Abstract

The extent to which women participate in the angel investment market has become an important topic of research and policy interest. Based on UK survey data, we demonstrate that there are systematic but not unequivocal differences between women and men investors on a number of key investor and investment characteristics. We also report indicative evidence that members of women-only networks do differ from women who join mixed networks. Drawing on these results, we develop a stereotype threat theory perspective on women’s angel investing which highlights the cues, consequences, outcomes and responses to stereotype threat. Specifically, we theorise that stereotype threat influences women’s widely reported lower participation in the angel investment market. In addition, stereotype threat theory helps explain both women’s overall active involvement in the angel investment market and their participation in women-only investor networks. We conclude that there is a case for women-only angel networks and training programmes to mitigate the performance and participation consequences of stereotype threat.

Introduction

The existence of gender differences in a wide range of entrepreneurial contexts, including business ownership, growth and performance, access to finance, networking, is widely accepted, although individual studies vary in the extent of the differences identified (Cabrera and Mauricio, 2017; Loza, 2011; Marlow and McAdam, 2013; Yadav and Unni, 2016). Specifically, a number of studies have highlighted the underrepresentation of women in the population of business angel investors, have identified the recent growth in the number of women angels and have profiled some aspects of their characteristics and behaviour (Amatucci, 2016; Amatucci and Swartz, 2011; Becker-Blease and Sohl, 2007, 2011; Coleman and Robb, 2017, 2018; Gavara and Zarco, 2015; Harrison and Mason, 2007; Sohl and Hill, 2007). While there appear to be differences between women and men investors, these are neither systematic nor consistent, and an early analysis that suggested that there was more heterogeneity within the women angel population than between women and men angels (Harrison and Mason, 2007) remains largely unchallenged.

However, in both angel research specifically, and entrepreneurship more generally, the possible explanations for any gender-based differences observed are less well-understood. It has been suggested that there is a lack of cumulative knowledge, adequate conceptualisation and theory building (Harrison et al., 2015), with a past tendency to analyse women’s entrepreneurship from the very limited perspective of the differences between men and women – the ‘gender as a variable’ approach. One consequence of this has been to attribute problems such as lower business growth performance, more problematic access to finance and lower participation as investors to women themselves instead of to wider social orders (the inter-related social structures, institutions, relations, customs, values and practices, which maintain and enforce specific patterns of relating and behaving – Hechter and Horne, 2003), so, emphasising the individual over the structural and situational. As such, it is argued, the current discourse on women’s entrepreneurship sustains a social order that benefits men as a group compared to women as a group and in emphasising the individualist perspective, diverts attention from structural and institutional arrangements (McAdam et al., 2019).

There have been some attempts to theorise women’s angel investing through a gender lens, drawing attention to the role of competition and performance (Harrison and Mason, 2007), glass ceilings (Gavara and Zarco, 2015) and stereotype threat (Idi Cheffou and Bellier, 2017; Gupta et al., 2014). However, there is no comprehensive model which can provide a justification for the development of effective initiatives, such as the growth of women-only angel networks, designed to overcome the structural and institutional arrangement of the business angel market. We reflect upon these issues by examining sui generis the characteristics and behaviour of women business angels, and how these differ from their male peers, and the implications of these, both for the specific issue of the participation of women in the angel investment market and for the wider issue of the gendered analysis of entrepreneurial action. The article is structured as follows. In the following section, we summarise the current fragmented state of knowledge about women as angel investors. This is followed by a discussion of the methodology of our study and a summary of the results. The next section develops a theoretical model of women’s angel investing, drawing on recent formulations of stereotype threat, defined as ‘the fear of stigmatized individuals to be judged or treated stereotypically (Steele et al., 2002)…[which] usually consists of a suboptimal performance in a task related to a judgement dimension in which that particular group is known to be weak…and also comes into play whenever people become aware of a negative stereotype about themselves’ (Gentile et al., 2018). The discussion section develops some of the implications for policy and practice and the conclusion considers directions for future research.

Literature review: women as angel investors

There has been significant research into gender and access to bank finance and institutional venture capital. The main conclusions of such have been that venture characteristics other than gender account for much of the observed differences (Bellucci et al., 2010; Leitch et al., 2018), with differences in initial start-up (growth) orientation being particularly significant (Guzman and Kacperczyk, 2019). There is also substantial evidence of an underrepresentation of women in mainstream venture capital (Brush et al., 2018; Kwapisz and Hechavarría, 2018; Vismara et al., 2017), although there are exceptions (Chen and Harrison, 2019). However, despite the importance of angel finance to the entrepreneurial economy, there are only a handful of studies of women angel investors (Amatucci, 2016; Amatucci and Swartz, 2011; Becker-Blease and Sohl, 2007, 2011; Coleman and Robb, 2017, 2018; Gavara and Zarco, 2015; Harrison and Mason, 2007; Sohl and Hill, 2007). These highlight both the low (but rising) proportion of angel investors who are women and their low participation in angel groups and networks. This is not a new phenomenon. Using late 19th- and early 20th-century data, it has been argued that women have been only ‘peripherally linked’ to male investor networks (Maltby and Rutterford, 2006; Rutterford and Maltby, 2005), highlighting an argument that women investors are different and are organised differently than their male equivalents. Subsequent research suggests that women investors face barriers as a result of investment inexperience, particularly in deal structuring and pricing (Sohl and Hill, 2007) with lower levels of confidence compared to their male equivalents (Becker-Blease and Sohl, 2007).

Women angel groups attract more funding applications from women-owned firms than other angel groups (Sohl and Hill, 2007), although the odds of women accessing angel capital from women angels are only about half the average when gender is not taken into account (Edelman et al., 2017: 309). The assumption that angel investing is a male activity that excludes women, or that women angel investors need to ‘prove’ themselves in a male-dominated investment world (Edelman et al., 2017), is countered by evidence profiling women investors in the context of masculinised normative definitions of angel investors (Harrison and Mason, 2007; Sohl and Hill, 2007) and reviews giving voice to women business angels (Amatucci, 2016). Notwithstanding a number of possible reasons for gender differences in participation rates as angel investors, including competition, acquired and innate differences and discrimination, (Gavara and Zarco, 2015), it has been argued that women angels actually differ more from each other, in demographics, experience and investment behaviour, than they do as a group from men (Harrison and Mason, 2007).

Nevertheless, it remains the case that ‘the theme of gender has been much underexplored, even if it could potentially produce high-impact research’ (Tenca et al., 2018: 20). The comprehensive review by Tenca et al. (2018) identifies only five papers specifically addressing gender and angel investing with many studies focused on gender and the demand for angel finance rather than on the supply of investment capital from women investors (e.g. Burke et al., 2014; Poczter and Shapsis, 2018).

This relative paucity of research reflects the generally low proportion of women angel investors. In Europe, this ranged from 1.3% (Netherlands) to 9.3% (France) (EBAN, 2010), and has since risen to around 11% overall in 2017, with higher proportions reported in central and southern Europe (30%) and Switzerland (18%) (EBAN, 2018). This still lags behind the steady growth in women’s participation in the angel market in the United States, which has increased from 5% in 2004 to 29.5% in 2018 (CVR, 2019). In Canada 17% of members of angel groups in 2018 were women, up from 14% the previous year, with two women angel groups accounting for just under 20% of the total (Mason, 2019). In the United Kingdom, the representation of women in the angel market has increased from 1% (2004) to 5% (2003), 8% (2008), and to 12%–14% (2014) (ERC, 2014; Mason and Botelho, 2014), although the most recent estimate for 2016–2017 is 9% (British Business Bank, 2018). With increases in the number of high networth women, 1 successful women entrepreneurs, the number of women in senior management positions and the number of women-led training groups and training programmes for prospective and active women business angels, this trend seems certain to accelerate. This is reflected in growing policy and practitioner interest in women angels and in new initiatives to support and encourage them (Coleman and Robb, 2017; GoBeyond, 2016, 2017; WA4E, 2018).

Previous research (Harrison and Mason, 2007) has identified few differences between male and female angels (who profile as ‘honorary men’). In this article, we present the results of a more recent analysis of the UK business angel market to investigate the extent to which this is changing as a result of the influx of new women angels. From this, we develop a theory of women’s angel investing which has implications for both further research and practice. Specifically, building on Tenca et al. (2018), we ask four research questions. First, is the profile of women angel investors different from that of men? Second, is the investment behaviour of women angel investors different from that of men? Third, are the characteristics of the businesses women angels invest in different from those of male investors? Fourth, is the profile of women angels joining women-only investment networks different from that of those joining mixed-gender networks?

Methodology

We explore these issues using data collected on business angels and their investments from a 2014 online survey of angel investors in the United Kingdom. It was promoted through angel groups, angel networking organisations and our personal networks. Of the 84 identified groups, 32 were willing to support the research and made it available to their members. This represents a response rate of 38% when measured in terms of groups supporting the research. As with virtually all studies of angels, it is biased to the visible market, which is estimated to account for only 10% of the total angel market (EBAN, 2018), with 86% of respondents being members of one or more angel groups. However, previous research has shown that many angels who operate in the visible market as members of angel groups also operate in the invisible market (Mason and Harrison, 2010), making investments privately in deals that they have sourced themselves. The survey attracted responses from 238 business angels, including 28 women (seven of which are members of a women-only group). At the time the survey was undertaken, this was the largest attained angel survey in the United Kingdom. Although some subsequent UK Business Angel Association (UKBAA)-sponsored surveys (British Business Bank, 2018; ERC, 2014) have larger attained samples, these studies are not independent and include responses from non-angel respondents, including crowdfunders. Our respondent investors were members of a total of 71 angel groups based throughout the United Kingdom. Just under half were members of more than one group. On average, participants had been investing as an angel for 11 years, and 34% of the sample had 10 or more investments in their portfolio. Besides demographics and investment experience questions, participants were asked to report information on their three most recent investments which produced details on a total of 472 investments.

The difficulties in collecting angel data have been extensively debated and include the invisibility of investors, the absence of sample frames, the absence of population parameters to judge sample representativeness, reliance on samples of convenience, relatively small sample sizes given the effort expended in data collection and the increased diversity of investor types (Harrison and Mason, 2008; Mason and Harrison, 2008). As a result, angel research is bedevilled by the challenges of representativeness: although the growth of angel groups has improved the visibility of the market and its actors, this raises new issues of the representativeness of those angels who choose to join these organisations (Bonini et al., 2018; Mason et al., 2019). These issues are, of course, compounded in the case of a rare phenomenon such as women angel investors. Accordingly, given that, as Cumming and Johan (2017: 360) argue, ‘in respect of angel investment, the data to date are so scant that it is hard to even quantify the overall investment levels’, the research reported here is exploratory rather than definitive.

Results

Male/female differences

The data allow us to examine male/female differences across a number of dimensions, including personal characteristics, angel group participation and behaviour, and investment criteria, investment behaviour and characteristics. We undertake a separate analysis to compare women investors who are members of women-only investor groups with those who are members of mixed-gender groups. We test for women/men differences using chi-square tests for categorical variables and independent t-tests of equality of means for investor and investment characteristics continuous variables. In the latter case, to ensure the assumption of equal variance between groups, Levene’s test of homogeneous variance was performed. Differences in personal and investment characteristics between women investors who were members of women-only groups and those who were members of mixed groups were also compared using chi-square tests and t-tests. In some cases, no significance test results are reported; this reflects the fact that in these cases, our data did not meet the requirements and assumptions of the test being applied.

We address the problem of small numbers inherent in angel research in the following way. We follow an unbalanced design with unequal sample size protocol (Shaw and Mitchell-Olds, 1993). As such, when testing the mean score for different groups, it is not required to have the same number of observations in each cell of the design (Field, 2013): the only requirement is to have at least some observations in each cell in order to have a factorial design. The tests do not assume equal sizes, so working with an unbalanced design does not violate any of the assumptions of t-tests or chi-square test. However, it is important to note that t-test is less robust to violations of the assumption of homogeneity of variances when the sample sizes differ by a large amount. As previously mentioned, unequal variances between samples affects the assumption of equal variances in t-tests. Having both unequal sample sizes and variances dramatically affects statistical power and Type I error rates (Rusticus and Lovato, 2014). To correct this effect, we have used Levene’s test (Derrick et al., 2018).

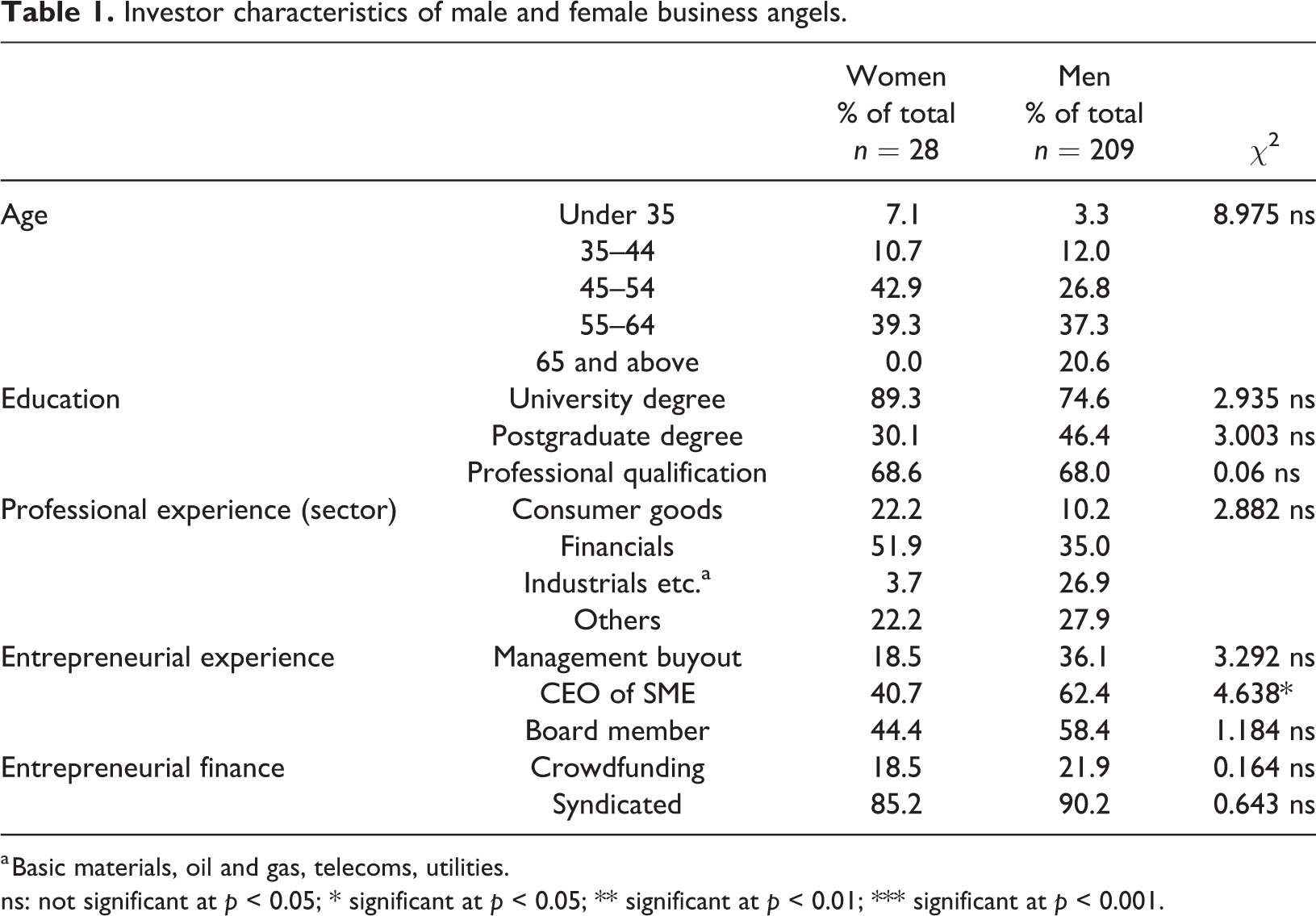

Based on our analysis of women/men differences in investment characteristics and investor characteristics and experience, there is some evidence to support the argument that women angels are different in terms of characteristics and behaviour. First, in terms of demographics and experience, and supporting previous research which found few gender differences (Harrison and Mason, 2007), when compared with male investors, women are younger and better educated, although these differences are not statistically significant, and are less likely to have entrepreneurial experience as CEO of an entrepreneurial venture (p < 0.05). However, there is no evidence that women angel investors have significantly less experience of management buyouts (MBOs), less board-level experience in larger businesses or have less industry experience. There also appears to be no significant male/female difference in entrepreneurial finance experience, as reflected in experience of crowdfunding (but see Malaga et al., 2018; Mohammadi and Shafi, 2018) and syndication with other investors (Table 1). This suggests that while the growth in the number of women angels is bringing in women with different backgrounds and experience, and is consistent with wider evidence that the UK angel market is changing in terms of motivations and backgrounds (Mason and Botelho, 2014), these differences are for the most part not significant.

Investor characteristics of male and female business angels.

a Basic materials, oil and gas, telecoms, utilities.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

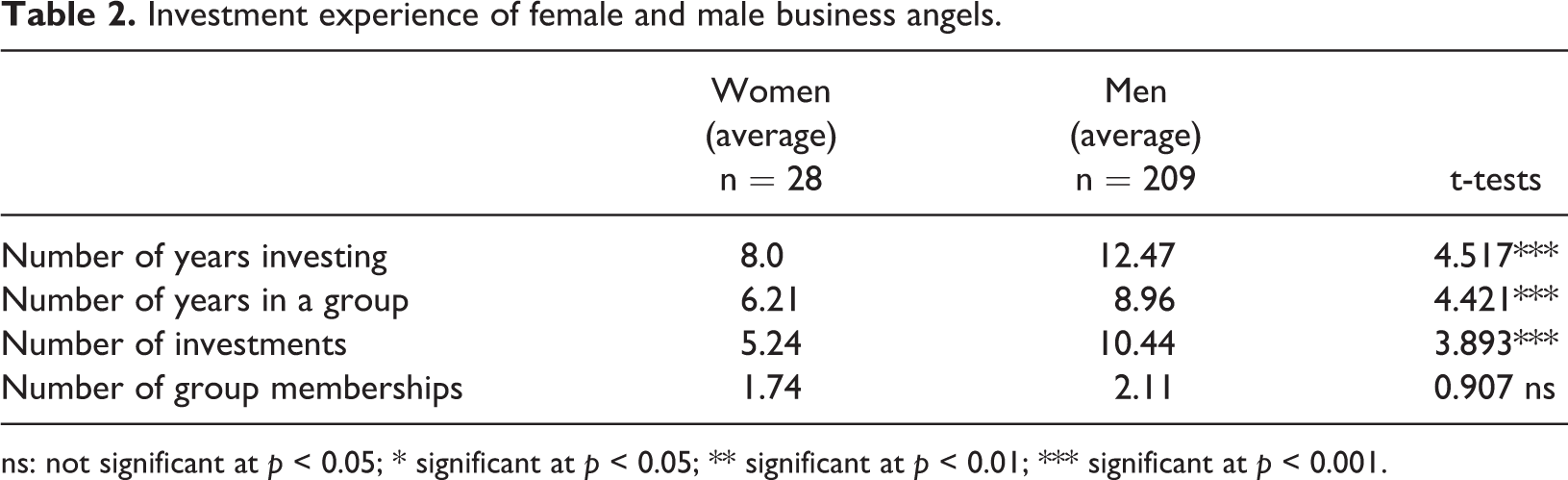

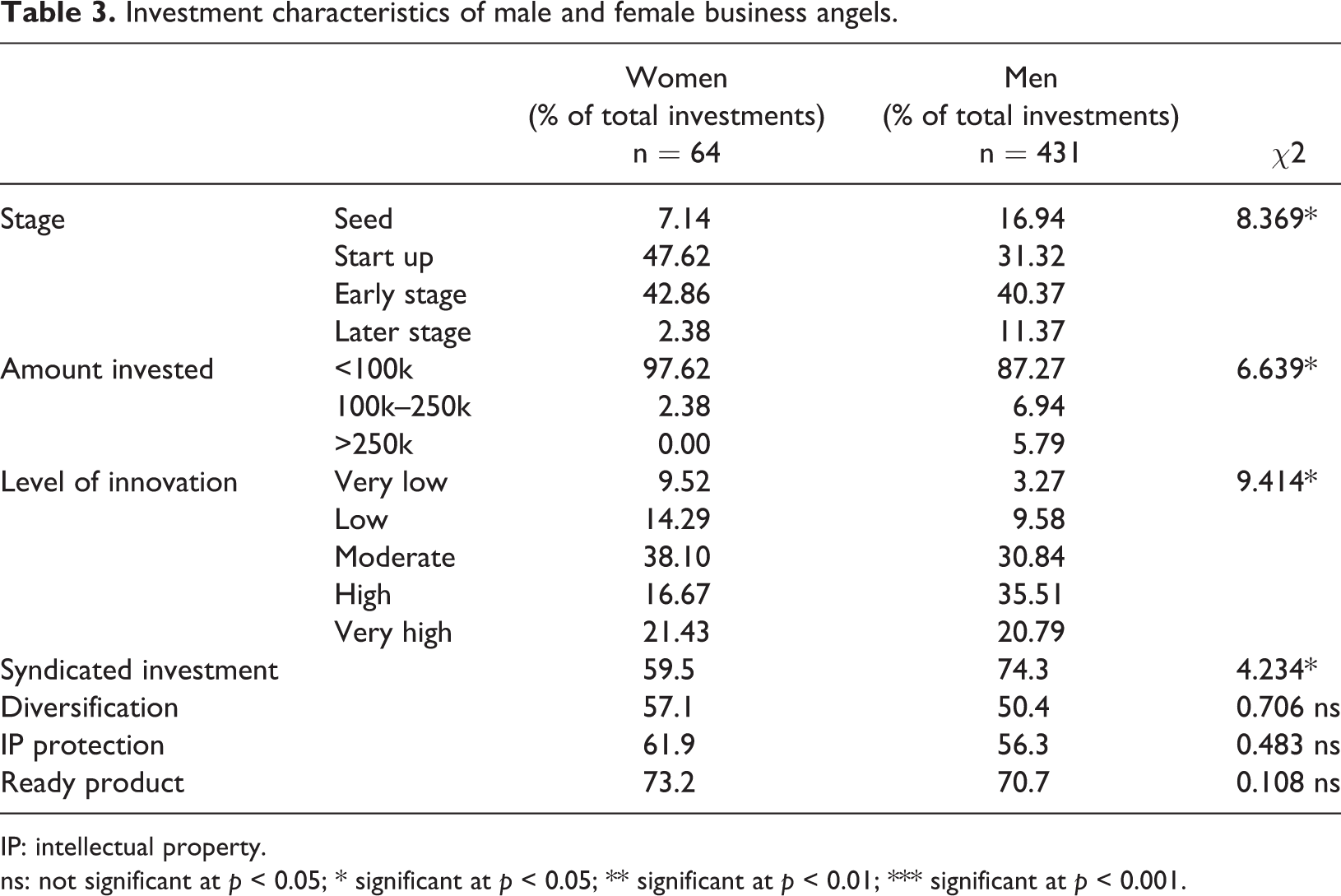

Second, in terms of investment experience, however, the picture is rather different (Tables 2 and 3): women investors had fewer years of investing experience (p < 0.001), made smaller investments (p < 0.05), made fewer investments overall (p < 0.001) and were less likely to invest in innovative ventures (following Lahti (2011), this was measured as a respondent’s perception of innovativeness on a 5-point Likert-type scale) (p < 0.05). Women were less likely to have invested at both seed stage and in later stage deals (p < 0.05) and were significantly less likely to invest in syndicated investments (p < 0.05). However, women were no more likely than men to invest in businesses showing other risk mitigating characteristics such as portfolio diversification, intellectual property (IP) protection or with a market-ready product or service. Notwithstanding the argument that ‘women are more risk averse than men’ (Borghans et al., 2009: 649; Nelson, 2015), this suggests that women angel investors are on balance no more risk averse than men, emphasising the complexities of the everyday understanding, practices and discourses of risk (Nygren et al., 2020). Indeed, risk assessment is highly contextual: while there is extensive evidence of a gender effect in investment such that women are more risk averse than men, this largely disappears once education, knowledge and access, marital status and wealth are taken into account (Maltby and Rutterford, 2012). Furthermore, in terms of risk aversion, women are not all the same: for example, women who enter into a finance career can be significantly different in their risk-aversion levels than women who do not enter into the finance profession and as a result, women in finance may have the same average levels of risk aversion as men in finance (Adams and Ragunathan, 2019). Prior research on woman angel investors is consistent with this interpretation (Coleman and Robb, 2018; Harrison and Mason, 2007).

Investment experience of female and male business angels.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

Investment characteristics of male and female business angels.

IP: intellectual property.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

Third, women overall were somewhat less likely than men to be members of angel groups (Table 2). The difference in the number of group memberships (1.74 vs 2.11) is not significant overall; however, once allowance is made for the 30% of women investors who were members of a women-only group, the women/men difference is weakly significant (p < 0.10). Consistent with their shorter track record in angel investing, women have been members of a group for significantly less time than their male counterparts (p < 0.001). This suggests that there is some evidence from our sample of activist choice homophily, the perception of shared structural barriers stemming from a shared social identity (Greenberg and Mollick, 2017) consistent with stereotype threat. This is reflected in the social networks and information sources used: similarity (in this case, maleness) does appear to breed connection in this market, as the evidence on participation confirms (see below). However, women did not differ from men in the number of sources relied on in the due diligence process. Other recent evidence suggests that women were less likely than men to invest as solo investors (15% vs 23%) but were three times less likely to lead deal-specific investment syndicates (British Business Bank, 2018).

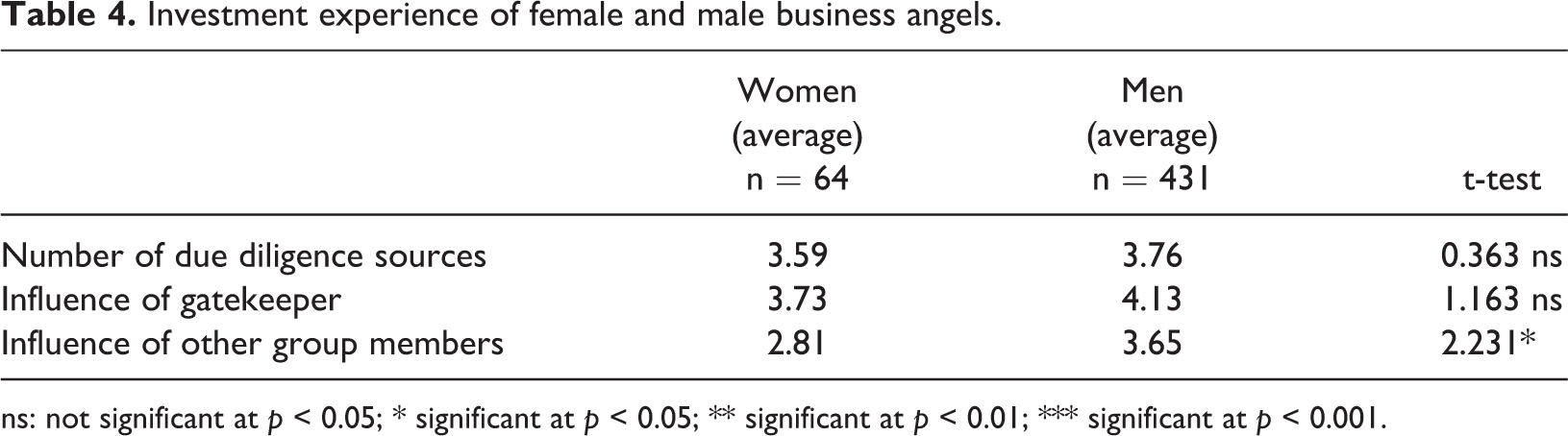

Fourth, women and men do appear to differ in how they participate in angel groups (Table 4). While women are members of (largely male dominated) angel groups they do not participate in them as fully as men and, in particular, do not use the knowledge and opinion of other investor members as extensively (p < 0.05). This is consistent with wider evidence that women underperform men in negotiation and decision-making situations (Carr and Steele, 2010; Kray et al., 2002) where women are concerned about being judged adversely on the basis of a negative stereotype (Spencer et al., 2016). It is also situationally specific; for example, there is some evidence 2 that women business angels are willing to admit what they do not know and ask ‘stupid’ questions, whereas men are too proud to admit that there are things they do not know by asking questions, so they do not ask. In mixed-gender groups, this absence of questions from men in practice deters women from asking sensible and legitimate questions, whereas they feel confident to do so in women-only groups. Overall, there is no evidence that women are less influenced by gatekeepers/network managers, although as we show below, women members in women-only groups are more likely than other women to be influenced in their decision-making by gatekeepers and other investors (Table 8). Excluding members of women-only networks the male/female difference is significant (p < 0.05) in the expected direction: women in mixed-gender networks are less likely than men to solicit from and rely on the group gatekeeper or other members for advice and support.

Investment experience of female and male business angels.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

Women angels: women-only/mixed-gender network differences

A key issue in the analysis of women’s entrepreneurial experience is the extent to which women-only networks can act as a ‘safe space’ for entrepreneurial action and support free from the pressures of the dominant masculinist hegemony (Harrison et al., 2020; Leitch et al., 2017; McAdam et al., 2019). Specifically, this raises the wider question of the extent to which the characteristics, profile and investment behaviour (the ABC – attitudes, behaviour and characteristics) of women who join women-only investor groups differ from those of women who join mixed-gender networks. Given the small number of respondents, the findings presented in this section are exploratory and cannot be regarded as conclusive; a more comprehensive analysis of women angel investors in women-only groups is an important direction for further research in understanding the dynamics of the evolution and operation of the angel market.

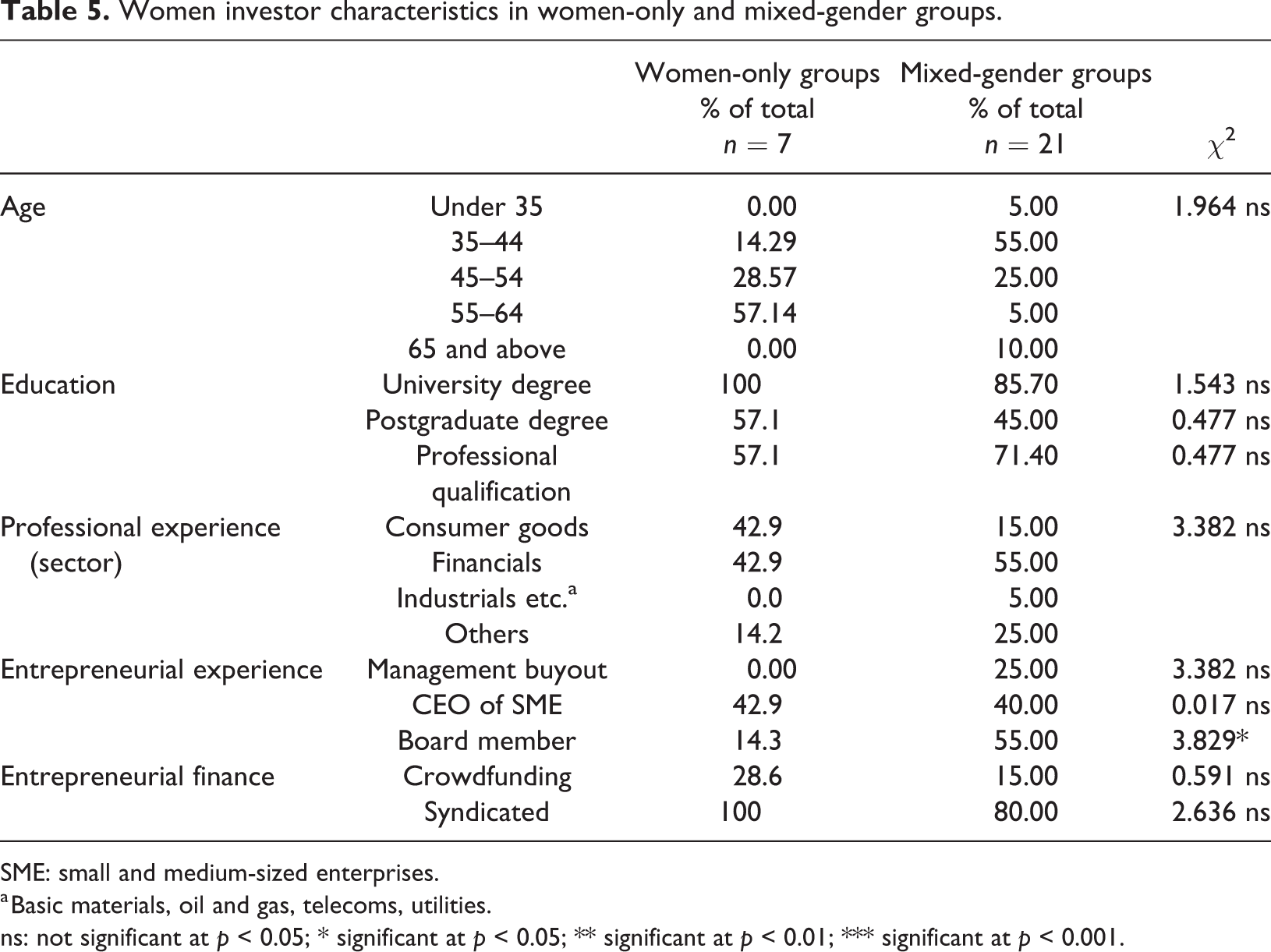

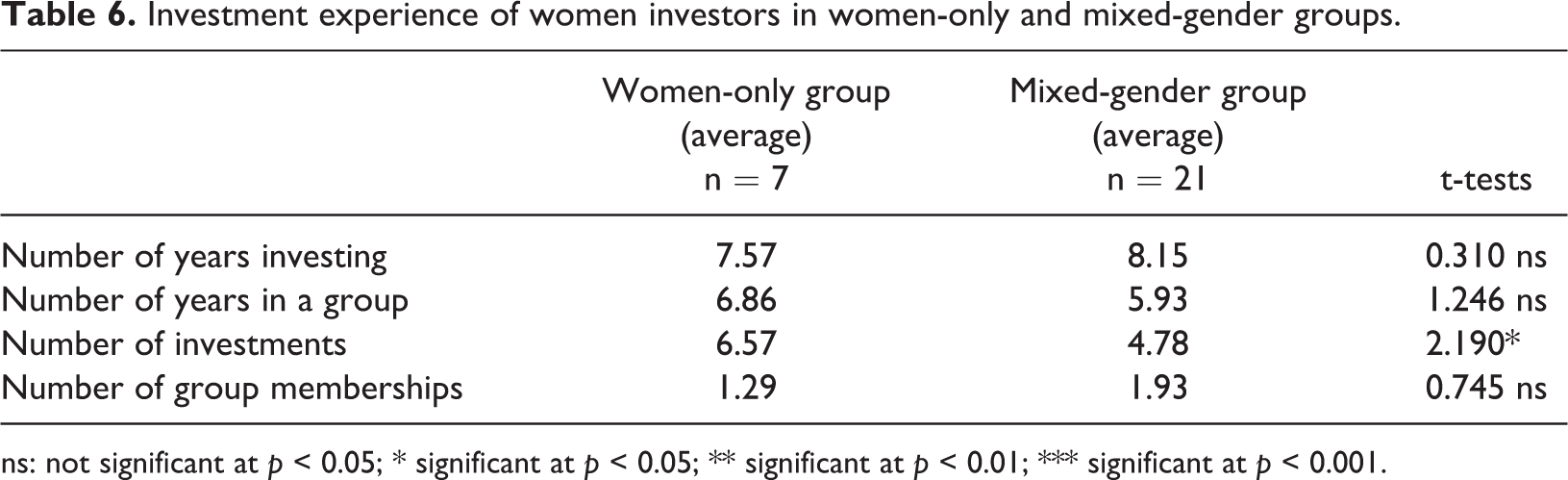

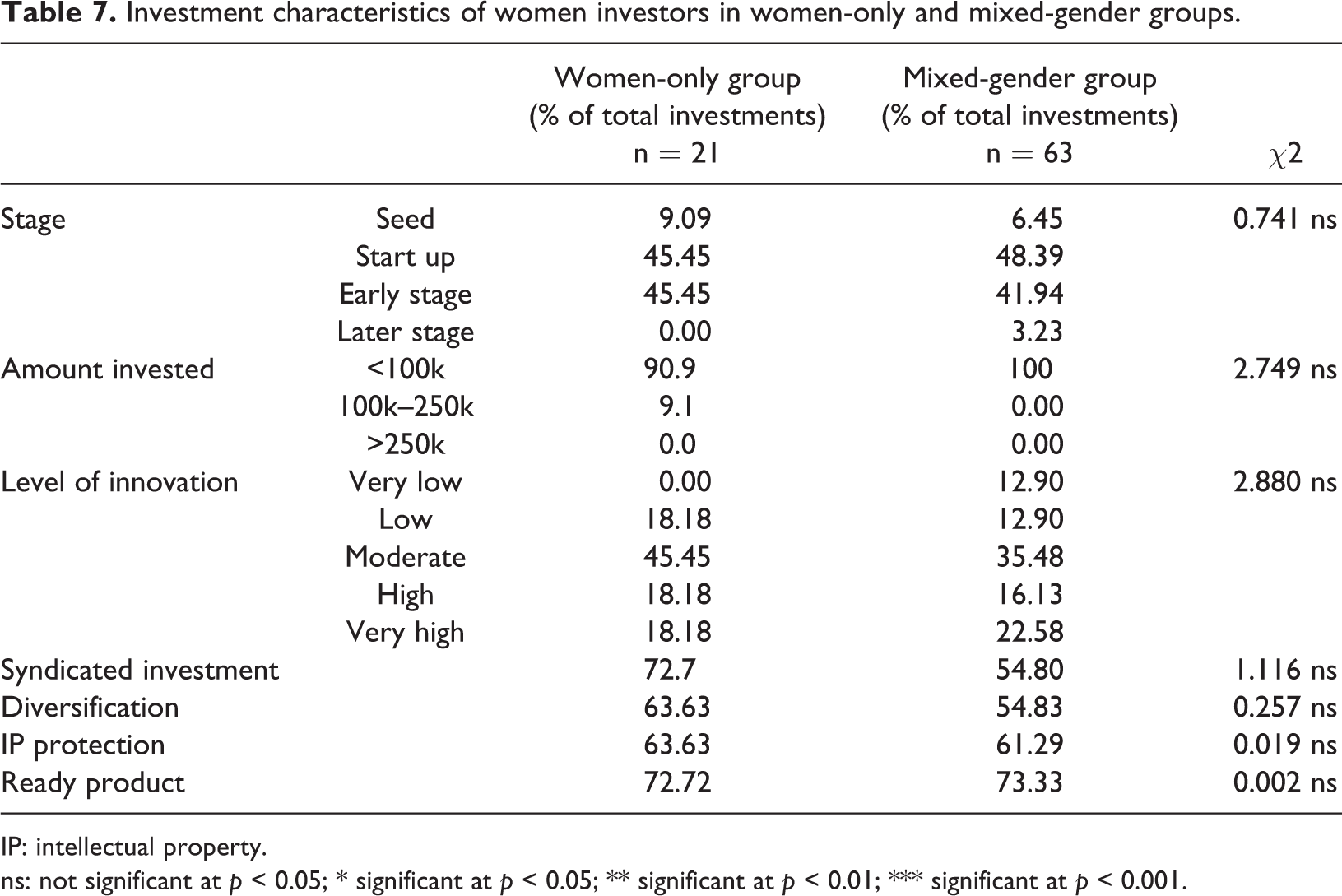

First, although women who join women-only groups appear to have a distinctly older age profile than those who join mixed-gender groups (Table 5), there is no significant difference in the age profile of women who were members of women-only networks compared with that of mixed-network members. However, although both groups have similar levels of entrepreneurial experience (as CEO of a small and medium-sized enterprise (SME)), members of women-only groups are significantly less likely to have board-level experience (p < 0.05). Although members of women-only groups appear to be more risk averse than members of mixed networks (in terms of making, on average, smaller investments in low- to medium-innovation projects), these differences are not significant (Table 7). Women members of women-only angel groups and of mixed groups have similar levels of investment experience, but the former have made significantly more investments (p < 0.05), suggesting that a women-only environment provides both a learning opportunity and a ‘safe space’ for investing (Table 6) (Coleman and Robb, 2018).

Women investor characteristics in women-only and mixed-gender groups.

SME: small and medium-sized enterprises.

a Basic materials, oil and gas, telecoms, utilities.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

Investment experience of women investors in women-only and mixed-gender groups.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

Investment characteristics of women investors in women-only and mixed-gender groups.

IP: intellectual property.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

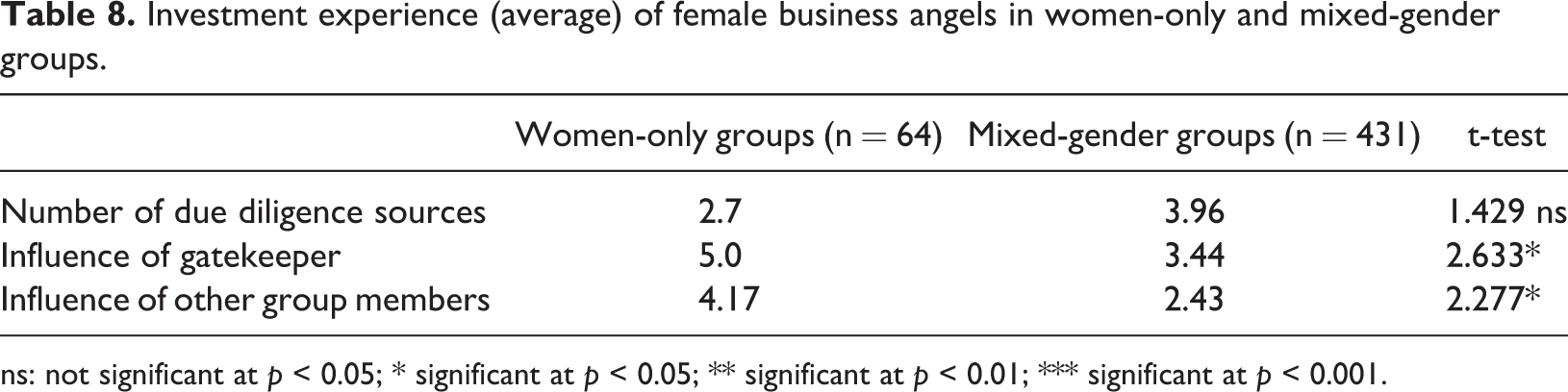

Finally, although there are no differences between the two groups of women investors in the number of due diligence sources used, members of women-only groups are much more open to the opinion of others (in the form of group gatekeepers and other investors) (p < 0.05) (Table 8). This finding reinforces the idea that women-only groups can provide a positive environment for female angels to listen to opinions of other investors: of the three groups of investors analysed in this research (men, women in mixed-gender groups and women in women-only groups), it is the women-only group members that report higher levels of influence from others (leading investor/gatekeeper and peer angels).

Investment experience (average) of female business angels in women-only and mixed-gender groups.

ns: not significant at p < 0.05; * significant at p < 0.05; ** significant at p < 0.01; *** significant at p < 0.001.

A stereotype threat perspective on women’s angel investing

Although based on unavoidably small samples, given the nature of the angel population, and therefore, indicative rather than definitive, our results prompt the development of an emerging model of women’s angel investing that can guide future research. Building on previous research that has pointed to the heterogeneity of women angels such that the within-group variance in their characteristics is greater than the between-group (male/female) variance (Harrison and Mason, 2007), we argue that not all women angel investors are alike. We have suggested that while women who join women-only angel groups and those who join mixed-gender groups are very similar in terms of demographics and experience (Table 5) and investment characteristics (Table 7), women-only group members make more investments (Table 6) and rely more extensively on gatekeepers and other group members for advice and support than do members of mixed-gender groups (Table 8).

This suggests the relevance to angel investing of stereotype threat theory (Pennington et al., 2016; Schmader et al., 2008). Based on the original research of Steele and Aronson (1995) and Steele (1997), stereotype threat theory posits that the activation of a negative stereotype of a minority group will interfere with the performance of group members in stereotype-relevant domains (Cadinu et al., 2005). In other words, stereotype threat is a self-evaluative threat that appears when an individual ‘is at risk of confirming a negative stereotype about him- or herself’ (Gentile et al., 2018: 95) and is concerned with being judged or treated negatively on the basis of this stereotype (Spencer et al., 2016). As such, it represents a lack of fit between women’s skills, characteristics and aspirations and those deemed necessary for effective performance (Hoyt and Murphy, 2016). For example, in experimental situations where women are required to perform a task, the performance of the treatment group (who are told that there are clear differences in the scores obtained by men and women in the task) is significantly poorer than that of the control group (who are told that there are no differences between men and women in task performance) (Spencer et al., 1999; Stoet and Geary, 2012). A number of recent studies of financial decision-making (Carr and Steele, 2010), opportunity identification (Gupta et al., 2014) and investment decision-making (Idi Cheffou and Bellier, 2017), all undertaken in stereotype threat typical environments where men outnumber women (Inzlicht and Ben-Zeev, 2000), point to the relevance of stereotype threat theory.

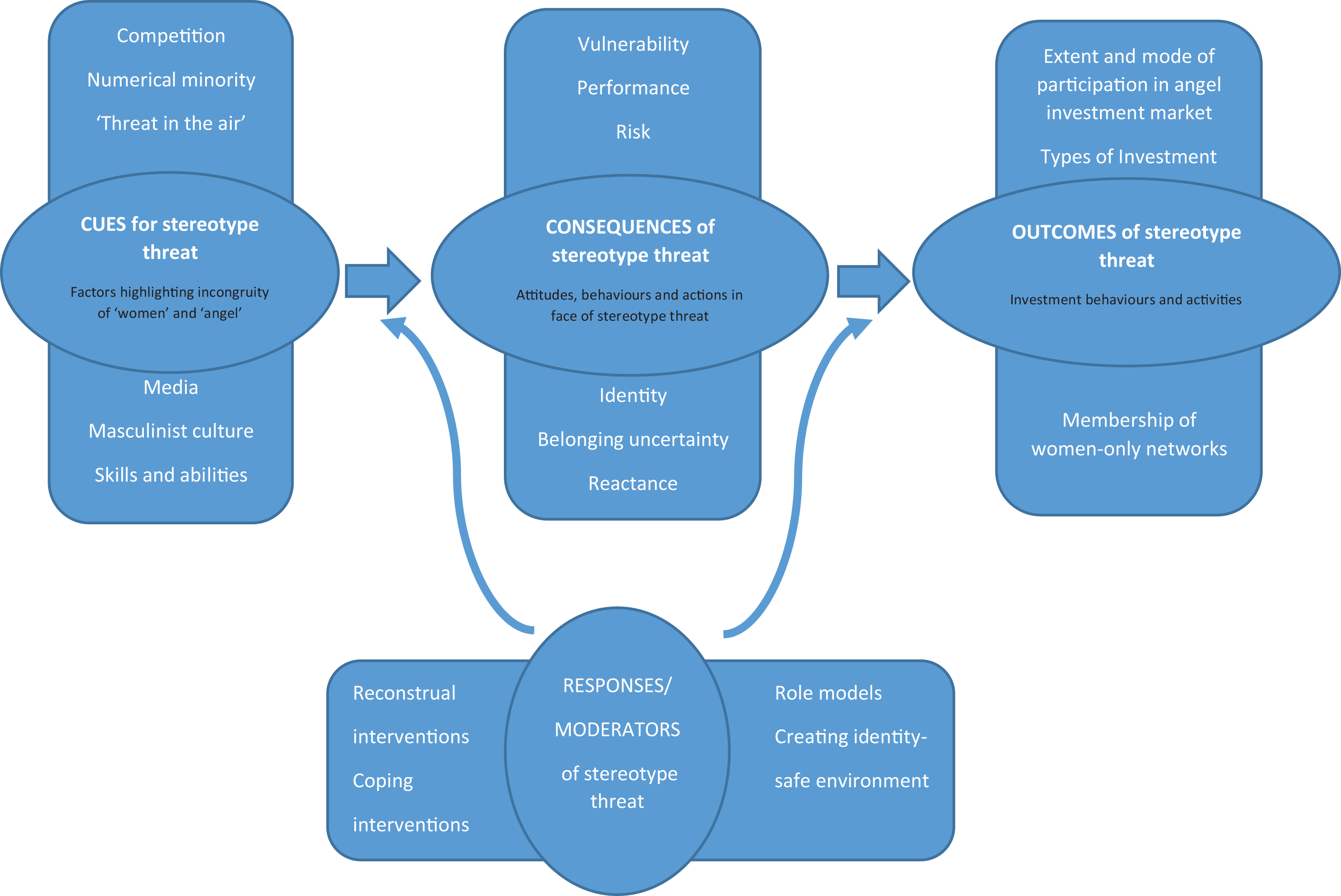

Building on the exploratory results of our research as reported above and on recent formulations of stereotype threat theory across a diverse range of contexts (Gentile et al., 2018; Hoyt and Murphy, 2016; Jouini et al., 2018; Spencer et al., 2016), we develop a stereotype threat theory of women’s angel investing as the basis for further research (Figure 1). This has four elements: the situational factors or cues that can signal stereotype threat; the consequences of stereotype threat, in terms of the attitudes, behaviours and actions taken in the face of stereotype threat; the outcomes of stereotype threat, in terms of investment behaviours and activities; and the responses to stereotype threat, in terms of the factors moderating its consequences and outcomes. We discuss each of these four elements in the light of both our exploratory results and the wider stereotype threat literature, and where appropriate, develop indicative propositions to guide further research.

A model of stereotype threat in angel investing (developed from Spencer et al., 2016 and Hoyt and Murphy, 2016).

Cues for stereotype threat

There are a number of sources of and cues for stereotype threat, that is, the factors underlying the supposed incongruity of ‘woman’ and ‘angel investor’. Many of these are in the form of situational cues that signal social identity contingencies (Purdie-Vaughns et al., 2008): stereotype threat arises where an individual has a social identity that is targeted by a negative stereotype in a given situation with implications for well-being and one’s sense of belonging in various environments (Spencer et al., 2016). Such cues come in many forms, including culturally held stereotypes, such as the masculinised culture of entrepreneurship, which alert the targets of stereotype threat that their group is devalued in a particular situation (Emerson and Murphy, 2015). These may be reinforced by media representations of the target group (women) and activity (entrepreneurship, angel investing) and by reminders of the target’s numerical minority in the relevant domain (Hoyt et al., 2010; Von Hippel et al., 2011a). Beyond this, there is evidence that where success is equated with inherent skill and abilities, women can feel threatened as they are stereotyped as not possessing such talent (Leslie et al., 2015). Specifically, cultures permeated by a competitive ethos are particularly threatening to women (Gneezy et al., 2003; Kray and Shirako, 2011; Niederle and Vesterlund, 2008).

Drawing on status characteristics theory and expectation states theory (Berger et al., 1972; Foschi, 2000; Ridgeway, 2001), the presence of a negative stereotype on the formation of self-confidence and on decision-making in achievement-related situations has substantial implications. Any stereotype ‘of lower ability (in the form of biased interpretation of success and failure in terms of ability) leads to gaps in confidence, in participation in risky/ambitious options and in performance’ (Jouini et al., 2018: 34). Even on the ex-ante assumption of differences in ability, the exaggeration of inter-group differences in objective ability distributions can itself generate negative stereotypes such that some groups are considered, and consider themselves, to be less able and hence, participate less in difficult options (Bordalo et al., 2016). Situational cues, however, do not have to be blatant in order to trigger stereotype threat; both can have negative influences independently and the specific characteristics of the source and target of the threat matter less than ‘the mere fact that the threat is in the air’ (Spencer et al., 2016: 418).

Consequences of stereotype threat

We can identify two categories of consequence following from stereotype threat: first, vulnerability responses that link to task performance (which we divide into performance, identity and risk consequences), and second, reactance responses, the active engagement in counter-stereotypical threat behaviour (Hoyt and Murphy, 2016).

Vulnerability: performance consequences

We have confirmed that angel investment activity continues to be a male-dominated activity; most ventures seeking capital are male-led, most investors are male and most business angel networks are male-dominated in terms of both investor membership and gatekeepers. The ability to compete is a predominant characteristic associated with successful entrepreneurship (Shane et al., 2003). Given this, the angel investment market encompasses many of the cues for stereotype threat. As the link between competition-related stereotype threat and performance is well-established, as a number of meta-analyses have demonstrated (Lamont et al., 2015; Stoet and Geary, 2012; Walton and Spencer, 2009), we draw on research into competition and performance in heteronormative environments to frame our discussion of women angel investors. This research suggests that women are less willing to compete and are usually outperformed by men under competitive conditions and accordingly perform less well in mixed-sex, rather than in single-sex environments (Dato and Nieken, 2014; Ergun et al., 2010; Gneezy et al., 2003; Gneezy and Rustichini, 2004; Niederle and Vesterlund, 2007, 2011). These conclusions have been established across a substantial body of evidence: Klege and Visser (2020), for example, report on 40 experimental studies across 18 countries following the Niederle and Vesterlund (2007) protocol, and experimental research has been complemented by real-world studies of rural entrepreneurship (Klege and Visser, 2020), problem solving (Borgonovi and Greiff, 2020), sport (Englert and Seiler, 2020), expert chess tournaments (Backus et al., 2016), feedback (Wozniak et al., 2016), decision-making (Carr and Steele, 2009) and managerial and leadership tasks (Bergeron et al., 2006; Hoyt and Blascovich, 2010). There is, in other words, at work a systemic process of role socialisation and acculturation, which is reflected in the positions women occupy and the roles they play in the labour market in general, and in entrepreneurship in particular. A process intensified by women’s unwillingness to compete which can influence their performance levels even after taking up such roles (Klege and Visser, 2020: 2). The social/cultural, rather than biological basis, for this is clear from research indicating that men are twice as competitive in patriarchal environments but women are more competitive in matrilineal environments (Gneezy et al., 2009).

In this article, competitiveness is indicated by the level of individual investor participation (membership, involvement) in angel groups. Our results (Tables 2 and 4) confirm the relationship between patriarchy and male competitiveness (Gneezy et al., 2009) and suggest that women do not participate as actively in (largely male dominated) groups, use more tentative language and are less fluent (McGlone and Pfeister, 2015), and are less likely to use the knowledge and opinion of other investor members, gatekeepers and network managers. In terms of Figure 1, this suggests the following propositions:

P1a. The stereotype threat implications of the angel investment market as a competitive environment will lead to a lower level of women’s participation in that market as compared to men.

P1b. The stereotype threat implications of the angel investment market as a competitive environment will be positively associated with women’s membership of women-only angel investment networks.

One important qualification to this competition–performance relationship must be noted (Walton and Cohen, 2007; Walton et al., 2015; Walton and Spencer, 2009). The latent ability effect suggests that in an environment in which stereotype threat has been reduced, members of negatively stereotyped groups outperform non-stereotyped groups at the same level of prior performance (Spencer et al., 2016). Accordingly, the creation of identity-safe environments can reduce stereotype threat, improve performance and unlock previously hidden latent ability (Leitch et al., 2017; Walton et al., 2015). This suggests the following proposition:

P1c. The performance of women angel investors in women-only angel groups will, ceteris paribus, exceed that of those in mixed-gender groups.

Vulnerability: identity consequences

The consequences of stereotype threat extend beyond its effect on performance to the dis-identification and disengagement from the given domain (Spencer et al., 2016). These identity challenges, or ‘belonging uncertainty’ (Hoyt and Murphy, 2016: 390–1), reflect the impact of stereotype threat on fostering negative emotions in the stereotyped domain. This diminishes perceptions of ability, reduces enjoyment and self-confidence while undermining a sense of belonging, motivation and belief in one’s ability to pursue success within the domain. There is substantial evidence that self-efficacy (the perception of one’s ability to complete a task) affects individual motivations and performance and that this can be environmentally specific (Bandura, 1986; Schunk, 1989). As a consequence, the situational salience of a negative stereotype will be manifest in lower levels of self-efficacy (Chung et al., 2010) and hence, in lower levels of entrepreneurial activity (Amatucci and Crawley, 2011; Wilson et al., 2007, 2009). However, the reverse relationship does not appear to hold, and self-efficacy does not mediate the impact of stereotype threat on performance (Mayer and Hanges, 2003; Spencer et al., 1999). This suggests the following proposition:

P2a. Women angel investors in stereotype threat environments will report lower levels of self-confidence and self-efficacy than those in identity-safe environments.

There is, however, a counter-hypothesis based on the argument that women angels are ‘honorary men’ (Harrison and Mason, 2007) and that to succeed in stereotype threat environments, women become more like men (Harrison et al., 2020). As such, they separate their work identity from their gender identity (Von Hippel et al., 2011a) in a process of identity bifurcation (Pronin et al., 2004). This ego protective behaviour can facilitate persistence and motivation in the short term but can also lead eventually to reduced motivation and performance and to eventual disengagement (Hoyt and Murphy, 2016). Accordingly, we propose:

P2b. Women angel investors in stereotype threat environments (mixed-gender angel groups) will not differ from men members in terms of self-confidence and self-efficacy.

Vulnerability: risk consequences

It is widely accepted that less risk-averse individuals are more likely to enter competitive situations and there are gender-based variations in risk attitudes such that women are more risk averse than men (Burow et al., 2017; Klege and Visser, 2020). The extent to which these risk preferences, as opposed to other influences, is disputed in terms of gendered differences in competition willingness (Nelson, 2015; Niederle, 2016; Van Veldhuizen, 2016). In other words, while women in a range of experimental and real-world situations (Adams and Ragunathan, 2019, caution against extrapolation from experimental to real world situations) appear to be more risk averse, this is more a manifestation of social learning than of innate gender traits (Booth et al., 2014; Fine, 2017; Rutterford and Maltby, 2005). There is no agreement on the ontological status of risk as ‘real’ or merely constructed, but there is, however, recognition of the relationship between the awareness of risk and the materialised consequences in the life of the individual (Nygren et al., 2020: 12). From this perspective, gender and risk are mutually constitutive. Gendered knowledge, norms and hierarchies are linked with understandings of what constitutes a risk; the tolerance of risk; the extent to which risk consciousness will be accepted or denied…; and whether risks are to be avoided and feared…[or]…valued as an experience and valorised as an opportunity. (Hannah-Moffat and O’Malley, 2007: 5–6)

P3a. The lower the situational propensity for engaging in risky activity of the woman angel investor, the lower their relative level of participation in the business angel market.

Given that relevant knowledge and experience can mitigate risk, we suggest the following proposition:

P3b. The lower the situational propensity for engaging in risky activity of the woman angel investor, the fewer, smaller and less innovative their investments.

Furthermore, risk propensity is influenced by stereotype threat, suggesting the following:

P4a. Increased stereotype threat will lead to reduced situational propensity for engaging in risky activity and hence to lower relative levels of women’s participation in the risk capital market.

P4b. Increased stereotype threat will lead to reduced situational propensity for engaging in risky activity and hence to higher women’s participation in women-only business angel networks.

In developing these propositions, we recognise that using behaviours (investment characteristics) to indicate attitudes and preferences (situational propensity for engaging in risky activity) is subject to the caveat that these behaviours could be due to a number of other factors, including women having lower amounts of financial capital to invest due to lower earnings/accumulated wealth, less investing experience and less tech company experience due to sectoral demographics. Furthermore, as a reflection of the role of situational cues for stereotype threat, including numerical minority, stereotypical media representations and a general ‘threat in the air’, women angel investors outside of established networks may invest less frequently, or invest smaller amounts. This may reflect the fact that they do not have access to the information that would give them the confidence regarding investment decisions. Writing in the context primarily of experimental work on competition and performance, Niederle and Vesterlund (2011) discuss three elicitation methods for risk preferences: revealing risk preferences from choices (behaviours) made in situations not involving competition; eliciting risk preferences from incentivised lotteries; and drawing on stated risk preferences from a questionnaire. Not every method discloses gender differences, and the explanatory power of risk preferences depends on which elicitation method is used (Niederle, 2016). This points to the importance in future research into attitudes and preferences of adopting a range of quantitative and qualitative methods, not least because the econometric estimation of risk is associated with an underestimation of the influence of risk in much of the literature (Van Veldhuizen, 2016).

Reactance responses

A further consequence of stereotype threat is seen in belonging uncertainty – the sense that women do not belong in a field, a social space and arena for strategic decision-making in which individual agency, through interactions, transactions and events, comes into play (Bourdieu, 1977; Grenfell, 2014). This leads to performance decrements that can accumulate over time and lead to disengagement, reduced aspirations, career attenuation and reduced opportunities to develop skill and experience (Hoyt and Murphy, 2016: 388). Glass ceiling and ‘glass wall’ effects (

Broadbridge and Fielden, 2015; Smith, 1988; Kephart and Schumacher, 2005; Weiler and Bernasek, 2001) are reflected in shorter duration career paths, attenuation of career diversity and skill development and exclusion from networks and groups (Weidenfeller, 2012). More specifically, for women entrepreneurs, the systematic disadvantage of a ‘second glass ceiling’ obstructs them in acquiring certain resources, particularly financial resources required for start-up and growth. This, in turn, reduces the likely exit value of their businesses thereby, reducing their potential to become business angels (Gavara and Zarco, 2015). Accordingly, women investors and would-be investors have shorter (as they are younger) and less diverse career tracks and lower levels of entrepreneurial backgrounds in terms of founder/CEO roles in SMEs in general and of founding scale-up companies that are attractive acquisition targets in particular. For example, one recent UK report suggests that men are five times more likely than women (2.4% of the working age population versus 0.5%) to build a business of over UK£1m annual sales (Rose, 2019), This is reflected in lower investment levels (Table 1). This suggests the following propositions:

P5. Women’s lower social and human capital will increase glass wall/ceiling effects and thereby reduce their relative levels of participation in the angel investment market.

Finally, the stereotype threat literature strongly suggests that women are much more likely to compete in same-sex environments and to compete with themselves over time (Apicella et al., 2017), while no such effects are found for men (Burow et al., 2017). This is reflected in our results in terms of women’s lower likelihood of joining angel networks (Table 2) and lower level of participation in the networks they join (Tables 4 and 8). Specifically, this suggests a homophily effect (McPherson et al., 2001; Reuf et al., 2003): women who join women-only networks appear to invest more than those who join mixed-gender networks and interact more with gatekeepers and other group members.

As women are in different social networks than men and as a result have different access to social capital, their investment activity will differ (Guzman and Kacperczyk, 2019). First, both homophily based on the similarity between individuals ( ‘interpersonal choice homophily’) and ‘induced homophily’, which reflects the likelihood that those in a particular social category will affiliate and form networks, will militate against female participation in largely or exclusively male networks. Second, however, members of underrepresented groups may choose to support each other on the basis of activist choice homophily, that is, where ‘the basis of attraction between two individuals is not merely similarity between them, but rather perceptions of shared structural barriers stemming from a common social identity based on group membership’ (Greenberg and Mollick, 2017). In the context of Figure 1, this suggests the following proposition:

P6. The higher stereotype threat, the greater the likelihood of homophilous behaviour and the more likely membership of women-only business angel networks.

Outcomes of stereotype threat

We identify three sets of outcomes of stereotype threat in the angel investment market, which represent, as it were, the dependent variables in any future analysis. The first and most fundamental of these is the extent to which and in what way women become involved at all as investors in the angel market. The second is in the nature and characteristics of the investments made by women who do participate in the angel investment market as compared with those made by men. The third is the extent to which women join women-only angel investment groups as an alternative to (usually) male-dominated open networks. We therefore develop the following propositions:

P7a. There is a direct positive effect such that higher levels of stereotype threat will be associated with increased membership of women-only networks.

P7b. There is a direct negative effect such that higher levels of stereotype threat will be associated with lower levels of women’s participation in the angel investment market.

4

P7c. As a consequence of stereotype threat, there will be significant differences between the types of investments made by men and women investors.

Responses to stereotype threat

Given the far-reaching potential negative consequences of stereotype threat, ‘finding practical means for individuals to deal with this threat in the air has become a critical issue’ (Spencer et al., 2016: 420). Three sets of response interventions, or modifiers, can be identified; these will affect both the consequences of stereotype threat and the outcomes recorded (Figure 1). First, construal interventions guide stereotype threat targets to reconsider a potentially threatening situation as non-threatening. Second, coping interventions provide targets with a way to cope with the threat. Third, creating identity-safe environments changes the environment to reduce the threat itself.

Construal interventions reduce stereotype threat effects not by objectively changing the situation but by encouraging participants to perceive a lower level of threat (Spencer et al., 2016). While easily done in the experimental situation, for example, by modifying the description of the test, in real-world contexts, this may involve changing participant perceptions of the level of threat. This may be by having them reinterpret their experience (Johns et al., 2008) or reconsider the threatened identity by a reminder of characteristics shared with the non-threatened group and the multiple roles and identities comprising their self-identity (Gresky et al., 2005; Rosenthal et al., 2007). There is evidence that individual responses to stereotype threat, and to the threat to their identity that this represents, is determined in part by their mindsets, that is, the lay theories they hold regarding the extent to which they believe their characteristics are malleable (growth mindset) or stable (fixed mindset) (Hoyt and Murphy, 2016: 392). For instance, one study has shown that experimentally manipulating beliefs that entrepreneurial ability can be increased ‘led women to show greater resilience, in the form of greater self-efficacy for future entrepreneurial endeavours, in the face of stereotype threat relative to those induced to believe in the fixed nature of entrepreneurial ability (Pollack et al., 2012)’ (Hoyt and Murphy, 2016: 392).

Coping interventions do not modify the overall high level of threat but reduce or eliminate its’ effect on performance and hence, outcomes in our formulation. These interventions include educating participants about stereotype threat, providing reassurance that the stereotype is illegitimate. This can be reinforced by self-affirmation, and specifically by encouraging participants to affirm an important value or self-attribute before undertaking the task, thereby restoring self-integrity and enhancing performance (Martens et al., 2006; Steele, 1988). There are, however, some limitations to the effectiveness of these interventions, not least because stereotype threat tends to have the most deleterious effects on those for whom the stereotype is most self-relevant and on those who are most motivated to perform well (Gupta and Bhawe, 2007; Hoyt and Murphy, 2016: 393).

Both reconstrual and coping interventions, which in intervening with the target are successful in reducing or eliminating performance decrements, further require creating identity-safe environments. In this context, identity safety involves removing the ‘threat in the air’ from previously threatening situations and removing the risk of being reduced to a negative stereotype targeting a social identity (Spencer et al., 2016: 427). Identity-safe environments challenge the ‘validity, relevance, or acceptance of negative stereotypes linked to stigmatized social identities’ (Davies et al., 2005: 278). This may involve at the individual level reassurance to threat-subject individuals that their stigmatised social identities are not a barrier to success in the targeted domain (Davies et al., 2005). It may also involve interpersonal interventions such as encouraging positive contact with members of the majority group (Walton et al., 2004) and using members of the targeted group as role models of successful group members (Shaffer et al., 2013). However, the effect of role models is potentially contradictory (Hoyt and Murphy, 2016). On the one hand, they demonstrate that success in the stereotyped domain is attainable and this can increase a sense of social belonging and inoculate against identity threats. On the other hand, role models can be self-deflating by highlighting how deficient one is in comparison, especially if the role model is an exceptional high-achiever. To be effective, role models need to be such that women can identify with them and believe that their success is attainable (Hoyt and Simon, 2011; Von Hippel et al., 2011b).

There is an argument that women-only entrepreneurship networks in general lead to the creation of ‘gendered niches’, making more difficult the legitimisation of women’s entrepreneurial activities in a stereotype threat environment (Harrison et al., 2020). However, in the specific context of women’s angel investing experience, reconstrual interventions, coping interventions and the creation of identity-safe environments all point to the development of women-only angel networks as an education, self-affirmation and self-attribute-enhancing environment which is identity-safe and supportive, and within which effective role models of ‘women like me’ can be developed and promoted (Coleman and Robb, 2019; GoBeyond, 2019).

Discussion and implications

Based on our exploratory analysis of the attitudes, characteristics and behaviour of women angel investors in the United Kingdom, we have proposed a stereotype threat theory of women angel investing based on understanding the cues, consequences, outcomes and responses to stereotype threat. In summary, we highlight the following features of the theory (Pennington et al., 2016). First, stereotype threat is a form of social identity threat where individuals perceive their social group to be devalued or stigmatised by others (Brown and Pinel, 2003). Second, stereotype threat is more likely to be elicited in tasks of high difficulty and demand, although there will be differences in individual perceptions of the extent to which a task is demanding (Iriberri and Rey-Biel, 2019; Nguyen and Ryan, 2008). Third, from a multi-threat perspective (Shapiro and Neuberg, 2007), we can distinguish between the target of the threat (one’s personal or social identity) and the source of threat (is it the in-group or out-group that judges performance?). While much of the stereotype threat literature has assumed that it is a singular construct experienced in a similar way by individuals and groups across situations, this overlooks the possibility of multiple forms of and responses to stereotype threats. These may be implicated in threats to an individual’s personal or social identity in situations where the performance of individuals may be, in their own perception, indicative of personal ability (Shapiro and Neuberg, 2007). Fourth, subtle cues in the environment, rather than explicit stereotype activation, can trigger stereotype threat and therefore, performance expectancies may be undermined when, as would be the case in angel investment decision-making within an angel group, stigmatised in-group members are required to perform a stereotype-relevant task in front of out-group members (Sekaquaptewa and Thompson, 2003; Stone and McWhinnie, 2008).

Given the evidence that women’s performance can be hampered by an implicit stereotype threat (Pavlova et al., 2014) and that in the angel investing context individuals experience a self-as-target threat from out-group (male) judges stereotype-consistent behaviour will be viewed as self-characteristic (Pennington et al., 2016: 3). The response, for at least some women, will be where possible to withdraw into non-threatening gendered niche environments such as women-only networks and groups (Harrison et al., 2020; McAdam et al., 2019). Although based on a small sample, our results are consistent with stereotype threat and suggest that members of women-only networks have less board-level experience, are more risk averse, are more open to the opinion of others and have made more investments than women members of mixed-gender groups. Based on the empirical analysis and theoretical model presented in this article, we can identify two broad sets of immediate implications from this research.

Angel characteristics and behaviour

Contrary to previous research which identified no significant differences between women and men angel investors, this study has identified significant differences in background, experience and behaviour. This suggests that the woman business angel population is a dual population. On the one hand are the ‘women angels as honorary men’ (Harrison and Mason, 2007), who are members of male-dominated business angel networks, share many of their characteristics and pattern their investment behaviour on their male counterparts, while being subject to the pressures of competition and stereotype threat (Idi Cheffou and Bellier, 2017). On the other hand are women who have recently entered the angel market, who are more likely to join women-only angel groups to reflect their characteristics and preferences, receive training and education, and avoid the competition and stereotype threat characteristic of male-dominated networks. This has implications for both research and practice, as the assumed homogeneous category of ‘women business angel’ is replaced by a more nuanced understanding of a structural dualism in the market. Given that, from a stereotype threat perspective, behaviour is influenced by social and cultural norms, to some extent, women will adopt the behaviours that they feel will help them succeed. Alternatively, behaviour can be influenced by an individual’s self-confidence, self-efficacy and belief in her ability to achieve her goals. Women who are more confident in their investing knowledge, skills and networks may be prepared to break new ground and engage in counter-stereotypical behaviour (Hoyt and Murphy, 2016).

As woman angel investing continues to grow, different types of investor backgrounds bring different challenges for researchers and raise new research questions. Five in particular can be highlighted. First, what are the implications for the value-added contribution of these ‘new’ angel investors, given their relative lack of direct entrepreneurial experience? Will these new business angels be able or willing to play an active value-adding hands-on role in their investee companies, and if so will this be a different type of relationship based on providing a different type of support, or will we see a rise in passive investment, and if so, with what consequences? Leveraging additional capital into the early stage risk capital market, notably by attracting more women angel investors, is not necessarily the same as attracting additional expertise, but more research needs to be undertaken on whether and the extent to which women angel investors are more passive and less involved in their portfolio companies than are men. If this is found to be the case, this suggests that the same stereotype threat theory factors that prevent women from becoming angel investors also discourage them from participating fully when they are angel investors. Second, is the role of homophily, albeit relatively weakly demonstrated in this study, likely to drive the emerging phenomenon of women investing in women, and if so how will this change our understanding of women’s access to capital (Poczter and Shapsis, 2018) and the dynamics of the investor-investee relationship? Third, to what extent will we see further differentiation within the women angel population emerging to reflect the heterogeneity already being observed in the population of men angels (Avdietchikova, 2008; Lahti, 2011)? Fourth, what are the wider implications of the changing demographics of the women angel population? We know that people with inherited wealth rarely, if ever, become angels as they appear not have the self-efficacy or networks to enable them to become angels. To what extent can recent initiatives designed to rectify this (such as GoBeyond, and the Rising Tide programme – Coleman and Robb, 2017, 2018) successfully expand the angel market? The potential and impact of such developments remains an important issue for future research. Finally, given the evidence that women angels are much less likely than men to lead in investment deals (British Business Bank, 2018), how, if at all, does the interaction between women angel investors and their investee businesses differ between women in mixed-angel groups and women in women-only groups, and what are the implications for the development of the angel investment market?

Public policy and entrepreneurial practice

Our evidence that the angel capital market, and women’s participation in it, is to some extent characterised by the existence and consequences of competition and stereotype threat has potentially wide-ranging implications in terms of public policy and entrepreneurial practice. The emerging heterogeneity of the women’s angel market we have demonstrated suggests that different kinds of support are needed. This might include support for the development of woman-only angel networks, and initiatives to mitigate or overcome the role of risk aversion, homophily, competition and performance and glass walls in constraining the potential of women angel investing. In terms of entrepreneurial practice, our findings, and the evidence from the analysis of specific women-only investment networks (Coleman and Robb, 2018; Go Beyond, 2017), strongly support the case for the establishment of women-only networks, in terms of providing legitimacy, a ‘safe space’ (Leitch et al., 2017) for networking and learning and support (from gatekeepers and other investors). This has the potential to address three constraints on the expansion of the participation of women in the angel market (EBAN, 2010): attitudes and mindsets; lack of awareness; and current market offerings.

In terms of attitudes and mindsets, women tend to underestimate their capacity to make ‘risky’ investments. In the absence of role models, they may have less understanding of the calculus of business angel investing, may be constrained by the conflict between the time demands of managing the domestic economy and their own careers and those of proactive angel investing and are discouraged through homophily and stereotype threat effects by the stereotypical image of the angel investor as a late middle-aged male ex-entrepreneur. This is at odds with self-perception of their skills and experience. In terms of lack of awareness, fewer women entrepreneurs have raised equity investment for their businesses, and so fewer have exited and become business angels; as such, there does not yet exist, apart from a few notable exceptions, a cohort of women business angels who discuss their angel investment activity in their professional and social networks. This is reinforced by evidence that historically women have been less likely than men to belong to professional, alumni, private and other networks (Harrison et al., 2020) and thus, are less likely to have been networked with other angel investors.

Given that the profile of most business angel network members is male, the services offered and the way they are delivered reflects this male audience. Furthermore, given that most network managers are also male and that ‘over 28% of BANs [in Europe]…having no women members in 2009, it is a confident woman who is prepared to join an all-male network as a novice investor’ (EBAN, 2010: 5). Finally, in terms of current market offerings, the modus operandi and services offered by existing business angel networks have evolved to meet the needs of their predominantly male clientele. This reflects aspects such as deal flow, meeting schedules and learning and development opportunities whereby women investors and potential investors may prefer structured training rather than a more ad hoc learning by doing (Botelho et al., 2018; Coleman and Robb, 2018), and support (Benko and Pelster, 2013).

Conclusion

We began this article by asking four research questions (Tenca et al., 2018): is the profile of women angel investors different from that of men? Is their investment behaviour different? Do women angels invest in different types of businesses? Do women angel investors joining women-only angel groups differ from those joining mixed-gender groups? In each case, our answer is a qualified ‘yes’, but we recognise the need for more extensive and detailed research on each of these issues. We have examined the extent to which entrepreneurial action – in this case women angel investing – is gendered by design, delivery and impact, with women participating, if at all, on terms established by the prevailing male hegemony and dominated by stereotype threat and its consequences. Based on this exploratory study of women angel investors in the United Kingdom, we have developed a novel approach to the analysis of women angel investment based on stereotype threat theory and its implications for competition and performance in stereotypically male tasks. This identifies the sources of or cues for stereotype threat, in terms of cultural (masculinised, media images, the ‘threat in the air’) and structural (competition, numerical minority, skills and abilities variation) conditions. We have argued that stereotype threat has consequences, particularly in depressing performance in the stereotyped group. These consequences in turn shape the outcomes of stereotype threat in terms of women’s decision to become involved in the angel investment market, how they participate in that market, the types of ventures in which they invest and their membership of women-only and other angel groups and networks.

Our analysis is limited by the small number of women respondents (reflecting the ‘rarity’ of the phenomenon) and our conclusions are necessarily provisional pending further detailed research. However, policies and initiatives designed to encourage and support women’s entrepreneurship, including the establishment of women’s business angel networks, appear to have a justification in addressing stereotype threat, attitudes and mindsets, lack of awareness and the gendered structuring of current market offerings (Pettersson et al., 2017). This leaves a wide and diverse research agenda, to which this article is a partial response. This agenda includes significant gaps in our knowledge of the following key issues (Tenca et al., 2018: 20): the factors underlying the underrepresentation of women angel investors in the market; the human capital characteristics of women angels and their impact on investment behaviour; the extent to which women angels have different mental constructs to evaluate deals, to take funding decisions and to manage capital and post-investment relationships; and the role of women-only angel groups in facilitating the matching between entrepreneurs and women business angels, shaping the relationship between angels and venture capitalists (VCs), and affecting the group thinking behaviour of investors.

Our evidence from the discussion of women-only business angel networks in particular confirms the findings from wider analyses of the development of women’s social capital. For some, what Fels (2004) sees as a problem – the lack of ambition and the ‘gender recognition differential’ – is the basis for an alternative approach based on the development of a more cooperative way of working and sharing recognition through an emphasis on women’s relationality and connectedness (Gilligan, 1982). There is wider evidence to suggest that gender and network roles are related in the development of social capital: networks with a high percentage of women members, such as women-only business angel networks, are more likely to provide support to other members. As Wellman and Frank (2001) express it, ‘it appears that a high percentage of women in a network potentiates the entire network to be more supportive. Or, perhaps egos at the centre of such networks have consciously organized their networks to provide more support’ (p. 252). Furthermore, there is evidence to support an empirical generalisation that ‘women express, men repress’: in other words, women interact in networks face to face by exchanging emotional support, while men interact side by side by exchanging goods and services (Moore, 1990; Perlman and Fehr, 1987). This general argument, and our specific albeit limited evidence, suggests that the reliance in the entrepreneurship literature on the maleness of reason (Bordo, 1987; Lloyd, 1984), that is, the experience of men of themselves as isolated rational egos reflecting from an objective standpoint a world of alien material fact, is limiting. Accordingly, ‘as the incidence of men in governing positions becomes less ubiquitous, and the authority of women grows, is it not time to turn our backs on men’s archaic metaphors and replace them with a new feminization of reason?’ (Broad et al., 2006: 105). Taking these observations on stereotype threat, competition, ambition and network roles and behaviours together provides a framework for the repositioning of gendered entrepreneurship research in general and business angel research in particular, which goes beyond simply using gender as another factor or variable to be included in a research design.