Abstract

Couples who pool their financial resources tend to report more positive relationship outcomes. The present research examines whether more financial interdependence is linked to better and more frequent communication about financial decisions. Individuals who fully pool finances with their partner reported better financial communication quality and more frequent discussions about finances than individuals who partially pool finances or keep finances separate, even after controlling demographic differences and after controlling overall relationship satisfaction (Study 1). Financial account pooling was also strongly associated with greater likelihood to discuss hypothetical financial decisions with the partner (Study 2), and when experimentally assigned to focus on joint rather than separate financial accounts, this focus on pooled financial resources resulted in more willingness to discuss financial decisions with their partner (Study 3). Together, these studies show a novel aspect of how financial interdependence affect everyday interactions between partners: Couples who pool their financial resources talk more about money.

Keywords

Introduction

Couples arrange their financial accounts in different ways, with some keeping their money in separate accounts, some pooling their money into one account, and some choosing a mixed approach maintaining both separate and joint accounts (Gladstone et al., 2022; Pahl, 2005). Pooled finances are a marker of greater interdependence between partners (Agnew et al., 1998; Rusbult et al., 1998), which has important implications for relationship functioning. Financial interdependence such as pooling finances in joint accounts has been linked to greater relationship satisfaction (Addo & Sassler, 2010; Gladstone, Garbinsky, et al., 2022; Kenney, 2006; Olson et al., 2023; Vogler et al., 2008). The present study examines a potential factor that might be part of the link between financial account pooling and relationship quality: communication about finances between partners. Better communication about finances has been linked with more relationship satisfaction (Hill et al., 2017; LeBaron-Black et al., 2023; Romo, 2015; Saxey et al., 2023; Wilmarth et al., 2014) and aspects that might underlie better communication, such as shared financial values, are more common among couples with joint accounts (Kruger et al., 2024; Olson et al., 2023; Sorgente et al., 2023). Partners who pool their finances might communicate more frequently and better about the day-to-day management of their shared money.

Pooling finances and relationship satisfaction

Couples prefer joint or separate arrangements of financial accounts for several reasons. Keeping separate accounts might keep boundaries and individual contributions to the running of the household clearly delineated (Singh & Lindsay, 1996; Treas, 1993). Pooling all money, on the other hand, might establish a sense of unity and couple identity (Emery et al., 2021; Fishman, 1983). Creating joint accounts and mingling financial resources is a marker of greater interdependence with the partner (Interdependence Theory, Agnew et al., 1998; Lange, 2011; Rusbult et al., 1998; Thibaut, 2017) and is particularly likely among couples who are married (Evans & Gray, 2021; Hamplova et al., 2009). There is converging evidence that couples who pool finances report more relationship satisfaction (Addo & Sassler, 2010; Gladstone et al., 2022; Kenney, 2006; Vogler et al., 2008), better financial goal alignment (Kruger et al., 2024; Olson et al., 2023), and fewer financial conflicts (Gladstone et al., 2022; Lim & Morgan, 2021; Rea et al., 2016). For example, individuals in relationships who reported pooling all of their finances with their partner reported higher relationship satisfaction at later surveys compared to those who pool part of their resources and those who kept their resources separate (Gladstone et al., 2022). Newly-weds who were instructed by researchers to pool their money reported less decline in relationship satisfaction over the first years of marriage than couples instructed to keep separate accounts (Olson et al., 2023).

Overall, the link between financial account pooling and relationship satisfaction maps on to the principles of Interdependence Theory (Agnew et al., 1998; Lange, 2011; Rusbult et al., 1998; Thibaut, 2017). The pooling of financial resources embodies mutual dependence and joint investment, which are key variables explaining the quality of relationships (Agnew et al., 1998; Rusbult et al., 1998; Thibaut, 2017). Greater financial interdependence might foster an overall mindset that facilitates communication about finances between partners. For example, when booking a hotel room for a vacation, those with joint accounts may be more likely to discuss the specific booking decisions with the partner than those paying from a separate account. Such discussions might increase the likelihood that both partners are satisfied with the decision and with the decision process. Indeed, one of the reasons for financial conflict between partners is one-sided financial decision making (Peetz et al., 2023), suggesting that more frequent discussions of purchases and other financial decisions might prevent conflict. The present studies examine the quality and frequency of financial communication as associated to account pooling.

Financial communication

In general, communicating well and often with one’s partner is associated with greater relationship satisfaction (Emmers-Sommer, 2004). More specifically, feeling comfortable communicating about finances in particular is linked with better relationship quality (Hill et al., 2017; LeBaron-Black et al., 2023; Romo, 2015; Wilmarth et al., 2014), and, conversely, higher marital satisfaction is linked to better financial communication (Saxey et al., 2023). For example, newlyweds’ rating of the quality of financial communication with their partner was linked positively to participants’ own and their partner’s relationship satisfaction (LeBaron-Black et al., 2023). In addition to better quality of communication, discussing money more frequently is also linked to fewer arguments about finances among married couples (Grobbelaar & Alsemgeest, 2016) and discussing finances earlier in the relationship is linked with better relationship quality later on (Saxey et al., 2022). This link is reflected in people’s beliefs: A qualitative study of couples who believed they had great marriages credited positive and frequent communication about financial decisions with being an important factor for relationship quality (Skogrand et al., 2011), and young adults reported believing that frequent communication about finances helps to avoid and to solve financial challenges in romantic relationships (Rea et al., 2016).

Several studies examining couples’ attitudes towards finances point to differences in the way partners interact when their finances are joint or separated. For instance, couples with pooled finances are more likely to agree on spending priorities (Kruger et al., 2024), report more similar financial behaviors (Sorgente et al., 2023), and report less financial conflict (Lim & Morgan, 2021). Newlyweds assigned to hold joint rather than separate bank accounts reported greater financial harmony two years later, and showed attenuated relationship quality decline in the first years of marriage compared to couples with separate finances (Olson et al., 2023). In sum, pooling finances may lead individuals to change the way they interact with their partner about money, including the way they communicate about financial decisions. Couples with joint finances might communicate better about money and might be more willing to discuss financial decisions, thus preventing small issues from developing into larger disagreements.

Overview of the present research

Across three studies, the association of financial account pooling with quality and frequency of financial communication was examined. Prior work has shown associations between the decision to pool finances and relationship satisfaction (e.g., Gladstone et al., 2022; Olson et al., 2023), associations between relationship satisfaction and financial communication (e.g., Hill et al., 2017; LeBaron-Black et al., 2023; Romo, 2015; Wilmarth et al., 2014), as well as evidence that couples interact differently when their finances are pooled versus separate (e.g., Kruger et al., 2024; Lim & Morgan, 2021; Sorgente et al., 2023). No research has yet directly examined whether the decision to pool finances affects the quality and frequency of communicating about finances in couples. Knowing the implications of financial interdependence with the partner for everyday communication might help couples decide whether to pool their money or help them navigate financial decisions better. Filling this gap in existing research will extend Interdependence Theory (Rusbult et al., 1998; Thibaut, 2017) by demonstrating a novel way in which financial interdependence is associated with couple interactions.

Specifically, the present studies test two hypotheses: Pooling finances to a greater degree may be associated with better quality of financial communication (Hypothesis 1) and with more frequent discussions about financial decisions (Hypothesis 2). A first study (Study 1) examined these hypotheses in a cross-sectional design assessing retrospective ratings of quality and frequency of financial communication in people’s relationships. A second study (Study 2) replicated and extended the initial study to examine these hypotheses with an alternative outcome variable: participants’ ad-hoc decisions to consult the partner across a range of hypothetical spending scenarios. A third study (Study 3) extended the examination of the link between account pooling and communication to an experimental design, shifting participants’ focus on either their joint or their separate financial accounts.

Study 1

The first study aimed to examine whether financial account pooling is associated with differences in communication about finances, specifically quality and frequency of discussions about finances. The hypothesized association was that fully joint financial accounts would be associated with better communication (H1) and more frequent discussions about money (H2).

The study design, sample size, inclusion criteria and planned analyses were preregistered (https://aspredicted.org/WCS_CMF). Survey, data, and syntax are available on the Open Science Framework (OSF): https://osf.io/kxvdb/.

Method

Participants

Demographic variables across studies.

Note. All samples were drawn from Prolific Academic, U.S. respondents only. Income measured on 11-point categorical scales, means presented are the category corresponding to the average value on this scale. Gender assessment did not distinguish transwomen/men and ciswomen/men. Education, employment type, and disability information was not collected in any of the samples.

Procedure

Participants first completed a demographic survey assessing age, gender, ethnicity, own and partner’s annual income, respectively, via 11 categories (e.g., under $10,000, $10,000-$19,999 etc. to $100,000 or more), relationship status (married, engaged, dating, single), and relationship length. Participants reported on their financial organization on a single item measure (Evans & Gray, 2021; Hamplova et al., 2009): Participants were asked how they manage their finances with their partner and were presented with five options. One option was “We each keep our own money separate” (27.1%), which was coded as having separate accounts. Another was “We pool all the money and each take out what we need” (43.7%), which was coded as fully pooled accounts. Finally, the following statements were collapsed (in line with Gladstone et al., 2022; total 29.1%), all of which capture some form of mixed account pooling: “We pool some of the money and keep the rest separate” (18.1%); “I manage all the money and give my partner his/her share” (6.5%); “My partner manages all the money and gives me my share” (4.5%).

Participants reported on the frequency of financial discussions on a single item (“In the last month, how often did you discuss financial decisions or money with your partner?”) on a 6-point scale (Never, Once, A couple of times, Several times, Many times, Often, All the time). Participants reported on the topics of discussion they had 1 and described a recent discussion on finances which served as attention and engagement check. Participants then reported on the quality of financial communication in their relationship on a five-item scale on financial communication (Day et al., 2009; Saxey et al., 2024; e.g., “My partner and I have good communication about household financial issues”, “My partner and I work together on the household financial budget.”) using scales from Strongly Disagree (1) to Strongly Agree (5). Items were averaged (Cronbach’s α = .86). This scale has been shown to have high reliability, high construct validity and predictive validity in both married and dating samples and among couples with joint or separate finances (Saxey et al., 2024).

Finally, participants completed the Relationship Assessment Scale (Hendrick, 1988) to measure participants’ relationship satisfaction. Participants rated seven items (e.g., “How well does your partner meet your needs?”) using seven 5-point bipolar ratio scales (e.g., Poorly to Extremely well; Unsatisfied to Extremely satisfied). Items were averaged (Cronbach’s α = .93).

Data analysis

To compare financial communication across participants who completely pooled their money with their partner, partially pooled their money with their partner, or kept money completely separate, one-way ANOVAs were conducted for each of the outcome variables: quality of financial communication (preregistered) and frequency of communication about finances (preregistered). Follow-up contrasts compared completely pooled finances to partially pooled finances and comparing completely separate finances to partially pooled finances (preregistered), in line with prior work (Gladstone et al., 2022). Follow-up contrasts included both linear and quadratic effects.

Additional robustness analyses (not preregistered) tested whether account pooling effects persisted when controlling for other group differences among those who pool their money with their partner. Univariate ANOVAs controlling for age, income, partner’s income, relationship length, and marital status examined the differences between account pooling groups for quality and frequency of communication holding these variables constant. Additional analyses (not preregistered) also tested whether the difference in financial communication by account pooling persisted when controlling for relationship satisfaction using univariate ANOVAs controlling for relationship satisfaction.

Results

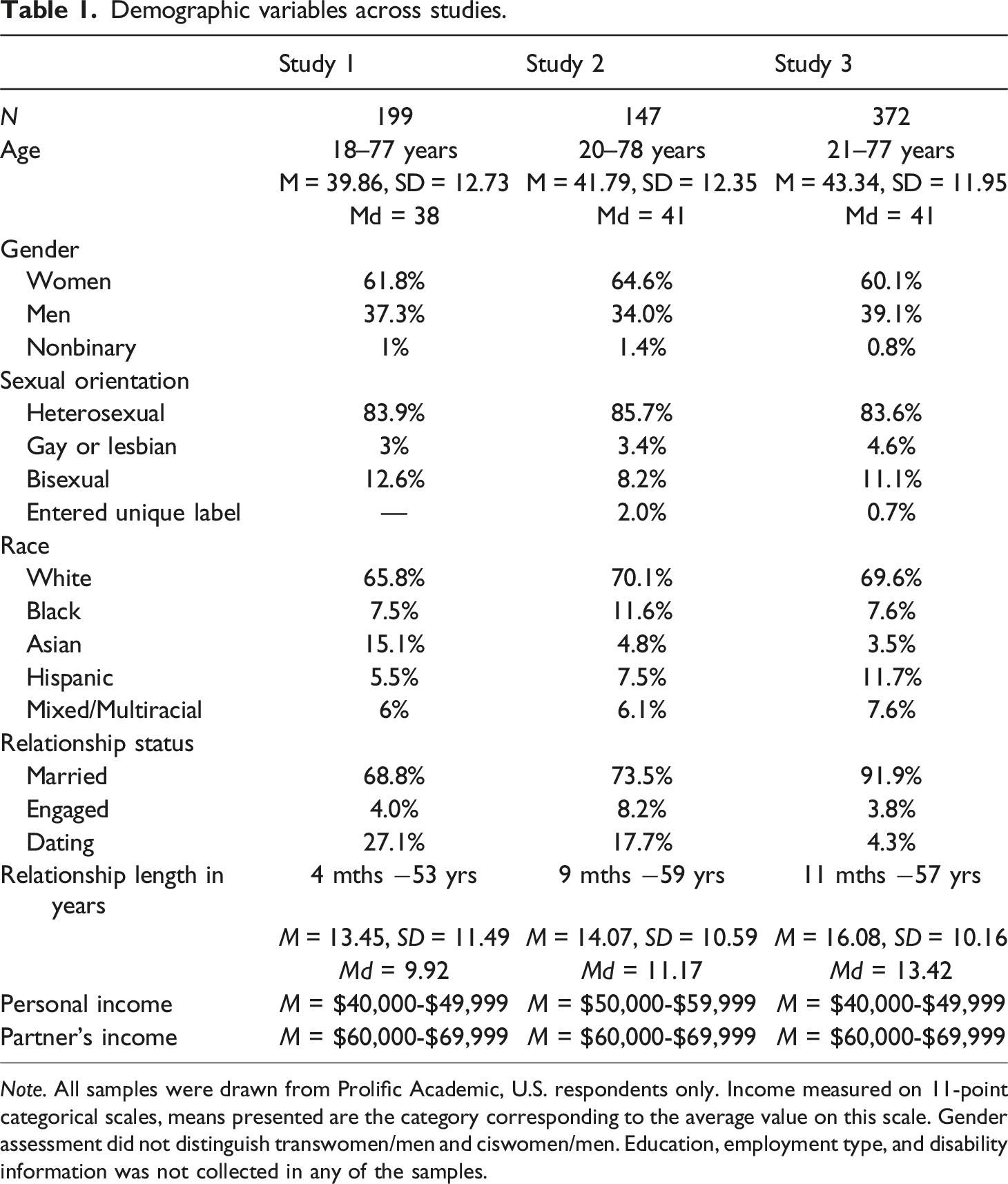

As expected, there was a significant account pooling effect on quality of financial communication, F (2,196) = 9.87, p < .001, eta2 = .09. Means by account pooling group are portrayed in Figure 1. Follow-up contrasts showed that participants who completely pooled finances with their partner reporting better quality of financial communication with their partner than participants with mixed account pooling, t (196) = 3.40, p < .001. Participants who completely separated finances with their partner did not differ on this measure from participants with mixed account pooling, t (196) = −0.58, p = .562. When testing linear and quadratic simple effects, the linear effect of financial account pooling was significant, t (196) = 3.96, p < .001, and the quadratic effect was not significant, t (196) = 1.48, p = .140. Average frequency and quality of financial communication by financial account pooling (Study 1).

There was also a significant financial account pooling effect on frequency of communication about finances, F (2,196) = 5.59, p = .004, eta2 = .05. Participants who completely pooled finances with their partner did not differ significantly from participants with mixed account pooling, t (196) = 1.22, p = .223, but participants who completely separated finances reported discussing finances marginally less often than participants with mixed account pooling, t (196) = −1.96, p = .051 (Figure 1). When testing linear and quadratic simple effects, the linear effect of financial account pooling was significant, t (196) = 3.41, p < .001, and the quadratic effect was not significant, t (196) = −0.52, p = .603.

Exploratory analyses with demographic covariates

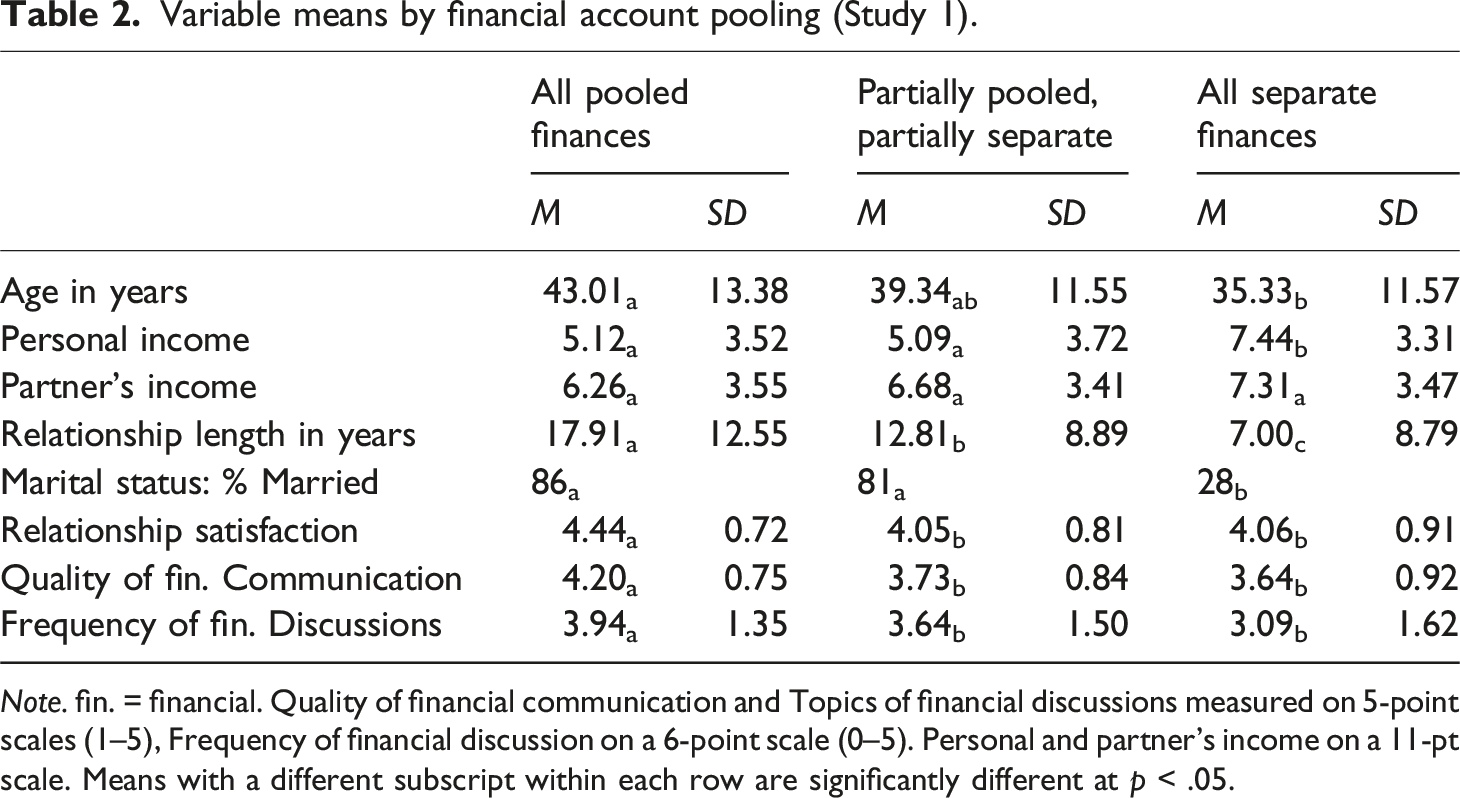

Variable means by financial account pooling (Study 1).

Note. fin. = financial. Quality of financial communication and Topics of financial discussions measured on 5-point scales (1–5), Frequency of financial discussion on a 6-point scale (0–5). Personal and partner’s income on a 11-pt scale. Means with a different subscript within each row are significantly different at p < .05.

It is possible, therefore, that demographic differences drive the difference between account pooling groups. However, when controlling for all significant differences between account pooling groups (age, income, partner’s income, relationship length, marital status) the difference in quality of financial communication between account pooling groups remained significant, F (2, 186) = 10.35, p < .001, partial eta 2 = .10. Frequency of financial discussions also remained significantly different between account pooling groups with the covariates in the model, F (2, 186) = 4.71, p = .010, partial eta2 = .05. See Table OS1 and OS2 in online supplements for all coefficients for covariate models.

Exploratory analyses with relationship satisfaction as covariate

Financial account pooling has been linked to increased relationship satisfaction (Addo & Sassler, 2010; Gladstone, Garbinsky, et al., 2022; Kenney, 2006; Olson et al., 2023; Vogler et al., 2008). Indeed, relationship satisfaction was higher among participants who fully pooled their money with their partner (see Table 2). It is possible, therefore, that the differences in financial communication are a proxy for these larger relationship quality differences between account pooling groups. However, when controlling for relationship satisfaction, the difference in quality of financial communication between account pooling groups remained significant, F (2, 195) = 4.47, p = .013, partial eta 2 = .04. Frequency of financial discussions also remained significantly different between account pooling groups with relationship satisfaction in the model, F (2, 195) = 4.06, p = .019, partial eta2 = .04. See Table OS3 and OS4 in online supplements for models with covariates.

Study 2

In the next study, rather than assessing participants’ perception of the quality of communication, their willingness to discuss financial decisions with the partner was assessed, using a range of hypothetical financial decision scenarios. This design controls the context of the financial discussions to be equal across account pooling groups, and examined the willingness to discuss finances independent of other lifestyle differences among couples with relatively more or less financial interdependence. Scenarios were based on ten common financial conflict themes identified in qualitative research (Peetz et al., 2023). A pilot test of this measure showed that the scenarios were seen as likely or realistic across all financial account pooling groups (see online supplement for details: https://osf.io/kxvdb/). This study was preregistered: https://aspredicted.org/ZZQ_HJH. Materials and data are available on OSF: https://osf.io/kxvdb/

Method

Participants

Participants were recruited on Prolific Academic, with the eligibility requirements of being in a relationship for at least one year. Only participants from the US were recruited. One-hundred and fifty participation slots were posted and filled, participants were compensated with $1. Three participants were excluded in line with preregistered criteria (two did not respond to the attention check and one simply answered ‘no’, a nonsequiteur). No outliers were observed, and missing data was less than 0.01%. See Table 1 for demographic descriptive statistics.

Procedure

Participants first completed a demographic survey assessing age, gender, ethnicity, annual personal and annual partner’s income, relationship status, and relationship length as in Study 1. Participants reported on their financial organization as in Study 1 (Evans & Gray, 2021; Hamplova et al., 2009). Responses were coded as completely pooled finances (40.1%), mixed account pooling (34.7%) and separate finances (25.2%). Participants also reported the time since joining finances with their partner (“How long, in years and months, have you pooled your finances with your partner?”), coded as missing values for those indicating fully separate finances.

Participants then read ten hypothetical scenarios describing a financial decision (e.g., “You booked a hotel for your vacation and a better deal becomes available at another hotel nearby. You want to cancel the first reservation and book the better deal.”). After each scenario they were asked “What would you do in this situation?”, with three response options including “I would discuss this decision with my partner”, “I would make this decision on my own (i.e., without my partner’s input)”, and “I would tell my partner to make this decision on their own (i.e., without my input)”. The number of times they selected the option of discussing the decision with their partner was aggregated into an index of financial discussions (i.e., possible range 0–10).

Participants also reported the expected frequency of financial discussions with the partner in the next month on a single item on a 6-point scale (Never, Once, A couple of times, Several times, Many times, Often, All the time). They also reported on the quality of financial communication in their relationship (Day et al., 2009; Saxey et al., 2024, Cronbach’s α = .86) using a scale from Strongly Disagree (1) to Strongly Agree (5). The index of financial discussions was positively correlated with anticipated frequency of financial discussions with the partner in the next month, r (145) = .43, p < .001, and quality of financial communication in the relationship overall, r (145) = .36, p < .001, providing convergent validity to the index of financial discussion decisions.

Data analysis

To compare willingness to discuss financial decisions across participants who completely pooled their money with their partner, partially pooled their money with their partner, or kept money completely separate, a one-way ANOVA was conducted for the overall index of financial discussion decisions (preregistered). Follow-up contrasts compared completely pooled finances to mixed account pooling and compared completely separate finances to mixed account pooling (preregistered). Follow-up contrasts included both linear and quadratic effects. Follow-up analyses (not preregistered) additionally controlled demographic variables (age, personal income, partner’s income, relationship length, marital status) in a univariate ANOVA.

Finally, exploratory analyses (not preregistered) examined the length of time participants had pooled finances for the subset of participants who reported fully or partially pooled finances (n = 105) in a linear regression model, regressing the index of financial discussion decisions on age, gender, personal income, partner’s income, relationship length, marital status and the years since first pooling any financial resources.

Results

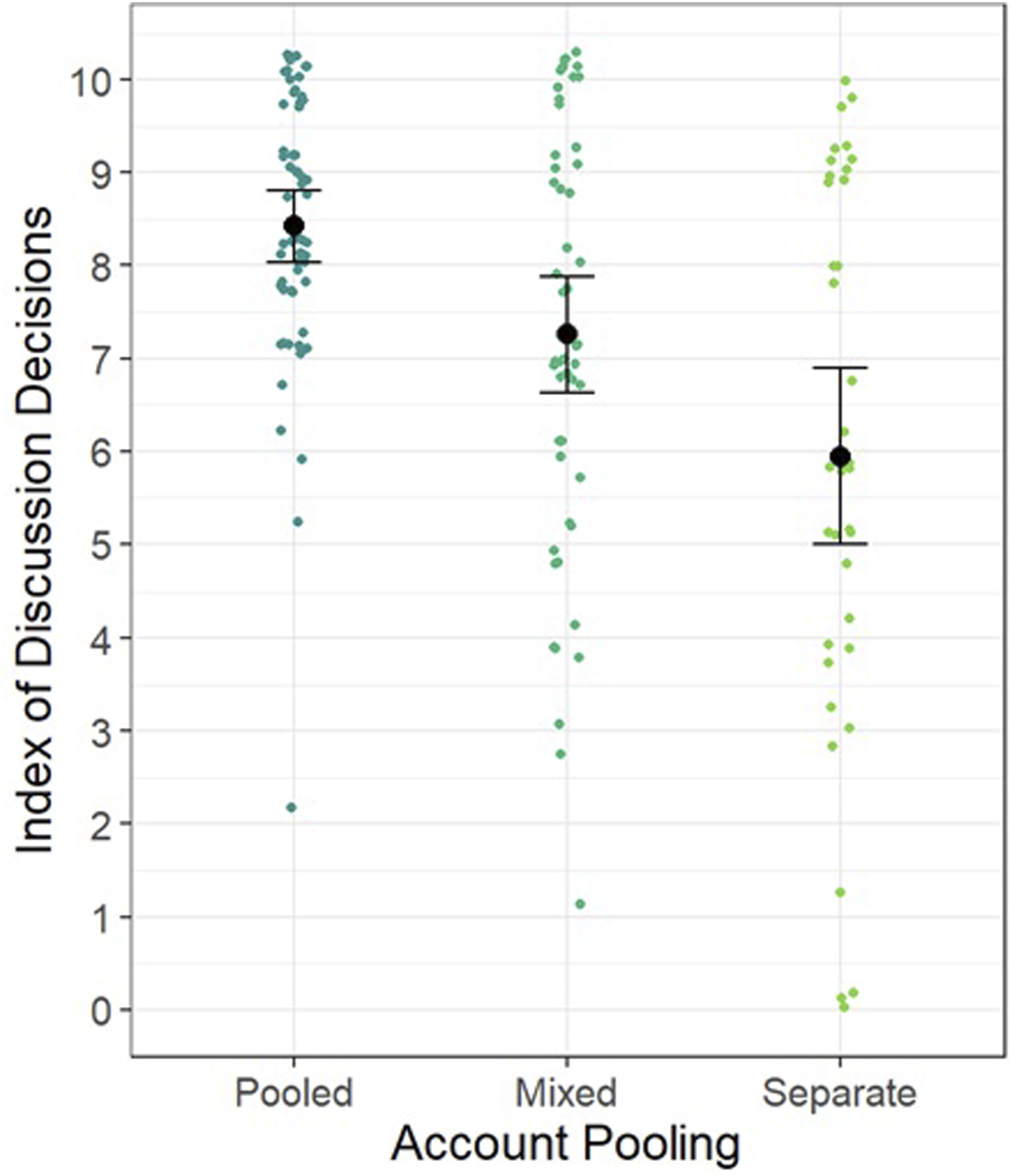

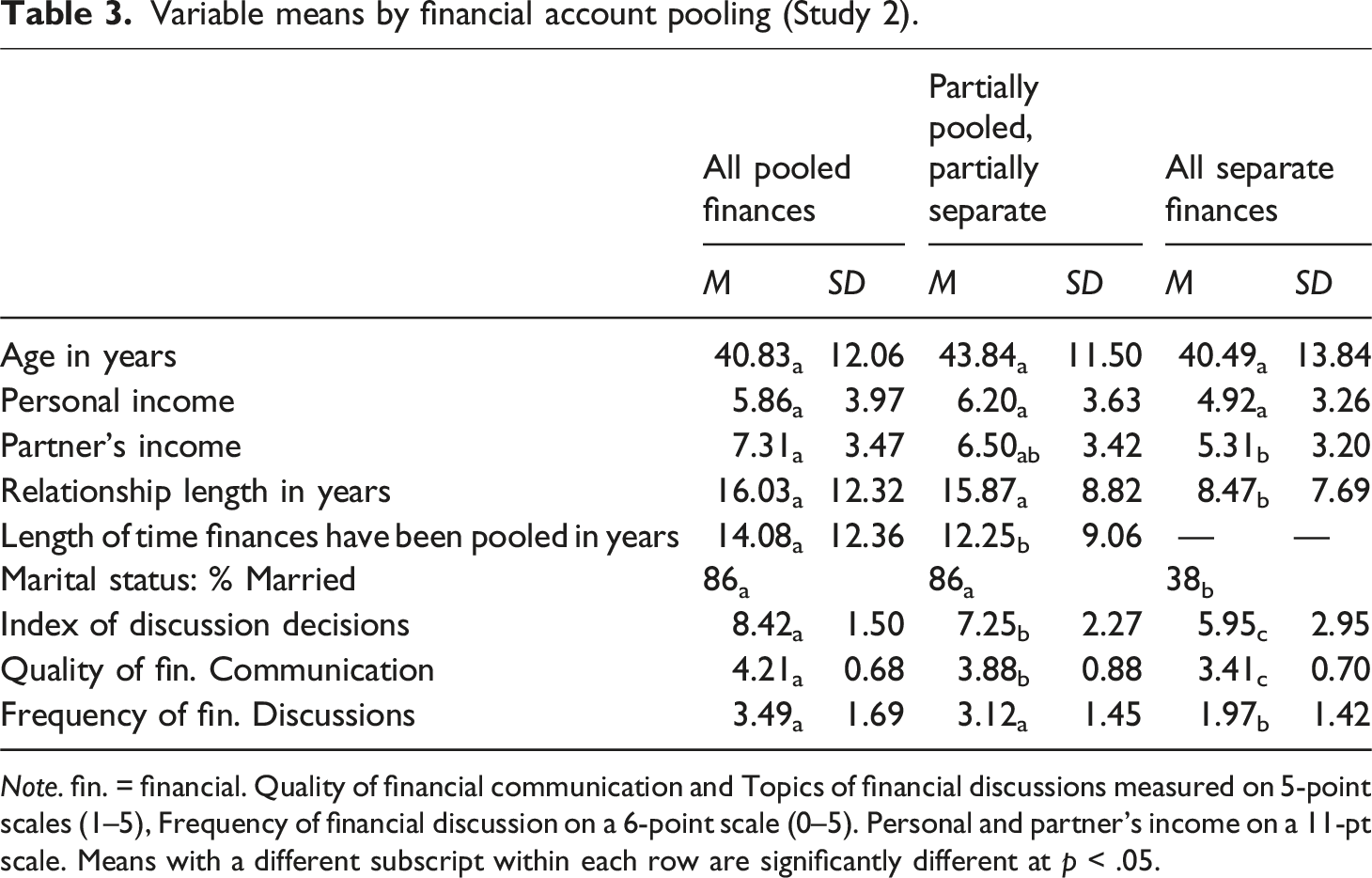

Financial account pooling showed a significant effect on the index of decisions to discuss finances, F (2,144) = 14.48, p < .001, eta2 = .17 (see Figure 2). Simple effect testing revealed a linear trajectory: Participants who fully pooled finances with their partner reported more willingness to discuss financial decisions than participants with mixed account pooling, t (144) = 2.77, p < .001, or participants who completely separated finances, t (116) = 5.35, p < .001. A quadratic effect was not significant, t (144) = 0.18, p = .856. Average willingness to discuss hypothetical financial decisions by financial account pooling (Study 2).

Variable means by financial account pooling (Study 2).

Note. fin. = financial. Quality of financial communication and Topics of financial discussions measured on 5-point scales (1–5), Frequency of financial discussion on a 6-point scale (0–5). Personal and partner’s income on a 11-pt scale. Means with a different subscript within each row are significantly different at p < .05.

Among the subset of participants who reported fully pooled finances or mixed account pooling (n = 105), the length of time finances had been pooled also mattered: When regressing the index of financial discussion decisions on age, gender, personal income, partner’s income, relationship length, marital status and the years since first pooling any financial resources, the sole significant predictor was years of pooled resources, unstandardized B = 0.12, SE = 0.05, standardized β = 2.56, p = .012. The longer participants reported having had joint finances, the more likely they were to state that they would discuss hypothetical financial decisions with their partner (see Table OS6 in online supplements for all model coefficients).

Study 3

Neither previous study can speak to the direction of the link between account pooling and communication. It is probable that couples who communicate well about finances are more likely to make the decision to pool their money. On the other hand, the decision to pool money might create feelings of interdependence and necessitate more frequent communication in daily life, creating habits of discussing financial decisions with the partner. In the next study, financial interdependence was experimentally manipulated. Specifically, the focus on pooled (vs. separate) finances was emphasized to test whether there was a resulting shift in willingness to discuss financial decisions with the partner.

Participants were individuals in relationships with both joint and separate financial accounts (identified using the pre-selection features of the recruitment platform Prolific Academic). Participants were instructed to focus on either their joint accounts or were instructed to focus on their separate accounts before completing the index of financial discussion decisions. The study design, inclusion criteria, and main analyses were preregistered (https://aspredicted.org/25L_NK6). Note that the sample size deviated from the initial preregistration: the initial preregistration specified a sample of 200 participants, based on a rule of thumb of 100 participants per condition, since the manipulation effect size was unknown. Analysis of this initial sample showed a small effect size of the condition, d = .26, which is too small to be detected reliably with a sample of 200 (42% power to detect an effect of this size, G*Power). A second preregistration specified collecting an additional 200 participants and preregistered the plan to combine both samples for a higher-powered test (75% power) of the planned analysis (https://aspredicted.org/2KJ_Q8H). Surveys, data, and syntax are available on the Open Science Framework (OSF): https://osf.io/kxvdb/.

Method

Participants

Participants were recruited on Prolific Academic, with the eligibility requirements of 1) being in a relationship for at least three months, 2) having a joint account with their partner, and 3) having a separate account from their partner. Only participants from the US were recruited. Overall, 400 participation slots were posted across two waves of data collection. Participants were compensated with $1. Participants were excluded if they reported that they did not have such accounts or did not answer when queried to elaborate on their joint accounts (n = 10) or separate accounts (n = 18). No outliers were observed and all participants were in relationships longer than three months. The final sample size (N = 372) allows us to detect a small to medium effect size (d = .26) difference between two groups with 70% power.

Procedure

Participants first completed a demographic survey assessing age, gender, ethnicity, personal and partner’s income, relationship status, and relationship length as in Study 1. Participants were randomly assigned to either a condition where they focused on their joint accounts with their partner (n = 189) or focused on their separate accounts (n = 182). In each condition, the manipulation included checking off all the accounts they held that were joint (vs. separate) on a list specifying checking account, saving – general, retirement saving, education saving, credit card, other line of credit, mortgage. They were then asked to think and write about a recent transaction from a joint account (vs. from a separate account). Finally, they were asked to describe in their own words “What do you like about having pooled finances or joint accounts with your partner?” (vs. “What do you like about having independent finances or separate accounts from your partner?”).

Participants then read ten hypothetical scenarios describing a financial decision as in Study 2. The number of times they selected “I would discuss this decision with my partner” was aggregated into an index of willingness to discuss financial decisions. Participants also reported the expected frequency of financial discussions with their partner in the next month on a single item on a 6-point scale as in Study 2.

Finally, as manipulation check, participants reported on their overall perception of how their financial accounts were organized on a Likert scale from We pool all the money (1) over We partially pool and partially separate money (4) to We each keep our own money completely separate (7). Participants assigned to think about their separate financial accounts reported more subjective financial separation on the manipulation check item (M = 3.61, SD = 1.89) than participants assigned to think about their joint accounts (M = 3.01, SD = 1.71), t (368) = 3.24, p < .001, d = .34, suggesting that the manipulation was successful.

Data analysis

To compare willingness to communicate about finances between conditions, an independent t-test was conducted with condition as predictor (joint condition = 1, separate condition = 0) for the overall index of discussion decisions (preregistered) and for the anticipated frequency of discussing money with the partner in the next month (not preregistered).

As follow-up analyses (not preregistered), regression models with index of financial discussion decisions and anticipated frequency of discussing money with the partner as outcome variables, respectively, and condition as predictor variable (joint condition = 1, separate condition = 0) added demographic variables (age, gender, personal income, partner’s income, marital status, relationship length) as covariates to the models.

Results

Participants who were assigned to focus on their joint financial accounts reported more willingness to discuss hypothetical financial decisions with their partner (M = 7.51, SD = 1.77) than participants who were assigned to focus on their separate accounts (M = 7.08, SD = 2.09), t (368) = 2.16, p = .032, d = .22. The effect of condition remained significant when controlling demographic covariates, unstandardized B = 0.48, SE = 0.20, standardized β = .12, t (351) = 2.35, p = .020. See Table OS7 in online supplements for all regression coefficients.

Participants who were assigned to think about their joint financial accounts did not anticipate discussing financial decisions significantly more with their partner in the next month (M = 4.59, SD = 1.50) than participants who were assigned to think about their separate accounts (M = 4.36, SD = 1.55), t (368) = 1.44, p = .151, d = .15. However, this condition effect was marginally significant after controlling demographic covariates, unstandardized B = 0.30, SE = 0.16, standardized β = .10, t (351) = 1.87, p = .063 (not preregistered). See Table OS8 in online supplements for all regression coefficients.

General discussion

Across several studies, individuals in relationships who reported relatively more financial interdependence with their partner also reported higher quality of financial communication, greater frequency of discussing finances, and greater willingness to discuss hypothetical financial decisions with their partner than individuals who reported relatively less financial interdependence with their partner. This link between financial interdependence and financial discussions was also evident in the length of time participants had pooled financial accounts (Study 2) and when participants with mixed financial accounts temporarily focused on their joint rather than their separate accounts (Study 3). Importantly, this link of account pooling and willingness to communicate was not due to other aspects about the relationship, such as marital status and relationship length, or other demographic differences.

While these studies cannot determine with certainty the direction of the financial interdependence and financial communication link, it is likely that the association is bidirectional. The experimental study (Study 3) found that random assignment to a task that temporarily increased perceived financial interdependence also increased willingness to discuss financial decisions with the partner, implying a directional link from account pooling to communication. However, this is likely only part of the story. It stands to reason that couples who communicate better about finances would find the prospect of joining financial assets and resources more appealing. The decision to pool finances might then in turn increase habitual discussions and check-ins with the partner and further increase the quality of financial communication between partners.

Theoretical contributions

The present research examines a novel outcome of financial interdependence: communication about finances with the partner. While prior research has shown account pooling to be connected to overall relationship evaluation (Addo & Sassler, 2010; Gladstone et al., 2022; Kenney, 2006; Olson et al., 2023; Vogler et al., 2008), the present studies focus on a more specific behavior in relationships: how well and often partners talk about money. Using Interdependence Theory (Rusbult et al., 1998; Thibaut, 2017) to explain the association between pooling finances and financial communication, it can be argued that greater intertwining of resources creates more interdependence between partners. The present research suggests that this financial interdependence may shift daily interactions about finances in couples.

Furthermore, the present studies suggest a novel explanation for the established link between account pooling and relationship satisfaction (e.g., Addo & Sassler, 2010; Gladstone et al., 2022): Couples with joint financial accounts might by necessity communicate more about day-to-day financial issues which results in overall better communication and more relationship satisfaction. It is also possible that there are bidirectional links between relationship satisfaction and financial communication (Saxey et al., 2023) which reinforce each other, especially among financially interdependent couples. Future scholarship should test whether quality and frequency of communication about finances might mediate the established association between joint bank accounts and relationship quality.

Practical implications

Pooling finances resources has well-established benefits; common advice among clinicians might already be recommending a ‘one pot’ approach rather than separate accounts for financial resources (e.g., Cruze, 2024). The present research suggests that beyond promoting joint bank accounts, relationship counselors should emphasize the importance of communicating with their partner about finances and involving their partner in financial decisions. Talking about money may be seen as difficult or taboo (Atwood, 2012), or might be avoided as a way to avoid conflict. The present studies suggest that pooling money may promote beneficial discussions about money and expenses. Such better communication may have lasting benefits; ultimately, couples who talk about finances may become more aligned in their financial goals, which not only benefits relationships but can also help them achieve long-term financial success (Olson et al., 2023).

Constraints on generalizability

The link between account pooling and relationship satisfaction is particularly strong among those who face financial hardship (Gladstone et al., 2022). Participants in the present studies reported earning at or just above average levels for the populations they were drawn from (Median individual income $37,683, US Census, 2022). The link between account pooling and communication might be stronger for samples drawn from lower-earning populations who experience high levels of economic uncertainty or stress. Communication about finances might be particularly important among those who are in financially precarious situations.

Samples were from the United States. Culture strongly affects attitudes towards money management (Çineli, 2022) and cultural norms dictate how and when communication about financial decisions is seen as appropriate versus taboo (Atwood, 2012). Thus, findings of the present studies are limited to Western cultures with a common-wealth background. Information about educational achievements, employment type, and disability was not collected in any of the samples. These variables might meaningfully influence the way couples communicate about finances and should be included in future studies (also see Karney, 2021, for a discussion of the relevance of socioeconomic variables in relationships).

Across samples, White participants were oversampled by about 6–10% compared to the demographic make-up the population they were drawn from (cf. US census 2022). Non-White minorities in the US have more varied family economic contribution arrangements (Reyes, 2018), which may affect the degree to which finances are pooled with other family members beyond the romantic partner. The present studies can also only speak to pooling finances within dyadic relationships. It is possible that sharing financial accounts benefits communication about money among any of the account holders, regardless of relationship. On the other hand, intergenerational or extended economic households might follow different power dynamics that affect money management and communication and thus limit applicability of the current findings.

The present research examined a range of relationships, including both dating and married individuals, with widely ranging relationship lengths. Very few participants were in short term relationships of less than one year (4% in Study 1, 0.7% in Study 2, 0.3% in Study 3) and the average relationship length was more than a decade in each study, suggesting that these samples mainly represent individuals in long-standing relationships. Individuals in new relationships or those who are newly married or newly co-habiting are likely experiencing changing and varied communication patterns around finances, as they adapt to the changing interdependence of their relationship. Notably, pooling finances might become a viable option for couples only at a certain point of commitment, such as when moving in together or when becoming engaged or married. To examine the limitations of the present findings in light of relationship status, analyses controlled for marital status (Studies 1, 2 and 3) and exploratory analyses ascertained that marital status did not moderate the associations of communication with pooling finances status (Studies 1 and 2) and that the reported associations remain significant for each study when only considering married individuals (see online supplements: https://osf.io/kxvdb/).

Limitations and future directions

The present studies assessed different aspects of financial communication: the quality of communication, the frequency of discussions, and ad-hoc decisions to discuss decisions across hypothetical scenarios. However, there are many other aspects of communication that might be relevant and for which the impact of account pooling remains to be determined. For instance, the manner in which a discussion about finances is introduced between partners (Archuleta et al., 2013) or the manner in which it is resolved (Rusbult et al., 1982) might also differ depending on the financial organization of a couple’s finances. The measure of communication quality used in the present studies has been shown to have high reliability, high construct validity and predictive validity in both married and dating samples and among couples with joint or separate finances (Saxey et al., 2024). The index of financial discussion decisions correlated well with other communication measures and was judged as realistic in a pilot study (see online supplements: https://osf.io/kxvdb/). The measure of communication frequency, however, was limited in several ways: This measure was a single item that (though face-valid) had not been previously validated, and included a subjective response scale (using hyperbolic response options such as “never” or “all the time” as scale endpoints rather than factual numeric values). More research is needed to develop better measures of the many diverse aspects of financial communication between couples.

Consequences of financial account pooling go beyond communication with the partner and might extend to spending decisions. For example, purchases from joint accounts are more likely to be for utilitarian products whereas those from separate accounts are more likely to be hedonic products (Garbinsky & Gladstone, 2019). Thus, differences in spending patterns or overall spending might be another avenue explaining the link between account pooling and relationship quality. It is possible that joint accounts encourage overall lower spending, which may reduce financial stress, the negative impact of which on relationships is well documented (e.g., Dew et al., 2012).

People are often unaware or biased about the factors in their life that make for happy relationships (Fletcher & Thomas, 1996). For instance, the desire to avoid financial conflict is often mentioned as a reason for keeping finances separate (Ford et al., 2020; Koochel et al., 2020), suggesting that some couples might believe that pooled accounts link to worse financial communication. More work is needed to determine lay theories about the relational consequences of shared finances. It is possible that benefits of financial interdependence are particularly pronounced among those who hold lay beliefs about the benefits (vs. detriments) of shared finances.

Conclusions

The way couples organize and structure their financial resources might create different dynamics in the relationship. The present studies suggest that couples who pool their financial resources to a greater degree or who focus on joint financial accounts with their partner communicate better about finances and are more interested in discussing spending decisions with their partner. The decision to join finances with a partner might shape subsequent interactions with the partner and promote how well and often couples talk about their shared money.

Supplemental Material

Supplemental Material - Talk about shared money: Account pooling is associated with financial communication

Supplemental Material for Talk about shared money: Account pooling is associated with financial communication by Johanna Peetz in Journal of Social and Personal Relationships

Footnotes

Author note

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was funded by a grant of the Social Sciences and Humanities Research Council of Canada (#435-2012-1211) to the author.

Open research statement

As part of IARR’s encouragement of open research practices, the authors have provided the following information: This research was pre-registered (data collection plan, hypotheses, main analyses) – links to preregistrations available in text. The data used in the research are available. The data can be obtained at ![]() . The materials used are available. The materials can be obtained at https://osf.io/kxvdb/.

. The materials used are available. The materials can be obtained at https://osf.io/kxvdb/.

Supplemental Material

Supplemental material for this article is available online.

Note

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.