Abstract

Recognizing crude oil’s pivotal economic role, this study investigates the complex interdependencies between the crude oil market and the markets for its refined products: gasoline, kerosene-type jet fuel, and heating oil, addressing a gap in existing literature that largely focuses on price dynamics without considering broader market interactions. Utilizing an advanced Global Vector Autoregressive (GVAR) model, a known model from international economics, and analyzing monthly data from 2005 to 2019, our research examines production, stocks, consumption, and pricing linkages across these sectors. Findings highlight the significant impact of crude oil price fluctuations on refined product markets and identify a notable interrelation between kerosene and heating oil markets. Conversely, the influence of refined products on crude oil is limited, highlighting the dominant role of crude oil in the energy markets. Overall, our analysis reveal the interdependencies between refined petroleum product markets, besides the pronounced impact of crude oil on energy markets.

1. Introduction

Crude oil plays a pivotal role in the global economy, primarily acting as the main raw material in the production of gasoline, kerosene-type jet fuel, and heating oil. The interplay between crude oil and their refined counterparts underscores a complex relationship. Production shocks in crude oil, as for example the OPEC oil embargo of 1973 to 1974, the Iranian revolution of 1978 to 1979, the Iran-Iraq War initiated in 1980, the first Persian Gulf War in 1990 to 1991, and the oil price spike of 2007 to 2008, have severe impacts on its price and ultimately on its refined products, especially on their availability and their prices, see for example Gajdzik et al. (2024), Hamilton (2013), and Q. Zhang et al. (2024). In contrast, Baumeister et al. (2018) state “demand for crude oil derives from the demand for refined products such as gasoline or heating oil,” therefore, demand fluctuations predominantly impact refined petroleum product markets and finally crude oil. For example, the outbreak of the COVID-19 pandemic caused ultimately negative futures prices in WTI crude oil. The complex relationship between crude oil and refined petroleum products emphasizes the importance of disentangling the spillover effects across these markets, as highlighted by Liu and Ma (2014).

Theoretically, the prices of refined petroleum products are closely linked to crude oil prices, as crude oil is a large component in their production costs, as noted by Karali and Ramirez (2014). Empirically, studies by Asche et al. (2003), Gjolberg and Johnsen (1999), Lahiani et al. (2017), and Serletis (1994) identify long-term price relationships between crude oil and its refined petroleum products. Meanwhile, research by Baruník et al. (2015), Chatziantoniou et al. (2022), Karali and Ramirez (2014), and Mensi et al. (2021) focuses on the spillover effects across energy prices. Yet, these investigations primarily focus on price interactions, paying less attention to the interplay of production, inventory levels, and consumption patterns.

Kilian (2010) acknowledges that disruptions in crude oil supply, variations in demand for specific products, or refinery outages not only impact crude oil but also affect the pricing of refined petroleum products. Following this, research by Ederington et al. (2021), Kaufmann et al. (2009), and Kilian (2010) investigates how shocks in the crude oil market affect the gasoline and heating oil markets. While these investigations provide valuable insights, they predominantly focus on the effects of crude oil market shocks on refined petroleum products, without thoroughly considering the reverse relationship—how disturbances in refined product markets might influence crude oil prices. Although Kilian (2010) explicitly models such feedback, this is limited to gasoline prices.

Our study aims to bridge this gap by examining the complex interdependencies not only from crude oil to refined products but also assessing how shocks within the refined product markets, like gasoline, kerosene-type jet fuel, and heating oil, feedback into the crude oil market. This comprehensive approach enables a deeper understanding of the bidirectional influences shaping the dynamics between crude oil and its derivatives. In addition, we investigate the interrelations among the refined petroleum product markets themselves. We introduce a novel framework tailored to the dynamics of energy markets. Specifically, we refine the Global Vector Autoregressive (GVAR) model, a methodology originally conceived for economic analysis by Pesaran et al. (2004) to reduce the dimensionality in vector autoregressions by linking country-specific VARs, and subsequently modified for application within commodity markets by Schischke et al. (2024). In particular, the GVAR model allows a statistical feasible analysis of interdependencies despite limited data availability. This approach enables us to intricately model the multifaceted interrelations among production, inventory levels, consumption patterns, and pricing mechanisms prevalent in the energy sector. Furthermore, this methodology provides a comprehensive understanding of market dynamics, while controlling for the relation between energy commodities and the economy.

In particular, we apply the GVAR model to examine the energy markets for crude oil, gasoline, kerosene-type jet fuel, and heating oil, employing monthly data spanning from 2005 to 2019. Hereby, this study innovatively assigns weights to link individual commodity markets, reflecting the proportions of energy commodities derived from crude oil during the refining process. Additionally, consistent with established literature, our model includes economic growth, foreign exchange rates, and interest rates to account for the economic interdependencies affecting energy markets, see among others, Karali and Ramirez (2014).

Overall, this study provides an in-depth analysis of the intricate interplay between the crude oil market and the markets for refined petroleum products, including gasoline, kerosene, and heating oil. We uncover and detail the significant influence that fluctuations in crude oil prices exert on the dynamics of these refined product markets, particularly impacting their inventory levels and production rates. Surprisingly, our findings indicate that the crude oil market itself shows relatively limited sensitivity to changes within the refined product sectors. However, our research highlights a notably strong interrelation between the kerosene and heating oil markets, suggesting a shared market behavior, which might be explained by the fact that refiners typically possess the operational flexibility to adjust kerosene production in response to market demand, which in turn reduces the yield of heating oil. Through this investigation, we shed light on the complex mechanisms driving these energy markets and reveal the pronounced impact of crude oil on the refined petroleum product markets.

The remainder of this paper is organized as follows: Section 2 reviews the relevant literature on energy market dynamics. Section 3 details our methodological framework, while Sections 4 and 5 present the empirical analysis and findings, respectively. Finally, Section 6 offers conclusions and outlines avenues for future research.

2. Literature Review

The interplay between crude oil prices and refined petroleum product prices is foundational to understanding global energy dynamics, as crude oil significantly influences the production costs of its refined products, see Karali and Ramirez (2014). While the literature extensively examines the relationship between crude oil and natural gas markets, 1 as well as regional price variations 2 and separate price volatilities, 3 few studies delve into the nuanced connections across different petroleum products. However, crude oil and their refined petroleum products are closely linked. On the one hand, the outbreak of the COVID-19 pandemic for example revealed that demand fluctuations predominantly impact refined petroleum product markets which ultimately affect the crude oil price. On the other hand, production shocks in crude oil, as for example the OPEC oil embargo of 1973 to 1974, the Iranian revolution of 1978 to 1979, the Iran-Iraq War initiated in 1980, the first Persian Gulf War in 1990 to 1991, and the oil price spike of 2007 to 2008, reveal the impact of supply shocks in crude oil on its price and ultimately on the refined petroleum products markets, see for example Gajdzik et al. (2024), Hamilton (2013), and Q. Zhang et al. (2024).

Studies such as Asche et al. (2003), Gjolberg and Johnsen (1999), and Serletis (1994) have established long-term cointegration between crude oil price and major refined product prices like gasoline and heating oil, signaling underlying structural relationships. Similarly, Lahiani et al. (2017) highlight long-term linkages across a broader spectrum of energy prices, additional including diesel. These findings suggest a deeply interconnected energy market, where crude oil acts as a pivotal element.

Advancements in analytical techniques also have shed light on the dynamic spillover effects between energy markets. Hereby, several studies have employed various forms of vector autoregressive (VAR) models. While Rahman (2016) reveals changes in the oil price are associated with changes in gasoline price, Han et al. (2015) investigate the interdependencies between crude oil and gasoline spot and futures prices and observe significant spillover effects in both directions for the spot prices, whereas only the gasoline futures price is affected by the crude oil futures price. Moreover, Baumeister et al. (2017) compare several real-time forecasting models for the US retail price of gasoline and identify that the simple bivariate VAR model, reflecting the relation between retail gasoline and Brent crude oil prices, is the most accurate individual model, however, a pooled forecast yields more accurate results than individual models or traditional no-change forecasts. In addition, Baumeister et al. (2018) deduce that product spreads, which represent the difference between refined product prices and crude oil prices, can enhance the accuracy of oil price forecasts. Specifically, models incorporating gasoline spot price spreads demonstrate a significant improvement in forecast precision, particularly for horizons extending up to two years. Furthermore, Kilian and Zhou (2023) analyze the extent to which prices of diesel fuel, jet fuel, natural gas and electricity create inflationary pressures.

Furthermore, several studies have adopted the Diebold-Yilmaz spillover framework. While Baruník et al. (2015) detect strong spillover effects in crude oil, gasoline, and heating oil prices, however, neither energy commodity is found to dominate the others in terms of general spillover transmission. Tiwari et al. (2023) also confirm a high level of volatility spillover among crude oil and petroleum products, whereas they detect heating oil as the highest contributor to others. In contrast, Mensi et al. (2021) conclude in their study that crude oil mainly causes the volatility spillovers in the other markets, whereas the gas oil, gasoline, heating oil, and natural gas markets receive the risks. Using a time-varying approach, Chatziantoniou et al. (2022) aims to uncover the intricate spillover dynamics between crude oil and refined products. Their analysis reveals that heating oil and kerosene are consistent net transmitters of shocks, while gasoline and propane predominantly receive these impacts. Using a GARCH-BEKK model, Karali and Ramirez (2014) analyze the time-varying volatility and spillover effects in crude oil, heating oil, and natural gas futures markets while controlling for exogenous factors and detect significant effects between the prices. Overall, these studies shed light on the complex dynamics characterizing interactions within energy prices. This complexity emphasizes the importance of meticulously examining the ways in which various commodity prices affect each other within the energy sector.

Despite these insights, the reverse causality—specifically, how shocks in refined product markets influence crude oil—remains underexplored. While studies such as those by Ederington et al. (2021), Kaufmann et al. (2009), and Kilian (2010) have delved into the effects of crude oil market shocks on refined products, they predominantly focus on analyzing the supply and demand shocks in the crude oil market and their subsequent impact on refined product markets. Kaufmann et al. (2009) thoroughly examine how crude oil price shocks affect inventory behaviors, refinery utilization rates and the price of motor gasoline. Similarly, Kilian (2010) explores the relationships between the crude oil and gasoline markets, noting a limited impact of crude oil supply shocks on gasoline prices and consumption. Instead, he finds that the gasoline market is more significantly influenced by oil-market specific demand shocks, and especially from the global demand for crude oil. In addition, he explicitly models a feedback from gasoline prices to the crude oil market. Building upon Kilian’s framework, Ederington et al. (2021) investigate the direction of Granger causality between crude oil, gasoline, and heating oil markets. They discover evidence of causality flowing from crude oil prices to refined product prices and, notably, from gasoline prices to oil prices in the period subsequent to 2005. This suggests a bidirectional relationship, where not only do crude oil price shocks affect refined product markets, but changes in refined product markets, particularly gasoline, can also influence crude oil prices. However, the extent and mechanisms of these reverse effects, especially the impact of demand shocks from refined products on the crude oil market, its price but also its production, are not fully understood. This gap in the literature presents a significant opportunity for further research, aiming to elucidate the complexities of these bidirectional influences and their implications for energy market dynamics.

In summary, while existing research confirms the interconnectedness and spillover effects between crude oil and refined product prices or spillover effects from the crude oil market to refined product markets, the reverse dynamics, the relations between the refined product markets themselves and the broader implications of these relationships warrant deeper investigation. Our study aims to bridge this gap by examining both directions of influence, thereby contributing to a more comprehensive understanding of global energy market dynamics.

3. Methodology

The objective of this study is to explore the intricate interdependencies within energy markets, focusing on how crude oil production impacts refined product markets and how consumption shocks in refined products influence the crude oil market. Beyond analyzing price dynamics, the study incorporates production volumes, inventory levels, and consumption patterns to provide a comprehensive perspective. To ensure statistical rigor, we utilize the global vector autoregressive (GVAR) model, originally developed by Pesaran et al. (2004) for economic analysis and later refined by Schischke et al. (2024) for commodity markets.

The GVAR model facilitates a detailed examination of individual commodity markets while accounting for their interconnections. Overall, we first model each commodity market separately, considering the interrelations between production, inventory levels, consumption and price, while taking into account the potential impact of the economy on the commodity market. By including the dependencies between the different commodity markets, spillover effects among crude oil and its refined product markets can be analyzed. Additionally, we introduce enhancements to the GVAR framework to more accurately reflect the economy’s role in shaping energy market dynamics, addressing the critical interplay between economic activity and the energy sector. This comprehensive methodology provides robust insights into the mechanisms driving energy market behavior.

In a first step, we model each commodity market separately. Thereby, we aim to reflect the multifaceted interrelations among production, inventory levels, consumption patterns, and pricing mechanisms. In particular, we model for each commodity

where

As energy markets and the economy are interrelated themselves, we do not assume exogeneity of the macroeconomic variables, in contrast to the study of Schischke et al. (2024), investigating metal markets. Therefore, we also need to model the economy, which will allow us to cover all energy markets as well as the economy in the final global model. In particular, we model the economy dependent on the energy markets by the following vector autoregressive model:

where

In addition, we assume the

Based on these individual vector autoregression models, the final GVAR model can be derived with basic matrix calculus, as all markets are linked via the weight matrices. Therefore, we define the

where

In addition, we define the

where

Subsequently, we define the

with the

Overall, the GVAR model provides a comprehensive framework for simultaneously modeling individual energy markets and the broader economy, capturing the nuanced interdependencies between these commodities and economic dynamics. To dissect the spillover effects within and across these markets, we employ generalized impulse response functions (GIRFs), as initially introduced by Koop et al. (1996). This approach, which aligns with the methodologies of Pesaran et al. (2004) and Schischke et al. (2024), offers the advantage of not necessitating a predefined order among the variables. It enables us to disentangle effects of a one standard deviation shock in a given variable across the network, particularly highlighting its impact on other energy markets, see Schischke et al. (2024) for more detailed information. Further, our analysis extends to the generalized forecast error variance decomposition (GFEVD), shedding light on the proportion of forecast error variance in each variable attributable to exogenous shocks in the others.

4. Data

The data used in this study comprises time series information for the energy markets, macroeconomic variables, and linkage parameters essential for integrating the individual market models into a cohesive global energy framework. Specifically, we examine the interconnectedness of energy markets, focusing on crude oil, and its refined products gasoline, kerosene-type jet fuel, and heating oil. Hereby, we utilize monthly data from the United States spanning from 2005 to 2019 to analyze these interdependencies, explicitly excluding the turbulent periods associated with the COVID-19 pandemic and the Russo-Ukrainian conflict. Each market is modeled through individual VAR models, consisting of key commodity-specific variables such as production volume, inventory levels, consumption (approximated by the product supplied data), 7 and price, all of which are sourced from U.S. Energy Information Administration (2023). Our analysis particularly emphasizes spot prices, given their direct correlation with physical delivery, as highlighted by Zavaleta et al. (2015). For crude oil, we consider the average domestic prices in the United States, as indicated by PADD prices, a reflection of the market’s regional diversity, see U.S. Energy Information Administration (2023). 8 Recognizing the profound linkage between energy markets and the broader economy—a relationship well-documented in the literature, for example by Ben Salem et al. (2024) and Karali and Ramirez (2014)—our model also integrates economic indicators. These include U.S. industrial production as a measure of economic growth, the dollar index to account for foreign exchange rate fluctuations, and the federal funds rate for interest rate trends. Data for these economic variables are sourced from the Board of Governors of the Federal Reserve System (U.S.) (2022b), ICE Futures U.S. (2022), and Board of Governors of the Federal Reserve System (U.S.) (2022a), ensuring a comprehensive analysis that accounts for both commodity-specific attributes and macroeconomic influences.

We apply the augmented Dickey Fuller (ADF) test to each of the variables to ascertain their stationarity, a crucial prerequisite for the validity of VAR models. Given that all time series initially exhibited non-stationarity, we proceeded to compute logarithmic returns, transforming the data into a stationary format. Given the seasonal fluctuations in energy prices, particularly those of heating oil, we seasonally adjust and normalize the logarithmic return data, ensuring a mean of zero and a standard deviation of one. The descriptive statistics for these transformed, seasonally adjusted, yet unnormalized variables are detailed in Table A1 within Appendix A.

To cohesively integrate the individual energy markets with the broader economic framework in our model, we employ a novel approach to connect these markets. Rather than utilizing trade weights as originally suggested by Pesaran et al. (2004) for linking economies, we assign weights according to the production ratios of energy commodities that are obtained from crude oil through the refining process. This method, informed by data from U.S. Energy Information Administration (2023), allows for a more accurate representation of the interrelations within the energy sector. A weighting scheme was constructed based on refined product production ratios, displayed in Table 1, based on data from U.S. Energy Information Administration (2023). Crude oil was initially assigned a unitary value. The weight associated with each individual commodity was calculated by setting its own value to zero, effectively isolating the contribution of the other commodities. The weights were then calculated by normalizing the remaining production ratios so that they summed to one. To illustrate the weighting procedure, we provide an example focusing on the calculation of the weights that represent the influence of gasoline, kerosene-type jet fuel, and heating oil on the crude oil market. For this specific calculation, the weights of crude oil itself and all other petroleum products not considered in this analysis are set to zero. The production ratios of gasoline (0.45), kerosene-type jet fuel (0.09), and heating oil (0.25), see Table 1, are then normalized to sum to one, preventing any commodity to be multiple counted or underestimated. This normalization results in final weights of 0.57, 0.11, and 0.32, respectively, reflecting the greater production volume of gasoline.

Production Ratios of Energy Commodities.

Note. The table reports the production ratios of energy commodities that are obtained from crude oil through the refining process, whereby crude oil, the fundamental input for all refined products, was assigned a unitary value.

Additionally, we posit that the crude oil market exclusively influences the economy, attributing a weight of one to crude oil and zero to the refined products to signify the paramount impact of crude oil. This assumption underlines the pivotal role of crude oil, suggesting that while other energy markets may affect the crude oil market, they do not directly instigate changes in the broader economy.

5. Empirical Results

The objective of this study is to disentangle the complex interdependencies between crude oil and refined product markets, shedding light on the dynamics that underpin these crucial segments of the energy sector. Therefore, our analysis initially focuses on examining the spillover effects between various energy markets, as detailed in Section 5.1. This investigation lays the groundwork for understanding the directional flows of shocks and their effects across the markets. Subsequently, the forecast error variance decomposition provides us further insights. Particularly, this analysis, detailed in Section 5.2, enriches our understanding by quantifying the relative impacts of specific shocks on market fluctuations. Together, these sections constitute a comprehensive examination of the interplay between crude oil and refined products, offering new insights into their interconnectedness.

5.1. Spillover Effects in the Energy Markets

First of all, we consider the spillover effects within and across the energy markets, employing the GVAR model as outlined in equation (5). This model is applied to the energy sectors of crude oil, gasoline, kerosene-type jet fuel, and heating oil, capturing their dynamics through their variables stocks volume, production volume, price, and consumption, while also incorporating the influence of macroeconomic factors. 9 These factors include the U.S. industrial production (IP), the U.S. dollar index (FX), and the federal funds rate (FFR), which are integrated into the model as weakly exogenous variables.

Through the use of generalized impulse response functions (GIRFs), following the methodology of Pesaran et al. (2004) and Schischke et al. (2024), we reveal the reactions of these energy markets to shocks in specific variables. The GIRFs reveal both the direct and indirect effects of a one standard deviation innovation in any given variable, see Dées et al. (2007). Inference is based following Kilian (2009) by applying the recursive-design wild bootstrap with 1,000 replications of Gonçalves and Kilian (2004). This approach is noted for its robustness, remaining valid even under conditions of conditional heteroscedasticity, which is crucial for the integrity of our inference. To construct our confidence intervals, we employ the one- and two-standard error bands around our point estimates. These bands represent the 68% and 90% confidence levels, respectively, as our residuals are normally distributed. Despite the cautionary notes from Runkle (1987) and Lütkepohl (1990) regarding the potential for impulse responses to generate false negatives, our analysis uncovers significant interactions within and between the energy markets.

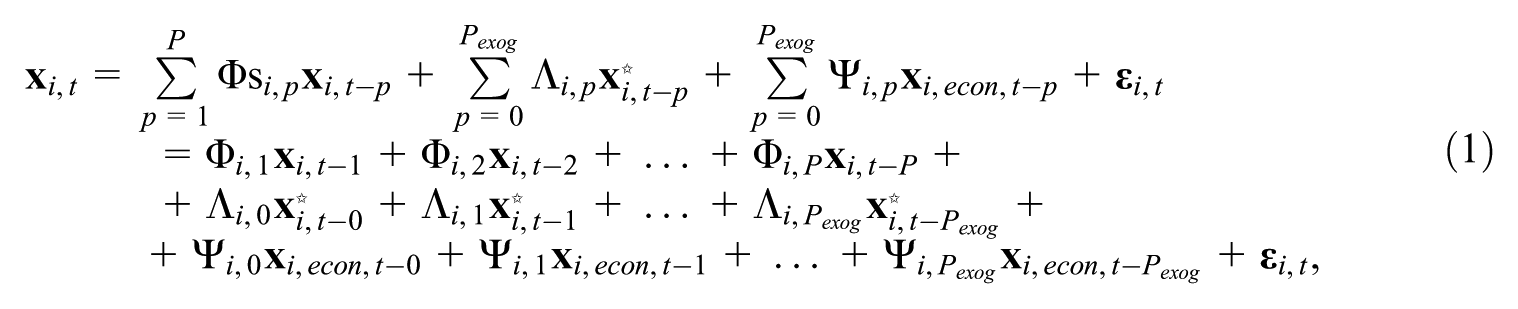

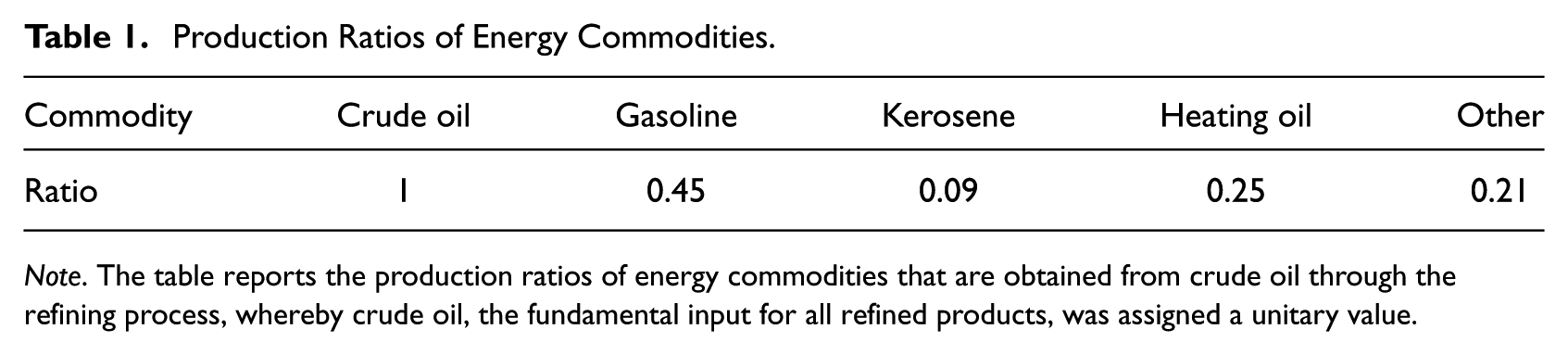

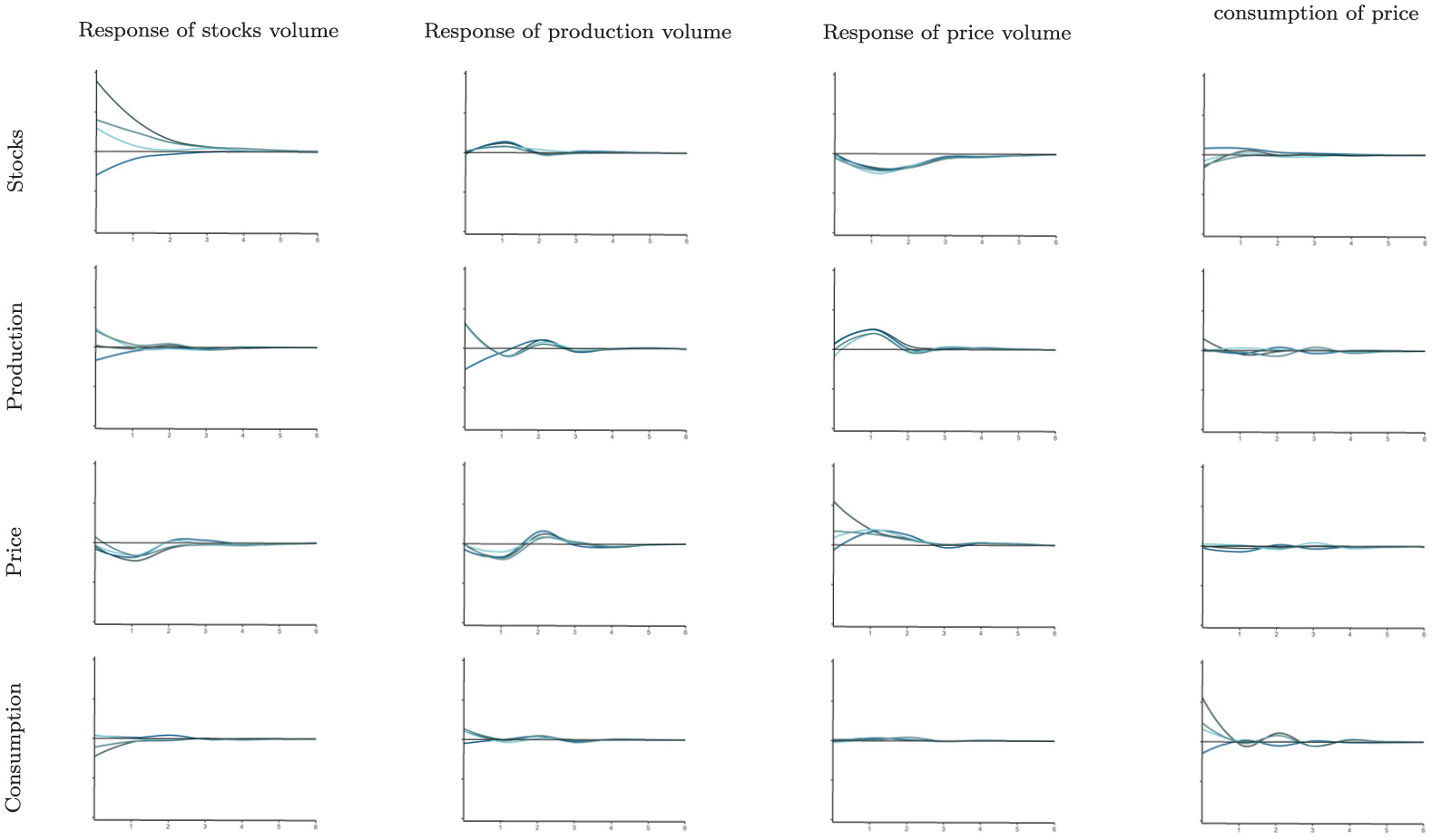

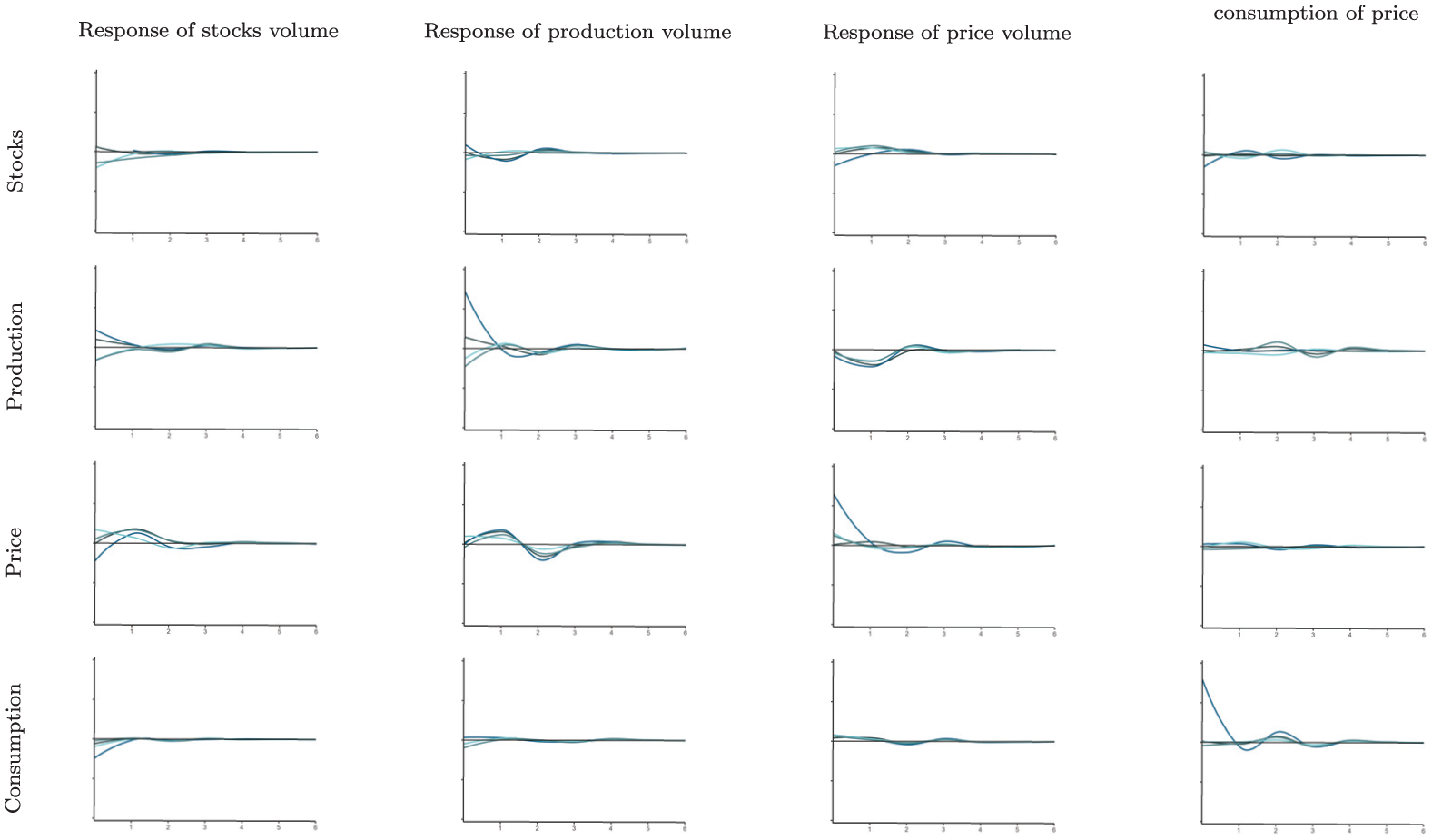

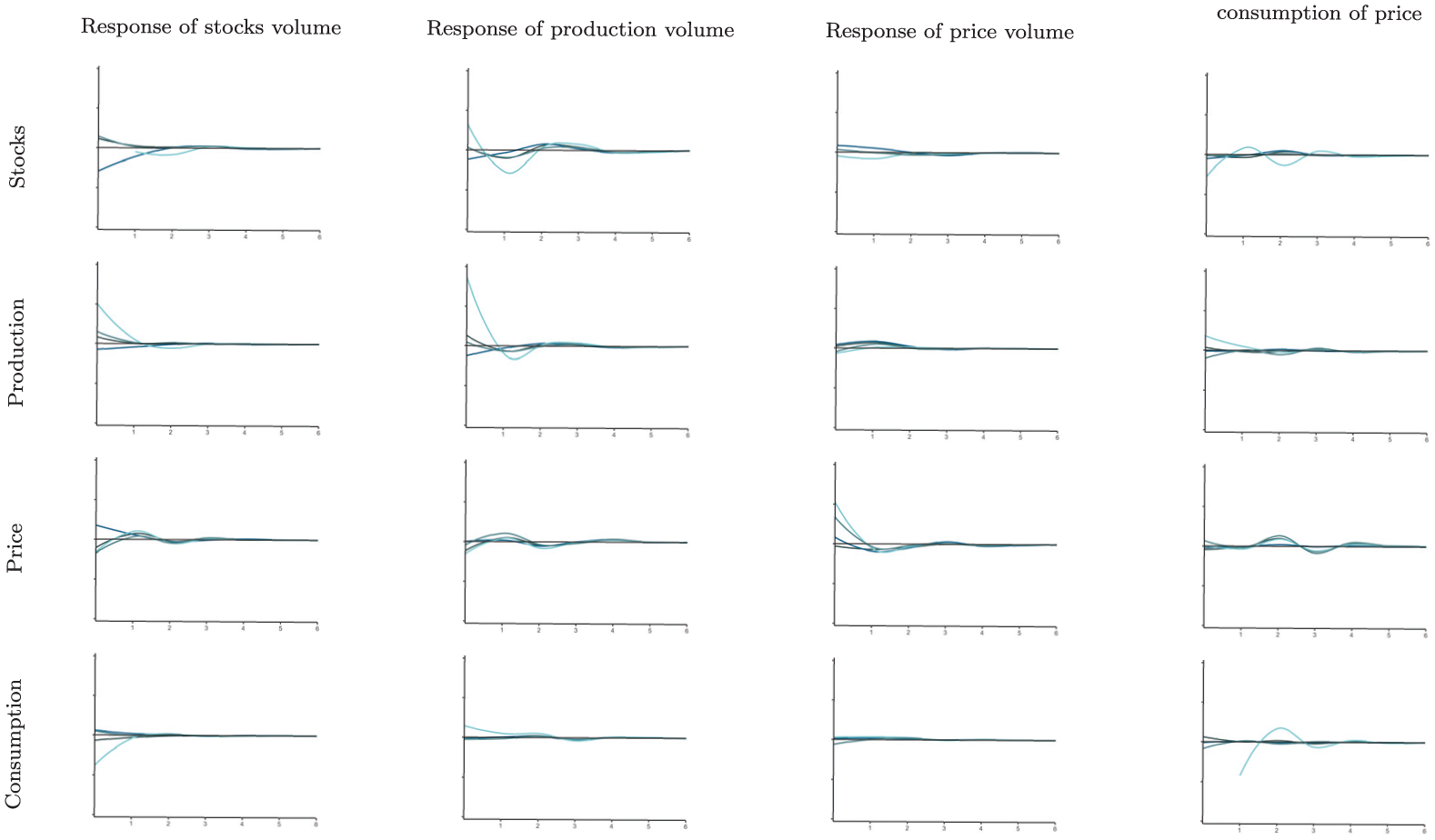

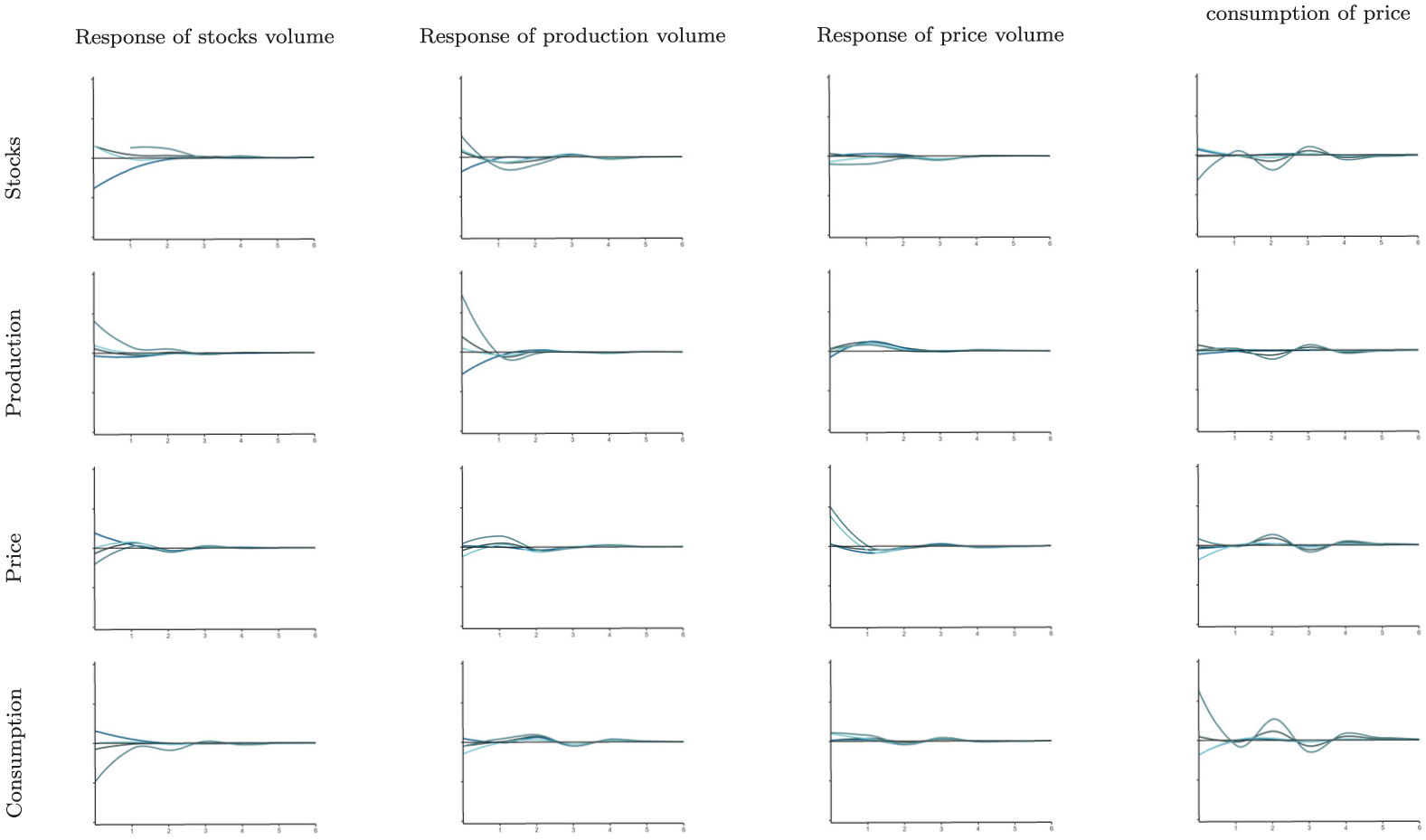

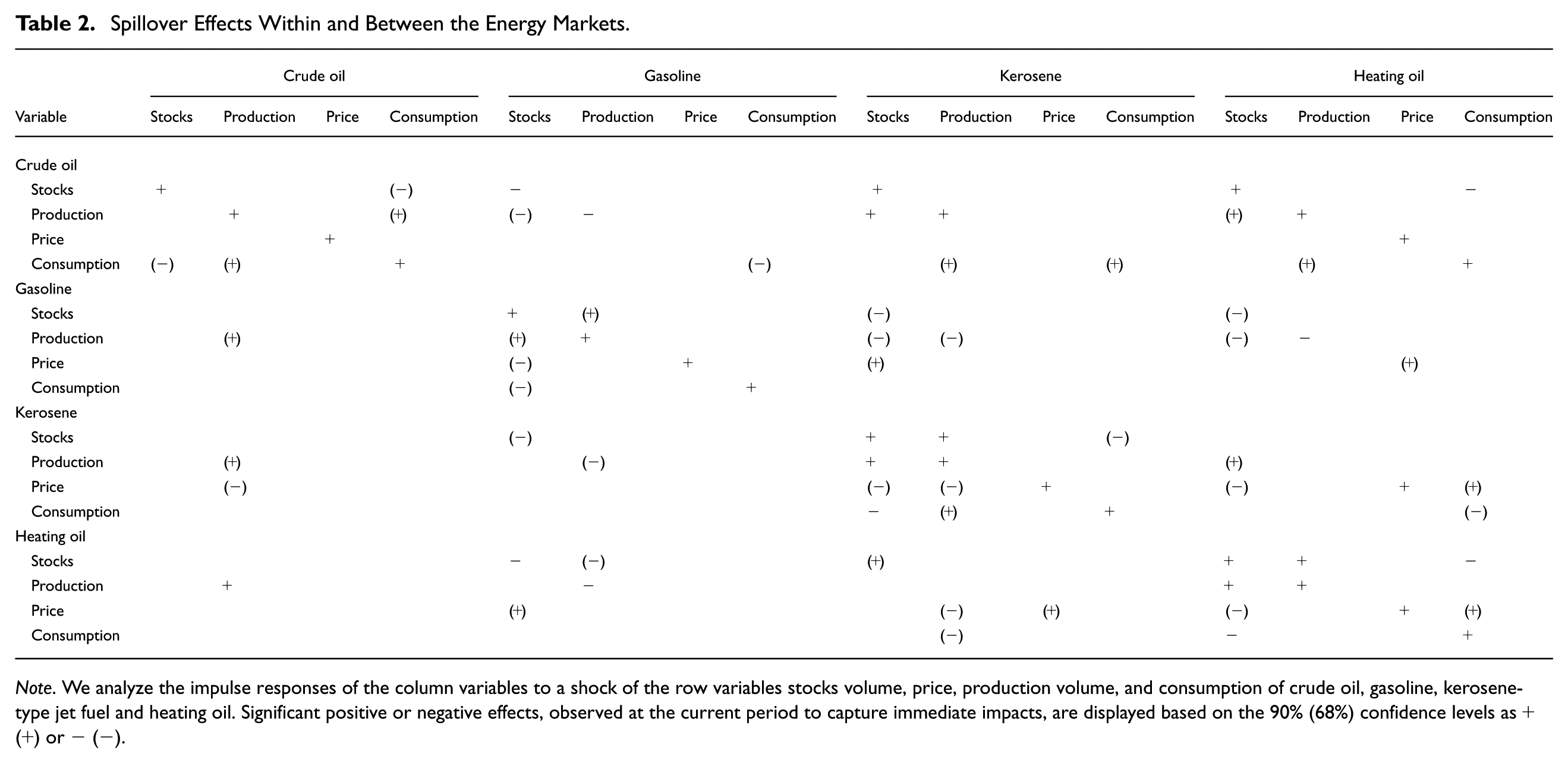

The resultant impulse responses, projected over a six-month horizon, are illustrated in Figures 1 to 4, corresponding to shocks in crude oil, gasoline, kerosene-type jet fuel, and heating oil markets, respectively. To synthesize these findings, Table 2 consolidates the data, presenting a comprehensive overview. Specifically, it denotes significant positive or negative responses of column variables to a shock in the row variables, indicated by a (+) or (−), respectively. While the diagonal of Table 2 shows unsurprisingly significant results, as it captures the effect of a shock to the response variable itself, we obtain numerous significant GIRFs in the cross-commodity dimension, underlining the energy markets are interrelated.

Impulse response functions for a crude oil shock.

Impulse response functions for a gasoline shock.

Impulse response functions for a kerosene shock.

Impulse response functions for a heating oil shock.

Spillover Effects Within and Between the Energy Markets.

Note. We analyze the impulse responses of the column variables to a shock of the row variables stocks volume, price, production volume, and consumption of crude oil, gasoline, kerosene-type jet fuel and heating oil. Significant positive or negative effects, observed at the current period to capture immediate impacts, are displayed based on the 90% (68%) confidence levels as + (+) or − (−).

To start, we examine the spillover effects within the individual commodity markets, before we focus on the effects in the cross-commodity dimension. In particular, the analysis of the crude oil market reveals an inverse relationship between stock levels and consumption as well as a positive correlation between production and consumption. Hereby, the reactions in stocks and production to a positive shock in the consumption indicate a direct response in production and a strategic adjustment in stock levels to changes in the demand of oil.

Regarding the gasoline markets, we notice the stocks of gasoline are directly influenced by the prevailing conditions in its own market. An increase in production typically results in elevated inventory levels, whereas stocks tend to decline when there is a rise in either price or consumption. The observed negative relationship between prices and inventory levels is consistent with the storage theory, which suggests that higher spot prices are typically associated with a higher convenience yield, and the convenience yield is negatively correlated with inventory holdings. This dynamic underscores the delicate balance between supply and demand within the gasoline market, where production adjustments and market responses closely govern inventory fluctuations.

When examining the various energy markets, the network of relationships among kerosene’s own variables—stocks, production, consumption, and price—emerges as notably more sophisticated and interconnected than those observed in other markets. An increase in production, for instance, leads to higher stock levels, while a surge in consumption or price typically results in a significant reduction of inventories, a phenomenon also observed in the gasoline market. However, kerosene’s market dynamics extend beyond this: we observe a strong positive correlation between production and stock levels. Likewise, increased consumption or rising prices serve to deplete stocks while concurrently spurring production increases. This bidirectional dynamic between stocks and production, further modulated by consumption and price fluctuations, underscores a distinctive trait of the kerosene market, spotlighting its finely balanced interplay between supply and demand.

The internal dynamics of the heating oil market also reveal significant interrelations among its variables. Similar to the patterns observed in the gasoline and kerosene markets, an increase in the price or consumption of heating oil tends to reduce its stock levels. Furthermore, there is a strong positive correlation between the stocks and production of heating oil, indicating that changes in one are closely mirrored by changes in the other. This pattern underscores the tight linkage between supply factors within the heating oil market, reflecting its responsive equilibrium to shifts in demand and pricing.

Turning our attention to the spillover effects across the energy markets, we first consider the impact from the crude oil market to the refined petroleum products. Within this context, we detect inverse reactions in the gasoline market, contrary to consistent patterns in the behavior of the kerosene and heating oil markets. While an increase in the production of crude oil causes rising production and stocks of heating oil and kerosene, the production and stocks of gasoline decline, indicating a positive shock to crude oil production leads to higher available amounts of kerosene and heating oil. Similarly, an increase in crude oil stocks precipitates an uptick in both kerosene and heating oil stocks, a phenomenon likely attributable to the refining and subsequent storage of the surplus in crude oil supplies. In contrast, gasoline stocks exhibit a decline, signaling a distinct behavioral pattern in response to fluctuations in the crude oil market. Moreover, we observe a concurrent rise in both consumption and production levels of kerosene and heating oil to a positive shock in the consumption of crude oil, underlining the synchronized movement with crude oil, whereas the gasoline consumption decreases. In addition, our analysis reveals a pronounced sensitivity of heating oil prices to fluctuations in crude oil prices, while gasoline and kerosene prices remain unaffected by shifts in crude oil prices.

While the markets for refined petroleum products are significantly influenced by the crude oil market, our analysis also reveals reverse spillover effects—where the crude oil market reacts to changes in the refined product markets. However, the impact of crude oil on the refined petroleum product markets is more pronounced. We only observe a higher crude oil production in response to higher production in the refined products. This suggests that the crude oil market’s dynamics are, to some extent, influenced by the production needs of the refined product markets, albeit this interaction is more restrained compared to the pronounced impact of crude oil market fluctuations on the refined product sectors.

Besides the impact from crude oil to its refined product markets, the markets of the refined petroleum products affect themselves. In particular, an increase in gasoline stocks and production is observed to lead to a decrease in the stocks and production of kerosene and heating oil, highlighting their inverse relationship. Conversely, an upsurge in the stocks and production of kerosene and heating oil results in a reduction of gasoline stocks and production. The inverse dynamics can be attributed to the flexibility within the refining process, allowing for adjustments in the production ratios to favor either gasoline or the heavier fractions like kerosene and heating oil, based on market demand or operational strategies. In addition, this may also explain the negative response of gasoline to shocks in the crude oil market, as gasoline is also indirectly affected by kerosene and heating oil market. However, a positive shift in gasoline prices significantly influences heating oil prices to rise, indicating a co-movement in the pricing of refined products, which underscores the interconnectedness of their markets.

In contrast, the influence of the kerosene-type jet fuel market on the crude oil and gasoline markets is minimal, as the kerosene-type jet fuel market is the smallest among refined product markets in terms of consumption volume. However, shifts in the crude oil, gasoline, or heating oil markets can significantly impact the kerosene market. Nonetheless, the heating oil market also reacts to changes in the kerosene market: a positive shock to kerosene prices not only elevates prices and consumption in the heating oil market but also leads to a reduction in heating oil inventories. The close connection between the two markets is underscored by the observation that an increase in kerosene consumption correlates with a decrease in heating oil usage.

Like the kerosene-type jet fuel market, the heating oil market exerts minimal influence on the crude oil and gasoline markets, yet it significantly impacts the kerosene market. An increase in heating oil stocks leads to elevated stocks levels in the kerosene sector, illustrating a positive interrelation between the stock levels and production activities of these two fuels. Additionally, there is a direct positive relationship between the prices of heating oil and kerosene, highlighting the co-movement between prices.

Overall, this study elucidates the nuanced interdependencies within the crude oil and refined petroleum markets, revealing a direct impact of crude oil fluctuations on gasoline, kerosene and heating oil markets. Hereby, crude oil significantly affects refined product markets, yet exhibits limited responsiveness to alterations within these markets. Moreover, the distinct behaviors of gasoline, kerosene, and heating oil underscore a sophisticated balance of supply and demand dynamics.

5.2. Forecast Error Variance Decomposition

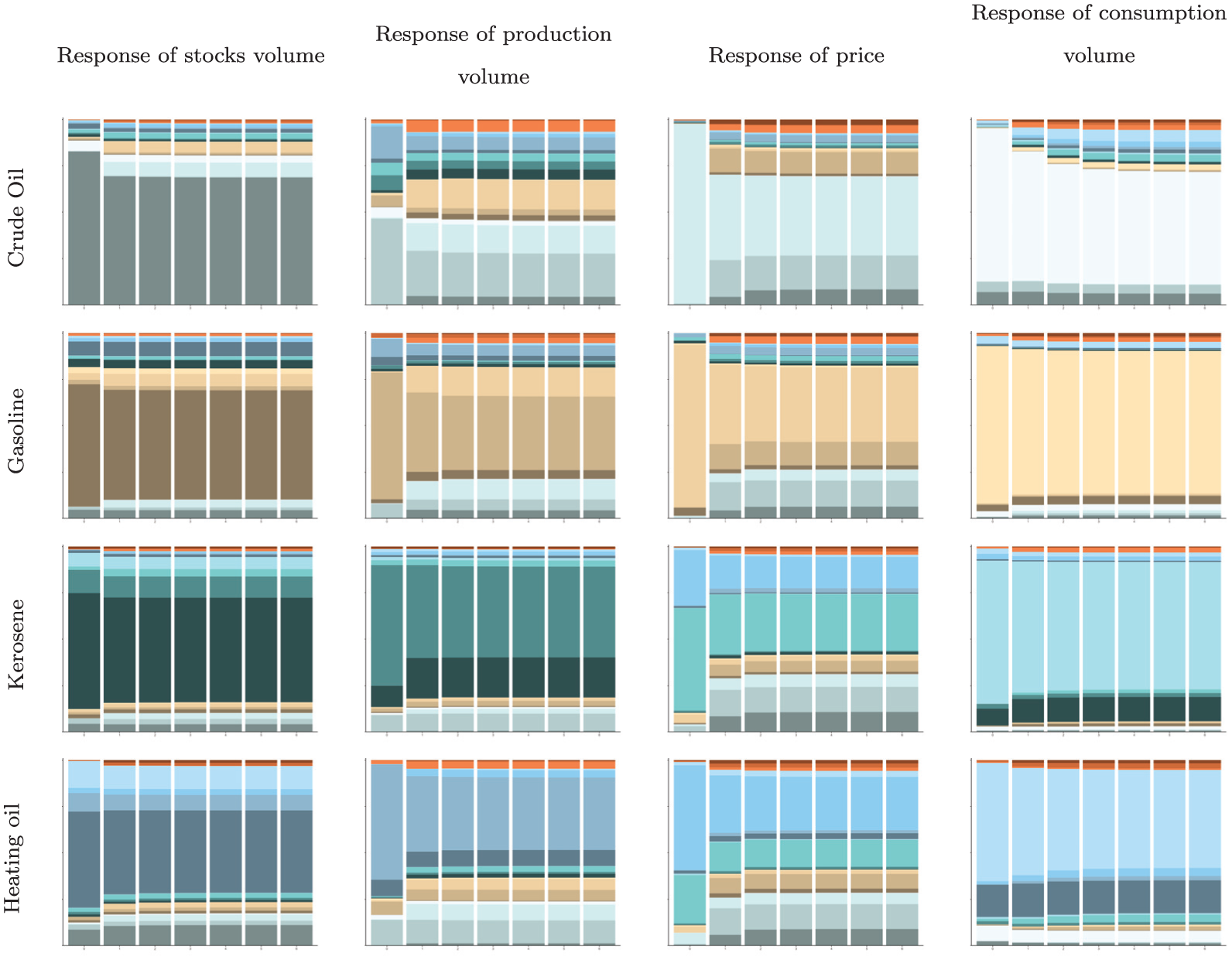

To enhance our comprehension of the interdependencies between the crude oil market and the refined product markets, we employ the generalized forecast error variance decomposition (GFEVD) method. This approach quantifies the proportion of the forecast error variance for each variable that can be attributed to exogenous shocks in other variables, providing insights into the interconnectedness of these markets. The results, presented in Figure 5 for a six-month horizon, offer a nuanced view of these relationships. Notably, the generalized version of this analysis avoids the sensitivity to variable ordering inherent in orthogonalized variance decomposition, making it ideally suited for our GVAR model.

Generalized forecast error variance decomposition for the period from 2005 to 2019.

Overall, the generalized forecast error variance decomposition (GFEVD) analysis reinforces the findings of the impulse response analysis, particularly highlighting the dominant role of the crude oil market in explaining the majority of variations observed within the refined product markets, especially on their production volumes and prices.

Focusing on the commodity-specific dynamics, our analysis reveals that the gasoline market notably impacts the forecast error variance of crude oil. Although the crude oil market predominantly accounts for its own stocks and consumption volume variations, particularly over short-term horizons, the most significant external influence originates from the gasoline sector. This is underscored by the assertion that “gasoline is one of the most important oil products,” as highlighted in Han et al. (2015), since gasoline accounts for roughly 50 percent of all petroleum products consumed. Hereby, the gasoline market exerts a considerable effect on the forecast error variance related to the production and, most notably, the pricing of crude oil. In contrast, the markets for kerosene-type jet fuel and heating oil have a lesser impact on crude oil’s variance, underscoring the unique position of gasoline within the energy sector’s interdependencies.

Although the gasoline market significantly influences the crude oil market’s variability, the forecast error variances of gasoline stocks and consumption show minimal impact from crude oil or the other refined product markets. This suggests, similar to the results of the impulse response analysis, that the gasoline market, especially its consumption, remains relatively insulated from fluctuations within the energy markets. Nonetheless, crude oil does contribute to the variance in gasoline production and price, highlighting that the production of this refined product, along with its pricing, is dependent on crude oil dynamics. This relationship underscores the intricate balance between the supply of crude oil and the operational aspects of the gasoline market, illustrating a nuanced interplay where gasoline can impact broader energy markets yet maintain a degree of autonomy from immediate market shifts.

The variability in kerosene-type jet fuel stocks and consumption is primarily accounted for by its own dynamics, while the influence of crude oil becomes increasingly significant in explaining the variations in its production volume and price across the evaluated timeframe. Notably, the kerosene-type jet fuel market’s minimal contribution to the forecast error variance of its own price underscores a heavy reliance on external energy markets for price determination. Furthermore, the heating oil market, alongside crude oil and gasoline markets, plays a crucial role in affecting the price fluctuations of kerosene-type jet fuel, highlighting the interplay between different energy markets in shaping kerosene’s price dynamics.

The price dynamics of heating oil are significantly influenced by crude oil, gasoline, and particularly kerosene, further underlining the close link between heating oil and kerosene. This relationship underscores the shared influences and market behaviors between these two commodities, emphasizing the results of the impulse response analysis. On the other hand, the production and stock levels of heating oil are predominantly shaped by fluctuations in crude oil prices, emphasizing crude oil’s foundational role in the heating oil market. In contrast, the variations in heating oil consumption are primarily driven by the market’s internal factors, suggesting that its consumption patterns are largely self-determined and less influenced by external market variables.

Overall, the comprehensive analysis of impulse response functions (IRFs) and forecast error variance decompositions (FEVDs) within this study reveals the interdependencies between the crude oil market and the markets for refined petroleum products, such as gasoline, kerosene-type jet fuel, and heating oil. While all energy markets predominantly account for their own variations, our findings underscore a pronounced impact of crude oil on the refined product markets, whereas the economy barely contribute to the forecast error variances. However, gasoline partly explains the variations in crude oil. In addition, we observe a close relationship between the kerosene and heating oil market. These insights not only contribute to a deeper understanding of the energy sector’s operational intricacies but also provide a foundation for more informed decision-making by market participants and policy makers.

6. Conclusion

While existing research has underscored the significance of price spillovers within the energy sector, our investigation expands this analysis to capture the complex interactions spanning the entire spectrum of the energy markets. This study delves into the nuanced interplay between prices, production volumes, stock volumes, and consumption rates across crude oil and its refined products, including gasoline, kerosene-type jet fuel, and heating oil. Adopting the advanced methodology of the global vector autoregressive (GVAR) model, we initially model each energy market individually through vector autoregression models that incorporate commodity-specific variables while also accounting for the impact of the economy. Subsequently, we integrate these individual models into a comprehensive GVAR framework, enabling a detailed examination of the interdependencies between these markets.

In conclusion, our comprehensive analysis elucidates the profound interdependencies characterizing the crude oil market and its downstream counterparts, notably gasoline, kerosene, and heating oil markets. While crude oil prices are a pivotal determinant of refined product market behaviors—significantly influencing their stock levels and production activities—the reverse influence of these markets on crude oil remains limited. Furthermore, our investigation reveal a marked interrelation between the kerosene and heating oil markets, probably due to the fact that refiners typically possess the operational flexibility to adjust kerosene production in response to market demand, which in turn reduces the yield of heating oil. In contrast to the strong positive interrelation among the kerosene-type jet fuel market and the heating oil market, our analysis reveal inverse reactions in the gasoline market. In addition, by dissecting the dynamic responses of each market to shocks in others, our research contributes valuable insights into the complex supply and demand dynamics underpinning the global energy sector. These results not only enhance our understanding of the energy sector’s market dynamics but also offer critical perspectives for stakeholders aiming to navigate or influence these markets.

In conclusion, our comprehensive analysis underscores the critical importance of considering a wide array of market variables and their interrelations to fully grasp the multifaceted dynamics of the energy sector. By extending beyond price interactions to examine production, stocks, and consumption interdependencies, this research enriches the existing body of knowledge and provides a robust framework for future investigations into the ever-evolving landscape of global energy markets.

Looking ahead, there is a compelling opportunity for future research to incorporate time-varying parameters into the analysis. Such an approach would shed light on the evolving nature of relationships within the energy markets over time, potentially revealing shifts in the significance of various spillover effects and interdependencies. Moreover, it would allow for a disentangling of potential differences in the relationship between stocks and prices during periods of backwardation and contango, offering deeper insights into how market structures influence inventory dynamics. An extension of the Diebold-Yilmaz methodology would represent a promising avenue for future research. While Guru et al. (2023) have already applied this methodology to analyze spillovers between the oil market and the stock markets of the G7 countries, as well as India and China, this approach could be effectively extended and then transferred to the study of the integration between the crude oil market and its refined product markets. Specifically, future research could expand this framework to account for the fact that both the crude oil and refined product markets are influenced not only by price dynamics but also by factors such as production, inventories, and consumption patterns. Such an extension would offer a more comprehensive understanding of the interdependencies within these markets. This direction promises to deepen our comprehension of the energy markets’ dynamics, offering valuable insights for policymakers, market participants, and researchers alike.

Supplemental Material

sj-docx-1-enj-10.1177_01956574251366190 – Supplemental material for Spillover Effects in Oil Markets

Supplemental material, sj-docx-1-enj-10.1177_01956574251366190 for Spillover Effects in Oil Markets by Amelie Schischke and Andreas Rathgeber in The Energy Journal

Footnotes

Appendix A

Acknowledgements

The authors would like to thank the participants of the Commodity Markets Winter Workshop 2024, the Global Finance Conference 2024 and the 7th J.P. Morgan Center for Commodities & Energy Management 2024, as well as the seminar participants at the University of Augsburg for their valuable discussion and comments.

Author Contributions

Conceptualization: Amelie Schischke; data curation: Amelie Schischke; formal analysis: Amelie Schischke; funding acquisition: Andreas Rathgeber; methodology: Amelie Schischke; resources: Amelie Schischke; software: Amelie Schischke; supervision: Andreas Rathgeber; writing—original draft: Amelie Schischke; writing—review and editing: Amelie Schischke and Andreas Rathgeber.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Declaration of Generative AI and AI-Assisted Technologies in the Writing Process

During the preparation of this work the authors used ChatGPT in order to improve the readability and language of the manuscript. After using this tool, the authors reviewed and edited the content as needed and take full responsibility for the content of the published article.

Supplemental Material

Supplemental material for this article is available online.

1

See for example Pindyck (2004b), Ewing et al. (2002), Hartley et al. (2008), Serletis and Rangel-Ruiz (2004), Batten et al. (2017), and ![]() .

.

2

See for example Pindyck (2004b), Ewing et al. (2002), Hartley et al. (2008), Serletis and Rangel-Ruiz (2004), Batten et al. (2017), and ![]() .

.

3

See for example Lee and Zyren (2007), Pindyck (2004a), and ![]() .

.

4

As gasoline, kerosene-type jet fuel and heating oil are refined from crude oil, we actually use their production share as weights.

5

With a single lag, each equation in the VAR model involves estimating eleven parameters, leading to a total of forty-four parameters for the entire model.

6

With a single lag, each equation in the VAR model involves estimating seven parameters, leading to a total of twenty-one parameters for the entire model.

7

8

9

We estimate the GVAR model with one lag for the endogenous variables and the weakly exogenous variables, based on the BIC criterion. While the results of the Durbin Watson test, and the OLS-CUSUM test indicate neither model suffers from autocorrelation, nor structural breaks at the 1% significance level, the Henze-Zirkler test implies the residuals of the GVAR model are multivariate normal distributed.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.