Abstract

This study provides strategic insights and a business model perspective on health insurance as a vehicle for financing healthcare. It uses both primary (expert interview) and secondary data to investigate the overall disease burden and healthcare industry trends and track healthcare financing through the health insurance mechanism in India. To identify the critical success factors and to gain a business model perspective within the health insurance industry, telephonic and face-to-face interviews were held with 27 experts in the healthcare, insurance, and strategic management field. The study’s findings suggest that the growth of health insurance as a healthcare financing mechanism in India has been challenged continuously and impacted by multiple changes in the health insurance and healthcare industry over the last decade. One of the critical challenges faced by insurance companies is the high incurred claim ratio. We find the Indian health insurance industry to be very competitive and that the focus on critical success factors can help insurance companies gain a competitive advantage. The health insurance business model is unique, with varying configurations, and broadly comprises strategic choices and consequences. In this article, drawing from the strategic management literature on the resource-based view (RBV) and insights gained from the interviews of healthcare and health insurance experts, we highlight the six critical success factors relevant for competing in the health insurance business. We also list five strategic choices that can help health insurance companies improve their profitability and gain a sustained competitive advantage. We recommend that the insurance companies design and develop an innovative business model centred around lowering the claim ratio and simultaneously increasing the customer willingness to pay. To increase the customer willingness to pay and reduce the claim ratio, the insurance companies should focus on the six critical success factors and invest in the five strategic choices.

Keywords

INTRODUCTION

The urgent call for a sustainable health system, characterized by the delivery of high-quality care while keeping the cost of that care’s provision reasonably low across the world, is not a recent phenomenon (Declaration, 2007). It had been argued that if nations’ health systems are not changed, it will lead to a health disaster and make the health system unsustainable. Globally, multiple visible trends can derail the healthcare initiatives and push the health system towards unsustainability (Miller & Xie, 2020). A failed attempt to address these threats and challenges will create huge financial burdens for both individual countries and the citizens living in them. The factors such as focusing on input-based financing and volume rather than value, changing demographic and lifestyle trends, increasing public health emergencies, and high medical inflation burden the health systems. Unless these factors are addressed, health systems are likely to become further unsustainable in future (Thomson et al., 2009). In India too, some of these trends can be seen. For example, hospitals are paid based on input or services delivered. Though some forms of value-based payments exist, their implementation is limited. During the financial year 2018–2019, the medical inflation stood at 7.14%, almost double the general consumer price index (Aggarwal & Buckle, 2020). Now, this may create a substantial financial burden for both individuals and governments. One possible way to manage the financial burden from healthcare is through risk transfer and using health insurance as a healthcare financing mechanism (Lu & Hsiao, 2003).

While examining the financing of healthcare through the insurance mechanism, it is essential to investigate the overall disease burden and the healthcare sector in India. India’s healthcare disease burden broadly comprises communicable and non-communicable diseases. Most public healthcare facilities are geared towards managing communicable diseases, such as HIV/AIDS (human immunodeficiency virus/acquired immunodeficiency syndrome), flu, tuberculosis, measles, hepatitis A and B, Ebola, etc. The recent 2019-nCov also falls in this list of communicable diseases. In addition to managing communicable diseases, the public sector healthcare delivery is also geared towards managing maternal and child health across the country. Concerning non-communicable diseases, the major ones are diabetes, hypertension, heart diseases, cancer, leukaemia, osteoporosis, etc. Most of the private health sector resources and infrastructure are focused on providing treatment for non-communicable diseases. When it comes to the diseases like diabetes, India ranks third globally, with more than 77 million individuals suffering from diabetes in India (Kannan, 2019).

As of 2016, the life expectancy at birth was 66.9 years for males and 70.3 years for females. Throughout 1990–2016, India underwent an epidemiological transition where the disease burden, in terms of the highest disability-adjusted life years (DALYs), shifted from communicable to non-communicable diseases. Diarrhoea and lower respiratory infections and cardiovascular and chronic respiratory diseases contribute to the maximum share of deaths in communicable and non-communicable diseases, respectively. Today, India faces a double disease burden. As per a World Health Organization (WHO) report, in the year 2017, just 32% of the healthcare spending came from public sources (World Health Organization, 2017). The government’s low spending on healthcare forces patients to reach out to private healthcare providers, increasing their out-of-pocket (OOP) spending. As per the Ministry of Finance, Government of India, from a financial perspective, India has one of the highest OOP levels globally, which is around 65%, contributing directly to the high incidence of catastrophic expenditures and poverty (Economic Survey, 2021). Thus, over the last decade, the disease burden has positively impacted the country’s health sector.

The healthcare sector has become one of India’s largest sectors— in both revenue and employment—and is ranked among the top three in incremental growth. It comprises multiple entities and stakeholders, such as hospitals, diagnostic centres, medical devices and equipment, telemedicine, medical tourism, clinical trials, and health insurance. The healthcare market in India is expected to be valued at ₹8.6 trillion by 2022, primarily driven by rising income levels, greater health awareness, increased precedence of lifestyle diseases, and government initiatives, such as Pradhan Mantri Jan Arogya Yojana (PM-JAY), National Digital Health Mission (NDHM), etc. The increasing medical tourism due to the availability of quality healthcare and highly qualified medical professionals, and improved access to insurance (Mishra & Shailesh, 2012; Vitthal et al., 2015), is also a contributing factor. Indian healthcare delivery is broadly categorized into the public sector (managed and run by the government) and the private sector. The public sector includes sub-centres, public health centres, and community hospitals at the village, block, and district levels. There are also public-funded government teaching hospitals that provide healthcare services to the poor population. As the government funds these public health institutions, most of the services are either free of cost or have a nominal user fee. The private sector includes nursing homes and hospitals that are privately funded. Therefore, there is a sense of competition and pressure to increase ROI (return on investments). The private-sector healthcare institutions have been able to attract foreign tourists, leading to the growth of medical tourism in India, and are expected to touch ₹628.83 billion (US $9 billion) by 2020 (Coverage, 2019).

HEALTHCARE FINANCING AND HEALTH INSURANCE

Both central and state governments have introduced various health insurance programmes to improve protection against catastrophic health expenditure. Private voluntary insurance has also grown in terms of lives covered and premium collected during the last decade. For example, as of 2018–2019, 24% of all lives covered under health insurance are private insurance. Similarly, health insurance as a healthcare financing mechanism had gained momentum in India with an increase of 17.16% in gross direct premium on a year-to-year basis, which has reached ₹516.38 billion (US$ 7.39 billion) in FY2020 (Healthcare Industry in India, 2021). There could be multiple reasons for this phenomenal growth in health insurance premium, for example, the privatization of insurance business, entry of standalone health insurance companies, introduction of third-party administrators (TPAs) to provide cashless hospitalization services, de-tariffication of the general insurance business, increasing healthcare costs, increase in disposable income, high OOP healthcare expenditure, shift from communicable to non-communicable diseases, standardization, and health insurance portability (Kumar, 2015). However, with low public spending on healthcare and a high share of OOP, health financing in India has been a significant challenge. The 2016 Household Income and Expenditure Survey in Bangladesh and the 75th National Sample Survey (NSS) in India suggest that healthcare financing through OOP payments results in catastrophic health expenditure and impoverishment in many Asian countries, including India (Ahmed et al., 2021; Yadav et al., 2021). Despite various initiatives, there is still a gap in providing coverage, especially to the middle class, often called missing middle.

Similarly, the Indian health insurance industry is also currently experiencing multiple challenges. There is a huge trust deficit between the health insurance companies and the healthcare providers (hospitals). It has been observed that the customer’s (insured patient) awareness about the health insurance policy terms and conditions is very poor, leading to poor customer experience. A lack of trained workforce and poor infrastructure poses a threat to the promise of healthcare access and affordability (Kumar & Rangarajan, 2011). Interestingly, fraudulent cases are reported wherein the insured try to get reimbursement of hospitalization bills that were never incurred in the first place. There is also an increase in the regulatory expectations for protecting policyholder interest and a lack of technology to make health insurance more appealing to the average citizen, justifying the negative media coverage and the poor penetration of health insurance in India. Among these multiple challenges, one of the critical challenges insurance companies face is a high incurred claim ratio (Kumar, 2015; Kumar et al., 2011). In response to the technological changes observed globally, companies are now adopting newer technologies and are ramping up their strategic investments towards research and development (R&D) and innovation efforts (Shaker & Covin, 1993). There is a need for sustained investments for developing healthcare infrastructure and a healthcare budget that has provisions for funding government-led insurance programmes (Gilks & Alemu, 2020).

There is an urgent need to devise strategies at a firm level to address the above-listed challenges. For an insurance company to formulate successful strategies, it is crucial to understand the competitive environment and the different critical success factors at the insurance industry level. The strategy should then help in the identification of various sources for gaining a competitive advantage. Thus, with an understanding and use of the theoretical lenses of both the resource-based view (RBV; Barney,1991; Grant, 1991; Penrose, 1959; Peteraf, 1993; Prahalad & Hamel, 1990; Rumelt, 1991) and competitive strategy literature (Bharadwaj et al., 1993; Black & Boal, 1994; Day & Wensley, 1988; Douglas & Ryman, 2003; Freeman & Boeker, 1984; Kindstrom, 2010; Porter, 1985; Zahra & Covin, 1993), and the grounded theory, an attempt is made in this article to reveal the strategic choices available to health insurance firms.

The RBV of competition draws upon the resources and capabilities that reside within an organization. Different kinds of resources are required to smooth the strategic and operational processes in the health insurance industry. It is a service industry that deals with multiple stakeholders. Therefore, both tangible (e.g., physical assets, financial, human resources, etc.) and intangible (e.g., intellectual property, brand image, reputation, organization’s ability to innovate, etc.) resources are required to be successful. While resources are essential, their configuration provides an organization with the attributes to compete in the marketplace, commonly called competencies. Core competency is derived from the collective learning of individual members within an organization and their ability to work across organizational boundaries. A core competency should be difficult to imitate, should make a significant contribution to profitability (measured in economic terms), and should provide access to a wide variety of markets (Prahalad & Hamel, 1990). Competitive advantage, as the name suggests, is relative to one’s competitor competing for the same set of customers. A firm is said to have a competitive advantage when its economic profit is higher than its average profitability. There is a state of competitive parity when the company’s profitability is the same as that of the industry average. When the firm’s profitability is lower than that of the industry average, it is assumed to have a competitive disadvantage. Thus, the higher the firm’s profitability relative to its competitor, the greater is its competitive advantage (Hill & Jones, 2013).

In the Indian health insurance industry, there are multiple sources for a health insurance company to gain a competitive advantage. To identify these sources, insurance companies need to focus on at least three things. First, they must understand the healthcare business and cost dynamics in India, that is, the hospital sector, hospitalization cost, and healthcare financing. Second, they must study the health insurance industry and its key players. Third, they must examine the health insurance business model. Understanding the dynamics of healthcare through the cost and financing lenses can provide insights into how to mobilize resources effectively. It will also help identify the health insurance industry’s critical success factors. In any industry, to be successful, it is vital to understand the competitive environment. Finally, the study of the business model can help the health insurance company identify the different factors that are important to be successful, to understand the relationship between difficult strategic choices and their consequences. Thus, based on the above discussion and study of extant literature, the following research objectives are proposed for the current study.

METHODOLOGY

Primary and secondary data were collected and analysed to achieve the research objectives. For the first research objective, that is, to study the healthcare scenario in India (with a focus on the hospital sector, hospitalization costs, and financing of healthcare in India), secondary data were used. The report of the 75th NSS and information available at the Ministry of Health and Family Welfare (MoHFW) website (e.g., National Health Policy) were studied. Additionally, the reports published on the Indian healthcare industry by WHO, different industry bodies, and leading consulting firms were studied.

To achieve the second and third research objectives, that is, to identify the critical success factors and business model within the health insurance industry, telephonic and face-to-face interviews were held with experts in healthcare, insurance, and strategic management. A total of 27 experts were interviewed over 11 months (between 2017 and 2018). The experts were selected based on their industry experience and professional qualifications. About 30% of the experts were from the healthcare industry, 56% were from the insurance industry, and 7% were from strategy consulting firms and advisory bodies, with experience in both healthcare and health insurance industry. The remaining 7% of the experts were from academic institutions, teaching subjects on healthcare management and strategic management. The cumulative experience of the expert group was of 658 years. Interviews were conducted in a semi-structured format. Three questions aimed at understanding the key success factors, suggested by Kenichi Ohmae in his book The Mind of the Strategist (Ohmae, 1982), were asked: ‘What do customers want?’ (this included both the customer buying insurance and the hospitals providing care), ‘How do insurance firms survive the competition?’ and ‘What are the critical success factors in the health insurance industry?’ Open-ended questions were asked to get strategic insights from a business model standpoint, for example, ‘What are the strategic choices for insurance companies for gaining a competitive advantage?’ ‘What actions can help increase the willingness to pay?’ and ‘How can an insurance company reduce the loss ratio and increase customer retention?’ The open-ended nature of the questions allowed the experts to relate the different aspects associated with the last two research objectives. The interview transcripts were reviewed to identify significant factors and were subsequently coded. The reviewers consulted each other to ensure consistency. The maximum and minimum years of experience of the experts were 40 years and 12 years, respectively. The average years of experience of the expert group were 16 years. The study’s initial findings were shared with some of the experts for their feedback and suggestions. Since most of the experts were based in different metro cities of India, telephonic interviews was preferred instead of face-to-face interactions. In addition to this, the various reports published by the Insurance Regulatory and Development Authority of India (IRDAI) were also studied.

RESULTS

Healthcare in India

As per the Entrepreneurs Association of India, the Indian healthcare sector is expected to register a compound annual growth rate (CAGR) of 22.9% during 2015–2020 to US $280 billion. The Indian healthcare system is quite complex, and concerns are being raised by different stakeholders (including the government authorities) to address the urgent need to improve its performance (Rao, 2004; Rao & Choudhury, 2012). Over the last decade, multiple changes have occurred in the healthcare industry in India. First, there has been a shift in health priorities from communicable to non-communicable disease. Second, there has been growth in the healthcare industry, coupled with economic growth and fiscal capacity. Third, there has been an increase in the incidence of catastrophic expenditure due to the rising healthcare costs. Medical inflation is outpacing the general consumer price index. Over 34.9% of the population had experienced catastrophic expenditure on health (OOP exceeding 10% of non-food expenditure), which pushed 4.48% population into poverty. Fourth, political will towards health assurance has emerged. Both central and state governments have launched various health protection schemes to protect people against catastrophic expenditure. PM-JAY and Chief Minister’s Comprehensive Health Insurance Scheme (CMCHIS) in Tamil Nadu are two examples.

Unfortunately, in India, the general government expenditure as a percentage of total health expenditure is less than 30% of the total healthcare expenditure; in contrast, in the United States and United Kingdom, it is 48% and 82%, respectively. As per the 2015 Healthcare Outlook of India published by Deloitte, India’s public health system is not robust. There are issues related to inadequate funding, more than 100% bed occupancy, leading to overcrowding, and poor access to healthcare in rural areas. These issues are amplified due to reduced funding and the non-utilization of the allocated budget by MoHFW. Even today, there are vast disparities and inequities in health outcomes for rural and urban areas, and there are inequities across different states in India. As per the draft National Health Policy, the tribal areas suffer the most. Even in states where the overall health indicators are improving, the districts with tribal areas perform poorly. There are concerns about the quality of care across the service range. There are problems associated with inefficiencies in fund utilization, poor governance, and leakages in the public sector. The private sector provides 80% of outpatient care and about 60% of in-patient care, and 72% of all private healthcare enterprises are family-run businesses. However, this trend is slowly changing with the growth and emergence of corporate and multi-chain hospitals.

Health Financing in India

India has been spending about 4% of its gross domestic product (GDP) on healthcare during 2000–2017. The health system is financed mainly by a mix of general tax, social insurance, and OOP expenditure. Public expenditure on healthcare stood at approximately 1.2% of the GDP over the last decade, despite attempts to increase it to 2.5%. The government could not provide a credible commitment to this change, resulting in a 32%-to-68% public–private expenditure split. The social insurance schemes are limited to the formal sector, and private health insurance accounts for less than 5% of the total health expenditure. The high OOP, which stood at 62.4% in 2017, is regressive and creates barriers to access. With the government health protection programmes funded by a general tax, especially PM-JAY, providing cashless services, the OOP expenditure is likely to come down.

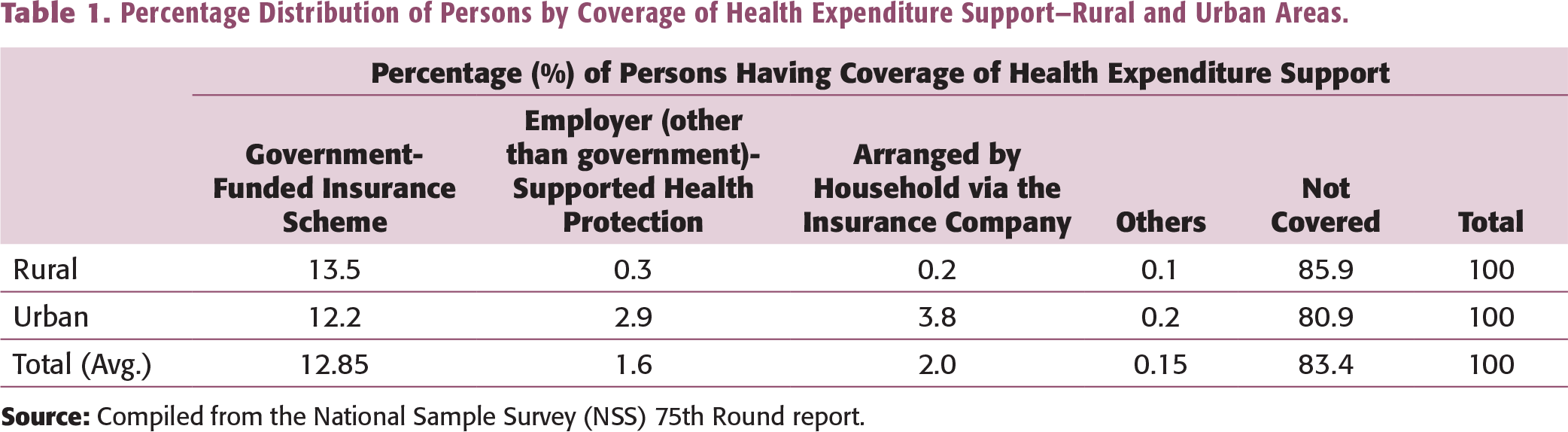

Percentage Distribution of Persons by Coverage of Health Expenditure Support—Rural and Urban Areas.

The data highlight that any form of insurance does not cover a significant proportion of the population. Thus, health insurance companies have a massive opportunity to tap the uninsured population. On the other hand, there is the challenge of identifying the different sources of competitive advantage to bridge the demand–supply gap in healthcare more efficiently and effectively. While doing this, health insurance companies should create value for all the key stakeholders and players in the health insurance industry.

Private Health Insurance in India

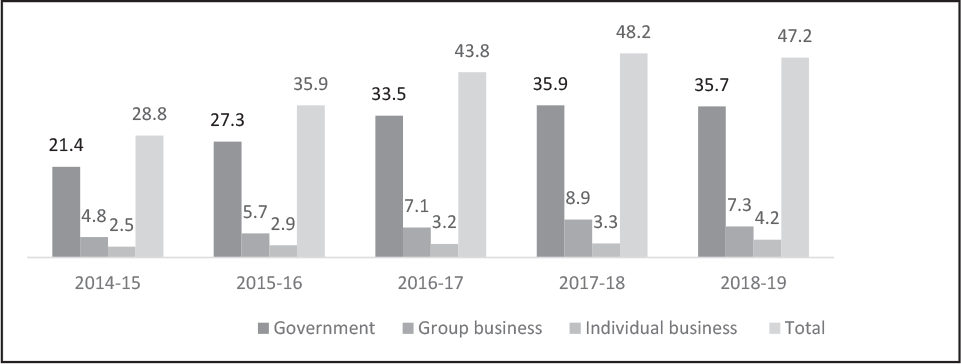

During 2018–2019, the gross health insurance premium collected was ₹448.73 billion, and the year-on-year premium growth was 21.2% (Insurance Regulatory and Development Authority of India, 2019). The public-sector non-life insurance, standalone health insurance, and private non-life insurance companies had shares of 52%, 24%, and 24%, respectively, in health insurance premium collected. Out of the three broad lines of business, that is, group, individual, and government, from 2014–2015 to 2018–2019, there was a decrease in the share of individual health insurance premium from 44% to 39%. During 2018–2019, the group health business was about 48%, and government business was about 13%. During 2018–2019, the non-life insurance industry issued policies covering 472 million persons, and government-sponsored health insurance schemes covered 75% of these lives (see Figure 1).

One of the critical concerns of the health insurance business has been the fluctuation of incurred claims ratio (ICR) over the last several years. The net ICRs were 101%, 106%, and 94% in 2014–2015, 2016–2017, and 2018–2019, respectively. The reason for the high ICR can be multiple. Broadly, the reasons could be classified into three areas: the premium (linked to the underwriting), claims cost (related to the payment made to the providers and the insured using a cashless benefit or through a reimbursement mechanism), and administrative expenses. Since Indian consumers are very price-sensitive, insurance companies must determine innovative ways to manage product pricing and claim cost. Among the various class of health insurance business, the net ICR is high, particularly for the group (business-to-business [B2B]) and government (business-to-government [B2G]) businesses, which was more than 100% for each of the preceding 5 years. Interestingly, this trend is now reversing in these businesses, through a decreasing ICR in B2B and increasing ICR in B2G businesses.

Source: IRDAI Annual Report 2018–2019.

Thus, for an insurance company to gain a sustained competitive advantage, it is essential for it to use the existing and future resources and capabilities to reduce the ICR. The use of innovative technology can also help achieve part of it. The Frost–Sullivan report suggests that by 2025, digital technology will become the backbone of health insurance operations; wearables, telehealth, mobile/smartphone payments, data security, and potentially new technology will be the future trends to watch out for.

Among the major suppliers to private health insurance companies are hospitals. All insurance companies that deal with the health insurance business are expected to have a list of network hospitals where the customers can avail of cashless hospitalization services. One of the most crucial aspects of purchasing a health insurance policy is the cashless hospitalization service. Under cashless hospitalization, the insured is not expected to pay OOP. The cost incurred for treating a healthcare ailment is paid directly by the insurance company to the concerned hospital, subject to the policy terms and conditions. This mechanism of cashless hospitalization has led to the introduction of TPAs and the growth of the health insurance business in India. It also impacts the profitability of the health insurance business. As the patient is not expected to pay OOP, there are no incentives for the patient to control the healthcare expenses, leading to a higher average claim cost in cashless hospitalization than in non-cashless health claims. Since the decision of the treating doctor and the facilities available at the hospital determine the hospitalization cost, it becomes critical for the health insurance companies to build a solid and long-lasting relationship with their network hospitals. Thus, if a health insurance company wants to achieve a sustained competitive advantage, it must develop strategies to manage healthcare costs and build strategic partnerships with the network hospitals.

The Hospital Sector in India

Among the key suppliers to the health insurance industry are hospitals (commonly referred to as healthcare providers or network hospitals). While the private sector owns approximately one-third of all hospitals, the public sector owns most of the beds. The private sector accounts for 74% of all hospitals and about 40% of the hospital beds in the country (Indian Brand Equity Foundation, 2018), with 72% of all private healthcare enterprises being family-run businesses. The hospital sector faces two key challenges: high capital investment and operating expenses. As per a CRISIL report, the capital cost to build a hospital is typically around ₹5 million–₹15 million per bed for a typical 200-bed multispecialty hospital in a Tier-I city. High operational expenditure is mainly driven by the labour-intensive nature, that is, the requirement for a skilled workforce, etc. There are problems associated with inefficiencies in fund utilization, poor governance, and leakages in the public sector.

Hospitalization Cost

The 75th NSS covering July 2017–June 2018 reports that the proportion of ailing persons (PAP), measured as the number of living persons reporting ailment (per 1,000 persons) during the 15-day reference period for different genders in the urban sector, increased to 142 people from the 91 people reported during the 60th NSS (January–June 2004). Similar trends are seen in rural areas as well, thus indicating an increase in the overall morbidity rate. Now, this has a direct impact in terms of increasing demand for healthcare services.

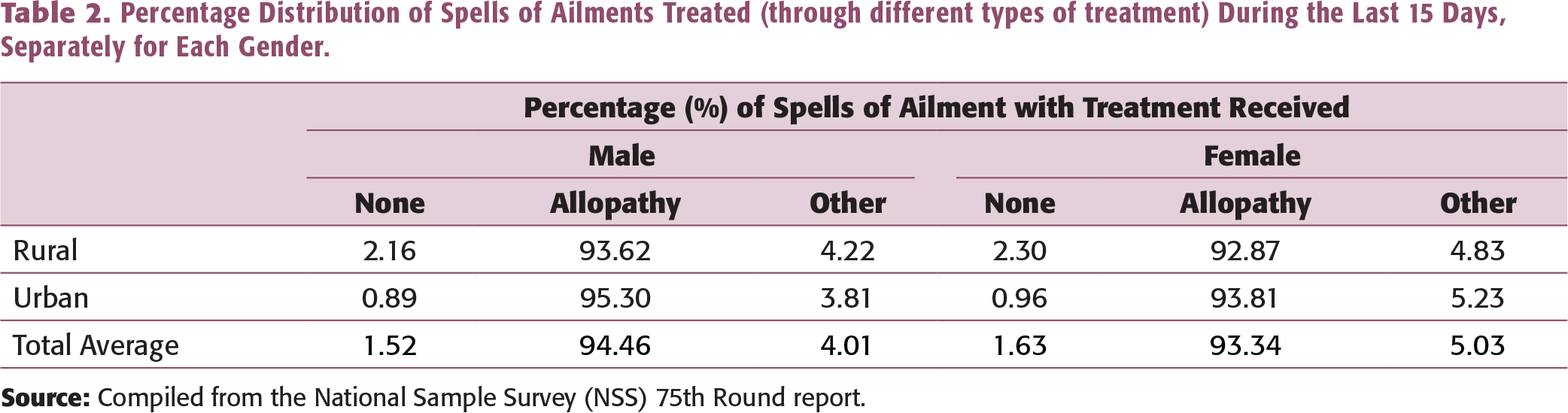

Percentage Distribution of Spells of Ailments Treated (through different types of treatment) During the Last 15 Days, Separately for Each Gender.

Source: Compiled from the National Sample Survey (NSS), 75th Round report.

Note: * Includes health sub-centres (HSC), primary health centres (PHC), and community health centres (CHC).

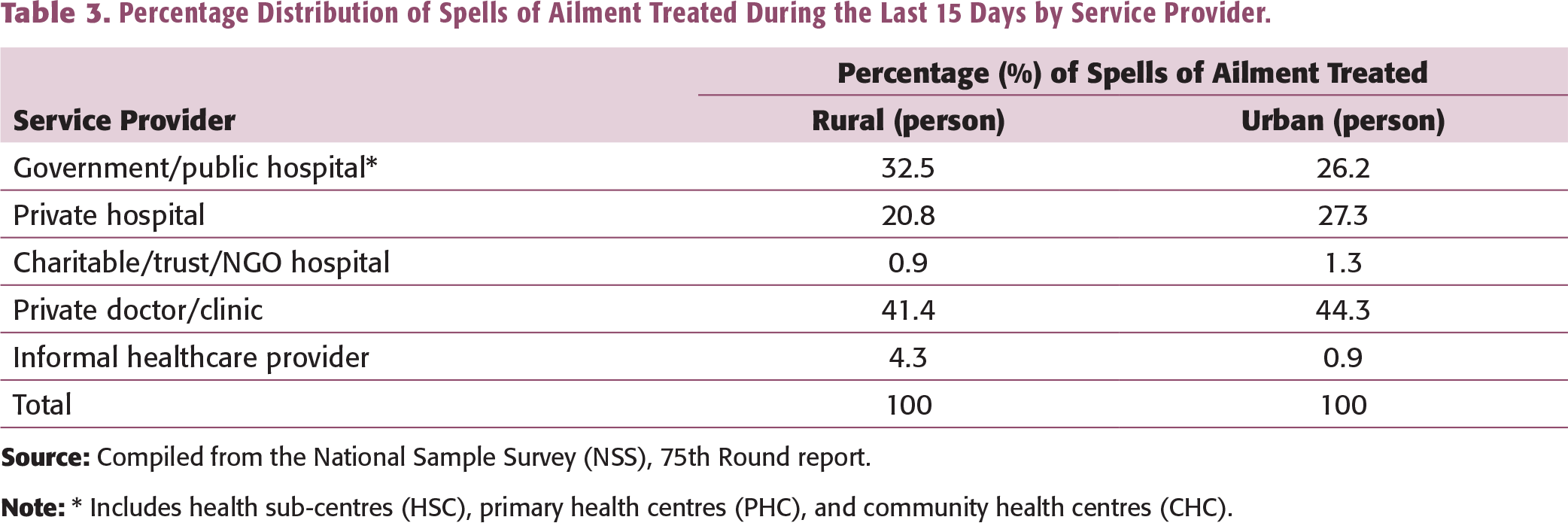

The share of government and private institutions in treating the hospitalized cases of ailments in the rural and urban areas for the last four NSS rounds (52nd Round—July 1995–June 1996, 60th Round—January–June 2004, 71st Round—January–June 2014, and 75th Round—July 2017–June 2018) indicate that preference is given to the private sector when it comes to hospital treatment.

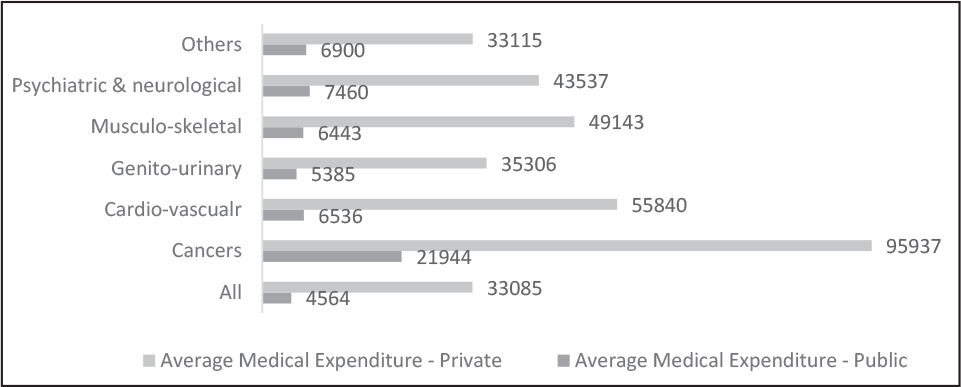

Figure 2 depicts the average total expenditure per hospitalization, highlighting the difference in average cost between private and public hospitals. The average hospitalization costs are ₹33,085 and ₹4,564 for private and public hospitals, respectively. The highest expenditure was incurred for cancer, followed by cardiovascular diseases. For cancer treatment, an average amount of ₹21,944 was spent in a public hospital, whereas more than four times that amount (₹95,937) was spent on the treatment in a private hospital. In fact, across all the major aliments category, it is observed that the average cost incurred in a private hospital is much more than that in a public hospital.

The average non-medical expenditures per hospitalization case were found to be ₹2,317 and ₹2,114 for rural and urban areas, respectively. It is interesting to note that the average non-medical expenditure is more in rural areas. This may be because of the cost incurred in travel and allied expenses. The hospital’s proximity from the place of residence of the patient has a role in increasing the non-medical expenditure. Thus, while examining hospitalization costs, one should include the cost incurred for treatment and the loss of income due to hospitalization. In health insurance, the cost of treatment is covered. However, few health insurance policies have hospital cash benefits, which is primarily meant to cover the loss of income due to hospitalization.

In the hospital industry, to be successful, there is a need to develop superior capabilities relative to competitors. Developing such capabilities within a specific local market can help hospitals gain higher economic rents than competitors (Douglas & Ryman, 2003). Here, the requirements suggested by the RBV are of utmost importance. Focusing on creating value, rareness, inimitability, and better organization can help a hospital gain a sustainable competitive advantage (Barney, 1995; Black & Boal, 1994). For example, developing the capability to deal with TPAs and health insurance companies can help the hospital in providing seamless, cashless hospitalization services and reducing errors in the billing of hospital costs (non-payable items as per the health insurance policy) that are to be paid by the customer at the time of getting discharged from the hospital. Most of the time, the fundamental issue between insurance companies and hospitals is related to billing, around who has to pay the difference amount—the insurer or the patient. Thus, a hospital that can build capabilities and processes for managing such issues will have an opportunity to create a long-term relationship with both TPAs and health insurance companies. It will be able to increase its insured-patient volume (leading to economies of scale and an overall reduction in cost per bed).

Source: Compiled from the National Sample Survey (NSS), 75th Round report.

Expert Views—Critical Success Factors in the Health Insurance Industry.

Critical Success Factors

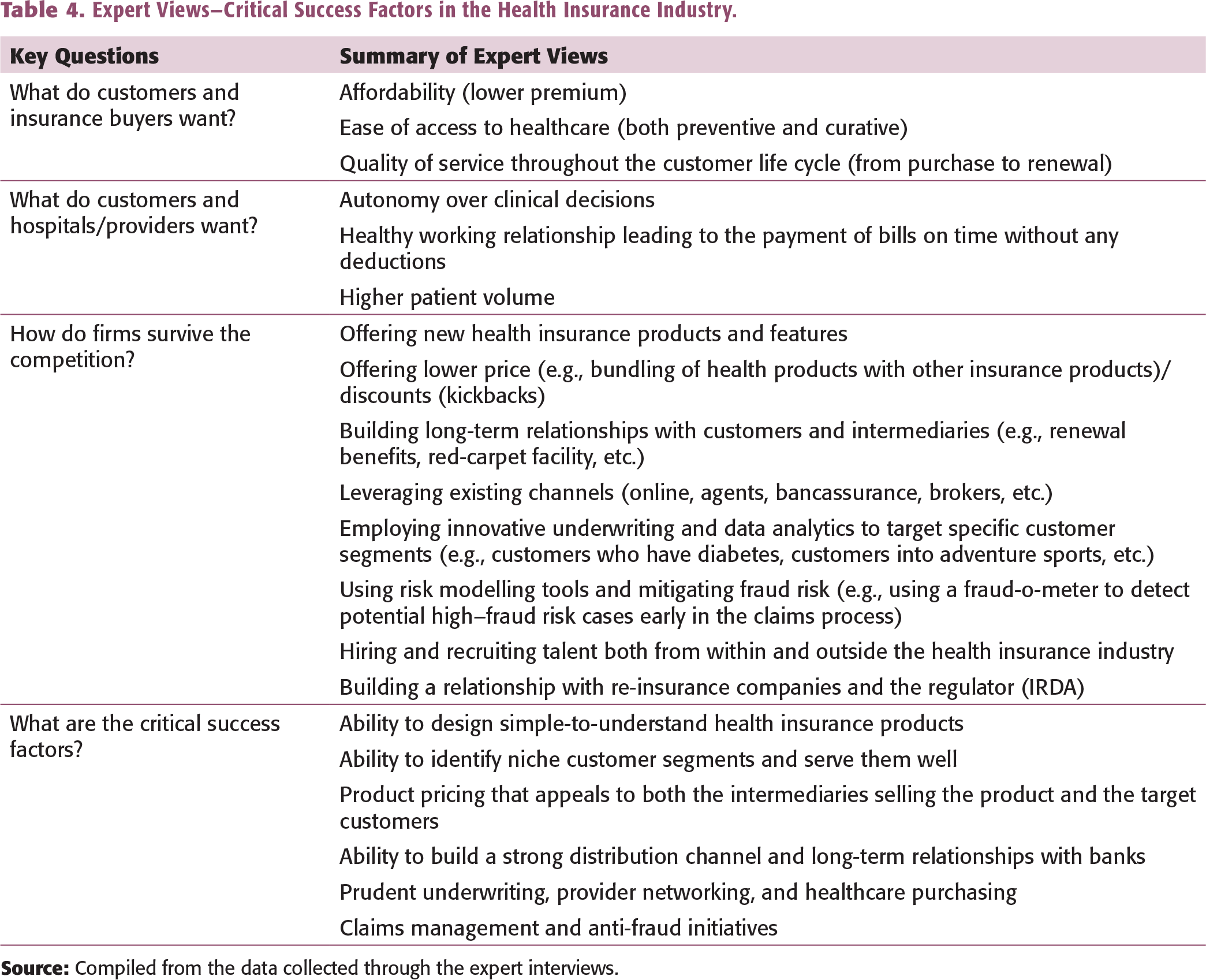

To perform activities more effectively than the rival firms, an insurer needs resources and capabilities that the competitors do not have. Here, the understanding of critical success factors is of utmost importance. Also, to address the different challenges faced by the healthcare financing industry, especially the health insurance industry in India, it is essential to identify the various critical success factors. The critical success factors are those factors that affect firm performance and profitability. To determine the different critical success factors, one must ask a few specific questions about the firm and its customer, competition, and survival (Ohmae, 1982).

The findings suggest that the customer may have different preferences regarding the product type, coverage, sum insured, hospitalization benefits, inclusions, and exclusion in health insurance. This also includes whether the customer is willing to pay a price premium for a particular company’s product because of the perceived brand value (e.g., the choice of a private health insurance company compared to a public sector undertaking, or vice versa), exclusivity, and quality. The analysis of competitors included studying the market forces (bargaining power of suppliers and customers, availability of substitutes, rivalry among existing players, threat of new entrants), the low barriers to entry, the level of seller concentration, how easy it is for the competitors to imitate the health insurance product features, what kind of product and service differentiation is possible, and whether it can yield a substantial price premium or not. A key or critical success factor (CSF) is defined as a skill or a resource that a company can invest in and is observed in the market in which the company is operating. The CSF explains a significant part of the observable differences in perceived value and or relative costs (Grunert and Ellegaard, 1993). Critical success factors encompass the assets and skills developed by a firm which help it improve its business performance and attain a competitive advantage relative to its competitors. They act as a high leverage function and include activities that the firm should master to outperform its rivals (Day & Wensley, 1988). With respect to the health insurance industry, the critical success factors may be the need to combine differentiation with low cost and speed of response to changing customer needs, which can lead to cost efficiency (e.g., healthcare purchasing, fraud risk management, low wage, etc.). Table 4 summarizes the key findings regarding the three questions raised above.

Privatization and the entrance of standalone health insurance companies and relaxation in investments by foreign players have led to increased competition within the health insurance industry. There are different ways through which the insurance companies are competing among themselves. The findings of the study suggest that insurance companies are doing multiple things to combat competition. The primary focus areas are introducing new health insurance products and features, offering lower premium through bundling healthcare products, and offering discounts to customers for purchasing multi-year products (3 years instead of 1 year). According to one of the experts:

Other than claims management and prudent underwriting, the top three drivers of profitability is product design, accessibility of services leading to clinical governance and use of technology, including data science.

Health insurance companies build long-term relationships with customers and different intermediaries (e.g., providing renewal benefits, the red-carpet facility at network hospitals), using innovative underwriting techniques and data mining tools, and designing underwriting policies covering diseases like diabetes and AIDS. They use risk modelling tools and mitigate fraud risk through technology (e.g., usage of fraud-o-meter to identify suspected claims). The war for talent and building long-term relationship with re-insurance companies has also been used as techniques to survive the competition.

The experts believe that six critical success factors are relevant in the Indian health insurance industry. In no specific order, the first is the ability to design simple-to-understand health insurance products. The second is the ability to identify niche customer segments and serve them well. For example, women aged between 24 and 45 years into trekking and fitness can be a niche customer segment. Another example is people with controllable diabetes living in Tier-II cities and healthcare workers working in private hospitals with less than 100 beds. The idea is to have a clear description of the unique characteristics of the chosen customer segment and an understanding of their unique needs from a healthcare standpoint. For example, women who are into trekking might need a health policy that covers the expenses for plaster (in case of a broken ankle) and air ambulance (in case of an emergency). Such types of cover are already offered in the travel insurance policies, and there is an opportunity to extend them to specialized health insurance policies. According to one of the experts:

In India, when we talk of retail business, most of the health insurance products are ‘copy-paste’. It is the same kind of product. Everybody is targeting metro cities; no one wants to go to Tier-I and Tier-II cities. 70% of the products related to health insurance are sold in only 6 States in India, and the remaining 30% is the rest of India. With only 3% of private retail health insurance business being captured, currently, the products are not designed to meet the need of 97% of retail customers. Fundamentally, there is a problem in designing the product. Insurance companies which can design customisable products that meet the needs of the niche customer segments will have a competitive advantage.

The third factor is product pricing that appeals to both the target customer and the intermediaries involved in selling the health insurance policy. The fourth is building a strong distribution network that includes agents, brokers, online channels, and bancassurance. According to one of the experts:

The younger population has a different belief and value system. You talk to young people…they do not want to be monitored 24X7 and will not like to use the agency model. They prefer doing business online. Another opportunity for health insurance distribution is the bancassurance channel….there are two distinct customer segment that goes to a bank, i.e., the high-net-worth individuals and the mass-market. Both have different needs and expectations. For success, it is critical to have an online playbook and focus on bancassurance.

Here, the ability to build an online channel and long-term relationships with at least one bank partner is essential. There are different ways of building long-term relationships, one of which is where the bank invests in the health insurance company. The recent news of Axis Bank acquiring a 9.9% stake in Max Bupa Health’s promoter entity (Market, 2021) is one such example and supports the study findings.

The fifth factor is managing the financial risk arising out of hospitalization and related expenses through prudent underwriting, provider networking, and healthcare purchasing. Prudent underwriting includes properly wording policies, drafting policies as per the client’s requirements, and following proper due diligence for accepting or declining the risk (Baporikar, 2021). Provider networking and healthcare purchasing strategy should be focused on building a long-term partnership and creating a win-win situation for both parties. According to one of the experts:

Currently, the underwriting approach is very flat. There is only one proposal form used for all customers. The philosophy is to price and manage the cost at the time of claim…health insurance companies do underwrite at the point of claim stage as 95% of people do not claim. This is the easy way out…prudent underwriting can be one of the key differentiators. Provider networks play a big role in the success of health insurance companies. They can influence the decision-maker, i.e., the doctors. It makes sense to have a long-term partnership with them. Unfortunately, most of the providers do not like the insurers controlling them. It is two B2B environment where both are working for profit. The key is to create a win-win situation.

The sixth factor is related to claims management and anti-fraud initiatives. Claims management (both cashless hospitalization and reimbursement) plays a vital role in customer satisfaction and protection of the bottom line of insurance companies. In addition to claims management, it is essential to focus on fraud risk management, where prevention, detection, and response strategies are aligned with the overall business model of the insurance companies. According to some of the experts:

When doctor see patient in OPD, they tend to ask: who is paying? If a customer says health insurance, they know the cost is not coming from his pocket. The customer’s mindset is that they have paid the premium, and they are not concerned about reducing hospitalisation cost…doctor take advantage of health insurance coverage. There is no tangible matrix that suggests what price should be charged. Doctors are smart to unbundle the package rate. Their IQ is more than the general population. When they look at a package, for example, Appendectomy at INR. 20,000 (approx. USD$ 272), some list them under different categories of surgery like incision of the skin, ligation of the appendix, retraction of muscle. So, what they do instead of a package, they un-bundle the package…instead of INR. 20,000 they charge INR. 30,000 (approx. USD$ 407). Claim journey needs to be simple and watertight. At times, the acquisition cost for the health insurance business goes up to 70%, and only 30% is the risk premium. So, the company manage claim cost by following the ‘not-to-pay’ game. This is not a good practice and should be curtailed.

These six critical success factors are among the strategic choices available to health insurance companies as part of their business model.

Health Insurance Business Model

A health insurance company can create more economic value than its competitors by either configuring its value chain differently from competitors or performing the activities more effectively. To conduct activities more effectively than the rivals, firms need resources and capabilities that the rivals do not have. Here, the understanding of the company’s business model is of utmost importance.

A business model provides a reference frame that helps the manager conceptualize how the firm’s strategy encompasses the key aspects of doing a business. The different elements are interlinked and should be meshed as if it is a harmonious whole. The business model also enables the firm to differentiate itself from competitors and gain a competitive advantage leading to growth and profitability. The critical components of a business model are the customer value proposition, profit formula (sources of revenue and cost), key resources, and key processes. As health insurance is primarily a service-based business, it is critical that while thinking about the business model the service aspect is considered. Studies carried out by Kindstrom (2010) on the service-based business model suggest that as there are different aspects of a business model, each aspect should be considered not in isolation but in a unified manner. A holistic approach that considers all critical areas of business, focusing on building long-lasting relationships with customers, should be adopted. The service offering should be dynamic and adaptive to the changing customer needs, and firms should be able to visualize both the tangible and intangible value created for the customer. According to one of the experts:

In healthcare, it is tough to quantify what is the rationale for doctor charges. There is no acceptable mathematical model to tell what a surgeon should charge or what a senior consultant—cardiology should charge. The customer has no choice but to pay…’. Health insurers sell to end consumer; they take care of hospitalisation cost. That is the promise to a customer when they onboard, they say: you do not need to worry about cost…but in reality, the health insurer is also into the profit-making business and not for charity. Investors are looking for ROI.

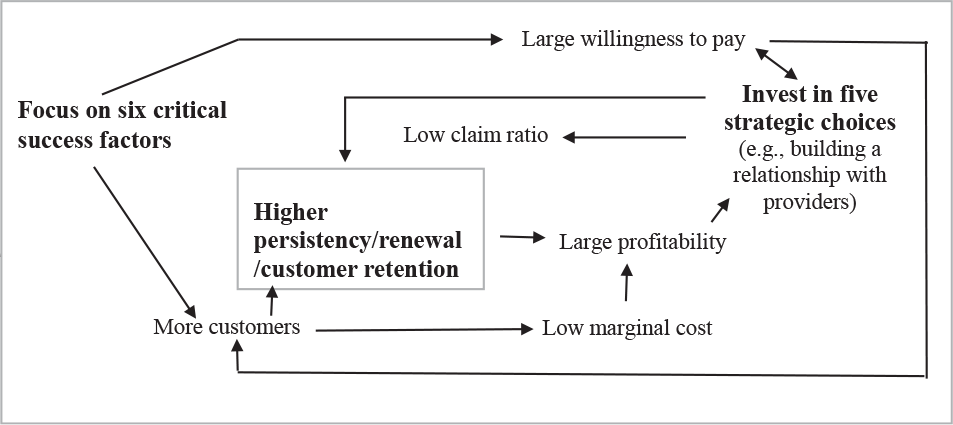

Building on this notion of viewing the business model that includes all critical aspects of the business (including the cyclicity and repetition of business transactions), and from a game theory perspective, a business model can be a cyclic process with an interplay between choices and their consequences. A typical health insurance business model proposed as part of the current study (based on the above-discussed points and the interactions with experts in the fields of healthcare, health insurance, and strategic management) is depicted in Figure 3. As can be seen, there are different choice options available with an insurance company concerning the premium price and making of investments in strategic choices (in Figure 3, the two choices are underlined). One of the key choices is to focus on the six critical factors, and the other one is to invest in five strategic options. Both these choices impact the profitability of health insurance companies. According to one of the experts:

The key drivers for profitability are the doctors and health insurer cannot control them. In a developed market, the health insurers try to control the rate, tariff, and ambiguity in treatment cost through managing the clinical protocols and pathways. The challenge is that there is no theoretical guideline on how to unbundle cost associated with a complicated surgery.

Now, these choices have consequences. The choices are connected with consequences by arrows. The cyclicity of the decisions leads to the accumulation of value. In the case of health insurance, it is the increased customer base and higher persistency. According to one of the experts:

The top three factors for customer retention and improved persistency are the promise (what you are trying to sell), the ease of continuity and relationships with customers (it could be an agent or anyone who has sold the product), and the agent sticking with the company.

Thorough knowledge of the interlinkages between the choices and consequences and how they help accumulate the desired outcome is essential for gaining a competitive advantage.

Competitive Advantage in Health Insurance

Competitive advantage deals with economic profit relative to competitors, and it varies in magnitude from a weak spectrum of competitive disadvantage to a strong and positive spectrum of sustained competitive advantage. For a firm to gain a sustained competitive advantage, different strategic frameworks (e.g., the VRIO framework) help understand the importance of customer value proposition, the rarity of resources, inimitability of products and services, and the organization of different resources and partnerships. In the health insurance context, overall profitability can be used as a proxy for economic profit. In health insurance, profitability is measured in terms of earned premium (revenue) and incurred losses (claims) plus expenses. The profitability is high if the claims-to-premium ratio is low. Excluding expenses, two of the critical components of profitability are the amount of claim paid to customers (cost) and the premium (revenue) collected. To be competitive and serve the Indian consumers who are very price-sensitive, there is very little companies can do to reduce the premium. Therefore, the focus must be on the other aspect of gaining profitability, that is, reducing the claim cost. The ability to build capabilities and competencies within this space will help gain a competitive advantage.

How to Gain a Competitive Advantage?

To gain a competitive advantage, a firm needs to manage its costs, as well as be able to differentiate itself from its competitors. There are two different sources for this: getting access to either unique resources (assets) or building distinctive skills (capabilities). The availability of superior resources and skills of the employees working in the firm can help the firm strengthen its capabilities. Superior skills themselves can act as a distinctive capability that can help the firm gain a competitive advantage (Day & Wensley, 1988). While looking at this broad set of different resources and capabilities to reduce costs and create differentiation, it is essential to also look into both the insurance company’s primary and secondary value chain activities. The implementation of a value-creating strategy also plays a vital role in gaining a competitive advantage. A firm can gain a competitive advantage by choosing a unique value-creating strategy that is not followed by other competing firms or through the superior implementation of the same strategy adopted by existing competitors (Barney, 1989). Here, a sustainable competitive advantage can be created if the firm can resist the erosion of value due to competitive behaviour (Porter, 1985) and avoid duplication by other competing firms (Barney, 1991). It has also been argued that a closer examination of the sources of competitive advantage can provide unique strategic insights, which might not be possible through an analysis of issues at an aggregate level (Bharadwaj et al., 1993). The insurance industry is facing stiff competition. It is necessary for firms to continuously look for ways to create a competitive advantage by developing new products and using innovative techniques (Epetimehin, 2011). According to one of the experts:

As a reinsurer, we do not tell our customers what product we have. Instead, we ask what you need? What will create value for our customers (insurance companies)? The same should happen in the case of health insurance. Insurance companies should ask the customer what they need, not to sell what they have. There is a need for innovative health insurance products, customisation, identification of niche customer segments, and serving them well.

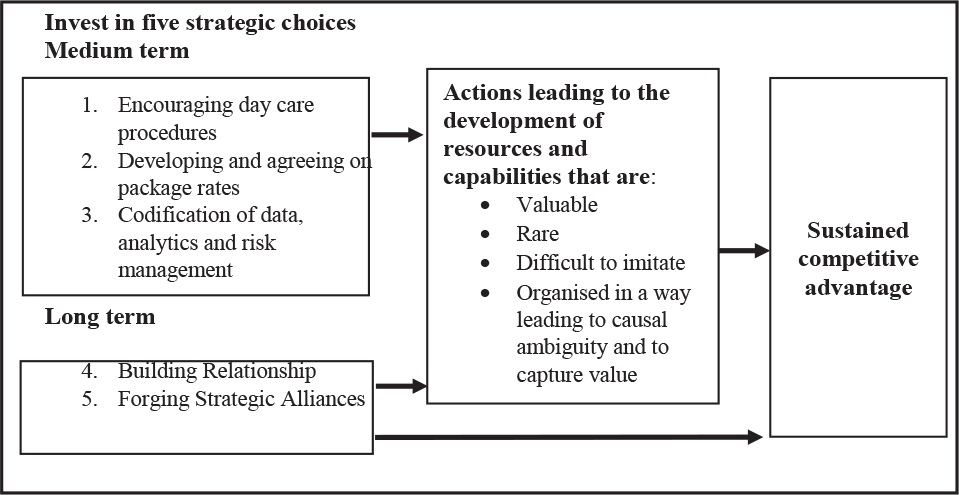

The findings of this research suggest that from a strategic standpoint, the insurance companies that can build the skills at coordinating its resources and putting those skills to productive use to reduce claim cost systematically will develop the necessary capabilities to gain a competitive advantage. The findings suggest that five strategic action choices are available with insurance companies to achieve a sustained competitive advantage. The first is to encourage day care procedures. The second is to develop and agree on package rates. The third involves the codification of data and analytics. The fourth choice is to build a strong relationship with treating doctors and nursing staff. The fifth is to forge alliances with pharmaceutical and medical equipment companies. The model proposed for achieving a sustained competitive advantage in health insurance is depicted in Figure 4. The medium and long term action that lead to the development of resources (both tangible and intangible) and capabilities which are valuable, rare, difficult to imitate and organised in a way to capture the value and which makes it difficult for the competitor to understand the relationship between the company’s inputs and its outputs.

Encouraging day care procedures and developing package rates would help negate the effects of average length of stay (ALOS) on claim cost. While developing and agreeing on package rates, the insurance companies can also propose a supply-side cost sharing mechanism to the network hospitals. Under a cost sharing mechanism, the focus is on altering doctors’ incentives and treating physicians’ to provide healthcare services (Ellis & McGuire, 1993). The codification of data and analytics on patterns of the line of treatment offered by treating doctors, the consumption of medicines (pharmacy wise), and diagnostics by diagnostic centres would build essential insights towards understanding where the leakages are taking place and help identify measures to curb them, thus reducing the cost of claims.

These three actions could be seen as an action item for the short to medium term. The Registry of Hospitals in Network of Insurance initiative by the Insurance Information Bureau of India (IIB), promoted by the insurance regulator IRDAI, to create a central repository for hospitals in the insurer’s network will also support the codification of data and analytics. Under this initiative, hospitals will be provided with a 13-digit globally unique identity and geographical coordinates based on their address. IIB is targeting registering 32,000 hospitals in the first phase. On the analytics front, the insurance companies can develop a ‘hospital performance scorecard’. This scorecard should provide an overall ‘picture of performance’ both at the individual and the group level.

The balance of two strategic options of building the relationship and forging an alliance would consume more time and be a long-term investment. There are benefits of building a relationship with treating doctors and nursing staff. The treating doctors decide whether to admit a patient or not and, if the patient is admitted, what line of treatment is to be followed. This may help avoid unnecessary treatment and reduce overconsumption of diagnostics and medications. According to one of the experts:

In developing market, all three elements (fraud, wastage and abuse) is prevalent. The decision-maker (treating doctor) is not a part of the health insurance business model. In healthcare, doctors are the decision-makers, and they themselves are influenced by their surroundings – pharmaceutical companies, lab and radiology, medical equipment companies and other associated services. When you go with normal cold and fever symptoms, whether you are given 1st generation antibiotics (Amoxicillin) or the 3rd generation (Augmentin) is driven by the surrounding. There is no scientific protocol that tells the doctor which drug to prescribe, amoxicillin or augmenting….there is abuse. So, it is paramount for health insurance companies to build a strong relationship with doctors and nursing staff.

A relationship with the nursing staff would ensure that the services offered during the hospitalization period are of good quality. The nursing staff could also become brand ambassadors and bridge the trust deficit between the key stakeholders. It is not that the Indian healthcare professionals, that is, the doctors, nursing staff, paramedical staff, hospital administrators, and managers, lack training, knowledge, or compassion. Instead, given the high demand for healthcare and low supply, these professionals are overstretched and work in a very complex and resource-constrained environment. Insurance companies that can work with the doctors and nursing staff to solve their day-to-day problems would gain an advantage in the long run—for example, providing expert observation and sharing quality survey data. The insurance company should make ‘invisible’ elements ‘visible’ to the healthcare professional using technology and advancement in data management. This will allow hospitals and providers to reduce cost while delivering the same level of quality or even better quality at a lower price. Allying with pharmaceutical and medical equipment companies directly benefits an insurance company in bringing down the cost. To make this a win-win situation, insurance companies should reciprocate by developing new products that help in consuming and utilizing drugs and diagnostics for both curative and preventive care.

STUDY LIMITATIONS AND FUTURE RESEARCH OPPORTUNITIES

Given the nature of the current study, and in any research endeavour, there are a few limitations. For example, in this study, only health insurance has been studied to finance healthcare in India. There is only a brief description of the other forms of healthcare financing mechanisms. The data were collected based on experts’ opinions on the critical success factors, business model, and strategies for gaining a sustainable competitive advantage in the health insurance business. The study’s findings can be generalized to India only and may not be equally valid for all emerging economies. However, India is the fifth-largest economy globally, with a population of 1.3 billion. The study’s findings, increasing competition among health insurance players, would be of value to health insurance companies, IRDA, and other research scholars interested in improving healthcare financing mechanisms in India. Also, the five strategic choices can be tested empirically by using data of different health insurance companies (strategic investments) and the respective financial performances. There is also an opportunity to study an individual health insurance firm and see how it is innovating its business model and creating a sustainable competitive advantage over time. A few case studies and experimental studies involving health insurance companies and the healthcare outcome of communities they serve can be undertaken to highlight the impact of the strategies beyond the firms’ financial performance and on the larger society. The proposed business model can also be used to develop and test a different hypothesis—for example, the impact of six critical success factors on a firm’s profitability and customer retention—and also the impact of the five strategic choices on customer willingness to pay and health insurance purchase decision.

CONCLUSION AND IMPLICATIONS

Over the last decade, multiple changes have occurred within the healthcare industry in India. These changes have impacted the growth of the health insurance industry as well. The analysis of average medical expenditure across different types of aliments indicates some of the reasons for low insurance penetration and insurance density. On the one hand, there is a massive opportunity for health insurance companies to tap the uninsured population. On the other hand, there is this challenge to identify the different sources of competitive advantage to bridge the demand–supply gap in healthcare more efficiently and effectively. Within the health insurance industry, different kinds of resources (both tangible and intangible) are required to smooth the strategic, operational, and innovation processes. There is a need to develop capabilities that will help build a strong relationship with different stakeholders, especially the providers, and make health insurance policies more affordable. For an insurance company to gain a sustained competitive advantage, it is essential, on the one hand, to use the existing resources and capabilities and, on the other hand, to invest in strategic initiatives such that it can reduce the ICR across the customer segments (i.e., B2C [business-to-customer], B2B, and B2G).

There are critical six success factors for the health insurance industry. An insurance company can create more economic value than its competitors by either configuring its value chain differently from competitors or performing the activities more effectively. Some factors include the ability to design simple-to-understand health insurance products and identify niche customer segments and serve them well, offering of product pricing that is attractive to both the intermediaries selling the product and the customers buying it, building of a strong distribution channel and long-term partnerships with banking channels, prudent underwriting, provider networking, healthcare purchasing, and claims management.

An insurance company must understand the critical success factors and the business model configuration (basically the ‘choices and their consequences’ analysis at the firm level). There are different options available with an insurance company regarding investments in strategic decisions that can either help them offer lower premium or help them build long-term relationships with providers. Investments in five strategic choices will allow insurance companies to gain a sustained competitive advantage in the Indian health insurance industry.