Abstract

Small- and medium-sized enterprises (SMEs) are one of the engines for inclusive economic growth. Yet little is known about the contribution of human resource management (HRM) practices to the success of SMEs. This study empirically examines how HRM practices determine different categories of innovation of SMEs in the context of a transition economy. Using a longitudinal dataset and applying the instrumental variable methodology to correct for endogeneity problems, our study uncovers that HRM practices positively affect the quality of employed human and physical capital assets of SMEs. More importantly, we find that that HRM practices significantly contribute to the launch of new products and improvement of existing products. In addition, we also find that the adoption of HRM practices facilitate labour productivity and value added. Taken together, these findings highlight that HRM practices are a strategic resource for innovation and development of SMEs in transition economies by rewarding them with higher-quality capital assets.

Introduction

Small- and medium-sized enterprises (SMEs) in transition economies constitute an engine for inclusive economic growth since they contribute to one third of total GDP. 1 Most of the SMEs are, however, weak and facing various constraints including limited access to entrepreneurship competences, workforce skills, finance, technology, infrastructure, networks and formal management practices (UN, 2012). These constraints prevent SMEs from efficiently carrying out innovation and managing human resources, which are considered as key sources of competitive advantages (Chowhan, 2016).

A large body of literature has evolved, that attempts to explain how human resource management (HRM) practices affect firm performance. Theoretically, it is widely agreed that better HRM practices lead to better HRM outcomes and improved performance of enterprises (Guest, 1987). Numerous empirical studies show that tackling the shortage of HRM practices is effective to enhance performance of enterprises (Saridakis et al., 2016; Sheehan, 2013). Nevertheless, Saridakis et al. (2016) point out that most of the previous studies are not rigorous to demonstrate the direction of causality. Moreover, little is known about the synergy between HRM practices and innovation of enterprises (Chowhan, 2016).

Nevertheless, none of these studies have analysed effects of HMR practices on various types of innovation of SMEs. Seeck and Diehl (2016) conducted a survey of all studies published during the period of 1990–2015 and found only 35 empirical studies investigating impacts of HRM practices on innovation. Of these 35 studies, only five were detected in developing countries and all of the five studies were conducted in China. None of these studies, however, distinguishes effects of HRM practices on different categories of innovation. Harney and Nolan (2014) also argue that future research to examine HRM in SMEs needs to better differentiate various categories of SMEs and takes into account SME’s specificity, which leads to unique HRM practices.

This study fills the gap in literature by empirically analysing causal links between HRM practices and different categories of innovation in SMEs by utilising a large dataset from five rounds of biannual SME surveys conducted in Vietnam from 2007 to 2015. SMEs are defined as independent enterprises with registered capital of no more than 20 billion VND or employing fewer than 300 workers on average over a year in Vietnam (Chinh Phu, 2009). We hypothesised that application of HRM practices helps SMEs employ higher-quality capital assets, increase possibility to gain innovation and achieve better performance.

Applying the resource-based theory to link HRM practices with innovation and performance of SMEs as well as an instrumental variable methodology to correct for endogeneity problems in estimation, the study finds that HRM practices positively determine the employment of higher-quality capital assets. The SMEs that apply HRM practices are more likely to achieve innovation in existing products and new production process. In addition, the study confirms a causal positive relationship between HRM practices and performance measured by labour productivity and total value added of the SMEs.

The rest of the study is organised as: The next section provides a theoretical framework and advances testable hypotheses. The third section presents methodology. Empirical results with discussions are presented in the fourth section. The last section concludes the article.

Theoretical Framework and Testable Hypotheses

The Resource-based Theory and a Transmission Linkage Between HRM Practices and Firm’s Competitive Advantages

According to the resource-based theory, heterogeneous enterprises acquire sustained competitive advantages by exploiting their strategic physical, human and organisational capital resources. Physical capital resources include firm’s physical technology, plant and equipment, and geographic location. Human capital resources include training, experience and intelligence of managers and workers. Organisational capital resources include firm systems of reporting, planning, controlling and coordinating. These strategic resources are scarce, valuable, imperfectly imitable and having no strategically equivalent substitutes so that they hold the potential of generating sustained competitive advantages. These firm-specific resources are hard to be imitated because of their attributes such as asset specificity, social complexity, path dependency and causal ambiguity (Russel et al., 1985). These strategic resources are not highly mobile so that firm’s competitive advantages are sustained (Barney, 1991). According to this theory, enterprises with these distinct and imperfectly inimitable resources are often strategic innovators. The resource-based theory assumes that the relationship between strategic resources and sustained competitive advantages is complex and not fully understood by both the owning firm and all of its competitors.

The resource-based theory provides a foundation to understand the link between HRM practices, human capital and the implementation of other strategic choices (Becker & Huselid, 2006; Wright et al., 2001). Using HRM practices to provide people with knowledge and skills, retain people, and induce people to be immobile, enterprises are building up high performance work systems (HPWS) that are essential to achieve sustained competitive advantages (Messersmith & Guthrie, 2010). Messersmith and Guthrie (2010) propose a theoretical model to link HPWS to firm performance. In this model, HPWS causally affect ambiguous firm processes to generate human capital and innovation, which determine performance of enterprises. The framework of these ambiguous firm processes is similar to the black box in Chowhan (2016), which was proposed as a transmission linkage between HRM practices and firm performance. In this black box, human capital and innovation are identified as major components. Following Messersmith and Guthrie (2010) and Chowhan (2016), this study argues that HRM practices act as a strategic source of human capital development and innovation that generates sustained competitive advantages for SMEs.

HRM Context in Vietnam

The Doi Moi (economic reform) started in 1986 has transformed Vietnam from a centrally planned economy to a market-oriented one, leading to rapid increase in income per capita. The economy of Vietnam has become more open with rising trade openness and increasing stock of foreign investment (MPI, 2014). Local enterprises have new opportunities when information, technology and knowledge on management become more affordable and markets are expanded. At the same time, enterprises face with intensified competition and rising vulnerability when they are exposed to dynamic markets.

In this process of integration, the economy has been undergoing radical adjustment of the growth structure. Policies to restructure state-owned enterprises (SOEs), which used to dominate in the economy, have been emphasised. Improving business environment including institutional, legal and economic aspects is on top of the government development agenda. The private sector has been receiving increasing attention and support to have better access to education and training, finance, information, technology and business development services. Reform in the education sector has been promoted to develop high-quality human resources for a growing demand of enterprises (World Bank and Ministry of Planning and Investment of Vietnam, 2016).

Within the private sector, SMEs account for the majority. Changes in management of SMEs have been taking place. Vo (2009) mentions that HRM is, however, a relatively new concept in Vietnam, which was just introduced in the 1990s by foreign invested enterprises. The life-time employment system in the former centrally planned economy was replaced by the individual labour contract system. Since the 2000s, collective bargaining has started. Labour unions have become more independent. Enterprises are given more autonomy to hire and fire employees. Many SMEs have been originally spin-offs from SOEs. As a result, HRM practices in the former were largely affected by that in the latter (Collins et al., 2018). Zhu (2005) points out that the political, cultural, legal and economic factors determine labour flexibility in Vietnam. Since great emphasis is on organisational and personal commitment in harmonious working environments, full deployment of functional flexibility is prevented in Vietnam. Thang and Quang (2005) evaluated functions of HR departments, recruitment and selection, training and development, performance appraisal and compensation schemes of enterprises in Vietnam and concluded that foreign-invested enterprises are more likely to use HRM practices than SOEs and SOEs adopt more HRM practices than local private enterprises.

Changes in institutions in general and industrial relations and HRM systems in particular in Vietnam have been similar to what has been taking place in other transition economies such as China (Collins et al., 2018). According to MPI (2014, 2016), industrial relations in private enterprises, particularly in SMEs, were lagging behind. Payment to workers has been low and fringe benefits have not been fully paid to employees leading to rising labour conflicts and strikes. Percentage of the SMEs that paid health and social insurance was 28.3% in 2014. This proportion among the micro sized enterprises was less than 10%. Working conditions in the SMEs have not been improved recently. More than 63% of the SMEs are owner-managed household enterprises, which have neither developed a separation of ownership and control nor employed professional managers (MPI, 2016). Most of SMEs adopt a flexible approach to labour relations. Salaries paid to employees are largely based upon fluctuating performance of SMEs.

Brief Information About SMEs in Vietnam

Before 1986, when the reform policies were implemented in Vietnam, the private sector and private enterprises had been prohibited. During the transition period, in addition to restructuring the state sector, the government has been greatly promoting the private sector (World Bank and Ministry of Planning and Investment of Vietnam, 2016). As SMEs have been constituting the majority of enterprises in the private sector, playing an increasingly important role in creating employment and generating higher and more stable income and becoming one of the engines for economic growth, policies to support the development of SMEs have been among the top priorities in the development agenda of Vietnam (MPI, 2016).

SMEs include micro, small, and medium-sized enterprises. By definition, micro-sized enterprises employ 1–9 workers, while small and medium enterprises employ 10–49 workers and 50–299 workers, respectively (Chinh Phu, 2009). SMEs in Vietnam are either state-owned, non-state or foreign invested enterprises, of which the majority is non-state. Over the last few decades, SMEs have emerged as a major dynamic force for economic growth in Vietnam. The recent report shows that SMEs contributed 45% to the national GDP and 31% to total budget revenue, and about 5 million jobs were generated by SMEs (MPI, 2019).

Nevertheless, SMEs still experiencing various operational difficulties and growth constrains. Due to the destructive effect of the global financial crisis in 2009, the competitive advantage and survivability of SMEs have damaged significantly. According to CIEM (2012), 60% of the surveyed SMEs reported that the crisis negatively affected their businesses and they have reduced investment and innovation. About 20% of more than 2,500 SMEs that participated in the survey in 2009 have closed their businesses by 2011 due to increasing difficulty in accessing credit, increasing inventories, and serious shortage of skilled labour. MPI (2016) indicated that nearly 50% of the new employees did not have skills required by employers in 2014.

Since 2013, SMEs have been gradually recovering from the crisis. Within 2013, more than 49,000 new SMEs were established, which was almost double the number of new entrants in 2003. Enterprises with small and medium size accounted for 21.2% and 1.6%, respectively. More recently, research by the World Bank (2020) shows that the percentage of SMEs has rose to more than 97% in 2019.

HRM Practices as a Strategic Resource of Employment of New Capital Assets in SMEs

Wright et al. (1994) argue that HRM practices are the organisational activities to manage the pool of human capital. HRM practices determine the development of human capital pool, which contributes to sustained competitive advantages. They emphasise that in an ever fast changing environment enterprises with higher levels of human capital are more dynamic to sense the need for change and efficiently develop and implement strategies to change. HRM practices, moderate the relationship between human capital pool and sustained competitive advantages by affecting human resource behaviour. In Vietnam, shortage of skills has been a constraint for enterprise development (Collins et al., 2018; Vo, 2009). MPI (2016) emphasises that in such condition SMEs are facing greater challenges because they have to compete with large and foreign invested enterprises in recruiting skilled workers and accumulating human capital to survive. HRM practices have become a valuable system to develop human capital pool for SMEs.

Ferligoj et al. (1997) point out that capital markets in transitional economies are less developed. SMEs in Vietnam seriously lack high-quality physical capital for development partly because of their limited access to finance and partly because of their limited access to labour skills, which are indispensable to operation of advanced machines and technologies (MPI, 2014, 2016). As pointed out by Chowhan (2016), it is reasonable to link HRM practices and SMEs’ ability to recruit and retain higher-quality human and physical capital assets. It is, thus, worth testing the following hypothesis:

HRM Practices as a Strategic Resource of Innovation of SMEs

Innovation of enterprises in the black box proposed by Messersmith and Guthrie (2010) and Chowhan (2016) is determined by HRM practices. Other studies support this argument by verifying important roles of HRM practices in innovation of enterprises (Kalleberg & Moody, 1994; Knoke & Kalleberg, 1994). Kalleberg and Moody (1994) point out that training of workers was important to the development of new products. Knoke and Kalleberg (1994) confirm that training of workers helps enterprises adjust to changes powered by technological innovation, market competition, and organisational restructuring. Ferligoj et al. (1997) emphasise that HRM practices determine competitive advantages of small enterprises in Slovenia by facilitating innovation. Nevertheless, Dabic et al. (2011) show that few studies have discussed the relationship between HRM and entrepreneurship, of which three components include novel technologies and processes as well as new products and services.

Earlier evidence shows that firms’ innovative capacity depends heavily on employees’ knowledge and creativity (Mumford, 2000). In addition, employees’ enthusiasm and support are also crucial for the development and implementation of innovative plans (Vrakking, 1990). Thus, human capital can be seen as a key resource of a firm’s innovation. Nonetheless, in Vietnam, many SMEs are facing insufficiency of capital and qualified staff (Dieu, 2006; MPI, 2014, 2016). This, as a consequence, imposes constraints for their investment in innovation activities, most of which are costly and risky (Sandberg & Aarikka-Stenroos, 2014). In this regard, when SMEs implement effective HRM practices such as training employees or offering suitable fringe benefits, they can be able to gain more strategic resources and might direct these valuable resources to carry out innovation. Thus, we hypothesise that:

HRM Practices as a Strategic Resource of Sustained Competitive Advantages of SMEs

It is widely agreed that human resources are important for building up firm’s competitive advantages. Even though enterprises’ competitors may realise that human resources are valuable, it is difficult for them to replicate (Razouk, 2011; Wright et al., 2001). HRM practices can be viewed as organisational competencies to influence employee behaviours such as motivation and loyalty (De Grip & Sieben, 2005). HRM practices are, thus, used to develop strategies that lead to sustained competitive advantages (Chowhan, 2016; Saridakis et al., 2016).

There is a large body of literature confirming that smaller enterprises tend to practice HRM more to gain competitiveness given their limited holding of other strategic resources. HRM practices conducted in small enterprises can be as sophisticated and diversified as they are in larger enterprises (Heneman et al., 2000). SMEs are fully aware of and more flexible to adopt changing HRM practices to improve performance (Lai et al., 2016). Nonetheless, Dabic et al. (2011) argue that there is a mixed picture of relationship between HRM practices and growth of SMEs.

Empirical studies used different indicators to proxy for enterprise performance. Delery and Doty (1996) investigate effects of HRM practices on financial performance. Huselid (1995) analyses their effects on employee turnover. MacDuffie (1995) examines the impact of HRM practices on operational performance measures such as quality, cost or delivery. Koch and McGrath (1996) found that utilisation of sophisticated human resource planning, recruitment and selection strategy positively affects labour productivity. Labour productivity is considered as one of the most desirable outcomes to proxy for enterprises’ performance because if a firm is good at utilising HRM practices, it should have highly productive employees (Patel & Cardon, 2010). Apart from labour productivity, another indicator frequently used to measure firm performance is value added (Sonobe & Otsuka, 2006). Therefore, we advance the following hypothesis:

Methodology

Data

This study is based on a dataset from five rounds of biannual surveys of manufacturing SMEs conducted in 10 provinces in Vietnam from 2007 to 2015. The surveys were conducted by the UNU-WIDER, the Institute of Labour, Science and Social Affairs under Ministry of Labour, Invalids and Social Affairs, the University of Copenhagen and the Central Institute of Economic Management. In each round of survey, more than 2,500 SMEs were randomly selected for the sample. In the following round of survey, a number of new SMEs were added to replace the exited ones from the previous rounds. In total, due to missing values, we have unbalanced panel data of 12,284 firm-year observations.

This dataset contains information about practices of HRM, characteristics of the SMEs including location, years of operation, number of workers, revenue from sales and other related information of the SMEs. Data of the previous year were collected during the current survey. For example, the survey in 2007 collected information of the SMEs in 2006. In a small number of enterprises with medium size, information about HRM practices is provided by either the person in charge or the head of department of human resources. In the majority of small and micro sized enterprises, owner-managers of the SMEs were the respondents of the surveys and provided all of the information related to the SMEs. Other related information is provided by the owner-managers of the SMEs. 2

Measurement of Variables

Innovation

Prior literature has employed a number of different proxies for firms’ innovation including new products and services, new methods and process, new technology, a new organisational structure, or a new market (Sonobe & Otsuka, 2006). In this study, based on the existing literature and availability of data, we evaluate SMEs innovation in three aspects: (a) product improvement; (b) process innovation; and (c) new product release.

Specifically, in the SME surveys, firms were asked whether they had (a) significantly improved a current product; (b) applied a new technology/production process since the preceding one; and (c) introduced a new product. Answers for these questions were code 1 and 0, with 1 indicating ‘yes’ (i.e., having applied a new technology/production process), and 0 otherwise. Thus, we construct three dummy innovation variables indicating product improvement, process innovation and new product release, respectively. We use these dummy variables as the main dependent variables to assess SMEs innovation.

In addition, we consider employment of higher-quality capital assets including human capital and physical capital as implementation of strategic choices. To that extend these strategic choices are equivalent to innovation as indicated in the black box proposed by Messersmith and Guthrie (2010) and Chowhan (2016). Quality of human capital assets of the SMEs is measured by ratio of full-time workers holding university degrees to total number of full-time workers. Quality of physical capital assets of the SMEs is measured by automaticity of machines. As many machines used in SMEs in Vietnam are outdated manual or semiautomatic, automatic machines are considered as new and higher-quality physical capital assets that can bring higher productivity and better performance for SMEs (MPI, 2016).

Performance of SMEs

We measure the performance of SMEs by total value added and labour productivity. Total value added is calculated as the natural logarithm of SMEs’ value added. Labour productivity is measured as total value added divided by number of full-time workers.

HRM Practices

HRM practices in this study are analysed in the broader human resource–performance literature. The selected HRM practices are commonly used in the literature of HPWS (Messersmith & Guthrie, 2010; Nguyen & Bryant, 2004; Razouk, 2011). Following Sheehan (2013) the selection of HRM practices in this study is based on five main areas of HRM: (a) recruitment and selection; (b) performance-based compensation pay; (c) training and development; (d) employee voice, consultation, participation and information sharing and (e) fringe benefits. Similar HRM practices are used in previous studies. Nguyen and Bryant (2004) adopted recruitment and selection, training, job descriptions, performance appraisals and human resource plans in their study about HRM. Similarly, Razouk (2011) included appraisals, participation, sharing information, compensation and communication in his analysis. It is noted that some of the usual HRM practices such as performance appraisal and internal recruitment are not available in the data. As a result, measures of HRM practices are largely about rewards and benefits to workers of the SMEs.

Previous studies have analysed effects of each single indicator of HRM practices on firm performance (Gerhart & Milkovich, 1990). Bundling complementary and mutually reinforcing HRM practices is shown to enhance the analysis (Pfeffer, 1998). In his study, Pfeffer (1998) considers that seven HRM practices are complementary to one another. For example, an organisation that offers employment security needs to selectively hire new workers, whose attitudes, values and behaviour fit with values of the organisation. With employment security, employees work together for a longer time and develop mutual understanding. Also, employment security retains employees longer so that it is more effective to invest in their training and education. Bundling these consistent and mutually reinforcing practices as a synergistic set is, hence, more effective than summing effects of the individual practices (MacDuffie, 1995).

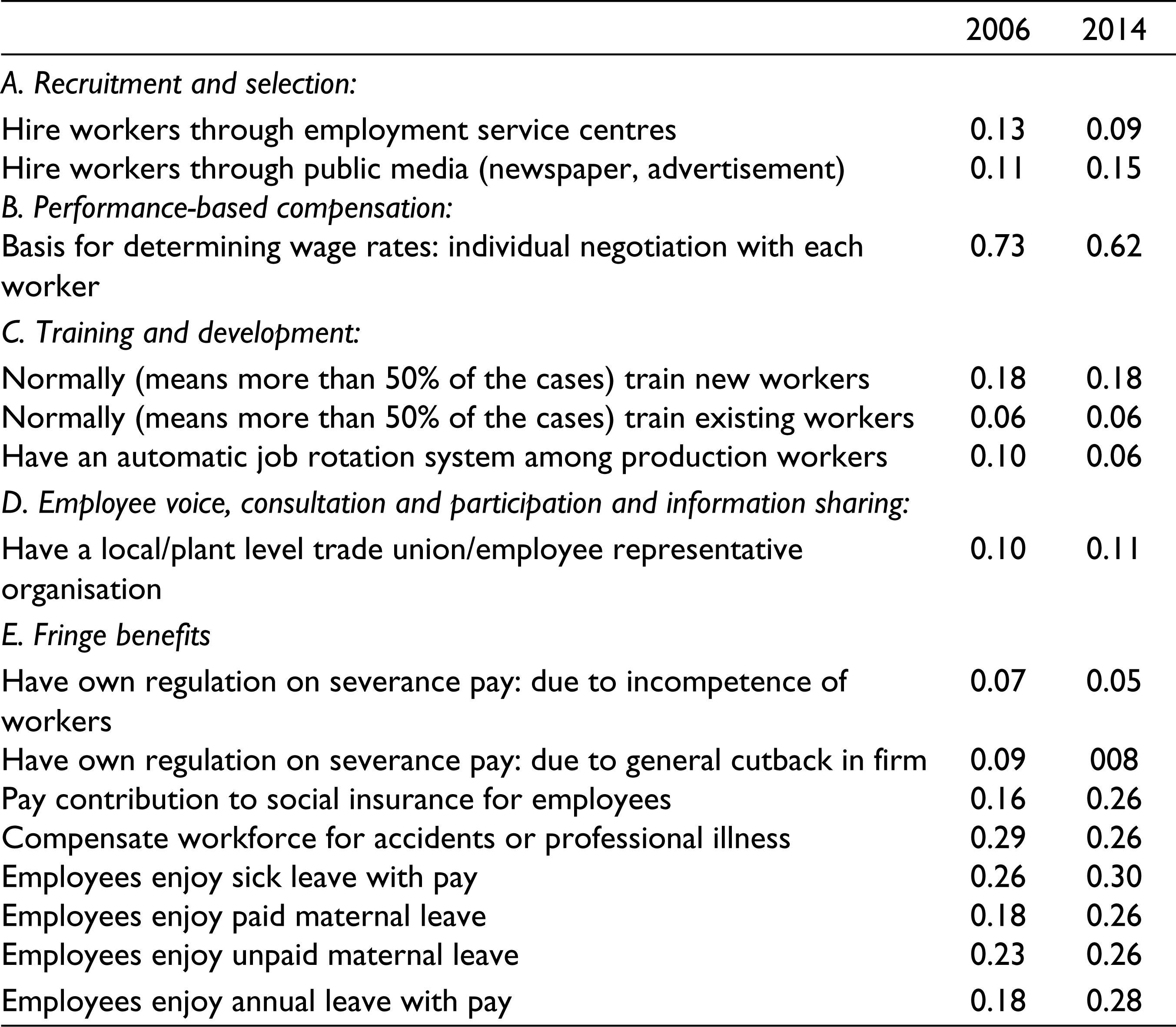

Therefore, in this study an HRM index is constructed by bundling 15 individual HRM practices. In each wave of survey, SMEs were asked if they (a) determined wage rates based on individual negotiation with each worker and (b) had a local/plant level trade union/employee representative organisation. In addition, regarding recruitment and selection, they shall answer whether or not they hired workers (a) through employment service centre and (b) through public media (i.e., newspaper, advertisement). With regards to training and development, firms were asked if they (a) trained new workers, (b) trained existing workers and (c) had an automatic job rotation system among production workers. Regarding fringe benefits, firms must answer whether or not they (a) had their own regulation on severance pay due to incompetence of workers, (b) due to general cutback in firm, (c) paid contribution to social insurance for employees, (d) compensated workforce for accidents or professional illness, (e) allowed employees to enjoy sick leave with pay, (f) provided employees with paid maternal leave, (g) allowed unpaid maternal leave and (h) provided employees with annual leave with pay.

Table 1 presents the average scores of individual HRM practices. In addition, we performed factor analysis to check if these 15 HRM practices formed different groups. A value of Cronbach’s alpha of 0.7 or more is used as a criterion for a reliable scale (Nunnally, 1978). The reliability analysis of these measures yielded a value of overall Cronbach’s alpha of 0.83. The factor analysis revealed that all of these measures loaded on to one factor and all individual HRM practices contribute strongly to the alpha value, justifying the synchronisation of these practices to form a single HRM index.

Score of Human Resource Management Practices Adopted by SMEs

Control Variables

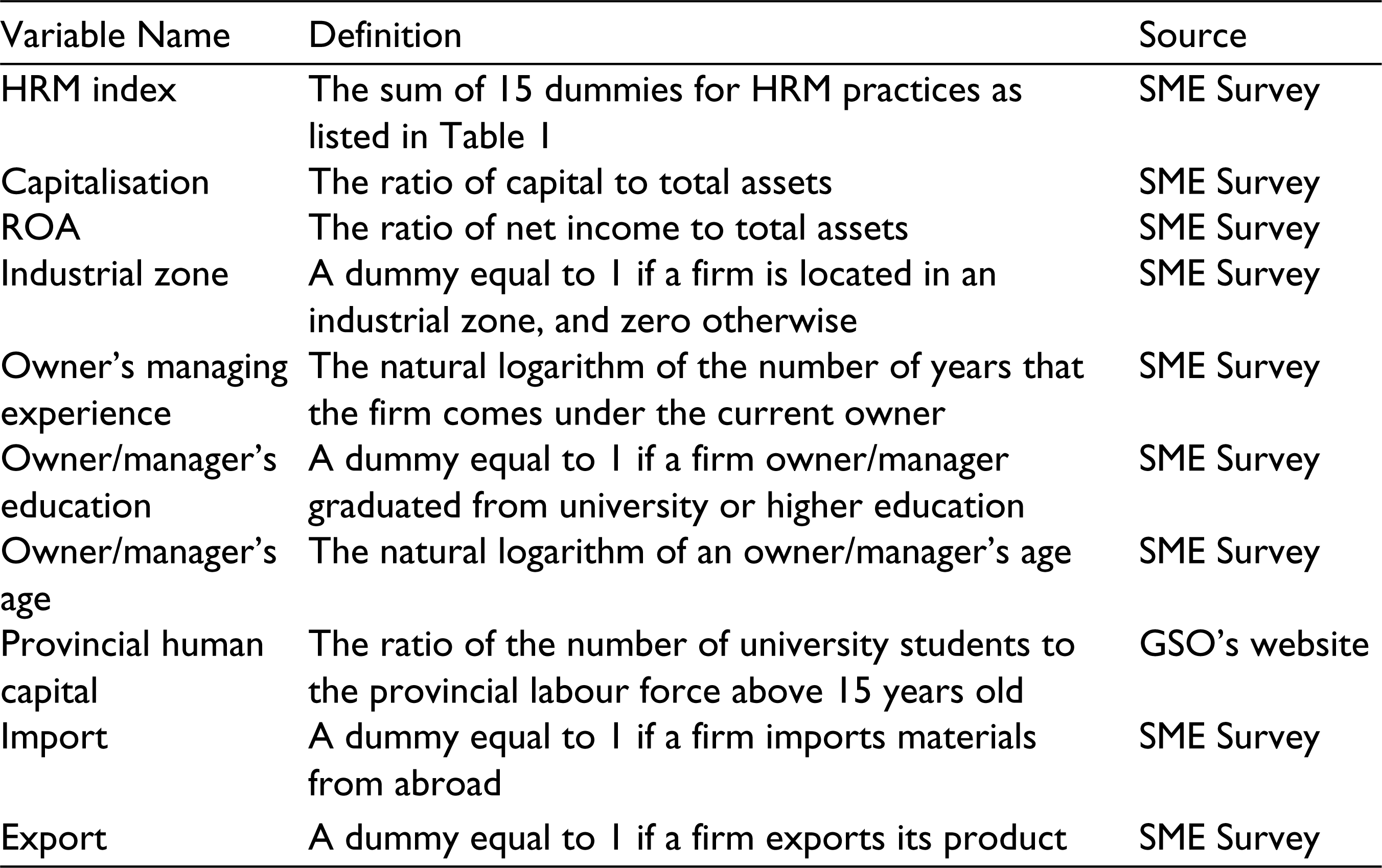

We also incorporate into our model specification several controls variables capturing SMEs characteristics that could possibly affect SMEs innovation. 3 Specifically, we add firm capitalisation, return on assets (ROA) and the specific location of the SMEs as our control variables. We measure firm capitalisation as the ratio of firm total capital to total assets. ROA is measured by firm net income over total assets. We included a dummy variable for those SMEs being located in industrial zones/industrial parks to capture possible effects of agglomeration economies. The SMEs in industrial zones or industrial parks also enjoy better physical infrastructure and more incentives provided by the government (Kikuchi, 2007). In addition, we also controlled owners/managers’ characteristics including owner’s managing experience, owner/manager’s education and age. Variables are defined in Table 2.

Variable Definitions

Summary Statistics

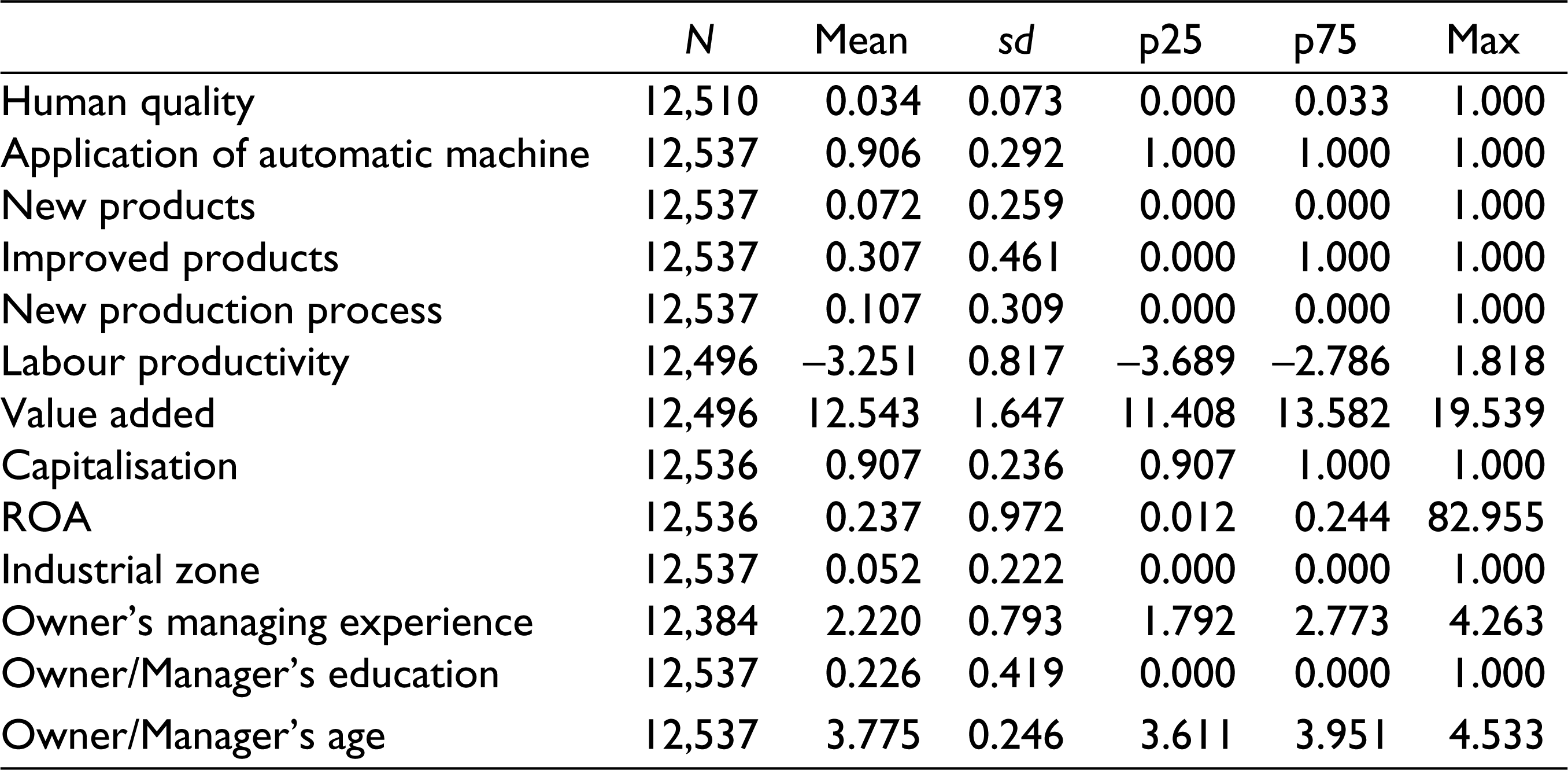

Table 3 presents the summary statistics of the main variables used in our study. The mean values for Human Quality, which is measured by the ratio of workers with university education or higher over the total employees, and Automatic Machine were 3.4% and 90.6% respectively. Regarding innovative activities, on average, there were 7.2% firms releasing new products, 30.7% improving their existing products and 10.7% applying new production process. The average value of labour productivity and value added are 3.3 and 12.5 respectively. Regarding control variables, our sample firms are profitable, reporting the mean ROA of approximately 23.7%. On average, firms’ total capital is 90.7% of total assets. In addition, there were around 5.2% of SMEs located in industrial zone. With respect to owner/manager’s characteristics, the mean values for Owner’s Managing Experience, which is measured as the natural logarithm of the number of years that a firm comes under the current owner, and Owner/Manager’s Age, which is measured as the natural logarithm of the owner/manager’s age, are 2.2 and 3.8 respectively. On average, there were 22.6% of the owners/managers in our sample firms educating from universities or higher education.

Summary Statistics

Model Specifications and Endogeneity Issues

We first argue that any strategy of the SMEs including application of HRM practices should aim to gain higher-quality capital assets to conduct innovation. Thus, to test this hypothesis, we propose the regression specification as follows:

where all variables are with time index to take advantages of the panel data; Resource Quality-it represents either (a) the qualification of workers or (b) the application of automatic machines in production. Xit is a set of control variables reflecting characteristics of SMEs and their owners/managers. In the Human Resource Quality model, we also control for the overall changes in provincial labour market quality by incorporating the ratio of total provincial university students to the provincial labour force above 15 years old (Provincial Human Capital). 4 Variable ai denotes SMEs specific unobserved time-invariant characteristics.

Next, to empirically test the second hypothesis of the impact of HRM practices on innovation, the second regression specification is proposed:

where Innovation-it can be one of three dummies for innovation activities of SMEs including (a) introducing new products, (b) improving existing products and (c) applying a new production process. In addition, we employ the same set of control variables as in Equation (1).

Finally, in order to investigate the effects of HRM practices on firm performance, we used the following regression model:

where Performanceit represents performance indicators of SMEs, which is either logarithm of total value added or logarithm of total value added divided by number of full-time workers. The same set of control variables as in Equation (1) is incorporated. We also used control for some factors that could affect firm performance, namely technological level (Automatic machine), firms’ import activities (Import) and export activities (Export). 5

It is worth noting that HRM Indexit and the three dependent variables Resoure Quality-it, Innovation-it and Performanceit—have potentially simultaneous effects. This is because, as one would expect that HRM practices affect these firms’ aspects, and at the same time, SMEs with more innovation and/or better performance might afford to adopt more HRM practices. Katou (2012) argues that because HRM policies may lead to high organisational performance and high-performing firms may afford HRM policies, the reverse causality between HRM policies and organisational performance should be taken into account. Variable HRM Indexit is, thus, endogenous. Direct estimation by using an OLS model will lead to a biased estimate of the effects of HRM practices on performance of SMEs. Separation of variable ai from the residual helps neutralise possible endogeneity problems to some extent. Therefore, we applied the Fixed Effects estimation method in all the regressions.

Even after removing ai, with the Fixed Effects estimation the relationships between HRM Indexit and Resoure Quality-it, Innovation-it and Performanceit are still potentially simultaneous because HRM practices are affected by other time-varying factors, which are not fully corrected by the Fixed Effects model. To deal with the endogeneity problems we apply the instrumental variable approach using the 2SLS regression model. Application of the 2SLS model amounts to finding of an instrumental variable that affects HRM Indexit but does not affect Resoure Quality-it, Innovation-it and Performanceit directly.

Following the prior literature, we instrument the HRM Indexit of a specific firm in a given year by using the mean value of the HRM score of other firms in the same industry and same province and in a year (i.e., HRM_Indus_Province). The use of the industry-province-year average as the instrumental variable for HRM practice of an SME is based on the ‘Bandwagon effect’, the phenomenon whereby a firm’s HRM practice is affected by the general practices adopted by other firms. The selection of this instrumental variable helps eliminate the biases caused by unobserved factors that are correlated with the HRM practices at the firm level and mitigate the problem of measurement errors which are idiosyncratic to the firm. 6

Results

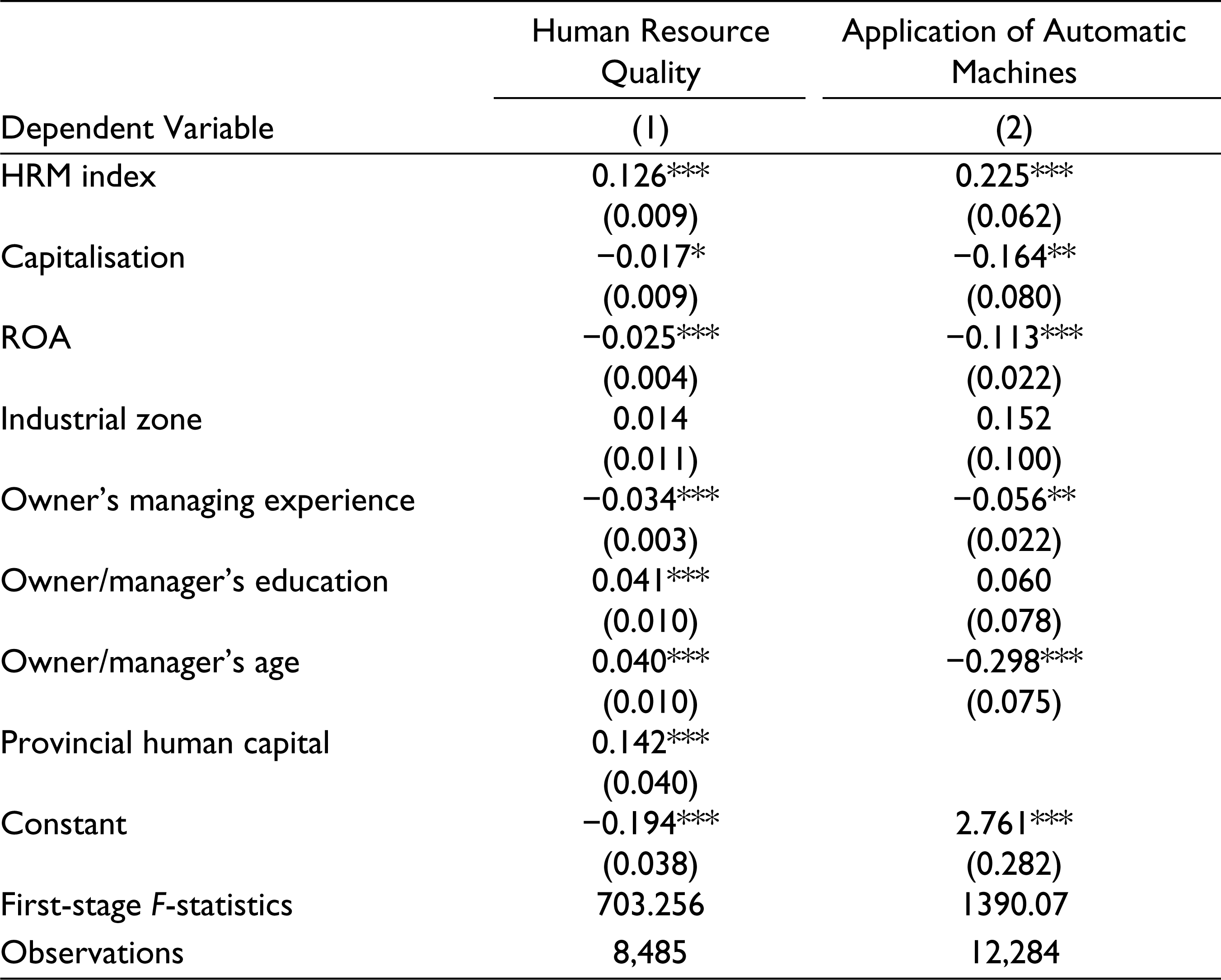

The effects of HRM practices on quality of employed human capital and physical assets are presented in Table 4. The SMEs that adopt more HRM practices, which are essentially providing more rewards and benefits to workers in this study, employ more workers with university degrees and apply more automatic machines in their production. The results show that better management of human resources with a focus on provision of rewards and benefits to workers does not only allow SMEs to be able to recruit and retain high-quality human capital assets but also allow SMEs to employ higher-quality physical capital assets in production. These findings support Hypothesis 1 qualification of workers, which represents human capital and quality of physical capital are complementary to each other and their interaction brings about higher performance. With this finding we may assume that HRM practices indirectly raise performance of the SMEs. Hence, we confirm the link between HRM practices, the strategic processes or the black box, and firm performance as proposed in Messersmith and Guthrie (2010) and Chowhan (2016).

HRM Practices and Qualification of Capital Assets

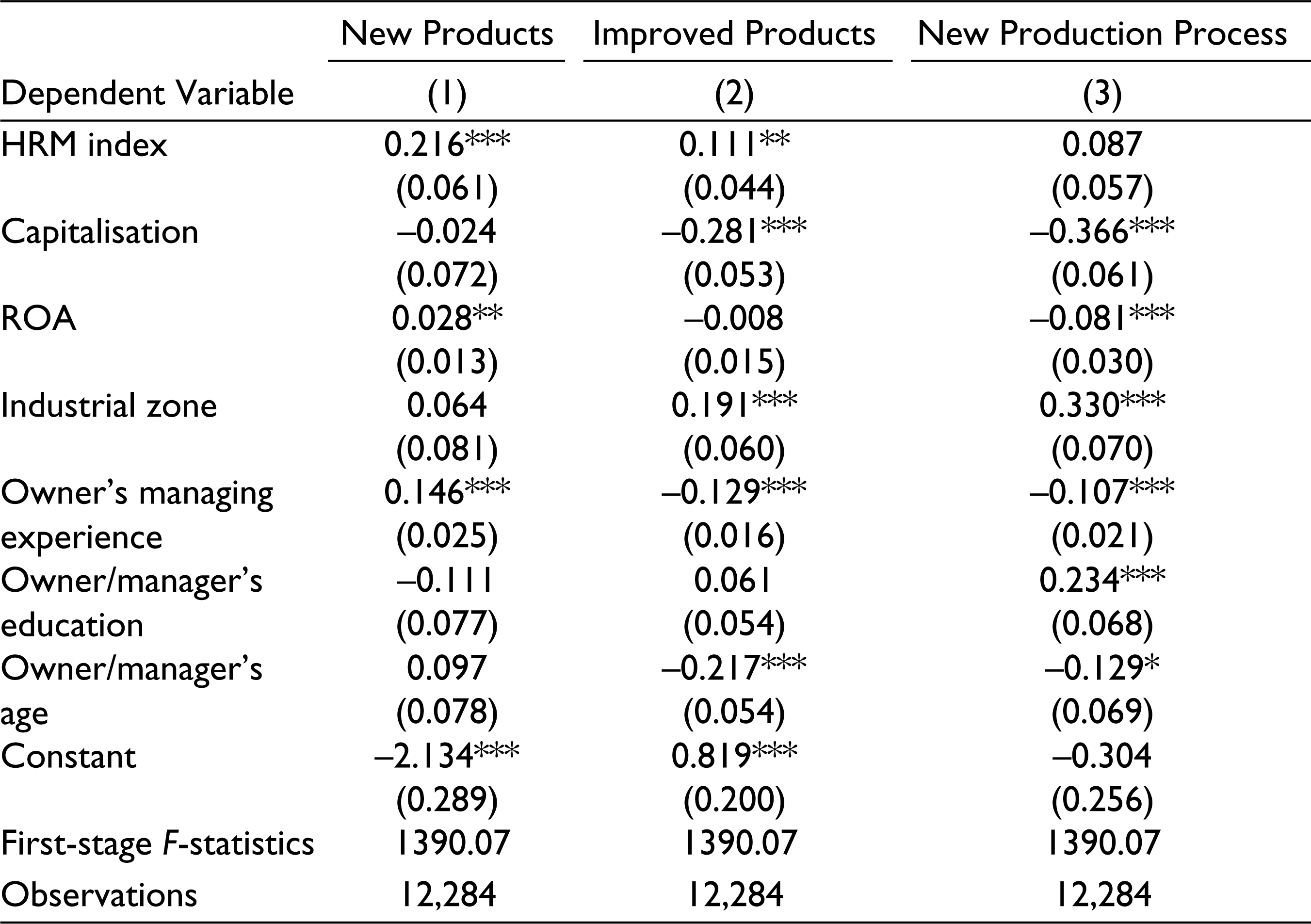

Table 5 presents effects of HRM practices on different categories of innovation of the SMEs. HRM practices have positive and statistically significant effects on the release of new products and the improvement of existing products. These findings support Hypothesis H2. Nevertheless, HRM practices have positive yet statistically insignificant effect on the introduction of new production process. This is consistent with what Messersmith and Guthrie (2010) find. While developing new products is often much more sophisticated for most of SMEs, developing new production processes can be simpler and more affordable by the SMEs. As a result, it is reasonable to conclude that HRM practices, which are largely based on the provision of rewards and benefits to workers of the SMEs in this study and serving as a strategic resource, are prioritised to spend on relatively more sophisticated innovation. This finding contributes to close the gap in literature about the relationship between HRM and entrepreneurship, which has been pointed out by Dabic et al. (2011).

HRM Practices and Multifaceted Innovations

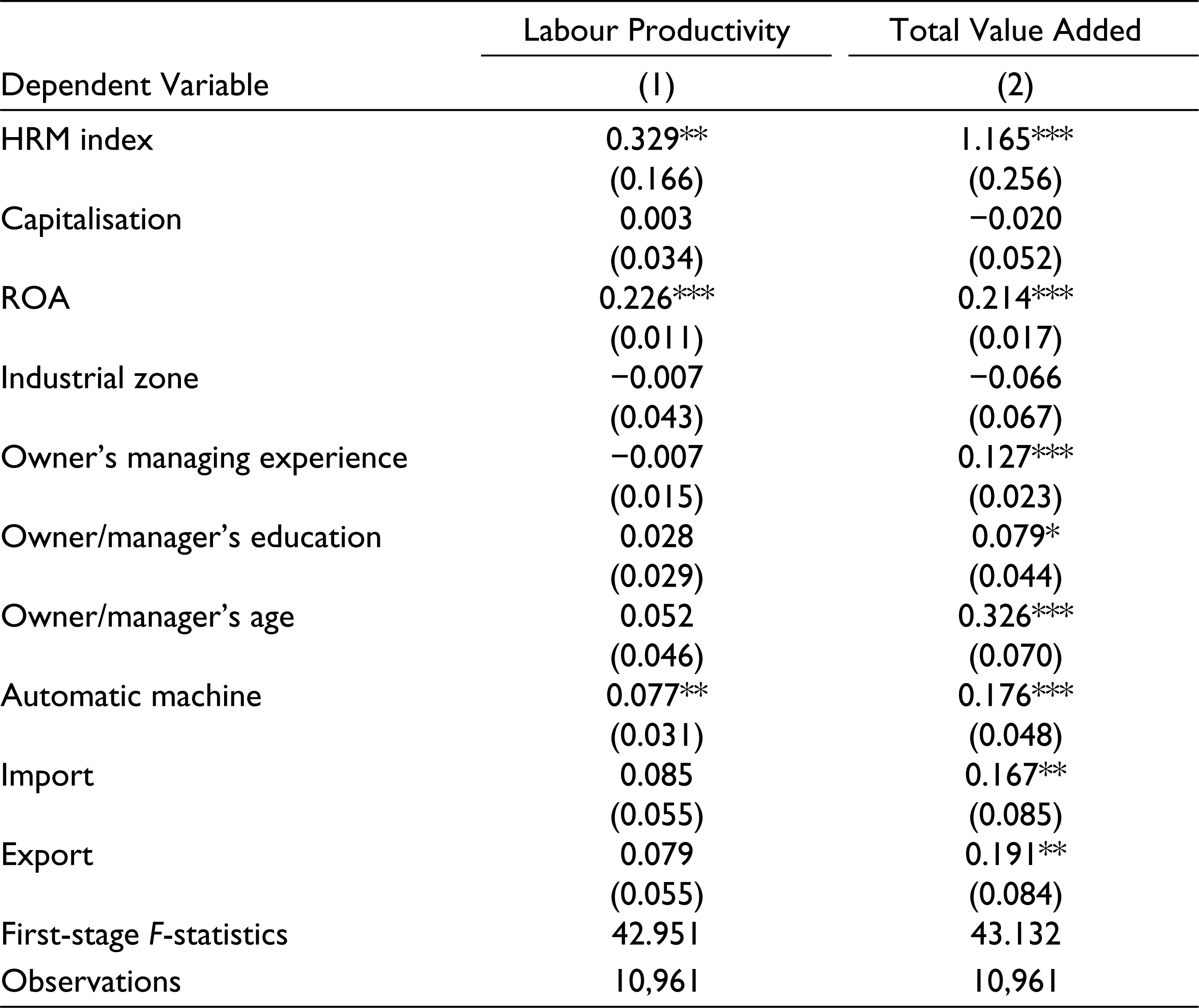

Results of effects of HRM practices on the performance of SMEs are revealed in Table 6. We applied the Fixed Effects panel data model with endogenous explanatory variables and heterogeneity for estimation. HRM practices have positive and significant effects on both total value added and labour productivity of SMEs. These findings support Hypothesis H3, suggesting that the SMEs adopting HRM practices have larger operation size and higher labour productivity. Our findings are not different from previous studies and confirm that adoption of HRM practices is not only important for performance of large enterprises but also essential for development of SMEs in transition economies, where HRM practices are often not extensively applied. In other words, we empirically verified that the mechanism of the black box as specified in Messersmith and Guthrie (2010) and Chowhan (2016) can be applied to small enterprises in transition economies.

HRM Practices and Firm Performance

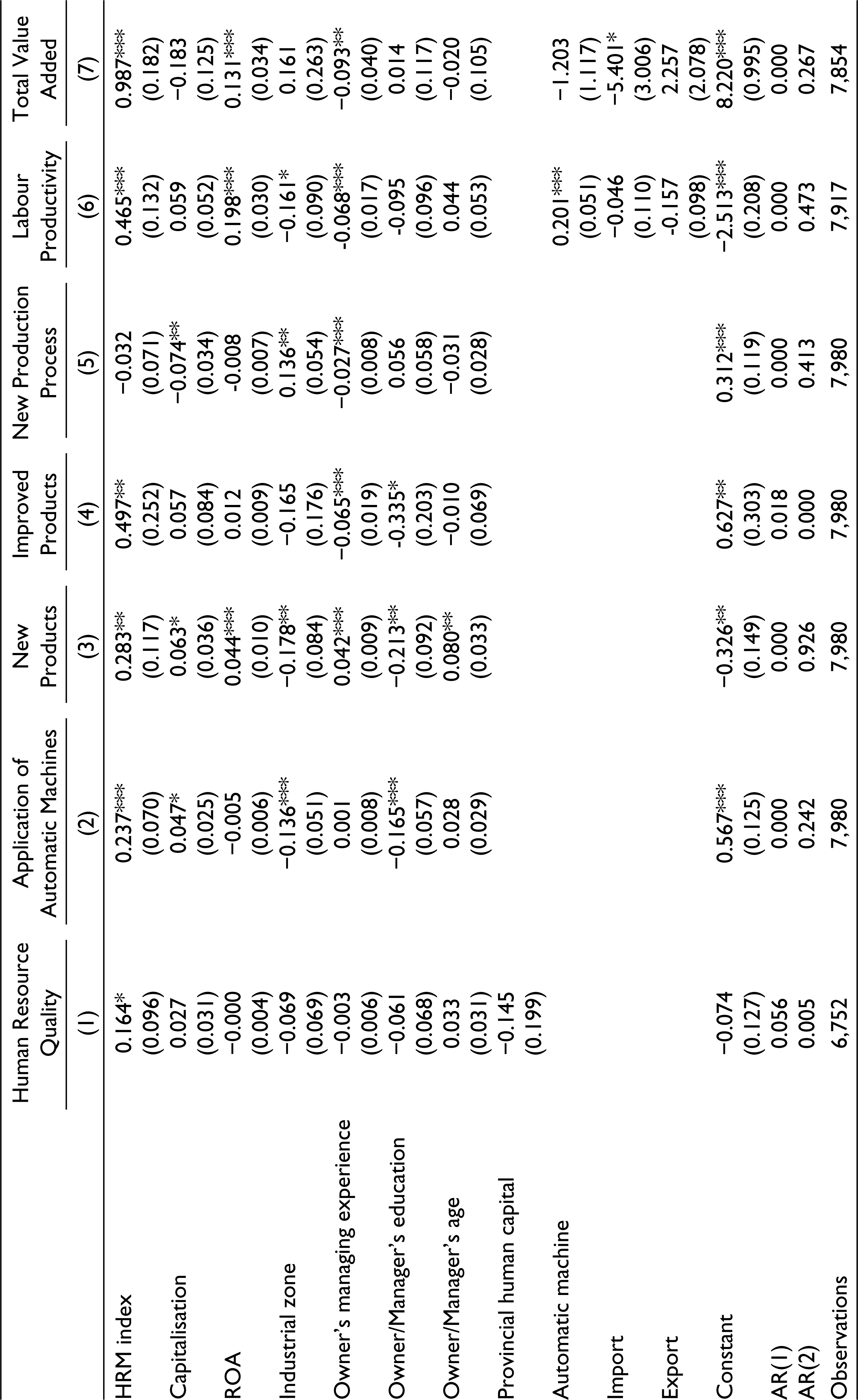

As an another effort to mitigate the endogeneity concern, we estimated the effects of HRM practices on quality of employed human and physical capital assets and on different categories of innovation of the SMEs using the Generalized Methods of Moment panel data model with endogenous explanatory variables and heterogeneity. 7 Results are provided in the Appendix. All estimation results are similar to our results presented in Tables 4–6. Overall, these findings further support our hypotheses. 8

Concluding Remarks

In a transition economy like Vietnam, HRM practices are not frequently adopted by SMEs, which account for a large proportion of number of enterprises. Reasons for this tendency might be that the adoption of HRM practices is costly and/or SMEs are not fully aware of benefits of HRM practices. Findings of this study support our hypotheses and show that after correcting for endogeneity problems by instrumental variables HRM practices, of which the focus is on providing rewards and benefits to workers, are found to determine the quality of employed human and physical capital assets of SMEs. Moreover, the study reveals that HRM practices positively influence some certain categories of innovation of SMEs. The SMEs that adopt more HRM practices are more likely to release new products and improve the existing ones. The study further confirms that HRM practices are an important factor that positively determine the performance of SMEs as measured by the expansion of operation size and enhancement in labour productivity. These findings are in line with previous studies that HRM practices are a strategic resource for sophisticated innovation and development of SMEs in transition economies. It is, therefore, warranted that promotion of adoption of HRM practices among SMEs is essential for enhancing their innovation and development.

This study contributes to literature by closing the gap in understanding effects of HRM practices on entrepreneurship of small enterprises in transition economies, where SMEs have been revitalised during the transition period and started to grow from small household-type businesses. The study also provides an important evidence for policy makers in transition economies to support innovation and development of SMEs by promoting adoption of appropriate HRM practices, which could be first focused on providing rewards and benefits to workers.

Finally, we must mention the several limitations of the study. First, the study has not analysed impacts of HRM practices on the process of innovation or investment in innovation of SMEs as information on investment in such as research and development activities is not available. Our study fails to provide insights into the mechanism through which HRM practices affect introduction of new production process and is not able to show why. Second, we are not able to confirm the whole mechanism as proposed in the black box of Messersmith and Guthrie (2010) and Chowhan (2016) with our current analysis as we lack appropriate instruments to correct for endogeneity problems when we link HRM practices with elements in the black box and performance of enterprises as a whole system. Third, lack of data has prevented us from fully understanding the effects of HRM practices on innovation and performance of the SMEs in Vietnam and, instead, focusing mainly on the effects of provision of rewards and benefits to workers. All of these limitations are caused by the nature of information available in the dataset. We intend to combine this dataset with additional information from surveys or personal interviews we may conduct in the future to deal with these limitations.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

Generalized Method of Moments

| Human Resource Quality |

Application of Automatic Machines |

New Products |

Improved Products |

New Production Process |

Labour Productivity |

Total Value Added |

|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

| HRM index | 0.164* | 0.237*** | 0.283** | 0.497** | −0.032 | 0.465*** | 0.987*** |

| (0.096) | (0.070) | (0.117) | (0.252) | (0.071) | (0.132) | (0.182) | |

| Capitalisation | 0.027 | 0.047* | 0.063* | 0.057 | −0.074** | 0.059 | −0.183 |

| (0.031) | (0.025) | (0.036) | (0.084) | (0.034) | (0.052) | (0.125) | |

| ROA | −0.000 | −0.005 | 0.044*** | 0.012 | -0.008 | 0.198*** | 0.131*** |

| (0.004) | (0.006) | (0.010) | (0.009) | (0.007) | (0.030) | (0.034) | |

| Industrial zone | −0.069 | −0.136*** | −0.178** | −0.165 | 0.136** | −0.161* | 0.161 |

| (0.069) | (0.051) | (0.084) | (0.176) | (0.054) | (0.090) | (0.263) | |

| Owner’s managing experience | −0.003 | 0.001 | 0.042*** | −0.065*** | −0.027*** | -0.068*** | −0.093** |

| (0.006) | (0.008) | (0.009) | (0.019) | (0.008) | (0.017) | (0.040) | |

| Owner/Manager’s education | −0.061 | −0.165*** | −0.213** | -0.335* | 0.056 | -0.095 | 0.014 |

| (0.068) | (0.057) | (0.092) | (0.203) | (0.058) | (0.096) | (0.117) | |

| Owner/Manager’s age | 0.033 | 0.028 | 0.080** | −0.010 | −0.031 | 0.044 | −0.020 |

| (0.031) | (0.029) | (0.033) | (0.069) | (0.028) | (0.053) | (0.105) | |

| Provincial human capital | −0.145 | ||||||

| (0.199) | |||||||

| Automatic machine | 0.201*** | −1.203 | |||||

| (0.051) | (1.117) | ||||||

| Import | −0.046 | −5.401* | |||||

| (0.110) | (3.006) | ||||||

| Export | -0.157 | 2.257 | |||||

| (0.098) | (2.078) | ||||||

| Constant | −0.074 | 0.567*** | −0.326** | 0.627** | 0.312*** | −2.513*** | 8.220*** |

| (0.127) | (0.125) | (0.149) | (0.303) | (0.119) | (0.208) | (0.995) | |

| AR(1) | 0.056 | 0.000 | 0.000 | 0.018 | 0.000 | 0.000 | 0.000 |

| AR(2) | 0.005 | 0.242 | 0.926 | 0.000 | 0.413 | 0.473 | 0.267 |

| Observations | 6,752 | 7,980 | 7,980 | 7,980 | 7,980 | 7,917 | 7,854 |