Abstract

Increasing (or eliminating) the caps on short-term wholesale prices is generally thought to promote long-term forward contracting for electricity. We find that a higher price cap typically enhances the incentives of electricity buyers (e.g., load-serving entities) to undertake forward contracting. However, a higher cap can diminish the incentives of electricity generators to engage in forward contracting. Consequently, higher wholesale price caps can reduce industry forward contracting.

1. Introduction

To protect consumers against price shocks, the maximum price that can be charged for electricity is explicitly limited in many restructured wholesale markets. 1 Wholesale price caps are often criticized, in part on the grounds that they reduce incentives to secure electricity via long-term “forward” contracts. 2 Forward contracting is valued for at least three reasons. First, like wholesale price caps, forward contracting can help to counteract short-term price volatility. Such volatility seems likely to increase over time as larger portions of electricity supply are generated by intermittent renewable resources (Joskow 2019; Newbery et al. 2018; Wolak 2022). Second, expanded forward contracting can encourage generators to increase the amount of electricity they supply in wholesale markets, thereby reducing wholesale prices (Allaz and Vila 1993). Third, forward contracting can encourage expanded investment in generation capacity. It can do so by allowing generators to secure in advance a stable revenue stream for the output that will ultimately be produced by the expanded capacity. 3

The reason why wholesale price caps are commonly believed to reduce incentives for forward contracting is straightforward. If buyers are protected against high prices in the wholesale market, they will be less inclined to sign forward contracts that offer protection against high wholesale prices for electricity. Wolak (2021, 86–7) observes that in the presence of a “limited prospect of very high prices because of [price] caps, retailers may decide not to sign fixed-price forward contracts. … The lower the [price] cap, the greater is the likelihood that the retailer will delay its electricity purchases to the short-term market.” Similarly, Mays and Jenkins (2022, 2) suggest that “[w]ithout the threat of high prices, consumers of energy have insufficient incentive to enter forward contracts with generators.”

The purpose of the present research is to assess this common wisdom formally, explicitly accounting for the strategic decisions of generators and the endogeneity of short-term and long-term electricity prices. We find that, although the common wisdom has considerable merit, it does not fully capture the effects of wholesale price caps on incentives for forward contracting for two reasons. First, although a higher wholesale price cap typically enhances an electricity buyer’s incentive for forward contracting, it does not necessarily do so. Second, and of greater empirical relevance, a higher price cap can reduce the incentives of generators to undertake forward contracting.

A higher price cap (

The regime shifting effect arises because an increase in

To determine whether the regime shifting effect can ever outweigh the revenue enhancement effect, causing forward contracting to decline as

Our analysis contributes to the extensive formal literature on forward contracting, which establishes that forward contracting can induce generators to compete aggressively and expand their outputs in wholesale markets. Allaz and Vila’s (1993) seminal work documents these effects of forward contracting in a non-repeated setting with Cournot competition and publicly-observed levels of forward contracting. Subsequent studies consider alternative forms of competition (Holmberg 2011; Holmberg and Willems 2015), repeated interactions (Green and Le Coq 2010; Liski and Montero 2006), and settings where prevailing levels of forward contracting are not observed publicly (Hughes and Kao 1997). Empirical studies also document the competition-enhancing effects of forward contracts (e.g., Bushnell, Mansur and Saravia 2008; van Eijkel, Kuper and Moraga-González 2016; Wolak 2000). This extensive formal literature largely abstracts from the impact of wholesale price caps on forward contracting. 6

This literature focuses on settings in which generators dictate the levels of forward contracting. In practice, large buyers of electricity are key counterparties in forward market transactions. Like our analysis, a few studies consider settings where buyers exercise some control over the extent of forward contracting (Anderson and Hu 2008; Schneider 2020; Brown and Sappington 2023a, 2023b). However, these studies do not consider the effects of wholesale price caps on equilibrium levels of forward contracting.

A distinct strand of the literature analyzes the effects of price caps in oligopoly markets, but does not consider forward contracting. Studies in this literature analyze the impact of price caps on output, consumer surplus, and welfare in settings with uncertain demand (Earle, Schmedders and Tatur 2007; Grimm and Zottl 2010; Reynolds and Rietzke 2018). Other studies identify conditions under which a wholesale price cap reduces incentives for capacity investment (Fabra, von der Fehr and de Frutos 2011; Zottl 2011).

We contribute to these strands of the literature by examining how wholesale price caps affect the incentives of both generators and large buyers of electricity to undertake forward contracting. We do so in a stylized model with linear demand and costs, a uniform density for demand uncertainty, and a regulated load serving entity that is required to serve the realized demand of its customers. We identify conditions under which the aforementioned common wisdom – that wholesale price caps reduce buyers’ incentives for forward contracting – prevails. 7 We further demonstrate that the common wisdom about buyers’ incentives does not readily extend to generators’ incentives. Consequently, any attempt to assess how a change in a prevailing wholesale price cap will affect industry forward contracting should consider both the relative influence of buyers and sellers in determining the levels of forward contracting and the distinct ways in which a price cap affects their incentives for forward contracting.

The ensuing analysis proceeds as follows. Section 2 describes the key elements of our model. Section 3 examines the electricity buyer’s incentives for forward contracting. Section 4 analyzes electricity generators’ incentives for forward contracting. Section 5 provides concluding observations. The Appendix provides the proofs of all formal conclusions.

2. Model Elements

A large buyer of electricity (e.g., a load serving entity) is required to deliver all the electricity its retail customers demand. Realized retail demand is

Commercial and industrial customers also consume electricity, which they purchase in the wholesale market at unit price

The corresponding inverse demand curve is:

Electricity is supplied by

The large buyer (

We adopt the standard assumption in the literature that the price of a forward contract,

If

Equation (3) reflects the fact that

When realized retail demand is

where

The timing in the model is as follows. After the regulator specifies the wholesale price cap

Before examining the levels of forward contracting that arise in equilibrium, it is helpful to examine the wholesale price and the generators’ outputs that arise in equilibrium, given the prevailing levels of forward contracting. Lemma 1 characterizes

Equation (7) implies that when

Equation (8) implies that multiple equilibria arise when

It remains to characterize the levels of forward contracting that arise in equilibrium. These levels vary according to whether the extent of forward contracting is determined by the buyer or by generators. Section 3 examines the levels of forward contracting preferred by the buyer (

3. The Buyer’s Preferred Level of Forward Contracting

To determine

where

Equation (4) implies that

Equation (10) implies that, because

Equation (11) implies that

Lemma 2 characterizes the impact of expanded forward contracting on

An increase in

An increase in

When

For expositional convenience, we will refer to

Proposition 1 indicates that an increase in

Proposition 1 also reports that high values of

Proposition 1 also identifies conditions under which an increase in

In summary, Proposition 1 implies that an increase in the wholesale price cap typically increases

4. Generators’ Preferred Levels of Forward Contracting

In practice, a buyer of electricity typically does not dictate prevailing levels of forward contracting unilaterally. Therefore, it is important to consider how a binding wholesale price cap affects generators’ incentives for forward contracting. To do so, let

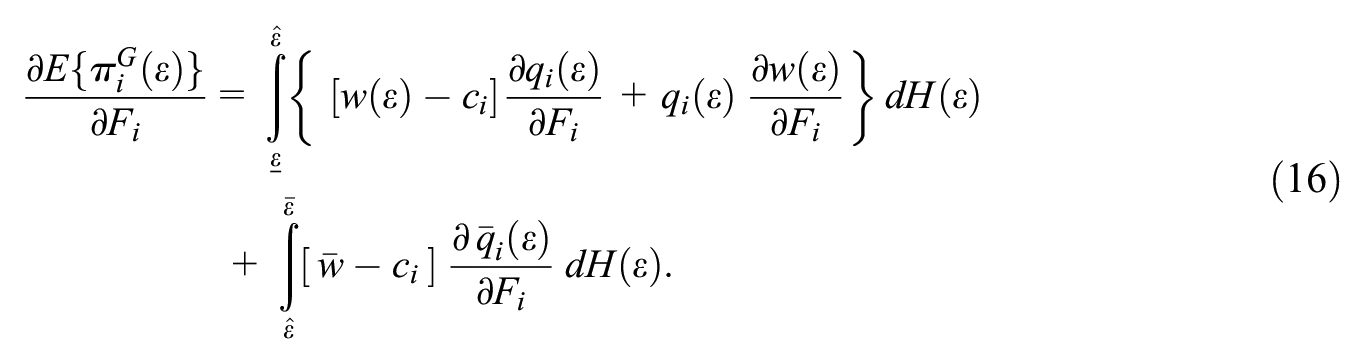

Equation (15) implies that the rate at which

Equation (16) implies that the impact of a change in

Equation (17) identifies two effects of an increase in the price cap,

The second of the two terms in equation (17) captures the regime shifting effect. This effect arises because an increase in

To determine whether

where

Lemma 3 examines how a binding price cap affects the impact of expanded forward contracting on a generator’s profit.

The conclusion in Lemma 3 reflects the following considerations. An increase in

Equation (7) implies that the rate at which

If

The following corollary to Proposition 2 identifies factors that enhance or diminish the impact of an increase in

Condition (i) in Corollary 1 reports that an increase in

The equilibrium wholesale price also increases as

Condition (iii) in Corollary 1 holds because the price cap becomes less likely to bind as

Proposition 2 also permits the specification of conditions under which an increase in

Corollary 2 reflects the following considerations. When

Corollary 3 provides an additional conclusion when the

Corollary 3 reflects the fact that

Corollary 3 establishes that an increase in

We select initial parameter values to reflect elements of actual electricity markets. However, the ensuing analysis does not necessarily reflect activities in any particular market because our model does not capture all relevant elements of actual electricity markets. In particular, for analytic tractability, our model abstracts from the sharply rising marginal cost a generator effectively experiences as its output approaches capacity. Our model of Cournot competition also does not account for the activities of fringe generators and must-run generation (e.g., wind and cogeneration). Furthermore, we take all demand realizations to be equally likely, whereas extreme deviations from expected demand typically are relatively unlikely in practice.

With this caveat in mind, we proceed to establish baseline parameter values (Part B of the Appendix demonstrates that the key qualitative conclusions drawn below persist as baseline parameter values change). The wholesale price cap is initially taken to be 1,000 (so

This expected wholesale price approximates the $33.92 quantity-weighted average wholesale price in the eight major U.S. electricity hubs in 2020. 33 The identified aggregate expected demand reflects the 8,487.88 MWh average hourly electricity consumption in a U.S. state in 2020. 34

We initially take the ratio of expected residential electricity consumption to industrial electricity consumption at the expected wholesale price to be 0.65, reflecting the corresponding ratio in the U.S. in 2020. 35 Therefore:

Each generator’s marginal cost of production is initially assumed to be 25 (so

We initially set

Table 1 summarizes these baseline parameter values. 38

Baseline Parameter Values.

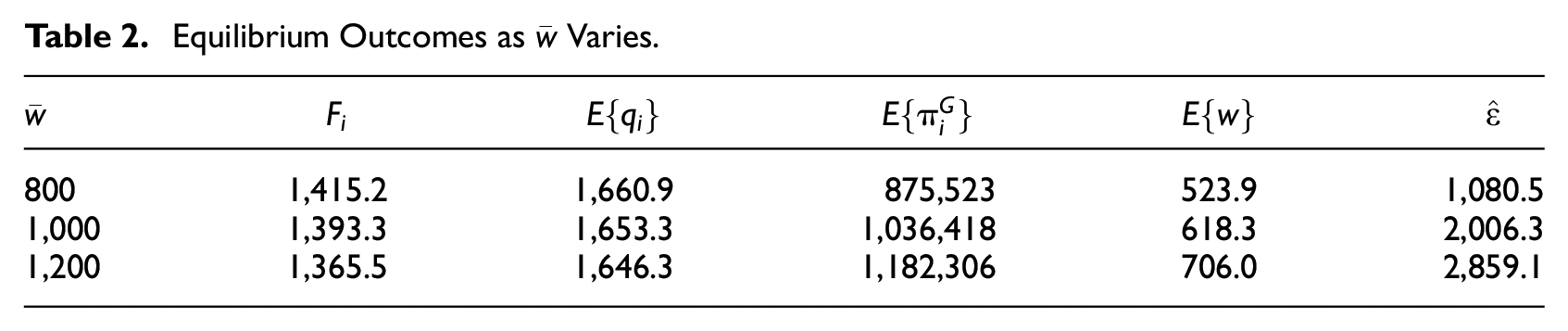

The middle row of data in Table 2 presents equilibrium outcomes in our model for the baseline parameter values. The first and third rows of data report the corresponding outcomes when the price cap (

Equilibrium Outcomes as

Table 2 reports that each generator reduces its equilibrium level of forward contracting as the wholesale price cap is increased. The reduced forward contracting and the higher price cap increase the expected wholesale price and expected generator profit, while reducing expected generator output. 40 The numerical solutions presented in Part B of the Appendix indicate that corresponding effects of an increased wholesale price cap arise as parameter values diverge from their baseline levels.

For the reasons explained above, the outcomes reported in Table 2 and in the Appendix do not imply that a higher wholesale price cap will always (or even often) reduce the levels of forward contracting preferred by generators in practice. However, the outcomes do suggest that this potential preference merits consideration when attempting to predict the effect of a change in the level of a wholesale price cap on industry forward contracting.

5. Conclusions

We have examined how a cap on the wholesale price of electricity affects incentives for forward contracting, explicitly accounting for the effects of forward contracting on short-term and long-term electricity prices. Our findings support the common wisdom that a price cap reduces a buyer’s incentive for forward contracting. When the maximum price it can face in the wholesale market declines, a buyer derives less benefit from securing electricity at the expected wholesale price rather than facing the actual wholesale price.

In contrast, a binding wholesale price cap can increase a generator’s incentive for forward contracting. Consequently, an increase in a prevailing price cap can reduce a generator’s incentive for forward contracting. This is the case in part because a higher price cap renders the cap less likely to bind, thereby increasing the likelihood that expanded forward contracting will reduce a generator’s profit by reducing the prevailing wholesale price. This regime shifting effect of an increase in

Our findings suggest that policymakers should consider the incentives of both buyers and generators when attempting to assess the likely impact of a change in the prevailing level of a wholesale price cap on industry forward contracting. The common wisdom that a higher price cap will enhance a buyer’s incentive for forward contracting does not necessarily extend to generators. Consequently, the ultimate impact of a higher price cap on industry forward contracting likely will depend in part on the details of the buyer-generator negotiations that determine the prevailing levels of forward contracting.

Future research should model these negotiations formally, allowing buyers and generators to bargain over both the number and the prices of forward contracts. To facilitate comparison with other studies in the literature, we adopted the common assumption that the price of a forward contract (

A broader investigation of whether a binding wholesale price cap is likely to diminish generators’ incentives to sign forward contracts in practice would be valuable. We found that these reduced incentives can arise in one particular environment. Corresponding investigations across a broad spectrum of environments that prevail in practice would be valuable.

Future research might also analyze the effects of risk aversion. Buyer risk aversion introduces an additional consideration that runs counter to the conventional wisdom. A higher price cap can reduce the variance of a buyer’s profit by reducing the buyer’s profit margin when the price cap binds.

44

The lower variance, in turn, can diminish the risk-reducing benefit a risk averse buyer derives from forward contracting.

45

Consequently, in principle, if this effect were sufficiently pronounced, an increase in

Footnotes

Appendix

Part A of this Appendix provides the proofs of the formal conclusions in the text. Part B presents additional numerical solutions. Part C considers an alternative rule for allocating

Acknowledgements

We thank the editor and two anonymous referees for very helpful comments and suggestions. Support from the Government of Canada’s Canada First Research Excellence Fund under the Future Energy Systems Research Initiative and the Social Sciences and Humanities Research Council’s Canada Research Chair program is gratefully acknowledged.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

1

To illustrate, the prevailing cap on the wholesale price of electricity is $999.99 per megawatt hour (MWh) in Alberta, Canada (Brown and Olmstead 2017) and $5,000 per MWh in Texas (Smith 2022). A lower cap is imposed in Texas if electricity generators are deemed to have secured sufficient profit from an extended period of high wholesale prices (![]() ).

).

2

Wholesale price caps are also criticized because they limit the profit that generators secure during periods of particularly high demand, and can thereby reduce investment in generator capacity (Hogan 2017; ![]() ).

).

3

4

5

Expanded forward contracting increases equilibrium output, which reduces the wholesale price when the price cap does not bind.

6

Holmberg (2011) analyzes a model in which firms choose forward contracts before competing via supply functions in the wholesale market. The author conjectures (p. 187) that “reducing price caps … would stimulate strategic [forward] contracting.” However, he does not investigate this issue formally. Yao, Oren and Adler (2007) develop an optimization program in which generators choose forward contracts and engage in Cournot competition. A wholesale price cap reduces the generators’ incentives for forward contracting in the numerical example the authors analyze.

7

We show that a buyer’s incentive for forward contracting depends in part on the nature of the retail price regulation it faces. This incentive typically declines as the regulated retail price tracks the expected wholesale price more closely.

8

Thus, we consider fixed-price, fixed-quantity financial forward contracts that are settled at the prevailing wholesale price. Such contracts are common in electricity markets.

9

If

10

When the generators choose the levels of forward contracting, they do so simultaneously and non-collusively.

11

See Allaz and Vila (1993, Appendix A) for a formal proof of this conclusion in a setting where generators determine the levels of forward contracting in the first stage of the game. Holmberg and Willems (2015) explain why the assumption that forward markets are efficient in this sense often constitutes a reasonable caricature of electricity forward markets. The concluding discussion considers alternative processes for determining the prices of forward contracts. This discussion refers to ![]() model in which the price of a forward contract is determined by a form of bargaining between a buyer and a generator of electricity.

model in which the price of a forward contract is determined by a form of bargaining between a buyer and a generator of electricity.

12

For example, as explained further below, the regulator might specify a unit price,

13

The values of

14

The maintained assumption that

15

For any set of such outputs, no generator has an incentive to reduce its output unilaterally because

16

This will be the case if

17

For expositional ease, the ensuing analysis focuses on the case where

18

The labels “deterministic” and “stochastic” should not be taken literally. Expected retail demand,

19

Equation (6) implies that ![]() ,

,

20

Equation (6) implies that ![]() reports that

reports that

21

When stochastic demand is negative, demand is relatively small. The price cap does not bind for the smaller demand realizations.

22

When stochastic demand is positive, demand is relatively large. The price cap binds for the largest demand realizations.

23

From equation (9), ![]() implies that

implies that

24

The conclusions reported in Lemma 2 (and in Proposition 1 below) also hold when ![]() is replaced by

is replaced by

25

Formally, suppose generators

26

Equation (17) and equation (54) in the proof of Proposition 2 in the ![]() demonstrate that the revenue enhancement effect of an increase in

demonstrate that the revenue enhancement effect of an increase in

27

![]() imply that the regime switching effect of an increase in

imply that the regime switching effect of an increase in

28

The expressions in the two preceding footnotes reveal that an increase in

29

![]() implies that

implies that

30

31

It is readily shown that if

34

35

37

![]() . Therefore,

. Therefore,

38

These baseline parameter values imply that

40

The relatively high expected wholesale prices reported in ![]() reflect the aforementioned special features of our model. A model that included a fringe of competitive generators, must-run generation, sharply rising marginal cost near capacity, and infrequent demand realizations well above expected demand would permit substantially lower expected wholesale prices while allowing the price cap to bind for some, but not all, demand realizations.

reflect the aforementioned special features of our model. A model that included a fringe of competitive generators, must-run generation, sharply rising marginal cost near capacity, and infrequent demand realizations well above expected demand would permit substantially lower expected wholesale prices while allowing the price cap to bind for some, but not all, demand realizations.

41

Anderson and Hu (2008) analyze a model in which a buyer proposes a level of forward contracting and associated compensation. The generator can either accept the buyer’s proposal or decline to engage in forward contracting altogether. The buyer’s bargaining power gives rise to an equilibrium price of a forward contract that exceeds the expected spot price of electricity. Ruddell, Downward and Philpott (2018) analyze a model in which buyers of electricity have demand curves for forward contracts with suppliers and for spot purchases of electricity. In this model, the equilibrium price of a forward contract exceeds the expected spot price of electricity. This price premium prevails because each buyer recognizes that signing a forward contract with a supplier will increase the supplier’s aggression in the ensuing Cournot competition. The increased aggression reduces the expected spot price of electricity at which the buyer will ultimately purchase a portion of its electricity consumption. The price premium persists even in the presence of speculators because each buyer values a forward contract with a supplier more highly than it values a forward contract with a speculator (since the latter contract does not induce increased aggression in the ultimate Cournot competition, and therefore does not directly reduce the expected spot price of electricity).

42

Some of our less central findings likely would change if the prices of forward contracts were determined by bargaining between buyers and sellers. For example, the equilibrium price of a forward contract might vary with the characteristics of the relevant buyer and seller (e.g., their size and market power). In addition, a buyer’s incentive for forward contracting might vary across generators. Furthermore, as in Ruddell, Downward and Philpott (2018), the equilibrium price of a forward contract might exceed the expected wholesale price, even in the presence of speculators.

43

To facilitate a tractable analysis, we have assumed that generators choose output levels. Models in which generators choose supply functions introduce considerable analytic complexity, including multiple equilibria (see Green 1999; Holmberg 2011; Holmberg and Willems 2015; Klemperer and Meyer 1989; Newbery 1998). ![]() identifies conditions under which a generator’s forward contracting induces its rival to shift its supply function inward. The author also notes that a more binding wholesale price cap can render the specified conditions more likely to arise. However, Holmberg (2011) does not undertake a systematic examination of the impacts of a wholesale price cap on incentives for forward contracting. Such an examination awaits future research.

identifies conditions under which a generator’s forward contracting induces its rival to shift its supply function inward. The author also notes that a more binding wholesale price cap can render the specified conditions more likely to arise. However, Holmberg (2011) does not undertake a systematic examination of the impacts of a wholesale price cap on incentives for forward contracting. Such an examination awaits future research.

44

45

In contrast, a higher price cap can increase a generator’s profit margin when the price cap binds, thereby increasing the variance of the generator’s profit. The increased variance can induce a risk averse generator to prefer a higher level of (risk-reducing) forward contracting.

46

We have extended our analysis to allow the buyer and the generators to have mean-variance preferences (e.g., Rolfo 1980; ![]() , 154–5). In the presence of such risk aversion, tractable analytic characterizations of equilibrium outcomes are difficult to derive. However, numerical solutions suggest that the buyer’s expected utility often increases systematically as its forward contracting increases for any price cap that binds for some, but not all, demand realizations. Thus, a risk averse buyer often prefers the highest feasible levels of forward contracting, regardless of the level of the price cap.

, 154–5). In the presence of such risk aversion, tractable analytic characterizations of equilibrium outcomes are difficult to derive. However, numerical solutions suggest that the buyer’s expected utility often increases systematically as its forward contracting increases for any price cap that binds for some, but not all, demand realizations. Thus, a risk averse buyer often prefers the highest feasible levels of forward contracting, regardless of the level of the price cap.

47

As noted above, a higher price cap can increase the variance of a generator’s profit and thereby enhance a risk averse generator’s incentive to undertake forward contracting. However, our numerical solutions reveal that when risk averse generators choose their preferred levels of forward contracting (non-cooperatively), a higher price cap can induce lower equilibrium levels of forward contracting, just as it can when generators are risk neutral.