Abstract

Executive Summary

The provision of non-audit services (NAS) by an incumbent auditor has remained a highly contentious issue. One school argues that the joint provision does not impair an auditor’s independence. Instead, it reduces total costs, enhances the ability to detect material misstatements, increases technical competence due to knowledge spillovers and leads to intense competition. However, a substantial tranche of an audit firms’ income is derived from NAS, and the joint provision increases economic ties with the client. Therefore, another school of thought perceives that the joint provision impairs auditor independence. It is also alleged that auditors expect non-audit work after finishing the auditing job. Their independence is also affected by the risks of self-review. Extant literature reveals that the majority of the studies on the issue are archival and experimental. The studies are concentrated in the US, UK, Australia, Malaysia, Nigeria, South Africa, China, and some of the European Union Nations. The article examines the perspective of chartered accountants (CAs) on the joint provision of NAS in India. The study samples 119 CAs. The reliability of the survey result was measured using Cronbach’s α, and a score of 0.77 indicated acceptable internal consistency reliability. The data were analysed using Wilcoxon signed-rank test and the Mann Whitney U test statistic. The summary of their suggestions for ensuring auditor independence is presented separately. The findings reflect that existing prohibitions imposed by the Companies Act, 2013, are not enough to ensure auditor independence, and the Management Services u/s 144 of the Act needs to be clearly defined. Practitioners do not support the proposition that joint provision should end and a separate category of professionals be mandated to render NAS. However, the recommendations include strengthening provisions to reduce the conflict of interest.

Keywords

INTRODUCTION

The provision of NAS by an incumbent auditor to audit clients has remained a highly contentious issue (Simunic, 1984). Meuwissen and Quick (2019) argue that even though joint provision enhances the auditor’s ability to detect material misstatements, it does not assure independence. A substantial tranche of audit firms’ income is derived from NAS, and therefore the possibility of impaired independence cannot be ruled out (Peel & O’Donnell, 1995). The joint provision increases economic ties with the client (Frankel et al., 2002) and intensifies the possibility of earnings management (Ferguson et al., 2004). Auditor independence is affected by the risks of self-interest, self-review, advocacy, familiarity or trust, and intimidation (European Commission, 2002). Impaired independence of a company auditor not only erodes stakeholder’s confidence in the company’s financial health but also poses a serious threat to the audit firm’s reputation. Due to impaired independence, the audit firm may lose prospective clients. Further, the client also becomes vulnerable and may lose the trust of present and prospective investors (Securities and Exchange Commission, 2001). Hence, auditor independence is relevant both from the perspective of the audit firm and the client.

The significant rise in NAS fee income of the auditing firms and domination of the big four have further exacerbated auditor independence (Quick & Warming-Rasmussen, 2005). It has been a concern in many countries, including the UK, Australia, etc. (Hay, 2017). To avoid conflict of interest UK’s regulatory authorities have issued directives that the big four should separate their audit practices from NAS operations by June 2024 (Peccarelli, 2020). On the contrary, large auditing firms generally disagree that the joint provision of NAS to audit clients impairs auditor independence. They argue that there is a special clientele base that consists of multi-national corporations (MNCs). Audit firms need scale, significant size and a handy team of experts in the audit team to meet their global demands and handle complex issues beyond accountancy. Big four opine that they make huge investments in artificial intelligence, big data analysis, and machine learning to match the size and scale of operations of these MNCs. Thus, the breakup of the big four might not offer a sustainable solution and would rather hurt the audit quality (Ellis, 2018).

However, NAS providers favour the split as their consultancy business is blooming with escalating mergers and acquisitions of companies. Post-split, the market may witness a hike in the audit fee, which is worth it, as the audit quality is also expected to improve. The NAS market is more competitive as the client has the prerogative of choosing other accounting firms and general business consulting firms over auditors (Zerni, 2012). A decline in NAS fees can be anticipated due to increased competition. Again, the consultancy firms would be free from controversies that often erupt because of their dual role as auditor and the consultant (Jonathan, 2018).

Auditor’s independence is ensured by objectivity, integrity, and impartiality in their conduct (Wines, 2012). However, their most significant professional asset independence has become questionable for their alleged involvement in the biggest frauds and corporate collapses of the 21st century, including Enron, AIG, Worldcom, etc. (Cahan et al., 2008). The year 2018 is marked by the failure of the big four in unearthing the scandals at the British outsourcing firm Carillion, the world’s most valuable bank Wells Fargo, unexpected insurance liabilities in General Electric, and accounting irregularities at Steinhoff International (Crooks, 2018; The Financial Times, 2018).

Because of deteriorating audit quality and to ensure auditor’s independence, Sarbanes-Oxley Act, 2002, was passed in the US. Section 201 of the Act prohibits public accounting firms from rendering certain NAS to their audit clients. Subsequently, Australia also enacted Corporate Law Economic Reform Program (Audit Reform and Corporate Disclosure) Act, 2004 (Crockett & Ali, 2015). European Union (EU) in 2014 brought reforms prohibiting the provision of certain NAS to public interest entities and capped the fees for the permitted NAS (European Parliament and of the Council, 2014).

MOTIVATION AND CONTRIBUTION OF THE STUDY

The rudimentary motivation for the study comes from the concern that auditor independence becomes questionable due to the provision of NAS to audit clients. NAS to audit clients is often positively associated with loss of public confidence (Onulaka et al., 2019). Management’s control over the appointment and remuneration of auditors has also been questioned (Tang et al., 2017). Questionable integrity of the auditors will have a pervasive impact and may cause serious damages to the reputation of the client and the auditor. Hence, the study of auditor’s independence due to the joint provision becomes vital.

The extant researches reveal that beginning with the pivotal work by Simunic (1984), the studies on the issue of NAS and auditor independence include (a) reviews (Francis, 2006; Francis et al., 2004; Hay, 2017; Tepalagul & Lin, 2015), including meta-analysis (Habib, 2012); (b) archival research (Abdul et al., 2020; Ashbaugh et al., 2003; Beardsley et al., 2021; Ezzamel et al., 1996; Frankel et al., 2002; Lim & Tan, 2008; Wahab et al., 2013; Wahab & Zain, 2013; Whisenant et al., 2003) including capital market reaction studies (Chaney & Philipich, 2002); (c) experimental studies (Aschauer & Quick, 2018; Causholli et al., 2014; Friedman & Mahieux, 2021; Meuwissen & Quick, 2019; Tang et al., 2017); and (d) survey research (Akinbowale & Babatunde, 2017; Harber & Maroun, 2020; Onulaka et al., 2019; Quick & Warming-Rasmussen, 2005 ). The majority of the studies are archival and experimental, limiting the ability to critique the existing regulations (Harber & Maroun, 2020). To find a sustainable solution, engagement with key stakeholders is vital. This study is an attempt to fill the gap in empirical research by presenting the practitioners’ perspectives.

Further, most of the studies are concentrated in the US (Ashbaugh et al., 2003; Davis et al., 1993; Mishra et al., 2005; Whisenant et al., 2003), UK (Ezzamel et al., 1996; Ferguson et al., 2004), Australia (Butterworth & Houghton, 1995; Craswell, 1999; Lee et al., 2009), Malaysia (Abdul et al., 2020; Ahmad et al., 2006; Wahab et al., 2013), Nigeria (Onulaka et al., 2019), South Africa (Harber & Maroun, 2020), China (Tang et al., 2017) and some of the EU Nations (Aschauer & Quick, 2018; Meuwissen & Quick, 2019; Quick et al., 2013; Quick & Warming-Rasmussen, 2005), etc. Very few studies have been carried out to present the Indian perspective. The study has implications for the ongoing debate on regulating the provision of NAS to audit clients. It will enable the policymakers to re-evaluate the existing provisional norms on NAS to audit clients in India.

LITERATURE REVIEW

Provision of NAS to Audit Clients: The Two Schools of Thoughts

Auditors are motivated to maintain their independence to avoid the risk of damage to reputation and litigation (Zhang & Emanuel, 2008). One school of thought argues that provision of NAS to the audit clients do not harm auditor’s independence instead reduces total costs, increases technical competence due to knowledge spillovers, and motivates more intense competition (Antle et al., 2006; Arruñada, 1999; DeFond et al., 2002; Krishnan & Yu, 2011; Lim & Tan, 2008; Svanström & Sundgren, 2012). High fees for NAS do not affect the audit quality (Ashbaugh et al., 2003; Carmona et al., 2015; Huang et al., 2007). Studies in the US, Germany, Spain, New Zealand, Bangladesh, etc., do not support the argument that NAS to audit clients impairs auditor’s independence (Alexander & Hay, 2013; Bloomfield & Shackman, 2008; Dunmore & Shao, 2006; Garcia-Blandon et al., 2017; Habib & Islam, 2007; Kohler & Ratzinger-Sakel, 2012; Quick et al., 2013; Walker & Hay, 2013). Unconditional restriction on joint provision ergo does not seem necessary (Kang et al., 2019).

Contradictorily, another school argues that NAS by audit firms is a threat to auditor’s independence (Antle, 1984; Government Accountability Office, 2003). The knowledge spillovers argument is highly debatable, and empirical results investigating the same are mixed (Zhang & Myrteza, 1996). Studies revealed that companies that pay higher fees for NAS rarely receive a qualified audit report (Ahadiat, 2011; Beattie et al., 1999). Further, the anticipation of securing non-audit work from the audit client may impair auditor independence (Causholli et al., 2015). Again, the auditors who render both audit and NAS to the same client certify their work. For instance, Deloitte Canada was fined for auditing its work (Cohn, 2018). A study on a sample of 504 audit clients, who also availed NAS from Arthur Andersen, supported the prohibitions imposed by Sarbanes-Oxley Act, 2002 (Lee, 2005).

Existing Regulatory Norms for Joint Provision of NAS to Audit Clients in India

Chartered Accountants (CAs) have requisite professional knowledge and technical skills and can render audit services. They have the largest market share in terms of NAS. The present regulations highlight the following facts about the rendering of NAS by CAs in India:

The Ethical Standards Board of the Institute of Chartered Accountants of India (ICAI) provides that an auditor in the same financial year cannot be the statutory auditor and stock auditor of a bank or any branch or a sister concern of the bank (The Institute of Chartered Accountants of India, 2021). However, the regulation does not restrict the auditor to undertake the job of stock audit in a subsequent financial year. In India, CAs in practice can accept professional investigation assignments from Insurance Companies (The Institute of Chartered Accountants of India, n.d.), which is not the usual practice in several countries. CAs can render the NAS approved by the Council of ICAI. A statutory auditor can render NAS to the audit client with restrictions on the remuneration to be charged (applicable only to a certain class of companies) (The Chartered Accountants Act, 1949). The remuneration charged for carrying out the Management Consultancy and all other professional services by the statutory auditor cannot exceed the fee charged for statutory audit. As per the Code of Ethics (2009) issued by the ICAI, an auditor can render 26 management consultancy and other services (The Institute of Chartered Accountants of India, 2009). As per the Companies Act of 2013, auditing firms are prohibited from rendering eight types of NAS. Management services are one of them. However, the Act has not defined the management services. The Committee of Experts constituted by the Government of India (GOI) for looking into the regulatory and other issues related to multi-national accounting firms has recommended expanding the list of prohibited NAS as per the Companies Act, 2013. It also recommends that the NAS fees be lowered for clients such that it should not be more than 50% of the audit fee (Agarwal et al., 2018).

Thus, the GOI has recognized the issue of auditor independence. The measures, even if not watertight, are indicative of the steps undertaken to ensure auditor independence in the context of the joint provision. The success of the measures lies in their proper implementation by the CAs in their work field.

OBJECTIVE

The present study is divided into two sections. Section I examines the issue of auditors’ independence in view of the joint provision of audit and NAS by auditors/audit firms in the Indian context. Section II attempts to present the summary of suggestions given by the practitioners to ensure auditors’ independence.

RESEARCH METHOD

Questions were framed after reviewing the existing literature. Strategically the study aimed at eliciting practitioners’ that is, CAs perspective.

The link of the pre-tested questionnaire (google form) was shared with the CAs enlisted as faculties in the Directorate of Continuing Professional Education of ICAI. The respondents were also requested to provide email IDs of some other CAs who may also be contacted for collecting responses.

The survey limited the number of questions to encourage a higher response rate. The other efforts to improve the response rate included-explicit statement of the research objective, a declaration regarding the pure academic nature of the study, assurance regarding confidentiality of individual responses, and an offer to share the survey results on request.

The first few questions pertained to the respondent’s demographic characteristics such as name (optional), age, gender, highest educational qualification. The questionnaire carried eight questions designed on a five-point Likert scale. Statements 1, 2, 3 and 8 argued that joint provision of NAS does not impair auditors’ independence. The respondents were advised to mark 1 for strongly disagree, 2 for disagree, 3 for neither agree nor disagree, 4 for agree and 5 for strongly agree. Whereas statements 4, 5, 6 and 7 argued that the joint provision of NAS impairs auditor independence. Accordingly, the respondents were advised to mark 1 for strongly agree, 3 for neither agree nor disagree, and 5 for strongly disagree.

The reliability of the survey result for the eight statements was measured using Cronbach’s α, and a score of 0.77 indicated acceptable internal consistency reliability.

FINDINGS

Section I

Descriptive Statistics

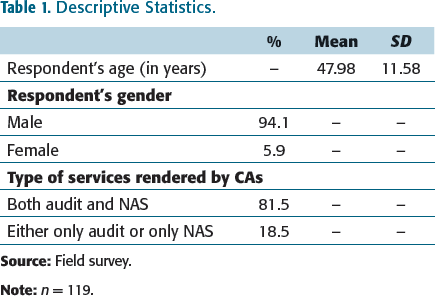

The information in Table 1 relates to the demographic characteristics of the respondents incorporating their age, gender and types of services rendered by them.

Descriptive Statistics.

Inferential Statistics

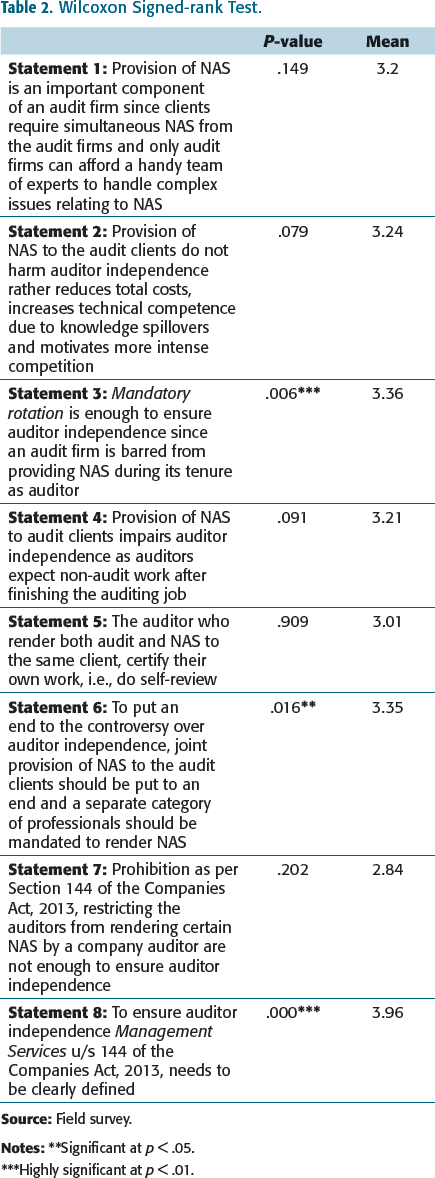

Wilcoxon Signed-rank Test.

***Highly significant at p < .01.

The result of the Wilcoxon signed-rank test makes it evident that respondents agree with statement 3 that Mandatory rotation is enough to ensure auditor independence since an audit firm is barred from providing certain NAS during its tenure as an auditor (mean 3.36). However, the results do not conform to earlier findings which indicate that mandatory rotation does not ensure auditor independence (Aschauer & Quick, 2018; Velte & Freidank, 2015).

The comparison of the ICAI Act and its different rules, laws, and the Companies Act, 2013, brought into light the paradox regarding the management services and the prevalent discretionary powers of the Board and the Audit Committee in India. If the Audit Committee approves any one of the 26 management services (as defined by the Code of Ethics) to be rendered by the auditors to the company, then legally Section 144 of the Companies Act, 2013, cannot debar the auditors from rendering such services. The respondents agree that to ensure auditor independence, Management Services u/s 144 of the Companies Act, 2013, needs to be clearly defined (mean 3.96) (statement number 8).

For the big four, the non-audit section is much more lucrative as they audit 97% of FTSE 350 companies in the UK. The dominance of the big four as audit and NAS providers and the repeated audit scandals raised serious concerns over the profitable oligopoly and sinister conflict of interests of the audit firms. It has, therefore, fuelled the debate over splitting up of the big four (Crooks, 2018; Plender, 2018; Plimmer, 2018; The Financial Times, 2018). Empirical evidence from Indian firms also revealed that auditors tend to charge an audit fee premium in the case of joint provision (Bhattacharya & Banerjee, 2020). In the present study, the respondents were asked whether to put an end to the controversy over auditor independence, joint provision of NAS to the audit clients should be barred, and, in its place, a separate category of professionals should be mandated to render NAS (statement number 6). The mean score of 3.35 indicates that they disagree with the statement.

Self-review threatens the perceived independence of auditors (Quick & Warming-Rasmussen, 2009). However, most of the respondents neither agree nor disagree with the 5th statement (mean score 3.01). Being ambivalent to this statement proves that it is a grey area for ensuring auditor independence (Table 2).

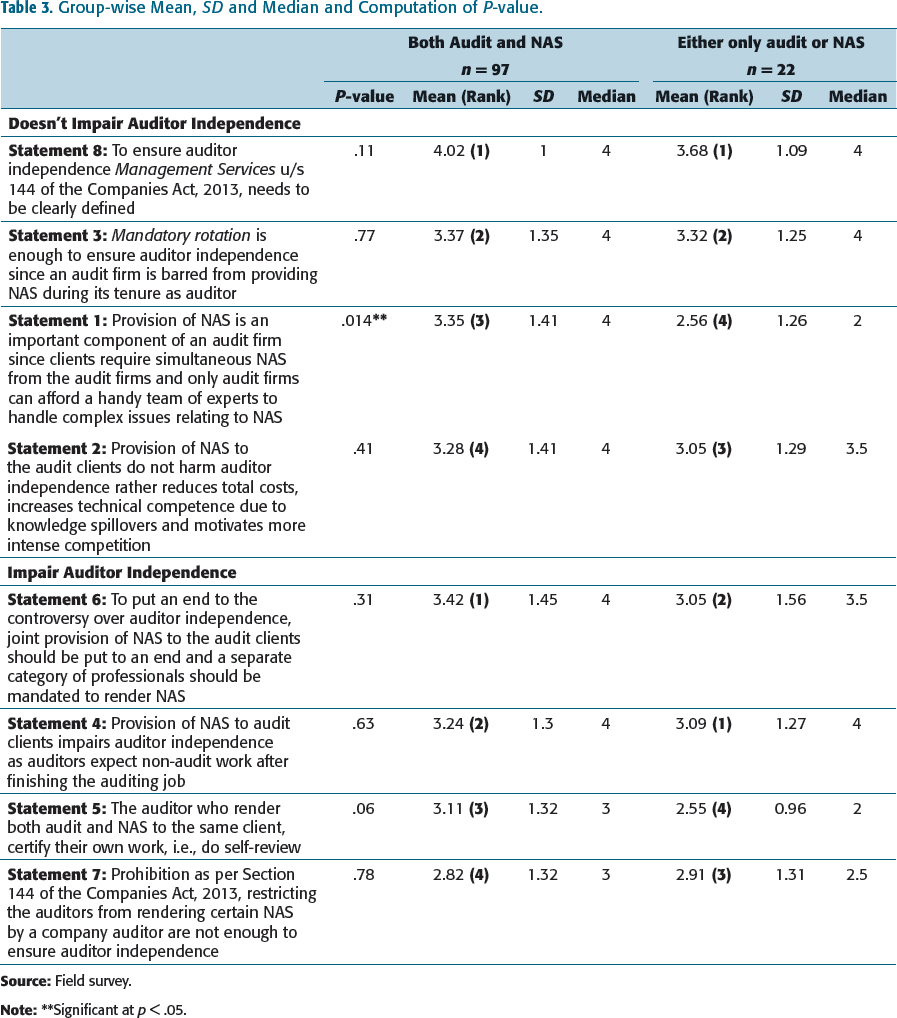

Table 3 highlights the result of the Mann Whitney U test that was carried out to test the formulated hypotheses. Table 3 also depicts the group-wise Mean, SD and Median of the responses.

Group-wise Mean, SD and Median and Computation of P-value.

Mann Whitney U test was further conducted to identify whether there was any difference between the groups relating to each of the eight statements. Statement number 1 depicts a significant difference (z = –2.453, p < .05) between the two groups. The mean score and median value for statement number 1 are 2.56 and 2, respectively, for the group who had provided either of the services. The mean score was 3.35 and 4 for the group who have rendered both. Thus, CAs rendering either audit or NAS disagree with the statement that provision of NAS is an important component of an audit firm since clients require simultaneous audit and NAS from the audit firms, and only audit firms can afford a handy team of experts to handle complex issues relating to NAS.

The majority of the respondents in both the groups agreed to statement number 8 that management services u/s 144 of the Companies Act, 2013, must be clearly defined. Considering the mean score and median value of the other statements, it has been substantiated that there is no significant difference between the two groups, which is also reflected by the p-values (p > 0.05) (Table 3).

Section II

Regulatory Suggestions for Ensuring Auditor Independence

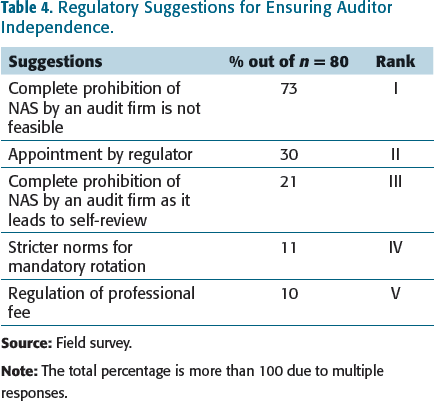

Regulatory Suggestions for Ensuring Auditor Independence.

Complete Prohibition of NAS by an Audit Firm Is Not Feasible

The majority of the respondents that is, 73 per cent, suggested that complete prohibition of NAS by an audit firm is not feasible. Extant literature also reveals that NAS is an economic necessity for the survival and growth of audit firms (Kang et al., 2019; Onulaka et al., 2019; Wahab & Zain, 2013). As audit services are periodic, the provision of NAS enables the audit firm to level out seasonal variation in demand and ensures a constant flow of revenue throughout the year (Quick & Warming-Rasmussen, 2005). The respondents also highlighted that the clients expect all services under one roof as it reduces their cost and is convenient. Hence, the complete prohibition of NAS is not feasible. These views correspond to the study by DeAngelo (1981) that joint provision reduces consulting risk, transaction costs and enhances confidence in the quality of NAS. Further, Lee et al. (2009) and Knechel and Sharma (2012) also stated that clients often prefer NAS from auditors as it increases auditor learning and facilitates avoidance of audit delays.

The respondents opined that too many regulations hamper auditing jobs, and regulations alone cannot guarantee independence. Firms with vested interests will always interpret laws as it suits them. The most important reason cited was that independence is a state of mind. It is a self-driven ethical decision. Audit firms should adopt a culture that maintains norms and standards to ensure independence. Firms need to provide either audit or NAS to a client/group of companies/related parties. The respondents opined that the audit firm should be allowed to render NAS to small and mid-sized clients. This will reduce the cost of compliance and ease doing business. Regulators need to be more vigilant with stricter norms to regulate the big four and network firms that cater to the large corporations.

Appointment by Regulator

Around 30% of the respondents suggested that the appointment of an auditor should be made by an independent body or regulator such as the Ministry of Corporate Affairs/ICAI/Comptroller and Auditor General of India/Securities and Exchange Board of India/National Financial Reporting Authority/Registrar of Companies. These views correspond to Tang et al. (2017) study, which states that auditors appointed by the regulator experience less pressure from the client and perceive themselves to be more independent. It should be mandatory for at least those entities where public money/interest is involved. Again, a joint audit can be made mandatory in case of companies above a certain threshold and where public money/interest are involved. Further, for periodical reviews of audit firms, an independent body should be established. One pertinent response in this regard is quoted below:

periodical evaluation of quality and capacity of the auditor should be made mandatory. Every year shops license is renewed, the pollution control board renews the license periodically, and so many permits are renewed. Since the quality of audit is impacting national savings, investments, production, demand–supply, prices, GDP, public trust hence these auditors permit need to be renewed based on the updated skill sets.

Complete Prohibition of NAS by an Audit Firm as It Leads To Self-review

Around 21% of the respondents suggested complete prohibition of NAS by an audit firm (with the same set of partners) as it leads to self–reviewing and impairs their independence. Auditors tend to misdefine their non-audit proposals and documents which they subsequently audit. This includes the use of affiliate companies which are shown as independent but managed jointly with profit and loss sharing. Again, the higher the level of NAS; the greater is the perceived risk that the auditor acquiesces to client pressure (Firth, 1997; Frankel et al., 2002; Securities and Exchange Commission, 2001). One of the respondents cited:

An auditor, audit firm or its associates being a ‘watch dog’ must be kept out of non-audit or management services. It must be made clear that an audit firm must not engage itself with the auditee in any other mode or method. Primarily, one must understand the risks associated with audit services and NAS; only then can a clear conclusion be drawn. If both the services are rendered by the same audit firm there would be, to some extent ‘conflict of interest’. It is something like putting parents on an interview panel when their child is appearing for the interview/test.

Stricter Norms for Mandatory Rotation

Due to anecdotal experience of nexus between long audit tenures and high-profile corporate failures, several studies suggest that mandatory rotation enhances auditor independence (Aschauer & Quick, 2018; Ball et al., 2015; Tepalagul & Lin, 2015). The audit partner rotation has been mandated in several countries, including India. However, a re-examination of the provisions for mandatory rotation is suggested by 11% of the respondents. They opine that many firms circumvent the spirit of regulation. They start a new firm with managers, etc., as partners and rotate audits among themselves. One of the relevant responses in this regard is quoted below:

Auditor rotation is a ‘managed activity’ in several companies. The independence of audit is largely impacted by the ‘tone at the top’ of the respective entity. While it is true that certain amendments to the Companies Act have had an impact, the crux of the matter is that other stakeholders to an entity like banks, creditors, Government, taxmen have also to conduct insightful due diligence on the entity concerning their mandate. Fixing responsibility solely on statutory audit reports/disclosures may not be a panacea for all the issues in a dynamic ecosystem.

Regulation of Professional Fee

Around 10% of the respondents suggest that audit and NAS fees must be standardized. It should be routed through a nodal agency. Also, reasonable allocation of work amongst auditors should be ensured. Presently, most of the work is concentrated amongst large firms. Two of the most relevant suggestions are quoted below:

Non-audit fees should be capped as a percentage of the audit fees-say 100%. the variation in audit fees should be explained by the auditors and that will ensure that all incremental fees are on account of approved non-audit services.

These suggestions are significant given the earlier findings that audit and non-audit fees are directly related (Butterworth & Houghton, 1995); both have a significant association (Bell et al., 2001) and are jointly determined (Whisenant et al., 2003).

CONCLUSION

The study examines the issue of auditor independence considering the provision of NAS to audit clients. The results are based on practitioners’ perspectives gleaned through an online survey. The findings reveal that the existing legislative regime is ambiguous and bestows discretionary powers upon the management. The prohibitions imposed by the ICAI and the Companies Act, 2013, are not enough to ensure auditor independence. Further, Management Services u/s 144 of the Companies Act, 2013, needs to be clearly defined, and the norms for mandatory rotation should be strengthened.

The study concludes that the joint provision of NAS does not impair auditor independence, and complete prohibition of NAS by an audit firm is not feasible. However, policymakers should make efforts to reduce conflict of interest. Self-review must be duly addressed. Appointment of the auditor should be made by an external agency/regulator. The enunciated suggestions of the practitioners should interest the stakeholders for ensuring better regulation and policymaking. The regulatory suggestions augmented by practitioners can contribute ensuring greater transparency and better corporate governance. The suggestions are significant for enhancing the credibility of the audited statements, which is critical for ensuring stakeholders protection.

LIMITATIONS AND FUTURE SCOPE

The scope of the study limits itself to the CAs perspective only. Hence, it is not free from limitations. It leaves scope for further research to elicit the views of other stakeholders such as shareholders, academicians, bankers (Bakar et al., 2005), auditee and lawyers (the most significant competitors of auditors for NAS).

Footnotes

ACKNOWLEDGEMENT

The authors would like to express sincere gratitude to Dr Hemanta Saikia, Assistant Professor of Statistics, Assam Agricultural University, Jorhat, Assam, for his valuable inputs in statistical analysis.

Declaration of Conflicting Interests

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.