Abstract

Metro rails mitigate problems of pollution and congestion in crowded Indian cities and are therefore a priority of the government. However, they are also very expensive to build and operate, making their operations loss-making. With increasing proliferation of metro rails and their continuous losses, there would be a need for repeated bailout packages for the metro rail sector in India, similar to the case of the power sector. There are a number of measures that can be taken to mitigate this outcome as apparent from the example of Hong Kong Metro.

Keywords

The Government of India has declared its intention to have metro rail in 50 cities by 2025 (Halder, 2018). Metro rails reduce pollution and congestion by substituting hundreds of thousands of personal vehicles for commuting in cities, but for metro rail operations to be financially sustainable, there is a requirement of huge footfalls, substantial non-fare revenue, and capturing value associated with appreciating property prices because of the metro rail investment. The huge upfront capital costs of metro rail (estimated at about ₹3 billion per km) combined with low passenger footfalls in some cities and the desire to keep fares even lower than the operation and maintenance costs of metro rail operations mean that they are perpetually loss-making entities. The losses of metro rail companies will erode the equity of the joint venture companies (JVCs) (most metro rails are 50:50 JVCs between the central and the state governments) and make them bankrupt in the near future. This will call for repeated bailouts for these JVCs similar to the power distribution companies in India.

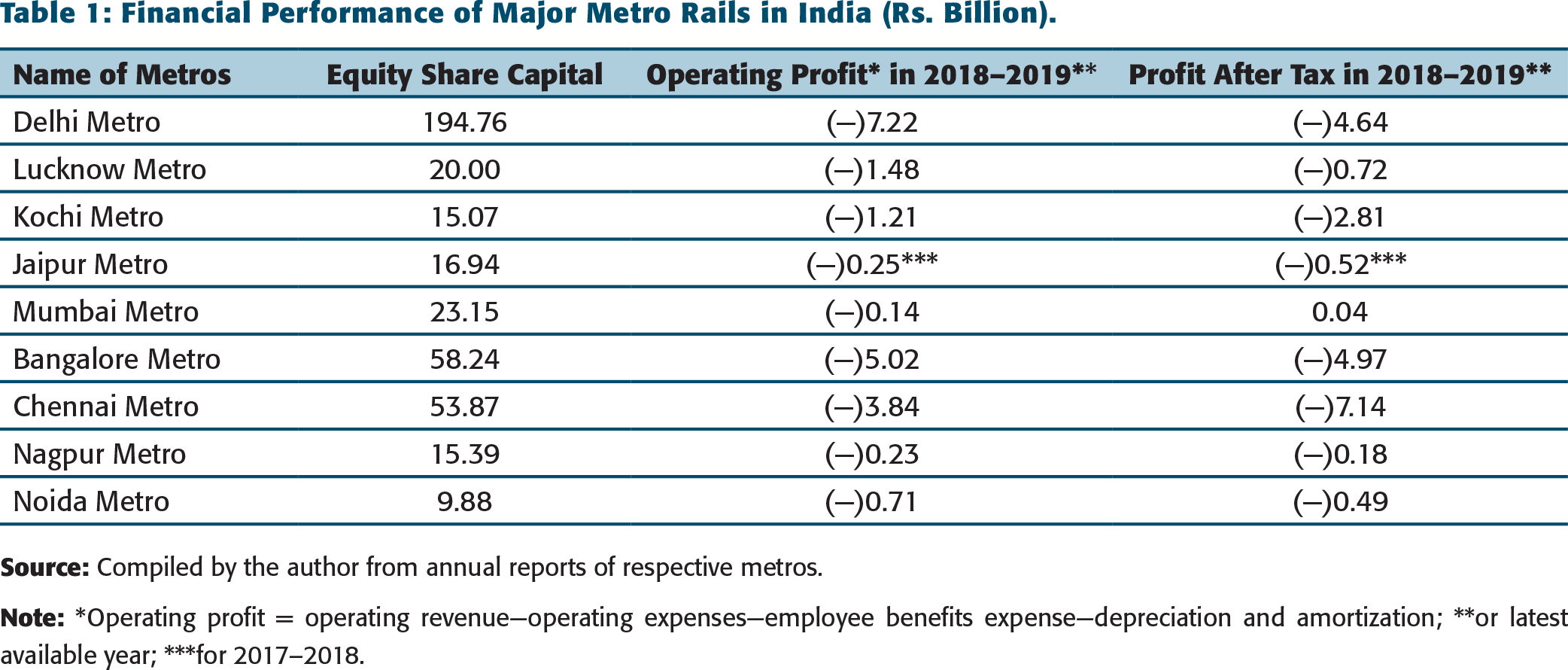

Financial Performance of Major Metro Rails in India (Rs. Billion).

Source: Compiled by the author from annual reports of respective metros.

Note: *Operating profit = operating revenue—operating expenses—employee benefits expense—depreciation and amortization; **or latest available year; ***for 2017–2018.

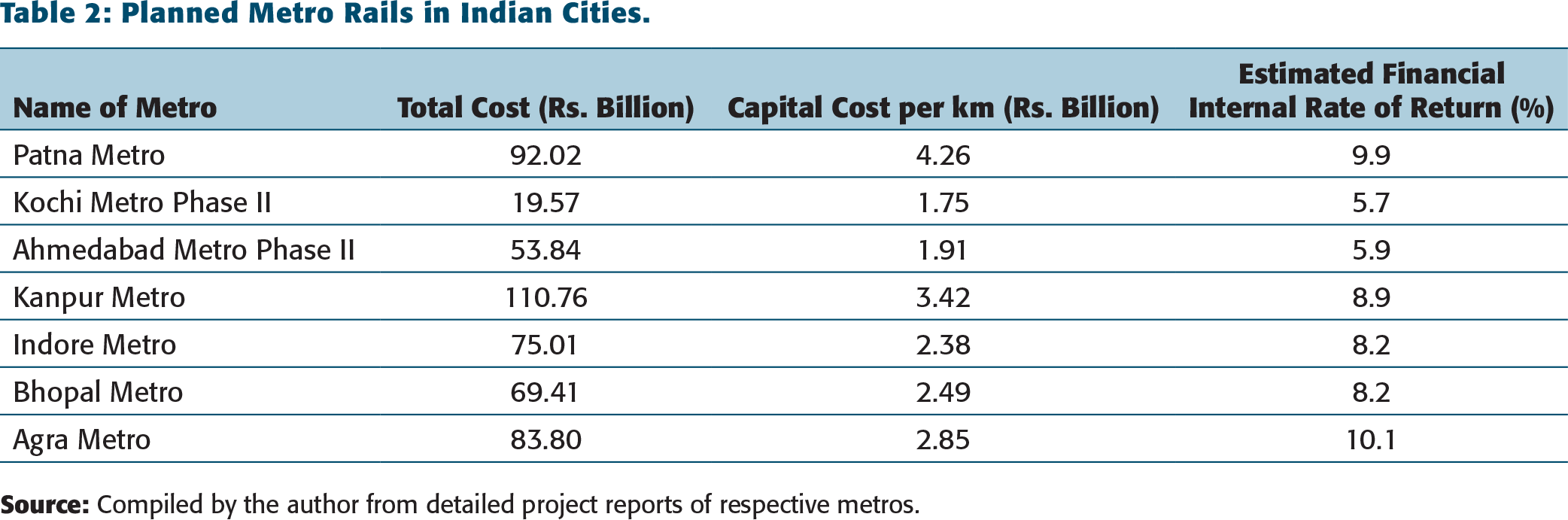

Planned Metro Rails in Indian Cities.

As metro rails spread across more cities in India, the financial distress of the JVCs running these metros will become more acute (Table 2). The estimated financial internal rate of return (FIRR) is projected as positive for these projects in their detailed project reports. However, the record of negative profit after tax (PAT) in operational metros of India (Table 1) implies that there is optimism bias in the estimates, and actually, the FIRR would turn out to be much lower.

FINANCIAL ANALYSIS OF SOME MAJOR METRO RAILS

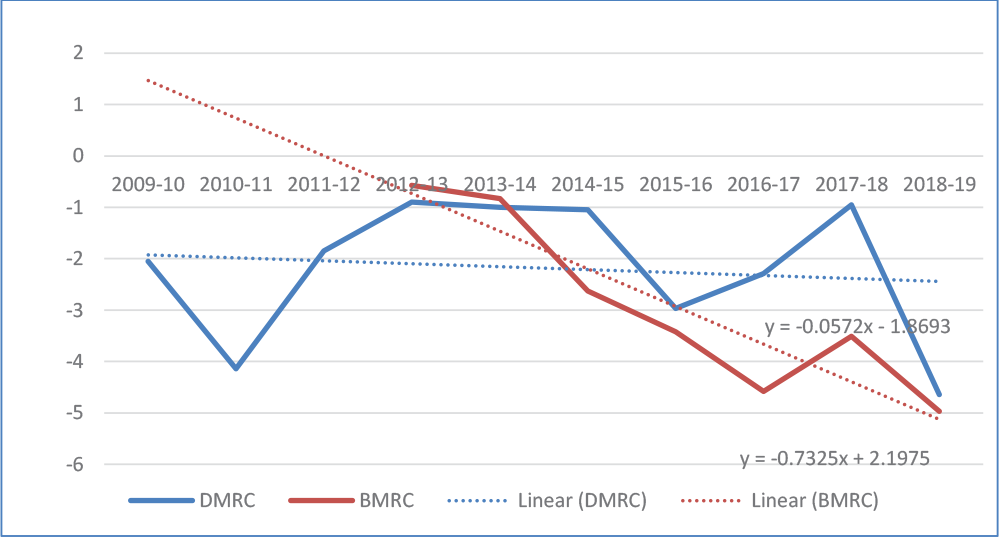

Delhi Metro Rail Corporation (DMRC) is the oldest, longest, and most developed metro in the country. Another major metro rail is the Bangalore Metro Rail Corporation (BMRC). The financial performance trends of both these metro rails are examined in this time-series analysis to understand the financial sustainability of metro rails in India. Figure 1 shows the trends of PAT in these two metro rails.

The PAT trends in DMRC and BMRC confirm our findings that metro rails are loss-making ventures in India. The negative slope of the trendline in both the metros points towards increasing financial unsustainability in the future.

IMPACT OF COVID-19 PANDEMIC ON METRO RAIL

Financial year 2020–2021 is likely to be disastrous for the financials of metro rail JVCs as metros were locked down for more than 6 months because of the COVID-19 pandemic. Even though the metro services had been resumed in October 2020, the ridership had been adversely affected by social distancing requirements. Estimates suggest that instead of 1,800–2,000 passengers, a typical metro train in Delhi is carrying 350–400 passengers to ensure social distancing, implying a carrying capacity of metros of about a fifth of the business-as-usual levels. McKinsey and Company (2020) reports that Transport for London, the government body responsible for the public transportation system in Greater London, estimates that with 2 m of physical distancing, the London Underground, or Tube, will be able to carry 13%–15% of the passengers that it usually does, even at full service. Ways to augment ridership, given the constraint of social distancing, would be to stagger office and school hours so that the ridership is more even throughout the day, compulsory use of thermal scanners at stations with normal temperature as a requirement to avail the services of the metro rail, and compulsory use of face masks, which can possibly increase the ridership to the range of about 40% of the peak capacity. This supply destruction caused by the pandemic is adversely affecting the already stretched financials of the metro rails. It has been estimated that the loss of daily revenue due to COVID-19 compared to business-as-usual is ₹100 million per day for DMRC, ₹16 million per day for Hyderabad Metro Rail, and ₹9 million per day for Mumbai Metro One (Roy, 2020).

FINANCIAL DISTRESS OF THE POWER SECTOR AND NEED FOR REPEATED BAILOUTS

As mentioned earlier, it is likely that the financial distress faced by the power distribution companies in India will be replicated in the metro rail sector. The power sector faces inter-related problems of stressed assets, low capacity utilization (low plant load factor), bankrupt power distribution segment, etc. The total financial losses of power distribution companies (DISCOMs) in the 5 years from 2013–2014 to 2017–2018 was ₹2,456.40 billion, with ₹333.65 billion losses in 2017–2018 (GOI, 2020). These losses have increased to ₹496.23 billion in 2018–2019 (PFC, 2020). The government has been regularly bailing out the sector, the last one being Ujjwal DISCOM Assurance Yojana (UDAY).

UDAY was launched in 2015 for operational and financial turnaround of distribution utilities through targeted interventions to lower the interest costs, reduce the cost of power, increase revenues, and improve operational efficiencies. A total of 27 states and 5 union territories joined the scheme. Total liability of ₹2,690 billion was to be restructured under UDAY through issuance of bonds. So far, bonds worth ₹2,320 billion have been issued, consisting of state bonds of ₹2,090 billion and distribution company (DISCOM) bonds of ₹230 billion (GOI, 2019).

The power sector woes are likely to increase in the future. In the recently concluded solar auctions, solar tariffs have reached a low of ₹2 per unit of power (compared to ₹6 per unit average cost of electricity supply for distribution utilities). The low cost of solar power means that it has reached grid parity and more, which is the primary driver for its rapid growth. Currently, India has an installed capacity of 35 GW of solar capacity, which is about a tenth of the country’s total installed power generation capacity, and there are ambitious plans to increase renewable (and solar) capacity as per India’s nationally determined contributions as part of the Paris Accord. India has pledged a reduction in the emission intensity of its GDP by 33%–35% by 2030 from 2005 levels and 40% cumulative electric power installed capacity from non-fossil fuel-based energy resources by 2030. This would obviously mean more renewables in the energy mix, pursuant to which the government had targeted a renewable capacity of 175 GW by 2022 (and 450 GW by 2030), of which 100 GW would be solar power.

The falling solar prices benefit the cause of open access in the power distribution sector (with consumers having a choice of electricity supplier just as in the telecom sector). Using open access, DMRC, for example, is sourcing 32% of its power requirements from the Rewa solar project in Madhya Pradesh. Open access in the power distribution sector is one of the neglected provisions of the Electricity Act, 2003, and operationalizing it would make the power sector competitive, which, in turn, would improve the cost competitiveness of the Indian economy.

However, the coming of age of solar power and open access in India would increase the power distribution sector’s challenges, dominated by the public sector power distribution companies (DISCOMs). These DISCOMs have existing long-term power purchase agreements (PPAs) with mainly coal-based thermal power generating projects. Any decrease in thermal power demand due to cheaper solar power and operationalization of open access would mean more financial stress for the DISCOMs. They would be required to pay the fixed costs of power. This may necessitate another DISCOM bailout soon, for which the government is ill-equipped in the current COVID pandemic times, with stressed fiscal deficit and growth rate (Pratap, 2020).

The Atma Nirbhar Bharat package refers to about ₹900 billion loan from Power Finance Corporation (PFC) and Rural Electrical Corporation (REC) to DISCOMs for payments to the power generation companies. However, without tackling the issue of low-cost recovery (there is a revenue gap of 72 paise per unit of electricity sold in the country [PFC, 2020]), there is little likelihood of the power sector becoming financially sustainable. Therefore, there would be a repeated need for bailouts in times to come. The path that the metro rail sector is following is alarmingly similar to the power sector.

THE CASE OF HONG KONG METRO

However, there is nothing in theory that precludes financially sustainable operations of metro rails. We find that Hong Kong Metro is generating huge profits year after year. Hong Kong’s Mass Transit Rail (MTR) system operates across 263 km, carrying 5.2 million passengers a day. The MTR Corporation (MTRC), which built and operates the system, reported a whopping HK$12.09 billion (US$1.56 billion) net profit in 2019. In fact, in the last 10 years (2010–2019), the net profits of Hong Kong Metro have been over US$18 billion, or an average of US$1.8 billion per year (MTRC, n.d).

MTRC follows the Rail plus Property (R + P) model. This model is based on the concept of value capture finance (VCF, which internalizes the externalities generated from large public investments). It is well accepted that the creation of infrastructure like roads or metro networks increases property values in and around the area of development. VCF aims to capture this positive externality generated through public funding to improve the financials of the project.

In Hong Kong, the government owns the land whose value is very high due to limited space. To develop the MTR system, the government entered into an agreement with MTRC, which has 70% government shareholding. The government then transferred the land and development rights to MTRC at a pre-rail price. MTRC, in turn, transferred the developmental rights to private developers at an after-rail price.

After metro rail development, the land value adjacent to the metro rail skyrocketed, and the difference between pre-rail and after-rail prices was substantial. The profit margin from this VCF mechanism was sufficient to meet the further development requirements of MTR. Also, the developer returned the land with premium value as a lease charge to the government, as well as shared a part of profit with MTRC, making MTRC highly profitable. Changes were made in the local land-use law to drive property development around stations. In some districts, a floor area ratio (FAR) of 10 was allowed to encourage dense development with a mix of residential and transport facilities.

MTRC is one of the largest property managers in Hong Kong. As of 31 December 2019, MTR managed more than 104,000 residential units and more than 772,000 m2 of office and commercial space in Hong Kong (MTRC, 2019).

Profits from property development and related business of MTRC, including Hong Kong station commercial business and Hong Kong property rental and management business, have accounted for more than 50% of MTRC’s total profit between 2000 and 2015. The R+P program enabled MTRC to capture real estate income to finance a part of the capital and running costs of new railway lines and increase transit patronage by facilitating high-quality, dense, and walkable catchment areas around stations (PPIAF, 2015).

A MORE SUSTAINABLE WAY FOR PROMOTING URBAN TRANSPORT IN INDIA

Cities are engines of growth for countries because of agglomeration economies. It has been estimated that while about a third of the Indian population lives in urban areas, it contributes two-thirds to the GDP (Sankhe et al., 2010). However, due to urbanization, there are pollution and congestion problems in Indian cities (6 of the world’s 10 most polluted cities are in India, as per the World Economic Forum, 2020). Urban transport is a major contributor to this pollution and congestion. Therefore, there is a need for more efficient urban transportation. However, the proliferation of metro rails across cities in India with little non-fare and property revenue, as is being done now, is not financially sustainable. The ameliorative measures that can be taken to improve the outcomes are suggested below.

First, it must be realized that metro rails are the most expensive form of public transport. Cheaper options like Bus Rapid Transit (BRT) System, light metro rail, etc. may be used to achieve the objective of efficient urban transportation while managing the adverse financial fallout of a full-fledged metro system.

Second, if it is decided that metro rail is the preferred option, then user charges should cover at least the operation and maintenance (O&M) costs of the metros. Low user charges and consequent inadequate cost recovery are widespread across infrastructure sectors such as metro rail, power, water, transport, and social sectors like health and education. In public utility services, full cost recovery, including both capital and O&M charges, may not always be desirable. However, reasonable user charges covering at least the O&M costs of assets would improve overall efficiency, help demand management, prevent waste, and would promote ownership and accountability. This is a measure that has been repeatedly emphasized by Finance Commissions, Expenditure Management Commission, etc.

Third, it is important that the operator generate non-fare revenue, including income generated through commercial, retail, advertising, consultancy, and other sector activities. Depending solely on user charges for the financial sustainability of metro projects is problematic because of the high capital costs of such projects.

Fourth, as apparent from the financial success of Hong Kong’s MTRC, there is a need for liberal use of VCF. The Hong Kong model has catalysed Transit Oriented Development (TOD), given the scarcity of land and the inherent need for high-density development above and near stations and depots where accessibility is highest. Achieving this density has been part of a deliberate long-term strategy for maximizing scarce land use and driving viability for the metro. The rail and property funding and delivery model for public transport projects is powerful—both for achieving financial sustainability and achieving development aims associated with transport. A key to making this work involves siting stations at the right location and providing foundations for future development. Developments are also carefully managed to ensure the mix of services that customers want. The result is developments that feed the metro in exchange for a metro that maximizes the value of developments (World Bank and RTSC, 2017). While Hong Kong is land-constrained and can generate substantial resources from VCF, the land constraint is quite pronounced in Indian cities too, making it possible to make efficient use of VCF tools.

VCF, as known widely in the world, is based on the principle that private land and buildings benefit from public investments in infrastructure and policy decisions of governments (e.g., change of land use or floor space index). These benefits are externalities generated from public investment and, hence, should not be included in user charges. Therefore, there is a need to deploy appropriate VCF tools to capture a part of the unearned increment in land and buildings value. These can be used to fund projects being set up for the public by the central/state governments and urban local bodies. This generates a virtuous cycle in which value is created, realized and captured, and used again for project investment. The Ministry of Housing and Urban Affairs has already developed a VCF policy that needs to be operationalized for metro rail development to be financially sustainable (GOI, n.d.).

Finally, if we need to expand metro rail, monetizing existing networks can provide capital expenditure (capex) funding for future expansions—an idea that can be implemented for Delhi Metro. Delhi Metro Rail Corporation is the fourth largest metro system in the world with a network length of 389 km and daily usage by about 3 million passengers. Currently, Delhi Metro Phase IV, which is 62 km long, is being built at a total completion cost of ₹249.48 billion, with external loan component of ₹129.31 billion. It would make more financial sense for DMRC to fund Phase IV’s construction by monetizing (though toll-operate-transfer model or infrastructure investment trusts [InvIT] model) one of the three completed phases of the Delhi Metro network. This will be another application of the Brownfield Asset Monetization initiative for more Greenfield investments, which is being pursued very vigorously in India’s road and power transmission sectors.

Footnotes

Declaration of Conflicting Interests

FUNDING

The author received no financial support for the research, authorship, and/or publication of this article.

Disclaimer

Views expressed are personal.