Abstract

Keywords

I am often asked a question by my friends, ëHow is it that a central bank can change just the policy rate and expect it to affect macroeconomic outcomes?í It is a deep question that is worth thinking about from first principles. In central banking parlance, the policy rate ëdialí turned by a central bank causes the economy to ëtraverseí along its contours of growth and inflation via a mechanism called monetary transmission. In other words, monetary transmission is the process through which changes in the policy rate by the central bank, in pursuit of the ultimate objectives of price stability and growth, are transmitted to the real economy. This transmission involves changes in the policy rate being reflected contemporaneously, or possibly over time, in the entire spectrum of interest rates relating to the inter-bank market, commercial paper, certificates of deposit, government securities and corporate bonds, and banksí deposits and loans. Ordinarily central banks do not directly control long-term rates. They do, however, control short-term rates by being monopoly suppliers of currency and reserves (bank deposits with the central bank). A smooth transmission from short-term rates to long-term rates is critical as changes in long-term interest rates subsequently influence spending decisions of businesses and households, and hence output and prices.

Efficient monetary transmission requires many pre-conditions to be satisfied. These include (a) availability of an efficient payment and settlement system for monetary transactions, (b) active liquidity management by the central bank so that the supply of liquidity matches its demand and thus inter-bank rates remain close to the policy rate, (c) well-integrated financial markets for facilitating interest rate arbitrage across financial market segments, (d) a healthy and well-capitalized banking system so that banks are not constrained in their lending operations, (e) liability and asset structure of banks that is responsive to interest rate changes by the central bank, and (f) the absence of distortions such as interest subvention and administered rates of interest that are out of sync with market rates.

Unsurprisingly, therefore, the issue of monetary transmission has all along been important for the Reserve Bank of India (RBI). However, it has assumed a special significance in the context of the amendment to the Reserve Bank of India Act in 2016, which mandates the RBI to conduct monetary policy for achieving price stability as its primary objective while being mindful of growth. This mandate is difficult to achieve unless supported by a robust transmission mechanism. The policy rate adjustments by the monetary policy committee (MPC) are intended to percolate down to the entire spectrum of interest rates, especially bank lending rates so that the economy stays close to its ësteady stateí, that is, inflation close to the mandated target and growth close to its potential path; and, in case there is any shock, the endeavor of the MPC is that the economy be brought back to the steady state by adjusting the policy repo rate. If the economy is overheated but lending rates of banks do not rise in response to the raising of policy rate by the MPC, then credit demand of firms and households would continue to remain robust, consumption and investment by households and firms will continue to rise, and, as a result, the corresponding aggregate demand conditions in the economy would not allow inflation to drop. Conversely, in an easing cycle of monetary policy, if a decline in the policy rate is not followed by a reduction in bank lending rates, consumption and investment demand will not increase to help bring inflation and growth back to the steady-state levels.

THE RBI’S PROPOSAL FOR MARKET BENCHMARKING OF FLOATING RATE LOANS

To enable monetary transmission, the RBI designed bank lending rate systems during the era of liberalized interest rates. These systems required that banks link the rates on their floating rate loans to a ëbenchmarkí rate determined by each bank. The benchmark rates were expected to respond to policy rates. Monetary transmission in India has, however, so far been considered to have been less than satisfactory (Acharya, 2017). In particular, neither the prime lending rate (PLR) system introduced in 1994 nor the benchmark PLR (BPLR) system in 2003 succeeded in providing effective monetary transmission. The base rate system introduced in July 2010 followed by the marginal cost of funds-based lending rate (MCLR) system in April 2016 also continue to suffer from the same rigid response of bank lending rates to policy rate changes as did the previous systems.

The Expert Committee to Revise and Strengthen the Monetary Policy Framework in its report released on 21 January 2014, observed that unless the cost of banksí liabilities moves in line with the policy rates as do interest rates in money market and debt market segments, it will be dificult to persuade banks to price their loans in response to policy rate changes. Hence, it was necessary to develop a culture of establishing external benchmarks for setting interest rates on bank loans as well as deposits. The committee felt that while these benchmarks should emerge from market practices, the RBI could explore playing a proactive and supportive role in their emergence (Patel et al., 2014).

The Report of the Household Finance (Chairman: Tarun Ramadorai), which was submitted in August 2017, also observed the deficiencies in the interest rate setting system in banks, especially the factors that delay transmission or complicate comparison across banks. It recommended that banks should quote loan rates not based on bank specific MCLR rates, but on the policy repo rate or some other standard market rate. The report argued that this would not only bring about transparency, as borrowers can easily compare across banks, but also improve customer protection (RBI, 2017).

Keeping in mind the observation made by the Patel Committee and the report on the household finance, the RBI constituted an Internal Study Group to Review the Working of the Marginal Cost of Funds based Lending Rate (MCLR) System (Chairman: Dr Janak Raj). The report of the Study Group, released on 4 October 2017, identified the factors that have impeded monetary transmission in India. The group also recommended that banks use market rates or the policy repo rate as benchmark for pricing floating rate loans (Raj et al., 2017). The RBIís response to the feedback received from banks and other constituencies was released in February 2018 as an addendum to the report (Reserve Bank of India, 2018).

Finally, on 5 December 2018, the RBI proposed that floating rate loans (personal or retail loans, loans to micro and small enterprises, and any other category of loans at the bankís discretion) extended by banks from 1 April 2019 shall be linked to either the policy repo rate or a market benchmark rate (three-month or six-month T-bills or any other rate produced by Financial Benchmark India Private Limited [FBIL]). The spread over the benchmark rate would remain unchanged unless the borrowerís credit assessment undergoes a substantial change and as agreed upon in the loan contract.

Let me elaborate on the important details around this sequence of events.

EVOLUTION OF LENDING RATE SYSTEMS IN INDIA

The first regime of prime PLR was introduced in 1994. However, both PLR and spread over PLR were seen to vary widely across banks/bank groups. Moreover, the PLRs continued to be rigid and inflexible in relation to the overall direction of interest rates in the economy.

With the aim of introducing transparency and ensuring appropriate pricing of loansówherein the PLRs truly reflected the actual costsóthe PLR was converted into a reference benchmark rate and banks were advised in 2003 to introduce the BPLR system, which gave them the freedom to lend below the BPLR. While lending below the BPLR was expected only to be at the margin, in practice about 77 per cent of banksí loan portfolio was at sub-BPLR. This clouded the true assessment of monetary transmission.

In a nutshell, both the PLR and BPLR systems did not produce adequate or uniform monetary transmission to the real economy.

In July 2010, the RBI replaced the BPLR system with the base rate system. The actual lending rate was the bank-specific base rate (for which an indicative formula was also prescribed) and the spread. However, the flexibility accorded to banks in the determination of cost of funds (average, marginal or blended cost), which was a key component of base rate calculation, resulted in opacity in the computation of base rate. In particular, the average cost of funds did not move much in line with monetary policy changes due to the term nature of fixed-rate deposits. Moreover, banks often changed over time the spread over the base rate for some borrowers, while leaving the base rate unchanged.

Given these deficiencies, the RBI introduced a new lending rate system for banks in the form of the MCLR, tied to the marginal funding cost of each bank, in April 2016. However, unlike the BPLR and the base rate, the formula for computing the MCLR was fully prescribed, though some discretion remained with banks. The MCLR has, however, continued to suffer from the same flaw as the earlier lending rate systems in that transmission to the existing borrowers has remained muted since banks adjustóin many cases in an arbitrary manneróthe MCLR and/or spread over MCLR, which has kept overall lending rates high in spite of monetary policy being accommodative from January 2015 to May 2018. 1

In his speech, in June 2016, ëThe Fight against Inflation: A Measure of Our Institutional Developmentí, the then RBI Governor Dr Raghuram G. Rajan noted that ëAll in all, bank lending rates have moved down, but not commensurate with policy rate cutsí.

MONETARY TRANSMISSION: RECENT EVIDENCE

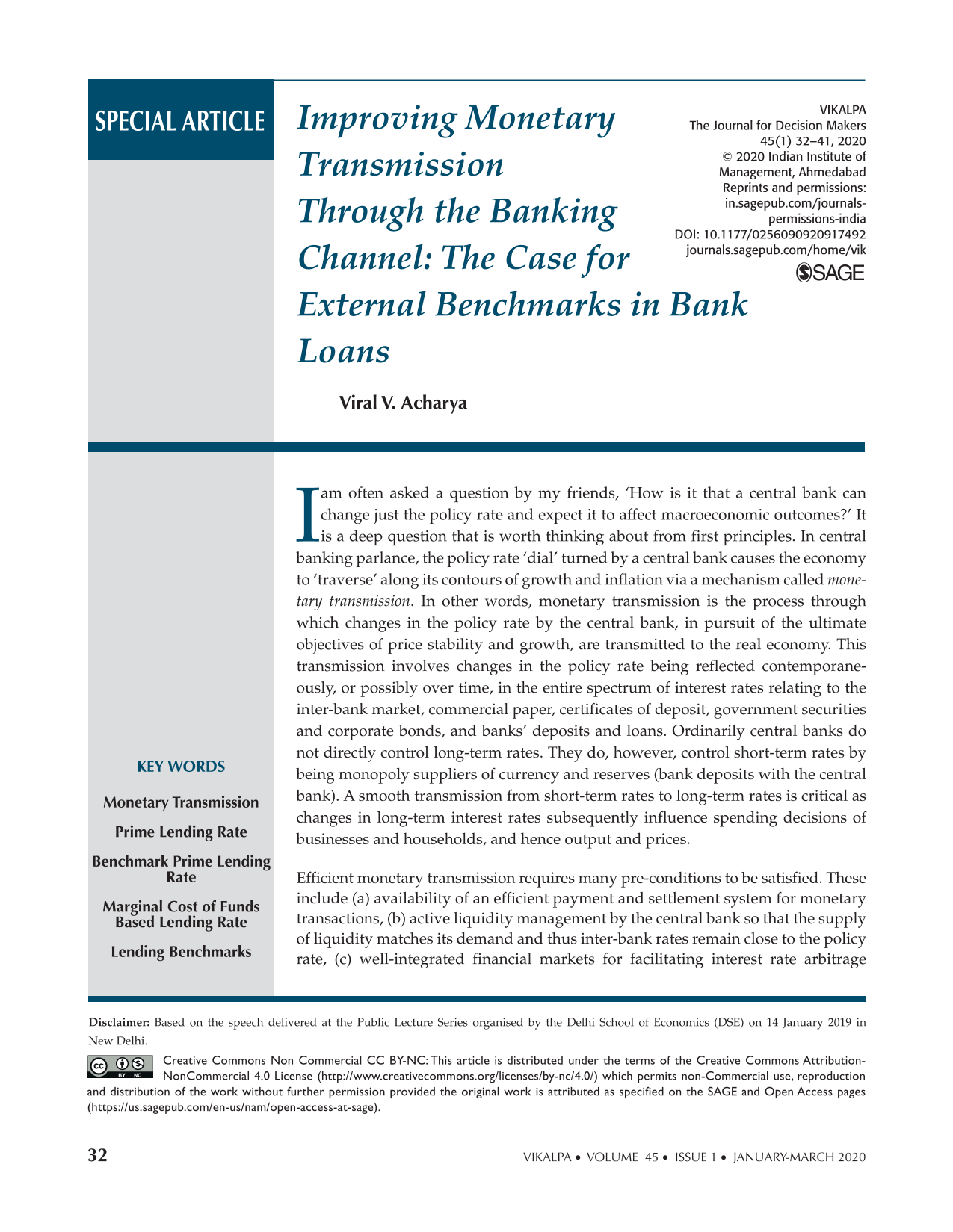

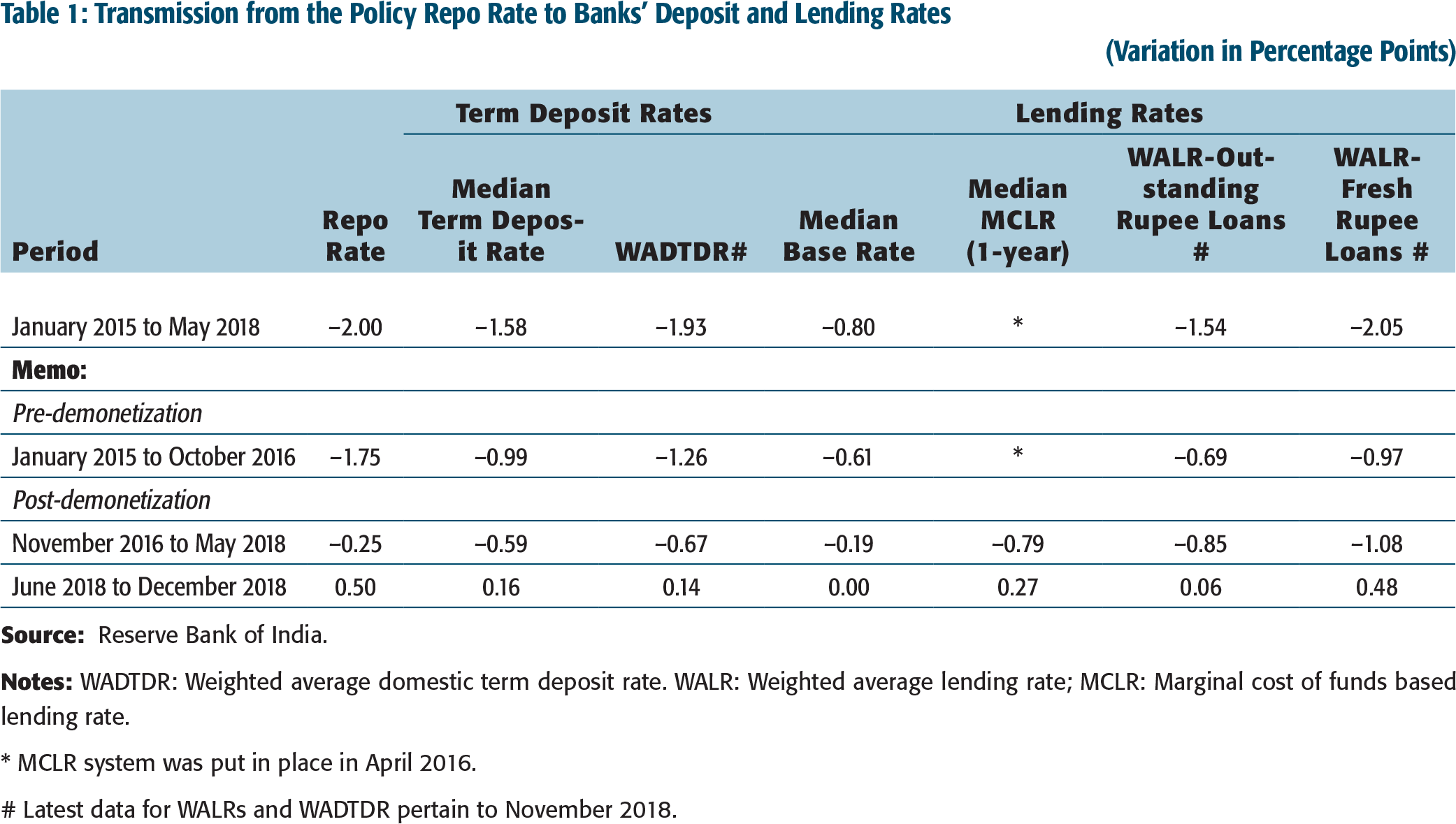

Evidence that monetary transmission in India has not been satisfactory in the recent period is presented in Table 1 and Figure 1. As against the policy rate cut of 200 basis points during January 2015 to May 2018, the weighted average term deposit rate (WATDR) declined by 193 basis points. However, the weighted average lending rate (WALR) on outstanding rupee loans declined only by 154 base points. Reduction in the WALR on fresh rupee loans was higher at 205 base points as the banks passed on the benefits in the reduction of MCLRs more to the new borrowers than to the existing borrowers. However, significant transmission occurred only post-demonetization following the increase in low-cost current and saving account deposits due to surplus liquidity with the banking system. In the more recent period, in response to the increase in the policy rate by 50 basis points (from June to December 2018), WALR on fresh rupee loans increased by 48 base points, but only 6 basis points on outstanding rupee loans. Also, the median base rate hardly moved (Figure 1). Since about 24 per cent of banksí loan portfolio is still at the base rate/BPLR, this impaired the overall monetary transmission to outstanding rupee loans.

Transmission from the Policy Repo Rate to Banks’ Deposit and Lending Rates

(Variation in Percentage Points)

* MCLR system was put in place in April 2016.

# Latest data for WALRs and WADTDR pertain to November 2018.

Let us now turn to the fundamental question of why monetary transmission through these benchmark rate systems employed to date has remained weak.

AN INTERNAL VERSUS EXTERNAL BENCHMARK

Each of the four above mentioned lending benchmarks prescribed so far in India can be considered as ëinternalí in that banks can set the benchmark rate themselves or choose at their discretion many of the elements that go into the prescribed formulae. Thus, being under the control of a bank, an internal benchmark is prone to be adjusted in a discretionary manner that suits the interests of the bank, possibly at the expense of borrowers and the economy. In fact, the report of the Study Group pointed out several instances where banks arbitrarily adjusted the MCLR/base rate, which impeded transmission of policy rate cuts to borrowers.

In contrast, the RBI policy rate and 91-day/182-day T-bill rate are ëexternalí benchmarks, which are exogenous to each bank and adjust automatically and likely contemporaneously to both expected and unexpected policy rate changes. 2

In rare cases, the possibility of collusion in the case of market-based benchmarks such as T-bill rate (but not the policy repo rate) cannot be ruled out.

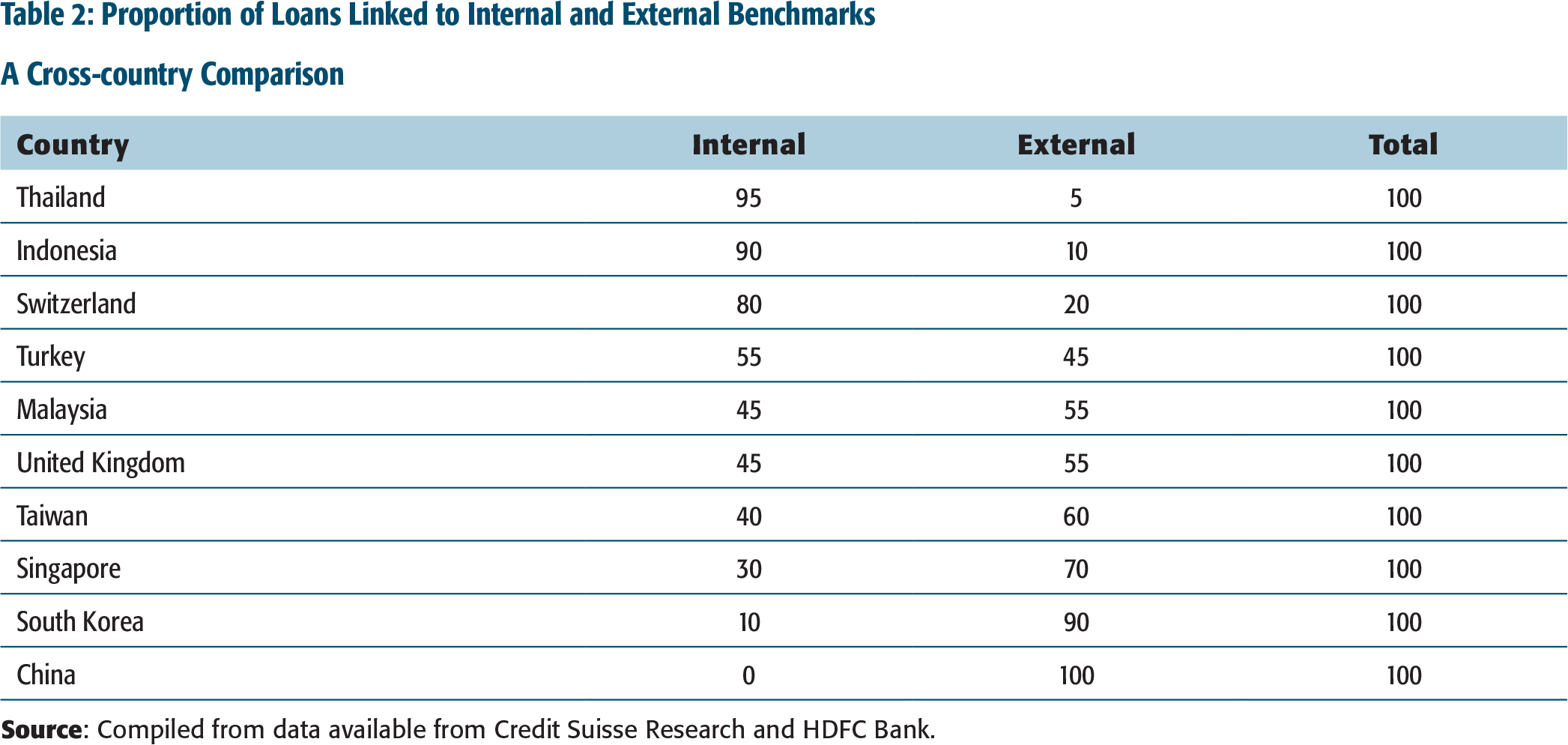

There is another distinct advantage of external benchmarks vis-‘a-vis internal benchmarks. An external benchmark is transparent and known to the borrowers and the lenders alike. An internal benchmark is bank specific and renders a product comparison of different banks difficult, whereas an external benchmark will be uniform across banks and facilitate product comparison. Given these advantages over internal benchmarks, external benchmarks are now used extensively in most countries in the world, especially the developed ones (Table 2).

An external benchmark alone, however, will not be sufficient to achieve the desired objective of effective monetary transmission and transparency as long as banks continue to have an absolute discretion to change the spread over the benchmark. The report of the MCLR Study Group pointed out several cases where banks changed the spread over the MCLR to offset fully or partly the changes in MCLRs. It was observed that while banks were keen to attract new customers by offering them competitive pricing, they often denied the benefits of changes in the MCLR to existing borrowers by changing the spread. This impeded monetary transmission of policy rate cuts as shown in Table 1. Indeed, such practices by banks also raised the issue of consumer protection. It is for this reason that the RBI has also proposed that the spread over the benchmark rate should remain unchanged through the life of the loan unless there is a change in the credit assessment of the borroweróan arrangement that can be contractually agreed upon between the bank and the borrower.

Thus, the proposals to introduce an external benchmark and keep the spread unchanged need to be seen jointly. The underlying philosophy is to make the entire process of setting lending rates by banks transparent and improve monetary transmission. Banks would have the complete freedom to fix the spread over the external benchmark for new borrowers at the time of the origination of the loan; the fixed spread over the benchmark through the tenure of the loan for the given credit quality would, however, limit the scope for arbitrary spread adjustments after the loans have been sanctioned and thereby preclude the undoing of changes in the benchmark rate.

ISSUES RAISED BY BANKS

Indian Banksí Association and some banks individually provided feedback to the RBI on the recommendations of the Study Group, essentially making the following three points.

External Benchmarks Recommended Do Not Reflect the Cost of Funds of Banks

Proportion of Loans Linked to Internal and External Benchmarks A Cross-country Comparison

Markets to Hedge Interest Rate Risk in India Are Illiquid

Second, banks in India are currently not in a position to hedge interest rate risk given the absence of a developed interest rate swap (IRS) market. In the absence of such a market, either bank profitability could come under pressure or loan spreads could become higher as compensation for interest rate risk. Banks also highlighted that in the absence of a reliable term money market, the use of any benchmark will leave the discretion on the pricing of term premium with the banks. Banks argued that the ideal benchmarkófrom the perspective of banksóshould be based on the deposit rates of the banking system as a whole. Banks also pointed out that they have experimented with floating rate deposits in the past but the response had not been encouraging. Retail depositors are particularly averse to such products. Even institutional/wholesale depositors prefer fixed rates when they perceive that interest rates have peaked and an easy cycle of monetary policy is about to begin, banks argued.

Banks Need Flexibility to Change Spread

Lastly, in a deregulated interest rate environment, spread over the benchmarkóbe it internal or externalómust be the exclusive domain of the commercial banks. Also, for a variety of pure commercial reasons, the spread cannot be fixed forever. The credit risk premium is time varying and expected credit losses do change over time. For example, the spread itself could become a function of the interest rate cycle. At times, banks may have to reduce spreads just to retain customers; some customers may back their loans with more collateral at a later stage of the loan, requiring a downward adjustment of the spread; for many project loans as risks decline after the gestation lag and based on repayment track record the spread may have to be lowered and so on. Therefore, according to banks, market competition alone should lead to convergence of spreads and regulatory prescriptions on whether the spread should change or remain fixed would not be in sync with the spirit behind the deregulation of interest rates.

Let me briefly respond to these issues raised by banks.

ADDRESSING THE CONCERNS RAISED BY BANKS

External Benchmarks Recommended Do Not Reflect the Cost of Funds

First, the argument that banksí funding cost is not related to the external benchmark as loans are funded mainly through deposits and not through market borrowings is not entirely persuasive. In a competitive market, loans should, like products in any industry, be priced at the level at which market clears them, not at cost. The only way cost-linked pricing can sustain is either through regulatory mandate or through cartelization. In either case, this is not in the interest of bank borrowers.

Furthermore, the argument that market benchmarks are not linked to the cost of funds is easily addressed by linking liabilities to market benchmarks as well. Fixed-rate loans can be funded using fixed-rate deposits. The gaps/mismatches can be managed through interest rate derivatives, a point to which I will turn later.

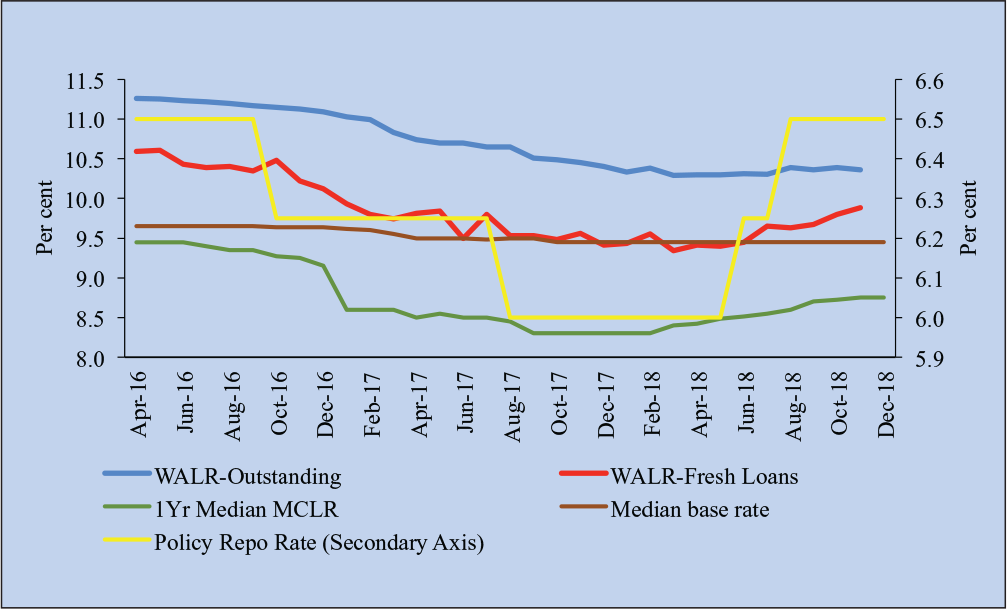

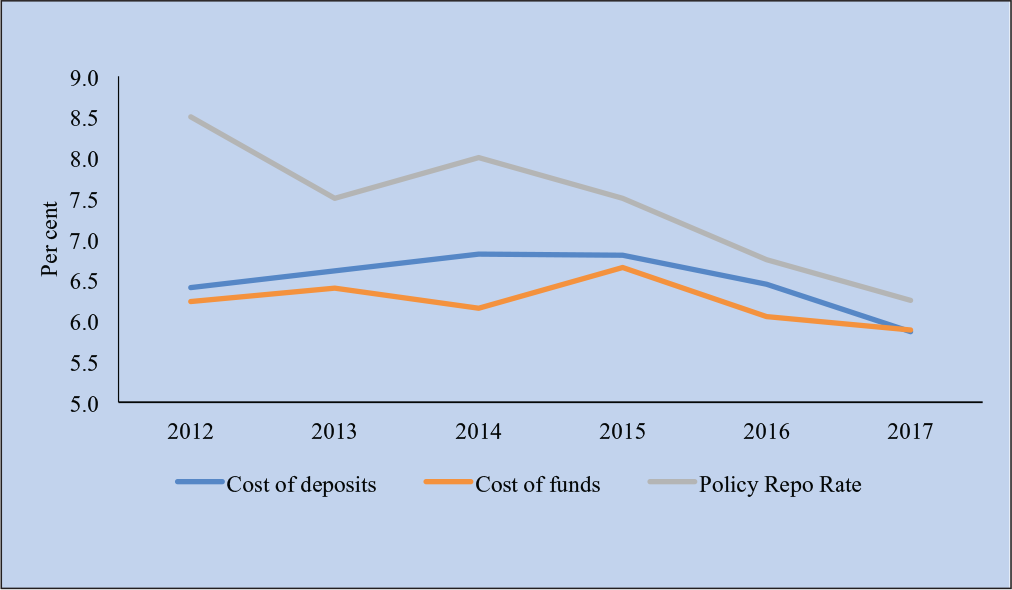

Moreover, the cost of deposits or funds of scheduled commercial banks is, in fact, getting closely aligned with the policy repo rate over the past few years (Figure 3). At any rate, banks would have the freedom to set the spread to factor in the extra cost of funding (the difference between the external benchmark and the average cost of funds), term premium, credit risk, or any other costs (such as operating costs).

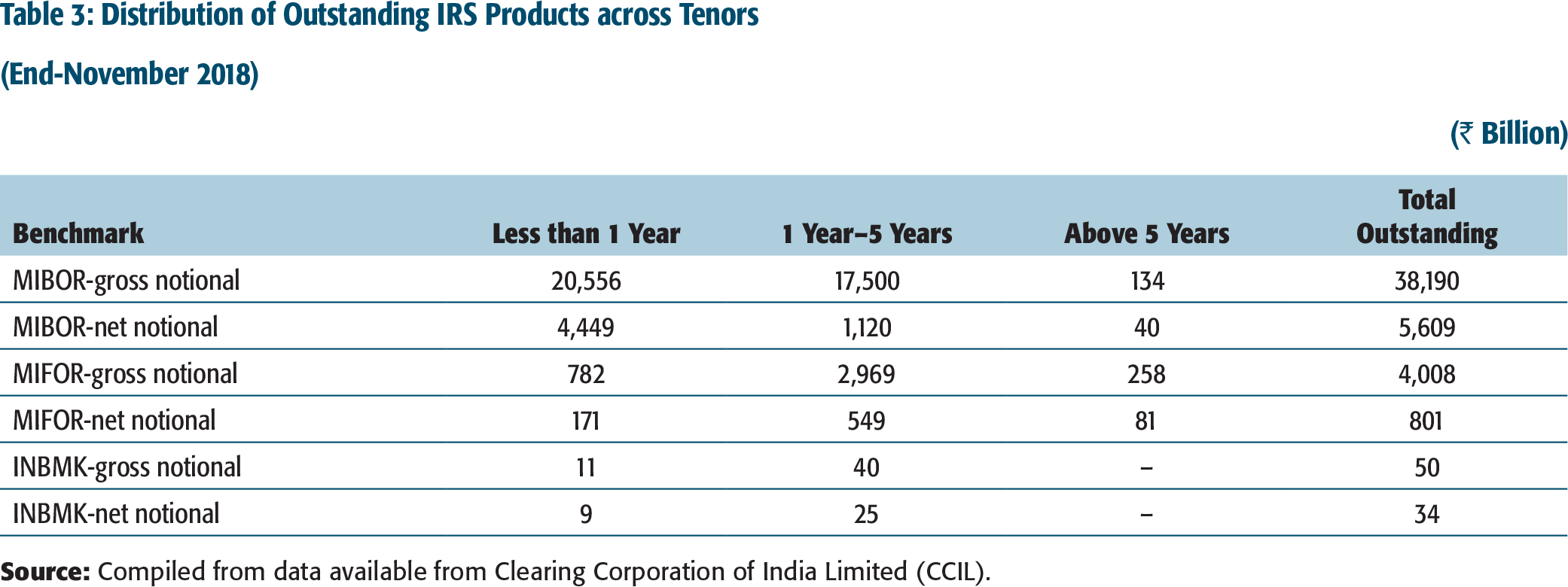

Distribution of Outstanding IRS Products across Tenors (End-November 2018)

(₹ Billion)

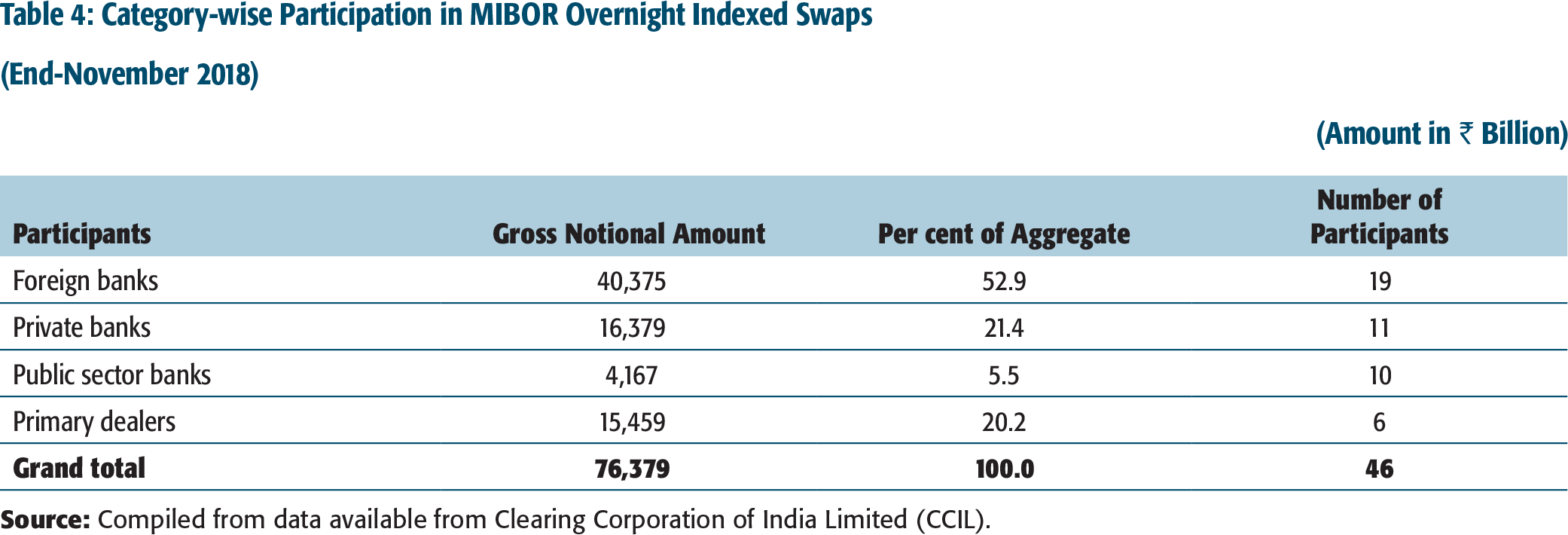

Category-wise Participation in MIBOR Overnight Indexed Swaps (End-November 2018)

(Amount in ₹ Billion)

Markets to Hedge Interest Rate Risk in India Are Illiquid

Let me now turn to the second issue that banks do not have adequate hedging facility for interest rate risk. Banks have rightly observed that in India, the IRS market is not yet fully developed. Apart from the Mumbai Interbank Offer Rate (MIBOR) based overnight index swaps (OIS), liquidity in the other instruments is rather thin (Table 3). 3

The OIS refers to the exchange of overnight floating interest rate with fixed interest rate. The OIS market in India has a term structure up to 10 years, but most segments are not liquid. The market participation is highly concentrated with only a section of the banks active in the OIS market. The daily volume in the OIS market is only around ₹150 billion as against an average daily bond market volume of ₹400–500 billion. Wider participation by banks in the OIS market is necessary for improving liquidity in these markets, which is necessary for banks to offload their significant duration risk onto others.

Banks, being the major intermediaries in the financial sector, have collective responsibility to contribute to market development, at least by active participation. Citing under-developed derivatives markets amounts to an admission of their joint failure to perform this role. Table 4 shows that not only is the participation of banks in the OIS markets not commensurate with size of their interest rate risk exposure, some banks do not at present participate at all in this market.

Indeed, a more market-linked balance sheet would encourage and incentivize banks to participate in the interest rate derivatives markets. The RBI, on its part, has taken several initiatives to give a fillip to interest rate derivatives markets which include the following:

Allowing introduction of money market futures and interest rate options. Easing constraints in the short selling market to encourage larger participation. Broadening participation base by proposing free non-resident access for hedging in the domestic market.

In particular, the proposal to extend non-residents access to the OIS market for purposes other than hedging could potentially address most of the concerns expressed by banks about lack of depth in the IRS market.

Banks Need Flexibility to Change Spread

Let me now come to the issue about the flexibility in fixing/re-fixing the spread any time during the term of floating rate loans. Such flexibility goes against the essence of floating rate loans. The only adjustable element in the floating rate loans linked to a benchmark should be the benchmark itself and not the spread, unless there is a large material change, for example, a mutually agreed credit event and attendant outcomes such as change in collateralization of the loan. It is important that these conditions that lead to a reset of the spread are part of the contractual loan conditions and are mutually acceptable. The responsibility of demonstrating that these conditions have not been used exploitatively should rest on the bank. The risk faced by banks from time-varying credit risk premium can be built into the spread at time of loan origination, at the complete discretion of banks, as is done in externally-benchmarked floating rate contracts in other parts of the world.

ALIGNMENT OF INTEREST RATE SETTING PRACTICES OF NBFCS WITH THOSE OF BANKS

Non-banking financial companies (NBFCs) have been growing rapidly in the recent period. The share of NBFCs in total credit extended by banks and NBFCs together increased from 9.5 per cent in March 2008 to 16.8 per cent in March 2018. As a result, the relative significance of NBFCs in the financial system has been growing and they are becoming increasingly important in monetary transmission. However, interest rate setting processes vary markedly across NBFCs. While some NBFCs link their lending rates to banksí base rates/MCLRs, others use their own PLRs to set interest rates. Some other NBFCs do not appear to have any interest rate benchmarkóinternal or externalófor pricing their loans. The periodicity of reset of interest rates on floating rate loans also differs from one customer to another and is set arbitrarily by the loan sanctioning authority.

For effective monetary transmission to the financial intermediaries and ultimately to the real economy, it is necessary that the interest rate setting processes of NBFCs are aligned with those of banksóin terms of interest rate benchmarks, spread remaining fixed over the benchmark during the life of the loan, the circumstances that could result in a change in the spread over the tenor of the loan, and the periodicity of interest rate reset. Such harmonization would provide banks and NBFCs a level-playing field to operate in, while at the same time facilitate effective monetary transmission across the entire range of financial intermediaries.

Keeping in view the proposed changes for banks, the RBI has constituted another Internal Study Group to (a) examine the current interest rate setting practices by NBFCs, (b) suggest measures to harmonize the interest rate setting processes of NBFCs with those of banks, and (c) suggest an appropriate roadmap for such harmonization.

CONCLUDING REMARKS

Past loan-pricing arrangements in India that provided banks with a one-sided facility to fix rates periodically have been inimical to monetary transmission. Such arrangements are increasingly discouraged in modern financial economies. The reaction to the policy announcement by the RBI on 5 December 2018 to link all floating rate loans (personal or retail loans and loans to micro and small enterprises, or any other category of loans at the bankís discretion) extended by banks to either the policy repo rate or a market benchmark rate from 1 April 2019 has generally been positive. Theoretically, a borrower deprived of monetary transmission by a bank could refinance the floating rate loan by going to another bank, but in practice, this competitive argument does not work well. The borrower is often left with little choice because of the cost and effort involved in shifting from one bank to another, especially because loans of different banks with internal benchmarks are not comparable. The RBIís proposed system of external benchmarking will increase the transparency of bank loan products. The proposed external benchmark system is not prescriptive, unlike the previous regulatory dispensations. In particular, banks will have greater flexibility (in choosing the external benchmark and credit spread), and the borrower will enjoy greater transparency compared to the current opacity in lending rates that are linked to an internal benchmark.

It is interesting to note that in March 2018, a foreign bank launched a mortgage product linked to an external benchmark, namely, the 3-month Treasury Bill (TBLR), which is the transparent reference rate published by FBIL. The interest rate on the loan benchmarked to TBLR is reset on a quarterly basis. While the bank has continued to offer one year MCLR linked home loan, 95 per cent of the new loans are now linked to TBLR, indicative of the widespread acceptance of an external benchmark by the home loan customers.

Ultimately, if banks do not pass on the monetary policy impulses to bank-dependent borrowers such as households and micro, small, and medium enterprises, then monetary policy would have to adjust more dramatically to move the economy towards the steady state. In the past this has meant that to bring the costs of bank loans down, interest rate cuts have had to be significantly large. However, this lowered market interest rates––that move in tandem with policy rates unlike internal benchmark rates––to levels that implied negative real rates of market borrowing for government and large corporates that can access financial markets. The resulting fiscal and corporate debt excess not only raised inflation to uncomfortable levels but also left the banking sector laden with massive losses, imposing significant ëtaxí on the poor and bank-dependent borrowers. External benchmarking of floating rate loans proposed by the RBI will thus not only improve monetary policy transmission but indirectly also help maintain macroeconomic and financial stability.

Footnotes

ACKNOWLEDGEMENT

I am grateful to Vineet Srivastava for his valuable inputs.

DECLARATION OF CONFLICTING INTERESTS

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

FUNDING

The author received no financial support for the research, authorship and/or publication of this article.