Abstract

Corporations have conflicts of interest among shareholders, debtholders and directors, and, corporate law gives each party avenues to pursue others, while protecting themselves. While debtholders are exposed to excessive risk-taking by directors and abuse of limited liability by shareholders, they are protected by legal institutions like directors’ liabilities to third parties and piercing of the corporate veil. Shareholders are subject to the risk of veil-piercing and director negligence, but they are protected by derivative suits. And directors, while under threat of liability suits by debtholders and shareholders, are protected by the business judgement rule, liability exemption and liability insurance of directors and officers (D&O). This web of legal institutions comprises a dual structure of economic and psychological factors, built upon economic incentives but also upon such psychological factors as bounded rationality, the chilling effect, the desire for certainty, loss aversion and the sense of fairness. Any change in the balance will affect their behaviour; greater protection of directors, for example, provokes greater risk-taking, both economically and psychologically.

Introduction

The purpose of this article is to analyse conflicts of interest, involving corporations from the dual perspectives of behavioural and economic analysis of law. In particular, the article looks at conflicts of interest among shareholders, debtholders and directors, and, the legal framework under which they hold others liable, while protecting themselves. While we focus on the Japanese legal system for these analyses, our results hold true for other jurisdictions as well, to the extent that we explore common behavioural and economic foundations, in order to understand the legal structure of corporations.

There is an intricate balance between the pursuit of liability and defence against it by means of legal institutions such as laws, case law and doctrines. In the Japanese legal system and all major jurisdictions, shareholders enjoy limited liability while also being exposed to its exception, the legal doctrine of piercing the corporate veil (Bainbridge & Henderson, 2016). Similarly, assuming that corporations have a separation of ownership and control (Berle & Means, 1932), shareholders can turn to derivative suits to hold directors liable. But case law on the business judgement rule protects directors against such claims, and corporate law further permits exemption from liability with certain limitations as well as the use of D&O insurance.

On the one hand, these mutual ‘offensive’ forces seem balanced from an economic perspective, as shown in a classic work by Easterbrook and Fischel (1991), based on an analysis of the economic incentives of each party under the legal structure. On the other hand, by harnessing developments in cognitive science (psychology), we can deepen our understanding of the structure of law from a behavioural (psychological) perspective as well. This approach—looking at the law as a dual structure of economic and behavioural layers—is part of behavioural law and economics research, as represented in leading literature, including Jolls, Sunstein, and Thaler (1998), Korobkin and Ulen (2000), Langevoort (2012), Winter (2018), and Zamir and Teichman (2018). In Japan, prior research from the behavioural-economic perspective includes Tanaka (2018) on hindsight bias in jurisprudence, Asaoka (2018) on boards of directors and Asaoka (2019) on mergers and acquisitions decisions.

A useful approach in economic analysis is to employ options to describe the distribution of wealth and conflicts involving shareholders and debtholders. Under a standard model, a position held by shareholders with limited liability is expressed as a call option, with the firm’s debt value as its exercise price, and one held by debtholders as a combination of a claim to its debt value and a short position in a put option with the same exercise price (Kraakman et al., 2017). Under this model, a traditional economic explanation is that shareholders with a call option have an incentive to take greater risk so as to increase the volatility of firm assets and raise the value of their position, while debtholders have an opposite incentive to decrease volatility so as to raise the value of their own position.

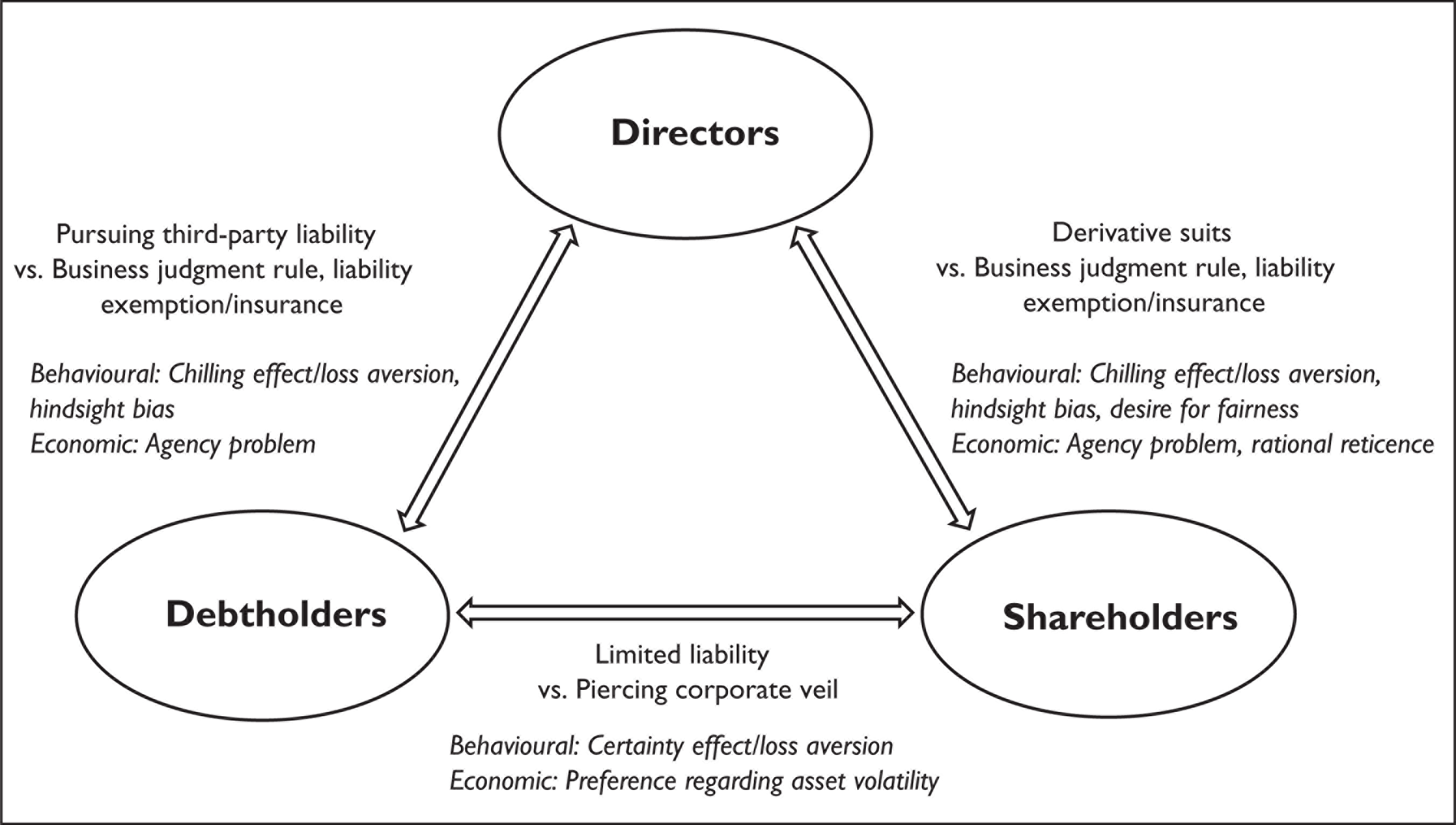

This article is original in adding a psychological layer: by analysing such relationships as dual structures of economic and psychological forces, we add to the interdisciplinary analysis of behavioural law and economics in the field of corporate governance. Decisions are made by humans, and although economic incentives underlie such decisions, as crystallised by Easterbrook and Fischel (1991), they are not the only factors at play. Combining legal and psychological analyses dates as far back as Franks (1930), who looked at psychological effects in jurisprudence, but recent experiments in behavioural economics and psychology enable us to harness both for a more complete understanding of the behavioural-economic structure of corporate law. Figure 1 shows the triangular relationship of conflicts of interest among shareholders, debtholders and directors in a dual layer of behavioural and economic factors, which is analysed in the article.

The article is organised as follows: within the triangular relationship, we first analyse the relationship between shareholders and debtholders in terms of limited liability and piercing of the veil, then the relationship between debtholders and directors in terms of directors’ liability towards third parties and, finally, the remaining side of the triangle, the relationship between directors and shareholders, in terms of derivative suits. We discuss the results of these analyses, relate them to directors’ compensation and conclude the article.

Shareholders and Debtholders

Limited Liability

In corporate financing, debt and equity are used as major instruments: correspondingly, both debtholders and shareholders are involved in a firm’s business activities and risks. A key characteristic of equity is limited liability. Limited liability in its modern form was established in 1811 in New York State, from where it spread throughout the USA, finally reaching California in 1931 (Shiller, 2004). Japan introduced this institutional invention in 1890 in its first modern Commercial Code, drafted by Hermann Roesler, a German legal scholar, at the invitation of the reforming Japanese government. The country then overhauled its corporate law in 1950, modelling it after the US Illinois Business Corporation Act of 1933 (West, 2001).

First introduced as a version of the sovereign immunity of public corporations, limited liability is found in the English East India Company in 1600 (Bainbridge & Henderson, 2016) and the Dutch East India Company in 1602 (Gelderblom, De Jong, & Jonker, 2013). The effects of establishing limited liability as a legal institution were twofold: economically, it gave a call option position to shareholders by limiting losses to the amount invested. Psychologically, it introduced the certainty effect, which causes people to have a strong fear of uncertainty—even when an uncertain situation is unlikely—to the extent that they assign a higher subjective probability to unlikely events than is objectively warranted and value certainty to a disproportionate extent (Tversky & Kahneman, 1981). The limit on losses with certainty was doubly important because of loss aversion, the tendency of people to dislike losses more than they like gains (Kahneman & Tversky, 1984). These tendencies cause people to place excessive value on limited liability, as opposed to rationally comparing the prices of securities having a very small probability of additional loss with those having none.

Further, despite the assumption that people will have the economic rationality to take into account the probability of all possible events, in actual decision-making, we do not dare to calculate all possible risks; rather, we deploy ‘satisficing,’ a cognitive heuristic of searching until an acceptable, even if not optimal, threshold is met (Simon, 1956). Limited liability allowed people to avoid losses under the assurance of corporate law without thoroughly researching the probabilities or fearing liability to creditors, with an expanded pool of risk capital as a result. Hence, in a world with limited time and information, limited liability is recognised as ‘arguably the most important characteristic of the modern corporation’ (Bainbridge & Henderson, 2016), on a par with Watt and Stevenson at the time of the Industrial Revolution (Halpern, Trebilcock, & Turnbull, 1980).

In summary, when seen through an economic lens, limited liability meant that the nature of a call option incentivised shareholders to prefer risk-taking, given that the value of their option position increased along with the volatility of firm assets. Seen through a psychological lens, however, there is another explanation: by removing excessive fear of losses as a low-probability event, the limit on losses gave them the comfort of certainty. This allowed them to satisfice by providing a handy litmus test for decisions—as long as they knew that their investments were in corporations, a format that provides limited liability, they would not lose money beyond the amount they had invested.

Piercing the Corporate Veil

Case law for piercing the corporate veil exists across major jurisdictions (Bainbridge & Henderson, 2016). A representative example is the US case of Walkovszky v. Carlton in 1966, which focused on a parent firm that founded and operated a number of subsidiaries, each of which owned one or two taxis. While denying the parent’s liability beyond its equity investment in each of the subsidiaries in a specific case where one of those subsidiaries injured a pedestrian through negligence, the court showed conditions under which it could pierce the veil and thereby hold shareholders liable beyond their equity investment. In Japan, a similar precedent was established by the Supreme Court 3 years after Carlton (Supreme Court of Japan, 1969).

Piercing of the veil offers an exception to limited liability, with a dual effect: shareholders lose not only economic protection against loss beyond their investment but also the psychological certainty effect and loss aversion that corporate law is meant to provide. Loss of the certainty effect is exacerbated by the ambiguity of its standard. For this reason, some academics argue for abolishing the veil-piercing doctrine altogether (Bainbridge, 2001).

The veil-piercing doctrine removed the limits on shareholder losses. The relationship between debtholders and shareholders was rewound to the years before limited liability existed, when debtholders sought recourse from shareholders’ own assets, even though debtholders did not always seek recourse from shareholders with legally unlimited liability at that time (Shiller, 2004). As long as the court can apply the doctrine, the key property of corporate limited liability vanishes, and so does the property of a call option arising from it, while the value of the position held by debtholders improves with the transfer of wealth from shareholders to debtholders.

Psychologically, the certainty effect for shareholders vanishes as well, despite the rational fact of there being a very low conditional probability of a firm’s going bankrupt, and, further, that its veil will be pierced. Even if its application is limited in practice, the doctrine reverses shareholders’ willingness to invest and deters the development of capital markets, in that investors must take a more careful look at their investees. A behavioural critique against veil piercing points, therefore, not only to its jurisprudential ambiguity but also to the chilling effect of removing certainty and reinstalling the asymmetric bias of loss aversion.

Debtholders and Directors

Directors’ liability to debtholders is stipulated in Japanese law as liability to third parties (§429, the Companies Act), under which debtholders are entitled to claim damages from directors in instances of gross negligence. Typically, the clause is used by commercial banks to recoup losses from loans to closely held firms (Kanda, 2019). Similar laws exist in other jurisdictions. The USA has a standard with the lowest intensity, requiring fraud to hold directors liable (Armour, Hertig, & Kanda, 2017).

The clause is predominantly applied to executive directors; independent directors are only rarely held liable (Fairfax, 2010). The Japanese board of directors is still dominated by insiders working under a system of lifetime employment and internal promotion (Asaoka, 2020). Such insiders make up 70 per cent of the boards (6.4 out of 9.1 directors on average) of listed firms in Section 1 (the largest section) of the Tokyo Stock Exchange (TSE, 2019).

When directors are found liable in court, cash flows out from directors to debtholders in the form of damages. This cash comes from the directors’ personal assets, part of which is their accumulated compensation. There is no prespecified upper limit to the damages to be paid by directors. While director compensation is more or less linked to shareholder value, Japanese directors do not have much upside. This is seen in the comparatively low level of their compensation (about one-tenth that of US, one-fifth of German, and a quarter of UK CEOs) and the high proportion of fixed salaries (42 per cent of total compensation, compared to 10 per cent in the USA, 24 per cent in the UK and 25 per cent in Germany) (Willis Towers Watson, 2019). The combination creates another version of a short-position put option, in that directors face a mix of unlimited loss and limited gain, which restrains their risk-taking incentive and reduces the volatility of firm assets. These restraints lift the value of the position held by debtholders at the same time.

When we analyse the clause from a psychological perspective, we see that it puts a chill on directors, influencing them to place excessive value on certainty when making risk decisions and to place avoidance of losses before pursuit of gains (Kahneman, Knetsch, & Thaler, 1991). Another factor relates to its uncertainty in terms of jurisprudence. While there is a wealth of cases and academic theses to refer to, the ambiguity of the standard for holding directors liable undermines the predictability of the clause (Goto, 2010).

It is arguable that individuals also have limited liability in the form of personal bankruptcy (Easterbrook & Fischel, 1991), but this is different from that enjoyed by shareholders, in that shareholders are able to partition and protect other assets from any loss a corporation might incur (Armour, Hansmann, Kraakman, & Pargendler, 2017). Moreover, unlike investors in diversified portfolios, individuals typically concentrate their human resources on one company through an employment relationship. When debtholders sue directors, cash flow from their employment may well be at risk. Reflecting this difference, one of the notable effects of a firm’s bankruptcy is the effect on its employees, who concentrate their human resources on the firm. The psychology of loss aversion by directors is, then, twofold: the fear of recourse to their personal assets and the fear that they may lose their claim to future cash flow. Therefore, despite there being a presumed limited liability for personal bankruptcy at the individual level, this does not alleviate the chilling effect on directors as it does for shareholders.

Countering these chilling psychological effects, there are legal institutions available to protect directors from the claims of debtholders. These include the business judgement rule and liability insurance. They are analysed in the next section as they have aspects in common with avenues taken by directors to protect themselves against shareholders.

Directors and Shareholders

Derivative Suits

With the expansion of a pool of shareholders as sources of capital, there is an inevitable separation of ownership and control, and, consequently, conflicts of interest between shareholders and directors. Here, we have the agency problem formulated by Jensen and Meckling (1976). To protect shareholders from this problem, the derivative suits clause (§847) enables them to recover lost profits indirectly by holding directors liable not to shareholders, but to firms. Shareholders cannot receive damages directly from directors. But as they are residual claimants to firms’ assets, the value of their position indirectly improves as damages increase the value of corporate assets.

While board directors have a duty to mutually monitor (Kanda, 2019), the psychological foundation for the right of shareholders to file derivative suits lies in its protection against self-serving bias on the part of directors, as people are known to make self-serving decisions even when aware of the existence of this bias (Babcock & Loewenstein, 1997; Valdesolo & DeSteno, 2007). Moreover, people adjust their fairness criteria to accord with their own position, regarding criteria favourable to themselves as fair (Thompson & Loewenstein, 1992). To deal with directors’ reluctance to hold their colleague directors liable, the law enables shareholders to sue directors by paying a court fee of just ¥13,000 (around US$120), regardless of the amount of damages sought.

The fact that shareholders are entitled to protect their stakes by suing directors alleviates the agency problem and gives shareholders an economic incentive to supply capital. However, unlike debtholders’ pursuit of directors’ liability, derivative suits have an inherent problem of rational reticence under dispersed share ownership (Enrique & Romano, 2019). When two types of shareholders coexist—those making efforts to recover their investment and those remaining reticent—the latter have a free ride on the efforts of the former, enjoying a proportionate gain of the total increase in shareholder value produced by damages paid by directors when the former win, less the litigation costs for which winning shareholders are compensated by the firm, while losing nothing when the former lose. By contrast, only the former shareholders are required to pay litigation costs when they lose, and they are even held liable for damages if the firm proves wilful misconduct (§852). This asymmetry reduces the incentive of shareholders to sue directors because of an unfavourable calculus in which they, and only they, must pay the costs and take the risks, albeit sharing in the gains only proportionately.

Psychologically, the rational reticence problem can be explained by a human desire for fairness. People put more emphasis on a fair distribution of wealth than predicted by a rational value maximisation standard (Guth, Schmittberger, & Schwarze, 1982). Even if we know we can enjoy a net increase in wealth by accepting a distribution of divided money among parties, we choose to receive nothing rather than accept less than what we believe is fair. Derivative suits are sensitive to this psychological effect as well, in that shareholders will choose not to take any action, even if their proportionate net gains are positive, when they perceive that other reticent shareholders will receive an unfair share of distribution in light of costs and risks.

The Business Judgement Rule

When directors are aware that they can be held liable through derivative suits, they have an incentive to reduce risk-taking. Were their losses limited, like those of shareholders, directors would have an incentive to take more risks. But since they do not have such protection, except for personal bankruptcy, they do what they can to avoid it. We see a trade-off: the law tries to restrain directors from gross negligence, but it restrains them from taking desirable actions at the same time (a type I error); the law tries to promote desirable risk-taking, but it induces reckless risk-taking as well (a type II error). The chilling effect on directors means less volatility for firm assets, which translates into less value for shareholders, but more for debtholders.

The business judgement rule, by which courts defer to directors’ decisions unless the contents and processes of their decisions are materially unreasonable, works as a counterbalance in saving directors from the chilling effect and loss aversion. It was adopted by the Japanese Supreme Court in 2010 (Supreme Court of Japan, 2010), following an earlier precedent in the USA (Dodge v. Ford Motor Co.) in 1919. This rule also has a psychological foundation. A representative example is hindsight bias (Stallard & Worthington, 1998), the tendency to believe that an event that has already occurred was likelier to occur than it actually was and to underestimate the likelihood that other events would occur. This happens because events that did not occur are unobservable and hypothetical after the fact (Teichman, 2014). This bias can hold directors unjustly liable for not taking appropriate measures to avoid a ‘predictable’ loss, essentially judging them strictly by the results of their decisions rather than by their behaviour in complex, changing environments. The business judgement rule protects directors from such a bias by giving them the comfort and latitude of the discretion to take risk. It thereby protects the value of the shareholder position, which benefits from directors taking risk rather than avoiding it.

Exemption of Liability

In corporate law, the clause on derivative suits is a mandatory one, which cannot be removed per se by contractual agreements between firms and shareholders. Corporate law does stipulate some exemptions from liability, however. Directors without gross negligence can be exempted entirely from liability by an unanimous vote of shareholders (§424) and partially by a majority vote of shareholders (§425), giving them exemption from liability for the amount exceeding the minimum liability stipulated (ranging from two to six times their annual compensation, depending on their executive authority). When so stipulated in articles of incorporation based on the approval of two-thirds of shareholders (§426), the vote by shareholders can be replaced with a majority vote of the board of directors. Further, a liability-exemption contract is allowed for non-executive directors, but not for executive directors, with a majority vote of shareholders ex ante (§427).

For executive directors, avenues for exemption are available only ex post and carry uncertainty. Based on the principle of freedom of contract, directors and shareholders may reach a better welfare-increasing agreement when allowed to negotiate a contract exempting directors from liability. From the economic perspective, this apparent inflexibility can be explained by transaction costs. If the law gave firms full flexibility in designing their governance structure, shareholders in the capital markets would need to understand each firm’s articles of incorporation and other contractual arrangements before trading in securities, thus increasing overall transaction costs on the market. The standardisation of corporate formats by a mandatory law saves costs by making it unnecessary for each investor to examine relevant articles of incorporation available on the market (Easterbrook & Fischel, 1991).

From the psychological perspective, people do not actually research and judge all the options available as described, preferring to satisfice. Satisficing is only made possible by standardisation and the prohibition of deviating from it. Moreover, the mandatory clause on limitations on exemption works to let investors avoid loss, something which is more in line with their loss aversion tendencies. Given this preference, a certain limitation on the level of directors’ exemption, at their expense, has the merit of attracting a wide pool of investors who are unwilling to check all the information available or negotiate terms.

Insurance

Despite the premise of the mandatory clause vis-à-vis shareholders, directors are broadly allowed to contract for D&O insurance, which compensates them for the damages they pay and neutralises their economic losses. In functional terms, this is an example of relaxing a mandatory clause in corporate law, which can be seen as a bundle of off-the-rack contracts available to parties, by a parallel contractual arrangement. There are often cases in which mandatory clauses of corporate law are functionally overridden by contractual arrangements (Kanda, 2019). Amendments to corporate law in 2019 accommodated such insurance practices for the first time and clarified that firms could pay a premium for such an insurance (§430-3). The amendments also provided for indemnification of directors by a majority vote of the board of directors (§430-2), by which firms would compensate directors for damages. The protection thus provided is narrower, however, than that afforded by insurance, in that indemnification requires that directors be without gross negligence. Firms are likely to buy insurance in any case, given the strict processes and limited scope of exemption and indemnification.

It seems inconsistent that ex ante exemptions are allowed as contracts with insurance companies, but not with shareholders. If directors were exempt with full flexibility on contracting, directors and shareholders would achieve fair pricing by agreeing to a relatively high premium to cover the risk of having directors’ decisions exempt from liability ex ante. By contrast, if directors were not exempt under the statutory limitation, shareholders would demand a relatively low premium for relatively low risk. Under the principle of a free contract, both of these combinations would be possible for both directors and shareholders. However, when presented with a combination of limited freedom of contract under corporate law and insurance outside of it, risk-averse directors choose to buy insurance and increase risk accordingly. This causes shareholders to require a higher premium. Alternatively, if directors believe shareholders will require a higher premium in the expectation that directors will buy available insurance and assume greater risk, directors will actually buy insurance to adapt to such expectations, creating a cycle of expectation and realisation.

In this combination of arrangements, insurance companies essentially monopolise exposure to directors’ risk and its premium, the price of risk transferred from directors to insurance companies. Shareholders are excluded from risk opportunity and access to information disclosed to insurance companies, even while it would be desirable for them to have a larger array of investments and to choose the level of risk they wish to incur. Shareholders who are actually willing to tolerate directors’ risk under exemption are worse off under the limitation by an amount equivalent to the premium they essentially pay to the firms’ insurance companies, such payments being unnecessary under a free contract.

One reason for allowing this monopolisation relates to the problem of rational reticence. When firms are owned by dispersed shareholders, monitoring by shareholders becomes inadequate due to both rational reticence and the psychological desire for fairness. But when insurance is introduced, shareholders expect monitoring to be performed by the insurers (Baker & Griffith, 2010). Insurance companies then become a component of corporate governance, assessing corporate information as a financial intermediary in the place of dispersed shareholders. From this perspective, Baker and Griffith’s argument that firms must disclose the main terms of contracts, including the premiums they pay, is supported not only by the general requirement for transparency in corporate governance but also by a monopoly essentially sanctioned by law. In return, the problems of rational reticence and desire for fairness, practically unsolvable through derivative suits, now have a solution to the extent that insurance firms are effective in their monitoring. As a result of this concentration of functions, the insurance companies now benefit from the law of large numbers. Typically, they also set deductibles in their contracts to deal with the moral hazards of insured directors. As long as both monitoring and deduction are effective, the level of risk involved in directors’ decisions falls somewhere between that which exists when full exemption is allowed and when none is allowed.

Discussion

Balancing Conflicts and Protections

The previous three sections analysed the relationships among shareholders, debtholders and directors in a two-layered behavioural and economic structure. Starting with limited liability, we first analysed the conflicts between debtholders and shareholders and their psychological effects. The option positions of shareholders and debtholders lead shareholders to prefer more risk-taking and debtholders to prefer less. By contrast, it was shown that the veil-piercing doctrine, which overrides limited liability while having somewhat uncertain standards, removes the psychological certainty effect and brings back the loss aversion bias alleviated under limited liability.

We also saw that the basic economic incentives of these investors and directors are affected by debtholder-protecting clauses and doctrines in corporate law, such as directors’ liability for third parties and piercing of the veil, and those which protect shareholders, like derivative suits. The effect of the clause on derivative suits can be restrained, however, by rational reticence and the psychological desire for fairness among shareholders. The clause’s mandatory nature entitles shareholders to hold directors liable. Directors who can be held liable by shareholders have unlimited liability ex ante, except for personal bankruptcy, while their compensation is limited; this leads them to choose less risk, increasing the tendency to avoid the pain of losses rather than seek the pleasure of gains. This chilling effect gives debtholders a stronger position overall and offsets the increase in value given by the derivative suit clause to the shareholders’ position.

The relative effect on the value of the positions held by debtholders and shareholders depends on the relative strength of the protection they are given. While shareholders in Japan are dispersed to a comparable extent to those in the USA and the UK (Aminadav & Papaioannou, 2020), debtholders are typically commercial banks with concentrated exposure to firms. This means debtholders are less hindered by rational reticence and better positioned to capture gains by their actions, even if only proportionately. Moreover, debtholders are entitled to recoup their investments directly through the clause on directors’ liability to third parties, although requisites are different, in that debtholders need to prove that directors have committed gross negligence, while shareholders need only to prove their breach of duty. Taken as a whole, these differences in incentives and degrees of concentration make debtholders better positioned than shareholders to recover their investments.

Further, Kinoshita (2016) argues that Japan provides debtholders with stronger protections than shareholders because debtholders, typically commercial banks, provide capital that is by nature equity capital in the form of debt capital. Banks will often waive their debt stakes and relax the terms of repayment for distressed firms, even before losses are felt by shareholders. They also hold shares of their borrowers, although such holdings have been unwound over the years. In such an environment, the seemingly stronger protection for debtholders, as seen in the clauses entitling them to directly hold directors liable and recover their investment, is, in effect, the protection of de facto shareholders in the name of debtholder protection. Corporate law is notably lacking in clauses enabling directors or shareholders to hold debtholders liable.

The chilling effect on directors produced by such strong debtholder protection lowers the value of the position held by shareholders. The business judgement rule—the legal doctrine protecting directors—alleviates this effect and thereby protects shareholders, who are better off when directors take more risk rather than less. Shareholder value is further improved by the availability of insurance through contractual agreement, which functionally overrides the mandatory nature of director liability. Although cash flows out in the form of premiums to insurance companies —essentially monopolising opportunities for risk investment—bounded rationality and the preference for a standardised format for decisions provides insurance with a raison d’être, along with the governance role that insurance firms then undertake on behalf of dispersed shareholders. Rational reticence and the psychological desire for fairness, which restrain the willingness of shareholders to file derivative suits, are alleviated to the extent that governance by insurance companies functions effectively.

These relationships reveal the economic and psychological factors that underlie corporate law clauses and doctrines on conflicts of interest among shareholders, debtholders and directors. Between shareholders and debtholders lies the economic contrast of a call option and a put option, as well as the psychological contrast of certainty and uncertainty regarding limited liability and the piercing of the veil. Both of these affect decisions on risk-taking and avoidance. Similarly, based on the economic foundation of the agency problem and the psychological foundation of hindsight bias, debtholders and directors deal with the contrast of liability to third parties and the business judgement rule, and directors and shareholders with the contrast of the business judgment rule and derivative suits.

We further found that the clauses on limitations on exemption and allowance of insurance for directors have an economic foundation, in that the standardised corporate format allows the saving of transaction costs for participants in the capital markets, and that concentrating governance functions in insurance companies acting as financial intermediaries addresses the problem of rational reticence among dispersed shareholders. There is a psychological foundation as well, as bounded rationality necessitates the standardised format for ease of information processing, while concentration alleviates the problem of the psychological desire for fairness among dispersed shareholders transcending an economic calculus. Corporate conflicts of interest among these groups are based on a triangular balance of psychological as well as economic factors.

Compensation of Directors

A key factor in such a dual structure is the effect on directors’ behaviour, which is influenced by the relative degree of protection for themselves and investors. If it is desirable to stimulate directors into taking risks rather than seeking a ‘quiet life’ (Bertrand & Mullainathan, 2003)—a plausible tendency, given the stagnant ‘lost decades’ experienced by the Japanese stock market not so long ago—it is also desirable, from a policy perspective, to tip the balance into alleviating the chilling effect by strengthening director protection through improved predictability of the legal doctrines of veil piercing and the business judgement rule, as well as the sanctioning of insurance. This is particularly effective when a root cause of the chilling effect is the response of directors to the comparative ease with which shareholders can initiate derivative suits.

This dual perspective allows us to shed a more layered light on the effects of compensation and director liability. In terms of compensation design, directors seem to have a long call option position, in that their compensation is more or less linked to shareholder value by such means as performance bonuses and stock options, where compensation cannot be negative. However, the possibility of liability and damages introduces a negative compensation, one which is unlimited, except when filing for personal bankruptcy. Therefore, the combination of compensation and liability gives directors a short position of a put option, similar to the position of debtholders. The sanctioning of insurance contracts neutralises the downside of the position, however, creating an intended long call position. This should incentivise directors to take more risk, which was the goal of the Japanese government in refining the design of directors’ compensation to stimulate the growth of Japanese firms (METI, 2019).

It is notable, however, that there also exists a form of psychological pain suffered by directors hit with lawsuits and negative media coverage, particularly in a social context where lawsuits are rare and may be socially shaming. There is no insurance against the psychological pain felt by directors under these conditions. If people were to put more emphasis on psychological effects than on pecuniary compensation—which is plausible, given the relatively low level of pecuniary compensation accepted by Japanese executives compared to those in other advanced economies—the alleviating effect of insurance on the chilling effect could be limited.

Furthermore, psychological research offers ambiguous, or even contradictory, results on the effects of pecuniary compensation on performance, particularly in regard to complex tasks where non-pecuniary compensation matters more (Ariely, Gneezy, Loewenstein, & Mazar, 2009; Thibault-Landry, Schweyer, & Whillans, 2017). If that holds true for directors’ decisions, presumably among the most complex tasks in modern society, directors may as well prioritise avoiding social criticism over pursuing pecuniary gains, despite an incentive design that encourages them to pursue shareholder value. For directors whose human resources operate under lifetime employment in an illiquid labour market, stable employment becomes a major interest. The existence of these psychological elements suggests that raising pecuniary compensation will have only a limited effect. In a similar vein, directors may pay more attention to whether their decisions are socially acceptable than to creating shareholder value, in which case protection by insurance gives them little, if not no, comfort in terms of stimulating their risk-taking decisions. Rather, it is arguable that the design of non-pecuniary, or psychological, compensation linked to risk-taking, including reputation, praise, social recognition, responsibility and status inside and outside firms, is as important as pecuniary compensation linked to shareholder value.

Conclusion

In this article, we analysed the relationship among shareholders, debtholders and directors of corporations from the viewpoint of the behavioural-economic analysis of law. In particular, the article looked at the dual structure of economic incentives and psychological effects in mutual relationships, involving the pursuit of liability and protection against it. The existence of clauses and doctrines in corporate law, and the uncertainties in their application, affects human psychology and behaviour.

Compared to traditional economic analysis, the behavioural analysis of law is helpful in understanding actual human behaviour, so essential to law and judicial judgement, as seen in bounded rationality, limitations on the processing of information, satisficing, the preference for certainty, loss aversion, the chilling effect, emphasis on fairness transcending economic rationality and responses to pecuniary and non-pecuniary rewards. In particular, the behavioural framework works to fill the gap between legal and economic analyses mediated by the observation of actual human behaviours. This article examined clauses and doctrines in corporate law and, in parallel, analysed the psychological elements underlying them, in an effort to achieve a layered analysis of conflicts of interest among shareholders, debtholders and directors. This type of analysis helps us more deeply understand the reasons why a legal clause or doctrine exists, from psychological as well as economic viewpoints. By examining each of the elements operating in an intricate balance, it gives us insights as well into how we can create the conditions for change, such as the policy approach of encouraging risk-taking by directors who might otherwise be seeking a quiet life and avoiding psychological or social pain rather than pursuing economic gain.

It is humans who structure corporate law; humans who make judgements while dealing with uncertainty and conflicts of interest. A deeper understanding of human beings leads us to deeper insights into legal institutions and their validity. The structure of conflicts and protection of shareholders, debtholders and directors are better understood by looking at its psychological as well as its economic foundations, particularly in terms of the complex balance maintained between each factor.

The limitations of this article and its future agenda are multifaceted. First, the article dealt mainly with executive directors. But boards are expected to include greater numbers of independent outside directors in the coming years, owing to important changes in the Japanese corporate governance architecture, following the introduction in 2015 of a corporate governance code requiring listed firms to place two such directors on the board on a comply-or-explain basis, and an amendment to the corporate law in 2019 that made it mandatory to have one such director on the board. As the roles of independent outside directors evolve, and boards become combinations of inside and outside directors rather than traditional ones dominated by insiders promoted under lifetime employment, analysing the inner workings of boards will become ever more important. In terms of liability and compensation, outside directors, while rarely held legally liable and receiving only modest compensation, place substantial importance on maintaining reputation, creating a significant difference in incentives and psychology between the two types of directors.

Second, while the behavioural-economic analysis of law is based on psychological research on human behaviour, such research on the Japanese is fledgling. The willingness of people to take risk is influenced in Japan by the society’s persistent idea of failure as social shame, along with its low opinion of the parvenu. Lack of entrepreneurship is another widely recognised feature of the country’s aging society. This suggests that there is room to analyse the psychology and social contexts that define people’s behaviours in a country-specific manner. While it is our general tendency to avoid loss and uncertainty, for example, more granular empirical research will provide a wider understanding of the law and corporate behaviours in comparative terms and shape the framework of the behavioural-economic analysis of law. Advances in behavioural-economic research suggest these interesting future agendas and promise a deeper understanding of the structure of corporate law and governance.

Footnotes

The author declared the following potential conflicts of interest with respect to the research, authorship and/or publication of this article: The author declares that there is no conflict of interest.

Funding

The author disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by JSPS KAKENHI [grant number JP19K13811].