Abstract

Organizations increasingly create specialized roles to address complex challenges that transcend established boundaries of expertise and practice. This study examines how members of a nascent occupation—responsible investment analysts—collaborated with asset management professionals to incorporate environmental, social, and governance criteria into conventional financial analyses. Drawing on ethnographic fieldwork and multiple data sources, we identify two distinct collaborative pathways: structured collaboration, which aligns nascent occupational contributions with existing frameworks, and generative collaboration, which involves sustained, iterative engagement to fundamentally transform established practices. We show that progression along each pathway is shaped by the interplay between nascent occupation members’ adaptive strategies and the epistemic assumptions embedded in professional domains—particularly shared beliefs about what constitutes valid expertise and how it should be evaluated. Our findings illuminate how knowledge co-creation unfolds when one party lacks institutionally validated expertise, how professional-level epistemic orientations shape opportunities for practice transformation, and how early collaborative arrangements condition nascent occupations’ ability to gain recognition and influence within organizations. These insights contribute to theories of knowledge co-creation across occupational boundaries and offer practical guidance for organizations seeking to address challenges that span established domains of expertise.

Keywords

Organizations increasingly face complex challenges that transcend established boundaries of expertise and professional practice (Augustine, 2021; Howard-Grenville, Nelson, Earle, Haack, & Young, 2017). In response, many organizations have created new occupational roles designed to bridge gaps between established professions and emerging demands (Fayard, Stigliani, & Bechky, 2017). However, members of these nascent occupations face a fundamental challenge: they must develop domain knowledge while simultaneously demonstrating value to, and securing cooperation from, established professionals whose work they aim to influence (Kitay & Wright, 2007; Werr & Styhre, 2002). This situation reveals important limitations in existing theories of knowledge co-creation, particularly when conventional markers of expertise—such as formal credentials or institutional affiliation—are absent.

Research on inter-occupational collaboration often assumes that each party possesses well-defined, institutionally recognized knowledge bases—knowledge that can be aligned or bridged through coordination mechanisms such as boundary objects (Bechky, 2003a; Carlile, 2002), or through relational strategies that mitigate status differences (DiBenigno, 2020; Huising, 2015). Yet nascent occupations typically lack institutional validation, and their members “need time to develop their skills and demonstrate their complementary abilities to incumbent professionals” (Dupin, Wang, & Wezel, 2022, p. 1896). Their roles are “notoriously vague,” their contributions “debatable,” and their qualifications subject to contested interpretation (Murphy & Kreiner, 2020, p. 872). This ambiguity creates distinctive challenges for collaboration and motivates our central research question: How do members of a nascent occupation collaborate with those from established professions to co-create knowledge and transform existing practices?

To explore this puzzle, we examine the collaboration between “first-generation” responsible investment (RI) analysts and asset management professionals at a French investment firm during a period of rising demand for socially responsible investing (SRI). In response to this demand, the firm established dedicated RI analyst roles to incorporate environmental, social, and governance (ESG) criteria into conventional financial analyses. Drawing on ethnographic fieldwork and multiple data sources, we trace how RI analysts worked with fixed-income and equity asset managers to co-create SRI knowledge and redesign investment processes. We identify two distinct collaborative pathways—structured and generative—that shaped both knowledge development and practice transformation. Structured collaboration, which emerged with fixed-income asset managers, involved adapting RI analysts’ contributions to align with existing decision-making frameworks. Generative collaboration, which developed with equity asset managers, relied on sustained, iterative engagement to jointly construct new evaluative frameworks and reshape core investment practices.

Through comparative analysis of RI analysts’ collaborations with different types of asset managers, we extend theoretical understanding of inter-occupational collaborations and knowledge co-creation in three key ways. First, we show how these processes unfold when one party lacks institutionally validated expertise. Prior research emphasizes that access to collaboration opportunities often depends on recognized expertise derived from institutionalized authority and jurisdictional claims (Anteby, Chan, & DiBenigno, 2016; Garman, Leach, & Spector, 2006). In contrast, our study unpacks how the collaboration process itself serves as a mechanism for developing and validating expertise through knowledge co-creation. The contrasting pathways we identify demonstrate how RI analysts navigated the absence of formal recognition by adapting their approaches to align with the different evaluative frameworks and collaborative norms of their asset management counterparts. In doing so, they gradually gained credibility and influence through carefully orchestrated collaborative engagement, without relying on conventional markers of authority. This insight builds on performative perspectives on expertise (Nicolini, Mørk, Masovic, & Hanseth, 2017; Treem & Barley, 2018) by illustrating how occupational recognition can emerge through situated interaction and engagement.

Second, we demonstrate how established professionals’ epistemic assumptions—their fundamental beliefs about the nature and validation of expertise—shape the conditions for knowledge co-creation and practice transformation in collaborations with nascent occupations. Our comparative analysis shows that these assumptions influence how contributions are assessed, the forms of engagement that emerge, and whether collaboration leads to incremental adaptations within existing frameworks or enables more substantial reconfigurations of practice. By illuminating these dynamics, we extend research on intra-occupational heterogeneity by showing how implicit epistemic assumptions about expertise shape not only knowledge-sharing patterns (Beane & Anthony, 2023; Wright, Zammuto, & Liesch, 2017), but also the scope and depth of practice transformation within organizational settings.

Third, our study sheds light on how early collaborative arrangements may shape the organizational positioning of nascent occupations over time. Our findings suggest that these formative interactions can significantly influence whether emerging roles remain peripheral or become more deeply integrated within established structures. In our case, the structured collaboration in fixed-income investing positioned RI analysts primarily as providers of supplementary inputs at predefined decision points—creating conditions that constrained their longer-term influence within that investment domain. In contrast, generative collaboration in equity investing enabled substantive involvement in core decision-making processes, creating conditions for deeper integration and recognition. These insights contribute to research on occupational emergence by highlighting how initial collaborative pathways can shape the trajectories through which nascent occupations gain recognition and develop influence within organizations (Fayard et al., 2017; Murphy & Kreiner, 2020).

The above theoretical insights also offer practical guidance for organizations integrating new roles that operate in “supportive” capacities—that is, roles designed to bridge gaps between established professional practices and emerging organizational demands. Our study suggests that successful integration depends not only on formal inclusion and opportunities for interaction, but also on how asymmetries in expertise and authority are negotiated at the outset of collaboration. Organizational arrangements that deliberately engage these asymmetries can shape the degree to which such roles are recognized as substantive contributors rather than remaining primarily peripheral to core decision processes. More broadly, these insights can inform strategies that foster cross-occupational innovation in contexts where evolving business and societal imperatives increasingly challenge conventional boundaries of expertise and authority.

Theoretical Grounding

Inter-occupational collaboration and knowledge co-creation

Organizations increasingly rely on collaboration across occupational boundaries to develop knowledge and drive innovation, particularly as work becomes more complex and specialized (Barley, Treem, & Kuhn, 2018; Okhuysen & Bechky, 2009; Zahra, Neubaum, & Hayton, 2020). While such collaboration can enhance organizational capabilities by bringing together diverse expertise, it often presents significant challenges—whether from incompatible knowledge bases that hinder information sharing (Bechky, 2003b; Black, Carlile, & Repenning, 2004; DiBenigno & Kellogg, 2014) or power dynamics that undermine cooperation (DiBenigno, 2020; Huising, 2015; Kellogg, 2019). Studies have documented, for instance, how mismatches in epistemological knowledge bases can create communication barriers, impeding knowledge transfer and exchange between collaborators (Alvesson, 2000; Kellogg, Orlikowski, & Yates, 2006). Similarly, asymmetries in power and status can lead more powerful counterparts to dismiss or devalue the contributions of less powerful counterparts (Briscoe, Maxwell, & Temin, 2005; Huising, 2015; Sandholtz & Burrows, 2016).

Research on inter-occupational collaboration has identified two broad approaches for addressing these challenges. The first focuses on structural mechanisms that facilitate knowledge exchange across occupational boundaries (Anteby et al., 2016; Carlile, 2004). Studies of boundary objects show how shared artifacts, such as common lexicons or models, enable coordination by making specialized knowledge accessible across domains (Bechky, 2003a; Spee & Jarzabkowski, 2009). Similarly, studies of “trading zones” highlight how designated spaces for negotiation and exchange make the work of different occupational groups “visible and legible to each other” (Kellogg et al., 2006, p. 22). These structural mechanisms enable collaborators to move beyond occupational differences and align their efforts, without requiring deep mutual understanding of their respective domains (Barley et al., 2018; Truelove & Kellogg, 2016; Zahra et al., 2020).

Beyond structural mechanisms, a second approach emphasizes relational strategies that address the interpersonal dimensions of collaboration. This perspective recognizes that effective collaboration depends not only on bridging knowledge differences but also on fostering the interpersonal trust and mutual respect often necessary for knowledge sharing and co-development (Fincham, Clark, Handley, & Sturdy, 2008; Garman et al., 2006). For instance, DiBenigno (2020) documents how mental health professionals used “rapid relational tactics” to elicit cooperation from military commanders despite lacking formal authority. Similarly, Sandefur (2015) highlights the role of relational expertise in professional work, showing that lawyers’ effectiveness depends as much on their ability to navigate relationships with clients, judges, and stakeholders as on their legal knowledge. This dynamic is particularly pronounced in service-oriented settings, where professionals frequently engage clients who “may not feel they need or may not appreciate professional advice” (Huising, 2015, p. 264). These examples underscore the importance of relational work in contexts where achieving successful outcomes requires not only technical expertise but also the ability to secure acceptance and deference from others (Anteby et al., 2016; Kahl, King, & Liegel, 2016).

Taken together, these streams of research have generated valuable insights into how knowledge is managed and shared across occupational boundaries (Carlile, 2004; Nonaka, Von Krogh, & Voelpel, 2006). However, much of this work is grounded in studies of established occupations—those with clearly defined roles and institutionally recognized knowledge bases (Abbott, 1988; Van Maanen & Barley, 1984). This emphasis on “expert talking to expert” (Fincham et al., 2008, p. 1149) tends to overlook the distinctive position of nascent occupations, whose members must navigate collaborative work without the benefit of recognized expertise or jurisdictional authority (Fayard et al., 2017; Kitay & Wright, 2007; Sandholtz & Burrows, 2016). While structural mechanisms enable knowledge exchange across established occupational boundaries (Carlile, 2002; Kellogg et al., 2006), they presuppose that each party brings a well-defined knowledge base to the collaboration. Similarly, relational strategies for building influence depend on opportunities to demonstrate capability and credibility (DiBenigno, 2020; Huising, 2015)—opportunities that may be limited for nascent occupation members. This raises important questions about how collaboration unfolds in contexts where one party’s expertise is still emerging and lacks formal institutional validation (Augustine, 2021; Vough, Cardador, Bednar, Dane, & Pratt, 2013).

Professionalization and emerging forms of expertise

Understanding how expertise develops and gains recognition requires examining both traditional pathways of professionalization and the emerging trajectories of new occupational roles. Occupations refer to organized groups of individuals performing similar types of work, often characterized by specialized skills in particular task domains (Nelson & Irwin, 2014; Van Maanen & Barley, 1984). Professions form a subset of occupations that have achieved high status and social legitimacy through the institutionalization of their expertise (Anteby et al., 2016; McMurray, 2011). This process of institutionalization typically involves credentialling mechanisms and the establishment of jurisdictional boundaries that define what counts as expertise, who is authorized to apply it, and under what conditions (Abbott, 1988; Kirkpatrick, Aulakh, & Muzio, 2021). These mechanisms position professions as gatekeepers of socially valued, scarce, and distinctive knowledge (Collins, Evans, & Gorman, 2007).

Within these institutionalized frameworks, expertise is traditionally understood to develop through a combination of formal education and informal socialization, whereby technical knowledge is reinforced through tacit understandings and experience-based judgment (De Jong & Ferguson-Hessler, 1996; Muzio, Kirkpatrick, & Kipping, 2011; Nicolini et al., 2017). Research on professions often highlights exclusivity, with jurisdictional boundaries safeguarding specialized knowledge and authority from encroachment by other groups (Abbott, 1988; Currie, Finn, & Martin, 2010). This perspective conceives expertise as relatively stable and bounded—rooted in defined knowledge domains and legitimized by the authority to act within them. It also draws a distinction between knowledge and expertise, emphasizing that expertise requires not only knowledge and competence, but also the social recognition and institutional validation to exercise authority (Gustafsson & Lidskog, 2018; Kellogg et al., 2006; Treem & Barley, 2018).

Recent occupational developments have given rise to “supportive” roles—such as climate change analysts, AI ethics advisors, and responsible investment analysts—that challenge conventional models of expertise development and legitimation. While these occupations vary in form and function, many operate at the intersection of multiple domains. Their work involves embedding emerging priorities into established organizational routines (Arjaliès & Durand, 2019; Augustine, 2021; Kitay & Wright, 2007). Unlike traditional professions that derive authority from credentialed knowledge and jurisdictional control, these roles often gain influence by enhancing or adapting dominant practices. Because their mandate is carried out “through” ongoing interactions with others, their expertise tends to be co-produced—shaped in relation to those who already hold recognized authority. In such contexts, established professionals serve as “signifiers of quality” (Cross & Swart, 2021, p. 1713; Hodgson, Paton, & Muzio, 2015), whose acceptance or rejection plays an important role in legitimizing new contributions. Absent conventional markers of authority, members of these nascent occupations rely on collaborative processes to make their work visible and credible within dominant professional domains (Anteby et al., 2016; Fayard et al., 2017; Fincham et al., 2008).

This reliance on collaboration creates a distinctive challenge for many nascent occupations. Members must develop sufficient understanding of established domains to engage effectively, while also contributing to the co-creation of new knowledge intended to transform the very practices they aim to influence. As such, established professionals and nascent occupation members enter collaboration from different positions: the former draw on recognized authority and familiar frameworks, while the latter navigate unfamiliar terrain they seek to reshape. To investigate these dynamics, we examine how “first-generation” responsible investment (RI) analysts collaborated with asset management professionals to incorporate environmental, social, and governance (ESG) criteria into conventional financial analyses.

Methods

Research setting

The emergence of socially responsible investment (SRI) in France was closely tied to broader debates about the role of financial markets in society. In the mid-2000s, the French government’s decision to introduce private retirement funds sparked widespread public controversy. Critics warned that this move could undermine France’s traditional social welfare model by promoting a form of Anglo-Saxon capitalism that prioritized profit at the expense of collective well-being. These concerns created an opportunity for investment firms to position SRI funds as a way to safeguard capitalism “à la Française”—framing these funds as balancing financial returns with positive social and environmental impact.

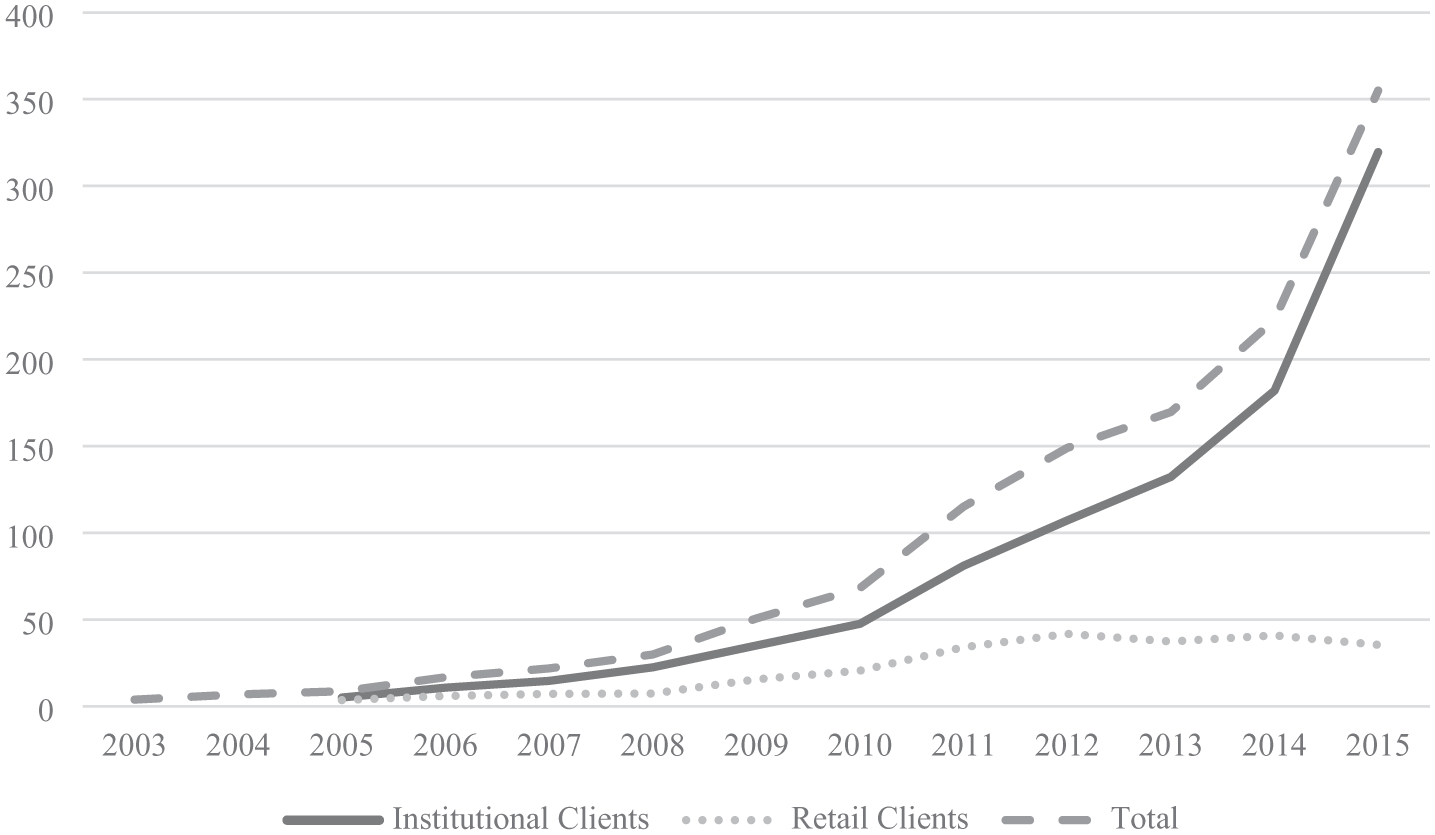

The growing demand for SRI led many French investment companies to introduce SRI funds that incorporated ESG criteria into conventional financial analyses (see Figure 1 illustrating the growth of French SRI assets). However, this integration was largely fragmented and ad hoc, as there was no consensus on what constituted “socially responsible investing” nor established guidelines for developing SRI funds. The nascent state of the field meant that expertise had to be cultivated from the ground up. In the early 2000s, fewer than two dozen RI analysts in the French asset management industry worked with SRI funds, and there were no formal training programs or professional certifications specific to the field. By 2015, however, SRI had gained mainstream acceptance in France, as reflected in the incorporation of responsible investment courses in business school curricula and the development of professional certification programs (Crifo, Escrig-Olmedo, & Mottis, 2019; Gond & Boxenbaum, 2013).

Growth of French SRI assets (EUR billion) (Source: Novethic).

Our study focuses on Alpha (pseudonym), a subsidiary of one of France’s largest mutual insurance companies. Despite being an early mover in SRI—having introduced funds that incorporated ESG criteria as early as 1998—Alpha’s position as a pioneer had eroded as competitors introduced their own SRI offerings. By the mid-2000s, when Alpha managed approximately €2 billion in assets with about 25 employees, the company was struggling to maintain its competitive position.

In response to Alpha’s declining position in the SRI market, its board of directors appointed new leadership in 2006, including a new CEO and a director of development & SRI. One of their first initiatives was establishing an SRI research analysis department staffed with four “first-generation” RI analysts. The analysts were deliberately selected for their diverse backgrounds: a former trade unionist brought experience in labor relations and corporate governance, a former analyst from a social rating agency contributed experience in ESG evaluation frameworks, a recent graduate from a prestigious business school in France offered fresh analytical perspectives, and a PhD candidate—who is also a co-author—provided institutional knowledge and research expertise, having previously worked in Alpha’s parent company. Despite their relevant and diverse backgrounds, none of the newly hired RI analysts had expertise in financial investment or prior experience in developing SRI funds.

About four months after establishing the SRI department, Alpha’s leadership created a temporary working group to develop and market the firm’s new SRI funds. This group brought together eight representatives from three departments: sales, asset management, and the newly formed SRI unit. Initially, Alpha’s leadership assumed that asset managers working with fixed-income and equity investments were similar enough to be included within a single working group. However, fundamental differences emerged in how each group of asset managers approached investment decisions and collaboration with RI analysts. These differences led to the working group splitting into two sub-groups, with RI analysts working separately with fixed-income and equity asset managers to develop SRI knowledge and investment funds.

Three RI analysts participated in both the fixed-income and equity working groups, alongside the director of development & SRI and his project manager. Each group included the respective department head (fixed-income or equity) and their assistant, while the CEO (also an equity asset manager) attended both groups periodically. While the working groups comprised a relatively small number of individuals, their activities were embedded within Alpha’s broader organizational structure and overseen by the parent company. The asset management department included six additional asset managers specializing in fixed-income and equity, and one managing funds that included both asset classes. Although these asset managers did not participate directly in the working groups, they were kept informed and provided feedback regularly. The heads of fixed-income and equity met weekly with the parent company’s director of finance and Alpha’s CEO to report on portfolio performance and proposed changes to the investment processes. This oversight structure ensured that the working groups’ decisions aligned with Alpha’s strategic objectives, as well as broader market practices.

Research design and data sources

Our research design employed an ethnographic approach to develop a “thick” understanding (Geertz, 1973) of how members of a nascent occupation collaborated with established professionals to co-create knowledge and transform existing practices. Between 2006 and 2015, we collected data through participant observation, semi-structured interviews, organizational documents, and field-level sources.

Participant observation

The core of our data collection centered on participant observation, which enabled us to track how collaborations evolved over time. The participant observer worked as an RI analyst at Alpha between 2006 and 2009. This privileged access was granted through a national French research agreement, which fosters partnerships between academic institutions and companies. 1 All managers and employees were informed about the researcher’s dual role as both an academic observer and an RI analyst, ensuring transparency throughout the data collection process.

Following reflexive ethnographic approaches (Golden-Biddle & Locke, 1993; Whyte, 1943), the participant observer maintained detailed field notes documenting daily observations, key events, and interpersonal exchanges, along with reflective memos capturing personal experiences and interpretations as an RI analyst. To mitigate potential biases and maintain analytical distance, the participant observer met regularly with the other members of the research team who served as a sounding board, questioning assumptions and offering alternative interpretations of events and interactions (Clark, Gioia, Ketchen Jr, & Thomas, 2010; Darlington & Scott, 2020; Überbacher, Jacobs, & Cornelissen, 2015).

Interviews

We conducted interviews in three waves to trace the evolution of collaboration between RI analysts and asset managers. The first wave in 2006 focused on gaining a general understanding of Alpha’s existing investment practices through interviews with key organizational members, including fund managers, financial analysts, senior leadership, and support staff. The second wave, conducted in 2009 after the working group had disbanded, gathered multiple perspectives on how the collaboration unfolded—specifically from working group members, other asset managers, and clients. The third wave, conducted between 2013 and 2015, explored specific incidents and interactions that multiple informants had identified as particularly significant. These interviews allowed us to probe more deeply into key turning points in the collaboration and the evolving relationship between RI analysts and asset managers.

Organizational documents

We collected and analyzed organizational documents to identify how knowledge and practices evolved over time. These documents included internal process documents (e.g., iterations of SRI and financial investment tools with supporting methodological guides, minutes of working group meetings, and company factsheets combining SRI and financial analyses), client-facing materials (e.g., marketing materials and fund overviews and requests for proposal detailing Alpha’s SRI capabilities to potential clients), and communication records (e.g., internal memos and presentations used to communicate changes to the broader organization, and email exchanges between working group members that captured real-time interactions).

External field-level data

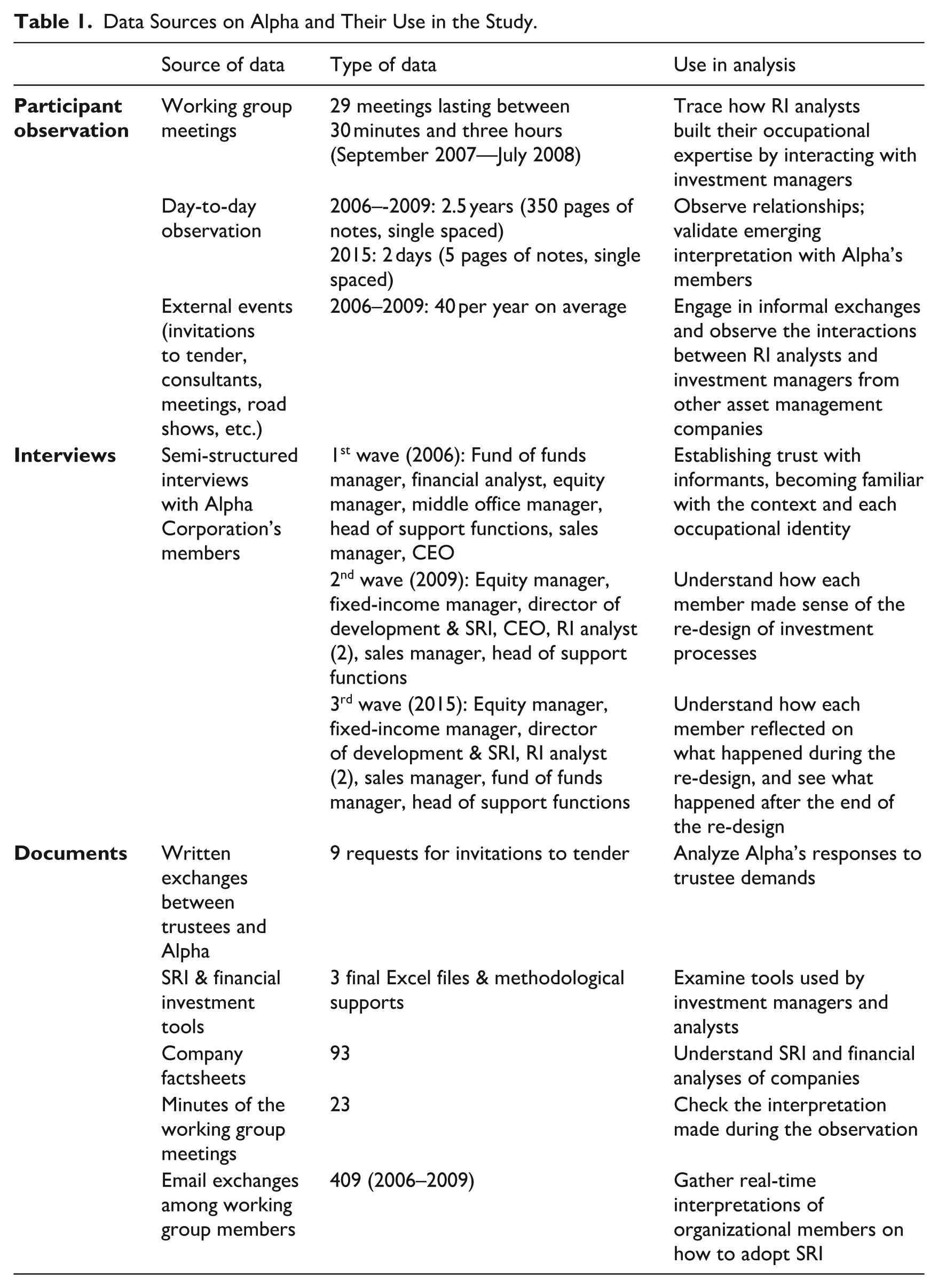

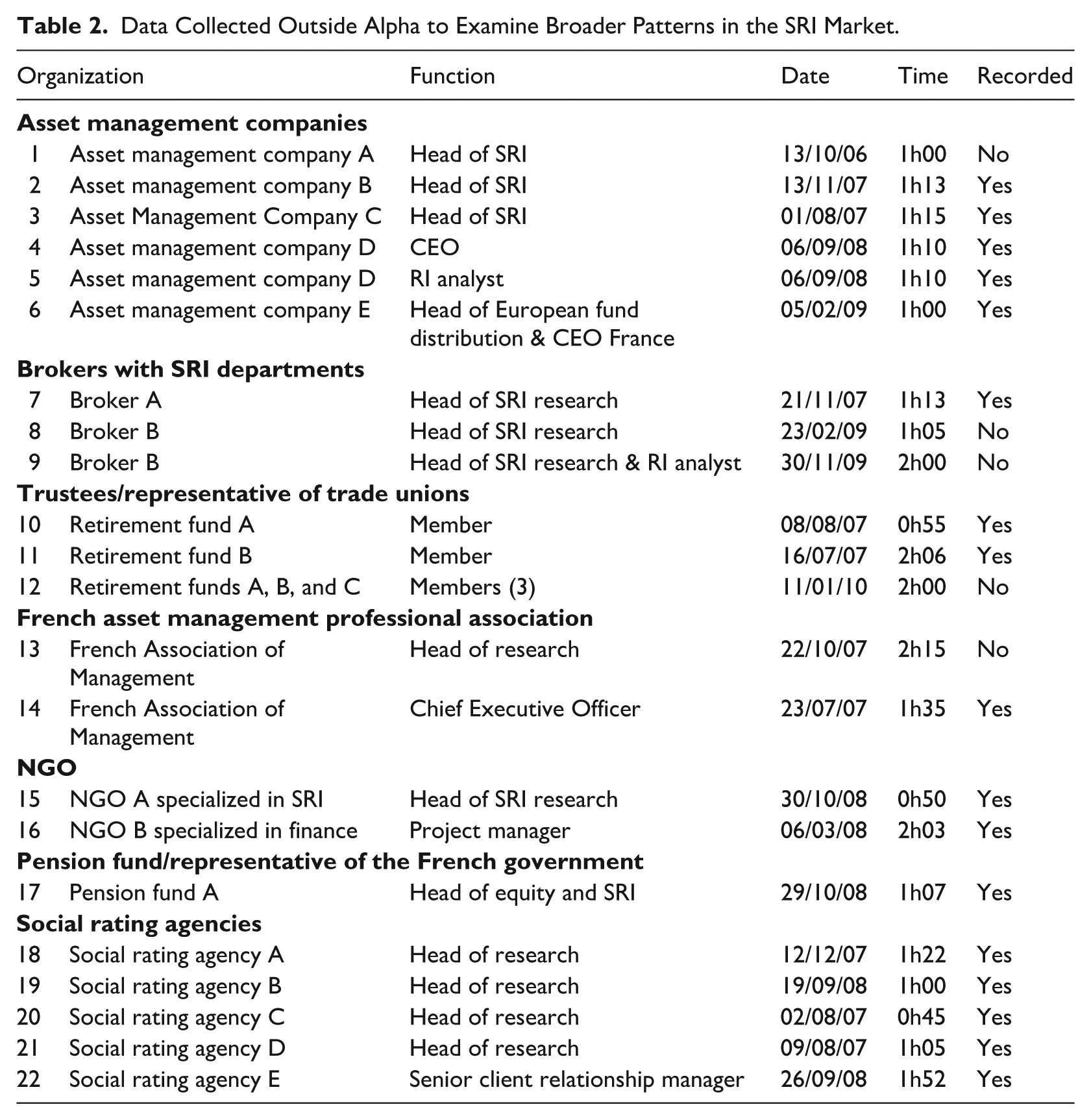

To understand whether Alpha’s experiences reflected broader industry patterns, we gathered additional field-level data through interviews with RI analysts and asset managers at other investment companies, observation of industry events, and analysis of secondary sources (e.g., professional publications, competitor materials, and French media coverage of SRI). This contextual data enabled us to confirm that the collaborative dynamics we observed were not unique to Alpha but representative of wider industry challenges during the rise in demand for SRI funds in France. Table 1 and Table 2 provide a detailed overview of the main data sources used in this study.

Data Sources on Alpha and Their Use in the Study.

Data Collected Outside Alpha to Examine Broader Patterns in the SRI Market.

Data analysis

Our analysis followed an iterative, abductive process that involved moving between data, emerging concepts, and the literature on occupational collaboration and expertise development. During the data collection process, we became aware of differences in the nature of interactions between RI analysts and two teams of asset managers—those managing fixed-income investments versus those handling equity investments. This observation prompted us to probe more deeply into the sources of these divergences and their implications for collaborative processes.

Following Huising (2015), we first identified and collated all data detailing interactions among working group members, including formal meetings, instances of conflict and disagreement, and more informal encounters. We used field notes, organizational documents (e.g., email correspondence and meeting minutes), and interview data to construct detailed chronologies of events. Interview accounts provided nuanced perspectives on key moments, allowing us to synthesize these insights into a “composite narrative” that captured recurring patterns and dynamics across multiple instances (Jarzabkowski, Bednarek, & Lê, 2014, p. 281).

To deepen our understanding, we compiled case reports that chronicled the content and context of interactions within the working group—e.g., noting what was said, done, and accomplished during meetings and how our informants described or recalled key interactions. Drawing from informants’ descriptions, we developed “impressions” that denoted the tone and tenor of interactions, using descriptions such as wary orskeptical, open, curious, or antagonistic. Throughout this process, we regularly compared our “embryonic ideas” with concepts from existing literature to refine our interpretations (Howard-Grenville, Metzger, & Meyer, 2013; Raynard, Lu, & Jing, 2020). We also shared our reports and ideas with select informants inside and outside Alpha to ensure that our interpretations aligned with their experiences and perspectives.

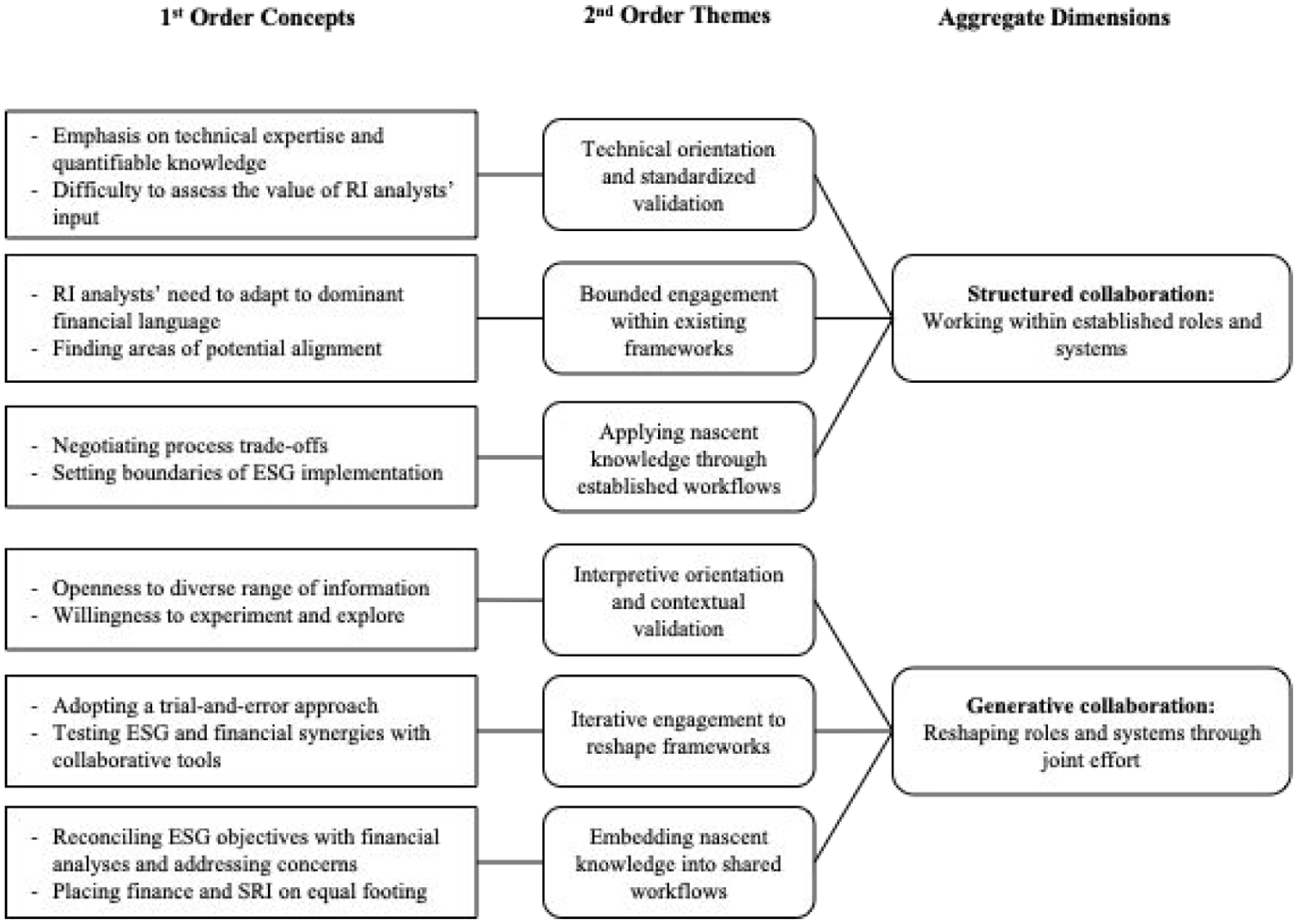

Our initial coding focused on understanding collaborative challenges and approaches to knowledge development and practice transformation. As we compared case reports and emergent codes, systematic differences emerged in how RI analysts engaged with fixed-income versus equity asset managers. For example, in analyzing interactions within the fixed-income working group, we coded statements emphasizing “technical expertise and quantifiable knowledge” and expressions of “difficulty assessing the value of RI analysts’ input.” In the interactions in the equity working group, we coded phrases that highlighted an “openness to diverse information sources” and “willingness to experiment and explore.” The “salience and consequences” of these differences (Huising, 2015, p. 270) became clearer as we examined their implications for collaboration dynamics and knowledge integration. This prompted us to revisit the data and refine our coding schema to focus on aspects such as how knowledge was shared and managed, approaches to task definition and execution, attitudes toward collaboration, and the development of tools and practices.

Through focused coding, we identified recurring patterns that we distilled into broader themes reflecting the distinct dynamics of collaboration between RI analysts and asset managers (see Figure 2). For example, codes highlighting fixed-income asset managers’ emphasis on technical mastery and the need for RI analysts to “adapt to dominant financial language” informed the themes “technical orientation and standardized validation” and “bounded engagement within existing frameworks.” Conversely, codes capturing equity asset managers’ openness to diverse information and how they worked with RI analysts to identify and test potential areas of synergy informed the themes “interpretive orientation and contextual validation” and “iterative engagement to reshape frameworks.”

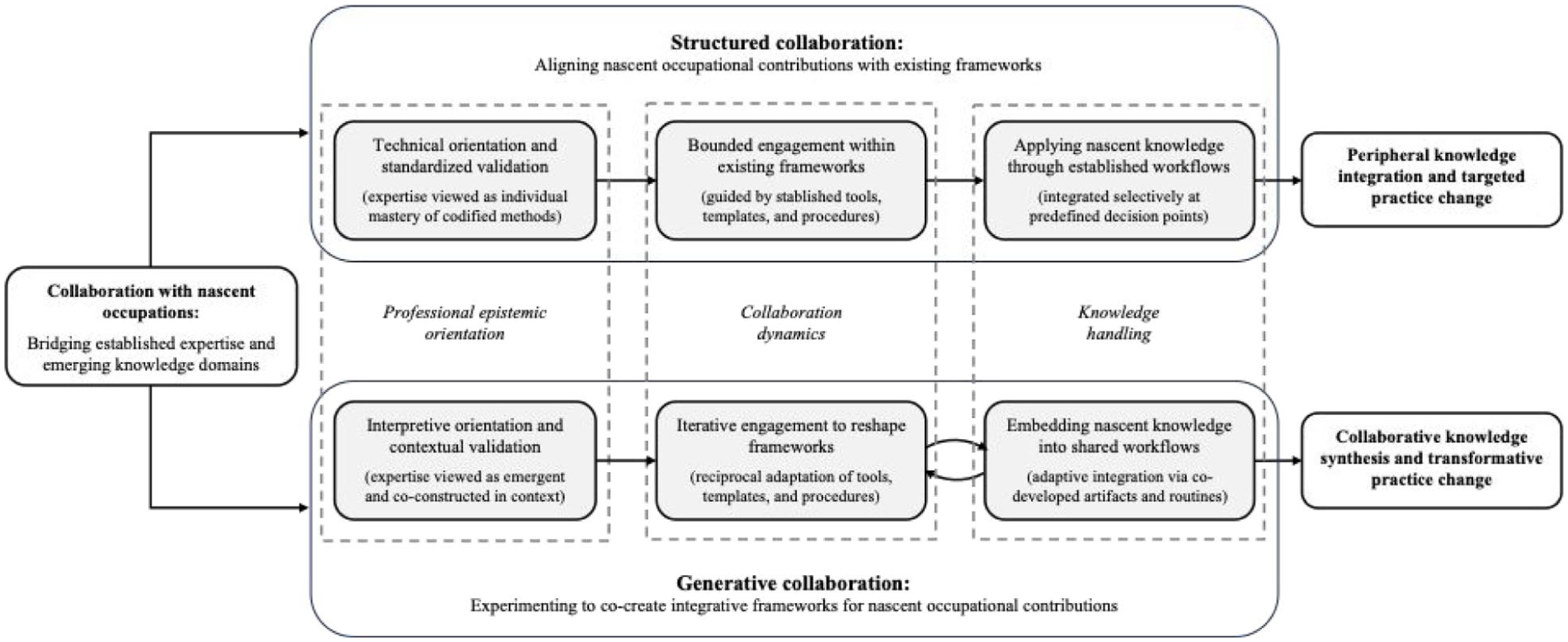

Data structure.

Following this analytical process of abstraction (Grodal, Anteby, & Holm, 2021; K. Locke, Feldman, & Golden-Biddle, 2022), we identified two overarching dimensions that captured fundamentally different pathways for collaboration. We labeled these aggregate dimensions “structured collaboration” and “generative collaboration.” To further refine our understanding of these pathways, we revisited the literature on inter-occupational collaboration—focusing on how our findings might extend existing theoretical frameworks. This step involved examining the interplay among the structural characteristics of asset management domains, prevailing conceptions of expertise, and the adaptive strategies employed by RI analysts. By situating our observations in contexts where one party’s knowledge is emergent and lacks institutional recognition, we identified key factors that shape collaborative knowledge co-creation and enable practice transformation. These insights informed the development of a conceptual model that delineates how different collaborative pathways enable the integration of nascent occupational contributions into established professional domains.

Findings

Our analysis revealed two distinct collaborative pathways through which RI analysts and asset management professionals worked to develop SRI knowledge and integrate ESG criteria into conventional financial analyses: structured collaboration in fixed-income investment and generative collaboration in equity investment. Although both pathways led to changes in investment processes, they diverged significantly in their underlying dynamics and outcomes. In fixed-income investing, collaboration centered on aligning ESG criteria with existing models and workflows, thereby minimizing disruption. In equity investing, by contrast, collaboration involved sustained, iterative engagement that enabled more transformative changes to established practices and decision-making routines.

Below, we detail how these two pathways unfolded, highlighting the key dynamics that shaped the co-creation of SRI knowledge and the adaptation of investment practices within each asset class. Figure 3 presents the model developed through our analysis, depicting how differences in domain orientations, collaborative approaches, and evaluative criteria gave rise to distinct patterns of engagement and influence.

Collaborative pathways for knowledge co-creation: Bridging nascent occupational knowledge and established expertise.

Structured collaboration: Working within established roles and systems

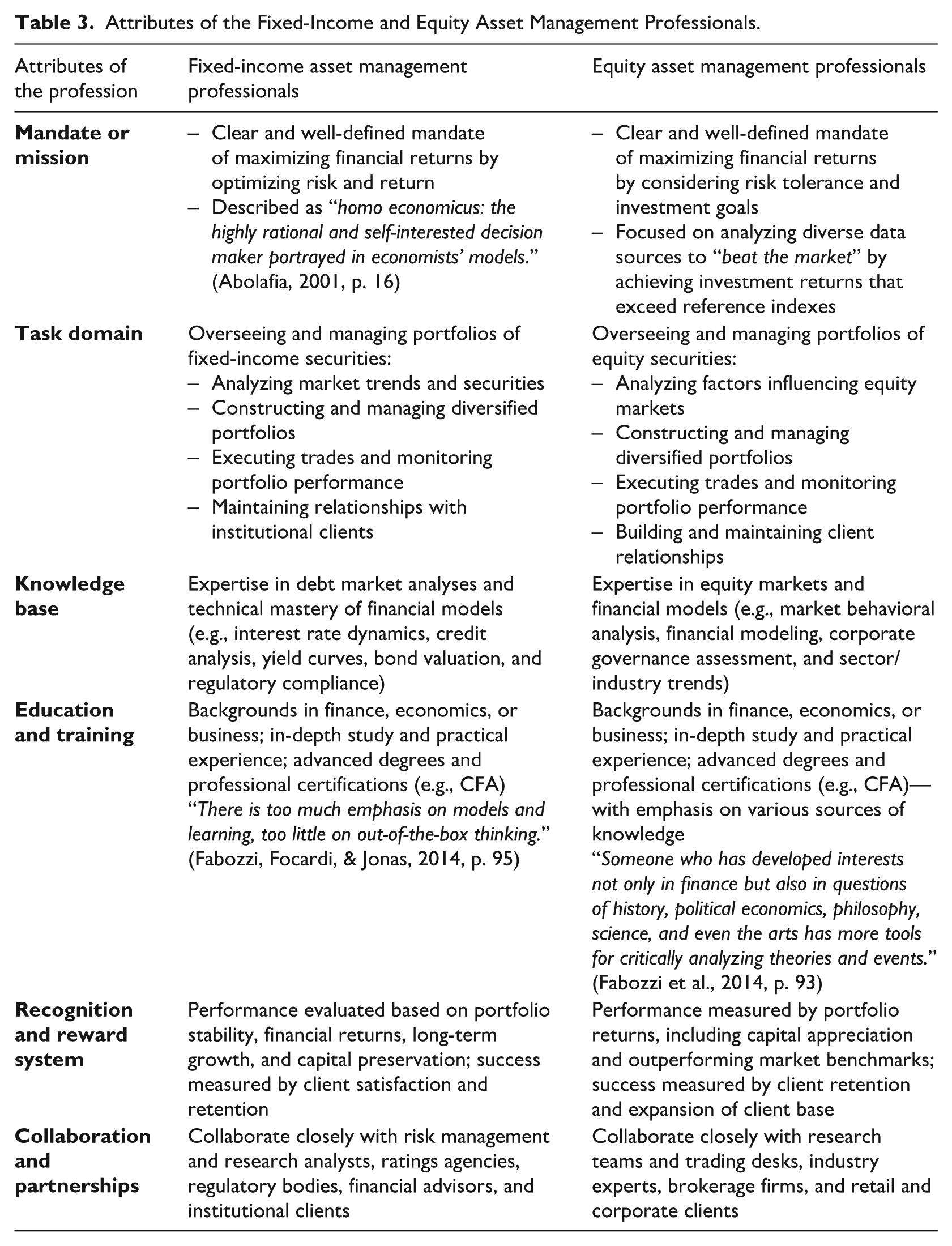

The collaboration between RI analysts and fixed-income asset managers illustrates the complexities of integrating nascent occupational knowledge into a highly structured and technical professional domain. Fixed-income investing, which involves managing debt securities that generate regular interest payments, relies on systematic methods and quantitative models to assess creditworthiness and manage financial risk (see Table 3). Within this context, the engagement between RI analysts and fixed-income asset managers took the form of what we call “structured collaboration”—a collaborative pathway in which the contributions of the nascent occupation were carefully bounded and adapted to align with established frameworks rather than substantially transforming them.

Attributes of the Fixed-Income and Equity Asset Management Professionals.

In what follows, we trace how this collaboration unfolded, showing how epistemic assumptions about expertise in fixed-income investing, the procedural demands of the domain, and the adaptive efforts of RI analysts shaped a process that incorporated new inputs while preserving core practices.

Technical orientation and standardized validation

Fixed-income investing privileges technical expertise and standardized validation processes, with mastery of complex financial models forming the foundation of professional identity. As one fixed-income asset manager explained: “You choose what you want to be at the beginning of your career. I am more the kind of rational person who likes it when things are clear and when phenomena can be traced through models” (fixed-income manager). Within this domain, expertise was understood as residing “within” individuals—acquired through formal training and certified through model-based performance.

This emphasis on technical mastery created significant barriers for RI analysts, who were perceived as lacking the requisite credentials to contribute meaningfully. Illustrating this perspective, one head of fixed-income remarked: Even people who work full time in the firm, who have genuine [asset] management functions, who have been working in the place for 20 years—I think even those guys only have a vague, compartmentalized view. (fixed-income manager)

To support their decision-making processes, fixed-income asset managers cultivated relationships with external experts who could provide “reliable,” quantifiable inputs (field notes, 2007). These included economists at major banks, who provided projections on central bank interest rates, and financial analysts at brokerage firms, who supplied detailed credit ratings. This reliance on codified information was evident in how these asset managers described the nature of expertise in their domain, for example: Fixed-income investment is technically more challenging to grasp than equity investment. [. . .]. It’s also much less publicized . . . just watch the TV news, the 8 o’clock news, . . . they talk about stocks, they talk about dividends, people know what a dividend is. Now, understanding what . . . a yield curve is, what a spread is, these are things that require. . . an understanding of actuarial calculations. (fixed-income manager; emphasis added)

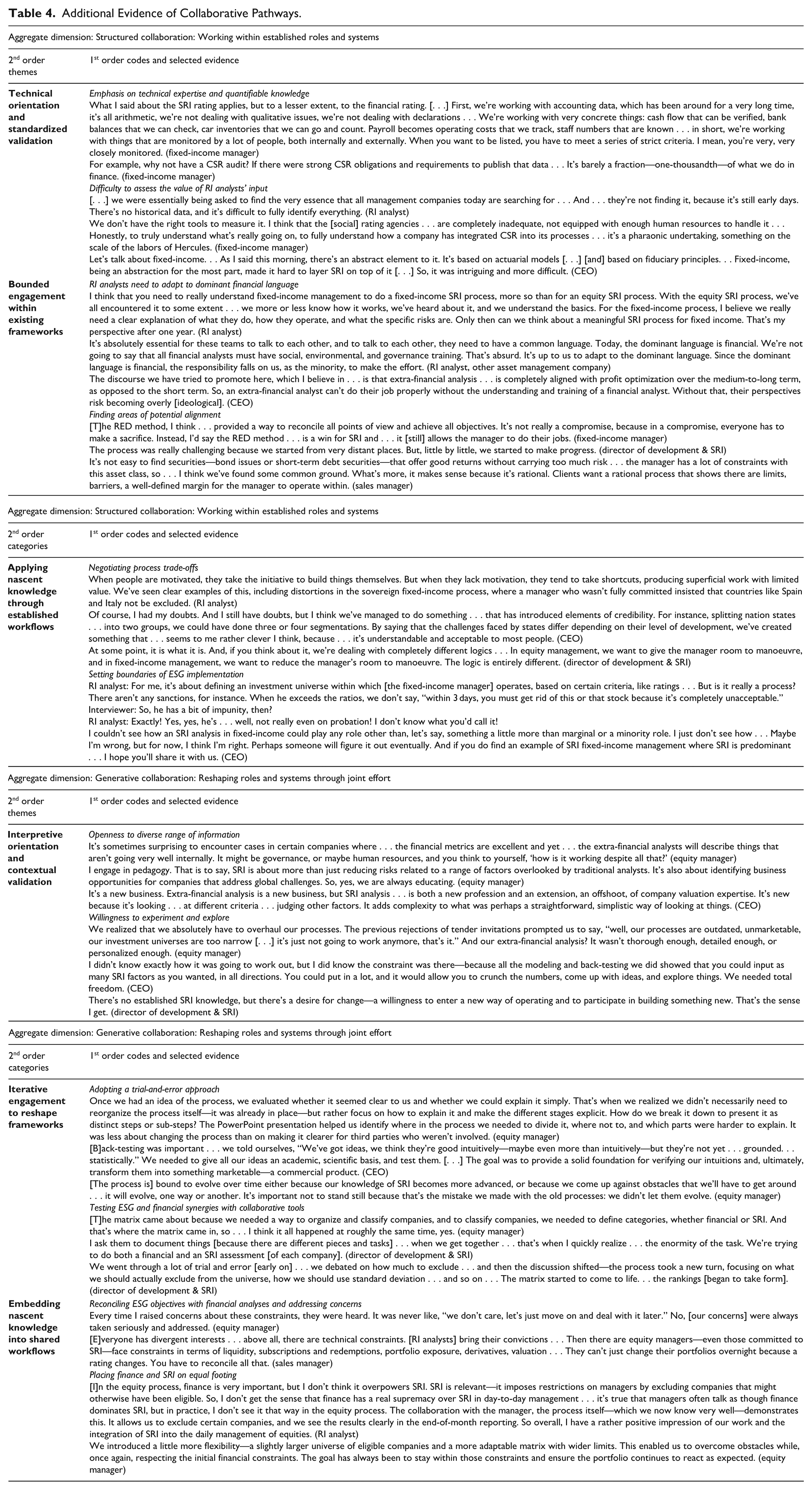

For RI analysts, the model-based orientation posed a steep learning curve as they worked to establish credibility and demonstrate the relevance of ESG criteria (see Table 4 for additional supporting evidence). Reflecting on this early period, one RI analyst candidly noted: “When I arrived, I had no idea what an SRI process was. I had no idea about it because, in a rating agency, you do your ratings, but then you don’t really know how they are used” (RI analyst). This learning process was further complicated by skepticism from fixed-income asset managers, who viewed the RI analysts’ early ESG assessments as “arbitrary” and “not serious”—a perception captured in the field researcher’s account in her role as an RI analyst: Today, I had a meeting with the head of the FI team. He wanted me to do an SRI report to respond to an invitation to tender. I showed him what I had already done in terms of analysis of extra-financial criteria. But for him, what we do in the SRI division is not serious at all, and the criteria we use are arbitrary, according to him. (RI analyst, field diary 2007)

2

Additional Evidence of Collaborative Pathways.

The head of fixed-income articulated his team’s concerns about the lack of rigour in ESG analysis using an analogy that compared it to weather forecasting without reliable instruments: It’s as if, for example, you had to do weather forecasting and . . . we asked if the study of pressure could be useful, and in fact, we had no barometer—no reliable barometer. Yes, it’s useful, but you can’t measure it, so there’s no point in being interested in it because you can’t measure it. (fixed-income manager)

This analogy underscored the expectation for standardized, measurable inputs, reinforcing the view that ESG data—unless quantifiable—could not be meaningfully integrated into fixed-income decision-making. Fixed-income asset managers expected RI analysts to show how ESG criteria impacted financial performance—ideally in ways that could be modeled without disrupting established analytical routines. As the field researcher later observed, this expectation resembled a search for “the philosopher’s stone of responsible investing” (RI analyst, field diary 2009). It placed RI analysts in the challenging position of having to demonstrate not only the credibility but also the compatibility of their contributions within the technical, model-driven logic of fixed-income investing.

Bounded engagement within existing frameworks

Despite early barriers to collaboration, interactions between RI analysts and fixed-income asset managers revealed areas of potential alignment—particularly where ESG criteria intersected with investment priorities. Governance-related issues, in particular, drew interest as indicators of issuer reliability and long-term stability: “Governance can be something positive. That’s why I asked [RI analysts] to try and study the link between governance and defects . . . Honestly, apart from governance, I think [the social aspect] is an illusion” (fixed-income manager).

Building on this narrow point of convergence, RI analysts sought to frame ESG considerations in ways that emphasized their relevance to risk management. They developed an initial “SRI constraint” aimed at screening out issuers with poor ESG performance, modeling it after the constraints and screening practices fixed-income asset managers used to manage credit risk and sector exposure. However, when presented to an external consultant, the feedback was discouraging, as the constraint was deemed “inadequate for effectively excluding issuers with poor ESG performance” (field notes, 2007).

Shifting their approach, RI analysts consulted with social rating agencies and heads of SRI at other firms to develop a classification system to identify “SRI stars” and “SRI laggards.” They proposed excluding companies in the bottom quartile, arguing that such exclusions could mitigate ESG-related risks to issuers’ financial viability and, by extension, the financial performance of investment funds. However, this proposal met strong opposition from the fixed-income team, who dismissed exclusionary criteria as “too radical” and “incompatible with financial management” (field notes, 2008). They explained to RI analysts that in some markets, only a single issuer was available—meaning that exclusions would prevent the team from investing in those markets altogether.

A particular point of contention was the exclusion of countries such as Greece and Italy, which had poor SRI grades but offered attractive risk–return profiles. Expressing his team’s frustration, the head of fixed-income argued that what the RI analysts were proposing would prevent them from fulfilling their professional mandate, comparing it to “asking an architect to build an 80-floor building with bamboo” (fixed-income manager). He went on to assert that investment decisions should remain the responsibility of asset managers, not the RI analysts: [The decision] has to come from the investment side, and not [because] today, SRI has decided they are interested in nuclear power. I don’t care. There’s no nuclear sector; it’s all public, and they don’t issue [bonds]. I’m not interested in nuclear power. [. . .] I don’t think that’s how investment decisions should work. (fixed-income manager)

The fixed-income team’s strong negative response to the proposed SRI constraint led RI analysts to reassess their strategy: they needed to better understand how fixed-income investment decisions were made before offering further recommendations. As an RI analyst explained, “[we] don’t know enough about what fixed-income asset managers really do to make more meaningful suggestions . . . we need a more detailed understanding of their practices, how they work, how they conceptualize risks” (RI analyst).

In their interactions with the fixed-income team, RI analysts emphasized that their objective was “not to restrict the investment options of fixed-income managers” or to “simply rate the portfolio from an SRI perspective” (field notes, 2008). This clarification led both sides to agree on “finding a solution that would enable fixed-income managers to preserve their operational freedom while adhering to SRI standards” (field notes, 2008). Rather than attempting to overhaul existing decision-making processes, the focus shifted to identifying specific decision points where ESG criteria could be integrated with minimal disruption to established workflows in fixed-income.

A key breakthrough came when they began mapping out absolute “no-go” boundaries for fixed-income asset managers. Among these were strict exclusionary criteria based on SRI profiles—as noted by the field researcher: “The head of the group did not allow us to exclude companies or countries from his investment universe” (RI analyst, field diary, 2008). The fixed-income team explained to RI analysts why simply identifying “SRI stars” had limited practical value: We had to explain to [them] . . . that it was fine to create lists, that it was fine to say . . . that the most socially responsible country was perhaps the Congo or that such and such a company was super socially responsible . . . but that if they didn’t issue [bonds], in concrete terms, we couldn’t buy them; and that if they did issue, but the bond was badly rated . . . or there weren’t enough details [about it], or it wasn’t liquid, then it wasn’t [a viable option] to go into it. (fixed-income manager)

Applying nascent knowledge through established workflows

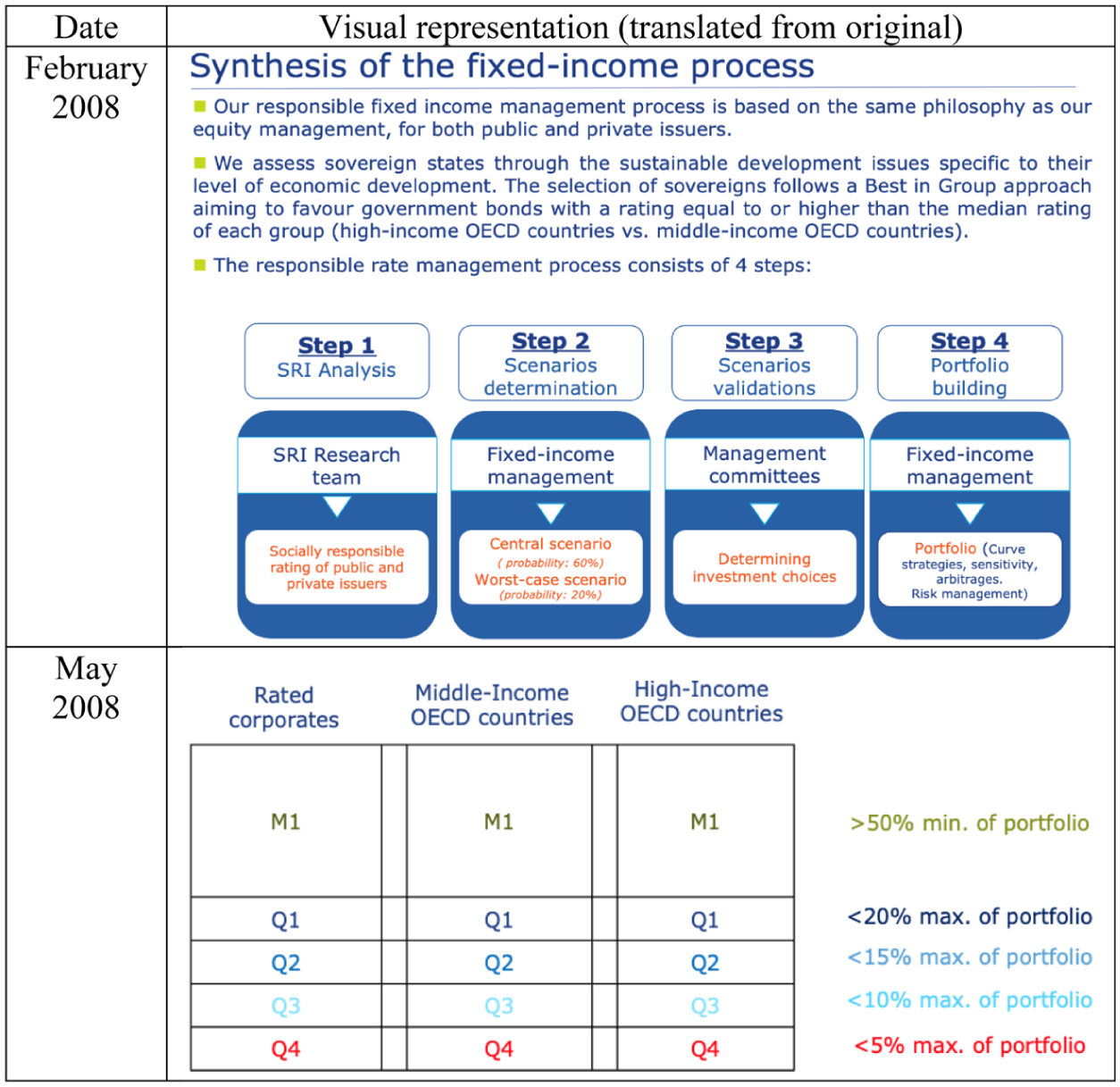

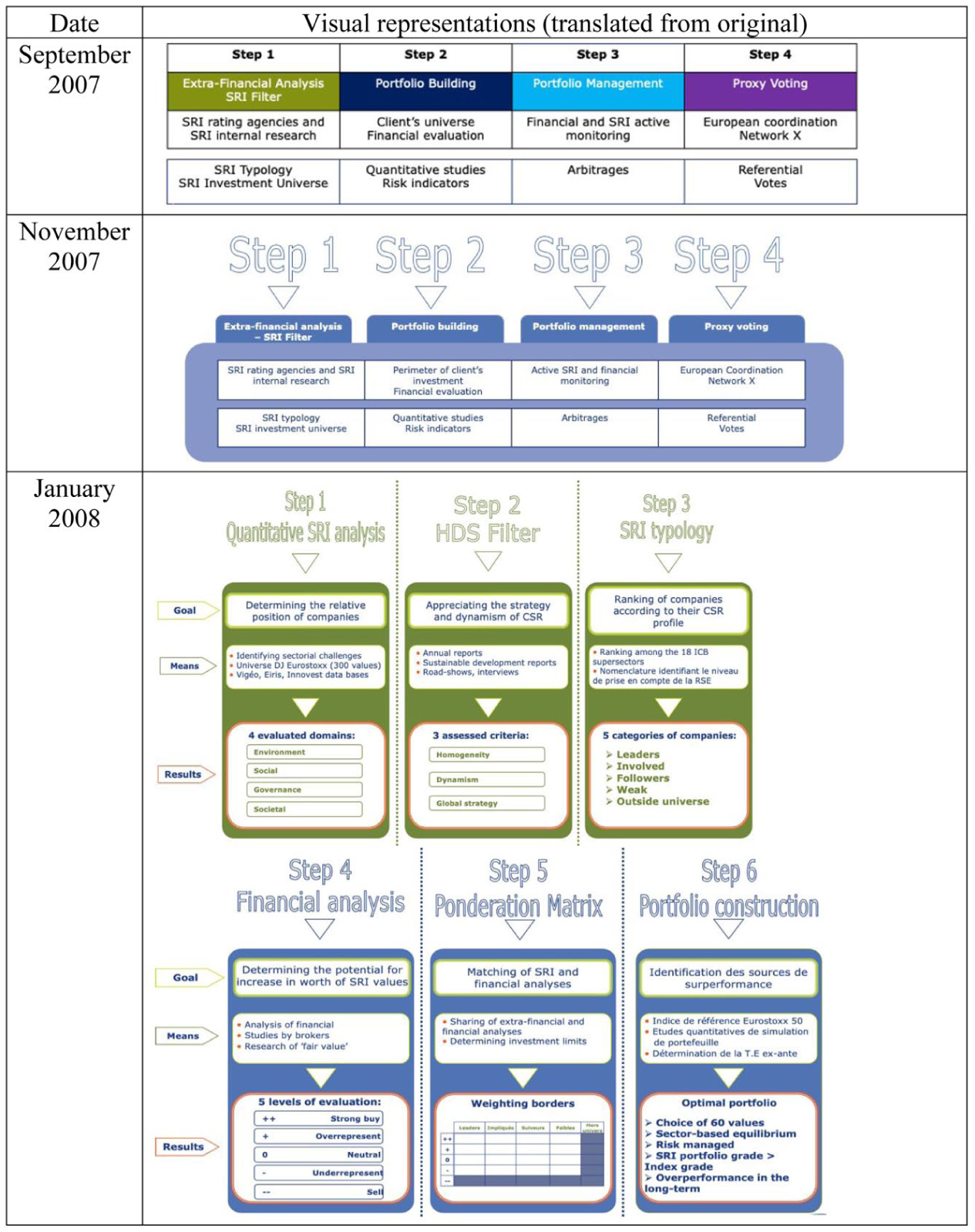

As RI analysts gained a better understanding of the “practical considerations” in fixed-income investment (field notes, 2008), they revised the screening criteria within the SRI constraint. The revised approach replaced strict exclusionary criteria with a portfolio-level threshold that allowed limited investments in issuers with lower ESG grades, provided the overall portfolio maintained a minimum ESG score. This constraint was applied at the beginning of the investment process to screen potential investments. Then, after the investment portfolios were created, RI analysts conducted monthly assessments to ensure ongoing alignment with SRI objectives. Figure 4 illustrates how ESG criteria were integrated into conventional financial analyses at both the initial screening and final evaluation stages of the investment process.

Evolution of the tool and criteria in SRI fixed-income investment.

While this arrangement established sufficient common ground to enable coordinated action, both sides viewed it as a significant concession on their part. Reflecting on the outcome, an RI analyst remarked: “We have become SRI data providers, not partners. At least, the SRI constraint is . . . better than nothing” (RI analyst). The head of fixed-income, similarly, noted: “I can’t invest how I’d like in some countries [. . .] If a client wants me to exclude a company because he doesn’t like rabbits or whatever, I will do it, but it does not make any sense” (fixed-income manager).

The knowledge generated through this structured collaboration was bounded but pragmatic, focused on incorporating ESG considerations without disrupting established workflows. This approach to integration was noted by an equity asset manager colleague, who observed: “I have the impression that it’s SRI that has adapted a lot to the constraints of fixed-income management . . . There has never been a search for true compromise . . . I’d almost say that the SRI part has become somewhat subservient to the fixed-income part” (equity manager). Over time, the limitations of this bounded integration became apparent, as noted by a board member of one of Alpha’s clients: RI analysts and fixed-income asset managers need to [continue speaking] to each other. This is clear when you look at what happened with Greece. We lost just over €200 million. Why? Not because we made the investment selection based on SRI, but because we didn’t. (pension fund board member, 2013)

In sum, the structured collaboration between RI analysts and fixed-income asset managers resulted in peripheral knowledge integration, where ESG criteria were adapted to fit within established workflows—as well as the constraints imposed by a strong emphasis on technical expertise and systematic decision-making. While RI analysts succeeded in incorporating ESG criteria through structured inputs at key decision points, the collaboration in fixed-income remained largely transactional, leaving core investment practices unchanged. This contrasts sharply with the more transformative collaboration that emerged in equity investment.

Generative collaboration: Reshaping roles and systems through joint effort

The collaboration between RI analysts and equity asset managers illustrates a pathway of “generative collaboration,” characterized by iterative experimentation, joint problem-solving, and the co-development of new evaluative frameworks that transformed established practices. Equity investing, which involves buying shares in publicly listed corporations to achieve capital growth through stock appreciation and dividends, requires navigating market uncertainty and drawing on a wide range of information sources to identify profitable opportunities (see Table 3). In this context, RI analysts and equity asset managers engaged in a more open exploration of integrating ESG criteria into investment decisions.

Interpretive orientation and contextual validation

Unlike fixed-income investing’s emphasis on technical mastery and standardized validation, equity investing was shaped by an epistemic orientation grounded in interpretation—one that understood expertise as contextually situated and emergent through interaction. This was evident in how equity asset managers approached investment decisions, combining financial analyses, market insights, and professional judgment to assess stocks’ growth potential and risk profile. As Alpha’s CEO explained, “A good equity manager can beat the market over the long term because he knows things others don’t. It is their added value” (CEO).

This interpretive approach created a more receptive environment for RI analysts’ contributions. Equity asset managers often relied on diverse information sources and recognized the potential for non-financial factors to provide valuable insights. As the field researcher observed: “Some love looking at weird things like a manager’s hubris, others love looking at pending trials—it is pretty diversified” (field notes, 2007). This perspective enabled more expansive collaboration with RI analysts.

From the outset, equity asset managers expressed interest in how ESG criteria could complement their decision-making. During the first working group meeting, representatives from the sales, equity, and SRI departments agreed on initial tasks—including rating companies’ ESG performance and creating integrated company profiles, or “factsheets,” that combined financial and ESG data to support SRI investment decisions. Although these early efforts were later described as “superficial” and “too static” to provide actionable insights (RI analyst, field diary, 2008), they signaled an openness to collaborative experimentation.

Equity asset managers’ receptivity also stemmed from skepticism toward assumptions of market efficiency, as reflected in the following comment: “I do not really believe in the [pure] efficiency of the markets. Otherwise, why would we be paid to manage [the funds]? . . . You need to know what is behind the numbers to get the full picture” (equity manager). Such views fostered a curiosity about inconsistencies between financial and ESG assessments. For instance, during one exchange, an equity manager expressed confusion about how a company could maintain strong financials despite reports of poor working conditions:

“What do you think about this company? They had a wave of suicides lately, but they still have a good financial outlook. I don’t get it.”

“We talked to our contacts inside the trade unions, and they seemed very worried. The pressure on employees is enormous—the social atmosphere is very bad. We think the financials will also deteriorate in the coming year.”

“How come this information is not factored into the analyses from the brokers?”

“We don’t know, maybe because management has not grasped or communicated the problem. I mean, it is obvious that the company won’t be able to thrive if they keep having major human resource problems.”

This exchange illustrates how the equity team engaged with ESG assessments not as predefined inputs, but as prompts for further inquiry and discussion. While they—like their fixed-income colleagues—sought to understand the “practical feasibility” and “ultimate implications” of ESG indicators, they showed a greater willingness to consider “how their investment strategies might be adapted to fit the rather ambiguous expectations of SRI” (RI analyst, field diary, 2007).

Iterative engagement to reshape frameworks

The collaboration between RI analysts and the equity team gained momentum as both groups moved beyond surface-level information sharing to actively explore potential synergies between their respective activities. A key turning point occurred during a working group meeting, where participants used a whiteboard to map their workflows. RI analysts explained how they gathered ESG data from social rating agencies to develop SRI ratings that could inform investment decisions. At the same time, the head of equity outlined the existing decision-making process for equity portfolio construction. Reflecting on this meeting, the head of equity remarked: As we were describing things, we could see that some parts were clear and easier to explain . . . This helped us identify the areas that were okay and those that we needed to work on . . . It was maybe the first time that we openly discussed the issues we had. It was interesting to actually see the process. (equity manager)

This mapping exercise pinpointed areas where their workflows could align, laying the groundwork for more “substantive” collaboration (field notes, 2007). Following this meeting, interactions between RI analysts and the equity team quickly evolved into continuous, informal exchanges. Instead of waiting for their scheduled weekly meetings, team members began consulting each other spontaneously whenever questions or challenges arose—as highlighted in the following comment: I would say that discussions with the SRI people were continuous and informal. We never waited for the committee meetings to discuss things. If we wanted to check the progress of a given process or to make sure everyone had the latest information, we would do that in the committee meetings. Otherwise, purely technical discussions [about revising the process] took place outside the meetings. (equity manager)

This fluid exchange of ideas reinforced a feedback loop in which the equity team provided practical, industry-specific insights that RI analysts used to refine their ESG criteria. These iterative exchanges not only enhanced the relevance of ESG assessments but also deepened mutual understanding. An RI analyst described the process: The process of delivering files to the manager and having him come back to me saying, “There are problems with this—I don’t understand why this one was excluded and not that one,” forces you to revisit your file and your formulas. That’s when you start to realize there might be areas for improvement . . . The manager’s input opens the door for RI analysts to uncover other errors or inconsistencies that weren’t originally on the radar. (RI analyst)

The implications of these exchanges could be seen in the evolution of SRI knowledge. Initially, RI analysts developed ESG assessments independently, drawing on quantitative data from social rating agencies. Over time, they began incorporating equity asset managers’ industry-specific insights, resulting in more nuanced perspectives on sectoral risks and opportunities. This process required reconciling different perspectives on SRI, as the head of equity recalled: I think that everyone may have had a slightly different vision of SRI [. . .] at some point, we had to strike a balance between extra-financial and financial perspectives so that we could ask ourselves, “With this extra-financial input and this financial analysis, what can asset managers actually do? What decisions can they make, and how much leeway do we give them?” (equity manager)

The equity team’s openness to experimentation and the RI analysts’ willingness to adapt their methods fostered a dynamic of mutual learning and iterative exchange. This dynamic shifted the nature of their collaboration, moving from surface-level discussion to continuous, real-time problem-solving. RI analysts gradually deepened their understanding of equity investment processes, while equity asset managers developed a greater appreciation of ESG assessments and how they could inform investment decisions.

Through sustained engagement and experimentation, the RI analysts and the equity team developed tools that fundamentally transformed investment processes. Central to this transformation was the creation of a decision matrix tool that systematically integrated financial and ESG analyses. The following describes how this tool emerged from practical needs and collaborative input: The construction of the “SRI Excel database” came from a simple idea: we all recognized that, with the growing complexity of the investment universe, we needed tools—decision support tools—that were more automated. The Excel database was the natural next step. It allowed us to consolidate all the information—both quantitative and qualitative—in one place, giving us a quick overview of each sector and company. From there, we could dive deeper into the details, but first, we needed a tool that provided a clear, high-level view. (equity manager)

Developing and refining the decision matrix involved a series of iterative adjustments aimed at balancing ESG criteria with portfolio competitiveness. RI analysts and equity asset managers worked closely to test the tool using simulated portfolios, focusing on exclusion ratios—thresholds for removing companies or issuers based on their SRI rankings. Initially set at 50%, the exclusion ratios were adjusted downward to 40% and then to 25% in response to concerns from the equity team that stricter thresholds limited their ability to construct competitive portfolios (see Figure 5 for an overview of different iterations of the tool and criteria). Describing how the process of refinement unfolded, an RI analyst remarked: Through the repeated exchanges . . . we were able to move forward, to identify errors in the process, to think, and to choose among alternative courses of action [. . .] As we became aware that the asset managers are too constrained when investing, we changed the SRI selectivity. (RI analyst)

Evolution of the tools and analyses in SRI equity investment.

Equity managers, in turn, agreed to exclude certain companies—an accommodation that was described as a “huge compromise” (RI analyst), given its potential implications for portfolio performance. This willingness to adapt underscored the importance of aligning financial objectives with ESG priorities. Reflecting on this challenge, the head of equity explained: “even though we have clients or prospective clients who are strongly committed to SRI, they still don’t want it to come at the expense of [financial] performance . . . So, I think it’s crucial to align extra-financial and financial analyses equally when building a portfolio” (equity manager).

Embedding nascent knowledge into shared workflows

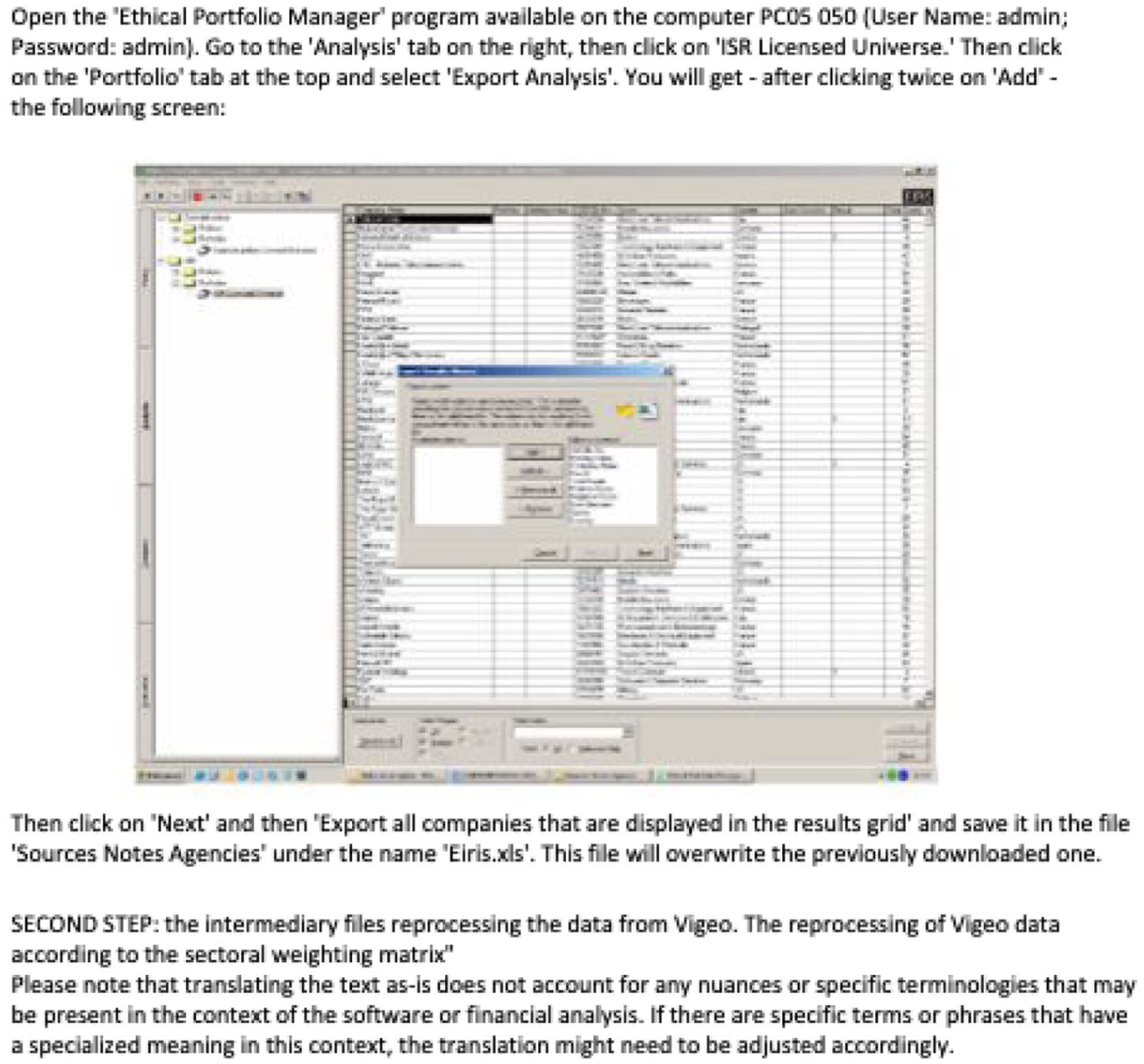

The integration of ESG criteria was formalized in a comprehensive methodological guide that detailed technical procedures and explained the rationale for combining financial and ESG analyses. The guide included extensive explanations, screenshots illustrating SRI grade calculations, matrix implementations, and solutions to common challenges (see Figure 6). Beyond its technical function, the guide reflected shift in equity investment decision-making and workflows. As the head of equity emphasized: I don’t want to keep a kind of watertight barrier between extra-financial analyses and my own work. I want it to be correlated. Otherwise, it would mean that I am using criteria that I don’t understand . . . the aim is not for me to do the work of an RI analyst or for them to do mine. Instead, we should have . . . a shared boundary . . . If I understand a little bit about the SRI chain, I think that gives me added value. (equity manager)

Example screenshot of the methodological guide developed in equity investment.

By the time the working group disbanded, the collaboration between RI analysts and equity asset managers had significantly transformed investment processes. Unlike the peripheral integration observed in fixed-income investing, equity managers’ willingness to experiment enabled a deeper alignment between ESG considerations and financial decision-making. ESG criteria were woven throughout the investment process, with financial and non-financial analyses given equal weight in developing SRI funds. This positioned RI analysts as active participants in investment decisions, moving beyond providing supplementary information. As the field researcher described: “We developed this system . . . to ensure that an RI analyst steps in during the evaluation process and gives a recommendation—exactly like a financial analyst would” (RI analyst, field diary 2009). The significance of these changes was noted by the head of equity: I think everyone got involved; everyone wanted it to succeed . . . We were asked to make changes, come up with new ideas . . . and in the end, [the CEO] endorsed everything we developed: the matrix, the method of analyzing the financial components, the approach to combining financial and extra-financial considerations, the overall framework for giving asset managers more latitude—all of it was approved. It’s really encouraging. (equity manager)

In summary, our analysis of collaborations between RI analysts and asset managers at Alpha illustrates how distinct pathways can emerge from the interplay between nascent occupations’ adaptive strategies and the epistemic assumptions of established professionals. In fixed-income investing, RI analysts navigated an emphasis on technical mastery and standardized validation by developing targeted interventions that integrated ESG criteria at specific decision points without disrupting established workflows. In equity investing, they leveraged an openness to interpretive reasoning to engage in iterative collaboration, enabling greater mutual adjustment and more substantive shifts in practice. Across both pathways, we observed how knowledge was co-created and practices reshaped as ESG criteria were negotiated, adapted, and embedded within established asset management domains.

Discussion

Our study advances understanding of how nascent occupations collaborate with established professionals to co-create knowledge and transform existing practices. Through an in-depth examination of how “first-generation” RI analysts worked with asset management professionals to develop organizational knowledge in SRI, we identify two distinct collaborative pathways—structured and generative—that illuminate how these processes unfold when one party lacks established authority and recognized expertise. This comparative analysis offers new insights into three key areas: (1) how collaborative engagement facilitates knowledge co-creation with nascent occupations; (2) how epistemic assumptions within professional domains shape the potential for practice transformation; and (3) how early patterns of collaboration influence the organizational positioning and trajectory of nascent occupations.

Collaborative knowledge co-creation with nascent occupations

Our first contribution deepens theoretical understanding of knowledge co-creation in collaborations involving nascent occupations whose expertise is still emerging. Prior research has largely focused on collaborations involving “expert talking to expert” (Fincham et al., 2008, p. 1149), where specialized knowledge serves as both a prerequisite for collaboration and a basis for meaningful knowledge exchange (Kellogg et al., 2006; Mitchell & Boyle, 2015). Implicit in this view is the assumption that expertise develops prior to collaboration—whether through formal training or informal processes such as experiential learning and socialization within existing communities of practice (Malhotra & Morris, 2009; Mclaughlin & Webster, 1998). However, this assumption overlooks the distinctive collaborative challenges faced by nascent occupations.

Nascent occupations—particularly those in supportive roles—often encounter a “catch-22”: they must demonstrate credibility to secure collaborative opportunities, yet the development and recognition of their expertise depend on these very collaborations. This tension is especially pronounced among emerging roles created to address cross-cutting organizational priorities, such as AI ethics specialists, sustainability managers, and diversity officers. Unlike occupations that demarcate their authority through proprietary frameworks or that seek to formalize exclusive domains of knowledge, these roles work across boundaries to reshape existing practices from within. Their expertise is not rooted in exclusive authority but must be cultivated in relation to the practices of those they aim to influence—requiring sustained interaction and gradual recognition of their contributions (Augustine, 2021; Cross & Swart, 2021; Fayard et al., 2017).

Our study identifies two distinct pathways through which nascent occupations can navigate this “catch-22” and collaborate with established professionals to co-create knowledge. Through structured collaboration, nascent occupation members build initial credibility by aligning their emerging expertise with existing frameworks, enabling incremental contributions that can be integrated with minimal disruption to established workflows. In the fixed-income domain, this approach allowed RI analysts to contribute to investment processes by developing bounded ESG inputs that fit within prevailing evaluative criteria. Through generative collaboration, in contrast, nascent occupation members engage in deeper mutual learning that enables more fundamental transformation of existing practices. This pathway, which emerged with equity asset managers, facilitated broader recognition of RI analysts’ contributions through iterative engagement and joint development of new evaluative frameworks.

By showing how credibility and expertise can develop concurrently through carefully orchestrated collaborative processes, our study shifts attention beyond traditional models of professionalization that position expertise as a precondition for exerting influence. Instead, we extend performative accounts of expertise (Nicolini et al., 2017; Treem & Barley, 2018) by showing how nascent occupations can strategically leverage different forms of collaborative engagement to build recognition and influence. This perspective highlights the relational and processual nature of expertise (Anteby et al., 2016; Black et al., 2004; Sandefur, 2015), emphasizing how it emerges at the intersections of established and emerging occupational domains.

Future research could examine how expertise development and occupational recognition co-evolve, particularly in settings where formal authority is absent and knowledge bases are still forming. Longitudinal studies could explore whether, and under what conditions, structured pathways transition to generative ones—illuminating factors that enable or constrain deeper integration over time. Future work might also examine how external institutional pressures—such as regulatory changes or shifting market demands—interact with these collaborative pathways to shape the emergence of occupational expertise.

Epistemic assumptions shaping knowledge management and practice transformation

Our second contribution illuminates how intra-occupational differences in epistemic assumptions—fundamental beliefs about what constitutes valid expertise and how it should be evaluated—shape the conditions for knowledge co-creation and practice transformation in collaborations with nascent occupations. While prior research on inter-occupational collaboration has emphasized structural mechanisms for bridging knowledge boundaries (Bechky, 2003a; Carlile, 2002) and relational strategies for navigating power asymmetries (DiBenigno, 2020; Huising, 2015), we show how underlying assumptions about expertise significantly influence collaborative dynamics and outcomes.

Our comparative analysis shows that different specializations within the same profession can hold fundamentally distinct beliefs about the nature and validation of expertise. In fixed-income investing, expertise was understood as residing “within” individual professionals—as something acquired through prolonged training and validated through technical mastery and codified methods (Abbott, 1988; Van Maanen & Barley, 1984). This orientation erected high entry barriers and fostered a structured form of collaboration, where nascent occupational contributions were expected to conform to existing evaluative frameworks and decision-making routines. By contrast, equity investing understood expertise as emergent and interactional, grounded in contextual reasoning and “judgments of value” (Robertson, Scarbrough, & Swan, 2003). This orientation created conditions for more generative collaboration, in which knowledge was co-created through sustained engagement and used to reshape core practices.

These contrasting epistemic orientations shaped not only how knowledge was shared (Barley et al., 2018; Gustafsson & Lidskog, 2018), but also the forms of collaboration that were perceived as appropriate and the depth of practice transformation that could occur. When expertise was perceived as individually held and rooted in technical mastery, collaboration tended toward structured accommodation that preserved established workflows, resulting in peripheral knowledge integration. However, when expertise was understood as emerging through interaction, collaboration enabled deeper synthesis and transformative change.

Our findings suggest that these epistemic differences become particularly consequential in collaborations involving nascent occupations, where ambiguity surrounding expertise and authority is heightened (Fayard et al., 2017; Murphy & Kreiner, 2020). Unlike collaborations between established experts where knowledge boundaries tend to be more clearly defined (Anteby et al., 2016; Bechky, 2003b; Kellogg et al., 2006), interactions with nascent occupations involve greater uncertainty over what constitutes a valid contribution. In such contexts, epistemic assumptions act as implicit “filters,” shaping which forms of collaboration and innovation are considered legitimate or even possible. This insight may help explain why similar change initiatives might succeed in some professional contexts but stall in others, even within the same organization (Barley et al., 2018). It also extends work on intra-occupational heterogeneity (Beane & Anthony, 2023; Wright et al., 2017) by showing how epistemic assumptions influence not only knowledge-sharing dynamics but also the scope and depth of practice transformation within organizational settings.

Future research could examine whether and how professional epistemic orientations evolve through sustained interaction with nascent occupations. For instance, do technically oriented specializations gradually become more receptive to emergent, interaction-driven forms of expertise after successful collaborative experiences? What factors make epistemic assumptions more malleable or more resistant to change? Studies might also explore how repeated collaborative efforts across multiple domains shape collective understandings of expertise within organizations, with implications for integrating emerging knowledge domains and enabling transformative change (Carlile, 2004; Robertson et al., 2003).

Organizational integration and trajectory of nascent occupations

Our third contribution provides insights into how nascent occupations become integrated into organizational structures and how early collaborative patterns shape their long-term trajectory. Previous research highlights the importance of interaction opportunities for building influence (Huising, 2015; Truelove & Kellogg, 2016), but nascent occupations face distinctive challenges in accessing and leveraging these opportunities. Unlike established professionals, who can draw on formal credentials and deploy “rapid relational tactics” to quickly demonstrate value (DiBenigno, 2020), members of nascent occupations typically lack the conventional markers of expertise that signal credibility and facilitate collaborative engagement (Fayard et al., 2017; Murphy & Kreiner, 2020).

Our study suggests that integrating nascent occupations requires sustained and differentiated forms of organizational support. While top management intervention can create initial opportunities for interaction—as observed in our case through the formation of a formal working group—these structures alone are often insufficient for meaningful integration. Instead, our comparative analysis suggests that successful integration depends on how well organizations tailor their support mechanisms to the epistemic orientations of different professional domains. In domains where expertise is viewed as technical and codified, nascent occupations may benefit from structured opportunities to demonstrate value incrementally while building practical experience. For example, organizations can implement “scaffolded” team arrangements (Valentine & Edmondson, 2015) that create progressive integration points, gradually expanding involvement as credibility is established. Conversely, in domains where expertise is understood to be context-sensitive and interactional, integration may be better supported by creating protected spaces for experimentation and iterative development of new practices (Bucher & Langley, 2016; Kellogg et al., 2006).

The different approaches to integration not only shape immediate collaborative dynamics but also influence the long-term positioning of nascent occupations within organizations. Our findings suggest that initial patterns of engagement can have enduring consequences that extend well beyond the formal collaboration period. When collaboration is tightly structured, nascent roles may remain narrowly defined, limiting opportunities to demonstrate broader value. In contrast, more generative forms of collaboration create opportunities for nascent occupations to demonstrate relevance across multiple dimensions and cultivate deeper influence. These initial patterns can fundamentally shape whether nascent occupations eventually gain recognition as valued contributors or remain peripheral to core organizational practices.

Future research might explore how different organizational arrangements enable or constrain the ability of nascent occupations to build credibility and exert influence across diverse professional domains. Studies could examine how nascent occupations maintain a coherent identity while adapting their approaches to align with the varying epistemic assumptions in different contexts. Research might also explore whether and how nascent occupations that successfully establish influence in one domain can leverage that position to gain traction in more resistant domains, potentially creating cross-pollination effects that gradually reshape organizational practices more broadly. Such research would generate valuable insights into how organizations can better support the integration of emerging expertise within existing structures.

Conclusion

Our study provides a framework for understanding how nascent occupations navigate the challenge of transforming established practices through collaborative knowledge co-creation. In response to complex business and societal imperatives that transcend traditional boundaries, organizations increasingly create new roles to bridge gaps between established practices and emerging demands. Our study shows that successful collaboration depends not only on demonstrating technical competence, but also on navigating deeply rooted assumptions about what constitutes valid expertise and credible contributions. The contrasting pathways we identify—structured and generative collaboration—illustrate how different epistemic orientations give rise to distinct forms of knowledge co-creation and possibilities for practice transformation. These insights lay the groundwork for future research and inform practical strategies for enabling collaboration, reshaping entrenched assumptions, and expanding the role of nascent occupations in driving organizational change.

Footnotes

Acknowledgements

We thank senior editor Graeme Currie and the three anonymous reviewers for their constructive and insightful feedback throughout the review process. We are also deeply grateful to all of our informants for generously sharing their time, experiences, and perspectives during the course of this research.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.