Abstract

We extend research on strategic communication by introducing a theoretical model of how newly appointed CEOs engage in sensemaking and sensegiving with the capital market through their first communication of strategic priorities. We conceptualize strategic topic novelty, the distinctiveness of the topics emphasized relative to the predecessors’, as an observable dimension of new CEOs’ priorities that reflects how they reconcile their desire to establish a unique vision with the need to legitimize their appointment. Our theory suggests that new CEOs draw on situational cues, particularly the nature of the succession (dismissal vs. routine) and the initial market reaction to their appointment, when determining how much novelty to introduce. Specifically, we propose that new CEOs communicate higher strategic topic novelty following dismissals and that this relationship may be strengthened by positive market reactions to their appointment and weakened by negative market responses. We further expect that the capital market responds more favorably to strategic topic novelty following dismissals. Applying textual analysis of new CEOs’ communication in earnings calls from 2004 to 2018, we find a positive relationship between dismissals and strategic topic novelty, which is weaker for more negative market reactions to the new CEO’s announcement. We also find more positive capital market reactions to strategic topic novelty following dismissals. Our findings advance understanding of how new CEOs approach their role by integrating sensemaking with sensegiving in research on CEO communication and highlight how new CEOs asymmetrically adjust novelty in response to positive versus negative market reactions.

Keywords

Introduction

“Whenever there is a change of chief executive [. . .], shareholders want to know what the new appointee plans to improve their mood.”

As new CEOs assume their roles, they are expected to articulate a compelling strategic direction early in their tenure. For new CEOs of public companies in particular, how effectively they communicate can shape investor confidence, impacting their ability to retain their positions and create value for the firm (Martin & Combs, 2011). Strategic communication thus becomes a critical aspect of their early leadership—one that presents a fundamental tension. New CEOs often seek to leave their mark on the organization (e.g., Fanelli, Misangyi, & Tosi, 2009; Quigley & Hambrick, 2012), but they must also secure legitimacy with the investment community, which evaluates their suitability under conditions of uncertainty and limited information (e.g., Whittington, Yakis-Douglas, & Ahn, 2016; Yi, Zhang, & Windsor, 2020). Importantly, these imperatives are not always aligned, as some situations call for continuity while others invite change. Complicating matters, how well the market views a CEO’s fit with the situation is rarely communicated directly. Instead, new CEOs must interpret subtle cues and manage considerable uncertainty in deciding how to address the market and communicate their strategic priorities.

Despite the importance of strategic communication for new CEOs (Whittington et al., 2016), we know little about how they approach this challenge. Extant research largely views strategic communication as a sensegiving activity, focusing on how CEOs’ communications shape stakeholder perceptions (e.g., Guo, Sengul, & Yu, 2021; Whittington et al., 2016). This focus has left largely unexamined the antecedent sensemaking processes, where CEOs interpret the demands of the situation before communicating (Gioia & Chittipeddi, 1991). For new CEOs, sensemaking involves assessing the firm’s strategic situation, evaluating market signals, and determining whether and how much to pivot from the strategic direction set by the predecessor (Hambrick & Fukutomi, 1991; Helfat & Bailey, 2005; Vancil, 1987). Thus, an important question remains: How do new CEOs make sense of their situation when determining and communicating their strategic priorities to the investment community?

In this study, we address this question by developing and testing a theoretical model that conceptualizes new CEO strategic communication as a dynamic, reciprocal process of sensemaking and sensegiving with the capital market. We argue that, before communicating their strategic priorities, new CEOs engage in a critical sensemaking process wherein they identify and interpret relevant environmental cues about what is expected of them and how the market evaluates their fit with the situation. These interpretations shape new CEOs’ sensegiving via early strategic communication, which in turn elicits further market reactions that feed back into CEOs’ evolving interpretations and subsequent strategic actions. Within our model, we conceptualize new CEO strategic communication in terms of the distinctiveness of the priorities emphasized relative to the predecessor’s. We argue that such distinctiveness will be evident in the topics that new CEOs discuss when first communicating their vision and priorities to the investment community, specifically via their emphasis on novel strategic topics—a concept we refer to as strategic topic novelty. Whereas a CEO’s vision reflects a broad and abstract direction, their strategic priorities translate that vision into a more concrete, communicable action plan. 1 Strategic topic novelty, therefore, captures how shifts in a new CEO’s vision and priorities relative to the predecessor are expressed through early communication with the capital market, before any strategic actions have been taken. As such, it reflects how new CEOs reconcile their desire to leave their mark on the organization with the need to gain legitimacy in the absence of a performance track record.

We identify two key contextual factors that shape new CEOs’ sensemaking of the situation and their perceived discretion in laying out novel strategic priorities: the nature of the succession and the capital market’s initial reaction to their appointment. Regarding the nature of the succession, we specifically distinguish between cases in which the predecessor is forced out by the board (i.e., dismissal) versus cases that reflect more routine succession (e.g., planned retirement, leaving to pursue new opportunities, etc.). Whereas a routine succession might imply continuity and signal that the previous strategic direction remains viable, dismissal of the predecessor creates a clear opportunity for the new CEO to distinguish themselves and gain legitimacy by introducing novel strategic priorities (Hambrick & Fukutomi, 1991; Keil & Zangrillo, 2021). At the same time, the capital market’s reaction to the new CEO’s appointment will affect how they interpret the situation. While a positive reaction will reinforce new CEOs’ interpretation, a negative reaction can complicate it, leading new CEOs to second-guess their direction and react in potentially maladaptive ways (Nicholson, 1998; Smither, London, & Reilly, 2005; Westphal & Graebner, 2010). Altogether, then, we posit that new CEOs’ initial strategic communication of their priorities will reflect a higher degree of strategic topic novelty following a dismissal than a more routine succession and that this relationship will be strengthened by a positive market reaction and weakened by a negative reaction to their appointment. Finally, we complete the cycle of sensemaking and sensegiving between new CEOs and the capital market by considering the market reaction to the new CEO’s communicated priorities. We hypothesize that the capital market will react more favorably to higher levels of strategic topic novelty following a dismissal relative to a routine succession.

We formally test our hypotheses using a sample of CEO successions in S&P 1500 firms from 2004 to 2018, leveraging textual analysis of earnings calls to assess strategic topic novelty. Our findings largely support our theorizing, providing several contributions to the strategic communication literature. By integrating sensemaking into the process of new CEO strategic communication, we deepen our theoretical understanding of how CEOs manage stakeholders’ perceptions and how they interpret and respond to complex and sometimes conflicting signals from the environmental context when deciding what to communicate. Our model also adds to the traditional view of strategic communication as a sensegiving activity by demonstrating that new CEO communication is a dynamic, reciprocal process with the capital market that can shape the strategic direction of firms. Not only does this perspective more accurately capture the dynamic nature of capital markets, but it also provides a deeper understanding of CEO successions by showing how external pressures and the initial reaction to new CEOs’ appointments influence their subsequent strategic communication decisions. The degree of strategic topic novelty communicated by a new CEO reflects a balancing act in interpreting and responding to environmental cues while actively shaping the firm’s narrative.

Strategic Communication and New CEOs

CEO Strategic Communication as Sensegiving

Extensive research in strategic leadership highlights the critical role CEOs play in shaping firm strategy and performance (Bromiley & Rau, 2016; Busenbark, Krause, Boivie, & Graffin, 2016; Campbell, Bilgili, Crossland, & Ajay, 2023). While much of this work has focused on quantifiable outcomes such as financial performance and strategic change (Bromiley & Rau, 2016), a burgeoning literature also underscores the importance of CEOs’ communications with internal and external stakeholders about the firm and its strategies. This literature emphasizes that organizational success and survival depend not only on the strategic actions taken by firms but also on how CEOs articulate their vision and strategies to key stakeholders (S. Brown, Hillegeist, & Lo, 2004; Gao, Yu, & Cannella, 2016; Gioia & Chittipeddi, 1991; Whittington et al., 2016). Argenti, Howell, and Beck (2005) refer to this idea as the “strategic communication imperative,” indicating that the purposeful communication of strategy is itself an integral part of the strategic management process contributing to firms’ positioning and their ability to achieve sustained success (see also, Steyn, 2003; Zerfass, Verčič, Nothhaft, & Page, 2018).

Conceptualized this way, strategic communication reflects a sensegiving activity through which CEOs frame the organizational context for stakeholders (Fiss & Zajac, 2006; Martens, Jennings, & Jennings, 2007; Whittington et al., 2016). Through their strategic communication, CEOs create a narrative and provide meaningful interpretations for patterns of potentially ambiguous information to shape stakeholders’ views “toward some intended interpretation of reality” (Maitlis & Lawrence, 2007: 58; see also, Thomas, Clark, & Gioia, 1993). Prior research underscores that CEOs utilize strategic communication not only to frame their vision in the case of major organizational changes (e.g., Gioia & Chittipeddi, 1991), but also to foster clarity and understanding in times of strategic stability (Maitlis & Lawrence, 2007). Strategic communication is therefore an important way for CEOs to frame the situation for stakeholders and foster support for their strategic vision, regardless of the firm’s situation (Fiss & Zajac, 2006; Gioia & Chittipeddi, 1991). As Gioia and Chittipeddi (1991: 446) express, strategic communication is “an encompassing feature of the role definition of an effective CEO, and not merely a desirable, but unessential, characteristic.”

New CEO Strategic Communication and the Capital Market

One setting where strategic communication is especially relevant is CEO succession (Fanelli et al., 2009; Whittington et al., 2016). As new CEOs take the reins of a company, they must not only decide on their strategic vision but also how to effectively communicate their vision and associated priorities to the capital market. In doing so, they face two key imperatives that may align in some situations but conflict in others. On the one hand, new CEOs typically seek to establish a unique vision that allows them to leave their mark on the organization (Fanelli et al., 2009; Quigley & Hambrick, 2012). As Porter, Lorsch, and Nohria (2004: 71) observe, this desire arises because “many new CEOs—even in the early days—[are] already thinking about their legacies.” As a result, new CEOs may be inclined to establish priorities that distinguish them from their predecessors. For example, Satya Nadella at Microsoft and Mary Barra at General Motors each moved early in their tenures to articulate strategic priorities that distinguished them from their predecessors while laying the groundwork for their own legacies. Nadella shifted Microsoft’s focus from devices and services to cloud computing and platform strategies (Gallo, 2018), while Barra elevated vehicle safety and operational accountability as core strategic imperatives, diverging from GM’s prior quality-focused shortcomings (Foroohar, 2014).

On the other hand, new CEOs must also secure legitimacy by addressing expectations about the firm and its strategic direction (Hambrick & Fukutomi, 1991). As Porter et al. (2004: 72) further note, “CEOs can easily lose their legitimacy if their vision is unconvincing . . . or if their self-interest appears to trump the welfare of the organization.” New CEOs will be particularly concerned with convincing the capital market of their vision, both because boards frequently rely on capital market feedback to inform their own evaluations of new CEOs (Graffin, Boivie, & Carpenter, 2013) and because shareholders’ investment decisions determine firms’ market performance, meaning they directly affect CEOs’ ability to fulfill their responsibility to create firm value (Busenbark et al., 2016). As a result, new CEOs are motivated to engage in sensegiving toward the capital market by strategically communicating their priorities early in their tenures, in an effort to establish credibility and increase investor confidence in their firms’ future direction (Fanelli et al., 2009; Whittington et al., 2016; Yi et al., 2020).

Recent studies support these ideas by showing that new CEOs engage in sensegiving activities toward the capital market, such as using strategy presentations to articulate their strategic priorities (Whittington et al., 2016) or employing self-promotion techniques to enhance investors’ perceptions of their leadership (Yi et al., 2020). However, a key limitation of this work is its failure to consider how new CEOs’ sensegiving activities are informed by the preceding sensemaking process. Sensemaking involves scanning and interpreting cues within the internal and external environments to identify key factors that could affect the organization (e.g., Gioia & Chittipeddi, 1991; Thomas et al., 1993). Through this process, CEOs assign meaning to environmental signals, which in turn inform their actions and the organizational outcomes they seek to achieve (Thomas et al., 1993). Based on a behavioral view of the firm, these processes are likely to be triggered when strategic leaders perceive a greater need for information (Pfeffer & Salancik, 1978).

In the context of the present study, new CEOs’ perceived need for information will naturally be high due to the inherent uncertainties associated with communicating with the capital market. Again, new CEOs’ ability to establish legitimacy depends on convincing market participants of the coherence and viability of their vision. But because market expectations are rarely explicit, new CEOs rely on environmental cues to interpret the situation and align their priorities accordingly. These cues inform the degree of discretion the new CEO has to chart a new course and reveal the opportunities or risks associated with emphasizing a unique strategic vision. As a result, sensegiving in new CEOs’ strategic communications with the capital market cannot be fully understood without accounting for the sensemaking process that precedes it. In this paper, we develop a model outlining the dynamic, reciprocal process of sensemaking and sensegiving between new CEOs and the capital market to better understand how new CEOs determine and strategically communicate their priorities when first taking office.

A Model of New CEO Strategic Communication

Strategic Topic Novelty in New CEO Communications

As newly appointed CEOs step into their roles, they must determine not only where they want to take the company but also how to signal that direction to investors. This process typically begins with the articulation of a vision—an abstract, aspirational picture of the firm’s future (Gioia & Chittipeddi, 1991). Yet visions, by their nature, are broad and must be translated into more concrete strategic priorities that convey how the vision will be realized (Fanelli et al., 2009; Whittington et al., 2016). These priorities are made visible through the strategic topics that new CEOs emphasize in their external communications (Eklund & Mannor, 2021). This might include, for example, whether the new CEO will focus more of their limited attention and firm resources on internal or external stakeholders, pursue cost-cutting strategies or innovation, or seek to restructure the company or expand into new markets.

A central consideration for new CEOs when communicating their priorities is whether, and to what extent, they should distinguish them from those of their predecessors. Not only does this shape the uniqueness of their vision and their potential to leave their mark on the organization (Fanelli et al., 2009; Porter et al., 2004; Quigley & Hambrick, 2012), but investors also naturally interpret a new CEO’s priorities in relation to those of the predecessor. Consistent with this logic, we frame new CEO communication as sensegiving in terms of strategic topic novelty, which we define as the degree of distinctiveness in the strategic topics that new CEOs emphasize relative to those of their predecessors. Thus defined, strategic topic novelty is an observable dimension of new CEOs’ communicated priorities that reflects how they reconcile their desire to establish a unique vision with the need to legitimize their appointment to the investment community.

In focusing on this construct, we highlight two other important considerations. First, we recognize that besides introducing novel topics, new CEOs may distinguish themselves by emphasizing the same topics as their predecessors but indicating that they are moving in the opposite direction. However, following the idea that new CEOs inherently desire to leave their mark on the company, establishing a legacy typically requires more than simply changing direction along topics emphasized by the predecessor; it requires bringing something genuinely new to the conversation. Moreover, even when charting a new course, new CEOs generally avoid publicly opposing their predecessors. This is partly due to norms of mutual support among corporate elites (McDonald & Westphal, 2011) and partly because overt negativity in public communications can be viewed unfavorably by investors (Price, Doran, Peterson, & Bliss, 2012). Consistent with this, we suggest that strategic topic novelty is the primary way that new CEOs manage the challenge of legitimizing their appointment while simultaneously seeking to establish their own unique vision. Second, while strategic communication by new CEOs precedes strategic action and can independently influence market reactions (Gao et al., 2016; Gioia & Chittipeddi, 1991), we do not view it as mere impression management. Rather, we suggest that there is generally intent behind the strategic topics communicated by new CEOs. This is because purely symbolic communication is likely to undermine the credibility that CEOs seek to establish when communicating their vision and priorities to the capital market (Busenbark, Lange, & Certo, 2017; Whittington et al., 2016).

Building on these ideas, we conceptualize strategic topic novelty as part of a reciprocal process of sensemaking and sensegiving between new CEOs and the capital market. Within this theoretical framework, strategic topic novelty is not viewed as “cheap talk” solely to manage investor perceptions, but as a serious reflection of new CEOs’ priorities and intended actions, informed by their sensemaking of the situation. Such sensemaking involves identifying and interpreting environmental cues regarding what the context demands and how the market evaluates the CEO’s fit with those demands. New CEOs must also consider how to reconcile their desire for distinctiveness with legitimacy concerns. Again, these imperatives may not always be aligned, and it is precisely this tension that generates variance in the degree of novelty communicated. As a new CEO considers how much to distinguish their priorities from their predecessor’s, two contextual cues become especially salient in shaping their sensemaking—the nature of the succession and the capital market’s initial reaction to their appointment. New CEOs’ interpretations of these cues guide their sensegiving through early strategic communications, which in turn elicit market reactions that feed back into CEOs’ ongoing interpretations of the situation. Together, these interactions form a feedback loop where new CEOs and the capital market continuously influence one another, shaping both the strategic narrative and the direction and actions of the firm during a CEO transition. We elaborate on each of these elements in the following sections.

The Nature of the Succession

The circumstances surrounding the predecessor’s departure set the stage for a new CEO, providing initial cues regarding how they might align their priorities with the situation and the latitude they have in outlining a novel strategic vision (Berns & Klarner, 2017; Schepker, Kim, Patel, Thatcher, & Campion, 2017; Zhang & Rajagopalan, 2004). A key distinction in this regard lies in whether the succession occurs following a dismissal or under more routine conditions. Dismissal occurs when a CEO is forced out of the company by the board, often in an attempt to pacify shareholders following periods of poor performance (e.g., Chen & Hambrick, 2012; Shen & Cannella, 2002a). In contrast, routine successions occur when the outgoing CEO departs under planned or stable conditions, such as for a retirement or voluntary exit to pursue new opportunities (Berns & Klarner, 2017; Gentry, Harrison, Quigley, & Boivie, 2021; Schepker et al., 2017). These conditions will have disparate implications for how new CEOs make sense of the situation and subsequently use their interpretations to frame their strategic priorities.

Dismissal sends a strong signal of dissatisfaction with the prior leadership, typically linked to the predecessor’s failure to meet performance targets or adapt to evolving market demands (e.g., Gentry et al., 2021; Hilger, Mankel, & Richter, 2013). Shareholders and boards often attribute these failures to the outgoing CEO’s strategic decisions, creating an expectation for the incoming CEO to chart a new course for the firm (Busenbark et al., 2016; Carpenter, Geletkanycz, & Sanders, 2004). Empirical evidence supports this view, showing that shareholders frequently react positively to dismissals as signals of impending change (Hilger et al., 2013). Under these circumstances, new CEOs’ efforts to establish legitimacy will align with their desire to establish a unique vision, so they are likely to perceive a high degree of discretion in introducing novel strategic priorities compared to their predecessor’s. Indeed, research indicates that successors following dismissals often exhibit low psychological commitment to their predecessors’ strategic legacies (Shen & Cannella, 2002b). At the same time, they are unlikely to publicly oppose or criticize their predecessors, based on the logic already presented. Anecdotal evidence illustrates this dynamic. For instance, after Hewlett-Packard’s board effectively forced out Mark Hurd in 2010 amid performance and conduct concerns, successor Leo Apotheker immediately highlighted novel strategic priorities such as spinning off the PC division and pivoting to software via the autonomy acquisition—moves framed as a strategic redirection for HP rather than critiques of Hurd (Mccracken, Saitto, & Ricadela, 2011). Similarly, Barnes & Noble’s William Lynch departed in 2013 under pressure from Nook losses, and new CEO Michael Huseby emphasized a return to physical stores and merchandising as the core strategy, distancing his priorities from Lynch’s digital bet without public attacks (A. Brown, 2013). Overall, when outlining their strategic priorities to the capital market, new CEOs following dismissals are likely to highlight novel strategic topics that deviate significantly from those emphasized by their predecessors. By doing so, they will be able to establish a unique strategic vision while simultaneously maintaining professionalism and respect for their predecessor and establishing legitimacy with the capital market through responsiveness to the situation.

In contrast to dismissals, routine successions often occur during times of positive firm performance, which fosters expectations of continuity by suggesting that the strategic direction set by the predecessor was effective (Karaevli & Zajac, 2013). In many cases, outgoing CEOs also groom their successors to ensure a smooth leadership transition, further reinforcing expectations for strategic continuity (Shen & Cannella, 2003). Thus, while they may still have an inherent desire to establish their own unique vision (Porter et al., 2004), they are likely to interpret routine successions as situations where legitimizing their appointment demands some degree of stability. This places constraints on the degree of novelty new CEOs can effectively communicate when outlining their strategic priorities. Under stable circumstances, introducing too much novelty or deviating substantially from the predecessor’s strategic legacy risks unsettling investors. Thus, when describing their strategic priorities to the capital market, new CEOs following a routine succession may be hesitant to deviate too far from the strategic topics their predecessors discussed.

Given that it is the predecessor’s departure that triggers the succession event, the nature of the departure is likely the first and most salient cue new CEOs use to make sense of their situation. Dismissals provide new CEOs with greater discretion to emphasize novel strategic topics, as gaining legitimacy in this case aligns with their desire to establish a unique vision. Conversely, legitimizing their appointment in the case of a routine succession requires that they signal some degree of continuity and stability, encouraging adherence to the strategic direction of their predecessor. Thus, we hypothesize:

Hypothesis 1 (H1): A new CEO’s strategic communications with the capital market will reflect a higher degree of strategic topic novelty following a dismissal than following a routine succession.

Market Reactions to the New CEO Appointment

While the nature of the succession provides the initial context for new CEOs’ sensemaking, we argue that initial market reactions to their appointment moderate the relationship between succession type and strategic topic novelty. The capital market’s initial reaction occurs immediately following the new CEO’s announcement and reflects investors’ evaluation of the selection (Graffin et al., 2013; Yi et al., 2020; Zhang & Wiersema, 2009). Thus, this reaction, which can be positive or negative, reflects how well the market thinks the new CEO fits the circumstances of the succession. Positive reactions occur when the announcement drives increased investor demand for the company’s stock, signaling confidence in the CEO and the firm’s future direction under their leadership. Conversely, negative reactions are marked by a decline in stock demand, reflecting investor concerns about the CEO’s suitability for the situation and the firm’s future prospects. Either way, investors are implicitly evaluating whether the CEO is the right choice for the situation, using the appointment as a proxy for potential alignment with the firm’s needs.

Importantly, this market response occurs after the predecessor’s departure but before the new CEO has communicated their strategic priorities or taken any action. 2 As Porter et al. (2004: 68) observe, CEOs are “always sending a message,” and “the first big message is in the CEO’s appointment itself . . . [which is] sent before the new CEO even does anything.” Recent research suggests that this initial reaction plays a role in shaping the board’s early evaluations of the CEO, with more negative reactions having the potential to trigger early dismissals (Graffin et al., 2013). Given the stakes, new CEOs are likely to pay close attention to the market’s reaction to their appointment. Because these reactions offer a salient signal of investor expectations, they can either reinforce or complicate CEOs’ initial interpretations of the succession context.

As we develop our moderating hypotheses regarding capital market reactions, we consider positive and negative reactions separately. While both positive and negative reactions can vary in intensity, the valence of the reaction is particularly critical because people interpret positive and negative feedback through distinct psychological processes (Kahneman & Tversky, 1979). Negative feedback is not simply the inverse of positive feedback; rather, it activates different cognitive and emotional responses (e.g., Rozin & Royzman, 2001). Examining these reactions separately allows us to uncover potential asymmetries in how the market’s optimism or skepticism interact with the nature of the succession, providing deeper insight into how new CEOs adjust their strategic framing in response to early market feedback.

Positive market reactions

In new CEOs’ quest to validate their initial interpretations of the succession context, positive market reactions reflect investor confidence in the firm’s future under their leadership (Graffin et al., 2013; Quigley & Hambrick, 2012). The degree of this initial endorsement provides an important piece of feedback to the incoming CEO. The higher the positive market feedback, the more it reinforces new CEOs’ confidence in their sensemaking, reducing uncertainty and bolstering their prior interpretations of the succession context.

Again, given dismissals suggest a general dissatisfaction with the prior leadership, following a dismissal emboldens new CEOs to emphasize more novel strategic priorities that take the firm in new directions. Dismissals create a disruptive context in which continuity is not expected and legitimacy can be gained by responding with change. A more favorable capital market reaction to the new CEO’s appointment can strengthen this effect, as it provides validation and psychological safety that reduce the personal and reputational risks of acting boldly. Rather than discouraging novelty, positive feedback in this context reinforces the CEO’s self-efficacy and discretion, enabling them to gain legitimacy by framing novel strategic priorities as decisive responses to the deficiencies implied by the predecessor’s dismissal (Ilgen, Fisher, & Taylor, 1979; London & Smither, 1995; Tolli & Schmidt, 2008). For a new CEO, this dynamic is likely to translate into a greater willingness to introduce novel strategic priorities, as the market’s endorsement further emboldens them to take advantage of the latitude afforded by a dismissal and to emphasize a more distinct vision relative to their predecessor’s.

By contrast, a more positive reaction to the new CEO’s appointment following a routine succession is likely to encourage greater commitment to continuity. Whereas a favorable reaction will still increase new CEOs’ self-efficacy (Tolli & Schmidt, 2008), more positive feedback in this context will reflect a higher degree of confidence in the CEO’s ability to carry on the legacy of the predecessor. That is, new CEOs following a routine succession are likely to perceive the market’s approval as an endorsement of the firm’s current trajectory and their suitability to sustain it (Vancil, 1987; Zhang & Rajagopalan, 2004). This reinforces the need for a measured approach when communicating their priorities to the capital market, as a way to signal stability and alignment with the predecessor’s priorities. In this context, greater emphasis on novelty would likely be perceived as unnecessarily risky, since it could irritate market participants and undermine the very legitimacy that positive reactions initially conferred. A more positive market response, therefore, amplifies the tendency of new CEOs in routine successions to emphasize less strategic topic novelty.

Altogether, more positive market reactions to a new CEO’s appointment strengthen the relationship between the predecessor’s departure type and the amount of strategic topic novelty communicated by the new CEO. Thus, we hypothesize:

Hypothesis 2 (H2): The positive relationship between predecessor dismissal (relative to routine succession) and the degree of strategic topic novelty expressed by a new CEO will be stronger when the market’s initial reaction to the new CEO’s appointment is more positive.

Negative market reactions

For new CEOs, negative market reactions complicate their sensemaking of the succession context (Graffin et al., 2013; Zhang & Wiersema, 2009). Because market responses shape public perceptions and carry career risks (Elsbach, 1994; Gamache & McNamara, 2019), negative reactions might be especially impactful. Negative feedback triggers feelings of self-consciousness, doubt, and disorientation (Rozin & Royzman, 2001; Swann & Buhrmester, 2012). These emotions can prompt defensive, self-preserving behaviors due to the abrupt mobilization of cognitive resources to process and mitigate perceived threats (e.g., Ito, Larsen, Smith, & Cacioppo, 1998; Rozin & Royzman, 2001; Taylor, 1991). The more negative the market reaction, the more likely it is to complicate new CEOs’ sensemaking and cause them to deviate from the initially expected behavior when laying out their strategic priorities to the capital market.

In the case of dismissal, these dynamics will decrease the new CEO’s perceived self-efficacy and discretion in introducing novel strategic topics. Because the market is usually optimistic about strategic improvements after a forced turnover (Hilger et al., 2013; Keil, Lavie, & Pavićević, 2022), a negative response to their appointment in this context will be particularly disorienting. That is, a negative reaction may lead new CEOs to doubt whether communicating more novel topics truly enhances legitimacy. These doubts are compounded by the possibility that introducing specific novel topics could expose them to further criticism (DesJardine, Shi, & Sun, 2022; Oehmichen, Firk, Wolff, & Maybuechen, 2021). Given this, and the fact that negative feedback tends to trigger defensive and self-preserving behaviors (e.g., Ito et al., 1998; Rozin & Royzman, 2001), we expect that new CEOs following a forced turnover who receive a negative response to their own appointment will adopt a more risk-averse approach. Thus, while dismissals typically provide latitude for strategic novelty, the more negative the market reactions the more they constrain this discretion, leading new CEOs to temper their strategic communications and communicate less novelty than they might otherwise.

In routine successions, negative feedback will similarly complicate new CEOs’ sensemaking. But in this case, such a reaction is likely to disrupt new CEOs’ commitment to continuity (Zhang & Rajagopalan, 2004). Faced with skepticism, new CEOs may question their initial interpretations of the situation and reconsider how to best reconcile the need to legitimize their appointment with their desire to establish a unique vision. We specifically posit that, during a routine succession, a negative reaction to the new CEO’s appointment may lead them to overcompensate and attempt to justify their appointment by making bolder moves than a routine succession would typically require. In their communications with the capital market, they may attempt to regain control of the narrative and attract investor attention by highlighting more novel strategic topics relative to their predecessor’s.

Overall, negative reactions complicate sensemaking and push new CEOs toward divergent approaches—manifesting as risk-averse adjustments following dismissals, but overcompensating through increased novelty during routine successions. Thus, we posit:

Hypothesis 3 (H3): The positive relationship between predecessor dismissal (relative to routine succession) and the degree of strategic topic novelty expressed by a new CEO will be weaker when the market’s initial reaction to the new CEO’s appointment is more negative.

Market Reactions to the New CEO’s Strategic Communication

To complete our theoretical model, we consider how the capital market reacts to new CEOs’ sensegiving in terms of their communicated degree of strategic topic novelty. Just as new CEOs engage in sensemaking and sensegiving by developing and then communicating their strategic priorities to the market, the capital market engages in sensemaking by interpreting these messages and gives sense through its reaction to the new CEO’s strategic communications. Compared to the initial market reaction to the new CEO’s announcement, which tends to be based on inferences and heuristics (Graffin et al., 2013), subsequent market reactions are based on more solid information. Prior research has shown that the capital market responds strongly to information released by CEOs (e.g., Eklund & Mannor, 2021; Kavadis, Heyden, & Sidhu, 2022; Yi et al., 2020), as it reduces uncertainty and enhances the predictability of firm strategy and performance (Falchetti, Cattani, & Ferriani, 2022; Graffin et al., 2013). Accordingly, we suggest that the degree of strategic topic novelty communicated by the new CEO will evoke an additional market reaction reflecting a revised evaluation of the CEO and how well their strategic priorities fit with the situation. The positivity or negativity of the response depends on the alignment between the succession context and the degree of novelty expressed by the new CEO.

Following a dismissal, the underlying expectation among investors is that the new CEO will provide a break from the deficiencies of prior leadership by charting a new course (Gioia & Chittipeddi, 1991; Hilger et al., 2013). In this context, the communication of novel strategic topics serves as an important legitimacy-building mechanism because it demonstrates responsiveness to the very shortcomings that triggered the dismissal. Thus, when new CEOs emphasize strategic topic novelty after a dismissal, investors are likely to respond favorably. Conversely, when a new CEO in this context fails to adequately distinguish their vision or priorities from those of their predecessor, the market may interpret this as a failure to recognize or address the firm’s pressing challenges. Such a signal raises doubts about the CEO’s fit for the role, triggering a negative reaction from investors.

In routine successions, the logic is reversed. Because routine transitions typically occur in periods of relative stability or success, continuity is the expected and legitimate course of action (Schepker et al., 2017). In such settings, investors are more skeptical of efforts by a new CEO to chart a novel direction, as excessive novelty may appear unnecessary or even egocentric—echoing concerns that CEOs can lose their legitimacy if their vision seems self-interested or contrary to the interests of the organization (Porter et al., 2004). Accordingly, when new CEOs emphasize substantial novelty following routine successions, investors are more likely to react negatively. But when they stress continuity and position themselves as building upon the momentum of their predecessors, investors are likely to respond more positively, interpreting such communication as both legitimate and credible. Therefore, we hypothesize:

Hypothesis 4 (H4): The capital market will react more positively to higher levels of strategic topic novelty communicated by a new CEO following a dismissal than following a routine succession.

Method

Sample and Data

We test our hypotheses using a sample of CEO successions in U.S. companies listed among Standard and Poor’s (S&P) 1500 between 2004 and 2018. We end our sample in 2018 to avoid distortions from the COVID-19 pandemic, which dominated earnings calls following the outbreak, and to allow sufficient time to observe subsequent strategic actions, ensuring that our measure captures strategic intent rather than impression management. We identify CEO succession events using Gentry et al.’s (2021) turnover database, which provides detailed, hand-collected data on CEO departure reasons from media coverage and press releases for S&P 1500 firms. In addition, we collect the exact dates when new CEOs were announced through manual searches of headlines in RavenPack. We evaluate new CEOs’ strategic communication by comparing the strategic topics they address with those of their predecessors in the presentation sections of quarterly earnings calls. Strategic topics were assessed using computer-aided textual analysis based on the dictionaries developed by Eklund and Mannor (2021).

Earnings calls are a critical communication channel through which CEOs engage in active information exchange with the capital market (e.g., Guo et al., 2021; Pan, McNamara, Lee, Haleblian, & Devers, 2018). Compared to other communication channels, such as strategy presentations or annual letters to shareholders, which are published either irregularly or delayed up to a year following a CEO appointment (e.g., Fanelli et al., 2009; Whittington et al., 2016), quarterly earnings calls are widely held within 90 days after an appointment. We consequently expect the first earnings call in a CEO’s tenure to be particularly informative regarding the new CEO’s initial strategic topics (Eklund & Mannor, 2021; Yi et al., 2020). Hence, we focus on the first earnings call of new CEOs and compare it to the strategic topics communicated by their predecessors during their last year in office. Earnings call transcripts were collected from Thomson Reuters Street Events and LexisNexis Full Disclosure Wire. We collect financial data from Thomson Reuters Datastream, CEO and board characteristics from BoardEx, CEO compensation from Execucomp, and data on institutional ownership from Thomson One Banker.

Our full initial sample consists of 2,765 CEO succession events in 1,522 firms where we are able to identify the first earnings call of the new CEO. We exclude 400 successions where the incoming CEO is an interim, given that interim CEOs are unlikely to experience the same legitimation pressure due to their temporary position. We further exclude 376 succession events in which no new CEO can be identified due to delisting or acquisitions, or no dismissal or departure rationale classification is available. In addition, to obtain an accurate picture of the predecessor’s strategic topics that is not solely driven by the succession process, we require the majority of earnings calls from the predecessor’s last year to be available and the CEO to have spoken at least 250 words per call, leading to the exclusion of 182 additional successions. The final sample with all necessary control variables comprises 1,647 succession events in 1,187 firms.

Independent and Dependent Variables

As noted previously, we assess strategic topic novelty by applying computer-aided text analysis to CEOs’ presentations in quarterly earnings calls and comparing the strategic topics of new CEOs with those of their predecessors. 3 We use the presentation portion of these calls because it can be designed according to the CEO’s ideas and plans, making it an ideal medium for strategic communication (Washburn & Bromiley, 2014). We identify CEOs’ strategic topics using the comprehensive categorization and dictionaries developed by Eklund and Mannor (2021), which consist of 13 distinct strategic topics ranging from financial risk management strategies to new market entry strategies. 4 We measure CEOs’ focus on each strategic topic by scaling the number of words they say within each respective dictionary, scaled by 1,000 words. Next, we compute the cosine similarity for the distribution of strategic topics between the first earnings call of the new CEO and the mean of the last four earnings calls of the predecessor CEO (Angus, 2019; Lee, 2016; Testoni, 2022). 5 The first earnings call is the earliest structured and widely publicized venue where new CEOs articulate their strategic priorities. As such, it is likely to contain the greatest amount of new information regarding their strategic priorities and be most salient to the capital market’s subsequent assessment of those priorities.6,7 We focus on the predecessor’s last four earnings calls to ensure we capture the full breadth of the strategic issues and initiatives emphasized by the predecessor toward the end of their tenure. The calculation is as follows:

The cosine similarity measure captures the uncentered correlation between two vectors, estimating the similarity in CEOs’ use of strategic topics (Angus, 2019). Reversing this value, the resulting variable strategic topic novelty is continuous and ranges from 0 to 1 with higher values indicating a greater degree of novelty in the new CEO’s strategic topics compared to their predecessor’s (Testoni, 2022). We provide illustrative examples of CEOs’ calls reflecting high and low values of strategic topic novelty in the Online Appendix B (Tables B2 and B3).

We classify succession types by reviewing the hand-collected departure rationales from Gentry et al.’s (2021) database of CEO departures for each succession in our sample. We do so to specify a conservative classification that is consistent with our conceptual argumentation from H1. For convenience when interpreting the results, we label the variable to specifically reflect dismissals, as compared to more routine successions. The resulting variable predecessor dismissal is binary and equals 1 if the turnover was forced by the board and 0 if the departure occurred under more routine conditions or circumstances that reflect organizational stability. The variable is coded in the first quarter where the new CEO participates in an earnings call. Of the 1,647 succession events in our final sample, we identify 254 (or approximately 15.5 percent) as dismissals, while the remaining 1,393 were classified as routine successions.

We assess capital market reactions to new CEO appointments using cumulative abnormal returns (CARs), which reflect the difference between the actual return of a security and its expected return over a given period. In keeping with prior management literature (e.g., Gangloff, Connelly, & Shook, 2016; Yi et al., 2020), we calculate expected returns by employing a standard market-adjusted return model and predicting returns with an estimation window from −241 to −21 days before the succession announcement. We use daily stock price data for each firm and market data for the S&P 1500 index over a three-day event window from one day before to one day following the succession announcement [−1; 1] (e.g., Gligor, Novicevic, Feizabadi, & Stapleton, 2021; Shi, Zhang, & Hoskisson, 2019). Short event windows offer the advantage of limiting the influence of possible confounding effects (Tian, Haleblian, & Rajagopalan, 2011). To isolate the differential effects of positive and negative market reactions in line with our hypotheses, we create distinct measures for positive and negative CARs using a spline function. To capture the positive market reactions to the new CEO for H2, we create the variable positive announcement CARs with negative CAR values set to 0 and positive values as continuous. To capture the capital market’s doubts about the new CEO, we construct negative announcement CAR by setting positive CAR values to 0 and converting negative CARs into their absolute values (Yi et al., 2020). This operationalization captures the intensity of market skepticism, such that higher values reflect stronger negative market reactions to the CEO appointment. This transformation also facilitates interpretation of the regression coefficients, as increases in the measure correspond directly to stronger negative reactions, consistent with Hypothesis 3. 8

We also use CARs to assess capital market reactions to new CEOs’ strategic topic novelty. In comparison to new CEO announcements, which may be unanticipated, the date of earnings calls is predetermined and known by capital market participants. Therefore, we follow prior research in strategy and accounting by measuring earnings call CARs over two days, including the earnings call date and 1 day after [0;1] (Pan et al., 2018; Price et al., 2012). In this way, we capture the capital market’s immediate reaction to the earnings call event (Pan et al., 2018). The abnormal returns are calculated by subtracting the S&P market returns from the observed returns to then accumulate them over the event period [0;1] (Price et al., 2012; Shi et al., 2019). 9

Control Variables

We control for factors at various levels of analysis with possible influences on strategic topic novelty, CEO succession processes, and/or the capital market’s perception of the new CEO. At the firm-quarter level, we include firm size (natural logarithm of total assets) (Quigley, Hubbard, Ward, & Graffin, 2020), leverage (ratio of long-term debt to total assets), and sales growth (percentage change in year-over-year sales, comparing each quarter’s sales to the same quarter in the previous year) (Davis, Ge, Matsumoto, & Zhang, 2015). To capture pre-succession financial performance as a major determinant of the content of strategic communication, we control for industry-adjusted return on assets (ROA) at the two-digit SIC level in the quarter preceding the succession. Finally, we control for earnings surprises as the difference between the actual quarterly EPS and the mean analyst forecast for the given quarter.

We also considered the potential influence of the top management team (TMT), board of directors, and key capital market stakeholders on new CEOs’ strategic communication. In line with our focus on succession, we assessed changes in the composition of the non-CEO top management team (TMT changes) and the board of directors (board changes), using dummy variables indicating whether at least one executive or director joined or left during the year, and 0 otherwise. To capture capital market stakeholder influence, we control for dedicated ownership (Bushee, 1998), analyst coverage (log number of analysts), and analyst consensus.

At the CEO level, we account for various differences between the new CEO and their predecessor, reflecting relative changes in characteristics that may shape both the capital market’s reaction to the new CEO and/or their strategic communication. For simplicity, we describe the base variable construction for each measure at the individual level, but controls included in empirical models reflect the difference between the new CEO (t = 0) and the predecessor CEO (t − 1). We control for CEO time in company using the number of years the CEO had worked in the company prior to the succession (Graffin, Carpenter, & Boivie, 2011), CEO duality (equals 1 if the CEO is also the chair of the board and 0 otherwise), prior CEO experience (equals 1 if the individual was CEO at another firm before becoming CEO of the focal firm and 0 otherwise), CEO functional background (equals 1 if the CEO’s primary experience is in accounting, operations, manufacturing, engineering, or finance, and 0 otherwise), and CEOs’ industry experience based on the two-digit SIC codes (equals 1 if the CEO worked in the same industry as the focal firm prior to being appointed, 0 otherwise). Additionally, we account for personality differences. We focus on CEOs’ levels of narcissism using the Open Language Chief Executive Personality Tool (Harrison, Boivie, Hubbard, & Petrenko, 2024).

Lastly, we control for additional features of the CEO’s communication in the presentation portion of earnings calls in order to isolate the effects of strategic topic novelty. We account for CEOs’ overall tendency to speak about strategy (sum strategic topics), which reflects the total number of words from the strategic topic dictionaries that the CEO uses per 1,000 words. We also control for strategic breadth using a Herfindahl index reflecting how broadly managerial strategic attention is distributed across strategic topics (Eklund & Mannor, 2021), and CEOs’ tone in models predicting earnings call CARs, measured as the number of positive words minus the number of negative words divided by the total number of positive and negative words spoken by the CEO, based on the domain-specific dictionaries developed by Loughran and McDonald (2015). 10

Data Analysis

We employ different analytic techniques. Because our dependent variable strategic topic novelty is bounded between 0 and 1, we use fractional probit regressions to test H1, H2, and H3 (e.g., Chow, Petrou, & Procopiou, 2023). To test H4, we predict earnings call CARs using ordinary least squares (OLS) regressions. We include year, quarter, and industry fixed effects to control for macroeconomic and industry-level effects and estimate all models using robust standard errors, which we cluster by firm to account for nonindependence from multiple observations being associated with the same firms. Further, we winsorize continuous variables at the 1st and 99th percentiles to mitigate the effect of potential outliers, and we lag all firm-related controls to reduce potential bias from contemporality and mitigate reverse causality (Tian et al., 2011; Zhang, 2008).

Because we only include successions of CEOs who have participated in earnings calls in our sample, we use Heckman’s two-stage approach to address potential selection bias (Certo, Busenbark, Woo, & Semadeni, 2016; Hill, Johnson, Greco, O’Boyle, & Walter, 2021). We created a dummy variable equal to 1 for CEO successions with earnings call transcripts available and 0 otherwise. After excluding succession events where no new CEO was appointed (for example, due to delisting or acquisition), we identify 114 successions in firms with no earnings calls, but where financial data and necessary controls are available. In the first stage of our analysis, we ran a probit regression on this dummy variable using the variable S&P 500 firm as an exclusion criterion. 11 We also included CEO, firm, and industry characteristics as controls (see Online Appendix D, Table D1). We then calculated the inverse Mills ratio from this regression, which we used as a control in the second stage regression models to account for potential sample-induced endogeneity.

Results

Primary Results

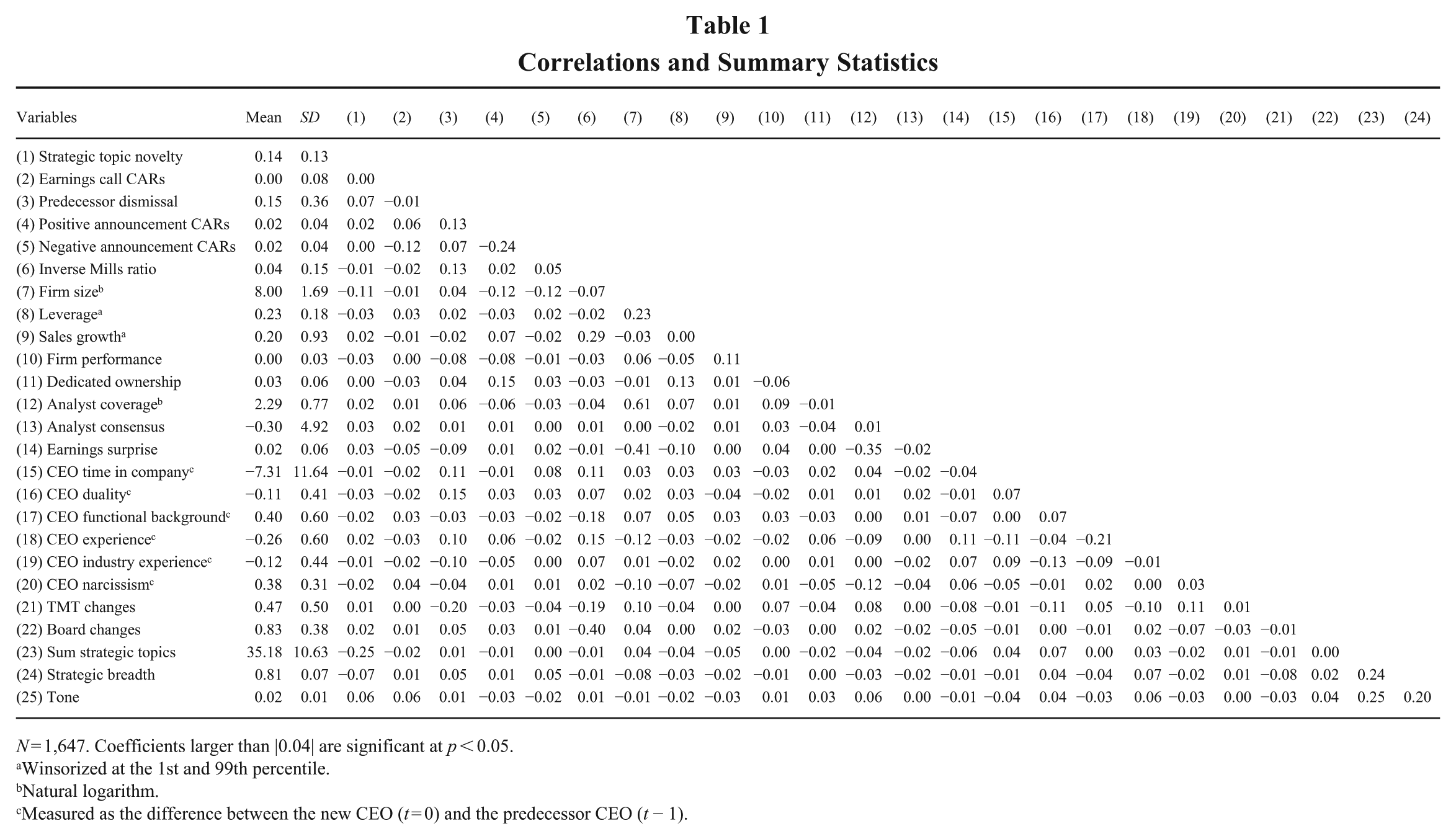

Table 1 provides descriptive statistics and correlations for all variables used in the regressions. Strategic topic novelty has a mean value of 0.14 and a standard deviation (SD) of 0.13, demonstrating relatively high variance across firms. Similar to other studies, predecessor dismissal accounts for 15 percent of the succession events in our sample (Shen & Cannella, 2002b). For announcement CARs, we observe a slight tendency for negative appointment reactions in our sample. The correlation between predecessor dismissal and strategic topic novelty is positive, providing first indications consistent with H1. To further illustrate the importance of strategic communication around the time of new CEO appointments, we compare strategic topic novelty for CEOs between earnings calls for a number of occasions at different levels of analysis (CEO-, firm-, industry-, and macro-level). As reported in Online Appendix B, Table B4, we find the greatest levels of strategic topic novelty for newly appointed CEOs across all contexts. 12 Pairwise correlations of all variables further suggest that multicollinearity should not be a major concern. To further assess this issue, we calculate variance inflation factors and observe that all values are below 3 (1.5 on average), which is below commonly accepted thresholds (Wooldridge, 2010).

Correlations and Summary Statistics

N = 1,647. Coefficients larger than |0.04| are significant at p < 0.05.

Winsorized at the 1st and 99th percentile.

Natural logarithm.

Measured as the difference between the new CEO (t = 0) and the predecessor CEO (t − 1).

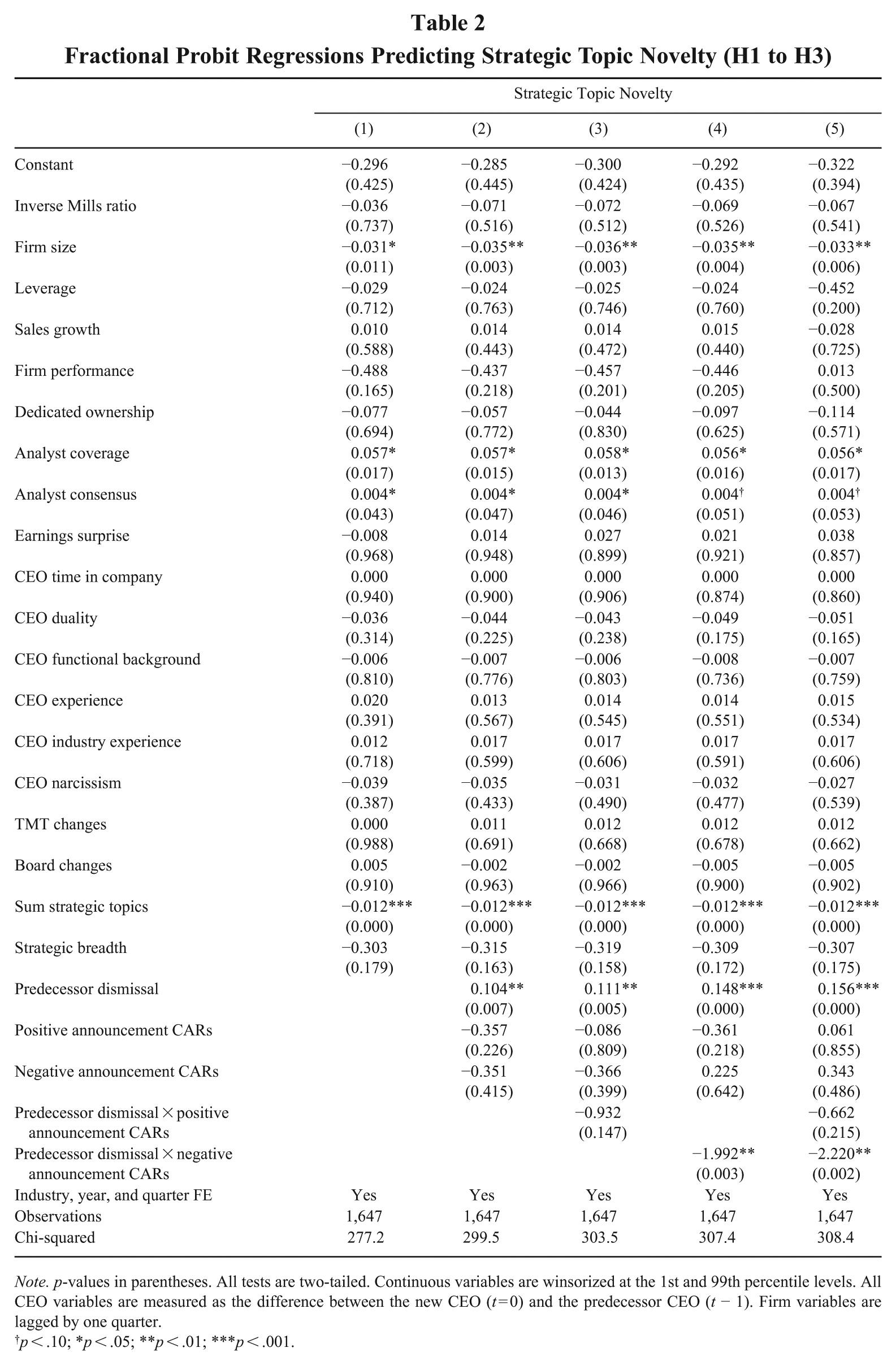

Table 2 presents the results of models testing our first three hypotheses. 13 Related to H1, we find a positive and statistically significant coefficient for predecessor dismissal in Model 2 (β = 0.104, p = .007). This is consistent with our expectation that new CEOs tend to communicate a higher degree of strategic topic novelty following a dismissal than following a routine succession. We assess the result’s practical significance by comparing predicted values of strategic topic novelty when the predecessor is dismissed by the board relative to a routine succession. Results in Model 2 indicate that strategic topic novelty is about 17.5 percent higher ((0.161 – 0.137) / 0.137) in the event of predecessor CEO dismissal. These results provide support for H1.

Fractional Probit Regressions Predicting Strategic Topic Novelty (H1 to H3)

Note. p-values in parentheses. All tests are two-tailed. Continuous variables are winsorized at the 1st and 99th percentile levels. All CEO variables are measured as the difference between the new CEO (t = 0) and the predecessor CEO (t − 1). Firm variables are lagged by one quarter.

p < .10; *p < .05; **p < .01; ***p < .001.

Model 3 includes the interaction term of predecessor dismissal and positive announcement CARs to investigate H2. The interaction is not statistically significant (β = −0.932, p = .147). Thus, while the main relationship between predecessor dismissal and strategic topic novelty holds positive (β = 0.111, p = .005), positive announcement CARs do not significantly alter this relationship. While the relationship is not significant, it is interesting that the sign is opposite to what we predicted in H2. The results thus provide no support for H2 but warrant attention. We discuss this result further in the discussion section.

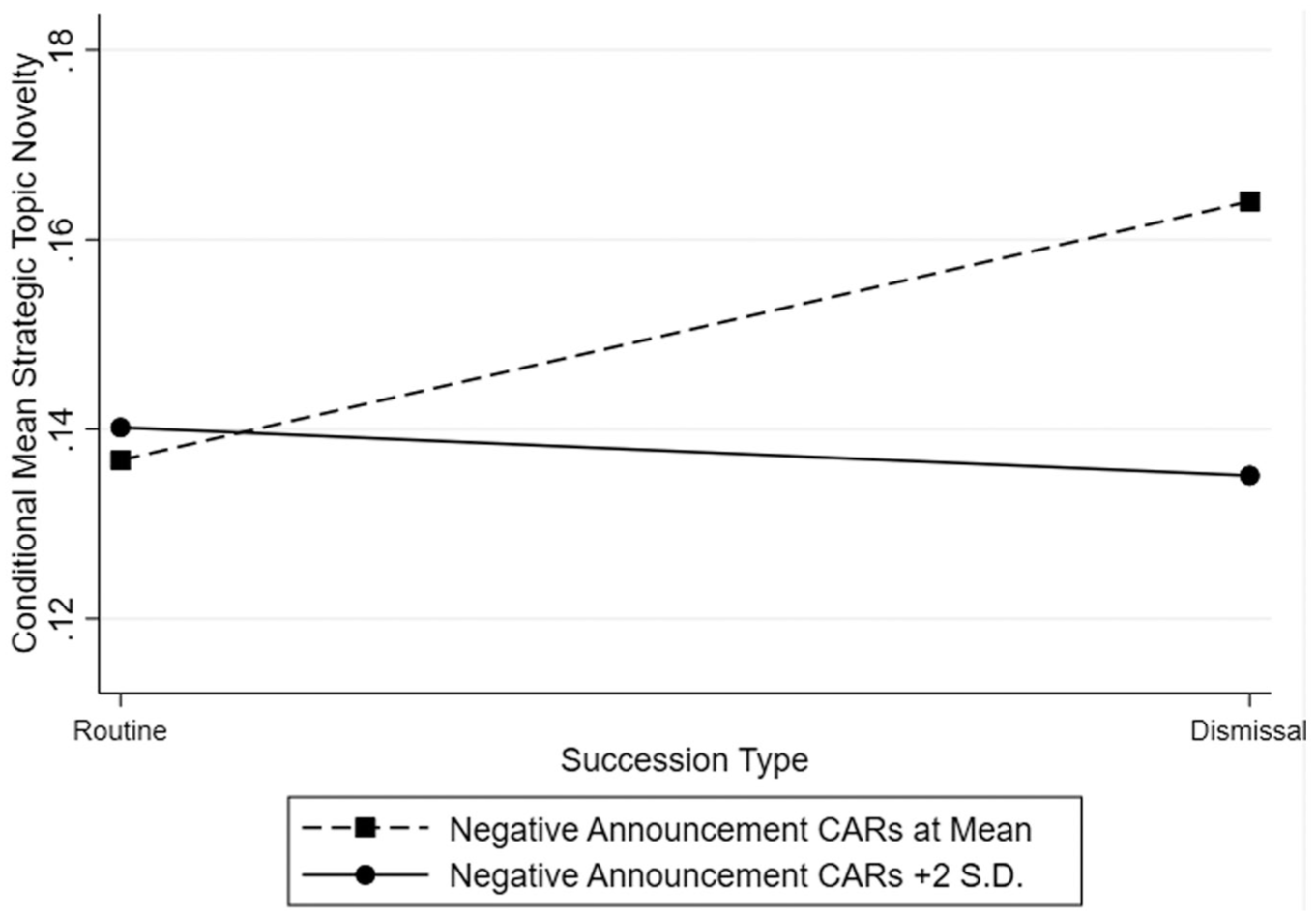

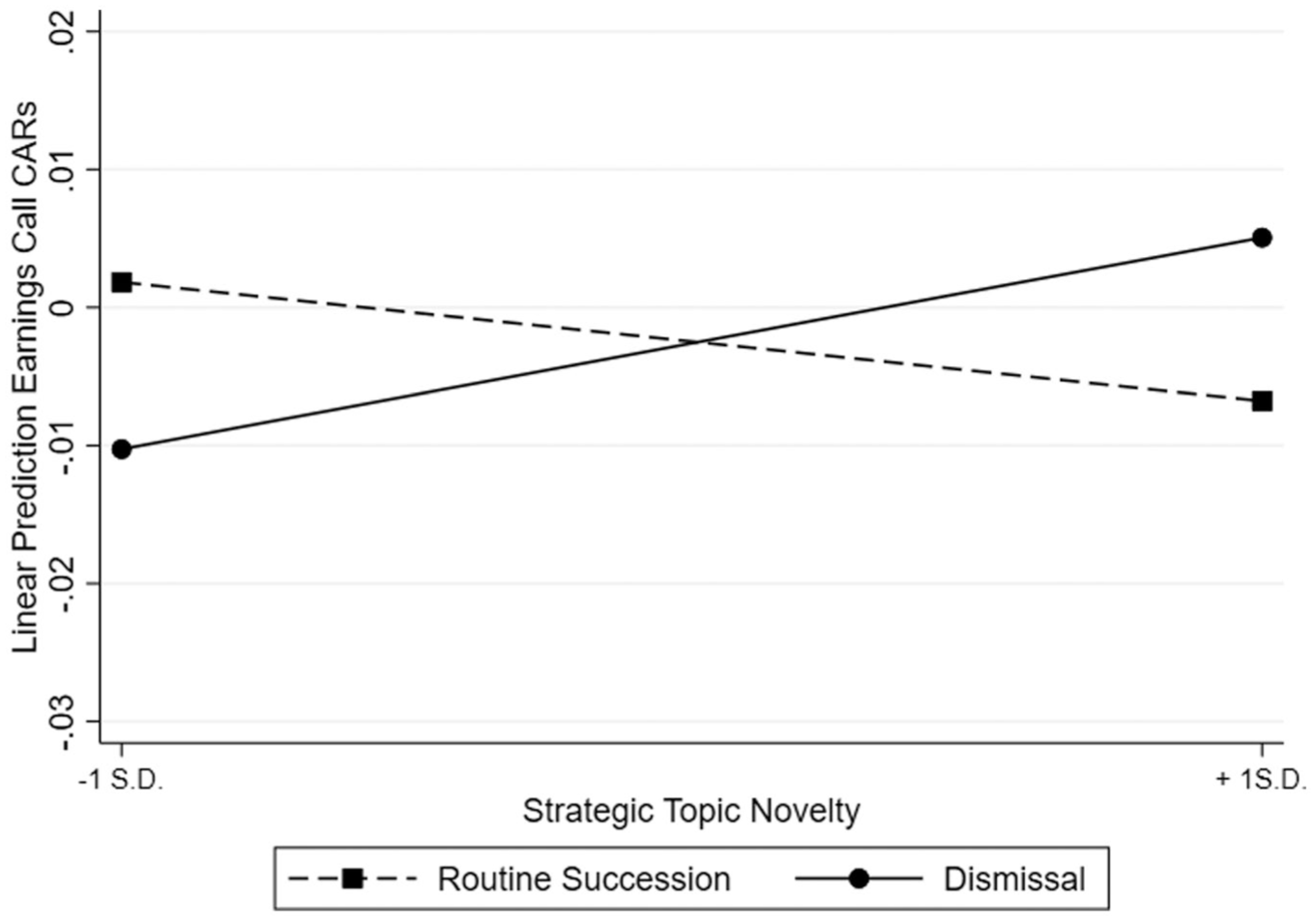

Model 4 includes the interaction term of predecessor dismissal and negative announcement CARs used to test H3. The interaction is negative and significant (β = −1.992, p = .003), showing that the positive main relationship between predecessor dismissal and strategic topic novelty (β = 0.148, p = .000) weakens with negative announcement CARs. We further explore this interaction by calculating and comparing predicted values of strategic topic novelty under circumstances of predecessor dismissal and routine succession when the capital market reaction is at its mean relative to when the capital market reaction is strongly negative (+2SD). The associated plot of the marginal effects is shown in Figure 1. Whereas dismissals vis-à-vis routine successions are associated with an increase in strategic topic novelty of 19 percent ((0.163–0.137) / 0.137) when the negative market reaction is at its mean, they are associated with a decrease in strategic topic novelty (i.e., more continuity) of 5 percent ((0.133–0.140) / 0.140) when the reaction to the new CEO appointment is strongly negative. Thus, H3 is also supported. 14

Succession Type × Negative Announcement CARs on Strategic Topic Novelty (H3)

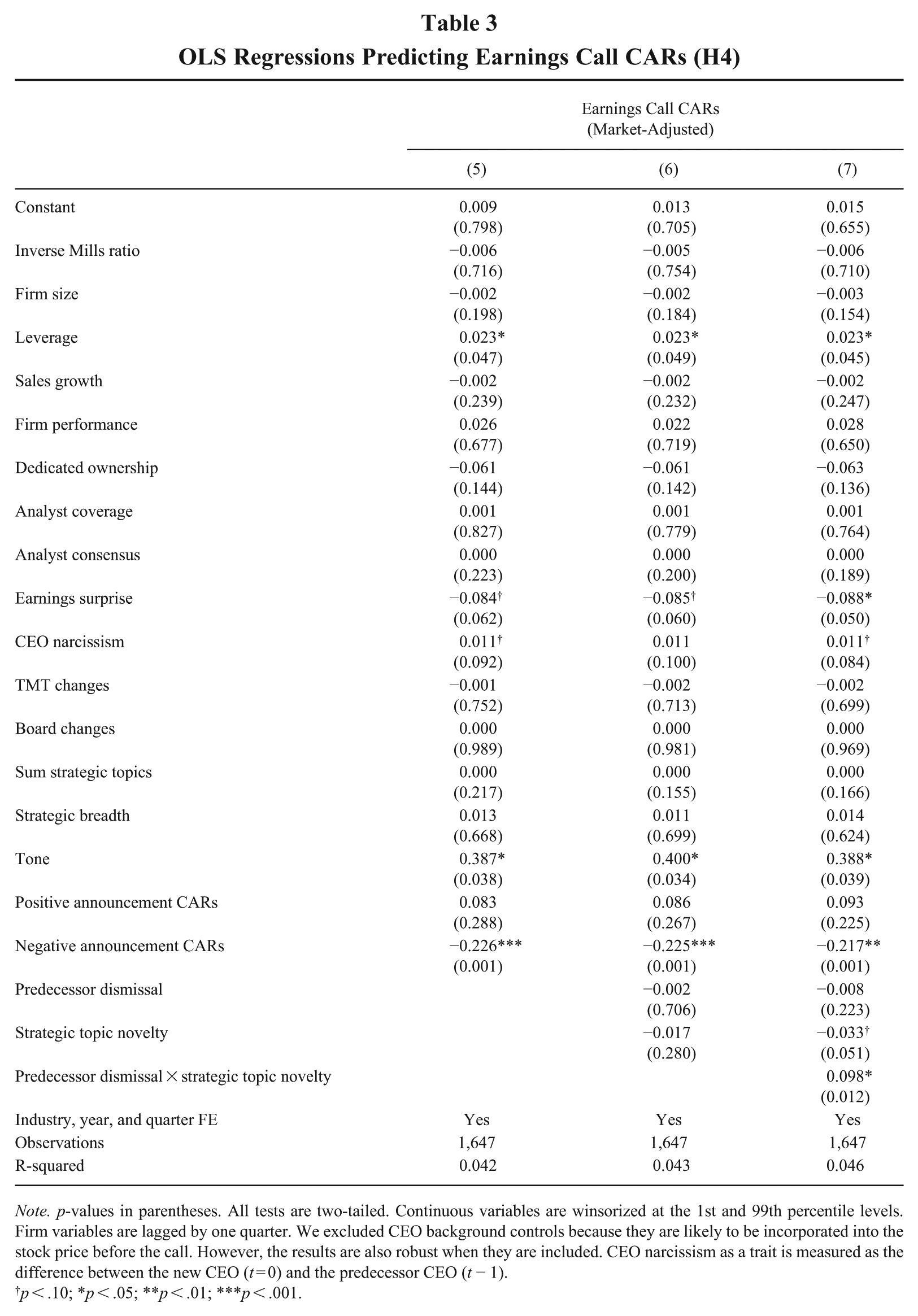

Table 3 presents results of the models testing H4, where we predict CARs following the new CEO’s first earnings call. Consistent with our expectation that the capital market will react more favorably to strategic communication that aligns with the succession context, we find a positive and significant coefficient for the interaction between predecessor dismissal and strategic topic novelty in Model 7 (β = 0.098, p = .012). Marginal effects analysis and the interaction plot in Figure 2 imply that the capital market reacts positively to new CEOs whose strategic priorities are more distinct from those of a dismissed predecessor and negatively to those who express less strategic topic novelty compared to a dismissed predecessor. In the case of predecessor dismissal, the predicted value of earnings call CARs is −0.014 at low values (−1 SD) of strategic topic novelty and 0.003 at high values (+1 SD) of strategic topic novelty. This corresponds to an increase in earnings call CARs of 1.7 percentage points (0.003–(−0.014)). Given the average market value of $10.36 billion in our sample, this implies an increase of approximately $176 million in market capitalization (0.017 × $10.36 billion), suggesting that variation in strategic topic novelty is associated with economically meaningful differences in market reactions following a dismissal.

OLS Regressions Predicting Earnings Call CARs (H4)

Note. p-values in parentheses. All tests are two-tailed. Continuous variables are winsorized at the 1st and 99th percentile levels. Firm variables are lagged by one quarter. We excluded CEO background controls because they are likely to be incorporated into the stock price before the call. However, the results are also robust when they are included. CEO narcissism as a trait is measured as the difference between the new CEO (t = 0) and the predecessor CEO (t − 1).

p < .10; *p < .05; **p < .01; ***p < .001.

Succession Type × Strategic Topic Novelty on Earnings Call CARs (H4)

For routine successions, the plot illustrates that the effect of strategic topic novelty reverses and is negatively associated with market reactions. That is, increasing from low to high values of strategic topic novelty in the case of routine successions is associated with a decrease in earnings call CARs of 0.84 percentage points ((−0.006)–0.0024). Given the average market value in our sample, this is equivalent to a reduction of roughly $87 million in market value (0.0084 × $10.36 billion). This pattern is consistent with the idea that the capital market will generally expect a greater degree of continuity in new CEOs’ strategic priorities relative to those of their predecessors in the case of successions. Overall, these findings support our prediction in H4 that the capital market responds more favorably to strategic communication aligned with the succession context, while it reacts more negatively to inconsistent cues between the new CEO’s strategic communication and the company’s strategic needs.

Endogeneity

We performed additional analyses to help alleviate potential endogeneity concerns. One concern is that new CEOs may be selected based on their paradigms and succession context. This might occur if individual-level differences for which the CEO was selected drive the relationship between the predecessor’s departure type and the degree of strategic topic novelty. Controlling for the difference in new and predecessor CEOs’ levels of narcissism accounts for this to an extent. Narcissism has been found to affect both strategic boldness and how new CEOs engage with external audiences (Hambrick & Chatterjee, 2007), meaning that boards may select CEOs whose traits fit the firm’s strategic needs in a given succession context. However, other individual-level differences between new CEOs and their predecessors may also influence these relationships. To address this potential source of endogeneity, we conducted supplemental tests controlling for additional individual-level differences, including demographic characteristics (e.g., age and gender) and personality traits (e.g., Big Five profiles). 15 The results are consistent with our primary findings, increasing confidence that our results are not driven by CEO-predecessor differences (see Online Appendix A, Tables A7 and A8).

We additionally estimated a treatment-effect model to account for potential nonrandom assignment into dismissal versus routine successions, following Lennox, Francis, and Wang (2012). This approach models the likelihood of dismissal and assesses whether our findings persist after accounting for systematic differences in treatment assignment. In the first stage, we predicted predecessor CEO dismissal using a probit model. Lagged board independence is included in the first stage as a theoretically motivated determinant of dismissal likelihood (e.g., Boeker, 1992; Hilger et al., 2013) but is not theoretically linked to the successor’s strategic communication. Empirically, board independence significantly predicts dismissal (see Online Appendix D, Table D2) but is not associated with strategic topic novelty in the main regression. In the second stage, we reestimated our main models, including the treatment correction term derived from the first-stage probit. The results remain robust (see Tables D3 and D4).

As a more general test of potential omitted variable bias, we further applied the approach by Oster (2019). This approach assesses coefficient stability and R-squared movements to quantify how strong the effects of unobserved variables would have to be to invalidate our main results (e.g., Oster, 2019). Detailed results of these tests are presented in Online Appendix D, Table D5. Comparing controlled and uncontrolled regressions for our three statistically significant findings, we find relatively small movements in coefficients accompanied by large R-squared movements. The bias-adjusted coefficients are also similar to the estimated coefficients with control variables. The analysis indicates that unobserved variables would need to be substantially more influential than observed variables for the treatment effects to be zero. Unobserved variables would have to be approximately 30 times, 14 times, and 57 times as important as observed variables for the effects associated with H1, H3, and H4 to be reduced to zero. Overall, these tests indicate that our findings are unlikely to be the result of omitted variable bias. 16

Supplemental Tests

We conducted additional analyses to validate our assumptions and generate further insights.

Analyses of new CEOs’ earnings calls

We performed detailed quantitative and qualitative analyses of new CEOs’ earnings calls to substantiate our claim that they tend to avoid publicly opposing their predecessor (see Online Appendix E, Table E1 and Figure E1). Our analyses revealed that only about 20% (322 out of 1,647 successions) of new CEOs in our sample explicitly mentioned their predecessor in the first earnings call. Of the 322 cases where they did mention the predecessor, a sentiment analysis revealed that, on average, new CEOs speak more positively about their predecessor than in the rest of the call and that sampled CEOs used more negative than positive words in only 15 cases, which were mostly driven by factual reporting rather than opposition or overt criticism. Ultimately, new CEOs in our sample directly criticized or opposed their predecessor in only two out of the total 1,647 cases (or about 0.1%). Table E2 in the Online Appendix E also provides 50 illustrative examples in which the new CEO mentions the predecessor; examples 49 and 50 present the two cases in which the predecessor is opposed.

Analysis of strategic intent

We provide further evidence of the strategic intent behind strategic topic novelty in the Online Appendix F, Tables F1 and F2, which present correlations between the strategic topics emphasized by new CEOs and subsequent strategic actions. Results show clear and systematic relationships between communicated topics and future actions. For example, emphasis on M&A and scope is positively associated with subsequent M&A activity and divestitures, emphasis on product innovation is associated with increased R&D spending, and emphasis on social strategies is associated with higher CSR performance. These and other relationships presented in the table give us confidence that strategic topic novelty is more than mere impression management.

Post-hoc qualitative insights

To further enrich our understanding of new CEOs’ early strategic communication, we conducted interviews to complement our quantitative analysis with qualitative insights. Interviewees included two current CEOs. “CEO 1” is a 55-year-old male leading a listed mining firm with approximately €4 billion in annual revenue. “CEO 2” is a 49-year-old male leading a listed logistics firm with more than €80 billion in annual revenue. Each CEO was asked four structured questions (provided in Online Appendix G) about their initial communications with the capital market and the role of their predecessor’s legacy.

Across both interviews, a recurring theme was the deliberate use of strategic communication to establish a personal mark on the organization while maintaining respect for the predecessor’s legacy. As CEO 1 put it, “Leadership is a relay, not a solo race . . . I treated my predecessor’s tenure with respect . . . then I shifted the conversation to the future, where investors really want my energy and conviction to be.” CEO 2 echoed this sentiment: “Public criticism of a predecessor is generally counterproductive: it signals instability, risks alienating employees and board members who supported prior decisions [ . . . ].” He continued, “The unwritten rule is to respect the past while positioning yourself as capable of making the changes the future requires.” These reflections align with our conceptualization of strategic topic novelty as the primary way new CEOs differentiate themselves without challenging their predecessors’ strategic choices head-on.

The interviews also underscore that early strategic communication is closely tied to credibility concerns, reinforcing our view that strategic topic novelty is not merely symbolic. Both CEOs emphasized that credibility with investors constrains what can be communicated early on. As CEO 1 explained, “I share only those priorities I fully intend to pursue, because I know the cost of overpromising.” CEO 2 similarly stressed, “Credibility is everything: if you overpromise and underdeliver early, it’s very hard to recover trust.”

Finally, the interviews also illustrate how CEOs calibrate the degree of novelty they communicate based on how they interpret the succession context. When a succession occurred following a period of positive performance, it was important to them to “make clear where I intended to focus future growth”; however, their approach in this case was not to deviate from the legacy of the predecessor but to “acknowledge the company’s strong foundation” and “[highlight] the momentum we would build upon” (CEO 2). In contrast, when there were known challenges associated with the predecessor’s tenure, CEOs described signaling greater scope for change—while still avoiding overt criticism—by pivoting more decisively toward new priorities and future-oriented themes. As CEO 1 noted: “Organizations thrive on stability, not finger-pointing . . . In private, with the board or my team, I will be candid about what needs to change. But in public, the focus is on progress, not blame.” CEO 2 echoed these ideas, describing his approach when there were “known challenges” during the predecessor’s tenure: The market reacts poorly to uncertainty or unnecessary drama, so I avoided dwelling on shortcomings. Instead, I framed my predecessor’s tenure as part of the company’s ongoing journey. I thanked them for their contributions, emphasized stability in core areas, and then pivoted quickly to my own priorities and vision.

Together, the qualitative insights illustrate how CEOs consciously navigate legitimacy and credibility concerns, complementing the patterns we have identified in our qualitative analyses.

Discussion

The primary objective of this study was to extend theory on new CEOs’ strategic communication by developing a model of sensemaking and sensegiving with the capital market. We examined how new CEOs navigate the dual imperatives of establishing a unique strategic vision while simultaneously expressing their strategic priorities in ways that legitimize their appointment and manage investors’ perceptions. At the core of our theorizing, we conceptualized new CEOs’ communication of more or less novel strategic topics as a sensegiving activity shaped by their sensemaking of key contextual cues surrounding the succession: the nature of the succession and the capital market’s initial reaction to their appointment.

Our findings highlight that dismissals serve as a critical driver of strategic topic novelty, as new CEOs communicate significantly higher levels of novelty following a dismissal compared to a routine succession. We also find that negative market reactions seem to complicate new CEOs’ interpretation of the succession context, leading new CEOs to communicate less strategic topic novelty following a dismissal but more strategic topic novelty following a routine succession. Interestingly, we do not find a statistically significant effect for positive capital market reactions. However, this nonfinding may not be surprising when considering psychological research showing that negative feedback weighs more heavily on the human psyche (Ito et al., 1998; Kahneman & Tversky, 1979). In the context of the present study, negative feedback appears to engender maladaptive responses, as it weakens the alignment between the succession type and the degree of novelty reflected in new CEOs’ strategic communication of their priorities. Yet, as we argue and show with our last finding, the market typically reacts more favorably to strategic communication that aligns with the succession context, and these reactions feed back into CEOs’ evolving interpretations and subsequent strategic actions.

Contributions to Theory and Research

Our study offers several contributions to the literature on strategic communication. First, we emphasize the pivotal role of sensemaking as a precursor to sensegiving in the strategic communication process, particularly for new CEOs. By integrating insights from the sensemaking and sensegiving literature with research on CEO communication, we demonstrate how new CEOs first interpret their environment before conveying their strategic priorities to the capital market. We illuminate the situational cues that influence new CEOs’ interpretations and shape their communication, particularly in terms of the novelty of the strategic topics they emphasize to the capital market. In doing so, we also extend prior research and practical insights related to how new CEOs approach their new role (e.g., Hambrick & Fukutomi, 1991; Porter et al., 2004; Whittington et al., 2016). Whereas others have suggested that new CEOs often seek to leave their mark on the organization early in their tenure, ours is the first study of which we are aware to directly consider the novelty of the priorities new CEOs emphasize when first communicating with the capital market. We also show that, when considered alongside the nature of the succession, the degree of novelty reflected in a new CEO’s communicated priorities is critical to the capital market’s assessments. Collectively, our theory and findings underscore the dynamic process of sensemaking and sensegiving between new CEOs and the capital market in shaping the firm’s narrative.

Second, we contribute to a deeper understanding of how capital market feedback influences new CEOs’ strategic communication. Our findings highlight an asymmetry in how new CEOs respond to positive and negative market reactions. Whereas negative reactions appear to create interpretive challenges for new CEOs regarding their approach to strategic topic novelty, positive reactions do not simplify interpretations in the same way. This asymmetry aligns with concepts from social psychology and behavioral economics, such as negativity bias (Rozin & Royzman, 2001) and loss aversion in prospect theory (Kahneman & Tversky, 1979). Negative feedback seems to carry greater psychological salience and uncertainty, signaling potential risks or doubts about the CEO’s effectiveness (Rozin & Royzman, 2001; Swann & Buhrmester, 2012). In contrast, while positive feedback might generally increase individuals’ self-efficacy, it does not demand the same level of cognitive effort or contextual reinterpretation, making it less impactful for strategic communication. As a result, negative feedback has a disproportionately strong psychological impact in our setting, driving CEOs to reassess their strategic communication more thoroughly than they would in response to positive feedback. Our study, therefore, underscores how negative external feedback can complicate new CEOs’ sensemaking processes, potentially reducing their ability to effectively articulate their strategic priorities (e.g., Keil et al., 2022).

Third, our investigation of new CEOs’ strategic topic novelty during their first earnings call offers a fresh perspective for the CEO succession literature. Prior research has predominantly focused on market reactions to new CEOs as singular events, emphasizing the antecedents and determinants of succession (Gligor et al., 2021; Shen & Cannella, 2002b). Our study brings attention to the strategic communication choices CEOs make in the early stages of their tenure (Berns & Klarner, 2017; Hilger et al., 2013). Moreover, while prior research has shown that new CEOs face heightened uncertainty and the risk of early dismissal (e.g., Martin & Combs, 2011), we know relatively little about how new CEOs navigate this uncertainty. Our theory and findings begin to address this question. They show that new CEOs tend to align their strategic topic novelty with the succession context but are also cautious about presenting overly unique visions in response to negative capital market feedback. This suggests that new CEOs are acutely aware of the capital market’s potential influence (perhaps to a fault) and take it into account from their first day, recognizing that they are unlikely to be granted any leniency.