Abstract

It is well known that the Covid-19 that hit the world caused a global economic crisis. This present study aimed at examining the economic impact of this crisis with respect to families with both quantitative and qualitative approaches. In this study, we intended to demonstrate how families (n=247) met their basic needs, how they coped with financial stress, how financial stress relates to family characteristics and how it affects marital, family, and life satisfaction. The impact of family characteristics on financial stress was examined through regression analysis. The impact of financial stress on marital, family, and life satisfaction was determined through content analysis. The results of the regression analysis showed that the influence of education, debt, minimum wage employment, and fear of being laid off on financial stress was significant. The qualitative results show that individuals' marital, family and life satisfaction were negatively affected due to the financial stress they experienced during the Covid-19.

Introduction

The COVID-19 pandemic has brought economic problems and financial concerns in addition to health problems around the world. At the macro level, the health crisis negatively affected the economies of countries, and at the micro level, the financial stress on families has been felt to a significant extent. United Nations [UN] (2020) describes the COVID-19 pandemic as far more than a health crisis. It has affected societies and economies severely. While the impact of the pandemic will vary from country to country, it will most likely increase poverty and inequalities at a global scale (UN, 2020). In a Covid-19 Survey, conducted by National Endowment for Financial Education [NEFE], 2020 with 2049 Americans, 84% of respondents reported experiencing financial stress due to Covid-19. The economic factors causing stress, as cited by the respondents to survey, were listed as having enough saved money (55%), paying bills (46%), paying debts (30%), income fluctuations (24%), and job security (24%) (NEFE, 2020). The Organisation for Economic Co-operation and Development OECD, 2021 Major Risks Report, conducted in 25 OECD countries, shows that families struggled to pay bills during this period, with some families seeking support from aid agencies.

Turkey has had its share of the global pandemic, with more than 1.60 million cases, more than 100,00 deaths, quarantines and other policy measures, not to mention families facing economic challenges. To respond to this, the government launched the Social Protection Shield program to meet to citizens' needs during the Covid-19 pandemic. The program included services, such as short-time work allowance, unemployment benefits, cash support, and social assistance. During this time, a fundraising campaign called “Biz Bize Yeteriz Türkiyem” (We have One Another to Rely on, My Turkey) was held by the government to provide cash assistance. Through these programs, more than 15 million people received financial aid, according to the latest official data, and the aid collected amounted to more than 45 billion TL (almost $6 billion at the time) (Ministry of Labor and Social Security, 2021).

People’s jobs were also protected by the government during the pandemic. With the labor reforms, layoffs were limited; however, employers were allowed to send their employees on unpaid leave if they deemed it necessary, in which case the employee received 1,170 TL (about $180 at the time) from the government as a short-term work allowance (Government Gazette, 2018).

Despite the above-mentioned support from the government, the negative economic impact of the pandemic on families could not be avoided. Indeed, according to the Turkey Income and Living Conditions Survey by the Turkish Institute of Statistics (2022), the proportion of households with debts other than housing related debts increased by 5.4% to 63.7% in 2021; the proportion of households that reported that these payments burdened them was 57.1%. In addition, 38.3% of households reported that they could not afford a meal of meat, chicken, or fish every other day, 33.4% could not afford unexpected expenses, 20.5% heating while 62.9% were unable to replace old furniture.

The Covid-19 pandemic has led to severe financial stress all over the world. Employing both quantitative and qualitative approaches to relate financial stress faced by families due to Covid-19, this present study sought answers to the following questions: 1- Do family characteristics have an impact on families’ financial stress during Covid-19 pandemic? 2- How financial stress impacted families’ marital, family and life satisfaction during Covid-19 pandemic?

The findings of this study are expected to guide policy makers in deciding on issues such as the adequacy of the short-time working allowance with respect to meeting the basic needs of individuals, what steps should be taken to ensure that families are financially prepared for periods of financial crisis such as pandemics, and determining the financial guidance requirements of families. Additionally, this study by employing a quantitative and qualitative approach, will contribute to current studies on this topic.

Method

Participants

The study population consists of married individuals who received short-time working allowance during the Covid-19. Snowball Sampling is used as a sampling method for this study. It is a sampling method whereby a contact is made with one of the units of the population; subsequently, another contact is made with the help of the contacted person, and then another contact is made in the same way, and thus the size of the sample grows in a line of chain, causing a snowball effect (Balcı, 2018). Since the size of the population was not determined in this study, we attempted to reach out to additional participants via the agency of those who had already participated in the study. In the end, we reached out to 247 people using the snowball method.

Procedure

This study received ethical approval from Ethical Commission of Hacettepe University in Turkey. The study data were obtained from married individuals benefiting from short-time working allowance via an online survey form in June–July 2020. Participants were informed about the study by the Consent Form. It was stated that the information obtained within the scope of the study would be used for scientific purposes, would be evaluated in confidentiality within the framework of scientific ethical rules and would not be used for any other purpose.

Measures

Being a mixed research study, we employed both qualitative and quantitative research techniques. The study used the online questionnaire technique as a data collection tool. The questionnaire, consisting of three sections, was designed by the researchers based on the literature.

The first section included demographic and descriptive information about the participants (sex, age, education level, employment status in a minimum wage job, family income before Covid-19, home ownership status, etc.).

The second part of the questionnaire included questions about information on debt and financial strain (debt level, use of low-interest personal loans due to Covid-19, fear of being laid off, level of financial strain, and level of satisfaction with financial situation).

The third part of the questionnaire included the qualitative part of the study. In order to determine the level of impact of financial stress experienced during Covid-19 on participants' marital, family, and life satisfaction, 3 statements were designed in the form of a 5-point Likert scale (1- Strongly Disagree, 5- Strongly Agree) (The financial stress I experienced during Covid-19 negatively affected my marital satisfaction (relations with my spouse). The financial stress I have experienced during Covid-19 have negatively affected my family satisfaction (parental relations, relations with children), the financial stress I have experienced during Covid-19 have negatively affected my life satisfaction). In addition, there were 3 semi-structured questions asked to the participants, who either gave the answer 4 - Agree and 5 - Strongly Agree to these statements, in order to obtain in-depth information about how their marital (relations with spouse), family (relations with parents, relations with children) and life satisfaction were negatively affected.

Data Analysis

Quantitative Analysis

The quantitative data obtained within the scope of the research were evaluated using the SPSS program. Data on demographic and explanatory variables in the first part of the questionnaire form were tabulated using frequency and percentage values. Logistic Regression Analysis was utilized to determine the variables that had an effect on the level of financial stress (Park, 2013:155). In the study, financial stress (dependent variable) was categorized as high financial stress and low financial stress. In the regression model, low financial stress was coded as “0” and high financial stress as “1.” The independent variables we wished to examine with respect to the level of financial stress in working life consisted of eight variables: gender, age, number of children, education level, demographic variables such as minimum wage salary and spouse’s employment status, as well as debt, and fear of lay off.

Dependent Variable

Financial stress was used as a dependent variable in the study. Financial stress level in the study was determined using the question; “How would you describe your current level of financial stress due to Covid-19?” Participants were asked to answer this question on a 5-point Likert scale (1- I am not stressed at all, 5- I am very stressed). In this framework, the mean financial stress score of the participants was 3.08 with a standard deviation of 1.26. In the regression analysis, scores above the mean were defined as high financial stress and scores below the mean were defined as low financial stress.

Independent Variables

The independent variables of the study were demographic variables such as sex, age, and education level, number of children, minimum wage salary, and employment status of spouse, as well as debt status and fear of lay off. Participants' debt status was determined using the question “Do you currently have any debts?” and the fear of lay off was determined using the question “Do you have a fear of being laid off?”

Qualitative Analysis

This study analyzed qualitative data using the content analysis technique. Content analysis is defined as bringing together similar data within the framework of certain concepts and themes and interpreting them by organizing them in a way that the reader can understand (Yıldırım & Şimşek, 2011). The participants' responses to the open-ended questions in the questionnaire form were analyzed and themes and codes were created. The themes and codes were tabulated as frequencies and percentages. Participants who gave the answer “Agree” or “Strongly Agree” to the questions, asked to determine the level of negative impact of financial stress experienced during the Covid-19 process on their marital, family, and life satisfaction, answered 3 open-ended questions to obtain in-depth information about how and in what way financial stress affected them. Not all participants answered the open-ended questions despite having stated that the financial stress they experienced negatively affected their marital, family, and life satisfaction, and some participants, whose statements were included in more than one theme, provided in-depth and detailed information for one question. For this reason, frequencies differ in the tables with themes and codes. In addition, examples of answers given by the participants were given as direct quotations. In order to ensure confidentiality while quoting answers, codes such as the participant’s gender information and survey number (Participant, M48) were used.

Results

General Information on Participants

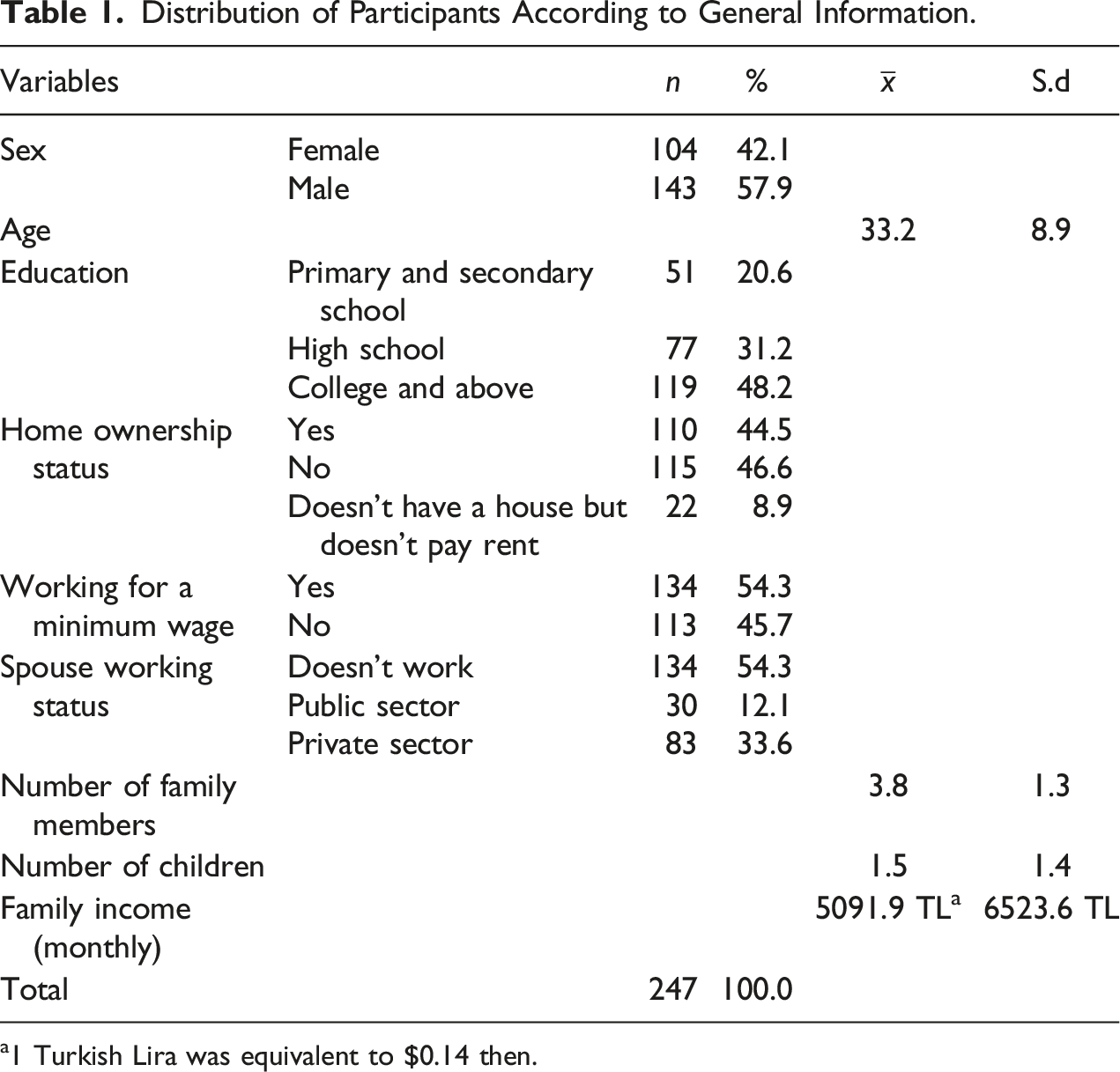

Distribution of Participants According to General Information.

a1 Turkish Lira was equivalent to $0.14 then.

Among the participants, slightly more than half (54.3%) was working for a minimum wage 46.6% of them did not own a house of their own. Approximately half of the participants’ spouse (54.3%) doesn’t work, while 33.6% stated that their spouse worked in the private sector (Table 1).

Participants selected for this current analysis reported on average 33.2 (SD = 8.9) years of age. The mean number of people in the family 3.8 (SD = 1.3) and participants has average 1.80 (SD = .50) children, The mean monthly family income was

Findings on the financial situation of participants during the Covid-19

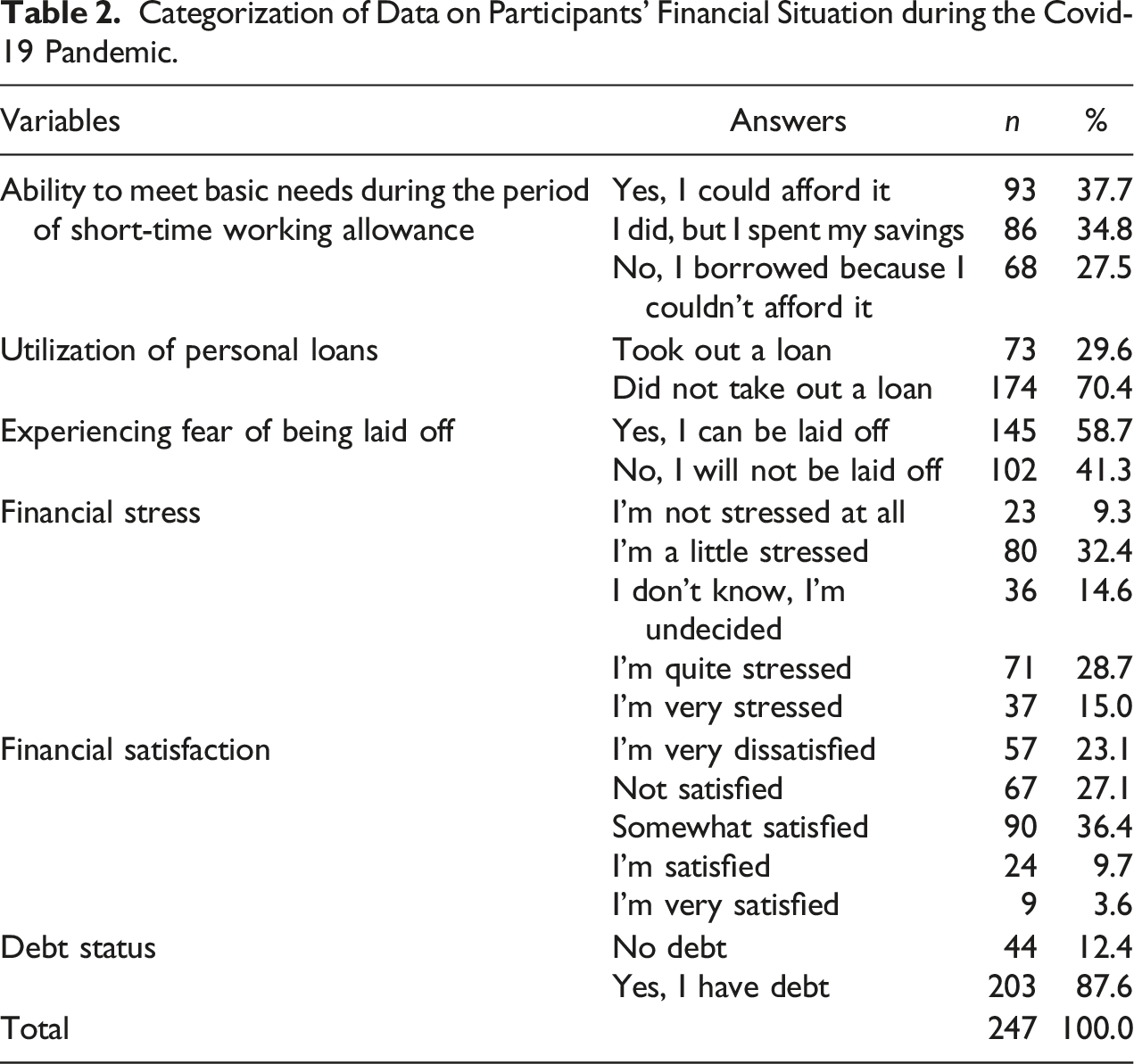

Categorization of Data on Participants’ Financial Situation during the Covid-19 Pandemic.

About half of the respondents (58.7%) were afraid of being laid off. In analyzing respondents' financial stress levels, respondents who reported being “a little stressed” were at the top with 32.4%, while 28.7% reported being “quite stressed” and 15.0% reported being “very stressed.” Within this framework, about half of the participants (50.2%) indicated that they were not satisfied with their financial situation (Table 2).

Considering participants' current debt levels, 87.6% of participants had debts (credit card debt, personal loans, debt to relatives and friends, etc.).

Logistic Regression Analysis Results

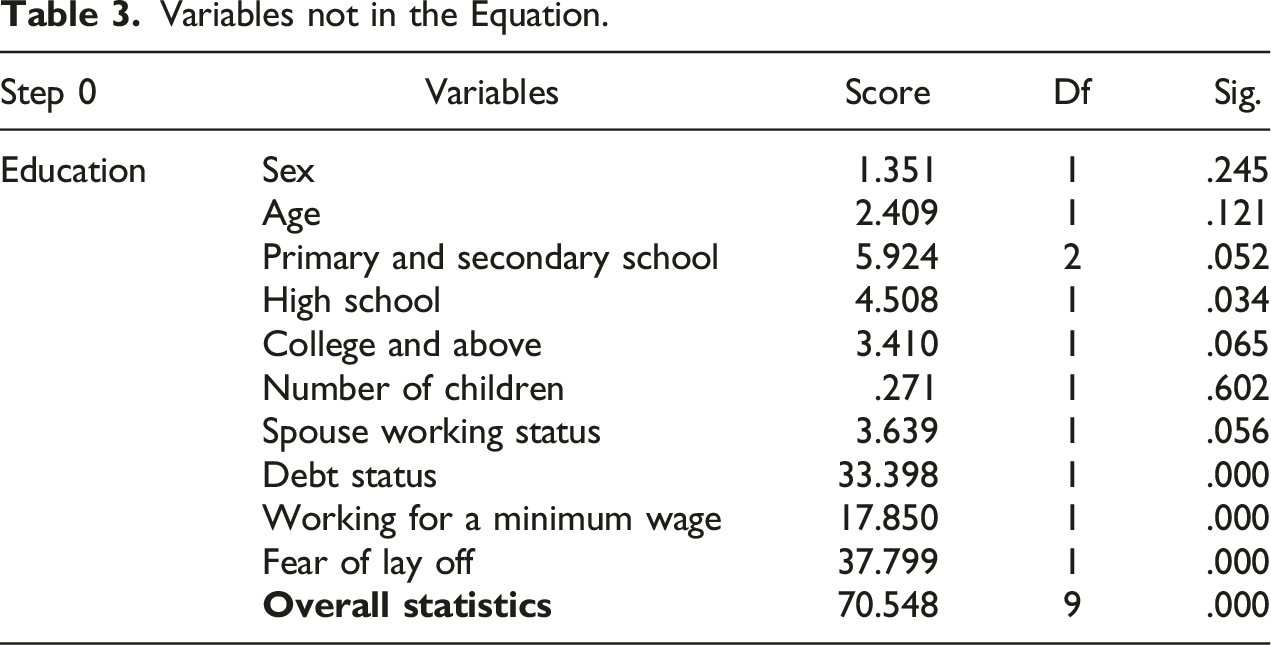

Variables not in the Equation.

The initial model has a -2log Likelihood (-2LL) value of 338,514. When all independent variables entered the model, the likelihood value of -2log decreased to 251,548. This indicates an improvement in model fit. The Cox & Snell R2 and Nagelkerke R2 values were .297 and 398, respectively. This result shows that the model explains about 40% of the change in financial stress. The results of the Hosmer and Lemeshow chi-square test, which evaluated the model fit, were not found significant (p > 0.05). This indicates the fit between the regression model and the data. The correct classification increased from 56.3% to 74.5% when independent variables entered the model.

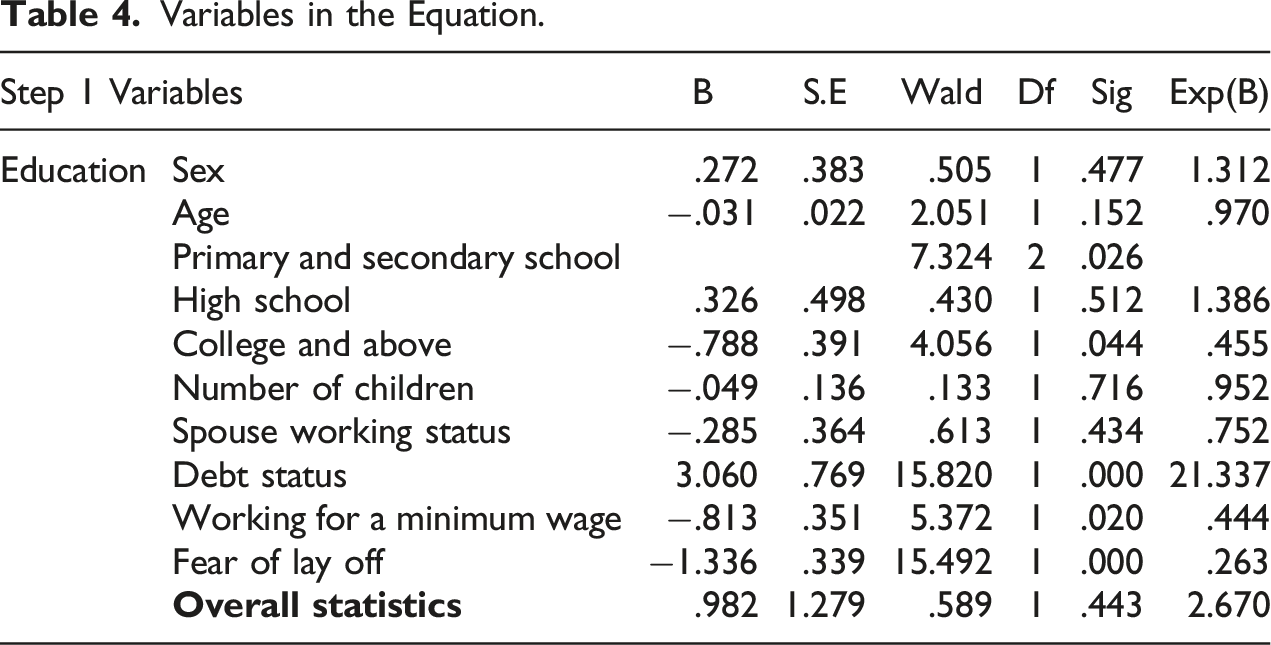

Variables in the Equation.

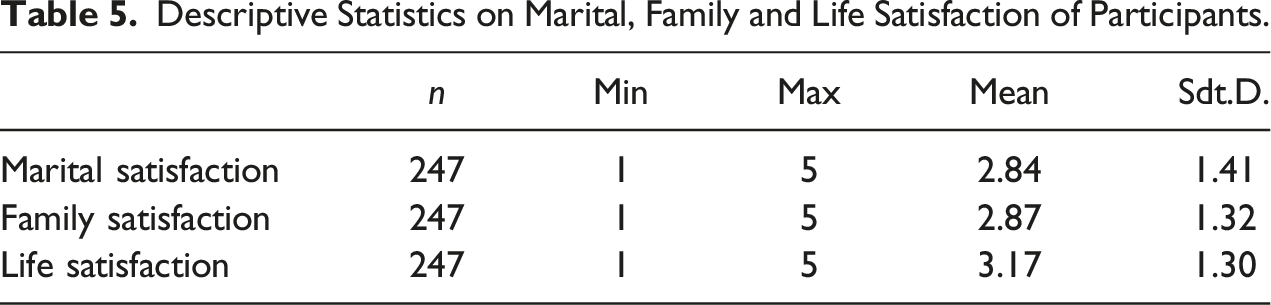

Results on the Impact of Financial Stress Experienced by Participants during the Covid-19 Pandemic on their Marital, Family, and Life Satisfaction

Descriptive Statistics on Marital, Family and Life Satisfaction of Participants.

Results of Content Analysis Regarding the extent of the negative impact of financial stress during the Covid-19 on participants' marital, family, and life satisfaction

Answering “Agree” and “Strongly Agree” to questions designed to determine how financial issues faced by the participants during the Covid-19 pandemic affected their marital, family, and life satisfaction, participants also answered open-ended questions to help us obtain more insights into how and in what ways they were affected by financial issues.

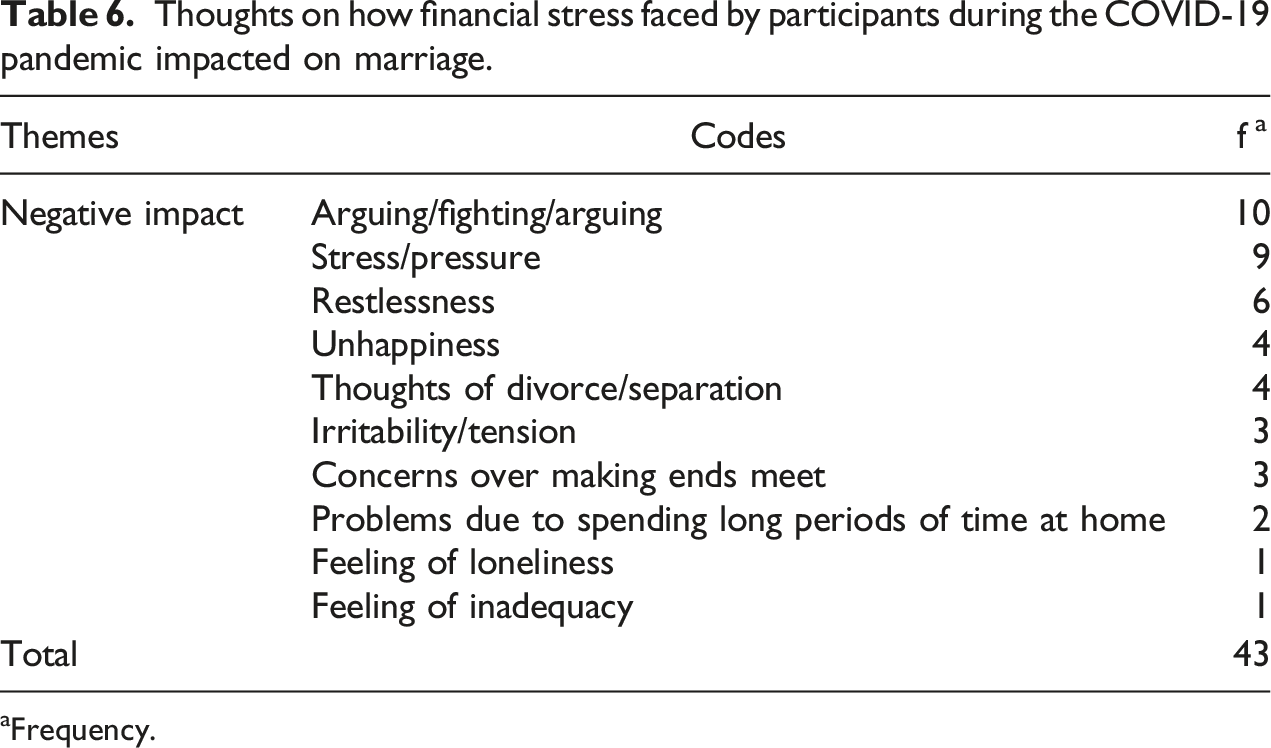

As can be seen in Table 6, participants' opinions regarding the impact of financial stress they experienced during the Covid-19 on their marital satisfaction were grouped into a single theme called Negative Impact.

Thoughts on how financial stress faced by participants during the COVID-19 pandemic impacted on marriage.

aFrequency.

Among the participants, there were also those who stated that they experienced “stress/pressure” and “restlessness.” Participant M94’s statement: “My relationship with my husband was affected by financial inadequacies. We argued a lot because of the stress.” Participant W64’s statement: “The debts and problems have increased, there is no peace.” and Participant M73’s statement: “We experience discomfort at home because of financial problems, stress, and incompatibility.” can be cited as examples related to experiencing stress/pressure and discomfort in marital life.

Of those who reported being “unhappy” and having “thoughts of divorce/separation,” Participant M97’s statement: “Because of the general financial difficulties, there is constant unrest in the family and unhappiness because we cannot meet our needs.” Participant W127: “It has brought us to the point of divorce and the financial difficulties have exhausted our psyche.” and Participant W131's statement: “It was quite overwhelming, it might even lead to separation.” were indicated that married life and relationship with spouse were affected.

Participant W148’s statement: “We were having money troubles. My husband is tense and angry at home every day.” was indicating “nervousness/tension” and “fear of making ends meet.”

Of those who indicated that staying home also caused problems, Participant M236 stated, “I was home more than usual and we fought more because of work stress.”

Those who reported experiencing “loneliness” and “feelings of inadequacy” expressed these thoughts as follows: “We have become individually isolated.” (Participant, W77) and “Our married life is severely affected because economic problems cause feelings of stress, inability to meet needs, feelings of inadequacy.” (Participant, W199).

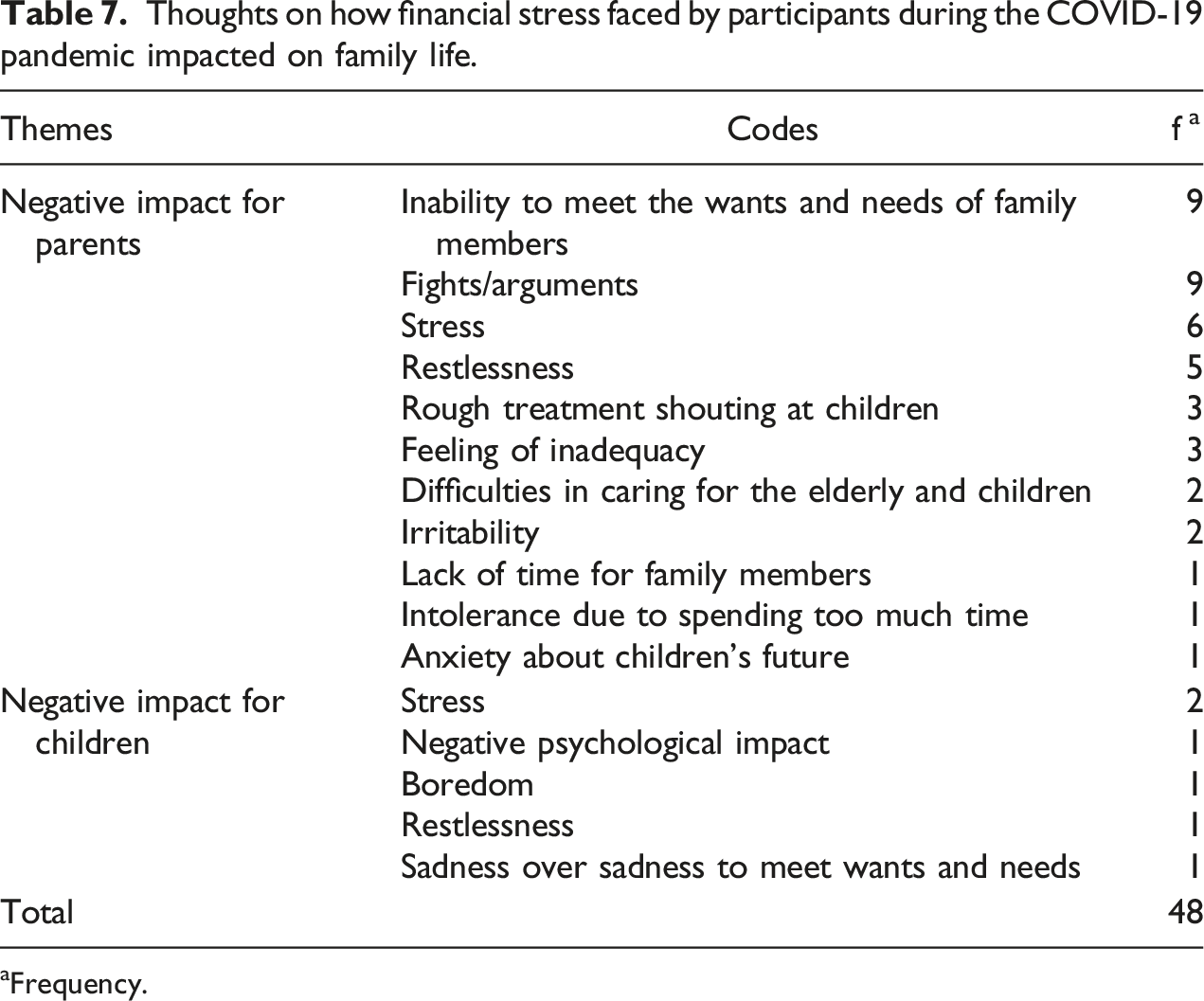

Participants' thoughts on the impact of financial stress they experienced during COVID-19 on their family satisfaction were grouped under two themes, namely “Negative Impact on Parents” and “Negative Impact on Children” and given in Table 7.

“I couldn't meet the needs of my children and my wife, and I was having great financial difficulties. I could only get part of my salary because employment opportunities were decreasing. I was stressed because although I was doing my best as a family man, it was not enough, and that made me very sad.” (Participant, M222) was an example of how the wants and needs of family members could not be met,

“Everyone was very restless, there were constant fights at home”. (Participant, M19) and:

“My wife and children were stressed all the time, when we talk they argue, when we don't talk everyone retreats to their own corner.” (Participant, M165) was an example of that there were arguments and moments of unrest,

“It has been too stressful and has affected our family peace.” (Participant, M16) and: “I couldn't spare time for them because I was under stress all the time. This weakened my relationships.” (Participant, M23) were examples of that the participants were stressed,

Thoughts on how financial stress faced by participants during the COVID-19 pandemic impacted on family life.

aFrequency.

Stating that he or she behaved harshly/shouted at his/her children due to the stress they experienced, Participant M48 said: “I started to treat them harshly because I was stressed and mentally impaired.” Participant M126 said: “I was stressed, I yelled at the kids a lot, I fought with my husband.” and Participant M236 said: “When I was nervous, it reflected on my child, too.”

The financial stress of participants led to problems related to the care of the elderly and children. Participant M106 said: “Caring for my elderly parents has become more difficult financially and mentally.” and participant W207 said: “I had difficulties with the caregiver.”

In our country, family members spent and continue to spend more time together due to temporary closure of businesses, switching to distance learning in education, and continuing to work from home under the flexible work measures to prevent the spread of Covid-19. Participant W213, who indicated that he or she struggled because of the increased time commitment, commented as follows: “We spent more time together, there were situations that reached the limits of tolerance.”

Financial stress experienced by families during Covid-19 also affected the children negatively, Participant M69 said: “My children were upset because they did not get everything they want.” and Participant W125 said: “The children became restless, bored, stressed.” indicating that children were negatively affected psychologically and upset because their wishes were not met.

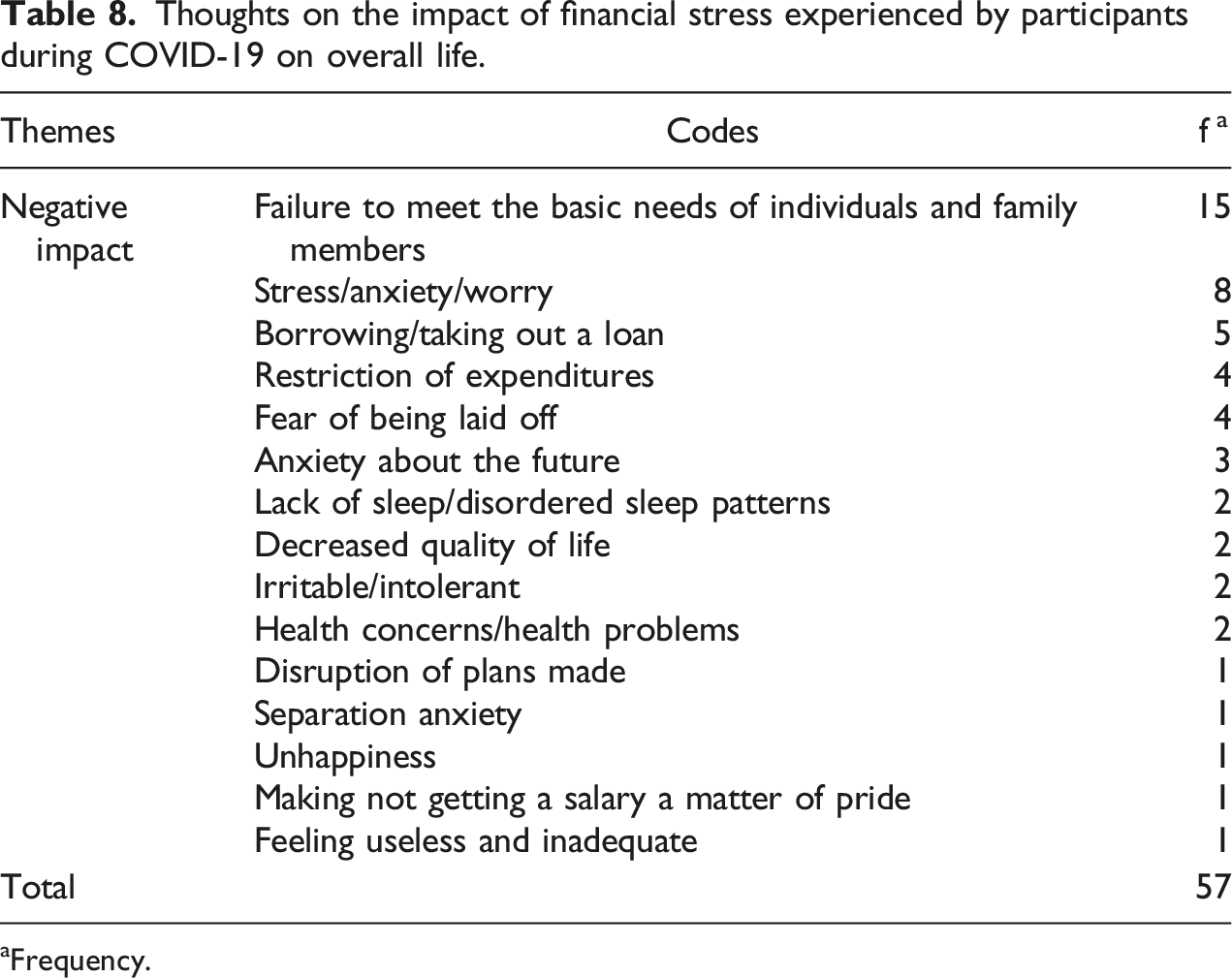

Thoughts on the impact of financial stress experienced by participants during COVID-19 on overall life.

aFrequency.

Participants who stated that the financial stress they experienced during COVID-19 primarily caused them and their family members to be unable to meet their basic needs said the following; “I could not shop, I could not pay the bills.” (Participant, M7), “I am unable to meet my needs. Stress at home increased, payments piled up. I could not sleep.” (Participant, M19), “We had trouble buying food, electricity and telephone debts flew through the roof.” (Participant, W148).

Among those who stated that they experienced stress/anxiety/worry, Participant W125 stated that they experienced difficult times saying: “I had an anxious life, I felt under constant stress and pressure.”

Participants who stated that they and their family members borrowed money and restricted their expenditures due to not meeting their basic needs expressed their experiences as follows: “I got into debt and could not meet many of my needs in normal life.” (Participant, M227), “I had to take a personal loan, I have difficulty in paying it.” (Participant, M159), “I had a hard time. 20 days ago, my wife gave birth. I borrowed money, I have not worked for 4 months.” (Participant, M60), “We had to make restrictions even for basic needs.” (Participant, M235) and “It was negatively affected due to restricted spending.” (Participant, M88).

Participants stated that staying at home longer, taking a break from work life or working from home impacted on the social life of individuals, weakened their social relations, and decreased their quality of life: “Staying at home, worrying about health affected me negatively.” (Participant, W33), “We did not leave home except for urgent needs. We could not meet our friends and relatives. We stayed inside the house with our nuclear family all the time. Days passed like nights and nights like days. Our sleep pattern changed a lot.” (Participant, M51), “I lacked a social life.” (Participant, M84), “We had certain plans, I couldn't realize them.” (Participant, M104) and “It has reduced our quality of life compared to before.” (Participant, W22). Although employer was not allowed to lay off staff to restrict layoffs due to Covid-19, the participants experienced fear of lay off and anxiety about the future. Participants had the following to say: “I have the fear of being laid off and the stress that I will live a worse life than my old life.” (Participant, W165), “I had financial problems. I got into debt. The children suffered a lot and so did my wife. We were living with the fear of being laid off.” (Participant, W175),“I have hesitations about unemployment now. I am a tourism worker; it is not clear what will happen.” (Participant, M30) and “I had problems with my family. My card debts increased, anxiety about the future increased.” (Participant, M126). “We have become angrier and more intolerant than normal.” (Participant, M25), “I had financial difficulties. My husband had to give me money and all our needs were met by one person, my husband. My husband's family and my family offered to help me with money. I made it a matter of pride and became very stressed and panicked. I felt useless and inadequate. I felt like an unnecessary person in this process. My psychology deteriorated.” (Participant, M6) and “We faced the fear of our family breaking up during this process.” (Participant, M152) are examples of statements from individuals who stated that they had grown more irritable and intolerant, had made not receiving a salary a matter of pride and felt useless and inadequate, and who feared the breakup of their family.

Discussion

The objective of this study was to relate micro-level financial stress on families caused by the Covid-19 pandemic to family demographics within the framework of a model and to examine how this financial stress affects marital satisfaction, family satisfaction, and life satisfaction among families.

Most participants were men, had a college and higher degree, did not own a house, worked a minimum wage job, and had spouses who were not actively employed. The mean age of the participants was 33.2 ± 8.9 years, the mean number of people in the family was 3.8 ± 1.3, and the mean number of children was 1.8 ± 0.5. The average monthly family income of the individuals was 5091.9 ± 6523.6 Turkish Lira.

According to the results of the study, roughly one third of the participants (37.0%) stated that they were able to meet their basic needs during the period they benefited from the short-time working allowance. Of the participants who could not meet their basic needs with the short-time working allowance, 34.8% spent their existing savings in order to meet these needs, while 27.5% met their basic needs by borrowing. Studies examining the financial problems experienced by families during the pandemic support this finding. For instance, in a study by Yuda and Munir (2022), since families lost their incomes due to the pandemic, they had to borrow to meet basic needs. Studies also stated that the health crisis due to Covid-19 turned into an economic and social crisis over time, and these crises affected family income, unemployment levels and family welfare (Brodeur, Gray, Islam & Bhuiyan, 2020; Brewer & Gardiner, 2020; Daks, Peltz & Rogge, 2020). Additionally, it is known that social isolation and staying at home also increase financial anxiety as it affects employment status and income (Morgan & Boxall, 2020; Reger, Stanley, & Joiner, 2020; Thunström et al., 2020).

The participants in the study had credit card and bank debts (due to personal, vehicle, and housing loans), and owed money to their immediate surroundings (relatives, friends, etc.). The fact that individuals were in debt during this period and that they received 60% of their regular income through the Short-time Working Allowance due to the quarantine, added to their level of financial stress. In addition, approximately one third (29.6%) of the participants stated that they had benefited from low-interest consumer loans provided by public banks due to Covid-19. Yuda and Munir (2022) interviewed 21 families with different income levels to determine the consequences of the pandemic on the socioeconomic resilience of families as well as the strategies adopted by families to overcome social vulnerabilities in an uncertain environment, and found that families adopted similar strategies regardless of their socioeconomic status, and one of these strategies was borrowing. Similarly, NEFE (2020) stated that individuals received economic support from family members and close friends. However, Rodrigues et al. (2021), in a study of Portuguese families, concluded that the majority of respondents had not yet considered taking out a loan to minimize the negative impact on family income.

Slightly more than half of the respondents (58.7%) feared being laid off. As can be inferred from studies conducted during the pandemic, large swathes of businesses suffered hefty financial losses, which meant ceasing or downscaling their activities, losing profits due to the drop in sales and laying off staff (Aksu & Orak, 2022; Balcı & Çetin, 2020:49; Mou, 2020). Although the introduction of a ban on layoffs to protect employees with the Omnibus Law No. 7233 in Turkey reduced individuals' fear of being laid off to some extent, the fact that employers were given the opportunity to put employees who cannot be laid off on unpaid leave for 3 months, and that a maximum of 60% of their salaries were paid from the Unemployment Insurance Fund with a daily payment of 39.24 TL (1,177 TL per month) (Government Gazette, 2018), has been a significant factor in reducing individuals' income, leading to a decrease in their economic welfare (Aksu & Orak, 2022). The majority of participants reported experiencing financial stress (76.1%), while about half of them were dissatisfied with their financial situation (50.2%). These results show that the pandemic conditions were instrumental in causing participants to experience financial stress and decreasing their satisfaction with their financial situation. NEFE (2020) surveyed 2049 individuals over the age of 18 living in the United States and found that most respondents (84%) were concerned about their personal finances. Quarantines to prevent the spread of Covid-19, restrictive measures and economic recession caused financial stress as they led to income losses (Manojkrishnan & Aravind, 2020). A study conducted by Wilson et al. (2020) with 474 participants in the USA was concluded that individuals experienced more job insecurity due to Covid-19.

According to the results of the regression analysis, in which the relationship between family characteristics and financial stress was analyzed, the level of education, debt status, employment in a minimum-wage job, and fear of lay off were found to affect financial stress. Accordingly, elementary school graduates, those who had debts, those who worked for a minimum wage, and those who had fears of layoff were more financially stressed. Socioeconomic conditions during the pandemic and the job insecurity associated with its aftermath led individuals to experience financial stress (Choi, Heo, Cho & Lee, 2020; Holmes et al., 2020; Shanahan et al., 2020). Likewise, Günay (2021) examined the determinants of financial stress experienced at work during the Covid-19 pandemic in Turkey and the role of trust in policies to combat the pandemic in reducing financial stress, and found that job insecurity and income had an impact on financial stress. A research conducted by NEFE (2020) found that people experienced financial stress due to job insecurity, difficulty in debt repayment/settlement, income fluctuations, etc. Rodrigues, Silva, and Franco (2021) concluded that Portuguese individuals suffered financial stress during the initial quarantines and that fear of lay off had a greater impact on the level of financial stress. Okumuş (2021) pointed out that quarantine practices impoverished some individuals and families due to the nature of some jobs, as individuals were unable to perform work from home or were laid off. Fear of lay off is known to affect family well-being, which is related to perceptions of job security (Stevenson et al., 2020). Similarly, Choi et al. (2020) found a significant relationship between job insecurity and financial stress in a study conducted with 1145 adults in the United States. Individuals who were afraid of being laid off and had low income experienced more financial stress. In reducing the financial stress of individuals, confidence in the policies to combat the pandemic—the measures Turkey took to combat the pandemic, the belief that it successfully combated the pandemic and that it can combat the economic consequences of the pandemic—was effective. The level of stress perceived by individuals in a life-threatening process such as the pandemic varies according to their individual, social, and cultural characteristics, personality traits and mental processes, and socioeconomic conditions (Kaya, 2020; Wang et al., 2020).

The fact that primary school graduates in this study experienced 2.22 times more financial stress than higher education graduates was an expected result considering the relationship between income and education level. Rodrigues, Silva, and Franco (2021) stated that the educational level of individuals was one of the factors affecting financial stress. Alkhiary (2011) concluded that high education level of individuals and having a secure working life reduced the level of financial stress.

The answers given to questions on the level of negative impact of financial stress experienced during Covid-19 on marital, family, and life satisfaction constituted the qualitative findings of the study. The results showed that most of the participants' marital, family, and live satisfaction were negatively affected due to the financial stress they experienced during Covid-19. Studies conducted during the pandemic found that emotional, psychological and economic difficulties and prolonged quarantine periods led to increased stress levels, anxiety, depression, and post-traumatic stress disorders, which negatively affected family and marital satisfaction (Alfawaz et al., 2021; Huang & Zhao, 2020). Rodrigues, Silva, and Franco (2021) reported that economic and social crises during the pandemic seriously affected overall well-being and family well-being. Social isolation, remote work, lockdowns etc. to prevent the spread of the pandemic affected the economy in macro terms, which meant a squeeze on family purses. Ruined family finances led to a decline in individuals life satisfaction and family well-being. Similarly, White (2007) mentions that family well-being is affected by financial stress and lack of social life.

In the study, citing the negative effects of financial stress on marital life, the participants stated that they were constantly arguing/fighting/tussling with their spouses, feeling restless and stressed out/pressured, and having thoughts of divorce/separation. Studies reported that economic, psychological, and social challenges faced during the pandemic as well as being in the same place and together all the time due to lockdowns, having fewer square meters per person in the house, not to mention children not having a room of their own, meant more domestic conflict, violence and divorce, and a decrease marital satisfaction (Alpar, 2020; Campbell, 2020; Pieh, O´Rourke, Budimir & Probst, 2020; Prime, Wade & Browne, 2020; Usher et al., 2020; Zhang & Ma, 2020). If conflicts between spouses cannot be managed, domestic violence, a decrease in marital satisfaction, and divorce are inevitable (Kaya & Akın, 2021).

The impact of financial stress experienced during Covid-19 on family life was categorized under two headings, that is, “negative impact on parents” (inability to meet the wants and needs of family members, fighting/arguing, stress, restlessness, being harsh/shouting at children, feeling of inadequacy, etc.) and “negative impact on children” (stress experienced by children, psychological impact, sadness due to their wants and needs not being met, etc.). Davis and Mantler (2004) define financial stress as “anxiety about not being able to meet one’s basic needs and economic demands.” If we consider how financial problems experienced during Covid-19 impacted on parents in light of this definition, the inability of parents to meet the wishes and needs of other family members caused financial stress. As a matter of fact, there are other studies reporting similar results. In Bozkurt’s (2020) study on the impact of Covid-19 on family relationships involving 5338 people, 40% of the participants stated that they had concerns about meeting their basic needs. Yıldız and Erdem (2020) pointed out that job insecurity was an important indicator in terms of family ties and that the fear of going hungry affected family communication and caused problems. Kaya & Akın, 2021 examined the negative impacts of the pandemic on family and marital life and concluded that children experienced both mental and behavioral problems causing them to perform worse at school. However, he cited deterioration in family interaction and conflicts as the negative impacts on family life. In Bozkurt’s (2020) study, it was concluded that 17% of the participants had increased communication problems within the family. In their study with nurses working in a pandemic hospital during the pandemic period, Özdemir et al. (2021) determined that being married increased the perceived stress level and decreased the perception of self-efficacy. In this present study, parents also reported that they felt inadequate in meeting the needs of their children. Shevlin et al. (2020) also concluded that being married and having children increased the stress level of individuals during Covid-19.

The “negative” impacts of financial stress on participants' life satisfaction were the inability to meet the basic needs of individuals and family members, stress/anxiety/fretting, weakening of social life/social relations, borrowing money/taking out a loan, restriction of expenditures, fear of lay off, future anxiety, etc. Covid-19 created sudden changes in social life causing stress among individuals (Manojkrishnan & Aravind, 2020). Similarly, Taylor et al. (2008) stated that life-threatening situations such as pandemics, epidemics, and disasters, changing living conditions due to these and adaptation processes created a high stress perception in individuals. In addition, layoffs, high inflation, increased indebtedness, cuts/reductions in income, transition to distance education, as well as anxiety about getting sick and dying, infecting loved ones, restrictions in daily life to prevent the pandemic, loss of social support systems caused difficulties with financial, social, emotional, psychological, mental, and private life (Alpago & Oduncu Alpago, 2020; Bozkurt et al., 2020; Godinic et al., 2020; Kaya & Akın, 2021; Koçak & Harmancı, 2020; Meltzer et al., 2010). In the face of these challenges, individuals may experience anxiety, uncertainty, uneasiness, fear, hopelessness, and depressive moods (Blumenstyk, 2020; Kaya & Akın, 2021; Wind et al., 2020). As a matter of fact, Göksu & Kumcağız, 2020 found that individuals' stress levels and anxiety levels increased during the pandemic. Kaya & Akın, 2021 also found that disruptions in social interaction and changes in daily life habits were the primary negative impacts of the pandemic on the social lives of individuals. A study by Aksu and Orak (2022) conducted during the pandemic, stated that layoffs, wage cuts, low unemployment benefits, and short-time working allowance caused financial anxiety among individuals. Conducted with healthcare professionals in Turkey, the study concluded that financial anxiety levels were higher in the aftermath of the pandemic compared to the pandemic process, and that Covid-19 worsened the financial anxiety levels of individuals (Aksu & Orak, 2022). Individuals had concerns about job losses and depressive symptoms due to Covid-19, which in turn created more social and financial anxiety (Wilson et al., 2020). Rodrigues et al. (2021) reported that the pandemic had a moderate impact on individuals' lives in general and that their working lives continued. In addition, 65% of the individuals in the study stated that their economic situation was affected by the first wave of the pandemic and lockdowns, and they felt the need to reduce their monthly expenses. Mou (2020) also stated that people spent less due to unfavorable economic conditions and uncertainties. Considering the findings obtained from this present study and the studies conducted during the pandemic, Covid-19 negatively affected the life satisfaction of individuals and families.

Conclusion

The aim of this study was to determine how families were able to meet their basic needs during the pandemic and how financial stress affected their marital, family, and life satisfaction. The findings of this current study showed that families were not financially prepared for this sudden crisis. Although some of the respondents (34.8%) reported that they met their basic needs by using their existing savings, the number of respondents (27.5%) who borrowed money, because the short-time working allowance given to them by the government was not enough, is too striking to be ignored. Indeed, judging by participants' own statements, this caused financial stress and negatively affected their marital, family, and life satisfaction. On this basis, individuals learned an important lesson from this process. Indeed, in NEFE’s (2020) study, the participants were asked what the Covid-10 process taught them. They responded that they should reduce their spending and create a savings plan and a fund for contingencies. In this framework, there is a need to identify the requirements of families with respect to financial planning, budgeting, etc. Organisation for Economic Co-operation and Development OECD, 2021 emphasized that family support services provided to families have become vital in the Covid-19 pandemic, emphasizing the importance of sustainable, effective, and long-term programs. These training courses should be integrated into family support programs and they should be delivered on a regular basis. Training programs should be developed and implemented in collaboration with family practitioners and other practitioners who help families make financial plans. Finally, given the reassuring impact of policies implemented in times of crises (Fetzer et al., 2020; Malhotra et al., 2020), it is important for policy makers to implement policies in a stable and reassuring manner to reduce the level of financial stress experienced by families and to ensure that families can maintain their functions in a healthy manner.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.