Abstract

Besides the extraordinary impact of Business Angels (BAs) as the leading contributors to fund entrepreneurship at the early stage, the value BAs perceive from their investment activity has not yet been fully explored. Based on a new holistic perspective resulting from marketing and consumer behaviour, this article builds on the concept of perceived investment value to create a new instrument that measures the overall value perceived by BAs in their investing activity. Data were collected through a survey questionnaire with 849 BAs from 79 countries. The instrument created was tested through Structural Equation Modelling. The results reveal that: (i) BAs are not purely financial investors and expect more than just money from their activity, as self-esteem, entrepreneurship, emotion and altruism are the main dimensions that explain angel perceived investment value (APIV), with economic and functional dimensions being the least influential; (ii) APIV positively influences their job satisfaction; and (iii) angels satisfied with their jobs are more likely to reinvest their money and engage in positive word-of-mouth. A multigroup comparison was implemented, validating the results for males and females, novices and veterans and light and heavy investors.

Keywords

Introduction

Business angels (BAs) play a crucial role in providing funding to companies during their early stages. Despite three decades of research on BAs, studies examining how their goals and motivations influence their investment decisions are scarce (Croce et al., 2020). Existing studies lack common ground, are fragmented and need further investigation (Taylor, 2019). Moreover, despite the growing interest in identifying distinct BA profiles over time (e.g., Morrissette, 2007; Tenca et al., 2018), there is not enough research to fully understand their motivations or the value they perceive from their investments.

BAs are a special kind of investor who invest their own money in startups they are involved with (Avdeitchikova et al., 2008; Mason, 2008). They differ from other investors, such as crowdfunders, stock investors or venture capitalists, as they invest their personal funds without agents or intermediaries (Wesemann and Antretter, 2022). Simmilarly, unlike passive stock exchange investors, BAs prefer to be actively involved with the startups they invest in (Murnieks et al., 2015; White and Dumay, 2020), aiming to create value and contribute to the success of the business. Furthermore, some consider their entrepreneurial involvement to be an essential element of the BA definition (Avdeitchikova et al., 2008; Lahti, 2011).

Perceived customer value, a central concept in marketing and strategy (Khalifa, 2004; Smith and Colgate, 2007), is defined as the utilitarian perception of “what I get for the price I pay” (Zeithaml, 1988: 13). It represents the consumer's overall assessment of the utility derived from a good/service based on their perception of the trade-off between the benefits received versus the cost and sacrifices involved. It reflects the interaction between the customer, with its hierarchy of goals and purposes, and the product or service, with its attributes and performances (Holt and Payne, 2001). Perceived customer value has generated significant interest in academia and industry (Sánchez-Fernández and Iniesta-Bonillo, 2007) and has been extensively applied in different industries, namely in online shopping (Bonsón Ponte et al., 2015), online services (Yang and Peterson, 2004) and stock market investments (Puustinen et al., 2013; Wang, 2015), but not yet in the BAs context. As BAs can be regarded as consumers of financial products or services — undertaking actions (investments and interactions with entrepreneurs and other angels) that involve the experiential hedonic aspects of entertainment, status, and personal symbolic meanings — just like the consumers of goods and services in retail, it is possible to argue that consumers and investors can be viewed as actors and players in a game (consuming or investing) according to specific rules to obtain desired value compensations (Allen and McGoun, 2001).

Based on: (a) Rintamäki and Kirves’ (2017) integrative framework that encompasses four dimensions of perceived value (economic, functional, emotional and symbolic); (b) Puustinen et al.'s (2012, 2013) perceived investment value (PIV) scale, applied specifically to the stock exchange market; and (c) the substantial differences between BAs, stock investors and venture capitalists (Lefebvre et al., 2022), this paper addresses the gap in understanding the perceived value of BAs. Specifically, it aims to answer the question of why BAs decide to invest their money and time in risky startups, popularised by the expression “what's in that for me?” As such, this paper aims to extend the research on PIV by proposing a new instrument — the angel-perceived investment value scale (APIV) — to assess the value perceived by BAs in their investing activity. This article goes beyond the purely financial ties linking BAs to their activity. By employing a human-centred approach, the article introduces a six-dimensional model — economic, functional, emotional, self-esteem, altruistic, and entrepreneurial — to test and validate the APIV.

After this introduction, the literature review presents the six dimensions comprising the APIV scale. Then, the methodology employed is outlined. Finally, the results are shown, followed by the discussion and conclusions.

Literature review

The concept of angel perceived investment value (APIV)

BAs are different from other investors as they are capable of assuming higher risks, making quicker decisions, and conducting lighter due diligences compared to venture capitalists, who are accountable to fiduciary responsibilities and must justify business failures to their investors (Van Osnabrugge, 2000). Furthermore, compared to passive stock exchange investors, BAs prefer to be actively involved with the startups they invest in (Murnieks et al., 2015; White and Dumay, 2020). Their aim is to create value and contribute to the success of the business, emphasising the entrepreneurial engagement of BAs in their core angel activities. Consequently, APIV can be defined as the holistic perception of value in angel investing, encompassing economic, functional, emotional, symbolic (esteem and altruism) and entrepreneurial aspects.

Economic APIV

Economic APIV refers to the perceived economic value BAs obtain as the result of investing money in a start-up or angel fund, with the expectation of financial/economic gain upon a liquidity event. BAs typically invest in the form of equity finance to achieve significant financial returns through an exit strategy (Mason et al., 2022). Financial return is considered by many, if not the sole motivation for investing (Morrissette, 2007), its major driver and foremost reason (Botelho et al., 2021; Croce et al., 2020). Angels perceive investing in startups as a way to make money that will exceed the returns obtained from alternative investment forms (Shane, 2005; Vroomen and Desa, 2018). The high expectations BAs have for startup gains may be the result of angels being prototypically cashed-out entrepreneurs (Riding, 2008) who obtained their wealth through one or more successful exits with high capital returns. Statistically, more than 50% of the investments may result in a partial or complete loss (McKaskill, 2009), but approximately 9% of startups generate returns more than 10 times the initial investment, compensating for the losses incurred by failed startups (Wiltbank and Boeker, 2007; Wiltbank et al., 2009).

Functional APIV

Following Puustinen et al. (2013), functional APIV is the perceived value derived from the convenience and proper outcomes of angel investing activity. Service convenience is defined as “a judgment made by consumers according to their sense of control over the management, utilisation, and conversion of their time and effort in achieving their goals associated with access to and use of the service” (Farquhar and Rowley, 2009: 434). Convenience captures the extrinsic utilitarian value resulting from the activity as a means to achieve some self-oriented purpose (Holbrook, 1999), such as time and effort savings (Rintamäki et al., 2006). Besides the economic outcome, investing in startups holds utilitarian value in maintaining an indirect entrepreneurial activity without the enormous time and energy needed to start and successfully manage a business from scratch (Shane, 2009). As one BA once said, “They [BAs] want to stay in the game, but not stay up to 2 A.M. anymore” (Hill and Power, 2002: 37). After working hard as entrepreneurs in their own companies, BAs seek to preserve the entrepreneurial spirit without the responsibilities or the demanding workload of working 60 h or more per week (Rose, 2014).

BAs primarily invest in startups close to their homes (Morrissette, 2007; Shane, 2005). The rationale behind this preference is that proximity reduces travel time and allows more opportunities for mentoring (Morrissette, 2007; Politis, 2008; Shane, 2005). In recent years, the digitalisation and re-organisation of angel investing have brought about changes in the way angels make their investments (Mason et al., 2019) facilitating access to a greater quantity and diversity of investment opportunities (Pierrakis, 2019; Wesemann and Antretter, 2022). Through structured investing platforms, angels can easily co-invest with others and build portfolios to achieve diversification and potentially higher performance (Antretter et al., 2020).

Emotional APIV

Emotional APIV is the perceived value derived from the positive emotional experiences or affective states generated by the act of investing as an angel investor. Emotional value encompasses the psychological benefits stemming from positive emotions and experiences related to consumption and investment, such as pleasure, enjoyment, entertainment, passion, exploration, fantasies, feelings and fun (Croce et al., 2020; Puustinen et al., 2013).

Besides trading for saving, risk management and speculation, some investors trade simply because they find it entertaining. In a subconscious demand for arousal, sensation-seeking BAs prioritise the intensity and novelty of the angel experience (Zuckerman and Aluja, 2015) and the excitement of playing the startup game (Croce et al., 2020), rather than solely focusing on money (Dorn et al., 2008; Dorn and Sengmueller, 2009). Literature suggests that angel investment is primarily driven by passion, enjoyment, and pleasure (Pierrakis, 2019; Rose, 2014; Taylor, 2019). Angel investing is an enjoyable activity (McKaskill, 2009), involving collaboration with entrepreneurs who value experienced investors and appreciate their contributions (Benjamin and Margulis, 2005). Unlike venture capitalists, who view financial rewards as their only incentive (Ibrahim, 2008), BAs develop emotional attachments to entrepreneurs and start-ups, which alters their risk perception (Franić and Drnovšek, 2019). Some BAs invest only purely for emotional fulfilment, seeking fun and pleasure (Ramadani, 2009), considering that investing is more intellectually stimulating and exciting than other hobbies (Freear et al., 2002). Moreover, BA activity is seen as “cheaper and more fun than buying a yacht” (van Osnabrugge and Robinson, 2000: 117) and “more fun than reading books or playing golf” (Shane, 2009: 26). Positive emotional experiences reduce the perception of risk, whereas negative emotional experiences tend to have the opposite effect (Chaudhuri, 2006; Taylor, 2019).

Symbolic APIV

Symbolic APIV is the perceived symbolic value resulting from angel investment activity, encompassing both esteem and altruism, and gaining meaning through personal transformations or social contexts.

Symbolic self-esteem APIV

Based on symbolic interactionist theory, individuals behave and interact with others governed by their self-conception, which needs validation in the eyes of others (Turner, 2012). When individuals receive positive feedback from others, their identity is affirmed, self-esteem is enhanced, and self-meanings are reinforced and internalised (Burke and Reitzes, 1991), becoming an essential part of oneself (Croce et al., 2020). Increased self-esteem is associated with self-development and improvement goals related to fulfilling personal advancement and professional growth (Franić and Drnovšek, 2019; Irving and Williams, 1999).

The literature suggests that BAs invest to cause a positive impression and enhance their reputation by associating themselves with successful investors and startups (Ramadani, 2009). Successful investments improve self-image and self-esteem (Benjamin and Margulis, 2005; Duxbury et al., 1996). Learning and self-development are significant motivating factors for BAs, as they awaken the angel identity and are positively associated with investment frequency and follow-on investments (Preston, 2004).

Symbolic altruism APIV

Using time and money to benefit others leads to higher levels of happiness (Aknin et al., 2013). In the context of APIV, altruism corresponds to positive feelings of benevolence in social contexts, understood as BAs’ genuine human concerns for people's well-being for their own sake (Blum, 2015; Khalil, 2004).

The literature suggests that many BAs feel an altruistic call: (i) to transfer their time, money and experience to help emergent entrepreneurs make their dreams come true (Ramadani, 2009); (ii) to help entrepreneurs avoid repeating the same mistakes they (BAs) already made (Ramadani, 2009); (iii) to assist less experienced BAs to become more investor-ready (Paul et al., 2003); (iv) to give back to the entrepreneurial community that made them wealthy (Ibrahim, 2008); and (v) to create local jobs and stimulate the local economy (Shane, 2009).

Sullivan and Miller (1996) segmented BAs according to their economic, hedonistic, and altruistic motivations. When motivated by feelings of altruism, BAs are more resilient and able to hold their investments for longer periods (McKaskill, 2009; Zacharakis and Shepherd, 2007) and stay longer with an underperforming startup than venture capitalists (Mason and Harrison, 2002). Investors may behave altruistically when investing their own money, time and credibility in the entrepreneurs before anyone else, often from scratch, when the start-up is in a pre-revenue phase, just because they feel good about contributing (intrinsic enjoyment) (Miller et al., 2019). Hill and Power (2002) argue that BAs feel fulfilled and live with a higher purpose when supporting entrepreneurship.

Entrepreneurial APIV

Entrepreneurial APIV is the perceived value obtained from involvement with entrepreneurship per se. David Rose, the founder of New York Angels, confirms BAs’ commitment and devotion to the entrepreneurial cause arguing that BAs are “…often strong believers in the ethos of entrepreneurship, excited by the prospect of supporting small companies that they believe may one day transform some segment of the business world, spurring economic growth for the benefit of millions” (Rose, 2014: 28). This entrepreneurial need may be understood as a result of the angels’ entrepreneurial career (Politis and Landstrom, 2002).

A BA's fortune is often the result of a successful and passionate entrepreneurial career that provides a considerable amount of human capital that can be used in favor of entrepreneurship (Fili, 2014). A substantial number of BAs view themselves as entrepreneurs, “co-creators” and “co-founders” of new ventures, rather than purely financial investors perpetuating the ethos of entrepreneurship (Fili and Grünberg, 2016). Research sustains the existence of similarities between BAs and entrepreneurs concerning their entrepreneurial behaviour. Both groups actively search for new business opportunities, look for innovative solutions, exhibit a high degree of risk-taking behaviour, manage resources and add value (Filion, 2011; Lindsay and Craig, 2002; Politis, 2008).

The relation between APIV, angel job satisfaction, word-of-mouth, and reinvestment intention

According to Puustinen et al. (2012, 2013), PIV can be considered a cognitive-based construct that captures the value obtained from the perceived benefits and sacrifices that are part of an (angel) investor's activity. Job satisfaction is essentially an emotional-affective consequence of how people feel about their job (Aziri, 2011; Spector, 1985). Moreover, the perceived value reflects a pre- or post-evaluation phenomenon or both, while satisfaction is only a post-evaluation outcome that requires a personal experience (Caruana et al., 2001; Tam, 2004). In the BA investment context, APIV can be measured at any stage of the investment process, including the pre-investment phase. In contrast, angel job satisfaction can be considered an evaluation of the overall experience of the angel investment activity.

There are positive correlations between perceived value and satisfaction in several areas, including retail (Rintamäki and Kirves, 2017), real estate (Shim et al., 2008) and stock investment (Puustinen, 2012; Puustinen et al., 2013). Perceived value is considered the most complete explanatory antecedent of global satisfaction (Babin and Kim, 2001; Gallarza et al., 2011).

In the early years of angel activity, the angel occupation was considered a “nice hobby” for wealthy managers and successful entrepreneurs (Hill and Power, 2002; Van Osnabrugge and Robinson, 2000). Politis and Landstrom (2002) introduced its perception as a career, arguing that angel activity is a natural step in the “entrepreneurial career”, even if the great majority of BAs maintain other occupations to reconcile with their angel activity (José et al., 2005).

By definition, a BA is actively involved in pre- and post-investment tasks (Fili and Grünberg, 2016; Politis, 2008). The classical BA role, either as a full-time job or as a recreational hobby, is to provide “smart money” to investee startups (Avdeitchikova, 2008). This task implies close involvement with a substantial amount of work and “hands-on” assistance (Madill et al., 2005). According to Marcus (2017), it is the capacity to experience the job as a pleasurable activity that gives the basis for a high degree of job satisfaction, creating a good fit between the person and the occupation. Although Puustinen et al. (2013) found that PIV positively impacts job satisfaction, there is no such evidence in the context of BAs. Nevertheless, it is reasonable to anticipate that the perception of the value of BAs is positively related to angel job satisfaction. Therefore, the following hypothesis is proposed:

Previous studies in various contexts, such as banking services (de Matos et al., 2013), clothing shopping (Menidjel et al., 2020) and tourism (Caber et al., 2020) provide evidence that customer satisfaction positively influences word-of-mouth and repurchase intention. These studies suggest that highly satisfied customers are more likely to recommend and repurchase goods and services compared to less satisfied customers. However, despite the recognised positive impact of satisfaction on word-of-mouth, this relationship has been largely overlooked in the context of angel investing. Furthermore, word-of-mouth information sharing is known to reduce information costs (Baker and Ricciardi, 2014) and plays a crucial role in angel investing, as most angels are primarily introduced to investment opportunities through referrals from entrepreneurs and other investors (Benjamin and Margulis, 2005). The European Business Angels Network (EBAN) (2018) asserts that word-of-mouth is vital for identifying investment opportunities, finding co-investors and recruiting new members to angel groups and networks. Successful BAs and well-developed networks enhance their entrepreneurial commitments and reputation through positive word-of-mouth (Politis and Landstrom, 2002). Additionally, the tacit endorsement and word-of-mouth of BAs serve as precious assets for entrepreneurs seeking investment investment (Hill and Power, 2002). Moreover, BAs are partial owners of startups in which they invest. Research supports the idea that ownership fosters self-enhancement motivation, which is positively associated with intentions to engage in positive word-of-mouth (Kirk et al., 2015).

Although no studies have specifically examined the impact of satisfaction on BAs’ reinvestment intentions, evidence from the investment context suggests that investor satisfaction contributes to reinvestment decisions. For example, Baharun et al. (2014) observe that satisfaction with mutual funds has a positive effect on purchase intention. Similarly, Prathiba (2018) highlights that satisfaction with returns, risk and wealth accumulation positively influence reinvestment intention in mutual funds. In the real estate industry, Shim et al. (2008) found that satisfaction with investments, including satisfaction with profitability, security and liquidity, positively influence reinvestment intention. Similar findings were reported by Pandey and Jessica (2019), who reveal that satisfaction with investments, specifically with return rates and the overall real estate investment experience, boosts reinvestment intention.

Based on the literature reviewed, it is reasonable to expect that BAs satisfied with their investment activity are more likely to engage in positive word-of-mouth and reinvestment. Thus, the following hypotheses are proposed:

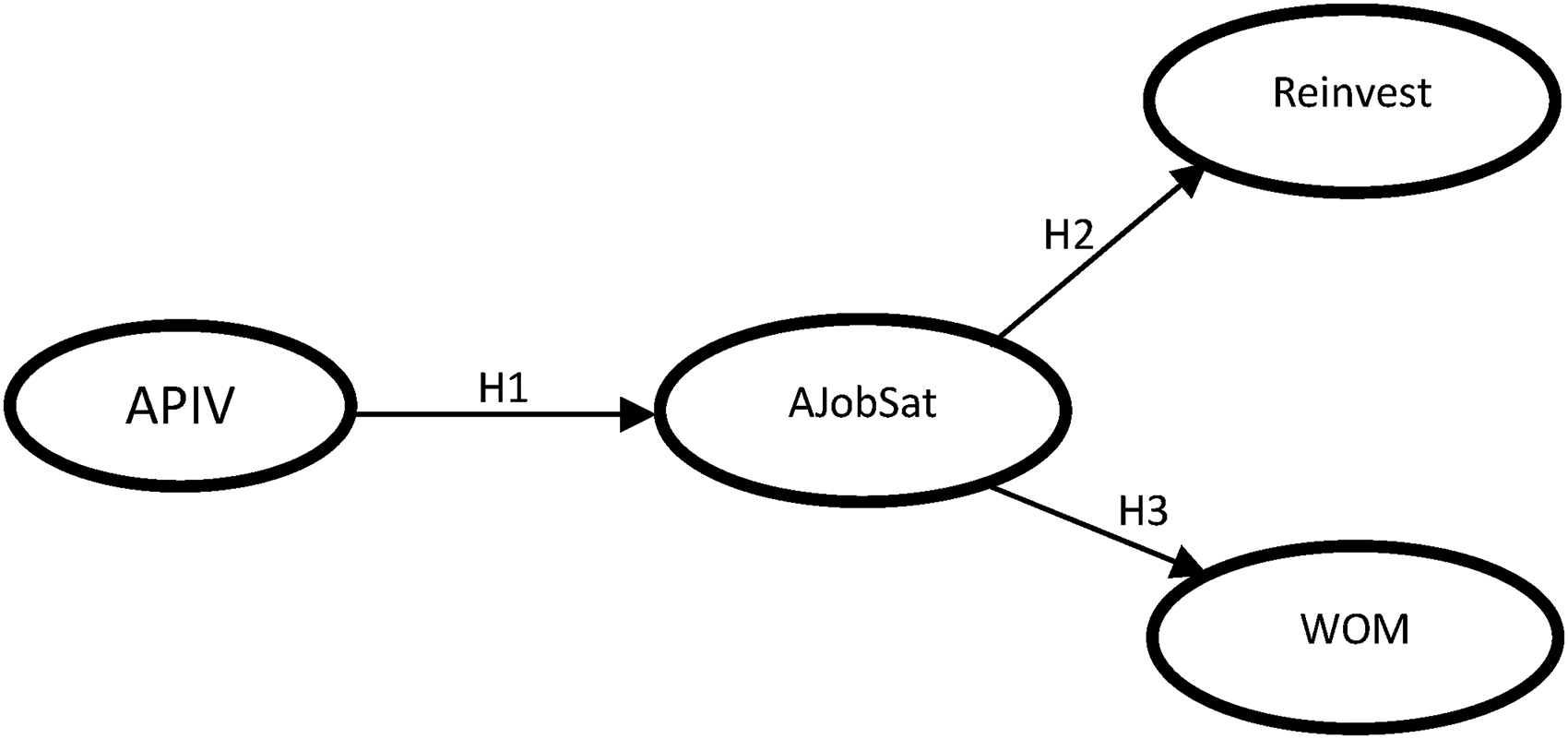

Figure 1 presents the conceptual model proposed in this paper and its underlying hypotheses.

Research methods

This paper follows the procedure used by Puustinen (2012), adapting the PIV concept employed in stock contexts (Puustinen et al., 2012, 2013) as a foundation for extending it to the field of BAs and proposing the APIV framework.

Conceptual model and hypotheses.

To reach a wide range of BAs in several countries, an online questionnaire was developed. A database of BAs was compiled using the following sources: (i) the Portuguese Federation of Business Angels (FNABA) database, an affiliate of the European Business Angels Network (EBAN); (ii) the IAPMEI — Certified Business Angels investing in Portugal database; and (iii) one of the authors’ personal database, which comprises connections to over 20,000 BAs worldwide via LinkedIn. The World Business Angels Forum (WBAF) provided support by distributing the survey to its members.

The questionnaire included items designed to measure APIV, job satisfaction, reinvestment intention, WOM and sociodemographic profiles of BAs.

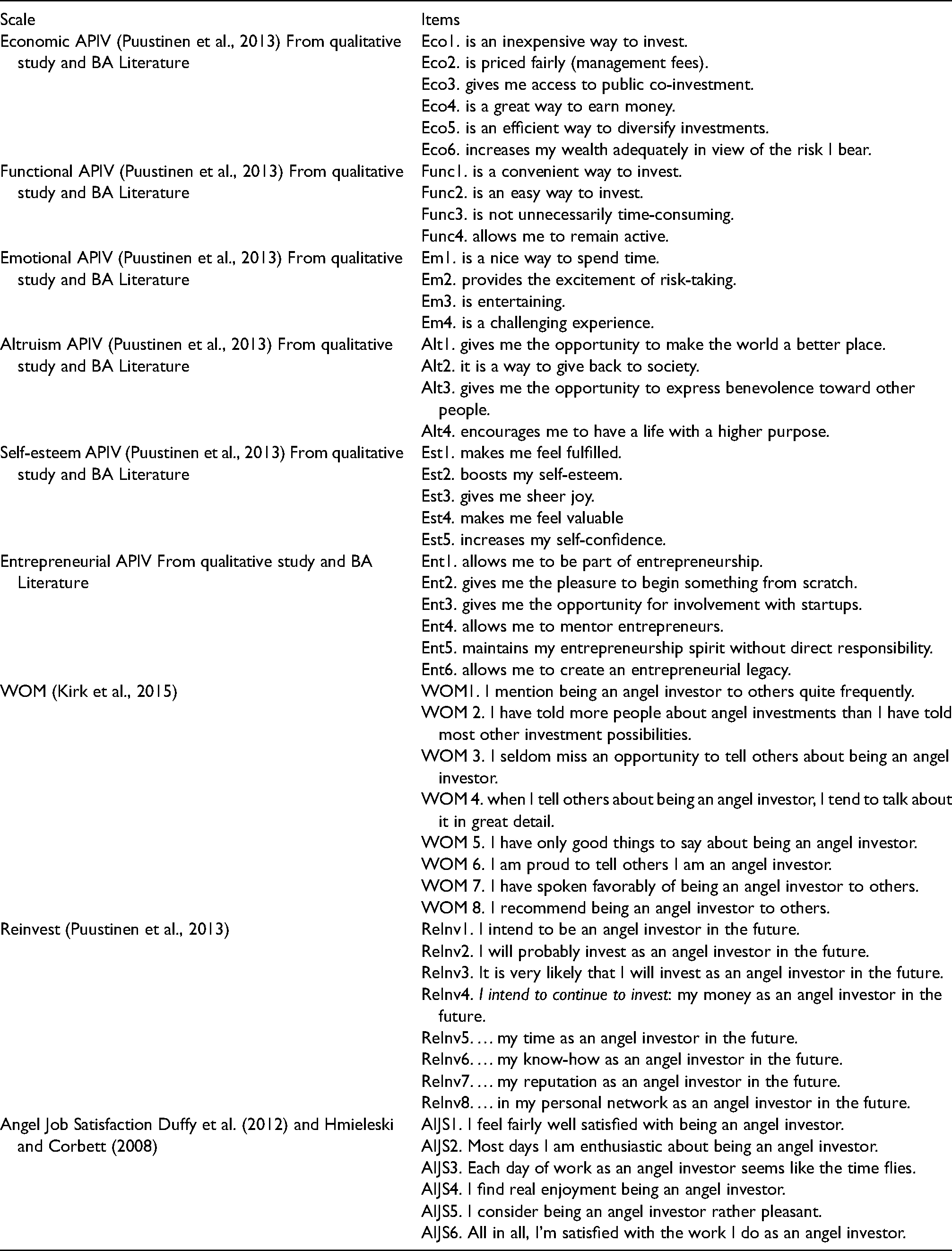

The operationalisation of APIV was grounded on three pillars: (i) the PIV instrument (Puustinen et al., 2013), adapted from marketing and retail to the context of stock exchange investment; (ii) a previous qualitative study on BAs by the authors that uncovered forty angel meta-goals (Falcão et al., 2023); and (iii) validation of item relevance by an external expert advisor and the President of FNABA. The qualitative study applied the laddering technique (Reynolds and Gutman, 1988) and the means-end chain model (Gutman, 1982) to 53 BAs and 35 entrepreneurs to uncover 883 goals for angel investment. The goals identified in that study were categorised into 40 meta-goals that represent the dimensions of the six goals discussed in the literature review here (Falcão et al., 2023): economic, functional, emotional, self-esteem, altruistic and entrepreneurial values. The APIV scale included in the questionnaire encompasses a set of 29 items, reflecting the six APIVs discussed in the literature review (see Appendix A).

The job satisfaction scale used in this study was based on Duffy et al. (2012) and Hmieleski and Corbett (2008), comprising six items (Appendix A). The word-of-mouth (WOM) scale included eight items adapted from Harrison-Walker (2001) and Kirk et al. (2015). The reinvestment intention scale also comprised eight items and was developed based on Puustinen et al. (2013). All scales in the questionnaire used a seven-point Likert-type scale ranging from strongly disagree (1) to strongly agree (7).

Sociodemographic questions gathered information on the BAs’ gender, age and country of residence. Finally, questions related to the BAs’ experience focused on the following aspects: years of experience as a BA; number of startups invested in; amount of money invested within the scope of BA activities; geographical area of investments; and the percentage of time dedicated to BA activities. Data confidentiality was assured in the questionnaire introduction.

The questionnaire was pre-tested with five BAs, and minor changes were made to reword some items. It was administered online from January to March 2019, with online administration and confidentiality measures implemented to minimise social desirability bias.

Out of 10,000 BAs contacted via e-mail, a response rate of 12% was obtained, resulting in 1225 answers from 79 different countries. However, 376 questionnaires were incomplete, leaving 849 completed questionnaires, representing a final response rate of 8.5%.

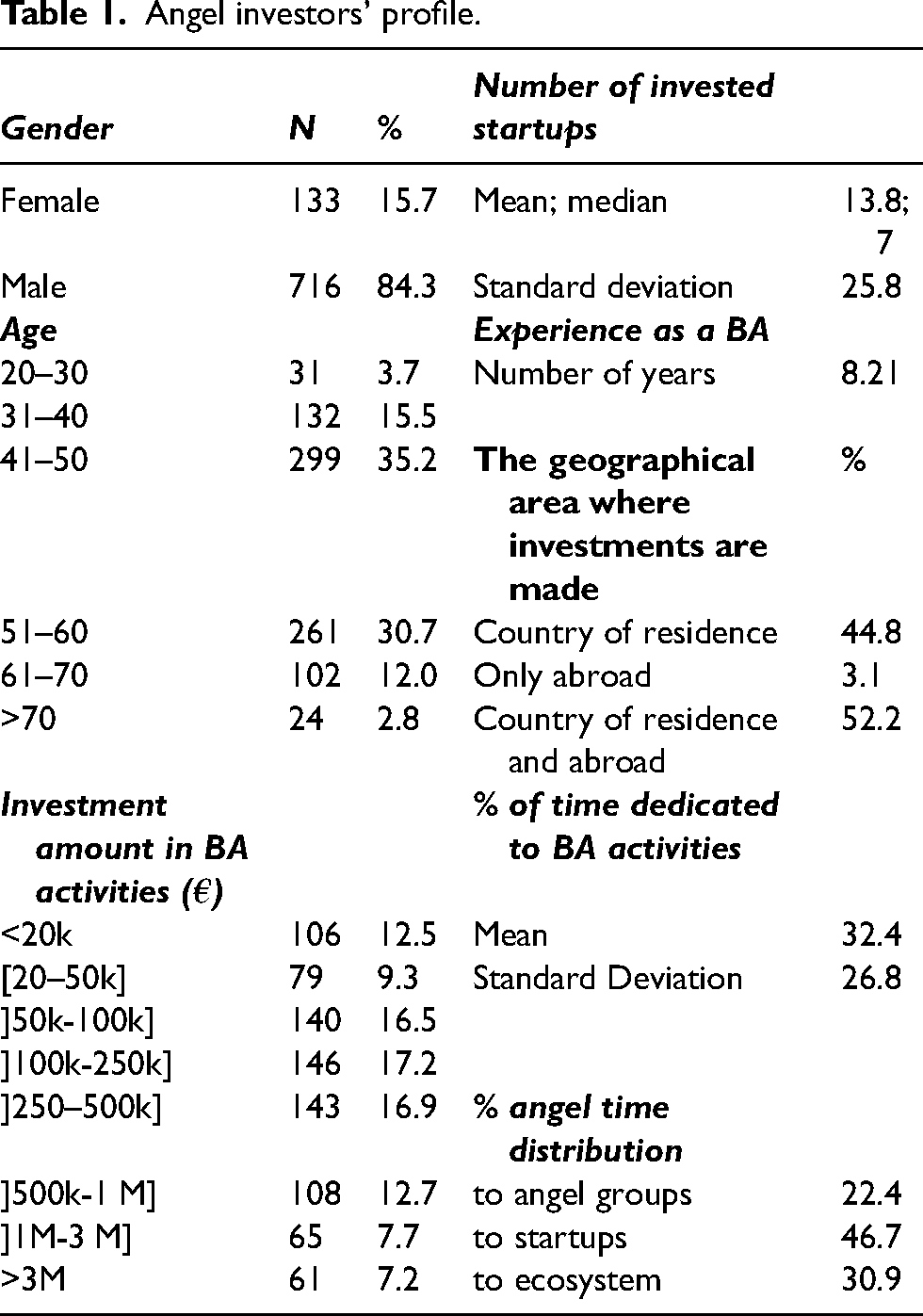

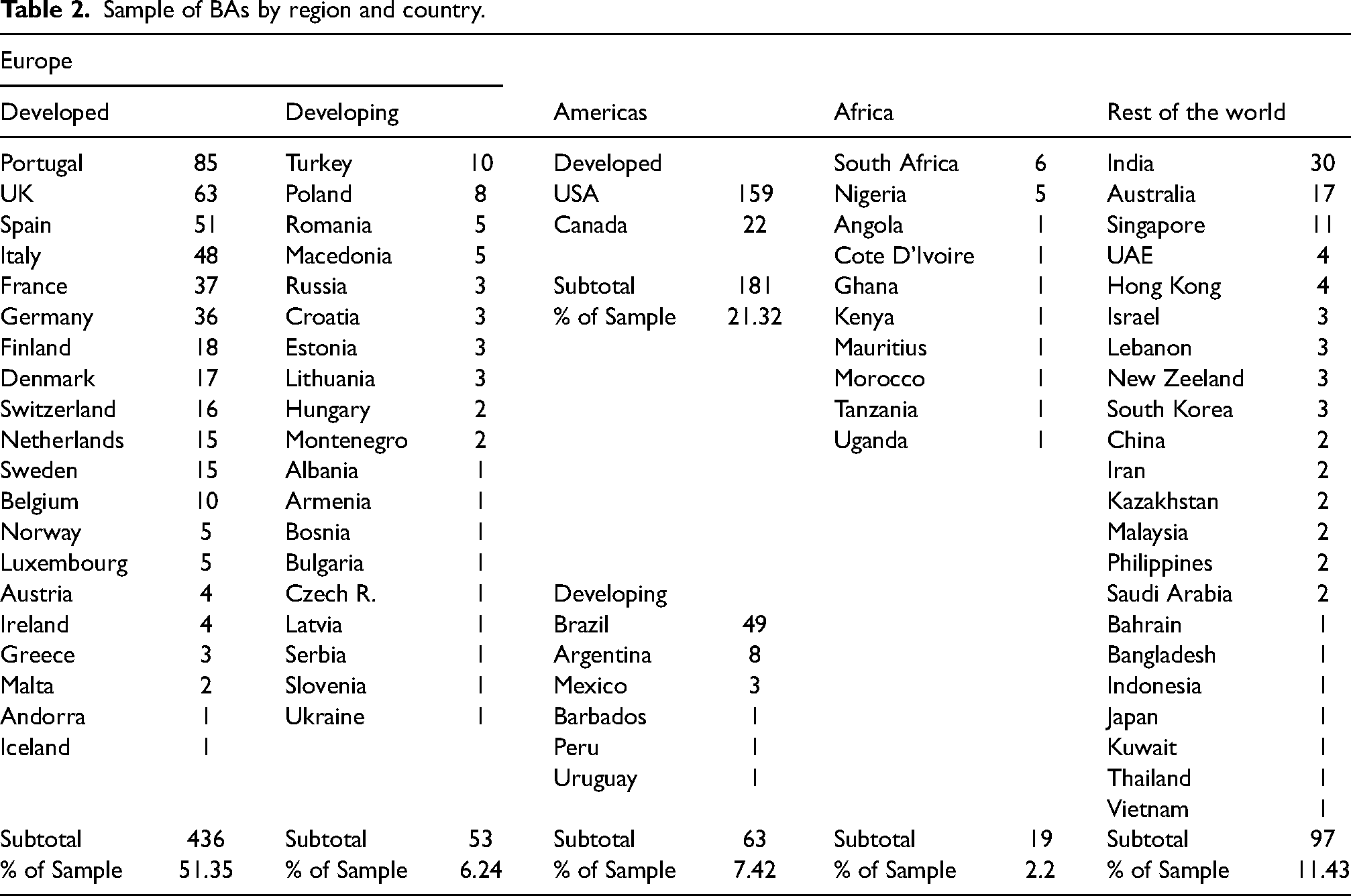

The majority of the respondents are male (84.1%), and fall within the age range of 41–50 years (35%) or 51–60 years (31%) (Table 1). The sample includes BAs from various countries (Table 2).

Angel investors’ profile.

Sample of BAs by region and country.

On average, BAs have 8.2 years of angel investing experience and have invested in 13.7 startups, mostly (50.6%) with amounts between 50 and 500 k. The majority (51.8%) have invested both in their country of residence and abroad, with investments made in up to 7 startups. BAs dedicate, on average, 32.2% of their working time to angel activity, primarily focusing on supporting startups (46.9% of their angel time).

The APIV scale was tested using Covariance-Based Structural Equation Modelling (CV-SEM) with IBM SPSS AMOS version 23.0, employing maximum likelihood estimation to assess the proposed hypotheses. Exploratory factor analysis confirmed item consistency with the original construct, and confirmatory factor analysis (CFA) was conducted to examine the psychometric properties of the scales.

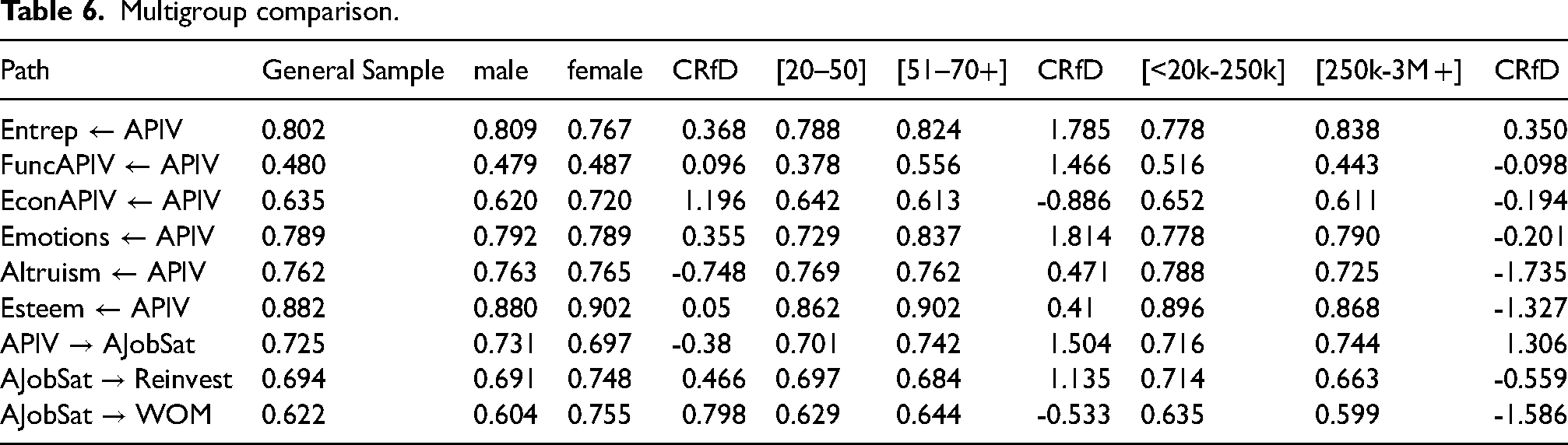

The validity of the APIV scale was assessed through three multigroup analyses (MGAs) comparing different groups: gender (males vs. females); previous experience (novice vs veteran); and investment level (light vs. heavy investors). Complementarily, MGAs also explored potential differences in path coefficients among the main variables analysed. Critical ratios for differences (CRfD) (Francisco, 2017) were used to test whether the groups’ paths were statistically different.

Based on Mentzer and Flint (1997), to assess potential non-response bias, the differences between early (n = 55) and late respondents (n = 72) were tested. We found that there were no statistically significant differences between the mean values of the metrics analysed. Therefore, non-response bias does not appear to be a concern in this study.

Analysis of results

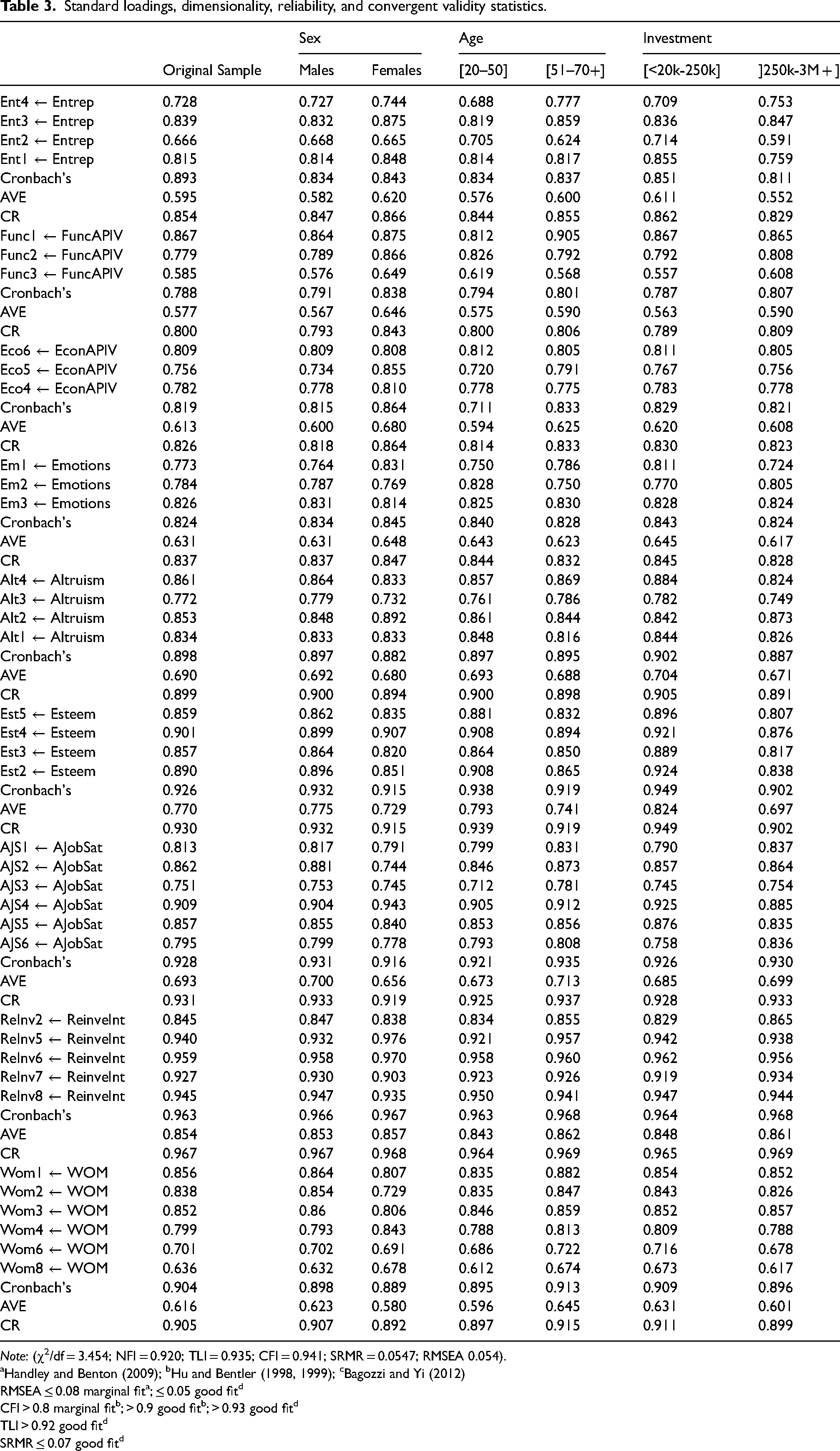

Following Hausman and Siekpe (2009), standardised loadings from CFA were evaluated for the purification process. A minimum factor loading score of 0.7 was used to confirm convergent validity (Hair et al., 2019). Consequently, some items were removed to improve the measurement model (Ent5, Ent6, Eco1, Eco2, Eco3, Func4, Em4, and Est1). Table 3 identifies all the items and constructs’ properties for both the global sample and for each of the three groups tested. The goodness of fit indices show a good fit for the global sample. However, taking into account that the χ2/df is greater than 3 and as it varies with size, we decided to test the model with a more homogeneous sample. For that, 427 responses from BAs from developed European countries were randomly selected. As the results (χ2/df = 2.397; TLI = 0.927; CFI = 0.935; SRMR = 0.0566; RMSEA = 0.057) show a good fit we decided to proceed with the whole sample, which is more representative of the whole population of BAs.

Standard loadings, dimensionality, reliability, and convergent validity statistics.

Note: (χ2/df = 3.454; NFI = 0.920; TLI = 0.935; CFI = 0.941; SRMR = 0.0547; RMSEA 0.054).

RMSEA ≤ 0.08 marginal fita; ≤ 0.05 good fitd

CFI > 0.8 marginal fitb; > 0.9 good fitb; > 0.93 good fitd

TLI > 0.92 good fitd

SRMR ≤ 0.07 good fitd

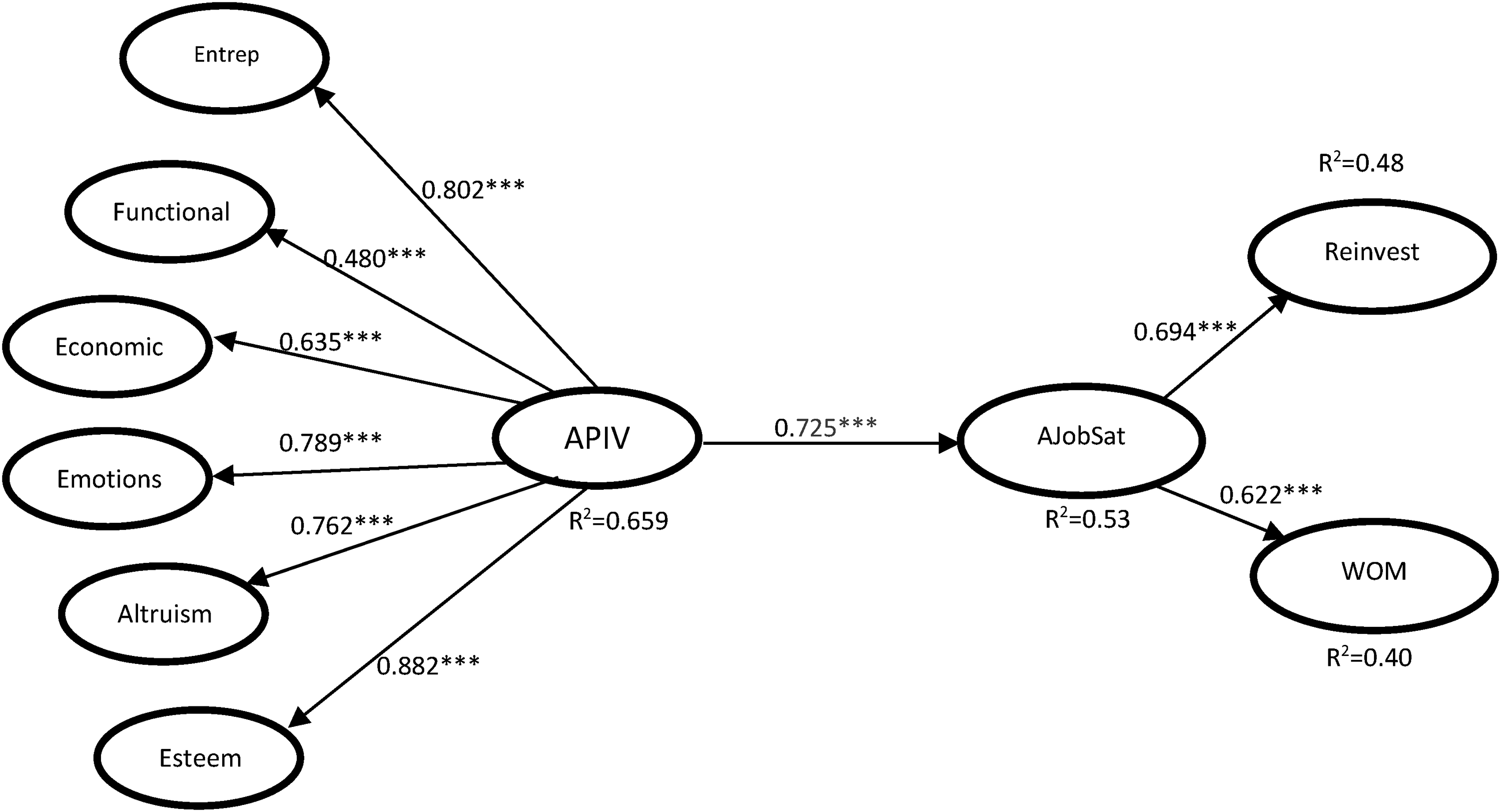

The importance of each first-order APIV dimension was verified by second-order factor analysis, which supported the six first-order factors. Overall, one can claim that APIV can be assessed through the six first-order dimensions.

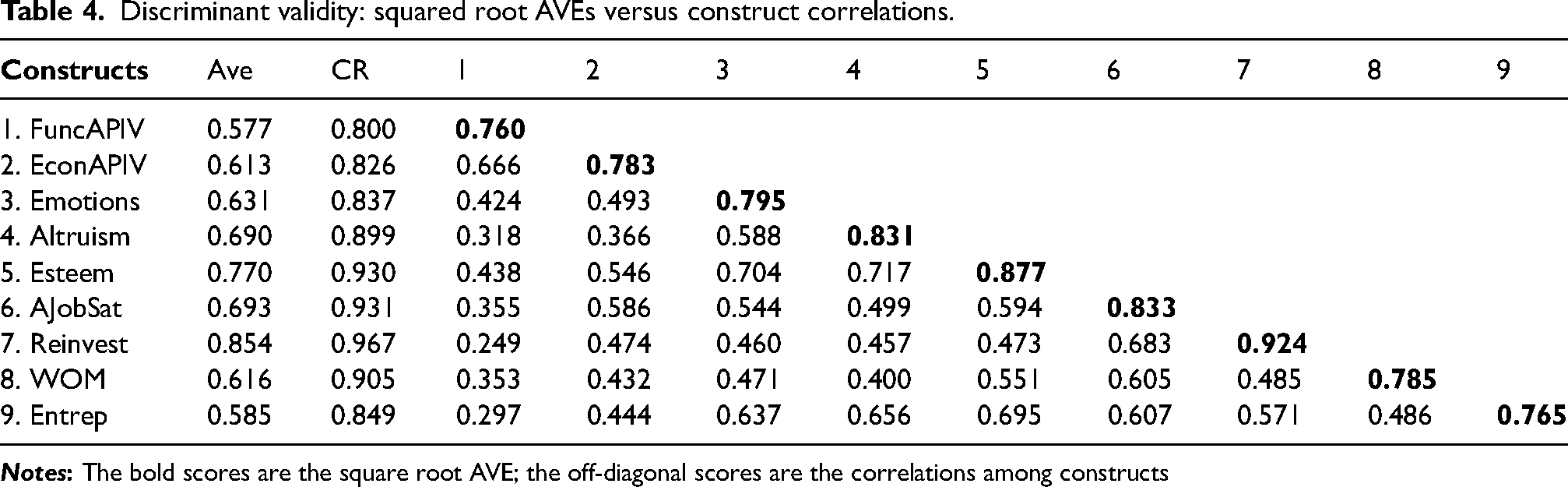

The correlations between constructs ranged from 0.249 to 0.704, and no pair exceeds the 0.9 limit recommended by Hair et al. (2019). As shown in Table 4 for the global sample, one can argue that discriminant validity is supported, as the squared root AVEs for all the variables are higher than the correlations among any pair of variables. Following the measurement purification process, CV-SEM was used to test the hypotheses within the research model.

Discriminant validity: squared root AVEs versus construct correlations.

Figure 2 shows the results of the structural model for the global sample. All fit indexes in the research model are acceptable (for the random sample of 427 responses from developed European countries the results are: χ2/df = 2.654; TLI = 0.914; CFI = 0.920; RMSEA = 0.062). APIV comprises all six factors: entrepreneurial, economic, functional, emotional, altruism, and self-esteem. Except for functional PIV, all the remaining factors have substantial importance in determining APIV. The second-order model explains 53% of angel job satisfaction (Figure 2).

Structural model.

Table 5 shows that the model confirms that APIV positively influences (β=0.725) job satisfaction. Moreover, it also reveals that satisfied BAs are more willing to reinvest (β=0.694) and engage in WOM (β=0.622) about their activity.

Research hypotheses.

Note: (χ2/df = 3.9; NFI = 0.905; TLI = 0.923; CFI = 0.927; RMSEA = 0.059).

*p < 0.1; **p < 0.05 and ***p < 0.01.

Table 6 presents the multigroup comparison and the main results of the general sample. The paths of the original model were examined by comparing the differences between males and females, age groups comparing novice vs veteran BAs and the amount invested by BAs. For each group, the difference in path coefficients between each group was compared using the DRfD, which is stricter than merely comparing the significance of the paths (Francisco, 2017). As seen, for the three groups, the paths show no differences between the groups as the CRfD is lower than ±1.96. This indicates that the results are quite robust for the general model and the six sub-groups analysed.

Multigroup comparison.

Discussion, conclusions, implications and future research

The APIV instrument proposed in this paper offers a comprehensive perspective on BAs by integrating finance, marketing, and consumer behaviour concepts. It reveals that angel investing serves a purpose beyond financial returns. Living the BA experience per se, with its potential for personal growth, helping others, and experiencing the emotions of the entrepreneurial journey, can be highly appealing. These aspects hold significant weight in the APIV instrument, even surpassing the importance of financial returns. Like a new entrepreneurial adventure, the BA's experience of investing is seen as a transformative journey that connects the dots of their entrepreneurial career and gives meaning to their lives.

The APIV instrument explains 65.9% of the value BAs obtain from their activity, based on a compound of six distinct value dimensions: self-esteem, altruism, emotional, entrepreneurial, economic and functional.

BAs perceive the primary value of their role as symbolic, as it enhances their self-esteem (λ=0.882) and allows for personal and professional growth. They derive enjoyment from helping entrepreneurs, which boosts their confidence. Altruism (λ=0.762) is another significant contributor to the symbolic value, as angel investment provides a sense of purpose and allows BAs to express benevolence by contributing to society and creating a better world.

BAs derive emotional value (λ=0.789) from perceiving their activity as an enjoyable way to spend time. It provides moments of excitement, risk-taking and diverse entertainment experiences. Equally relevant is the opportunity to remain involved in entrepreneurial activities, experiencing the pleasure of starting something from scratch and mentoring entrepreneurs. This fosters a strong sense of entrepreneurial value for BAs (λ=0.802).

In terms of economic value (λ=0.635), BAs assess the balance between potential gains and the costs and risks associated with their investments. BAs see investing in startups as a means to diversify, earn money and increase wealth. However, their perceived economic value may be biased by overconfidence, particularly among angels with previous entrepreneurial experience, as mentioned by Blohm et al. (2022).

The findings contradict the rational economic perspective in angel literature, which highlights that BAs’ primary motivation is to earn money (Mason et al., 2015). Instead, the results indicate that BAs generally place relatively lower importance on economic value (λ=0.635) compared to other types of value. The results align with the behavioural perspective prevalent in angel literature, where BAs invest for the experience. This perspective suggests that becoming a BA enhances opportunities for self-improvement, learning from experienced angels, co-creating value with entrepreneurs, earning money and experiencing the emotional excitement of starting a startup from scratch without the time and effort constraints faced by initial founders (Benjamin and Margulis, 2005; Ramadani, 2009; Shane, 2009).

The results confirm that while BAs recognise the functional value (λ=0.480) of their activity, acknowledging the time and effort involved, it is not as highly valued as the other dimensions of the APIV framework. In other words, angel investing is not perceived as a simple, effortless, or time-saving activity by all.

The findings highlight that the significance of the angel experience is not solely grounded on financial benefits but rather on a combination of symbolic, emotional, economic and entrepreneurial value. These conclusions were consistent across different groups, including men and women, novice and veteran BAs, and heavy and light investors. Functional and economic values consistently contributed the least to the perceived value among all groups.

Additionally, the APIV framework explains 53% of angel job satisfaction, which strongly influences their word-of-mouth communication (40%) and reinvestment intention (48%). The relationships between APIV, angel satisfaction, word-of-mouth and reinvestment intentions hold true for the various groups analysed.

The results disclose a contemporary approach to understanding the role and positioning of BAs, with several implications. Firstly, angels reveal they value an experiential approach to their activity, aiming to attain symbolic, emotional, and entrepreneurial goals in parallel with economic ones. It is fundamental for BAs to engage in the investing adventure with a focus on personal development. This entails opportunities for learning investment skills, networking, interacting with entrepreneurs and other angels, and experiencing progress and growth. Failing to meet these personal goals may result in dissatisfaction, decreased likelihood of reinvestment, and a higher chance of abandoning the angel activity.

Secondly, for entrepreneurs to attract BAs to their ventures, it is important to emphasise the personal and career development aspects of the angle's involvement. Demonstrating opportunities for learning, active participation and value co-creation can enhance their attraction.

Thirdly, gatekeepers and angel group managers should act as facilitators rather than substituting BAs in their activities, ensuring that BAs can pursue their personal non-economic goals. Angel work encompasses more than passive investing and financial outcomes. Angel groups should actively promote and support angel involvement. Looking ahead, we suggest that angel groups develop their unique value proposition tailored to the diverse segments of angels.

Overall, these implications shed light on the multifaceted nature of the angel experience and provide guidance for BAs, entrepreneurs, and angel group managers to foster a more fulfilling and successful angel investment ecosystem.

Policymakers should focus on developing initiatives that encourage the personal development and organisation of BAs. This would motivate angels to advance in their careers and support the professionalisation of angel groups. Policymakers need to recognise that BAs offer more than just financial investment and appreciate the value they bring through their involvement and mentoring work with startups, which is often overlooked or undervalued.

Furthermore, it is crucial to publicly acknowledge and provide professional certification for BAs. Certification would contribute to their career development and serve as recognition for their unique role in supporting innovation and promoting local development. There is an evident alignment of purpose between BAs, local development policies and incentives for innovation.

While this paper tested the APIV instrument and explored its consequences, it has certain limitations. Firstly, the heterogeneity of the angel market poses a challenge in explaining the angel phenomena on a larger scale. BAs reveal substantial differences in cultural backgrounds, experience, investment preferences and type of involvement. Some angels engage in angel investing as a hobby, while others are full-time professionals.

Additionally, the data analysed are based on self-perceptions, which may introduce social desirability bias despite ensuring data confidentiality. Future research should consider capturing perceived value based on cultural differences, geographic realities, investment typologies and angel profiles.

The third limitation is the dynamic nature of the angel market, which has undergone impressive changes in the past decade, driven by the dynamic nature of BAs themselves. This research is cross-sectional, and in a fast-changing entrepreneurial world, many things occur in a short time. Therefore, more longitudinal research is needed to understand the evolution of angel goals across an investor's life and to grasp the dynamics of the angel market. Lastly, it is worth noting that the mediation role of satisfaction between APIV and both word-of-mouth and reinvestment intention could be explored in future research. Comparing results across different groups of angels, including males and females, novices and veterans, and light and heavy investors, would also provide valuable insights for assessing those mediators.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Appendix A: Measurement items used.

| Scale | Items |

| Economic APIV (Puustinen et al., 2013) From qualitative study and BA Literature | Eco1. is an inexpensive way to invest. |

| Eco2. is priced fairly (management fees). | |

| Eco3. gives me access to public co-investment. | |

| Eco4. is a great way to earn money. | |

| Eco5. is an efficient way to diversify investments. | |

| Eco6. increases my wealth adequately in view of the risk I bear. | |

| Functional APIV (Puustinen et al., 2013) From qualitative study and BA Literature | Func1. is a convenient way to invest. |

| Func2. is an easy way to invest. | |

| Func3. is not unnecessarily time-consuming. | |

| Func4. allows me to remain active. | |

| Emotional APIV (Puustinen et al., 2013) From qualitative study and BA Literature | Em1. is a nice way to spend time. |

| Em2. provides the excitement of risk-taking. | |

| Em3. is entertaining. | |

| Em4. is a challenging experience. | |

| Altruism APIV (Puustinen et al., 2013) From qualitative study and BA Literature | Alt1. gives me the opportunity to make the world a better place. |

| Alt2. it is a way to give back to society. | |

| Alt3. gives me the opportunity to express benevolence toward other people. | |

| Alt4. encourages me to have a life with a higher purpose. | |

| Self-esteem APIV (Puustinen et al., 2013) From qualitative study and BA Literature | Est1. makes me feel fulfilled. |

| Est2. boosts my self-esteem. | |

| Est3. gives me sheer joy. | |

| Est4. makes me feel valuable | |

| Est5. increases my self-confidence. | |

| Entrepreneurial APIV From qualitative study and BA Literature | Ent1. allows me to be part of entrepreneurship. |

| Ent2. gives me the pleasure to begin something from scratch. | |

| Ent3. gives me the opportunity for involvement with startups. | |

| Ent4. allows me to mentor entrepreneurs. | |

| Ent5. maintains my entrepreneurship spirit without direct responsibility. | |

| Ent6. allows me to create an entrepreneurial legacy. | |

| WOM (Kirk et al., 2015) | WOM1. I mention being an angel investor to others quite frequently. |

| WOM 2. I have told more people about angel investments than I have told most other investment possibilities. | |

| WOM 3. I seldom miss an opportunity to tell others about being an angel investor. | |

| WOM 4. when I tell others about being an angel investor, I tend to talk about it in great detail. | |

| WOM 5. I have only good things to say about being an angel investor. | |

| WOM 6. I am proud to tell others I am an angel investor. | |

| WOM 7. I have spoken favorably of being an angel investor to others. | |

| WOM 8. I recommend being an angel investor to others. | |

| Reinvest (Puustinen et al., 2013) | ReInv1. I intend to be an angel investor in the future. |

| ReInv2. I will probably invest as an angel investor in the future. | |

| ReInv3. It is very likely that I will invest as an angel investor in the future. | |

| ReInv4. I intend to continue to invest: my money as an angel investor in the future. | |

| ReInv5. … my time as an angel investor in the future. | |

| ReInv6. … my know-how as an angel investor in the future. | |

| ReInv7. … my reputation as an angel investor in the future. | |

| ReInv8. … in my personal network as an angel investor in the future. | |

| Angel Job Satisfaction Duffy et al. (2012) and Hmieleski and Corbett (2008) | AIJS1. I feel fairly well satisfied with being an angel investor. |

| AIJS2. Most days I am enthusiastic about being an angel investor. | |

| AIJS3. Each day of work as an angel investor seems like the time flies. | |

| AIJS4. I find real enjoyment being an angel investor. | |

| AIJS5. I consider being an angel investor rather pleasant. | |

| AIJS6. All in all, I’m satisfied with the work I do as an angel investor. |