Abstract

This article is the first to explore the consequences of migration for asset accumulation from a multi-site and intergenerational perspective that moves beyond the prevailing migrant versus “native” comparisons performed within single destination-country contexts. It specifically investigates the non-financial investments (i.e., house, land, and business-related asset holdings) made in the country of residence by three family generations of migrants with origins in Turkey: those who resided in Europe (i.e., settlers), those who moved to Turkey (i.e., returnees), and those who remained in the origin country (i.e., stayers). The data are drawn from the 2000 Families Survey, which involved personal interviews with 5,980 individuals nested within 1,770 families. The analysis shows that migration’s greatest economic beneficiaries are returnees, who display a significant tendency to accumulate the most assets across all generations and asset types. Across all three groups, intergenerational family transfers are found to make a positive difference to younger generations’ non-financial investments. The chances of reaping the benefits of such transfers, however, is shown to be particularly limited for the descendants of settlers, given this group’s propensity to accumulate the fewest (especially house and land type) non-financial assets in European destinations where they reside. Through these unique multi-site and intergenerational comparisons between migrants and stayers, this article sheds new light upon the little-explored relationship between international migration and asset accumulation, and the economic dis/benefits of migration.

Keywords

Introduction

Much of the empirical literature exploring the economic outcomes of international migration draws on migrant-“native” comparisons of income, earnings, employment, and/or occupational status, which tend to be performed to test assimilation theorists’ (e.g., Alba and Nee, 1997) expectation that migrants’ economic performance would resemble that of natives as time passes (e.g., Borjas 1987; Büchel and Frick, 2005; van Tubergen, 2006; Bratsberg, Raaum and Røed 2014). Assimilationists predict the prospects for migrants’ children to be even more favorable, since they do not face the same initial adjustment challenges as their parents (e.g., Todaro 1969). The scope of the above-sketched literature has been extended to the second and even third generation (e.g., Boyd and Greco 1998; Trejo 2003; Reitz, Zhang, and Hawkins 2011) to determine if this prediction holds true. This body of work, however, has often proceeded without establishing a familial link between the generations studied (Güveli et al. 2017, for exceptions, see Güveli et al. 2015).

Generational focus notwithstanding, migrant-“native” comparisons shed only partial light upon the extent to which migrants economically benefit from their decision to move. To complete the picture, one would also need to know the counterfactual (i.e., What would have happened to migrants and their descendants if they had decided to stay in the origin country?). While it remains very difficult to establish the outcomes of people’s unmade choices in the social world, comparisons that have recently been drawn between migrants and stayers successfully approximating this hypothetical situation (e.g., Eichenlaub, Stewart, and Alexander 2010; Bartram 2013; Güveli et al. 2015; Baykara-Krümme and Platt 2018; Curtis 2018; Eroğlu 2020). However, none of these rare comparisons focus on migrants or their descendants’ financial (i.e., intangible) or non-financial (i.e., tangible) investments.

This article is, thus, the first to compare the non-financial asset holdings of three family generations of “migrants” who span multiple destinations and who returned to the origin country with their counterparts who did not leave their origins. Through these unique multi-site and intergenerational comparisons between migrants and stayers, it not only uncovers the relationship between international migration and asset accumulation that is currently understudied but also throws new light into the economic dis/benefits of the migration process itself. As the article shows, of migrants and their descendants originated from Turkey, those settled in different destinations in Europe have benefited the least from the migration process. This group of migrants proved less able than their returnee and stayer counterparts to accumulate non-financial assets in the country in which they currently live.

The structure of this article is as follows. It first reviews the diverse empirical works focused on the asset or wealth accumulations of minority (ethnic and migrant) and left-behind populations within origin- and/or destination-country contexts. It then presents the theoretical approach taken here to inform variable selection for the statistical modelling of the relationship between migration and asset accumulation. The theory section is followed by a presentation of the research design, method, and findings. The research limitations and questions that warrant future exploration are addressed in the conclusion.

An Empirical Review: Asset and Wealth Accumulation in Origin and Destination

The bulk of the research literature on asset or wealth accumulations of minority populations explores the nature, extent, and likely determinants of ethnic and racial inequalities in wealth distribution within the United States (e.g., Blau and Graham 1990; Conley 1999; Oliver and Shapiro 1995; Keister 2004; Killewald 2013). These works collectively show significant and persisting disadvantages for different ethnic minority groups. While this part of the literature examines the significance of race and ethnicity relative to a wide range of demographic, socio-economic, and geographic factors—from marital status, family size, and structure to income, educational and occupational status, and residential location—it rarely takes into account migration-related influences to demonstrate the importance of migrant and/or non-national status in creating further disadvantages (Campbell and Kaufmann 2006; Meschede, Darity and Hamilton 2015)

The body of research that specifically investigates international migration’s role in asset or wealth accumulation is less developed. Of the three strands that can be identified, the first involves studies of migrant populations living within a single destination in Europe or the United States (e.g., Kumcu 1989; Merkle and Zimmermann 1992; Hao 2004; Cobb-Clark and Hildebrand 2006; Akresh 2011; Painter, Holmes, and Bateman 2016). This strand of research conducts between- or within-group analyses of different migrant populations or compares them with “natives” to, for example, uncover the likely effects of migrant, citizenship, and nativity status, origin country, length of stay in the destination country, and return plans on asset or wealth accumulation. To illustrate, Hao (2004) demonstrates wealth in the United States to be stratified more along lines of national origin than nativity. Cobb-Clark and Hildebrand (2006) show that established migrants in the United States are more likely to have equity in real estate than are recent migrants while the reverse is true where their financial wealth (e.g., savings) is concerned. Two studies with coverage of migrants from Turkey to Germany (Kumcu 1989; Merkle and Zimmermann 1992) demonstrate a significant tendency for migrants with return plans to save more than those without.

The second strand of research examining international migration’s role in asset or wealth accumulation also investigates migrant populations, but studies from this strand are rare in that they explicitly link migrant origins to destinations by incorporating investments made in the origin country into their analyses. Using 1988 data from the German Socio-Economic Panel, Dustmann and Mestres (2010) show that migrants with return plans are likely to deposit a larger portion of their savings in the origin than in the destination. Similarly, De Haas, Fokkema, and Fihri (2015) reveal that migrants with investments in the origin country are more inclined to have return plans. Ülkü’s (2012) study of Turkish migrants in Germany complements these findings by indicating a greater tendency for those with deep roots in Turkey to invest in the country. There are also two studies on 19th-century internal migration in the United States, comparing migrants with non-migrants or “persisters” (Herscovici 1998; Stewart 2006). Both confirm migration’s significant benefits for wealth accumulation.

The third strand of scholarship on international migration’s role in asset or wealth accumulation directs attention to migrant origins, mostly to investigate the contributions of economic remittances to the asset or wealth accumulations of left-behind populations (i.e., recipient households or communities; Massey and Parrado 1994; Yang 2008; Prabal and Ratha 2012; Ahmed, Mughal, and Klasen 2018). The investments of migrants who returned to their origins, however, remain little explored. There is only one study by Wong, Palloni, and Soldo (2007) that suggests a long-term positive effect on personal wealth from migration for middle- or old-age returnees from the United States to Mexico. A few other studies investigate the role of return migrants’ overseas savings in shaping their entrepreneurial behaviors or re-integration performances. Some find evidence of increased entrepreneurial activity among those with greater savings (McCormick and Wahba 2001; Piracha and Vadean 2010), while others show that this group of returnees is more likely to be economically inactive and to waste skills (Coniglio and Brzozowski 2018).

None of the existing explorations of the relationship between international migration and asset or wealth accumulation have a generational focus. As recently reviewed in Güveli et al. (2015, 2017), intergenerational studies within the international migration literature track and explain changes in attitudes, beliefs, or educational/occupational status over time, but the great majority of them capture no more than two generations and draw on migrant, as opposed to nested family, generations (Güveli et al. 2017). While the works of the 2000 Families Survey team establishes the family link between three generations to allow exploration of intergenerational transmission (e.g., Baykara-Krümme 2014; Spierings 2014; Güveli et al. 2015; Eroğlu 2018, 2020), none of them are concerned with migrant investments. Hence, the impact of intergenerational asset or wealth transfers on asset accumulations of younger generations remains understudied. In fact, only a few ethnic and racial studies examine the likely effects of such transfers on asset or wealth inequality through a focus upon parental wealth status and/or the receipt of inheritance or inter vivo payments from parents for their children’s education or house purchases (Menchik and Jianakoplos 1997; Conley 1999; Meschede, Darity, and Hamilton 2015). These studies indicate a significantly reduced propensity for families from ethnic minority backgrounds to make such transfers.

Overall, then, the empirical literature exploring international migration’s consequences for asset or wealth accumulation remains underdeveloped. Most existing works examine either migrant or left-behind populations. The link between migrant origins and destinations is rarely explored, and except for some historical research on internal migration, none of the existing studies on asset or wealth accumulation compare migrants and stayers. Moreover, contrary to the ethnic and racial research on wealth inequality, the relevant parts of the international migration literature lack a generational focus. This article is an attempt to address these research lacunae.

Theoretical Framework

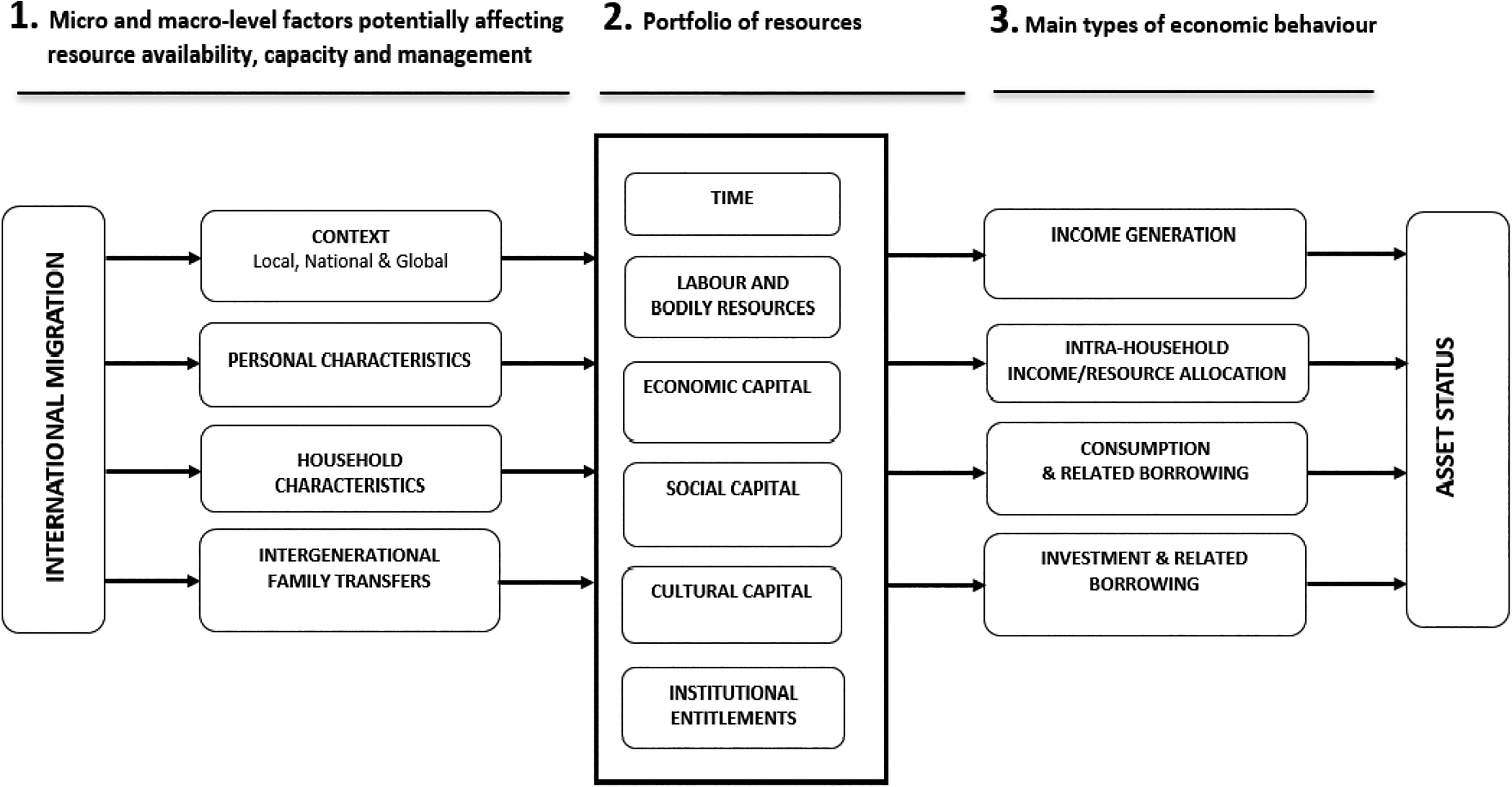

Figure 1 presents the theoretical model used here to inform variable selection for the statistical exploration of the relationship between (international) migration and asset accumulation. This model was originally designed and applied by Eroğlu (2011) to examine the likely influences upon household responses to poverty from a resource-based perspective. The improvements it makes upon the past variants of this perspective were discussed in Eroğlu (2013), and the model was subsequently adapted to understanding migration-related effects on self-employment and gender equality (Eroğlu 2018; 2020). Here, it is advanced further to explore migrants’ investment behavior and the particular role played by the migration process.

A Resource-Based Approach to Migration and Asset Accumulation.

This model is borne out of the need to demonstrate the complex causal paths between various macro- and micro-level influences, migrants’ resources and economic behaviors, and their interactions with the migration process. While variants of the resource-based perspective have been widely used within the poverty and livelihoods literatures (e.g., Swift 1989; Moser 1998), this perspective has only recently been applied to researching migrant assimilation and subjective well-being (Alba and Nee 2003; Ryan, Dooley, and Benson 2008). Alba and Nee’s (2003) new institutionalist theory of assimilation recognizes the role of contextual influences, such as institutional structures, cultural beliefs, and social networks in shaping migrants’ and their descendants’ resources and purposive actions. However, like Ryan’s approach (2008), this theory neither provides an exhaustive list of resources nor establishes the link between migrant resources and livelihoods. The same applies to the modes of incorporation (Portes 1995) and mixed embeddedness (Rath 2000) approaches developed for understanding the context-related effects upon migrant resources or economic actions (e.g., entrepreneurship).

The model proposed here moves beyond the aforementioned theorizations and establishes the link claimed to be missing from existing conceptualizations of the connection between international migration and development (De Haas 2010) by situating migration processes within the broader framework of household resources and livelihoods. This framework not only accounts for contextual effects on migrant resources and economic behaviors but also recognizes the key influences operating at the individual and household levels and across family generations. The core features of the model are summarized further.

To start, the model recognizes key micro- and macro-level factors that potentially influence migrants’ economic behaviors and asset status by enhancing or constraining the availability, capacity, and management of their resources. One’s asset status is represented here by his/her combined financial and non-financial holdings. The former denotes intangible assets that can take various forms (e.g., bonds, shares, and bank deposits), while the latter comprises tangible or physical properties (e.g., house, land, and business; Eroğlu 2011).

Second, the model divides economic behavior into the following main categories: income generation, intra-household income allocation, 1 consumption, investment, and related borrowing. It also identifies core resources that can potentially be applied in such behavioral activities—namely, time, labor and bodily resources, economic capital, cultural capital, social capital, and institutional entitlements. While the first three elements of the resource portfolio are self-explanatory, the boundaries of the remaining resources need to be clarified further. Like Bourdieu (1986), the term cultural capital is used here to denote the skills, knowledge, and qualifications attained formally through schooling and informally throughout the life course. The term economic capital is also used in a similar way to Bourdieu to embrace financial and non-financial assets that are immediately and directly convertible into money. One may invest more in financial than non-financial assets or vice versa and, at any point in time, would have the choice to convert these assets in part or in full to one another. While these assets can be re/invested throughout the life course, at a specific point in time, they compose the stocks that represent one’s asset status.

Social capital is defined here more narrowly than Bourdieu to refer to relatively durable relations established inside and outside markets. This particular definition is closer to the one proposed by Pizzorno (2001), but unlike his, it includes market-based contacts. Institutional entitlements cover rights of access to various monetary and non-monetary benefits (e.g., cash, assets, goods, and services) granted by governmental and non-governmental organizations. The model does not assume a straightforward positive link between resources and asset accumulation because the outcome depends on the capacity of the resources to deliver benefits and this capacity may well be restricted by various (structural) factors. For example, Eroğlu (2010) demonstrates that poor people with large volumes of social capital make little economic gains from these contacts due to being mostly connected with people of limited resources or due to their inability to reciprocate with better-off people on an equal footing.

Third, the model categorizes the key micro- and macro-level factors likely to affect the composition of migrant resources into four main types. The first relates to one’s personal features (e.g., age, sex, ethnicity, nationality, and migration history). For example, the economic, social, and cultural capital resources utilized for investment are likely to increase with age and time spent in the destination country. Likewise, citizenship or resident status can determine one’s rights to own assets in the destination country. The second set of factors concern household characteristics (i.e., household size, composition, and stage in the life-cycle), which potentially affect the availability of labor resources that can be deployed for income generation and, hence, the amount of money that can be generated and invested. The third set of factors refers to intergenerational family transfers or transmissions (i.e., endowments passed from other family generations in the form of beliefs, values, resources, and behaviors). The financial skills, contacts, and tangible and intangible assets comprise some of the endowments whose transmission can potentially enhance one’s asset or wealth status. The final set of factors encompasses a wide range of local, national, and global contextual influences from labor and asset market conditions and government policy to public attitudes toward migrants.

Within this model, international migration is conceived as a major life-changing process that reconfigures migrants’ resources, behaviors, and asset or wealth status by changing the local and national contexts in which they function, some of their personal and household features (e.g., national and ethnic identity, and household composition), and/or the nature and extent of family transfers across generations. For instance, the process of migration may change migrants’ national identity through acquisition of citizenship or reshape their ethnic identities by altering their perceptions of themselves and sense of belonging to a community. Equally important, by recognizing the structurally conditioned nature of economic outcomes for migrants, this model departs from assimilation theory, which predicts an improvement upon their economic standing over time and across generations (e.g. Alba and Nee, 1997). It concurs more with segmented assimilation theory, which points to a range of structural factors that can lead to migrants’ and their descendants’ downward assimilation (Portes and Zhou 1993).

The structural constraints upon one’s economic performance are likely to bear more heavily upon migrants than stayers in the origin, due to the additional layer of adversity caused by public hostility towards migrants in destination countries, which is likely to block their access to labor market opportunities or bring low monetary returns on their educational qualifications (Gordon 1995; Feagin 2006). Given the evidence that nearly half of Europeans are against migration flows from poorer non-European countries (Blinder and Markaki 2018), discrimination remains a real possibility for the lives of migrants from Turkey. The small-scale businesses they have been compelled to set up since the economic crisis of the mid-1970s may present them with a low-status option for asset accumulation (Eroğlu 2018). However, when coupled with asset market conditions in Europe, their chances of making sizeable investments in the destination country are likely to decline considerably. As for return migrants, neo-classical economic theory classifies them as less favorably selected for “failing to make it” within the destination context (Chiswick 1986). However, the evidence reviewed ealier shows that migrants with return plans are likely to save more. With the help of favorable conversion rates from European to Turkish currency, returnees are likely to convert their savings into sizeable assets in the origin (i.e., current country of residence) and, thereby, fare better than stayers. Intergenerational asset transfers are likely to occur across all groups, as parents from Turkey are expected to financially support their children at every stage of their lives. However, for aforementioned reasons, settler migrants may have fewer assets to transmit.

To conclude with a point about migrant selectivity, the proposed model acknowledges that migrants may have certain observed or unobserved characteristics that systematically distinguish them from their ‘non-migrant’ counterparts (Chiswick 1986). To illustrate, it remains theoretically probable for migrants, especially those who moved for economic reasons, to own fewer assets prior to migration. This is to say, those who left their origin country may be “negatively self-selected” in terms of their pre-migration asset status. In situations where the level of assets owned prior to migration remains unknown, comparing return migrants with stayers in the origin country would, to an extent, help disentangle the migration and self-selection effects.

Research Design and Method

The article’s analysis draws on the unique 2000 Families Survey 2 (hereafter Survey) that was conducted between 2010 and 2012. The Survey located 1,580 migrant men from five high-migrant sending regions in Turkey who moved to Europe during the guest worker years (1960–74) and 412 men from the same regions who stayed behind. It charted their family genealogies and followed their descendants across Turkey and Europe, up to the fourth generation, applying a sampling quota to ensure that 80 percent of the sample came from “migrant” families (i.e., had a male migrant ancestor) and the remaining 20 percent from “non-migrant” families (i.e., had a non-migrant male ancestor). The family members followed by the Survey do not necessarily share the gender or migration status of their male ancestors. Those who moved to or were born in Europe and who had spent a year or more there are referred to here as “migrants” (or “movers”). They form a heterogeneous group consisting of (a) settlers who had resided in Europe for more than a year and (b) returnees who moved (back) to Turkey after spending a year or more in Europe. The use of the label “settlers” should not be taken to mean that all members of this migrant group planned to indefinitely remain in Europe but were likely to do so, considering that the majority of them were male guest workers and their descendants. Stayers, on the other hand, were composed of those who had not left their origin country for more than a year.

The Survey only contains information about the ownership of house, land, and business-related assets. For this reason, the article’s empirical focus is restricted to non-financial investments. In the Survey, stayers were only asked about their holdings in Turkey. Settler and returnee migrants were, on the other hand, asked separate questions about the assets they kept in Turkey and in Europe. The great majority of returnees responded to questions concerning their holdings in the country of residence (i.e., Turkey), with only 95 out of 921 reporting their assets based in Europe. Thus, it was not possible to compare the three groups’ non-financial investments in Europe and in Turkey separately or jointly. However, survey information was available on the non-financial assets held in the country of residence for 96 percent (5,738 out of 5,980) of the sample, which allowed comparisons to be drawn between three family generations of settler and return migrants and their stayer counterparts to explore the following research questions: Do settlers and returnees accumulate more or less than stayers? Do significant differences exist in the type of non-financial assets in which settlers, returnees, and stayers invest? Do subsequent generations accumulate more or less than their male ancestors? Do significant generational differences exist between settlers, returnees, and stayers in terms of the size and nature of their non-financial investments? To what extent do intergenerational family transfers have an effect on younger generations’ non-financial investments? Do significant differences exist between the three groups in the extent to which parental non-financial holdings contribute to their own children’s accumulations of similar assets?

The Survey drew parallel samples of “migrant” and “non-migrant” families from five Turkish regions that had witnessed high outmigration during guest-worker years: Acıpayam, Akçaabat, Emirdağ, Kulu, and Şarkışla (Güveli et al. 2016. See also Güveli et al. 2015 for details regarding the choice of regions.). Eligible migrant families had a male ancestor who (a) might be alive or no longer alive, (b) was or would have been between the ages of 65 years and 90 years, (c) grew up in one of the selected regions, (d) moved to Europe between 1960 and 1974, and (e) stayed in Europe for at least five years. The same criteria were applied to non-migrant families, the only difference being that their male ancestors had to have stayed in Turkey rather than migrate to Europe. The respective quota of 80:20 was applied in every region in sampling migrant and non-migrant families.

A clustered probability sampling technique was applied in the regional screenings. One-hundred primary sampling units (PSU) with random starting points were drawn from the Turkish Statistical Institute’s (TURKSTAT) address register, ensuring that each PSU’s size was proportional to the estimated population size of the randomly chosen locality. A random walk strategy was then adopted to screen each PSU. The strategy entailed going to the random starting point and knocking on every door if the locality had fewer than 1,000 households and on every other door if the number of inhabitants was 1,000 or above. Four migrant families were sampled for every non-migrant. The random walk ended when 60 households were screened or eight families were recruited.

The screenings were performed in two stages. The study was first piloted in Şarkışla in Summer 2010. The main-stage fieldwork was conducted in Summer 2011 to screen the remaining four regions. Approximately 21,000 addresses were visited to meet the target of 400 families per region. The strike rate (i.e., the proportion of eligible families) was around one in every 12 households, resulting in 1,992 participant families.

The Survey adopted multiple instruments and two distinct modes of interviewing to generate data. Those present in the field were interviewed in person, while phone interviews were conducted with those who were absent. The data used in this study are drawn from the personal interviews performed with male ancestors and their randomly selected male and female descendants aged 18 years or above. Those eligible for personal interviews included all living male ancestors, their two children, two adult children of these two children (i.e., male ancestors’ grandchildren), and these grandchildren’s adult children if any (i.e., male ancestors’ great grandchildren). The family trees constructed for all participating families were used as a sample frame to select the siblings with initials closest to A and Z. The overall response rate was high (61 percent), amounting to a total of 5,980 personal interviews with members of three generations nested within 1,770 families. The non-response rate due to reasons other than non-contact (e.g., refusal) was similarly low across eligible family members living in Turkey and Europe, at about 6–8 percent. However, by the end of the main-stage fieldwork, it was observed that the non-contact rate for potential respondents residing in Europe was higher by approximately 18 percent. This imbalance was redressed through additional three-month tracing performed in 2012 to make contact and interview hard-to-reach family members in Europe. The tracing process yielded 515 interviews, increasing the response rate for this group of respondents by about 20 percent.

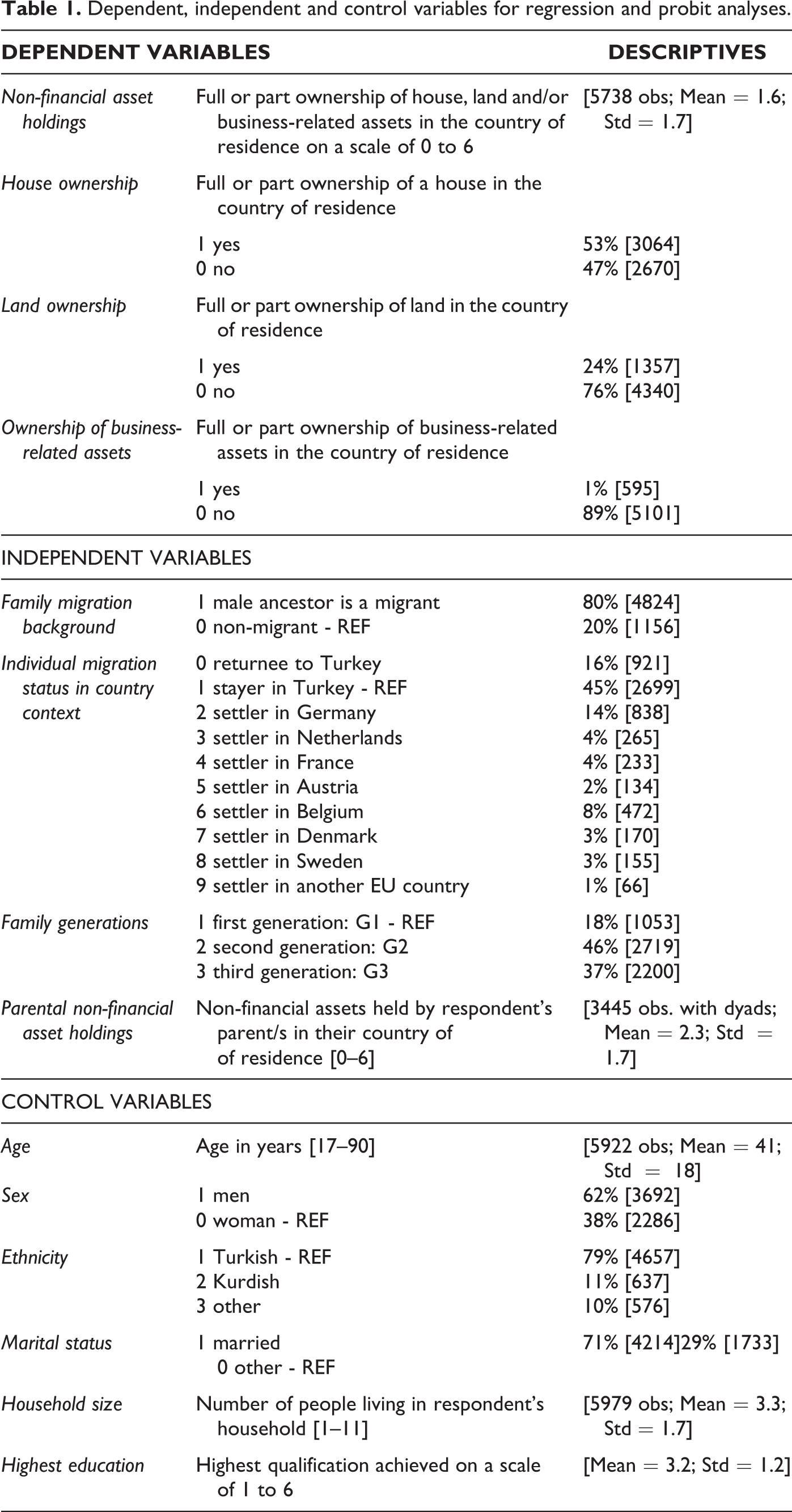

The analyses performed here combine linear regression models of overall non-financial asset accumulation with probit estimations of house, land, and business-related asset ownership. The overarching aim in conducting multi-variate analyses is to examine migration’s likely effects from a multi-site and intergenerational perspective. Hence, the relationships described within the resource-based framework and the review of past findings (see Figure 1) were used to guide the selection of key dependent, independent, and control variables rather than to identify all possible determinants of asset accumulation. That said, considerable effort was made to capture the core components of the resource-based framework relating to personal and household characteristics and family generations, along with some aspects of the resource portfolio and the migration and context-related influences upon them. The selected variables are listed in Table 1.

Dependent, independent and control variables for regression and probit analyses.

Four dependent variables were constructed from six questions about house, land, and business-related asset ownership in Turkey and Europe, with response categories of 1 “yes, full ownership”; 2 “yes, shared ownership”; and 3 “no ownership.” The first dependent variable is a scale that estimates respondents’ overall non-financial asset accumulations in their country of residence, using all of the aforementioned items. These items were first recoded to ensure that higher scores indicate greater accumulation (range 0–2). Scores were then summed to create a six-point scale. Due to an absence of information on the market prices of the assets involved, the scale generated would be insensitive to the possibility of similar type of assets having different exchange values within and across different contexts. Hence, it cannot be used to measure wealth per se but remains a useful indicator of one’s overall stock of non-financial assets. The other three dependent variables are binary in nature, representing part or full ownership of (a) house, (b) land, and (c) business-related assets (which should not be equated with entrepreneurship as people can invest in this type of assets for a range of reasons, not just to set up a business). Due to a lack of information on the exact location of the assets generated, the introduction of the binary variables does not remove the aforementioned obstacles to wealth measurement but does allow a focus on the nature of non-financial assets being generated. Hence, these binary variables complement the aggregate scale that measures the size of one’s overall holdings.

The same set of independent and control variables were employed across all statistical estimations, reflecting the following features of the resource-based framework. Migration-related influences are represented by the variables of family migration background (i.e., whether one had a migrant ancestor) and individual migration status. Some critical aspects of one’s migration history (i.e., duration of stay in Europe) could not be explored because otherwise, all stayers would have received a score of zero. Likewise, citizenship and nativity status had to be excluded due to all stayers being Turkish nationals.

Personal characteristics are indicated by age, sex, ethnicity, and position in the family tree. Due to substantial age differences within family generations (Mean age for

Household characteristics are captured by the variable of household size. The ideal would have been to calculate the household dependency ratios by combining information about household size, composition, and stage in the domestic lifecycle, potentially affecting the availability of labor and monetary resources required for income generation and investment. However, due to the lack of data on all members’ employment status or age, household size was chosen as a proxy. The existing survey data on partner’s employment status could not be used, as they would have reduced the sample size to 4,517.

Intergenerational family transfers are indicated by the proxy variable of parental non-financial asset holdings. In the absence of data to determine the value of the assets inherited by the children and/or inter vivo payments they received from their parents toward their education, business, or asset purchases, the transfers could not be measured directly. Hence, they had to be inferred from parental assets. Such an inference is considered reasonable, given (a) the likelihood that some of them had some capacity to generate cash (e.g., rent) that parents could mobilize for building their own children’s asset portfolios and (b) the expectations within Turkish culture of parents assuming a supporting role.

As for context, an attempt has been made to control for possible national-level influences affecting the origin and destination countries by differentiating settlers according to their country of residence in Europe. Local-level effects, however, remained uncontrolled for, due to the lack of location data to distinguish at least between urban and rural residents.

The statistical estimations also cover parts of the resource portfolio. Those concerning time, labor resources, and institutional entitlements have been addressed earlier in relation to age, household size, nationality, and duration of stay in Europe. The remaining are the three capital resources, which warrant further discussion. The formal aspects of cultural capital were captured by the variable of highest educational qualification achieved. The effects of previous deployments of economic capital could not be estimated due to the survey’s cross-sectional nature. A proxy for social capital could have been generated from the question “I want to ask a question about the people you are acquainted with. By acquaintanceship, we mean that you know their name and would stop and talk at least for a moment if you run into them on the street. Roughly speaking, how many people are you thinking of?” However, apart from questions it raises in terms of validity and reliability, the use of this variable would have caused the problem of endogeneity, since the survey’s cross-sectional nature renders it unclear as to whether the non-financial assets were accumulated before or after social contacts were established. Therefore, the social capital variable was removed from the statistical analyses.

The analysis involved estimating linear regression and probit models to answer the research questions set out earlier. The first regression function (MODEL 1) was developed (a) to examine the differences in the overall stocks of non-financial assets held by settlers, returnees, and stayers and (b) to trace generational trends (RQ1 and RQ3a). The second (MODEL 2) was designed specifically to investigate the impact of intergenerational family transfers (or transmissions) (RQ4a). To allow exploration of direct family transfers, dyads had to be established between parents and own children. Dyads describe a relationship between a pair of individuals, and here they link the members of the second and third generations to their own parents to generate parental information about non-financial investments. Since personal data contain no information about the male ancestor’s parental investments, a dyad could not be established between him and his parents. Therefore, MODEL 2 had to be restricted to the second and third generations. Auxiliary linear regression models were estimated separately for settlers, returnees, and stayers, using the same variables as those specified in MODEL 1 and 2 to provide further insight into whether the observed generational trends and intergenerational family transfers varied according to individual migration status (see RQ3b and RQ4b). The linear regression models were complemented with separate probit estimations of house, land, and business-related asset ownership to explore the likely differences in the nature of non-financial investments made by settlers, returnees, and their stayer counterparts (RQ2). All statistical models were cluster-corrected to account for within-family association.

The Results

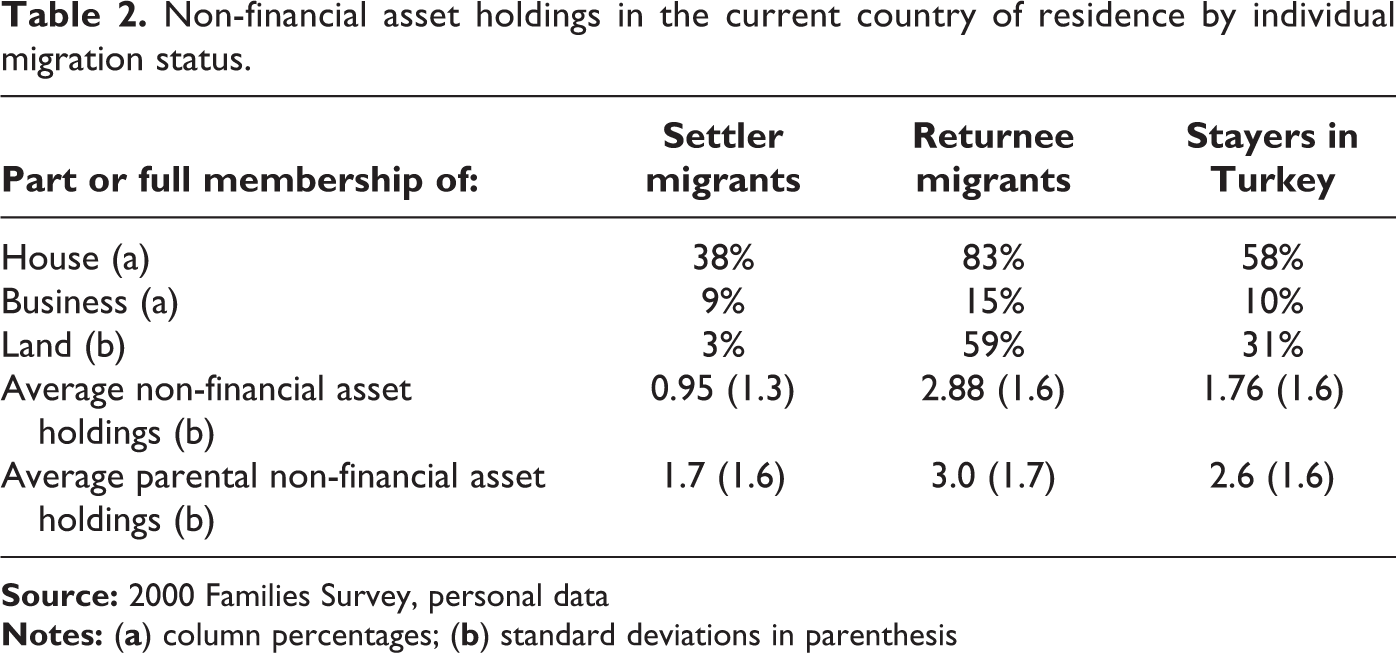

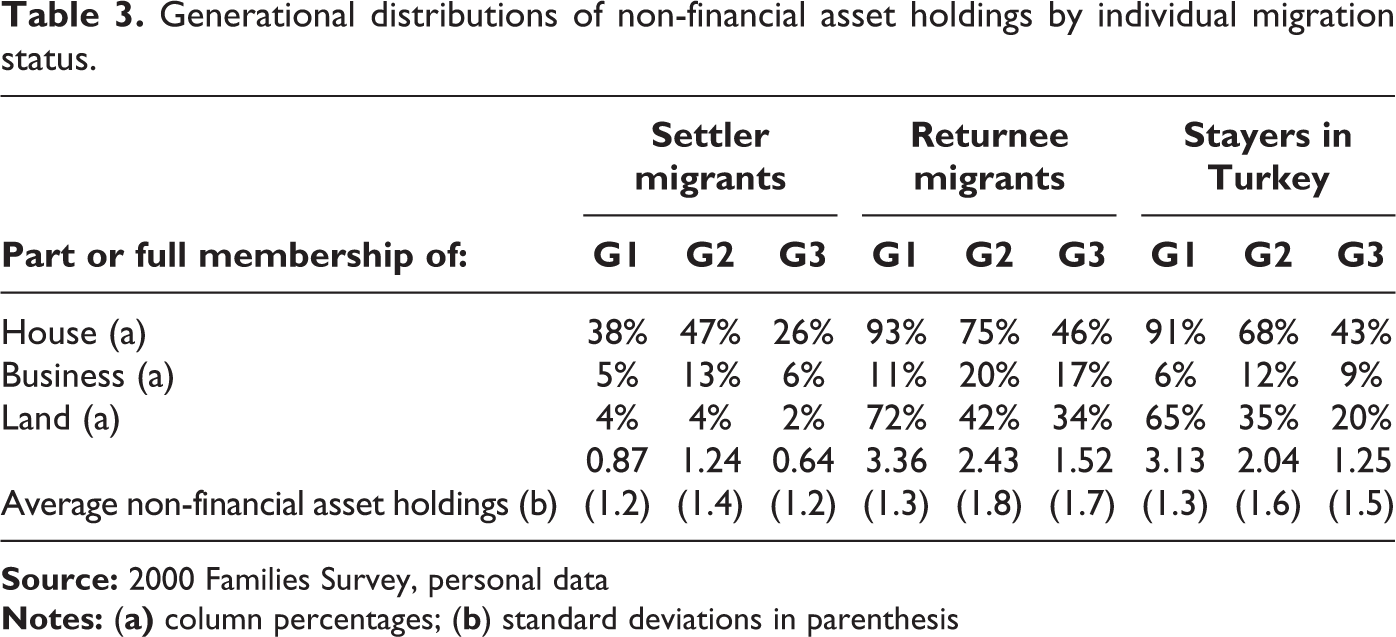

Table 2 demonstrates the distribution of the non-financial assets that settlers, returnees, and stayers invested in their country of residence. The distribution is broken down further by family generations in Table 3. From these tables, the following tendencies emerge as key. First, on average, the overall stocks of non-financial asset holdings were highest for returnees to Turkey and lowest for settlers in Europe. Second, settlers tended to possess the fewest assets across all types, with land being the least owned asset by this group, at 3 percent. Third, the second and third generations tended to own fewer assets than first-generation men across all groups, except for the second generation of settlers in Europe. The statistical significance of the observed tendencies is explored further.

Non-financial asset holdings in the current country of residence by individual migration status.

Generational distributions of non-financial asset holdings by individual migration status.

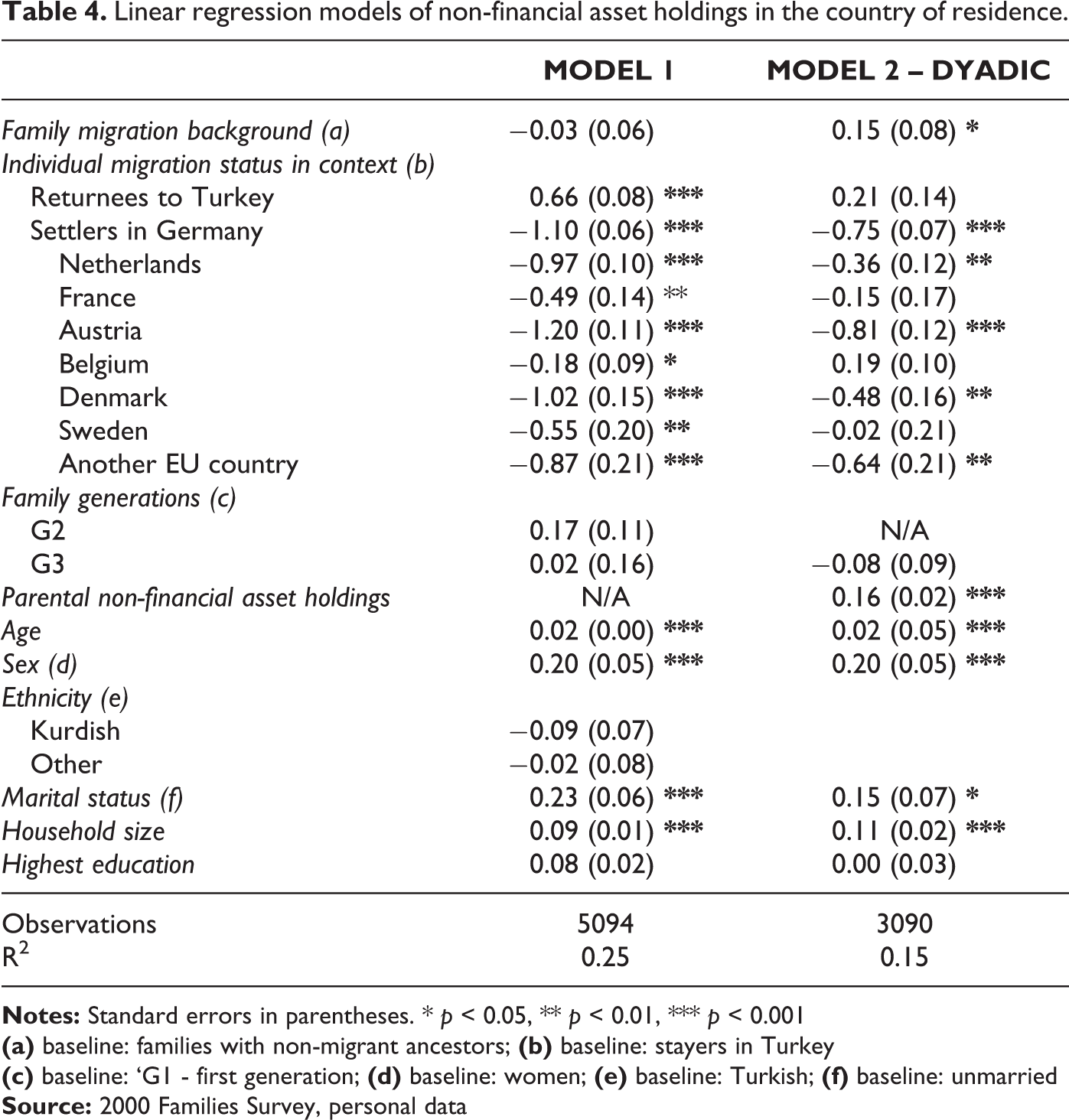

Table 4 presents the results obtained from the regression analyses. Starting with MODEL 1, it appears that family migration background, or having a migrant male ancestor in the family, bears no relationship to non-financial asset accumulation. The respondent’s own migration status, however, does. The results indicate a significant tendency for settlers across all destination countries to own fewer non-financial assets than their stayer counterparts, while the reverse is true for returnees. No significant differences emerge between family generations when age is controlled for. However, the auxiliary analyses performed separately for the three groups suggest that the second generation of settlers was significantly more likely than their first-generation counterparts to own non-financial assets in their country of residence [regression coefficients, standard errors and p-values for

Linear regression models of non-financial asset holdings in the country of residence.

Rather strikingly, MODEL 1 indicates no significant association with educational attainment. Auxiliary analyses carried out separately for settlers, returnees, and stayers, however, indicate some group differences in terms of education’s possible effects [regression coefficients, standard errors and p-values for

MODEL 2 demonstrates a positive, significant relationship between the non-financial asset holdings of parents and their own children across all three groups [

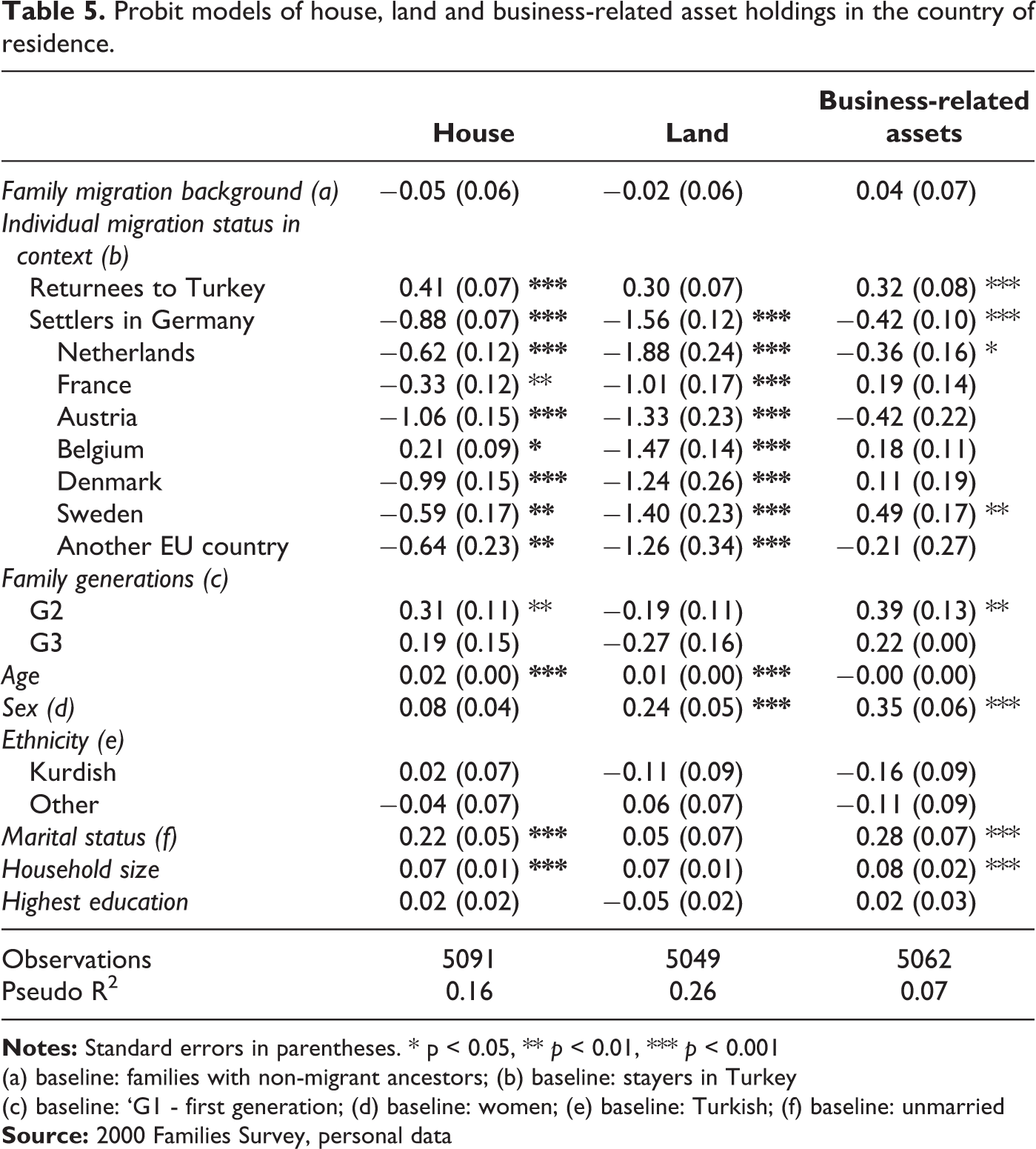

Results from the three probit analyses performed to disaggregate the non-financial asset accumulations of settlers, returnees, and their stayer counterparts are presented in Table 5. The analyses show that the type of non-financial asset owned does not depend significantly upon family migration background but, instead, on one’s own migration status. Return migrants displayed a significantly greater tendency than stayers to own a house, land, and business-related assets. Settler migrants across all destination countries comprised the group least likely to own land. Except for those based in Belgium, they also were less likely than stayers to own a house in European destinations where they resided. Generally speaking, observed differences between stayers and settlers in terms of ownership of business-related assets tended to be insignificant. The tendency for business-related asset ownership is, however, significantly higher for settlers in Sweden and lower for those based in Germany and the Netherlands. Finally, across the entire sample, the propensity for house and business-related asset ownership appears to be greater among members of the second generation. As is evident from Table 3, this trend is particularly applicable to settlers. Their returnee and stayer counterparts tended to possess more business-related assets than their ancestors, but the reverse remains true for house ownership.

Probit models of house, land and business-related asset holdings in the country of residence.

(a) baseline: families with non-migrant ancestors; (b) baseline: stayers in Turkey

(c) baseline: ‘G1 - first generation; (d) baseline: women; (e) baseline: Turkish; (f) baseline: unmarried

The Story: Making Sense of the Results

Mass migration from Turkey to Europe began when many Western European countries, including Germany, France, Belgium, Austria, and the Netherlands, made bi-lateral labor recruitment agreements with Turkey and with Eastern and Southern European countries to tackle the labor shortages they experienced in the aftermath of the Second World War (Akgündüz 2008). About one million people, mostly men, moved from Turkey to Europe between 1961 and 1974 to work in the mining, manufacturing, and construction, industries and they came to represent the largest guest-worker population in the continent (ibid.). The economic crisis in the mid-1970s brought the labor recruitment agreements to an end, yet migration flows from Turkey to Europe have continued to date for reasons ranging from family formation/unification to education, employment, and political asylum (Güveli et al. 2017). Today, approximately five million people with origins in Turkey are estimated to reside in Europe, spanning multiple destinations and generations (ibid.). This article captures a good portion of this Diaspora (i.e., the first goers, their migrant descendants, and descendants of “non-migrant” male ancestors who moved subsequently). However, not all men who moved from Turkey to Europe during guest-worker years stayed there. Some returned to Turkey to join the wives and children they left behind or to start anew while others came back, leaving their descendants in Europe.

Returnees in our analysis are shown to have made more non-financial investments in their country of residence (Turkey) than settlers and stayers across all generations and asset types. Since the net worth of their investments remains unknown, one cannot be certain as to whether they are the wealthiest. However, on average, they possessed the largest stock of assets, and, on this basis, they can be said to have benefited most from their migration decisions. They are likely to have taken advantage of the lower asset prices in Turkey and favorable currency conversion rates they obtained for their savings abroad. For returnees, the power of migrant money appears to have fundamentally altered the relationship between education and asset accumulation by enabling both the more and less educated members of this group to make non-financial investments in Turkey. Some may have increased their stocks through investments in the origin regions where asset prices tended to be considerably low. That said, there are stayers residing in the same regions, who owned fewer assets than returnees. Hence, this group’s economic successes can be attributed to migration, to a degree. Due to economic reasons being a dominant motive for migration (especially among guest workers), it remains highly likely that those who decided to leave their origins had fewer assets than stayers prior to migration. Migration processes and the power of migrant money can, hence, be suggested to have helped reverse such negative self-selection while diminishing the importance of educational attainment for returnees.

Among stayers, the less educated tended to have more assets, which can be attributed to the low house and land prices in the origin regions. However, this tendency, I argue, may also be reflective of the complex wealth distribution mechanisms operating in Turkey, altering the meritocratic relationship between educational attainment and asset accumulation. One such mechanism concerns the clientelist networks that allow people from different educational backgrounds to engage with the ruling party to benefit informally from state resources in exchange of political loyalty. This mechanism might well have enabled those stayers with allegiance to the ruling party to generate assets even if they occupied low positions in the educational scale.

The positive relationship between education and asset accumulation seems to have been maintained in the case of the settlers in Europe. Given that only 15 percent had a university degree or beyond and 68 percent had completed lower or higher secondary education, one might attribute the observed tendency for settlers to own fewer assets in almost all European countries to low educational attainment. While it is plausible to argue that most settlers were not educated enough to attain prestigious and well-paid jobs that allowed them to make sizeable investments in the destination country, the picture is more complex than it appears at first sight.

An exploration of why settlers were unable to attain high educational levels is beyond this article’s scope. However, it is worth mentioning the fairly weak relationship observed between their educational and occupational attainment levels (Pearson’s r = 0.40 p<000.1 between highest educational qualification and ISEI scores). These results imply that some highly educated settlers were unable to attain prestigious positions in the labor market but still managed to invest. One possible route is via self-employment in small, low-status yet profitable businesses in which settlers from all educational backgrounds were shown to engage to a significant extent possibly due to blocked opportunities in salaried parts of the labor market (Eroğlu 2018). So, highly educated settlers are likely to have been compelled to forego occupational prestige and become self-employed in low status businesses to be able to make money and accumulate assets. Another complementary explanation concerns the conditions prevalent within the local asset markets. It remains likely that settlers accumulated less than returnees and stayers in Turkey, due to their being more concentrated in areas where house and land prices are considerably higher and/or where certain assets such as land are particularly scarce.

Generationally speaking, differences observed in returnees’ and stayers’ non-financial investments are more connected with their age than with their position in the family genealogy. However, in the case of settlers, one can speak of a particularly significant generational effect. The first goers did not move to Europe with the intention to settle there; they were mostly sojourners, motivated to make money and return to their origin country (Akgündüz 2008; Berger and Mohr 1975/2010). Thus, until they were granted residency rights in Europe, this group of migrants was unlikely to have directed their investments to the destination country and would have instead focused their investments on Turkey. Subsequent generations, especially descendants of first-generation settlers, were, however, not sojourners; they were European residents possibly more connected to the destination country, which could be one reason they were less inclined to invest in Turkey. Settlers’ asset holdings in Turkey and Europe will be compared in future work, but this explanation is supported by auxiliary analyses that demonstrate a greater tendency for the first generation of settlers than their second- and third-generation counterparts to hold non-financial assets in Turkey (Mean non-financial assets in Turkey for settlers from

The second generation of settlers appear more inclined than their first-generation counterparts to own house or business-related assets in the country of residence. The aforementioned reasons may partly be responsible for this tendency; however, the high level of business-related asset ownership among the second generation can be attributed to the unfavorable economic climate in which they found themselves after the end of guest-worker agreements in the mid-1970s. Unlike first-generation men for whom opportunities to work in manufacturing, mining, or construction sectors were in abundance, the second generation possibly faced more blockages in the salaried parts of the labor market, due to increased unemployment and/or discrimination, and turned to business in greater numbers to circumvent such barriers (see also Güveli et al. 2015; Eroğlu 2018).

However, across all groups, the children of asset-rich parents tended to be the ones who accumulated more. The precise nature of the direct transfers from parents to children remains unknown, but it can take various forms, from the purchase or transfer of actual asset/s and monetary contribution toward their own children’s education to asset purchases or business ventures. Whatever form they take, parental transfers appear to enable both migrant and stayer children to build up their asset stocks. However, considering settlers’ tendency to accumulate less in Europe, their descendants who (plan to) remain there are least likely to benefit from such transfers.

Conclusion

This article has drawn unique comparisons across three family generations of migrants and stayers to shed light upon the little-explored relationship between international migration and asset accumulation. By investigating the non-financial investments of settler and return migrants spread across multiple generations and destinations with their counterparts who did not leave their origins, it provided a new insight into the economic dis/benefits of the migration process for migrants and their descendants.

The research findings demonstrated that regardless of their position in the family genealogy, returnees benefited the most from the migration process as far as their non-financial investment in the country of residence were concerned. Benefits for settlers, however, proved to be less straightforward. Their current holdings in Europe might be greater than they would have been if they had remained in Turkey, but on average, they were able to accumulate fewer assets than returnees and stayers. Since the net worth of their current accumulations remains unknown, it is not possible to reach a firm conclusion about their wealth status. Their assets may be more valuable, and if one day they decide to move (back) to Turkey, like returnees, they might be able to convert them into a larger stock of assets and take advantage of favorable currency rates and/or lower asset prices. However, these people are currently residing in Europe, and most may well continue to do so. In this case, settlers will have fewer transferable assets that are of real use and exchange value within the European context in which they operate. They will have fewer house and land-type assets to transfer as stayers. The land-type assets owned by stayers in the origin regions might be low in value, but house ownership is undoubtedly of significant use, if not exchange value, regardless of the context. Considering the significance of intergenerational family transfers for asset accumulation, settlers’ reduced tendency to make non-financial investments in their country of residence is particularly likely to disadvantage their descendants planning to remain in Europe.

Additionally, returnees were shown to owe their economic success not so much to their educational achievements but to their migration decisions and the power of migrant money. Better-educated settlers in Europe were found to have accumulated more, but not necessarily by attaining prestigious positions in the labor market. Self-employment in small, low-status business was suggested to have contributed to some degree toward enhancing the non-financial assets held in the destination countries by subsequent generations of settlers. Hence, the slight improvement in their asset status cannot readily be taken as evidence of their successful integration into the destination societies.

Overall, this article showed that while the great majority of migrants and their descendants had a shared migration history and ancestry connecting them to the guest-worker movement that has made a substantial contribution to the rebuilding of Europe, they were unable to share in the economic benefits of their (ancestors’) migration to the European Continent. The process proved to be least beneficial for settlers in Europe, who were found less able to make non-financial investments than their returnee and stayer counterparts currently living in Turkey. A major implication of these findings for the wider study of international migration is that the rosy picture painted by the assimilation theorists does not reflect the reality of migrants who moved from Turkey and are now living in various destinations in Europe, spanning multiple family generations. Their reality seems better represented by the segmented assimilation theory, emphasizing the role of structural influences (e.g., labor and asset market conditions and public hostility toward migrants) in constraining the economic performance of migrants and their descendants.

Like all research, this article is not without limitations, particularly vis-à-vis the 2000 Families Survey’s scope (see Güveli et al. 2017 for further discussion of the Survey’s strengths and weaknesses). First, results are not representative of the entire Turkish Diaspora in Europe because of the Survey’s specific focus on labor migration from Turkey to Europe between 1961 and 1974. The Survey was not designed to represent all Turkish migrants from this period but rather, to reflect their typical features through a careful selection of the regional origins of migration. Second, due to data constraints, the analyses had to be restricted to non-financial investments in the country of residence, potentially biasing results against settlers. Considering the propensity for first-generation settlers to invest more in the origin country than their second- and third-generation counterparts, this group of settlers might have fared better if their investments in Turkey and Europe had been jointly covered. Third, for reasons of data unavailability, it was not possible to capture respondents’ financial assets (i.e., savings) or to estimate their total wealth (i.e., net worth of financial and non-financial assets minus outstanding debts). Hence, it remains inconclusive as to whether those with greater stocks of non-financial assets were wealthier than those who owned fewer assets. Also, the lack of coverage of financial investments made it impossible to explore whether certain groups had a propensity for investing more in tangible than in intangible assets (or vice versa) and thereby, to provide a better representation of their asset status. Finally, some aspects of the resource-based framework and their potential effects on asset accumulation (e.g., social capital and local contextual factors such as asset market conditions) went unaccounted for either because of data limitations or because of the survey’s cross-sectional nature.

This article, thus, leaves a number of questions for future exploration. A more detailed inquiry is needed to explain the observed tendency for settlers to own fewer non-financial assets in Europe. A related question concerns migrants’ choice of country for their investments. Are settlers more likely to invest in Turkey or in Europe? Are there significant generational differences in settlers’ country choice, and if so, why? The 2000 Families Survey allows an exploration of these questions through a focus on their non-financial investments, as is explored in future work.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the NORFACE, New Opportunities for Research Funding Agency Co-operation in Europe, under the grant number 235548.