Abstract

As the Global South shifts towards increased manufacturing, the negative effects on climate change and environmental pollution raise serious concerns. These global effects are increasingly felt locally, as reflected in health surveys throughout the Global South. The world cannot afford to wait for a natural development process to take place in which rising incomes might curb pollution. This article examines the challenges of reforming manufacturing in the Global South towards more sustainable practices. It also focuses on the lessons of the Sustainable Manufacturing and Environmental Pollution Program (SMEP) which has funded a series of environmental improvement projects across sub-Saharan Africa and South Asia aimed at reducing pollution in the manufacturing process. The lessons learned from these projects include the need to improve the tracking of the negative effects of the environmental damages caused by manufacturing and analyze the manufacturing supply chain processes to better identify potential points of intervention; as well as the need for more external financial and technical resources to expand these projects.

Keywords

Introduction

Manufacturing is one of the main sources of global pollution. While it is not the largest source of greenhouse gas emissions—it lags energy, transport, and agriculture—emissions from industry have grown the fastest (cumulatively) since 1990 at 187%, according to the World Resources Institute (2021). 1 More promisingly, manufacturing offers multiple pathways towards sustainability. The often-centralized locations for manufacturing (Rosenthal & Strange, 2001) mean that businesses and policymakers can focus on key supply-side interventions to transform supply chains, rather than relying upon unpredictable market shifts or technological breakthroughs (Cedillo-Campos, 2014; Leopoulos et al., 2007).

Manufacturing is growing fast in the Global South. Manufacturing value-added 2 in sub-Saharan Africa (SSA) and South Asia (SA) has seen an approximately three-fold and seven-fold increase, respectively, between 1990 and 2020 (World Bank, 2021). With this accelerated industrialization has come an increasing burden of environmental pollution and disease. Beyond contributing to climate change, manufacturing contributes to the ambient particulate matter in the earth’s atmosphere, now the sixth leading cause of deaths across the globe (Health Effects Institute [HEI], 2018). The most significant number of deaths from pollution is concentrated in SSA, SA, and some parts of the economies in Eastern Europe. The contaminants spread through air and water, lead exposure, occupational and contamination sites, and pesticides are leading causes of disease (Landrigan et al., 2018).

Very few assessments of potential pathways towards green or sustainable manufacturing in the Global South exist. The literature is too nascent to arrive at any clear conclusions about moving forward. There is not even consistent monitoring of the effects of manufacturing pollution. Commonly cited factors inhibit the transition to environmentally sustainable economies, such as inefficient and dirty energy systems and the lack of finance, knowledge, and market incentives to make this transition.

This article focuses on a series of experiments to reduce manufacturing pollution at its source in the Global South. It shares lessons from the Sustainable Manufacturing and Environmental Pollution Program (SMEP), which has a series of projects in SA and SSA funded by the UK Government at £24.6 million to reduce pollution and promote a more circular production process. These SMEP projects have revealed additional obstacles beyond those cited in the literature, including informality, the lack of centralized waste infrastructure, and the need for greater public-private collaboration and awareness-raising.

The Growing Challenges of Pollution in The Global South

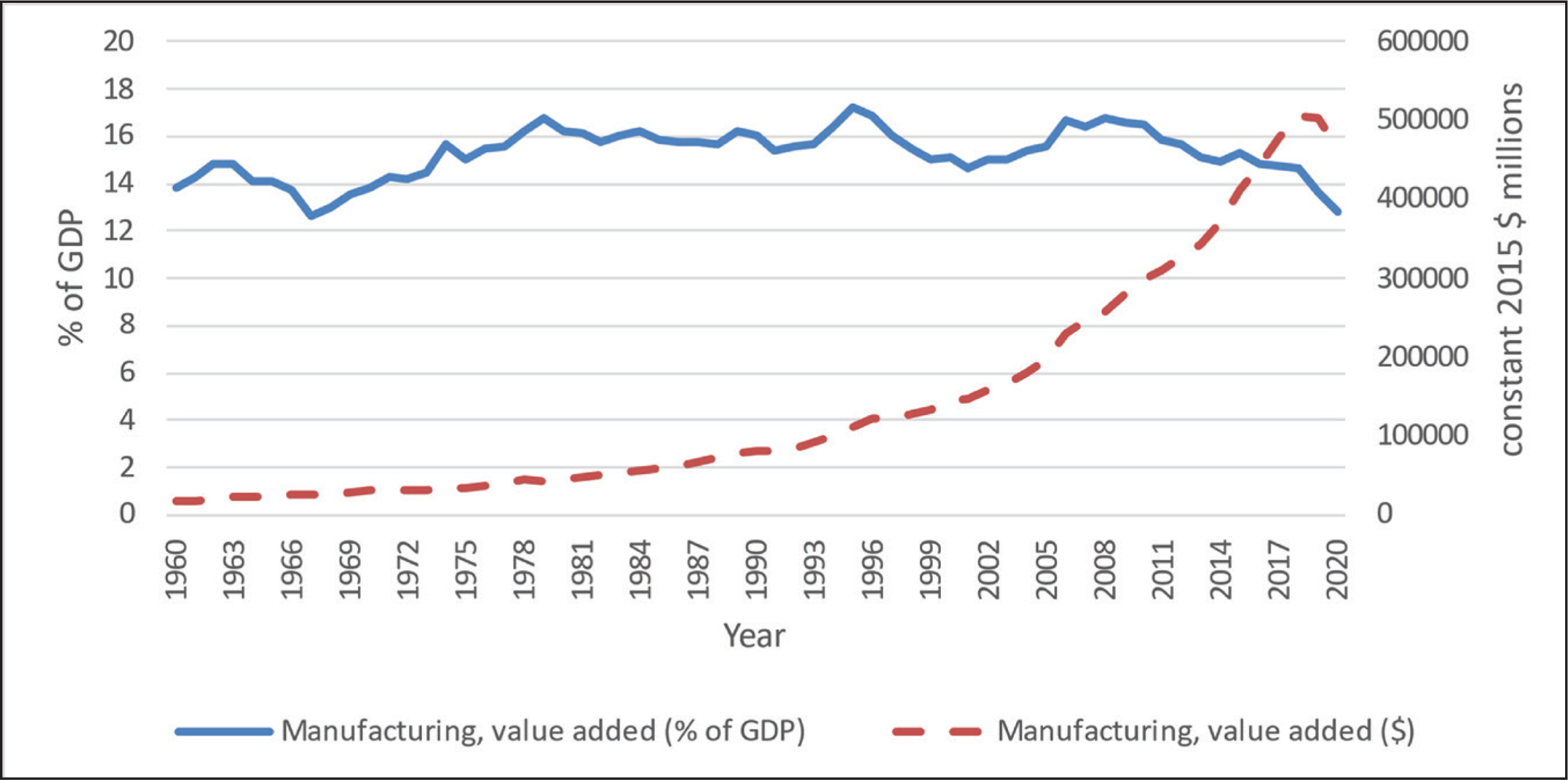

The low wage levels and high population growth in SA and SSA make them centers for future global manufacturing growth. The expansion of manufacturing is slowly radiating outwards from China, where labor costs have increased. As revealed in Figure 1, while manufacturing has stayed relatively stable in SA as a percentage of GDP, the overall value of manufacturing has risen rapidly in the region, particularly since the 1990s. A slight dip due to the COVID pandemic in 2020 is also noticeable.

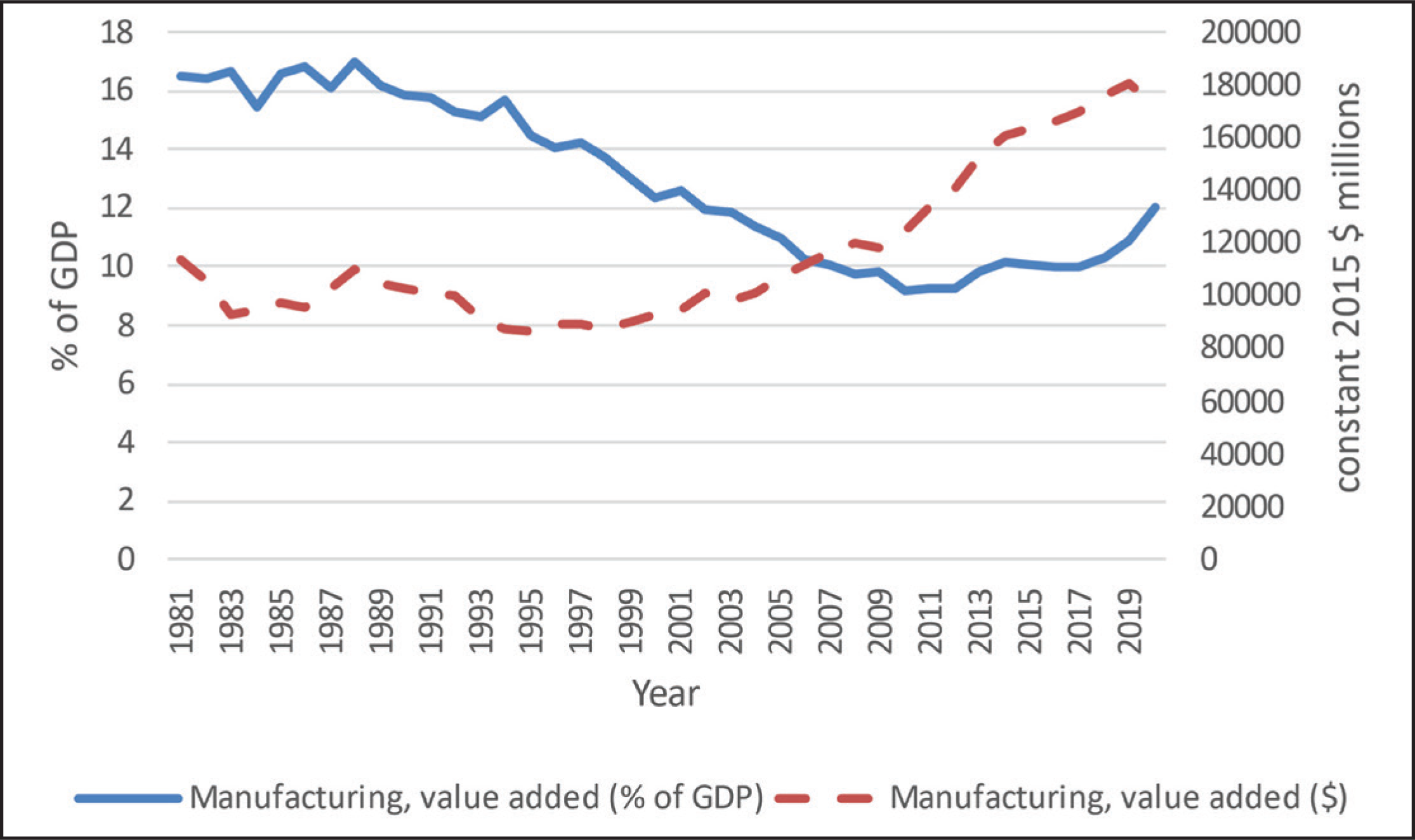

Much of SSA production remains centered in agriculture, and manufacturing’s overall regional contribution to the GDP has dipped in recent years (see Figure 2). It is still at a level far below the regions in Asia. Yet, we can also see the rapid increase in absolute volumes of manufacturing activity, principally since the 2000s. Manufacturing in this region tends to be concentrated in a few of the largest economies, such as Nigeria, Ethiopia, Kenya, and South Africa.

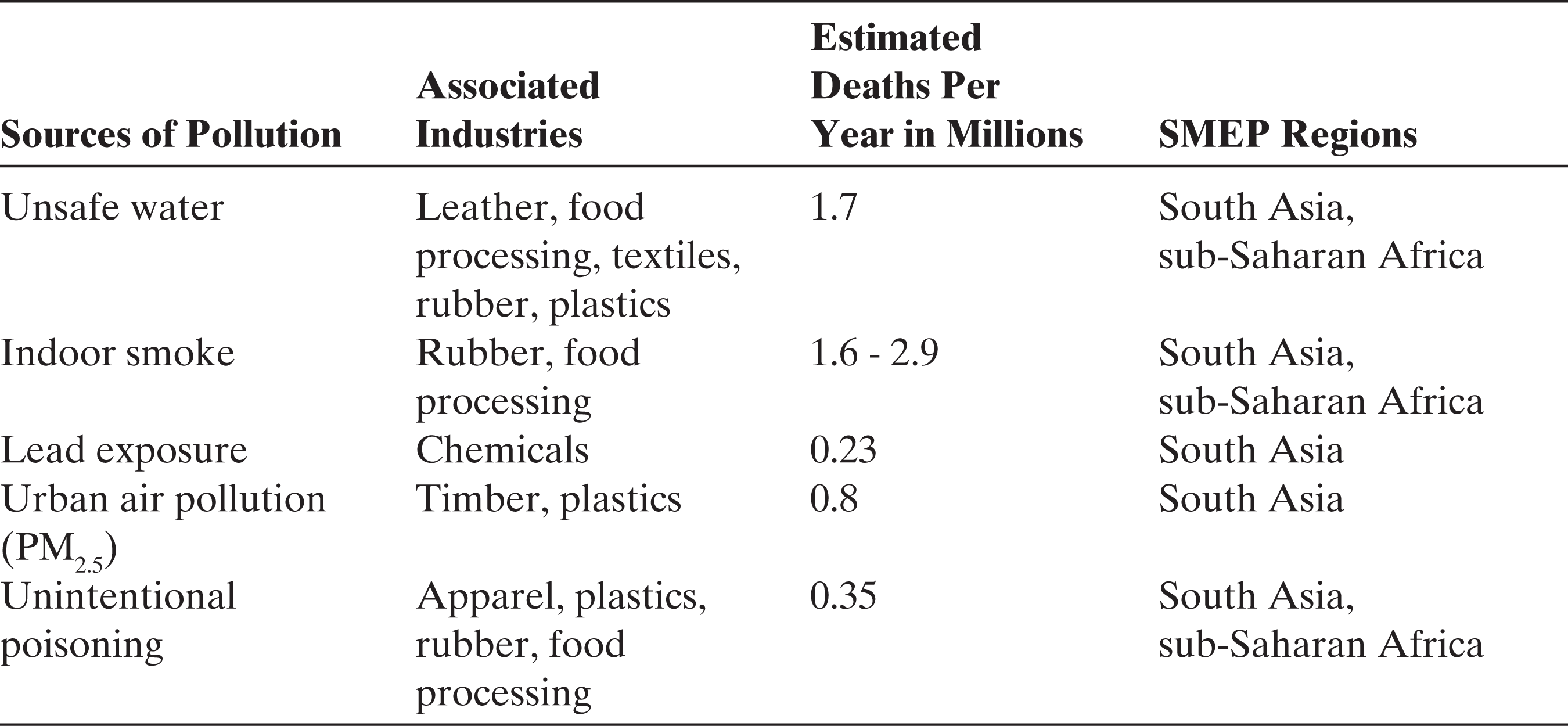

With this growth has come health concerns. According to the United Nations Environment Programme (UNEP, 2021), annual global health costs in 2016 in terms of mortality and morbidity caused by exposure to air pollution (measured in PM2.5) were approximately equivalent to 7.3% and 3.0% of the GDP in SA and SSA, respectively. Table 1 shows the relationship between the SMEP (2018) regions and global estimated deaths per year for the leading sources of manufacturing pollution:

Estimated Deaths from Leading Manufacturing Industries

Rapid increases in manufacturing have raised the accompanying effects of waste and pollution. While it’s impossible to separate the individual causes of pollution, there is no doubt that manufacturing causes increased health burdens in the Global South (Soledayo Babatola, 2018). In Africa, for example, air pollution was responsible for 1.1 million deaths in 2019, with ambient air pollution deaths rising from 361,000 in 2015 to 383,000 in 2019. In fact, in 2019, ambient air pollution was responsible for 9.3% of all deaths on the continent (Fisher et al., 2021). SSA has some of the highest concentrations of ambient air pollution globally, following the Middle East (HEI, 2018).

And Asia is the fastest-growing region for industrial emissions. China’s rapid transformation into an industrial powerhouse leads the way. However, other parts of Asia are also industrializing rapidly. In India, for example, Jain (2017, pp. 113–118) points out that manufacturing output increased by 12% and pollution load by 24% from 2004–2010. This is up considerably from the preceding period of 1990 to 1998, when the figures were 7% and 8% respectively. The top polluting industries have remained relatively stable, with cement, metals, and vegetable and animal oils and fats topping the list.

There are increasing concerns about environmental issues and natural resource depletion in SA. This region of 1.9 billion people, or 23% of the world’s population, is rapidly urbanizing. While economic growth has reduced poverty in the region, from 50% in 1999 to 33% in 2010, there are increasing signs of environmental stress. Estimates of the costs of pollution are 10% of GDP in 2016. Air pollution is responsible for an estimated 13%–22% of deaths in the region. There are growing problems with municipal solid waste, of which there were an estimated 334 million tons in 2016. Yet only 50% of waste is collected, and open dumping or informal collection remains the norm (South Asia Co-operative Environment Programme [SACEP], 2019; The Energy and Resources Institute [TERI], 2019).

More optimistic discussions in previous decades expected a gradual shift in environmental values, an “Environmental Kuznets Curve” (EKC) over time as countries industrialized, which assumed increased incomes would result in a gradual shift towards greater environmental values. The expectation was that pollution would increase for a few decades and then decline as countries reached a certain income threshold and started developing post-industrial service-based industries. This EKC theory has been highly contested (Arpegis & Ozturk, 2015; Churchill et al., 2018; Özokcu & Özdemir, 2017). Industrialization has not yet peaked in most of the Global South, and we cannot yet see if pollution will decline with any certainty. This uncertainty feeds the fear there will be growing global environmental crises, especially climate change. The urgency about climate change and increasing awareness of the health costs of pollution felt locally in the Global South have pushed policymakers towards considering how to develop more green and circular forms of manufacturing.

Impeding the development of manufacturing is untenable, given the need for economic growth to reduce poverty and provide the kind of incomes and employment needed to raise living standards. More importantly, there does not appear to be a clear trade-off between environmental quality and economic development. For example, the Liu et al. (2018) modeling of Chinese manufacturing finds no apparent adverse effects on employment for firms adopting environmental pollution reduction and/or control measures. They suggest pollution control may add substitute jobs for those that are reduced by environmental protection. However, the effects are heterogenous in terms of the industry, region, and form of ownership.

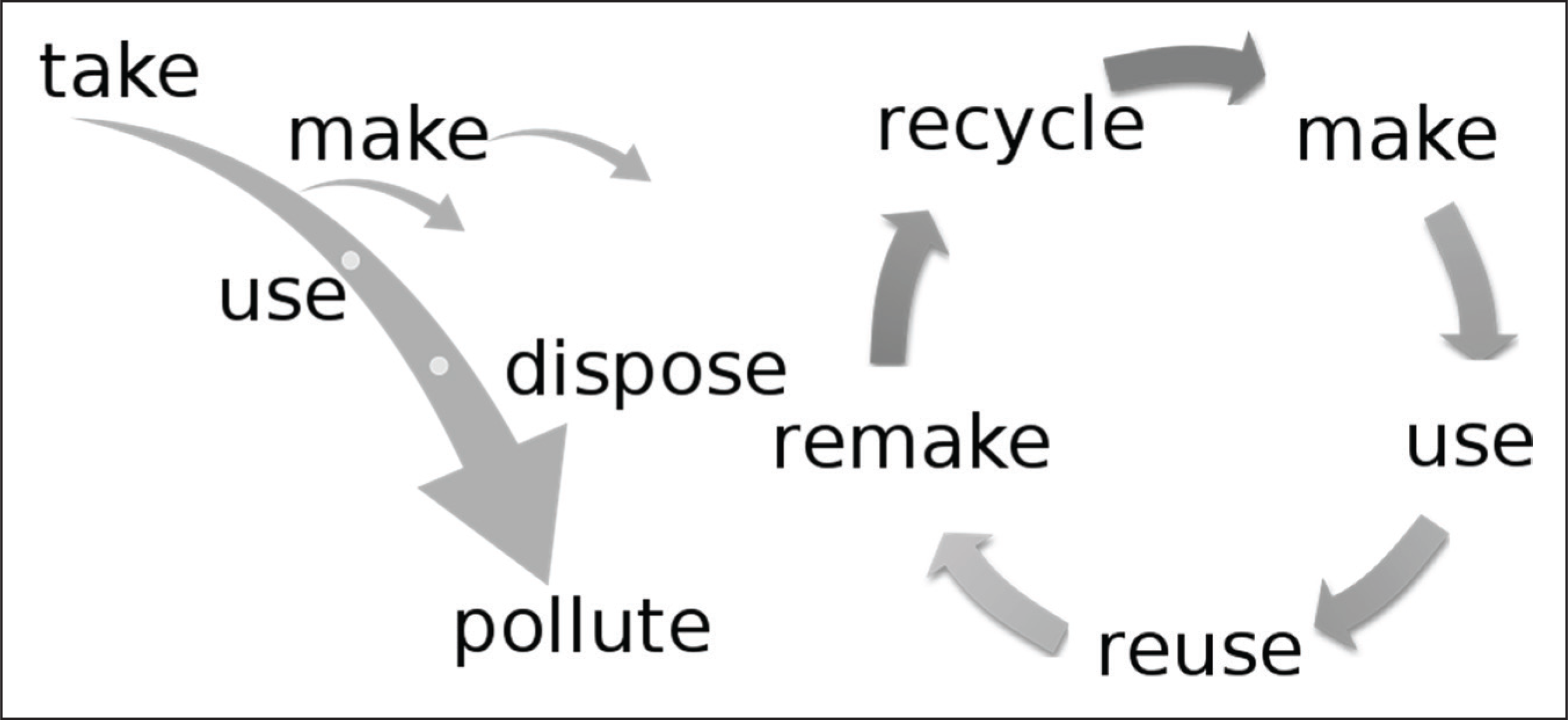

As discussed in the first article in this special issue, the entire production process needs to be transformed from a linear to a circular or closed-loop approach (Blanco & Cottrill, 2014). Geissdoerfer et al. (2017) define a circular economy (CE) as “a regenerative system in which resource input and waste emission and energy leakage are minimized by slowing, closing and narrowing material and energy loops.” Figure 3 is a simple diagram that contrasts the ‘take, make, use, dispose, pollute’ linear approach with the ‘make, use, reuse, remake. recycle’ CE approach, which is still a contested concept.

Multiple Pathways Towards Circularity in Manufacturing

According to the United Nations Intergovernmental Panel on Climate Change (IPCC), industrial processes offer multiple pathways for reducing emissions, including the following: energy efficiency; production process efficiency; product/process redesign; collaboration with other sectors such as sharing resources, including heating and cooling; and developing new supply chains for reuse and recycling (see Fischedick et al., 2014, pp. 743–744). However, each pathway presents its own adoption obstacles.

Energy is one of the most significant inputs for manufacturing and offers the most immediate saving opportunities. According to the IPCC (2014, pp. 747, 753), cement, iron ore, ammonia, aluminum, and paper are the most important industrial products, and their production requires copious amounts of energy. The production of electricity and heat are the most significant contributors to emissions. The shift to renewable energy requires large capital investments and technology transfers. Beyond that, intermittency and lack of electricity grid infrastructure are also major obstacles.

Co-location offers advantages for pollution reduction. Excess heat or wastewater can be shared multiple times across co-located industries. Because of economies of scale, manufacturing tends to be concentrated, and changing the processes of one factory can be a lot easier than changing the habits of thousands of consumers. The centralized location of industrial processes also opens the way for shared waste facilities, permitting greater reuse and avoiding redundancies, such as multiple wastewater treatment facilities. For this reason, co-locating industries in industrial parks appears to be one important way to increase cooperation and sharing.

A recent World Bank (2021) report provides an overview of eco-industrial parks (EIPs), which offer a ready mechanism for increasing energy efficiency. This report notes the benefits of co-location, whereby waste products, energy, heat, and water can be shared among different industries in these parks. Similarly, renewable energy generation and waste treatment costs can be shared in these parks. Because of these benefits and growing knowledge about them, EIPs grew from less than 100 in 1990 to 438 in 2020. The implementation of these parks requires careful planning and coordination, as the concentration of industries can also strain local resources. East Asia and the Pacific boast the largest number of EIPs, with 220, followed by Europe and Central Asia with 147. SA has just 11, and SSA with only 4.

Public sector engagement appears central, with 67% of all EIPs being owned and managed by the public sector and 10% through public-private partnerships. The public sector operator helps plan and coordinate centralized services for the parks, including maintaining a data system to optimize resource-use and pollution control systems. It can invest in shared infrastructure such as solar energy farms, rainwater collection systems, waste heat recirculation, and anaerobic digesters for waste gasification. For this infrastructure, a financial plan for investing in and operating each EIP is needed. EIPs can help promote the adoption of new technologies and enforce standards more effectively.

A recent report by the United Nations Industrial Development Organization (UNIDO, 2017) notes there is growing interest in EIPs in the Global South. UNIDO has helped to set up pilot EIPs in India, Tunisia, South Africa, China, Viet Nam, Morocco, Peru, and Colombia. The report notes the importance of having a local independent lead organization, such as a university, to improve the support for such projects and the importance of a robust data system to show “quick wins” to consolidate support among key government ministries. There are fewer EIPs in the Global South than in the Global North because of a lack of access to finance, weak regulatory and policy capacity, and less infrastructure investment.

Creating a solid governance model around the management of these parks is crucial for ensuring smooth operations and regulatory compliance. At the same time, there need to be adequate business incentives for park viability. Thus, the initial scoping process should deeply consider whether there is a business case for an EIP, including the availability of technology and transportation. The park’s actual location is crucial for all the factors noted earlier, to increase synergies with local waste production, and to ensure local support.

Repair, reuse, and by-product use are possibilities. Along with improving the effectiveness of waste disposal, they fall broadly under the umbrella term of “reverse logistics,” or how to manage the entire waste supply chain. For example, scrap metal or plastic can be reused to develop the same or new products. “Upcycling” refers to using scrap materials to create new products of higher value-added. Remanufacturing is a term that refers to restoring used products. During World War II, these processes were common due to limited input availability (Rochester Institute of Technology, 2020). Remanufacturing requires a separate set of processes, including disassembling, cleaning, inspection, sorting, refurbishing, and reassembly (Lieder & Rashid, 2016). In general, actual examples of such circular supply chains are now rare. Customers prefer new products, and virgin input materials are often cheaper than refurbishing old ones. Disassembly of materials can also be a hazardous and labor-intensive process.

Collection of used materials for reassembly can be costly and challenging; by contrast, recycling is cheaper, though it creates more waste (Gungor & Gupta, 1999; Steeneck & Sarin, 2017). Moreover, it is not easy to develop solid and reliable remanufacturing/reuse systems since not all used materials will be in the same condition. So remanufacturing will likely contain a mix of new and used materials. In many consumer-product lines, innovation continues, and this inhibits remanufacturing or refurbishment. In general, there is a lack of understanding about how to construct or manage remanufacturing supply chains.

Product and process redesign offers opportunities for improving both material and energy efficiency in manufacturing. Product design can also help facilitate and significantly reduce the costs of recycling and remanufacturing. For example, Ford’s European Mondeo model is supposedly 85% recyclable. BMW offers US customers a $500 credit if they turn in their old vehicle to a dismantling center (Gungor & Gupta, 1999). Redesign in the future could use more biodegradable materials and less packaging. However, product design and innovation capacities can be quite limited in the Global South, impeding this pathway.

Managerial processes can also significantly accelerate the shift towards circularity. There is a gradual shift among northern firms to develop deeper relationships with input suppliers and customers to reduce emissions and waste. The term “pull production” refers to downstream customers signaling their needs, leading to adaptation by upstream suppliers. Such efforts are more generally termed “environmental collaboration.” This requires regular and close contacts among key managers in each firm. The results can be significant. For example, Vachon and Klassen (2008) cite a commercial printer that reduced the number of chemicals in its printing stock from 80 to 24 through collaborative efforts with its suppliers. Still, the authors also point out that such measures are not comprehensive regarding pollution, as they do not include effects on the natural environment and tend, understandably, to be limited to processes that improve profits. More fundamentally, this paradigm hides a critical tension between the resource-based view (Teece, 1980) of competitive firm advantage, which posits that this lies in specific and non-transferrable assets at the firm level, and this requires a more collaborative view of supply chains. The tension will always exist concerning the former because almost every firm/customer has an incentive to have multiple suppliers compete for their business.

A related pathway is “lean” or “smart” manufacturing. Based on Japanese production techniques developed after World War II, the lean movement seeks to eliminate waste caused by excess use of materials, capacity, or inventory. This pathway is accomplished by assiduously and continually improving the manufacturing process to improve efficiency and quality, particularly to reduce the number of defective products. An essential part of the management process is to include discussion with shopfloor workers and take statistical samples of products based on process alterations and to break the process down into small parts. However, lean processes also constrain the flexibility of the production process (Hines et al., 2004).

For example, if inputs are unavailable or a sudden increase in demand arises, the manufacturing line will be slow to respond. A related proposal involves a new approach called “agile manufacturing,” which suggests creating a more flexible and rapid-fire response to changes in the environment, customer needs and technology. The increasing digital tools for increasing flexibility in supply chains are related to “smart” customized production, but this requires more profoundly re-orienting companies towards rapid response. The movement towards lean manufacturing requires excellent infrastructure, a comprehensive data inventory and sales system, supply chain communication, and coordination, which present considerable obstacles in the Global South (Gunasekaran, 1998).

Any movement towards circularity involves policy and regulatory reform and stakeholder coordination. In addition, technology transfer and development, even in the absence of cost pressures, is vital to improving the efficiency of manufacturing processes. Changing business processes and regulations around manufacturing offers the possibility to internalize external costs, for example, through a carbon tax, that levels the playing field for all firms involved in a particular industry. For example, offering more sustainable sources of inputs, such as the possibility to use scrap instead of forging new metal, can create CE synergies that lead to new supply chains—in this case, metal recyclers.

Additional Challenges for Manufacturing Transitions in the Global South

The limited literature around manufacturing transitions in the Global South suggests a standard set of factors that inhibit the transition to circularity. However, our understanding of causal pathways that might lead to pragmatic recommendations remains murky. The general categories can be summarized as weak market forces; weak regulations; lack of knowledge and access to technology at the state, managerial, and consumer levels; the need for financial and tax/subsidies given the lack of market incentives; the catalyzing role that export markets can play (UNCTAD, 2021c); and the need for stakeholder coordination to move along regulatory reform.

One part of the literature focuses on market forces, such as lack of competition in supply chains and markets more generally in the Global South. For example, Barrows and Olivier’s (2018) study of product mixes among Indian manufacturing firms finds that more competitive markets lead to lower pollution intensity. A larger amount of sales and a narrow mix of products are also correlated with lower pollution.

Related to market forces are weak and poorly enforced regulations. Esfahbodi et al. (2016) surveyed 128 manufacturing firms’ supply chains in China and Iran. They trace sustainable initiatives primarily to regulatory and customer pressure. They find that adopting sustainable supply chain practices leads to better environmental performance but “does not necessarily lead to improved cost performance.” “Firms need to undertake SSCM (sustainable supply chain management) practices in a bearable and equitable sense that do not harm their financial bottom line.”

Sahu and Narayan’s (2016) econometric study of Indian manufacturing firms highlights the importance of R&D activities in explaining the difference between firms who adopt green standards from those who do not. This jives with the general literature on environmental activities by companies that around internal capabilities for knowledge and technology acquisition. The literature also highlights challenges of lack of access to knowledge, technology, and managerial strategies. This lack extends to inadequate training systems for producing highly qualified manufacturing and knowledgeable consumer about the price of pollution.

Even where environmental awareness and motivations exist, a lack of access to financial resources inhibits action, especially important since the literature is ambiguous about whether there are market incentives for the green transition. For example, Kusi-Sarpong et al.’s (2018) study of five different Indian manufacturing firms emphasizes finance, followed by technical expertise and capabilities as the main factor inhibiting sustainable supply chain transition. Yuan and Xiang’s (2018) study of Chinese manufacturing firms using data from 2003–2014 similarly finds that environmental investment tends to “crowd out” investment in R&D, though it can improve energy efficiency. This information contradicts the famous Porter and van der Linde (1995) hypothesis that innovation and green investment go hand-in-hand, and it suggests the need for promotional industrial policies, such as regulation, taxes, and subsidies, to promote the green transition of supply chains.

By contrast, Afum et al. (2020) find a positive relationship between green practices and profits in Ghana. Kamand and Lokina’s 2013 study of Kenyan manufacturing firms also finds a correlation between profitability and environmental practices. However, Namagembe et al. (2019) study of small- and medium-sized manufacturing enterprises in Uganda, where higher environmental practices are correlated with higher costs, highlight the importance of internal management practices. These authors cite the positive influence of Ugandan environmental regulations and the United Nations’ sponsored National Cleaner Production Centres to help reduce costs. There is an overall potential for a virtuous circle, whereby better environmental practices lead to healthier workers and clients and to preserving the natural environment as a continuing source of inputs and natural waste processing.

Arguably, the most important transformation pressures come from overseas buyers’ demands, linked to Global Southern exports. The principal impetus for these comes from the European Union’s (EU) sustainability standards for imports. The EU has proposed a Carbon Border Adjustment Mechanism (CBAM) that would add tariffs to imports based on their production emissions. The proposed CBAM would exclude the “least developed” countries and allow duty-free imports from lower-middle-income countries up to a proposed threshold. The CBAM’s focus is matched by standards for environmental sustainability in imports, such as food and minerals (Lowe, 2021; UNCTAD, 2021a Usman et al., 2021). Similarly, the EU’s Sustainable Products Initiative strives to address the presence of harmful chemicals in textiles, electronics, and chemical products and regulations on illegal, unreported, and unregulated products (European Commission, 2021).

Such instruments have limited effectiveness in the absence of local parallels and substantial support. Barash-Harman (2018) studies five Indian firms in textiles, petrol, and pharmaceuticals and finds that those oriented towards product differentiation and exports were significantly more likely to comply with environmental regulations. He finds that such regulations tend not to be enforced, and customers do not demand green performance locally, leaving the main pressure to the purchasing MNCs.

There is likewise a growing panoply of voluntary standard-setting by industry associations and private firms. These emerging global standards include promises to abide by environmental and labor sustainability principles regardless of where production occurs (UNCTAD, 2021b). Prominent examples include the Forest Stewardship Council and the Roundtable on Sustainable Palm Oil and “socially responsible investment”. So far, the results of such voluntary efforts have had limited to no effect (Hira, forthcoming, 2020). Even if well-meaning, both public and private standards for sustainability will cause significant strain on exporters, especially small and medium enterprises in the Global South (Higgins & Richards, 2019; Plassmann, 2018).

Environmental regulators in the Global South generally lack the resources or ability to enforce provisions where they exist, reflecting more general challenges of stakeholder coordination that would enable regulatory reform. Regulations are vital to igniting secondary markets. For example, mandatory eco-labeling could help to inform consumers. Public procurement could also be an important lever for the green transition. Adeoti’s (2002) examination of Nigerian manufacturers offer some positive reflections on the ongoing evolution of Nigerian firms towards more environmental-friendly technology, particularly in end-of-pipe wastewater treatment, and in the development of labs for regulators to conduct water testing. He posits that environmental policy is the main driver for change. However, there is a shortage of qualified personnel in regulatory agencies. While obstacles vary by sector and firm, he finds that lack of knowledge is generally not as significant as access to capital. Jakhar et al. (2020, p. 2649) are quite skeptical of the potential for environmental regulations to be effective in India, in contrast to China, stating, “In the Indian context, the regulatory pressures can easily be overcome using symbolic gestures or superficial efforts without entailing many costs.” Likewise, according to the UNEP, most SSA countries do not have legal instruments containing ambient air quality standards (UNEP, 2021). These institutional challenges in Africa also extend to the limited availability of national ambient air quality monitoring networks (UNEP, 2021).

Unlike China, most manufacturers in SA and SSA are small- to medium-sized enterprises (SMEs) with limited capacity to export, with some notable exceptions in India. In Ghana, for example, the estimate is that 85% of the manufacturing is SME. Beyond the lack of access to credit (similar to China), they also suffer from low capacity in R&D, and limited managerial and technical skills that prevent them from taking advantage of global markets (Asare, 2014). As Mathiyazhagan et al. (2013) point out in their study of the Indian auto industry, the SMEs that dominate most manufacturing in the Global South face additional hurdles to achieve green or circular supply chains. These include a lack of awareness by suppliers and customers, challenges in measuring environmental performance, lack of government support, inability to take risks because of tight margins, lack of human resources and technical or managerial expertise, failure to engage in the complex redesign and general lack of access to technology, disbelief that it is their responsibility, financial access constraints, high costs, and lack of options for safer waste disposal. One can even go even further in highlighting the importance of natural resource-based industries in the Global South, which bring vital revenues and create powerful lobbies of resistance to change but limit the ability to scale up the value chain.

Lessons for Improving Manufacturing Circularity from the SMEP

The SMEP highlights the growing importance of interventions to reduce manufacturing pollution in the Global South and adds important new insights into the challenges. While the key factors presented in the literature around production and process redesign, access to finance, technology, managerial techniques, and weak regulation are echoed in the project documents (SMEP, 2021), 3 new factors are also brought to light through the projects. These include a lack of awareness of pollution costs, the challenges presented by large informal and fragmented industrial sectors, and the daunting obstacles of creating stakeholder coordination around a new regulatory framework and sustainable business models. The SMEP indicates that challenges tend to be sector-and even-product-specific, thus reinforcing the need for animating local actors to understand the local context to drive the transition process. The reports also offer concrete suggestions. These include reducing upstream causes of industrial pollution, creating centralized waste infrastructure, and spurring stakeholder collaboration around regulatory reform.

SMEP (2020) commissioned a baseline study to examine the levels of manufacturing pollution in exports from SA and SSA as a first step to the SMEP. The report conducts an environmentally extended input-output analysis (EEIOA) and a lifecycle analysis (LCA) to measure the pollution results of key industries in the regions. The study notes that the countries of interest across the two regions (excluding India and South Africa) together account for just 0.9% of global trade. The levels of trade openness vary considerably by country, from 28%–70%. The SSA countries rely heavily on commodity trade, while the SA countries produce more labor-intensive exports. The report notes that each country suffers from multiple factors that impede the development of higher value-added production, particularly capital formation. At the same time, manufacturing exports have been increasing over time, from $26 billion in 2001 to $108 billion. In 2019 for SSA, and from $6.5 billion to $48 billion in SA over the same period (UNCTAD, 2021c, p. 10). With this massive increase comes more pollution.

Beyond carbon emissions is a host of other issues from toxicity for humans and ecosystems on land and sea to the acidification of lands and to water contamination. SMEP estimates the costs of yearly pollution for the studied countries as $12.1 billion for the SA cases and $6.8 billion for the SSA countries (SMEP, 2018, p. 25). The report (2020) more explicitly identifies points of concern with manufacturing pollution pathways, namely, toxic metals, dyes, bleaching agents, air pollutants, pharmaceuticals, and noise. Its recommendations are sector-specific, beyond energy efficiency, and the categories of recommendation overlap sectors, particularly from toxic waste sites. Identified health effects include inflammation and cardiovascular effects, respiratory issues, carcinogenic disease; neurotoxic effects; and antimicrobial resistance. Because of the challenges and costs of remediation, the report suggests that efforts reduce pollution at the source.

The UNCTAD (2021c) report for the SMEP further observes that the challenges and effects of manufacturing pollution tend to be sector specific. Many of the countries specialize in 1–2 industries, facilitating intervention. For example, Bangladesh and Pakistan are focused on textiles and apparel, while Kenya and Tanzania are both concentrated in food and beverage production. In the case of textiles and apparel, there is growing international pressure and accompanying initiatives to push production towards greater sustainability.

In Bangladesh, SMEP partners Pure Earth conducted a study of lead-acid battery (LAB) recycling that highlights the additional challenges of manufacturing transition in the Global South. This project highlights the importance of a lack of knowledge of pollution costs among supply chain actors and the general public. It also highlights the role of informality, a factor underestimated in the literature. LABs are increasingly used in transport, energy, and manufacturing. The market for LABs is estimated at $129 million and is growing at 12% per year in Bangladesh. Around 50 battery factories, 30 Chinese-owned, produce 500,000–600,000 units per year. This finding undermines the claim in the literature that foreign investment leads to improvements in sustainability; perhaps the conditions of foreign investment matter. A LAB lifespan is estimated at only two years, creating a major hazardous waste issue. Environment and Social Development Organization (ESDO, 2021) further notes no enforced regulations around child labor in the sector, which may affect children’s average lead concentration levels, estimated at eight micrograms per deciliter, while five is the generally accepted level for triggering a health warning. Bangladesh thus loses an estimated $15.9 billion in GDP from lead exposure. Dependence on batteries also reflects the lack of access to reliable grid-based energy. While there are other batteries, such as nickel-metal hydride, nickel-zinc, Sodium-Nickel, and Lithium-Ion, these are considerably more expensive than LABs.

Lead can act as a neurotoxin in the body, creating serious issues for children’s development, though knowledge of lead’s dangers appears limited in the country. However, most battery recycling efforts remain in the informal sector; there are an estimated 1,100 recycling sites, of which only six are in the formal sector. Thus, an estimated 80% of batteries are informally recycled. Yet, there are insufficient market incentives or enforced regulations to shift activity back to the formal sector; in fact, informal recyclers require little capital or equipment. The report recommends a deposit refund scheme and/or a green tax for batteries, a single environmental standard agreed upon by government and private sector stakeholders, the development of a battery swap system for e-rickshaws, and a new hydrometallurgical recycling process. The last would need to be developed first as a pilot project. Each of these solutions would require significant government and private sector consensus and foreign partner investment and technology transfer. The dominance of informality appears to make such tasks quite challenging, so the report also recommends a vigorous public health campaign (SMEP Pure Earth, 2021). Moreover, the government lacks the personnel capacity to develop a sound environmental management plan for the sector; this is reflected in the lack of effort to enforce licensing among existing recyclers (ESDO, 2021).

Most prominent among the findings is the need to rethink production processes in supply chains. SMEP’s (2020) general suggestions for intervention include materials substitution for less toxic inputs where possible; air and water effluent treatment; personal protective equipment; waste recycling and reuse; and generally improving training and production processes. The report also calls for improved pollution standards and more rigorous enforcement of existing ones. Therefore, a multi-stakeholder approach is needed to enlist and engage the private and public sectors and local communities affected by pollution.

Another commissioned report (PA Consulting, 2019) for SMEP signals additional intervention points. The first is to reduce the number of product lines produced as changing processes is wasteful. The second, they suggest, is “identifying manufacturing pinch points” by referring to bottlenecks that slow down manufacturing lines. The third is to reduce waste during the processes through improved quality control; this helps to reduce the number of sub-par or unacceptable batches. The fourth is to improve the technology available. More generally, they suggest looking at how goods are transported, reducing inventory over-stock, and enhancing personnel’s know-how. These intervention points should be overlaid with a robust data system and access to capital for upgrading.

The project reports note the importance of capital injections, technology, and managerial strategies to improve circularity and shift production processes. They also emphasize the need to bring together stakeholders to reform regulatory processes. For example, SMEP Open Capital (2021) examined pollution mitigation across Kenya and Uganda across 12 manufacturing sectors, focusing on the two most polluting: food and beverage; and textiles, clothing, and leather and footwear. The food and beverage sectors are the fastest growing in both countries, at an estimated annual rate of 10%. The project recommends a wide array of solutions falling into the general categories of waste collection and recycling, raw material substitution, energy efficiency—including switching to locally sourced biofuels—waste treatment, including anaerobic digesters—and pollution monitoring technologies.

A study of distilleries, tanneries, and textiles in Kenya, Ethiopia, and Tanzania (SMEP Teifa IQ, 2021) similarly highlights specific interventions to transform supply chains, particularly processing with environmental safeguards. Currently, water from various manufacturers in Kenya is primarily discharged without treatment into the Nairobi River and Lake Victoria. The distilleries study focused on solid and water waste treatment, including installing anaerobic digestion to produce biogas. (See the last article in this special issue for details on the tannery study.)

The textile sector in Tanzania is also a source of concern, despite its rapid growth to become the largest in East Africa. It emits sulfur dioxide, heavy metals, various chemicals, and organic waste. The industry also burns biomass. These pollutants can lead to various health issues, including respiratory and carcinogenic problems and the contamination of nearby water bodies. In this case, the project recommends finding substitute materials that would be less toxic, pollution abatement technologies, personal protection equipment, and introducing renewable materials. The study focused on the leather sector in Ethiopia because it is one of the fastest sources of exports, increasing from a value of $53 million in 1996 to $135 million in 2017.

Meanwhile, employment grew from 11,365 in 2012 to 21,094 in 2017, mostly in leather footwear, where 50% of the labor force are women. These are driven by foreign investment. Most of the environmental footprint is from upstream inputs of leather products, including the use of hexavalent chromium in the tanning process. Workers in surrounding areas often have more respiratory problems than others; however, solid waste is also a concern. There is also the possibility for by-product production, creating glue or biogas from wet fleshing residues. The report recommends developing a new environmental plan to manage tanneries, including improved effluent treatment and better disposal of solid wastes, including anaerobic digestion.

One place where SMEP findings differ from expectations in the literature is that increases in exports have not, for the most part, led to a natural improvement in environmental technologies. However, growing sustainability requirements in import markets such as the EU and pressure on multinational enterprises (MNEs) are and could increasingly catalyze the transformation of manufacturing. Absent sustainability transition, they could otherwise find themselves shut out of important revenue and employment-generating activities.

For example, the textile industry in SA is a focal point for Western activist pressures on large MNE clothing buyers that have changed supply chain consideration, such as the Better Cotton Initiative. The good news is that SMEP reports suggest very feasible ready alternatives, some relatively low-cost, and almost all involve already proven technologies that could be introduced to lead to significant improvements. Organic waste seems to be open to accessible solutions. To introduce such interventions would require a concerted effort by global and local stakeholders, including efforts at regulatory and policy capacity.

UNCTAD’s summary report (2021c) emphasizes that transformations in supply chains, managerial practices, and financial and technology transfer require business processes and regulatory reform to work hand-in-hand. It suggests that countries in both regions study how to strengthen their environmental disclosure, transparency, and public participation on the domestic level and consider policy coordination, including through multilateral environmental agreements, on the regional level. They also recommend considering green manufacturing guidelines, the development of EIPs, and a national industrial symbiosis program that would enhance capacity building, regulation, and sustainable management practices. The report recommends developing local environmental management system (EMS) certification and adopting resource-efficient and cleaner production (RECP) measures. In general, they suggest creating more training opportunities for CE concepts and identifying transition opportunities. The significant size of the informal sector means any efforts have to be widely available. Last but not least, campaigns to raise awareness across society of the costs and solutions for environmental degradation are vital. In line with this, a more rigorous monitoring system Is required.

Conclusion

The SMEP projects support the existing literature’s identification of the key barriers to circularity, including insufficient finance, knowledge, technology, and management capacity in the public and private sectors, They also have revealed the additional challenges of knowledge and metric deficits, informality, lack of infrastructure, insufficient regulatory and private sector capacity, and deficient supply chain and stakeholder coordination in response to exporting requirements.

Fortunately, in many countries of the Global South, manufacturing tends to be primarily geographically concentrated, which facilitates coordinated interventions. In Tanzania, for example, 80% of all industrial pollution is concentrated around the city of Dar es Salaam (World Bank, 2019, p. 84). In this case, industrial pollution and urban resident pollution, such as e-waste and solid waste, can be tackled together. Similarly, energy and water systems can be redesigned to serve both industry and local residents.

There is a vast opportunity for learning across the globe as various policy and private sector experiments to shift towards circularity get under way. For example, while being cognizant of important contextual differences, the needs for tanneries, as we see from SMEP, are similar in Bangladesh and Ethiopia. Thus, solutions pursued on a regional or global level will accelerate the process. Another example is integrating renewable energy systems can enhance demand-side management and improve the diversity and resiliency of energy sources.

Regarding increasing Western trade requirements for sustainable production processes, the desire for transformation can only occur if the West pro-actively assists the Global South by sharing knowledge and promoting harmonized labeling. In sum, the sharing of knowledge, and regulation and policy-building as well as financial and technology transfer need to occur on the global level.

Transforming industrial processes in the Global South into greener alternatives allows us to reduce pollution without harming reducing poverty. These efforts can be seen as “win-win” in more direct terms as reductions in emissions in the Global South can be counted as “offsets” for northern partners in some cases through the Clean Development Mechanism and other arrangements, particularly the significant commitments made by Western countries to the Global South as part of the Paris Agreement on climate change. In the end, pollution affects everyone, so its dissipation in manufacturing is a global public good.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The development of this article was made possible with partial funding from UK-Aid as part of the SMEP programme.