Abstract

The board of Tata Sons shocked corporate India by sacking their chairperson, Cyrus Mistry, on 24 October 2016 (a little less than four years after he was made chairperson), and replacing him with his predecessor, Ratan Tata, as an interim chairperson. The Tatas are the biggest private business group in India, comprising over 100 operating companies spread across six continents. Twenty-nine of these companies are listed with an aggregate market capitalization of ₹ 8,471 billion/US$127 billion 1 making their share 7.2 per cent of Bombay Stock Exchange’s total market capitalization (The Tata Group, 2017).

BACKGROUND OF TATA GROUP

Tata Group was founded by Jamsetji Nusserwanji Tata. It was in 1858 (Britannica, 2017) that Jamsetji joined his father’s export trading firm soon after graduation. He helped expand the company to countries such as Japan, China, Europe, and the USA. In the 1870s, he successfully set up cotton manufacturing mills at Nagpur, Bombay and Kurla. He was the first to introduce hydroelectric power plants in India, which later became part of Tata Power.

In 1901, his vision gave India its first large-scale ironworks—Tata Iron and Steel Company (now Tata Steel)—which became the largest privately owned steelmaker in India and the flagship company of the group. Over the years, the Tatas set up several large manufacturing companies over a range of products including cement, chemicals, watches, trucks, and locomotives. The Tata Group converted Jamshedpur (popularly known as Tatanagar) into a large industrial town, with schools, hospitals, and other municipal facilities.

The Tatas were equally involved in service industries such as hotels, telecommunication, broadband, and financial services. In 1998, Tata Motors launched the first fully indigenous Indian passenger car, the Indica, and in 2008 launched the Tata Nano, the world’s cheapest car. Tata Consultancy Services (TCS) was founded by JRD Tata in 1968, long before most people had even touched a computer. It is one of the largest IT service providers in the world, with a market capitalization of ₹ 4,928 billion/US$73.88 billion, contributing almost 60 per cent of the group’s total market value (The Tata Group, 2017).

GOVERNANCE STRUCTURE OF THE TATA GROUP

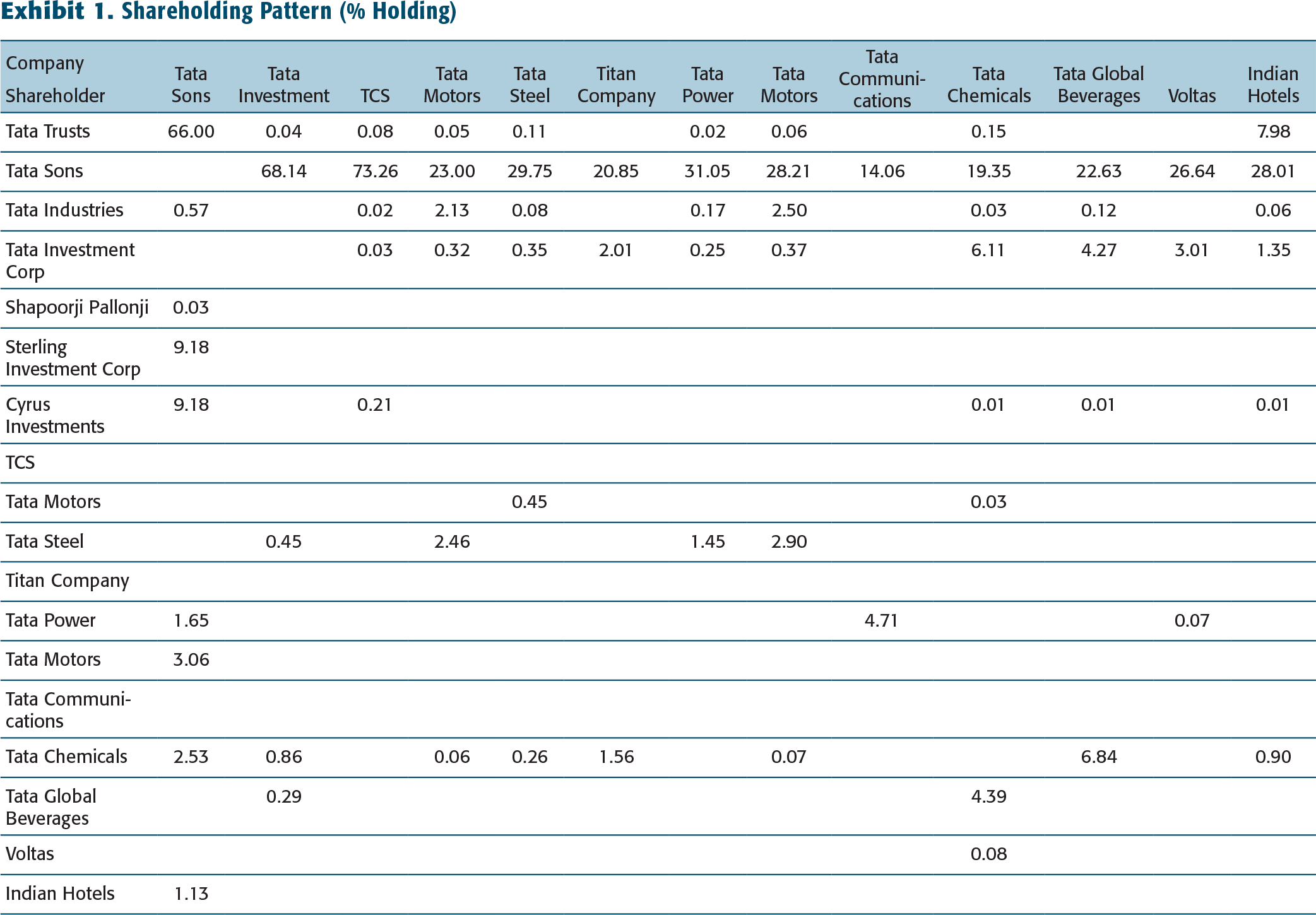

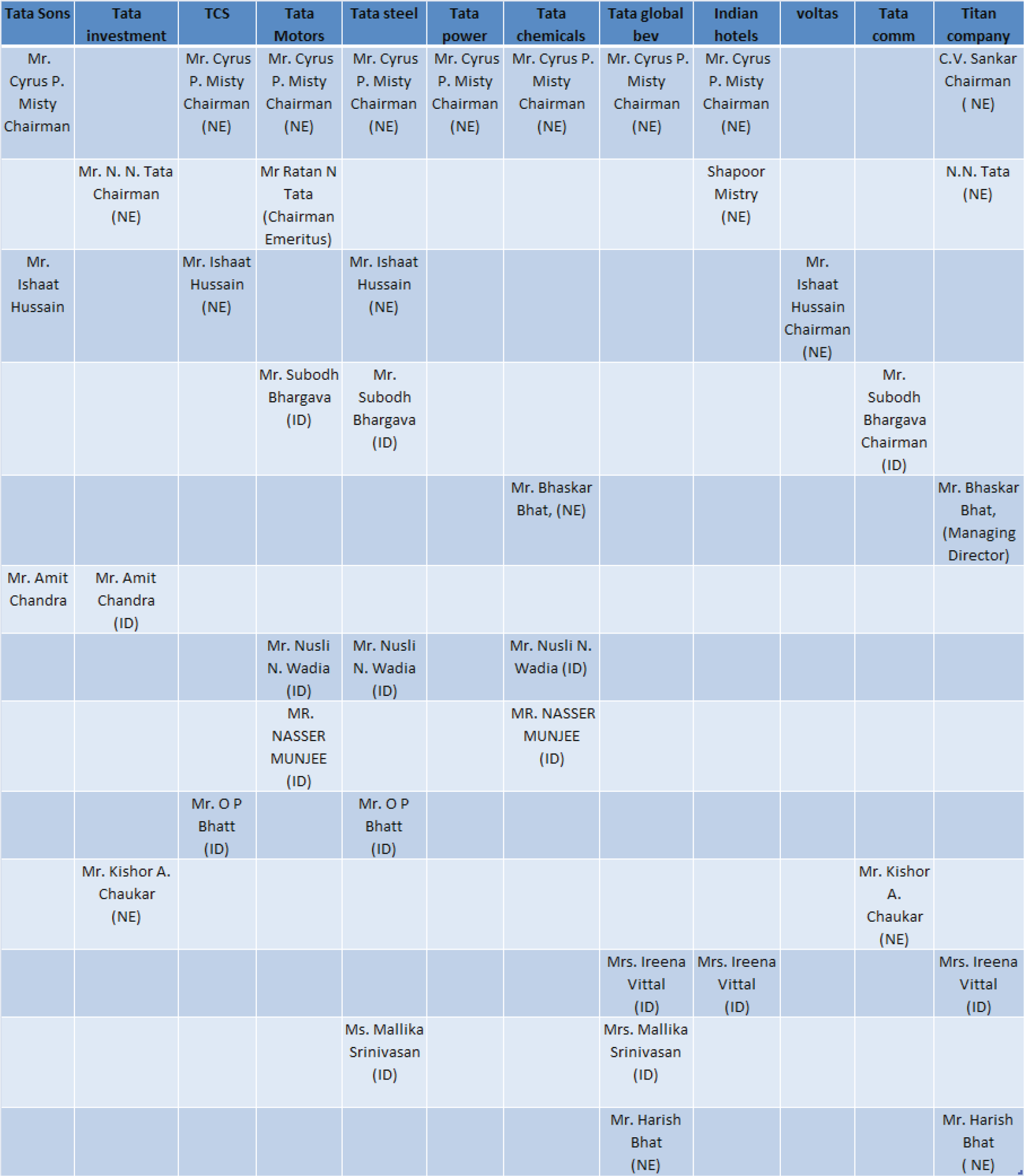

Tata Sons, as the promoter of the major operating Tata companies, owns significant shareholdings in these companies. Tata companies together are commonly referred to as the Tata Group. The chairperson of Tata Sons is the defacto chairperson of the Tata companies. The companies are further networked through cross-holdings (see Exhibit 1), interlocking directors (Exhibit 2), and even trustees.

About 66 per cent of the equity capital of Tata Sons is held by philanthropic trusts endowed by members of the Tata family. The largest of these trusts are the Sir Dorabji Tata Trust and the Sir Ratan Tata Trust, which were created by the sons of Jamsetji Nusserwanji Tata, the founder. Another 18.4 per cent is held by the Shapoorji Pallonji Group, the only other major but non-Tata shareholder in the company. A few of the bigger Tata companies also own shares in the promoter company.

Shareholding Pattern (% Holding)

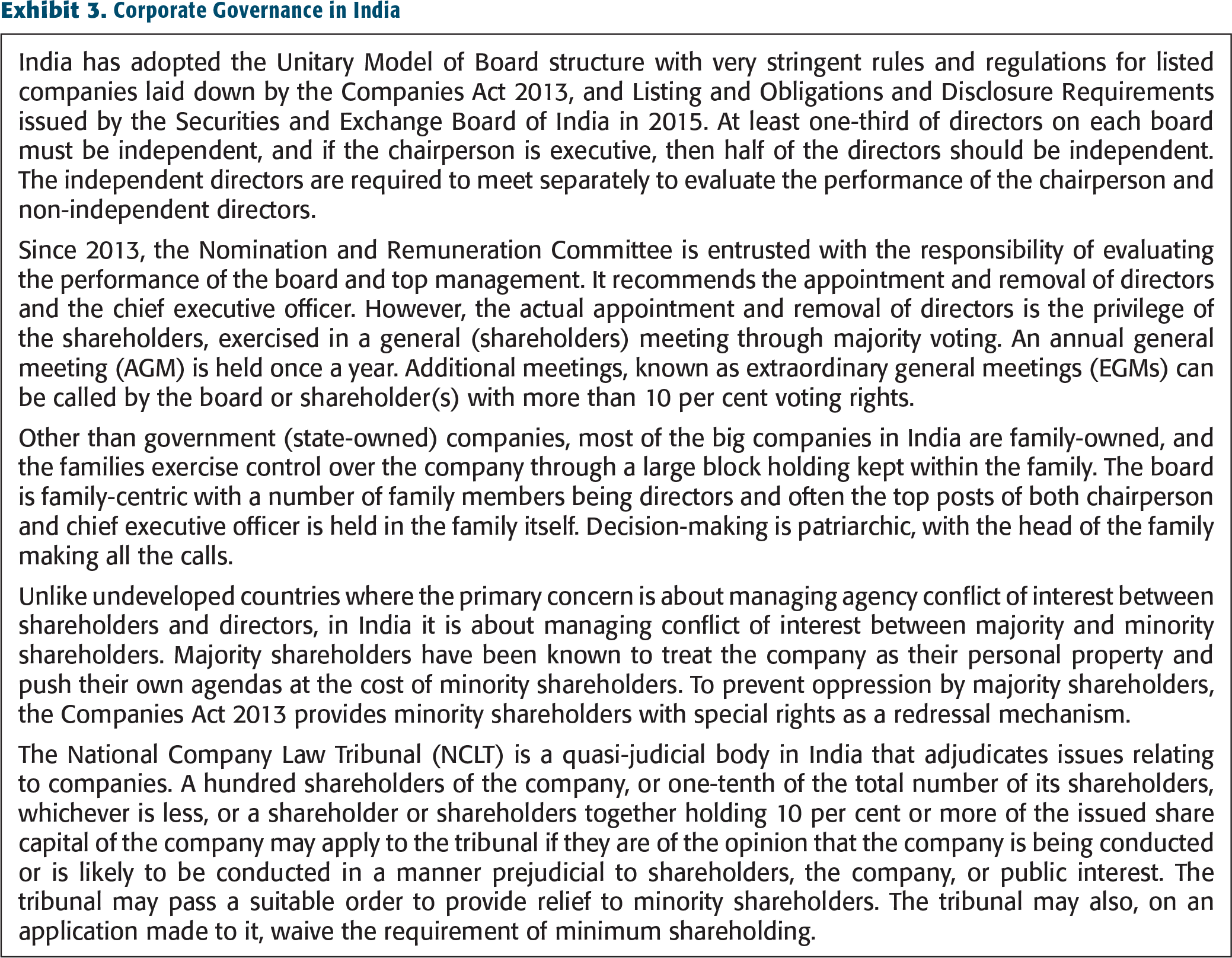

Corporate Governance in India

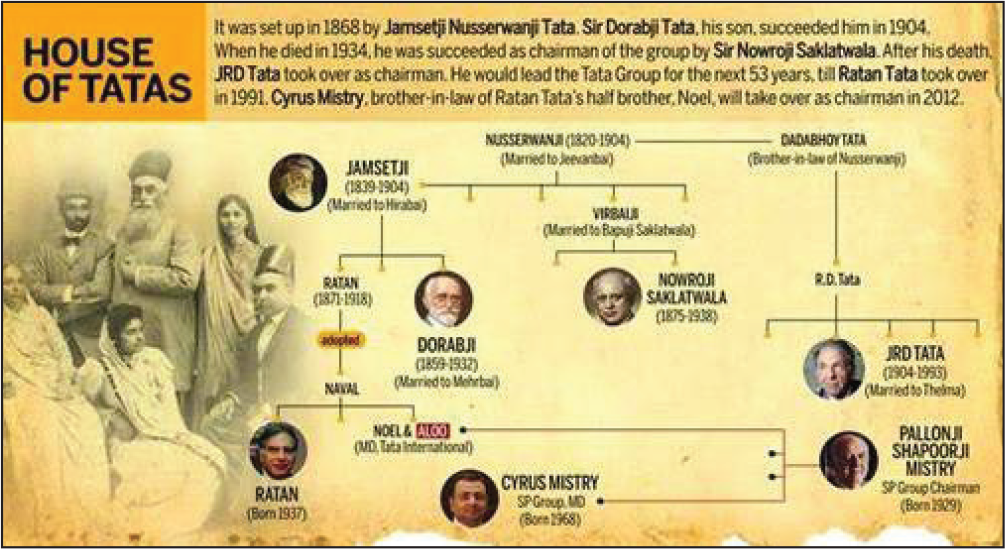

CYRUS MISTRY: A SHORT STAY AT TATA HOUSE

Cyrus Mistry, a civil engineer and management graduate from London Business School with experience of managing a big conglomerate, was chosen as Ratan Tata’s successor in November 2011. He was initially appointed as deputy chairperson of Tata Sons. On Tata’s retirement in December 2012, he was appointed as the sixth chairperson of Tata Sons to head the Tata Group. He was selected by a panel comprising of Ratan Tata, Venu Srinivasan, Amit Chandra, and Ronen Sen (who were later made board members of Tata Sons), and Kumar Bhattacharyya of Warwick, UK (who was a close friend of Ratan Tata). Incidentally, Mistry is the grandson of Shapoorji Pallonji Mistry, whose family holds 18.4 per cent equity in Tata Sons. He joined the board of Tata Sons when his father retired in 2006. According to Mistry, Bhattacharya had courted him to accept the post (Vijayaraghaven & Philip, 2016). Bhattacharyya had described Mistry at the time as ‘bright and selfless’ (The Economic Times, 2016) and Ratan Tata considered him ‘intelligent and qualified to take on the responsibility’ as chairperson (The Hindu, 2016).

Traditionally, once appointed a chairperson would remain at the helm of affairs until retirement. J. R. D. Tata was chairperson for more than 50 years, and Ratan Tata for 20 odd years until his retirement at the age of 75. Mistry, who was 48, should then have continued for a fairly long time. However, he was unceremoniously removed on 24 October 2016—a few months before his contract was up for renewal. Six board members voted in favour of the resolution to oust Mistry, two abstained, and Mistry himself voted to stay. Mistry was neither served any show-cause notice for removal nor given a chance to be heard or defend himself. Surprisingly, no reasons were provided at that time by Tata Sons for this sudden removal. A spokesperson said, ‘[t]he Tata Sons board in its collective wisdom and on the recommendation of the principal shareholders decided that it may be appropriate to consider a change for the long term interest of Tata Sons and the Tata Group’ (Ghoush, 2016). Unexpectedly, some members of the committee who selected Mistry were also among those who voted him out. However, he remained a director of Tata Sons.

It is interesting to note that before Mistry, every chairperson of the Tata Group was a member of the Tata family (see Exhibit 4). As the head of the two Tata trusts, Ratan Tata controls 66 per cent of Tata Sons and hence yields significant control as the promoter shareholder. Before Mistry was made chairperson, the post of the head of the trusts and the chairperson of Tata Sons had always been held by the same person.

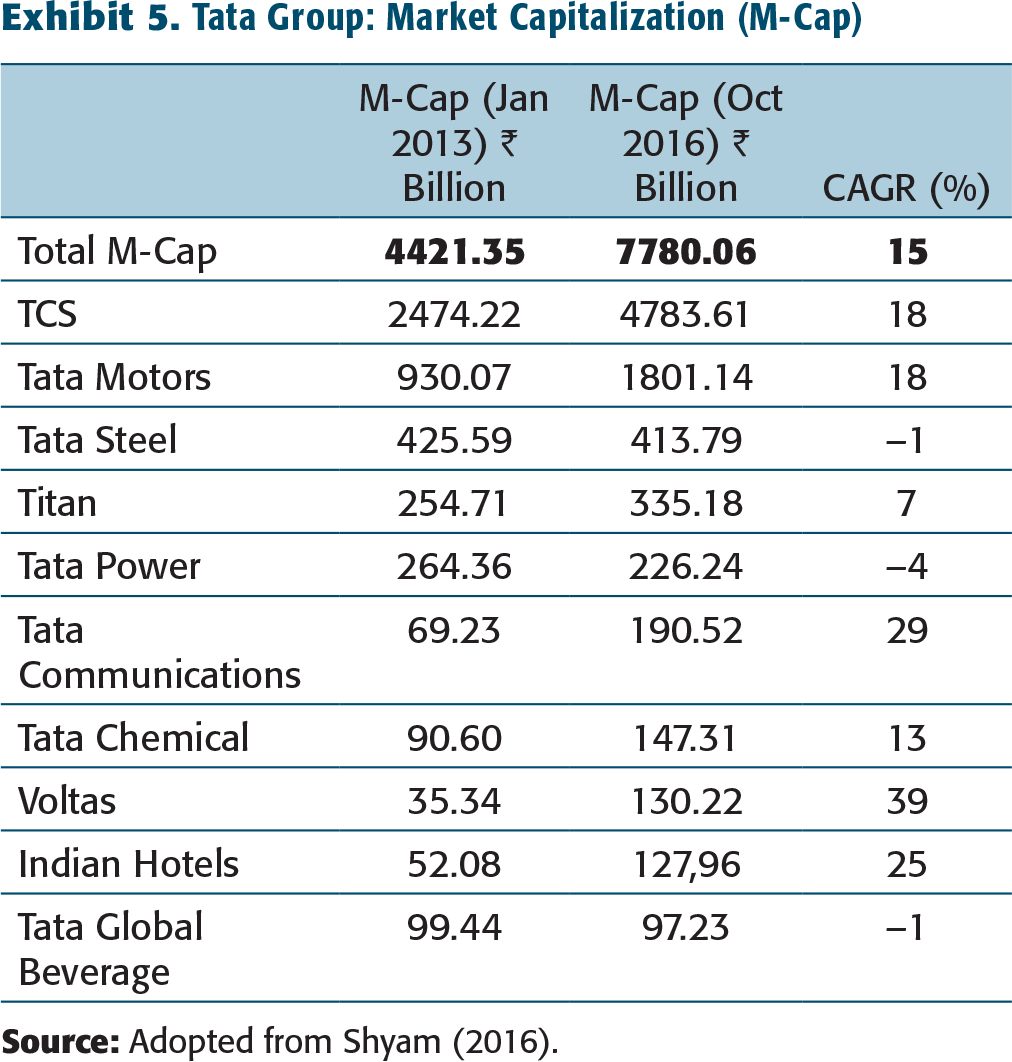

Tata Group: Market Capitalization (M-Cap)

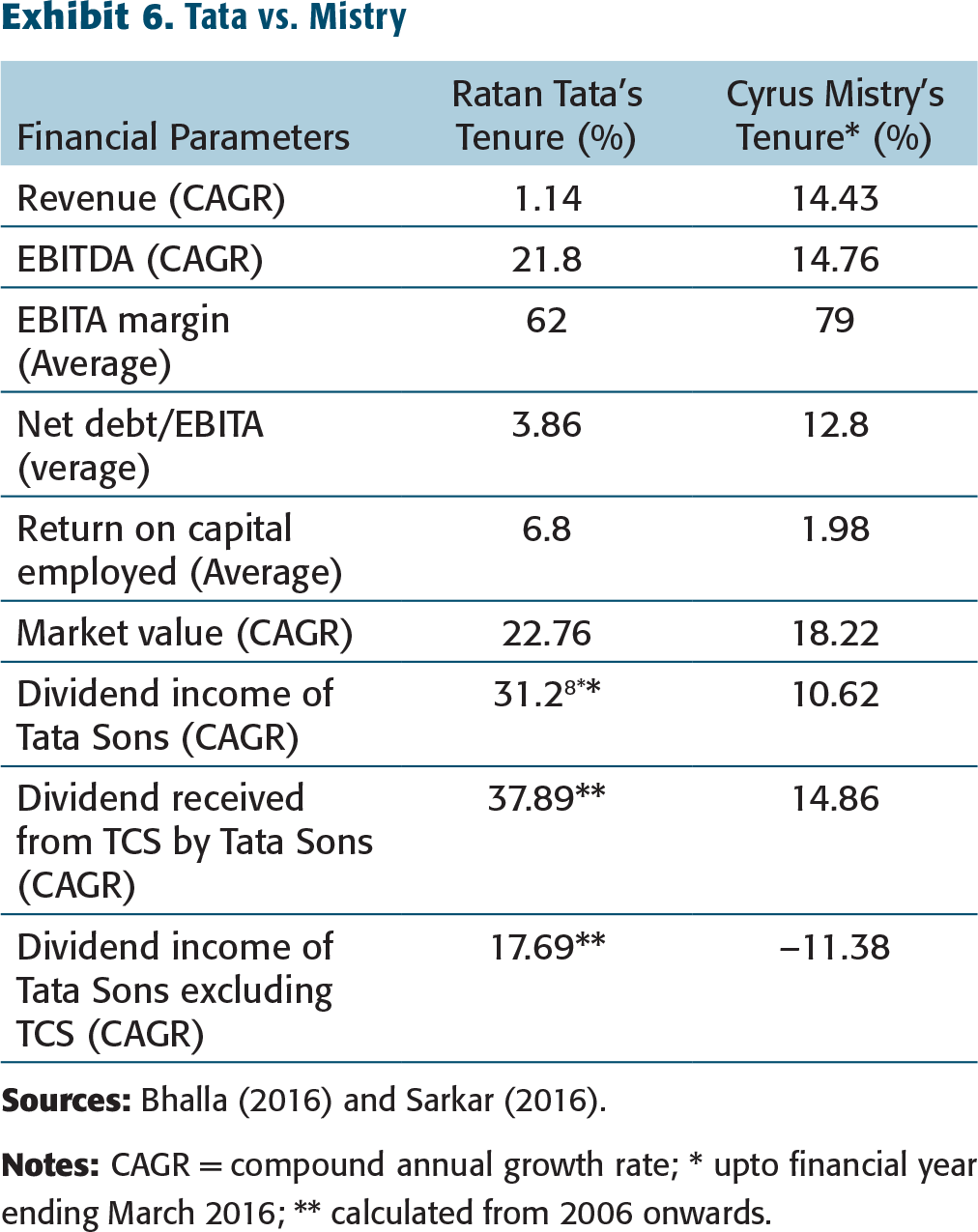

During Mistry’s tenure, the revenue grew from about ₹ 50 billion to over ₹ 80 billion, and average operating margins by 79 per cent. The market capitalization of the group showed a compound annual growth rate (CAGR) of 18.22 per cent compared to the Sensex’s 2 10.4 per cent (see Exhibits 5 and 6). This would have been much higher if it had not been for Tata Steel and Tata Power, which are debt-laden and losing market value. Tata Steel had been accumulating losses since 2009, long before Mistry was made in charge.

Tata vs. Mistry

The Tata trusts had expressed concern as their philanthropic activities were dependent on dividend income from Tata Sons. The dividend declared by Tata Sons had increased in 2011 and remained constant from 2011 to 2016, except in 2015 when it was much higher as Tata Sons had a bonus income from TCS. Hence, the Tata trusts’ income from Tata Sons was not really affected (but maybe marginally reduced, by their direct investment in other Tata companies, such as Indian Hotels, which had not declared a dividend in 2014 and 2015). Meanwhile, the trusts’ expenditure on grants and charity had increased more than their income.

Bhattacharyya, in his praise of Mistry in September 2016, just a month before the removal said as follows:

He is building firm foundations to ensure Tata’s expansion lasts not a quarter or two, but a decade and more. Tata Sons is more than just a business—it is an icon, a global symbol for doing business with integrity and long-term vision. As such, it should not be judged by the ‘market hawker’ standard of quick profits and opportunism. (Vijayaraghaven & Philip, 2016)

THE RIFT: THE MYSTERY UNFOLDS

Soon after taking charge as chairperson, Mistry replaced Ratan Tata’s selected CEOs of Indian Hotels, Tata Motors, and Tata Steel with younger persons of his choice (Datta, 2017). He sold off the loss-making and debt-burdened Corus in the UK. Ratan Tata had acquired the British company. As a result, Tata Steel had become among the top 10 largest steel producers in the world. Tata had acquired the company at an auction for £6.08 pounds per share, a 33 per cent increase from their original quote of £4.55 per share (Wikipedia, 2017). At the time, the opinion in the business world was that Ratan Tata had overpaid just to win the bid. This suggests it held significant sentimental value for him. However, it was incurring losses almost from the beginning. Uday Chaturvedi, who had worked for more than 40 years with Tata Steel and had a stint as managing director of Corus Strip Products, a unit of Tata Steel Europe, said, ‘I had foreseen in 2012 (that would be before Mistry became chairperson) that this would happen. Tata Steel had put in a huge amount of financial resources, but the technical resources were not there’ (Dutt, 2016). Tata Steel’s former managing director, J. J. Irani, said he was happy that the Tata Steel board had decided to divest the UK business (Dutt, 2016). Tata Sons, in its statement (Ray, 2016) expressed Mistry’s inability to turnaround Tata Steel Europe as one of the foremost indicators of his poor performance. When Ratan Tata became interim chair, Tata Steel had to reassure institutional investors that the sale of the UK speciality business would be undertaken as already proposed.

Mistry’s biggest mistake was probably wanting to get rid of Nano (operating at just 15% of capacity), the dream project of his predecessor—the cheapest car in the world that never really took off. Ratan Tata envisioned providing a people’s car which the middle-class family in India could afford. The much-hyped car ran into problems from day one. The original factory was meant to be set up in West Bengal. However, due to political agendas and social activists challenging the acquisition of farmers’ land, the plans had to be changed. The factory finally relocated, but this led to significant delays and cost escalations. The car had already been priced at ₹ 1 lakh, half the price of the cheapest car anywhere else, making the project unviable from the beginning. Ratan Tata, while unveiling the Nano in 2008, said, ‘[s]ince a promise is a promise the standard dealer version will cost ₹ 1 lakh’ (Krishnakumar, 2008). Later, due to some technical glitches, a few cars caught fire on the road. The Indian customer (who had once lined up to buy the Nano) rejected it.

J. R. D. Tata set up the first airlines in India—Tata Airlines—in 1932. It was later taken away from the Tatas and made the national carrier, Air India. In the early 1990s, private airlines were again permitted in India, Ratan Tata began trying to set up another airline business. The Tatas re-entry in the airline industry, which hits an emotional chord for the group began with a joint venture with Air Asia in 2013. Overcoming several setbacks, a new airline under the brand of Vistara was finally launched in January 2015 (along with Singapore Airlines, where the Tatas have a majority stake). Mistry, on the contrary, was reluctant to pump more money into the aviation business.

Dissatisfaction with how Mistry handled the Docomo negotiations with the Japanese partners in the telecom business was the final nail in the coffin. The two have very different leadership styles and business strategies. The simmering discontent slowly reached its boiling point. In 2011, when Ratan Tata cherry-picked Mistry, it was seen as the victory of youth. ‘Be your own man’, was Tata’s advice to his then 43-year-old successor (The Hindu Business Line, 2012). ‘But soon, youth was perceived as insolent, precocious and out to destroy the core values that the group stood for, for close to 148 years’ (Kalesh et al., 2016). The Tata Sons board claimed that Mistry was removed as they were not happy with his performance. Yet just a few months earlier, on 25 June, the Nomination and Remuneration Committee of the Tata Sons board had put on record an appreciation and recommended a raise for the chairperson, Cyrus Mistry.

Mistry, in a letter to the Tata Sons board the day after his removal, commented as follows:

Prior to my appointment, I was assured that I would be given a free hand. The previous chairman was to step back and be available for advice and guidance as and when needed. After my appointment, the Articles of Association were modified, changing the rules of engagement between the Trusts, the Board of Tata Sons, the Chairman, and the operating companies. (First Post, 2016)

Mistry has alleged that he was reduced to being a ‘lame duck chairman’, while Ratan Tata remained a towering figure influencing the decisions even during the board meetings, which forced him to circulate a corporate governance note ‘in order to clarify the distinct roles of Tata Trusts, Tata Sons Board and the Boards of the operating companies’ (First Post, 2016). On 25 June, the Nomination and Remuneration Committee of the Tata Sons board had discussed formalizing the governance structure among various entities of the group such as Tata Trusts, the trustees, boards, and directors of group operating companies, and the same was up for discussion in the 25 October board meeting.

Ratan Tata, on the other hand, argued that Mistry made it his personal fiefdom, took unilateral decisions, and did not keep the board apprised of major decisions even though he had been specifically asked to do so, particularly for large capital investments and appointment and pay packages of senior management. Further, they contended that construction dealings with Pallonji Group caused a conflict of interest. Pallonji has historically carried out construction activity for the Tata Group, and most of the projects were ongoing from before Mistry took charge.

His selection of leaders was also questioned. It was argued that he had failed for two years to appoint a CEO for Tata Motors, and the position of group CFO was vacant for three years (Barman, 2016). Mistry had, in fact, given three options for CEO of Tata Motors; all of them were rejected.

THE CORPORATE MAHABHARATA 3 : A WAR OF MANY BATTLES

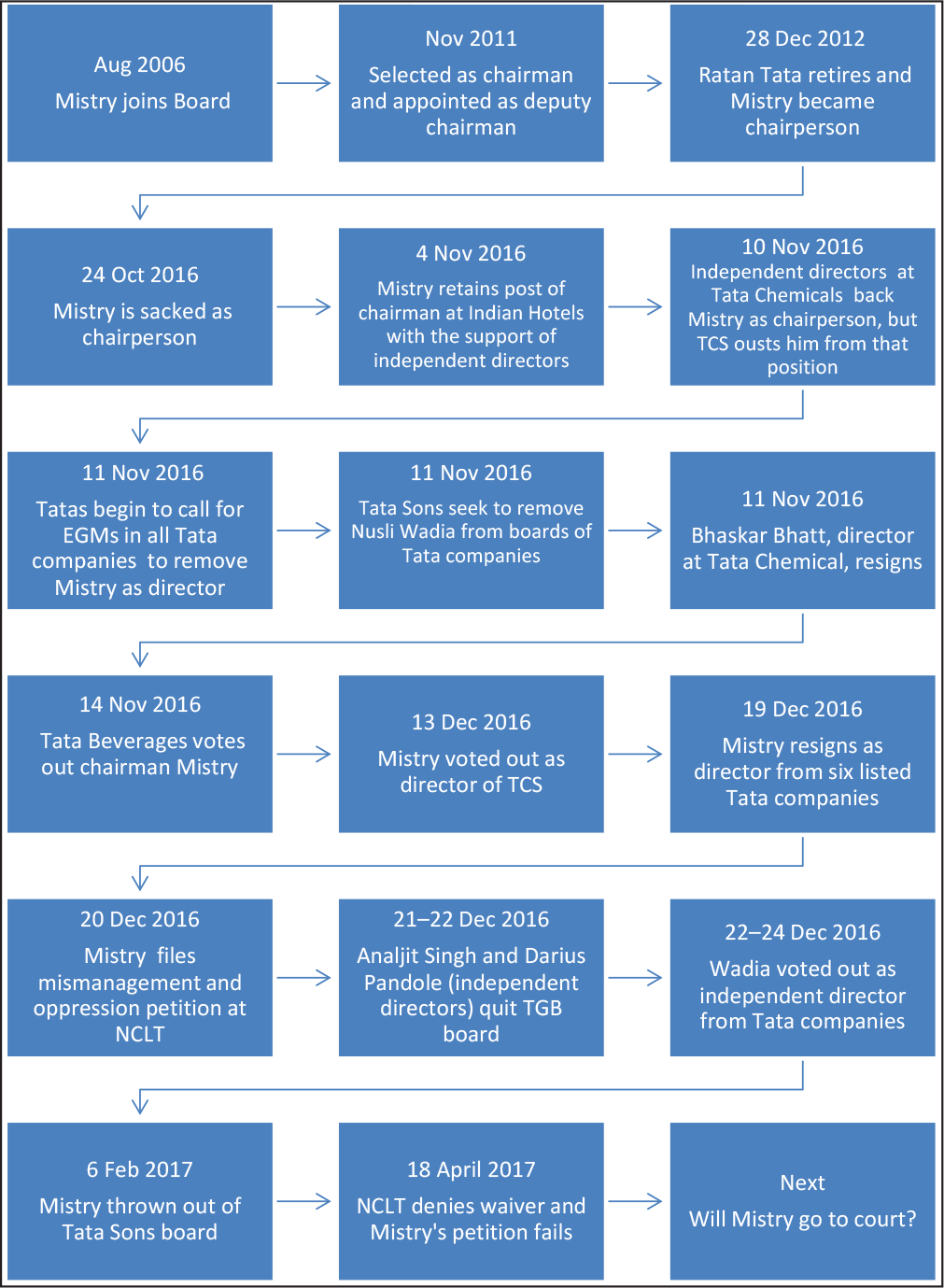

The corporate war between the Tata and Pallonji family that began with the first attack on 24 October was fought over many boardroom battles, EGMs, and legal clashes (see Exhibit 7). After sacking Mistry from the chairpersonship of the Tata Sons board, they began proceedings to have him fired as chairperson from other Tata companies’ boards too.

The first boardroom battle was won by Mistry as he retained the chairpersonship at Indian Hotels with the support of the independent directors. Tata Chemicals also backed him, citing good performance. Independent directors at Tata Motors refused to take sides, but said they stood by decisions that were made by the board. This was also the case with Tata Steel.

The setback began with Tata Sons exercising their rights under the Articles of Association of TCS to remove Mistry from the chairperson’s post (The Economic Times, 2016c). This was followed by seven of ten directors and three out of five independent directors of Tata Global Beverages (TGB) voting against him (Mandavia, 2016).

The Corporate Mahabharata

Meanwhile, EGMs of the Tata companies were called by Tata Sons for passing a resolution removing Mistry as director. Passing a resolution requires a 51 per cent majority. Tata Group owns 25 per cent to 35 per cent of the equity in the listed companies of the group (with the exception of TCS, where they own more than 70%), and therefore they needed to garner the support of other shareholders.

Road shows were conducted to woo both foreign and domestic institutional shareholders. Ratan Tata personally met top Life Insurance Corporation (LIC) executives. LIC is the largest institutional investor, with 13 per cent shares in Tata Steel and Tata Power, and about 10 per cent in TGB (The Economic Times, 2016d). Tatas also planned to buy more shares of Tata Motors so they would hold enough voting power to take out Mistry at the EGM.

Mistry was voted out in the EGM of TCS. Interestingly, 44 per cent of institutional shareholders abstained from voting, and it was a close call with 42.5 per cent of those voting, supporting Mistry and 57.5 per cent voting against him. Of the 40 shareholders who spoke at the EGM, only 5 even brought up the issue (Mendonca & Mandavia, 2016). Finally, on 19 December, Mistry resigned from the board of all listed companies, including Tata Power, Tata Motors, Tata Chemicals, Tata Steel, and India Hotels. He cited his reasons as, ‘best interests of employees, shareholders and other stakeholders of the Tata Group would be better served by moving away from the forum of the extraordinary general meetings … to a larger platform and also one where the rule of law and equity is upheld’ (Business Standard, 2016).

Other directors got caught in the crossfire. Non-executive, non-independent director of Tata Chemicals, Bhaskar Bhatt, who was also the managing director of Titan and chairperson of Tata Singapore airlines, resigned in protest. After independent directors of Indian Hotels and Tata Chemicals supported Mistry, Tata Sons advised independent directors of Tata companies to think carefully about the future of the group in their decision. Nusli Wadia of Bombay Dyeing, an independent director of TCS, Tata Steel, and Tata Motors had been associated with Tatas for several decades (having joined the Tata Steel board in 1979). He had helped them deal with heavyweights such as Russi Modi (the former chairperson and managing director of Tata Steel). When Wadia voted in favour of Mistry, Tata Sons sought to remove him as director of these companies for ‘acting in concert with Cyrus Mistry against the interest of principal shareholder’ (The Economic Times, 2016a). Following Mistry’s resignation, independent directors, Analjit Singh and Darius Pandole, also quit the TGB board.

Mistry challenged his ouster at National Company Law Tribunal (NCLT) by filing a petition of mismanagement and oppression of minority shareholders, through Cyrus Investments Pvt. Ltd and Sterling Investments Pvt. Ltd, which together hold 18.4 per cent in Tata Sons, mostly through preference shares. However, the petition was not accepted, as their ownership falls to 2.17 per cent if preference shares are not considered, making it less than the 10 per cent required by the Companies Act. Their request for a waiver of minimum holding on account of public interest was denied. Mistry can now go to court or let bygones be bygones.

The war saw key players take sides with two camps forming, each slamming the other with accusations and defamatory statements. It was as mucky as two politicians of opposite parties contesting for a seat, thrashing each other out in the media.

GOVERNANCE PITFALLS IN FAMILY-RUN BUSINESSES

This case highlights governance intricacies in large family-run businesses struggling to balance the interest of the promoters with the interest of all the other stakeholders in the network of companies of the group.

Family Dynamics

What was the basis for selecting Cyrus Mistry? Was it his professional capability, as claimed? There is no solid proof of poor performance; a conservative view may be that jury is still out. But what is on record is that his performance was awarded a raise in remuneration just four months before his dismissal.

Did he become chairperson by virtue of his family holding in the group? Ratan Tata has no children; his half-brother, Noel Tata, was initially expected to take over from him. However, Noel was never among the big boys. The relations between the Tatas and the Pallonjis have been cordial over the years. The catch is that Mistry is married to Noel’s sister. Was appointing Mistry some sort of a family compromise that later fell through?

Family dynamics strongly influence the governance of family businesses, and family feuds can lead to splits in a company (Reliance Group being a point in case) and even its downfall.

Promoters’ Need for Control

Traditionally, family businesses have always been run by a member of the family. In recent years, companies are coming around to the idea of having their businesses run by professional managers. Businesses are the babies of the promoter, raised with their blood and sweat. Promoters want to continue having a say in major decisions. Seeing someone else now deciding the future of the company is very difficult for them, particularly if it is being taken in a different direction. They are apprehensive about their legacy being destroyed. Clearly, in Ratan Tata’s mind, his legacy was slowly vanishing before his eyes.

Group Overshadowing Companies

The purpose of having the chairperson of the holding company as the chairperson of other companies is that decisions taken all across are in the interest of the group as a whole, even if they are to the detriment of individual companies. Tata Power’s decision in June 2016 to acquire Welspun Renewables without informing Tata Sons had not been well recieved and had been one of the factors for firing Mistry. Tata Power’s board had unanimously approved the deal. There is no legal argument for Tata Sons, the promoters, to be kept abreast of decisions of other Tata companies, and needless to say, prior approval is completely out of the question. The company’s right to make corporate decisions belongs to its board, and bigger decisions need the approval of shareholders in a general meeting. Giving promoters any special say violates the fundamental principle of corporate governance that each shareholder, small or big, has the same rights. A group of foreign institutional investors (FIIs) holding more than 10 per cent shares of Tata Motors had expressed similar concerns to its board (The Economic Times, 2016d). Directors and senior executives have a fiduciary duty to keep company information confidential unless it is officially made public. On the same grounds, on ceasing to be a director, Ratan Tata, by virtue of being a major shareholder, had no basis for influencing the board of Tata Sons.

Dependence on Group

One of the strengths of the Tata Companies is the use of the brand name ‘Tata’. But for using it, each company has to pay a royalty to Tata Sons, notwithstanding that the brand has been built because of the older operating companies in the group. The Tata team had threatened withdrawing rights to the use of the brand name and loan guaranties if Mistry remained at the helm. This would have been detrimental to the business of the companies. Group companies are dependent on the group for resources—financial, legal and technical know-how; and often shared common brands and infrastructure such as software platforms or business processing units. Inter-company business and trading is prevalent. The entire business and governance structures are built in a way that companies are heavily interdependent. FIIs who own 13 per cent equity had objected to independent directors about cross-holding of Tata Steel (Bhalla & Singh, 2016). In the past, it has been seen that when resources, specifically funds and corporate heads, are taken away from healthy profit-making companies to save a sinking ship, the whole group is brought down as a result.

Several proxy advisory firms had recommended to shareholders to vote in favour of the removal of Cyrus Mistry as director from TCS. This, despite agreeing that there was no clear justification for it and that the company had performed well under his guidance. But his continuance would have split the board into two and ultimately affected performance and eroded value (Mendonca, 2016). Mehta, an independent director, when questioned by shareholders at the EGM of TCS said that independent directors supported the move because ‘[w]hen you have lost the support of the promoter, and when that trust has broken down, it goes beyond performance’ (Mendonca & Mandavia, 2016).

Risk of Insider Trading

Giving prior information to the promoter about board proposals could be considered as disclosing price sensitive information, triggering insider trading provisions. Insider trading by promoters has been a concern not only in India but also across the world, including in the UK and the USA.

Insider vs. Outsider

All decisions in a family-run business are taken with a view of the long-term benefits of the family. They are not only interested in tomorrow or even next year, but in the growth, success, and survival for generations to come. Professional managers need to prove their performance through quarterly and annual results, their appointment and remuneration is usually tied to them. Thus, they tend to hold a short-term view. The difference in strategy between Ratan Tata and Cyrus Mistry could stem from this. Ratan Tata did not have to prove his mettle or justify his appointment in the short run. As one shareholder pointed out at the EGM of TCS, if Noel had been appointed, the chairpersonship would have remained in the Tata family, and these problems would not have arisen. Unclear roles and a split in power between the chief trustee, a family representative, and the chairperson, an outsider, had proved detrimental.

Family vs. Company

Family managers tend to make decisions that balance the interest of the family and company. Emotions and sentiment seep into the decision-making process (unwillingness to sell Nano, steel units of Europe). Appointment to key managerial posts is kept in the family, or outdated ancestral factories are held on to because a great-grandfather built them, or because they have been in the family for generations. Professional directors, as agents and trustees, are expected to protect the interest of all shareholders. As stewards, it is their duty to steer the company in a way that best achieves its goal. This can lead to family interests being hurt, and thus the promoter being unhappy with the chosen non-family chairperson or chief executive officer.

Succession Planning

Just like in the days of royals, training the prince would begin from early childhood so that when the time came, he would become a great king and rule his kingdom well, business families such as the Tatas or Birlas start grooming their children from a young age in a manner that instils in them a business acumen enabling them to take charge of the business empire. However, the problem arises when there is no child, or the child is not upto the task—or perhaps is not willing. Mistry was brought in just one year prior to Ratan Tata’s retirement. No long-term succession planning was put in place. Business families in India, like kings, crave a son to carry on their family name and (business) empire. In the absence of a natural son, they adopt one. Ratan Tata chose not to have a family. He should then have mentored someone to become his successor, who would then share his values and management style.

Dilemma of Independent Directors

Independent directors do not owe allegiance to major shareholders. Their fiduciary duty is to promote the interest of all shareholders. The Code for Independent Directors enshrined in the Companies Act, 2013 states that an independent director must

exercise his responsibilities in a bona fide manner in the interest of the company; refrain from any action that would lead to loss of his independence; assist the company in implementing the best corporate governance practices, safeguard the interests of all stakeholders, particularly the minority shareholders and balance the conflicting interests of the stakeholders. (Ministry of Corporate Affairs, 2013)

In family-controlled businesses, the whole purpose of independent directors is to protect the interest of the minority. If, in their wisdom, they wanted to support Mistry, then so be it. But if the Tatas withdrew their support, the company would suffer, and as a consequence, minority shareholders would see their investment value fall. The EGM notices of TCS and other Tata companies expressed the board’s support of the principal shareholder’s desire to remove Mistry as a director. TGB, in its statement removing Cyrus as chairperson, stated it was done ‘keeping in view the long term interest and alignment of all stakeholders and stability’ of the company (The Economic Times, 2016b). Any stance against Tata Sons would lead to the possible removal of directors, as was seen in the case of Wadia. While defending his standpoint, Wadia, iterated that as an independent director of Tata Steel his ‘fiduciary duty is only towards Tata Steel and not an undefined Tata Group’ (Singh, 2016). Independent directors are vulnerable, and they serve at the pleasure of the promoter. Both appointment and continuation of independent directors is at the mercy of the majority shareholder, putting their independence into question. One solution to this could be that the promoter/majority shareholder is not allowed to vote in the appointment or removal of independent directors.

Independent directors not coming to a common stance has raised some eyebrows. Butshould independent directors hold a common view, or do contradicting views indicate ‘independence’, and therefore good governance? If everyone thinks alike, is there a need for a board of directors, or will one director be enough?

Inactive Non-Promoter Shareholders

The lack of active participation by institutional shareholders and small shareholders gives promoters unchallenged power. Almost half the institutional shareholders, including LIC, the largest institutional investor in Tata companies, and more than 80 per cent of the public shareholders did not even vote in the EGM held by TCS to oust Cyrus Mistry. Hardly any of them enquired about the reasons for his removal. Only one shareholder challenged the actions of the Tatas and the role of independent directors. Expressing his dissent and asserting that Mistry was chairperson of the company and representative of all shareholders, he yelled, ‘I don’t understand what you mean Tata has lost confidence. (Mistry) is my chairperson. What has he done that you have lost trust in him?’ (Mendonca & Mandavia, 2016). The need for enhanced activism by institutional and retail investors is all the more pronounced in family businesses—not only to act as a check and balance on the powers of the board but, more importantly, to control the promoter’s supremacy.

Board Processes

Board processes are very loosely structured, and deliberations and decision-making processes can tend to take on an informal turn. The dominant member, generally the promoter, is able to control and steer discussions. The agenda of Tata Sons did not include the removal or replacement of the chairperson of the board. Mistry was removed without show-cause notice or a chance to defend himself. In fact, alteration of articles of Tata Sons to allow Ratan Tata, post-retirement, to participate in the board meeting is itself questionable.

Also at TCS, Tata Sons used their powers under the Article of Association to remove Mistry without passing any board resolution (The Economic Times, 2016e). The board processes at TGB was also questioned, as they failed to provide the video recording of the meeting in which Mistry was removed. 4 TGB later passed a circular resolution confirming the removal, to prevent any legal action (Vijayaraghaven & Mandavia, 2016). Resolutions are circulated for routine matters or in an emergency when it is not possible to hold a meeting. If removing a chairperson is unusual, doing it by circulating a resolution was unprecedented.

Ethics of Corporate Leaders

Since usually, one or two people exercise full control in family firms, the culture and values of the organization depend on the ethical behaviour of these individuals. Ratan Tata’s unceremonious removal of Mistry and Mistry’s refusal to step down from Tata group companies reflect their ethical standards. The blatant disregard and mutual public mud-slinging leave much to be desired in terms of behavioural benchmarks being set by the captains of Indian industry.

A MISTY FUTURE

The Tata trusts are registered as philanthropic entities, which entitles them to tax exceptions, raising questions of their direct involvement in corporate affairs. The public feud has caught the attention of the income tax department of India which is reassessing the status of the trusts. The whole episode has impacted the 148-year-old conglomerate’s image in the eyes of its stakeholders and its reputation as a good corporate citizen. Tata trusts’ partnering with the Department of Science and Technology of India to fund social entrepreneurship is probably a move to rebuild it.

The removal of Mistry from the group is still mystifying. The praises levied by NCLT judges on Tata Group appear uncalled for, and thus are suspicious. The Mahabharata was about the victory of good over evil, but in this case, who is the good one, and who the evil one? When Mistry was removed, Ratan Tata informed the prime minister and later even met up with the finance minister of India (Samanta, 2016). Is there more going on than meets the eye?

What is clear is that the governance framework between the three powerhouses—Tata trusts, Tata Sons, and the listed Tata Group companies—must be addressed. This will also determine how succession planning happens in each of them, and who gets to sit on the US$100 billion throne. 5

The boardroom battles witnessed in India’s biggest conglomerate portray the weakness in governance systems of modern corporations. Are companies the right framework for our businesses, or do we need to rethink the legal structure under which they operate?