Abstract

Executive Summary

A business projects its financial performance through its financial statements. An audited financial statement is considered to be genuine and dependable by the stakeholders of the business. Therefore, statutory auditors should be self-regulating so that they can perform their professional role without being influenced by the management. The current regulatory framework for statutory auditors defines independence requirement for a statutory auditor in a professional engagement, points out circumstances that may create threats to independence and also proposes some measures to safeguard the same. However, in recent corporate accounting scandals, company’s failure led to devastating cost to the stakeholders, and audit failure was identified to be one of the causes behind them. Following investigations also sensed possible impairment of statutory auditors’ independence in those scams.

In this backdrop, based on the existing literature on this subject, this article identifies variables influencing positively or negatively statutory auditors’ independence in their professional engagement. Opinions of statutory auditors and select other groups of respondents were collected. Most of the respondent groups believe that statutory auditors fail to detect irregularities in financial books due to their lack of independence and professional scepticism as was observed in this study. Several legal case decisions also support this finding. A long association between a statutory auditor and a client is one of the major reasons behind statutory auditors’ lack of independence. Opinions of respondents supported by applicable legal case decisions also proved that lax disciplinary measures and inadequate inspection framework caused audit failures in many recent cases.

This study also analyses a significant difference of opinion among respondent groups and identifies the groups having a similar line of thought for each variable. One-way analysis of variance (ANOVA) and Tukey’s honestly significant difference (HSD) test were conducted, respectively, for these purposes. The result shows that significant differences exist among the respondent groups for most of the variables. Moreover, corporate executives have shown a significant difference of opinion from professional accountants, especially on the issue of statutory auditors’ negligence. While corporate executives believe statutory auditors are negligent in their duty, professional accountants oppose their views. Applicable legal case decisions also support such findings. Investors have shown similar views in line with academicians and students.

The financial result of a business enterprise is projected through its profit and loss account, balance sheet and other financial reports prepared according to the applicable generally accepted accounting principles (Banerjee, 2002). Stakeholders of the business make their financial judgement based on these statements. But sometimes immoral objectives of showing an inflated financial position lead the management of a company to manoeuvre its financial statement. It sometimes even calls for the company’s termination impacting most of its stakeholders. Therefore, the legitimacy and dependability of the financial statement should be certified by a proficient authority external to the business enterprise. Statutory financial auditors carry out this role. They are professional accountants appointed to check the financial statement of the company and express their opinion on the working affairs of the business (Gupta, 2005). Apart from being competent to do their job, they should be ethical towards their professional obligation. Therefore, independence of professional accountants serving as statutory auditors are of supreme importance to the stakeholders who take financial decisions based on their report. With a view to supporting statutory auditors to perform their responsibility with required integrity and objectivity, governing regulatory bodies in a country issue certain regulatory pronouncements (Bakshi, 2000). In India, chartered accountants execute the function of statutory financial auditors. With a view to ensuring their independent operation as statutory auditors and achieving quality audit from them, their governing regulatory bodies (e.g., Institute of Chartered Accountants of India, 2009, 2010; Ministry of Corporate Affairs, 2013; Securities Exchange Board of India, 2013) issue certain regulations (e.g., Code of Ethics for Professional Accountant, Standards on Auditing, Standard on Quality Control, Companies Act, 2013, and Listing Requirements) that clarify their independence requirement as a statutory auditor (Ghosh, 1999).

However, even with the existence of a strong regulatory structure, statutory audit failure has been witnessed in most of the accounting scandals in different countries (e.g., Enron Corporation Ltd. and Parmalat SpA). Statutory auditors in those companies failed to identify and report accounting wrongdoing in the company’s financial statement that resulted in the company’s failure affecting the country’s economy and a huge segment of society. Ensuing investigation also proved statutory auditors’ close nexus with management in some of those scandals (Copeland, 2005). Accounting scandal at Satyam was a classic example of statutory audit failure due to a lack of independence (Banerjee, 2011). In this company, statutory auditors certified inflated financial statement of the company as free from irregularities. They also failed to detect control deficiencies. After the revelation of the scandal, it was proved in the court of law that statutory auditors did not comply with the applicable independence requirement and aided management to commit the accounting fraud (Central Bureau of Investigation, Hyderabad vs Subramani Gopalakrishnan, 2011). This had put a big question mark on the integrity of the accounting and auditing profession. In this backdrop, this article seeks to analyse the perception of statutory financial auditors and respondents from other occupational groups having knowledge on this issue.

A Survey of Literature

Statutory auditors’ independence is a matter of huge significance in ensuring consistency and validity of financial statements prepared by a company’s management. However, recent corporate accounting scandals have reflected statutory auditors’ lack of judgement and scepticism in the audit of those companies. Following investigation also proved that statutory auditors were not completely independent from the management in those audit engagements. This situation brings about a great deal of concern among notable researchers all over the world. Extensive research has been conducted on this issue, causes behind the lack of independence of statutory auditors have been identified, and solutions have been proposed so that statutory auditors’ independence could be safeguarded for the protection of stakeholders’ interest.

An auditor plays an important role in the validation of a financial statement. Integrity, objectivity, and independence of a statutory auditor influence the utility of the financial statement (Saxena, 1993). As stakeholders take their financial decision based on the judgement of the auditors (Chakraborty, 2004), the latter should consider their interest with top precedence (Mehta, 1998; Pyne, 1995). Therefore, statutory auditors are an important segment of the entire corporate governance mechanism of the company (Garg, 2001). In some studies, scholars provided a historical count of the evolution of professionalism and independence of statutory auditors (Freier, 2004). Several studies have covered the stories of recent corporate accounting frauds (Enron, Satyam, etc.) and proved statutory auditors’ lack of independence in those scandals (Arens & Elder, 2006; Copeland, 2005; Pinto & Pinto, 2006; Thibodeau & Freier, 2010). Whenever a corporate accounting scandal occurs because of a false financial statement, auditors are considered to be one of the main parties behind the fraud (Crutchley, Jensen, & Marshall, 2007; Jennings, 2003). Several authors have analysed different corporate accounting scam cases and identified several intimidation to statutory auditors’ independence. The appointment procedure (Ghosh, 1999) and the provision of non-audit services (Beaulieu & Reinstein, 2006; Freier, 2004) are two such examples. We have reviewed several perception-based studies that ratify the conceptual studies. Safeguards to these threats offered by an audit client, profession or audit firm are also analysed in these studies (Fearnley, Beattie, & Brandt, 2005).

Some researchers have critically analysed the usefulness of the present regulation in protecting statutory auditors’ independence (Chakrabarti, 1996; Narielvala, 1998; Rossouw et al., 2010; Shah, 2000; Singh, 2009). Compliance with applicable regulatory framework helps a statutory auditor to gain public trust (Bakshi, 2000). However, in some studies, it has been proved that the present legal structure is insufficient to address the issue of statutory auditors’ independence (Dastur, 1998; Gowthrope & Blake, 1998; Maurice, 1996). Regular alteration in the current regulations and their appropriate execution could protect statutory auditors’ independence (Rao, 2009). Non-compliance with applicable regulations brings punitive measures against statutory auditors. Penal sanction against statutory auditors is diverse in different countries. However, the presence of a strong disciplinary framework deters an auditor from compromising his/her independence (Bakshi, 2000). The enactment of Sarbanes Oxley Act, 2002, following the Enron scandal is considered to be a significant regulatory milestone in the history of statutory auditors’ independence (Arens & Elder, 2006). Several perception-based studies have been carried out on the effectiveness of SOX Act, 2002. Subject to certain reservations, most of the authors have concluded that this new Act is very effective in improving statutory auditors’ independence and corporate governance structure of a company (Carillo, 2008; Hill, McEnroe, & Stevens, 2005; Rezaee & Riley, 2002). After the enactment of SOX Act, 2002, the importance of an oversight authority is deeply realized. Oversight bodies like Public Company Accounting Oversight Board (PCAOB) supervise audit operations in a country and decrease the scope of any possible nexus between statutory auditors and management (Godbole, 2004). In the present-day environment, when statutory auditors are extending their operations in global frontiers, several authors have proposed the convergence of individual code of ethics of the individual countries and the enactment of a uniform code of conduct all over the world to help statutory auditors avoid any ethical dilemmas in cross-country audit engagements (Pendergast, 2002; Vittal, 2000).

Apart from regulatory measures, another important safeguard to statutory auditors’ independence is the audit committee. It is an important board committee with majority of members as independent directors and is responsible for controlling issues that have significant influence on statutory auditors’ independent operations (Godbole, 2004). Therefore, independence of the audit committee from the management can go a long way towards the effective implementation of independence requirement for statutory auditors (Tipgos & Keefe, 2004). External review of the audit work is another important safeguard to statutory auditors’ independence. An independent third party makes a statutory auditor more careful about his/her independence obligation. In India, it is known as the peer review process. Studies have also compared external review in India with that of other countries of the world (Gerotra & Baijal, 2002).

All these mechanisms discussed earlier in the article externally influence statutory auditors’ independence. But until the statutory auditors internally realize the need for these independence obligations, effective results cannot be obtained. Only ethics and values can internally guide a person to attain a cherished result. Therefore, ethics has always remained an important area of research under this theme. Some researchers focused on the concept of ethics, its evolution, and different ethical concepts proposed by ethical leaders of our society (Duska, Duska, & Ragatz, 2011; Maurice, 1996) while others conducted several perception-based studies with advanced statistical tools to analyse ethical dilemmas faced by statutory auditors and the means to resolve them (Jeffrey, 2004; Roy, 1997; Zadek, Pruzan, & Evans, 1997). An ethical audit gives a statutory auditor enormous contentment which cannot be measured in monetary terms (Chauhan & Gupta, 2007). However, in the present sociopolitical environment, ethics and values are incessantly decreasing not only in auditing profession but in every sphere of our life (Ghosh, 1999; Ray, 1995). Tainted family values, ethical sense and cultural framework are the main reasons behind recent ethical failures. Accounting regulators, business, audit firms, and academic institutes should work hand in hand to provide a moral framework for statutory auditors (Copeland, 2005; Mayper et al., 2005). Ethical orientation of a person in this profession can get better only through education, practical training, and orientation programmes.

Some authors affirmed that the present curriculum for professional accountants was not sufficient to improve their ethical orientation (Ravenscroft & Williams, 2004). Therefore, a complete modification of the accounting course was proposed with an emphasis on ethics (Arens & Elder, 2006; Banerjee, 1993; Chakraborty, 2008; Earley & Kelly, 2004; Ghaffari, Kyriacou, & Brennan, 2008; Gowthrope & Blake, 1998). Criminology, psychology, and other behavioural sciences should also come under the purview of the current curriculum of professional courses (Curtis, 2008). Based on different statistical methods, the impact of an accounting scandal on the moral thinking of prospective statutory auditors was also analysed. It was thus found that practical training on ethical needs would help statutory auditors to understand the regulations with a practical approach and to resolve their ethical dilemmas in professional engagements (Bakshi, 2000; Lomax, 2003).

In recent times, researchers have identified some emerging areas in auditing that could play an important role in reducing accounting scandals. One such area is forensic audit where statutory auditors along with experts from other professions investigate the financial misdeed by a company and propose solutions. Forensic audit is also gaining importance in the current accounting curriculum (Curtis, 2008).

Research Gap

From the above discussion, it is clear that researchers, who have contributed their considerate opinion on this issue, identified specific threats and safeguards to statutory auditors’ independence. Ethics and values are important considerations for independent operation of statutory auditors. Therefore, many studies have incorporated ethics as an important determinant of statutory auditors’ independence. Several perception-based studies on independence or ethics with complex statistical techniques have been reviewed as well. Studies reviewed so far have only dealt with specific issues that positively or negatively affect statutory auditors’ independence. There is, however, an absence of a comprehensive discussion taking into consideration all the issues together. Besides, the perception of only statutory auditors has been considered so far. But the opinion of other respondent groups that by virtue of their occupation are closely related with the statutory audit process or are in a position to give an opinion on this issue has not been considered in those studies. This gap in the existing literature prompts us to take up this current study and empirically analyse the opinion of statutory auditors and other groups of respondents on statutory auditors’ independence for protecting stakeholders’ interest.

Objectives of the Study

The major objectives of the study are as follows:

To analyse the overall opinion of sample respondents from each occupational category on select variables influencing statutory auditors’ independence. To empirically analyse the significant difference in the opinion of select occupational groups for those variables. To statistically group individual respondent categories for select variables based on a significant difference of opinion among them. To draw a suitable conclusion on statutory auditors’ independence for protecting stakeholders’ interest.

Research Methodology

Data

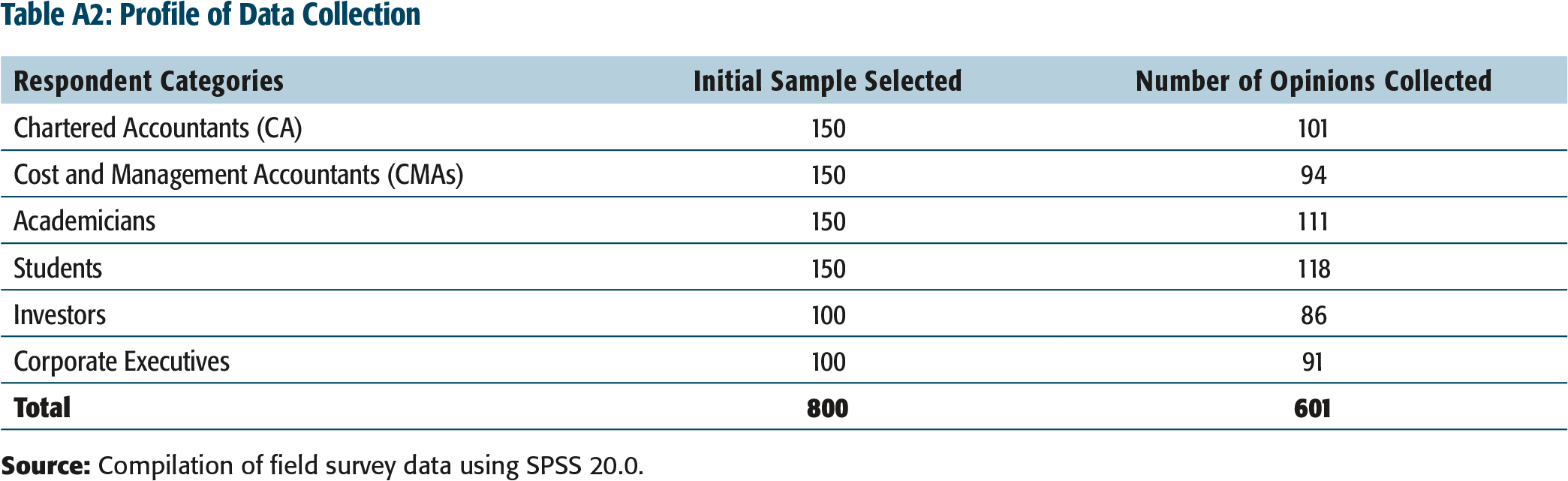

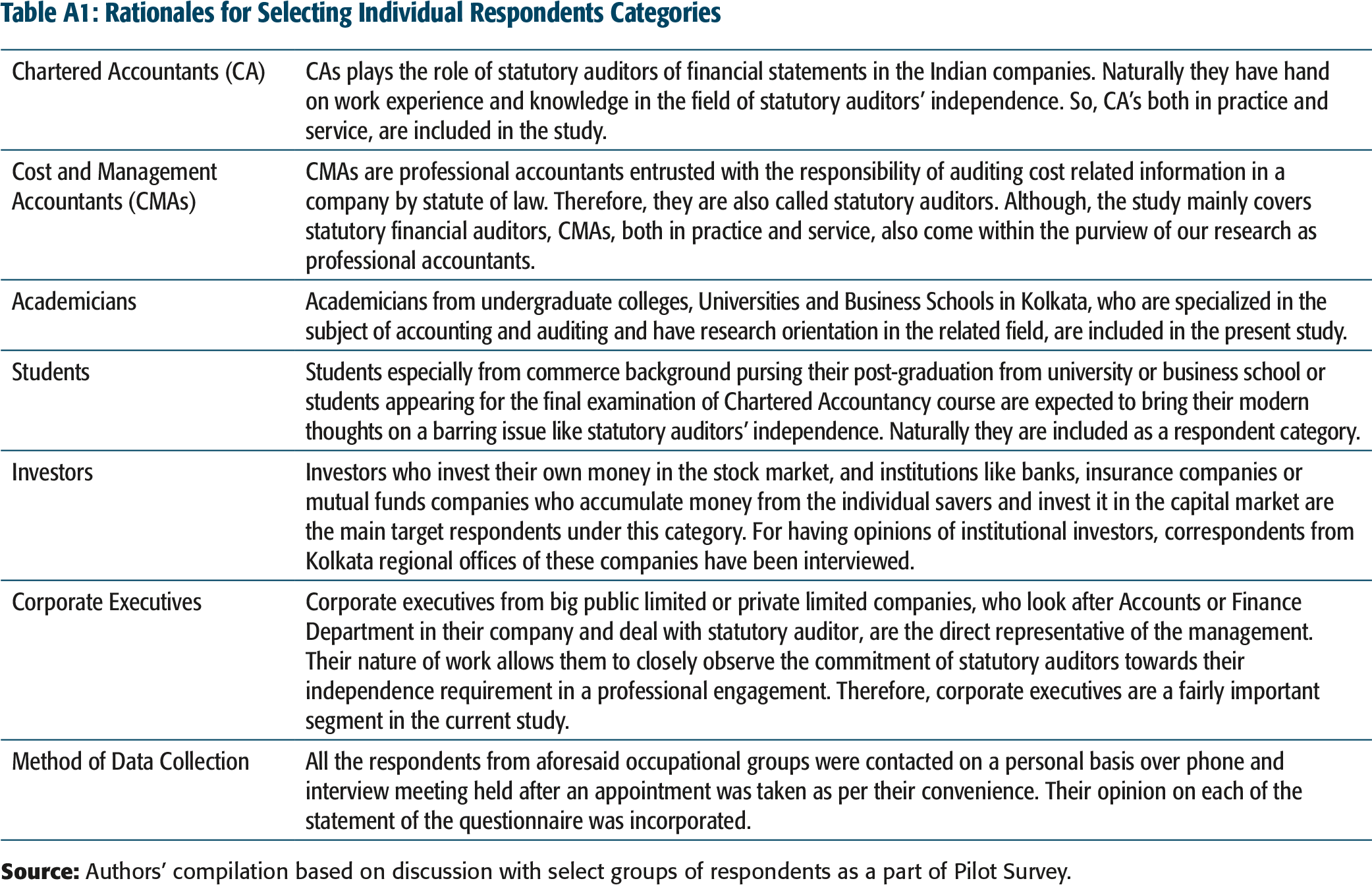

This study is exploratory in nature and is based on both primary and secondary data, the latter being collected from books, journal articles, newspaper articles, and legislations. Several legal case decisions in India especially of the Supreme Court of India involving statutory auditors’ duties and responsibilities in different companies were also considered, as they have direct bearing on the interpretation of various laws, rules, and regulations governing statutory auditors’ independence. Primary data were collected from Kolkata, West Bengal, during June 2011 to December 2013 through pretested, close-ended, and structured questionnaire. Through convenience sampling (Ho, Ong, & Seonsu, 1997), respondents were selected from different occupational groups, for example, chartered accountants, cost and management accountants, academicians, students, investors, and corporate executives. The rationales for selecting individual respondent categories and profile of respondents are given in Table A1 and Table A2.

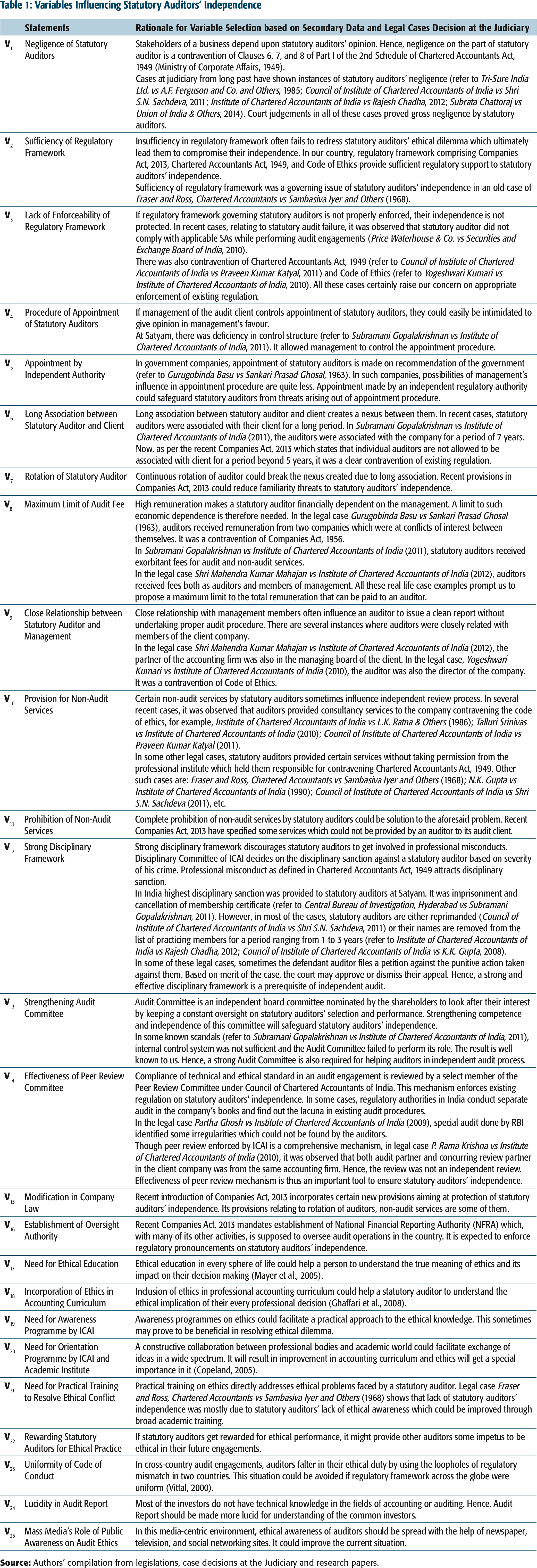

Based on books, research papers and judicial case decisions, 25 variables were selected. These variables were converted into statements and incorporated in the questionnaire with Likert 5-point scale (5 representing ‘strongly agree’ (SA), 4 representing ‘agree’ (A), 3 representing ‘neutral’ (N), 2 representing ‘disagree’ (D), 1 representing ‘strongly disagree’ (SD)) (Kothari, 2010).

Analysis of Collected Data

The mean sample score of each respondent category for each variable was calculated in addressing the first objective of the study. Mean scores represent the opinion of a particular respondent group. As far as the second objective is concerned, one-way analysis of variance (ANOVA) was conducted to analyse significant difference of opinion among respondent groups. Finally, Tukey’s honestly significant difference (HSD) test was conducted in order to group individual respondent categories into homogeneous subsets. SPSS 17.0 was exercised for the purpose of analysis.

Selection of Variables

Variables Influencing Statutory Auditors’ Independence

Perceptions of 601 respondents from different occupations on these variables were collected using a pretested, close-ended, and structured questionnaire based on the method specified in the research methodology.

Demographic Profile of Respondents

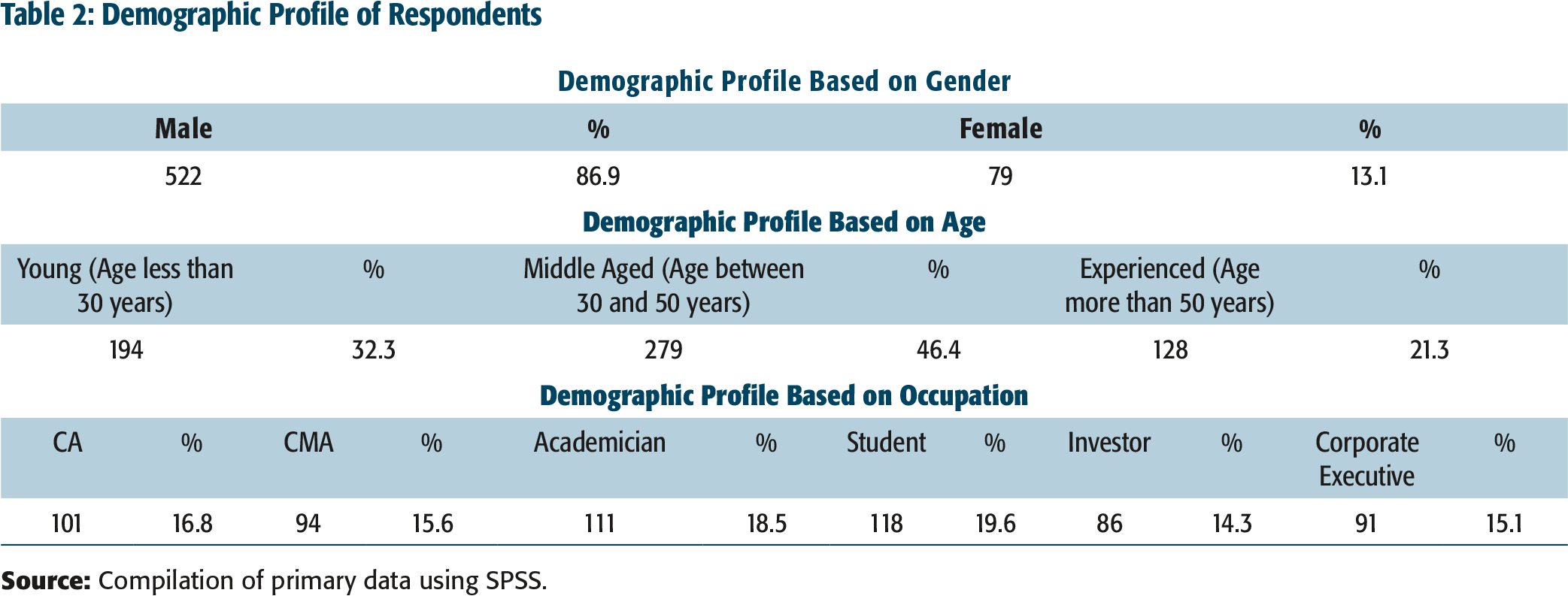

A brief demographic profile of the respondents is given in Table 2.

Table 2 reflects the general characteristics of the sample: Small proportion of female respondents indicates male domination in the sample. Demographic profile of respondents based on their age signifies that respondents with diverse level of experience have participated in the study.

Sample respondents were selected on the basis of their occupation. From the demographic profile, it is clear that there was maximum participation from academic communities (academicians and students), followed by statutory auditors – Chartered Accountants (CAs) and Cost & Management Accountants (CMAs). Other two groups are also important for the current research. Though the proportion of respondents from investors and corporate executives is less than the other four groups, their considerable participation makes the total sample a balanced one.

Results and Discussion

Analysis of Overall Opinion of Individual Respondent Categories for Each Variable

Demographic Profile of Respondents

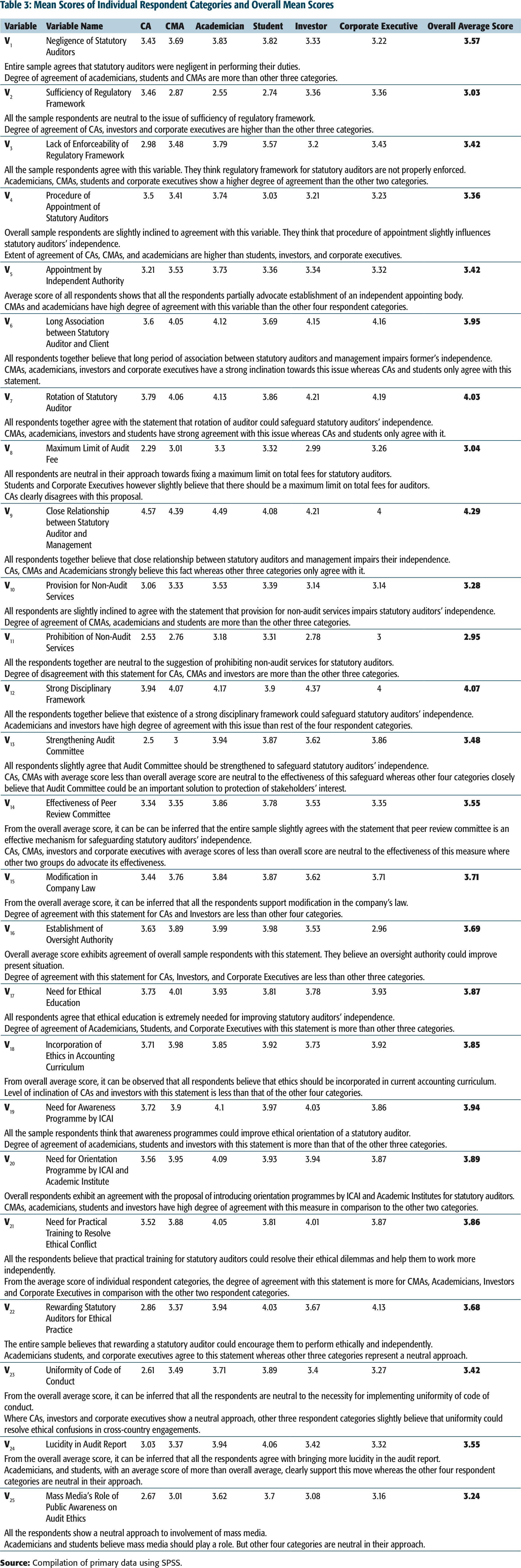

Mean Scores of Individual Respondent Categories and Overall Mean Scores

Following inferences can be drawn from Table 3:

All the respondents believed that statutory auditors were negligent in performing their duties in the case of recent corporate setbacks. Some of the legal cases, referred to in this study, also point to the same conclusion. In some of these cases, statutory auditors failed to verify assets of the company (refer to Council of Institute of Chartered Accountants of India vs V Rajaram of V Rajaram and Co., 1959), while in some other cases, they failed to perform with due diligence (refer to Council of Institute of Chartered Accountants of India vs R Ayyavoo, 2003). There were some cases where statutory auditors published their report without collecting sufficient and appropriate pieces of evidence on a particular issue (refer to Narayanan Nambudiri vs Institute of Chartered Accountants of India, 2005). In a nutshell, there are ample examples where statutory auditors failed to detect irregularities in the books of accounts of a corporate enterprise (refer to Council of Institute of Chartered Accountants of India vs R N Bahl, 2006). Some audit failures were due to absolute negligence on the part of the auditor, while others were due to their alleged lack of independence. All these legal case examples support the empirical finding of this study that statutory auditors are negligent in performing their duties.

Long association with audit client and close relationship with management impairs a statutory auditor’s independence in a professional engagement. In the legal case, Tri-Sure India Ltd. vs AF Ferguson and Co. and Others (1985), statutory auditors were associated with the client for a long period of time. However, at that time, rotation of the auditor was not a mandatory requirement. The result on close professional relationship is also supported by the legal case Subramani Gopalakrishnan vs Institute of Chartered Accountants of India (2011).

Rotation of the auditor, maximum limit of audit fee, strong disciplinary framework, external review of audit work, modification in company law, establishment of oversight authority, and all the activities that go on improving ethical orientation of statutory auditors have been proposed as a measure of solution by the entire sample. Cases like Satyam (refer to Talluri Srinivas vs Institute of Chartered Accountants of India, 2010) could be avoided if there was a limit on the total remuneration at the time of the Satyam scandal. A strong disciplinary structure could also escape many more fraud cases (refer to Council of Institute of Chartered Accountants of India vs Praveen Kumar Katyal, 2011) that took advantage of the lax disciplinary framework. Individual respondents are widely segmented among themselves for their opinion on each variable.

In most of the cases, the sample from academic community is found to behave uniformly. On the other hand, statutory auditors represented by CAs and CMAs have similar views on some issues. Corporate executives mostly go with the views of academic community. Investors are rather sceptical on the solutions provided to improve statutory auditors’ independence.

Analysis of Significant Difference in the Opinion of Select Occupational Groups

With a view to analyse the significant difference in the opinions of select respondent categories, the following steps were taken:

Hypothesis. The opinion of individual respondent categories is represented by their mean scores. Therefore, with a view to test whether a significant difference exists in the opinion of the population of individual respondent categories, the following null and alternate hypotheses were proposed: Null Hypothesis (H0): Population mean of individual respondent categories are equal. Alternate Hypothesis (H1): Population mean of any two respondent categories are not equal. Statistical Test. With a view to test the aforesaid hypotheses for each of the variables selected under this study, one-way ANOVA (Driscoll, 1996) was conducted. It is a parametric test conducted to determine whether an independent variable has an influence on the dependent observations. In this study, the occupation of respondents is the independent variable. If significant difference does not exist among individual respondent categories, it can be inferred that occupation does not have significant influence on individual observations of respondents. Test Statistics. Test statistics (F) in one-way ANOVA is calculated based on the following formula (Kothari, 2010):

where MS (Mean Square) between = SS (Sum of Square) between/(C–1); MS within = SS within/(N–C).

C = Number of categories N = Total sample size. Degree of Freedom (DF). Degree of freedom is the number of values in the final calculation of statistics that are allowed to vary. For one-way ANOVA, mean squares are calculated by dividing the sum of squares by their respective DF. Therefore, in one-way ANOVA, there are two DFs: C – 1 and N – C. In this study, the number of categories is 6 and the total sample size is 601. Therefore, DFs calculated for each variable under study is 6 – 1 and 601 – 6, that is, 5 and 595, respectively. Level of Significance. The level of significance refers to the probability of rejecting a true null hypothesis. If the level of significance for a particular research is 5 per cent, it may be inferred that the decision of acceptance or rejection of the null hypothesis is 95 per cent true. In social science research, this level of significance may vary from 1 per cent to 10 per cent. This study has considered 5 per cent level of significance. Decision Rule. With a view to taking decision on acceptance or rejection of the null hypothesis for a particular variable, this study used the F distribution table to find out a value very close to the test statistics at 5,595 DFs. For this value, the corresponding (P-value) was then identified. This is the probability of getting the test statistics at 5,595 DFs. If it is at more than 5 per cent significance level, the test statistics is considered to be in the acceptance region. So, H0 is accepted. But if this probability is less than 5 per cent, H0 is rejected, following the same rule. Accordingly, inferences are drawn on the significant difference of opinion between respondent categories for select variables and the impact of occupation on the opinion of respondents.

Based on the data collected from the sample respondents, the result of one-way ANOVA and the inferences for each categorical variable have been incorporated in Table 4.

Result of One-way ANOVA

The following inferences can be drawn from Table 3:

Respondent categories significantly differ among themselves regarding their opinion on the negligence of a statutory auditor. Though the result suggests that corporate executives do not consider statutory auditors to be negligent, there are instances where the corporate executive or client has been found to have lodged a complaint against the statutory auditors for their alleged lack of independence (refer to legal case: Tri-Sure India Ltd. vs A. F. Ferguson and Co. and Others, 1985).

Individuals, irrespective of their occupation, believe that ethical education is needed for ethical orientation of statutory auditors, thereby calling for its incorporation in the present accounting curriculum of professional courses.

Individual occupational groups are significantly different in their opinion for all other issues that positively or negatively influence statutory auditors’ independence. It shows occupation having an important influence on the opinion of respondents for these variables. In the legal case, Yogeshwari Kumari vs Institute of Chartered Accountants of India (2010), the client had lodged a complaint against the auditor for being the director of the client company. From this case, it can be inferred that the perception of the client and the auditor about the impact of a relationship with the management on independence is completely different. This case supports the empirical finding of this study on close relationship with management.

Homogeneous Groups of Occupational Categories

The null hypothesis of equality of population mean in one-way ANOVA is rejected if any one of the population means is significantly different from that of the others. Therefore, it is possible that while some population means are statistically different, some means are not. With a view to analyse exactly which population means are statistically different, sample mean differences of each individual pairs of categories were calculated. A null hypothesis was proposed that population mean differences are not statistically significant. To test it, Tukey’s HSD test, a post hoc test to one-way ANOVA (Malhotra, 2003) was applied, using the same degrees of freedom and significance level as that of ANOVA. If the P-value for each mean difference is less than the significant level, H0 is rejected and it is concluded that there is a significant mean difference between that pair.

Homogeneous Groups Formed Based on Significant Mean Differences in Individual Respondent Categories

Following inferences can be drawn from Table 5:

For most of the variables, professional accountants behave uniformly. Such unanimity of behaviour is also observed between the people from academic community. Corporate executives have significant difference of opinion from professional accountants.

Investors have close allegiance with people from academic community for the variables that propose measures for safeguarding statutory auditors’ independence.

For issues that improve ethical orientation of statutory auditors, all occupational categories exhibit a similar line of thought.

Summary of Findings

Considering the entire sample, procedure of appointment, tenure of service, and close relationship with management emerged as the major influencing factors of statutory auditors’ independence.

Rotation of auditors, strong disciplinary framework, external review of audit work, and all the activities that improve the ethical orientation of the statutory auditors are considered to be important safeguards to statutory auditors’ independence.

Individuals irrespective of their occupation believe that ethical education is needed for improving ethical orientation of the statutory auditors and it should be immediately incorporated in the accounting curriculum of professional courses.

Individual occupational categories are significantly different in their opinion for all other variables that positively or negatively influence statutory auditors’ independence.

Most occupation categories believe that the lack of enforceability of regulatory framework, procedure of appointment, tenure of service, and provision of non-audit service could impair statutory auditors’ independence.

Most of the occupation categories also believe that the rotation of auditors and strong disciplinary framework strengthen the audit committee, and that effective peer review committee, modification in company law, awareness, orientation and training programmes, and rewards for ethical service could restore statutory auditors’ independence.

Most of the occupational categories do not think that fixing a maximum limit on remuneration would in any way reduce cases of statutory audit failure.

Limitations of the Study

This study has the following limitations:

Multivariate statistical techniques, for example, factor analysis or cluster analysis are not applied for the current dataset.

Difference in the opinion of respondent categories could also be tested using the non-parametric Kruskal–Wallis Test.

Apart from statutory auditors’ independence, no other governance related issues that protect stakeholders’ interest are considered.

Conclusion

Statutory auditors validate ‘truth and fairness’ in financial statements. Financial statements authenticated by statutory auditors are considered trustworthy by the stakeholders of the business. They take their financial decision based on the financial statement with utmost good faith in statutory auditors. However, in an in-depth examination of the recent corporate accounting scandals, a few outrageous companies have been found to falsify their financial statement for quite a long period of time. Big and highly regarded accounting firms related with these companies as statutory auditors failed to recognize those frauds resulting in the publication of a false financial statement which ultimately led to a catastrophic consequence to the company impacting most of its stakeholders. In this backdrop, this study critically reviews relevant literature and identifies certain variables that positively or negatively influence statutory auditors’ independence. The opinion of respondents from different occupational categories is collected on these variables. The mean score of individual respondent categories represents their opinion for each select variable. The overall mean score shows the opinion of the entire sample. Different occupational categories are significantly different in their opinion for most of the variables except for ethical education to build ethical orientation of statutory auditors. Significant differences of opinion between all individual pairs of respondent categories are analysed and respondent categories are grouped into homogeneous subsets. It is observed that professional accountants and academic communities normally behave in a distinct fashion. Investors and corporate executives align with these two major groups based on the nature of a particular variable. If the study findings are given due importance in times to come, an all-round improvement in statutory auditors’ independence can be expected.

Acknowledgements

The first author is highly obliged to his research supervisor, Dr Siddhartha Sankar Saha, for his valuable guidance in designing this research paper which is directly related to his PhD work. He is also grateful to the University Grants Commission for awarding him with Junior Research Fellowship and subsequently Senior Research Fellowship for conducting his PhD work under the Department of Commerce, University of Calcutta.

Appendix

Rationales for Selecting Individual Respondents Categories

Profile of Data Collection