Abstract

Executive Summary

This article examines the impact of open market share repurchase announcements on stock returns in the Bombay Stock Exchange (BSE). The main objective is to examine whether share repurchase announcements under the open market route have any significant impact on the returns of the stocks traded in the BSE. The article covers the period from 2009 to 2013. For sample selection, two criteria were used: first, the firm should have been listed in the BSE for at least 28 trading days before the repurchase announcement date, and second, the firm should have all relevant data required by this study. A total of 95 repurchase announcements fulfilled these criteria. The analysis period extended from –28 to +28 trading days relative to the repurchase announcement date (t = 0). The findings of the study will help us to understand how the market responds to share repurchase announcements in India and whether a firm actually benefits by repurchasing its own shares from the market.

This study uses a standard event methodology based on an ordinary least squares market model with the aim of finding out whether repurchase announcements generate any abnormal return around the repurchase announcement date. While applying the market model for estimating the abnormal returns, the regression is estimated based on the stock return of the firm and market return of the previous 120 trading days. So, here the estimation window takes into account 120 observations. Using this, the expected returns are generated and then the abnormal returns are derived for the event window, 28 days prior to the event date and 28 days after the event date.

The findings of the study indicate that share repurchase announcements do not necessarily generate abnormal stock returns in the Indian equity market unlike developed economies like the US, Canada, and Australia. The whole sample is further divided into various subsamples on the basis of firm size and size of repurchase. The subsample analyses reveal that smaller firms do not necessarily experience higher abnormal stock returns following repurchase announcements than that of the larger firms. The findings weakly support the view that larger repurchase size generates greater abnormal stock returns than the smaller ones.

Share repurchase (hereinafter referred to as repurchase) by companies first originated in the US in the late 1960s, and assumed wide popularity by mid-1980s. This corporate practice is very much popular in the US, Canada, and the UK. The explicit motives behind share repurchases by firms include returning surplus cash to shareholders, increasing promoters’ stake, improving earnings per share, reducing takeover threats, and most importantly, preventing undervaluation of shares in the stock market. India recognized this corporate practice in the financial year 1998–1999, when Indian companies were allowed to repurchase their own shares for the first time. In India, firms can repurchase their own shares from the market by following the Open Market Method or they can buy their shares back by using the Tender Offer Method. However, unlike developed countries like the US or Canada, the number of repurchase announcements has been very low in India since its inception. But in the recent past, an upward rising trend in the share repurchase programme has been evident in the Indian corporate sector.

Share repurchase is believed to inject some buoyancy into stock prices since the repurchase price is set at a level higher than the prevailing market price and, thus, it is considered as an essential measure to ‘rescue a plunging stock market’ (Liao, Ke, & Yu, 2005). Preventing undervaluation of stocks in the market is considered to be one of the most prominent objectives behind share repurchases. Most of the Indian firms report on their repurchase offer documents that the main objective behind share repurchase is to prevent undervaluation of their shares in the market. Through share repurchase, a firm conveys a signal to the market that presently its share is being undervalued in the market but the firm expects its share price to increase. Does this signalling really work? Some US and Canadian market based studies document that share repurchase announcements reflect positive information to the market. Dann (1981), Vermaelen (1981), Netter and Mitchell (1989), and Ikenberry, Lakonishok, and Vermaelen (1995, 2000) find a significant positive market reaction to the stock repurchases announcements.

In this backdrop, this study attempts to examine whether share repurchase announcements under the open market route have any significant impact on returns of the stocks traded in the Bombay Stock Exchange (BSE). The findings of the study will help us to understand how the market responds to share repurchase announcements in India and whether a firm actually benefits by repurchasing its own shares from the market. The findings show that share repurchase announcements by Indian firms in the BSE do not certainly increase their share prices in the market.

The entire sample is further divided into subsamples based on firm size and size of repurchase announcements. Empirical results show that the smaller firms do not always experience greater abnormal stock returns following share repurchase announcements compared to the larger firms. With regard to the size of repurchase and stock price reaction, our results find that firms with larger repurchase size experience greater abnormal stock returns than firms with smaller size of share repurchase.

LITERATURE REVIEW

Majority of the studies on share repurchases have been conducted in the developed economies like the US, Canada, and the UK. Several studies have examined the underlying motives behind share repurchase announcement, and the most common motives emerging out of those studies are returning surplus cash to shareholders, capital structure redesign, anti-takeover mechanism, and the application of preferential tax rates (Liao et al., 2005). Badrinath and Varaiya (2000), Western and Siu (2002), Financial Executive Internationals (1999), etc., also report similar motives behind share repurchase announcements.

However, in reality, the principal reason behind share repurchase is to prevent undervaluation of share prices in the market. Dann (1981), Vermaelen (1984), Netter and Mitchell (1989), and Comment and Jarrell (1991) find support of the undervaluation hypothesis and observe significant positive abnormal returns around repurchase announcement period in the US. Comment and Jarrell (1991) document that during the period of announcement, abnormal returns are highest under the tender offer method of share repurchase and lowest under the open market repurchase method, indicating that the tender offer method is more informative for the market. Ikenberry et al. (1995, 2000) and Balachandran and Troiano (2000) also support the undervaluation theory. Liao et al. (2005) observe significant negative abnormal returns in most of the days prior to the announcement day and significant positive abnormal returns on the announcement day and during the first few days of the post-announcement period in the Taiwan Stock Exchange (TWSE).

On the other hand, Eberhart and Siddique (2004) find lack of consistent evidence of positive stock returns following repurchase announcements, and opine that liquidity change is the dominating factor in explaining announcement period’s abnormal stock returns. Cook, Krigman, and Leach (2004) also find support to the liquidity hypothesis. Chatterjee and Rakshit (2008) observe that the positive influence of share repurchase on stock price is not prevalent in the Indian context in all the repurchase cases as hypothesized theoretically. An analysis of share repurchases during 1999–2003 in India shows that the actual repurchase price is less than one half of the maximum price in nearly 50 per cent of the cases analysed (Gupta, Jain, & Kumar, 2005). Hertzel (1991) reports that repurchase announcements had little or no effect on the share price of rival firms; the information contained in repurchase announcements is primarily company specific.

The regulatory framework around the share repurchase activity varies across countries and has significant impact on this activity from different angles. Repurchase announcement during changes in the regulatory framework governing share repurchase is linked to positive but statistically insignificant abnormal returns, which is contrary to the evidence of American firms and the researchers are of the view that this is possibly because of the overregulated share repurchase environment in Australia (Harris & Ramsay, 1995). Rau and Vermaelen (2002) observe that the form and intensity of the share repurchase activity in the UK is influenced by the tax consequences associated with pension funds. The UK firms earn smaller excess returns through repurchase announcements compared to the US firms primarily because of the regulatory provisions in the UK which make it less likely that the firms can disseminate superior information to repurchase shares under the situation of undervaluation of stock prices.

As pointed out earlier, while several studies have been conducted on share repurchase and its implications on the market as well as on the firms announcing repurchase, most of the studies have been conducted in developed nations like the US, the UK, Canada, and Australia. In India, this area has remained under-researched. There is lack of in-depth studies on this corporate activity and its implications for the Indian corporate and the market at large. This article is expected to fill up this gap by contributing to the existing literature with a primary focus on the impact of open market stock repurchase announcement on stock returns.

DATA AND METHODOLOGY

In India, firms can repurchase their shares either by the tender offer method or through the open market route. Under the tender offer method, a firm commits to repurchase a specific number of shares from the shareholders either at a fixed price or at a price that is arrived at through the book-building process. Under the open market route, firms repurchase their shares from the stock market. Here the repurchasing firm does not commit to buy a specific number of shares and also there is no commitment on the part of the company regarding the minimum repurchase price. Only the maximum price for repurchase is announced. The actual price may vary. The maximum size of repurchase is limited to 25 per cent of the total paid up capital and reserves of the firm. This study considers only open market repurchase programmes.

The study covered the period from 2009 to 2013. 1

The financial year in India is from 1 April to 31 March of the following year. Thus, the financial year 2009 covers the period from 1 April 2008 to 31 March 2009.

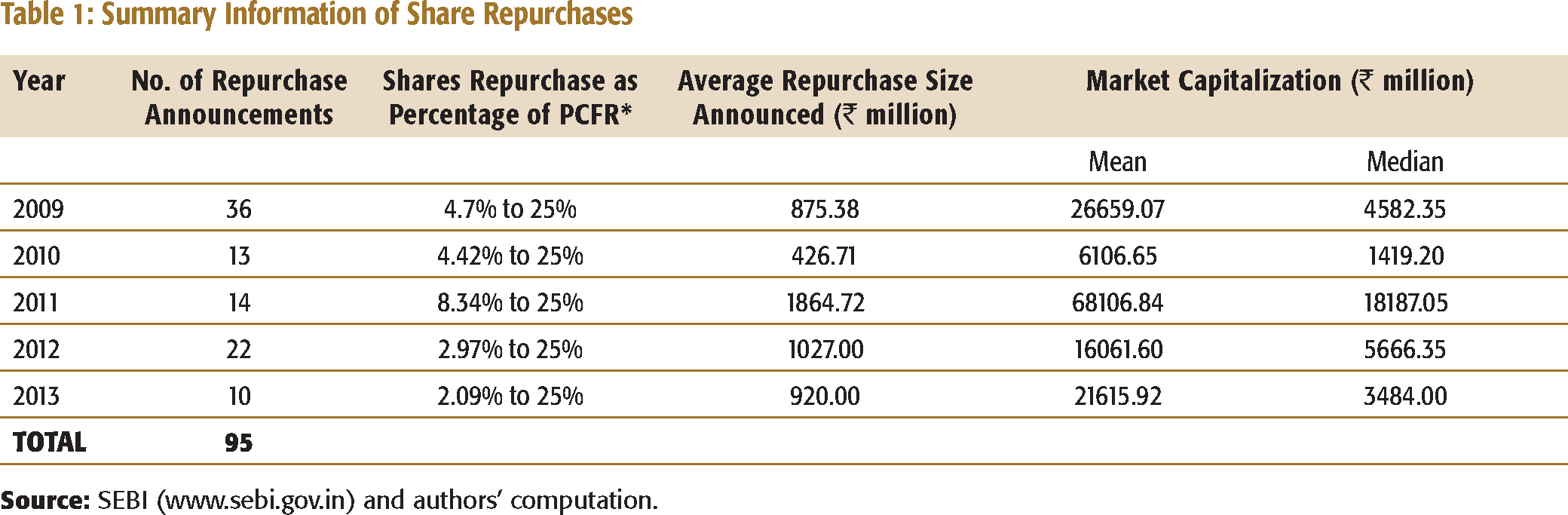

This study covered all the repurchase announcements made through the open market route. The data on market return was based on S&P BSE 500, which was sourced from the official website of the BSE. The reason for considering S&P BSE 500 instead of Sensex for computing market return was that most of the repurchasing firms were not part of the Sensex and they mostly belonged to the BSE small-cap and the BSE mid-cap category. The information on repurchase announcements were collected from the SEBI website. The share price data of the sample firms were collected from the BSE website. Table 1 presents the summary statistics related to the repurchases.

Table 1 shows that 2009 has the highest number (36) of repurchase announcements. The amount of share repurchase as a percentage of paid-up capital and free reserves ranges between 2.97 per cent and 25 per cent over the period of study. The average buyback size shows a reduction in 2010 (`426.71 million) from the year before (`875.38 million) and then again a substantial increase in the year 2011 (`1,864.72) million. Thereafter, a declining trend is evident. In this context, it is worth noting that almost all the repurchasing firms have disclosed ‘maximizing shareholders value’ as the primary objective behind their repurchase announcements.

Summary Information of Share Repurchases

This study used the standard event methodology based on the ordinary least squares (OLS) market model 2

For details on the market model, refer to Campbell, Lo, and MacKinlay (1997).

In a market model, under the assumption that asset returns are jointly multivariate normal and independently and identically distributed through time, the model is correctly specified. This model establishes a linear relationship between the market return and the individual stock return and that follows from joint normality.

where,

Rjt indicates return on stock j and Rmt implies market return.

The equation is estimated using the estimation window which is shown as follows:

Here, t = 0 implies the event date (here, the repurchase announcement date); A0 + 1 to A1 is the estimation window and A1 to A2 is the event window.

From Equation 1, aj and bj are estimated by running OLS on the data pertaining to the estimation window. Thereafter, using these estimates, abnormal returns for security ‘j’ at time ‘t’ in the event window is computed as:

Finally, average abnormal returns (AARs) and cumulative abnormal returns (CARs) were computed based on these abnormal returns.

In the market model, the expected return is estimated by regressing the firm’s stock return on market return. The abnormal return is then derived as the difference between this expected return and the actual return. While applying the market model for estimating the abnormal returns, the regression is estimated based on the data of the firm and market return of the previous 120 trading days. So, here, the estimation window took into account 120 observations. Using this, the expected returns were generated and then the abnormal returns were derived for the event window, 28 days prior to the event date and 28 days after the event date. Here the event date was the announcement date (t = 0). Before starting the analysis, all the series were tested for stationarity using the Phillips–Peron unit root test. As expected, both the returns were found to be stationary.

The analysis is presented in two ways. First, the effect of the repurchase announcement around the announcement date was measured. To achieve this objective, daily AARs for all stock repurchase announcements were computed over –28 and +28 trading days in response to the announcement date 0. For each of the days prior to and post announcement, the hypothesis that return is significantly different from zero was tested. In addition to that the CARs were also computed over different window ranges. Next, the entire sample was divided into subsamples based on the size of the firm and the size of repurchase in order to examine whether abnormal returns around repurchase announcement varied with the firm size and the size of the repurchase. Therefore, the hypothesis that there is difference in abnormal returns between the categories (firm size and size of repurchase) was also tested. For firm size, firms were categorized according to their market capitalization. If market capitalization of the firm at the time of repurchases announcement fell below `2,000 crore, it was categorized as small-cap. If it was between `2,000 and 10,000 crore, it was called mid-cap; and if the market capitalization exceeded `10,000 crore, the firm was classified as large-cap. For size of repurchase, firms were classified as top 25 percentile and bottom 25 percentile and also top 50 percentile and bottom 50 percentile firms based on the repurchase size, defined as the proposed amount to be used for the share repurchase programme as a percentage of paid up capital and free reserves. Firms could also be categorized into another group based on the announced motives behind share repurchase announcements. But in the study sample, almost all the firms announced ‘maximizing shareholders value’ as the primary motive behind their repurchase announcements. Hence, such categorization was not followed for this study.

EMPIRICAL RESULTS

Abnormal Returns around the Announcement Date

This section presents the analysis of how stock returns are influenced by repurchase announcements in three time periods—during repurchase announcement date, prior to the announcement date, and post announcement date.

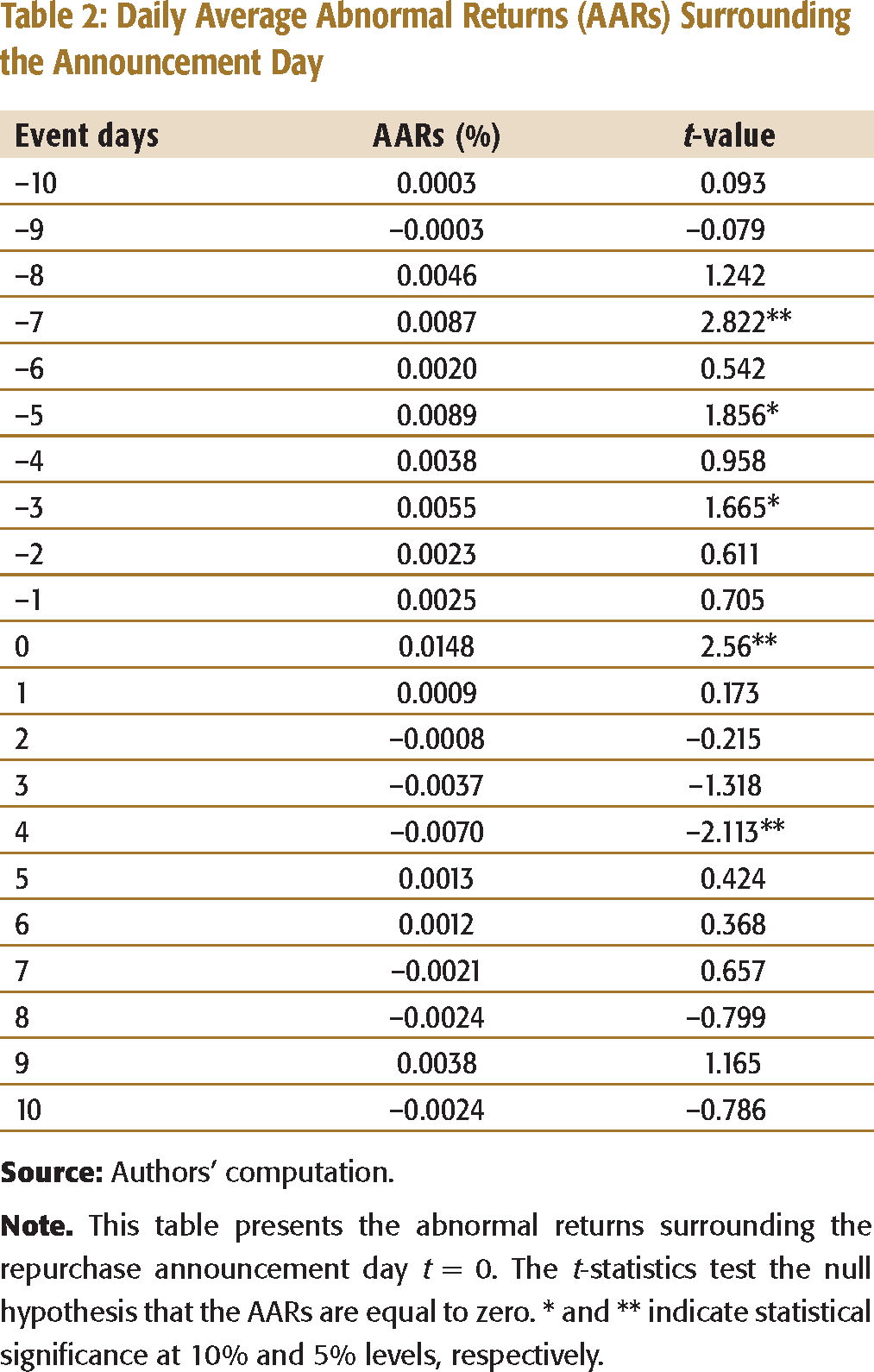

Daily Average Abnormal Returns (AARs) Surrounding the Announcement Day

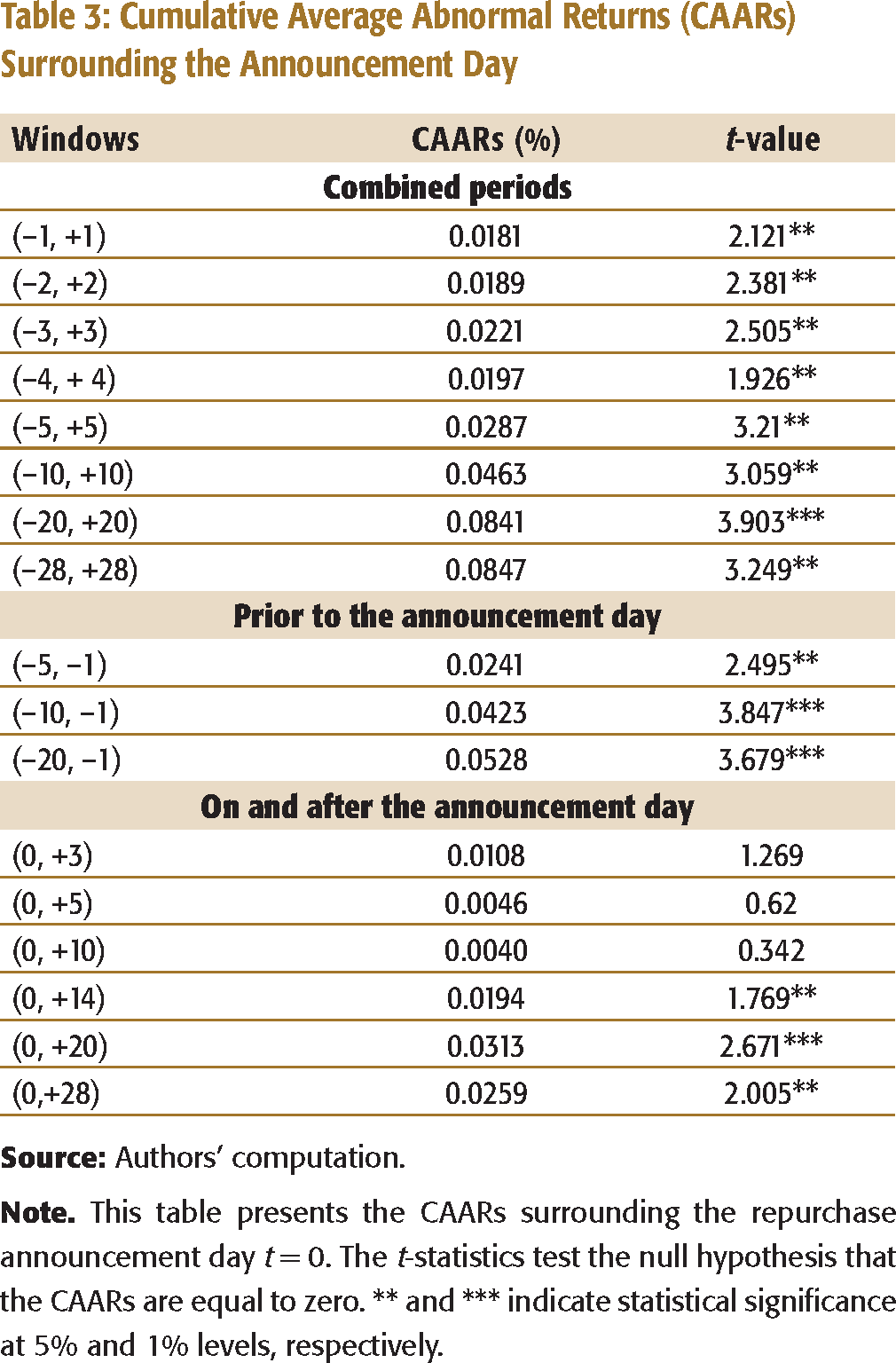

Cumulative Average Abnormal Returns (CAARs) Surrounding the Announcement Day

As reflected in the prior empirical studies, a share repurchase announcement is often described as a mechanism to signal the equity undervaluation. If corporate managers believe that the firm’s share price is being undervalued by the market, they use repurchase announcement to disclose this potentially value-increasing information. Findings in the US market experience poor pre-announcement performance and, subsequently, outperformance after the repurchase announcements, thereby supporting the undervaluation hypothesis. Our finding is contrary to that. This simply signifies that share repurchase announcements in the BSE do not necessarily support the ‘undervaluation hypothesis’ and it is also quite surprising that the objective of ‘maximizing shareholders’ wealth’ is not achieved through share repurchase announcements by Indian firms.

Difference Analysis

The results above have shown that share repurchase announcements do not necessarily generate abnormal stock returns in the Indian equity market. To test the effects of firm size and the size of repurchase, this study categorized the entire sample into various subsamples. The findings are presented in the following.

Firm Size and Price Response

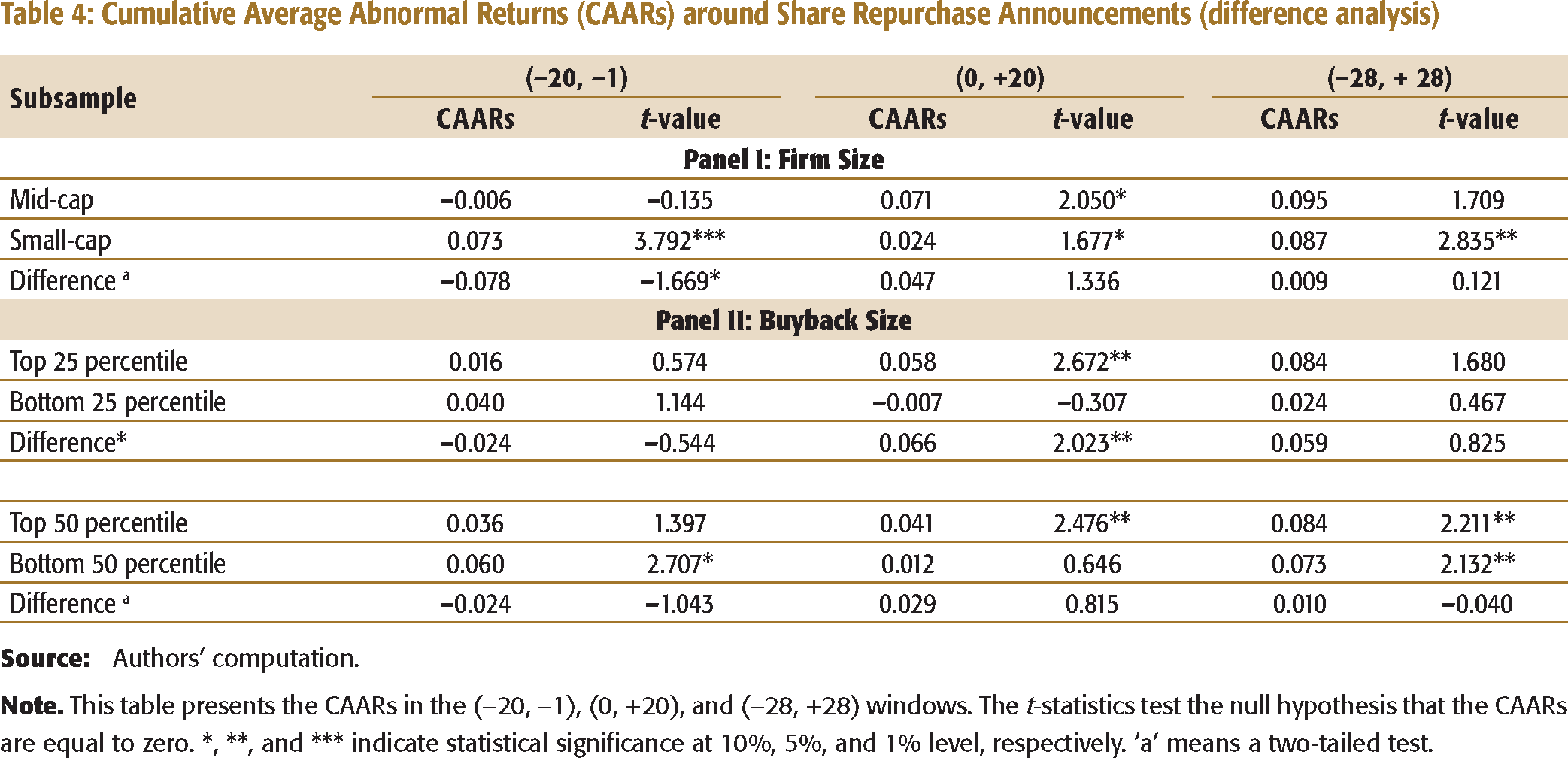

Vermaelen (1981), Ho and Michaely (1988), and Ratner, Szewczyk, and Tsetsekos (1996) document that the stock price reaction of large firms is less positive than that of small firms around share repurchase announcements. On the other side, Barry and Brown (1984) observe that the mass media tend to provide less news coverage of small firms than large ones, which ultimately leads the large firms’ prices to be more information-efficient. Here, sample firms were categorized on the basis of their market capitalization, defined as the firm’s share price in the market multiplied by the number of shares outstanding at the time of share repurchase announcement. As per the size of market capitalization described earlier, there were 75 firms under the small-cap category and 14 firms under the mid-cap category. Only six firms were classified as large-cap; hence, they were ignored.

Cumulative Average Abnormal Returns (CAARs) around Share Repurchase Announcements (difference analysis)

Size of Repurchase and Stock Price Response

The size of repurchase is often used as a proxy for information, in which large repurchasing conveys more information regarding the cash flow position of the firm (Liao et al., 2005). Davidson and Garrison (1989) and Ratner et al. (1996) observe a positive association between abnormal stock return and size of repurchase. In this subsample analysis, firms are partitioned by the size of repurchase. As noted earlier, in India, the maximum permissible size of repurchase is 25 per cent. Firms are ranked from the largest to the smallest on the basis of the size of repurchase. Then the sample is partitioned into the following two groups: the top and the bottom 25 percentile and the top and the bottom 50 percentile of the size of repurchase. The statistical significance and magnitude of the stock returns for the top groups are compared with the bottom groups. The subsample tests by repurchase size measure the impact of repurchase size on abnormal stock returns. Panel II of Table 4 presents the empirical results.

The results show an insignificant difference in the means between the top and bottom 25 percentiles (t =

CONCLUSION

The present study uses event methodology to empirically examine the impact of open market share repurchases on stock returns in the BSE. The findings of the study indicate that share repurchase announcements do not necessarily generate abnormal stock returns for the repurchasing firms in the Indian equity market unlike the developed economies like the US. The results derived from the analyses of AARs and CAARs show that the undervaluation hypothesis does not hold good in the Indian equity market implying that through share repurchases Indian firms are not able to enhance their share prices in the market. While analysing whether stock return following repurchase announcements varies across firm size, a mixed result is evident. The difference in the CAARs between the small-cap and mid-cap group is statistically significant only in the pre-announcement period (

The holistic result indicates that share repurchase announcements in India do not carry much information to the investors, and Indian firms are not able to ‘maximize shareholders’ wealth’ through this corporate activity. The possible reason behind this could be the nature of the ownership structure of the Indian firms, which is distinctively different from those in the US. Indian firms are mostly owned or otherwise controlled by the founding members (termed as promoters) unlike the widespread equity ownership model in the US. Indian firms may go for share repurchase announcements to counter the takeover threats or to enhance promoters’ stake in the business. The regulatory norms surrounding share repurchase have also material impact on this corporate practice and vary across nations. These areas need to be investigated further for better understanding of this corporate activity.