Abstract

The value of an idea lies in the using of it. —Thomas A. Edison

INTRODUCTION

Globally startups are considered nation-builders due to their contribution to the economy through multiple channels—employment, foreign capital, advanced technology, competitive products, technological innovations, wealth creation and equitable distribution. The contribution of intangible assets to a nation’s economic prosperity is presented in the OECD (2013) study, which argues that young firms with a large number of intangible assets have generated nearly 47% of all new jobs in OECD economies during 2001–2011.

Startups require capital for business setup, expanding operations, penetrating research and development spending. In addition, startups often need short to mid-term capital to supplement it during various funding stages. With limited tangible assets in their possession, startups find it difficult to succeed through the stringent credit appraisal process of commercial banks. They are forced to borrow at exorbitant rates from non-traditional lenders (Panda & Joy, 2019). The use of intellectual property rights (IPR) as collateral is an emerging business opportunity that may help capital-starved startups to fund their life and growth capital.

Today, India has a key position in knowledge capital development. Its knowledge economy continues to witness steady growth in recent years, aided by growing IPR awareness at the grassroots level and with innovations getting encouraged at schools, colleges, and universities. Being the third-largest startup hub and with increasing IP capital recognitions, India needs to utilize this unique position to be considered a knowledge and innovation-driven economy. The present study tries to identify the growth potential of the Indian economy based on these relatively unexplored growth agents, that is, IPR dominated startups. The structure of the study is as follows. The next section presents the emergence of startups and problems associated with their funding cycle. Subsequent sections cover the development of knowledge capital in India and reviews selective literature on IPR-based debt financing. The section that follows presents the institutional setup in India for IPR-based debt financing and suggests certain debt financing options that can possibly be explored by Indian banks. The last section outlines the constraints (including market imperfections) of IPR-based debt financing to startups in India, followed by a conclusion.

FINANCING VIABILITIES OF INDIAN STARTUPS

A startup is defined as ‘a newly emerged, fast-growing business that aims to meet a marketplace need by developing a viable business model around innovative product, service, process or a platform’ (Springboard, 2017). The startup landscape has been evolving in India. Both the central and the state governments are actively promoting the startup ecosystem by encouraging entrepreneurial activity, creating an enabling environment, implementing business supporting policies, capacity building through infrastructure creation and training, providing funding support and offering various tax incentives.

Currently, India is one of the important global startup destinations. As of July 2021, the Indian startup space was occupied by 53,435 companies recognized by the Department for Promotion of Industry and Internal Trade (DPIIT), Government of India. Going by the Indian Tech Startup Funding Report H1 2021 report (INC42 PLUS, 2021), in the first half of 2021, Indian startups raised ₹792.18 billion (USD 10.8 billion) in 614 funding rounds. With 56 Unicorns (startups valued over ₹73 billion (USD 1 billion), India is home to the 3rd largest unicorn community in the world. In H1 2021, 16 Indian startups acquired the unicorn status. India has nearly 300 incubators and accelerators managed by academic institutes, corporates, commercial banks, and government entities.

Despite this, it is disheartening that many startups are being shut down every year. According to the IBM Institute for Business Value and Oxford Economics (2017), despite India’s entrepreneurial strength, the startup economy still has not reached maturity. More than 90% of startups fail within the first five years of inception. Among the major roadblocks leading to the failure of startups, the lack of sufficient funding (65% opined this), lack of innovation (77%) and lack of skilled workforce (70%) were listed as major challenges.

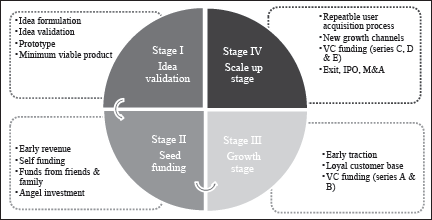

Given the four critical phases of the startup life cycle (Figure 1), the need for external capital arises mainly after completing the second phase. The financing aid at this stage supports the startup in surviving the most crucial stage, often termed as the ‘valley of death’.

INTELLECTUAL PROPERTY AND ITS DEVELOPMENT IN INDIA

United Nation’s World Intellectual Property Organization (WIPO) defines IP as

creations of the mind and covers inventions; literary and artistic works; and symbols, names and images used in commercial activities. IP is similar to any other property rights, where creators/owners of patents, trademarks or copyrighted works are benefitted from these works or investment in a creation (UN, 2011).

IP is divided into two major categories: industrial property and copyright. The industrial property includes patents (an exclusive right granted for a limited period for the invention of a product or process that provides a new way of doing something or offers a new technical solution to a problem), trademarks (a distinctive sign identifying certain goods or services produced or provided by an individual or a company), industrial designs (the aesthetic aspect of an article, where the owner is assured an exclusive right and protection against unauthorized imitation of the design by third parties), and geographical indications (a sign used on goods that have a specific geographical origin and possess qualities or a reputation due to the place of origin). Copyright is associated with literary works, films, music, artistic works and architectural design.

Development of Knowledge Capital in India

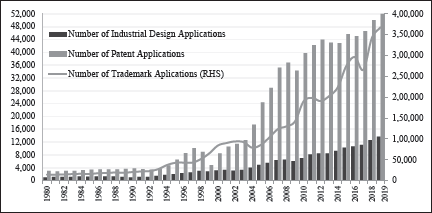

The role of IPR as an important factor for the success of the Indian startup ecosystem cannot be denied. A significant number of Indian startups own at least one IP asset (WIPO, 2020). India currently occupies the 5th position in trademark registration, 6th in patent registration and 11th in industrial design registration. Total patent applications in India have grown from 3,024 in 1980 to 53,627 in 2019, a compound annual growth rate (CAGR) of 7.7%, aided by increased IPR awareness across sectors and robust government policies. Similarly, the number of ‘industrial design’ registration have grown from 1,033 in 1980 to 13,723 in 2019, a CAGR of 6.9%. At the same time, trademark registrations reached 367,764 in 2019 from 14,397 in 1980 (Figure 2).

The possession of registered IPRs can offer an edge to the startup to compete effectively against large corporates. For example, an unpatented invention by the startups might be copied and marketed by larger rivals, effectively negating the startup’s effort. Today, Indian consumers are more aware, and without branding (a type of IPR), consumers are sceptical whether a product marked with a logo is genuine or not. Hence, startups are incentivized by applying for registering their niche ideas. On the other hand, the underdevelopment of the IPR market in India and certain bottlenecks have prompted many startups not to register. As India is now a knowledge-driven economy with significant growth in its research and development, the utilization of IPRs (intangible assets) as collaterals by startups can further accelerate the growth momentum.

LITERATURE REVIEW ON IPR-BACKED DEBT FINANCING

The world economy has undergone a spectacular change. It is now more of a knowledge economy, where knowledge/intangible assets remain the predominant form of economic assets, more valuable than tangible assets. The top five valuable companies of the world, that is, Apple, Microsoft, Amazon, Alphabet (Google), and Facebook, are mainly intangible asset dominated companies, with a market valuation of ₹150.8 trillion (USD 2,051 billion), ₹130.7 trillion (USD 1,778 billion), ₹114.5 trillion (USD 1,558 billion), ₹102.4 trillion (USD 1,393 billion), and ₹61.7 trillion (USD 839 billion), respectively as on 31 March 2021. As per the Global Intangible Finance Tracker 2020, physical assets account for only 4% of Amazon’s net worth, while the corresponding numbers were 6% for Apple, 7% for Microsoft, 16% for Facebook, and 26% for Alphabet. Brand Finance (2020) shows that more than 16% of the stock of patents in USA has been pledged as collateral at some point.

The pilot survey on the Indian startup sector by the Reserve Bank of India (RBI) from November 2018 to April 2019, covering 1,246 startups from public/private limited companies, partnership firms, limited liabilities partnerships and others, has portrayed the financing difficulties faced by Indian startups, as only 36% of the participating startups availed loans from institutions including banks. Families & friends emerged as the largest source of funding (43%) for Indian startups (RBI, 2019).

Khanna (2018) has discussed the issues and challenges in IP asset securitization in India. Risks related to uncertainty in the valuation of IP assets and the associated infringement litigations working against IP securitization are obstructing the growth of the market. In their study (2018), British Business Bank presented that firms with IP assets have lower default and loss rates than those without it.

Corrado et al. (2013), in their seminal study, have argued the role of intangible assets in increasing labour productivity. The study argued that during 1997 and 2005, intangible assets accounted for 23% of labour productivity growth in Europe and 32% in the USA. Debt financing for startups is important in countries where financial industries are in their infant stage. Amable et al. (2010) has presented the positive effect of IP-backed debt financing on firms’ innovation and growth. The use of patents as collateral increases the leverage effect of R&D, boosting the effect on innovation’s returns. While this resolves the issue of credit shortage, it encourages firms with promising technologies to grow. Hall and Lerner (2009) have reported that with startups being generally young with limited track records, lenders find them risky to finance due to scanty balance sheet information. Harhoff (2009) has argued that startups possessing IPRs signals better quality and attracts equity participation through venture capital (VC) funding even during a weak market sentiment.

SCOPE OF IPR-BASED DEBT FINANCING FOR INDIAN STARTUPS

In a knowledge economy, intangible assets are the predominant form of assets. Monetization of IPR is based on the logic of transforming the innovative idea into a financial asset where the underlined IPR is used as collateral in raising capital (Nithyananda, 2012). Usage of IPR and other intangible assets as security for debt financing is an old concept though not popularized. For instance, in the 1880s, Thomas Edison first used his patent on the light bulb as security to borrow the money needed to launch the General Electric Company. Apart from equity financing, some major economies, including the USA, Japan, Sweden, the UK, and few European countries, are the prominent leaders in IPR-based debt financing. The success of USA as a market for IPR debt financing is mainly because of the development of IPs as independent assets. Hence, IP valuation remains relatively easy, and they serve as collateral for debt finance. On the other hand, regulatory constraints and lack of supportive infrastructure in Japan does not support debt financing of IPRs, rather equity financing remains the popular concept in the country. IPRs being ‘embedded’ in business make it almost impossible to assess their value separately (Shimizu, 2017).

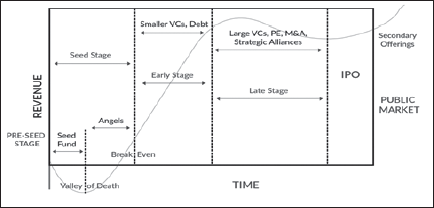

As of now, institutional and non-institutional investors, including friends & family, angel investors and VC play a pivotal role in providing life-supporting capital to Indian startups. VCs guide the startups to grow and ensure that startups provide noticeable returns in short to medium term. As defined by the Startup India Policy, depending on the stage of a startup, the investor types are classified as angel investors, early-stage investors and late-stage investors. An angel investor is an affluent person or a high net worth individual that provides initial capital to the startup at its infancy stage. Early-stage investors are the institutional investors who come in at the early growth stage when a product is ready and has been validated. Late-stage investors are the venture capitalists (VCs) or private equity firms investing in startups at the growth or late stage when the startup has reaped some revenues and gained market traction. A typical start-up financing life cycle is presented in Figure 3.

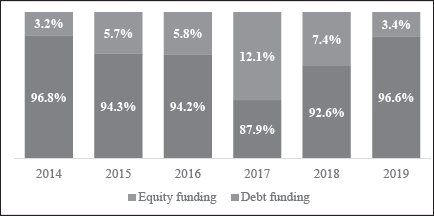

Equity financing is one of the most common funding channels for Indian startups. Most of the Indian banks (both private and public sector banks) have been financing startups through their VC arms which are predominantly equity financing in nature. The lack of preparedness of Indian banks to lend to startups (debt finance) has compelled the startups who require funding though not at the cost of diluting their stake, to look for alternative debt funding avenues. Unfortunately, in India, banks are not very keen on exploring new avenues of lending to startups based on knowledge capital, as most startups fail during the traditional credit appraisal models of banks. In 2018, only 7.4% of funding to startups were through the debt channel, which fell further to 3.4% in 2019 (Figure 4).

The underdevelopment of the domestic IPR-backed debt financing market is attributed to both demand and supply factors. On the demand side, many innovative businesses are not fully aware of IPRs and their associated benefits (Bennett, 2006). The policy bottleneck and lack of security mechanism in the IPR filing process discourage IPR registration by startups, while expensive IPR registration processes hinder market penetration (Verma, 2006). The startup promotion mechanism of South Korea, Singapore and China have aided in scaling up IPR registrations in these countries. Some of the incentives offered by those governments include financial support for registration, acquisition and research and development expenditure of IPRs, up to 80% discount on official fees and attorney fees, rewards for patent and utility model utilization and direct subsidies for patent filing, prosecution, and maintenance, etc., among others.

On the supply side, unlike niche lenders who are specialized in IPR financing, commercial banks in India lack IPR valuation expertise. With the valuation mechanism still nascent in India and the absence of a centralized valuation mechanism, lenders become risk-averse. Hence, the disincentives of accepting IPRs as collateral outweigh the incentives. Debt financing at competitive rates using IPRs as collateral remains a major concern for Indian startups. The IPR-based debt financing offers tremendous scope for Indian banks to expand their balance sheet. Building up the necessary valuation, and other infrastructure will address the market failure by creating a win-win situation for commercial banks and startups.

In recent years, venture debt has emerged as a preferred mode of investing in Indian startups. Venture debt funding is similar to a bank loan, which brings individual or VC investors a steady interest from the borrowing business along with a structured repayment plan. To compensate for the risk of business failure, interest rates are higher. Alteria Capital is one of the prominent players in India’s venture debt fund for startups. Today, more and more VCs are turning to debt rounds to help assess the long-term potential of a startup. The timing of the debt funding is more crucial as startups need to have the revenue to pay it back. Fintech, e-commerce, transport tech, consumer services, and health tech are some of the leading sectors receiving debt funding, at present.

Given the intense competition and less scope of interest income business, Indian banks are exploring every possible method to generate non-interest income to sustain and survive. In such a scenario, exploring this relatively new area of financing would tremendously boost the market confidence.

Alternative Business Models for IPR-backed Debt Finance

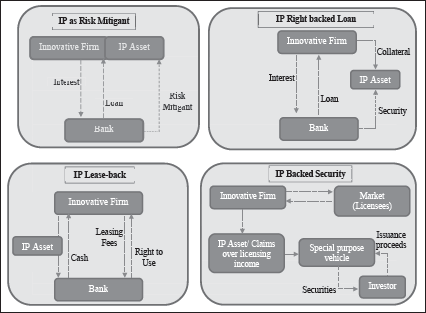

IP assets stand a good chance of being accepted as collateral for financing, conditional upon their liquidity and detachment from the individual/company’s business. IPRs may signal the investors about the quality of the management and may work as a safeguard in the later stages in case of financial distress. Some of the existing IPR-backed lending methods followed across geographies are explained as follows (Figure 5).

Proposed Lending Model Using IPRs as Collateral

As IPR-based debt financing is one of the less popularized business models, very few niche lenders around the globe are specialized in IPR-collateralized debt. Due to the absence of specialized lenders in countries like India, traditional commercial banks venture into this specialized business. The conventional asset-backed loans model assures the lenders of the tangible assets in credit appraisal. By arrangement, the loanee grants a security interest in the asset to the lender as collateral against the loan. The same mechanism works for IPR-backed loans where the loanee borrows a percentage of the value of its IP asset by using these assets as collaterals.

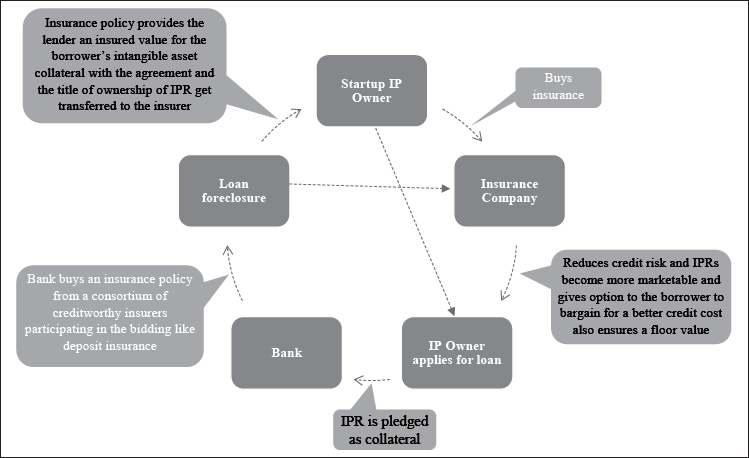

To enhance the value of IPR collateral, the owners of IPRs use-value enhancement instruments like insurance on the value of the IPR for a specific period. The lender could buy an insurance policy from a consortium of creditworthy insurers participating in the bidding. The insurance policy provides the lender with an insured value for the borrower’s intangible asset collateral with the agreement that the title of ownership gets transferred to the insurer in case the borrower’s loan goes into foreclosure.

However, it is proposed that a provision be made that the lender may not be obligated to sell the insured intangible assets to the insurer. The lender will always be guaranteed to get no less than the insured value while maintaining any upside should the assets be worth more than the insured value.

Proposed IPR-backed Debt Finance Model.

Thus, these instruments ultimately reduce credit risk, and IPRs become more marketable and gives an option to the borrower to bargain for a better credit cost. By guaranteeing the valuation of IPR, the value enhancer instrument makes it easier for companies to use IPR as collateral for borrowings. It provides the lender and regulators with a creditworthy floor value to determine lendable IPR advance rates. The proposed IPR-based lending model is presented in Figure 6.

CONSTRAINTS IN IPR-BASED DEBT FINANCING IN INDIA

Some of the constraints with the development of IP-based debt financing in India include:

Impact of Asymmetric Information and Moral Hazard

Asymmetric information arises if the IP owner has more information on the quality and marketability of his/her IP asset. Being a ‘lemons market’, the lender finds it challenging to segregate good and bad IPs and demands a premium to compensate for financing a bad IP asset. Similarly, the conflicting interests of lenders and owners intensify the moral hazard problem. Sometimes, the entrepreneur wishes to continue a project as they are confident about the business model and prefer to invest for a longer duration. In contrast, the financer may prefer to terminate the project and exit. This results in possible delays in investment decisions. The market failure and imperfections are peculiar and are connected to the debt financing of innovation.

The IP assets are predominantly in the form of knowledge capital. Therefore it is difficult to appropriate for the financier in the event of distress. A significant chunk of the expenditure of intangible asset owned startups are on innovation and R&D activities. As the output is in the form of an intangible asset, which, unless codified, is only embedded in the human capital of the firm’s employees, lenders find it difficult to exit midway. The IP asset owned startups are generally at high risk at their inception. Most of the time they fail to bring about a successful innovative product due to competition and other market factors. The higher risk levels require more significant risk premiums and periodic re-assessment of investment decisions by the financier during the project lifetime. Thus, market failure due to associated moral hazards and asymmetric information leads to uncompetitive interest rates, lack of external funding and limited options to use IPRs as collateral.

Institutional Mechanism for IPR-based Financing in India

Given the importance of startups to the domestic economy, the Government of India has initiated many schemes to promote them. India’s first IPR policy in May 2016 (GoI, 2016) has proposed securitization of innovation rights, allowing them to be used as collateral to raise funds for their commercial development. The policy highlights the financial support for developing IP assets through banks, VC, angel funds and crowdfunding mechanisms. The IPR policy aims at promoting a holistic and conducive ecosystem to catalyse the full potential of knowledge capital for India’s economic growth and socio-cultural development. The Indian IPR policy complies with World Trade Organisation’s agreement on TRIPS (Trade-Related Aspects of IPRs).

Start-up India initiative is a favourable step towards the development of IPR-based firms by improving their access to finance. Additionally, the startups action plan of the government has also proposed for establishment of a panel of facilitators to help file patent and IP applications and raise finance for further innovation and research. The IPR policy strongly believes in creating public awareness of the socio-economic and cultural contributions of IPRs.

The Indian banking system has already made provisions for the acceptance of intangibles as collaterals. Section 2(1)(t) of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI) defines the expression property, and it specifically includes intangible assets being knowhow, trademark, copyright, licence or franchise. Further, Section 2(1)(zf) defines ‘security interest’ as a right, title or interest of any kind upon property created in favour of the secured creditor and includes such rights as title or interest in intangible assets. The associated security interests that are created over property rights in favour of the lender are the transfer of interest or rights in the property. In the event of default in repayment of loans secured by the security interest, lenders have the right to sell the property and realize their defaulted loans. The same principles are applicable in respect of intangible property rights such as trademarks, copyrights, or patents and are clearly aimed at enabling the creation of security rights over intangible properties for facilitating credit to the IP owners and rights holders, thereby enhancing the value of the IPRs as security for credit.

In India, the Federation of Indian Chambers of Commerce and Industry (FICCI) and the Federation of Micro, Small and Medium Enterprises (FISME) drive the commercial activity in IPR. FICCI, in association with the Ministry of Micro, Small and Medium Enterprises (MSME) has established the Intellectual Property Rights Facilitation Centre (IPFC), aiming at promoting awareness and adoption of IPRs amongst small entrepreneurs and startups. Recognizing the growing contribution of IPR to member organizations, FISME has initiated several programmes with assistance from the national manufacturing competitiveness programme under the Ministry of MSME. FISME has been focusing on IPR valuation and the creation of a mechanism to sell the IPR and realize the value. To promote debt financing of IPRs, the government needs to robust the IPR market infrastructure.

CONCLUSION

The potential of startups in driving India to a ₹370 trillion (USD 5 trillion) economy by FY 2024–2025 cannot be understated. The role of intangible assets has gained prominence, with knowledge-intensive innovation activities becoming the central drivers of competitive advantage in the modern world. Intangible assets currently account more towards a firm’s market value than tangible assets. In advanced economies, IPR is treated as an asset and a substantial part of the company’s portfolio. This practice is not extensively prevalent in emerging and developing economies, particularly in India, because of the relatively insufficient IPR related infrastructure. Imperfections in the capital market restrain the pace of knowledge-driven growth in India by financially constraining young and innovative firms, which are the key drivers of economic growth.

As startups usually do not own enough tangible assets for use as collateral, debt financing for startups has not been widely adopted. This results in startups and fund providers remaining dependent on equity financing. With innovative firms being relatively young and having limited track records, they remain risky prospects for lenders.

Collateralizing commercial loans and bank financing by granting a security interest in IP is a growing practice in advanced economies. With the unique position of the Indian economy, as the third-largest startup hub globally and increased recognition of IP assets as growth engines, India needs to utilize its potential to accelerate inclusive growth. Startups and—innovation-driven enterprises are scaling up in the domestic economy. They require increased access to capital and market to monetize their IPR for business growth and expansion.

Debt financing to startups at present is mainly funded by VCs. IPR-based debt financing is an untapped source of financing for startups in India. As an untouched area till date, it offers tremendous scope for Indian banks to expand their balance sheet. As IPR-based debt financing requires a number of essential infrastructures, including creation, maintenance and proper valuation of IPRs, India needs to strengthen its IP valuation and protection mechanism. The role of the policy support for the smooth functioning of IP-based debt financing has become more urgent post-COVID-19 pandemic as the Indian startup sector has been severely affected by the pandemic.

The NASSCOM survey (2020) found that nearly 40% of startups have either temporarily shut down or are on the verge of closing and 70% of startups have less than three months of cash runway. Though lately, the RBI has realized the financial constraints faced by the startups and has assigned priority sector lending (PSL) status to India’s startup sector (RBI, 2020), which may offer some relief to small startups and enable access to bank credit for their working capital support.

Footnotes

Declaration of Conflicting Interests

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.