Abstract

The research article has been divided into three sections to achieve the core aim. The first section provides a background to the paper. The second section compares the essential provisions in the United Nations Commission on International Trade Law (UNCITRAL) Model Law with the relevant provisions of the Insolvency and Bankruptcy Code, 2016 (IBC). The third section explores the challenges and opportunities regarding the cross-border system in the IBC, including a critical analysis of the Insolvency Law Committee’s (ILC) recommendations. The last section of the research article lays down the concluding remarks and suggestions.

The main findings of the research article can be summarized in three points. First, the UNCITRAL Model Law can serve as a great blueprint for designing the cross-border insolvency system in India. As evident from a reading of Sections 234 and 235 of the IBC, the scheme of entering into separate bilateral agreements or issuance of letters of request is not very efficacious, and therefore, the Indian transnational insolvency system should have a proper mechanism of cooperation and coordination between local courts and insolvency representatives on one hand, and foreign courts and foreign representatives on the other hand. The ILC’s recommendations should be given due regard in this scenario.

Second, while the ILC has recommended the retention of the public policy exception, it may be invoked to deny recognition of foreign proceedings. This can be a huge challenge for the foreign creditors who seek to get relief under the cross-border insolvency system as proposed under the IBC. Third, with the incorporation of a separate part in the IBC, in consonance with the recommendations of the ILC, it is possible to have a robust cross-border insolvency framework in place. However, certain changes as proposed by the author may be beneficial to the policymakers.

First, the foreign creditor may lay claim on the assets of the corporate debtor in a different country wherein the proceedings have been initiated. In this case, if the creditor is Mr X and the company is ABC Ltd, would Mr X follow the cross-border insolvency process as required by the country, P, where proceedings have been initiated against ABC Ltd? Second, the corporate debtor may have assets in more than one country, apart from the country where the proceedings have been initiated. For instance, if ABC Ltd has five branches or places of business, R, Q, S, and T, apart from the principal place of business, P, and the proceedings have been initiated in P, how would the insolvency process affect the foreign creditor? Third, if the corporate debtor is subjected to multiple proceedings in P, Q, and R, how would the foreign creditor, Mr X, get relief in this instance? The recognition and enforcement of such proceedings would depend on the system adopted by the country concerned. There could be three scenarios in this regard.

First, if the country follows the ‘territorialism’ approach, it would resort to its domestic set-up for resolving the cross-border insolvency (Trautman et al., 1993). One example would be Singapore which under the old Companies Act followed this school of thought (Halimi, 2017). Second, if the country follows the ‘universalism’ approach, the proceedings in the debtor’s home country would gain worldwide recognition in the other countries where it has assets (McCormack, 2012). This concept has been articulated by Lord Hoffman in the Cambridge Gas Corp case (Cambridge Gas Corp v. Official Committee of Unsecured Creditors, 2006). He stated that universalism in insolvency proceedings is a concept that should be treated as the golden thread of common law. However, subsequently, the judiciary in the United Kingdom showed an inclination to adopt another school of thought which has been discussed further.

Third, if the country follows the ‘modified universalism’ approach, it would ask the other competent countries to try out the proceedings in their respective courts to yield to the jurisdiction of that country’s court for a more equitable allocation of the corporate debtor’s resources or assets if the main assets of the debtor are located in that country (Clift, 2004). One example in this regard would be the United States, wherein Chapter 15 of the Bankruptcy Code refers to the United Nations Commission on International Trade Law (UNCITRAL) Model Law (US Bankruptcy Code, Section 1501). The Model Law espouses the concept of modified universalism. The rationale behind this school of thought is that instead of pursuing corporate insolvency in a piecemeal manner, it is better that one court takes charge of the proceedings and distributes the assets as per the relevant provisions and principles. The critical question that arises at this stage is this: What is the scheme in India concerning cross-border insolvency?

The Insolvency and Bankruptcy Code (IBC) is an important piece of legislation that seeks to make the insolvency resolution process more robust, quick, and efficient. It consolidates and amends the laws relating to the insolvency resolution process for companies, LLPs, partnership firms, and individuals (IBC, Preamble). It has repealed some of the previous outdated laws such as the Presidency Towns Insolvency Act, 1909 and the Provincial Insolvency Act, 1920 (IBC, Section 243, subject to certain savings), while amending certain other laws such as The Indian Partnership Act, 1932, The Central Excise Act, 1944, The Income-tax Act, 1961, The Customs Act, 1962, The Recovery of Debts due to Banks and Financial Institutions Act, 1993, The Finance Act, 1994, The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002, The Sick Industrial Companies (Special Provisions]) Repeal Act, 2003, The Payment and Settlement Systems Act, 2007, The Limited Liability Partnership Act, 2008, and The Companies Act, 2013 (IBC, Sections 245–255).

The Code contains a provision for overriding other laws. This was tested in the Innoventive Industries Limited case wherein the Supreme Court held that the IBC is an exhaustive code on the subject of insolvency relating to corporate entities (Innoventive Industries Limited v. ICICI Bank Limited, 2017). The IBC also focuses on developing entrepreneurship in India, maximizing the availability of credit in the market, balancing the interests of the relevant stakeholders, while also establishing the Insolvency and Bankruptcy Board of India in the country (IBC, Preamble). The IBC contains five parts, dealing with aspects such as insolvency resolution and liquidation for corporate persons, insolvency resolution and bankruptcy for individuals and partnership firms, and regulation of insolvency professionals, agencies, and information utilities. The scheme dealing with cross-border insolvency is contained in just two provisions under Part V of the Code. At this point, it is pertinent to have a brief overview of the history leading to the inclusion of the cross-border insolvency provisions in the IBC.

There have been some studies on the incorporation of cross-border insolvency provisions in India. In 2000, the high-level committee on Law relating to the Insolvency and Winding Up of Companies, under the chairmanship of Mr Justice V. Balakrishna Eradi, suggested an amendment to the Companies Act, 1956 for the inclusion of provisions relating to cross-border insolvency along the lines of the Model Law (High Level Committee on Law, 2000). The report of The Advisory Group on Bankruptcy Laws, under the chairmanship of Dr N. L. Mitra, is one of the most comprehensive studies dealing with cross-border insolvency in India. The report advocated the adoption of the Model Law in the country (Export Committee on Bankruptcy, 2001). The most recent Bankruptcy Law Reforms Committee (BLRC) report also emphasized the importance of having a framework to deal with cross-border insolvency in India. The BLRC specifically mentioned in its Interim Report that there is a requirement of deeper analysis before the adoption of a framework based on the Model Law.

The BLRC also emphasized that other documents including the EC Regulation on Insolvency Proceedings, the American Law Institute’s NAFTA Transnational Insolvency Project, and the International Bar Association Cross-Border Insolvency Concordat, may be considered before drafting the domestic cross-border insolvency framework (Bankruptcy Law Reform Committee, 2015). Additionally, it noted that the adoption of the cross-border insolvency scheme should take place after the other provisions of the IBC have been adopted as the success of the former would depend upon the success of the latter. The Insolvency Law Committee (ILC) is one of the latest bodies to provide comments relating to the cross-border insolvency system in India. It underscored the need for a comprehensive cross-border insolvency framework in the country in its first report (ILC, 2018a, p. 13). However, similar to the observations of the BLRC report, it noted that the adoption of a framework along the lines of the Model Law is a complex exercise and would require an analysis of international practice in this regard. The ILC report highlighted that recommendations relating to cross-border insolvency would be released upon the completion of such an exercise.

The ILC released its second report advocating the inclusion of the draft Part Z in the IBC (ILC, 2018b, pp. 50–69). The Committee recommends that the cross-border system under the Code can be initiated for corporate debtors. It can be expanded to cover individual insolvency subsequently. It refers to Singapore as an example. The Committee also recommends certain amendments to the current provisions under the Code, including Section 234, to make room for the smooth streamlining of the new Part. The ILC unambiguously recognizes that the current cross-border system is a mechanism that is bound to encounter delays and uncertainties. It also notes that while the resolution of insolvency regarding enterprise groups could be tricky, the evolution of the Model Law inspired framework could provide for that at a later stage. Recently, the Working Group on Group Insolvency produced a report dealing with group insolvencies. However, the Working Group does not address group insolvencies in the cross-border context. It adopts a similar line of reasoning as the ILC stating that it could be implemented at a later stage, focusing only on the domestic entities in the first phase (Working Group on Group Insolvency, 2019).

While the ILC has produced a very comprehensive report on cross-border insolvency, it does not refer to some of the other documents as proposed by the BLRC such as the American Law Institute’s NAFTA Transnational Insolvency Project, and the International Bar Association Cross-Border Insolvency Concordat. If the Committee had referred to these significant international documents before suggesting the recommendations, it might have proposed a more comprehensive cross-border framework. The Model Law has been adopted by various countries. Some notable adoptees include Canada, New Zealand, the United Kingdom, and the United States. Countries which have not yet adopted the Model Law include Brazil, China, India, and Russia. As noted by Mohan (2012, pp. 12–19)

For instance, Mexico, Romania, and South Africa have incorporated provisions dealing with reciprocity in their domestic insolvency laws, and Japan has made substantial modifications regarding concurrent proceedings (ILC, 2018b, pp. 18, 44). However, it is very pertinent to note that none of the BRIC nations, that is, Brazil, Russia, India, and China, have adopted the Model Law. Given the potential for foreign investments in all these countries, they should create effective mechanisms for dealing with cross-border insolvency (Kargman, 2014). The comments in the BLRC and the ILC reports regarding the creation of a cross-border insolvency system in India, drawn from the Model Law, are very encouraging, and if adopted immediately, it will undoubtedly provide relief to several parties affected by cross-border insolvency proceedings in the country.

THE FRAMEWORK OF CROSS-BORDER INSOLVENCY UNDER THE UNCITRAL MODEL LAW

The UNCITRAL Model Law

The UNCITRAL Model Law on Cross-border Insolvency was enacted in 1997 to help nations in designing their insolvency laws to address issues stemming from cross-border proceedings (UNCITRAL Model Law, 2019c). The Model Law aims to facilitate an efficient, fair, and cost-effective manner of managing transnational insolvency cases. While there was an increase in cross-border insolvency proceedings since the 1990s, there was no uniform framework which the states could adopt for dealing with transnational insolvency. The Model Law is an excellent document adopted by about 44 countries, as of 2019, including the United States, Canada, Australia, New Zealand, Japan, Singapore, and South Africa (UNCITRAL, 2019a).

The UNCITRAL has worked tirelessly to promote the adoption of the Model Law in different jurisdictions. It collaborates with prominent international bodies such as the Asian Development Bank, the World Bank, the International Bar Association, and the International Association of Restructuring, Insolvency and Bankruptcy Practitioners to spread awareness about the benefits of adopting the Model Law (Mohan, 2012, p. 8). For instance, the World Bank’s Principles for Effective Insolvency and Creditor/Debtor Regimes refers to the Model Law and reiterates the drive to ensure consistency with the UNCITRAL Legislative Guide on Insolvency Law (World Bank, 2019a). The UNCITRAL Legislative Guide is a remarkable document which strives to help different countries enact or review current domestic insolvency laws (UNCITRAL, 2019b). It makes quite a few references to the Model Law so that the countries are encouraged to adopt the same. It also encourages the countries to adopt suitable cross-border insolvency provisions in their domestic laws.

The Model Law essentially has a broad scope of application, covering all types of debtors. However, Article 1 (2) includes the possibility of excluding certain entities such as banks or insurance companies, which are usually subject to special insolvency regimes in the concerned states. Many jurisdictions have adopted laws that exclude these entities from their insolvency regimes in line with the Model Law (Mohan, 2012, p. 14). For example, in the United States, the insolvency law does not apply to banks and railways, although the application of the law does not exclude foreign insurance companies (US Bankruptcy Code, Section 1501). In the United Kingdom, the insolvency regime does not apply to credit institutions and insurance undertakings (The Cross-Border Insolvency Regulations, 2006). Reciprocity is not a requirement under the Model Law. However, countries such as the British Virgin Islands, Mexico, and South Africa have adopted the same either de jure or de facto (Chan Ho, 2012).

The Model Law has four key elements concerning cross-border insolvency. First, ‘access’ (as stipulated under Chapter II of the Model Law), wherein foreign creditors are provided with a right of access to the courts of the enacting state for seeking assistance with regard to the insolvency proceedings. According to Article 9 of the Model Law, a foreign representative can apply directly to a local court (UNCITRAL Model Law, art. 9). Article 11 of the Model Law specifies that a foreign representative can commence a proceeding for insolvency under the local laws if the conditions commencing such a proceeding are otherwise met (UNCITRAL Model Law, art. 11). Article 12 of the Model Law enables the participation of a foreign representative in a local insolvency proceeding of the debtor, upon recognition of a foreign proceeding (UNCITRAL Model Law, art. 12). Article 13 of the Model Law provides the right of access to foreign creditors vis-a-vis local/domestic creditors. Article 13.2 also requires that at the minimum, foreign creditors must receive the treatment provided to general unsecured creditors, unless they constitute a class of creditors where the domestic creditors would also be subordinated (UNCITRAL Model Law, art. 13).

Second, ‘recognition’, wherein qualifying foreign proceedings are recognized to save time and resources. A qualifying foreign proceeding can be either recognized as the main proceeding at a jurisdiction where the debtor has its centre of main interests (COMI) at the date of commencement of the foreign proceeding) or a non-main proceeding at a place where the debtor has an establishment. This establishment can be any place of operation where the debtor carries out a non-transitory economic activity with human means and goods or services (UNCITRAL Model Law, arts. 2. c & 2.f). Article 15 of the Model Law allows foreign representative to apply for recognition of the foreign proceeding by enclosing certain documents such as the certified copy of the decision commencing the foreign proceeding and the certificate from the foreign court affirming the existence of the foreign proceeding (UNCITRAL Model Law, art. 15). While Articles 15 and 16 of the Model Law lay down the application procedure for recognition of the foreign proceeding, Article 17 provides that once the requirements have been met, a foreign proceeding shall be recognized as a foreign main proceeding or a foreign non-main proceeding depending on the criteria enshrined under the Model Law (UNCITRAL Model Law, art. 17).

Third, ‘relief’ accorded to assist the foreign proceeding is one of the principal aims of the Model Law. Central elements of the relief available include an interim relief provided by the court at its discretion, a stay upon recognition of a foreign main proceeding, and relief provided by the court at its discretion, in connection to both foreign main and non-main proceedings. Article 19 of the Model Law provides that the court, to protect the interests of the creditors or protect the assets of the debtor, may grant provisional relief upon application by the foreign representative. Some of the interim reliefs include staying execution against the debtor’s assets and entrusting the administration or realization of the debtor’s assets to the foreign representative or another person designated by the court (UNCITRAL Model Law, art. 19). The effect of recognition depends on whether the foreign proceeding is a foreign main or non-main proceeding. Article 20 states that upon recognition of a foreign main proceeding, certain automatic reliefs such as a stay of actions of individual creditors against the debtor, a stay of execution against the debtor’s assets, and suspension of the debtor’s right to transfer or encumber its assets can be availed (UNCITRAL Model Law, art. 20).

Fourth, cooperation and coordination, wherein the Model Law empowers the courts to communicate directly with the foreign courts and coordinate concurrent proceedings. Articles 25 and 26 of the Model Law provide that the local courts and insolvency representatives should cooperate to the maximum extent possible with foreign courts or foreign representatives (UNCITRAL Model Law, arts. 25 and 26). Article 27 lists the different forms of cooperation possible such as communication of information by means deemed appropriate by the court, coordination of the administration of the debtor’s assets, and implementation of agreements (by courts) regarding the coordination of the insolvency proceedings (UNCITRAL Model Law, art. 27). Article 28 of the Model Law deals with the commencement of a local insolvency proceeding upon the recognition of a foreign main proceeding. Such commencement can proceed if the debtor has assets in the state, or in other words, even if he does not have a local establishment, the initiation of the proceedings can be done (UNCITRAL Model Law, art. 28).

Article 29 states that when there are concurrent local and foreign proceedings, the court should cooperate under Articles 25, 26, and 27 and grant appropriate relief (UNCITRAL Model Law, art. 29). Article 30 provides that in the circumstances of multiple concurrent foreign proceedings, the court should seek cooperation and coordination among the proceedings under Articles 25, 26 and 27 of the Model Law (UNCITRAL Model Law, art. 30). Therefore, the Model Law presents a modest (Westbrook, 2005a), yet viable approach (LoPucki, 2005) for resolving cross-border insolvency issues. Certain aspects of the Model Law are not extremely clear such as the determination of the COMI of the corporate debtor, procedural due process (Bufford, 2005), recognition of foreign discharges (Westbrook, 2005b), and choice of law. It is, however, an important step towards dealing with transnational insolvency proceedings.

The IBC’s Cross-border Insolvency Provisions

There are only two sections in the IBC that are relevant as far as cross-border insolvency is concerned: Sections 234 and 235. These two provisions were inserted as enabling provisions following the recommendations of the Joint Parliamentary Committee (Joint Committee on the Insolvency and Bankruptcy Code, 2016). Section 234 of the IBC deals with agreements entered into with foreign countries. It provides that the Indian Government may enter into an agreement with the government of another country for enforcing the provisions of the Code. The Indian Government may direct that the application of the IBC, as regards the assets of the corporate debtor or debtor, located in a country outside India with which reciprocal arrangements have been made, shall be subject to the conditions as stipulated (IBC, Section 234). The IBC, therefore, emphasizes reciprocity as observed in the insolvency regimes of countries such as South Africa (Ailola, 1999).

Section 235 of the IBC deals with letters of request to countries situated outside India in certain cases. It lays down that if during the pendency of the insolvency resolution process, or liquidation, or bankruptcy proceeding, the resolution professional, liquidator, or bankruptcy trustee feels that the assets of the corporate debtor or debtor are located in a country outside India with which reciprocal arrangements have been made, he may apply to the Adjudicating Authority (the National Company Law Tribunal) under the Code regarding the procurement of evidence or initiation of action in relation to such assets. The Adjudicating Authority, upon the receipt of such application, may issue a letter of request to a court or a competent authority to deal with the request on being satisfied that evidence or action with regard to the foreign assets is required in connection with the insolvency resolution process, or liquidation, or bankruptcy proceeding (IBC, Section 235). While the inclusion of these two provisions in the IBC is noteworthy, certain challenges should be addressed.

OPPORTUNITIES AND CHALLENGES UNDER THE IBC

Opportunities

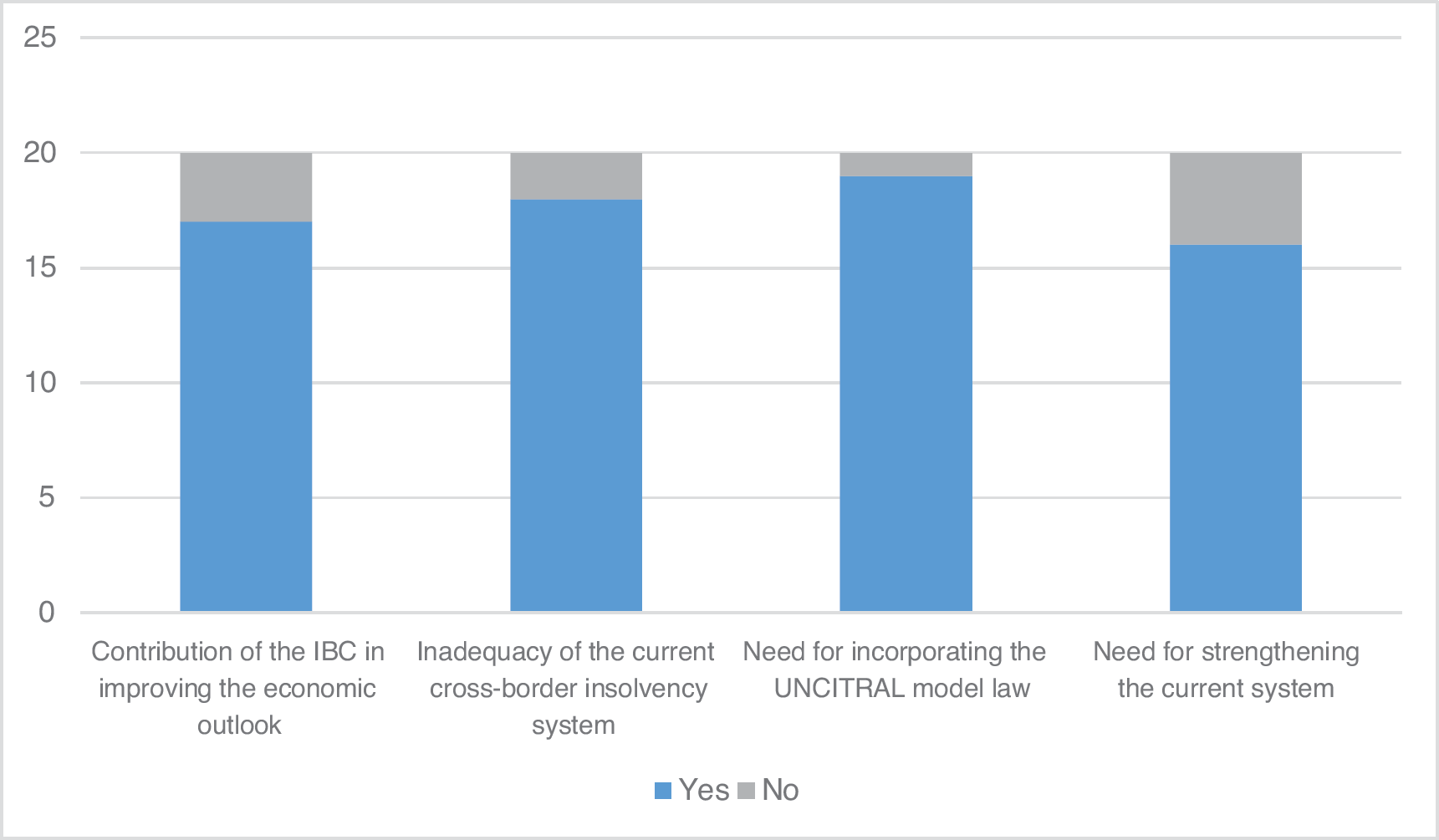

The IBC was introduced to deal with the scheme of insolvency and bankruptcy in India. Following the introduction of the IBC, there has been a remarkable improvement in India’s ease of doing business ranking, as per the latest World Bank report. The report lauds India’s attempt to make insolvency more accessible by adopting the new Code (World Bank, 2019b). The two provisions dealing with cross-border insolvency were inserted to ensure that the Code was not incomplete, and they certainly add to the overall presentation and organization of provisions in the IBC. The author reached out to eminent academics, experts, and practitioners in this area to gather their perspectives on the impact of the IBC in India. The respondents were asked to provide their feedback through the questionnaire shared by the author. The questionnaire had both objective and subjective components. Most of the respondents who provided their feedback on the questionnaire circulated by the author felt that the adoption of the IBC can create a positive economic environment for the creditors and can improve India’s ease of doing business ranking in the near future (17 out of the 20 respondents provided such feedback to the questionnaire). Further, ASSOCHAM and EY in their joint study point out that the Code does not maintain any distinction between the domestic and foreign creditors, therefore, leading to the assumption that the two categories of creditors would be treated in an equivalent manner (ASSOCHAM India & EY, 2017, p. 29).

The ILC recommends that while the foreign creditors will have access to the domestic courts under the current framework of the IBC, the cross-border system should be incorporated based on reciprocity, which can be taken away later depending on the evolution of the insolvency regime in India (ILC, 2018b, pp. 18–19). This indicates that the ILC has adopted a rather cautious approach towards the inclusion of the cross-border insolvency system, perhaps, keeping in view the unique circumstances of the country as regards insolvency and bankruptcy. While the Code is exhaustive as regards the domestic insolvency proceedings, the incorporation of just two provisions relating to cross-border insolvency is grossly inadequate to deal with this transnational problem effectively. This view is supported by the feedback of the majority of the respondents (16 out of the 20 respondents provided such feedback). The BLRC and the ILC reports underscore the need to adopt an effective framework dealing with cross-border insolvency under the IBC, drawn from the Model Law. Therefore, the main opportunity presented in the IBC to address the issue of cross-border insolvency stems from the inclusion of Sections 234 and 235. The challenges associated with having just two provisions relating to cross-border insolvency have been discussed further.

Challenges

The majority of the respondents who provided their feedback on the questionnaire felt that the two provisions dealing with cross-border insolvency under the IBC were not sufficient (18 out of the 20 respondents provided such feedback). First, dealing with Section 234 of the IBC, as the Indian government needs to enter into bilateral agreements with different countries, it may not be practically feasible to negotiate such agreements which could be long drawn and time consuming. Second, there is a possibility that each country may choose to incorporate different provisions in their bilateral instruments which would only lead to fragmentation of India’s cross-border insolvency regime. Last, this could lead to the multiplicity of litigations in cases where a corporate debtor has assets in more than one foreign jurisdiction, wherein the countries would fall back on their separate bilateral agreements to raise claims in connection with the insolvency proceedings. While the IBC has provisions for imposing a moratorium on all suits and proceedings against the corporate debtor in India during the insolvency resolution period, a creditor or contract counterparty can initiate proceedings in another jurisdiction (Kumar, 2017). Further, even though Section 234 of the IBC has been notified, India has not entered into any bilateral agreement so far.

Section 235 of the IBC promotes the spirit of cooperation between a local court and a foreign court/authority as embodied in the Model Law, however, there are certain lacunae. First, there are no specific provisions which lay down the manner of cooperation between the local authorities and the foreign court or competent authority. Second, there is no mechanism for dealing with the coordination of concurrent proceedings. Last, the dependence on letters of request for cooperation may cause an unnecessary delay as they have to be routed through the official channels of the local and foreign jurisdictions. They can in turn cause inconvenience to the creditors affected by such insolvency proceedings. The noteworthy inferences drawn from the responses received through the questionnaire are illustrated in Figure 1.

The draft chapters proposed by the ILC seem promising. The chapters should be incorporated into the IBC after certain modifications. Chapter II deals with access of foreign representatives and creditors to the Adjudicating Authority, wherein Clause 7 specifies that the foreign representative shall be entitled to apply to the Adjudicating Authority, subject to the code of conduct as prescribed. While this seems to be in line with the access principle stipulated under Article 9 of the Model Law, the main departure from the Model Law concerns direct access. The ILC has discussed few reasons why a direct access system may not be conducive for India, including the inability of foreign lawyers to practice currently and the fledgling nature of the country’s cross-border insolvency regime. The ILC notes that the foreign representatives may be represented by domestic insolvency experts and left it to the discretion of the Central Government to provide subordinate legislation as regards the extent of the right to access. The ILC recommended the inclusion of the code of conduct provision as the Model Law does not prohibit the domestic courts from penalizing the foreign representatives for any misconduct (ILC, 2018b, pp. 26–29). While this provision serves an important function, perhaps, the legislators may provide a detailed code of conduct in the subordinate legislation itself instead of explicitly including it in Clause 7 (2).

The second pillar stipulated in the Model Law deals with recognition of the foreign proceedings. Chapter III of the draft Part provides for the provisions in this regard. Clause 15 draws heavily from Article 17 of the Model Law to decide whether the foreign proceeding should be treated as a foreign main proceeding or a foreign non-main proceeding. The foreign proceeding would be treated as a foreign main proceeding if the corporate debtor has a COMI in the foreign country and a foreign non-main proceeding if the corporate debtor has an establishment in that country (ILC, 2018b, p. 35). However, as per Clause 4, which reflects Article 6 of the Model Law, notwithstanding anything contained in the draft Part, the Adjudicating Authority may refuse to recognize a foreign proceeding if it manifestly violates India’s public policy. While the ILC states that India could draw inspiration from the practices of the courts in the United States where the public policy exception has been construed narrowly (ILC, 2018b, p. 23), the Adjudicating Authority still has the discretion to interpret the scope of the exception in a slightly broad fashion. This is not very encouraging for the foreign creditors and could very well defeat the purpose of the draft Part in the IBC.

The third pillar dealing with relief is stipulated under Clauses 17 and 18 of the draft Part. The ILC discouraged the inclusion of ‘interim relief’ under the draft Part due to the bad example set by the cases brought under the Sick Industrial Companies (Special Provisions) Act, 1985. Clause 17 deals with ‘mandatory relief’ and reflects Article 20 of the Model Law wherein it provides for the imposition of an automatic moratorium upon the recognition of a foreign main proceeding. Clause 17 (2) provides that the moratorium as regards foreign main proceedings should be similar in scope to the proceedings, as provided in Section 14 of the IBC, including the exceptions and limitations (ILC, 2018b, pp. 30–38). Clause 18 is drawn from Article 21 of the Model Law and specifies that ‘discretionary relief’ would be provided by the court irrespective of whether the proceeding is a foreign main proceeding or a foreign non-main proceeding (ILC, 2018b, pp. 38–41). The ILC notes that Section 14 of the IBC should guide the provision of mandatory and discretionary reliefs as regards foreign proceedings (ILC, 2018b, pp. 37–38). While the moratorium may not be modified (ILC, 2018b, p. 37), the legislators should leave additional space for the provision of discretionary reliefs as the foreign proceedings may require certain other mechanisms. While Clause 18 (1) (f) that deals with the possibility of additional reliefs, seems to be a catch-all provision, the legislators may specify the principles that would guide the application of this provision in the subordinate legislation.

The final pillar, dealing with cooperation and coordination has been provided under Chapters IV and V of the draft Part. The relevant provisions concerning cooperation have been incorporated in the draft Part without substantial modifications. The ILC notes that direct communication, as provided under Article 25 of the Model Law, between the Adjudicating Authority and the foreign courts is premature at this stage. Therefore, the ILC recommends that the Central Government should frame guidelines in this regard, as reflected in Clause 21 of the draft Part. Chapter V deals with concurrent proceedings, and as per the recommendation of the ILC, the relevant provisions of the Model Law have been incorporated without significant deviations in the draft. The ILC notes that as the provision of interim reliefs has not been included in the draft Part, the same shall be excluded from Chapter V (ILC, 2018b, pp. 42–47). While Chapter V seems to be adequately comprehensive, Chapter IV of the draft Part requires more clarification from the legislators due to the lack of specific provisions. Perhaps, the legislators could make this chapter more robust following the application of the proposed provisions to cross-border insolvencies in India.

Conclusion

One of the recent instances which highlight the impact of not having an effective cross-border insolvency resolution framework is the Nirav Modi episode which rocked the nation. One of the news reports notes the ingenious ways in which some of the entities associated with Nirav Modi have filed for bankruptcy in the United States, in an attempt to avoid dealing with the Indian regulators (Merwin, 2018). Another case which the National Company Law Tribunal is dealing with relates to the Jet Airways fallout. The Tribunal in Mumbai had refused to provide relief to the Dutch insolvency administrator when it was approached for recognition of the foreign proceedings. The administrator, therefore, moved the National Company Law Appellate Tribunal to hear the matter (Solanki, 2019). The Appellate Tribunal has allowed the Dutch administrator to attend the company’s Committee of Creditors’ meetings while also finalising the cross-border insolvency protocol that would apply to Jet Airways (Jet Airways (India) Ltd. v. State Bank of India, 2019). Given the lack of a proper framework to deal with cross-border insolvency under the IBC, the observations made by the Appellate Tribunal indicate the potential of India to develop positive judicial trends as regards cross-border insolvency.

Such cases should, however, serve as a clarion call for the Indian legislators so that the entire process of framing the detailed provisions dealing with cross-border insolvency is expedited. The Model Law provides an efficient system of dealing with cross-border insolvency proceedings. However, since India has not adopted the Model Law yet, its transnational insolvency regime is yet to develop like it has evolved in other countries that have adopted the Model Law. The Model Law can serve as a great blueprint for designing the cross-border insolvency regime in India, and therefore, positive work towards this direction could be beneficial for the country (19 out of the 20 respondents supported this view). The scheme of entering into separate bilateral agreements or issuance of letters of request is not very efficacious. Therefore, the Indian transnational insolvency system should have a proper mechanism of cooperation and coordination between local courts and insolvency representatives on the one hand and foreign courts and foreign representatives on the other hand, in line with the provisions of the Model Law.

The ILC has stated in its second report that it has considered the international practice with reference to cross-border insolvency. It is imperative, however, to have clarity about the effective incorporation of the Model Law in other domestic frameworks (16 out of the 20 respondents supported this view). Different countries such as Colombia, Greece, Japan, Poland, and South Korea which have adopted the Model Law have made several deviations concerning the coordination of multiple proceedings. The ranking of claims, especially in relation to the foreign creditors, the recognition of foreign proceedings, and the provision of interim relief (Mohan, 2012, p. 18). As recommended by the ILC, given the special nature of banks and insurance companies, the legislators may exclude the applicability of the cross-border insolvency provisions to such entities, as stipulated in Article 1 (2) of the Model Law. With regard to India, the insolvency of these institutions can critically affect the financial interests of several members of the public. It may require quick decision-making, requiring specialised insolvency regimes (ILC, 2018b, p. 17).

(Late) Mr Arun Jaitley, while talking about the IBC, had pointed, “You can’t amend the law every time, but certainly this is a point worth consideration on the agenda…” (NDTV Profit, 2018). While the IBC presents amazing opportunities for improving the domestic insolvency system in the country, it is high time that India implements a comprehensive framework dealing with cross-border insolvency under the Code, in line with the recommendations of the ILC, without delay. Policy prescriptions adopted at the right time can significantly add to the overall effectiveness of these instruments. Therefore, it would be beneficial if the law makers and legislators exercise a far-sighted approach in incorporating important provisions in legislation in the future. For instance, if the draft Part dealing with cross-border insolvency was a part of the IBC from the beginning, it might have aided the courts/tribunals to have a clear picture of the entire system. It would also promote the government’s pitch in portraying India as a trade and investment hub where resolving cross-border insolvency is quick and efficient.

Before incorporating the draft Part, as proposed by the ILC, the legislators may also consider the American Law Institute’s NAFTA Transnational Insolvency Project and the International Bar Association Cross-Border Insolvency Concordat. While the former primarily focuses on the resolution of insolvencies associated with corporations and other commercial business enterprises, the latter suggests certain general principles which the participants can tailor to their unique circumstances and needs. Given that the ILC has chosen to keep the cases of individual insolvencies beyond the purview of the cross-border system under the IBC (for now), reference to these two international documents could add tremendous value to the efficacy of the cross-border insolvency system in India. The legislators may also consider the Regulation (EU) 2015/848 of the European Parliament and of the Council that deals with insolvency proceedings as regards members of group companies. The cross-border insolvency regime in the country could be at its nascent stage, currently, but with steps in the right direction India can serve as a model for other countries.

Footnotes

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship and/or publication of this article.