Abstract

Financial crises, austerity, and rising living costs have adversely affected the financial situations of many in the UK over the past decade and more. Debt is commonplace and has become a typical means of managing financial turbulence. However, managing debt and navigating financial changes pose significant policy challenges for low-income families like lone parents. Despite policy emphasis on personal financial responsibility, the impact of structural financial changes should be more evident. This article presents a novel secondary mixed methods study that uses two distinct national-level datasets to shed light on the heightened debt burdens faced by lone parents. The findings reveal that debt burdens frequently stem from factors outside their control, including reduced incomes, high living costs, adverse life events, and an insufficient welfare system. Intersecting inequalities compound these issues, forcing lone parents to make tough financial decisions with limited alternatives.

Introduction

Following the 2008 global financial crisis (GFC), the UK has seen numerous further socioeconomic transformations that have negatively impacted the financial lives of many. These changes include an economic recession, government austerity (particularly changes to the welfare system), increased household debt, falling incomes, labour market anxieties, and rising living costs. Each of these is implicated in contributing to the disproportionate and worsening financial situation of low-income individuals and families, like lone parents (Brewer et al., 2013; Hills, 2015). The mid-2010s were a critical period of socioeconomic change, and since then, challenges such as the COVID-19 pandemic and cost-of-living crisis have further intensified economic pressures on lone parents. These evolving circumstances underscore the continued pertinence of the financial challenges and risk of debt that they face. Studies have emphasised low income as the primary structural issue concerning debt among the most vulnerable, limiting their ability to resolve their situation (Orton, 2009). The Women's Budget Group (2017) finds that the real incomes of lone parents in recent years, especially lone mothers and those from minority ethnic backgrounds, have been the most negatively affected of all groups in society. In the context of this research, this can mean an inability to meet their family's needs and pay pressing bills, which can lead to mounting debt burdens.

There are 1.8 million lone parent families in the UK, who make up almost a quarter of all families with dependent children, with 92% headed by lone mothers (ONS, 2019). Hirsch and Stone (2019) estimate 993,000 children in non-working lone parent families and most in working families (862,000 children) live below the minimum income standard. Given their prevalence in society, lone parents continue to face some of the most challenging financial and economic conditions in which to manage their finances and debt.

The economic crises and austerity of the last decade and more, alongside surging levels of personal debt (Dagdeviren et al., 2019), have resulted in individuals taking on more self-reliance and personal responsibility in their everyday lives (Montgomerie and Tepe-Belfrage, 2016). Questions remain about how financial changes of recent years have impacted lone parents’ ability to stay financially secure and out of debt. Systematic research is greatly needed to address how financial decisions are made in vulnerable families, given their challenging circumstances and responsibilities (Hall, 2015).

This article utilises quantitative and qualitative approaches to characterise lone parents’ financial challenges and how they manage debt. It alludes to a body of literature that shifts away from focusing on debt levels and repayment rates (see Kempson et al., 2004) and instead delves into the day-to-day experiences and perspectives of those in debt (see Dawney et al., 2018). This research examines the factors that impact changes in financial circumstances and debt burdens. Moreover, it aims to explore the personal accounts of those at the forefront of government policies to understand how they act to try and solve their financial problems in the context of constrained finances.

This article first discusses the macroeconomic setting and findings concerning lone parents’ financial situations and debt. The data analysis is presented after describing the study's methods and empirical data. A novel secondary analysis of mixed-method data is outlined, which includes analyses of quantitative and qualitative secondary data sources. Finally, the main findings are underlined with recommendations on how policy could better support lone parents facing financial challenges and debt.

Background

Crisis, austerity, and changing financial situations

Social scientists and policymakers are increasingly interested in how individuals and families in low-income situations manage their everyday lives in challenging economic times (Dagdeviren et al., 2016; Daly and Kelly, 2015). With growing income inequality in the UK (Brewer et al., 2007), vulnerability to changes is critical to understanding financial outcomes. This section examines the social, political and economic changes that have impacted families, particularly those since the 2008 financial crisis. It describes the effect of these changes on the UK's lowest-income families, focusing on lone parents.

The GFC and UK recession brought about notable labour market changes that caused unemployment and underemployment rates to rise while real wages decreased. In 2008, approximately 55% of lone parents in the UK were employed (Harkness, 2013), increasing to 70% a decade later (DWP, 2017). The increasing number of lone parents seeking employment can be partly attributed to welfare changes, including Lone Parent Obligations (LPOs). This policy mandates that lone parents receiving welfare benefits must actively seek employment based on the age of their youngest child. Since 2017, this requirement has been applied to parents whose youngest child has reached three years old (Johnsen and Blenkinsopp, 2018). For lone parents, this increase in employment has resulted in rising levels of precarious and zero-hour work (where working hours are not guaranteed) (Tinsley, 2014) and significant income fluctuations (ONS, 2018a). Recent estimates by the Joseph Rowntree Foundation (2018) indicate that half of working lone parents earn low wages, compared to 37% of second earners and 21% of primary earners in couples.

Under post-2010 Conservative-led UK government austerity, new welfare regulations for claiming working-age benefits were among the most drastic in a generation. Tougher sanctions, benefit cuts and freezes were implemented, including the overall benefit cap, the two-child limit, changes to tax credits, and the roll-out of universal credit. These changes are part of the broader political discourse that proposes that poverty can be eliminated by forcing individuals into employment and making them personally responsible for their financial situations (Carey and Bell, 2020; Johnsen and Blenkinsopp, 2018). However, securing employment does not always guarantee financial stability, as many jobs are low-paying and insecure. For lone parents, attempts to enter the workforce have often failed to lift them out of poverty (Harkness, 2013). According to the Women's Budget Group (2017), since 2010, tax and welfare changes have reduced lone parents’ living standards by £9000 (18%). Between 2010 and 2014, tax and benefit changes led to a real-term income loss for lone parents. Those in work lost 5%, and those out of work lost 10% more than the overall population (Hills, 2015: 229–30).

Despite signs of stabilisation in the UK economy pre-COVID-19 pandemic in early 2020, low-income families, especially lone parents and mothers, still faced disproportionate financial challenges. Welfare budget cuts continued to severely impact their ability to balance job-seeking, employment, and childcare responsibilities (Women's Budget Group, 2017). Expensive childcare costs, which are the highest in Europe, make it difficult for mothers to work or work full-time (European Commission, 2013; Norman, 2014). In addition, everyday expenses, such as food and energy, remained costly. Analysis of the Living Cost and Food Survey shows that lone parents spend more of their income on living costs than coupled households and spend the highest of any household on housing and fuel costs (ONS, 2018b, 2010).

Life events like relationship dissolution and work transitions pose risks to lone parents’ financial stability. Partner separation often worsens mothers’ financial situations due to a rapid decline in income, leading to a period of needing support (Jenkins, 2011). Employment decisions can lead to fluctuating incomes, with lone parents struggling to manage finances effectively when moving into work, working reduced hours, or not in work (Coleman and Lanceley, 2011). Moreover, lone mothers are often the most financially excluded. The gendered precarity of lone mothers concerning work can mean they endure more significant financial difficulties than lone fathers, leading to needing to find ways to get by and debt (Levitas et al., 2006; Pantazis and Ruspini, 2006).

The noteworthy changes since the recession have led to a shifting socioeconomic environment in which lone parents have had to find ways to make increasingly difficult financial choices. Given their challenging circumstances, the following section now turns to debt and how low-income families like lone parents have attempted to manage it.

Debt, decisions, and resourcefulness

Household debt levels in the UK grew substantially preceding the UK recession, with current estimates indicating it to be around 150% of net disposable income, remaining relatively unchanged since 2015 (OECD, 2023). Given concerns about rising debt levels during the recession, government policies aimed to prevent people from facing debt burdens (also commonly referred to as indebtedness or problem debt) through financial education initiatives. These individualised policies, originating from New Labour's financial exclusion strategy (pre-2010) and accelerated under the Conservative-Liberal Democrat Coalition government (post-2010), focused on improving financial capability and literacy—the skills and knowledge necessary for effective money management, financial decision-making, and financial resilience (Money Advice Service, 2019). However, this approach has been criticised for oversimplifying broader structural problems by placing undue emphasis on individual responsibility; as Appleyard (2021) argues, an adequate income is necessary for saving and paying bills. Furthermore, Montgomerie and Tepe-Belfrage (2016) point out the gendered impact of these policies, which disproportionately blame lone mothers for experiencing poverty, insecurity, and debt.

The Money Advice Service (2017) estimates that 8.3 million people in the UK have problem debt – when a debt or bill becomes unaffordable and when payments are not made. Debts are commonly linked to formal borrowing and credit. While unsecured or secured borrowings can allow for income smoothing in times of turbulence, this is rarely the case for disadvantaged low-income groups. Not all low-income households use unsecured credit borrowings, such as high street loans and credit cards, but they are considerably more likely to have debt problems (Hartfree and Collard, 2015). Rather than financial mismanagement, income inadequacy is a primary reason people fall into debt in the social policy literature (Davies et al., 2019). Earlier research on family debt obligations and liabilities found that lone parents are twice as likely as couple parents to have problems with repaying credit debts and household bill arrears (Kempson et al., 2004).

The burden of debts can significantly affect people's health and well-being and place greater demands on support services (Clayton et al., 2015; Gathergood, 2012). Lone parents are more likely to access communal debt advice than other families. Among clients of users of StepChange, a leading debt advice provider in the UK, female clients have risen by a fifth over the previous year (62%), with lone parents making up a quarter of all debt clients (24%) – four times the actual proportion of lone parents in the general population (6%) (StepChange, 2019).

While debt is a problem for many vulnerable families, lone parents are more likely to face gendered social and economic costs to their families. This can constitute a barrier to their agency, including achieving economic independence and financial security (Orton, 2009; Women's Budget Group, 2020). Previous qualitative research has found that lone parents often make decisions that minimise the immediate impact of their insecurity by protecting their families from poverty and helping them maintain a reasonable standard of living (Millar, 2007). However, according to a longitudinal study on lone mother families, work, and relationships, these decisions are made to avoid the harshest effects of financial challenges, given the different insecurities they face (Millar and Ridge, 2009, 2017). As a route into debt and given lone parents’ limited resources, they may prioritise the most pressing and immediate needs over potential future demands (Mullainathan and Shafir, 2013). Furthermore, while relationships with close family and friends can be a significant emotional and financial resource in times of crisis (Millar and Ridge, 2009), these relations may deteriorate when money is requested or borrowed and not repaid.

At a superficial level, these findings could indicate that lone parents are used to being resourceful and resilient in the face of challenging and low resources. However, it is yet to be determined how experienced changes in their financial situation, over which they have little control, can affect lone parents’ ability to keep out of debt, including income reductions, increased household and childcare costs, and changing circumstances.

Research approach and aims

This article draws on secondary mixed methods data from lone parents, many of whom have low incomes and are at risk of challenging financial situations and debts. The approach addresses the dominant framing of political elites towards low-income families, which forefronts notions of debt as an individual rather than a structural and social issue (Orton, 2009). In these conversations, the views of those who experience financial problems are often absent. Using a secondary mixed methods approach balances out the limitations of each method, providing stronger evidence than in previous research. Placing lone parents at the centre of the analysis allows generalisable findings alongside lived experiences that challenge the unequal power structures that underwrite marginalised perspectives.

This research aimed to examine the interplay between changing financial situations and debt in terms of the socio-demographic makeup of lone parents. In the context of constrained circumstances, the research also aimed to explore the personal accounts of those at the forefront of government policies to understand how lone parents manage their finances and act to solve debt burdens when they occur. The rest of this article presents the novel data and methods used in this research, followed by a presentation of the findings. Finally, the article concludes with a review of the issues presented with suggestions for policymakers and future research.

Data and methods

A secondary mixed methods approach

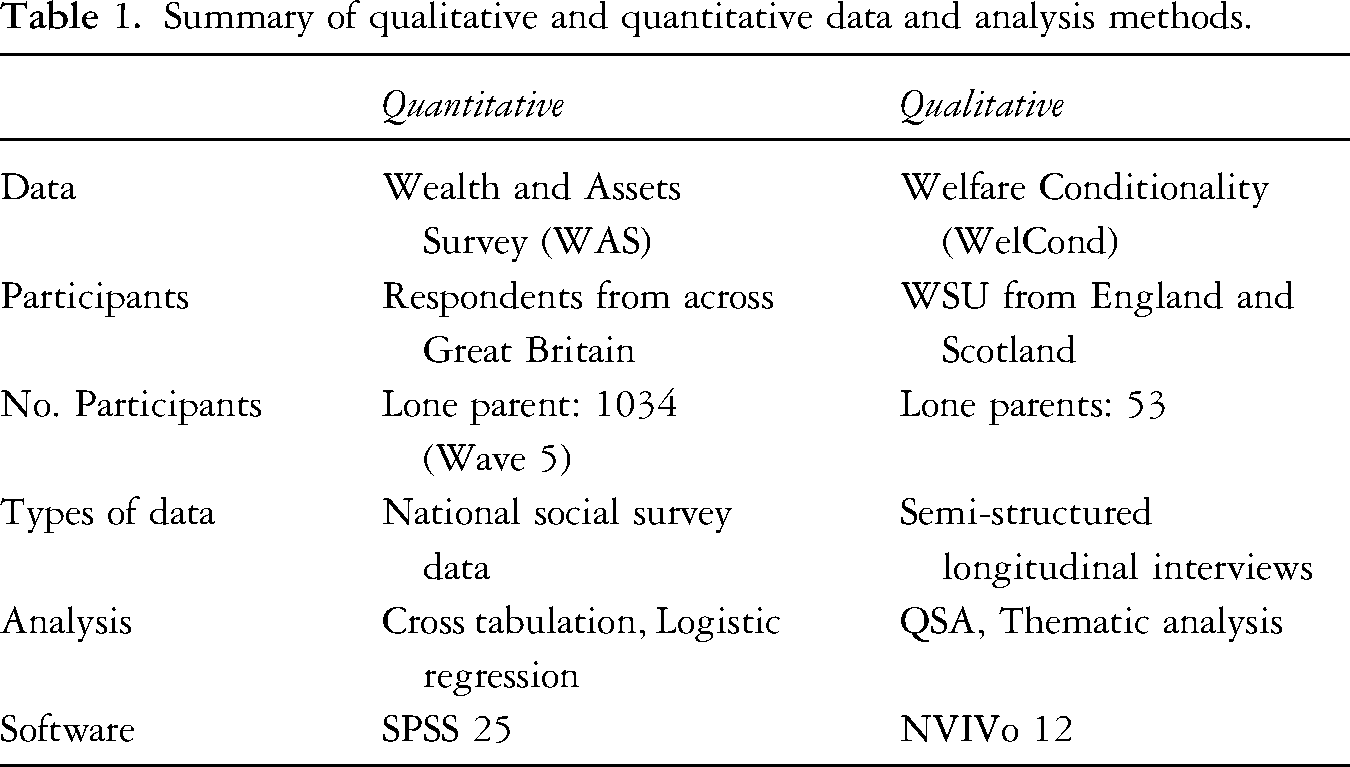

Table 1 summarises the data and corresponding methods used in this study. The complementary and novel nature of the mixed methods approach used in this study combined the strengths of national survey data with the detailed understanding of experiences gained from in-depth semi-structured interview data (Bryman, 2006; Daphne, 2023). The utilisation of secondary data for quantitative analysis has become more prevalent, while qualitative secondary analysis (QSA) remains underutilised (Hughes and Tarrant, 2020). Nonetheless, QSA remains a valuable and pertinent tool, particularly when fieldwork is restricted. This section outlines the data sources, methodologies, and research strategies employed.

Summary of qualitative and quantitative data and analysis methods.

Survey

Quantitative findings were drawn from an analysis of the Wealth and Assets Survey (WAS) data (ONS, 2020). The biannual and nationally representative survey samples 18,000 households where 40,000 people aged 16+ live. It is a primary source for tracking people's economic well-being related to their assets, savings, income, debt, and planning (ONS, 2020).

The survey analysis focussed on reported changes in lone parents’ financial situation and their debt burden. Given the complex nature of personal finance, there is no fixed way to measure financial changes or when a household or individual is ‘indebted’ (D'Alessio and Lezzi, 2013; Kempson, 2004). Measuring these concepts can be done through various “subjective” or “objective” proxies. The latter relies on legal or statistical indicators such as income and liabilities. Meanwhile, subjective proxies ask respondents to reflect on their current financial resources and demands and whether they face debt-related challenges. According to Clark et al. (2019), subjective measures offer a better understanding of how individuals perceive their financial situation. Objective indicators, especially those related to debt liability, including the debt-to-income ratio, number of debts and repayments, may overlook the impact on people's overall well-being. Therefore, this study suggests that respondents are the best source of information to gauge their financial status and assess whether their debt is manageable and how it affects them.

Three self-reported questions were used to measure lone parents’ financial situation and debt burden. The first question asked if respondents’ current financial position had changed over the last two years, with three response categories: better, same, or worse. Respondents who were financially worse off than two years ago were classified as having worsened finances. In addition, multiple responses to the reasons why were also examined. The second question asked respondents if keeping up with debt repayments was a burden, with three response categories: not at all, somewhat, or a heavy burden. Finally, those who answered that they had found debt a heavy burden were classified as having a debt burden.

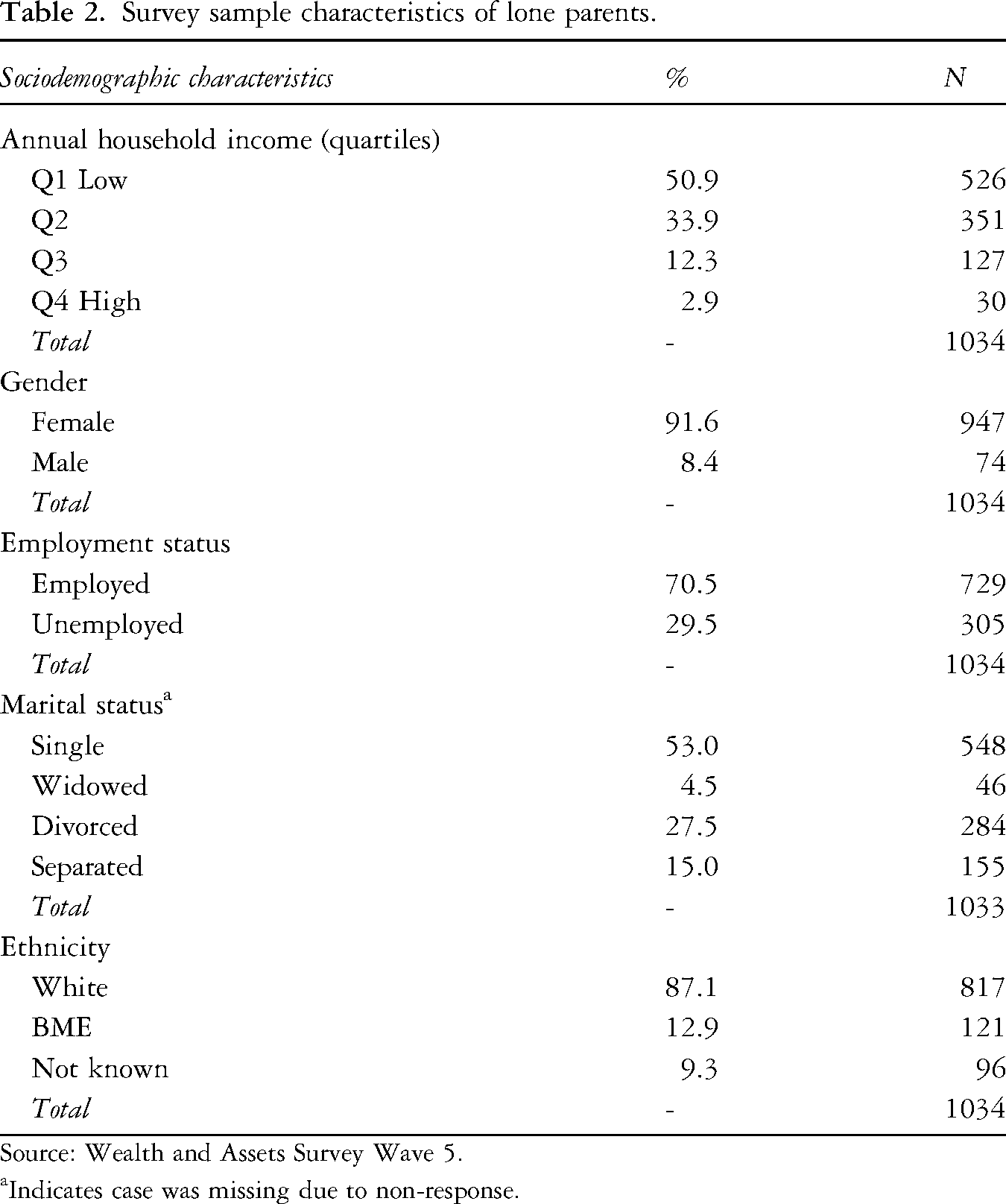

The lone parent sub-sample from WAS Wave 5 (2014–2016) (Table 2) was 92% female (ONS, 2019), with half in the lowest income quartile; an equivalised household income in the lowest 25% of the population. Around 70% were employed, aligning with national estimates (for the lowest income quartile employment is 50%). Wave 5 was situated within a similar timeframe to the data collected in the qualitative study, accounting for a time when considerable national reforms to welfare policy and payment restrictions took place, including the overall benefit cap, changes to child tax credits, limits to working-age benefits, and the removal of spare room subsidies (Johnsen and Blenkinsopp, 2018). From an initial examination, lone parents’ responses to their financial situation were fairly equally divided between the categories. In contrast, 29% of lone parents found debt a burden, compared to 11.6% of couple parents in the survey.

Survey sample characteristics of lone parents.

Source: Wealth and Assets Survey Wave 5.

Indicates case was missing due to non-response.

Interviews

The qualitative findings were drawn from an analysis of Welfare Conditionality: Sanctions, Support and Behaviour Change data (WelCond) (Dwyer et al., 2019). This was a five-year qualitative longitudinal panel study (Corden and Millar, 2007) conducted by six universities in England and Scotland. The study delved into experiences of welfare conditionality among claimants, where entitlement to welfare is determined by the willingness to fulfil conditions instead of just their needs (Johnsen and Blenkinsopp, 2018).

WelCond included interviews with 53 purposively sampled lone parent interviewees from six urban case study areas, collected over three waves between 2014 and 2017. Most interviewees were female (85%), with 26% working in at least one wave; as welfare service users (WSU), employment was underrepresented. However, this sample mirrors the findings of the national debt charity StepChange (2016), where many clients had limited availability for full-time work due to childcare, lived in social or rented housing and faced income constraints.

Despite its potential, few frameworks are available for researchers to apply QSA. The WelCond data provided a unique opportunity to reuse previously collected qualitative interviews by re-contextualising and repurposing them for use in this new research (Hughes and Tarrant, 2020). While initially designed to explore circumstances and experiences of welfare conditionality, to align with questions asked in the WAS, attention was directed to interview questions gleaned from the WelCond data around participants’ financial situation, how they managed financially, and whether they had built up debt.

Strategy for analysis

Quantitative and qualitative data were used in an explanatory framework to understand lone parents’ financial situations (Bryman, 2006). Limitations of using separate secondary data include different sampling strategies given their distinct research focus. Family structures are also complex, meaning that where participants fit into specific categories may not be clear. Moreover, given the different questions and sample variability, unique experiences may be harder to detect. While the WAS survey offers a broad overview of lone parents, the WelCond data are more limited due to limited diversity. Therefore, the process adopted in this study brought each dataset into dialogue, starting with an analysis of the quantitative data and then qualitative data, adding complementary and unique insights into facets of the research problem (Mason, 2011). Where possible, integration was built into the process to strengthen the sum of joint knowledge claims.

The survey data were analysed using SPSS 25. All data used were weighted to account for representativeness and non-response. Descriptive analysis, including multiple response analysis and cross-tabulations, was produced at the population level across survey waves. Using logistic regression, odds ratios (OR) were calculated to examine the association of critical socioeconomic characteristics, enabling the comparison between groups on the proposed outcome.

All transcripts from the interview sub-sample were analysed using reflexive thematic analysis as outlined by Braun and Clarke (2006), following its six-stage process. This approach was selected for its suitability in identifying patterns across a broad dataset, making it ideal for a mixed methods approach that uses large amounts of secondary data, where a comprehensive thematic overview was appropriate. This contrasts with Interpretive Phenomenological Analysis (IPA), which is used for profoundly exploring personal lived experiences, prioritising in-depth analysis of a small number of participants rather than broad thematic patterns (Pietkiewicz and Smith, 2014; Smith et al., 2009).

First, an iterative approach involved immersing myself in the previously collected data as the researcher. Second, an initial coding schema produced summaries inductively. Third, classifications and unique attributes were summarised and refined based on emerging themes from a close reading of transcripts. Lastly, to ensure clarity and coherence in reporting, details of these themes were added to the thematic coding supplemented with indicative quotes, selected to define and name the theme when reporting, maintaining both depth and breadth in the analysis (Braun and Clarke, 2006). Reflexive thematic analysis facilitated the exploration of both common and contrasting themes related to debt and financial management among lone parents, allowing for meaningful comparisons.

Findings

This section presents findings from the mixed-methods analysis. Survey evidence on lone parents’ financial situation and the relationship with debt is presented while highlighting the relationships with fundamental factors. Interview evidence presents personal accounts of lone parents and how they have attempted to manage their finances in constrained circumstances. Finally, some findings were integrated to provide an overview of the main conclusions.

Survey evidence: Worsened finances and debt among lone parents

Worsened finances and debt burdens

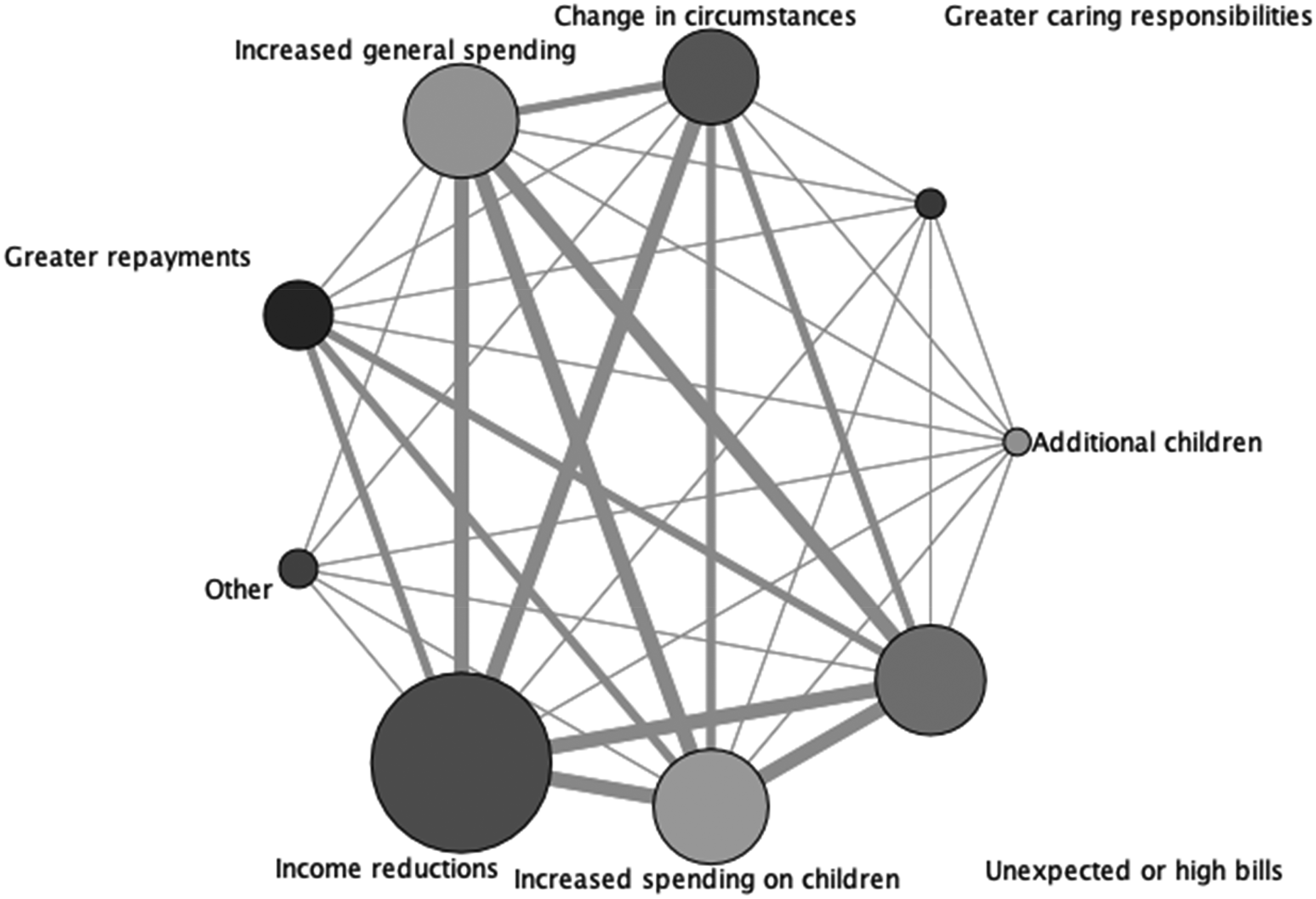

Lone parents were asked if their financial situation had changed in the last two years, with 32.6% stating their financial situation had worsened (32.6%). Those who responded that their financial situation was worse (n332) could select multiple reasons for why. Figure 1 shows the map of response categories and combinations. Most participants selected one (43.8%) or two (30.3%) responses. Income reductions were the most frequent response category (50.1%), followed by general spending increases (31.2%), increased spending on children (30.8%), unexpected or high bills (28.6%), a change in circumstances (25%) or increased debt repayments (16.7%). When pooling responses, income reductions with a change in circumstances were the most frequent response combination.

Map of category responses for reasons why financial situations worsened.

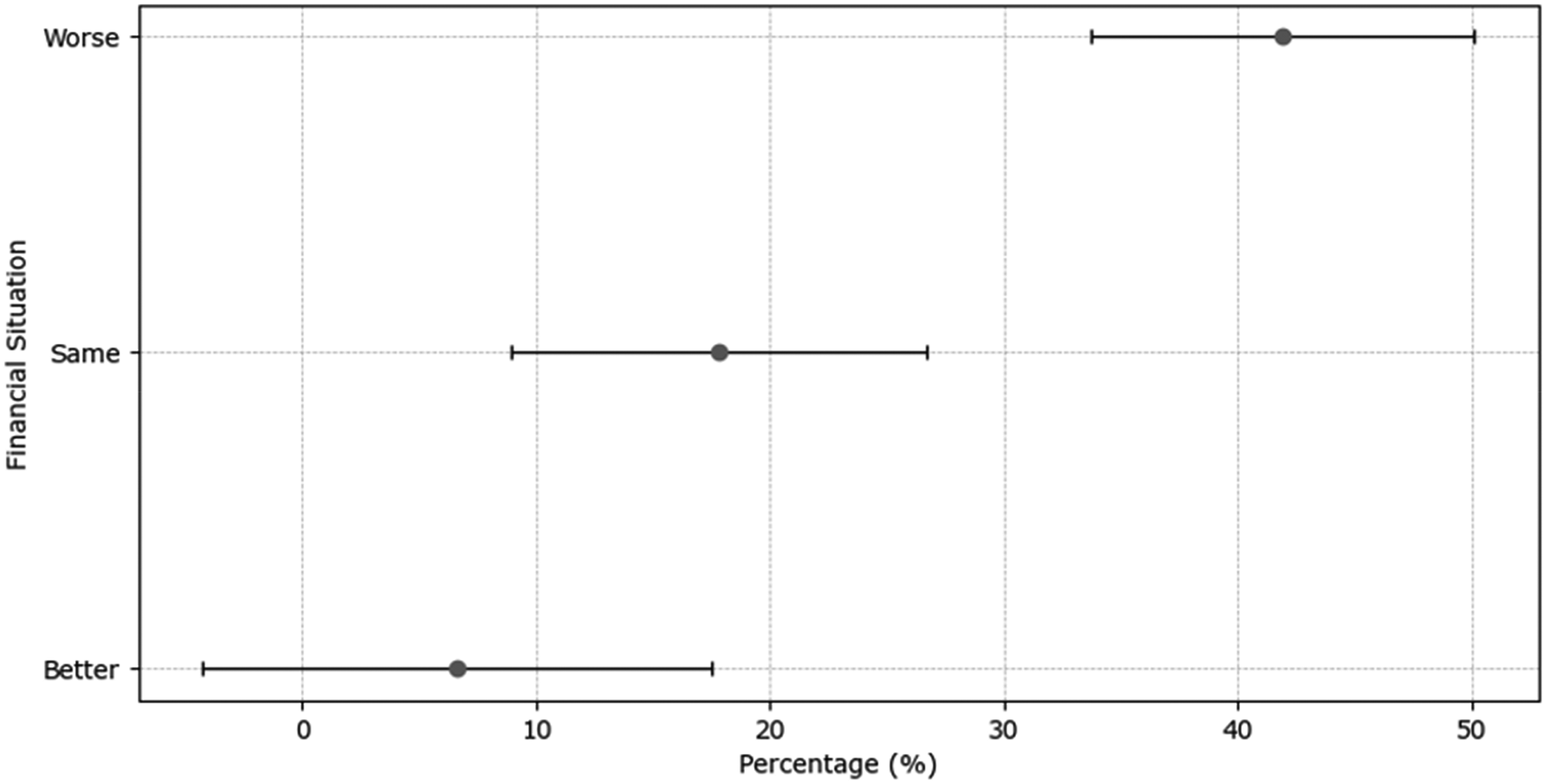

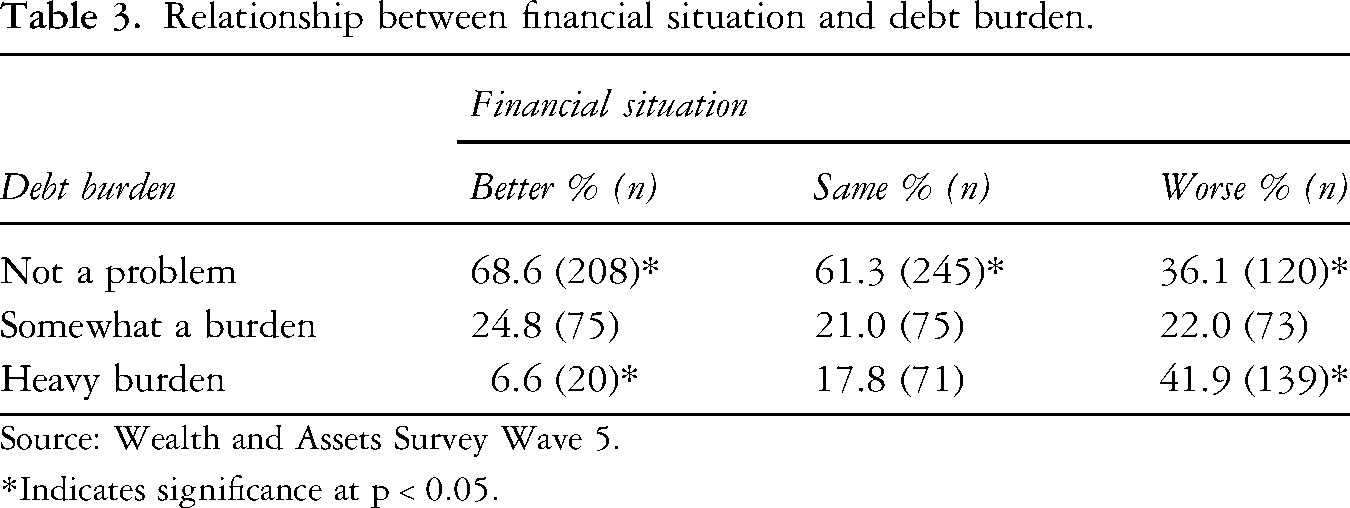

Table 3 and Figure 2 display the significant relationship between worsened finances and debt burdens. Two-fifths of those who reported worse finances than two years ago found debt a heavy burden. Those with worsened finances were nearly five times (OR: 4.84 CI: 3.55, 6.59) more likely to report experiencing a heavy debt burden than those who had maintained or improved their financial situation. The next section analyses the link between socioeconomic factors, worsened finances, and debt burdens.

‘Heavy’ debt burden category by financial situation (95% CI).

Relationship between financial situation and debt burden.

Source: Wealth and Assets Survey Wave 5.

*Indicates significance at p < 0.05.

Socioeconomic factors

The study examined household income among two groups: those with low household income (Q1) and those with higher income (Q2 to Q4). The study found a clear association between low income and a higher risk of reporting worse financial situations and debt burdens. Gender was also examined, but the confidence intervals for lone mothers and fathers were overlapping for both outcomes, making it hard to generalise the results to the broader population. There were no significant differences between ethnic groups in terms of reporting worse finances. However, compared to white lone parents, BME lone parents were more likely to report having a debt burden. The study also found that separated lone parents reported worse finances and debt than other marital groups. Unemployed lone parents were likelier to report worse finances than employed lone parents, but the two groups had no difference in debt burden. This suggests that unemployed lone parents have worse finances, but both groups face similar burdens with debt.

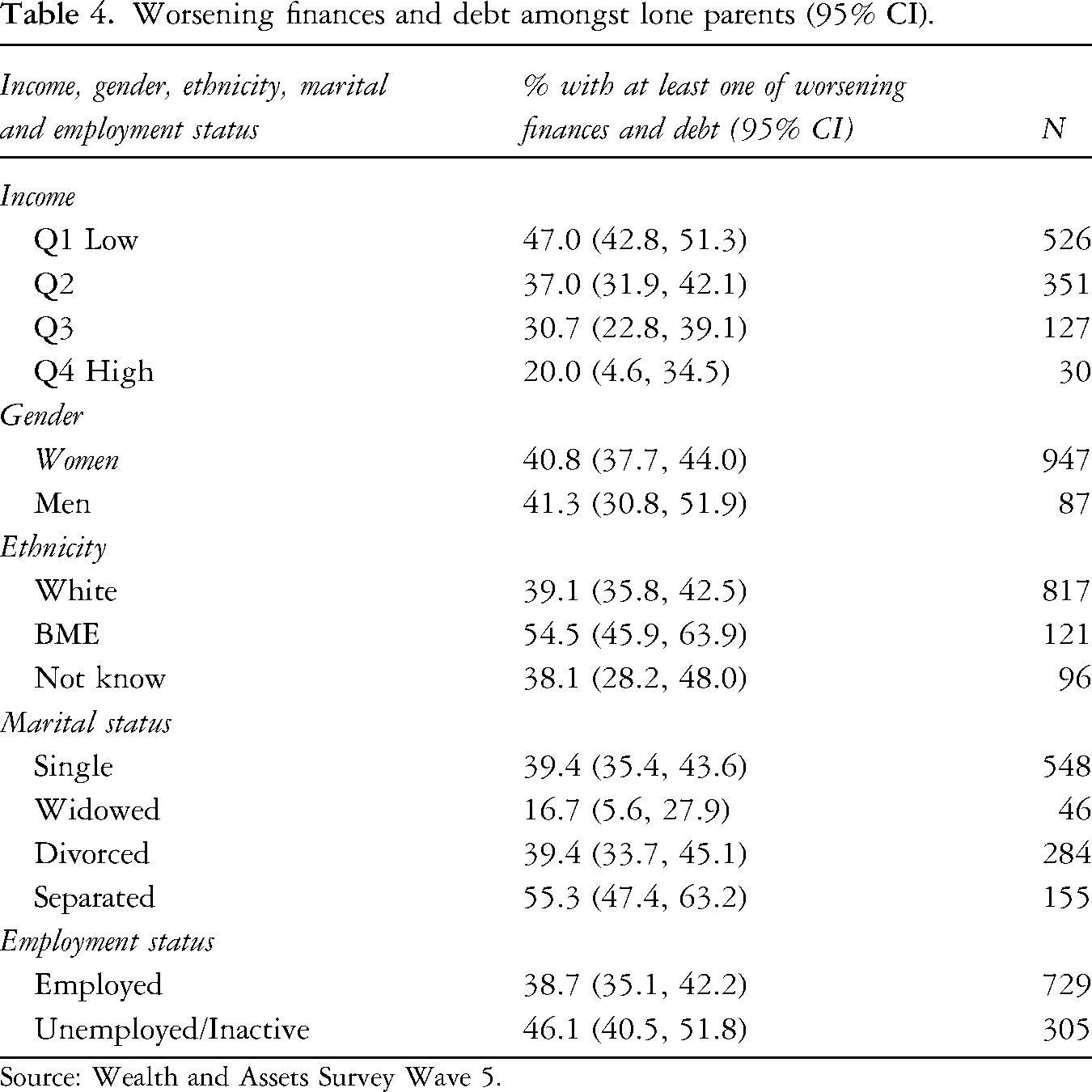

To account for the strong association between worse finances and debt burdens, a binary measure combining the two was created for participants who responded to at least one outcome. Table 4 compares socioeconomic factors using this measure. Results indicate that individuals with low income were significantly more likely to report worsened finances and debt, with the gap widening as income increased. BME and those who are separated reported having worsened finances and debt more than white and single lone parents. Contrastingly, widowed lone parents were generally less likely to report worsened finances and debt than other marital statuses. Lastly, the unemployed were more likely to report experiencing worsened finances and debt than the employed.

Worsening finances and debt amongst lone parents (95% CI).

Source: Wealth and Assets Survey Wave 5.

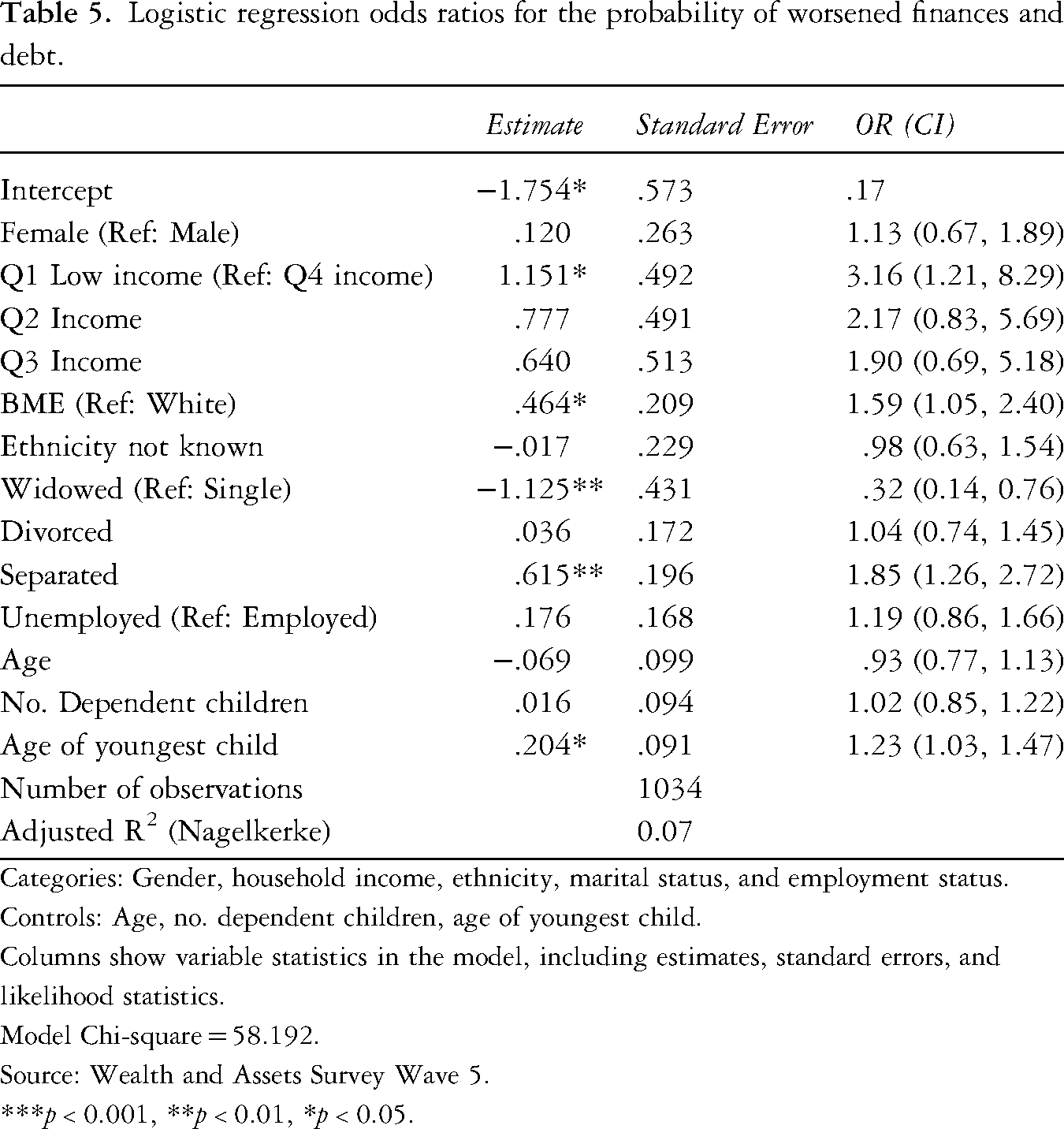

Table 5 reports on a logistic regression model and odds ratios used to measure the likelihood of worsened finances and debt among lone parents. The model included multiple socioeconomic factors and control variables relevant to lone parents’ backgrounds, life stages, and family arrangements. Odds above 1 indicate more likely, and those below 1 are less likely, to have worsened finances and debt.

Logistic regression odds ratios for the probability of worsened finances and debt.

Categories: Gender, household income, ethnicity, marital status, and employment status.

Controls: Age, no. dependent children, age of youngest child.

Columns show variable statistics in the model, including estimates, standard errors, and likelihood statistics.

Model Chi-square = 58.192.

Source: Wealth and Assets Survey Wave 5.

***p < 0.001, **p < 0.01, *p < 0.05.

After accounting for gender, ethnicity, marital status, employment, age, youngest child's age, and the number of dependent children, it was found that income was strongly associated with worsened finances and debt. Low-income lone parents were three times more likely to report worsened finances and debt compared to the highest-income group. Interestingly, no significant differences were found between lone mothers and fathers. However, BME lone parents were more likely to report worsened finances and debt than white lone parents. In addition, widows were two-thirds less likely, and those separated were twice as likely to report worsened finances and debt compared to those who were single. No significant differences were found between the employed and unemployed groups in terms of the outcome measure. Interestingly, the youngest child's age – an often-used policy indicator for lone parent entitlement to welfare benefits – showed that as the child aged, lone parents reported worsened finances and debt.

To examine lone parents’ financial challenges in more depth, the individual circumstances and experiences of a group of low-income lone parents are now considered.

Interview evidence: The financial challenges of lone parents

Around two-thirds of the qualitative sample of lone parents faced financial challenges. These were often consequential and triggered by complex issues. Building on the quantitative findings which showed associations with worsened finances and debt, the key themes emerging from the qualitative interviews sought to explain the temporalities around: (a) reasons for falling into debt – the multiple and intersecting factors that compound debt, (b) worsening finances, debt, and difficult decisions – the experience of managing day-to-day finances (c) limited choices and support – having minimal financial options and access to resources, and (d) affected futures – how constrained finances impact financial planning.

Reasons for falling into debt

As the quantitative findings observed, many participants struggled with debts, particularly household arrears. Half described this happening at least once. The main explanations were a shortfall between income and expenditure and changing circumstances. Life events such as separation, changes in employment status, and administrative errors with welfare benefits were often cited as the main reasons.

After separating from her husband, a migrant unemployed lone mother discussed experiencing a ‘bad financial situation’ (see Table 3), leading her to borrow money from multiple sources to get by (see Jenkins, 2011). Unfortunately, the support they received was time-limited, and repayment of these debts depended on her finding work and increasing her income.

Among the fifth of lone parents whose employment status had changed across waves of the interviews, this also meant confronting the complexities of the welfare system. Another lone parent described moving into work, which led to owing over £4000 for an overpayment of housing benefits. Now unemployed and once again claiming, they were informed of the need to repay this money. Reflecting on the deepening worries this caused and the risk they faced with destitution, they commented: ‘I am in more debt now than I was in … if they half that debt, then I still owe £2000, for what reason? I couldn't afford to facilitate my life, let alone pay my rent.’

Transitions between employment and unemployment were common, which meant being exposed to income loss through administrative errors in welfare benefits (see Table 3). Lone parents were put on the wrong benefits and lost considerable income, as did those sanctioned for not meeting certain conditions. In many cases, changing circumstances triggered notable financial insecurity and a deepening of debt, with only a few instances where work provided some security.

Managing debt and making difficult decisions

For two-thirds of the participants who described experiencing a worsening of their finances, the main concern was navigating how to meet their families’ everyday needs, including decisions on how to manage debt and arrears best. Shedding further light on the quantitative findings, the costs associated with caring for children as they age and move on to school were a contributory factor. Having just celebrated a child's birthday, a lone parent described how affordability and struggles with debt meant having to ‘manage’ their money closely. They commented: ‘I'm still struggling with that [debts] but I'm managing. I'm coping. I'm not desperate. This week is a very poor week for me … I've just got to manage’.

Worryingly, many of these lone parents needed help to meet basic costs associated with childcare, clothing (including school uniforms), and transportation. Some lone parents spoke of using food banks to get by. In a few instances, the choices were stark, with parents making sacrifices to ensure their children had enough food and warm water (Dermott and Pomati, 2016).

As the quantitative findings above found, income reductions were a common reason for worsened finances, which can lead to worries about needing more money to manage daily expenditures. Despite the UK government's denial of the harshness of sanctions, lone parent sanctions increased from less than 200 to 5000 per month in 2014 (Fawcett Society, 2015). While sanctioned, a lone parent reflected on the need to find money to pay for everyday expenses and their reliance on borrowing (see Table 3). Various strategies were used to manage a lack of disposable income, such as borrowing from credit cards, payday loans, or (where able) borrowing from family and friends (see Millar and Ridge, 2009, 2017), which for some led to strained relationships and limited help.

Not all lone parents coped well with financial shortfalls. Bailiffs regularly contacted those with debt burdens, with some receiving court summons letters. Because of the severity of their situation, some spoke of a need to find ways to manage debts actively. In a few instances, the debt obligations were not their own but still weighed heavily on them. For example, a separated lone mother described how multiple thousands of pounds of debt were left to her by her former partner. These debts left her needing to make difficult decisions. Interestingly, close kin were referred to as a moral compass to help steer her through this difficult time. She commented: ‘I've sold off [everything] very sadly, heirlooms of my parents, my grandparents … [it's] heartbreaking still, but then I know my father would have said ‘You need it, sell it. Feed your children.’

It was clear the difficulties many lone parents faced with keeping debts manageable. At times, this meant making arrangements with creditors that later became unaffordable. This did not deter one lone parent from pushing to resolve their debts, who commented: ‘I have a few payment plans that I wasn't able to honour or delaying … It's around £5000 I think … I don't shirk from anything. You have to face everything head on.’

Contrary to the political-moral belief that lone parents are ineffective at managing their finances, the interviews suggest a different view: that they act in ways that limit the immediate and detrimental effects on their families by attentiveness to immediate pressures. In some instances, this included decisions to seek debt advice and advice for other issues, such as welfare benefits and housing, when they faced severe problems.

Limited choices and support

Many lone parents found they had few financial choices and limited access to support. After already undertaking a form of insolvency through a debt advice agency, this unemployed lone parent was concerned about how they would get by with the bit of money they had: ‘I can't survive on this, but I need to do something for the future, so I don't end up back like this … I did a debt relief order like a few years ago, so if I get into debt again now … can't wipe it off or like have anybody help me. I don't have people that pay my bills.’

In a later interview, this lone parent became homeless and described still being threatened with bailiffs and formal proceedings to collect outstanding debts: ‘I've tried to contact them. They're not interested. I'm saying to them I'm homeless right now, I cannot afford to give you anything more than I've got right now … I said where are you going to come, where are you actually going to come and take me stuff because I don't have anything?’

Like the quantitative findings, high debt repayment was a source of deteriorating finances because servicing debts meant no money was available (Hartfree and Collard, 2015). Like the previous lone parent, whose debts remained burdensome even after accessing debt advice, this was triggered by having few options to find additional help.

Affected futures

The final theme to discuss is affected futures. Many lone parents indicated they were struggling financially and worried about immediate financial issues, which limited their focus on planning (see Mullainathan and Shafir, 2013). For example, a pregnant, unemployed lone parent with unaffordable rent arrears of £120 described being unable to afford to pay back her arrears alongside meeting pressing everyday outgoings. As a result, she was summoned to court, with additional fees later added, generating stress and fear that she would lose her family's home. She described the effect of debt and low income on financial planning, commenting: ‘I don't like to plan ahead. I just take each day as it comes.’ This suggested a narrowing of focus to the immediate present and to control her finances closely now, as opposed to being able to think about future development.

Another unemployed lone parent, whose washing machine and fridge had broken down, described using a rent-to-own store to purchase new appliances on credit. As part of the agreement, the high and long-term repayment costs meant paying £33 a week, estimated at £5000 over the next three years. In her reflection on how the burdening effect of debt has impacted the materialisation of future ambitions, they commented: ‘It does make you think well … you can't do anything about it [Debts] right now, but I'm not that type of person and it will affect my future, it will affect the fact that I want to be able to own my own home.’

The concern of paying back expensive and high-interest debts appeared to generate a state of inertia, an inability to see further than the ‘next bill’, with immediate demands prioritised over longer-term goals.

The experiences of these lone parents took place against the backdrop of the removal of government support, including the withdrawal of access to emergency loans that tide people over (Dabrowski, 2021). Only a fifth of participants described accessing emergency loans, and some even recognised that using emergency funding would have been more affordable.

Integration of findings

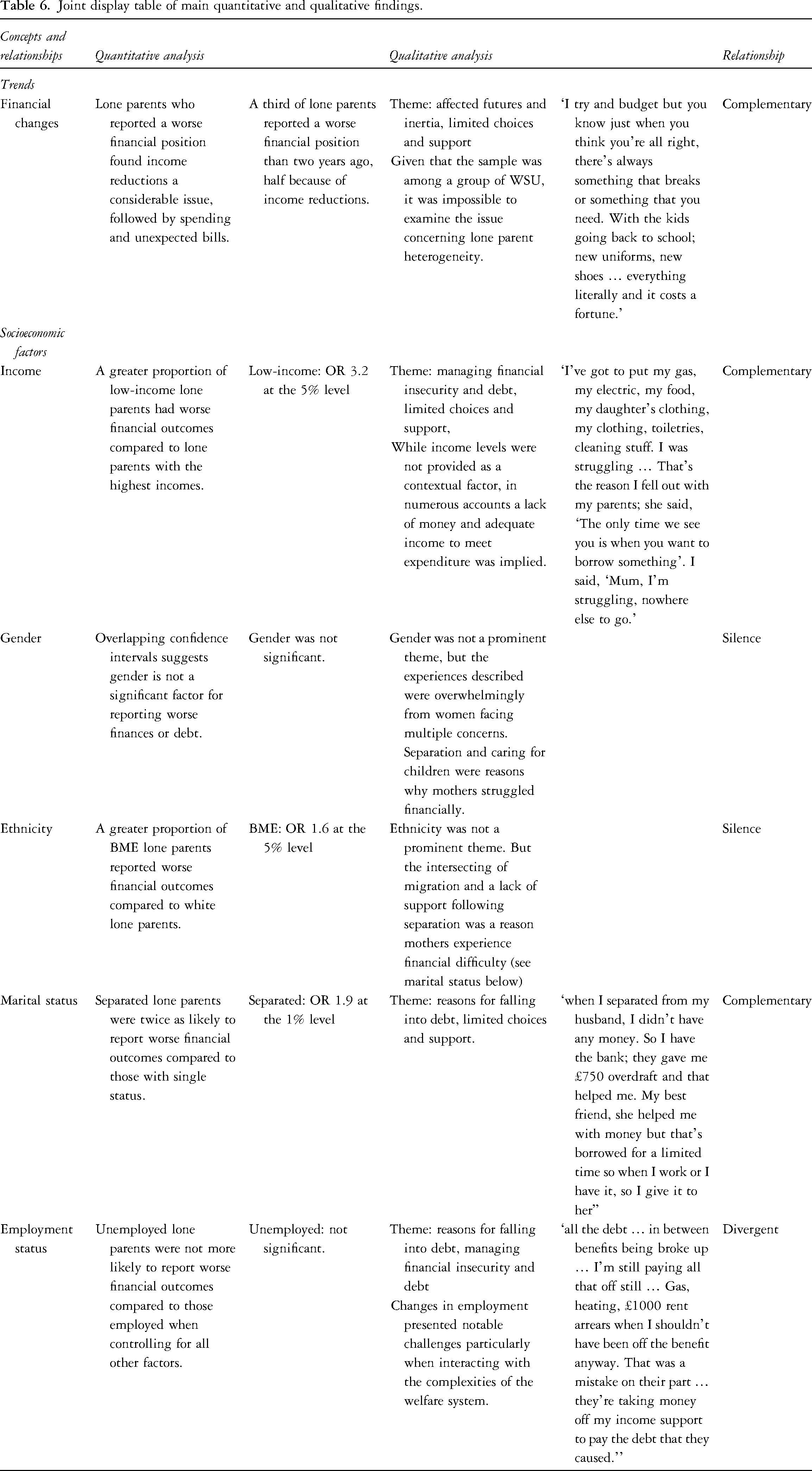

Table 6 shows a joint display table exploring the relationship between each strand following the research aims. Findings aligned to the fundamental concepts of (1) changes in a financial situation and (2) socioeconomic factors, with findings, statistics, themes, and quotes from the research presented alongside these concepts (Bazeley, 2016). The relationships between findings were evaluated to determine whether they were complementary, divergent, or silent. Complementary findings between qualitative and quantitative strands included understanding factors that limit financial situations, particularly regarding income adequacy. The qualitative results confirmed that lone parents were acutely aware of the changeability of their financial situation and income constraints, which impacted future courses of action. There is a sense of powerlessness to address these issues, particularly among those in debt. Intersecting life courses and events, leading to worsening finances, often triggered debt burdens. These intersections impacted participants, leading some to borrow money from friends and family or use formal credit to make up for shortfalls, limiting the money they had available to correct further deficits.

Joint display table of main quantitative and qualitative findings.

The quantitative results found no clear relationship between unemployment and worsening finances or debt, but diverging accounts were found in the qualitative data, where changes in paid employment meant reductions to welfare payments. A key factor that worsened lone parents’ financial outcomes was how changes in their employment status interacted with the complexities of the welfare system, leaving them at risk of facing administrative errors and needing to pay money back to the government. There is a need to understand employment on a more granular level.

The relative silence across both datasets regarding gender and ethnicity should not be taken to imply that these dimensions are unimportant in understanding lone parents’ worsening finances and experiences of debt. While not central analytical variables, their significance must be acknowledged. In the quantitative data, over 90% of the lone parent sample identified as female, while the small number of male lone parents limited meaningful statistical comparison. However, this gender imbalance reflects broader demographic patterns of lone parenthood. Gendered dynamics were apparent in the qualitative data, particularly around caregiving responsibilities, barriers and expectations around financial provision, although not always framed explicitly in gendered terms. Although statistically associated with worse financial outcomes in the quantitative data, ethnicity was not as prominent in the qualitative narratives. This absence may reflect limitations in how these themes were captured in the original study design rather than a lack of relevance. Given that the sample was predominantly composed of lone mothers and that ethnic minorities experience greater financial insecurity in the wider population, it is likely that underlying structural inequalities shaped participants’ experiences. These intersecting dimensions may help to contextualise and unpack the findings.

Discussion and future implications

The impact of changing financial situations and debt is complex and better understood by combining and integrating the strengths of quantitative and qualitative methods. This study draws on evidence from the mid-2010s, a period marked by significant socioeconomic change, including welfare reforms and increasing precarity in employment. While the findings provide critical insights into the financial pressures faced by lone parents during that time, it is essential to recognise the evolving context, including the COVID-19 pandemic and the ongoing cost-of-living crisis, that have likely exacerbated financial vulnerabilities for this group. These developments highlight the need for ongoing research to build upon these findings, ensuring policies address both historical and emerging challenges lone parents face.

This article has examined the extent to which lone parents in the UK face financial changes and how they attempt to manage their debts, given considerable constraints. A secondary mixed-methods analysis cast new insight into this area of research. This analysis builds on previous research that examined the financial circumstances of lone parents by providing updated evidence through an examination of a national-level survey and previously collected interview data. Together, this has further highlighted the ongoing challenges that lone parents face. Through interrogation of personal testimonies, themes on the impact of worsening finances and limited choices have emerged as a critical debt mechanism.

The associations presented in this research show a clear and often complex picture of lone parents’ financial challenges, particularly in the proportion of those with debt burdens. The qualitative and quantitative evidence finds agreement on the strong relationship between inequality, debt, and its negative impact on people's agency (Orton, 2009). Furthermore, given wider austerity and the low-income status of lone parents impacted by socioeconomic changes (Gingerbread, 2019; Womens Budget Group, 2017, 2020), they are often forced to find ways to solve their financial situation. This reflects previous findings of a growing body of research on low-income families (Brewer et al., 2013; Daly and Kelly, 2015; Hills, 2015).

The qualitative interview data revealed multiple risks for lone parents, with competing financial priorities contextualising the difficulties of managing debt. Income reductions and changing circumstances compounded concerns about being able to provide for their families and meet living costs and household expenses. In addition, financial disruptions limit future planning and often shape the ways lone parents use money (Millar and Ridge, 2017), which can sometimes lead to debt being used to cover shortfalls. Overall, lone parents bear significant debt burdens compared to other families, which are repercussions of their trying to manage daily finances. Given these challenges, it is difficult to see how the most susceptible to worsening finances could benefit from financial literacy policies to prevent poverty and debt, where there is an apparent lack of money to manage basic needs.

Participants often described difficulties with a lack of support, particularly during life events and transitions, with a pressing need for lone parents to find alternative ways to cater for their family's needs. As borne out in quantitative and qualitative findings, compared to lone parents who may be more used to managing less money, those who had separated were a particular concern and most often worse off (Jenkins, 2011). In particular, this meant making tough decisions, which led to debt burdens. A further finding revealed that while unemployed lone parents have a worse financial position, there are reasons other than the burden of debt that impact them. These include low-income, income reductions, increased spending, and earning capacity, particularly given their care responsibilities.

Even if their financial situation later recovers, lone parents can encounter financial difficulties with debt that is not of their own making and will later need support. This study reflects evidence of the harshness of welfare policies over the last decade of austerity, which are linked to experiences of financial insecurity (Taylor-Gooby, 2015). Negative experiences of unsupportive welfare conditions, including receiving the wrong benefits and the threat posed by sanctions, can and do undermine lone parents’ ability to manage financially, particularly during unavoidable changes and transitions in their situation, such as moves into, between and out of paid employment. Overall, these findings reveal how experiences of debt burdens are compounded further by the socioeconomic disadvantages and inequalities that lone parents already face in terms of gender, race, and class. (Johnsen and Blenkinsopp, 2018).

Informing policy

The implications of this research for policy and practice are based on data collected well before the COVID-19 pandemic. However, the critical implications of the findings discussed here are even more profound for lone parents and their families. Therefore, the recommendations are based on results related to current circumstances and are most relevant for lone parents. This research reinforces the importance of specific policies that could be targeted to support lone parents by incorporating an understanding of their varying circumstances. The findings primarily show that for half of lone parents in the UK, those in the lowest income quartile and earning under the benefit cap (see DWP, 2020) remain at the highest risk of debt. Most families relying on government support as a source of income are vulnerable to the negative impacts of high-cost debt. Issues among welfare recipients were a clear and concerning feature of this research. Many found that the welfare system hindered their ability to progress and mobilise in financial, social and economic life.

Policies should address ways to support lone parents by acknowledging how their circumstances often differ from other families with more and better access to resources and affordable credit. Reinstatement of access to crisis funds would help lone parents in financial need, especially those at transition points. Schemes such as those launched during the COVID-19 pandemic, which increased child benefits and tax credit payments, would help reduce poverty among these families and their children (CPAG, 2020). Furthermore, free-to-all money and debt advice services remain a lifeline for families and require ongoing support to remain free and accessible to communities.

Study limitations and future research

The study had limitations. The size of the survey sample limited some of the analysis. Interviews were also taken from a sample of over-represented WSUs. In the context of austerity, where low-income groups are exposed to changes in the welfare system, negative experiences could be expected to impact families supported by welfare significantly. Despite its limitations, this study's use of a secondary mixed methods approach and analyses of large, rich, and diverse data from which key insights were drawn is a particular strength. QSA provided a unique way to complement and expand quantitative findings, focusing on temporal and socioeconomic changes and helping offer new understandings of financial insecurity and debt. Future research should aim to achieve greater synthesis and better understand the intersectional variations by using a broader qualitative sample and a larger quantitative sample.

Footnotes

Acknowledgements

I would like to thank Professor Jackie Carter and Professor Sarah Marie Hall for their guidance while conducting the research that forms the basis of this article. I would also like to thank Timescapes archive and UK Data Service for access to the data used in this article. Thanks also to the Economic and Social Research Council (ESRC) for funding of this research.

Funding

The author received funding from the Economic and Social Research Council (ESRC) for the research, authorship, and/or publication of this article.

Author biography

Email: gb501@cantab.ac.uk