Abstract

The world is facing an unprecedented health crisis—the COVID-19 pandemic—which has caused global economic disruptions, affecting almost all economic activities across countries. To curb the spread of the virus, containment measures such as lockdown, social distancing and quarantine were adopted in almost all countries, which resulted in the shutting down of the majority of the economic activities and locking people in their homes, at least in its initial phases (Lonergan & Chalmers, 2020). Curtailed mobility led to a decrease in the labour supply, closure of workplaces and disruption in supply chains globally (Ernst & Young, 2020). Fear of contagion, uncertainty about economic revival and fear of wage cuts or job loss compelled people to spend less. Consequently, the demand in the economy declined. Therefore, the spread of COVID-19 and policy measures to contain its spread have caused both supply and demand shocks to the economies across the world (Bekaert et al., 2020; del Rio-Chanona et al., 2020; El-Erian, 2020; Guerrieri et al., 2020).

Like other countries, India also imposed a nationwide lockdown for 21 days—from 25 March 2020 till 14 April 2020—to minimize the spread of COVID-19, with relaxation in a few economic activities pertaining to essential commodities and services. People were confined within their homes because of the restrictions on movement. All transport services were suspended, excluding transportation of essential goods, fire and emergency services, and police and civil defence. It resulted in the closure of nearly all factories and services, which severely affected the economic activities in the country. It also led to the shutting down of the majority of the economic activities (both production and distribution), causing disruptions in supply chains in the economy. It severely affected firms, particularly small enterprises, and millions of people. Although the pandemic has affected all firms irrespective of their size, the micro, small and medium enterprises (MSMEs) are more vulnerable to such hazards, given the lack of financial and human resources in comparison to large firms (Bartik et al., 2020; Prasad et al., 2015; Shafi et al., 2020). The closure of business activities forced millions of migrant workers, primarily working in the informal sector, to return to their villages (Srivastava, 2020).

The lockdown was continued in a phased manner until 31 May 2020. However, conditional relaxations were given in areas where the spread had been contained or reduced. From 1 June 2020, the government began unlocking in a phased manner with lockdown restrictions limited to containment zones. To support all segments of the economy (individuals and enterprises) amid the lockdown during the pandemic, the government introduced stimulus packages under Prime Minister Garib Kalyan Yojana (PMGKY; announced on 26 March 2020) and Atmanirbhar Bharat (announced on 12 May 2020). Furthermore, the Reserve Bank of India (RBI) also announced several measures to pull the economy out of the slump. Given the limited financial resources, MSMEs are at a high risk of closure or becoming stressed by the measures introduced to curb the spread of COVID-19.

Small businesses, particularly in the informal sector, have been heavily affected. According to a survey conducted by Endurance International Group (EIG), many MSMEs shut their businesses due to the lockdown. Many believe that it may take up to 6 months to return to regular business (EIG, 2020). Apart from playing a pivotal role in the supply chains in the economy, MSMEs employ millions of people and contribute significantly to the generation of domestic demand. MSMEs are critical for sustaining a functioning economy and assuring the delivery of goods during and after public health emergencies (Burton et al., 2011; McCall, 2020). Since MSMEs contribute significantly to the supply chains and demand generation in the economy, there is a need to understand the impact of COVID-19 on MSMEs in India and the implications of policy initiatives.

ECONOMIC DISRUPTIONS CAUSED BY COVID-19

Previous experiences with similar diseases indicate that preventive measures such as lockdown, social distancing and quarantine to curb their spread have created significant economic costs (Brahmbhatt & Dutta, 2008). COVID-19 is not different. Economies around the world also suffered due to the spillover effects of the disruption in Chinese production and supply chains caused by the outbreak of COVID-19 in China. However, it has created demand–supply shocks in almost every segment of the economy (Bekaert et al., 2020; del Rio-Chanona et al., 2020; El-Erian, 2020; Guerrieri et al., 2020). The most-affected sectors include travel and tourism, hospitality, entertainment and financial industry (Han et al., 2020; Kaushal & Srivastava, 2021).

The World Economic Outlook, June 2020, indicate contraction in the world economy by –4.9% in 2020 (IMF, 2020). Decline in projection of annual change in real GDP of advanced economies is –8.0% which is much higher than that of emerging markets and developing economies (i.e., –3.0%). In comparison to China, impact of the COVID-19 on the Indian economy is much severe. The projected growth in real GDP of Indian economy for the year 2020 is –4.5%, while that of the Chinese economy is 1.0%. According to an estimate of Asian Development Bank (ADB), the loss to the global economy due to the COVID-19 would be $2.0 trillion to $4.1 trillion (ADB, 2020) which would have significant impact on decline in employment and labour income. A World Bank study using computable general equilibrium (CGE) modelling shows that COVID-19 will cause significant reduction in GDP across countries, increase in trade costs, decline in trade, increase in inflation and reduction in employment and supply of capital (Maliszewska et al., 2020). The projected contraction in world trade volume (goods and services) in 2020 is –11.9% (IMF, 2021). Therefore, it can be understood that COVID-19 has a severe impact on global GDP, trade flow and foreign direct investment, which may significantly affect other development indicators (e.g., poverty, inequality, etc.) across countries.

Indian economy is well connected with other economies through trade and movement of human resources. The spillover effects of economic disruptions generated in China due to the spread of COVID-19 have severely affected the Indian economy. The United Nations Conference on Trade and Development (UNCTAD) estimated about $350 million in trade impact for the Indian economy, which is among the 20 most-affected economies in the world due to the slowdown in China’s economy caused by COVID-19 (UNCTAD, 2020). The sectors most affected due to China’s economic slowdown include chemicals (37.28%), textiles and apparel (18.50%), automotive (9.83%), metal and metal products (7.80%) and machinery (6.94%). Since these sectors have significant inter-sectoral linkages with other sectors in the economy, it is obvious that output and domestic supply would be severely affected which would further bring a sharp decline in employment opportunities in the country, at least in the short run.

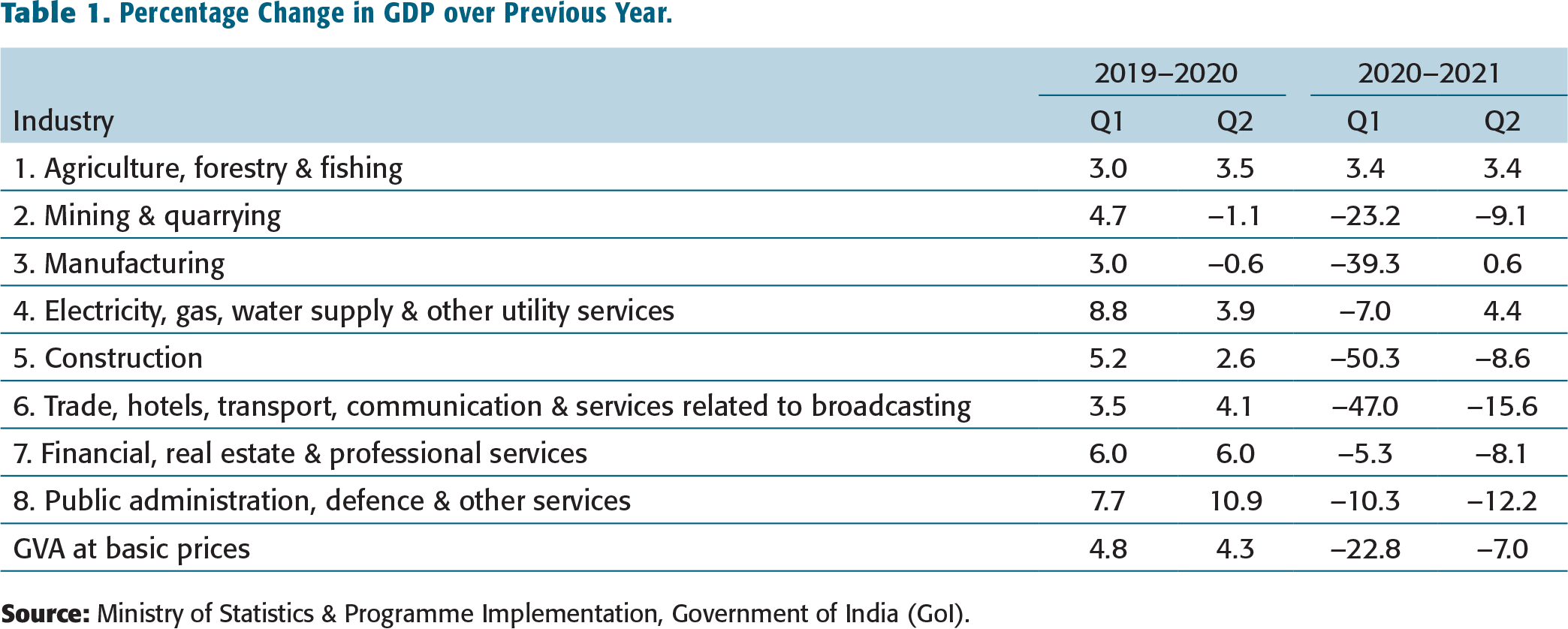

Further, India imposed a strict nationwide lockdown on 25 March 2020, which continued till 31 May 2020 with gradual relaxations in areas where there were none or few cases of infection from the COVID-19. Economic activity was resumed gradually from 1 June 2020 in a phased manner. Gross value added (GVA) decreased by around 23% in the first quarter (April to June), primarily during the lockdown period (Table 1). Though the second quarter (July to September) indicates a sign of improvement in GVA and revival of the economy, still it is negative at 7%. However, it shows a ‘V’ shape recovery in the economy. This has happened mainly because of the phase-wise relaxations during the lockdown that allowed the economic activities to restore and the support measures announced by the government and the RBI. However, according to Economic Survey 2020–21, the Indian economy will grow by –7.2% in the financial year 2020–2021 as against 3.9% in the financial year 2019–2020 (Ministry of Finance, 2021), which indicates an overall contraction in the Indian economy due to the COVID-19 pandemic.

Percentage Change in GDP over Previous Year.

The sudden and strict lockdown, at least in its initial phases, resulted in the closure of the majority of the businesses, which led to an increase in unemployment and a decrease in demand in the economy. It forced millions of migrant workers, primarily employed in the informal sector, to return to their villages (Srivastava, 2020). According to centre for monitoring Indian economy data, the Indian economy observed the highest unemployment in the months of April and May in both rural and urban areas and at the national level. Just after the imposition of the lockdown in the last week of March, the unemployment rate reached around 24% in the country, with 25%–26% and 23% in urban areas and rural areas, respectively. However, the employment condition in the economy showed a sign of revival in June when the economy was gradually reopened in phases. Unemployment rates declined in June and July and reached around 7.43% in the country, with 9.15% and 6.66% in urban and rural areas respectively. Therefore, these observations about trade, GVA and employment in 2020 clearly indicate that the Indian economy has also been severely affected by the spread of COVID-19 and the imposition of containment measures to curb its spread.

IMPACT OF COVID-19 ON THE MSME SECTOR IN INDIA

MSMEs play a pivotal role in the sustainable growth of the Indian economy by contributing significantly to the GDP and exports and employing millions of people, particularly those at the bottom of the socio-economic hierarchy. According to the MSME Annual Report 2020–21, the MSME sector in India contributes 30.27% and 33.50% in GDP and GVA, respectively (M/o MSME, 2021). Further, the share of MSMEs in export is around 48% of the total exports from India (M/o MSME, 2019). Since both the GDP and the export of the country (like in many other countries) have been severely affected by the spread of COVID-19, the MSME sector will experience a similar or greater impact in terms of reduction in its output and exports. Further, the MSME sector, which is largely unorganized and comprises small-sized individual units, has faced a large-scale reverse migration of labourers triggered by the lockdown; hence, more MSMEs in urban areas may face labour scarcity which will affect the production and services of the business units. Studies indicate that the lockdown has had a more severe impact on MSMEs than on large firms in India given their size, scope of operation and limited resources (Ghosh, 2020; Rathore & Khanna, 2020; Sahoo & Ashwani, 2020; Sipahi, 2020).

Although it is unlikely for any firm, regardless of size, to have strategies to face a pandemic like COVID-19, larger firms have some formalized plans in place to address such situations (Rebmann et al., 2013). But MSMEs lack financial resources and knowledge to survive such shocks without government assistance (Watkins et al., 2008). For MSMEs, the biggest challenge for recovery— both short term and long term—is the lack of financial resources (Cumbie, 2007; Farrell & Wheat, 2016). Therefore, MSMEs are at high risk of permanent closure after a large-scale disaster (McCall, 2020; Rebmann et al., 2013; Schrank et al., 2013). The other challenges for their recovery include local quarantine policy, business reopening permits, health regulations at workplace, broken supply chains and logistics, low market demand and worries about revenue and cash flow (Bouey, 2020).

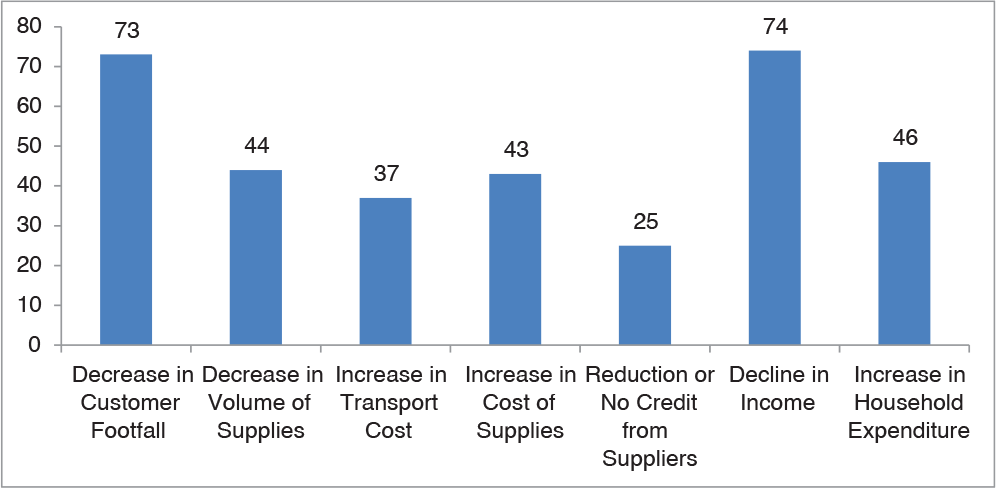

A study of micro and small enterprises by MicroSave Consulting shows that around 74% of businesses, largely engaged in retail trade in essential commodities, were operating while the remaining 26% were shut in April 2020. Around 73% of the businesses reported a decline in customer footfall while around 44% reported a decline in the volume of supplies (Figure 1). Increase in transport cost and cost of supplies were reported by approximately 37% and 43% of the businesses, respectively. Around 25% businesses reported reduction or non-availability of credit from suppliers. Most importantly, 74% of businesses reported a decline in income while 46% reported an increase in household expenditure. These findings show that MSMEs are facing multiple challenges, including a decline in customer count, an increase in the cost of production/operation, a reduction in supplier’s credit, and a decline in income due to COVID-19 and the lockdown. An increase in household expenditure along with a decline in income will further worsen the condition of small enterprises by forcing them to dig into their savings. However, the report also indicates that some enterprises have benefitted by panic buying or bulk buying.

POLICY INITIATIVES BY THE GOVERNMENT AND THEIR IMPLICATIONS FOR MSMES

The unprecedented recession caused by COVID-19 has significantly influenced corporate investment decisions and government investment policies across the world (UNCTAD, 2020). Many countries have taken protective measures to revive the economy and support critical domestic industries through relief packages, including income transfer, easing liquidity flow to financial sector, deferment of loan repayment and fresh loans on easy terms (International Labour Organization, 2020). The GoI has also announced many initiatives to revive the economy. The finance minister announced a relief package of ₹1,700 billion on 26 March 2020 under the PMGKY. This relief package includes insurance cover for health workers; distribution of free food grain to the poor; free gas cylinders to the poor households; cash transfer to farmers, Jandhan account holders, and pensioners (the elderly, widows and specially abled persons); wage hike under Mahatma Gandhi National Rural Employment Guarantee Act; and contribution in employee’s provident fund accounts. Alongside this, the RBI also announced policies supporting reduction in interest rates and delayed debt repayment to boost the confidence of the investors (RBI, 2020).

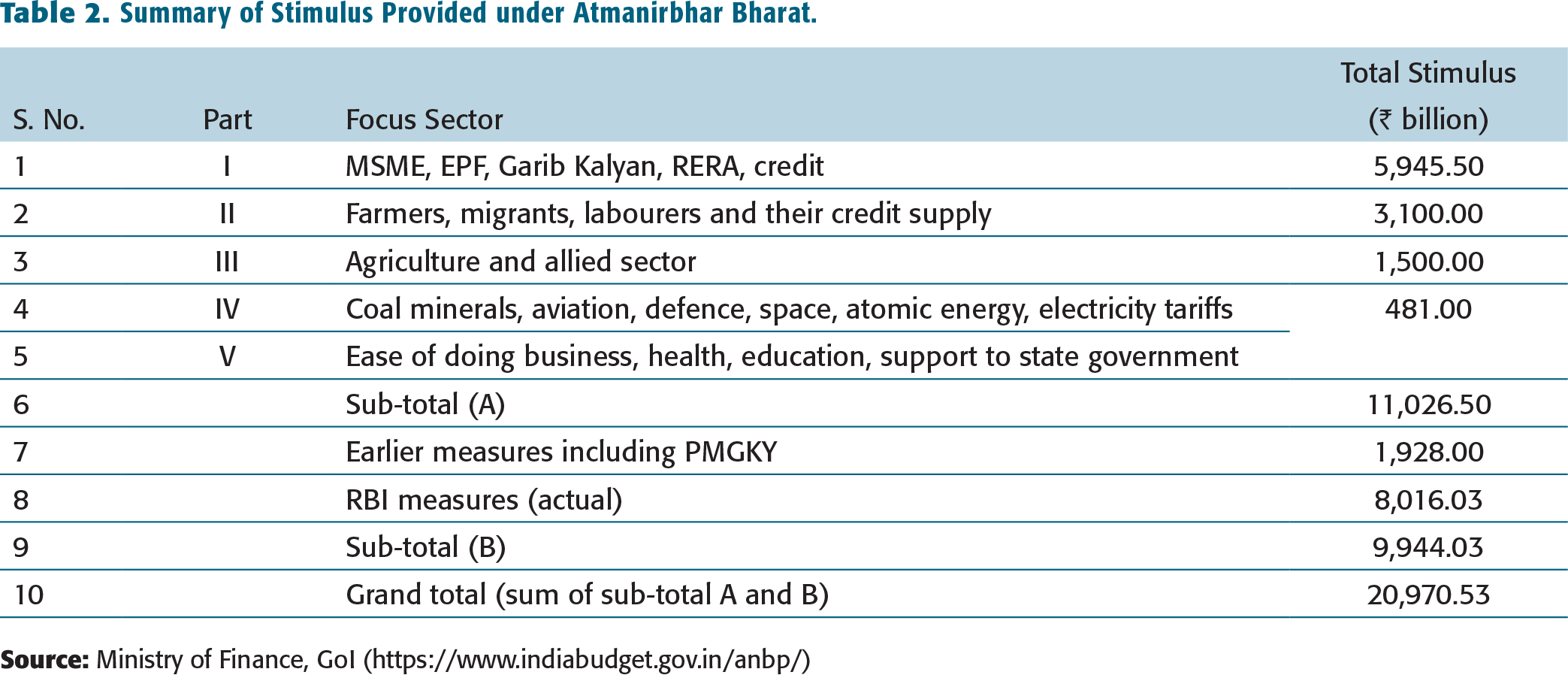

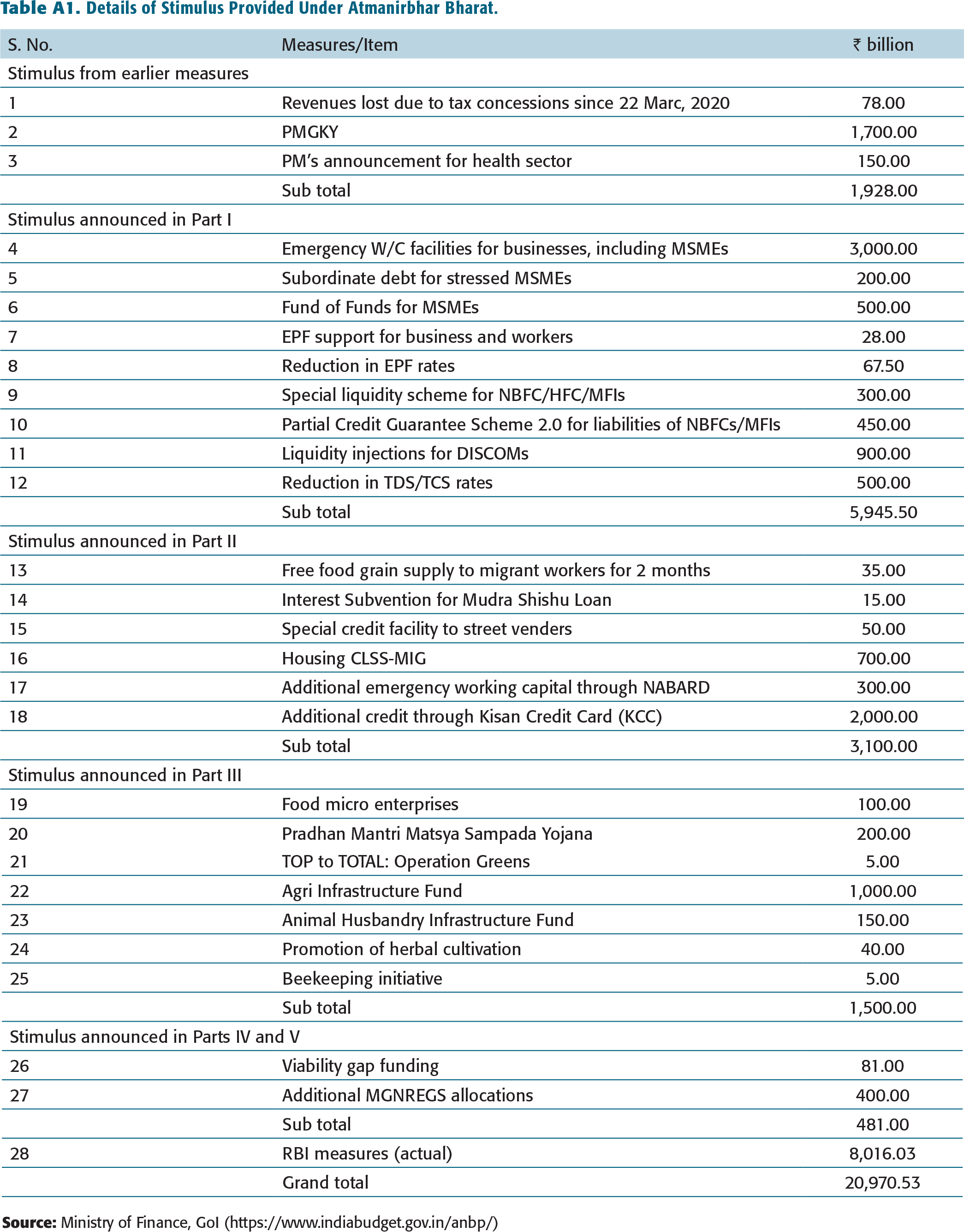

Further, the prime minister announced a relief package of around ₹21,000 billion, equivalent to almost 10% of GDP, with a clarion call for Atmanirbhar Bharat [Self-reliant India] on 12 May 2020. The stimulus packages under Atmanirbhar Bharat—announced in five parts that focus on land, labour, liquidity and laws—aim to support the five pillars of self-reliance: economy, infrastructure, system, vibrant demography and demand (Table 2). This package also includes previous relief packages by the government and decisions taken by the RBI in order to address financial challenges of firms/individuals posed by the containment measures. The package caters to all sections of the society and economy including labourers, middle class, agriculture, cottage industries, MSMEs and the industry as a whole (for details, see Table A1). It also emphasizes on local industries, local markets and local supply chains.

Summary of Stimulus Provided under Atmanirbhar Bharat.

Since the economy is interlinked, any relief package or initiative by the government and the RBI, whether focusing on MSMEs or not, will impact the sector, directly or indirectly. However, the key initiatives for MSMEs in the Atmanirbhar Bharat stimulus package include (a) revision in the definition of MSMEs, (b) Emergency Credit Line Guarantee Scheme, (c) Credit Guarantee Scheme for Subordinate Debt, (d) equity infusion for MSMEs through ‘Fund of Funds’ (e) Interest Subvention Scheme for Shishu loans under Pradhan Mantri MUDRA Yojana (PMMY), (f) modification in global tender norms in favour of MSMEs, (g) promotion of e-market linkages and (h) MSME dues to be cleared within 45 days. Given the focus of the article, select policy measures having direct implications for MSMEs have been discussed below.

Revision in the Definition of MSMEs

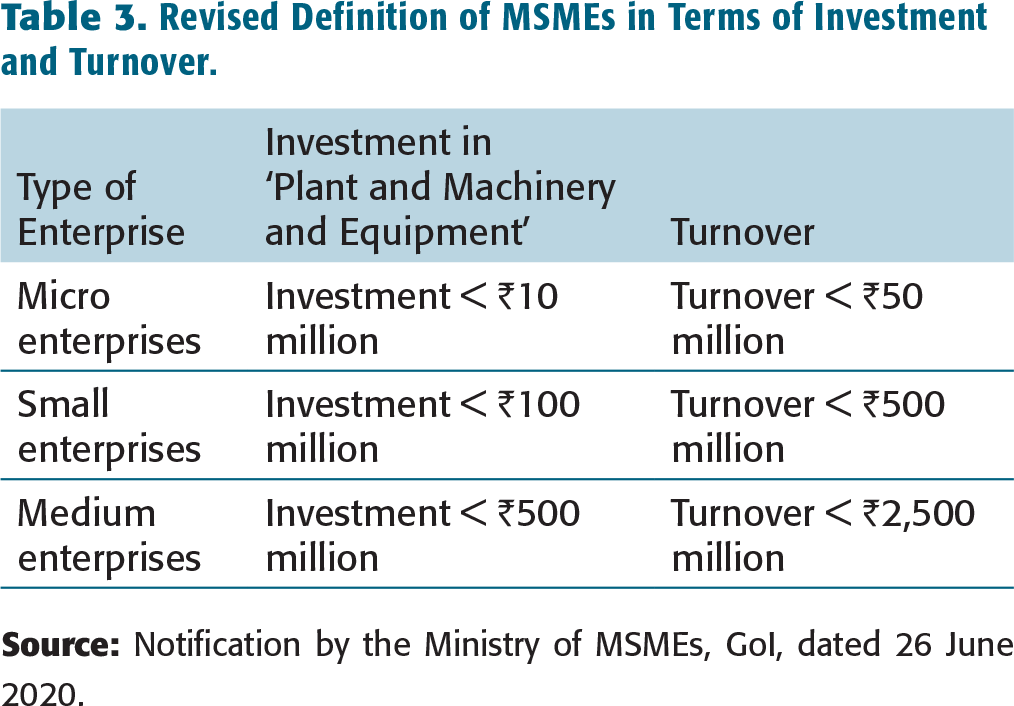

As per the notification dated 1 June 2020, the GoI revised the definition of MSMEs and included ‘turnover’ as an additional criterion for defining an MSME. The notification was further revised on 26 June 2020 to modify the composite criteria of the definition of MSMEs in terms of investment in plant and machinery or equipment and turnover (Table 3). As per this notification, an enterprise shall be classified as (a) a micro enterprise, where the investment in plant and machinery or equipment does not exceed ₹10 million and the turnover does not exceed ₹50 million, (b) a small enterprise, where the investment in plant and machinery or equipment does not exceed ₹100 million and the turnover does not exceed ₹500 million and (c) a medium enterprise, where the investment in plant and machinery or equipment does not exceed ₹500 million and the turnover does not exceed ₹2,500 million (GoI, 2020). The revised definition of MSMEs is effective from 1 July 2020. Under the new classification, if an enterprise crosses the ceiling limit specified for its present category in either of the two criteria of investment or turnover, it will be placed in the next higher category. On the other side, no enterprise shall be placed in the lower category unless it goes below the ceiling limit specified for its present category in both the criteria of investment and turnover.

Revised Definition of MSMEs in Terms of Investment and Turnover.

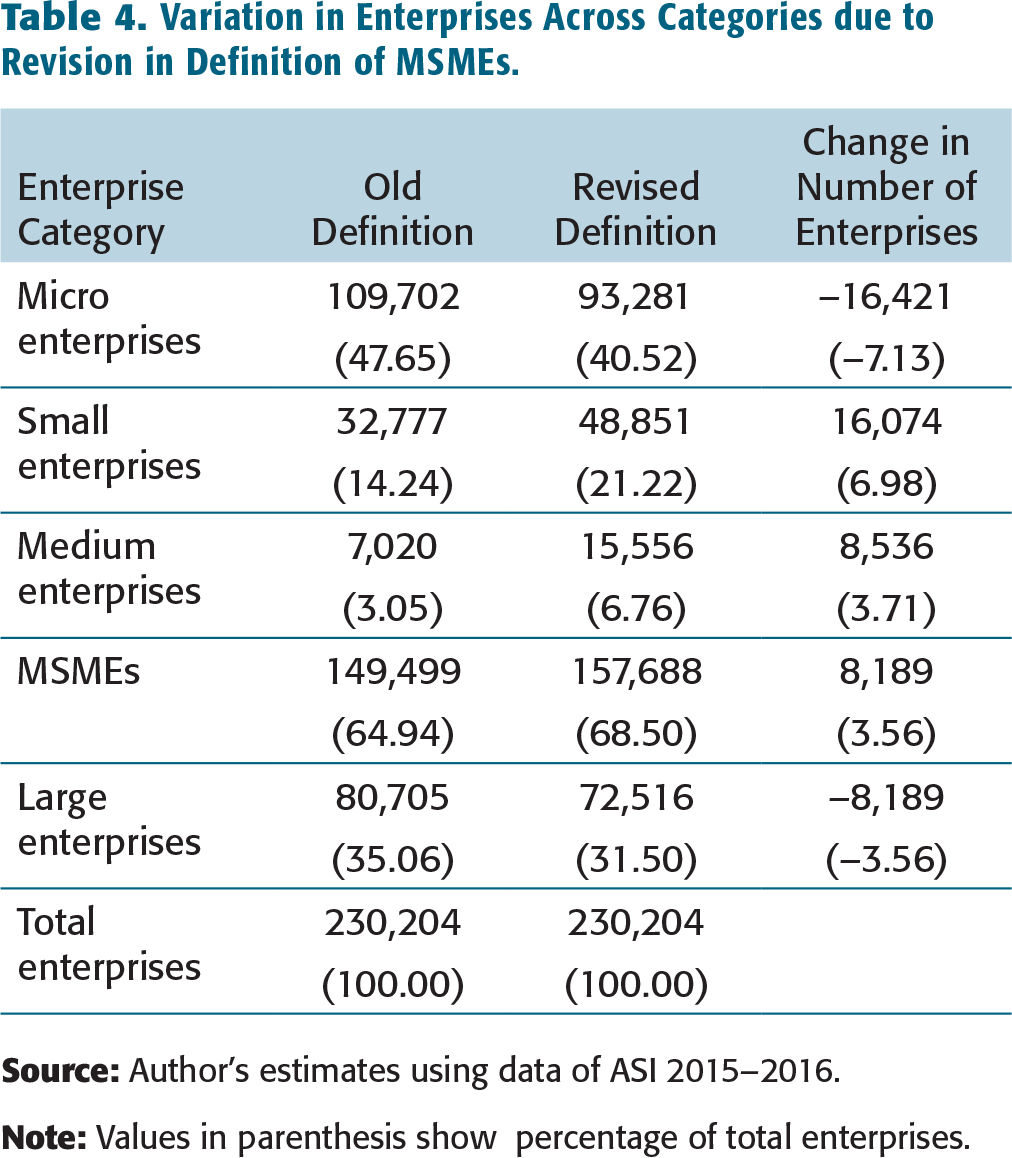

In India, MSME census has not been conducted after 2006–2007. The latest available data about MSMEs which is widely used for analysis is 73rd round survey of unincorporated non-agricultural enterprises (excluding construction) conducted by National Sample Survey Office (NSSO) in 2015–2016. Since this data does not include large enterprises, movement of enterprises from large to MSMEs categories cannot be studies. In order to assess the implications of revision of the definition of MSMEs, the Annual Survey of Industries (ASI) 2015–2016 data has been used. Although the data covers only manufacturing enterprises registered under Factories Act, 1948, it can depict variation in enterprises across categories due to the revision in the definition of MSMEs. Table 4 clearly shows that the share of MSMEs in total manufacturing enterprises covered under ASI 2015–2016 has increased to 68.50% from 64.94% due to revision of the definition of MSMEs. Similarly, the share of large enterprises has declined from 35.06% to 31.50%. It clearly shows that the revised definition of MSMEs will allow more enterprises to be scategorized as MSMEs and enable them to avail the benefits thereunder.

Variation in Enterprises Across Categories due to Revision in Definition of MSMEs.

The share of small enterprises increased from 14.24% to 21.22%, and for medium enterprises from 3.05% to 6.76% (Table 4). Surprisingly, the share of micro-enterprises declined from 47.65% to 40.52%. It may be due to the inclusion of turnover limits in the composite criteria for defining MSMEs. Some micro enterprises with higher turnover may shift into the category of small and medium enterprises. However, since the definition of MSMEs is linked with their Goods and Services Tax (GST) returns, a firm’s categorization as the micro, small or medium enterprise may vary over time with variation in its investment and turnover (excluding export). The exclusion of value of exports of goods or services or both from the calculation of turnover will help increase the export capacity. The inclusion of turnover will provide a realistic measure for banks and financial institutions to evaluate the firms and enable cheaper and easy access to credit.

Emergency Credit Line Guarantee Scheme

A collateral-free term loan at a concessional rate of interest is provided to business entities for additional working capital finance of 20% of outstanding credit as of 29 February 2020. The scheme aims to provide ₹3,000 billion collateral-free loan with a 100% credit guarantee to more than 45 lakh MSMEs, as per an estimate by the government. Initially, the scheme was available to those business units whose accounts are standard, with up to ₹250 million outstanding and turnover of up to ₹1 billion. As per a recent notification dated 4 August 2020, the scheme has been extended to individual loans given for business purposes, if such loans fulfil the eligibility criteria under the scheme. Further, the upper ceiling of loans outstanding and annual turnover have been increased to ₹500 million and ₹2.5 million, respectively, given the modification in the definition of MSMEs. Under this scheme, a total of ₹3,000 billion liquidity—100% guaranteed by the GoI—will be provided to more than 4.5 million MSMEs that will help them resume their business activities.

Certainly, collateral-free loans to MSMEs will enhance their liquidity and working capital base and enable revival during the COVID-19 period. An estimate from the 73rd round survey of unincorporated non-agricultural enterprises (excluding construction) conducted by the NSSO in 2015–2016 shows that around 31% of MSMEs are registered. The low registration of MSMEs is a serious hurdle in accessing government assistance and formal credit even though it is collateral-free or subsidized. Micro enterprises constitute around 99.5% of the total MSME establishments. These firms face more challenges in terms of access to credit and government support. Further, with the revision of the definition of MSMEs, larger firms will be eligible to avail of the MSME benefits. Therefore, it may be possible that a significant fraction of MSMEs facing challenges due to COVID-19 may not be able to avail the benefits under the Emergency Credit Line Guarantee Scheme.

Credit Guarantee Scheme for Subordinate Debt

The Credit Guarantee Scheme for Subordinate Debt is a sub-debt (as equity or quasi-equity) support scheme for stressed MSMEs whose accounts have been standard as on 31 March 2018 and have been in regular operations, either standard account or non-performing asset (NPA) account, during subsequent financial years, that is, 2018–2019 and 2019–2020. Under the scheme, promoters of eligible MSMEs will get a personal loan, equal to 15% of one’s share or ₹75 lakh, whichever is lower, from scheduled commercial banks. The scheme covers 90% of the guarantee cover while 10% would be covered by the promoters. For this purpose, the government has introduced a ‘Distressed Assets Fund - Subordinate Debt for Stressed MSMEs’ worth ₹200 billion. This scheme will benefit about two lakh stressed MSMEs providing support to restart their businesses and create new jobs. This scheme aims to target a very small fraction of the MSMEs. Therefore, it has minimal relevance for small firms facing credit problems due to COVID-19.

Equity Infusion for MSMEs Under ‘Fund of Funds’

Government has set up a ‘Fund of Funds’ with a corpus of ₹100 billion. The fund aims to infuse ₹500 billion equity in MSMEs with growth potential even while facing a lack of finance. The scheme aims to cater to 2.5 million MSMEs that have an ‘AAA’ rating. The scheme proposes to buy up to 15% of the growth capital in high credit MSMEs. This will expand the size and capacity of the MSMEs despite facing shortage of equity and help them get listed on stock exchanges. In terms of structure, the Fund of Funds may be operated by the National Small Industries Corporation or other government authorities and will be managed by a mother fund in addition to a few daughter funds. These funds will enable MSMEs to grow in capacity and size and encourage them to list on the stock exchanges. Very few MSMEs are registered in stock exchanges.

Further, given the low registration level in MSMEs, only a small segment would be able to avail capital through this scheme. This scheme aims at targeting only 2.5 million MSMEs, which is a very small fraction of the total MSMEs, that is, 63.4 million units. Therefore, it has very limited relevance for the small firms facing credit problems due to COVID-19.

Interest Subvention Scheme for Shishu Loans Under PMMY

The government announced a 2% interest subvention on loans up to ₹50,000 secured by small businesses under the Mudra scheme’s Shishu loan category. The interest subvention will be offered to encourage payees to make regular payments for 12 months. The total relief amount under the subvention to Shishu loanees making regular payments will be ₹15 billion. It will help micro enterprises to get loans under the PMMY Shishu loan category as well as motivate them to pay on time. Micro enterprises represent around 99.5% of the MSMEs. Therefore, this initiative may be beneficial to a large fraction of the MSMEs.

Modification in Global Tender Norms in Favour of MSMEs

The government announced amendments to the General Financial Rules, disallowing global tenders for government contracts up to ₹2 billion. The global tenders up to ₹2 billion will be awarded to MSME companies, creating opportunities for domestic MSMEs in the government contracts. This initiative will encourage small domestic firms to participate in tenders with high values. But, with a lack of formalization among MSMEs, particularly the micro-enterprises, the benefits of such initiatives will be mainly availed by the small and medium enterprises.

Promotion of e-Market Linkages

Since there would be fewer trade fairs and exhibitions due to the social distancing norms to curb the spread of COVID-19, the government announced the promotion of e-market linkages. It would help small firms to cater to domestic demand as well as international demand. An estimate from the 73rd round survey of unincorporated non-agricultural enterprises (excluding construction) conducted by NSSO in 2015–2016 shows that the most severe problems MSMEs face is shrinkage in demand (16.80%). The COVID-19 crisis has further worsened it. With the revival of the domestic economy and relaxation in the curb on international movement of goods and services, this initiative will definitely encourage MSMEs to embrace e-commerce platforms.

MSME Dues to be Cleared Within 45 Days

One of the major challenges faced by MSMEs is delayed payment. As per the MSME-Samadhaan portal, there are huge dues pending with the public sector units. In order to avoid undue financial distress to MSMEs, the government announced that all dues of MSMEs pending with the government’s public sector units would be cleared in 45 days. Another estimate from 73rd round survey of unincorporated non-agricultural enterprises (excluding construction) conducted by NSSO in 2015–2016 shows the second most severe problem faced by the MSMEs is recovery of financial dues (9.48%). It affects the financial condition of MSMEs as well as their investment decisions. This initiatives may be helpful to MSMEs, if it is implemented effectively.

INITIATIVES TAKEN BY RBI AND THEIR IMPLICATIONS

The RBI announced a slew of measures on 27 March 2020 to provide relief to the financial sector and the industries facing challenges posed by the outbreak of COVID-19. The measures include loan moratorium, reduction in cash reserve ratio, repo rate and reverse repo rate, targeted long-term repo operations, ease of working capital financing, deferment of net stable funding ratio and marginal standing facility.

In order to provide relief to individuals and business entities facing difficulties in repaying loans and interest, the RBI initially announced a moratorium in March 2020 for three months, which was later extended for additional three months till August 2020. It applies to all commercial banks, regional rural banks, small finance banks, co-operative banks and non-bank financial companies, including microfinance and housing finance. The deferment of loan payment is expected to postpone the financial burden of MSMEs. However, it may be helpful to small firms in the short run.

The other initiatives of RBI (such as reduction in cash reserve ratio, repo rate, reverse repo rate and targeted long term repo operations) will enhance the lending capacity of the financial institutions in the country. As observed in Figure 1, around 75% of small firms have faced a decline in income. With the decline in the incomes of firms, loan repayment to banks will become difficult. It may affect the lending capacity of the banks. Therefore, such initiatives by the RBI may enhance the liquidity of banks and encourage them to lend to firms facing credit problems due to COVID-19. Firms can only approach banks for borrowing if there is a demand for their products/services in the economy and expect a positive investment return. Further, in spite of liquidity, banks can only be encouraged to lend to firms if they find that their lending would not be converted into NPAs. Therefore, the success of initiatives by the RBI to enhance the lending capacity of banks depends upon market sentiments.

CONCLUSION

All economies have become interconnected in the last few decades due to globalization and through production networks. Therefore, economic disruptions generated in one country will affect the other country or the world economy to the degree it is economically connected with other countries. COVID-19 has affected almost every country in the world, impacting domestic economies, causing disruptions in the supply chains. The GoI and RBI have taken many initiatives to overcome the economic shocks, including PMGKY and Atmanirbhar Bharat, which together are a package of around ₹21,000 billion .

The measures taken by the RBI aim to increase liquidity in the financial market, reduce the burden of timely repayment, and encourage individuals and industries to borrow at cheaper rates from banks. At the same time, the stimulus packages by the government indicate a multi-pronged approach to revive economic growth by supporting all sections of the economy, particularly the weaker sections and the MSMEs. It focuses on local enterprises. Apart from encouraging MSMEs to borrow from banks, the stimulus initiatives will also motivate them to seek funds from the capital market in the form of equity and bonds.

By introducing a composite criterion to define MSMEs in terms of investment and turnover, increasing the upper limits of investment and turnover may increase the number of enterprises under MSMEs. It may be possible that some large enterprises may fall under the category of MSMEs because of the revised definition of MSMEs. Given the high degree of informality in the MSME sector, the majority of the MSMEs, particularly micro-enterprises that represent a major part of the sector, may not be eligible to avail the benefits announced for MSMEs. However, it may encourage formalization in the MSME sector in future. Further, large firms which may be categorized as MSMEs due to the revision in the definition would be in front, availing benefits granted thereunder. Further, micro enterprises are very diverse and localized in their operation and access to market. Therefore, there is a need to design more schemes specifically for supporting micro enterprises.

Since the initiatives and measures announced by the government and the RBI have limited scope to support the MSME sector, given the high-level informality, there is a need to bring out additional measures to revive small firms, particularly the diverse micro enterprises. A broad national policy may not address their concerns. Rather, government measures designed after consultation with local business associations may benefit local enterprises.

Appendix

Details of Stimulus Provided Under Atmanirbhar Bharat.

Footnotes

Acknowledgement

This research paper is an outcome of a study entitled ‘Understanding Criticality of Flow of Funds for Robust Growth of MSMEs’ conducted by Institute for Studies in Industrial Development, New Delhi. This study is sponsored by the State Bank of India, Bank of India, UCO Bank, Canara Bank, Corporation Bank, and United Bank of India.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.