect on exit via merger, its interaction term with the crisis dummy has no significant effect. This indicates that firms managed by founder-CEOs are less likely to exit via merger than those managed by successor-CEOs, regardless of macroeconomic conditions. Thus, Hypothesis 4 is not supported.

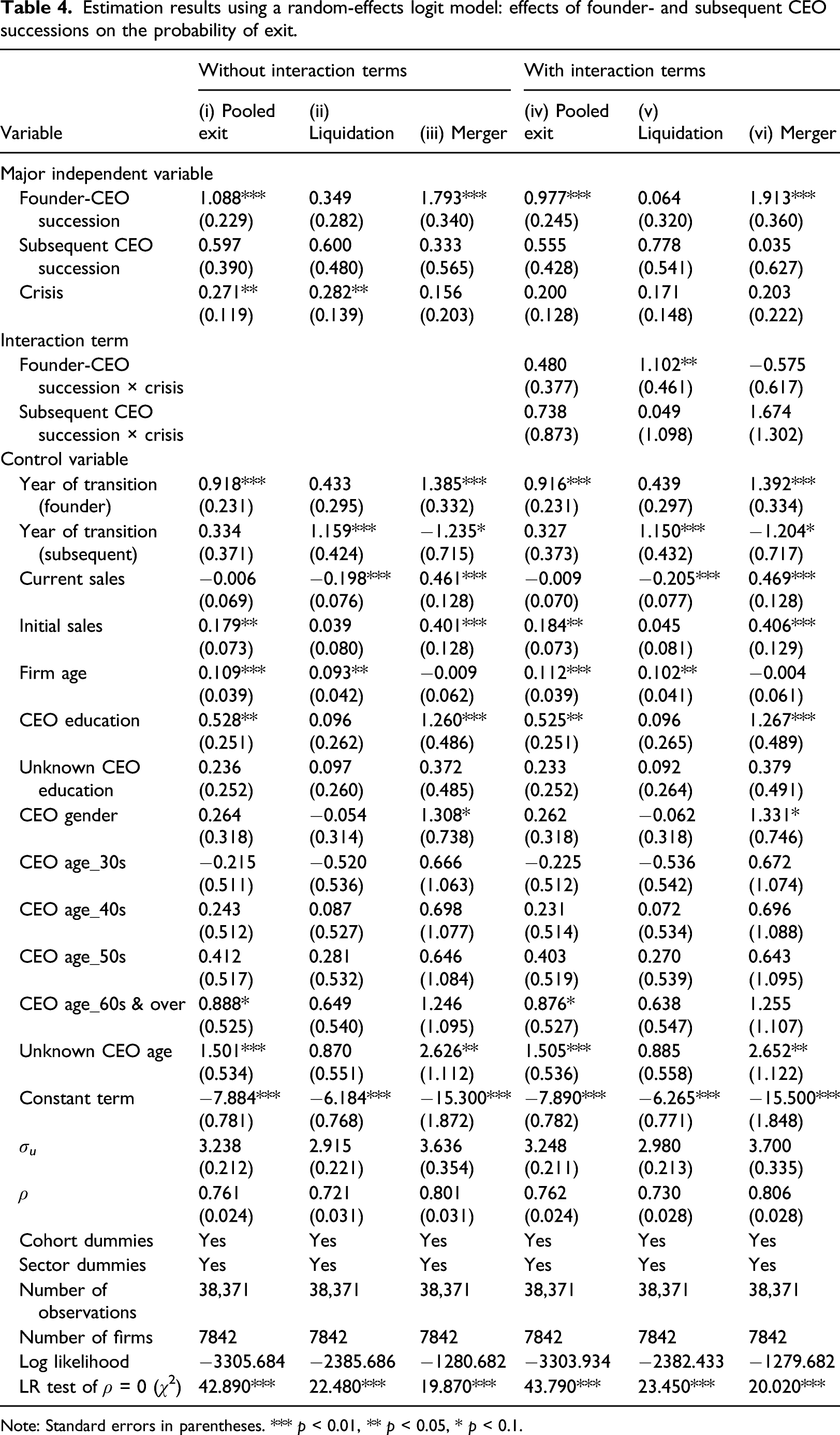

Estimation results using a random-effects logit model: effects of founder- and subsequent CEO successions on the probability of exit.

Note: Standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

In summary, our results indicate that the probability of liquidation increases with founder-CEO succession, especially during the 2008–2009 financial crisis. Furthermore, the probability of exit via merger increases with founder-CEO succession, regardless of macroeconomic conditions. These findings suggest that founder-CEOs are more resilient than successor-CEOs in surviving a crisis.

Robustness checks

While we examine the impact of founder-CEO succession on firm survival and exit, there may be some unresolved empirical issues. Founder-CEO succession is likely to be a strategic decision for new firms. CEOs who are no longer convinced of their businesses may make decisions to liquidate their firms due to a negative future perspective. Therefore, some factors, including firm performance, may affect a firm’s decision to replace CEOs or the CEO’s decision to step down. Therefore, we conduct robustness checks to ensure causality between founder-CEO succession and firm survival.

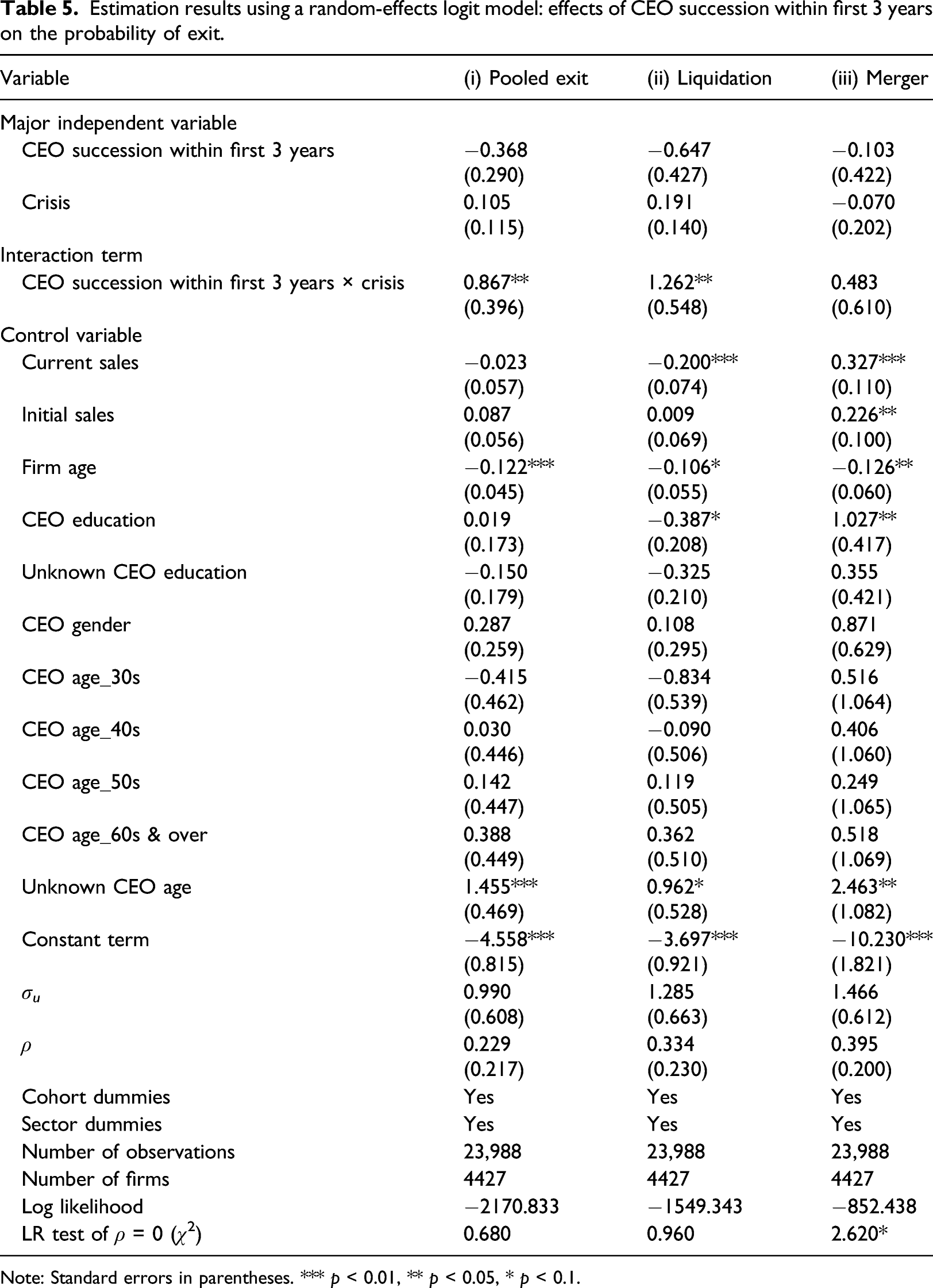

Estimation results using a random-effects logit model: effects of CEO succession within first 3 years on the probability of exit.

Note: Standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

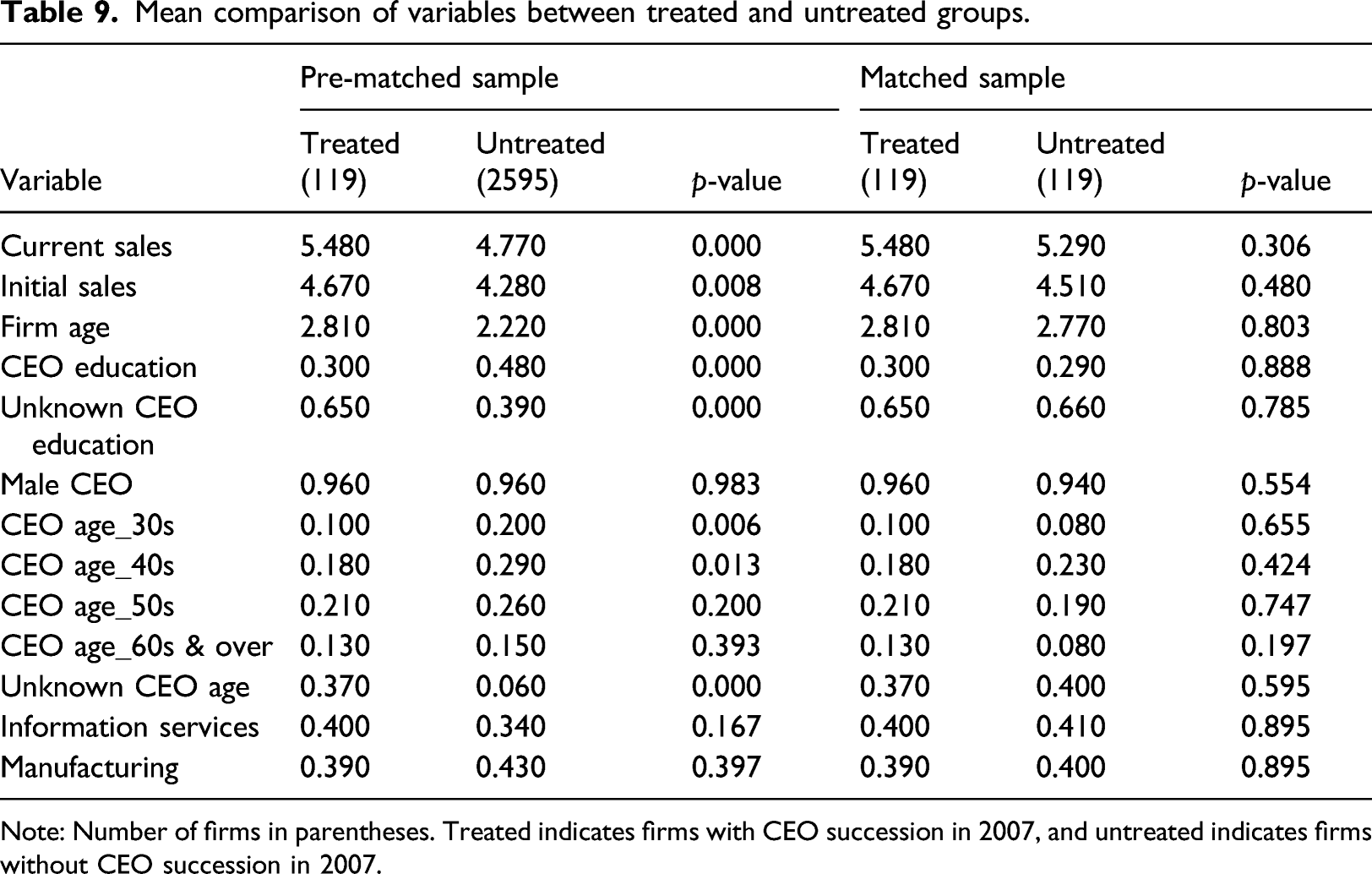

Moreover, we address the selection issue of founder-CEO succession using propensity score matching. To compare the probabilities of exit between firms with and without founder-CEO succession, we first estimate the determinants of founder-CEO succession using a logit model. We conduct one-to-one nearest neighbour matching based on logit regression. Using the matched sample, we estimate the effects of founder-CEO succession on firm survival.

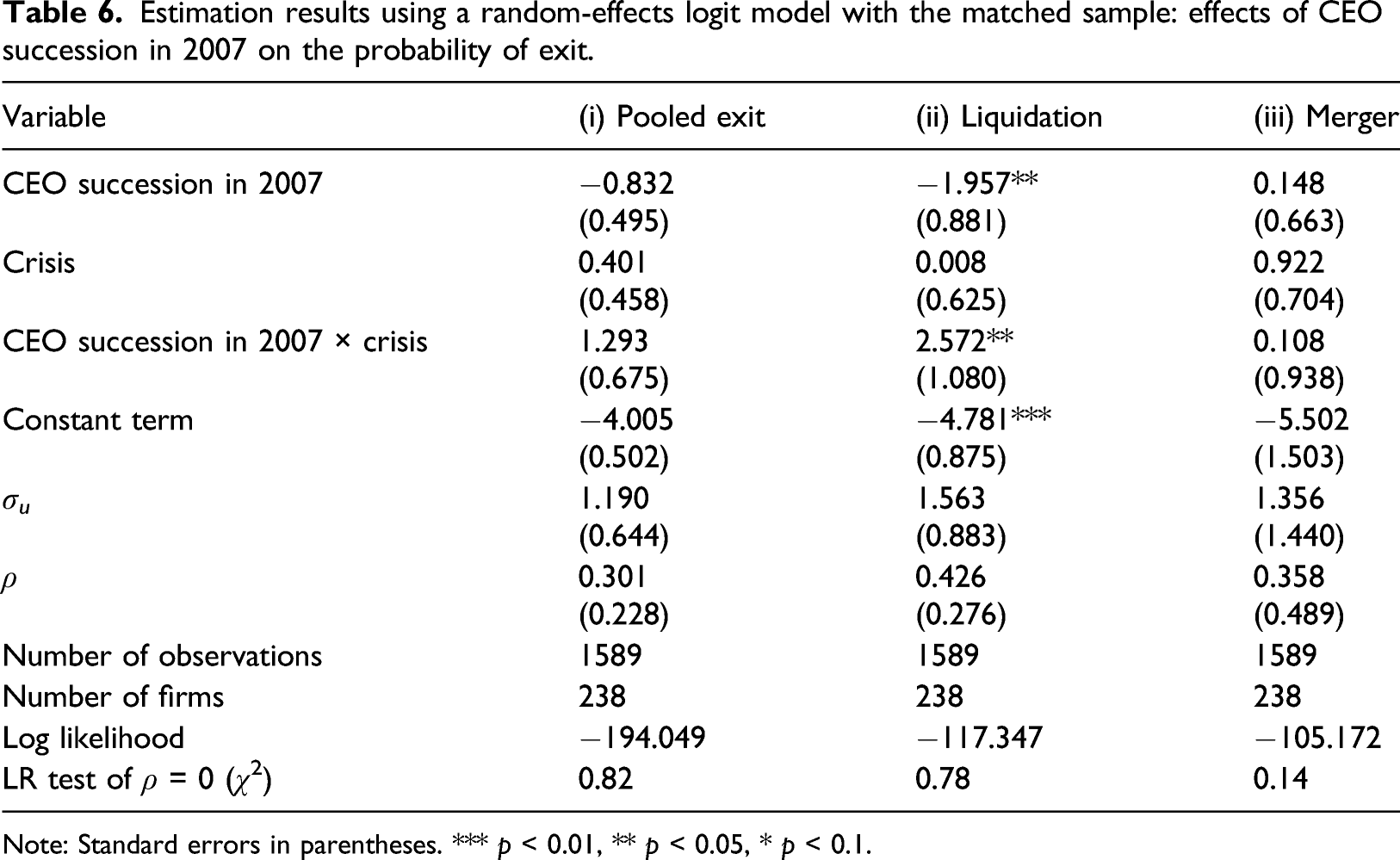

As shown in Table 2, the number of founder-CEO successions tends to be small in the early years of observation (0 in 2003, 6 in 2004, 36 in 2005, and 75 in 2006). When we compare the probabilities of exit between firms with and without founder-CEO succession until 2006 by year, there are no significant differences between these firms, partly because of the lower matching quality. Therefore, we report only a comparison between firms with and without founder-CEO succession in 2007. For the samples before and after matching, the mean comparison of the variables between treated (119 firms with founder-CEO succession in 2007) and untreated groups (119 firms without founder-CEO succession in 2007) is presented in Table 9 in the Appendix. As shown in Table 9, there are no significant differences between the treated and untreated groups for any variables in the matched sample, whereas significant differences between the groups exist for many variables in the pre-matched sample. Using the matched sample, we estimate the random-effects logit model for the effect of founder-CEO succession in 2007 on the probability of exit in subsequent years.

Estimation results using a random-effects logit model with the matched sample: effects of CEO succession in 2007 on the probability of exit.

Note: Standard errors in parentheses. *** p < 0.01, ** p < 0.05, * p < 0.1.

Moreover, we attempt to use different cut-off points of our sample regarding start-up size, such as 10 or 20 employees, although our sample consists of firms with 50 employees or less, in the first year of observation. The results using the different cut-off points are generally consistent with those in Tables 3 and 4. In addition, while the maximum age for a ‘new’ firm in our sample is 10 years, previous studies used different cut-off points in their definition of new firms, and some selected cut-off values of six or 8 years (Cefis and Marsili, 2011; Song et al., 2008). Therefore, we run the model with a restriction on the maximum firm age of 8 years and find generally similar results.

Furthermore, we estimated the impact of the financial crisis, using real GDP growth instead of the crisis dummy, to check whether the results depend on the measurement of macroeconomic conditions. We found a positive effect of the interaction term between founder-CEO succession and real GDP growth on liquidation. Therefore, our results are robust to different macroeconomic measures.

Discussion and conclusions

Summary and contributions

This artilce has explored differences in the probabilities of survival and exit between new firms managed by founder-CEOs with those managed by successor-CEOs. Using a sample of Japanese firms founded during the 2003–2010 period, we examined the impact of founder-CEO succession on new firm survival, especially in times of crisis. Drawing on the entrepreneurial resilience perspective (Bullough and Renko, 2013; Corner et al., 2017; Santoro et al., 2020, 2021), we argued that founder-CEOs are more resilient in times of crisis than successor-CEOs. Our findings indicate that new firms managed by founder-CEOs are less likely to liquidate than those managed by successor-CEOs during the 2008–2009 financial crisis. This suggests that founder-CEOs tend to have entrepreneurial resilience, which influences firm survival in times of crisis. In addition, new firms managed by successor-CEOs are more likely to exit via merger than those managed by founder-CEOs, regardless of macroeconomic conditions.

This study makes a significant contribution to the literature on CEO succession. Although scholars have examined the impact of CEO succession on the performance of large established firms (Beatty and Zajac, 1987; Worrell and Davidson III, 1987), very few have examined the impact of CEO succession among new firms (Chen and Thompson, 2015; Wasserman, 2003, 2017). Our analysis of longitudinal data, which includes the time of incorporation, enables us to address the question of whether and how the transition from founder-CEOs to successor-CEOs as a distinctive succession event, compared with subsequent CEO successions, affects new firm survival. Our findings suggest the uniqueness of founder-CEOs over successor-CEOs in terms of resilience. In addition, we provide new evidence on firm exit routes. By distinguishing between exits via liquidation and merger, we evaluate the impact of founder-CEO succession on the post-entry performance of new firms more precisely. Without distinguishing between exit routes, we may misinterpret the determinants of firm exit, which includes both failures (liquidation) and non-failure outcomes (exit via merger). Furthermore, we provide comprehensive evidence that founder-CEO succession has a significant impact on liquidation in times of crisis. Resilience is often a key factor in explaining entrepreneurial success (Ayala and Manzano, 2014). However, previous studies have been limited to evidence from subjective measures of entrepreneurial resilience obtained from questionnaire surveys, and exit cases with entrepreneurial resilience could not be identified. Thus, previous studies lack compelling evidence on whether entrepreneurial resilience is helpful for new firm survival in the face of adversity. Our analysis has helped fill the gap between theory and practice from an entrepreneurial resilience perspective; in effect, our findings reinforce the importance of entrepreneurial resilience in the survival of new firms.

Practical implications

This study has two practical implications. First, our analysis indicates that new firms managed by founder-CEOs are less likely to liquidate during the financial crisis, suggesting that the transition from founder-CEOs to successor-CEOs is detrimental to firm survival in times of crisis. From a strategic perspective founder-CEO succession in new firms should be conducted carefully in times of crisis, such as the recession caused by the coronavirus pandemic 2020 - which could increase the probability of bankruptcy. Conversely, if necessary, it may be effective to promote founder-CEO succession under ordinary conditions other than times of crisis. Founder-CEOs derive intrinsic benefits by virtue of their firms (Gao and Jain, 2012), possess strong psychological attachment, and express commitment to their firms (He, 2008; Nelson, 2003). Our findings suggest that founder-CEOs—although they do not necessarily have superior management knowledge and skills in business sustainability—are more resilient than successor-CEOs in a recession. Rather, persistence in top management may help new firms survive under adverse conditions.

Second, our findings indicate that the transition from founder-CEOs to successor-CEOs promotes exit via merger, regardless of macroeconomic conditions. Founder-CEOs have more incentive to sustain their businesses, rather than to liquidate their firms, in addition to exit via merger. Conversely, promoting founder-CEO succession increases the probability of ownership transfer, which may lead to an effective strategy to achieve the successful exit of new firms. From the perspective of policymakers, promoting management transfer increases a firm’s mobility, which may stimulate the stagnant economy in countries with declining birth rates and ageing populations, such as Japan. Meanwhile, the private equity market, including mergers and acquisitions (M&A), for new firms has not been developed so far in Japan, compared with other advanced countries, such as the United States (Honjo and Nagaoka, 2018; Kato et al., 2021). The findings also suggest that policymakers should promote a division of labour through CEO succession, to foster the efficient allocation of resources in new firms via merger, which may also contribute to the development of the private equity market for M&A. It should be noted that further research on the impact of founder-CEO succession on successful exit, including mergers, is warranted.

Limitations and future avenues of research

Although this article has contributed to our understanding of the relative effects of founder and successor CEO on new firm survival, the study has some limitations with implications for further research. First, we addressed the endogeneity issue of CEO succession in the previous section, by not only using data on CEO succession in the first 3 years after incorporation but also applying propensity score matching. To ensure causality, however, further analysis would be useful to employ data on exogenous CEO succession events, such as a CEO’s sudden death (Lee et al., 2018). Second, as this article has focused on CEO succession in new firms, we ignored the role of top management team members, other than CEOs. However, top management team members play complementary roles in their firms (Klotz et al., 2014; Yusubova et al., 2020). Further analysis should consider the succession of a firm’s resources by other members. Third, we need more detailed analysis including CEO knowledge and learning via previous managerial experience to better understand the impact of CEO succession on new firm survival. Finally, a debate exists on the origin of successor-CEOs, including the question of whether insider CEOs differ from outsider CEOs (Agarwal et al., 2006; Chung et al., 1987; Georgakakis and Ruigrok, 2017). Considering the origin of successor-CEOs would lead to a more precise evaluation of the effects of CEO succession. Furthermore, for the robustness of the findings, it would be worthwhile to use alternative measures of post-entry performance, such as growth, profitability, and innovation. Addressing these aspects in further analyses would further clarify the effects of CEO succession in new firms.

Supplemental Material

sj-pdf-1-isb-10.1177_02662426211050794 – Supplemental Material for Are founder-CEOs resilient to crises? The impact of founder-CEO succession on new firm survival

Supplemental Material, sj-pdf-1-isb-10.1177_02662426211050794 for Are founder-CEOs resilient to crises? The impact of founder-CEO succession on new firm survival by Yuji Honjo and Masatoshi Kato in International Small Business Journal: Researching Entrepreneurship

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is financially supported by a Grant-in-Aid for Scientific Research from the Japan Society for the Promotion of Science (Number: JP20K01618, JP17K03713, 26285060).

Notes

Supplemental material

Supplemental material for this article is available online.

Appendix

Summary statistics and correlation matrix of variables. Note: The number of observations is 38,371. Number of exits by exit route. Mean comparison of variables between treated and untreated groups. Note: Number of firms in parentheses. Treated indicates firms with CEO succession in 2007, and untreated indicates firms without CEO succession in 2007.

Variable

Mean

SD.

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(1) Pooled exit

0.018

0.132

1

(2) Liquidation

0.012

0.108

0.810

1

(3) Merger

0.006

0.078

0.579

−0.009

1

(4) Founder-CEO succession

0.075

0.264

0.027

0.010

0.033

1

(5) Subsequent CEO succession

0.013

0.112

0.015

0.007

0.015

0.396

1

(6) Crisis

0.233

0.423

0.012

0.009

0.008

−0.046

−0.035

1

(7) Year of transition (founder)

0.033

0.178

0.030

0.010

0.037

−0.053

−0.021

0.003

1

(8) Year of transition (subsequent)

0.010

0.098

0.019

0.021

0.003

0.345

0.178

−0.011

−0.018

1

(9) Current sales

4.569

1.467

0.018

−0.017

0.054

0.186

0.106

0.028

0.088

0.086

1

(10) Initial sales

4.111

1.477

0.024

−0.008

0.053

0.106

0.056

0.035

0.055

0.050

0.786

1

(11) Firm age

3.666

2.197

−0.012

−0.010

−0.007

0.282

0.168

−0.222

0.010

0.092

0.243

0.128

1

(12) CEO education

0.408

0.492

0.002

−0.007

0.013

−0.030

−0.008

0.023

−0.044

−0.028

0.110

0.035

0.053

1

(13) Unknown CEO education

0.467

0.499

0.007

0.010

−0.003

0.074

0.027

−0.035

0.072

0.044

−0.121

−0.058

−0.054

−0.778

1

(14) CEO gender

0.946

0.226

0.005

−0.003

0.013

0.003

0.007

0.007

−0.012

0.012

0.102

0.090

0.018

0.051

−0.073

1

(15) CEO age_30s

0.175

0.380

−0.023

−0.021

−0.010

−0.050

−0.029

0.034

−0.025

−0.024

−0.063

−0.101

−0.080

0.066

−0.080

0.020

1

(16) CEO age_40s

0.270

0.444

−0.013

−0.007

−0.012

−0.058

−0.030

0.003

−0.042

−0.035

−0.015

−0.036

−0.009

0.036

−0.067

−0.003

−0.280

1

(17) CEO age_50s

0.237

0.425

−0.006

−0.002

−0.007

−0.009

0.005

0.001

−0.025

−0.001

0.064

0.083

0.028

0.083

−0.086

0.010

−0.257

−0.339

1

(18) CEO age_60s & over

0.192

0.394

0.009

0.010

0.002

−0.011

−0.005

−0.012

−0.035

−0.019

0.064

0.097

0.108

−0.010

0.009

0.038

−0.225

−0.297

−0.272

1

(19) Unknown CEO age

0.106

0.308

0.044

0.026

0.040

0.181

0.084

−0.043

0.171

0.109

−0.045

−0.032

−0.023

−0.237

0.308

−0.080

−0.159

−0.210

−0.192

−0.168

1

Year

Pooled exit

Liquidation

Merger

2003

1

0

1

2004

6

3

3

2005

23

15

8

2006

43

29

14

2007

64

41

23

2008

99

64

35

2009

86

57

29

2010

95

65

30

2011

105

69

36

2012

104

72

32

2013

58

37

21

Total

684

452

232

Pre-matched sample

Matched sample

Variable

Treated (119)

Untreated (2595)

p-value

Treated (119)

Untreated (119)

p-value

Current sales

5.480

4.770

0.000

5.480

5.290

0.306

Initial sales

4.670

4.280

0.008

4.670

4.510

0.480

Firm age

2.810

2.220

0.000

2.810

2.770

0.803

CEO education

0.300

0.480

0.000

0.300

0.290

0.888

Unknown CEO education

0.650

0.390

0.000

0.650

0.660

0.785

Male CEO

0.960

0.960

0.983

0.960

0.940

0.554

CEO age_30s

0.100

0.200

0.006

0.100

0.080

0.655

CEO age_40s

0.180

0.290

0.013

0.180

0.230

0.424

CEO age_50s

0.210

0.260

0.200

0.210

0.190

0.747

CEO age_60s & over

0.130

0.150

0.393

0.130

0.080

0.197

Unknown CEO age

0.370

0.060

0.000

0.370

0.400

0.595

Information services

0.400

0.340

0.167

0.400

0.410

0.895

Manufacturing

0.390

0.430

0.397

0.390

0.400

0.895

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.