Abstract

This article proposes a network signalling theory approach to analyse small firm internationalisation in the digital economy. We use a data set of 4446 small- and medium-sized firms extracted from Funderbeam and logit regression models to test five hypotheses about internationalisation. Exploring a firm’s digital presence indicates that the number of social media followers is a better indicator of internationalisation than website traffic, highlighting the importance of engagement signals in the digital space. Investment signals such as the time and size of funding are also positively related to internationalisation but surprisingly, not the number of investors, suggesting that more focused investment strategies work better in the international context. To complement our international network signalling approach, controlling for firm factors such as age and size and environmental factors such as competition and industry provides a more detailed analysis. Our contribution lies in extending signalling theory in the context of international networks using a novel and extensive data set.

Introduction

Conceptualising entrepreneurship and internationalisation signals requires a closer analysis of digital network opportunities and multilateral relationships with investors. Networks have become increasingly important for the process of internationalisation (Prashantham et al., 2019) as potentially, they accelerate internationalisation and expansion processes by providing resource access (Tang, 2011) and reduce the liability of foreignness (Johanson and Vahlne, 2009). The importance of networks for internationalisation is also related to performance outcomes (Stoian et al., 2017) or the speed of internationalisation (Li et al., 2015). Clearly, international networks are complex. As such, international investors have to rely upon both public and private information signals that differ across industries and countries, to adjust their decisions and plan asset payoffs (Brennan et al., 2005). Thus, digital platforms, such as Funderbeam from which the data for this study are drawn, now have an important role in such network signal exchanges in international business and consequently, require further examination.

Information asymmetry and signalling are common problems between entrepreneurs and investors; therefore, studying them in the changing context of digital presence and international networks is important. Traditionally, signalling between ventures and investors has been undertaken through dividends (Asquith and Mullins, 1986; John and Williams, 1985) and more recently, through the reputation of top management structures (Certo, 2003; Cohen and Dean, 2005) or strategic affiliations with partners (Plummer et al., 2016). Signalling theory aims to explain this problem of entrepreneur–investor information asymmetry (Connelly et al., 2011) but the focus has typically been upon interorganisational relationships. Research on crowdfunding expands signalling to a broader context, suggesting a combination of signals from the start-ups and backer endorsement signals for successful funding (Courtney et al., 2017) related to social capital and identity links between entrepreneurs and backers (Kromidha and Robson, 2016). Whether perceived value depends on the firm’s management and investment signals (Cohen and Dean, 2005) or it is created through relationships and interactions in a network environment (Freiburg and Grichnik, 2012), remains an ongoing debate. Digital network technologies have not only improved signalling opportunities, but also increase the complexity of signalling decisions (Reuber and Fischer, 2009), especially in a broad international context. They may accelerate internationalisation and expansion processes by providing resource access (Tang, 2011) and reduce the liability of foreignness (Johanson and Vahlne, 2009). The importance of networks for internationalisation is also related to performance outcomes (Stoian et al., 2017) or the speed of internationalisation (Li et al., 2015).

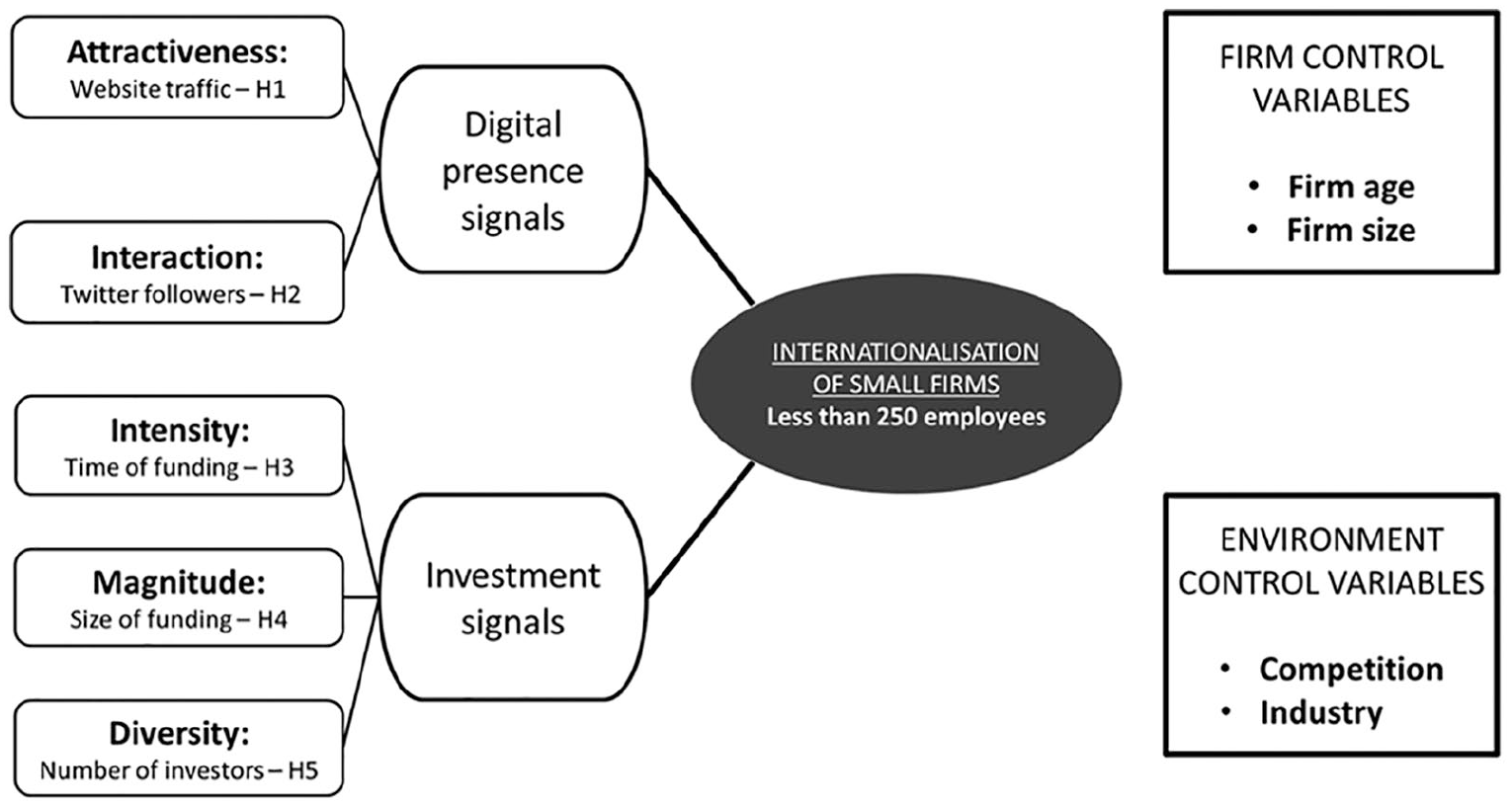

Managing international activity and presence signals at the same time is challenging. In this article, we draw upon signalling theory (Connelly et al., 2011) applying it to international networks facilitated by digital means to advance current knowledge. Signalling theory has traditionally been used to explain dual entrepreneur–investor information asymmetry and relationships. Understanding network signals in terms of digital presence and investment positioning, as opposed to network exchanges, is proposed to address the research gap in the context of digital entrepreneurship networks and internationalisation. Rather than challenging these assumptions, we identify and address a conceptual gap by exploring the following research question: How can digital presence and network investment signals explain the internationalisation of small firms?

This article offers three contributions. First, we use and extend the scope of signalling theory in the international network environment of the digital economy. Second, our work suggests a set of measures to apply signalling theory in this broader international context of small firms, their digital presence and investment signals. Third, for international investment researchers, practitioners and policymakers, our article contributes to a better understanding of digital global networks for internationalisation. Such contributions are informed by empirical evidence from Funderbeam.com, a digital international network platform for firms and investors.

We commence with a theoretical discussion of signalling theory beyond bilateral entrepreneur–investor relationships exploring digital presence and investment signals for the internationalisation of small firms in a network environment. The ‘Methodology and data collection’ section outlines the methods used in this study; the ‘Results’ and ‘Discussion’ sections draw attention towards the symbiotic nature of a digital presence and investment signals in the digital network space for internationalisation where firm identity, performance and relationships need to be carefully managed.

Digital changes in internationalisation processes

Conceptualising internationalisation signals and networks requires an analysis of digital network opportunities and multilateral relationships with investors. In international online markets, firm reputation and position signals are important (Reuber and Fischer, 2009); yet, for individual firms and business groups, using their reputation signals as a critical success factor might not be tenable in a broader international context (Mukherjee et al., 2018). As a consequence, managing international activity, digital presence signals and investment signals at the same time is challenging for new firms. A better understanding of firm digital presence and investment signals in an international network context is required to learn about digital entrepreneurship (Nambisan, 2017) and internationalisation (Monaghan et al., 2020; Ojala et al., 2018) by exploring how digital artefacts influence internationalisation.

Traditional theories of firm internationalisation focus upon the incremental increase of commitment to foreign markets by using the gradual acquisition, integration and use of knowledge about such markets and operations (Johanson and Vahlne, 1977). This perspective is based on the assumption that firms prefer foreign markets with some degree of similarity to their own domestic market to reduce risk (O’Farrell et al., 1996). Due to critical reviews (Forsgren, 2002; Petersen, 1996), this model shifted its focus from internalisation to coordination of networks (Vahlne and Johanson, 2013). Access to multiple geographic networks and entrepreneurial orientation is positively related to internationalisation prospects of small firms (Felzensztein et al., 2015). Besides resources, access to international networks also helps firms to improve capabilities and knowledge (Casillas et al., 2009). Networking capability and experiential learning combined with entrepreneurial orientation leads to superior international performance (Karami and Tang, 2019), but our knowledge of how this happens, and more specifically, the role of signals between stakeholders in international networks is limited.

Digital developments and international entrepreneurship are increasingly related to ibusiness platforms (Brouthers et al., 2016; Chen et al., 2019). Monaghan et al. (2020) explain that born digital firms thrive internationally through stakeholder engagement, automation, networking, flexibility and scalability. Ibusiness platforms, however, refer to digital networks for users to interact and co-create as they expand internationally (Brouthers et al., 2016). Drawing on social network theory, Chen et al. (2019) suggest that internationalisation in ibusiness models depends on the user’s collective interactions rather than the firm’s market commitment. We know that information, knowledge and collaboration are closely associated with the internationalisation of small firms (Costa et al., 2016). This has a general application as focusing only on born globals and ibusinesses leaves many others with some degree of digital presence, investor relationships and international prospects in this shadow.

Digital platform providers, and how they enable the global expansion of businesses, have attracted considerable attention (Ojala et al., 2018). Entrepreneurial ecosystems have changed as a result of digital affordances, business model innovations, knowledge spill-overs and external relationships (Autio et al., 2018). Yet, despite clear evidence that digital capabilities spur growth, according to the Federation of Small Businesses (FSB) in the United Kingdom, 26% of businesses lack confidence in their digital skills and 25% of businesses do not consider them important (FSB, 2017). Clearly, digital technologies have an important role in the life of firms, their operations and interaction with the environment including internationalisation. What deserves more attention is the content that flows in the form of digital presence signals and investment signals.

A signalling theory perspective in digital entrepreneurship (Giones and Miralles, 2015) suggests that entrepreneurs use market, technology and social capital signalling to mitigate uncertainty and grow. This means that in international networks, digital platforms have an important role, but we need to look beyond firm technological affordances and use. Evidence from born globals (Monaghan et al., 2020) or the ibusiness platforms (Brouthers et al., 2016) show how digital technologies can help international expansion, but we need to acknowledge that not all firms are fully digital. Various degrees of digitalisation need to be considered, along other aspects of internationalisation such as firm age, size, competition and industry. This article advances this argument and signalling theory for the digital entrepreneurship global ecosystem by exploring digital presence and investment signals for internationalisation by controlling for firm size, age and industry.

Theoretical perspective and hypotheses

A digital network signalling theory perspective for internationalisation

Signalling theory analyses the dynamics of information asymmetry between two parties (Spence, 2002). Originally, the theory was applied to job markets or how CEOs can re-establish trust and leadership (Spence, 1973). More recently, this theory has expended to explain cross-organisational relationships at the intersection of international management (Taj, 2016), economics (Bandyopadhyay et al., 2018), marketing (Taoketao et al., 2018) and entrepreneurial crowdfunding finance (Kromidha and Robson, 2016). In the typical investment relationship, entrepreneurs possess inside information they need to communicate to attract investors (Connelly et al., 2011). Bergh et al. (2014) argue that the primary predictive mechanism of the theory is to draw attention to the signals sent and received to reduce information asymmetry. These can be information about founders, the performance of the firm, key assets or requests from investors to reveal similar information. In research and strategic decision-making, signals have been used for valuation purposes in the case of initial public offerings (Park et al., 2016) or venture capital (VC) deals (Busenitz et al., 2005). In these cases, signalling theory focuses upon how organisations interact with each other. Yet, even in the case of ibusiness platforms, internationalisation in or through digital networks remains challenging due to greater liabilities of outsidership (Brouthers et al., 2016).

The application of signalling theory to explain internationalisation network processes is limited. We know that the foreign ownership of firms sends equity structure signals that lower the cost of borrowing (Chen et al., 2014). At this macro level, a panel analysis of 54 countries suggests that institutional signals on business regulations condition entrepreneurial activity (Levie and Autio, 2011). On a micro level, legitimacy and social capital signals that facilitate business relationships between investors and entrepreneurs have been identified in the context of women entrepreneurs (Murphy et al., 2007) and crowdfunding (Kromidha and Robson, 2016). Similarly, in digital network platforms such as Kiva.org that link international funders and projects, microfinancing narrative signals have an important role in successful financing (Moss et al., 2015). Signalling theory establishes a link between the social and economic environment by explaining communication strategies used to mitigate risk, establish trust and overcome barriers. We draw upon signalling theory to analyse international network relationships among entrepreneurs and investors following advice to look more carefully at the links rather than the actors (Thomas et al., 2011). Our focus is upon digital presence and investment signals; thus, the nature of communications in the digital network space and the multidimensional nature of an investment network add a novel dimension. Both digital presence and investment signals can be considered intangible assets related to firm identity, brand image, marketing and relationships with stakeholders. In the digital economy, many of these intangible assets exist, are developed or shared in digital network spaces such as digital social media platforms through which companies can reach out towards many stakeholders. Compared to 124 firms in 2013, by 2018, 191 in the S&P 500 have below-zero net tangible book values (Gandel, 2018), confirming the importance of intangible asset. Hence, the value of using signalling theory (Connelly et al., 2011) to analyse how firms use their digital presence and investment signals as the two underpinning constructs to inform this study.

Since most firms have digital presence, this can be related to investment signals in the international network space. This is noted in research on online crowdfunding networks where web visibility signals are positively related to successful funding (Bi et al., 2017). We, however, explore how both these factors are related to the internationalisation of firms. Digital presence and investment signals should be considered as complementary, rather than unrelated, as they both have rational signalling elements related to the performance of firms and relational signalling elements related to firm connections (Moss et al., 2015). Accordingly, we structure our study around a digital presence and investment signals for our independent variables, while we control for firm and environment variations, as shown in Figure 1. We know that managing information asymmetry and a strong signalling environment between the firm and its stakeholders are important (Taj, 2016). What remains largely unexplored, but increasingly important, is the role of signals related to firm attractiveness and interactions for internationalisation, tested by H1 and H2 (see below).

A network signalling theory framework of internationalisation.

Investment signals are key determinants for initial public offerings (Reuer et al., 2012), so deserve more attention in the context of international networks. The new venture creation process depends not only on the appropriate resources, but also on exchanges between the entrepreneur and their networks (Hung, 2006); signals of value, commitment and competence towards potential investors are important for early-stage firms seeking finance (Busenitz et al., 2005). To explore the role of investment signals in international networks, we acknowledge not only the signals regarding the number of investors for each firm in the international network, but also signals related to the magnitude and intensity of funding received (see H3, H4 and H5).

Digital presence signals and hypotheses

Attractiveness: website traffic

A digital presence is related to marketing opportunities (Alford and Page, 2015), but a lack of knowledge and the inability to measure its return on investment are constraining (Kim et al., 2013). The network signalling theory approach can be useful in this respect since a network-centric view of entrepreneurship in digital platforms acknowledges that success is related to links and coordination (Srinivasan and Venkatraman, 2018). Website traffic is a key measure used by many online tools such as Google Analytics, Spring Metrics, Woopra, Clicky, Mint and so on helping any website owner to track and analyse traffic data (Ibeh et al., 2005; Meyerson, 2015) analysing e-branding of Internet companies argue that a significant proportion perceived web visibility to be important for differentiation, improving value, increasing customer loyalty and assisting long-term survival and success. Clearly, website analytics are an important measure of digital presence and entrepreneurial success that sends important signals to firm stakeholders globally. Yet, we have relatively little evidence regarding their efficacy; thus, we develop the following hypothesis:

Hypothesis 1 (H1): The higher the website traffic, the higher the internationalisation prospects of a firm.

Interaction: online followers

Online social capital interactions in digital networks can enable entrepreneurs to make better use of opportunities in the digital economy (Smith et al., 2017). In addition to economic capital, in traditional settings, social capital has played an important role in entrepreneurial networks and growth (Anderson et al., 2010; Anderson and Jack, 2002; Baron and Markman, 2003). This can explain the importance of social capital interactions in international networks. De Carolis and Saparito (2006) and De Carolis et al. (2009) draw from social cognitive theory (Augoustinos et al., 2014; Bandura, 1986; Fiske and Taylor, 2013) to explain entrepreneurial behaviour as a result of social networks and cognitive biases. Social capital signals in this context can be linked to trust and firm performance, especially in times of crisis (Lins et al., 2017). Fischer and Reuber (2011) suggest that Twitter-based interaction can increase familiarity between entrepreneurial firms and their networks, but they can also cause confusion. Community orientation and community norm adherence are the two dynamic capabilities proposed for managing the consequences of social interaction through Twitter (Fischer and Reuber, 2011). This informs the following hypothesis:

Hypothesis 2 (H2): The higher the number of online followers, the higher the internationalisation prospects of a firm.

Investment signals and hypotheses

Intensity: funding time

Entrepreneurial growth is commonly constrained by internal finance (Carpenter and Petersen, 2002). Traditionally, firms had to build on their internal capabilities to access sources of finance from banks or venture capitalists to improve their performance and accelerate growth (Lee et al., 2001). However, new players such as crowdfunding, peer-to-peer lending, accelerators and family offices are transforming the entrepreneurial finance landscape in the digital economy relying on the value of network access (Block et al., 2018). Technology, entrepreneurial global vision, foreign market knowledge and network ties seem to accelerate internationalisation (Langseth et al., 2016). For international investors, portfolio flows are strongly influenced by past returns from foreign markets (Froot et al., 2001). It has been argued that many international investors are risk averse, especially when investing in emerging economies (Lizarazo, 2013). This could influence the speed of their investment decisions; we explore this through the following hypothesis (where funding time is the time between the last two funding rounds):

Hypothesis 3 (H3): The lower the funding time, the higher the internationalisation prospects of a firm.

Magnitude: size of funding

In the context of digital crowdfunding, the size of early contributions combined with social capital influence successful financing (Colombo et al., 2015). This indicates the importance of funding size signals in a network environment. The herding behaviour, whereby the size of funding influences others to invest, is acknowledged in the case of mutual funds (Wermers, 1999) or peer-to-peer funding networks (Herzenstein et al., 2011). What these studies do not consider in detail however, is the relationship to internationalisation. Lockett et al. (2008) discuss the resources and routes to internationalisation but it is clear that there is a lack of consensus on the contributions of investors other than the provision of finance for equity. We build upon Lockett et al.’s (2008) study which analysed VC finance in the context of exporting propensity and exporting intensity; they focused upon the following two investment stages: early-stage seed start-up and late-stage management buy outs and management buy ins (MBO/I). In this study, we have access to signals about VC and non-VC finance stages, so we are able to build a hypothesis pertaining to these different stages of funding, their magnitude signals and internationalisation.

Hypothesis 4 (H4): The larger the size of funding, the higher the internationalisation prospects of a firm.

Diversity: number of investors

Signalling theory has been traditionally focused on the signals investors share with entrepreneurs (Connelly et al., 2011), but has not considered the number of investors as a signal in itself because in bilateral relationships, that would have been irrelevant. However, in an international network of entrepreneurs and investors, we theorise that the number of investors becomes an important signal. Supporting arguments for this addition to signalling theory are provided by Coviello (2006) explaining that the growth and internationalisation of new ventures is positively related to the size of their networks. It has been noted that investors are influenced by other investors in a so-called ‘herding effect’; this has been illustrated in the case of institutional investors (Nofsinger and Sias, 1999), information-based trading (Zhou and Lai, 2009) or online social trading (Kromidha and Li, 2019). In addition, since stock returns are influenced by diversification choices of investors (Kumar, 2007), more investors could mean more diversified risk signals. However, there is some debate and evidence that a limited number of investors could be beneficial to avoid the information disparity problem related to raising capital (Varma, 2001). These studies do not consider the internationalisation aspects of the firms, but we found some inconclusive evidence of investors ‘herd following’ to international markets (Chen, 2013). To gain a better understanding of the relationship between number of investors as a network signal, and internationalisation, we propose the following hypothesis:

Hypothesis 5 (H5): The higher the number of investors, the higher the internationalisation prospects of a firm.

Setting context: Funderbeam.com – A digital international network of firms

Funderbeam.com is an online database and network of businesses and investors that can be considered as ibusiness (Brouthers et al., 2016; Chen et al., 2019). At the time of the study, it contained 138,851 company profiles, 25,418 investor profiles, US$524.81 billion of disclosed funding and was running 152,304 daily updates (Funderbeam, 2017a). The platform started in 2013 in Tallin, Estonia, its current headquarters is in London and it has offices in Singapore, Copenhagen and Zagreb (Funderbeam, 2020). It began as a database of start-ups, established ventures, competitors and investors, but has evolved into a network for raising funds, investment and trading. Organisational members of the network and the general public can use Funderbeam to discover, track and analyse firms and market opportunities for investment. Users can track firms of their choice, review the competitive landscape, benefit from estimates of firm valuations from big data machine learning algorithms, or ask for custom support and performance benchmarking (Funderbeam, 2017b). What Funderbeam does can be referred to as social stock exchanges (Wendt, 2017) or impact investing (Laul and Wendt, 2017), aiming to provide more democratic capital investment opportunities through an online, open and transparent digital networking platform. The manner in which Funderbeam attempts to enable informed decisions, based on shared business and social capital information in the network, captured our attention. In September 2015, we received detailed records about the most recently funded firms. From the 4446 small- and medium-sized enterprises (SMEs) analysed, we found that 9% of the firms were international new ventures operating in at least two different countries and were less than six years old. This is consistent with earlier studies (Brush, 1995; Zahra et al., 2000) that also limit the age of new ventures to six years.

Methodology and data collection

Data sample

Detailed records of the 6000 most recently funded companies shown in Funderbeam were received through collaboration with one of the platform managers. Eliminating large firms, as well as missing values for the variables to be included in our models, resulted in 4446 usable firms. There were no statistically significant differences at the 5% level or better by industry and location when we compared the usable and the full data sets of firms. We utilise data on 4446 SMEs extracted from Funderbeam. These data were provided upon request by Funderbeam itself who have permission to share it with third parties. From the group, 9% of the firms were identified as international firms operating in more than one country in the past six years, covering 58 different countries. Most fall into the category of geographically focused start-ups according to the classification of international new ventures proposed by Baum et al. (2011) because they have offices rather than simply export to one or a few countries. Large-sized firms are excluded from our sample and we focus upon firms with less than 250 employees. These data are cross-sectional and from one point in time and this limitation needs to be acknowledged and as with other studies of firms it is necessary to treat the results carefully.

Firm control variables: age and size

Research on the relationship between firm age and internationalisation prospects shows complex results. Some studies indicate that firm age is positively correlated with international activity (De Noni and Apa, 2015; McDougall and Oviatt, 1996), and some indicate the opposite (Love et al., 2016). Internationalisation presents a ‘shock’ that requires a degree of flexibility that younger smaller firms possess more compared to older, larger firms where organisational rigidities have become more established (Sapienza et al., 2006). This explains why older and larger firms are more likely to be international, but younger and smaller firms grow faster when they internationalise. Our sample consists of only small- and medium-sized firms, but we control for firm size and age to have a better understanding of digital presence and investment signals for internationalisation.

Environment control variables: competition and industry

A key motivation for new ventures to internationalise is to avoid direct competition with established firms in home markets (McDougall et al., 1994). This motivation to internationalise is often enabled by knowledge and network technology as mediators related to foreign markets (Oviatt and McDougall, 2005). However, competition exists in an international market and understanding it could be a costly process for new ventures (Fernhaber et al., 2007). Therefore, studying controlling for competition signals in the international network context is important.

Competition might vary across different sectors so controlling for industry factors is important to understand the internationalisation of new ventures (Evers et al., 2015). Some of these factors are competition within the industry, structure, life cycle, concentration, knowledge intensity, local clustering and global integration (Andersson et al., 2014). De Jong and Vermeulen (2006) identify significant variations among 1250 small firms across seven industries: manufacturing, construction, wholesale and transport, retail, hotel and catering, knowledge intensive services, and financial services. A study of 57 manufacturing industries across 91 destination countries shows that sectors characterised by larger and more dispersed firm sales are more likely to be international (Pietrovito et al., 2016). To make our findings comparable with extant research, we control the internationalisation of new ventures across seven industries: health care, technology, consumer services, finance, consumer goods, industrials and utilities.

Measures

Dependent variable

In our main regression models, the dependent variable is a dummy variable which is ‘1’ if the firm is an international venture that operates in at least two countries – the country where the headquarters is located plus at least one other country, and ‘0’ otherwise.

Independent and control variables

Age, size and the number of competitors were included as continuous variables in our models. Age is the logarithm of the age of the firms in years. Size is the logarithm of the number of employees. Industry is captured using seven industry dummy variables (Technology, Consumer Services, Finance, Consumer Goods, Industrials, Utilities and Health Care) where the last variable in parentheses is the comparison industry. Website traffic is the logarithm of the cumulative number of website visits on the firm’s page. Online followers are the second independent variable and that is the logarithm of the number of Twitter followers. Funding Time is the number of months between the last two rounds of funding. The size of funding is measured by the last stage of investment in the firms by a series of six dummy variables (Non-VC, Seed-Funding, Round A, Round B; Rounds C, D, E and F; and Round X) where Round X is the comparison variable in the regression models. Investors are the last of the independent variables and that is the number of investors in the firm.

Data analysis

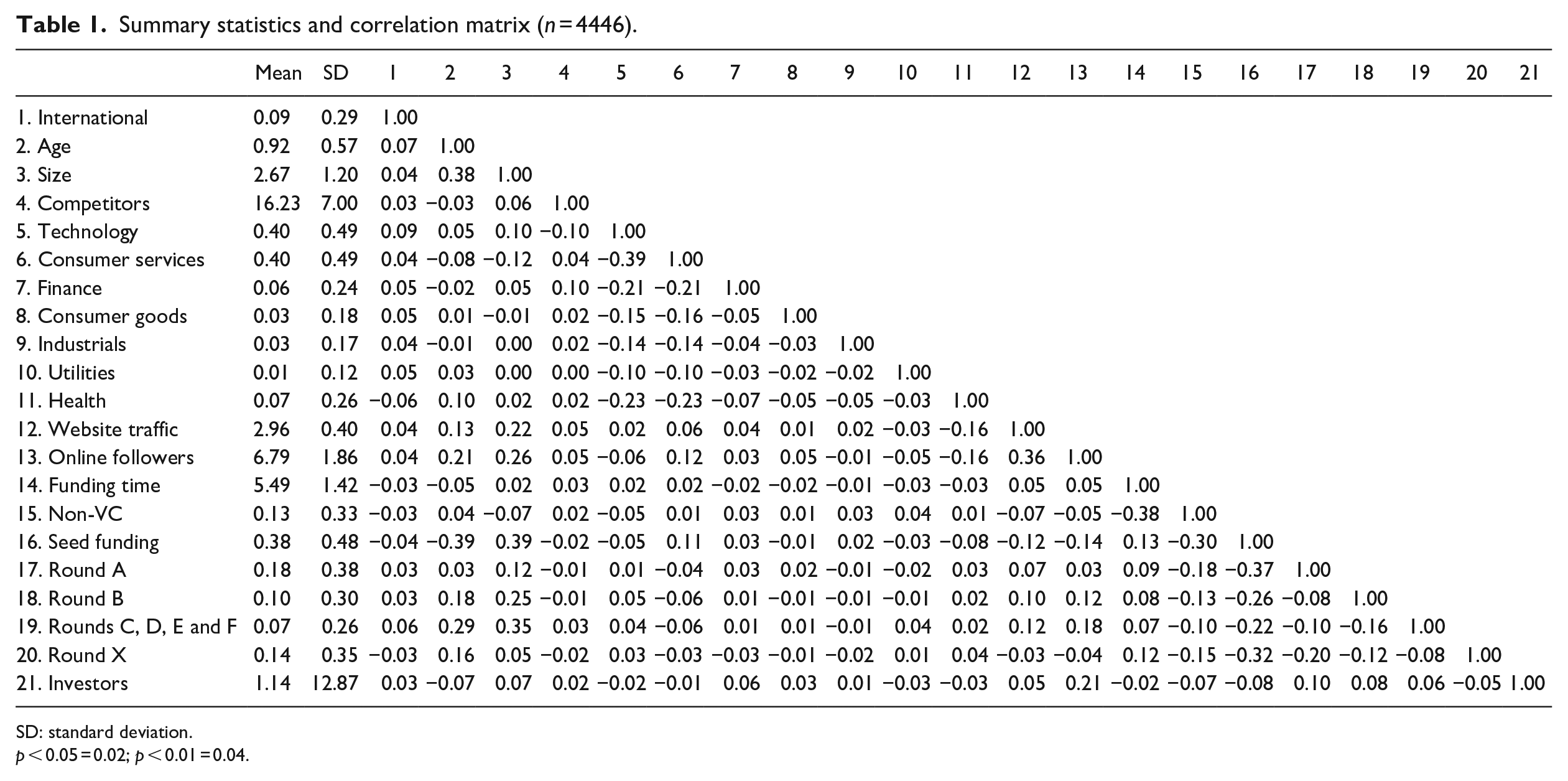

A correlation matrix of the dependent, control and independent variables is presented in Table 1. Summary statistics are also reported in Table 1. None of the correlation coefficients in Table 1 suggest that multicollinearity is a problem. Common methods bias (CMB) was tested using the Harman’s one-factor test (Podsakoff and Organ, 1986) and also the Marker Variable Technique (Jarvenpaa and Majchrzak, 2008; Malhotra et al., 2006; Pavlou et al., 2006). The Harman one-factor test and the Marker Variable Technique found no evidence to suggest that CMB is a problem with the study. Logit regression techniques were used to estimate the models (Greene, 2012) considering the dependent variable has a binary response of international or non-international.

Summary statistics and correlation matrix (n = 4446).

SD: standard deviation.

p < 0.05 = 0.02; p < 0.01 = 0.04.

Results

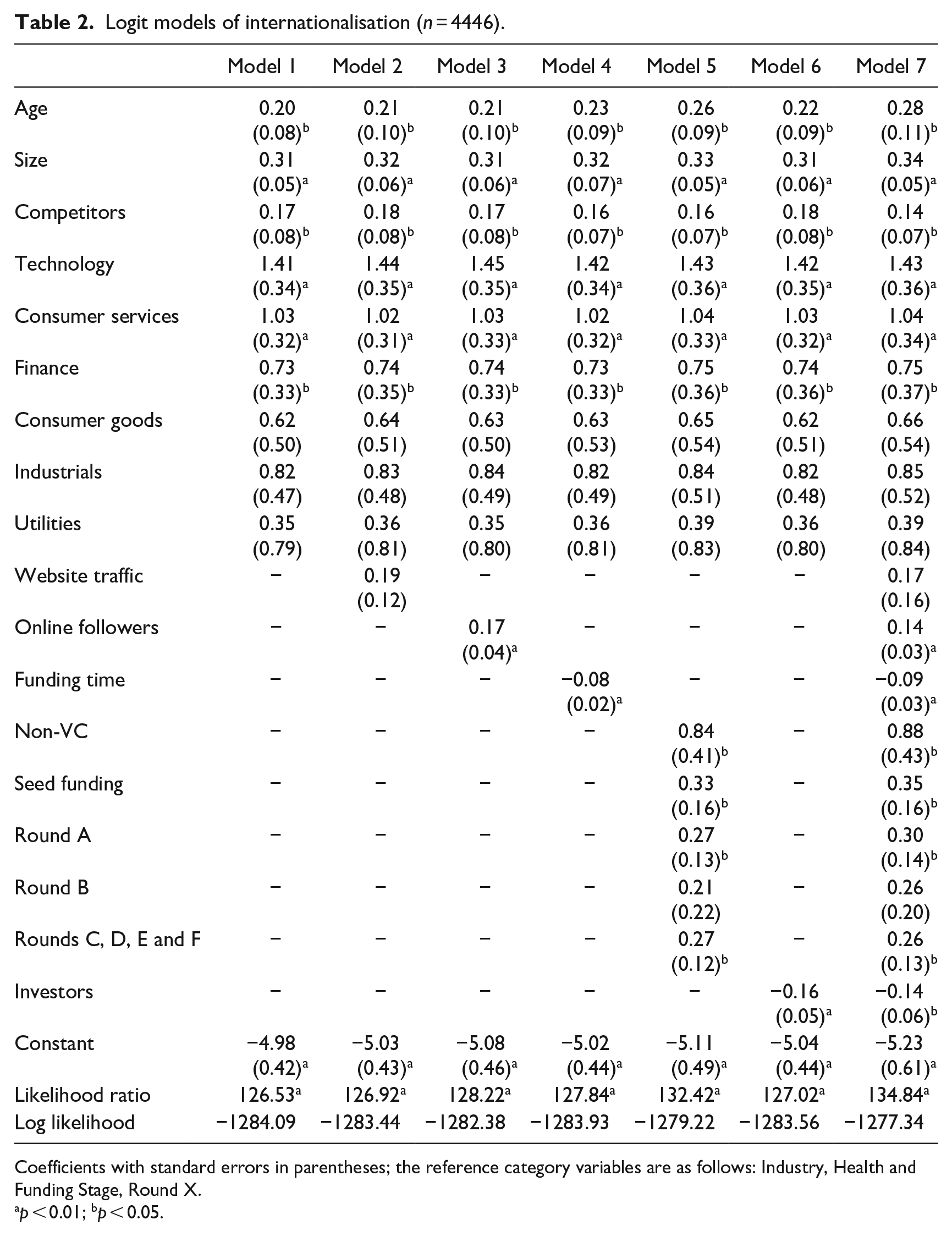

Table 2 reports the logit models of the internationalisation of the firms. Model 1 includes the age and size of firms, the number of competitors and the industry variables which are the control variables. In model 2, the independent variable of the amount of website traffic is added to the control variables. In model 3, the independent variable of the number of online followers is added to the control variables. In model 4, the funding time of the investment augments the control variables. In model 5, we included dummy variables of the last stage of investment in the firms. In model 6, the number of investors was added to the control variables. Finally, model 7 shows the results of combining all the independent variables to the control variables. In all the models, the results converged quickly and within five iterations (Greene, 2012). The likelihood ratio chi-square tests are all highly statistically significant in all of the models which tells us that at p = 0.01, or better, the models fit significantly better than empty models. We see that the volume of website traffic is not statistically significant in models 2 and 7 and thus, H1 is not supported. The number of online followers is statistically significant at p = 0.01 in models 3 and 7. Thus, we find evidence to support H2. In models 4 and 7, there is a highly statistically significant relationship at p = 0.01 between the funding time of the investment and internationalisation and in the full model this relationship also holds. Thus, the results support H3 that the lower the funding time, the higher the internationalisation prospects of a firm.

Logit models of internationalisation (n = 4446).

Coefficients with standard errors in parentheses; the reference category variables are as follows: Industry, Health and Funding Stage, Round X.

p < 0.01; bp < 0.05.

In models 5 and 7, we see that firms which have received seed funding at the last stage of investment are more likely to be international compared to firms which have received Round X of funding and this relationship is statistically significant at p = 0.05. Firms which have received Round A funding are more likely than firms which have received Round X funding to be international and this relationship is statistically significant at p = 0.05. In contrast, we see the Round B funding dummy is not statistically significant at p = 0.10 or better. Firms which have received Rounds C, D, E and F are more likely than firms which have received Round X funding to be international and this relationship is statistically significant at p = 0.05. These relationships are also found in the full model. Taken together, the aforementioned results provide strong support for H4. In models 6 and 7, we find that the number of investors is negatively significantly related to internationalisation at p = 0.01 and p = 0.05, respectively. Thus, this is counter to our expectations and H5 is not supported.

Turning to the control variables related to the firm, we see that the age and also the size of the firms are both positively related to internationalisation at p = 0.05 and p = 0.01, respectively. We also included control variables related to the environment. The number of competitors is also positively related to internationalisation at p = 0.05. Three of the industry control variables technology, consumer services and finance industries are statistically significant at the p = 0.05 level, or better, in models 1–7.

Discussion

Digital presence signals

We analysed the role of digital presence on internationalisation by analysing digital attractiveness measured by the number of website visits and digital interaction measured by the number of Twitter followers. We expected that the higher the website traffic, the higher the internationalisation prospects of a firm. However, we found that website traffic is not systematically related to international activities. While the Internet can be useful as an international sales channel (Arenius et al., 2005), our findings demonstrate that the digital presence signals of the firm itself, do not play a significant role. Although e-branding and perceived web visibility is considered to be important for differentiation (Ibeh et al., 2005), our evidence suggests that internationalising firms should consider adapting to existing and well-established digital networks beyond their own portals.

While qualitative research has shown the benefits of networking for growth and development ( Anderson et al., 2010; Anderson and Jack, 2002), when we analysed the number of social media followers as measured by the number of Twitter followers we found that this was positively related to internationalisation prospects of a firm. Fischer and Reuber (2011) suggested that Twitter-based activities can be beneficial by triggering effectual cognitions for firms and their networks, but they also warned about possible negative effects from high levels of Twitter interactions. Our findings suggest that social capital interaction signals can be related to trust and firm performance (Lins et al., 2017) even in the context of international networks. The digital presence measures of website traffic and social media followers are novel to this study. They expand the traditional view of signalling theory (Connelly et al., 2011) beyond the dual entrepreneur–investor information asymmetry and relationships.

Investment signals

Regarding the accelerating speed of funding rounds, we found that the lower the funding time, the higher the international prospects of a firm. This supports the view that new firms constrained by limited internal finance (Carpenter and Petersen, 2002) could use external funding networks for accelerated growth (Lee et al., 2001). Our research confirms that firms expanding faster through external finance and disclosing such signals to reduce information asymmetry are more likely to internationalise. Analysing the size of funding signals, firms receiving early-stage and mid-stage VC investments benefit more regarding internationalisation. VC involvement in this case is beneficial for firms facing dynamic and uncertain market and business conditions (Filatotchev and Wright, 2005), and to facilitate internationalisation (Lockett et al., 2008). Digital disclosure of access to such early-stage funding and the sources thereof, seem to be positively related to the internationalisation of firms. The shaping and legitimising of international expansion (Harrison, 2017) in this case is assisted by sharing such signals, reducing information asymmetry and greater transparency regarding funded growth in the international funding network.

Surprisingly, the number of investors is negatively related to the firm internationalisation; this relationship is statistically significant at p = 0.05 level, or better. Our result contradicts Coviello’s (2006) general argument that the growth and internationalisation of new ventures is positively related to the size of their networks including the number of investors. The negative relationship in our study suggests that the type of relationship with investors is more important than the number of investors. Small firms working with fewer investors might be able to develop stronger relationships compared to those who interact more loosely with a greater number of investors. While external finances can help a firm grow in the international environment (Anand and Delios, 2002; Meyer et al., 2009), they need to remain focused on a few strategic investors to better succeed with internationalisation plans. The number of investors might not send the right positive signals for internationalisation, but a smaller and more focused number of investors in a digital funding network however, may do so.

Firm and environment factors

Controlling for firm factors, our study confirms that age (De Noni and Apa, 2015; McDougall and Oviatt, 1996) and size (Sapienza et al., 2006) are positively correlated with internationalisation. Sharing firm signals about these indicators in a digital investment network could give further reassurance to potential new partners and customers for growth in the international marketplace.

We confirm that international new ventures try to avoid direct competition in home markets (McDougall et al., 1994) based on the negative relationship between the number of investors and internationalisation prospects. Although the competition signals shared in the digital funding network could have discouraged SMEs to internationalise, this does not seem to be the case. This indirectly indicates that there are opportunities to collaborate with competitors (Galdeano-Gómez et al., 2016); digital investment networks could help by managing the signals shared among international new ventures and investors.

In models 1–7, we see that several of the industrial activity control variables are systematically related to internationalisation. Firms in technology, consumer services and finance were more likely than firms in health care to be international; this offers a more refined analysis than that of De Jong and Vermeulen’s (2006) responding to their call for investigating opportunities digital platforms offer for firms and investors. The discussion on local clustering, global integration and industry variations (Andersson et al., 2014) is expanded in the context of digital investment network signals.

Network signalling in a digital global context

We introduce a network signalling theory approach of internationalisation for the digital economy to address the information asymmetry problem in traditional signalling theory (Connelly et al., 2011) and act as a balancing mechanism (Bergh et al., 2014). The view proposed in this study suggests that establishing social capital links through digital presence signals and economic capital links through investment signals becomes more important than the identity of the actors in the network. This is important in order to have a broader perspective in the case of VC deals (Busenitz et al., 2001, 2005) or initial public offerings (Reuer et al., 2012). A network signalling theory approach converges with similar research on crowdfunding (Kromidha and Robson, 2016) and microfinancing narrative signals (Moss et al., 2015). The key implication for digital entrepreneurship and internationalisation is that digital presence and investment signals go beyond entrepreneur–investor bilateral relationships.

The network signalling theory approach adopted in this article proposes two new sets of variables to understand information asymmetry and signalling in the context of ibusiness networks and internationalisation: digital presence signals and investment signals. It is important to bear in mind the role of Funderbeam as an ibusiness firm (Brouthers et al., 2016) where entrepreneurs and investors collaborate and internationalise. Analysing website visits and social media followers as signals in an ibusiness confirms what Chen et al. (2019) suggest based on social network theory, that internationalisation depends more on user interactions. We also offer a convincing explanation on how network ties (Langseth et al., 2016) and network access (Block et al., 2018) accelerate internationalisation.

Contrary to the traditional stance of focusing upon bilateral relationships between firms and investors, our findings suggest that information asymmetry does not depend only on users own strategies, valuation, management board or affiliations. Instead, information asymmetry can, and should be, better addressed collectively and interactively. This clarifies how information asymmetry between two parties (Spence, 2002) becomes a multidimensional issue in a digital platform and network of firms and investors. Investment signals are also magnified in a network environment. We demonstrate that signals related to the time and size of funding, but not the number of investors, are good predictors of internationalisation. This expands the traditional signalling theory view suggesting that signalling occurs through dividends (Asquith and Mullins, 1986; John and Williams, 1985), top management structures (Certo, 2003; Cohen and Dean, 2005) or strategic affiliations (Plummer et al., 2016). Analysing digital presence and investment signals promotes a better understanding of ibusiness networks (Brouthers et al., 2016; Chen et al., 2019), and the related internationalisation of small firms.

Limitations and directions for future research

Inevitably, this study has several limitations. Our models use firm characteristics. Future research should also use the characteristics of entrepreneurs (Westhead et al., 2001) and consider firm location firm – both in relation to being domestic only and in regard of international firms, the countries in which they operate. This research opportunity would build upon the work of Oviatt and McDougall (2005) who stress the importance of location and the capacity to exploit foreign location advantages. We are also confined to cross-sectional secondary data provided by Funderbeam, the ibusiness platform for investors and entrepreneurs. This limits our choice to digital presence and investment signals to website traffic and the number of online Twitter followers which they consider important to share. We are aware that firms can use also different digital platforms for internationalisation as shown by a study of 14,513 SMEs across several sectors in 34 countries (Eduardsen, 2018). In addition, the nature and purpose of digital platforms should be taken into consideration. For example, the manner in which small firms in New Zealand use Alibaba to enter the Chinese market (Jin and Hurd, 2018) can be different from how they use Twitter, or other social media platforms. The investment signals used are also limited to time, size and number of investors shared by Funderbeam. There are, however, other factors that have an important role as investment signals for internationalisation such as cultural distance and country characteristics (Majocchi et al., 2015). Yet, the purpose of introducing a network signalling theory approach is to generate a discussion around digital presence signals and investment signals for internationalisation. We analyse evidence that supports the importance of both, but we leave it to future researchers to refine the model and contribute further to signalling theory.

Conclusion

The network signalling theory approach proposed in this article suggests that theoretical mechanisms to understand internationalisation in network environments need to evolve. This is necessary to reflect changes on the digital presence and investor relationships signalled and shared in international network markets; a digital presence and investment signals are two sets of measures proposed and used to achieve this. We found that website traffic signals are not systematically related to internationalisation, but in contrast, the number of social media followers is strongly related to internationalisation. Our results suggest that relationship management is more important than unilateral marketing and firm identity messages. Analysing investment signals indicates that the lower the time between investment rounds and the higher the size of such investments, the greater are internationalisation prospects. The number of investors, however, is negatively related to internationalisation, suggesting that the importance and depth of the relationship between firms and few investors could be more important than pursuing relationships with multiple investors for global expansion.

Controlling for firm and environment conditions, firm size and age are both positively and significantly related to the internationalisation. This is consistent with the body of research in this field, explored in an innovative way with data from a digital platform where such information is shared publicly. Although there are variations across industries, the positive relationship between the number of competitors and internationalisation confirms that international new ventures constantly seek new markets. The fact that competition signals, even in the international space beyond the home market, are present and shared in a common digital environment does not seem to discourage small firms to internationalise.

Footnotes

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.