Abstract

While prior work suggests that ambiguous frames may be helpful in promoting institutional change, we still know little about their impact on field-level change. Drawing on contemporary accounts of organizational fields as structured around issues, we investigate the rise of responsible investment in South Africa, examining how proponents’ use of frame ambiguity drew in a broader range of field actors but ultimately stalled the institutionalization of new meanings and practices in the investment field. Our study suggests that to promote change, proponents should seek a balance between enough ambiguity to invite participation, and enough specification to regulate the understanding of the problem, promote the experimentation of new practices, and clarify the impetus for action. We also contribute to the conceptualization of field settlement by distinguishing among rhetorical, incremental, and disruptive field settlements, highlighting that field settlements are not always indicators of further substantive change processes in a field.

Introduction

Much research has pointed to the generative potential of ambiguous frames in promoting institutional change (Ferraro, Etzion, & Gehman, 2015; Howard-Grenville, Nelson, Earle, Haack, & Young, 2016). Prior work has also highlighted the value of using ambiguity to initiate change processes around contentious issues (Ferraro et al., 2015; Gioia, Nag, & Corley, 2012); to encourage the collective engagement of organizational actors without requiring explicit consensus (Van Wijk, Stam, Elfring, Zietsma, & Den Hond, 2013); and to enhance actors’ ability to maneuver between pluralist institutional demands (Meyer & Höllerer, 2016). Consistent with these arguments, research has also pointed to the importance of avoiding value clash or negotiation breakdowns (Hoffman & Jennings, 2015) given that change is often the result of pragmatic actions undertaken by distributed actors (Ansari, Wijen, & Gray, 2013; Wijen & Ansari, 2007).

Yet, the outcomes of the use of ambiguous frames aimed at institutional change remains poorly understood (Howard-Grenville et al., 2016; Litrico & David, 2017) particularly at the level of fields. For instance, scholars have raised concerns about the risk of misalignment between organizational commitments (Greenwood, Raynard, Kodeih, Micellota, & Lounsbury, 2011; Meyer & Höllerer, 2016) and the possibility of purely symbolic responses (Edelman, 1992; O’Sullivan & O’Dwyer, 2015). Moreover, prior studies on the use of ambiguity in change processes have predominantly relied on organizational-level examples to infer field-level outcomes (Ferraro et al., 2015; Gioia et al., 2012), or have only indirectly attended to conditions of ambiguity at the field level (Howard-Grenville et al., 2016; Van Wijk et al., 2013), leaving largely unexamined the interplay between framing activities, meaning construction, and the interpretive dynamics of various field constituents (Litrico & David, 2017; Meyer & Höllerer, 2010).

In this article, we argue that an issue-based approach to institutional fields (Furnari, 2018; Hoffman, 1999; Litrico & David, 2017; Meyer & Höllerer, 2010) could help address these gaps. Defining fields as “centers of debates in which competing interests negotiate over issue interpretation” (Hoffman, 1999, p. 351), this approach brings attention to the role of framing (Goffman, 1974; Purdy, Ansari, & Gray, 2017) in field-level change. Building on this perspective, we ask: how does frame ambiguity affect institutional change at the field level?

To empirically explore this question, we examine the rise of responsible investment and its effect on the field of financial investment in South Africa, a jurisdiction with an enabling regulatory framework with regard to responsible investment. Described as ambiguous and interpretively flexible (Ferraro et al., 2015), the concept of responsible investment has been used to challenge what is “normal” and “legitimate” in the field of financial investment and align investors with broader societal objectives by promoting the integration of environmental, social, and governance (ESG) factors into mainstream investment processes. Considering that the majority of the world’s institutional investors have officially adopted responsible investment (PRI, 2017b), the framing approach used to promote the concept has been described as a success (Ferraro et al., 2015); yet, the field’s practices, behaviors, and expectations have remained largely unchanged (Himick & Audousset-Coulier, 2015; PRI, 2019). By analysing primary and secondary data gathered in the South African financial industry between 2013 and 2019, we investigate how the ambiguous frame employed by proponents of responsible investment influenced the interpretive dynamics of the field constituents and affected field-level change.

In our setting, the use of frame ambiguity to promote responsible investment allowed for a false impression of progress, inhibited material changes, and concealed differences between actors, revealing that high levels of frame ambiguity may be counterproductive for realizing field-level change. Differentiating between the degrees of ambiguity generated by each component of a frame—diagnostic, prognostic, and motivational—we suggest that an instrumental use of ambiguity to promote change should strive to establish a balance between enough ambiguity to invite participation and reduce unease, and enough specification to “bound” (Hoffman, 2001) how actors interpret the frame, seed experimentation, and regulate how actors perceive the urgency and salience of action. We also highlight how frame ambiguity may affect the nature of field settlements and contribute to the conceptualization of field settlement by distinguishing among rhetorical, incremental, and disruptive field settlements.

Background

We begin by combining a processual with a structural perspective on frames and the effects of framing on organizational and institutional change processes. We then delve into the role of ambiguity in framing and its potential impact on field dynamics.

Framing in issue fields

Fields can be viewed as spaces of dialogue and contestation, forming around issues that are salient to the interests and practices of a particular collective of organizations (Hoffman, 1999, 2001). An issue-field perspective helps to address how collective rationality evolves during periods of uncertainty or change (DiMaggio & Powell, 1983), highlighting how framing processes influence, and are influenced by, institutional beliefs and practices within organizations (Hoffman, 2001). Distinguishing between the institutional environment and organizational dynamics, an issue-field perspective draws attention to the relationship between the frames used strategically by certain field constituents to transform field activities and the resulting interpretative responses by other organizations in the field (Furnari, 2018; Hoffman, 2001). Importantly for our analysis, it also provides a conceptual framework to analyse how frames can influence the negotiation of meaning systems that guide the interpretations and actions of field constituents.

Any major transformation of a field implies some sort of “frame-breaking” experience (Gioia et al., 2012; Goffman, 1974) in which field actors’ primary frameworks (Goffman, 1974) are challenged and revised into new meanings and activities. Primary frameworks are “schemata of interpretation,” shared meaning systems, and taken-for-granted socio-cognitive schemas that others sometimes refer to as frames of reference (Thornton & Ocasio, 2008). They shape field actors’ understanding of the reality around them, helping them to answer the question “What is it that’s going on here?” (Goffman, 1974, p. 25). Rooted in “structural and social forces” and generally experienced by individuals in a non-reflexive and holistic manner, primary frameworks are bound by “certain historical patterns of interaction” and routines that create a self-reinforcing narrative and consensus about appropriate and legitimate behavior (Diehl & McFarland, 2010, p. 1744).

By engaging in the act of framing, proponents of change seek to alter the primary framework through which other field actors interpret reality, and thus guide the activity of a field (Hoffman, 1999; Werner & Cornelissen, 2014). Framing is thus a process used by certain actors to influence meaning structures and institutional processes. As conceptualized by Entman,

[t]o frame is to select some aspects of a perceived reality and make them more salient in a communicating text, in such a way as to promote a particular problem definition, causal interpretation, moral evaluation, and/or treatment recommendation for the item described. (Entman, 1993, p. 52)

Framing is “an active, process-derived phenomenon that implies agency and contention at the level of reality construction” (Snow & Benford, 1992, p. 136).

Through the act of framing, actors produce frames: interpretative packages created to help individuals or organizations make sense of experiences or change processes, and guide action (Snow, Rochford, Worden, & Benford, 1986; Werner & Cornelissen, 2014). A frame can imbue new meaning to the activity of a field by adding a “layer” or “lamination” onto the primary framework (Diehl & McFarland, 2010). Frames have also been described as a key (Goffman, 1974; Purdy et al., 2017), “a set of conventions by which a given activity, one already meaningful in terms of some primary framework, is transformed into something patterned on this activity but seen by the participants to be something quite else” (Goffman, 1974, pp. 44–45). The framing process involved in the design of a key is called keying and performs a critical function in transforming what actors think is going on in a given field (Goffman, 1974; Purdy et al., 2017).

A frame is articulated around three main components (Benford & Snow, 2000; Entman, 1993). The first, the diagnostic component, defines the core problem by pointing to a problematic situation and attributing responsibility or blame to culpable agents (Benford & Snow, 2000; Entman, 1993). The second component, the prognostic component, concerns the articulation of potential solutions, strategies, or tactics that can be implemented to remedy the issue (Benford & Snow, 2000; Entman, 1993). The third component is motivational, providing a “calls to arms” or compelling accounts to stimulate participation and rally adherents (Benford & Snow, 2000).

Frames tend to evolve continuously through contestation, adaptation or transformation, as they diffuse or spread from one movement or group to another (Benford & Snow, 2000). One way in which frame transformation occurs is when an adopter or importer assumes an active role in strategically selecting and modifying components of an existing frame to make it more resonant to the targets of mobilization (Benford & Snow, 2000). This process of adapting the lens through which the initial key of a frame is interpreted and evaluated is referred to by Goffman (1974) as rekeying. Rekeying adds an additional layer to the initial key or transposes it to make it resonant with another primary framework (Diehl & McFarland, 2010).

Taken together, the process of framing, the content of frames, and the interpretive responses of field actors help to explain the recursive processes through which new meanings emerge, spread, and, in some cases, become the basis for new field settlements (Cornelissen & Werner, 2014; Fligstein & McAdam, 2011). A field settlement occurs when field actors agree on an altered primary framework and begin to follow its template for action (Cornelissen & Werner, 2014; Fligstein & McAdam, 2011). However, a field settlement is not easily achieved as it reflects a degree of consensus regarding the new nature and meaning of shared activities. To a large extent, it implies that actors “break down traditional structures and beliefs that have become institutionalized over decades” (Hoffman, 2001, p. 147).

The role of ambiguous frames in institutional change

Recent research points to the value of ambiguity, and in particular, the creation of ambiguous frames, to help mediate between the various interests of field actors and support efforts towards institutional change (Ferraro et al., 2015; Litrico & David, 2017; Van Wijk et al., 2013). Prior studies have proposed that ambiguous frames help to facilitate the mobilization of field actors with respect to complex and contested issues (Ferraro et al., 2015; Litrico & David, 2017; Van Wijk et al., 2013), to open up lines of action without requiring explicit consensus (Gioia et al., 2012; Jarzabkowski, Sillince, & Shaw, 2010), and to enable the coexistence and progressive alignment of stakeholders’ rhetorical positions (Sillince, Jarzabkowski, & Shaw, 2012). Ambiguity is also thought to enhance actors’ ability to maneuver between diverse and possibly contradictory institutional demands, limiting the need for purely ceremonial responses to external pressures while maintaining dynamism and heterogeneity in change efforts (Greenwood et al., 2011; Howard-Grenville et al., 2016; Meyer & Höllerer, 2016).

Ambiguity has been defined as “the special doubt that can arise over the definition of the situation” (Goffman, 1974, p. 302) and is associated with either vagueness in meaning or multiple possible interpretations (Gioia et al., 2012). Goffman (1974) notes that vagueness stems from keying that does not sufficiently reference a primary framework, leaving actors unsure how to proceed. Whereas the possibility of multiple interpretations, referred to by Goffman (1974) as uncertainty, often originates from the use of false connectives such as language and terminology that could be consistent with multiple primary frameworks, allowing field actors to interpret a frame in line with the primary framework that is most natural to them. Notwithstanding this distinction, the majority of studies have treated ambiguity as a homogeneous concept and in some instances have conflated ambiguity and vagueness (Gioia et al., 2012).

Despite the promise of ambiguity, concerns have been raised regarding the effect of sustained ambiguity on change interpretation and implementation (Gioia et al., 2012; Howard-Grenville et al., 2016; Meyer & Höllerer, 2016). For instance, Gioia et al. (2012, p. 3) argue that ambiguity must be contained “within manageable bounds” and must be followed rapidly by clear measures guiding the implementation of any changes. Concerns have been raised that ambiguity could lead to lower accountability levels (Meyer & Höllerer, 2016), the emergence of tensions over goals and directions (Sillince & Mueller, 2007), the establishment of groups pursuing divergent interests (Howard-Grenville et al., 2016), the lack of substantive adoption of new practices or decoupling (Edelman, 1992; Etzion & Ferraro, 2010), and the risk of cooptation (O’Sullivan & O’Dwyer, 2015).

Thus, there is still much to be learned about the effects of ambiguous frames on field-level change and the conditions needed to establish a balance between the advantages and the risks associated with ambiguity. Furthermore, prior research on ambiguous frames has predominantly been set at the organizational level (Gioia et al., 2012; Jarzabkowski et al., 2010; Meyer & Höllerer, 2016), has used mainly individual or organizational-level examples to infer field-level outcomes (Ferraro et al., 2015; Furnari, 2014), or has only indirectly attended to conditions of ambiguity at the field level (Howard-Grenville et al., 2016; Litrico & David, 2017; O’Sullivan & O’Dwyer, 2015; Van Wijk et al., 2013). As a result, the effects of ambiguous frames on the dynamic processes of frame acceptance, meaning construction, and change implementation within and across field actors remain relatively opaque (Cornelissen & Werner, 2014). Our study sets out to try to bridge some of these gaps in our understanding of the role of frame ambiguity in promoting field-level change.

Methods

To study the role of frame ambiguity in field-level change, we turned to the field of financial investment in South Africa. Engaging in a grounded analysis of primary and secondary data gathered between 2013 and 2019, we analysed the frame employed by proponents of responsible investment, the interpretive responses of field constituents and the impact on field-level change.

Research setting

The field of financial investment globally and in South Africa has been driven by a primary framework focused on advancing shareholder value through financial market growth and short-term profit maximization (PRI, 2017b). The duty of institutional investors has been interpreted strictly in financial terms, fulfilled through the maximization of beneficiaries’ financial interests in excess of industry benchmarks. This primary framework of maximization of returns was perpetuated within organizations through a set of practices and incentive structures focused on managing determinate risks in order to maximize short-term profit (Blyth, Szigety, & Xia, 2016).

Yet, in response to the rise of the socially responsible investment (SRI) movement and pressure from non-governmental organizations to align investment flows with environmental and social sustainability (Richardson & Cragg, 2010), proponents within some of the world’s largest institutional investors began a process of importing and adapting elements of the SRI frame for mainstream investors, as evidenced in reports such as Who Cares Wins (UN Global Compact, 2004) and the Freshfields Report (UNEPFI, 2005). In 2006, these proponents came together to create the Principles for Responsible Investment (PRI), an initiative supported by the United Nations Environment Programme Finance Initiative and the United Nations Global Compact that sought to redefine what was considered normal and legitimate in the field of financial investment by promoting the integration of ESG concerns into mainstream investment practices (Sandberg, 2011).

In contrast to the SRI (or ethical investment) movement that looked at how investment decisions affected sustainability issues and promoted the integration of ESG factors as a way to address societal challenges, responsible investment considered how ESG issues could affect investment returns and proposed to integrate ESG issues on the basis of their relative financial risks and opportunities to investors (Richardson & Cragg, 2010; Woods & Urwin, 2010). Despite the definitional and terminological ambiguities between the coexisting concepts, a certain level of standardization of the terminology has occurred through the PRI and its effort to promote responsible investment into mainstream investment processes and ownership practices (Woods & Urwin, 2010). As such, most field constituents putting pressure on institutional investors and their service providers, including NGOs, academics, sustainability consultants, activists, investors, and the press, have increasingly used the term “responsible investment” to designate the change effort (Richardson & Cragg, 2010). This has led responsible investment to be used as an “umbrella term” for a range of different investment practices that integrate certain non-financial concerns in the investment process (Woods & Urwin, 2010).

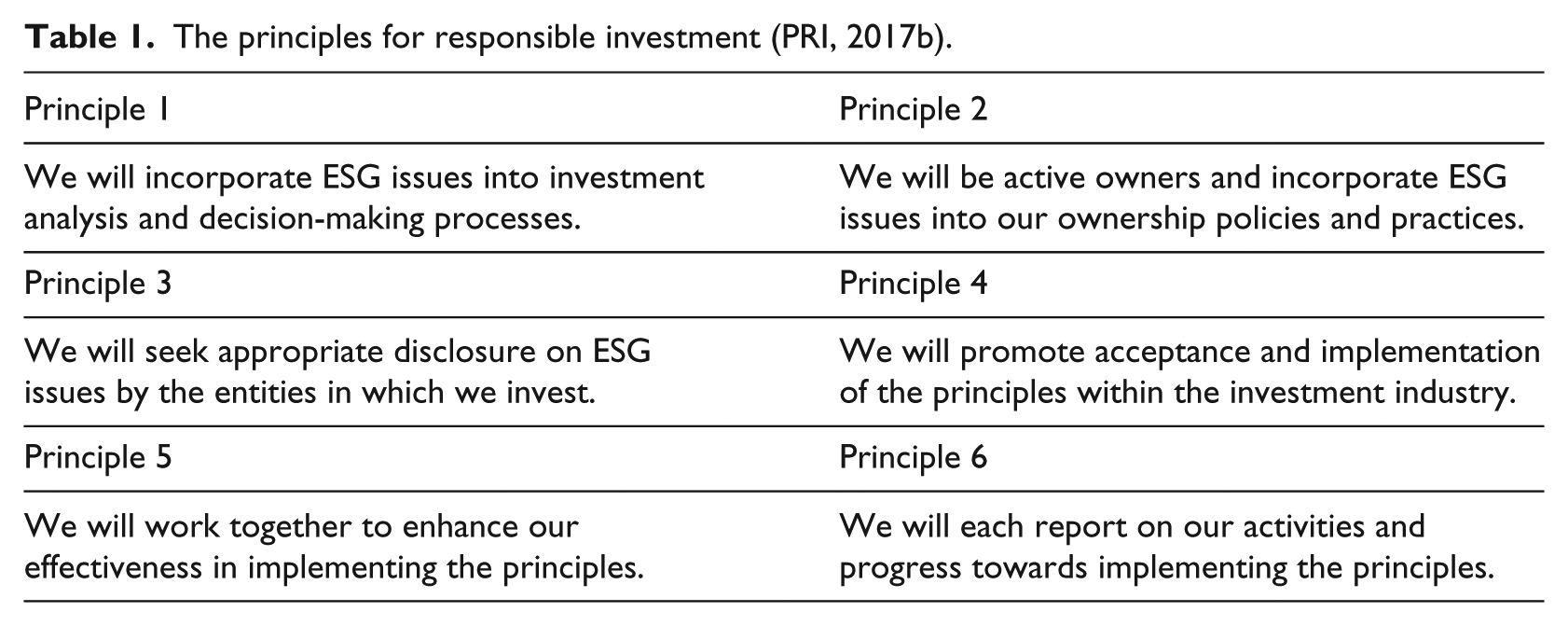

As framed by the PRI, responsible investment is structured around six voluntary and aspirational principles, detailed in Table 1, while offering processual guidance with a menu of possible actions (PRI, 2017b). The frame promoted by the PRI has been described by prior research as “interpretively flexible” or “multivocal,” focused primarily on mobilizing adoption (Ferraro et al., 2015). The flexible and voluntary character of the PRI principles allows organizations to interpret and translate responsible investment in the context of their activities (PRI, 2017b). While targeting asset owners, asset managers, and asset consultants, the PRI’s approach relied on asset owners to drive field-level change by integrating ESG considerations in the policies, mandates, and reporting systems that structure their relationships with service providers (PRI, 2017b).

The principles for responsible investment (PRI, 2017b).

While responsible investment has gained momentum among large asset owners and asset managers, attracting more than 2,000 signatories that collectively manage more than US$89 trillion and together represent more than half of the world’s assets under management (PRI, 2019), prior research has demonstrated that it appears to exert only negligible pressure on corporate behavior and short-term investment trends (Busch, Bauer, & Orlitzky, 2016; Himick & Audousset-Coulier, 2015). According to the PRI, “Despite growing awareness, an implementation gap remain[s] with capital markets often not accounting for the sustainability-related risks and opportunities associated with ESG issues such as climate change” (PRI, 2019). This paradoxical situation, which seems to have prompted the PRI to adjust the framing of responsible investment in 2017 (PRI, 2017a), offers a rich setting in which to explore how ambiguous frames enable or constrain field-level change.

We situate our study more particularly within the context of the South African investment industry, a jurisdiction that largely conforms to leading financial trends and where changes to investment process have not materialized despite an enabling regulatory environment requiring investors to integrate ESG factors in investment decisions (Tomlinson, Bertrand, & Martindale, 2017; Viviers & Els, 2017). Active lobbying by the chairman of the Government Employee Pension Funds, John Oliphant, to promote the PRI principles led to the formal adoption of responsible investment by South African regulatory institutions (Tomlinson et al., 2017). In 2011, an amendment to Regulation 28 of the South African Pension Funds Act 24/1956 included a statement requiring all South African pension funds to consider a responsible investment approach as part of their fiduciary duty. The mainstreaming of responsible investment was further supported by the release of the Code for Responsible Investment in South Africa (CRISA), a “soft regulation” (Sahlin-Andersson & Wedlin, 2008) or governance initiative organized by the Institute of Directors of Southern Africa and supported by the Association for Savings and Investment South Africa. CRISA was designed to support the implementation of the amended Regulation 28 by defining responsible investment and guiding South African institutional investors in the implementation of responsible investment practices (Viviers & Els, 2017). While CRISA was not created as a formal legal structure and has not employed any staff, the initiative has benefited from voluntary industry contributions. A CRISA committee composed of about 20 industry members meets every two months to analyse the uptake of responsible practices and discuss the way forward.

We identified the PRI, CRISA, and South African regulatory institutions as the proponents of the responsible investment frame, answerable for its content and meaning. Similarly, we identified the financial organizations (asset owners, asset managers, and asset consultants) as the recipients of the frame, required to interpret and implement its content. We designate field actors, such as civil society organizations, academics, SRI shareholders or sustainability consultants, as ancillary participants. Having pushed for field-level change using related concepts such as SRI or ethical investment, these ancillary actors were, in theory anyway, monitoring whether incumbent investors engaged in substantive changes.

Data collection

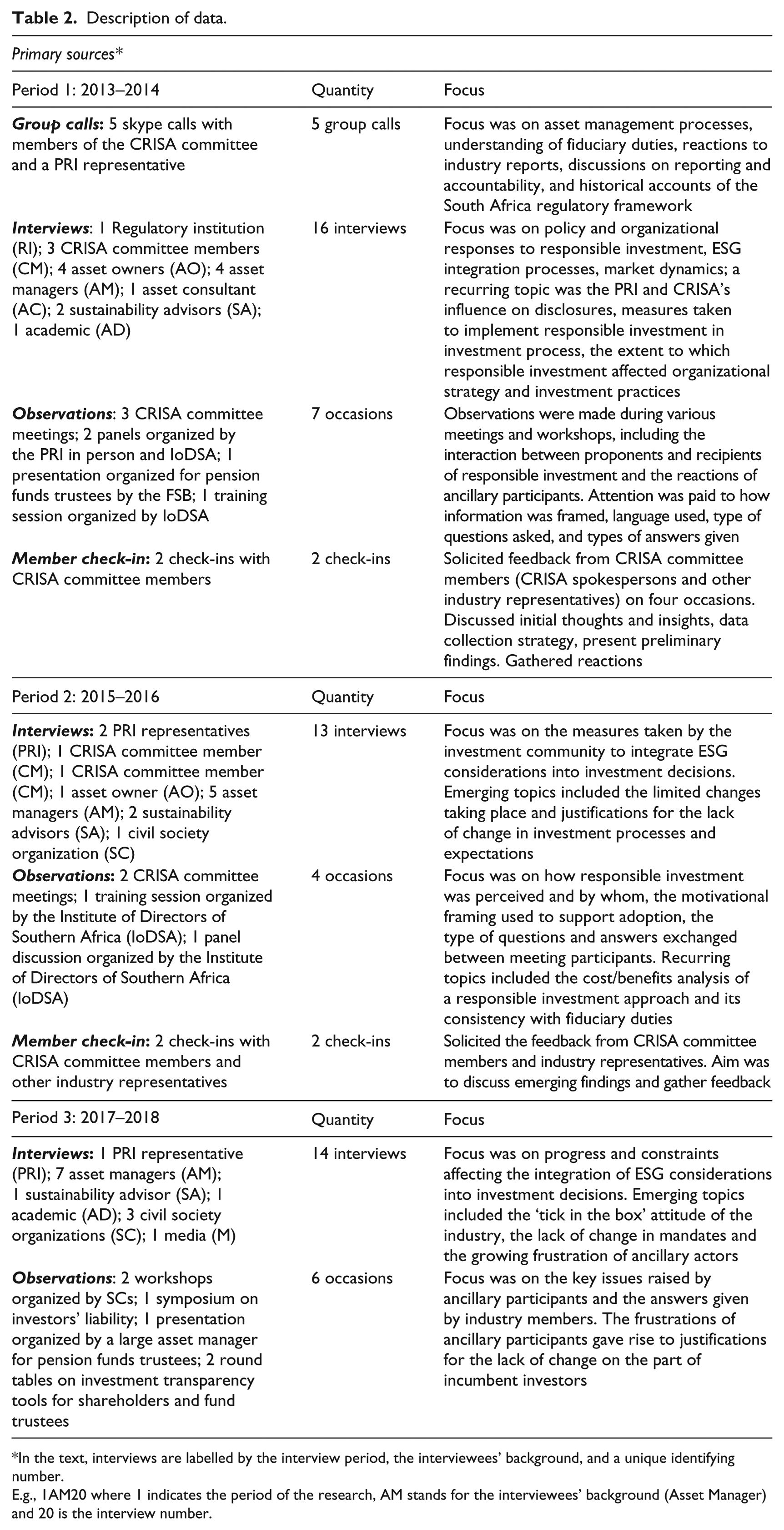

Our data consists of both primary data and secondary documents as outlined in Table 2. Our primary data emanated from group calls, interviews, observations, and member check-ins conducted during three periods: in 2013-2014, in 2015-2016, and in 2017-2018, providing insights into the day-to-day realities and perceptions of individuals either influencing, implementing or observing change within the field, and allowing us to track changes over time. Interviewees were selected among three types of field constituents: proponents of responsible investment (such as representatives of PRI in South Africa, members of the CRISA committee or representatives of regulatory institutions) actively framing and promoting the uptake of responsible investment; recipients of the frame (asset owners, asset managers, and asset consultants) interpreting and implementing responsible investment; and ancillary participants (such as civil society groups, academics, or sustainability advisers) observing or contributing to the field-level pressure to change. A total of 41 individual interviews and 5 group discussions (conference calls) were undertaken, each lasting between 45 and 60 minutes. Two participants were interviewed on two occasions during the study.

As outlined in Table 2, observations were made on 17 occasions at CRISA committee meetings, industry panel discussions, training sessions, presentations, workshops, roundtables, and symposia. These observations provided additional insights into the interpretive dynamics and the “positioning” of the responsible investment debate by the industry, helping to identify what was considered acceptable and legitimate by organizations. These occasions also provided the opportunity for informal interviews and discussions with attendees. Finally, member check-ins were used to elicit feedback from a range of actors (including representatives of PRI in South Africa, industry members sitting on the CRISA committee, and representatives of regulatory institutions) with respect to the emerging findings and to improve the validity of our interpretations.

Description of data.

In the text, interviews are labelled by the interview period, the interviewees’ background, and a unique identifying number.

E.g., 1AM20 where 1 indicates the period of the research, AM stands for the interviewees’ background (Asset Manager) and 20 is the interview number.

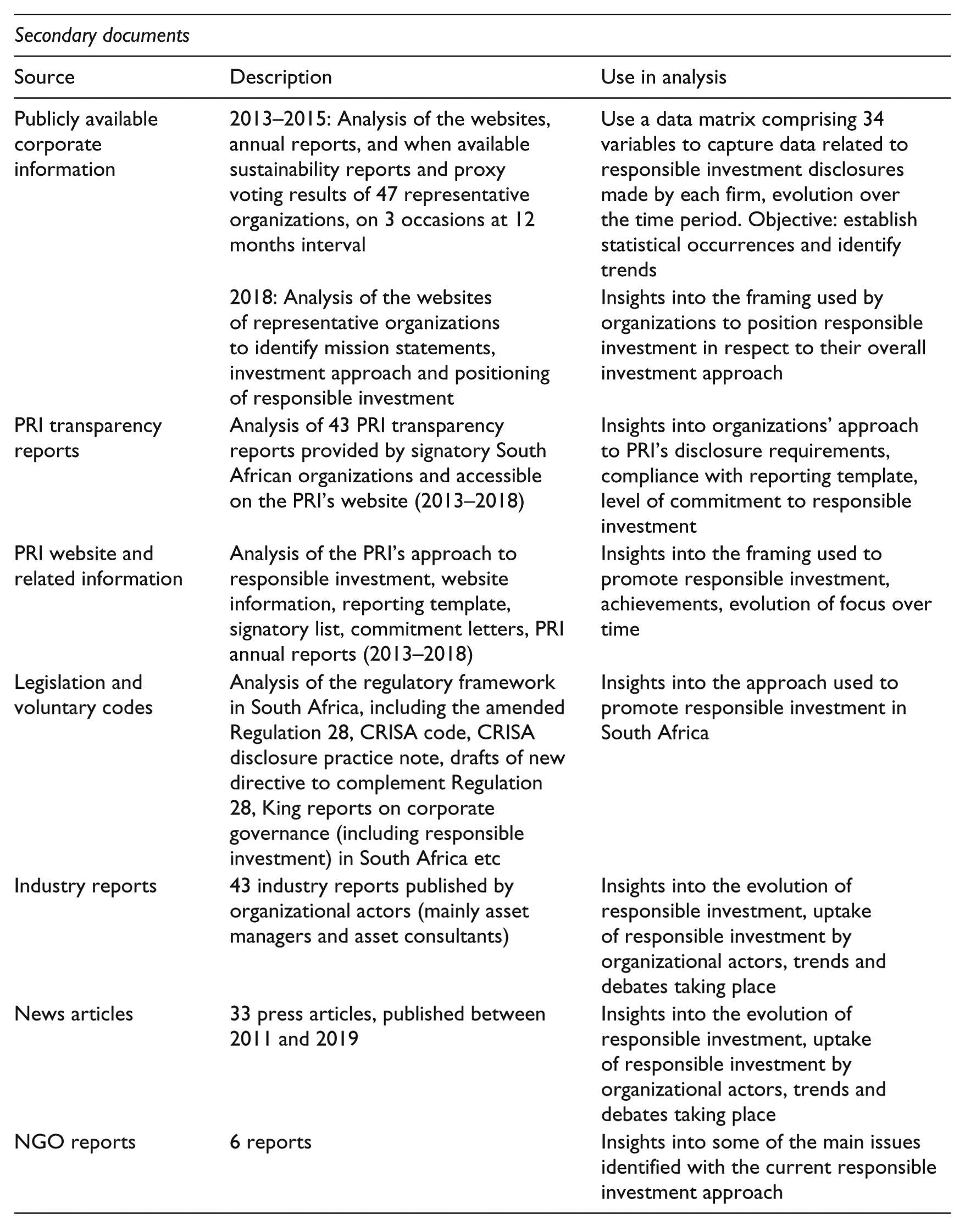

Our secondary data collection strategy involved three interrelated stages and covered data spanning from 2006 to 2019. First, we collected documentary data from the PRI website; the PRI’s annual reports and related publications; South African legislation; and CRISA-related publications to trace the development of the frame used to promote responsible investment since the launch of the PRI in 2006. Second, we gathered data from the websites, annual reports, and, depending upon availability, sustainability reports and PRI transparency reports of South African investment organizations between 2013 and 2016, to understand how the frame translated at the organization level into responsible investment disclosures. Data was collected at 12-month intervals from a sample of 47 South African financial institutions. The sample includes 29 asset owners (20 pension funds and 9 large financial institutions) and 18 service providers (14 asset managers and 4 asset consultants). Institutions were selected based on their size to ensure that the sample included a minimum of 80% of the assets under management per category of institution and overall in South Africa (estimated at around $600 billion). To facilitate a systematic comparison and establish disclosure patterns over the period, we compared the publicly disclosed information to the guidelines provided by the CRISA Disclosure Practice Note published in 2013. To do this, we captured data in a matrix (Miles, Huberman, & Saldaña, 2014) that included 32 variables or questions structured around the three elements of the CRISA disclosure framework (IoDSA, 2013); namely, the disclosure of policies, the disclosure of ownership practices, and the comprehensive disclosure of the implementation of the five CRISA principles. As outlined in Table 3 (see Appendix), we used the matrix to convert the qualitative data captured into numerical codes that were then used to establish the availability and progress of public disclosures across the South African investment industry. As outlined in Table 4 (see Appendix), we then rated the quality of the information provided as comprehensive, under-specified, minimal, or not available. Not applicable refers to certain types of disclosures not required for service providers. Finally, we reviewed South African press articles, industry reports, as well as NGO reports to gain a contextual understanding of key debates, actors’ positions, and other dynamics at play since the launch of the PRI in 2006.

Data analysis

We adopted an abductive approach to data analysis, working iteratively between making sense of our data through conceptual groupings and reviewing prior research to identify connections to our developing theory (Charmaz, 2011; Locke, 2011). Our coding focused on the framing activity of proponents of responsible investment, the interpretive responses of the other field actors and the practical changes they reported.

First, we used a data triangulation summary table (Miles et al., 2014) to combine our quantitative and qualitative data, tracking patterns in disclosure and practice changes related to responsible investment across the industry. A sub-sample of this table presenting illustrative data is presented in Table 5 (see Appendix). This mixed method approach suited our multilevel analysis (Hoffman, 2001), permitting us to gain both textured organizational-level understandings of how change was positioned across the field and specific individual-level insights related to how actors interpreted issues. Coding for changes in practice further enabled us to distinguish public disclosures from substantiated outcomes.

Next, we contrasted the diagnostic, prognostic, and motivational components of the frame of responsible investment with the SRI frame, we coded for the different ways in which financial organizations engaged with the frame, and examined the reactions of ancillary participants. Finally, we worked to establish connections between our emerging conceptual groupings and prior research. For example, coding related to the interpretation of responsible investment including “business-as-usual,” “discursive adjustments to policies,” and “inconsequential changes” was grouped as “rhetorical changes.” We were then able to contrast these findings with Cornelissen and Werner (2014)’s suggestion that field settlements implied new lines of action, leading us to differentiate between rhetorical, incremental, and disruptive field settlements.

Findings

We first describe the approach taken by the proponents of the responsible investment frame to promote field-level change, contrasting their articulation of the diagnostic, prognostic, and motivational components of the frame with the approach taken by SRI proponents. Next, we examine how the recipients of the frame responded and put into practice the responsible investment frame—by dissociating, normalizing, and moderating—and discuss the limited change these actions generated. Finally, we reflect on how ancillary participants, such as civil society representatives and academics, made sense of the frame and how their interpretation of it affected their ability to hold incumbent investors to account.

The proponents’ approach to framing

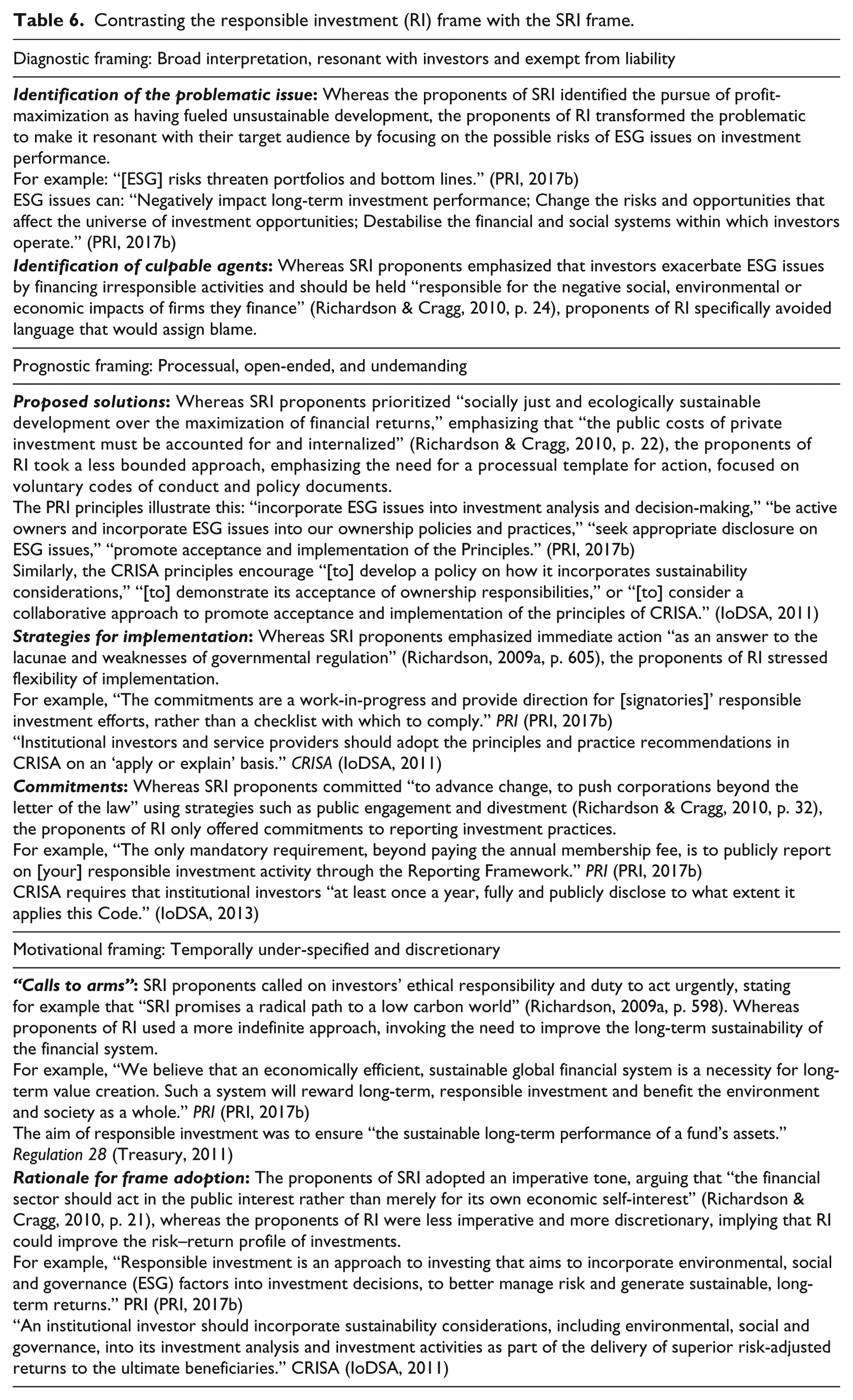

In the South African context, the PRI and CRISA were the principal proponents of the responsible investment frame. To better understand their approach to framing responsible investment and their use of ambiguity, we compare the underlying components of the responsible investment frame and the SRI frame. As outlined in Table 6, the responsible investment frame was structured around a diagnostic component that reinterpreted—or rekeyed (Goffman, 1974)—the problematic to make it both resonant with frame recipients and exempt of blame. The prognostic component of the frame was structured around a processual template for action that stressed an open-ended implementation process. The motivational component used a temporally indefinite and discretionary approach, emphasizing the opportunity to improve the long-term sustainability of the financial system and the risk–return profile of investments.

Contrasting the responsible investment (RI) frame with the SRI frame.

The diagnostic component

In outlining the core problem, the proponents of responsible investment used language and terminology similar to that employed by the SRI proponents (PRI, 2017b), touching on themes such as environmental problems, social issues, and sustainability, and even referencing specific ESG factors such as climate change, working conditions, or executive pay (PRI, 2017b) but avoiding language that would assign blame. Whereas SRI proponents lamented how beliefs and practices focused on profit maximization had fueled unsustainable development, the proponents of responsible investment emphasized the risks carried by ESG issues for investment performance, as evidenced in the declarations endorsed by signatories of the PRI:

As institutional investors, we have a duty to act in the best long-term interests of our beneficiaries. In this fiduciary role, we believe that environmental, social, and corporate governance (ESG) issues can affect the performance of investment portfolios (to varying degrees across companies, sectors, regions, asset classes and through time). We also recognize that applying these Principles may better align investors with broader objectives of society. (https://www.unpri.org/signatories/become-a-signatory)

Thus, the core problem, as articulated by the PRI, was that ESG factors carried “risks and opportunities that have a material effect on returns” (PRI, 2017b) and that considering them could contribute towards a better alignment between investors and society. As pointed out by a representative of the PRI, “it’s been more about ESG as an [investment] concept rather than addressing specific ESG issues” (PRI 11). Whereas the proponents of SRI articulated clearly that investors should be held responsible for exacerbating ESG issues and financing irresponsible activities (Richardson & Cragg, 2010), the PRI and CRISA only made reference to the fiduciary duties that investors have towards investment beneficiaries, stating that “investors could incorporate financially material ESG issues as part of their fiduciary duties” (PRI, 2017b).

The prognostic component

Whereas the SRI proponents prescribed prioritizing social and ecological impact over the maximization of financial returns and emphasized the need for immediate action (Richardson & Cragg, 2010), the proponents of responsible investment vaguely prescribed “win-win” outcomes that could be easily obtained by signing up to voluntary codes of conduct and engaging in minimal practice adjustments and reporting processes. For instance, the principles developed to guide the implementation of responsible investment gave options of “possible actions [emphasis added]”, such as “address[ing] ESG issues in investment policy statements,” or “ask[ing] for ESG issues to be integrated within annual financial reports” (PRI, 2017b).

Signatories were also left free to define the extent of their action, being required only to integrate responsible investment “where consistent with [their] fiduciary responsibilities” (PRI, 2017b). CRISA also outlined process-oriented principles that were only slightly more onerous, recommending an “apply or explain” approach and asking institutional investors “[to] develop a policy on how it incorporates sustainability considerations,” or to “consider a collaborative approach to promote acceptance and implementation of the principles of CRISA” (IoDSA, 2011).

The only prognostic elements with any degree of specification from either party related to reporting (in the case of the PRI) or disclosures (in the case of CRISA). In 2012, the PRI reporting framework became compulsory for all signatories after their first year: “It is one of the explicit commitments that signatories make when signing the Principles. Signatories that fail to report are delisted” (PRI, 2017b). Similarly, the initial publication of CRISA was complemented in 2013 by a Disclosure Practice Note “presenting a guideline with reference to content, timing and medium for CRISA disclosure” (IoDSA, 2013) that focused on the disclosures of policies, ownership practices, and CRISA implementation.

The motivational component

The motivational framing adopted by the proponents of responsible investment contrasted with the urgency expressed by SRI proponents. The PRI and CRISA focused on the need to establish “a more sustainable global financial system,” encouraging investors to consider “long-term value creation” (PRI, 2017b) and urging investors “to ensure that investment portfolios are resilient to the financial implications [of ESG]” (PRI, 2017b). They relied on familiar industry language to emphasize how responsible investment was straightforward to integrate and aligned with existing practices: “[responsible investment] simply involves including ESG information in investment decision-making, to ensure that all relevant factors are accounted for when assessing risk and return” (PRI, 2017b). According to their framing, responsible investment did not restrict investors and could “be pursued even by the investor whose sole purpose is financial return” (PRI, 2017b); investors only had to “consider those issues that could potentially negatively or positively impact on [their] investment and manipulate the positives or the negatives to actually achieve a better outcome” (PRI11). As articulated by another PRI representative (PRI 12):

Responsible investment is . . . the same [as conventional investing], but it’s just saying, “Well, [to be] a good steward of other people’s money, we need to consider [ESG] issues and we need to take a longer-term position on some of these issues.

South Africa’s Regulation 28 built on the PRI approach, motivating the adoption of responsible investment as a way to generate “sustainable long-term performance” (Treasury, 2011). Similarly, CRISA inscribed the consideration of sustainability and ESG factors “as part of the delivery of superior risk-adjusted returns” and justified responsible investment based on sound governance (IoDSA, 2011). As summarized by a CRISA member (1CM 9), the rationale for adopting responsible investment is centered around “being a good investor, not necessarily being a responsible investor. In trying to mainstream responsible investment, the view was, ‘Let’s rather downplay the moral obligation and rather say it’s about good business sense, good investment decision making’.”

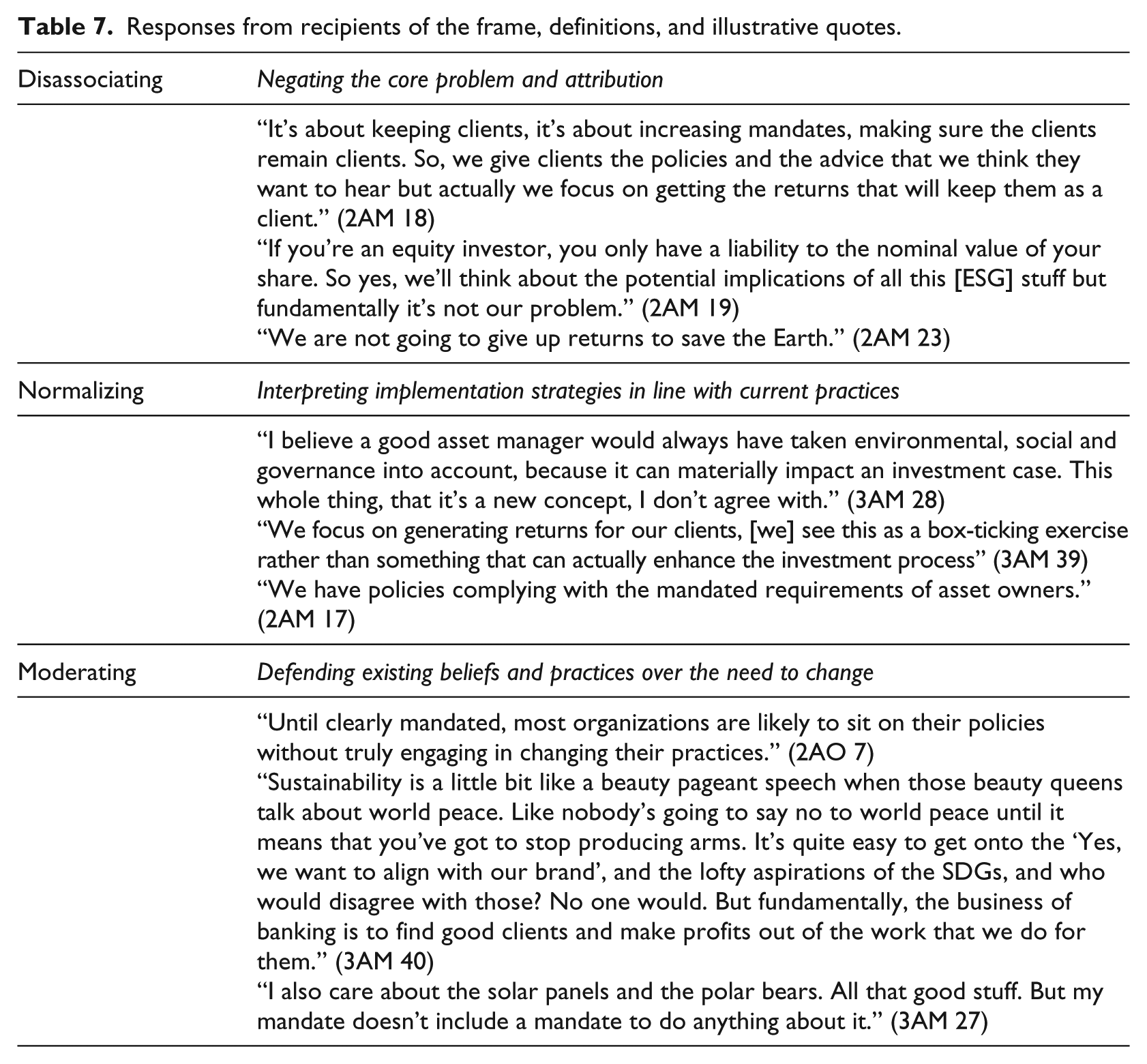

Categorizing the frame recipients’ interpretive responses to responsible investment

To better understand the interpretive responses of frame recipients—asset owners, asset managers and asset consultants—we categorized how individuals within these organizations perceived each component of the frame, identifying three key responses: dissociating, normalizing, and moderating. As outlined Table 7, dissociating was the main response to the diagnostic component of the frame. A majority of asset managers did not perceive the existence of a significant problem and distanced themselves from any responsibility. They rejected the need for any adjustments to practice on the basis that they were incompatible with the dominant framework and questioning the value of ESG integration with respect to dominant expectations. For instance, one respondent (2AM 19) emphasized that the role of investment managers was “to deliver outperforming financial results compared to the sectors’ benchmarks” while another (2AM 17) commented, “my responsibility is to get the right price and the right return. ESGs are not factual things I can respond to.” Many respondents questioned the value of “fluffy” environmental or social data that are difficult to accurately integrate in current investment practices.

Responses from recipients of the frame, definitions, and illustrative quotes.

The dominant response to the prognostic component of the frame could best be described as normalizing. Most analysts and portfolio managers within asset management firms would describe the implementation of responsible investment as “no big deal” and stressed that it would not fundamentally change investment priorities. For instance, an asset manager (2AM 19) noted, “we take all factors into account in our modelling, but we don’t want to overreact or for ESG factors to distort the fundamentals of our analysis.” An asset consultant (1AC 24) further described the open-ended and undemanding nature of ESG integration, explaining, “We pursue a low-lying fruit approach, focusing on what is easiest first and leaving the rest to be implemented when we have more clarity.”

Finally, moderating was the main response to the motivational component of the frame. Respondents would explain why existing beliefs and practices took priority over the need to change, citing the misalignment of timeframes and the constraints of the investment process. For instance, a sustainability manager at an asset manager (3AM 40) explained,

The timeline is probably the biggest problem because sustainability forces you to look at long-term horizons, while in banking, a year is long term. Asking people to look at the long term doesn’t make any sense because we’ve made our money before [anything is] even an issue.

Instead, the main rationale for adoption centered around the identification of risk–return opportunities. For instance, when asked to provide an example of “successful” ESG integration, one investment analyst (3AM 21) reflected on his decision to purchase Lonmin’s stock following an incident of social unrest in Marikana resulting in the death of 34 mine workers at the hands of police by noting that “the Lonmin stock had been oversold. Taking into account ESG factors enabled us to identify this stock as a buying opportunity.”

The recipients’ implementation of the frame

Our analysis reveals that the majority of recipients publicly supported responsible investment and engaged in some form of PRI reporting and/or CRISA disclosure (See Tables 3 and 4 in the Appendix). By 2016, 50% of the organizations we studied reported having one or more of the policies suggested by CRISA and 40% made these publicly available. Additionally, 40% published information regarding their voting results, 23% of which met CRISA’s guidelines. Furthermore, 70% of organizations that were PRI signatories published a PRI transparency report.

Yet, except for a few leaders, the changes appeared mostly rhetorical in nature, limited to the creation of policies and the publication of voting results that did not require a departure from a “business-as-usual” framework. The policies consistent with CRISA’s recommendations pertained to ownership and conflict of interest, while sustainability policies were mostly basic or insufficient, at best using tailor-made definitions and limited to a few sentences. Only 6% of our sample had comprehensive sustainability policies or provided evidence of some practical implementation. Only two asset owners comprehensively disclosed having reviewed the mandate determining how funds were managed, and only one asset owner (1AO 2) reported working with their asset manager “to align voting positions, agree on engagement strategies, and develop tools to better assess investee companies.”

The interviews we conducted sought to check that firms did not under-report their performance to avert allegations of greenwashing or that firms reporting more succinctly than others did not actually perform better than their reporting suggested. However, our interactions with respondents strongly indicated that the public support for responsible investment was mostly symbolic and was not part of a process leading to more substantive actions. Even among leaders, investment practices remained largely unchanged. As explained by a portfolio manager (3AM 39), “because we haven’t really set our business up with that ESG focus, they are often an irritation coming at the wrong time in the investment process.” While recent corporate scandals had raised awareness around governance issues, the integration of environmental or social factors was rarely taken into account. At best, ESG integration was tailored to fit existing industry practices and focused on “integrated analysis,” a practice that enables investors to consider ESG risks without fundamentally modifying their investment strategies, where ESG analysis was used as an added tool to take advantage of under-analysed themes in stock picking and stock selling (EUROSIF, 2015).

Existing practices were also reinforced by reward and incentive structures that remained largely unchanged. For example, one asset manager (2AM 25) explained, “the pressure is on short-term returns”, adding, “we are paid on the basis of the performance of our investment choices, and this is rarely measured in the long term!” An investment analyst (3AM 21) also pointed to the role of asset consultants in perpetuating the short-term focus of investment, explaining that “[asset consultants] are remunerated based on the short-term performance of the funds they recommend.”

Moreover, while the PRI and CRISA framed asset owners as driving change in the industry, the asset owners did not take on the leadership role that was assigned to them. As a pension fund representative (1AO 2) explained, “many [asset owners] have a limited understanding of responsible investment and are reluctant to engage in alternative and poorly understood strategies.” The apathy of asset owners seemed to deter asset managers’ engagement, creating a circle of blame and inertia:

A manager will say “well, why isn’t this stuff included in the mandate?” A consultant will say “it’s a good idea but we won’t do it until we speak to the trustees.” The trustees are like “well, it’s a good idea but we only act on behalf of the beneficiary so you have to speak to them,” and so it goes. In that kind of circle, there’s a lot of systemic inertia that prevent things from shifting. (3AM 27)

Consequently, the early frame employed by the PRI and CRISA to promote responsible investment has left the industry largely unchanged and unchallenged. We did not find any significant evidence that, over time, investors made material changes to their investment practices. Observable changes were limited to the rhetorical adjustments of policies and some disclosures, while practices and expectation remained anchored in what came before. Respondents referred to a tick-the-box attitude and a focus on legal compliance. As a respondent (3AM 28) explained, “I think there’s a lot of the emperor wearing no clothes just to keep the status quo, to improve the size of the mandate that you have for a particular client.” Our findings are consistent with recent research commissioned by the PRI (Tomlinson et al., 2017, p. 7), concluding that the challenge was for “the intent of regulation and principles-based codes to be reflected in the investment processes and decisions,” and that South African investors might be “aware of ESG issues in theory, but may not understand what it means in practice.”

Why didn’t the ancillary participants hold other field actors to account?

While one might have expected ancillary participants such as civil society organizations, academics or sustainability consultants—who had been active SRI voices—to act as countervailing forces pushing investors to engage in more substantive actions, this did not materialize in this context. Rather, there appeared to have been some confusion among ancillary participants around the meaning of responsible investment and the types of field-level changes it ought to yield. Over time, this led to growing levels of frustration, with some of these actors claiming that responsible investment was not “strong enough” to engender the level of institutional change needed to address pressing societal challenges, and that a new period of “organized civil society activism” was needed.

Initially, ancillary participants were congratulatory of the change effort initiated by the PRI and CRISA. They appeared to interpret the responsible investment frame as a version of SRI made more “palatable” to mainstream investors by taking into account their reservations pertaining to fiduciary duties, reducing the investment universe, or the perception that ethics would be driving investment decisions (Richardson, 2009b; Woods & Urwin, 2010). Numerous academic articles, press articles, and NGO reports—globally and in South Africa—began to use the terms “responsible investment” and “socially responsible investment” almost interchangeably. For instance, documents exploring the implementation of the PRI principles or CRISA have titles such as Being virtuous and prosperous: SRI’s conflicting goals, Sustainable and responsible investment (SRI) in South Africa: A limited adoption of environmental criteria, or Socially responsible investment and fiduciary duty: Putting the Freshfields report into perspective. In line with this interpretation of the responsible investment frame, the majority of ancillary participants seemed initially favorable to this “mainstreaming of SRI” (Child, 2015), expecting PRI or CRISA adopters to engage with societal issues such as climate change or inequality—albeit “on the basis of the relative financial risks and opportunities to the investor” (Richardson, 2009a, p. 598).

As time passed, the lack of change within the industry has led ancillary participants to question the effectiveness of responsible investment “to do good” (Busch et al., 2016; Himick & Audousset-Coulier, 2015). In South Africa, Viviers and Els (2017, p. 144) have highlighted the “tamed” nature of shareholder engagement and limited ESG integration, commenting that a “significant mind set shift [was] required” among local PRI signatories. In various events organized by the Institute of Directors of Southern Africa between 2015 and 2017 to discuss progress towards responsible investment, ancillary participants increasingly voiced their frustration. As such, a member of a civil society group (2CS 35) described financial institutions as “masters of vagueness” and declared, “We just don’t seem to be speaking the same language! We see very little outcome from local investors.” A sustainability advisor (3SA 36) explained, “Currently, we don’t see much beyond reporting. We see reporting as a willingness to engage, but it’s not what makes things change.” Another member of a civil society group (3CS 37) commented, “We are so far from adequate engagement that what we see is closer to misleading information.” This was echoed by a member of the financial press (3M 31), indicating there is a growing feeling that the industry has embarked on a strategy “to make believe that ESG is important [thereby] preventing change from happening.”

The initial frustration gave way to more organized and collaborative forms of advocacy. By 2017, several civil society organizations were starting to coordinate efforts with other advocacy groups and engage more forcefully with incumbent investors. Using media campaigns, online petitions, developing transparency tools, organizing seminars, engaging with management in private, and pushing forward shareholder resolutions, these civil society organizations were becoming collaborative platforms pushing for more regulatory pressure and trying to publicly hold investors to account. They inaugurated what appeared to be a new period of strong activism for change.

Discussion

Our study makes two key contributions to our understanding of frame ambiguity and its effect on field-level change. First, we differentiate between the impacts of the ambiguity generated by the diagnostic, prognostic, and motivational components of frames. While a certain degree of ambiguity may help to draw in a broader range of field actors, we caution that excessive ambiguity may ultimately stall field-level action. Second, we contribute to the study of field settlements by differentiating between rhetorical field settlements, incremental field settlements, and disruptive field settlements.

The bounding of ambiguous frames

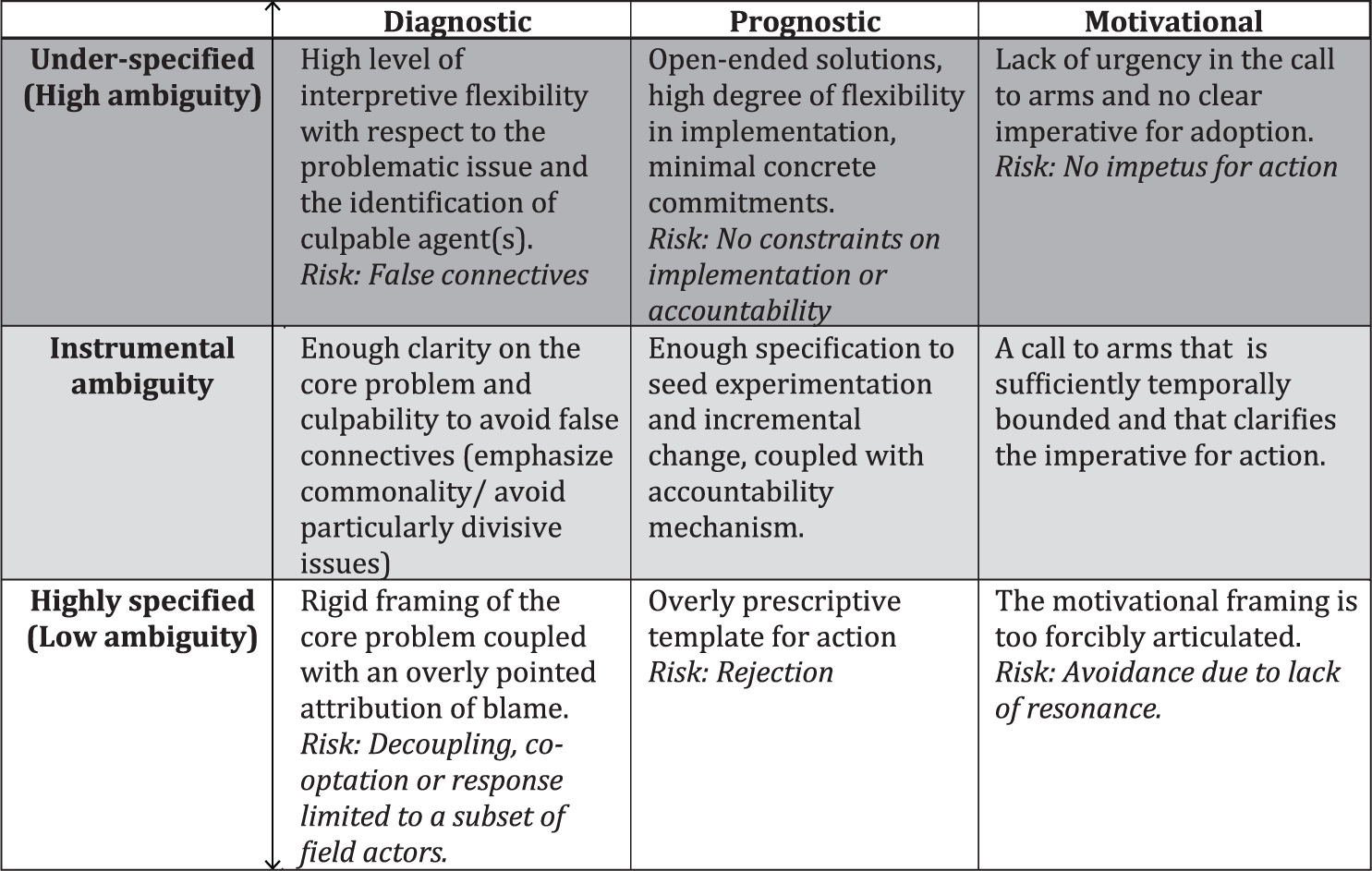

While recent research has emphasized that the framing of complex and contentious field issues is likely to benefit from ambiguity (Ferraro et al., 2015; Van Wijk et al., 2013), our study demonstrates that when under-specified, frame ambiguity may hinder rather than advance field-level change. It also challenges earlier suggestions that symbolic actions may lead to more material changes (Boxenbaum & Jonsson, 2008; Bromley & Powell, 2012; Edelman, 1992). Instead, we submit that highly ambiguous frames can lead to false impressions of progress, which can be counterproductive to the realization of change. As outlined in Figure 1, we propose that the degree of ambiguity of each component of a frame—diagnostic, prognostic, and motivational—is likely to generate distinct outcomes with respect to frame adoption and field-level action.

The impact of diagnostic, prognostic, and motivational frame ambiguity on field-level change.

We begin on the left-hand side of Figure 1 by exploring the generative potential of diagnostic ambiguity. The diagnostic component of a frame defines the problematic situation to be addressed and identifies the culpable agents. Prior work on ambiguity was likely referencing the diagnostic component as it counselled proponents of change to emphasize commonality and avoid divisive issues in order to foster cooperation between diverse actors (Ferraro et al., 2015; Gioia et al., 2012) and reduce the risk of decoupling by adherents (Greenwood et al., 2011). However, as outlined in Figure 1, care must be taken not to under-specify the diagnostic component of a frame by actively encouraging flexible interpretations that conceal irreconcilable differences and avoid assigning responsibility, or by making use of language that allows for false connectives (Goffman, 1974) between the frame and multiple primary frameworks that are fundamentally at odds. A generative use of ambiguity would emphasize commonality while providing enough clarity on the core problem and culpability to avoid the risk of false connectives and misdirected action.

For instance, the proponents of the responsible investment frame used language emphasizing “ESG integration” and “long-term sustainability” that financial organizations interpreted in the context of conventional investing, but that ancillary participants, such as civil society NGOs, interpreted as signaling the mainstreaming of the SRI movement. These false connectives acted to conceal what amounted to profound differences in associated meanings and may have lent the impression that the frame was promoting more transformational changes than it actually was. These false connectives may also help explain why it took so long for ancillary actors to begin to hold incumbent investors to account. Furthermore, while leaving the attribution of responsibility unspecified may have helped to get investors on board and avoid an “adversarial framing” (Gamson, 1995), it exempted investors from having to “responsibilize” their behavior and address the causes of “irresponsible” investment.

The central column of Figure 1 explores the generative potential of prognostic ambiguity. The prognostic component of a frame articulates potential solutions, strategies for implementation, and commitments to remedy an issue. Here we caution against open-ended solutions that provide a high degree of implementation flexibility and require limited concrete commitments. Instead, we argue for the need to more concretely specify the prognostic component in order to create boundary objects and accountability mechanisms that seed experimentation and around which frame recipients can negotiate new practices and construct new meanings. This is consistent with research that suggests that placing more emphasis on the implementation of policies can ultimately result in substantive change over time (Bromley & Powell, 2012; Edelman, 1992) and that templates for action portrayed in concrete terms and more prescriptive accountability mechanisms create the conditions for the negotiation of new meanings consistent with the new activities and practices (Etzion & Ferraro, 2010).

In our setting, the limited changes we did observe were centered on reporting and disclosures, the only explicit element of the prognostic component required by PRI and CRISA. In contrast, the remaining changes associated with responsible investment in this setting would be described as rhetorical at best, leaving established meanings and practices largely intact. We attribute this outcome to the processual, open-ended, and undemanding nature of the other principles promoted by PRI and CRISA, which allowed financial organizations—the recipients of the frame—to implement responsible investment in close alignment with the rules and premises of conventional investing. The lack of constraints on implementation and accountability mechanisms allowed financial organizations to interpret the template for action as close as possible to existing practices, thereby suppressing the need for active engagement in experimentation and change processes.

Finally, the right-hand column of Figure 1 explores the impact of ambiguity on the motivational component of a frame. The motivational component provides a “call to arms” and a rationale for frame adoption. Here we highlight that a lack of temporal boundaries and imperative for adoption can limit the impetus for action (Benford & Snow, 2000) whereas articulating the urgency too assertively risks narrowing the resonance of the frame. We argue that, to be generative, the motivational component ought to provide realistic temporal guidelines and clarify the urgency for action. This is consistent with research highlighting the important role of framing in regulating attention and helping field actors to negotiate competing priorities with conflicting temporalities (Reinecke & Ansari, 2015).

In our setting, the proponents of responsible investment invoked the need for change without stipulating any timeframe and while emphasizing a discretionary approach that positioned responsible investment as optional (but possibly advantageous). Efficient at lowering the barriers to entry and ensuring the frame’s resonance with its recipients, it fell short of providing incumbent investors a compelling rationale for change.

The main contribution of our study is to signal that a high degree of ambiguity risks being counterproductive to field-level change efforts, concealing a lack of progress and inhibiting material changes. We thus suggest that an instrumental use of ambiguity to promote change should seek to establish a balance between enough ambiguity to invite participation and reduce unease, and enough specification to “bound” (Hoffman, 2001) how actors interpret “what’s going on” (Goffman, 1974), promote the experimentation of new practices, and regulate understandings pertaining to the urgency and salience of action. We caution though that the over-specification of any one component of a frame is likely to run the risk of having field actors reject or avoid the frame. Rather, we propose that each component of the frame should be specified just enough to mobilize action while still allowing for flexibility and improvisation—creating what Rao (2008) would describe as a hot cause and a cool mobilization.

A good example of instrumental ambiguity might be found in how recycling advocates in the United States reframed the recycling social movement into a for-profit model in the 1980s (Lounsbury, Ventresca, & Hirsch, 2003). Providing enough specification, proponents of recycling drew public attention to the consequences of incineration and dumping by solid waste actors, they proposed to rely on the labor of citizens who already knew how to clean and sort while making use of existing solid waste infrastructure, and they motivated action both by developing new revenue streams and working with regulators to de-institutionalize certain practices. Yet, the frame was flexible enough to open up a discursive and practical space for experimentation, enabling field participants “to become part of the broader dialogue that shape[d] the range of possibilities” (Lounsbury et al., 2003, p. 96).

Ambiguous frames and field settlements

Our study also has implications for our understanding of the nature and outcomes of field settlements. The phenomenon of field settlement has been described as an agreement over an altered primary framework (Cornelissen & Werner, 2014; Fligstein & McAdam, 2011). When McAdam and Scott (2005) initially discussed the notion of field settlement, they suggested that there is likely to be a range of possible settlements whereby small settlements may ultimately culminate in profound institutional changes. Indeed, recent work examining field settlements has argued that they often serve as an indicator for further substantive action (Furnari, 2018; Litrico & David, 2017; Zietsma, Groenewegen, Logue, & Hinings, 2017). Yet, the settlement around responsible investment that we observed in this case appeared to reinforce the status quo rather that spur substantive action.

This leads us to distinguish between three types of field settlement: incremental, disruptive, and rhetorical settlements. Incremental field settlements are the result of frames that are specified enough to compel field actors to try and figure out “what is going on here.” In this instance, interpretations remain plural and contested, but actors are actively engaging in the experimentation and implementation of new policies and practices. For example, Litrico and David (2017)’s study of the field of civil aviation shows how front-stage actors progressively integrated new policies and practices into their core operations while retaining a plurality of understanding of issues. In contrast, disruptive field settlements draw upon the notion of a frame-break (Goffman, 1974) to signal a shift in the primary framework. In disruptive field settlements, actors reach a new shared understanding of the rules and premises guiding action. Disruptive field settlements are thus likely to include substantial changes to field membership rules, and/or standards and practices. For instance, Zietsma and Lawrence (2010)’s study of the field of coastal forestry in British Columbia offers a good example of a disruptive settlement, whereby the position of dominant actors was seriously challenged, new harvesting practices were defined, and new rules and standards were adopted.

In contrast, we propose that in the context of excessive frame ambiguity, field settlement may be primarily rhetorical, where differences in interpretations are obscured by false connectives and where there is limited—if any—impetus for the experimentation of new practices, an outcome we call rhetorical field settlement. We propose that rhetorical field settlements are primarily the result of under-specified frames that mislead actors’ interpretive dynamics and do not encourage the emergence of new patterns of action. Giving the impression of a consensus, they conceal dissensions between field actors about “what is going on.” This outcome is well captured by Goffman (1974, pp. 1–2) who notes, “[d]efining a situation as real certainly has consequences, but these may contribute very marginally to the event in progress. . . [o]ften, once these are negotiated, we continue on mechanically as though the matter had always been settled.” Whereas incremental field settlements might be an indicator for further substantive action, potentially leading to disruptive field settlements as actors experiment and construct new meanings, rhetorical field settlements are instead likely to frustrate field-level change processes. In the longer term, rhetorical field settlement could exacerbate actors’ positions, leading to open disputes rather than a progressive alignment regarding the course of action (Goffman, 1974).

Limitations

While drawing upon secondary data for our analysis of field-level trends has a number of advantages, it also comes with some limitations. For instance, although websites and annual reports are recognized instruments of presentation and communication, they may not capture the full extent of the conversation that led to these public statements, which could have introduced biases to our interpretation. We also acknowledge that a real-time study investigating a field’s evolution over a longer timeframe could lend additional insights into how ambiguous frames evolve over time in conjunction with organizational responses and field-level change. Further studies could also consider whether organizational responses to ambiguous frames differ across locations, cultures, and regulatory frameworks. Finally, there would be value for future research to investigate how rekeying might be used by adopters to decouple policies from practices or means from ends (Bromley & Powell, 2012; Meyer & Höllerer, 2016), and whether false connectives in frames could facilitate field-level co-optation by certain actors (O’Sullivan & O’Dwyer, 2015).

Conclusion

We set out to better understand how frame ambiguity affects field-level change. Based on our analysis of the rise of responsible investment in South Africa, we highlight that excessive frame ambiguity may be counter-productive and ultimately stall field-level action. While helping to draw in a broader range of field actors and giving an appearance of success, highly ambiguous frames may inhibit material changes and conceal a lack of progress. In crafting a frame we suggest proponents should aim to balance between enough ambiguity to invite participation and reduce unease, and enough specification to regulate the understanding of the problem, promote experimentation with new practices, and clarify the impetus for action. Our study also challenges the assumption that a field settlement is an indicator of further substantive change processes in the field. By distinguishing among rhetorical, incremental, and disruptive field settlements, we respond to the call by Zietsma et al. (2017, p. 415) to disentangle the processes and outcomes of field-level changes, including possible “pathways that lead to failure rather than success.” As many institutional fields are under pressure to transform in response to material societal issues, understanding how to construct frames that can help fields transcend beyond current business-as-usual frameworks represents an important agenda.

Footnotes

Appendix

Sample of data from the coding of “sustainability policies” and “application of CRISA Principle 1.”

|

|

|

|

||||

|---|---|---|---|---|---|---|

|

|

|

|

|

|||

|

|

|

|||||

| Referencing clear definitions consistent with CRISA, showing a detailed and reflective approach, covering several elements or aspects of the disclosure required, providing some information on practical application | “Sustainability means meeting human needs and wants in a systematic, forward-looking and holistic manner, while staying within nature’s limits. [. . .] The sustainability perspective holds that to drive business by shareholder value alone is largely unsustainable. [. . .] Profits should be harmonized with people and the planet (hence ESG).” (Company 1) |

Creation of a team/Committee formally mandated to co-ordinate and drive the organization’s approach to sustainability Quarterly release of reports to the CEO and Executive Committee Establish and publish list of most important issues the organization is willing to engage (Company 1) |

“Responsible investing marks a change in the objective of investment management from maximizing returns, to earning adequate risk-adjusted returns. [. . .] The objective of responsible ownership is to include all financially-material ESG issues systematically in investment analysis and activities, by focusing on how companies manage ESG issues strategically over and for the long term. The UN PRI’s third principle requires investors to seek appropriate disclosure on ESG issues by the entities in which they invest.” (Company 21) |

Research into investment-related environmental and social risks and opportunities Vote on all resolutions Possible engagement with investee company on material environmental and social issues Creation of ESG funds (Company 21) |

||

“The board of trustees have been entrusted with the achievement of the responsible investment objectives. This includes taking a 3 to 5 year view on ESG issues such as climate change, diversity or remuneration” (1AO2—from within this 6% of firms) |

“The ESG team has grown in three years from one person to a team of four, including a very senior and experienced sustainability executive.” (2AM15—from within this 4% of firms) |

|||||

|

|

|

|

||||

|

|

|

|

|

|||

|

|

|

|||||

| Referencing tailor-made definitions and partial or narrow focused information usually in line with business-as-usual, disclosing minimum levels of information, providing limited information on practical application | “[Company 26] recognizes that the sustainability of the business lies in its ability to attract and retain clients. Meeting the targets set by the Financial Sector Code (“FSC”) is an important component of client retention in the institutional market. It is also an important aspect in the context of contributing towards the broader transformation of South Africa to an integrated, balanced and growing society and economy.” |

The head of sustainability reports to [the company]’s Financial Director on the following issues: • Audit • Fair practices • Risk and compliance • Ethics and transformation (Company 26) |

“We consider economic, social and governance (ESG) factors as part of our fundamental investment analysis, since we recognize that these issues can carry risks that could affect our environment and broader economy, as well as diminish potential investment returns for our client portfolios. [. . .] Investment decisions are made after giving appropriate consideration to all factors that influence an investment’s risk or return . . . we typically invest in assets that we believe are mispriced because the market is overly pessimistic on their future prospects.” (Company 32) |

Review at Audit, Risk and Compliance Committee (Company 32) |

||

“Our approach to sustainability is promoting “the long-term financial performance and viability of the company.” (1AM20—from within this 17% of firms) |

“We recognize the merit in considering ESG, but our priority is in getting the right return.” (2AM19—from within this 30% of firms) “Our legal-compliance team has worked to show that we are compliant.” (3AM21—from within this 30% of firms) |

|||||

|

|

|

|

||||

| Disclosure limited to a brief mention, with no definitions, no explanation, and no information on practical application | “Responsible and sustainable investing is an important consideration for [our company]”. (Company 34) |

No references to implementation among these firms |

“Our investment-decision making process has been designed to adhere to global best practice including amongst others: • United Nations Principles for Responsible Investment (‘UN PRI’) • Code for Responsible Investing in South Africa (“CRISA’)” (Company 36) |

No references to implementation among these firms |

||

“[Our company] is one of the largest corporate donors in South Africa.” (2AM23—from within this 17% of firms) |

“We will be very careful about which battles we will fight, if you want to put it like that, because we want the best outcome for our clients. Too much focus on ESG issues by asset managers could detract from the ‘old-fashioned’ metrics of evaluating a company.” (3AM29 -from within this 13% of firms) |

|||||

|

|

|

|

||||

Acknowledgements

We would like to thank John Sillince and three anonymous reviewers, who helped shape and improve this article.

Funding

This research was supported by the Social Sciences and Humanities Research Council of Canada.