Abstract

Private equity firms and institutional stakeholders increased their investments in television production amid the streaming boom of the late 2010s and early 2020s. Taking advantage of new regulations and demand from streaming services for localized production in Europe, U.S.-based private equity firms started purchasing local film and television production companies and concentrating power in regional production conglomerates. A simple “follow the money” approach to this phenomenon might over-assign ownership and thereby operational control to these financial stakeholders. However, a more holistic approach to following the money, which offers a plastic and relational ecology with different axes of power between different stakeholders for a given television production, complicates our understanding of private equity in transnational television. This article examines the transnational financial ecology of one of these private equity firms’ regional production conglomerates (KKR’s Leonine Studios) and the capital threads connected to one of its programs (Pagan Peak). Relying on publicly available industry deep texts and background interviews with television professionals, this case study presents the paradoxical opportunities that private equity capital specifically and television investment generally offer at the same time that they can exploit, concentrate, and extract.

Keywords

Introduction

In the premiere episode of the German-language television program Pagan Peak (Sky, 2019–2023), a body is found in a snowy mountain pass that separates Germany from its southern neighbor Austria. The lead German detective on the scene, Ellie Stocker, debriefs her late-arriving Austrian counterpart, Detective Gedeon Winter, about the condition of the body. She explains that the victim was found “laid across a border stone. . . . To be precise, his upper body in Austria, legs in Germany.” In addition to a provocative introduction to this noir, the prologue provides a neat allegory for the program’s financing: the “equal” business partnership between its two regional producers, epo-film of Austria and Wiedemann & Berg (W&B) of Germany. Press articles on the series would go out of their way to connect the show’s border setting to the cross-national partnership between Austrian and German production companies. These narrative and paratextual articulations together perform a sort of regional, cross-national collaboration that ties the shared authorship of this text to two nations’ media industries. Belying this celebratory tone is the show’s underlying ownership: when one “follows the money” back to the corporate owner behind this program, one discovers that this local production was actually connected to a powerful Wall Street private equity firm, Kohlberg Kravis Roberts & Co. (KKR), which owned the parent company, Leonine, of Pagan Peak’s lead producer, W&B. Critically, KKR is a leading leveraged buyout firm, long known for exploitative and extractive practices.

This method, however, plays into a common industry lore: that following the money trail behind a media project will eventually lead to some secret controlling organization that dominates our culture. A more material and cultural analysis of even just this television program reveals how media financing and financial power are much more economically, geographically, and discursively diffuse. If one were to instead follow the money in a more holistic fashion—folding in a myriad of stakeholders across financing (private and public), development, production, distribution, and consumption—it would be possible to construct a fuller ecology of the key stakeholders involved in global television.

Pagan Peak represents a compelling case study to develop this theory of transnational financing because, first, it represents a highly visible and overt example of a cross-national co-production. Second, the show’s primary production company was connected to one of the largest private equity firms in the world, KKR, thereby offering an important case study on a recent industry trend: U.S. private equity firms acquiring local production companies and forming regional television conglomerates. Third, in researching Pagan Peak through a “follow the money” methodology, one is forced to reckon with other threads of capital that traveled in directions too diffuse to contain the show’s “control” to just KKR, even while private equity and financial capital played a key role. Tying the “money” in this sense to any one institution or political actor misses the plasticity of contemporary capitalism. As the cynical Detective Winter caustically jokes in Pagan Peak in response to the positioning of the body and jurisdictional oversight of the investigation, “Well, we should deal with this the German way: one gets the head, and one gets the ass.” Just as splitting a body for a police investigation is improbable, assigning financial ownership to two or three stakeholders is an equally fraught endeavor.

Building upon work in critical political economy and media industry studies, this article finds that the financing and ownership of cultural production, particularly in transnational contexts, needs to be understood as a material, symbolic, diffuse, and relational process. In the first section of this article, I offer a method that re-gears “follow the money” methodologies to understand the financing, production, and circulation of Pagan Peak. The core case study then examines the first-order stakeholders financially connected to Pagan Peak and follows the capital tendrils connected to this cultural object.

This article offers two key findings using this case study. First, financial exchanges often involve non-financial stakeholders and non-financial forms of capital (Bourdieu, 2013). This requires moving beyond purely market analysis to wrangle non-financial sources and documents, including trade press (Corrigan, 2018), statements of industrial self-disclosure (Caldwell, 2008), social media, piracy websites, and even the text of the show itself. These findings are also informed by background interviews with television producers, distributors, and financiers in the U.S. and Europe who offer ambivalent feelings about private equity. Second, I find that the contemporary state of financialization and globalization has not necessarily led to more domination or more freedom for particular groups in the film and television industries. Instead, they have generated complex topographies of power that depend upon varying dialectics of opportunity and constraint at distinctive temporal and geographic conjunctures (Curtin, 2020). For regional players, private equity has represented an opportunity to compete against global streaming services at the same time that it has concentrated the sector.

Financial ecologies

Television financing can be understood from both spatial and temporal dimensions as an “ecology” of interconnected actors and objects. This ecology is increasingly shaped by “financialization”: the omnipresence of financial institutions, instruments, and logics in all aspects of the economy and culture in the 21st century (Epstein, 2005). Pike and Pollard (2009: 31) argue that “financialization is broadening and deepening the array of agents, relations, and sites that require consideration in economic geography and is generating tensions between territorial and relational spatialities of geographic differentiation.” With an ecological approach, it becomes clearer how financialization can be an ambivalent process and can relate to different actors and objects in different ways at different times and places.

Methodologically, this article combines a “financial ecology” framework with Lash and Lury’s (2007) “follow the object” method. Building upon Appadurai (1986), Lash and Lury outline a framework that follows cultural objects in a manner that decenters human agency and “supply chain” linearity. As objects move, they take on new meanings and become intertwined with other concepts and phenomena; thus, meaning is contextual and internal to a given object. This case study therefore centers the agency and movement of a particular object—in this case, money—so the role of media practitioners is only ever considered relative to the object. Just as “following the object” can trace a commodity’s journey of global circulation, the “follow the money” method that is utilized in critical geography (Christophers, 2011) can build “a picture of all the money flows in the chosen case study” (Hughes-McLure, 2022: 1306). These flows “unfold across space and evolve in relation to geographical difference” (French et al., 2011: 812). The terms of “geographical difference” are subject to the “changing nature of states and capitalism” (Ong, 1999: 4) and the “shifting scales of opportunity and constraint” (Curtin, 2020: 99).

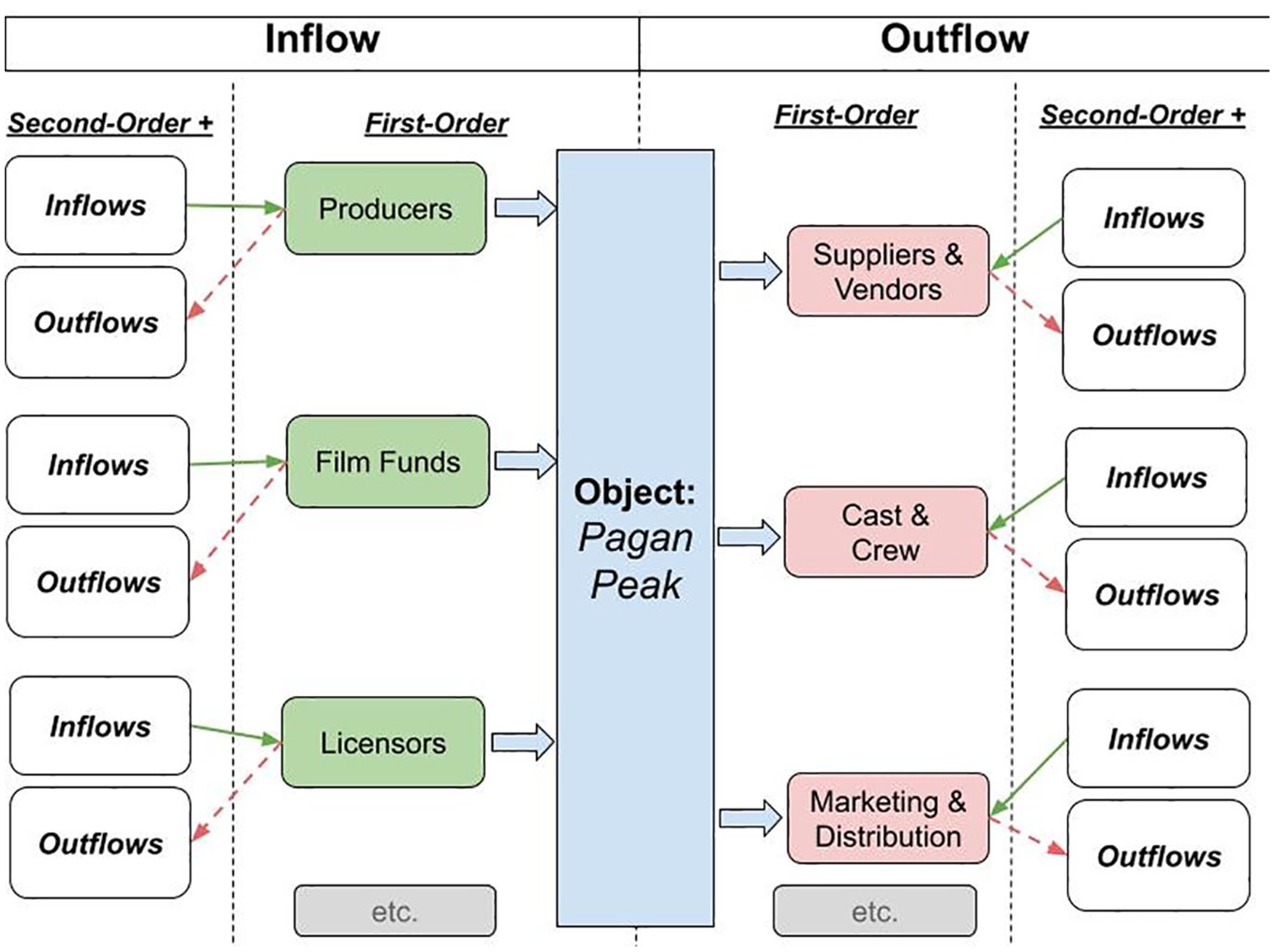

This article offers a simple application of this method. First, it begins with “the object”—here, the German television series Der Pass (German title) / Pagan Peak (English title). It then follows the lines of capital that flow “to” and “from” the object. For clarity, I distinguish first-order relationships from second-order and higher-order relationships relative to the focal object. For example, a vendor that provided lighting for Pagan Peak is a first-order relation, while a financier of that lighting vendor would be (relative to the focal object) second order. Per Figure 1, I start with the exchanges closest to the series, follow each of those “first-order” nodes to “second-order” nodes that emanate from there, and then move to higher-order stages. Christophers (2011) notes that any “follow the money” study needs to decide where to start and where to stop, as money has neither an “origin” nor an “endpoint.” Methodological constraints provide the necessary starting and stopping points. I follow the capital threads “forward” and “backward” until there is no more public information available.

Follow the money methodology in media industries.

Follow the money: Pagan Peak

The “object” of this study—Pagan Peak—is a crime thriller about a cross-border police investigation into a series of mysterious murders that include quasi-pagan rituals. The writers of the series were inspired by the style, motifs, and narrative of the Danish-Swedish co-production The Bridge (2011–2018), which similarly began with a body found precisely along a national border (on a bridge connecting Sweden and Denmark). Pagan Peak is just one of many adaptations and remixes of The Bridge, which itself was inspired by the German-Danish police thriller The Killing (2007–2012). These overlapping adaptations point to the increasing “velocity of appropriation” of transnational remixes in financialized media industries (Curtin, 2020: 99).

Pagan Peak came to life when Sky Germany commissioned the program to air on its pay television channels. Such commissions traditionally serve as the “green light” for producers to begin pre-production, wherein this distributor often covers a portion of the budget (Lotz and Sanson, 2021). The subsections below follow the money in more detail for seasons one and two—which premiered in January 2020 and January 2022, respectively—across different categories of capital flows: financing, production, and distribution.

Financing: Film funds

In following the money, perhaps the most obvious place to start is with the first-order stakeholders that fund the series. These financiers span local and transnational producers, local and global distributors, and regional and national film funds. Each of these stakeholders has its own higher-order financiers that are dispersed spatially and industrially, which requires a close follow the money approach. This section demonstrates how television funding and corporate financing include non-financial stakeholders and non-monetary sources of value.

One key group of financiers for all three seasons was state-run film funds. For instance, the state-backed German Motion Picture Fund served as a first-order financier, providing €1.156 million, or approximately 13% of the €9 million budget, for season two (Beauftragten, 2022); at the time of writing, season one figures were unavailable. In addition, FilmFernsehFonds Bayern (FFF Bayern) was another highly visible regional German film fund for all three seasons. For season two, FFF Bayern provided €1 million, or 11% of the budget (FilmFernsehFonds Bayern, 2019). The backers of FFF Bayern included the following second-order public and private funding sources: the State of Bavaria, the Bavarian Regulatory Authority for New Media, Bayerischer Rundfunk, Zweites Deutsches Fernsehen (ZDF), Seven.One Entertainment, RTL Television, and Sky Germany (FFF Bayern, n.d.). Notably, Sky Germany was already a distributor and commissioner of Pagan Peak that was paying producers for the right to air the series on its network in addition to being a co-financier of FFF Bayern, thereby highlighting how one firm can play multiple financial roles and the circular nature of media financing.

In addition to these two high-profile German funds, Austrian funds—at the national and local levels—provided financing for the show’s first season. The Austrian Television Fund (national level) provided €700,000; the Cinestyria Film Commission and Fund (city level) provided €100,000; the Film Commission of Graz (regional level) provided an undisclosed amount; and the Film Fund of the State of Salzburg (city level) provided an undisclosed amount (Ude, 2019). The non-disclosure and opacity of contributions by the two latter commissions suggest that their contributions may have been minor. While such film funds often do not receive equity in a program, they can receive other types of financial benefits. Indeed, incentives require that a certain amount of the provided funds be spent on local suppliers, cast, and crew. The film fund in Salzburg, for example, mandates that “expenditures in Salzburg amount to at least 200% of the awarded support . . . while at least 100% must be spent on goods and services in the Salzburg film industry” (State of Salzburg, n.d.).

The benefits for regions and cities are more than financial. Attracting a globally distributed series like Pagan Peak provides municipalities with a discursive opportunity to promote themselves as cultural centers and tourist destinations. This was certainly at play in Salzburg, where the Österreich Journal reported, in the context of Pagan Peak’s release, that Salzburg is the “location of well-known industry-specific companies and a technical college,” and film productions have clear “advertising value” for the border city (Österreich Journal, 2018). Similarly, the Provincial Councilor from Styria proclaimed, “The eight-part crime series . . . [has] enormous advertising value, since Styria is perfectly portrayed” (State of Steiermark, 2017). Although the Austrian press coverage and state press releases for Pagan Peak emphasized the role of the Austrian-based epo-film (e.g., Österreich Journal, 2018; Ude, 2019), German, European, and U.S. press emphasized W&B Television and Sky Germany (e.g., Hopewell, 2018; Whittock, 2017). In addition, Austrian film funds were not cited as financiers of season two or three, which suggests that Austrian funds needed to take on more upfront risk in betting on an unproven series but were cast aside (at least in publicly available documents and trade press) once the series was more established. When following the money, therefore, it becomes difficult to avoid these sorts of dialectics of opportunity (i.e., Austrian film funds’ acquisition of cultural capital and visibility by investing in a locally produced program) and constraint (i.e., Austrian film funds bearing more risk for season one).

Financing: Production firms

In addition to state-run commissions, two key production companies contributed an undisclosed amount to the show’s development and supervised its production: epo-film and W&B Television. If one “follows the money” connected to the first-order Austrian production firm epo-film, its smaller footprint (versus W&B) becomes clear. epo is privately owned: 26% by Austrian producer Dieter Pochlatko, 23% by his son Jakob Pochlatko, and 51% by Neue Studio Film (epo-Film, n.d.). Circuitously, Jakob Pochlatko is the sole listed shareholder of Neue Studio, so, in the aggregate, he owns 74% of epo (epo-Film, n.d.). No additional financial details about epo were readily available to identify higher-order relationships, such as whether epo maintained a line of credit with a local bank or had investments in other properties.

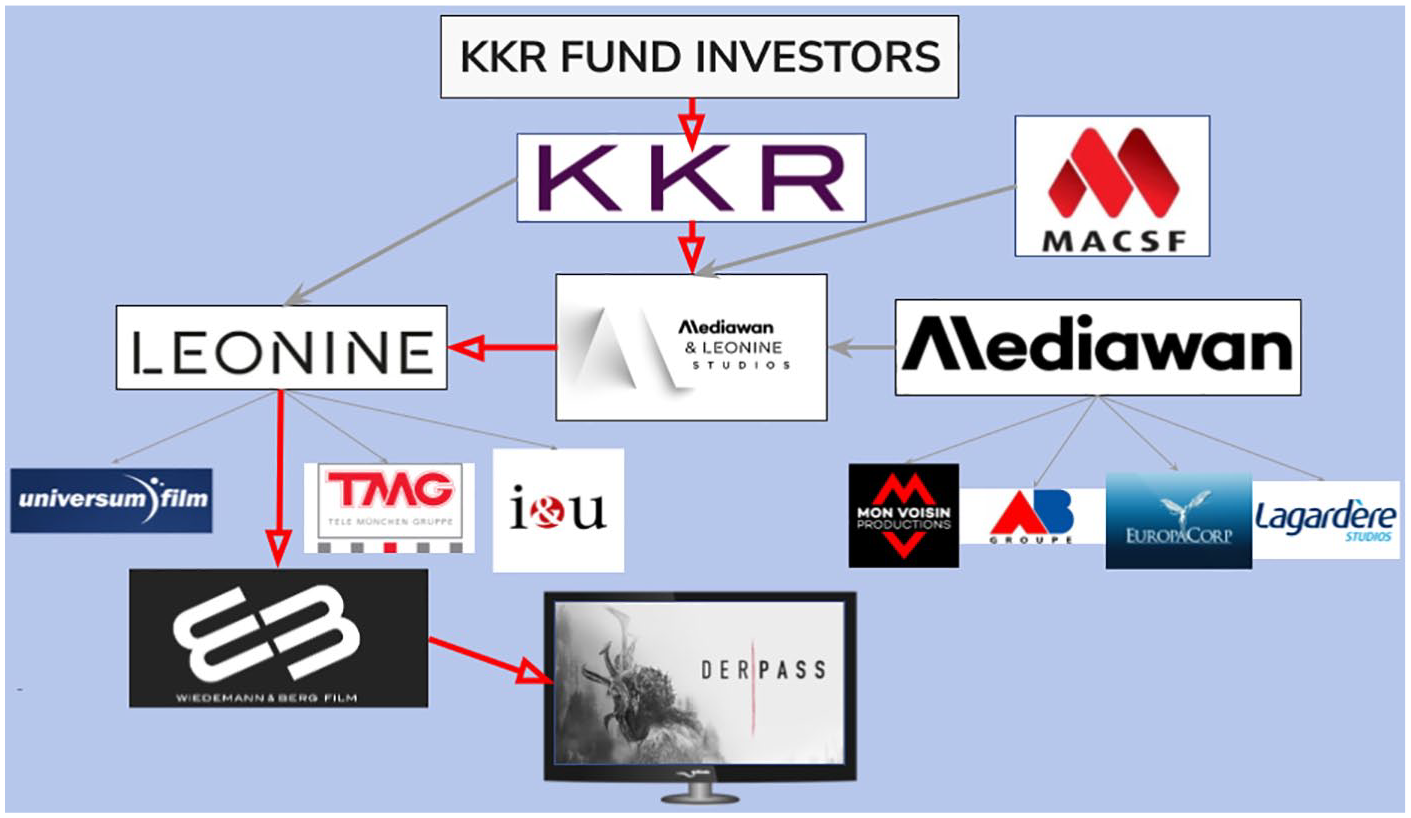

A significantly more complex capital flow begins with the first-order relation of W&B (Figure 2). In a second-order relationship, the regional film and television production conglomerate Leonine Holdings owned W&B. When the series was commissioned in 2017, W&B was a subsidiary of a different regional conglomerate, Endemol Shine, also owned by a private equity firm, Apollo Global Management (Whittock, 2017). In 2019, the U.S.-based private equity firm Kohlberg Kravis Roberts (KKR) and U.S.-based investment firm Atwater Capital purchased several German production companies, including W&B, which eventually were all combined under the banner “Leonine.” This was part of a broader trend in Europe and the United States, whereby private equity firms purchased local production companies to account for the “surging demands for programming” from streaming platforms in the late 2010s, particularly to meet local production quotas mandated by new European Union legislation (Middleton, 2019). KKR planned to “bundle the companies together to create an independent ‘German content’ company to supply both local networks and international platforms” (Roxborough, 2019). In this case, KKR represents a third-order relationship to Pagan Peak, while KKR’s investors—which could have consisted of pension funds, university endowments, and other institutional investors—represent fourth-order relationships. Private equity funds like KKR raise “pools” of capital from these accredited investors every few years with the intent of returning capital in approximately 5 years. Leonine’s investors were tied to a pool titled “European Fund IV” of an undisclosed value raised in 2014 (Official Journal of the European Union, 2020). Unfortunately, U.S. federal statutes do not require the U.S.-based KKR to disclose its investors, as they are classified differently than publicly traded investors (KKR European Fund IV, 2014), and no European laws or public filings provide visibility into European Fund IV.

W&B Television’s capital chain.

Complicating matters further, the French production conglomerate Mediawan purchased a minority stake in Leonine in 2020 via a joint venture, called Mediawan Alliance, which represented a third-order relationship to the series alongside KKR (Tartaglione, 2020). Embodying one of the many overlapping webs of media ownership, Mediawan was backed by not only the French insurance company MACSF but also KKR. Therefore, KKR maintained a third-order relationship to Pagan Peak via Leonine and a fourth-order relationship via Mediawan Alliance in this chain of capital sprouting from W&B.

KKR’s role in local European production reveals a tension between “corporate imperialism” and “bottom-up counterflows” amid financialized capitalism. On the one hand, regional conglomerates like Mediawan and Leonine were touted by KKR Managing Director Philipp Schaelli as counterattacks against invading U.S.-based streaming platforms and offered a way to take advantage of new European Union mandates, which required streaming platforms to include a minimum amount of locally produced content for each territory (Schaelli, 2020). As Doyle et al. (2021: 109–111) note and my interviews with independent producers corroborate, some producers—particularly those outside of media capitals like Hollywood—actively seek out private equity, despite its reputation for extractionary tactics. Typically, producers choose between outside financial buyers like private equity, which offers more capital and scale but less expertise, and industrial buyers, which usurp more operational/creative control but offer more sector-specific expertise and reputational capital (Paterson, 2022). In this case, KKR’s “roll up” investment strategy in Europe—with Leonine in Germany and Mediawan in France—resolved this choice by bringing together several production companies under one scaled entity to share expertise.

On the other hand, the financial ownership of Leonine and Mediawan remained in the hands of a powerful and historically exploitative private equity investor. KKR’s track record suggested that it would pressure Leonine to improve short-term productivity and profitability, which could be at odds with creativity and long-term viability (Crain, 2009; deWaard, 2020) and push cultural producers in Europe from public to commercial mandates. As Curtin (2020: 96) notes, “financialization mercilessly pressures employees to do more with less, privileging commercial calculation over creative purpose and wringing out cost economies that show little regard for creative sacrifices or safety risks.” Given the time window of private equity returns, KKR was likely seeking a sale of Leonine by approximately 2023 to 2026. It indeed found one in 2024 via its merger with Mediawan, again its own property. Therefore, KKR’s involvement ultimately resulted in relative sectoral concentration.

These two countervailing tensions foreground the ambivalences of contemporary global media industries. Deregulation and financialization led hegemonic U.S. financial institutions to purchase and potentially exploit mid-sized production firms transnationally. At the same time, they provided producers with the capital, collaboration, and scale necessary to compete against entrenched local players and new global streaming platforms like Netflix and Amazon Prime Video. Only focusing on the former process would neglect the opportunities—however limited and short-lived—resulting from financialization. In other words, media industries are “situated within plastic and multipolar topographies where each player refigures cultural texts and institutional operations according to shifting scales of opportunity and constraint” (Curtin, 2020: 99).

Production vendors

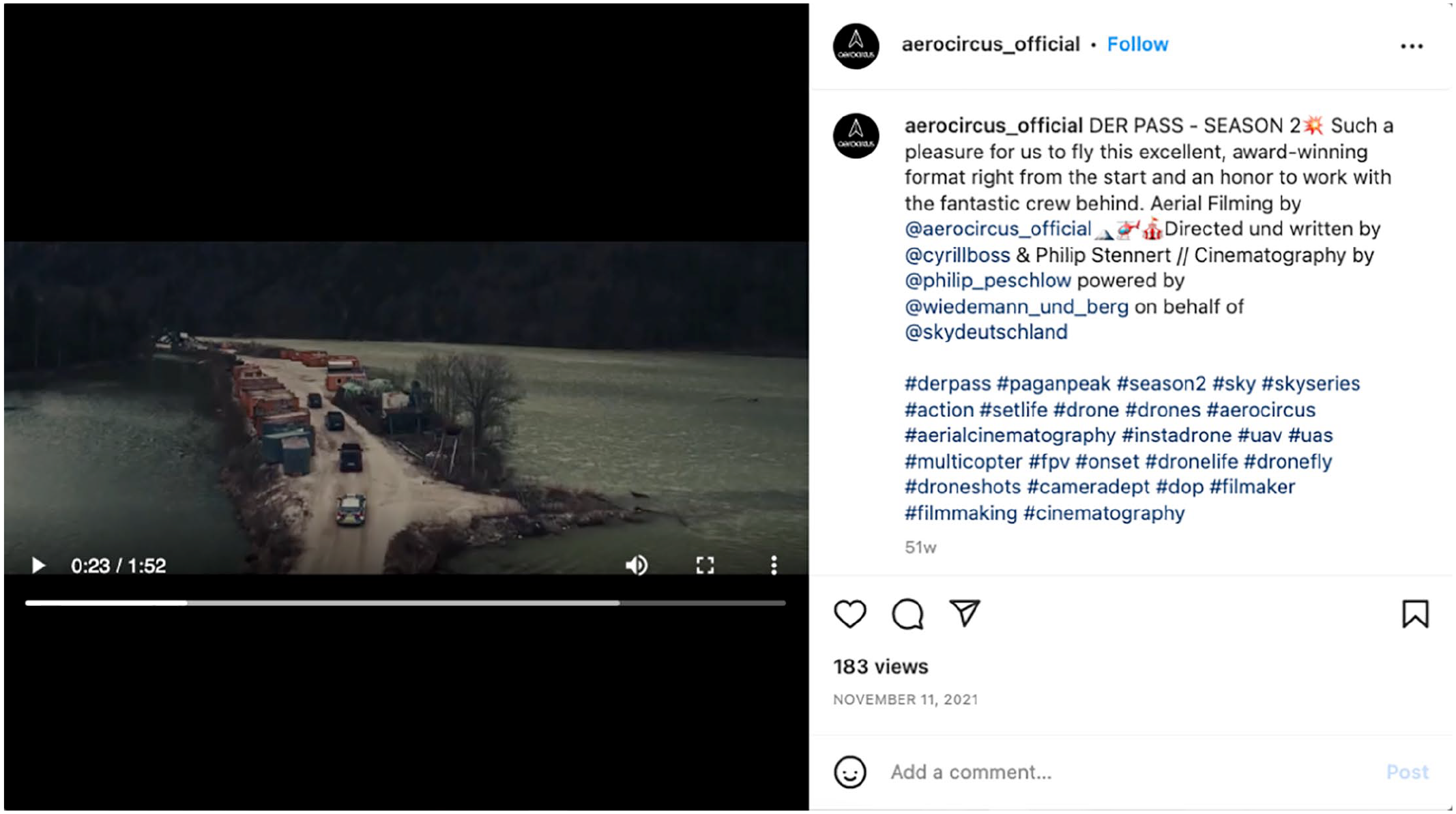

While financial investors represent the most obvious sites of financial exchange, other stakeholders cannot be separated from the show’s financial ecology. As detailed in Supplemental Table 1, production vendors for season one included those that provided props, vehicles, catering, cameras, lighting equipment, and even toilets—in addition to a host of post-production services. First-order intermediaries ranged from Wolfgang Petters Filmbau & Filmservice, which provided transportation services for the crew on the snowy mountain pass featured in the first season, to filmobil, which provided trailers for the cast and crew. Further, two first-order vendors provided camera equipment. Vantage Film provided the production with basic film cameras, lenses, and accessories, but the production needed to further outsource to aeroCircus to provide drone equipment for the aerial shots featured heavily in the brooding crime thriller. Beyond service fees, the association with a transnationally distributed program like Pagan Peak provided these small businesses and their employees with valuable cultural-industrial capital. For example, aeroCircus’s six Munich-based employees can add this high-profile production to their résumés, while the firm can feature the sweeping mountainscapes in Pagan Peak in its “award-winning showreel” (aeroCircus, n.d.) and social media posts (Figure 3).

aeroCircus’s social media promotion of Pagan Peak.

Notably, given the more prominent role of Austria and Salzburg in the first season of the series, there were several Austrian vendors and partners in the first season. This was necessary to adhere to the co-production agreement and the stipulations of local funding commissions (O’Regan, 2008). For example, the season one vendor Ö wie Knödel—a catering service—maintained locations in both Munich and Vienna. Similarly, Herz Medicalgroup, located in both Germany and Austria, provided consulting advice on the script and various medical services, such as COVID-19 safety oversight, medical props, and first-aid equipment. In addition to suppliers, there were also 154 crew members and 56 cast members who contributed to the first season and received first-order payments for their labor (Crew United, n.d.).

Distribution

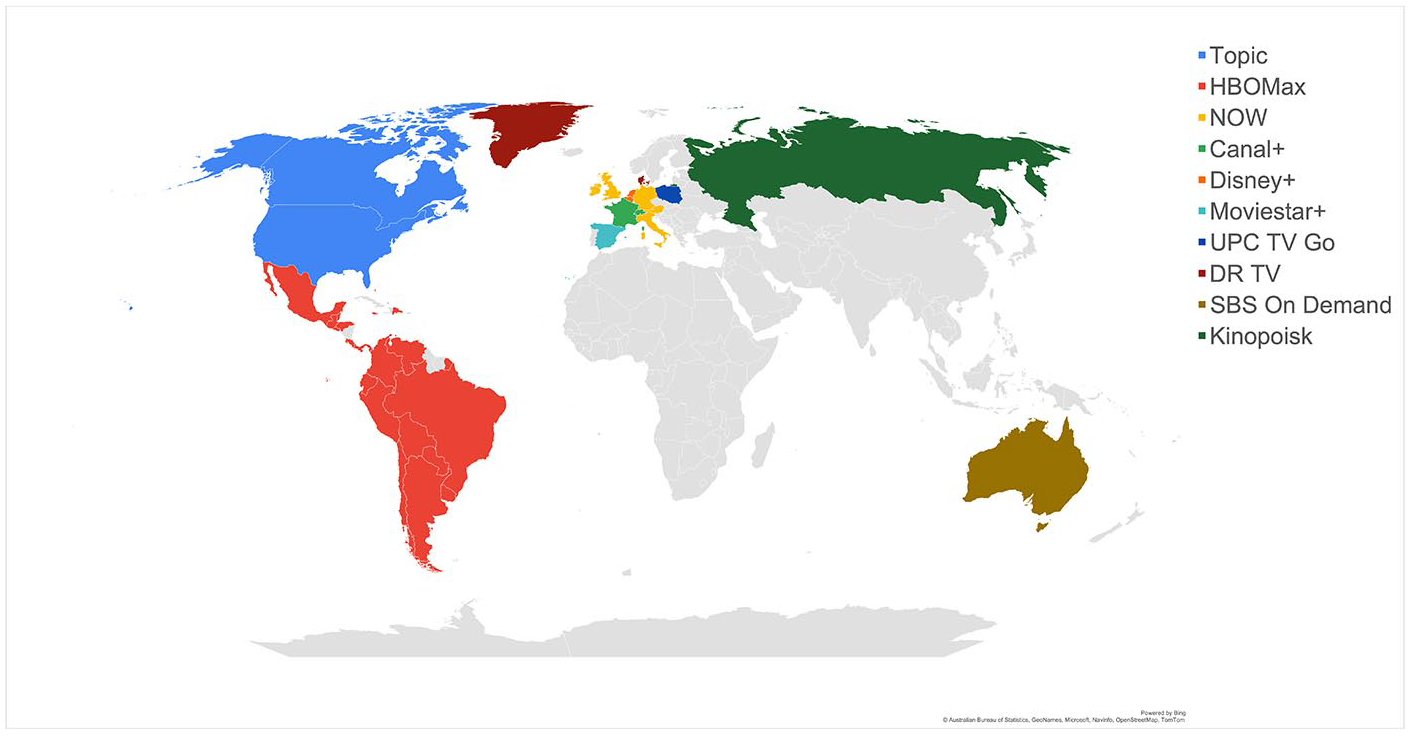

Moving the scope forward, a multiplicity of distributors on linear and streaming television licensed the rights for Pagan Peak. Unlike another highly popular German-language drama from W&B titled Dark (Netflix, 2017–2020), which was commissioned and distributed exclusively by a single platform (see Figure 4), Pagan Peak partnered with a third-party sales agent (Beta Films) to sell the series on a territory-by-territory basis—a practice more common before the entrance of global streaming buyouts. Figure 5 illustrates the distinctive firms that exhibited Pagan Peak in their respective territories, which are bounded by both legal geo-blocking restrictions and national-cultural imaginaries (JustWatch, n.d.). This type of region-by-region distribution became less common between approximately 2017 and 2022 as global streamers like Netflix and Amazon Prime accounted for more commissions of local content and required producers to hand over global rights. However, there were signs in 2023 and 2024 that territorial deals, a la Pagan Peak, would become more common again due to industrial contraction.

Distribution of W&B’s Dark.

First season “Pay 1” distribution window of Pagan Peak.

Pagan Peak also features a first-order relationship with Sky Germany, which is distinctive from its other distributors because it was the “commissioner” of the program. Sky guaranteed distribution of the series, which allowed the producers to secure financing and start selling it to other territories or find co-producers. It also indicates that Sky effectively co-financed the series (Hopewell, 2018). Complicating the notion that Pagan Peak was a locally produced and financed series, however, Sky Germany is owned by the broader pan-European conglomerate Sky Group (second order), which itself had been owned by the U.S.-based Comcast (third order) at the time of production (Goldsmith, 2020). Notably, Vienna’s public broadcaster also had the opportunity to contribute €500,000 to the first season and become a fellow “commissioner” alongside Sky, but officials in Austria “feared not having enough say” against the more powerful Sky and decided against it (Ude, 2019).

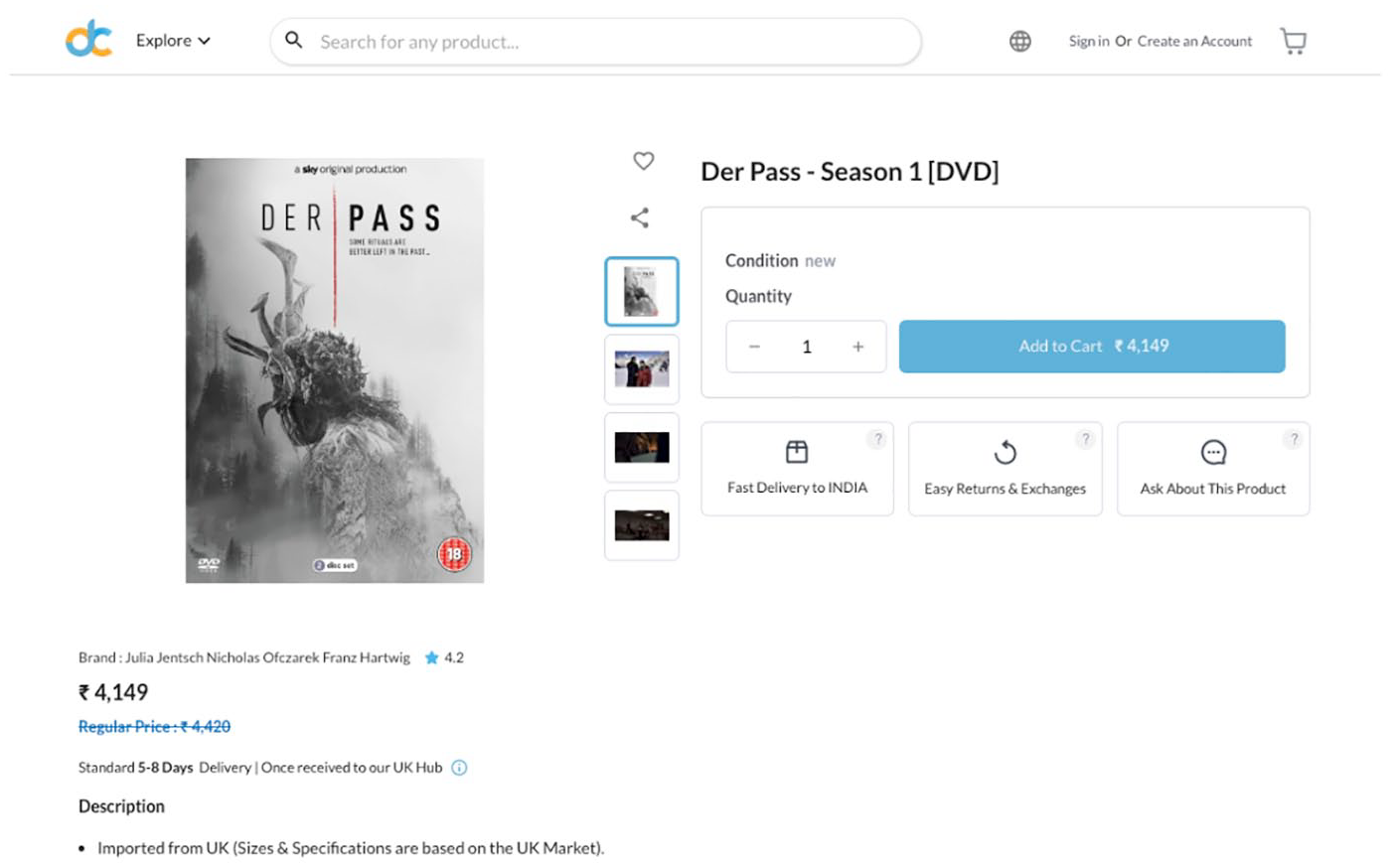

These formal distribution agreements do not even include the informal economies in which the media object circulated. For example, there were a number of unknown-order capital flows that represented the physical circulation of Pagan Peak in different geographies, such as a Pagan Peak season 1 DVD imported from the U.K. to India via the site Desertcart (Figure 6) (DesertCart, n.d.). Given the opacity of the process by which that DVD may have traveled from the first-order manufacturer of the DVD to non-corporate sellers on platforms like Desertcart or eBay, it is difficult to track the complete flow of money when following this object. Still, the fragmented story and incomplete information about this capital chain are paradigmatic of the nearly endless idiosyncratic routes of capital that intersect with a single cultural product.

Pagan Peak DVD for sale on Desertcart.

In addition, an emphasis on formal financing and distribution elides the pirated forms of Pagan Peak circulating in non-financial economies. For example, Pagan Peak was available on the unsanctioned website 0123Movies (among many other piracy sites), which provides a full library of searchable pirated titles. Unlike other economies connected to Pagan Peak that rely on financial capital, the economy of 0123Movies and other piracy sites is driven by other types of capital, such as the cultural and social capital among community members, and by the “gift economy” that perpetuates an ecosystem of free pirated content.

Conclusion

As this case study demonstrates, simply tracing money (or ownership) back to a single financier does not tell us enough about the relationships between media industry stakeholders. Certainly, the financial hegemon KKR had a heavy hand in the corporate consolidation of two regional production conglomerates connected to the show, but several other entities financed the show, some of which had non-pecuniary motivations, including the pursuit of cultural, social, and political capital. Ironically, when we try to follow the money, we find that we cannot just follow the money, as we end up bumping into other axes of power, sociality, and capital that are paradigmatic of the shifting and relational ecologies of contemporary capitalism.

There are several items beyond the scope of this article that represent opportunities for future research. The limited space of this article precludes the possibility of addressing all stakeholders. For example, this case study excludes other distributors and audiences, so there remains an opportunity to consider the ways that viewers are involved in financial ecologies. Alternatively, this method could more explicitly be applied to axes of identity, such as race, gender, ethnicity, etc., or to case studies in the Global South if such approaches are methodologically possible. Beyond Pagan Peak, researchers could ask how and why the dispersion (or lack thereof) of finance may be different for other films and television series, particularly those commissioned by global streaming platforms. Additionally, the role of private equity and financial investors, particularly their role in the consolidation of European production in the 2019 to 2024 period, could be further explicated.

Supplemental Material

sj-docx-1-mcs-10.1177_01634437251341232 – Supplemental material for The financial ecologies of transnational television production: “Following the money” from private equity to Sky Germany’s Pagan Peak

Supplemental material, sj-docx-1-mcs-10.1177_01634437251341232 for The financial ecologies of transnational television production: “Following the money” from private equity to Sky Germany’s Pagan Peak by Peter Arne Johnson in Media, Culture & Society

Footnotes

Acknowledgements

The author wishes to thank Shanti Kumar for his generative feedback on an early draft of this project.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Ethical approval and informed consent statements

Not Applicable.

Data availability statement

Not Applicable.

Other Identifying Information

None.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.