Abstract

Development plans across the Gulf Cooperation Council emphasise logistical infrastructure as a driver of economic diversification. Investments in maritime ports, roads, rail, airports and logistics cities are transforming the economic geography of the region. This study aims to make visible this neglected aspect of the physical transformation of the Gulf Cooperation Council with a focus on the understudied maritime container ports in Oman and Qatar. Shifting the analysis to emergent maritime logistical infrastructure at a regional level gives insight into the uneven developments within the Gulf Cooperation Council’s integration project. Three key features emerge: (a) a large degree of duplication in maritime port infrastructure across Gulf Cooperation Council states; (b) a regional hierarchy among Gulf Cooperation Council states that are resource rich and those dependent on public–private partnerships and (c) increasing competition among internationally dominant port operators looking to gain access to the Gulf Cooperation Council maritime port market. These features both reflect and reinforce competitive tensions within the regional integration project.

Introduction

The suspension of diplomatic ties and effective blockade of Qatar by Saudi Arabia, the United Arab Emirates (UAE), Bahrain and Egypt which came into effect in June 2017 brought to the fore the unevenness within the Gulf Cooperation Council (GCC)’s logistical infrastructure. 1 Most strikingly, the maritime and air blockade disrupted trade routes into Qatar with many commentators raising the spectre of possible food and other commodity shortages. These prospective shortages were a direct result of Qatar’s underdeveloped maritime routes and its reliance on Dubai’s Jebel Ali Port for basic imports. In a move that went virtually unnoticed in the international press coverage of this crisis, one of Qatar’s responses to the blockade was the use of Omani ports as an alternative to Jebel Ali’s conventional role as a gateway to the region. Within days of the crisis, Maersk Line announced its Qatar coverage plan, utilising a feeder line from Salalah Port; Qatar Ports Management simultaneously launched two direct shipping services linking New Hamad Port with Oman’s Sohar and Salalah (Reuters, 2017). The basic logistical problems facing Qatar in the wake of the suspension of ties with its powerful neighbours points to the uneven patterns, tempo and future direction of logistics in the Gulf. While the GCC is often analysed from the prism of the hydrocarbons trade, a focus on logistical infrastructure is revealing of the regional tensions and hierarchies.

Over recent years there has been an increasing scholarly interest in analysing the ‘science of business logistics’, namely the significant shifts in the conception and management of commodity circulation in the global economy through complex supply chains across networked transport infrastructure, logistics hubs and trade corridors (Bonacich and Wilson, 2008; Cowen, 2014; Mezzadra and Neilson, 2015; Sekula and Burch, 2011). While Cowen rightly dates ‘the most significant conceptual and calculative shifts underpinning the logistics revolution’ to the 1960s and investment in intermodal infrastructures to the 1970s, it was in 1990s that ‘the capacity for countries to participate in the physical circulation of global trade became itself a measure of development’ (Cowen, 2014: 58). 2 Neoliberal policies, diffused through international institutions, helped to foster this trend and have come to dominate development planning at the state level. The rise of these logistics networks is thus closely connected to the globally structured character of commodity circulation in contemporary capitalism, which ‘can be assured only through the creation of an efficient, spatially integrated transport system’ (Harvey, 2006: 377). Harvey notes, however, that the concrete form of these infrastructures of circulation needs to be understood in relation to existing patterns of capitalist accumulation, as ‘revolutions in productive forces within the transport industry always have location specific effects’ (Harvey, 2006: 378).

This article aims to map and analyse such ‘location specific effects’ in the context of the GCC, a region largely neglected in the critical literature on logistics spaces. Whereas the corporate press is rife with information about opportunities in the GCC logistics market, scholarly work analysing this development lags behind. Most work on maritime infrastructure in the Gulf has focused on the emirate of Dubai, as the location of the Gulf’s largest ports and the Gulf city most integrated into global trade networks (Akhavan, 2017; Jacobs and Hall, 2007; Ramos, 2010). Although Dubai’s Jebel Ali Port will feature heavily in the following analysis, my aim in this paper is to examine the emerging logistical hierarchies in the region and situate the development of Gulf maritime ports within the broader context of the GCC regional integration project, contributing a regional perspective to the logistics literature. There is a need to move beyond the Dubai-centric character of much of the logistics literature to more fully incorporate the wider dynamics of the GCC as a whole and to take full account of the impact of rapid absorption into internationalised logistics chains on specific regions.

While the logistics literature has largely focused on the major logistical nodes in the Global North and/or East Asia, broadening the literature to incorporate emergent maritime infrastructure across regions allows us to examine the contradictory and uneven developments in logistics space. Authors examining business logistics have rightly argued that logistical systems modelling looks to construct an uninterrupted space of supposedly seamless trade, forging globally integrated networks. Yet, despite its totalising ethos, logistical modelling incorporates states and specific cities into global logistics chains differentially. In the case of the GCC, it has led to a contradictory process of infrastructural duplication and increased competition among both states and global port operators to dominate the important trade route. I argue for a more critical theorisation of unevenness in the development of logistics across regional spaces, in other words an understanding that the logistics revolution remains an unfinished and contested process which in particular instances may accentuate regional hierarchies.

In carrying out this analysis, I pay particular attention to the construction of container ports and industrial zones in Oman and Qatar. For the past 10 years, Oman has stood at number three regionally in terms of container throughput, and there are plans for massive expansion in its maritime and logistical infrastructure. Much more recently, Qatar has identified expansion of ports and associated logistical infrastructure as a key strategic priority, largely associated with the country’s successful bid for the 2022 World Cup. Although Qatar’s expansion of maritime infrastructure is still at an early stage, it is now the site of the largest transport infrastructure projects in the GCC. The recent crisis facing Qatar has highlighted the uneven logistical terrain across the region, yet the solutions found through Oman’s ports highlight the different moments of logistics development in the GCC. By looking at these emergent maritime infrastructures in their regional context, we can see the ways that hierarchies across the GCC are accentuated and reinforced by the development of the logistics sector in places other than the dominant ports of the UAE. The current crisis has highlighted the significance of Qatar and Oman in particular. On one hand, Qatar’s reliance on Jebel Ali became all too apparent. Oman on the other hand holds a particular mediating role and has positioned its logistical infrastructure to be able to circumvent Jebel Ali’s dominance as has happened in this case. The specific entry of international port operators through public–private partnerships, elaborated below, has given the non-oil rich state leverage at the regional level, at the same time allowing international port operators to take advantage of regional tensions, quickly moving to absorb any business lost by Jebel Ali. The two cases highlight the contested impact of the logistics revolution in the region and are particularly revealing of the emerging geo-spatial politics of the GCC.

A focus on Qatar and Oman reveals that while the GCC is avowedly about collective security and closer economic and political integration, it is also simultaneously a project riven by competitive tensions and existing hierarchies between the various Gulf states. These two cases in particular, due to their positioning in the regional order, and in light of the recent crisis, expose the key features of this contradictory process: (a) a large degree of duplication in port infrastructure in the region; (b) divergent modalities of logistics development that are particularly marked by differences between those GCC states that are resource rich and those dependent on public–private partnerships to develop their transport infrastructure and (c) increasing competition among internationally dominant port operators looking to gain access to the GCC maritime port market. All of these trends act to accentuate the hierarchical structure of the GCC itself, and in turn act back upon the potential future trajectories of logistics infrastructure at the national level.

The article begins by outlining some of the recent academic insights into the global logistics industry and the position of the GCC within this. I then turn to examining the development of four specific container ports in Oman and Qatar (Sohar, Salalah, Duqm in Oman and New Hamad in Qatar). Each of these emerging ports is under either construction or re-development, and, as a result, the expected capacity growth over the next five years will considerably shift the economic geography of trade in the GCC. The discussion draws upon extensive multi-year fieldwork in the region, including attendance at regional logistics industry conferences, tours of major ports, and semi-structured interviews with managers and legal experts drawing up public–private partnerships in the region. After mapping these changes across Oman and Qatar, I turn to situating these port developments within the wider GCC frame, arguing that these new projects likely herald a major shift in political and economic relations in the Gulf over the coming years.

The ‘Logistics Revolution’

The focus on constructing mega transport infrastructure and creating logistics hubs in the GCC is in line with what researchers have termed the international revolution in logistics (Allen, 1997; Bonacich and Wilson, 2008). As a ‘science of circulation’ (Cowen, 2014: 25) business logistics manages commodity circulation across internationalised supply chains, attempting to produce supposedly seamless and secure trade. Central to the globally structured character of commodity circulation in contemporary capitalism is the logistical cartography of networked infrastructures, trade corridors, gateways and logistics hubs. In other words, internationalised patterns of production and consumption are mapped onto a ‘landscape of logistics in which more land area is given over to accommodate the shipment, staging and delivery of shipped goods’ (Waldheim and Berger, 2008: 220).

The main features of the logistics revolution took shape during what McNally described as a ‘major spatial-geographical reorganization of capitalism’ in the neoliberal period, ‘with the massive development of global sweatshops, many located in low-wage and capital-friendly export processing zones that gave rise to new centres of global accumulation, most notably in China’ (McNally, 2011: 44). Related to this shift, a substantial body of literature has discussed and debated the ‘international division of labour’ and ‘global commodity chains’ (Bair and Werner, 2011; Jenkins, 1984). Enabling this ‘major spatial-geographical reorganisation’ to take shape was a series of technoscientific shifts in the transport industry. For example, standardisation, closely linked to the introduction of the shipping container, as well as increased reliance on information technology, helped to speed up circulation and manage production and distribution along internationalized supply chains through different modes of transport (Levinson, 2008; Notteboom and Rodrigue, 2009). Critical authors have discussed such technoscientific developments and management techniques at the core or the logistics revolution and traced its origins in the field of military logistics. An important consideration in the literature on the logistics revolution has been labour’s ability and its unique position to contest such logistics space by disrupting trade routes. Neilson explains, for example, ‘logistics workers have realized they hold a strategic position in global production systems’ (Neilson, 2012: 331). Although forms of contestation are also space specific and logistics chains tend to incorporate highly uneven modalities of labour.

The palpable changes in the sinews of commodity trade have been reflected in academic debates about maritime ports specifically, with theorists urging a ‘re-think’ of the port (Olivier and Slack, 2006: 1409) in the context of global supply chain management (Robinson, 2002; Song and Panayides, 2008). Studies focused attention on the changing ‘geography of port terminal operators’ within integrated international networks (Notteboom and Rodrigue, 2012: 249), as increasing privatisation of typically state-operated infrastructure resulted in the expansion and consolidation of privately owned global terminal operators. One consequence of this has been the internationalisation of global network terminal operators (GNTs) (Notteboom and Rodrigue, 2012; Olivier and Slack, 2006; Slack and Frémont, 2005), with port operations divided among a handful of influential global corporations overseeing an integrated international network of terminals. Harvey, among others, has pointed to the production of such immense concentrations of corporate power in the transport sector (Harvey, 2011). Today, the top five GNTs are Hutchison Port Holdings (HPH), Cosco Shipping Ports, APM Terminals, PSA International and Dubai Ports World (DP World); in 2015, these five firms controlled a remarkable 49.2% of total world container throughput (DP World Limited, 2017: 11). Anderson has noted that such ‘Global Network Terminal Operators have not only driven the privatisation of the port sector, but also led the development of the port sector in the world’s new trading zones, and often in countries where independent unions are either historically weak or altogether illegal’ (Anderson, 2013: 129). This shifting terrain of GNTs has in turn had regionally specific implication in the GCC, accentuating competitive tendencies as discussed below.

Aside from the overarching trends towards concentration and privatisation of maritime port assets, the specific technoscientific innovations associated with logistics have also given the industry a role in constructing economic space. For example, mega container ships, which have doubled in capacity in a decade, ushered the developments of mega-container ports. This is especially significant in the context of the GCC because states are devoting massive lands, reclamation projects and resources to constructing such ports. Yet, another spatial reconfiguration has been, a Dubai innovation, the logistics city – a space dedicated in its totality to the circulation of commodities through warehousing, packaging and the like (Cowen, 2014: chapter 5). The impact of such spaces on the economic geography of the GCC has been stark and largely under theorised.

GCC logistics space

The GCC has become a central node in the worldwide circulation of commodities. The reasons for the growth of the Gulf’s logistics infrastructure relate to its strategic geographic location along the Asia–Europe trade route, which has propelled massive levels of expenditure on mega transport infrastructure in various GCC states, including ports, airports, trains and roads. More than 60% of the total expenditure on ports in the Middle East is located in the GCC. 3 Both new mega port construction and expansion of existing ports are taking place, with new, highly automated ports designed to accommodate the largest container ships in the world. These port projects are also integrally linked to the development of wider logistics networks, including passenger and freight railway schemes, airports, special economic zones and so-called logistics cities. Even in relation to humanitarian assistance in the conflict-ridden wider Middle East region, Dubai’s International Humanitarian City has become the regional logistics centre, hosting nine United Nations agencies.

Although there had been strong trade ties between the GCC, South Korea and Japan previously, China’s insertion into the global economy, in particular, prompted a substantial increase in the export of oil, gas and petrochemical materials from the GCC region eastwards, and very significantly, in reverse, the import of a vast array of commodities from East Asia for internal GCC consumption and re-export to Europe and other areas. 4 The ensuring consolidation of domestic GCC conglomerates, especially in the construction and retail sectors, helped to cement the GCC as a significant import zone for commodities manufactured elsewhere (Hanieh, 2011). In addition to being central to commodity circulation from Asia to Europe, GCC maritime ports are also positioned as crucial feeder ports to smaller East African ports. According to the International Monetary Fund (IMF) Direction of Trade Statistics, 67% of total GCC exports are to Asia and only 18% are to the West, while 40% of total imports are from Asia and 45% are from the West.

Surprisingly, given these trends, maritime infrastructure has not featured centrally in analysis of the contemporary Gulf region. There has been a very rich discussion of urbanisation and liberalisation in the GCC, much of it focused on the city-state of Dubai, but these have typically been more concerned with the role of construction megaprojects and architectural forms, the spatiality of urban life (Acuto, 2010; Elsheshtawy, 2008, 2004), and the evolving corporatist models that underpin state–capital relations in the Gulf (Buckley, 2013; Buckley and Hanieh, 2014; Kanna, 2011). More recently, scholars have turned to looking at the ways in which these features of the Gulf urban landscape are being generalised to other parts of the Middle East, putting forward categories such as the ‘Dubai model’ (Elsheshtawy, 2010; Hvidt, 2009) and the ‘megaproject phase of development’ (Rizzo, 2014) that find their genesis in the Gulf and then spread to other Arab countries (Pierre-Arnaud, 2010). Importantly, all of these features of the Gulf’s urbanisation process are closely related to the role of maritime infrastructure and associated logistical networks, yet these have been downplayed in the general literature on the region.

Moreover, much of the critical literature on the Gulf tends to focus on individual states or cities; there is a relative neglect of the wider GCC project and its impact on national development. This is a major gap, as the changing global location of the GCC has occurred concomitantly with the deepening (albeit contradictory) integration of GCC member states (Ulrichsen, 2011). Formed in 1981, the initial impetus for the GCC was increasing military tensions in the Gulf, specifically the 1979 Iranian revolution and the nearly decade-long war between Iraq and Iran. In this context, the United States – the main foreign power in the Gulf – fully backed the attempt to bring the six hydrocarbon-rich monarchies within a single security umbrella that would be closely linked to the US military. Since those early days, however, the GCC has also developed into a closer political and economic alliance, with agreements (not always fulfilled) aimed at encouraging a single common market, a customs union, free movement of citizens between the different Gulf states, and standardised treatment around tax, pensions, social welfare and capital ownership (Hanieh, 2011: 104). Many commentators have drawn analogies with European integration, although the Gulf has progressed at a much slower and more hesitant pace than its larger neighbour.

Significantly, however, GCC integration did not extinguish ‘tensions within and between different [Gulf] states’ (Hanieh, 2011: 105). While capital flows across the pan-GCC scale have increased dramatically over the past decade, leading tangentially towards what Hanieh describes as ‘Khaleeji Capital’, this has been a highly uneven and hierarchical process (Hanieh, 2011: 103). Most specifically, Saudi Arabia and the UAE have emerged as the core zones of this structure – with considerable levels of cross-border investment flows, closer alignment on political questions and numerous joint economic initiatives between these two states – while the other Gulf states have been integrated as junior partners in the process.

Logistics infrastructure provides an important lens through which to analyse these tendencies. All Gulf states have heavily prioritized infrastructure development as part of wider diversification strategies aimed at reducing the region’s reliance on hydrocarbon exports. A key feature of these strategies (discussed in further detail below) is the building of a more robust regionally integrated logistics network, aimed at promoting cross-border trade. At the same time, as we shall see below, these plans and the projected port developments herald fierce competition over trade routes and international markets, which play out in considerable duplication, overcapacity, and heightened rivalries between Gulf states.

But despite the utility of logistics infrastructure as a frame for understanding these dynamics, there has been little scholarly attention paid towards the Gulf logistics sector. One partial exception to this lacuna is work on Dubai’s Jebel Ali Port, the world’s ninth largest container port by traffic. Ramos’s perceptive Dubai Amplified: The Engineering of a Port Geography (2010) placed Jebel Ali Port centrally in the city-state’s urbanisation process and development trajectory. 5 Jebel Ali is important because its development model is the prototype that is being replicated across the GCC. One core feature of this model is an emphasis on intermodal transport and automation, with the movement of commodities seamlessly linked between free trade zones and different kinds of transport networks. Jebel Ali, for example, contains a free zone and Logistics City, which are connected to Dubai’s World Central complex and Al Maktoum Airport in one large customs-free area. 6 This integration is aimed at speeding up the turn-over time of commodities through Dubai, the wider Gulf, and global markets, with the logistics sector acting as the underlying substratum for this circulation. As a Jebel Ali Free Zone marketing manager explained in a fieldwork interview: ‘We have created a streamlined process for our customers. They only interact with one person to set up their business and trade here. This is the quickest process in the region’. 7

Other states, including Oman and Qatar, are replicating this process by developing their regulations in a similar fashion and constructing ‘one-stop shops’ for investors. While some authors have commented on the internationalisation of the Dubai model in the production and management of logistics space (Cowen, 2014; Jacobs and Hall, 2007), the model’s regionalisation across the GCC has not been adequately explored. Studying this replication through the emergent GCC maritime port map helps to clarify the contradictory process of GCC integration. It suggests that the GCC integration project is a complicated and uneven one, whereby plans for both integration and diversification are based on the ability to accumulate across regional space, but within a framework of interregional competition and much duplication of development initiatives. We have here both integration and competition as contemporaneous tendencies; it is this hierarchical structure that is vital to keep in view while mapping the development in the region.

The Gulf’s logistics space and the rise of Oman and Qatar

A key theme of economic policy-making in the GCC is the notion of diversification: an attempt to expand alternative industries beyond that of hydrocarbon production. Over the last few years, these diversification strategies have been elaborated through a series of multi-year ‘vision’ documents, which outline the prioritisation and proposed investment for those sectors envisioned as holding potential for high growth. These vision documents are written in elaborate corporate style language, typically drafted by foreign consultancy firms and advisors. 8 They form the centrepiece of economic planning in all GCC states. 9

Although there has been some debate about the likely success of such diversification plans (Hvidt, 2013), one of their striking features is the prominence of integrated trade infrastructure and the construction of logistics hubs. Echoing the emphasis placed on trade infrastructure by international financial institutions, 10 all Gulf states have earmarked enormous amounts of funding for the building of new ports, free trade zones and other intermodal transport networks. The Saudi government, for example, has announced the establishment of four new economic cities, the largest of which will be the US$93b King Abdullah Economic City (KAEC). KAEC will include the largest port in the Red Sea region and a logistics and industrial area. 11 Similarly, the United Arab Emirates vision focuses on the country’s position as a ‘regional business hub’ (UAE Vision 2021, n.d.: n.p.). Likewise, Kuwait’s Vision 2035 aims to develop Kuwait as a financial and commercial hub; as part of this, Kuwait’s new Mubarak Port is designed to enhance its position into a regional trade hub. 12 Echoing these trends, Bahrain’s Vision 2030 projects Bahrain as a regional manufacturing and logistics hub, built around several special investment zones, including Bahrain International Investment Park, Bahrain Investment Wharf and Bahrain Logistics Zone, which have been set up close to the Khalifa bin Salman Port at Hidd. 13

The strategic plans of Qatar and Oman also highlight this general orientation towards trade and logistics infrastructure development in the Gulf. Qatar holds about 14% of the world’s gas reserves – the third largest on the global scale, following Russia and Iran. The transport of this gas has been crucial to the country’s economy and thus Ras Laffan, Qatar’s main liquefied natural gas export facility, has been expanded to become the world’s largest. However, Qatar’s strategic planning extends well beyond a focus on gas, and the country’s National Vision 2030 has highlighted the construction of ‘world-class infrastructure’ as a principal element of its future development (General Secretariat for Development Planning, 2008: n.p.). Much of this new building is a consequence of Qatar’s successful bid to host the 2022 World Cup, which has necessitated an upgrade of logistics infrastructure in order to cope with the import of basic construction materials. The key example of this is construction of the New Hamad Port, discussed further below.

With smaller oil reserves than its neighbours, Oman has had a very advanced diversification agenda, aiming both to reduce reliance on oil and to deal with the issue of endemic youth unemployment by investing in newer sectors of the economy. Oman’s diversification efforts aim to steadily position it as a trade gateway into the wider region by adopting plans that from their inception take into account connections to multiple modes of transport. In the maritime port sector specifically, the Omani state aims to leverage the position of ports outside the Strait of Hormuz to establish itself as a regional logistics hub. 14 The country has focused these efforts on three key container ports that are undergoing current construction or major expansion: Sohar, Salalah and Duqm.

Ports in Oman and Qatar are all in advanced stages of construction. 15 As noted above, however, these two states are at different moments of logistics expansion, with Oman ranking number three in GCC port capacity and Qatar only recently beginning its entry into this industry. A closer examination of these new and upgraded ports illustrates both the emulation of Dubai’s Jebel Ali model. Through this discussion, we can see the trends towards regional integration intrinsic to the GCC project, but also the sharpening competition between different Gulf states.

Sohar Port (Oman)

Sohar Port and Freezone brands itself as the ‘cornerstone in the region’s fast developing road-air-rail infrastructure’ (SOHAR Port and Freezone, 2017: n.p.). It is managed by the Sohar Industrial Port Company, a 50–50 joint venture between the Port of Rotterdam and the Omani government, and falls within the Greater Sohar Industrial Zone. The specific container terminal within this larger project, the Oman International Container Terminal, is a joint venture between HPH, the government of Oman, Steinweg (Netherlands) and a number of local private investors. 16 HPH is a subsidiary of the multinational conglomerate CK Hutchison Holdings Limited (Hong Kong), a leading global port developer and operator. The project brings Sohar Port into HPH’s international network, spanning 26 countries. The Sohar Freezone on the other hand is operated through a joint venture between the government of Oman, the Port of Rotterdam and India’s SKIL Infrastructure. Within the free zone, 100% foreign ownership is permitted, and there is a 10-year tax exemption that is extendable depending on the rate of ‘Omanization’ the company undertakes. Sohar Port’s three major clusters are logistics, petrochemicals and metals. A major terminal to handle agricultural bulk cargo is also underway. The port replaced Mina Qaboos in Muscat, which will in turn be transformed into a tourist destination for cruise ships (tourism is another focus of Oman’s diversification efforts).

The port is positioning itself clearly against the well-established Jebel Ali Port. During fieldwork in Dubai in February 2017, the author noted a large advertisement for Sohar Port just outside Jebel Ali reading, ‘Why go through the Strait when you can go straight to the Gulf?’ This statement captures the clear contrast and advantage that Sohar Port is attempting to sell to its customers. It also illustrates that despite the broader framework of GCC economic integration and cross-border investments, such megaprojects compete against each other for market share, aiming to attract foreign investment in newly constructed free trade zones and logistics parks.

There has been substantial dredging work involved in deepening Sohar Port’s access channel, the turning basin, a navigation channel and the existing fishing port. Part of the dredged sand was used to reclaim land for the future container terminal. This confirms AlShehabi and Suroor’s argument that land reclamation is connected to a shift ‘towards “privatisation” of the land, with the state largely playing the role of a land broker and facilitator’ (AlShehabi and Suroor, 2016: 839). In this instance, there is privatization not only through concessionary agreements but also through land reclamation and the essential gifting of state land to international and domestic capital groups. To give but one example, an agreement between Muscat’s Supreme Council of Planning, Sohar Freezone and Al Siraj Investment Holding saw a sizeable logistics services complex built at the Sohar Freezone. The aim was to create a logistics centre for the distribution of vehicles and spare parts. Those holding local agency rights for car products, such as Suhail Bahwan Automotive (handling Nissan and BMW) and Oman Trading Establishment (Hyundai), will be the main groups to benefit from this space (Times of Oman, 2012: n.p.). The Bahwan Group and Oman Trading Establishment are two longstanding and large Omani conglomerates controlled by well-established merchant families. This arrangement illustrates the production of privatised logistics space for the benefit of domestic and international capital.

Salalah Port (Oman)

Salalah Port is made up of a container terminal with seven berths and a general cargo terminal, with infrastructure to handle the world’s largest container vessels, as well as bunkering and warehousing. It operates mainly as a transhipment hub. Oman’s Ministry of Transport and Communications plans to expand Salalah Port further. The port is owned and managed by the Salalah Port Services Company, a joint venture between Danish APM Terminals (30%), the Oman Ministry of Finance (20%), HSBC Bank (14%) and a host of local private sector investors, government pension funds and investors on the Muscat Securities Market. In 1996, APM Terminals signed a 30-year concession agreement with the government of Oman to build and manage the port. APM Terminals has a geographical presence in 39 countries, including 65 port and terminal facilities and 200 inland services (UNCTAD, 2015: n.p.). Such concessions bring Oman’s Salalah Port into APM Terminals’ international network, also establishing APM Terminals’ sister company, Maersk Line, the world’s largest container shipping company, as the main shipping line at the port. Aside from embedding Salalah in APM’s international network, the project seeks to break Jebel Ali’s monopoly as the main port of entry for leading international shipping companies. The importance of this has been illustrated in the recent dispute between Qatar and Saudi Arabia/UAE (discussed further below).

Duqm Port (Oman)

The last of Oman’s ports, Duqm, is the centrepiece of the Duqm Special Economic Zone (DSEZ). It will cover an area of 1777 square km and 80 km of coastline along the Arabian Sea. DSEZ will be the largest free trade zone in the Middle East and North African region thus far, and among the largest in the world. Duqm is an interesting case of an ‘integrated economic development comprising a seaport, industrial area, fishing harbour, tourist zone, a logistics centre and an education and training zone’ (Port of Duqm, 2017: n.p.). Financing for the Duqm Port Project came from the Kuwait Fund for Arab and Economic Development, and the Japan Bank funded the Duqm Port and Dry Dock project.

The Duqm Special Economic Zone Authority (SEZAD), established by royal decree in October 2011, is the main regulatory and supervisory body for the DSEZ and is responsible for managing and developing all economic activities, including construction of the port. However, direct management is by the Port of Duqm Company, a joint equal venture between the Consortium Antwerp Port Company and the Omani government on a 28-year concession. SEZAD will be the focal point for potential investors and will have a one-stop shop to help new investors. This is a similar model to the Jebel Ali Free Trade Zone. As with other special economic zones in the GCC, SEZAD will entice private investment by allowing 100% freehold for international corporations, tax exemption for up to 30 years renewable for a similar period and minimal labour regulations.

New Hamad Port (Qatar)

The New Hamad Port project is among the largest of Qatar’s infrastructure developments. Located to the south of the capital, Doha, Qatar’s new port, estimated at a cost of US$7.4b, was inaugurated on 9 February 2015 (a year ahead of schedule) with the flooding of its main basin. The project, when completed, will cover 26.5 square km and will consist of the port itself, a new naval base for the Qatar Emiri Naval Forces and the Qatar Economic Zone 3, which will host a series of logistics parks. The completion date for the project has been brought forward from 2030 to 2020.

In line with its investment in transport and logistics infrastructure, Qatar is also at various stages of constructing several specialized economic zones: Ras Bufontas (near the airport), Um Alhoul (in conjunction with the New Hamad Port) and the Al Karaana (by the Saudi border, and on hold at the moment). Each of these zones is strategically connected to the New Hamad Port and three planned logistics parks that will be located inside the port itself (Al Wakra, Birkat Al Awamir and Aba Salil). 17 These logistics parks aim to seamlessly link the production efforts in the economic zones to transhipment from the port itself. Although Qatar’s economic zones are significantly less developed than those of the UAE, the Ministry of Economy and Commerce is planning to emulate the UAE model through the establishment of one-stop-shop registration for domestic and international companies.

Emulation, integration and competitive hierarchies

Emerging from this account of port construction in Oman and Qatar is the clear attempt by governments in these two countries to replicate the logistics model pursued by Dubai and attempt to capture some of the container traffic handled by Dubai’s Jebel Ali Port. The goal is to build very large-scale port infrastructure, which would allow Omani and Qatari ports to accommodate the ever-increasing growth in container ship size and cargo throughput. The orientation is towards connecting with international markets, and establishing their respective ports as important nodal connections to global trade flows. The development of these ports is thus conceived not simply for supplying the needs of domestic markets, but rather as an attempt to achieve a foothold within wider regional and global flows.

Key to this is the notion of intermodalism. As with Jebel Ali, both Oman and Qatar seek to build an integrated logistics space that connects maritime ports, airports, rail and road. An important linking feature of these connected corridors is the creation of free zones that can assemble, label and repackage commodities due for re-export, thereby embedding these countries firmly in international supply chains through value-added logistics activities. This hard infrastructure is augmented by a soft infrastructure that seeks to incentivise international firms to relocate their activities to the new logistics spaces. Provision of 100% foreign ownership, zero corporate tax and import/export duties and no restriction on capital repatriation are principal elements of this incentivisation.

This regional emulation of Dubai’s model needs to be situated, however, in the context of GCC regional integration. The vision documents noted above highlight the goal of advancing intra-regional trade and integrating Gulf infrastructure within a single pan-GCC network. The strategic planning for Oman’s ports, for example, emphasizes how they will be linked to the pan-GCC railway system that is currently being constructed across the Gulf; the goal is to move (at an ever-increasing pace) commodities from and through Oman to other states in the GCC.

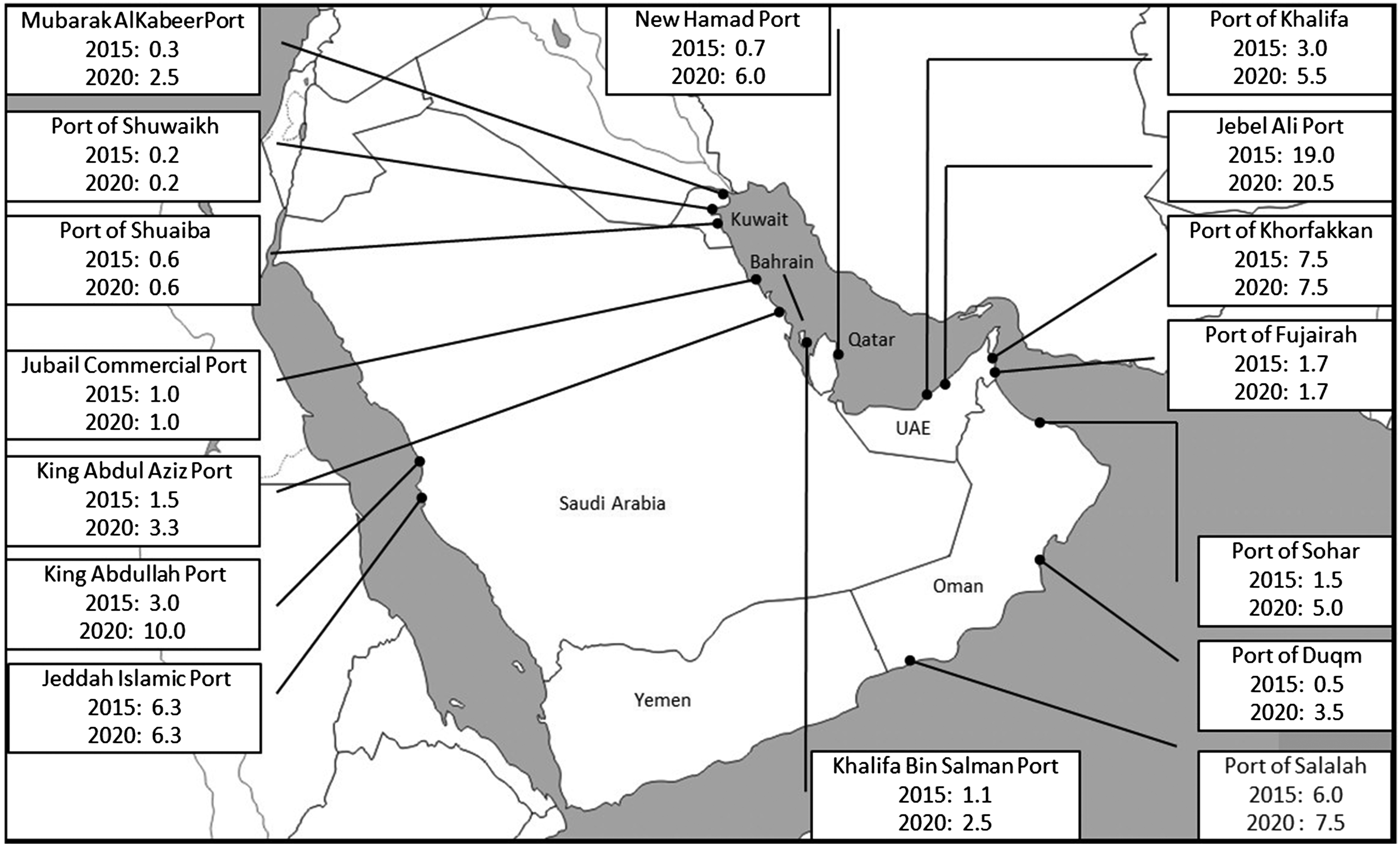

In this context, Figure 1 maps the location of all Gulf ports and their planned capacity increases from 2015 to 2020. If planned port construction and capacity expansion continue at current rates across the GCC, total port capacity is due to increase from 25 m 20-foot-equivalent units (TEUs) in 2010 to 60 m TEU by 2020 (Roscoe, 2012). The map demonstrates the striking increase in port competition heralded by the projected capacity increases in Qatar and Oman. In 2015, the four UAE ports (Jebel Ali, Khalifa, Khorfakkan and Fujairah) constituted 31.2 m TEU, while ports in Qatar (New Hamad Port) and Oman (Sohar, Duqm and Salalah) made up 8.5 m TEU of the total GCC port capacity. By 2020 – in only five years’ time – Oman and Qatar’s combined port capacity will have grown to 22 m TEU, a more than 250% increase, exceeding that of the regional behemoth, Jebel Ali.

Container ports in the GCC – current and future capacity. Map by author, based on industry reporting in Middle East Economic Digest Projects.

We thus have here a process of increased competition – structured by the Gulf’s insertion into global commodity chains – alongside the professed goals of tighter regional integration and harmonisation. This raises the very real scenario of port overcapacity in the Gulf over coming years, particularly if projections of a slowdown in global trade volumes prove correct. Growth in global container port demand is predicted to slow to less than 3% per annum due to the sharp decline in China’s export growth (Drewry, 2016: n.p.).

This likely scenario of heightened intra-GCC competition and overcapacity needs to be overlaid by the trends in the concentration of global port operation noted earlier. One way this plays out in the GCC is the modalities of port infrastructure financing. As the narrative above illustrates, Oman, with its more limited oil reserves, is relying heavily on concessionary agreements through joint ventures with (mostly) European port operators. Oman is unique in this respect, rolling out public–private partnerships (PPPs) that facilitate privatisation through concession/lease agreements or Build Operate and Transfer (BOT) arrangements between the government and private terminal operators. 18 Such PPPs, including with the Port of Rotterdam (in the case of Sohar), Antwerp Consortium (Duqm), Hutchinson Holdings (Sohar Container Port) and APM Terminals (Salalah), increasingly join Oman’s ports with the wider networks of market-dominant port operators. Moreover, through these joint ventures, international port operators are entering the GCC maritime market. However, this process is also accentuating the competition between UAE-based operators (such as DP World and Gulftainer) and other international companies. The tendency towards increased competition between global port operators is thus refracted through the GCC regional integration project. The pan-GCC scale acts to mediate and heighten the competition between global port operators and local, Gulf-based firms.

An important consideration in assessing these future scenarios is the possible impact of a prolonged period of low oil prices. Much of the funding for port infrastructure in the GCC over the past decade took place during a time of rising oil prices, but since mid-2014, the oil price has fallen by more than half, fluctuating around US$50 per barrel during the first half of 2017. One of the critical consequences of the resulting drop in oil revenues is a move by Gulf states, other than Oman, to establish regulatory frameworks for the use of PPPs in infrastructure financing. Kuwait revamped its PPP laws in 2014, new PPP laws were introduced in Dubai in November 2015, and Qatar is in the process of drafting a PPP framework. This is an important emerging trend, as thus far these GCC states have avoided utilising PPPs for infrastructure projects, opting for their management through state-owned conglomerates and drawing upon oil revenues for funding. A likely outcome of these new financing arrangements is a further deepening of international competition in the GCC logistics sector, as the major international port operators vie to gain access to this important node of global trade.

Conclusion

This paper has foregrounded logistics as a lens to understand the nature of intra-GCC relations. The drive towards intermodal transport infrastructure, conceived to speed circulation of commodities through all segments of the logistics chain, is central to GCC development plans and continues to impact the regional landscape through immense dredging and land reclamation projects, as well as the use of large tracts of land for industrial port zones, free trade zones and logistics cities. In a region central to global trade (especially in oil and gas) and thus imperial interests, this emerging Gulf transport infrastructure reveals much about the nature of development in the Gulf, and the ways in which different Gulf states are positioned within the wider GCC project. A focus on the ports and logistics spaces in Qatar and Oman underlines the differential incorporation of GCC states in internationalised logistics chains. The large-scale, intermodal logistics infrastructures planned by Oman and Qatar present a challenge to the UAE’s supremacy in the Gulf’s maritime industry. This duplication presents the very real possibility of overcapacity in this sector – particularly if there is a further downturn in the global economy. As this article was being written, the saliency of these trends was powerfully illustrated by the crisis that emerged between Saudi Arabia and the UAE, on one side, and Qatar, on the other, making rivalries more apparent. The divergent financing models of port development, specifically Oman’s use of PPPs and joint ventures with global operators, are accentuating these competitive tensions between GCC states. This is particularly important for the future global position of Dubai’s DP World, which depends so critically on Jebel Ali Port as its ‘stronghold’.

The effective embargo by Saudi Arabia and the UAE confirms the main lines of intra-GCC rivalry noted throughout this paper; it also shows just how critical the logistics and maritime infrastructure sector is to understanding these rivalries and the spatial geopolitics of the region. We see here the ways in which the trends discussed throughout this article are vital to understanding the emerging contours of GCC relations, in terms of both competitive rivalries and mutual interests. Precisely because Salalah had been embedded in APM’s international network through the processes described above, it has (at least partially) broken Jebel Ali’s monopoly as the main port of entry for the Gulf. As the planned port construction unfolds over the next five years, these features of the Gulf’s logistics space will be become ever more central to understanding the politics of the region.

Footnotes

Acknowledgements

I am grateful to Martin Danyluk, Charmaine Chua, Deborah Cowen, Laleh Khalili and three anonymous Society and Space reviewers for their constructive feedback on earlier drafts of this article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by Economic and Social Research Council grant number ES/L002833/1.