Abstract

Conflicts about money and finances can be destructive for both the quality and longevity of relationships. This paper reports on a descriptive analysis of the contents of financial conflicts in two samples. Study 1 examined severe financial conflicts in social media posts (N = 1014) from reddit (r/relationships). Eight themes were identified via thematic analysis: “unfair relative contributions” “who pays for joint expenses”, “job and income”, “exceptional expenses”, “terms of financial arrangements”, “discrepant financial values”, “one-sided financial decisions”, and “perceived irresponsibility”. Study 2 examined reports of more mundane financial disagreements recalled by married individuals (N = 481). Seven themes were identified via thematic analysis: “relative contributions”, “job and income”, “different values”, “exceptional expenses”, “mundane expenses”, “money management”, and “perceived irresponsibility”. In both samples, themes could be ordered along the dimensions of “concerns about fairness” and “concerns about responsibility”. The association of relationship outcomes (perceived partner responsiveness, couple satisfaction) with each theme and demographic predictors (income, relationship length, shared finances) were explored. Independent t-tests suggested that participants who recalled disagreements fitting the themes at the extreme ends of the two dimensions (“unfair relative contributions” and “perceived irresponsibility”) reported worse relationship outcomes. In contrast, participants recalling disagreements fitting the theme of “mundane expenses” reported better relationship outcomes.

Introduction

There are disagreements and conflict in any relationship. While money and finances are not the most frequent disagreement topic in relationships, it is one of the most persistent (Papp et al., 2009) and ultimately destructive type of conflict in relationships (e.g., Dew et al., 2012). There are many possible reasons a couple might disagree about money-related decisions and many possible issues to fight about. In the present paper, we propose a framework of themes of financial conflicts in relationships, based on a thematic analysis of a large sample of social media posts seeking relationship advice and a sample of recalled financial conflicts in married couples. The identified themes of financial conflicts in relationships link to previously studied predictors of relationship satisfaction and financial harmony, but also highlight gaps in existing research.

Frequency of financial conflicts

How prevalent are conflicts about finance and money issues in relationships? Finances were the primary reason for relationship conflict in 40% of disagreements reported among people in long-term relationships (Meyer & Sledge, 2022). The perhaps most informative study on frequency of financial conflicts to date followed 100 married couples over the course of 15 days, tracking and rating 748 conflict instances over this time (Papp et al., 2009). Conflicts about money constituted 18.3% of conflicts described by husbands and 19.4% of conflicts described by wives. Thus, money and finances were not the most frequent topic of conflict. However, money conflicts were more stressful and threatening for couples than other conflict topics (Dew et al., 2012; Papp et al., 2009).

Consequences of financial conflicts

Evidence for the detrimental effects of financial conflicts for relationships abounds (S. Britt et al., 2008; S. L. Britt & Huston, 2012; Dew, 2008; Dew et al., 2012; Dew et al., 2021; Jackson et al., 2023; Kelley et al., 2018; Kerkmann et al., 2000; Wheeler & Kerpelman, 2016). In a longitudinal study of married women spanning more than 25 years, women who reported arguing “often” about money in marriage were nearly three times more likely to divorce compared to those who “sometimes” or “hardly ever” argued about money (Britt & Huston, 2012). Financial conflicts also appear to be particularly detrimental compared to other conflicts in a large sample of couples from the National Survey of Families and Households (Dew et al., 2012; Wheeler & Kerpelman, 2016). Couples rated the frequency of disagreements about various topics in their relationship, such as chores, finances, time spent together, sex, and in-law relations. Only frequency of disagreements about finances and sex were significant predictors of divorce 5–7 years later. The link between financial conflicts and divorce remained significant even when controlling for objective financial well-being (assets, debt, income of the couple; Dew et al., 2012). In sum, financial conflicts are potentially destructive for both the quality and the longevity of relationships.

Reasons for financial conflicts

When relationship partners are having “money conflicts” (Papp et al., 2009), “financial conflicts” (Saxey et al., 2022a) or “disagreements about finances” (Dew et al., 2012; Morgan et al., 2021), what exactly are they fighting about? Information about the content of financial conflicts can be important to guide research towards understudied areas of financial conflicts. Information about how different financial conflicts might be grouped within larger themes may help understanding whether one conflict experience may generalize to adjacent experiences. For individuals in relationships, learning about the range of different types of conflicts may put their personal experiences in context and normalize experiences. Knowing different types of common financial conflicts might also help people identify and label their own experiences better. Thus, there are multiple benefits to knowing the content of financial conflicts in relationships. While research has yet to detail the content of financial conflicts directly, indirect evidence points to multiple financial variables that are linked to worse relationship outcomes and which may feature in financial conflicts between partners.

Financial Stress

One financial factor linked to relationship satisfaction are the financial struggles in the couples’ life (S. Britt et al., 2008; Kelley et al., 2018; Kerkmann et al., 2000; LeBaron et al., 2020; Totenhagen et al., 2018). Subjective financial stress among married individuals reduced not only the stressed individuals’ own perceived marital quality but also showed partner effects, where wives’ financial stress reduced their husband’s marital quality and vice versa (Kelley et al., 2018). Furthermore, daily variations in subjective financial stress predicted daily relationship satisfaction (Totenhagen et al., 2018). Thus, one type of financial conflict is likely attributable to struggling to make ends meet, perhaps due to unexpected expenses, income reduction, or recent unemployment. Partners might blame each other for losing income or emotions might run high due to financial stress. This reason for conflict might be particularly prevalent in times of economic adversity. Notably, financial struggles do not always spell trouble. In two studies, specific financial stressors (e.g., inability to pay bills, eviction) increased relationship commitment (Dew et al., 2018; LeBaron et al., 2020), as long as financial family support was present.

Spending behaviors

Another financial factor linked to relationship satisfaction is the partner’s spending behavior (Britt et al., 2008; Kelley et al., 2022; Li et al., 2020; Mao et al., 2017; Ross et al., 2017; Wilmarth et al., 2021). Perceiving the partner’s spending behavior as responsible was linked to greater relationship satisfaction (Li et al., 2020). Perceiving positive partner behaviors such as spending within a budget and investing for long-term goals were linked to better relationship satisfaction (Mao et al., 2017; Totenhagen et al., 2019; Wilmarth et al., 2021) whereas seeing the partner as ‘spender’ was linked to worse marital satisfaction (Kelley et al., 2022). Thus, partners might fight over specific financial decisions or general spending patterns they see as irresponsible or negative such as lack of budgeting or saving.

Organization of finances

Another financial factor linked to relationship satisfaction and commitment is the sharing of funds and decision-making power. Greater financial integration such as pooling finances as a couple has been linked to better relationship quality (Addo & Sassler, 2010; Gladstone et al., 2022; Kenney, 2006; Lim & Morgan, 2021; Steuber & Paik, 2014). This positive effect even occurs when experimentally assigned to pool financial resources in the lab (Gladstone et al., 2022). The benefit of joint finances has been primarily explained by perceived level of investment and the resulting commitment to the relationship. However, another factor might be that joint accounts remove potential conflicts over respective contributions to expenses – when resources are shared there is no need to argue over who pays how much and how often. Thus, some financial conflicts might be about the coordination of partners' contributions to joint expenses.

(Dis)similar values

Another financial factor relevant to relationship quality is the degree to which partners view money in the same way (Archuleta et al., 2013; Mao et al., 2017; Rick et al., 2011; Romo & Abetz, 2016; Totenhagen et al., 2019). Perceiving more shared financial values between the partner and the self (e.g., agreeing with statements such as “we have similar financial goals”) was correlated with current relationship satisfaction (Archuleta et al., 2013; Mao et al., 2017) and predicted better relationship satisfaction two years later (Totenhagen et al., 2019). In studies examining couple’s actual similarity on financial values such as saving or spending orientation (‘tightwads’ vs. ‘spendthrifts’), greater differences between partner’s saving orientation was linked to worse marital well-being, and more conflict over money (LeBaron-Black et al., 2022; Rick et al., 2011). Relatedly, in semi-structured interviews of 40 individuals in long-term, committed relationships an overarching struggle underlying people’s financial talk with their partners was about “money is everything” versus “money isn’t everything” (Romo & Abetz, 2016). Specifically, participants reported being at odds with their partner over different ideas of how much importance financial success has for one’s self-worth, or how money is prioritized over other goals such as relational well-being, or the extent to which each partner endorses materialism. In sum, shared financial values and a similar outlook on financial issues appears to be a distinct feature of financial harmony, and conversely, financial conflicts might arise from discrepant financial values and different outlooks on financial issues.

The Current Research

In the present research, we examine the content of financial conflicts in relationships. We seek to answer the research question: When couples fight about money, what do they fight about? Prior research has indirectly identified a number of possible reasons for couple’s disagreements about finances: financial stress, irresponsible spending behaviors, organization of finances (joint vs. separate), and dissimilar financial values. However, our review of the literature did not show any studies that examined the content of financial relationship conflicts inductively. To address our research question in a bottom-up, descriptive design, we conducted qualitative analyses of two samples capturing financial conflict discussions. One sample captured relatively more severe conflicts and provided a large range of conflict experiences: In Study 1, we conducted a thematic analysis of social media posts about financial conflicts on a forum dedicated to relationship advice. In a second sample, we captured more mundane, minor, financial conflicts: In Study 2, we recruited married individuals and asked them to recall a recent financial conflict with their partner. We coded these recalled conflict descriptions qualitatively and also examined their link with other self-reported relationship variables correlationally.

Study 1

Given that conflict situations are an irregular occurrence (Papp et al., 2009) and financial conflicts are just a subset of these situations, it is a challenge to find a sufficiently large and diverse sample of different financial conflicts among relationship partners. To this end, we drew our data from a large diverse pool of financial conflict descriptions existing on social media advice forums. Specifically, we conducted a thematic analysis (Braun & Clarke, 2012; Clarke et al., 2015; Terry et al., 2017) of posts on r/relationships of the social media page reddit. This particular forum specializes in relationship advice and allows anyone to post descriptions of their relationship problems, soliciting anonymous advice from other forum users. The posts analyzed in this study thus represent spontaneous financial conflict descriptions from people struggling with a conflict in their relationship. Other work has analyzed the content of reddit posts (Apostolou, 2019; Kimiafar et al., 2021) and descriptions on this social media page provide rich detail and information, as well as having the advantage of candidness due to the writer’s anonymity.

Method

Data retrieval

The data was collected using an original Python script that was connected to an open-domain access token for Reddit API (application programming interface). The search parameters of the script were restricted in several ways. First, the search engine was set to only collect posts from the “r/relationships” subforum of the Reddit website. In terms of query keyword, only posts that included the words “money” or “finance” keywords in their text were collected from the overall pool of posts available on the forum (no derivatives of these words were included as keywords). Posts were set to be collected between midnight (12:00:00) on January 1, 2021, to midnight (23:59:59) on December 31, 2021. Additionally, English was set as the primary language of communication, therefore no posts in any other languages were recorded.

Data screening

The total number of posts retrieved from r/relationships was 8,673. As this was an unmanageable number of posts to individually screen, we considered only those posts that received attention by other users, i.e., had garnered at least 10 comments (n = 3,488). Selecting for posts that received more comments ensured that we focused on posts that described an issue comprehensively and intelligibly (see Kimiafar et al., 2021, for a similar selection procedure). The average number of comments for the retained posts was 52.70 comments (SD = 80.53). These 3,488 posts were read in full by one of three coders and were screened for two eligibility criteria: Posts were included if they were about a current romantic relationship (posts about ex relationships, hypothetical future relationships, or non-romantic relationships were excluded) and if they were about a financial conflict (posts that were not about a financial conflict but mentioned money or finances coincidentally were excluded). A total of 1,014 posts were deemed eligible and formed the set of posts used in the thematic coding. These posts represent a total body of text comprising 571,070 words (average length of posts was 565.18 words, SD = 425.19).

Data coding

First, two researchers read all 1,014 eligible posts and collected a list of unique elements occurring across the described financial conflicts in relationships (i.e., “codes”). Coders did not consider existing research in their initial code compilation and took a completely data driven approach in identifying codes. This list comprised 47 initial codes. Posts were then coded using the software Nvivo. Posts were coded on a sentence-level, where any information pertaining to the poster’s financial conflict situation was assigned to the relevant code. If a sentence was deemed relevant to multiple codes, it was coded to multiple codes. Information not pertaining to a financial conflict was not coded.

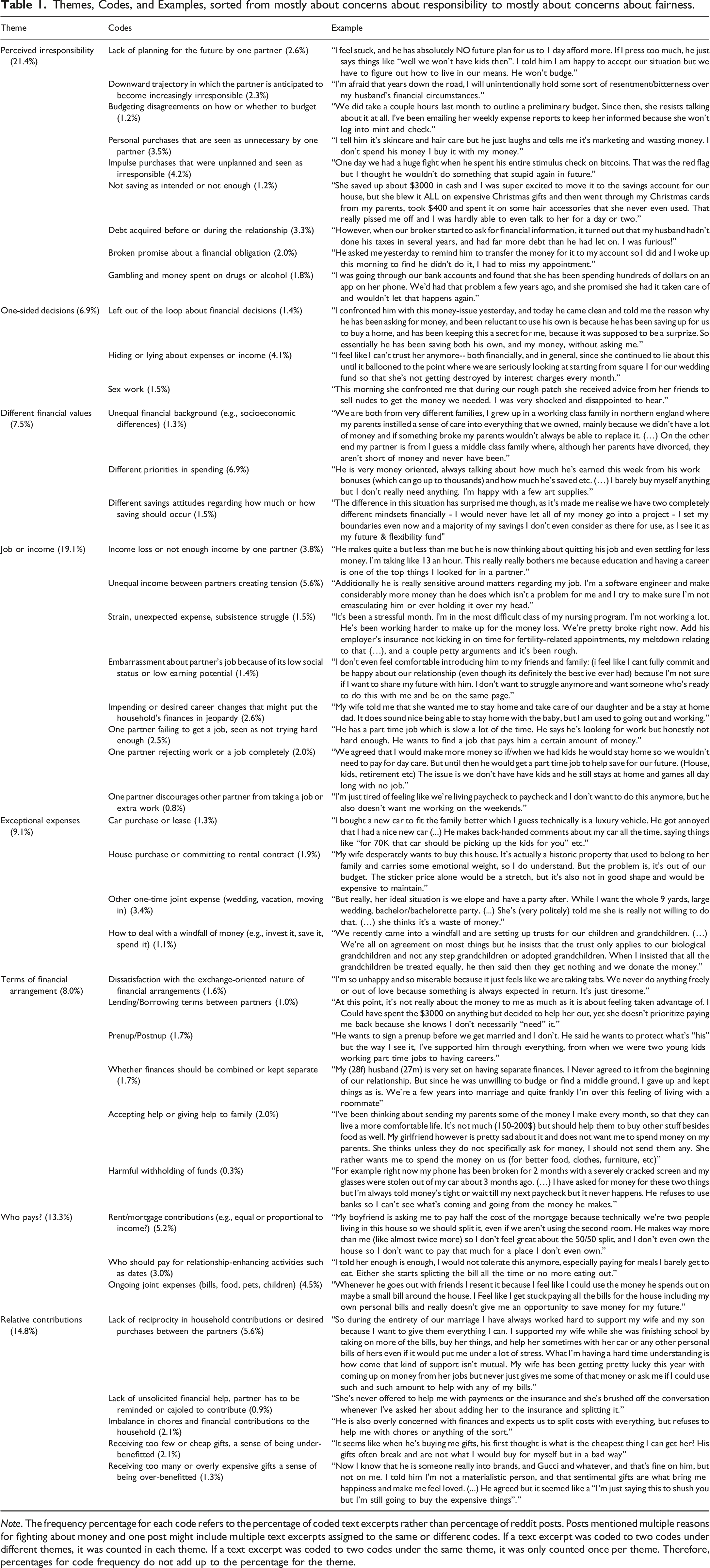

Themes, Codes, and Examples, sorted from mostly about concerns about responsibility to mostly about concerns about fairness.

Note. The frequency percentage for each code refers to the percentage of coded text excerpts rather than percentage of reddit posts. Posts mentioned multiple reasons for fighting about money and one post might include multiple text excerpts assigned to the same or different codes. If a text excerpt was coded to two codes under different themes, it was counted in each theme. If a text excerpt was coded to two codes under the same theme, it was only counted once per theme. Therefore, percentages for code frequency do not add up to the percentage for the theme.

Across all steps of the coding process, an additional 26 posts were deemed ineligible upon closer reading (e.g., because they described conflicts that were not truly financial in nature or were about the form rather than the content of the discussion such as emotional escalation) leading to a total of 988 coded social media posts about a financial conflict between romantic relationship partners.

Thematic analysis

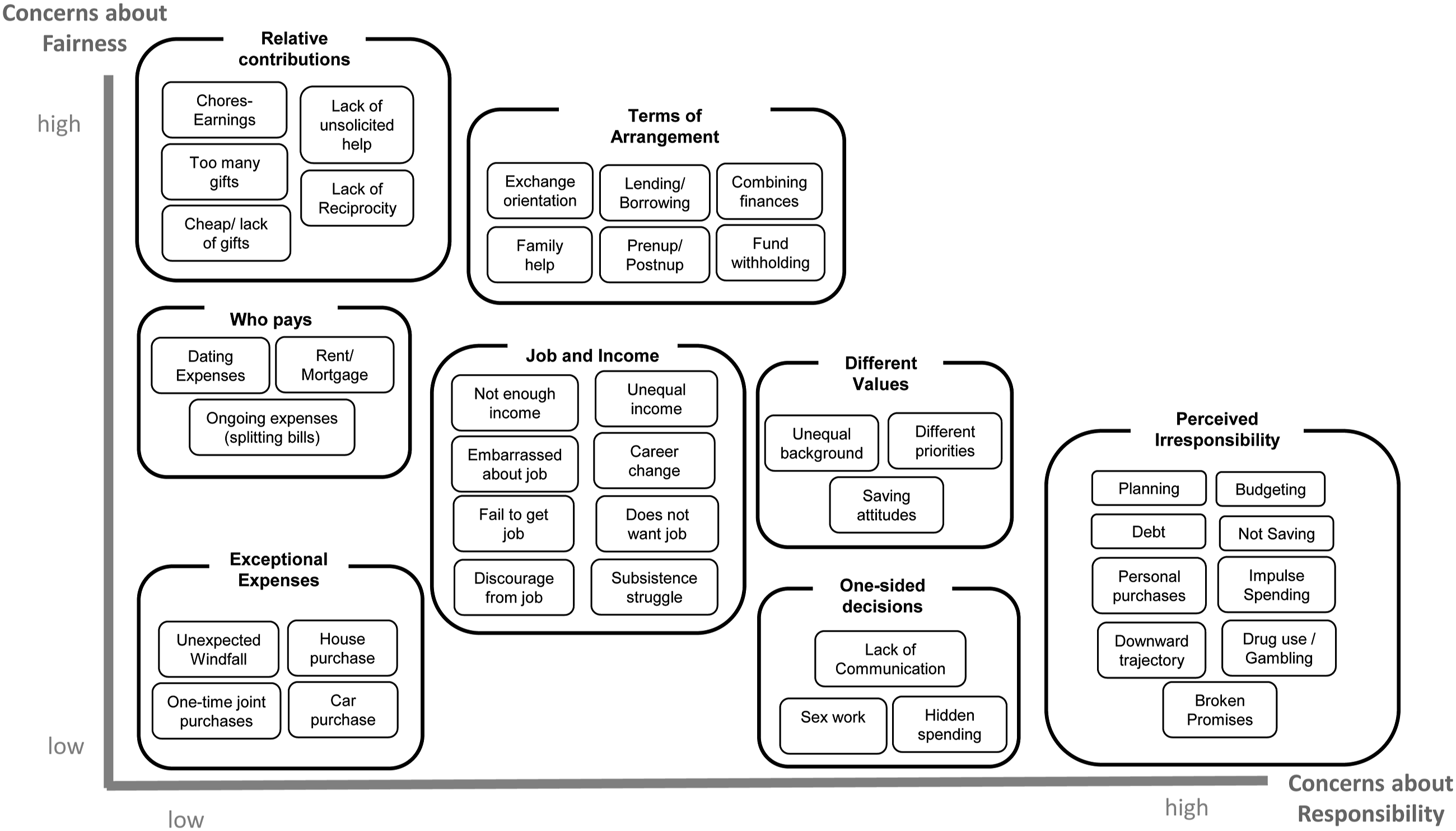

In a discussion among all three researchers, the codes were collapsed into nine themes. In a thematic review, two researchers read through all coded data extracts assigned to each theme, to determine if these data extracts formed a coherent, consistent and distinctive pattern pertaining to the theme. In this process, two themes were folded into one theme due to high overlap, resulting in eight themes. In this thematic review, coders judged that the data extracts fit the eight themes well. The list of themes can be found in Table 1. Further discussion suggested that these themes could be ordered within the dimensions of two overarching themes of “concerns about fairness” and “concerns about responsibility”.

Researcher bias

Coders were White women of middle-class Western background. One of the coders was familiar with some existing research on finances and relationship research in a general, the two main coders were naïve to existing theories and research about finances.

Results

Themes and Codes are depicted in Figure 1 and described in Table 1. The eight themes each included several codes, listed in Table 1 along with examples. The frequency of text excerpts pertaining to each theme and code (i.e., the number of statements coded to the theme or code) are listed in Table 1. Themes were ordered along two dimensions: one dimension capturing “concerns about responsibility” of the partner’s financial decisions and another dimension capturing “concerns about the fairness” of financial decisions in the relationship. By far the most frequently mentioned theme was “perceived irresponsibility” by the partner (21.4% of text excerpts coded to this theme). This theme was linked to the theme of conflicts about “one-sided financial decisions” and the theme of “different financial values” between partners, with conflict description frequently touching on both of these themes. The second most frequently mentioned theme was about “jobs or income” (19.1% of text excerpts coded to this theme), which pertained to the overarching theme of irresponsibility to a lesser degree and also sometimes referenced the theme of fairness (e.g., when one partner’s lack of income impinged on the household’s financial situation). The third most frequently mentioned conflict theme was about perceived unfairness in “relative contributions” to the household (14.8% of text excerpts coded to this theme), which often co-occurred with the theme about “who pays” for joint expenses and “terms of financial arrangement”. Themes and Codes of Financial Conflict in a Social Media Sample (Study 1).

Discussion

A thematic analysis of social media posts about financial conflicts showed that the content of these posts seeking advice or describing struggles could be organized along two overarching dimensions – concerns about fairness and concerns about responsibility – and included eight themes and 41 unique conflict topics within these themes.

One advantage of examining spontaneous unsolicited financial conflict descriptions in anonymous relationship advice forums is the diversity of conflicts and the diversity of ‘participants’. It was evident from the descriptions that individuals were in vastly different life situations, relationships, and social economic situations. This diversity also prevents generalizability of findings to specific groups – some themes might only be relevant to dating couples who do not live together, some might only be relevant to long-term married couples with children. In this sample, the demographic make-up of the sample is unknown and cannot be linked to specific themes. An additional limitation to generalizability is that social media posts might specifically select for ongoing conflicts in a relationship that remain unresolved, and thus selects for more severe financial conflicts that relationship partners feel they cannot discuss with real-life friends or family or solve on their own. Thus, these types of conflicts might differ from more mundane and minor financial conflicts.

Study 2

The second study focused on more minor, mundane financial conflicts. This study also assessed demographic make up of participants, to allow for a comparison of themes with regards to relationship characteristics and conflict characteristics. This study elicited recalled financial disagreements in the recent past from one member of the couple. Recalled conflict descriptions were coded independently from the themes found in Study 1. This inductive rather than deductive process allows for the identification of different themes of conflict in this second sample. However, in an additional analysis, we also coded all disagreement descriptions according to the 41 codes and eight themes identified in Study 1, to examine applicability of these themes to this entirely different context of financial conflicts. When using the previously identified coding scheme, all themes but not all codes were represented in the data. This analysis is reported in Table OS1 in online supplements: https://osf.io/f7g2s.

Method

Participants

Participants were recruited through Mturk (Huff & Tingley, 2015) from U.S. and Canadian MTurk workers for a larger study on financial attitudes and were compensated with US$1.5 (approx. $6 hourly rate). Data were collected in May to June 2022. Several precautions were taken to ensure data quality (participants had passed Cloudresearch quality checks, completed a reCAPTCHA check before beginning the study). To ensure that participants were in a committed relationship, only workers who were registered in the Cloudresearch system as ‘married or common-law’ were eligible to participate. The initial sample included 596 participants. Of these, 116 did not report a recent financial conflict (33 did not write anything, 13 reported that they never have disagreements about finances, 13 reported a financial discussion that was not a disagreement or conflict, and 57 wrote about a conflict that was not about finances) and were excluded. The eligibility was determined by two coder’s ratings of the descriptions (agreement was very high, k = .85, p < .001).

The final sample (N = 481) included 206 men and 275 women. The majority reported a heterosexual orientation (95.4% heterosexual or straight; 1% lesbian or gay, 3.3% bisexual). In line with Cloudresearch-based eligibility requirements, 96.7% were married, 1% reported being engaged, 2.3% reported they were dating. We retained these nonmarried participants as they were in long-term relationships (range: 1–8 years, M = 3 years) and were living together, thus they fit our requirement of being in a committed common-law relationship. Across the fukk sample, relationships had lasted between 11 months to 56 years (M = 16 years, SD = 10.8 years; Md = 13 years), 73.2% of the sample had children and 98.3% were living together. Participants were between 19 and 78 years old (M = 43.27 years; SD = 11.71, Md = 40) and the sample was predominantly White (80.7% White 7.5% Black or African-American, 6.2% of Asian decent, 3.7% Hispanic). Frequency distributions for age and relationship status are available in online supplements: https://osf.io/f7g2s. No information on disability status or social class was assessed. Income ranged widely but the combined income between the self and the partner was, on average, in the $90,000 to $110,000 bracket (which is similar to the 2019 US median for married couple households: $96,930). About half of the participants (59.7%) reported fully joint finances, and 40.3% reported separate or partly separate finances.

Procedure

Participants first completed a demographic survey and the 16-item Couple Satisfaction Index (Funk & Rogge, 2007) on 6-point scales. Items were averaged into a Couple Satisfaction Index (α = .96; M = 4.76, SD = .98). Participants were instructed to recall and describe a recent financial disagreement (i.e., “Now please think of a recent disagreement with your partner where you were discussing financial decisions and money habits. Please describe the disagreement briefly here”). On average, participants wrote 31.79 words (SD = 23.98). After the disagreement description, participants reported how responsive and understanding they felt their partner was during the financial disagreement (4 items, Van Erb et al., 2011, “During the discussion about this financial topic… - My partner was understanding toward me.”, “I felt supported by my partner”, “I felt I was valued in our relationship”, “My partner treated me with respect”) on a scale from Not at all (1) to The whole time (5). Items were averaged into an index of responsiveness during the conflict discussion (α = .95; M = 3.74, SD = 1.15). No other questions about the disagreement description were included in the survey. Full survey and data are available at https://osf.io/wy9tj/.

Data coding

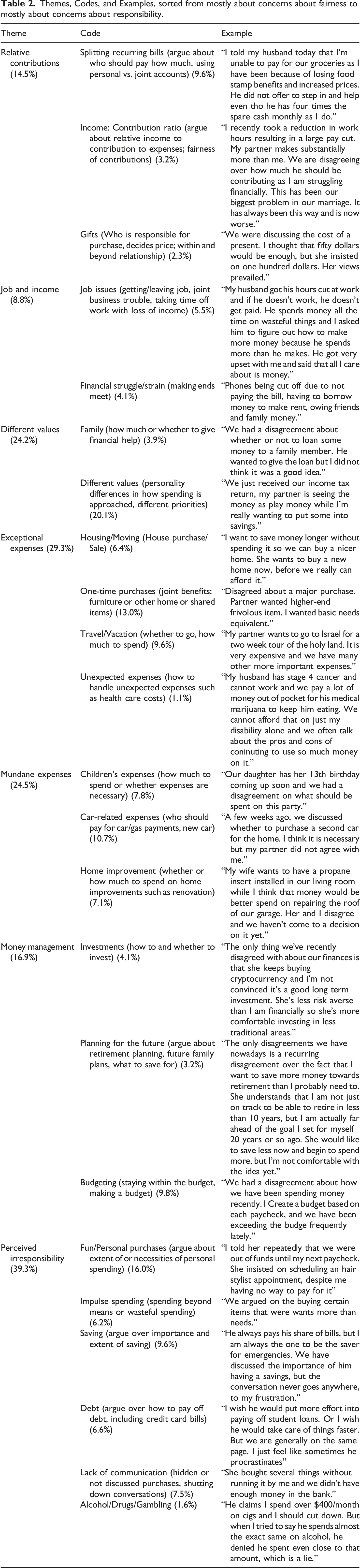

Themes, Codes, and Examples, sorted from mostly about concerns about fairness to mostly about concerns about responsibility.

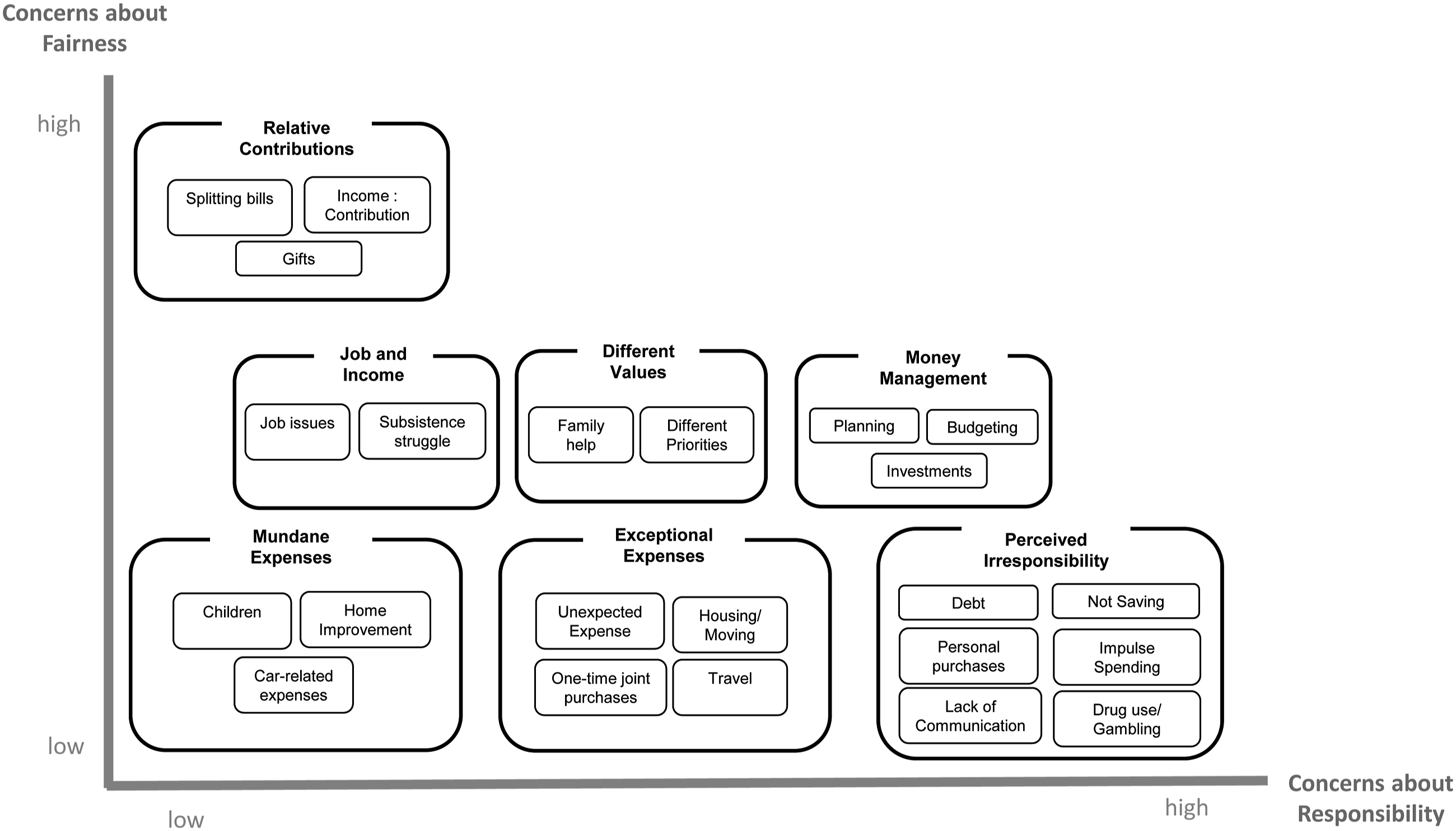

Next, codes were collapsed into larger-order themes. Seven themes were created in discussion among coders that aggregated the codes (Figure 2). As in Study 1, two overarching themes of “concerns about fairness” and “concerns about responsibility” organized the themes. Compared to Study 1, three themes did not emerge in this study: The theme of “who pays” did not emerge in this analysis, with related codes being folded into “relative contributions” and the new theme “mundane expenses”. The theme “terms of arrangement” was not present in Study 2 though some conflicts touched on codes included in this theme (Family help), which were folded into “different values” as the conflicts described therein concerned fundamental philosophy clashes. The theme “one-sided decisions” was not present in Study 2 though some conflicts concerned content included in this theme (Hidden Finances, Lack of Communication), which were folded into perceived irresponsibility”. Finally, two new themes emerged in this study: “mundane expenses” and “money management”, both of which included disagreements about minor day-to-day financial decisions. Themes and Codes of Recent Financial Disagreements in a Married Sample (Study 2).

We calculated weighted Kappas to examine the interrater reliability for each theme. Interrater agreement was substantial for “relative contributions” (k = .62), “exceptional expenses” (k = .74), “mundane expenses” (k = .78), and was on the high end of moderate for “perceived irresponsibility” (k = .58), “money management” (k = .59), “job and income” (k = .59), and was lowest, but still moderate, for “different values” (k = .41).

Results

Themes and Codes are depicted in Figure 2 and described in Table 2. The themes each included between two to six individual codes. The frequency of themes and codes are listed in Table 2 and are based on the number of disagreements that were coded as referencing each theme by either one of the coders.

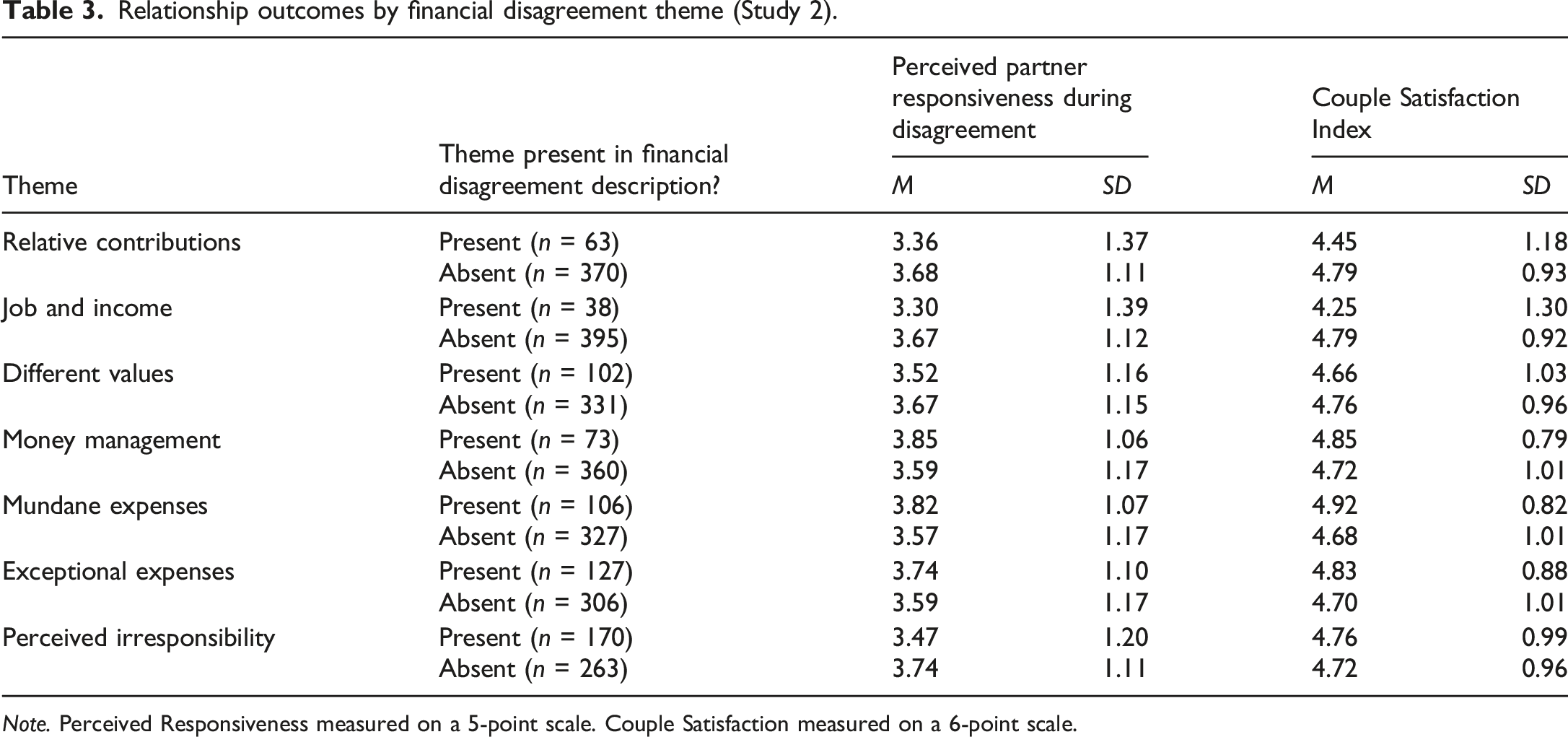

Relationship outcomes by financial disagreement theme (Study 2).

Note. Perceived Responsiveness measured on a 5-point scale. Couple Satisfaction measured on a 6-point scale.

Next, we examined whether demographic characteristics were associated with specific themes of financial disagreements. In logistic regressions, we entered relationship length, couple income, and joint finances (0 = partly or fully separate; 1 = fully joint) as predictors and each of the seven themes as outcome, respectively. Across all seven logistic regressions, only the models predicting “relative contributions”, “job and income”, and “different values” were significant (See Table OS2 in online supplements [https://osf.io/f7g2s] for all regression coefficients). Specifically, higher couple income predicted less presence of the theme “relative contributions”, B = −.12, SE = .04, Exp(B) = .89, p < .001, and less presence of the theme “job and income concerns”, B = −.15, SE = .05, Exp(B) = .86 p < .001. Relationship length predicted more presence of the theme “different values”, B = .002 SE = .001, Exp(B) = 1.00, p = .011. Joint versus separate finances did not predict any of the themes, however, replicating prior research (Addo & Sassler, 2010; Gladstone et al., 2022; Kenney, 2006) those with joint finances reported better relationship outcomes (perceived responsiveness: t (346.20) = 4.07, p < .001, d = .41; couple satisfaction: t (307.45) = 3.60, p < .001, d = .37).

Discussion

A thematic analysis of married individuals’ recalled financial disagreements suggests that the content of these descriptions could be organized along two overarching dimensions as the social media conflicts in the previous study – “concerns about fairness” and “concerns about responsibility”. Those financial disagreements that were at the extremes of these dimensions were associated with most detrimental relationship outcomes in this sample of married couples. Conversely, married couples that were discussing, even in disagreement, mundane everyday expenses and spending reported more positive relationship outcomes.

General Discussion

This research contributes to an understanding of the role of finances in romantic relationships, specifically financial conflicts in relationships. Information about themes of financial conflict among advice seekers on social media and about themes of financial disagreements among married couples might guide future research and might contextualize people’s own experiences. In times of economic adversities such as the widespread cost-of-living crisis and economic recession (e.g., CBC, 2022; NYT, 2023), managing these financial pressures is particularly critical. Understanding the content of financial conflicts and their links to relationship outcomes might help identify conflict severity or whether a couple should seek help. For instance, Study 2 suggests that disagreements that include references to fair contributions to household finances and disagreements that include references to perceiving the partner as irresponsible are particularly detrimental to relationships. Couples who find themselves arguing about these types of financial conflicts might be particularly in need of intervention. Conversely, Study 2 also suggested that disagreements about daily mundane expenses were associated with better relationships. This might be an indicator of beneficial relationship practices – communicating about small financial decisions might prevent more detrimental conflicts later.

There was considerable overlap between the two samples: overarching themes of fairness and responsibility were relevant in both studies, and several themes were found in both instances (“relative contributions”, “exceptional expenses”, “job and income”, “different values”, and “perceived irresponsibility”). Other themes emerged primarily in the social media sample (e.g., “who pays”; “one-sided decisions”; “terms of arrangement”) – perhaps not surprisingly, as this sample included a much wider range of types of conflicts. Two themes emerged primarily in the married sample (“mundane expenses”; “money management”) – reflecting the relatively low stakes, day-to-day disagreements that made up the financial conflict descriptions in this study. Also notable was that while developed independently of existing lines of research in the relationship literature, the themes identified do reflect previous research on related topics.

Research related to the identified themes

The theme of ‘irresponsible decisions’ as a topic of financial conflicts may reflect past research findings that positive spending behaviors – mostly defined as contributing to saving accounts – are linked to better relationship satisfaction (e.g., Li et al., 2020; Mao et al., 2017; Ross et al., 2017; Wilmarth et al., 2021). This theme might also reflect the link between partner instrumentality to goals and the closeness someone feels for that partner (e.g., Fitzsimons & Fishbach, 2010): Perceived irresponsibility in a partner might create conflict as it threatens one’s own financial goals.

The theme of ‘different values’ reflects research on the benefits of feeling similar to one’s partner (e.g., Acitelli et al., 2001), and the benefits of perceiving shared financial values (Archuleta et al., 2013; Mao et al., 2017; Totenhagen et al., 2019). One reason for this beneficial effect of similarity in financial values is that couple who share values are better able to communicate about financial issues (LeBaron-Black et al., 2022), underlining the possibility that they might have fewer or more productive disagreements about money.

The theme of “one-sided decisions” might relate to research in financial deception and secret consumption behavior. Research on relational consequences of financial secrecy has been mixed. Hiding financial decisions per se was not linked to relationship satisfaction in some studies (Garbinsky et al., 2020), and keeping minor consumer behaviors intentionally from one’s partner has been linked to feeling guilty and consequently making more prorelational decisions as consequence (Brick et al., 2022). However, financial deception in a large sample of emerging adults was linked to less relationship flourishing (Saxey et al., 2022b) and participants who reported having kept a financial secret from their partner reported less marital satisfaction (Jeanfreau et al., 2018). The ‘one-sided decisions’ theme might capture the conflicts that occur once the hidden financial behaviors come to light, whereas people who engage in financial secrecy successfully might not experience relational detriments to the same degree.

The theme “relative contributions” reflects research showing a strong overlap between conflicts about chores and conflicts about money (Dew et al., 2012) and that disagreements over money tend to spill over into other conflicts (e.g., Wheeler & Kerpelman, 2016). As expressed in the social media posts, considerations of what might be fair in a partnership take into account not only each partner’s earnings but also their contributions to the household in terms of chores. More generally, this theme is linked to social exchange theory that discusses the detrimental consequences of feeling over-benefitted or under-benefitted in a relationship (e.g., Cook et al., 2013) and unequal financial power in relationships (LeBaron et al., 2019). The topic of gift giving was a prominent concern in this theme and has been studied as a factor in relationships (e.g., Dunn et al., 2008).

The themes of ‘terms of arrangements’ and ‘who pays’ perhaps reflect conflicts that become more likely when partners keep separate finances rather than pay everything from one joint account. Thus, these themes might reflect research showing that couples who pool finances tend to report more relationship satisfaction (e.g., Addo & Sassler, 2010; Kenney, 2006) and fewer financial conflicts (Gladstone et al., 2022). The “terms of arrangement” theme also reflects work showing that discrepant financial roles (i.e., partners giving conflicting reports of who is responsible for managing finances in the relationship) are linked to more financial disagreements (Morgan et al., 2021).

The theme capturing conflicts about “income and job” perhaps reflects the detrimental influence of financials stress and economic struggles (Britt et al., 2008; Kelley et al., 2018; Kerkmann et al., 2000; LeBaron et al., 2020; Totenhagen et al., 2018; 2019). It is notable that in Study 2, the presence of this theme in financial disagreements between partners was most strongly linked to relationship outcomes, underlining the importance of financial worry in relationships.

Limitations and future directions

Process versus Content

Note that for consequences of financial conflicts it might matter less what the topic is than how partners discuss their conflict. For example, a soft versus hard start-up to conflict discussion can affect relationship satisfaction (Archuleta et al., 2013) and a hot versus calm conflict tactic might play a role in likelihood of conflict resolution (Dew & Dakin, 2011). Similarly, it might be the timing of when financial disagreements are raised that matters more than the content of these conflicts: Initiating financial discussions earlier in a relationship benefitted quality of financial communication between partners (Saxey et al., 2022a). Future studies should examine the types of conflict in relation to timing within the course of the relationship and in relation to how these conflicts are experienced by relationship partners.

Samples

The first study relied on social media posts, which are likely made as a last resort, by people at their wits’ end. Thus, they might represent extreme examples of financial conflict, once-in-a-relationship type of issues rather than every-day financial conflicts. On the one hand this aspect of the data leads us to capture a fuller range of possible financial conflicts, including those that are rare. On the other hand, this aspect of the data might bias the frequency of the identified themes. The second study examined much more mundane financial disagreements among married individuals and identified relatively different frequencies. Perceived irresponsibility was the most frequent theme in both samples, but conflicts about job and income were much more frequent in the social media sample than the married sample.

The marriage status of the sample in Study 2 also limits generalization of the findings. Married individuals are in an economically advantaged position, as marriage status is proxy for having the financial resources to get married in the first place, often indicates mainstream sexual orientation majority, and often means the household can rely on two incomes and two people’s contributions. Even across both studies, this research cannot draw conclusions about the frequency of themes of financial conflicts in other samples – its aim was limited to identify and explore the range of topics and themes.

Future research should examine the topic of financial conflicts in other populations. For example, there may be unique challenges associated with living together as unmarried couple, parenting young children, with living in separate households, or when living in larger multigenerational households. Similarly, some of the conflicts identified in both our studies might be irrelevant for some populations: negotiating prenups or house purchases might be relevant only to couples in specific phases of their life, and discussion on who pays for joint expenses might not apply to those couples who have fully joint finances.

Timing of data collection

Data was collected from 2021 (Study 1) and in 2022 (Study 2). Thus, the data collection of Study 1 occurred during the tail-end of the COVID-19 pandemic and associated economic struggles due to lay-offs, restricted hours, increased housing and grocery prices. Pandemic-associated financial hardship might have amplified financial conflicts (e.g., Schmid et al., 2021), just as conflict among partners may be more likely when experiencing hardship (Kelley et al., 2018; Kerkmann et al., 2000; LeBaron et al., 2020). Very few of the social media posts (and less than 0.01% of the elicited disagreements in Study 2) made references to the COVID-pandemic. The references were indirectly related to the financial conflict: for example, someone described having lost their job due to pandemic lay offs but the main financial conflict was the partner’s lack of effort in gaining new employment. Thus, it is unlikely that the pandemic introduced new types of conflict, but it might have amplified conflict that was already there.

Intersectionality and bias in qualitative coding

Qualitative analysis is subject to potential bias due to the rater’s perspective. Raters were White middle-class women who might have a limited perspective on issues related to money and power, due to their own privileged social position. Raters might lack understanding of the experiences and challenges faced by individuals from marginalized groups, who may face structural inequalities that affect their relationships and their financial situation. Participants in Study 2 were also primarily White with an average income comparable to the US average (i.e., not lower income) and might have reported conflicts with the limits of this experience. Future research should extend to specifically seek to understand the experiences and financial conflicts of lower income and minority groups.

Practical Implications

People in relationships might take away several messages from our studies. First, they might be relieved to find that disagreeing with the partner is not unusual (almost every participant could recall a recent financial disagreement with the partner when prompted), and that there is a vast range of conflict topics connected to finances, even if these disagreements are not about money at first glance. For example, many reddit users complained about the distribution of chores in the household as unfair in light of each partner’s financial contributions. Being aware of the underlying connection to financial concerns in some of their disagreements might help partners discuss and resolve these conflicts better. Second, as counterpart to considering financial connections more, couples who argue about individual financial decisions might consider underlying concerns more. Partners could reflect whether their deeper concerns about fairness and irresponsibility might bias their view of a specific financial disagreement. Being aware of these potentially underlying larger concerns about the partner’s attitudes might put individual financial disagreements into context. Third, as disagreements about everyday mundane financial issues were linked to more positive feelings about the partner and the relationship, people might find that discussing small everyday financial decisions with the partner can be beneficial. Staying in touch with the partner’s financial perspective through repeated discussions about day-to-day purchases might prevent the festering of small disagreements into larger concerns.

Conclusions

Discussions of money remain one of the ‘last taboos’ (Petronio, 2002) in Western culture. However, financial concerns are particularly threatening to people as they put not only psychological but physical well-being at risk (e.g., eviction, food insecurity). Financial concerns might also be particularly threatening to romantic relationships because of the interdependent nature of living in the same household, with joint expenditures. This research identifies themes to organize the topics of people’s financial struggles with their romantic partner. These themes of financial conflicts might provide a stepping-stone for future research on financial conflicts in relationships or the role of finances in relationships more generally.

Supplemental Material

Supplemental Material - When couples fight about money, what do they fight about?

Supplemental Material for When couples fight about money, what do they fight about? by Johanna Peetz, Zoe Meloff, and Courtney Royle in Journal of Social and Personal Relationships.

Footnotes

Acknowledgement

We thank Thalia Charlebois, Erika Doucette, Odin Fisher-Skau, Ari Melikhova, and Sienna Miller for research assistance.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research was funded by a grant of the Social Science and Humanities Research Council of Canada (#435-2012-1211) to the first author.

Open Research Statement

As part of IARR’s encouragement of open research practices, the authors have provided the following information: This research was not pre-registered. The data used in the research are available. The data can be obtained at ![]() . The materials used in Study 2 are available. The materials can be obtained at https://osf.io/wy9tj/?view_only=b3ddb5db95ee4b97b65ef02c8e8db5b1

. The materials used in Study 2 are available. The materials can be obtained at https://osf.io/wy9tj/?view_only=b3ddb5db95ee4b97b65ef02c8e8db5b1

Supplemental Material

Supplemental material for this article is available online

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.