Abstract

As television is embracing a new set of internet-related technologies, the medium is transitioning from broadcasting to streaming. With it, a new mode of distribution has emerged: the streaming platform. This research makes a three-pronged effort to assess their impact on the TV industry: it analyses the way platforms monetize content; it distinguishes types of streaming platforms based on a set of criteria that includes supply-chain arrangements and the way they structure commercial transactions among different sets of participants, and it considers the ownership of streaming services. This article contributes to media and communication studies by combining the platform literature with global value chain (GVC) theory in order to foster our understanding of streaming platforms. It contextualizes streaming platforms in the history of television and analyses how they are transforming the medium.

Keywords

Introduction: looking beyond lead firms

The emergence of the Internet as a means of video distribution is turning out to be among the most radical transformations the medium has ever seen (Johnson, 2019). As television is embracing a new set of internet-related technologies that combine cloud infrastructure with tools such as artificial intelligence and machine learning (AI/ML) and content delivery networks (CDNs), the medium is transitioning from broadcasting to streaming. With it, a new mode of content distribution has emerged: platforms (Boyle, 2019). This article contributes to media and communication studies by combining the platform literature with global value chain (GVC) theory in order to foster our understanding of streaming platforms. It contextualizes platforms in the history of television and analyses how they are transforming the medium.

This research makes a three-pronged effort to assess the impact of platforms on the TV industry. First, it examines the way platforms monetize content. Have platforms developed innovative business models or do they rely on pre-existing monetization strategies? The next section distinguishes three types of streaming platforms based on a set of criteria that includes supply-chain arrangements and the way they structure commercial transactions among different participants. It aims to gauge the distinctiveness of streaming platforms: how similar are they from the archetypical digital platform described in the literature? The final section considers the ownership of streaming services: are they controlled by tech firms or traditional media and entertainment companies? Its objective is to evaluate the extent to which the platformization of television involves new industry perimeters and entrants. The conclusion evaluates the depth of the sectoral transformation brought by the platformization of the TV industry.

The platform literature is growing and diverse but most studies adopt a similar epistemological standpoint. The discourse on platforms is dominated by the hypothetico-deductive approach (Nola and Sankey, 2007: 170–184). Its knowledge and theoretical base rest on a few well-known and powerful ‘super platforms’, which have become the ideal type to which all others are measured and compared. The laws and principles that govern platforms are inferred from a small sample that involves a strong survivor bias.

Platformization may be a widespread phenomenon but its impact is far from uniform across sectors. Even within the creative industries, the scope and nature of platformization vary between, say, music and gaming (Poell et al., 2022: 194). As Thomas Poell et al. state, ‘one should avoid starting one’s platform analysis at “year zero,” disregarding the long-term trends and developments in the cultural industries that precede the rise of platforms’ (Poell et al., 2022: 181). Television is a mature industry with well-established production patterns and markets, and the rise of platforms entails both changes and continuities.

This article addresses these issues by combining the platform literature with GVC theory. A value chain refers to the value-adding activities and the range of economic actors that participate in the design, making and delivery of a product or service (Gereffi et al., 2005; Gereffi and Fernandez-Stark, 2016; Sturgeon, 2009). Unlike the platform literature and media industry studies which invariably focus on lead firms, the GVC framework is a holistic approach that takes the entire production network as unit of analysis. Taking lead firms as the unit of analysis does not make sense when they are no longer vertically integrated and their business model is predicated on outsourcing and the management of complex production networks. It is these networks that produce and deliver TV programmes to audiences, not lead firms on their own (Chalaby, 2023). The GVC framework enables us to differentiate streaming platforms according to the type of suppliers they work with and the type of supply chain they orchestrate.

GVC theory is based on inductive research methods, ‘moving from the particular to the general’ and ‘making empirical observations’ about phenomena by way of making a contribution to theory (Woiceshyn and Daellenbach, 2018: 185). In our case, it involves adopting a sector-specific perspective and observing streaming platforms before drawing any conclusion. It enables us to give a more accurate assessment of streaming services by steering clear of a one-size-fits-all approach and integrating the historicity and specificity of the TV industry into the analysis.

Platforms and the monetization of content

Digitization is supplanting industrialization as the growth engine of Western economies, leading to the formation of online marketplaces and digital multinational enterprises (UNCTAD, 2017). As capitalism changes, so do its most emblematic firms. The vertically integrated modern industrial enterprise, Alfred Chandler argued, was the linchpin of Western economies as they industrialized in the late 19th century and 20th century. Conglomerates like General Electric or Bayer dominated their respective sectors as they expanded their organizational capabilities and market reach in search of economies of scale and scope (Chandler, 1990). In the same way the Chandlerian firm expanded on the back of new technologies that reformed multiple industrial processes (Chandler, 1993), the growth of internet connectivity has spurred a new type of organization: the digital platform (Gawer, 2022).

Platforms are the hallmark of the digital economy and have become prevalent because they are ‘are particularly well-adapted to the novel ways in which value can be created and captured under the new technological circumstances’ (Gawer, 2022: 110). Airbnb, eBay, Amazon Marketplace and Uber transform the way goods are exchanged and consumed in entire sectors. Their new-found pre-eminence is reflected in idioms such as ‘platform capitalism’, ‘platform economy’ or ‘platform revolution’ (Kenney and Zysman, 2016; Parker et al., 2016; Srnicek, 2017; Steinberg, 2019). The firms that operate them (e.g., Alibaba, Amazon, Alphabet, Apple, Microsoft) are the most valuable in the world (Jacobides et al., 2019: 8; Kenney and Zysman, 2020: 57).

The digital economy is a sector in its own right which exists alongside others such as manufacturing and retail (Jordan, 2020: 1–17). Some firms are identified as operating within it, such as software developers and video game publishers. Most businesses and sectors, however, are not born digital but have embarked on a process of digitization. It is the case of media and entertainment, and the platformization of television is among the most visible signs of this process. Streaming platforms can be defined as those whose business model rests on video monetization. They overlap but are distinct from social media platforms that stream videos but whose business case does not entirely rest on them (Cunningham and Craig, 2019). The former includes Facebook Watch, Netflix and YouTube, the latter Facebook, Instagram and Twitter.

Streaming platforms predominantly operate in the field of Video on Demand (VoD), which entails four possible monetization models. Subscription Video on Demand (SVoD) requires members to pay a monthly fee in exchange for unlimited access to the provider’s catalogue. With Transactional Video on Demand (TVoD), customers are charged on a per-item basis. Advertising Video on Demand (AVoD) is a model where content is free to access for viewers and content providers sell the audience to advertisers. The AVoD model includes FAST services (Free Ad-supported Streaming Television), which have the particularity of having both linear channels and on-demand content. These services are available on platforms such as Freevee and Pluto TV. Free Video on Demand (FVoD) designates public broadcasters’ streaming services. While these organizations are usually financed through licensing fees or tax revenue, FVoD services are freely accessible at the point of watching.

While VoD pre-existed streaming and was developed by cable and satellite pay-TV services (Rooke, 2009: 216–234; Tydeman and Kelm, 1986; Vittet-Philippe, 1999), platforms have brought changes to the monetization formats. Advertising has always been a key revenue stream for broadcasters, but it is streaming that brought AVoD to the forefront of the TV industry in the 2000s. Pay-TV operators have long charged a subscription fee for access, but the concept of charging a (cheaper) fee for an entire catalogue is new to the platform era. Furthermore, SVoD involves less complex contractual arrangements than TV subscription. It is usually unbundled to connection services such as broadband and telephony and can be terminated at short notice. Cable and satellite operators’ pay-per-view is the ancestor of TVoD, which is only used as a payment option within AVoD and SVoD environments.

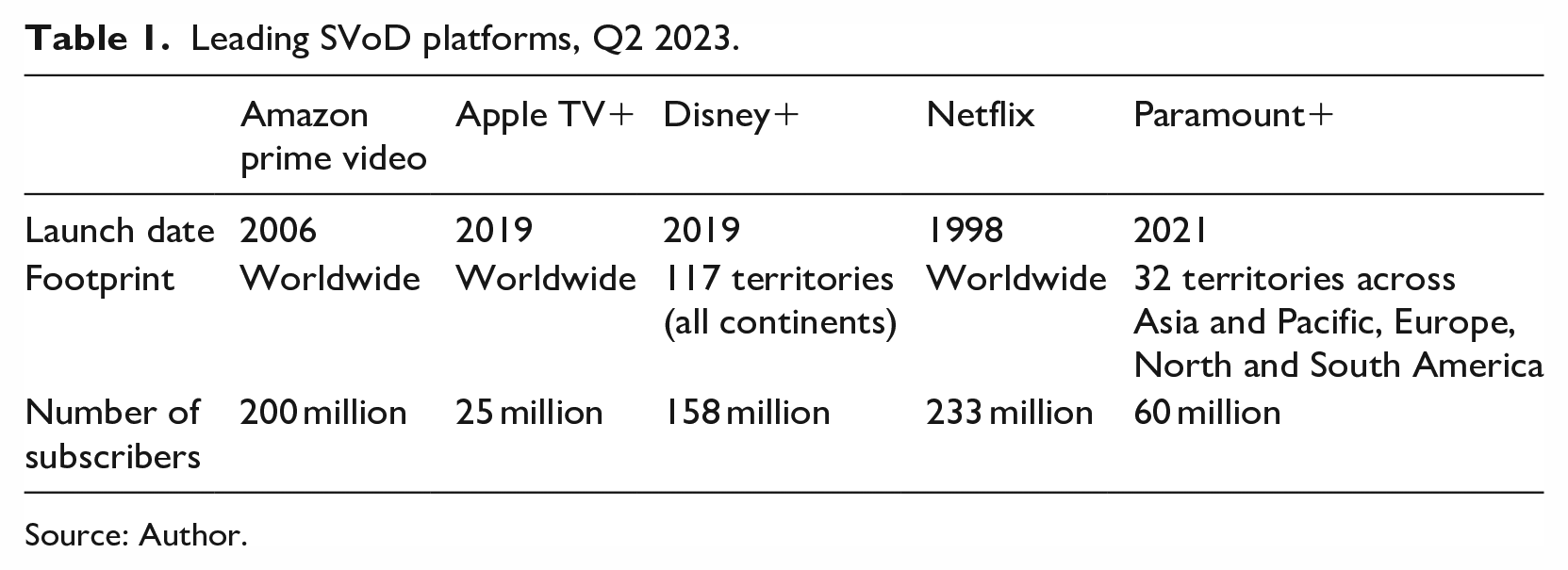

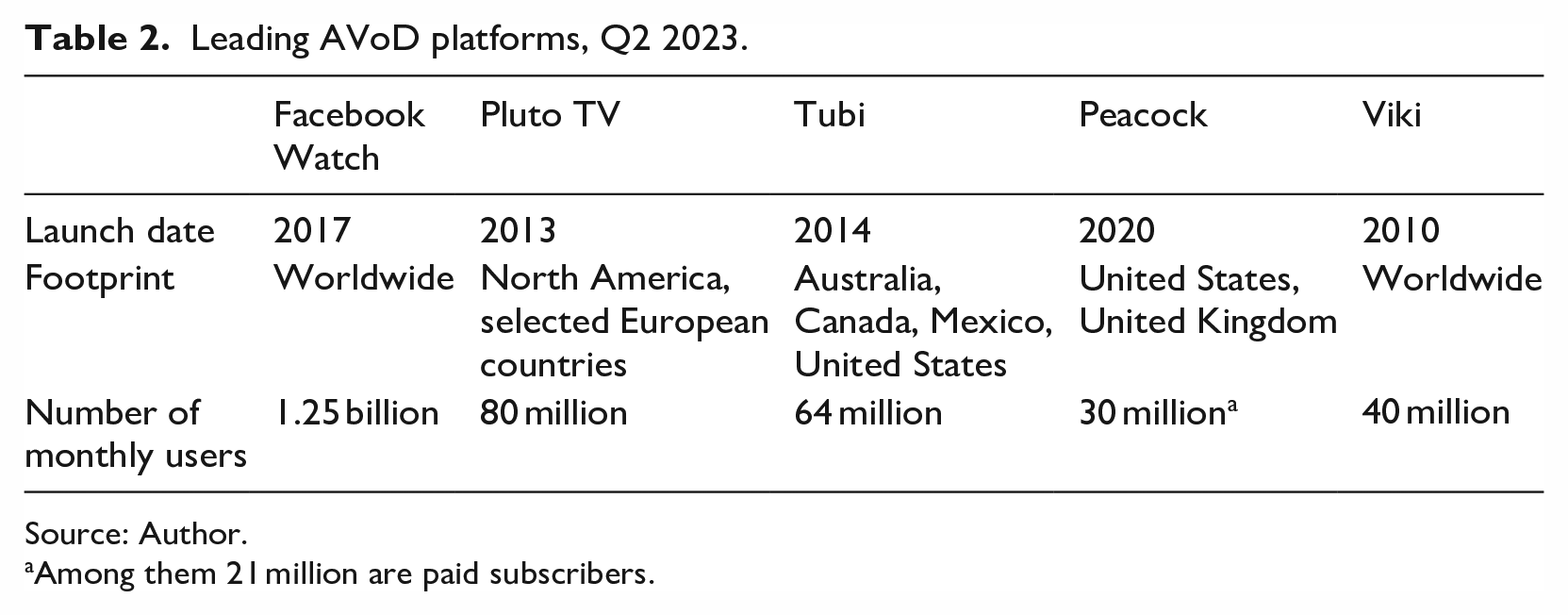

Even though most platforms offer multiple price points and payment plans, they are predicated on either the AVoD or SVoD model (Tables 1 and 2). In SVoD, Hulu’s ad-supported plan is the cheapest but still costs US$7.99 a month at the time of writing. Netflix, which has shed subscribers in the first half of 2022, has introduced a lower-priced ad-supported tier in twelve countries. AVoD services primarily monetize their content through advertising, even though all have a premium option giving subscribers access to their content commercial-free. For instance, Comcast’s Peacock has three tiers, the first is free with advertising and limited content, the second requires a subscription and is all inclusive but still includes advertising, and the third is all inclusive and ad-free.

Leading SVoD platforms, Q2 2023.

Source: Author.

Leading AVoD platforms, Q2 2023.

Source: Author.

Among them 21 million are paid subscribers.

Streaming platforms innovate on two other counts. First, they are scaling up these monetization models. Pay-TV services operated on a national or multinational basis. The world’s largest, Sky, has developed a presence in a handful of European territories and claims around 17 million customers. Broadcasting was a national industry that progressively internationalized, streaming is a global business that is progressively localizing. No platform is born global and even Netflix waited several years before crossing borders (Randolph, 2019). However, once the decision is made platforms achieve international coverage at breakneck speed. Many streamers have a worldwide footprint, covering up to 190 territories (Tables 1 and 2).

Two SVoD services, Disney+ and Paramount+ have launched relatively recently but are making up for lost time. As of June 2023, Disney+ has reached 158 million subscribers across more than 100 territories and Paramount+ has 60 million subscribers in 32 countries. Warner Bros. Discovery claims 95.8 million subscribers across Discovery+, HBO and Max. Max has undergone a US relaunch but Discovery+ has wide international reach. Universal coverage, however, is impossible to achieve as Western services are banned in China, Iran, Russia and North Korea (Griffiths, 2019). TikTok, whose parent company is based in Beijing, is threatened with various bans in the USA but is barred from India and Pakistan (Chin, 2021).

Operating across large swathes of land, streaming services garner subscribers and monthly users at unprecedented levels in the history of television, and three SVoD platforms have more than 100 million subscribers (Table 1). Serving large subscriber bases, major streamers’ libraries contain thousands of hours of programming, including a fair amount of originals, content that is exclusive to them (Afilipoaie et al., 2021). Netflix, for instance, released 398 original shows in 2022 (Considine, 2022). Streamers’ libraries also contain a healthy number of ‘quality’ movies (rated 6.0 or above on IMDb) and ‘quality’ TV shows (rated 6.0 or above on IMDb) (Clark, 2022). 2429 movies on Amazon Prime Video, 2,141 films on HBO Max, and 2456 titles on Netflix met this standard in 2022 (Clark, 2022).

SVoD platforms operate libraries (as opposed to broadcasters’ schedules) (Lotz, 2022: 44–55), which vary in territorial diversity. Disney+’s content remains similar across multiple countries, as the operating company relies on the platform to distribute its global franchises online. Amazon Video Prime and Netflix are far more localized, to the point that Ramon Lobato calls the latter ‘a series of national services linked through a common platform’ (Lobato, 2018: 245). As Netflix expands the number of titles it commissions locally, the platform’s national libraries become more distinct (Lotz et al., 2022).

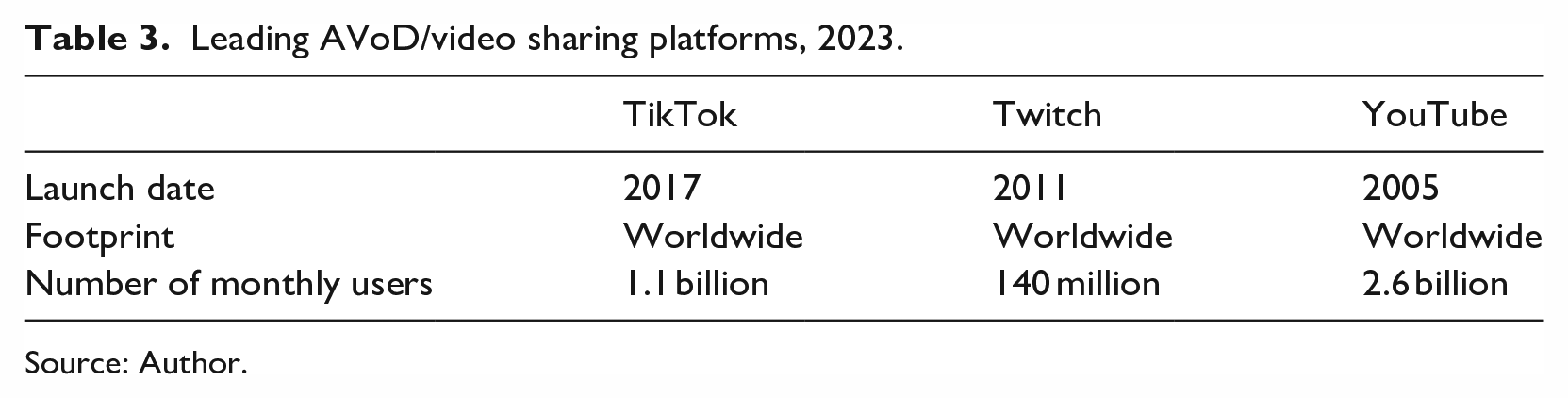

Further, streaming platforms have introduced a whole new genre to television: user-generated videos, which are uploaded and shared on video-sharing websites (Shifman, 2011). They constitute a new type of platform because content creators have multiple options to monetize their content (see section below). However, from the perspective of the platform owner, these services fall under the AVoD model because user-generated content is primarily monetized through advertising. The video-sharing market is incredibly concentrated because of the strong network effects at play, which means that the value of the platform to users increases as their number grow. These effects are called same-side (or direct) when they affect ‘users of the same kind’ and are deemed cross-side (or indirect) when ‘users benefit from an increase in the number of participants on the other side of the market’ (Parker et al., 2016: 29–30). As the number of videos uploaded on a service expands, more users log on the website since it is more likely they will find content that retains their interest. In turn, as the number of viewing hours increase, advertisers flock to the platform. These cross-side network effects combine to give the leader an unassailable position and create a winner-takes-all market (Parker et al., 2016: 16–32; Sturgeon, 2019: 44).

Three platforms dominate the field (Table 3). YouTube launched in 2005 and was acquired by Google the following year (Burgess and Green, 2018; Chalaby, 2022). It is the market leader with over two billion visits a month and one billion hours of video viewed every day. Five hundred hours of content is uploaded every minute and the library has expanded to 10 billion videos. Worldwide advertising revenue is in sharp growth, increasing from US$ 19.8 billion in 2020 to US$ 28.8 billion in 2021 and US$ 29.2 billion in 2022 (Alphabet, 2023: 32).

Leading AVoD/video sharing platforms, 2023.

Source: Author.

Twitch launched in 2011 as a spin off from Justin.tv, a platform streaming user-generated live video content which had started in 2007 (Spilker et al., 2020). The platform was acquired by Amazon in 2014 and is the leading platform for live streaming. It is known for game streaming and esports events, but it is home to a wide variety of streamers ranging from arts and crafts, cooking, and software development.

TikTok was founded by Beijing’s ByteDance in 2012 and began to internationalize 3 years later. The short-form video hosting service has since become one of the most downloaded applications of all times (Jia and Liang, 2021). In terms of global application traffic share, TikTok ranks fourth behind Netflix, YouTube and Disney+, ahead of Amazon Prime Video, Hulu and Facebook Video (Sandvine, 2023: 12). The streamer’s advertising revenue rose from US$4 billion to US$10 billion between 2021 and 2022.

Most other video-sharing services have closed or have been acquired by one of the leading services. In order to compete successfully, both Twitch and TikTok have had to come up with a clear strategy and positioning (live streaming for the former and short-form video for the latter). However, the San Bruno-based platform responded with YouTube Live and YouTube Shorts, and these services represent a challenge for the two streamers. YouTube Shorts reached an all-time record of five trillion views last year (Sandvine, 2023: 12), and while TikTok has clearly scope for growth, its 2022 revenue was below most analysts’ expectations.

Streaming platforms’ monetization models rest on formulae (advertising, subscription, and pay-per-view), which date from television’s broadcasting era. Yet, the innovations they bring about disrupt classic monetization models. SVoD updates the subscription model by offering novel content more cheaply and conveniently than pay-TV. AVoD has become a stand-alone monetization strategy in the platform era. Furthermore, streaming represents a major shift in scale: while broadcasters predominantly operate at national level, leading streamers combine cloud technology and powerful network effects to achieve global scale. Their monetization strategy is predicated on the amortization of investment across multiple territories, enabling them to offer an unparalleled amount of content to an unprecedented amount of subscribers and users.

Types of streaming platform

The ‘super’ platforms that are most commonly examined by the literature share three attributes: they are digital, have a transformational impact (e.g., Amazon and retail) and are market leaders (e.g., Uber in the ride-sharing industry). They come in two varieties (Cusumano et al., 2019: 18–21): innovation platforms are ecosystems that are built and owned by the platform architect, whose functionalities are enriched by complementors that develop and monetize their own products and services. Examples include Google Android, Apple iOS and Amazon Web Services (AWS) (Cusumano et al., 2019: 18–19). Transaction platforms are ‘pure exchange or trading platforms’ (Gawer, 2009: 57) and can be conceived of as interactive ecosystems that coordinate transactions among two or more groups of agents (Cusumano et al., 2019: 20–21; Parker et al., 2016: 1–15; Steinberg, 2019: 95–125). Airbnb, Amazon Marketplace and Ebay provide illustrations.

How do streaming services compare to these illustrious businesses? This section distinguishes three types of entertainment platforms based on their supply-chain arrangements, categories of participants and the flow of commercial transactions among them. To a certain extent, these types match the monetization models, but based on these criteria video sharing becomes a distinct category. While this classification is informed by the literature, it is based on empirical observations. This typology allows for an in-depth understanding of each type of streaming services, notwithstanding the similarities they bear with the archetypical digital platform.

SVoD services: engineering platforms

SVoD services are platforms in the engineering sense of the term. Netflix, for instance, is a platform because it is designed as a configurable modular system: it is a collection of building blocks that subscribers can configure to their taste. Each subscriber selects different building blocks from the same system (or possibly the same building blocks but in a different order), and there are as many Netflix variants as there are subscribers, even though the differences between variants can be minimal (Baldwin and Woodard, 2009: 25).

SVoD platforms make full use of technology to operate this system. From a media delivery perspective, the broadcast path is a push system as content is sent out via the airwaves and the receiver simply tunes in. It is a unicast system as all receivers within the airwaves range get the same copy at the same time. By contrast, the streaming path is a pull mechanism as users must request their own copy of the material, and it is a multicast transmission mode as each one gets their own file. SVoD services are built for a multicast environment where subscribers are sent their own material upon request, thereby enabling them to select building blocks from the modular system.

Streaming delivery includes a return path, enabling platforms to collect precise data about viewing, browsing and scrolling behaviour. Data is stored, processed and fed into recommendations systems, which are based on algorithms that filter and rank content based on the probability that users will watch it. Viewers access SVoD platforms through an interface that is fully personalized, from titles selection to the artwork and visuals that depict each title (Chandrashekar et al., 2017; Chong, 2020; Meltzer, 2020).

In terms of infrastructure, platforms use the cloud to distribute their content. In order to manage risk and prevent loss of data due to outage or natural disasters, SVoD services have multiple server locations that host their entire library. These servers are based in ‘hyperscalers’, very large data centres that form the backbone of the Internet (Floerecke et al., 2023). Content delivery networks (CDNs) are then used to cache the most popular files in the edge of the network and close to where the users are (Stocker et al., 2017). For instance, if a Netflix subscriber based in Milan streams a video that is locally popular, this video will come from one of Netflix’s edge locations in Northern Italy. If, however, this particular video is rarely requested there, it will come from a large data centre located further away from the user.

SVoD providers do not own the infrastructure they use and outsource media delivery. They contract cloud providers such as Amazon Web Services and CDN specialists such as Akamai Technologies (Chalaby, 2019). This outsourcing strategy is consistent with the behaviour of digital platforms across sectors. The recourse to cloud providers dispenses them from heavy tech investment which a single user cannot amortize, and offers ‘upside flexibility’ (Sturgeon, 2002: 458), which enable them to scale up capacity according to demand at very short notice.

SVoD services behave like digital platforms from a tech perspective but a GVC analysis reveals that they do not share many of the characteristics of either innovation or transaction platforms. The latter’s distinctive feature is their ecosystem which is ‘a set of actors with varying degrees of multilateral, nongeneric complementarities that are not fully hierarchically controlled’ (Jacobides et al., 2018: 2264; italics in original). In such ecosystems, actors are participants or complementors in a marketplace rather than suppliers in a value chain tightly controlled by a lead firm. Complementors have direct access to the market, even though this access is subject to rules and parameters set by the platform architect (Humphrey, 2018; Jacobides et al., 2018). Complementors include the app and software developers which operate in the marketplaces created by Apple iOS or Google Android (Cusumano et al., 2019: 19).

SVoD providers behave like classic lead firms located at the apex of value chains (Gereffi et al., 2005; Gereffi and Fernandez-Stark, 2016). They may have different ways of acquiring inventory but in all cases their producers are suppliers with no direct access to subscribers and no transaction occurs between the former and the latter. SVoD services can acquire the rights of pre-aired programmes, commission or co-commission content, or produce it themselves either by using their own facilities or paying for the entirety of the production costs plus margin (Afilipoaie et al., 2021). Amazon Prime Video and Netflix are extremely active in the content market and deal with hundreds of suppliers worldwide. As often, the power asymmetry between a few lead firms and their suppliers creates governance issues. Streaming is an important new market for film and TV producers, but global streamers are far and few between and their deep pockets make them the most powerful actor in the content value chain. Grievances from producers include squeezed margins, staggered payment systems and poor visibility on the platforms (Nicolaou and Rennison, 2019). In the UK, a House of Commons committee was told that Amazon Prime Video did not always clearly label some of the BBC content (Digital, Culture, Media and Sport Committee, 2021: 28). In addition, streamers keep ratings data to themselves and do not share them with producers (Turton and Opie, 2019).

AVoD services as multi-sided platforms

AVoD services are multi-sided platforms because they bring multiple markets together, which mutually benefit ‘from interacting through a common platform’ (Rochet and Tirole, 2003: 990). The video game market provides a case in point, with game publishers and gamers interacting through a console, just as debit cards bring together merchants and consumers (Rochet and Tirole, 2003; Rysman, 2009). In both instances, these sides are interdependent and need one another to grow. The success of a platform depends on its ability to expand both sides of the market, requiring investment and strategy (Cusumano et al., 2019: 65–104; Gawer, 2009: 57–58). Network effects are in full force with multi-sided markets. Video game publishers need access to a large market to amortize their investment, while gamers purchase consoles with a substantial choice of games. Merchants select cards that are commonly used, while consumers want their card to be accepted in a large range of outlets. It is no coincidence that the aforementioned sectors are quasi-duopolistic markets, with two platforms dominating each (PlayStation and Xbox; Visa and Mastercard).

AVoD platforms’ business model is predicated on bringing together viewers and advertisers. This principle is not new and AVoD services were preceded by the 19th-century newspaper and the 20th-century broadcasting station. Newspapers have always relied on advertising income, but late 19th-century press magnates were the first to transform the newspaper content in order to build mass audiences and establish a correlation between the price of ad space and the number of readers (Chalaby, 1997; Curran and Seaton, 2018: 33–41). Today, when an AVoD platform acquires or produces content, it sells it as inventory to advertisers. No commercial transaction occurs between rights holders and viewers or between advertisers and viewers. All transactions happen through the platform, which is the sole mediator between parties. However, AVoD services innovate in the way they bring the two markets together. Using streaming’s return path to collect audience data, they optimize the buying of inventory by personalizing advertising and targeting consumers according to a range of criteria such as digital behaviour and location.

Video-sharing services as transaction platforms

Video-sharing websites are the only streaming services that can be considered transactional. Their assets and boundaries are different from other streaming platforms and they ‘exploit and control digitized resources that reside beyond [their] scope’ (Gawer, 2021: 1). Unlike other streaming services, video-sharing websites do not own any content, whose rights remain in the hands of people and organisations which upload it. These platforms curate content through governance rules (Poell et al., 2022: 77–105). For instance, YouTube prohibits pornographic and violent material (including the display of dead bodies), and content that infringes these guidelines is promptly removed (see below). Video-sharing services involve a new set of transactions among digital advertisers, content creators and viewers.

Video-sharing platforms share advertising income with content creators who are paid by the platform according to the number of views and the location they occur: the cost per 1000 impressions charged to advertisers varies strongly from one territory to another. YouTube, for instance, has paid more than US$30 billion to creators, artists and media companies in the last few years (company source). Furthermore, there is the possibility of direct transactions occurring between advertisers and content creators. Advertisers have two key options when partnering with them. Sponsorship arrangements entail the insertion of a logo and/or video in the creator’s content for a fee. Content providers can also become ‘brand ambassadors’ and receive free samples and/or cash in order to advertise products and services (Rundin and Colliander, 2021). Viewers, on their side, can rate and share content, subscribe to channels and sponsor the streamers they have most affinities with. YouTube offers the possibility of paid channel memberships.

Video-sharing websites are distinct from all other types of streaming services because they control assets they do not own, allowing them to monetize content that lies beyond their boundaries. They manage this feat by coordinating a multi-sided market and the transactions that occur among participants from different sides. The contrast is stark with AVoD and SVoD streamers, which are forced to make heavy investment into programming. The leading US media conglomerates are spending an estimated US$134 billion on content in 2023. Walt Disney is leading the pack, investing around US$32 billion on content, followed by Warner Bros. Discovery with a total spent estimated at US$20 billion. Netflix’s budget has remained stable for several years and is set at US$17 billion, (Maglio, 2023).

This section illustrates the importance of analysing the platform economy in context. Production processes and market structures vary across industries, partly explaining why platforms differ from one sector to another. Among streaming services, video-sharing websites are the only ones that match the characteristics of the archetypical digital platform that is analysed (and sometimes celebrated) by the literature. These businesses owe their scale and market valuation to the fact that they create value with assets and workers that lie outside their boundaries. In television, it is a model that works well when creators are happy to share content for uncertain rewards or non-monetary reasons. 1 However, it does not apply to professionally made programming. The latter requires investment and once it is produced or acquired, it is legally owned and commercially protected. None of this content finds its way into video-sharing sites. YouTube, for instance, received no less than 722 million copyright infringement claims in the first 6 months of 2021 alone (99.5 per cent of which were undisputed) (Alphabet, 2021: 10).

Neither AVoD nor SVoD services share all the attributes of the super platforms typical of the digital economy. While they are digitally engineered and take advantage of internet connectivity in order to deliver content across borders ‘without necessarily locating any physical resources in the country where the service is offered’ (Autio et al., 2021: 5), they remain set, commercially and organizationally, in classic value chain arrangements. Once they have acquired content, no further transactions occur between suppliers, viewers and any other participant. By way of contrast, video-sharing websites are new organizational forms that match the criteria of typical digital platforms. They alone among streaming services shift firm boundaries by controlling assets they do not own and coordinating transactions among multiple participants.

Platform ownership

This section examines the ownership of streaming platforms. Are they predominantly in the hands of tech firms or traditional media and entertainment businesses? The answer will help us assess whether TV platformization is simply a technological evolution to which legacy media companies adapt, or is expanding the perimeter of the industry by allowing tech firms to make inroads in television (Oliver and Picard, 2020).

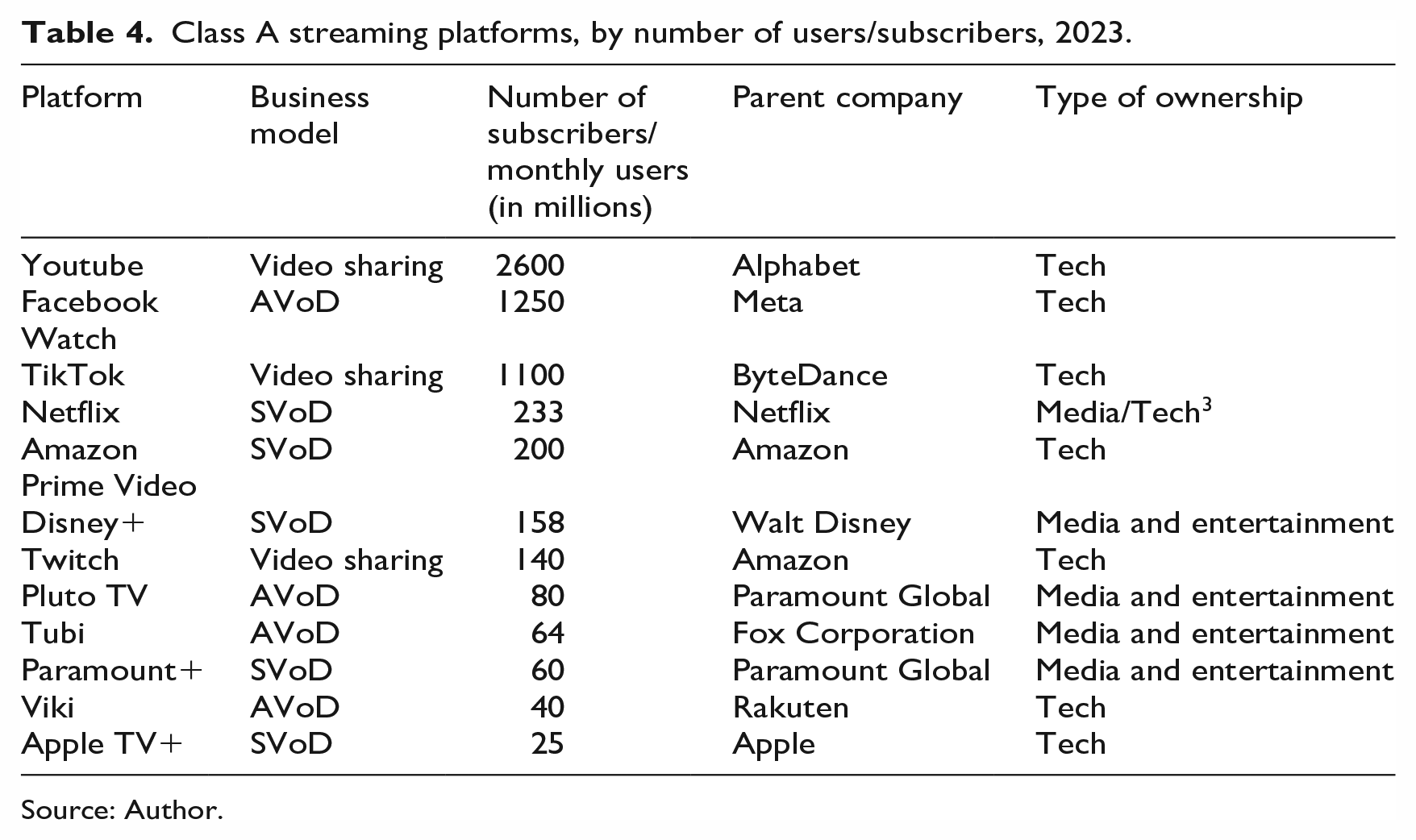

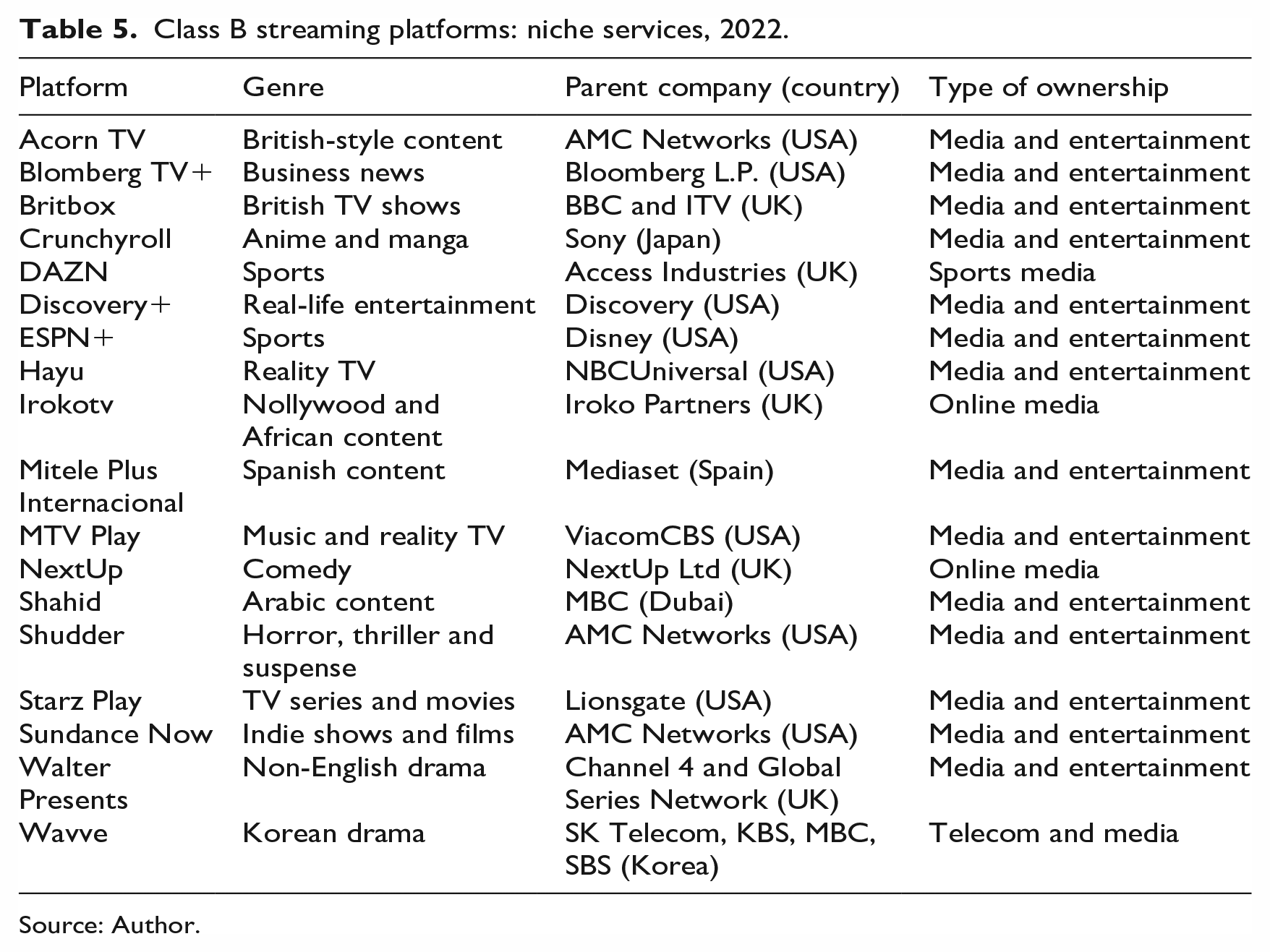

Numerous streaming services operate around the world, around 200 in Western Europe alone (European Audiovisual Observatory, 2017: 19), and close to 50 in North America. In terms of size (revenue and geographical reach), this population can be divided into two classes: A and B. Class A is made of the world’s twelve leading platforms according to the number of subscribers (SVoD), monthly viewers (AVoD) and monthly users (video sharing) (Table 4). 2 Most have a global footprint or are seeking to obtain it rapidly. Class B platforms have either a more restricted geographical span and/or focus on a niche genre (Table 5).

Class A streaming platforms, by number of users/subscribers, 2023.

Source: Author.

Class B streaming platforms: niche services, 2022.

Source: Author.

A difference emerges in the prevalent type of ownership between the two classes: while traditional media and entertainment companies dominate class B ownership, tech firms have carved out a strong presence in class A. Most class-B streaming services belong to legacy media firms such as pay-TV companies or commercial and public service broadcasters. Examples include Walt Disney’s Hulu and NBCUniversal’s Peacock in the USA, and Viaplay in the Nordic territories (Gunnarsson, 2022). Some of the earliest streaming services were established by public broadcasters. In the UK, the BBC and Channel 4 played a pioneering role in streaming delivery and launched their platforms, BBC iPlayer and 4oD, in 2006 and 2007 respectively. However, most public platforms have a limited geographical span, either because of inherent limitations or expansion is not part of their remit (Muñoz Larroa, 2021).

Class A presents evidence that TV platformization is changing the structure of the TV industry and provides an opportunity for tech companies to enter. These firms constitute the second wave of new entrants and were preceded by telcos (telecom companies). AT&T and Comcast in the USA, BT in the UK, Telefónica in Spain and Telia in Sweden are among the telecom companies that have made substantial investments in television in recent times (Oliver and Picard, 2020). Tech firms are further expanding the boundaries of the sector, an evolution not without implications.

The size of tech giants involved in the streaming business far exceeds that of any media and entertainment company. Even after the sharp financial market correction that occurred in 2022, Alphabet, Amazon and Apple’s combined market valuation is 5.9 US$ trillion at the time of writing. There is a profound size asymmetry between these firms and most media and entertainment companies. The scale of tech giants, combined with their cash reserves and access to capital give them unrivalled investment clout. This translates into sizeable content budgets. In addition to Netflix (above), Amazon Prime Video’s 2023 content budget is estimated at US$10 billion, and that of Apple at US$7 billion (Maglio, 2023). Tech giants can also decide to spend unprecedented amounts of money on a single show. Amazon Studios reputedly invested US$465 million on the first season of Lord of the Rings: Rings of Power, after acquiring the rights from the Tolkien estate for an estimated US$250 million (Hibberd, 2021). Two years later, the studio sank US$300 million in Citadel, a six-episode spy-thriller which received a mixed bag of reviews (Armstrong, 2023). In between these two series, Amazon had cash left for further investments and acquired MGM, a Hollywood major, for US$ 8.5 billion in March 2022. While US-based media and entertainment conglomerates might match these sums (see above), they are well out of reach of any European broadcaster.

These firms also own much of the infrastructure necessary for streaming. YouTube rests on Alphabet’s proprietary communications infrastructure, which consists of 21 data centres (including some hyperscalers), 22 cloud regions, 140 points of presence, multiple investments in subsea cable networks and availability in over 200 territories. This is how the video-sharing website enables ‘anyone in the world [to] share a video with everyone in the world’ (Kyncl, 2017: x). The largest cloud infrastructure, however, belongs to AWS, with 26 cloud regions, 84 availability zones, and 410 points of presence across 245 territories.

The literature underlines the symbiotic relationship between infrastructure and platforms (Constantinides et al., 2018; Gawer, 2022; Plantin et al., 2018). Constantinides et al. (2018) observe that platforms sit on top of digital infrastructures, raising the question of ‘how do platforms and infrastructures scale on each other?’ (p. 389). Tech giants can leverage their cloud infrastructure across multiple services and platforms which, together, form a digital enterprise ecosystem (Jacobides et al., 2018; Nambisan et al., 2019); their streaming platforms are constituents of these ecosystems.

Alphabet has nine services with at least one billion users: Android, Chrome, Gmail, Google Drive, Google Maps, Google Play, Google Photos, Google Search and YouTube. All these products run on the same global infrastructure not only concurrently but often in an integrated manner. YouTube, for instance, is connected to Gmail, Google Search and Google Maps. This ecosystem enables Alphabet to generate both economies of scale (adding new users to existing services) and scope (adding new services to the existing infrastructure).

Amazon Prime Video’s underlying technology is provided by AWS, the cloud provider that the parent company developed for its e-commerce platform. Amazon Prime Video can choose among more than 200 products and services that AWS offers its clients. It uses AWS Elemental MediaTailor to insert personalized commercials, which runs on Amazon DynamoDB, a highly scalable database. Amazon Kinesis and Amazon Elasticsearch Service monitor the quality of the video service and collect streaming data in real time. Video files, live or otherwise, are distributed via AWS’ own CDN, Amazon CloudFront.

This ecosystem delivers strong benefits for the parent company. In terms of costs, Amazon is not only able to spread them among its own platforms but all its AWS clients. In media and entertainment alone, the cloud provider serves more than 5000 companies, covering everything from advertising and gaming to publishing and streaming (Disney+ and Netlix are among its customers) (Chalaby and Plunkett, 2021).

The second advantage is scale and scalability. Scale comes from the size of Amazon’s digital infrastructure. With AWS, Amazon Prime Video can distribute its content to customers across the world. Scalability is the ability to scale up capacity when needed and comes from the elasticity – or upside flexibility – of cloud services. As a result, Amazon Web Services can stream Indian Premier League (cricket) matches, NFL (American football, USA) and Premier League (football, UK) games, live to tens of millions of fans on hundreds of types of TVs and devices.

On the one hand, media and entertainment companies are showing their willingness and ability to adapt by evolving into streaming and developing their own digital services. On the other, internet distribution is changing the perimeters of the industry by opening it up to new entrants. Tech firms have made their presence felt and operate some of the largest platforms. As they work best at scale, tech giants may well hold a determining advantage in the long term.

Television and the platform economy

As television embraces the Internet and adopts streaming, it is entering the digital economy. It is a transition that involves multiple changes, not least the emergence of platforms as an organizational form and method of video distribution; they innovate on multiple counts.

Platforms have updated business models. Like broadcasters, streamers primarily rely on advertising and subscription, but AVoD and SVoD are more convenient and flexible than commercial TV channels and pay-TV subscription. Streamers have also considerably scaled up these models. Not all platforms have reached global coverage, but the underlying commercial and financial dynamics have changed. Streaming is an industry that thrives at scale. Broadcast television was essentially a national industry, while streaming is predominantly international. The cloud is a borderless technology which is at peak efficiency when its infrastructure is leveraged and amortized across borders. Only a few countries – pre-eminently China – have the capacity and political will to stop the Internet at their frontiers. Powerful network effects ensure that a few winners prevail in each monetization model. Entertainment platforms require unprecedented levels of investment and market leadership can only be attained by spending tens of US$ billions on content. This necessitates significant revenue, which can only be achieved with a transnational subscriber base, and access to capital, which requires considerable market capitalization. Tech firms hold an advantage in the long term, having the capital and infrastructure to thrive in a globalized industry. These changes mirror the evolution of the platform economy, restructuring the space of capitalist accumulation by concentrating wealth and power in fewer hands and fewer postcodes (Kenney and Zysman, 2020).

Platforms have also introduced a new genre, user-generated content, which has come to play a significant role in popular culture at large (Allocca, 2018; Burgess and Green, 2018; Kyncl, 2017). Video-sharing websites are far more popular with young audiences than broadcasters’ fare. In advanced markets, such as the UK, young adults spend considerably more time on social media and streaming platforms than linear TV (Ofcom, 2022). Video-sharing services play host to an army of content creators, often struggling in precarious careers and striving to make a living out of their work (Poell et al., 2022). Broadcasters and sports organizations also make extensive use of these platforms to engage with fans and garner interest for their events (Chalaby, 2022).

Entering the digital economy has many implications for the TV industry. It involves a reshuffling of the cards, new methods of production and distribution and new modes of consumption. It does not mean that ‘no rules rules’ as Reed Hastings, Netflix co-founder and CEO, would like us to believe (Hastings and Meyer, 2020). The perimeters of the industry have expanded, traditional media and entertainment groups have to contend with new and powerful competitors, but there is continuity between broadcasting and streaming.

While the ‘gale of creative destruction’ unleashed by digitization is powerful (Schumpeter, 1947: 87), it is not rewriting all the rules of capitalism. Digital platforms change some rules and accept others, they make new laws and abide by old ones. They undoubtedly innovate in the way they capture value but they do so unevenly across sectors. The scope and pace of digital transformation varies across industries precisely because some of the fundamentals of value capture remain stable and differ from one sector to another (Furr et al., 2022).

Prices and types of goods (e.g., rival versus non-rival) influence consumption patterns. Even within the creative industries, platforms are not as dominant in television as they are in gaming (e.g., PlayStation, Xbox) or music (e.g., Spotify) (Poell et al., 2022). Professionally made content, which constitutes the bulk of video consumption, remains produced and distributed in classic supply chain configurations. Rightsholders may develop digitally engineered platforms but they do not match the characteristics of the archetypical super platform.

The platform literature is apt at detecting cross-sectoral trends but tends to over-emphasize change. Its approach is deductive and is based on core concepts that de-historicize and de-contextualise the platform phenomenon. It is a literature that works well in the digital sector but that is less applicable to those for which digitization is a process. The input from GVC theory delivers several benefits. A sector-specific perspective enables us to highlight both change and continuity in the evolution of television. The TV industry is certainly changing fast but the specificity of video production and consumption means that its path to digitization remains distinctive. While some streaming platforms match some of the features of digital platforms, others do not.

Further, the GVC framework enables us to approach platforms in the context of the entire value chain in which they operate. The platform literature and media industry studies invariably focus on lead firms, resulting in a partial and incomplete analysis. The growth and business model of platforms is entirely predicated on outsourcing and the management of complex production networks. An understanding of how streaming platforms operate necessitates the full analysis of these value chains, the mode of governance that prevails in them, and the types of suppliers they involve.