Abstract

Executive Summary

Financial Inclusion is considered to be a critical indicator for development and well-being of the society around the globe. Providing inclusive financial services, that is, financial services affordable for all, has become a basic priority in many countries including India. G-20 Nations have emphasized on financial inclusion as a facilitator for achieving gender equality and other sustainable development goals. Women empowerment is a radical approach concerned with transforming power relations in favour of female gender and considered essential for global progress. Thus, an inclusive financial model is being adopted in developing nations to achieve fundamental to formative objectives. The current article investigates the dimensions of women empowerment, that is, social, political, and economic. It also undertakes a test to see if the dimensions change with financial inclusion. The authors draw upon literature to develop a structured questionnaire on women empowerment and financial inclusion through schemes like Pradhan Mantri Jan Dhan Yojana (PMJDY), Pradhan Mantri Jivan Jyoti Bima Yojana (PMJJBY), Pradhan Mantri Suraksha Bima Yojana (PMSBY), and Atal Pension Yojana (APY) on women living in urban slums in the industrial town of Ludhiana, Punjab. The data were collected from 737 females living in urban slums with PMJDY bank accounts. The result indicated that PMJDY scheme has been quite successful especially in case of women in slums and has a positive influence on social, political, and economic dimensions of women empowerment. The study contributes to existing literature by advancing the debate on women in urban slums and identifies the substantial need for the development of formal financial system to enhance the scale of financial inclusion.

There is no tool for development more effective than women empowerment.

—Mr Kofi Annan

In 2005, the former general secretary of the United Nations quoted this statement to address the issue of gender inequality as a barrier in global development. He also emphasized upon the significance of ‘Inclusive Financial Sector’ to ensure gender economic equality. As per Findex data of Word Bank, 1.2 billion adults have access to financial services since 2011, yet close to one-third, that is, 1.7 billion adults are still unbanked. About half of the unbanked population includes poor households or out of workforce (The World Bank, 2018). The G-20 summit, in 2010, perceived financial inclusion (FI) as one of the paramount pillars of the worldwide progress. In fact, financial inclusion has been identified as facilitator for seven of the 17 sustainable development goals. World Bank considers FI as the key to boost prosperity by poverty reduction. Since 2010, more than 60 countries have launched a national strategy directed towards attaining Universal Financial Access by 2020.

Women empowerment is a radical approach to transform power relations in favour of female gender that leads to better gender equality (Batliwala, 2007). This enables females to make their life choices, which in turn, effectively improves their well-being. Gender equality and women empowerment are essential to global progress and it can be enhanced by providing affordable financial services to women (Holloway, Niazi, & Rouse, 2017). After the persuasions by G-20 in 2014, financial services were perfused to a vast section of the society, and the period between 2011 and 2014 witnessed an upward trend in the number of first-time adults as bank account holders. On the flip side, it was not able to fill the gender gap for access to basic banking services (Ghosh & Vinod, 2017). This led to social exclusion and gender disparity, highly rampant in case of developing country as compared to a developed country (Ahmed, Aurora, Biru, & Salvini, 2001; Dawar & Singh, 2016). In the words of Noble Laureate Amartaya Sen, ‘Poverty is not merely lowness of income, but deprivation of basic capabilities’ (2014). Thus, accomplishing complete financial inclusion does not just determine the issues identified with financial structure, rather its centre is annulling the condition of social exclusion (Rangarajan Committee, 2008). Thus, the inclusive financial model has emerged as an arrangement in developing nations to achieve formative objectives. Formulation of mechanism to achieve women empowerment through affordable financial services is a rigorous approach to achieve sustainable growth globally.

The concerns for women empowerment have been rising in India over last few decades. Series of political events post-2014 in India has heightened societal concerns about women’s role in economic life as well as critical roles within their households. Mostly, empirical articles in this literature have studied the effects of financial inclusion on women empowerment that has evaluated an over-broadened meaning of empowerment or a truncated part of it (Goetz & Gupta, 1996). Most investigations are typically cross-country research (Demirguc Kunt, Klapper, & Singer, 2013; Lampietti & Stalker, 2000; Quisumbing, Haddad, & Pena, 1995). Within a nationalized context, the studies address the conduct of female-headed family units concentrating basically on financial access alone (Fletschner, 2008; Hazarika & Guha-Khasnobis, 2008; Rawlings & Rubio, 2005). Another set of studies implies presence of gender gap due to lower financial literacy (Fernandes, Lynch, & Netemeyer, 2014), behaviour biases (Frisancho, 2016) and institutional segregation (Corsi & De Angelis, 2017). Estimation of women empowerment is another glitch as it cannot be straightforwardly observed and has numerous features (Beteta, 2006; Mason, 2005; Swain & Wallentin, 2009).

In the Indian context, most of the studies (Datta & Singh, 2018; Ghosh & Vinod, 2017; Swamy, 2014) have used publicly available data to determine the extent of FI. Studies using primary data are limited in number. For women, the phenomena of urbanization and the growth of city ghettoes have unique causes and unique consequences, and yet these issues are largely ignored by prior studies in this area (COHRE, 2008). Only a handful of studies specifically focussed upon links between south Asian slums and women empowerment (Fisher, 2008; Hazarika, 2010; Kaur, Singh, Gupta, Bahuguna, & Rani, 2015; Nasrin, 2012). These studies relied solely on reviews of existing literature and evaluations based on secondary data. On the other side, the current study utilizes primary data from urban ghettos. The convincing motivations to examine women empowerment in this study are multifold. First, women represent two-fifth of work power, yet access to formal financial channels is very low. Second, government and RBI, both, have attempted strides to improve the number of financially included women, and its effect is yet to be assessed. Third, India is one of the developing economies for which the household-level information is promptly accessible, on both access and usage of financial inclusion schemes, by gender orientation. Fourth, most studies in literature have discussed financial inclusion of rural poor to evaluate and formulate strategies so that the involvement of rural poor may be enhanced in economy. However, the state of financial inclusion among the slum dwellers is largely underexplored in the literature. This is useful and relevant because the evaluation of expenditure, saving, and credit pattern among urban poor may help in formulating effective strategies to make them inclusive.

To contribute to literature, the current study investigates the degree of women’s financial inclusion in urban ghettos and how it empowers them. To be increasingly explicit, the study inspects the present status of financial inclusion plans of the Government of India for women in ghettos of industrial city, that is, Ludhiana (India) and how it may affect women. In this study, empowerment is estimated based on social, political, and economic empowerment of women in ghettos. The research framework estimates the impact of the financial inclusion schemes like PMJDY, PMJJBY, PMSBY, and APY on women living in urban slums in the industrial town of Ludhiana. The outcomes in the study are robust to demonstrate that there is a huge increment in the women empowerment due to the above-mentioned schemes. To control the extreme rate of deviations in this study, the sample has been drawn from the population of women who possess bank accounts under PMJDY. This study anticipates that the pace of women empowerment is probably going to trend upwards after they begin benefiting with higher financial inclusion schemes.

Financial Inclusion in India

Financial inclusion brings unbanked and under-banked people in the financial system to provide them the opportunity to access the financial services in order to create economic growth and leads to empowerment opportunities (Lenka & Barik, 2018). The Reserve Bank of India (RBI), in 2015, defines financial inclusion as ‘the process of ensuring access to appropriate financial products and services needed by vulnerable groups such as weaker sections and low income groups at an affordable cost in a fair and transparent manner by mainstream institutional players.’

Financial exclusion is a concern for developed as well as developing countries (Dymski, 2005). Even a ‘well-developed’ financial system has not been successful in bringing universal financial inclusion in many countries (Lenka & Barik, 2018).

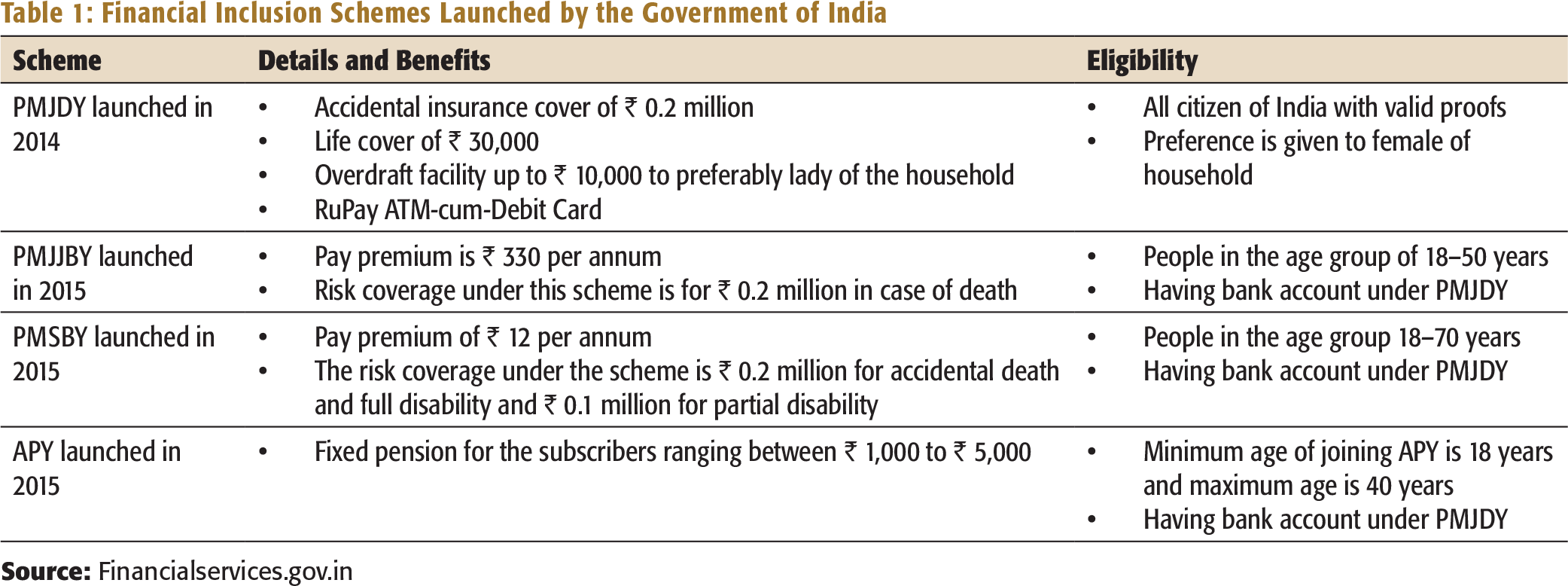

Financial Inclusion Schemes Launched by the Government of India

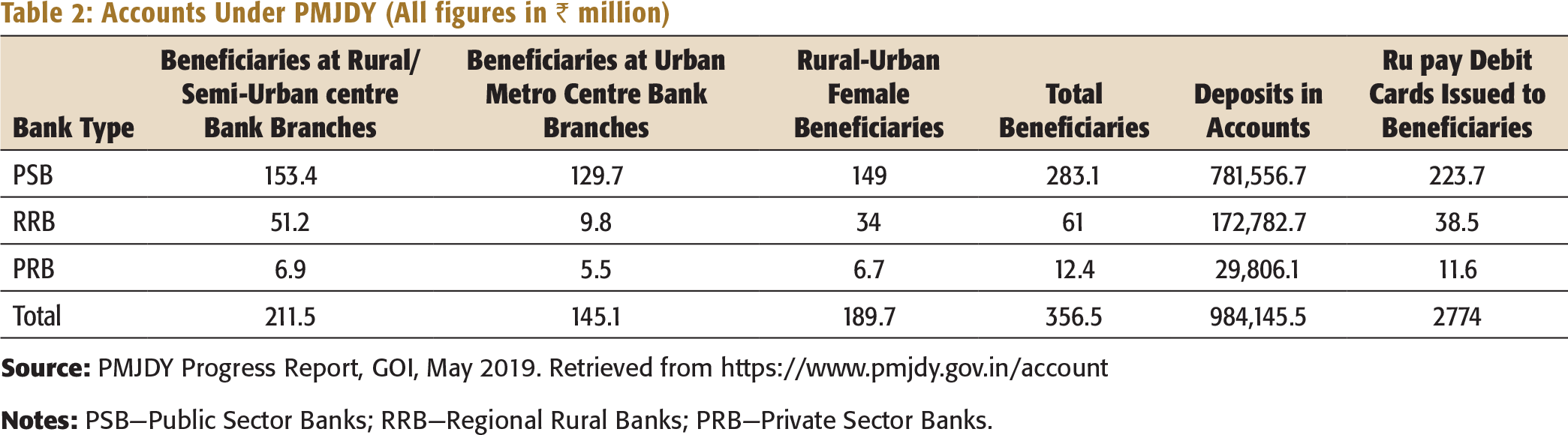

Accounts Under PMJDY (All figures in ₹ million)

Current State of Research on Financial Inclusion

Majority of the literature has focussed on the theoretical and conceptual development of financial inclusion in contexts of micro-finance institutes and self-help groups. An immense assemblage of literature can be found on financial inclusion in India for instance, self-help groups (Basu & Srivastava, 2005; Shah, Rao, & Shankar, 2007; Sinha, 2006; Swain & Varghese, 2009), and loans without collateral by the Grameen banks (Dev, 2006; Yunus, 2004), and current conditions of financial inclusion schemes that propelled after 2014 (Pillai, 2016; Singh & Naik, 2018; Tulasi, Golait, Sethi, & Goel, 2017; Verma & Garg, 2016).

A significant number of studies have measured financial inclusion with secondary data sets to identify the levels of financial inclusion in different regions using multidimensional index of banking services (Ambarkhane, Singh, & Venkataramani, 2014; Kim, 2016; Laha, 2015; Laha & Kuri, 2014; Park & Mercado, 2016; Raichoudhury, 2016). The basis of index construction is ‘distance-based approach’ used by UNDP. Chakravarty and Pal (2013) constructed financial inclusion index through axiomatic method covering data of Indian States from 1972 to 2009. Certain financial inclusion indexes were created using principal component analysis method (Bagil & Dutta, 2012; Lenka & Bairwa, 2016; Lenka & Sharma, 2017). Some of the studies (Arora, 2010; Bihari, 2011; Kumar & Mishra, 2009) created financial inclusion index based on financial access, availability, usage of formal financial services, demand side, and supply side indicators.

The research using primary data set is limited. A few studies attempted to identify the crucial factors for the extent of financial inclusion in India, that is, education, income, financial information, access, usage, and self-help groups (Bhanot, Bapat, & Bera, 2012; Bhutoria & Vignoles, 2018; Siddiqui & Siddiqui, 2017). Thus, the variable ‘financial inclusion’ is measured along these lines, that is, accessibility and ease of use of financial services for various group of individuals. The current data set in India shows that the number of bank account holders has risen to include around 80 per cent of adults under formal financial framework (Global Findex Report, 2017). As per RBI, 251 million account holders use mobile banking in 2018 and volume of transactions through mobile banking has crossed 3,047 billion in 2018–2019. The ongoing financial inclusion plans, such as PMJDY, PMSBY, and PMJJBY, have encouraged poor and marginalized Indians to open zero-parity ledger and avail insurance protection schemes at affordable rates (Barik & Sharma, 2019). These schemes have helped to top off financial inclusion gaps among various gathering of populace with 55 per cent expansion in women citizens’ share. Recently, Bapat and Bhattacharya (2016) investigated changes in financial inclusion of urban poor through a qualitative survey. Using a sample data of 202 slum dwellers in Pune (India), the study indicated that nuclear families with younger age groups and higher willingness-to-save have positive influence on financial inclusion of urban poor. These families have keen interest in availing loans from formal financial institutions.

Despite the fact that substantial advancement has occurred towards financial inclusion in India, a large number of the accounts have been underutilized by the bank account holders. According to Global Findex database, only 20 per cent of Indian adults have active savings bank accounts. The circumstances concerning access of credit from formal financial establishments are even more regrettable as only 7 per cent of Indian adults can access credit from their accounts. Significant reasons for this exclusion from the financial framework are low financial literacy (Fernandes et al., 2014; Lusardi & Mitchell, 2014), social inclinations (Frisancho, 2016; Karlan, McConnell, Mullainathan, & Zinman, 2016), institutional biases (Agier & Szafarz, 2013; Brana, 2012; Corsi & De Angelis, 2017; Fletschner, 2009; Muravyev, Talavera, & Schäfer, 2009), social limitation (Bylander, 2014; Guérin, Kumar, & Agier, 2013; Hummel, 2013), and absence of trust on financial organizations (Karlan, Ratan, & Zinman, 2014; Mehrotra et al., 2016).

EMPOWERMENT DIMENSIONS

Empowerment is defined as ‘Multi-dimensional social process that helps people gain control over their own lives. It is a process that fosters power in people, for use in their own lives, their communities, and in their society, by acting on issues that they define as important’ (Page & Czuba, 1999). Of the 17 objectives of United Nation Sustainable Development Goals (SDG) which are considered imperative for worldwide congruity and harmony, objective # 5 for gender balance and women empowerment is viewed as significant for transforming the world through giving equal chance to both of the genders. There are significant empirical evidences recommending that gender imbalance, to a great extent, harm economic advancement (Klasen, 2002), and gender difference in employment and education prompts negative effect on nation’s long stint development (Klasen & Lamanna, 2009).

Kabeer (1999) has defined women empowerment as ‘the ability to make strategic life choice in context where this ability was previously denied to them’. Women empowerment has received increased scholarly attention in last several decades as an avenue of enhancing mobility, health, economic condition, and participation in decision-making by women (Afrin, 2008). ‘Empowerment’ is a multidimensional concept and illustrates proliferation of end results. Owning bank account improves financial well-being of women (Ashraf, Karlan, & Yin, 2010; Swamy, 2014).

Political Empowerment

Gender equality is the core to human rights and a bedrock for achieving sustainable development. Increasing women participation in political leadership and decision-making is essential for economic and social development of economy (United Nations, 2018). Thus, political factors such as political quotas, awareness, and voting rights are important interventions in this regard (Armendáriz & Morduch, 2010; Deininger & Liu, 2013; Kabeer, 1999; Sundström, Paxton, Wang, & Lindberg, 2017). Administrative framework, social standards, independence in basic leadership, social versatility and systems additionally significantly affect women empowerment procedures (Bandiera et al., 2018; Beteta, 2006; Chatterjee, Gupta, & Upadhyay, 2018; Kumar et. al., 2019). Political empowerment is advancement of political inclusivity and supporting political involvement as per rights and legitimate job of women. Political empowerment can be accomplished through political awareness, position of power, support in political action, and participation in political groups (Chatterjee et al., 2018). Expanding female portrayal in administration, casting a ballot, and political contribution and inclusion in casual groups to straighten out network issues leads further women empowerment (Bardhan & Klasen, 1999).

Economic Empowerment

Economic empowerment is the capacity to contribute towards the growth processes in a way that recognizes the value of their contributions and makes a fair distribution of their wealth to enhance the access of economic resources (OECD, 2011). Swain and Wallentin (2009) found that economic factor contributes significantly to women empowerment. In another study, Al-Mamun, Wahab, Mazumder, and Su (2014) investigated the change in women empowerment through qualitative survey that quantified economic empowerment utilizing following criteria: decision-making at household level, financial/economic security, resource control, say/control in familial decisions, legal awareness, and mobility. Based on the sample data of 242 low-income urban women in Malaysia taking interest in micro-credit programme, the study quantified the effects of household basic leadership. In an extensive study, Chiapa, Prina, and Parker (2016), through field investigations of female heads of households reviewing 1,236 families in urban ghettos, found that access to savings bank accounts help poor families to handle their assets better, to prioritize education and consumption expenditure, and to feel more responsible for their financial/economic circumstances.

Social Empowerment

Social empowerment means giving power or authority to an individual to improve their livelihood. Person-to-person communication and correspondence, and more noteworthy, social versatility, help in empowerment of women (Swain & Wallentin, 2009). Searing and Chiappori (1998) recommended that social pressure may likewise adjust the women’s capacity inside family unit for decision-making. Economic empowerment incorporates economic independence, budgetary self-adequacy, and financial literacy that leads to learning and aptitudes to deal with financial prosperity (Postmus, 2010; Postmus, Plummer, McMahon, & Zurlo, 2013). Nonetheless, all the dimensions of empowerment, such as social, political, and economic empowerment, are all well-integrated and cannot be secluded (Taylor, 2000).

The relationship between financial inclusion and gender inequality has been underexplored and needs further investigation. Several studies (i.e., Fraser, 2011; Karim, 2011; Roodman and Qureshi, 2006) have raised questionable record on financial inclusion and women empowerment. For example, Bateman (2012) has criticized financial inclusion as ‘emerging new label’ and considered it mere rebranding of microfinance. Also, financial inclusion drives over indebtedness and lacks demonstrable poverty impact (Duvendack et al., 2011; Guérin, Labie, & Servet, 2015; Stewart et. al., 2012). However, significant number of studies claimed that having bank account can improve the financial well-being of women (Ashraf et al., 2010; Swamy, 2014).

Thus, the proposed hypothesis is as follows:

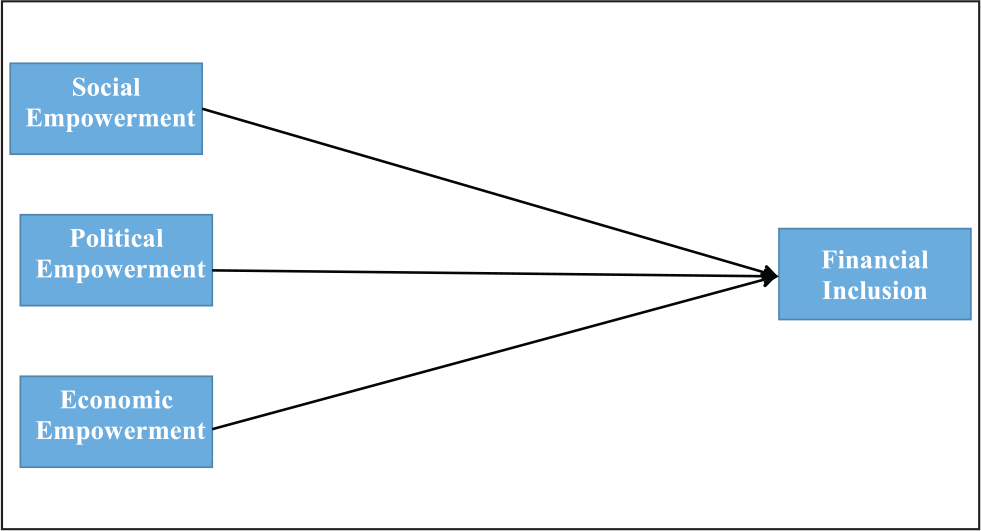

The framework of the current study is shown in Figure 1, that is, financial inclusion leads to women empowerment. There is tremendous literature on financial inclusion and its capacity in impacting women empowerment. But few studies have examined the role of financial inclusion in empowering female ghetto inhabitants. This is important because there is far too much vulnerability in the lives of the poor and those just living above poverty line. Around 93 per cent of labour forces work in the informal sector. Vulnerability with respect to women managing finance at home rises due to the lack of access to formal financial services. This study attempts to examine financial inclusion of women in urban ghettos of Ludhiana post-PMJDY. Punjab is the fifth most urbanized state in India. With 133 urban centres recently included in Ludhiana city, it has the highest urban population in Punjab. Ludhiana (Punjab) is a prime industrial centre in northern India and is centre point for the hosiery industry and other small-scale industries.

Framework of the Study

Thus, the particular goals of the present investigation are to explore the compass and utilization of financial inclusion schemes like PMJDY, PMJJBY, PMSBY, and APY among female slum dwellers at Ludhiana, and to examine the effects of aforementioned schemes on their social, political, and economic empowerment (as shown in Figure 1).

RESEARCH METHODOLOGY

The current study explores positive effect of financial inclusion on lives of women living in urban slums. This study is both relevant and important for conceptualizing and actualizing programmes for poor, and particularly women.

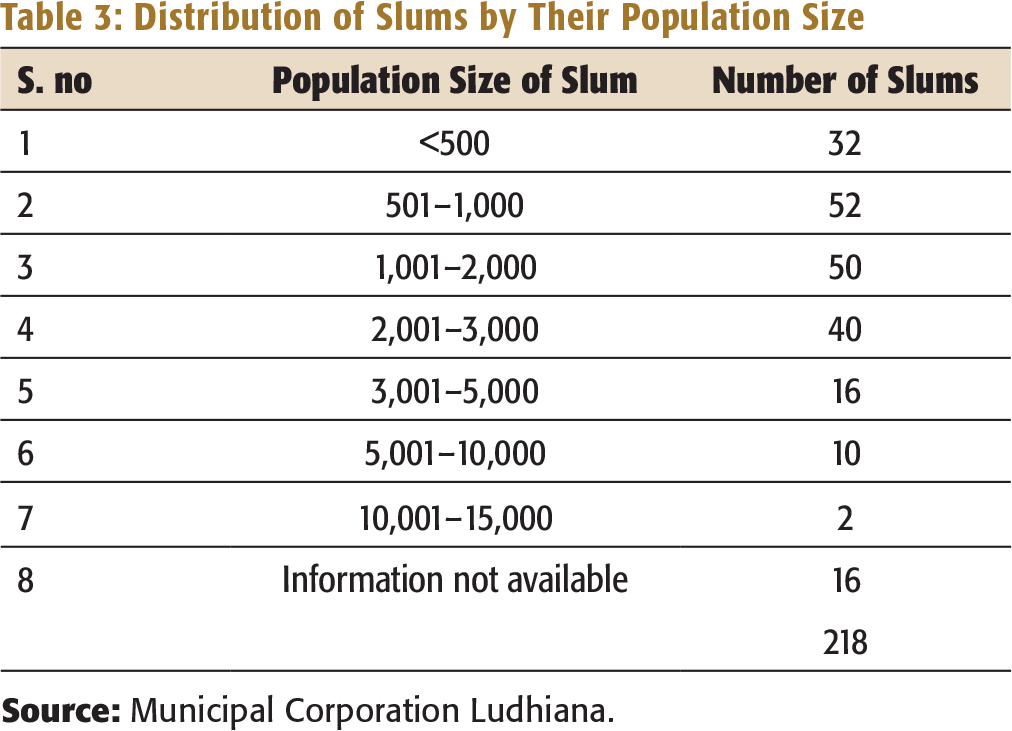

Distribution of Slums by Their Population Size

The sampling unit, that is, women in slums, was chosen using simple random sampling for this study. To test the hypothesized relationships, a questionnaire-based survey approach was used with 12 items for the constructs in this study. The questionnaire was partitioned in two sections. The first section analysed socio-economic status and access to different financial inclusion schemes of the Indian government. Second part collected the information for social, economic, and political women empowerment. The items of political empowerment were adapted from Niemi, Craig, and Mattei (1991) and Boley, Ayscue, Maruyama, and Woosnam (2016); the items of social empowerment were adapted from Basu (2006) and Boley et al. (2016); and the items of economic empowerment were adapted from Raj et al. (2018), Postmus et al. (2013) and Basu (2006). All estimations in the investigation were subjective assessments of the respondents utilizing five-point Likert scale (where 1 represents strongly disagree and 5 represents strongly agree).

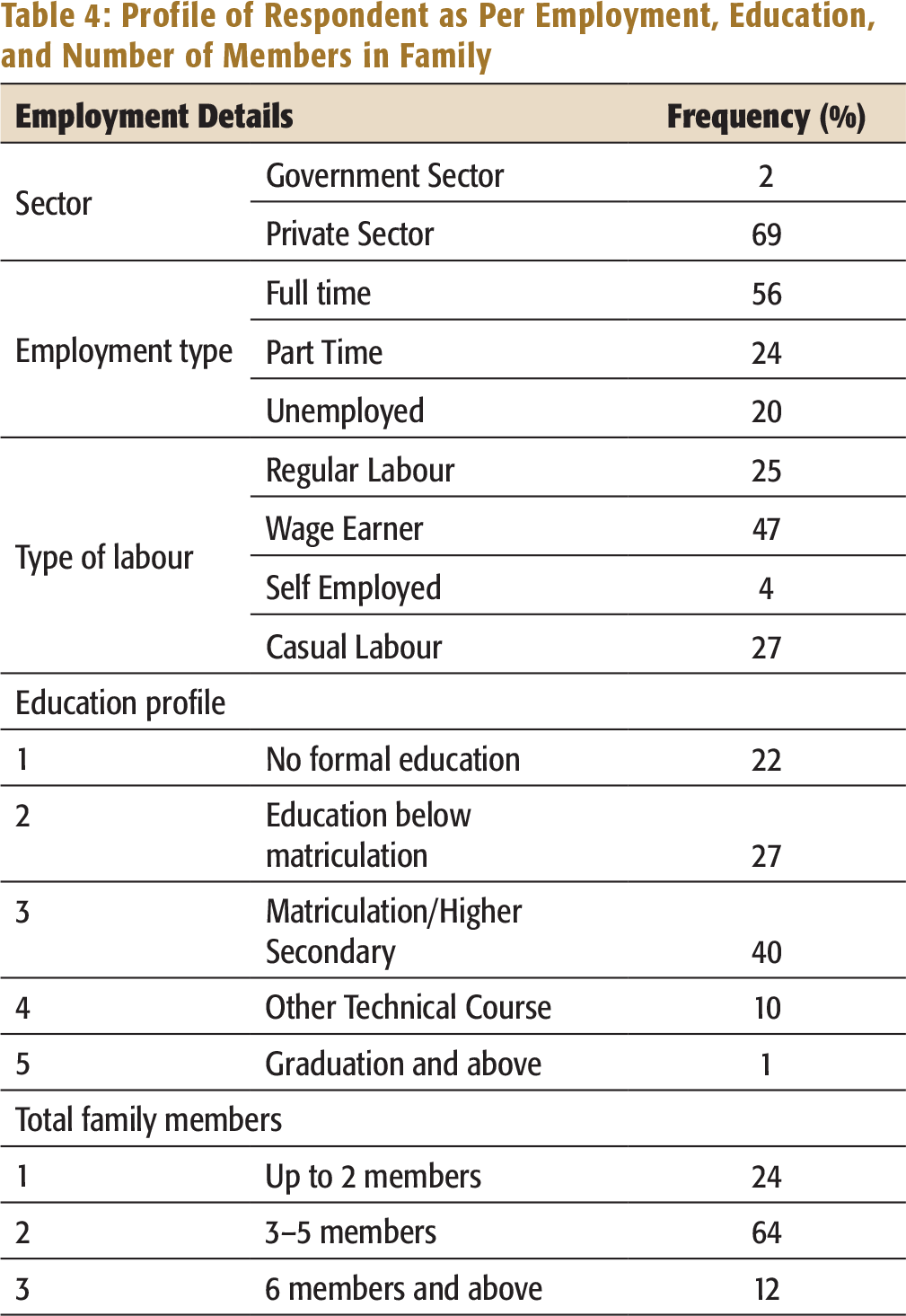

Profile of Respondent as Per Employment, Education, and Number of Members in Family

Data Collection Process and Analysis

The sample consisted of women living in urban slums and the profile of respondent is provided in Table 4. Respondents for the survey were randomly selected and the eligible respondents for the survey were women owning PMJDY bank accounts. This ensured the eligibility of respondents to enrol into financial inclusion schemes. In total, 1,000 respondents were approached, of which 737 substantial responses were gathered (73% response rate). In order to identify and validate the constructs, the exploratory and confirmatory factor analyses were applied on the data. Further, to test the hypothesis, one-way analysis of variance (ANOVA) was applied.

ANALYSIS AND FINDINGS

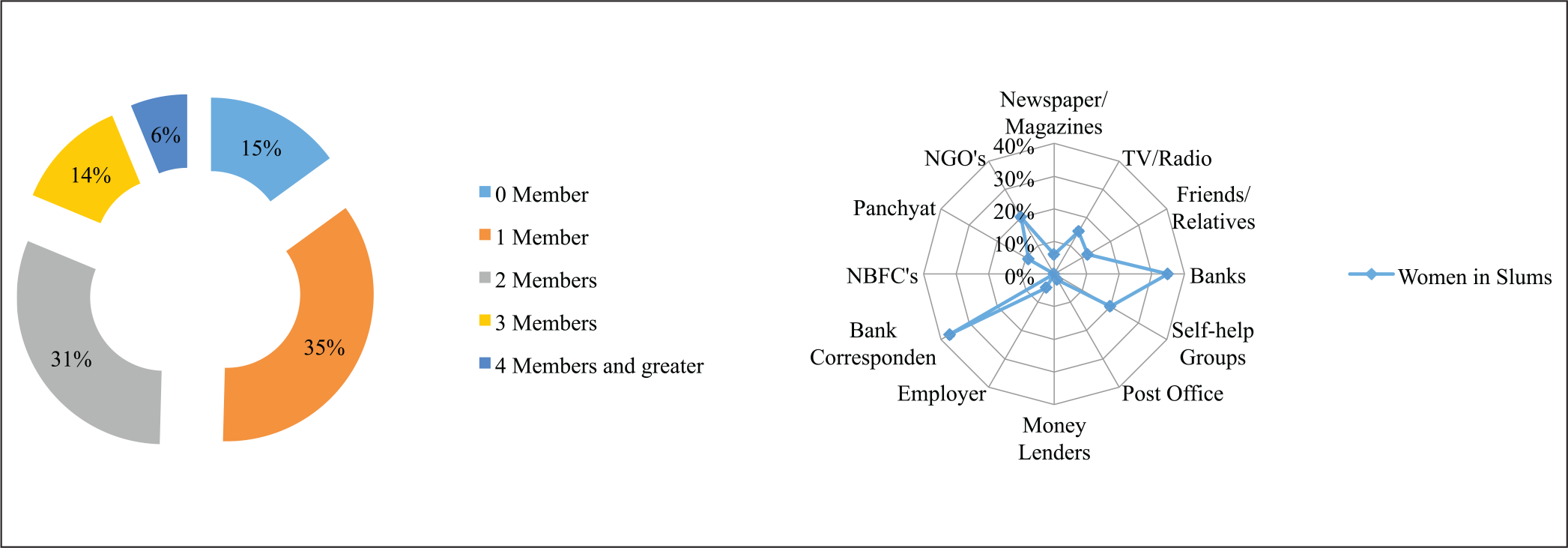

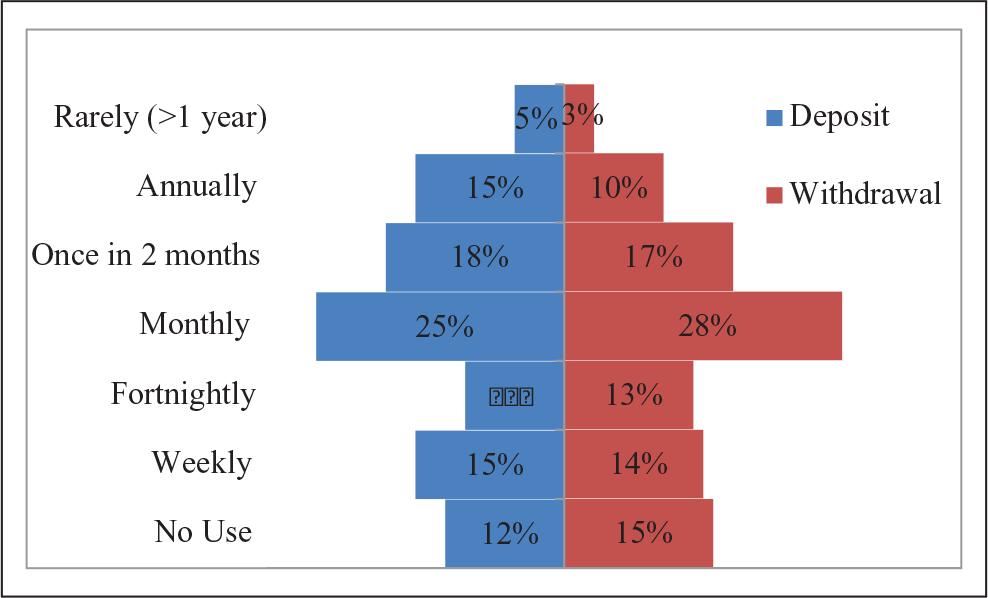

The collected data were further analysed to know the current status of financial inclusion among female slum dwellers. Figure 3 shows the access of PMJDY accounts as per household and sources of awareness of respondents for PMJDY accounts. Figure 4 shows the frequency of operation of the PMJDY account.

PMJDY Accounts as Per Households, Awareness, and Use of Accounts

Frequency of Operation of PMJDY Account

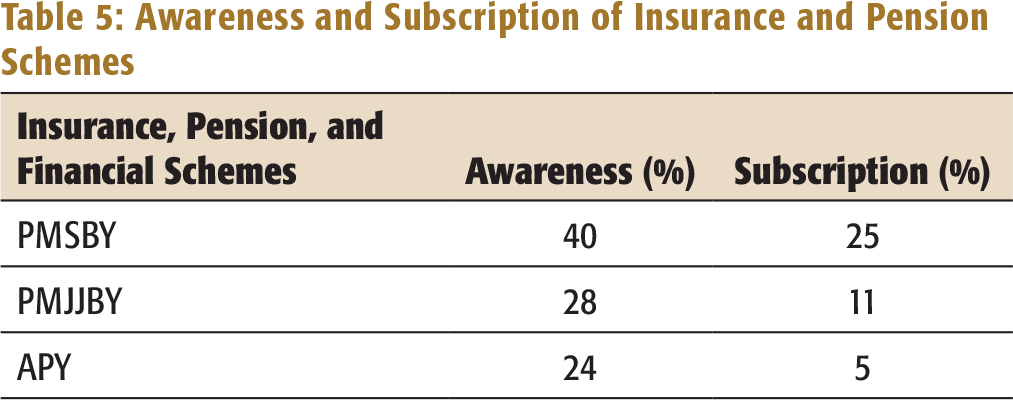

Awareness and Subscription of Insurance and Pension Schemes

To upgrade the level of financial inclusion in the country, the Indian government has introduced three social security schemes, namely, PMJJBY, PMSBY, and APY in the last 5 years. The goal of these schemes is to serve the objective of universal financial inclusion by penetrating insurance towards the bottom of the pyramid, that is, the weaker sections.

It was found that majority of women were aware about PMSBY and this scheme had higher subscription rate. It was also found that the general awareness and financial literacy for life insurance, accidental insurance, and pension were very low among slum dwellers at Ludhiana (Table 5).

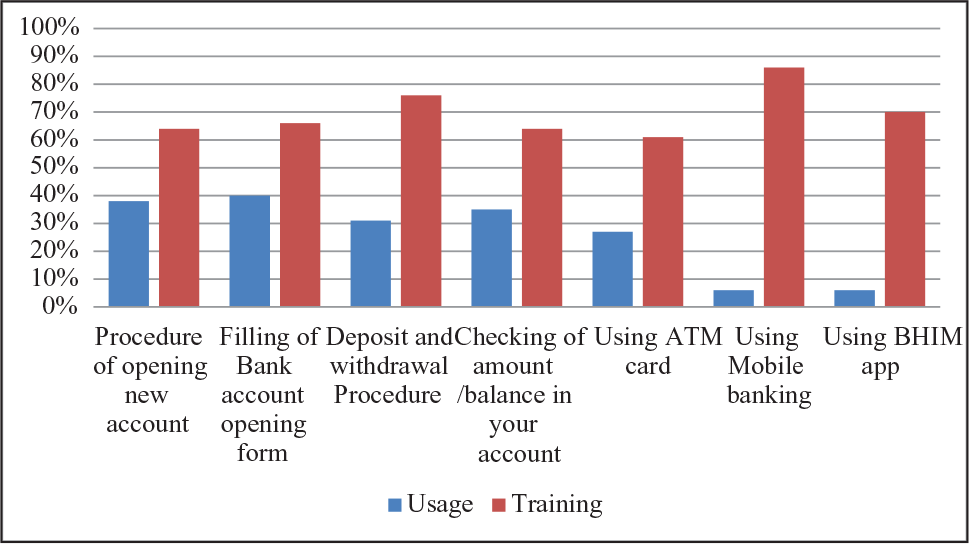

Usage and Training in Banking Services

The respondents were further intrigued regarding the usage of banking services and their training needs. It was found that 40 per cent of women at slum could fill bank account opening form, 35 per cent of women could check their account balance, and only 6 per cent of them could use mobile banking facilities. Respondents listed the need for training in mobile banking, withdrawal and deposit procedure, and operating Bharat Interface for Money (BHIM) mobile payment app (Figure 5).

Exploratory Factor Analysis (EFA)

Exploratory factor analysis was applied using principal component analysis and Varimax rotation (SPSS 22.0).

The factor analysis was suitable for this data as the Kaiser–Meyer–Olkin 1

The Kaiser–Meyer–Olkin measure of sampling adequacy is a statistic that indicates the proportion of variance in your variables that might be caused by underlying factors. High values (close to 1.0) generally indicate that a factor analysis may be useful with your data. If the value is less than 0.50, the results of the factor analysis probably will not be very useful.

Bartlett’s test of sphericity tests the hypothesis that your correlation matrix is an identity matrix, which would indicate that your variables are unrelated and therefore unsuitable for structure detection. Small values (<0.05) of the significance level indicate that a factor analysis may be useful with your data.

Confirmatory Factor Analysis (CFA)

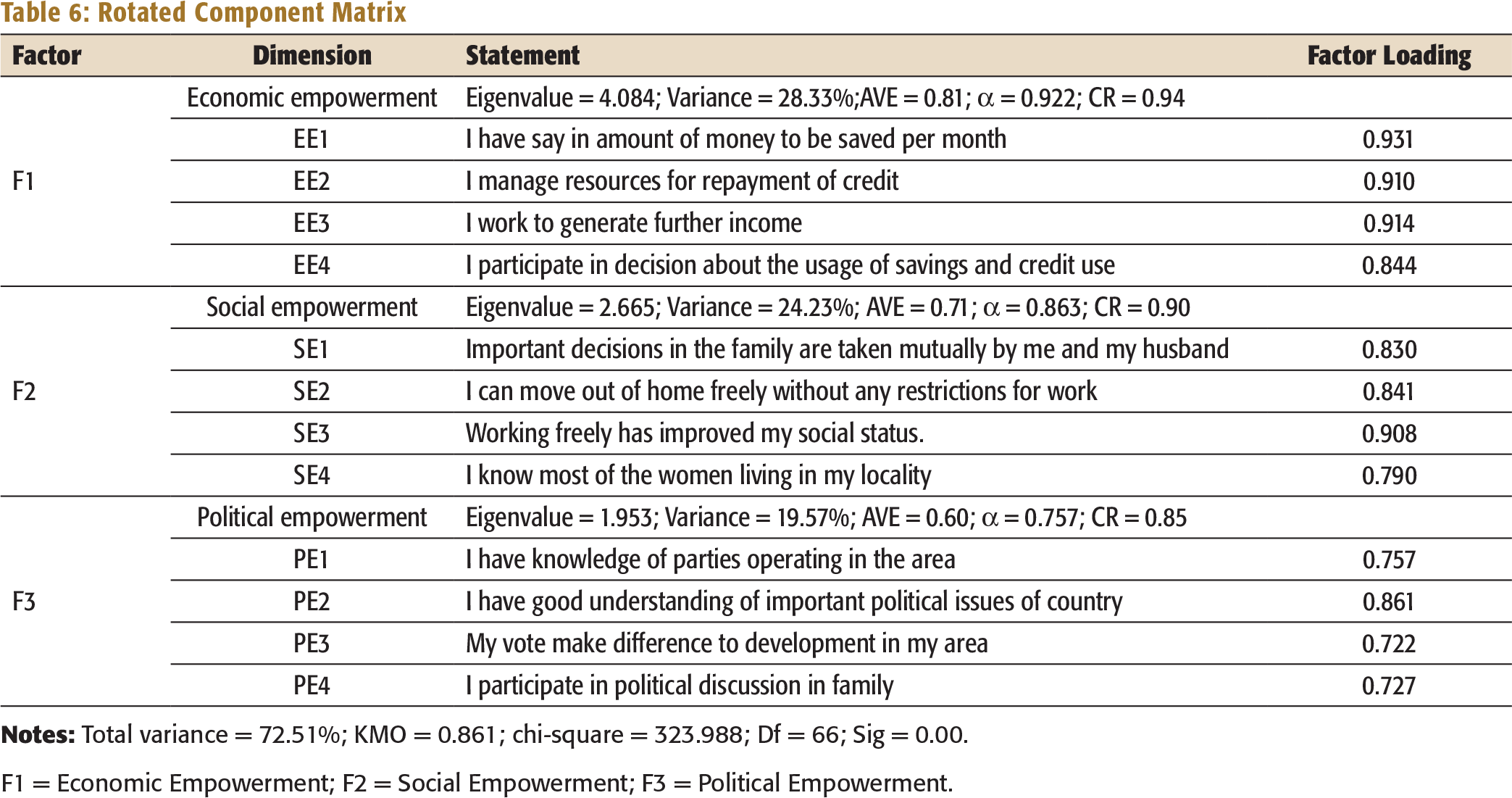

The multi-factor CFA was applied on 12 items to test the measurement model using the maximum likelihood method. The model fit was assessed appropriate, and the three-factor model had the best overall fit for the data with a χ2/df = 1.2 (χ2 = 694.545, df =0 564); CFI as 0.960; GFI as 0.922; AGFI as 0.901; and RMSEA as 0.078. The discriminant value was checked though average variance explained (AVE) values for all constructs were more than 0.5 and smallest items of test measurements were more than 1.96 (α=0.05) (Fornell & Larcker, 1981). The composite reliability of each factor extended from 0.85 to 0.94 (reported in Table 5), which surpasses the suggested level of 0.6 (Hu & Bentler, 1999). The hypothesis for relationship was assessed by applying one-way ANOVA.

One-Way ANOVA

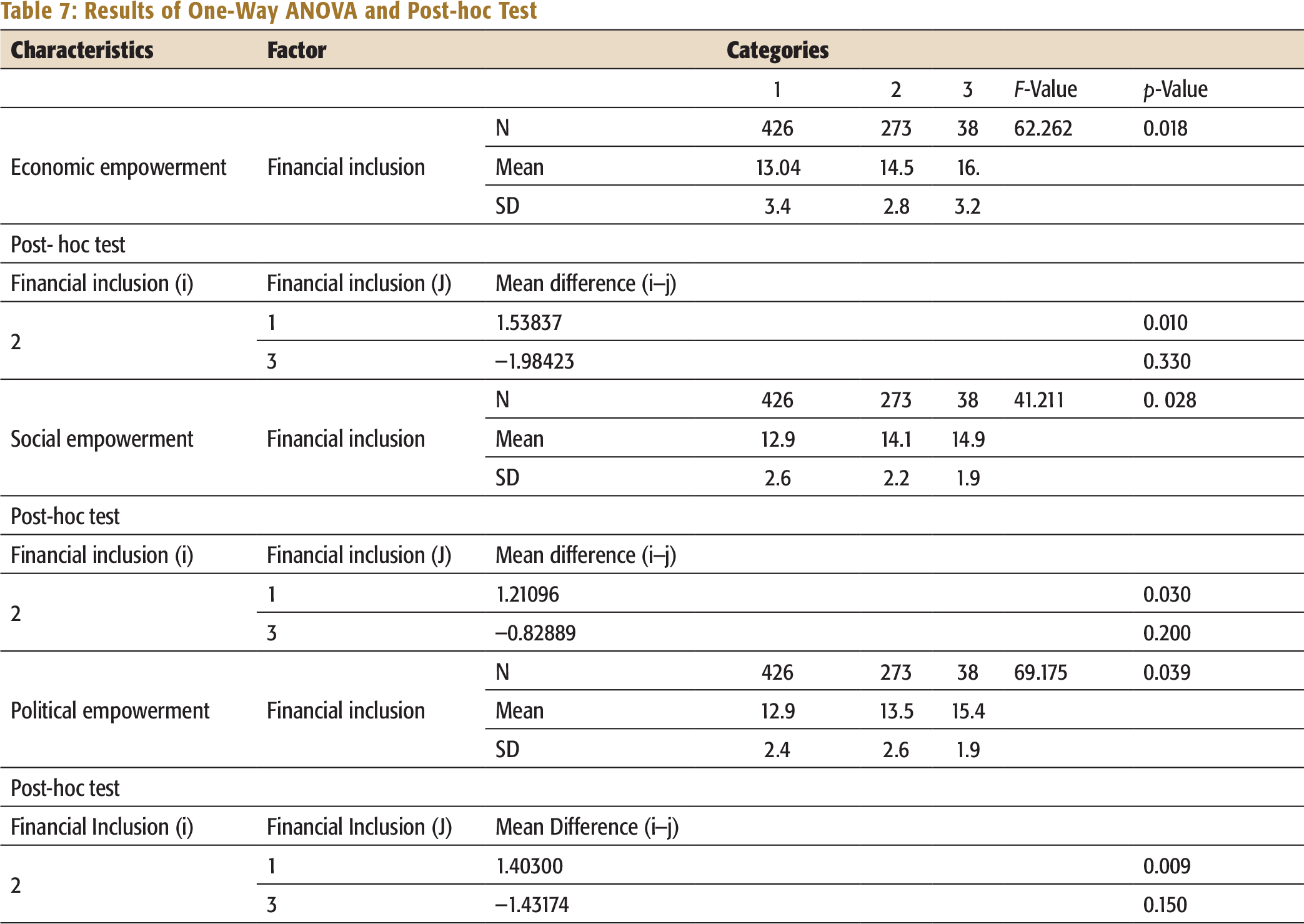

The study examines whether there is a significant mean difference in financial inclusion levels on social, political, and economic empowerment of women in slums. Financial inclusion has been divided into three levels based on accesses and usage, that is, PMJDY, PMSBY & PMJJBY, and APY. The results of one-way ANOVA showed there is significant difference between the overall financial inclusion and empowerment indicators. Games-Howell post hoc test was used to identify the difference in financial inclusion (Table 7). Table 7 shows the result of one-way ANOVA and statistically significant difference between the group means. The p-value for PMJDY, PMSBY, and PMJJBY for economic empowerment is 0.010, for social empowerment is 0.030, and political empowerment is 0.039, which are below 0.05. Thus, there is a statistical difference in the empowerment of the respondents who have availed PMJDY and PMSBY and PMJJY. As per the mean difference, the empowerment of the respondents has increased by availing the insurance schemes of PMSBY and PMJJY. On the other hand, the mean for economic, political, and social empowerment is not statistically significant for APY.

DISCUSSION AND CONCLUSION

Rotated Component Matrix

F1 = Economic Empowerment; F2 = Social Empowerment; F3 = Political Empowerment.

Results of One-Way ANOVA and Post-hoc Test

As recognized in this study, all sorts of financial inclusion processes have the ability to impact the empowerment of women and this is in line with the available literature which suggests that financial inclusion has an impact on the social empowerment of women (Al-Mamun et al., 2014; Basu, 2006; Blattman, Green, Annan, & Jamison, 2013; Chatterjee et al., 2018; Goetz & Gupta, 1996; Rahaman, 1999; Weber & Ahmad, 2014; Wrigley-Asante, 2012). Similarly, the results of financial inclusion and political empowerment (Basu, 2006; Bhattacharyya, 2019; Hashemi, Schuler, & Riley, 1996; Kabeer, 1999; Malhotra & Schuler, 2005) and economic empowerment (Datta & Sahu, 2017; Bayulgen, 2015; Hashemi et al., 1996; Kabeer, 1999) are consistent with the literature. Consequently, this study presents an all-encompassing replication of well-built inclusive-credibility connections. Replication studies with extensions are important to break down the use of results on a wide scale (Hermes & Lensink, 2011) to identify generalization of relationships, for both with Indian population of slum dwellers and in context of financial inclusion.

The outcomes reveal that distinctive components of empowerment are statistically significant by joining formal financial services. Women empowerment is related to each one of the measures of empowerment which reverberate the hypotheses in this study and past investigations. The study also reveals that women with higher access and usage of financial services, such as opening bank account and availing insurance, have higher social, political, and economic empowerment. This has implications for increasing women’s bargaining power in society, that is, greater negotiations, freedom for political choices, taking financial decisions at work, and decision-making within family, leading to higher women empowerment.

The results of the current investigations regarding the effect of financial inclusion on empowerment dimensions for women in urban slums also indicate that women with access to PMSBY and PMJJBY have higher overall social, political, and economic empowerment. However, women accessing APY show no significant impact on the social, political, and economic empowerment. One of the plausible reasons may be that women with higher pool of savings have keen interest in inclusive insurance (Fletschner & Kenney, 2014). It may be due to the financial coverage, especially in the time of disaster and risk.

The results suggest that the PMJDY scheme, launched in 2014–2015 by the Government of India as a part of financial inclusion strategy, has been quite successful especially in case of women in slums. It was noteworthy that even less educated women have joined formal banking system and had sound awareness regarding these financial inclusion schemes. However, the subscriptions to these schemes were not considerable. Both, non-profit organizations and SHGs, play a vital role in increasing awareness regarding these schemes among women in slums. However, the digital payments and usage of mobile banking applications are still a challenge. The Indian government should create a supportive environment to enhance the impact of these schemes.

The second objective was to confirm the convergence of dimensions of empowerment for women in urban slums. The strong relationships between women empowerment and financial inclusion provide insights to policy makers.

Third objective was to show the linkage between financial inclusion and dimension of women empowerment. A positive influence of financial inclusion on social, political, and economic dimensions of women empowerment was found. But the long-term sustainability of these schemes relies upon its involvement in generation of economic activities for women. The policy decisions should accelerate procedures through supportive mechanism, and develop superior systems and easy interaction on platforms among different stakeholders.

This study also revealed that women in urban slums did not lack access to financial institutions but suffered from (a) economic risks such as unsteady earnings, non-contractual informal jobs, (b) financial risks such as reliance on cash economy, informal credit, and (c) social risks such as social fragmentations. Considering these differences, there are substantial gaps in the lives of poor urban women. In order to bridge this gap, there is a need to systemically understand financial lives of these households and customize the delivery mode such that it is affordable and scalable. Thus, there is a need to create new points for information collection, so that more inclusive financial system for women in slums may be created.

This study makes several contributions to theory and practice. The study advances the debate on women empowerment of women ghettoes through financial inclusion schemes of the Government of India. The study identifies the substantial need for the development of formal financial system that may enhance the scale of financial inclusion.

This study has certain limitations. Data were collected from the industrial city of Ludhiana (Punjab) that restricts the generalization of results to the Indian population. The questionnaire approach was the only way to gather primary data and thus, the results might have a common-method bias. This research does not consider longitudinal research structure and is cross-sectional in nature which, in turn, does not permit considering long haul interactions between women empowerment and financial inclusion measures.

A pan-India, city and state study to examine whether comparable outcomes can be produced. This will provide an all-encompassing perspective useful in planning future research strategy at national level. An exhaustive qualitative research in the future may create a wide-going thought regarding financial inclusion and women empowerment.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.