Abstract

Executive Summary

A healthy financial system is important for the growth process of an economy. It affects growth by influencing the saving, investment and technological innovations. In fact, researchers argue that low-income countries like Nepal need a much more robust and active financial system when compared to the developed world. Therefore, this study examines the relationship between financial development and economic growth using annual time series data for Nepal during the period 1984–2014. Because Nepal has a bank-based economy, the study used credit issued by banking and financial institutions to the private sector as the proxy for financial development. The economic growth has been measured using real gross domestic product (GDP) growth and real GDP per capita growth (constant 2005 US$). The autoregressive distributed lag (ARDL) bounds testing approach is used to investigate the cointegration among variables in the presence of structural breaks. The study used Zivot and Andrews’ (ZA) unit root test in order to find the structural breaks in the variables. The study finds that the structural change in private credit took place in 2007 when the government of Nepal and Maoists (the then rebels) signed a Comprehensive Peace Agreement and the Maoist rebels joined the interim government, which formally ended the 10 years long civil war in Nepal. Similarly, the study observes break points in real GDP growth and per capita growth in 2001 when the Royal Massacre and a state of emergency took place in Nepal. After allowing for structural breaks, the study finds evidence of a cointegration relationship between financial development and economic growth when economic growth is used as the dependent variable. Thus, it can be argued that the long-run causality is unidirectional from financial development to economic growth in Nepal. The estimates of the ARDL approach suggest that financial development has a significant positive impact on economic growth in both long run and short run. However, the estimates show that gross domestic saving, a control variable, has a negative impact on economic growth in Nepal. It clearly indicates that Nepal has long not been able to utilize the savings in the productive sector. The political instability, poor investment policies and securities and hence the lack of foreign investment and lack of technological innovations could be the causes for Nepal not benefiting from the country’s savings. It is also found that trade openness has a negative relationship with economic growth in the long run: possibly the cause of the persistent trade deficit of Nepal with the rest of the world. However, in the short run, the result shows a positive relationship between trade openness and growth. In fact, it is found that the magnitude of the positive impact of trade openness in the short run is higher than the magnitude of its negative impact in the long run. Thus, the policymakers should give more emphasis on trade and investment policies that could reduce the prolonged trade deficit and help the nation in getting long-term benefits from international trade.

The endogenous growth model also tries to shed some light on the finance–growth relationship more precisely. According to Bencivenga and Smith (1991), the endogenous growth model is concerned with the financial markets, savings, investments, and growth. Financial intermediaries affect growth by altering the savings (Bencivenga & Smith, 1991; Pagano, 1993). In this way, Dermirguc-Kunt (2006) argued that a well-functioning financial system is a foundation on which sustained economic development can be built. However, the financial system in low-income countries like Nepal is still underdeveloped. The political turmoils, corruption, weak regulatory and legal policies, poor information systems, and the poor technological innovations have been major barriers to the development of the financial sector in Nepal. In fact, it is argued that political instability and corruption are the major factors behind the poor financial system in low-income countries (Detragiache, Gupta, & Tressel, 2005).

Nepal initiated its financial sector reform programme in the late 1990s, which resulted in several positive changes in the Nepalese financial system (Bhetuwal, 2007; Shrestha & Chowdhury, 2006). However, a decade-long civil war, from 1996 to 2006, in Nepal has further stagnated the development of the financial sector. The current Nepalese financial system is comprised of the banking and non-banking financial industry, the insurance industry, and the capital market. Nevertheless, the new constitution and federalism system in Nepal is yet to make major changes in its financial system, especially in the banking sector. To this end, it has become more important than ever in Nepal to analyse the relationship between finance and growth because it helps policymakers in the course of policy formulation.

Although few studies have investigated this relationship in Nepal (see Bhetuwal, 2007; Gautam, 2014; Kharel & Pokhrel, 2012; Timsina, 2014), there still exists a huge gap regarding the methodology used in these studies. For example, although the stationarity and cointegration phenomena are well recognized in time series data, studies on finance growth in Nepal are majorly based on the Johansen (1988) system-based approach to cointegration. This technique, however, has been criticized for different reasons. Pesaran, Shin, and Smith (2001) argued that Johansen’s cointegration test is sensitive to the sample size. Similarly, another key issue with these studies is that they make no attempt to address the issue of structural breaks. Perron (1989) argued that ignoring the issue of potential structural breaks can invalid the statistical results not only of unit root tests but also of cointegration tests. Thus, it is not clear if the estimates of these studies represent a valid inference or a spurious inference. Identifying these issues of importance, this study aims to fill this gap by analysing the finance–growth relationship using recent estimation technique of the Autoregressive-Distributed Lag (ARDL) approach to cointegration1 in the presence of structural breaks.

REVIEW OF THE RELATIONSHIP BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH

The relationship between financial development and economic growth has been studied in depth, but the direction of the causality and the relationship remained argumentative. Schumpeter (1911) argued that financial development is a prerequisite for economic growth. He forwarded the argument of financial development and technological innovations causing growth. This argument has further been supported by different studies on financial growth. A pioneering study by King and Levine (1993a), using a data set of 80 countries, found that financial development is strongly associated with the real per capita GDP growth, the rate of physical capital accumulation, and improvements in the efficiency with which economies employ physical capital. A large number of studies using either cross-sectional data, time series data, firm-level data, or a combination of them have also found positive relationship between financial development and economic growth (Bist, 2018; Christopoulos & Tsionas, 2004; De Gregorio & Guidotti, 1995; Durusu-Ciftci, Ispir, & Yetkiner, 2017; Herwartz & Walle, 2014; Jedidia, Boujelbène, & Helali, 2014; Khan & Senhadji, 2000; King & Levine, 1993b; Muhammad, Islam, & Marashdeh, 2016; Pradhan, Arvin, Hall, & Nair, 2016; Rajan & Zingales, 1998; Samargandi, Fidrmuc, & Ghosh, 2014; Uddin, Sjö, & Shahbaz, 2013; Zhang, Wang, & Wang, 2012). Similarly, Beck, Levine, and Loayza (2000) raised the issue of simultaneity and studied not just the relationship between finance and growth but also the source through which economic growth is influenced. They concluded that financial intermediaries have a large positive impact on total factor productivity growth, which feeds through to overall GDP growth.

On the other hand, Lucas (1988), a neoclassical theorist, argued that the role of financial development on economic growth is over stressed. Similarly, giving the reasons of (a) volatility in stock pricing, (b) stock and currency market interactions in unfavourable economic shocks, and (c) the unsuitable impact of stock market development in the group banking system on developing countries, Singh (1997) argued that financial development may not be beneficial for economic growth. The view that there is no relationship or negative relationship between finance and growth has also been supported by various studies (Al-Malkawi, Marashdeh, & Abdullah, 2012; Andersen & Tarp, 2003; Arestis & Demetriades, 1997; Ayadi, Arbak, Naceur, & De Groen, 2015; De Gregorio & Guidotti, 1995; Ductor & Grechyna, 2015; Grassa & Gazdar, 2014; Mhadhbi, 2014).

A more diverse view was forwarded by Gerschenkron (1962): Economic backwardness of a country determines the role of finance. According to Gerschenkron, economically backward countries need a more active financial system whereas countries that are developed do not need an active financial system. This argument was further expressed by Patrick (1966). Patrick forwarded two views namely (a) the supply-leading pattern and (b) the demand-following pattern. Patrick argued that the supply-leading effect dominates during the early stage of the economic development and the demand-following financial response becomes dominant as the modern sector of the economy develops. However, this hypothesis has also been remained controversial over the period. Jung (1986) found some evidence in support of Patrick’s hypothesis, whereas Wood (1993) rejected the same on the empirical ground. Jung (1986) found that underdeveloped countries are characterized by the causal direction running from the financial development to the economic growth; however, developed countries are characterized by the reverse causality direction. Similarly, Abu-Bader and Abu-Qarn (2008), Adu, Marbuah, and Mensah (2013), Agbetsiafa (2004), Bojanic (2012), Christopoulos and Tsionas (2004), Enisan and Olufisayo (2009), Ghali (1999), Hsueh, Hu, and Tu (2013), Khadraoui and Smida (2012), Masih, Al-Elg, and Madani (2009), Menyah, Nazlioglu, and Wolde-Rufael (2014), Pradhan, Arvin, Bahmani, Hall, and Norman (2017), and Pradhan, Dasgupta, and Bele (2013) also found some evidence for the supply-leading hypothesis.

In contrast to the supply-leading hypothesis, Robinson (1952) argued that it is not the finance that causes growth rather it is the growth that creates demand for the finance. This view, the demand- following hypothesis, has also been supported by various empirical works (Al-Awad & Harb, 2005; Ang & McKibbin, 2007; Hassan, Sanchez, & Yu, 2011; Kar, Nazlıoğlu, & Ağır, 2011; Liang & Teng, 2006).

Further literature review shows that another group of studies has reported that finance and growth cause each other. For example, Al-Yousif (2002), Apergis, Filippidis, and Economidou (2007), Demetriades and Hussein (1996), Eslamloueyan and Sakhaei (2011), and Pradhan (2009) found a bi-directional causality feedback response between financial development and economic growth. A more recent study by Pradhan et al. (2017) shows that causality is sensitive to the use of financial development proxies. The study accounted a unidirectional causality running from banking sector development to economic growth. However, a bidirectional causality was observed between stock market development and economic growth, and insurance sector development and economic growth.

In the context of Nepal, Bhetuwal (2007) found a bidirectional causal relationship between liberalization of the financial sector and level of financial development. Similalry, Gautam (2014), Kharel and Pokhrel (2012), and Timsina (2014) empirically showed that financial development has been contributing to the economic growth. This study seeks to contribute to this debate using Nepal as a case study. First, there is limited knowledge on the finance–growth nexus using the recent data in Nepal. To the best of our knowledge, no study has been found to have analysed finance–growth nexus in Nepal, using the most recent time series data analysis technique like the ARDL approach and cointegration in the presence of structural breaks. Second, this study analyses both the short-run and long-run effects of financial development on economic growth, which is also lacking in the context of Nepal. Furthermore, this study also includes trade openness, savings, and inflation as the control varaibles. By all means, these techniques were used in different time series studies on finance–growth nexus in other countries. However, the results of these studies could not be generalized in the context of Nepal because of the differences in political system, financial system, policies and regulations, and other country-specific factors that affect the finance–growth relationship. Therefore, this study contributes to the literature by providing recent evidence on finance–growth nexus in Nepal using the ARDL approach to cointegration in the presence of structural breaks.

MEASUREMENT OF FINANCIAL DEVELOPMENT AND SELECTION OF THE VARIABLES

Several indicators of financial development have been proposed in the literature such as monetary aggregates; narrow (M1) and broad money supply (M2) (Arestis & Demetriades, 1997; King & Levin, 1993a, 1993b), total bank deposit liabilities (Christopoulos & Tsionas, 2004; Luintel & Khan, 1999), composite index of financial development; sum total of banking sector development and stock market development (Pradhan et al., 2013; Pradhan et al., 2017), liquid liabilities (King & Levine, 1993a), and credit to private sector (Beck et al., 2000; Kar et al., 2011; Levine, Loayza, & Beck, 2000). However, Khan and Senhadji (2000) argued that M1 and M2 are poor proxies of the financial development as they are more related to the ability of the financial system to provide transaction services than to its ability to channel funds from savers to borrowers. The liquid liabilities, on the other hand, do not accurately reflect the provision of financial services in an economy (Levine et al., 2000). Beck et al. (2000) argued that the credit to private sector is a better representation of financial development as it shows the real picture of the movement of funds from savers to borrowers. Private credit isolates credit issued to the private sector as opposed to credit issued to governments, government agencies, and public enterprises. Furthermore, it excludes credits issued by the central bank (Beck et al., 2000; Khan & Senhadji, 2000; Levine et al., 2000).

Therefore, for this study, choosing an appropriate measure of financial development is very crucial as it provides a complete picture of development in the financial sector in Nepal and the the capacity of Nepalese financial sector to channel funds from savers to borrowers. Currently, Nepalese financial market is comprised of the banking and non-banking financial institutions, the capital market, and the insurance sector. Because the Nepalese stock market is in its initial phase and started operating only from 1994, the indicators of financial development for the stock market are not included in this study due to the penalty of losing a significant number of observations. As far as the nature of the Nepalese economy is concerned, it is a bank-based economy because banks are the dominant financial institutions in the financial system of Nepal. For example, commercial banks group alone occupies 78.7 per cent of total assets/liabilities of Nepalese financial system (NRB, 2015). Therefore, the indicator of the financial development, in this study, is limited to the development of the banking sector. More specifically, private credit, defined as credit issued by the banks and banking institutions to the private sector, is used as an indicator of financial development.

The relationship between financial development and economic growth has further been controlled by gross domestic saving (GDS), trade openness, and inflation. There may, of course, be other variables that affect the finance–growth relationship in an economy; however, these are the major factors that have significant impact on the development of financial sector and economic growth as identified by a large volume of literature (inflation [Beck et al., 2000; Christopoulos & Tsionas, 2004; et al., 2000], trade openness [Menyah et al., 2014; Salahuddin & Gow, 2016; Samargandi et al., 2014] and GDS [Beck et al., 2000; Levine et al., 2000]). Levine (1997) argued that financial development affects growth by changing the saving rate. Likewise, trade grants a country access to advancements in technological knowledge of its trade partners. Most importantly, trade grants developing countries access to investment and intermediate goods that are vital to their development processes (Yanikkaya, 2003). However, Nepalese economy is facing a prolonged trade deficit. Thus, there is a need to probe the effects of Nepalese international trade on growth during the study period. Inflation, on the other hand, affects not only growth but also the financial activities of the country by affecting the interest rate which has a direct impact on the deposit collection and credit flow of banking and financial institutions.

In a similar way, based on the literature (Andersen & Tarp, 2003; Beck et al., 2000; Christopoulos & Tsionas, 2004; Jung, 1986; King & Levine, 1993b; Khan & Senhadji, 2000; Levine et al., 2000; Wood, 1993), this study used two indicators of economic growth; the real GDP growth to measure the total productivity of the country and the real GDP per capita growth to control the population of the country. The real GDP is measured at constant US$ year 2005 prices.

DATA AND THE MODEL SPECIFICATION

This study has used time series data for Nepal covering the period from 1984 to 2014. The data were collected from World Development Indicators of the World Bank. Based on the empirical studies on finance and growth nexus (Beck et al., 2000; Christopoulos & Tsionas, 2004; Khan & Senhadji, 2000; Levine et al., 2000), the estimated equation 1 can be expressed as:

Because the direction of the causality is not clear between financial development and economic growth, this study followed the procedure used by Christopoulos and Tsionas (2004) to solve the causality nexus, and hence equation 2 has also been developed as:

Both the equations (1 and 2) are considered to be long-run or equilibrium relations. Where Y is economic growth (annual percentage change in real GDP and real GDP per capita [constant 2005 US$]), PRVT is the credit to the private sector as a percentage of nominal GDP, GDS is the gross domestic saving as a percentage of nominal GDP, OPE is the trade openness (import plus export) as a percentage of nominal GDP, and INF is the inflation defined as percentage change in consumer price index. The subscript t represents the year and u and v are the error terms.

THE METHOD AND EMPIRICAL RESULTS

Test of Stationarity

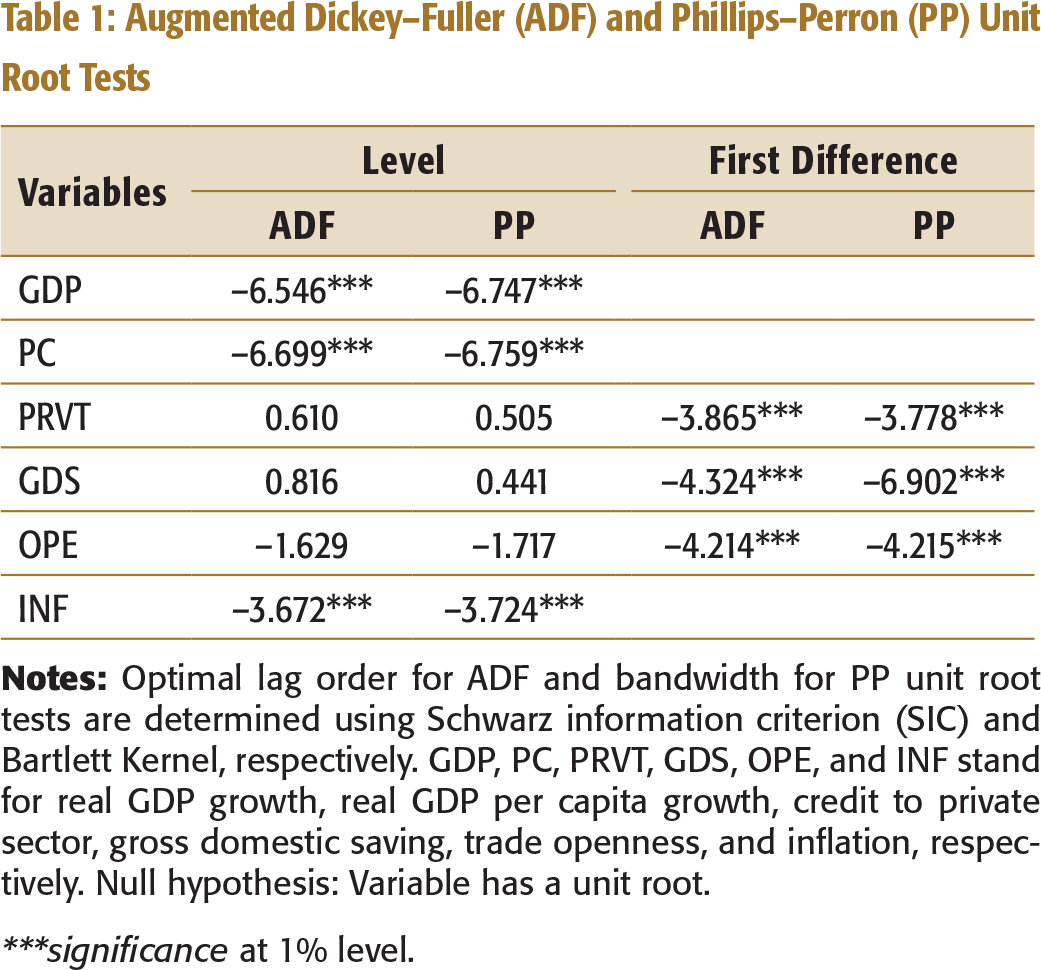

Although the ARDL framework does not require the pretesting of variables as it can be applied irrespective of whether the underlying variables are I(0), I(1) or a combination of both, this approach will not be applicable if an I(2) series exists in the model (Pesaran et al., 2001). Thus, Augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) unit root tests are applied to ensure that none of the variables is integrated of order 2 or above. Table 1 presents the results of Augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) unit root tests.

Augmented Dickey–Fuller (ADF) and Phillips–Perron (PP) Unit Root Tests

***significance at 1% level.

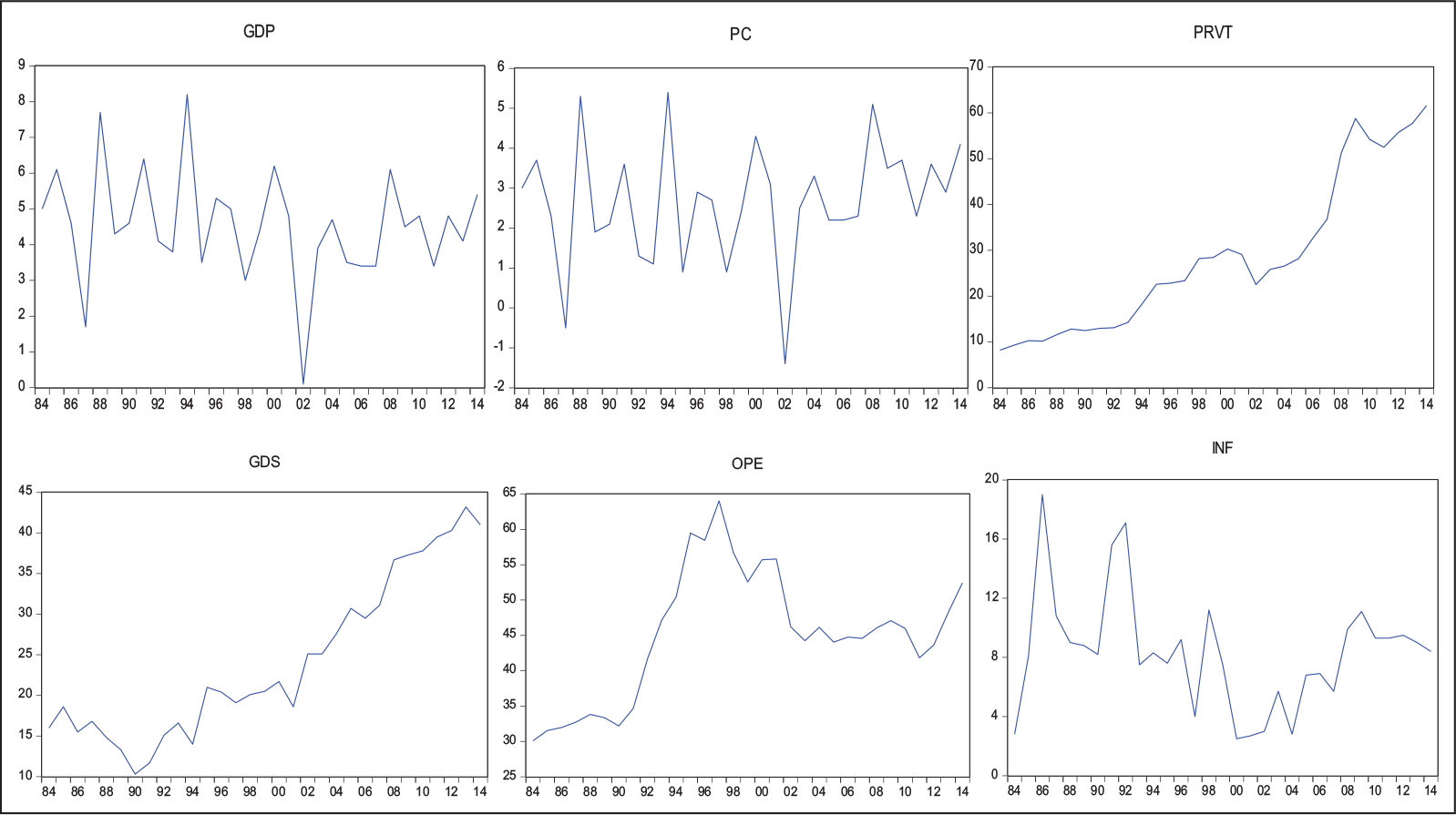

Yet Lee and Chang (2005) argued that the standard ADF and PP tests which lead to the non-rejection of a unit root may be suspected when the sample under consideration incorporates economic events capable of causing shifts in the regime. The plot of the series also suggests that the data might have a structural break in trend (Figure 1).

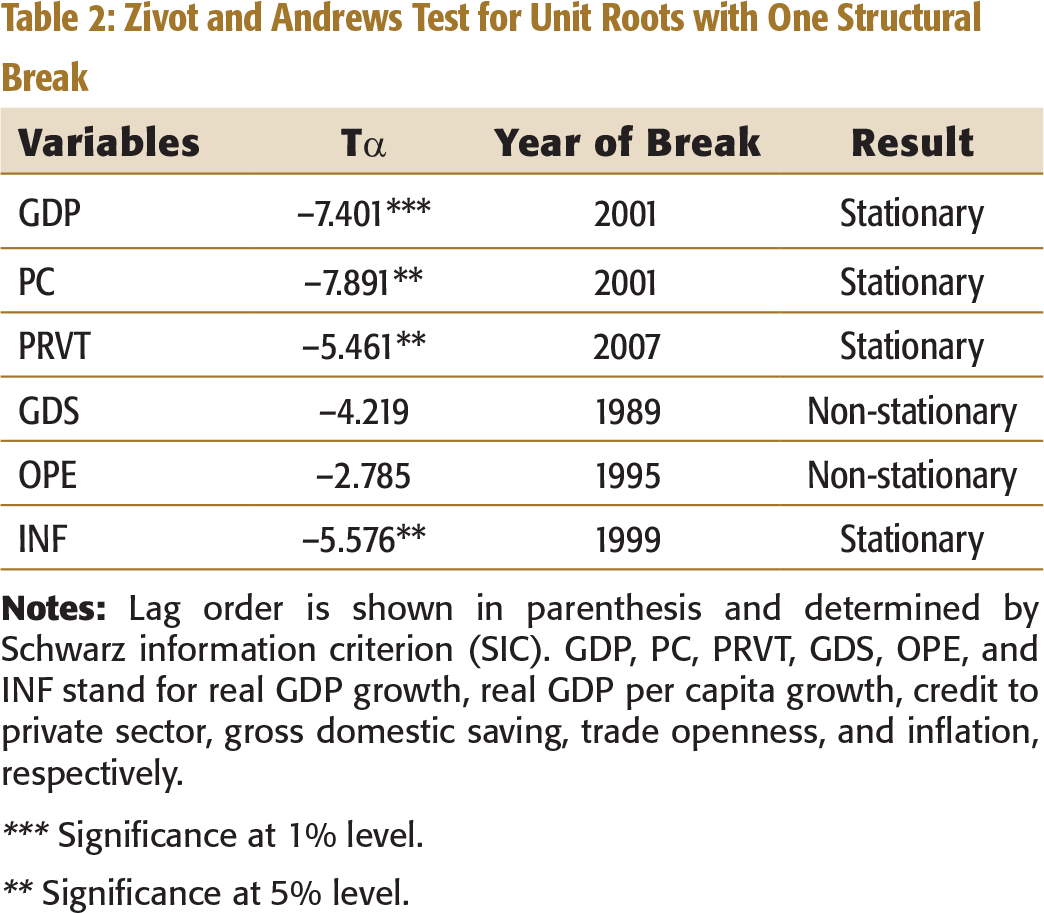

Zivot and Andrews Test for Unit Roots with One Structural Break

*** Significance at 1% level.

** Significance at 5% level.

Table 2 shows that unlike the ADF and PP tests, the ZA test for unit roots suggests that private credit exhibits stationary properties at the level when a possible break in the data set is accounted. The result shows that the structural change in private credit took place in 2007 when the government of Nepal and Maoists (the then rebels) signed a Comprehensive Peace Agreement (November 2006) and the Maoist rebels joined the interim government, which formally ended the civil war in Nepal. The data reveal that private credit to GDP ratio jumped to 51.2 per cent in 2008 from 36.77 per cent in 2007. However, the null hypothesis of a unit root is not rejected for both GDS and trade openness at level. ZA test results find that there is a break point occurring in 1989 in GDS and in 1995 in trade openness. To match these break points, this study found some critical political and economic events during 1989–1995. The break point in GDS in 1989 can be attributed to the economic sanctions over Nepal by the Indian government. It is also important to note that various trade liberalization reform programmes took place during the 1990s in Nepal. In 1995, as a member of South Asian Association for Regional Cooperation (SAARC), Nepal signed South Asian Preferential Trading Agreement (SAPTA) which attempted to reduce tariffs and non-tariff barriers among the SAARC member countries (Pant, 2005). Therefore, it seems possible that the structural break in trade openness in Nepal took place in 1995. According to ZA unit test results, break points in real GDP growth and per capita growth are detected in 2001, possibly a result of the Royal Massacre and the declaration of a state of emergency in Nepal by the then King Gyanendra Shah.

Cointegration and Causality

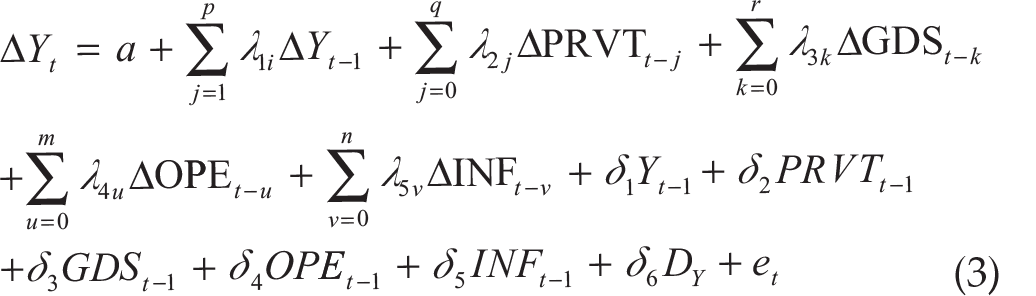

Once the presence of structural breaks is confirmed within the underlying variables, it cannot be ignored while estimating the cointegrating relationships. Therefore, taking into account the nature of the variables (that is a mix of I(1) and I(0)) and the presence of structural breaks, this study used the ARDL approach to cointegration to estimate the long-run relationship between financial development and economic growth. Because ARDL itself does not take the issue of potential structural breaks into the system, a dummy variable is introduced in the model to represent the break point in series. Thus, the estimated ARDL representations of equations 1 and 2 take the following forms:

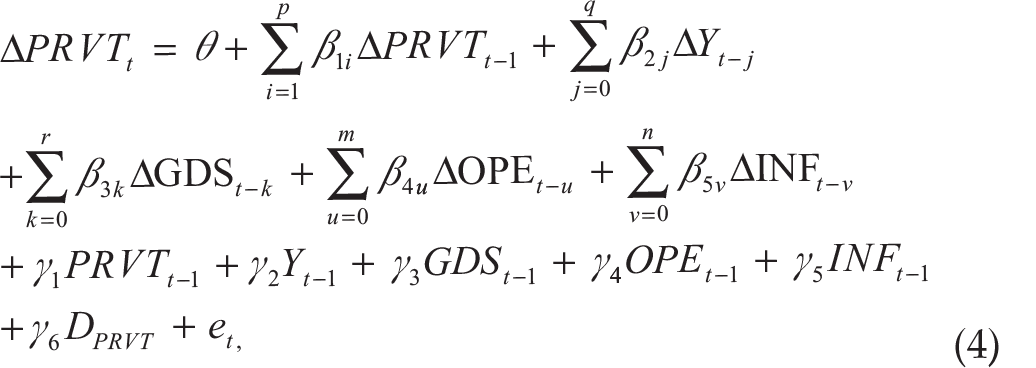

where Δ is the difference operator and Y represents the economic growth. Because the result of ZA test shows that the dependent variable (economic growth) undergoes a structural break in 2001 (real GDP growth and real GDP per capita growth), the dummy variable DY is introduced in equation 3 to represent the structural break. The dummy variable (DY) takes the value of 0 until 2001 and 1 thereafter for both the GDP growth and GDP per capita growth. Similarly, the dummy variable DPRVT is introduced in equation 4 to include the structural break in the regress and PRVT as follows:

where the dummy variable DPRVT takes a value of 0 until 2007 and a value of 1 from 2008 onwards. The coefficients (λ1 – λ5 and β1 – β5) represent the short-term dynamics of the model, whereas δ1 – δ5 and γ1 – γ5 are the long-run coefficients. The values (p, q, r, m, n) are the selected number of lags for the cointegrating equations based on SIC. The bound testing has been performed to test for the existence of a long-run relationship among the variables by conducting an F-test for the joint significance of the coefficients of the lagged levels of the variables. The wald coefficient restriction test has been performed to test the level effect with the null hypothesis of no level effect, that is:

Pesaran et al. (2001) provided critical values, upper bound and lower bound critical values, which have to be compared with the calculated F-statistics in order to reject or not to reject the null hypothesis. If the calculated F-statistics exceeds the upper critical bound, the null hypothesis of no cointegration is rejected. Similarly, if the calculated F-statistics is below the lower bound, the null hypothesis of no cointegration is not rejected. However, if the F-statistics falls within the upper and lower bound values, the result is inconclusive.

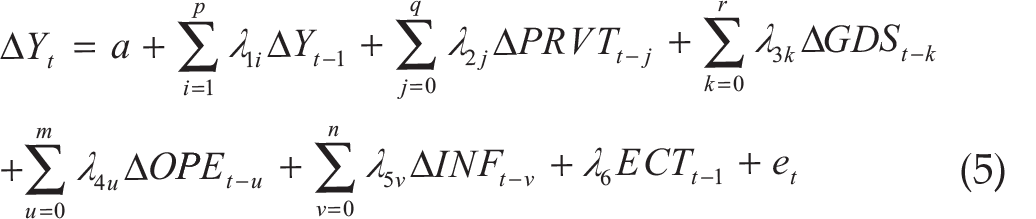

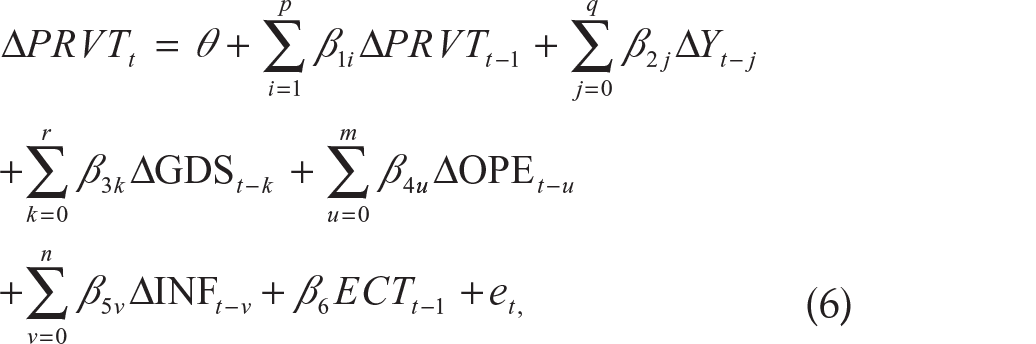

Engle and Granger (1987) argued that if two variables are cointegrated, then, the first variable may Granger-cause the second variable, the second variable may Granger-cause the first variable or each variable may cause another variable. This study, therefore, tests Granger-causality between financial development and economic growth using the Vector Error Correction Model (VECM) approach. This model has two advantages over simple Granger causality test. The VECM approach enables us to find both long-run and short-run causality. The VECM is represented as:

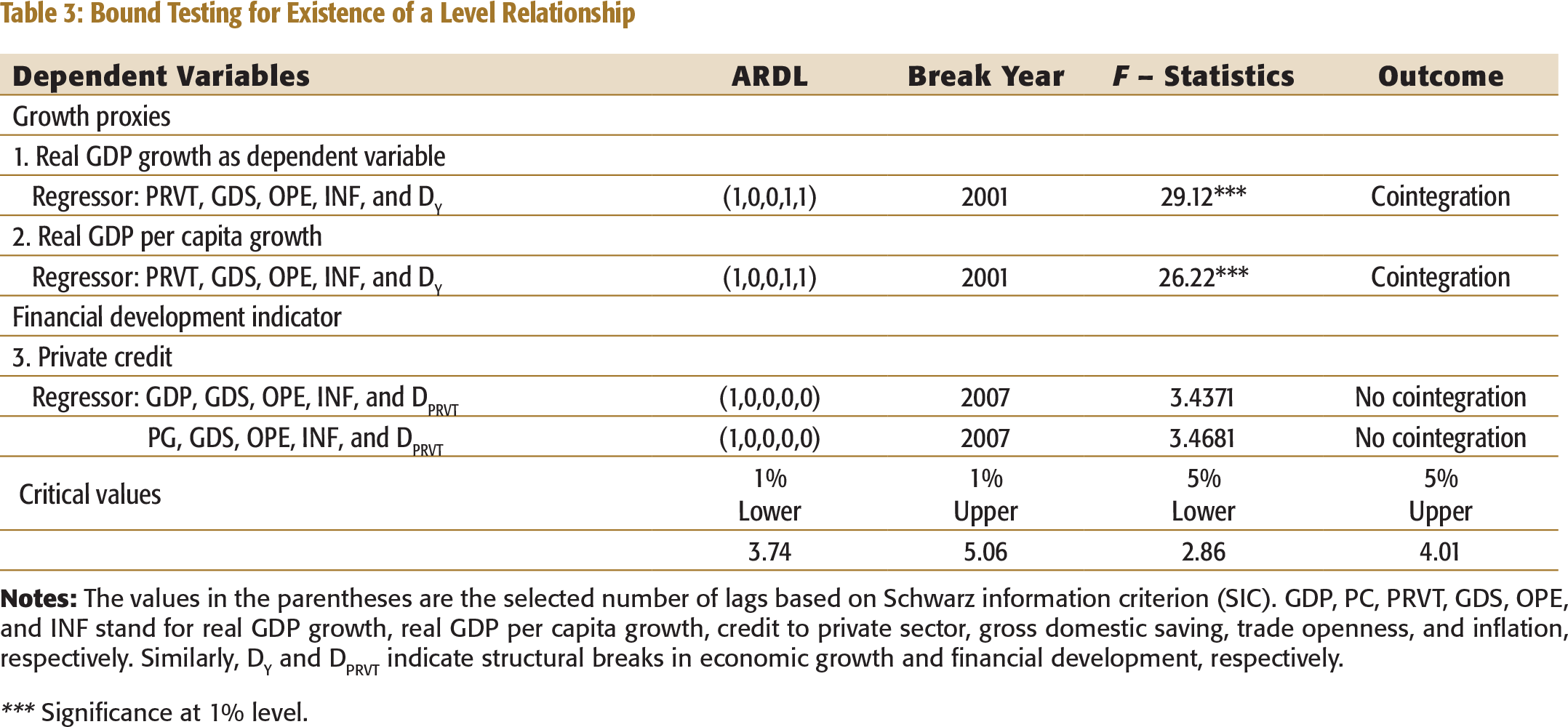

where Δ is the first difference operator and ECTt–1 is the lagged value of error correction term. There may, of course, be more VECMs making saving, trade openness, and inflation as dependent variables. However, the major objective of this study was to analyse the relationship between financial development and economic growth and other variables are used to control the relationship. Therefore, VECM is restricted to only financial development and growth. The short-run causality from financial development to economic growth is tested by H0: λ2 = 0 as shown in equation 5. Similarly, the short-run causality from economic growth to financial development is tested by H0: β2 = 0 as shown in equation 6. The error correction term (ECT) indicates both long-run causality and the speed of adjustment. The first important issue that is considered is whether λ6 ≠ 0 and β6 ≠ 0. If this is not the case, the cointegration findings would not be reliable. The results of the bound testing are reported in Table 3.

Bound Testing for Existence of a Level Relationship

*** Significance at 1% level.

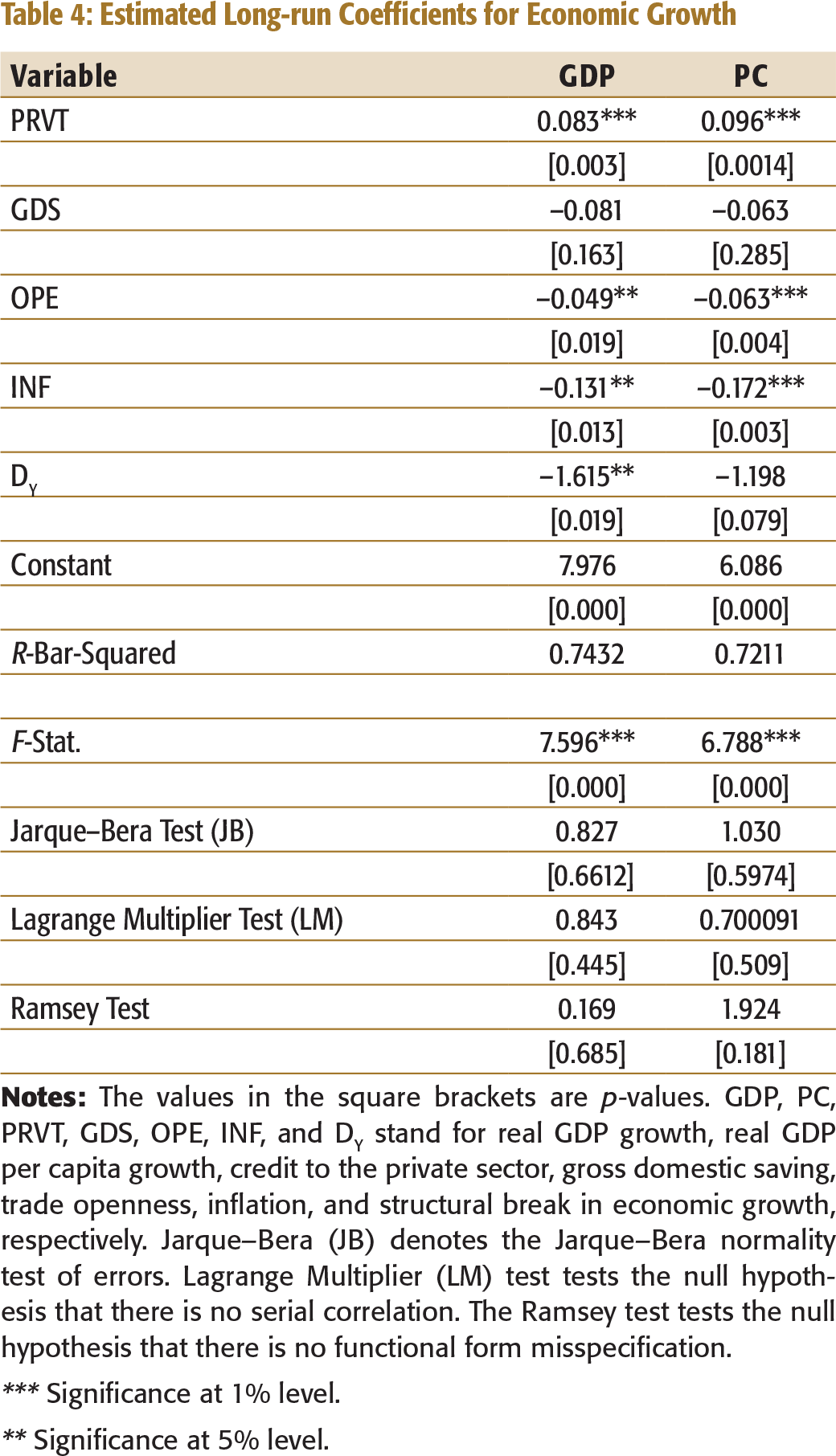

After the confirmation of a cointegration among the variables, the long-run estimates were estimated and the results are presented in Table 4.

Estimated Long-run Coefficients for Economic Growth

*** Significance at 1% level.

** Significance at 5% level.

Table 4 also shows that GDS has a negative impact on economic growth in the long run. However, the result is not significant. The negative long-run coefficients for GDS indicate that domestic saving does not matter for growth in Nepal. This finding is against the endogenous growth model which states that savings matter for growth. However, Aghion, Comin, Howitt, and Tecu (2016) argued that domestic saving does not always matter for growth.

According to Aghion et al. (2016, p. 1),

growth in relatively poor countries results mainly from innovations that allow local sectors to catch up with the current frontier technology. But catching up with the frontier in any sector requires the co-operation of a foreign investor who is familiar with the frontier technology and a domestic entrepreneur who is familiar with the local conditions to which the technology must be adapted. In such a country, domestic saving matters for technology adaptation, and therefore growth.

However, Nepal has not been able to build on the potential technological and other innovations that foreign investments can introduce to the process of development (Pant, 2010). Therefore, Nepal has failed to catch up with the current frontier technology, and hence domestic saving does not have a positive impact on economic growth.

Likewise, the result shows that trade openness too has a negative and significant impact on economic growth in Nepal for the period 1984 to 2014. The result shows that in the long run, keeping other things constant, a 1 pp increase in imports plus exports to GDP will lead to a corresponding decrease of 0.049 pp and 0.063 pp in real GDP growth and per capita growth, respectively. This finding is not consistent with the trade openness theory which states that trade grants developing countries access to investment and intermediate goods that are vital to their development processes (Yanikkaya, 2003). The negative trade openness and economic growth may be due to the fact that Nepal has been facing a persistent trade deficit after the trade liberalization policy reforms started in the 1990s (Chaudhary, 2011). For example, Nepalese trade with India, a major foreign trade partner of Nepal, has been characterized by a widening deficit. The ratio of Nepalese exports to India and Nepalese imports from India declined from 47.6 per cent in 1975–1976 to 13.8 per cent in 2012–2013 (Chaulagai, 2014). The long-run estimates also reveal that inflation has a negative impact on economic growth. If all other things remain the same, the result indicates that a 1 pp increase in inflation decreases real GDP growth and per capita growth by 0.13 pp and 0.17 pp, respectively.

The diagnostic statistics also reveal that the ARDL model used is data congruent and free from specification errors. The result shows that error terms are normally distributed (JB test), serially independent (LM test) and dynamically stable (Ramsey Test). Thus, the strong link between finance and growth does not appear spurious.

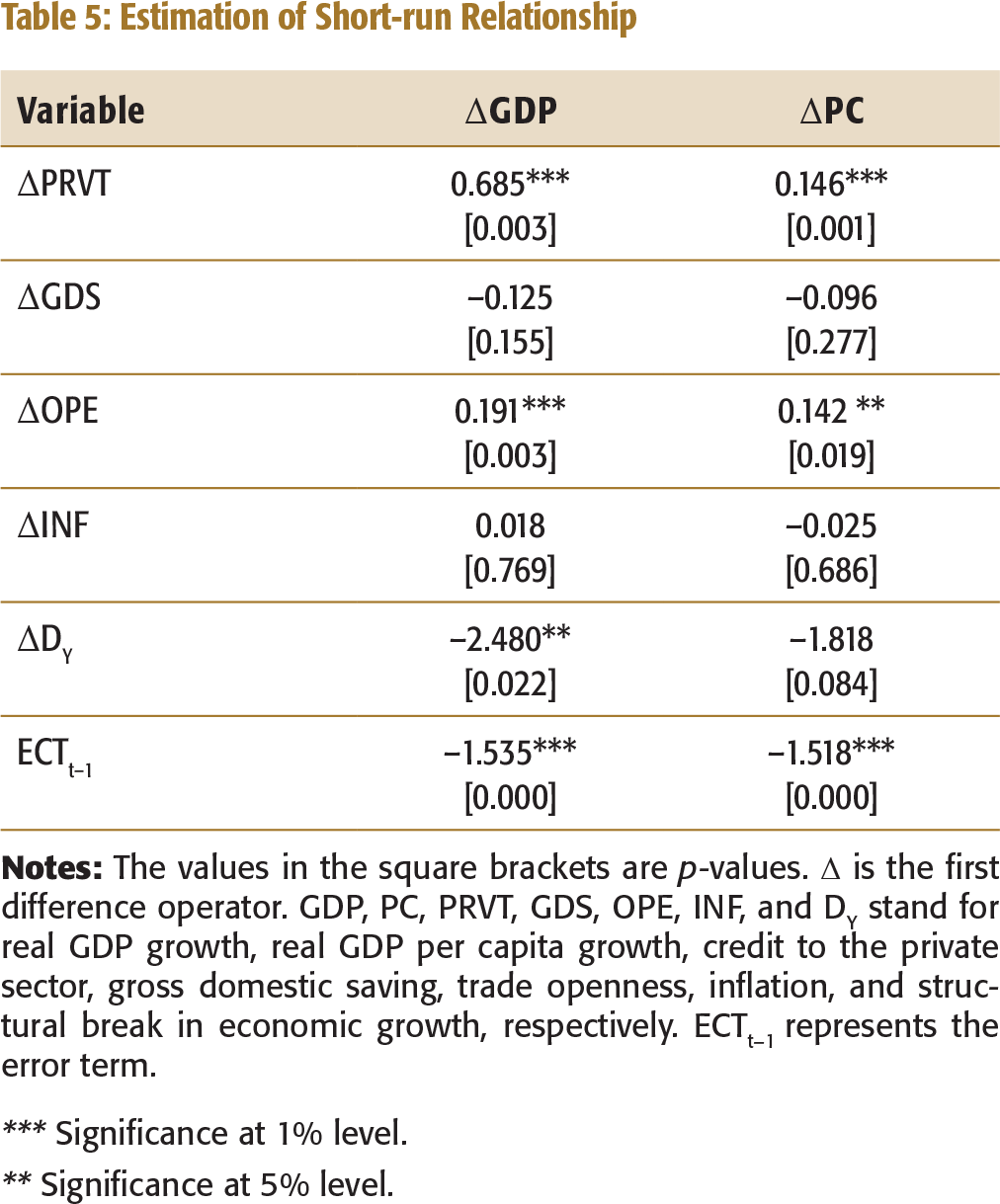

The results of the short-run analysis are reported in Table 5. The result indicates that financial development has a positive and significant impact on economic growth. As a result, a 1 pp increase in credit to private sector increases real GDP growth and per capita growth by 0.685 pp and 0.146 pp, respectively, in the short run. Similar to the long-run findings, the study further found that GDS has a negative impact on economic growth in the short run, but the impact is statistically insignificant. However, unlike in the long run, the impact of trade openness on economic growth is positive in the short run, and it is statistically significant. The estimates reveal that keeping all other things constant, a 1 pp increase in trade openness is equivalent to 0.191 pp and 0.142 pp increase in real GDP growth and per capita growth, respectively, in the short run. It is also important to note that the magnitude of the short-run positive effect is higher than the magnitude of the long-run negative effect of trade openness on economic growth (i.e., short-run coefficient (0.191) > the long-run coefficient (/0.049/) for real GDP growth). This indicates that although Nepalese economy is facing trade deficit for the years and, hence, the trade openness has a negative effect on growth in the long run, the economy is compensating this negative effect by a higher level of positive effect of trade in the short run. Now, the policy implication of this finding is that policymakers should formulate the trade and investment policies in such a way that they could attract the foreign technology and investment in Nepal and help to reduce the prolonged trade deficit. The inflation, on the other hand, shows mixed relationship with growth proxies in the short run. It is negatively related to the real GDP growth and positively related to the per capita growth. However, the relationship is statistically insignificant.

Likewise, the value of ECT is found to be negative and statistically significant. This indicates that economic growth, indeed, has a co-integrating relationship with financial development and other control variables. The coefficients of ECT lagged one period (–1.535 and –1.518) indicate that there is a high speed of adjustment to equilibrium after a shock.

Estimation of Short-run Relationship

*** Significance at 1% level.

** Significance at 5% level.

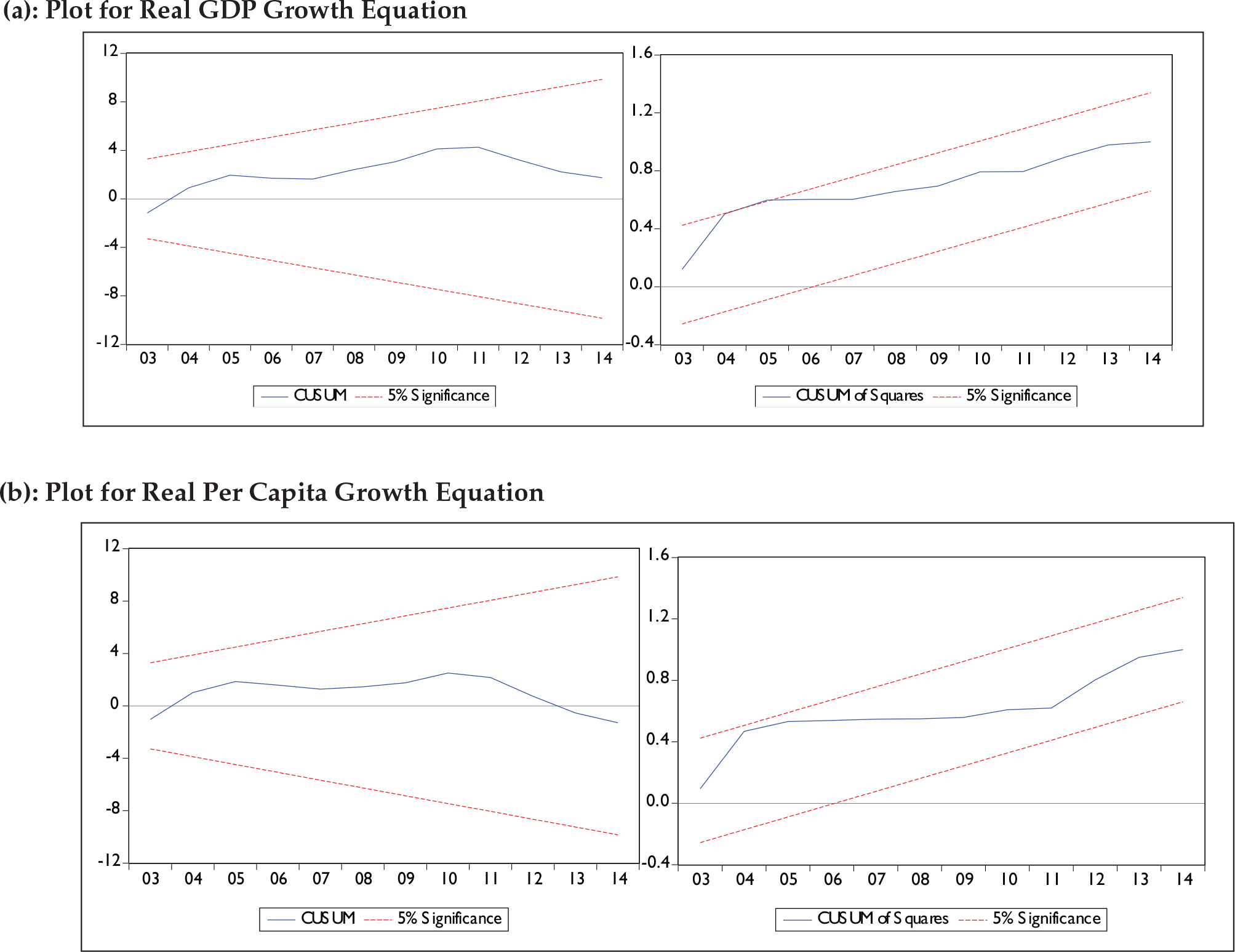

CUSUM and CUSUMSQ Plots for Stability Test

It can be seen from Figures 2(a) and 2(b) that the plots of CUSUM and CUSUMSQ statistics are well within the critical bounds, implying that both the models are stable over time.

SUMMARY AND CONCLUSIONS

The objective of this study was to examine the relationship between financial development and economic growth in Nepal. For this purpose, the empirical analysis was based on data for the period of 31 years beginning from 1984 to 2014. The time series properties of the data were, first, analysed for the possible structural breaks using the Zivot and Andrews (1992) model. The ARDL approach to cointegration in the presence of structural breaks was employed to analyse the long-run relationship.

The empirical evidence indicates that there is a stable long-run relationship among economic growth, financial development, GDS, trade openness and inflation in the presence of structural breaks. The long-run and short-run estimates of the ARDL model indicate that financial development has a significant positive effect on economic growth, indicating that the higher the flow of credit to the private sector, the higher the economic growth would be. Similar to the results obtained by Christopoulos and Tsionas (2004), this study found a long-run unidirectional causality running from financial development to economic growth. These findings imply that Nepalese policymakers should lay more emphasis on development of the financial sector in order to stimulate economic growth. However, the results revealed that both trade openness and GDS have a negative impact on economic growth in the long run. These findings indicate the weaknesses of Nepalese financial sector to mobilize the savings to productive sector and weaknesses of the country to benefit from international trade. Therefore, it creates urgency in the formulation of policies that enhance the effective mobilization of savings to the productive sector. Likewise, the negative relationship between trade openness and growth requires the attention of concerned bodies to formulate policies in such a way that they reduce the prolonged foreign trade deficit in Nepal.

We strongly suggest that generalizations from this research should be made with caution. The main limitation corresponds to the country considered in this study. The study is confined to the Nepalese context. Therefore, results may not depict the true picture in other countries. Similarly, this study is limited to the use of only banking sector development as the proxy for financial development. Hence, the findings might not be applicable to issues regarding other sectors of financial development.

DECLARATION OF CONFLICTING INTERESTS

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

FUNDING

The authors received no financial support for the research, authorship, and/or publication of this article.

NOTE

1. Pesaran et al. (2001) argued that this approach is superior and provides consistent results for small sample.