Abstract

Purpose of review:

Owing to the high cost of care and huge treatment gap associated with mental illnesses in India, this review investigated the implementation of mental health insurance coverage in India following the mandate of the Mental Health Care Act of 2017 (MHCA 2017).

Collection and analysis of data:

We systematically identified health insurance providers in India through the Insurance Regulatory and Development Authority of India (IRDAI) website. We meticulously searched and obtained policy documents from either the IRDAI website or the respective insurance company websites. Our classification process involved determining if a policy explicitly covered mental illness, which we discerned by examining definitions of mental illness, indemnification clauses or the presence of International Classification of Diseases-10 codes within the policy.

Conclusion:

We evaluated 235 policies provided by 30 insurance companies and found that 37.5% (88) of policies covered mental illnesses, 11.5% (28) covered persons with disabilities, whereas 51% (119) did not offer any coverage. The majority of the companies did not cover suicide and substance use disorders. There are disparities in the outpatient care offerings, including extended waiting periods for coverage of mental illness.

This review highlights the importance of aligning insurance practices with MHCA 2017s provisions to promote mental health equity in India. It also advocates for comprehensive mental health coverage that includes outpatient care, substance use disorders and suicide as well as a need for standardized definitions and transparent policy communication.

As per the Global Burden of Disease study conducted between 1990 and 2017, one in seven Indians was affected by mental disorders, and the proportional contribution of mental disorders to the total disease burden has almost doubled since 1990. 1 The National Mental Health Survey (NMHS) of India in 2015–2016 also highlighted a significant disparity in mental health services needs and treatment-seeking behaviour. It has been reported that the existing treatment gap for mental health is as high as 84% with nearly 150 million Indians need mental health services and active intervention; however, less than 30 million seek treatment. 2 The economic loss to India due to mental illness is estimated to be USD 1.03 trillion between 2012 and 2030 due to loss of productivity. According to a recent study based on 75th National Sample Survey data, only 23% of those hospitalized had some health insurance coverage and it was just 3.4% among the poorest economic group. 3 This urges strong advocacy for health policies that include physical and mental health illness coverage. 4

The Mental Health Care Act of 2017 (MHCA 2017), was introduced to provide a legal framework to improve mental healthcare services and to emphasize the rights of individuals with mental disorders on 7 April 2017, in the background of this high mental health morbidity and huge treatment gap. This Act aims to promote mental healthcare and access to mental health services nationwide. One of the pivotal aspects of this legislation is providing mental health insurance coverage aimed at reducing financial barriers to mental health care. MHCA 2017 section 21 clause 4 says, ‘Every insurer shall make provision for medical insurance for treatment of mental illness on the same basis as is available for the treatment of physical illness’. 5 In pursuance, IRDAI (Insurance Regulatory and Development Authority of India) issued a circular (IRDA/HLT/MISC/CIR/128/08/2018) to all insurers to comply with MHCA 2017 and provide insurance coverage for mental illness and all insurers were instructed to disclose on their respective websites the underwriting philosophy and approach with regard to offering insurance coverage to persons with mental illness (IRDAI/HLT/MISC/CIR/129/06/2020).6, 7 In response to the numerous complaints received by IRDAI regarding non-adherence to the above circular, a new circular (327/IRDAI/HLT/MHCA/CIR/220/10/2022) has been issued, mandating that all insurers must provide coverage for mental illness in accordance with the provisions of MHCA 2017 by 31 October 2022. 8 An expert committee (IRDAI/HLT/ORD/Gen/73/03/2023) was formed for effective implementation and guidance on mental health coverage. 9

Mental illnesses constitute one-sixth of all health-related disorders in India, and a study revealed that 18.1% of monthly consumption expenditure is spent on mental health, causing about 20% of households to be pushed into poverty. 10 The social drift hypothesis of mental illness explains how suffering from mental illness can downgrade the person’s socioeconomic status in the ladder due to high expenditure spent, loss of employment and reduced productivity. 11 This high cost of care and out-of-pocket expenditure on mental health indicates the need for financial risk protection for mental health care by including mental health in insurance policies, which was already brought into the limelight by the new MHCA 2017.

It is noteworthy that as of 2020, only HDFC Ergo was identified as an insurance provider offering mental health coverage, as reported in a Lancet study, 12 whereas, in a 2021 article, five companies were identified as offering this coverage—MaxBupa, Manipal Cigna, HDFC Ergo, Digit health and ICICI Lombard. 13 To the best of our knowledge, our study is the first to comprehensively review all 30 insurance companies providing health insurance, specifically focusing on mental health insurance coverage and its extent. This study aims to shed light on how these insurance providers address mental health needs within their policies, contributing valuable insights into an often-overlooked aspect of healthcare coverage.

Hence, this review aimed to investigate the effectiveness of implementing this provision of mental health insurance at par with physical illness as mandated by MHCA 2017 by health insurance companies in India, the discrepancies in the terminologies adopted in the policies covering mental illness and the recommended directions for adequate coverage in the future.

Methodology

Two authors (AVR, SMG) independently searched the IRDAI and health insurance policy issuing company websites. We accessed and downloaded policy wordings or terms and conditions from health insurance websites or the IRDAI website. The data extraction was done independently by two authors (AVR, SM) on a predefined worksheet to ensure accuracy and reduce any chances of bias. If there were any disagreements on the extracted data, it was resolved after discussion and consensus with the third author (SA). The first step in evaluating individual and family floaters’ health insurance policies was finding policies that included mental, psychiatric or psychological conditions. Suppose a policy covers mental health conditions based on the definition of ‘mental illness’ in Chapter I 14 of the MHCA 2017 or mentions the International Classification of Diseases (ICD)-10 Chapter V 15 codes related to mental and behavioural disorders, we consider it to provide mental health coverage. When a policy does not note mental illness in its definitions or explicitly lists it in its exclusions, it is considered not to offer mental health coverage.

From the policy wording documents, we analysed the following.

The coverage for mental illness

The waiting period for mental illness

The coverage for treatment of substance use-related disorders

The coverage for self-harm or suicide

The coverage for outpatient consultation, diagnostics and prescription expenses.

We did not include the government-funded schemes that provide coverage for mental illnesses such as Ayushman Bharat, CGHS, EHS, Nirmaya and other state government-funded schemes.

Results

An analysis of 30 companies’ health insurance policies offered by private and public entities was conducted as part of our research. Our evaluation examined policies designed for individual and family health coverage, emphasizing mental health coverage.

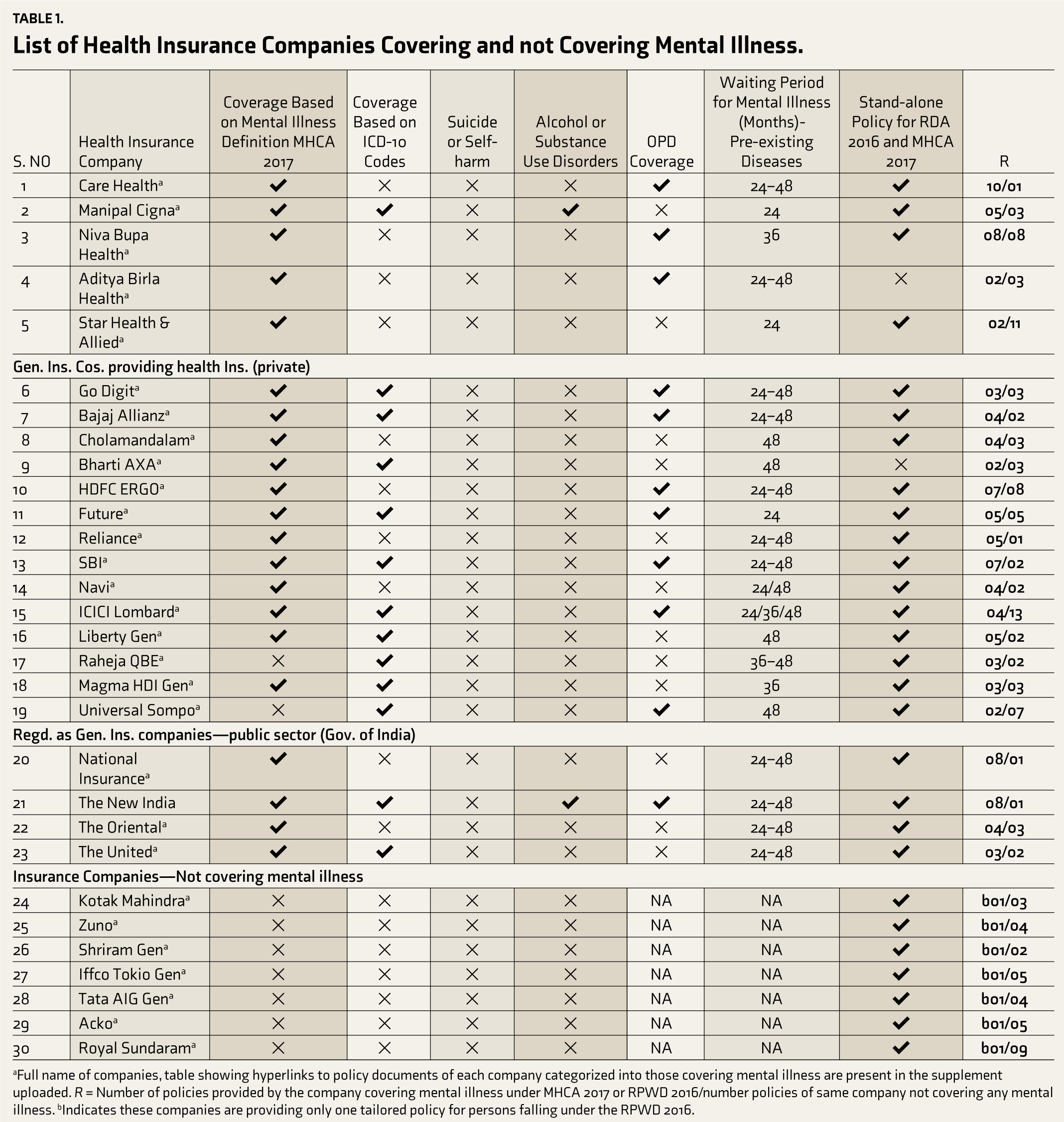

In India, 30 health insurance companies offer various health insurance plans, of which five are stand-alone, and 25 are general insurance companies registered with IRDAI. Four of these companies are public sector entities. Table 1 displays the number of policies that include coverage for mental illness treatment. Tailored health insurance policies for persons with a disability falling under the RPWD 2016 or MHCA 2017 are listed in a separate column in Table 1.

List of Health Insurance Companies Covering and not Covering Mental Illness.

aFull name of companies, table showing hyperlinks to policy documents of each company categorized into those covering mental illness are present in the supplement uploaded. R = Number of policies provided by the company covering mental illness under MHCA 2017 or RPWD 2016/number policies of same company not covering any mental illness. bIndicates these companies are providing only one tailored policy for persons falling under the RPWD 2016.

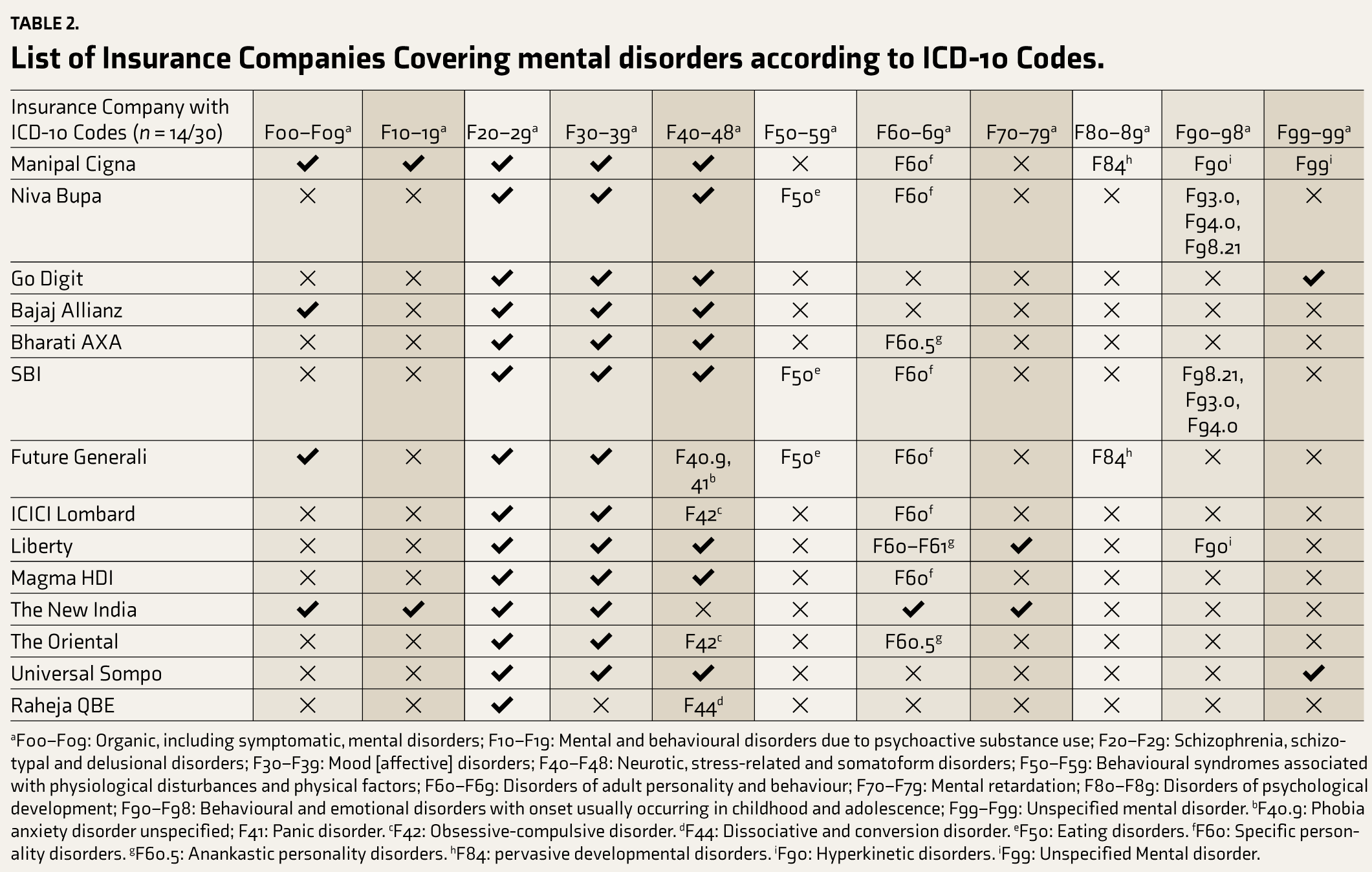

After reviewing the policy wording, it has been determined that 22 companies offer health insurance policies covering mental illness treatment. Typically, these policies abide by the definition of mental illness outlined in the MHCA 2017, Chapter 1, clause (2) definitions and subclauses. 14 In addition, the companies have adopted the definitions of ‘mental health establishment’, ‘psychiatrist’ and ‘mental health nurse’ from MHCA 2017. The following companies—Manipal Cigna, Go Digit, Bajaj Allianz, Bharti AXA, SBI, Future Generali, ICICI Lombard, Liberty, Magma HDI, The New India and The Oriental—use ICD Chapter V codes 15 to specify covered mental illnesses along with mental illness definition from the MHCA 2017. Universal Sompo and Raheja QBE had used ICD-10 codes only to specify coverage for mental illness. These companies do not consistently use ICD-10 codes across their mental health policies; instead, they rely on the Mental Health Act 2017 to rewrite definitions in such cases. This inconsistency in the terminology of the definition used across the various insurance policies indicates the need for the involvement of stakeholders of mental health that include IRDAI, mental health experts, policy users and insurance policy providers into the policy development as well as future revisions with respect to definitions and eligibility criteria to ensure uniform decision making for policy providers and users (refer to Tables 1 and 2).

List of Insurance Companies Covering mental disorders according to ICD-10 Codes.

aF00–F09: Organic, including symptomatic, mental disorders; F10–F19: Mental and behavioural disorders due to psychoactive substance use; F20–F29: Schizophrenia, schizotypal and delusional disorders; F30–F39: Mood [affective] disorders; F40–F48: Neurotic, stress-related and somatoform disorders; F50–F59: Behavioural syndromes associated with physiological disturbances and physical factors; F60–F69: Disorders of adult personality and behaviour; F70–F79: Mental retardation; F80–F89: Disorders of psychological development; F90–F98: Behavioural and emotional disorders with onset usually occurring in childhood and adolescence; F99–F99: Unspecified mental disorder. bF40.9: Phobia anxiety disorder unspecified; F41: Panic disorder. cF42: Obsessive-compulsive disorder. dF44: Dissociative and conversion disorder. eF50: Eating disorders. fF60: Specific personality disorders. gF60.5: Anankastic personality disorders. hF84: pervasive developmental disorders. iF90: Hyperkinetic disorders. iF99: Unspecified Mental disorder.

This study found that all insurance providers universally excluded coverage for incidents related to suicide or self-harm. In practical terms, if a patient is hospitalized due to an attempted suicide or self-harm, their mental illness treatment expenses will not be covered by their insurance policy.

Only two of the 30 insurance companies (6.6%) studied (Manipal Cigna and The New India Assurance Company) cover alcohol and psychoactive substance use disorders. However, the majority of 28 companies (93.4%) do not cover these disorders.

Eleven out of 30 insurance companies (36.6%) analysed, namely Care Health, Go Digit, Niva Bupa, Aditya Birla, Bajaj Allianz, HDFC Ergo, Future, SBI, Universal Sompo, New India and ICICI Lombard, provide coverage for outpatient department services for mental illness. However, the level of coverage offered is not uniform across all policies and is mainly restricted to premium policies. Some companies offer coverage in the form of special discount rates or certain plans on consultation, pharmacy and diagnostics (CARE, HDFC, SBI, ICICI), while others set a cap on the coverage amount based on the sum insured in the policy (Go Digit, Future). In addition to the above insurance providers, a few others (Reliance, Bharati AXA, Cholamandalam) are providing outpatient coverage as an add-on.

In health insurance, a waiting period for mental illness coverage is a specific period after the policy starts, during which the policyholder cannot file a claim for mental illness. However, the waiting period for mental illness coverage differs across the policies. Manipal Cigna and Star Health have a waiting period of 24 months, whereas Niva Bupa and Magma HDI have a waiting period of 36 months. Cholamandalam, Bharati AXA and Liberty Gen have a waiting period of 48 months. Other insurance companies’ waiting periods range from 24 to 48 months, depending on whether mental illness is a pre-existing disease or the specific diagnosis of mental illness. ICICI allows selecting a waiting period of 24/36/48 months, with shorter durations attracting higher premiums.

Almost 28 of the 30 companies (93.3%) examined provided tailored policies to cover individuals with >40% disability who fall under RPWD 2016 and the MHCA 2017. These policies offer health insurance to people who have intellectual disabilities, mental illness, specific learning disabilities, speech and language disabilities and autism spectrum disorder, etc. These 28 policies that are available to people with benchmark disabilities had restricted the total sum insured to 10 lakhs.

A thorough review of the policies of 30 insurance companies included a total of 235 health insurance policies. Of these policies, only 11.5% (28) were designed to cater to individuals with disabilities, whereas 37.5% (88 policies) of the insurers provided mental illness coverage in some form. Unfortunately, a significant 51% (119) of the insurance policies did not offer any coverage for mental illness. However, the insurance taker or the policyholder has to note that the availability of mental health services can vary among different insurance providers, underscoring the importance of checking what specific services are included and excluded in coverage is essential to choosing the policy.

Companies vary in the number of policies they offer that include mental health coverage as part of their range of health insurance options. Companies such as Care Health Insurance, HDFC Ergo, SBI Insurance, Reliance Insurance, National Insurance Company and Liberty General Insurance are committed to mental health and offer many policies covering mental illness. However, Aditya Birla, Star Allied Health Insurance and ICICI Lombard appear to have a limited focus on mental health coverage, with many policies excluding it. Meanwhile, some companies like Niva Bupa Health Insurance, Go Digit Health Insurance, Bajaj Allianz, Bharti AXA, Future Insurance, Navi Health Insurance, Raheja QBE, Magma HDI General Insurance, The Oriental Insurance Company and The United Insurance Company offer both policies covering and not covering mental illness to maintain a balanced approach. Most of the health insurance policies provided by The New India Insurance Company cover mental health support. These findings highlight the importance of individuals reviewing insurance policies carefully to ensure that they get adequate mental health coverage based on their specific needs and preferences.

Companies such as Kotak Mahindra, Shriram General Insurance, Universal Sompo, IFFCO Tokio, Tata AIG, Acko and Royal Sundaram Insurance offer coverage for patients with a disability under RPWD 2016. These companies combined, offer 36 health insurance policies, however, none of them provide mental health coverage. This finding highlights a notable gap in mental health coverage within the offerings of these insurance providers, emphasizing the need for increased attention to mental health support.

Table 2 shows the ICD-10 codes from Chapter V that are covered by the mental health insurance policies of the companies studied. A total of 14 of 30 companies that used ICD-10 codes did not use these consistently across all their health policies covering mental illness.

The most common mental health conditions covered by all companies are schizophrenia, mood disorders and anxiety disorders. In anxiety disorders, the emphasis was on phobic disorders and obsessive-compulsive disorders. Future Generali and SBI cover eating disorders. Specific personality disorders (F60) are also consistently covered, but only Bharti AXA and Oriental Insurance cover anankastic personality disorder (F60.5). Mental retardation is covered by Liberty and New India Assurance; pervasive developmental disorders (F84) are covered by Manipal Cigna and Future Generali; and Manipal Cigna and Liberty Insurance cover hyperkinetic disorders (F90).

Discussion

Our comprehensive analysis of health insurance providers and their policies examined 30 companies offering health insurance coverage in India. As part of our analysis of health insurance providers in India, we focused on policies covering mental health, particularly those encompassing individual and family coverage. Previous literature on mental health and insurance stated that only a few companies offer this coverage.12, 13 Our study aligns with the information presented on the floor of the parliament, where the Finance Minister, Smt. Nirmala Sitharaman responded to a question about mental health insurance. She stated that, as of 15 September 2019, 111 insurance products had registered products with the IRDAI that covered mental health insurance. 16 This acknowledgement from the finance minister underscores the significance of our research, as it corroborates the growing recognition of mental health coverage within the insurance industry and the need for comprehensive analysis and awareness in this regard. The increase in companies recognizing the importance of mental health insurance indicates a positive evolution in the Indian insurance industry. Sustainable development goal 3.8 that aims to achieve universal health coverage by 2030 also encompasses access to essential healthcare services including mental health and it also aims to protect individuals from financial risks associated with healthcare expenses. This can be achieved through effective policymaking that includes mental health insurance. 17 It is imperative to continue advocating for mental health inclusion in insurance policies and making mental health coverage a standard feature, ensuring comprehensive benefits for patients suffering from mental illness.

In our study, all the insurance companies covering mental illness used the definition of mental illness as per Chapter 2 subclause (s) of MHCA 2017, 14 which uses the words ‘substantial’ ‘grossly’ ‘recognition of reality’ ‘ability to meet the ordinary demands of life’ and ‘mental conditions associated with the abuse of alcohol and drugs’ definition of mental illness. For insurance providers, this definition helps in accuracy in clinical diagnosis, reduced moral hazard (faking of mental illness) and cost control. Due to the subjective nature of these definitions, their interpretations may vary, which may potentially hinder individuals with less severity from accessing the mental health care they require. 18 Despite the MHCA definition covering substance use disorders as mental health conditions, many insurance companies have not provided coverage for it. A more objective and clear definition is crucial to ensure that those in need can access the necessary support without undue ambiguity.

While most insurance companies have incorporated the mental illness definition outlined in the MHCA 2017, few have used ICD-10 Chapter V codes in their policies. The findings from the 2016 NMHS indicated that common mental disorders were prevalent in 10% of the population, a higher rate compared to the 0.8% prevalence of severe mental disorders. It is worth noting that insurance companies tend to prioritize severe mental disorders over the more widespread common mental disorders. This imbalance in prioritization could significantly contribute to the existing treatment gap and the substantial burden on mental health care. 19 Insurance companies also have no consistency regarding the mental illness-related ICD codes they cover. The ICD-10 codes for organic, substance use, eating and childhood disorders are inconsistently and sparsely covered across the policies. The above inconsistencies raise concerns about equity and fairness, making it difficult to choose a policy that aligns with their mental health needs. Transparency in policy communication, advocacy, and the vital role of the regulator (IRDAI) in adopting international definitions of mental illness from the latest WHO ICD edition will help patients make informed choices when buying insurance.

Suicide and Self-harm are excluded by all insurance companies covering mental illness. 173,347 deaths in 2019 were from suicide in India. 20 Apart from that suicide and suicide attempts often co-occur with psychiatric illness as reported in a recent review with 28%–40% with psychotic episodes,19%–50% with bipolar disorders, 21%–40% with depressive disorder, 18% with anxiety disorders and 19% of OCD patients attempt suicide. 21 This implies a great need for evaluation and management of those are harbouring thoughts of suicide or attempting suicide. Section 115 of MHCA 2017 presumes that a person attempting suicide is under severe stress and needs treatment. However, continued use of suicide/self-harm as an exclusionary clause by the insurance companies will hinder the reporting as well as access to treatment. 22 This further triggers the vicious cycle of public and self-stigma attached to the topic of suicide due to discrimination caused by exclusion.

The Mental Health Parity and Addiction Equity Act in the United States is a federal law that requires group health plans and health insurance issuers to provide equal coverage for mental health at parity with physical health. The states with parity laws saw a notable 5% decrease in suicide rates compared to states with ‘mandated offering’ laws. This suggests that comprehensive mental health coverage integrated into insurance packages can contribute to suicide prevention and improved mental health outcome. 23

Only six of the 30 health insurance providers studied offer coverage for alcohol or substance use disorders. This could be due to the standardization of exclusion of ‘Treatment for Alcoholism, drug or substance abuse or any addictive condition and consequences thereof’ in standard exclusions 12 by IRDAI. 24 An expert committee constituted by IRDAI has opined that excluding treatments for substance use disorders unless associated with mental illness, could lead to complex issues. This could be due to their frequent co-occurrence, leading to challenges in categorizing treatments as exclusively related to one or the other in the background of a high treatment gap of 91% for substance use disorders as per NMHS 2016. 19 This exclusion criterion will deny treatment of substance use disorders and potentially reject the insurance coverage to other mental illnesses if they have co-existence of substance use or mention of substance use in their case notes.

The definition of mental illness used by insurance companies adopted from MHCA 2017 includes ‘mental conditions associated with the abuse of alcohol and drugs’. 14 Based on a 10-year retrospective chart study from a South Indian hospital, 19% of patients diagnosed with alcohol and psychoactive substances required hospitalization. 25 Excluding substance use disorders will be in contradiction to the spirit of MHCA 2017. State parity laws mandating equitable coverage for substance use disorders in the United States are associated with increased treatment-seeking among individuals with alcohol use disorders, a 10% rise in SUD treatment rates, 26 substantial reductions in crime rates, an estimated economic benefit of $2.5–4.8 million, 27 and a noteworthy 4%–9% decrease in traffic fatalities underscoring the potential for comprehensive insurance to yield substantial societal benefits and harm reduction. 28 With these positive findings, we recommend the inclusion of alcohol use disorders under mental health insurance.

Of the policies we examined, only a limited number of them offer outpatient facilities, encompassing consultation, diagnostics and pharmacotherapy, with the amount payable varying either as a proportion of the sum insured or in the form of discounted rates on the mentioned charges. Psychiatric patients often seek outpatient consultations, which comprise a significant percentage of their visits. The Key Indicators Report of Household Social Consumption in India: Health, 75th round revealed that approximately 4%–4.5% of disorders in India are psychiatric or neurological. Furthermore, 95% of the population preferred allopathic treatment, with 23% of individuals receiving treatment in a private hospital and 43% consulting a private doctor or clinic. The major expenses consisted of medicines (64%–82%), diagnostic tests (9%–15.7%) and doctors’ fees (2.4%–5.8%). Overall, 9.7% of households consulted psychiatric outpatient department (OPD). The percentage of households falling below the poverty line in psychiatric disorders was (22.9%), The Poverty Head Count Ratio represents the percentage of households that fall below the poverty line due to out-of-pocket expenses related to psychiatric conditions, which was observed to be 53.1% for both hospitalization care and OPD care. Almost two-thirds of out-of-pocket spending for mental health care comes from prescription drug expenses. 29 Considering this, OPD coverage, including consultation fees, diagnostics and pharmacotherapy, should be part of mental illness coverage in all insurance plans.

Our study found that some insurance companies specify waiting periods of 24, 36 or 48 months for mental health coverage. However, there is variation across policies, with some companies considering mental illness as a pre-existing condition and imposing a 48-month waiting period, while others based on the type of mental health condition. This creates confusion and inequities in access to mental health care, delays treatment, discourages coverage and disproportionately affects vulnerable populations. Balancing these factors is crucial for fair coverage.

We recommend that the insurance companies should modify their standard exclusion criteria as set by IRDAI, to include coverage for substance use disorders and self-harm when these are part of a psychiatric diagnosis confirmed by a mental health specialist. This change would ensure that individuals with these conditions receive essential medical support and treatment, recognizing the significance of mental health in overall healthcare. The psychiatric expert committee formed by IRDAI should develop guidelines to facilitate the inclusion of substance use and self-harm treatments under mental illness coverage, moving away from their standard exclusion as substance use and suicide are pertinent public health issues.

This study has limitations in terms of its scope. It is important to note that analysing policy documents involves interpreting complex legal and medical language, which may result in varying interpretations. Although authors tried to contact some service providers, it is important to acknowledge that obtaining comprehensive policy documents and data from all insurance providers can be challenging and as a result, there may be variations in data accessibility. As we are obtaining policy wording from the company website the companies may have changed their policy wording which may not be updated on the website can also result in variability.

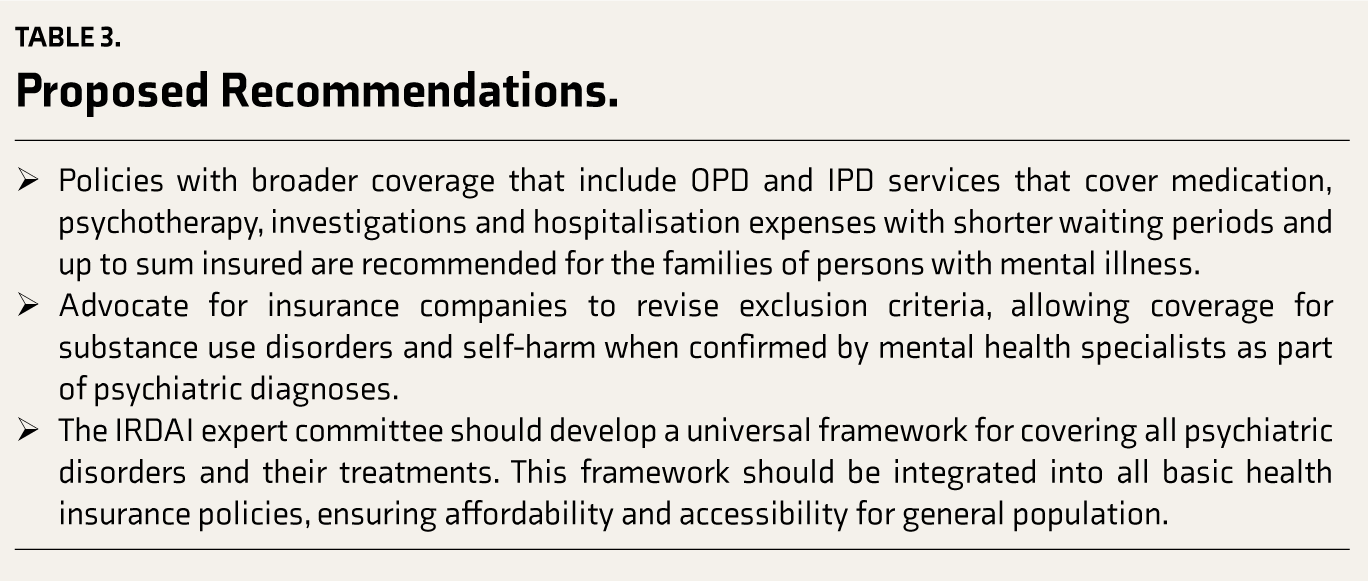

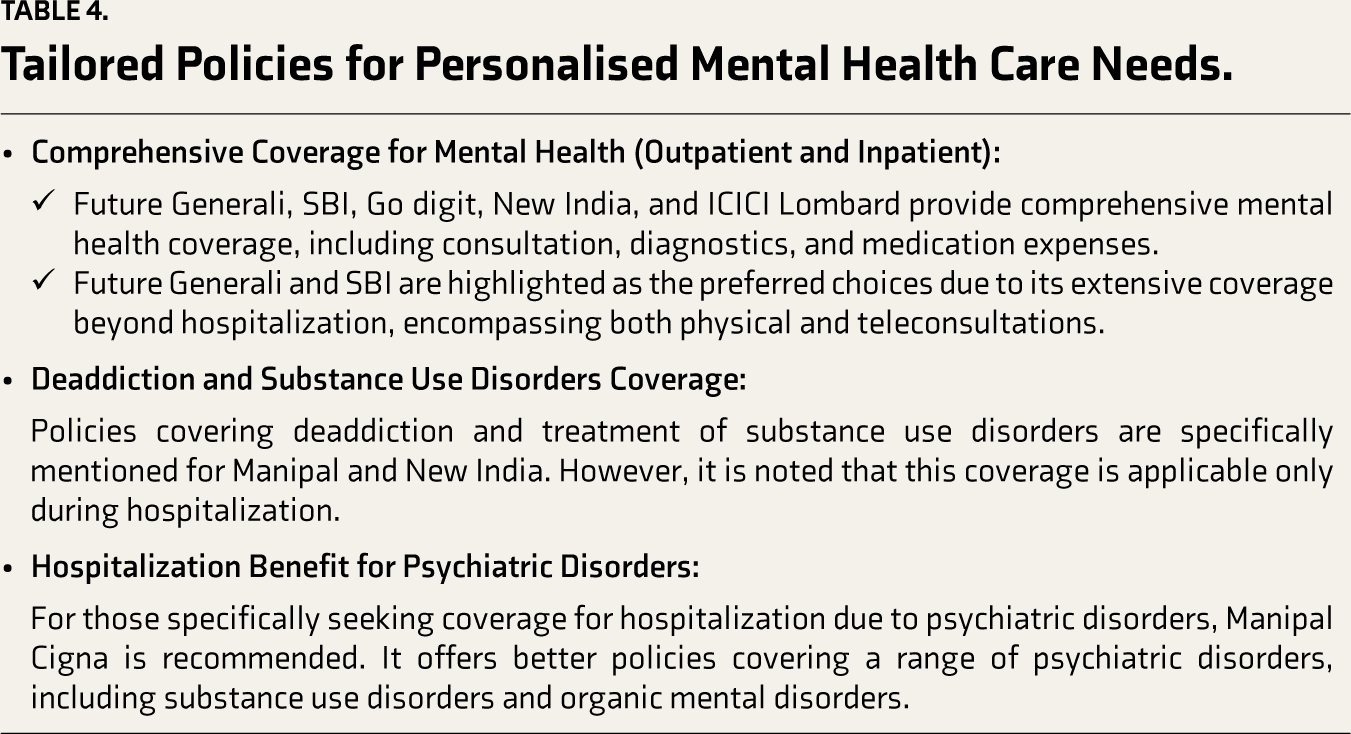

The proposed recommendations and suggested changes required in future policy reforms targeting various stakeholders have been mentioned in Table 3 and based on the analysis of various policies (refer to supplementary Table 2), the key highlights and recommendations are made regarding the best health insurance policies for various mental health care needs in Table 4. It emphasizes the need for continued awareness, collaboration and advocacy for making mental health coverage a standard feature in insurance policies, ensuring comprehensive benefits for patients suffering from mental illness.

Proposed Recommendations.

Tailored Policies for Personalised Mental Health Care Needs.

Conclusion

Despite the multiple circulars mandating for inclusive mental health in the health insurance policies, the implementation appears partially addressed and it is essential to note that health insurance exclusions can negatively affect individuals seeking mental health treatment. However, on a positive note, India’s health insurance system has been evolving for better than before to address the mental health needs of its population as par with physical health.

To conclude, our comprehensive analysis of health insurance providers in India sheds light on how mental health coverage is evolving within the insurance industry. Despite the growing recognition of the importance of mental health insurance, several challenges remain, such as the need for clear and objective definitions of mental illness, consistent coverage of ICD codes, and the inclusion of suicide and self-harm.

Further, the narrow coverage for alcohol and substance use disorders, inconsistent waiting periods, and the absence of outpatient facilities in many policies highlight areas that require improvement. Providing equitable and comprehensive mental health coverage requires advocating for standardization, transparency in policy communication and adoption of international definitions, while also considering the potential societal benefits of expanding coverage for mental health conditions and substance use disorders.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Declaration Regarding the Use of Generative AI

None used.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.