Abstract

BAJAJ GROUP

BEL was a part of the Bajaj family, which started doing business in 1905 when Bachhraj Bajaj established a cotton ginning factory in Wardha, Maharashtra. The Bajaj Group was founded by Jamnalal Bajaj, the adopted grandson of Bachhraj Bajaj, in 1926. He was a philanthropist and freedom fighter greatly influenced by Mahatma Gandhi. He built the Bajaj Group on Gandhian values with a legacy of helping society at large. When India became independent in 1947, there was a transition from the controlled economy to the ‘license raj’, which restricted free competition. Domestic entry and export competition were regulated, which eliminated product diversification beyond what was licensed, penalized unauthorized expansion of capacity, prevented the reallocation of imported inputs and eliminated all aspects of investment and production (Chittoor & Aulakh, 2015). Over the years, the group diversified into automobiles, financial services, insurance, steel, electrical and consumer appliances, material handling, etc. There were 34 affiliated companies under the business group with an approximate turnover of ₹1,535 billion. Bajaj Auto Ltd. was the flagship company of the group and the world’s fourth-largest two and three-wheeler manufacturer with an international presence in Africa, Asia, and Latin America and a turnover of about ₹300 billion. Bajaj Electricals was relatively small with a turnover of about ₹6 billion.

INDIAN BUSINESS LANDSCAPE IN 1990s

With the liberalization of the Indian economy in 1991, government control reduced, and the economy transitioned towards a market-based economy. During the transition period, various financial and legal reforms were undertaken that led to the entry of foreign multinationals. Competition in the domestic market increased, and incumbents had to realign themselves to remain competitive. Firms also had to encounter ‘institutional voids’ (Khanna & Palepu, 1997) and confront underdeveloped capital and labour markets and limited enforcement of liability laws. The Indian business landscape was also dominated by diversified business groups which had common ownership and control. These business group firms dominated the economic landscape, with the highest proportion of revenues and significant investments in R&D capabilities. Firms affiliated with business groups could overcome institutional voids by drawing upon the group’s resources, including financial, managerial, and reputation. These firms found it easier to compete in international markets compared to standalone firms.

BAJAJ ELECTRICALS

BEL started as Radio Lamp Works Limited in Lahore (Pakistan), on 14 July 1938 by Kishenchand Kaycee to manufacture electric lamps. In the next two decades, it forayed into fans (The Asian Age, 2000), glass shells for electric lamps, transformers, and fluorescent lighting fixtures. In 1958, it became the sole selling agent of Kassel fans. Since the portfolio of products was expanding beyond lamps, the firm came to be known as Bajaj Electricals in 1960 to represent its interest and activities in diversified businesses. BEL diversified into the engineering and projects (E&P) sector, with high-mast lighting business in the mid-1980s with imported products from the UK. In 2002, BEL entered the premium segment of small consumer appliances through a technical and brand licensing alliance with Morphy Richards. With the changing demographic and regulatory environment in India, BEL leveraged the opportunity to enter into LED (light emitting diode) lighting and intelligent lighting. It leveraged these competencies into enhancing its competence in the engineering and projects business. See Exhibit 1 for a profile of BEL. By 2016, lighting contributed 22.9%, consumer durables contributed 43.4%, and engineering and projects contributed 33.6% revenues. BEL was a market leader in volume in small appliances and had a pan India network of 400,000 retail outlets, 1,000 distributors, 5,000 dealers and 315 service centres.

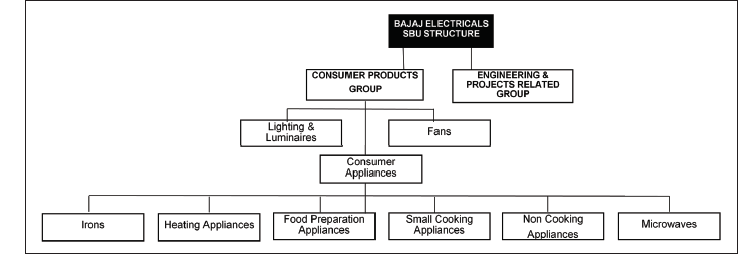

Product Portfolio of Bajaj Electricals

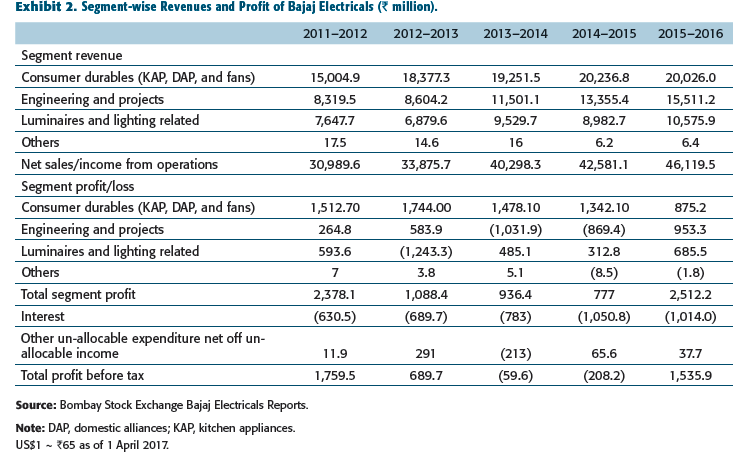

Segment-wise Revenues and Profit of Bajaj Electricals (₹ million).

US$1 ∼ ₹65 as of 1 April 2017.

Lighting and Luminaires

The lighting business comprised two segments: lamps and luminaires. The former included general lamps, fluorescent tube lights, sodium vapour lamps and halogen lamps. The luminaires segment included fittings, chokes, and accessories (Business line, 1997). The lighting and luminaries business in India was worth ₹190 billion. It was dominated by Philips with ₹27.4 billion revenues in 2015. The industry was expected to touch ₹350 billion by 2020 (Bajaj Electricals, 2015–2016). The lighting and luminaires business accounted for ₹10.5 billion in BEL revenues in 2015. BEL was the industry leader in large area and roadway lighting, especially flood lights, street lights, and industrial lighting. BEL manufactured general lighting service lamps at its factory at Kosi. Fluorescent tube lights were manufactured at Hind Lamps at Shikohabad near Agra, in which BEL had a 60% stake, while the remaining stake was held by Philips. Philips also provided technology for lamps (Business India, 1994). However, the pace of growth of the bulb industry was slow (5%), due to which the Kosi plant was under-utilized and suffered a loss of ₹16.7 million (The Economic Times, 2016).

Through a distribution agreement with German-based Trilux-Lenze, BEL moved into high-end lighting in 2005. The compact fluorescent lamps segment was growing at 25%. Hence, BEL acquired a 32% stake in Starlite Lighting at Nashik, Maharashtra, in 2007. The lighting industry was undergoing a paradigm shift towards energy efficiency and aesthetics, resulting in demand shifting to LED-based lighting. Moreover, with the launch of Prime Minister Narendra Modi’s ‘UJALA’, a national programme for LED-based home and street lighting in January 2015 (PMO, 2015) and the decision of the Power Minister to replace 770 million incandescent lamps along with 35 million street lights with LEDs by 2019 (Gupta, 2015), LED was expected to account for ₹216 billion or more than half of the lighting business by 2020 (Bajaj Electricals, 2016). BEL, Philips, and Crompton Greaves leveraged this opportunity. They started supplying LED bulbs to Energy Efficiency Services (EESL), a joint venture company of the public-sector undertakings of the power ministry. Philips was targeting 45% of its revenue from LED business by 2018. Philips had technology leadership in LED bulbs with an extensive portfolio of LED and SSL (solid-state lighting) related patents which were licensed to about 300 companies. BEL also started manufacturing, assembly, and distribution of LED lights in 2009 through an exclusive license agreement with US-based RUUD Lighting. These were priced at ₹86 as compared to ₹100 of Philips (Chatterjee & Kar, 2014). In 2016, intelligent lighting emerged as the next big thing for new-age electrical solutions companies. BEL entered into a strategic alliance with the UK-based Gooee to create lighting solutions on the Internet of Things (IoT) platform to deliver IoT applications to shape customer needs of smart controls used for dimming and monitoring (Kurup, 2016).

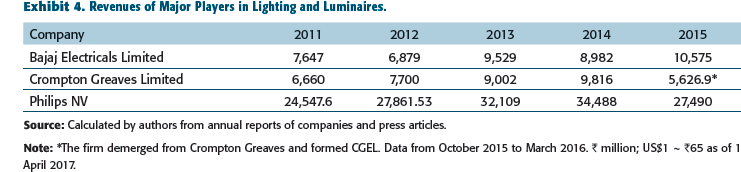

Luminaires comprised 22% of the industry (Mint, 2017). Luminaires business of BEL accounted for around 10% of the overall business in 2015. The luminaire products were sourced from dedicated vendors in Daman and Himachal Pradesh in India, and through imports from China. The main competitor, Philips started importing luminaires from China but gradually set up a design and research centre in the national capital region (NCR) of India, where it also started manufacturing and assembling operations. See Exhibit 3 for profiles of the two major competitors and Exhibit 4 for revenues.

Profiles of Major Players in Lighting, Luminaires, and Fans.

Air Treatment Products

Air Treatment comprised a variety of fans, air conditioners and air coolers. Fans dominated the segment with 87% revenues, followed by air conditioners with 7.1% and air coolers with 5%. BEL had a presence in fans since 1939, but not in air coolers and air conditioners, though a large segment of the affluent urban population was shifting to air-conditioned homes. Fans included wall-mounted fans, ceiling fans, exhaust fans, pedestal fans and table fans. The products were classified into premium, economy and energy efficient categories. Premium ceiling fans had high air delivery and high speed, with superior finishing. In 1998, BEL started manufacturing fans at Chakan in West India and procured related components from vendors in Himachal Pradesh and Uttarakhand in North India, Hyderabad in South India and through imports from China (Bajaj Electricals, 2009). The Chakan plant had a capacity of 800,000 units per annum. In 2001, BEL entered an alliance with G. D. Midea, one of China’s largest appliance makers and world’s leading brand in air treatment products, to market Midea table, pedestal and wall-mounted (TPW) fans under the brand name ‘Bajaj Midea’. The technology and designs were shared by Midea while BEL marketed the fans and gained a 15% share in the market (Mascarenhas & Maradia, 2004). Simultaneously, Usha and Polar also entered into an alliance with Midea to import 150,000 portable fans each. At that time, Midea was manufacturing 10 million portable fans while India was manufacturing 8 million fans. To cater to children who were evolving as a significant consumer group, BEL entered a licensing agreement with Walt Disney to market children’s fans with Disney characters since this was a niche area where products were priced twice higher than conventional products (Mukherjee & Jacob, 2012).

Revenues of Major Players in Lighting and Luminaires.

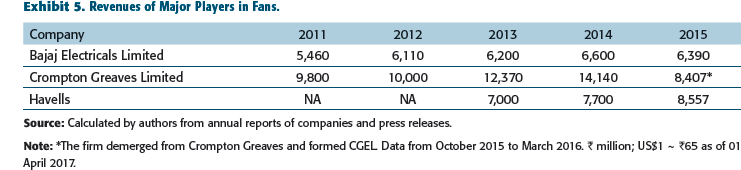

Revenues of Major Players in Fans.

Market Share of Fans (% volume).

A scheme launched by the Government of India (GOI), the ‘Pradhan Mantri Awas Yojana’ (Prime Minister’s Housing Scheme), to provide housing for all by 2022 by constructing 20 million houses in urban areas triggered demand for fans. Under the government’s ‘National Energy Efficient Fan’ initiative, five-star rated fans were being procured at approximately 60% the market price to replace 160 million fans by 2019 (Motilal Oswal, 2016). BEL, Crompton Greaves and some other players were part of the initiative.

Consumer Appliances

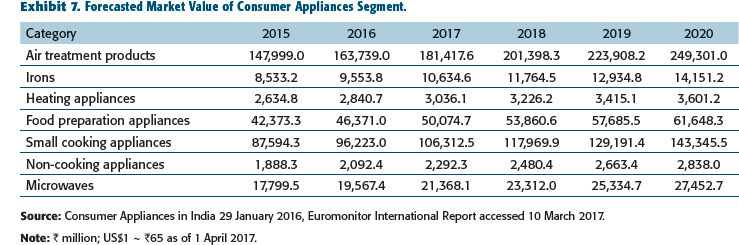

Forecasted Market Value of Consumer Appliances Segment.

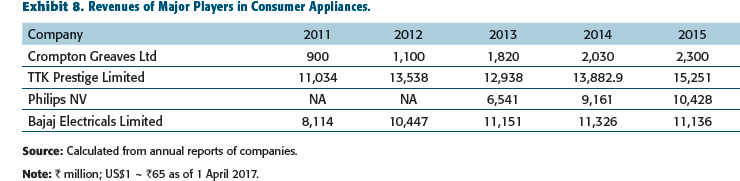

Revenues of Major Players in Consumer Appliances.

Profiles of Major Players in Consumer Durables.

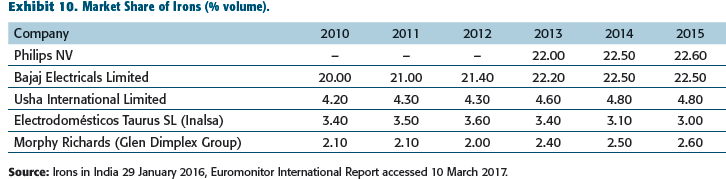

Irons

Market Share of Irons (% volume).

Heating Appliances

Market Share of Heating Appliances (% volume).

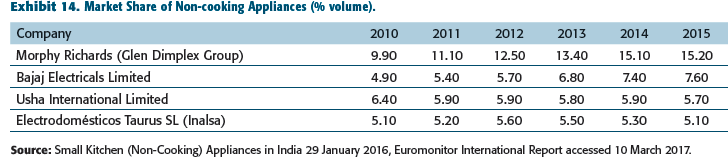

Small Kitchen (Non-cooking) Appliances

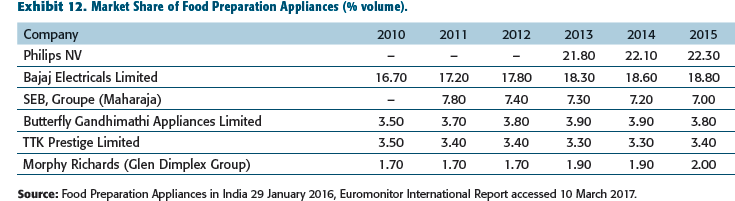

Market Share of Food Preparation Appliances (% volume).

Food Preparation Appliances

Food preparation appliances had a market of ₹42.3 billion in 2015. The segment comprised blenders, mixers, food processors, and juice extractors. Food preparation appliances grew by 6.3 and 14.16% year-on-year in retail volume and value, respectively, between 2010 and 2015. Changing lifestyles and the convenience of such appliances over traditional methods were the key reasons for their growth, particularly in metro cities. Countertop blenders and grinders dominated the category with a 67% volume share in 2015. Countertop blenders were more popular in South India, where grinding was required for many dishes. Other food preparation appliances such as juice extractors and hand mixers were niche products due to low perceived utilization in food preparation and availability of low-cost traditional alternatives. The segment was fragmented, with more than 20 companies jostling for a 71% share of volume sales in 2015.

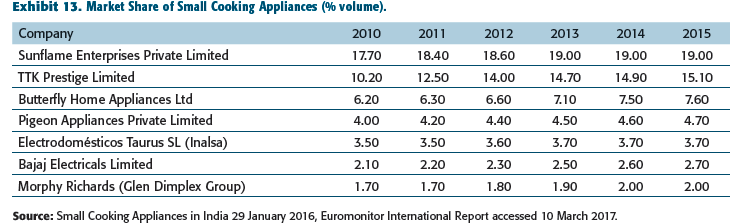

Market Share of Small Cooking Appliances (% volume).

Small Cooking Appliances

Small cooking appliances had a market size of ₹88 billion in 2015. This segment comprised freestanding hobs, toasters, coffee machines, cookers, and ovens. Freestanding hobs dominated the category with a 78% volume share in 2015, driven mostly due to the increase in the number of households in India. The small cooking appliances segment grew by 6.1% in retail volume year-on-year and 10.7% in retail value between 2010 and 2015. Growth in this segment was the result of changing lifestyles and food habits of urban consumers. Changes in the breakfast menu fuelled the growth of coffee machines and toasters, whereas reduced cooking time led to a need for appliances such as rice cookers and electric steamers. A preference for a steamed or grilled diet over fried food was another reason for the growth of electric grills and electric steamers. The overall size of coffee machines in India was much smaller than those in other countries. Partly because the consumption of coffee remained lower than tea, with consumption proportionally higher in South India. Electronics and appliance specialist retailers accounted for 71% volume share in 2015. Croma and Reliance MART were major players in small towns because of their increased penetration in such cities.

Market Share of Non-cooking Appliances (% volume).

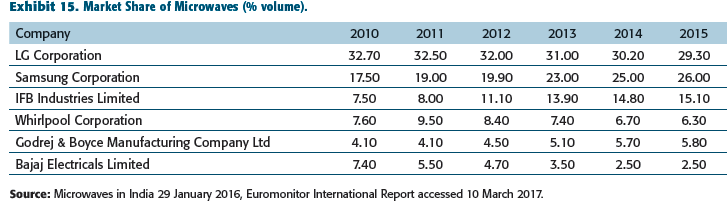

Microwaves

Market Share of Microwaves (% volume).

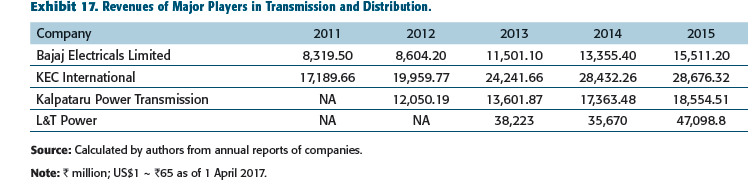

Engineering and Projects

Globally, the engineering & projects (E&P) industry was classified into power transmission and distribution (T&D) and infrastructure projects. Power generation, transmission and distribution were the three stages of the electricity supply chain, with power generation mostly under government control. The T&D segment comprised engineering design, procurement, fabrication, erection, installation, and commissioning power transmission lines and turnkey projects. These included manufacturing transmission line towers, substation structures, pre-fabricated structures, and illumination projects. BEL’s E&P business contributed ₹15.5 billion in 2015, with year-on-year growth in sales of 13.26% between 2010 and 2015. BEL entered the turnkey projects execution space in the 1960s with 20 people and provided lighting packages for power plants and industrial facilities. It had a turnover of ₹20 million. With a change in business portfolio, the division was named Engineering & Projects Division (EPD) in 2002 as emphasis shifted to design and execution of electrical projects with three divisions—High-mast and Street Lighting, Transmission Line Towers, and Special Projects. BEL was a small player in the T&D business compared to Kalpataru Power Transmission, KEC International, L&T Power, Tata Projects, and Jyoti Power Corporation, which had a combined market share of 60% in 2015. These firms had a wide product and service portfolio catering to domestic and international markets (Exhibits 16 and 17).

Profiles of Major Players in Engineering and Projects.

Revenues of Major Players in Transmission and Distribution.

BEL was the pioneer in propagating the High-mast concept in India. To counter the high import duty of around 70% for high-masts products, BEL started the Ranjangaon plant in 2000 with a capacity of 35,000 tons per annum as an import substitution method with in-house galvanizing and fabrication. Ranjangaon ranked among the top five integrated manufacturing facilities of its kind in the world. It had a 65% market share in high-mast products and had the distinction of illuminating the Wankhade stadium for the World Cup in 2011 (Bajaj Electricals, 2011).

The GOI identified the power sector as the key focus sector and had budgeted ₹1,000 billion (Sharma, 2016) in 2015. Additionally, country-level initiatives were launched by the government for the provision of electricity to 18,500 villages under the Deendayal Upadhyaya Gram Jyoti Yojana (DUGJY) to provide power to households. Around 70–80% of the revenues came from the government’s rural electrification projects, whereas the balance sales were from other projects. GOI had approved ₹980 billion for the Smart Cities Mission, which planned the development of 100 Smart Cities across the country in 2015. To leverage the opportunity, BEL started developing high-end lighting and smart solutions for the cities. However, since around 97%–98% of the orders in the E&P business were tender-based, with the lowest bidder winning the contract, margins tended to be low in this segment.

FUTURE STRATEGY

Bajaj wanted to decide whether or not to be in the businesses in which BEL was. He wanted to make BEL nimble and future-ready by offering superior-quality products at affordable prices in the B2C market. His long-term objective was based on the changing marketplace where the rural market was expected to expand. Given the rural demand, product availability and distribution would play a vital role to make an impact in India. Therefore, BEL, with its strong brand and sale service, required a really strong distribution network to ensure availability in every counter. To achieve that, Bajaj was planning to do something nobody else in the industry had either thought of or implemented. He planned to implement the FMCD model for small consumer durable products like small appliances and fans by making them available dealer to dealer, retailer to retailer on a regular weekly basis. He voiced his thoughts:

It will take another year and a half by which everything will stabilize, and we will be future-ready to take on competition because we already have the best service set up. We already have a brand which is very strong. Once we have a distribution network in place and the other area which we are looking at because that is something which is taken for granted but in India a lot of work has to be done is in the quality. We think there is still a lot of scope and still trying to improve quality so that the requirement of services goes down and to that extent we make much more over customer satisfaction and that is an attitude thing rather than cost. For improving quality, you do not need to increase your cost but it if you are having proper processes, the quality can improve. So, that is our objective. (The Economic Times, 2016)

Bajaj was optimistic about the FMCD distribution model, quality improvement, and putting the right processes in place. He wanted to discuss his plans in the next board meeting and solicit suggestions from the board members to take BEL to the next level and reassess the growth and profit potential of each of the businesses. Would this be sufficient to make the company future-ready to take on the competition?

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship, and/or publication of this article.

e-mail:

e-mail: