Abstract

The development of an online screen industry, dominated by a few American and Chinese streaming TV services and video-based platforms, triggers critical questions about the commercial and technological dependence of cultural producers within this industry. Drawing on research in media industries and platform studies, this paper develops a conceptual framework to systematically examine this dependence. Pursuing this aim, we propose to shift the focus from specific video platforms or streaming TV services as the starting point of the analysis to the perspective of cultural producers. Through a discussion of current research, we identify four major sources of dependence encountered by cultural producers in the online screen industry: (1) access to data, (2) algorithmic curation, (3) contractual relations, and (4) monetization. While we recognize that there are vital differences between platforms and streaming TV services, we argue that producers throughout the online screen industry face similar challenges in trying to navigate the four sources of dependence. In short, limited access to data and lack of control over content visibility put cultural producers in a fundamentally weak position vis-à-vis tech companies when negotiating contractual relations and terms of monetization.

Keywords

Introduction

Over the past two decades, an online screen industry has emerged, dominated by a few large American and Chinese tech companies. Streaming TV services, 1 operated by Netflix, Amazon, and Apple, have become global producers of audiovisual content (Evens and Donders, 2018; Lobato, 2019; Lotz and Lobato, 2023). While video-sharing platforms, 2 video-heavy social media, and live-streaming platforms have dramatically altered how audiovisual content is created, distributed, and monetized (Burgess and Green, 2018; Cunningham and Craig, 2019; Poell et al., 2021). These developments raise concerns about the dependence of cultural producers in the online screen industry on a handful of companies. This paper develops a conceptual framework to systematically examine this dependence and its socio-political implications.

The question of dependence in cultural production has, so far, especially been raised in relation to platforms. Examining the platformization of cultural production, Nieborg and Poell (2018) have argued that cultural producers are increasingly dependent on the economic models, governance frameworks, and infrastructures of digital platforms. While the notion of dependence has not yet been centrally adopted by TV scholars, producers in the TV and film industry are increasingly tied to the business models, infrastructures, and contractual terms of streaming TV services (Johnson, 2019; Lobato, 2019; Lotz, 2017). Szczepanik (2024) argues that dependency is in fact a vital concept in relation to streaming, noting that such a framework is still lacking. Building on this call to action, this paper will demonstrate that there are crucial correspondences and variations in how dependence takes shape across platforms and streaming services in the online screen industry.

The role of large companies in cultural production has long been a central concern in media and communication research. In the second half of the 20th century, leading theorists famously criticized the industrialization and commercialization of cultural production in modern mass media (Habermas, 1962; Herman and Chomsky, 1988; Horkheimer and Adorno, 1944). This early work especially focused on the standardization of cultural goods and the demise of public debate.

In response to this first wave of critical work, the focus has shifted, from the early 1990s onward, to the impact of commercialization on the diversity and equality of cultural expression and public discourse (Bennett and Entman, 2001; Dahlgren, 1995; Negt and Kluge, 1993). Many of these concerns centered on broadcast television, the audiovisual mass medium par excellence, which both reflects and produces contemporary culture (Fiske, 2010). Critics have questioned whether the economics of the broadcast television industry, driven by the constant need to capture mass audiences and attract advertisers, leave sufficient space for content from diverse backgrounds (Bennett and Entman, 2001; Dahlgren, 1995).

Strikingly, the development of the internet was, initially, seen as a vital counterbalance against a perceived lack of diversity and equality in broadcast television and mass media more generally (Dahlgren, 2005; Jenkins, 2006; Rheingold, 1993). The nature of the internet potentially allows anyone to produce and distribute content. Fast forward two decades, it is clear that today’s online environment is dominated by a few major platforms and streaming services, which have already developed a questionable reputation in terms of how they (fail to) govern content (Gillespie, 2018). Because these platforms and services are hugely influential in the contemporary screen industry, we urgently need to revisit the question of dependence of cultural producers on large companies.

So far, such a comprehensive assessment is missing, as current research has primarily focused on specific industry segments, which have developed around particular business models and distribution infrastructures. There are, for example, in-depth studies on the dependence of creators vis-à-vis specific video-sharing and social media platforms (Caplan and Gillespie, 2020; Cunningham and Craig, 2019; Kaye et al., 2021). And although not centrally using the notion of dependence, there is also insightful work on the position of film and television producers in relation to streaming TV services (Jenner, 2018; Johnson, 2019; Lotz and Lobato, 2023). These distinct fields of research share many concerns regarding commercial influence and economic and infrastructural dependence. At the same time, there is limited insight into how specific sources of dependence work across the online screen industry, as well as how industry segments vary in terms of economic and technological dependence.

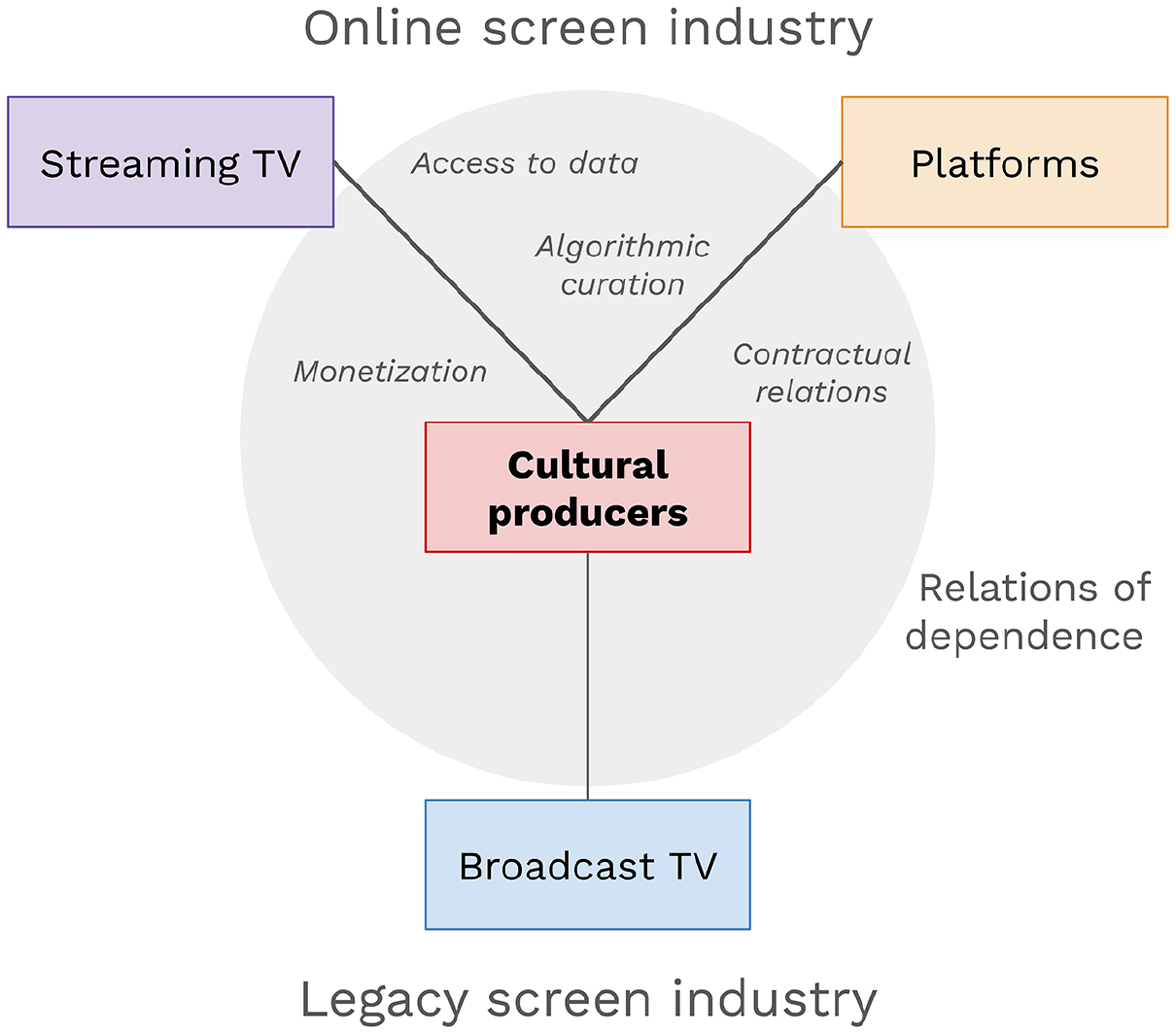

To develop such insights, we propose to analyze the online screen industry from the perspective of cultural producers. Rather than focussing on a particular business model or type of digital infrastructure as other research has done, we examine the key sources of dependence encountered by producers within this industry. As we will discuss, these sources especially revolve around: (1) access to data, (2) algorithmic curation of content, (3) contractual terms set by technology companies, and (4) monetization options available to producers.

From the perspective of cultural producers, it appears increasingly urgent to consider how these sources of dependence work across the online screen industry. For a growing number of producers, the distinction between platforms and streaming TV services is becoming blurred. Beyond platforms serving as promotional tools for films and series, these services are also progressively seen as potential outlets for this type of content. YouTube is, for example, a key distributor for filmmakers and TV producers in India (Mehta, 2020), Nigeria (Simon, 2022: 77–103), and Turkey (Koljonen, 2023: 55). And vice versa, there are many examples of platform creators pursuing parallel careers in broadcast and streaming television (Potvin, 2022). As a recent industry report suggests, there is increasing crossover between different segments of the online screen industry, with many producers experiencing it as one industry (Koljonen, 2023: 53).

In the light of these considerations, the challenge is to simultaneously gain insight into the variety of relations of dependence, as well as into how particular sources of dependence work across the online screen industry. This analysis should be seen against the backdrop of the larger historical shift in which an offline screen industry dominated by national broadcasters is transforming into an online industry dominated by global tech companies. Developing this analysis, the paper draws on scholarship from a number of traditions, including media industries studies, platform studies, and political economy, discussed in the next section. The subsequent sections identify and compare the different sources of dependence that tie cultural producers to streaming TV services and platforms. The aim is to provide a conceptual framework to systematically examine dependence in the online screen industry, understand how these forms of dependence are fundamentally interrelated, and how the development of online services and platforms is changing the political economic position of cultural producers in the screen industry at large.

Current research

Reviewing the scholarship on the online screen industry, it is striking how siloed this research is. The different types of services underpinning this industry have each sparked their own research traditions, which have, so far, not been systematically connected. At the most general level, we can distinguish between research on streaming TV services and research on platforms.

Starting with the former, we observe several core aspects of TV production affected by how tech companies operate these services: business models, intellectual property (IP) rights, performance-based remuneration, and visibility of content. Studies have demonstrated that the business model of the leading streaming TV services has a large impact on production and distribution practices (Lotz, 2017). As Lotz (2017) shows, especially the shift from advertising- to subscription-based revenue is vital. In the subscription model of Netflix and Amazon Prime, the production of original content has become a key differentiator between services, with exclusive IP rights as the cornerstone. This shift from traditional licensing agreements, which allowed producers to retain IP rights, in tandem with a departure from performance-based residuals to buy-out contracts and lump sum payments is a major concern for cultural producers (Cunningham and Craig, 2019: 100; Lacourt et al., 2023: 22; Szczepanik, 2024: 221).

Focusing on the Netherlands, Idiz et al. (2021) find that the lack of IP rights and residuals indeed puts the sustainability of producers’ careers at risk when creating content for Netflix. In turn, interviewing Korean producers, Kim (2022) observes how “selling content to Netflix restricts producers and broadcasters from gaining additional revenues by utilizing the content’s intellectual property” (p. 1517). Holding on to ownership rights and gaining fair remuneration are, as we will discuss, major challenges for cultural producers in negotiations with streaming TV services. Yet, in a few years multinational streamers have become almost unavoidable. These services are able to commission content at a scale national services simply cannot compete with, leading to the notion of “Netflix imperialism” (Davis, 2023). Thus, Kim (2022) raises concerns “over the growing dependence of producers on Netflix’s money” (p. 1516), a power imbalance which renders negotiating better contractual and economic terms extremely difficult.

Given that streaming TV services are generally algorithmically curated, cultural producers are also dependent on these services for the visibility and discoverability of their content (Lobato, 2019: 40; Johnson, 2019: 132–157). Ranaivoson (2019) highlights how recommendation systems are characterized by biases, such as a so-called “presentation bias” through the promotion of exclusive content and through the recommendation of content similar to what users have previously watched. Lobato (2019: 243) stresses that Netflix provides little insight into why particular content gets promoted. Similarly, there is a structural lack of access to performance and viewing data (Navar-Gill, 2020), which producers need for contractual negotiations. Netflix has even been called a “black box when it comes to data” (Idiz et al., 2021: 437). Rasmussen (2024) refers to this as “data secrecy,” arguing that: “insights from viewing data play a vital role in the battle for eyeballs, but this information is kept under lock and key [by streaming services such as Netflix and Amazon] in a way that sustains fundamental power imbalances” (p. 2). This again marks a significant break from the legacy commercial screen industry, in which producers generally had access to such data through third-party data measurement firms such as Nielsen and Barb (Napoli, 2011).

Turning to platform research, scholars observe a similar increase in dependence on tech companies, stemming from: monetization, governance, control over data, algorithmic curation, and moderation. This research shows that platform companies have increased their control over monetization, enhancing the economic dependence of producers. Johnson and Woodcock (2019), for instance, trace how monetization through the game live-streaming platform Twitch has become increasingly embedded within the platform’s infrastructure. The authors identify seven monetization strategies available to live-streamers, in the majority of which Twitch acts as an intermediary and takes a cut of the revenue. This is also observed by Partin (2020) who uses the notion of “platform capture” to describe the process by which platform independent forms of monetization are slowly absorbed. This is especially clear in the case of donations, which originally took place outside Twitch via third parties like PayPal until Twitch introduced “Bits,” a virtual currency (Johnson and Woodcock, 2019; Partin, 2020). This allowed the platform to take 30% of each donation made with Bits (Partin, 2020).

Furthermore, important to note for the present inquiry is that economic opportunities – shaped by platforms’ Terms of Service (ToS) – are by no means equally distributed. Caplan and Gillespie (2020: 7–8) highlight, as an example, the tiered governance structure of YouTube’s Partner Program, in which different tiers give access to different benefits, economic opportunities, and data analytics. Similarly, only TikTok creators with a large enough following are able to directly monetize their content through LIVE (Kaye et al., 2021), and these same creators consequently receive enhanced analytics and strategic insights related to this feature through the “LIVE Center” (TikTok, 2023). Moreover, scholars have argued that the data creators do have access to requires significant labor and learning to make sense of (Beer, 2018; Bishop, 2020; Gray et al., 2018).

There has also been extensive research on the challenges of visibility in algorithmic systems of platform curation. Researchers especially highlight the lack of insight producers are given into these opaque and constantly changing systems (e.g. Duffy and Meisner, 2023; Poell et al., 2021). Moreover, the algorithmic curation and moderation systems of leading platforms do not appear to promote diversity and equality. There is ample evidence of discrimination against people of color and LGBTQ+ creators (Bishop, 2019; Caplan and Gillespie, 2020), as well as of the prominence given to successful and better-resourced creators (Duffy and Meisner, 2023). In the case of YouTube, it appears, for instance, that the incentivization of “ad-friendly” content goes hand-in-hand with algorithmically punishing content (and creators) deemed risky to advertisers (Kumar, 2019).

Taken together, the research on streaming TV services and platforms shows both differences and similarities between segments of the online screen industries in terms of dependence on large tech companies. Yet, we lack a systematic understanding of these sources of dependence and their implications for cultural production.

Our approach

Reviewing current research, it becomes clear there are a number of key sources of dependence that shape the relationships within the online screen industry. These sources concern: (1) limited access to performance and viewing data; (2) lack of control over the algorithmic curation of content; (3) unequal contractual relations; and (4) limited control over monetization. Building on these insights, we develop a cross-disciplinary conceptual framework, as schematized in Figure 1. This framework positions cultural producers at the center, variably tied to different online and offline actors in the screen industry by relations of dependence. In doing so, it should enable a nuanced and comprehensive understanding of these different mechanisms, their interrelations, and impact on cultural producers. Shifting the focus to cultural producers brings to light the inextricable links between the four sources of dependence. Pursuing this analysis, we conceive of cultural producers as “the broad range of actors and organizations engaged in the creation, distribution, marketing, and monetization of symbolic artefacts” (Poell et al., 2021: 9).

Conceptual framework.

Developing this conceptual framework, it is important to see that while the relations between the leading tech companies and cultural producers are highly unequal, there is always space for negotiations (Poell et al., 2021). Across the online screen industry cultural producers frequently resist and contest the economic terms and policies set by TV streaming services and platforms (Petre et al., 2019; Pham, 2022; WGA, 2023a). Moreover, producers continue to find ways to distribute and monetize content beyond leading services and platforms. Simultaneously, we need to acknowledge that the space of negotiations is often limited and not equally available to different types of cultural producers.

In the online screen industry, the spectrum of cultural producers ranges from individual video creators and live-streamers to large television production companies, which employ a number of producers, screenwriters, and other creatives. And, we can distinguish between those who primarily work in legacy media production (film and television) for services like Netflix and Amazon Prime and those who distribute and monetize content through platforms like YouTube, TikTok, Instagram, and Twitch. Thus, we observe many variations between cultural producers in terms of levels of professionalization, organizational embeddedness, types of content creation, forms of revenue, and relations to distributors. As discussed in the following sections, large and successful production companies tend to have better access and more leverage than individual creators, affecting how dependence takes shape within the online screen industry (Caplan and Gillespie, 2020).

Access to data

Access to performance and viewing data is a key source of dependence for cultural producers, as they need it for contractual negotiations, to understand their audiences, and to optimize their content. Historically, the commercial screen industry has worked with third parties such as Nielsen and Barb to gain access to viewing data (Napoli, 2011). This data was initially based on small group sampling, but has become more complex (Kelly, 2019; Napoli, 2011). As Napoli (2011) argues, ratings are “social constructions of media audiences” (p. 3) which evolve and are shaped by technologies and institutions. In the online screen industry, this data is primarily controlled by the streaming services and platforms, rather than third party audience measuring firms, marking a significant shift. Thus, these tech companies have become gatekeepers of valuable data.

The dependence that follows from tech companies’ control over audience data is hard to evade for cultural producers, as these companies also control content distribution and monetization. This is particularly clear in the case of streaming TV services, which gather far more data than their linear counterparts, control all of it, and share little with producers. From sporadic tweets of viewing numbers (Reilly, 2019) to ad hoc insights into the most popular content and viewership (Netflix, n.d., 2023), accessing performance and viewing data from streaming TV services has been a Wild West for producers. Even when such data is released, scholars have argued that, rather than providing transparent or useful information to producers, it likely serves a strategic promotional purpose (Scarlata, 2022; Wayne and Uribe Sandoval, 2021). It has also been found that the data shared by streaming services like Netflix and Amazon is “stratified” (Rasmussen, 2024) or tiered, with different producers provided with different levels of data access. Interviewing 30 European screen workers in 11 countries, Rasmussen found that these individuals had received “snippets of streaming data” ranging from metrics related to specific development issues, to different types of performance figures, to target “taste communities” (Rasmussen, 2024: 9–10). Crucially, the level of data accessed appeared to hinge on the roles and experiences of particular workers, with showrunners often gaining more insights than others (Rasmussen, 2024: 9).

In the last couple of years, there has been a slight resurgence of third-party measurement with Nielsen starting to measure streaming viewership in the US (Koblin, 2021) and Netflix signing up with Barb in the UK (Barb, 2022). However, the geographic scope and methodological reliability of these measurements remain limited. For instance, Nielsen’s streaming data relies on audio-recognition software and does not count content viewed on phones, tablets, or computers (Koblin, 2021), thus missing a significant portion of the viewing on the streaming services. For producers, having limited and uneven access to performance and viewing data weakens their position in terms of contractual negotiations (Cunningham and Craig, 2019: 50; Idiz et al., 2021: 437) and impacts their remuneration, which no longer tends to be performance-based or proportionate to success.

Although access to data on platforms is less restricted than in the case of streaming TV services, it is even more unequal and comes with its own set of barriers. Most platforms provide customized data analytics through dashboards and limited access to general platform data through application programming interfaces (APIs). Moreover, access to data is tiered (Caplan and Gillespie, 2020): those with larger followings generally have access to more analytics. TikTok’s analytics, for example, provides creators with a LIVE account, only accessible for users with +1000 followers, (Kaye et al., 2021: 241), LIVE-specific data, including deeper data-driven insights and tips to improve viewer engagement (TikTok, 2023). Data access in itself is, however, not sufficient. For producers to turn data into useful insights, a high degree of “data infrastructure literacy” is required (Gray et al., 2018: 6). This is where so-called “data intermediaries” (Beer, 2018) or “algorithmic experts” (Bishop, 2020) come in to help producers organize their production, distribution, and monetization strategies on the basis of platform data.

Overall, it is evident that limited access to data and/or limited data literacy undermine the negotiating position of cultural producers vis-a-vis the tech companies that operate the leading TV streaming services and video platforms, and which control both access to vital data and the distribution and monetization of content. Simultaneously, it is also clear that access to data is a source of inequality within the online screen industry, as producers do not all have the same level of access, even when distributing content through the same streaming services or platforms. Large producers tend to have better access to data than individual creators. Consequently, infrastructural dependence and economic power differences go hand in hand. To gain a deeper understanding of these relations, we need to examine the other sources of dependence, particularly: control over the curation of content.

Algorithmic curation

In 1974, Raymond Williams coined the term “flow” to designate the viewer experience of watching broadcast television, characterized by the consumption of multiple programs interspersed with advertisements within a fixed linear schedule (Williams, 1974). Where content discovery used to hinge on what was on at particular times and on particular channels, the nonlinear catalogs of streaming TV and platforms offer viewers an entirely different experience: a choice among a wide variety of content curated through personalized algorithmic recommender systems. In broad terms, recommendation algorithms work by “populat[ing] [home] screens with related content units” (McKelvey and Hunt, 2019: 4). As there are a very large number of content units available, visibility and discoverability is a key challenge for producers in online environments (McKelvey and Hunt, 2019). This raises the question: “what happens when engineers—or their algorithms—become important arbiters of culture?” (Hallinan and Striphas, 2016: 131). And particularly, how does this impact cultural producers?

The algorithmic curation of personalized content is a core function of streaming TV services, which directly affects the ability of producers to distribute and monetize their work, marking another strong break with the legacy screen industry. These algorithms of course are not neutral, nor do they serve a mandate akin to public service media (PSM), which aim to expose consumers to a diverse range of content and promote particular public values. Instead, they prioritize content which matches perceived subscriber preferences and serves commercial interests. For instance, studies of the most popular content on Netflix – which likely correlates to the most recommended – suggest that Netflix Originals from the US dominate (Idiz et al., 2024; Scarlata, 2022).

From an economic perspective, although producers rarely receive performance-based residuals, their success or failure still depends on performance. For example, Netflix tends to cancel series that do not reach target numbers within the first 28 days, pitting producers from smaller markets against the biggest shows in the catalog (Adalian, 2018; Idiz, 2024). Despite the fundamental importance of visibility for content performance, cultural producers are largely kept in the dark about the core visibility mechanisms and have no sense of the prominence given to their content.

Producers for the leading streaming services have sought to change this situation through strikes in Denmark and the US, where viewing data and performance-based remuneration were core issues (Pham, 2022; WGA, 2023a). These strikes prove that negotiations with these powerful entities are possible, though they involve large-scale collective action. The WGA’s new contract addresses streaming data transparency (although what data streamers will exactly share remains to be seen), increases foreign streaming residuals, and establishes a one-time “viewership-based streaming bonus” for hit series (WGA, 2023b). In Denmark, a deal was struck around “success-based remuneration” which extends until late 2024 (Pham, 2022). These efforts are continuous and ongoing, with the most recent actions coming from Directors UK threatening to withhold copyright unless streaming residuals are improved (Goldbart, 2024). As pushback against the leading streaming services spreads across the US and Europe, it also becomes apparent that these actions do not necessarily make the contractual arrangements around monetization and data transparency more equal, with different countries achieving varied results, depending on the negotiations of their respective creative unions (Whittock and Goldbart, 2023).

Similar issues have been observed in the case of platforms which, as often highlighted, also employ algorithms to determine the visibility of content (Bishop, 2019; Caplan and Gillespie, 2020; Cunningham and Craig, 2019; McKelvey and Hunt, 2019). Many forms of revenue – ad-sharing, sponsorship, donations – are, in turn, directly contingent on this visibility. Yet, the inner workings of platform algorithms are both obfuscated from creators and constantly changing (Caplan and Gillespie, 2020; Cunningham and Craig, 2019: 103; Kumar, 2019). In response, creators have developed knowledge sharing practices and made attempts to resist or game the algorithm (Bishop, 2019; Kumar, 2019; Petre et al. 2019), as well as develop cross-platform strategies to decrease their economic dependence (Caplan and Gillespie, 2020: 5).

To understand the impact of algorithmic systems on cultural producers, it is important to attend to the variations between these systems, which affect production practices and content. To illustrate, visibility on Twitch is channel-based, requiring creators to engage significantly with subscribers (Johnson, 2021; Taylor, 2018: 20), while visibility on TikTok is “post-based” (Abidin, 2021), so creators are incentivized to produce viral content. These types of differences shape how relations of dependence between platforms and cultural producers unfold.

In general, platform curation generates inequality, rewarding producers with large followings. Algorithms tend to make the content of already successful and well-resourced cultural producers even more visible, generating winner-take-all dynamics (Poell et al., 2021). Algorithmic curation also presents problematic biases. YouTube’s recommender system and autoplay feature have, for example, been found to discriminate against people of color and LGBTQ+ creators (Bishop, 2019; Caplan and Gillespie, 2020) and promote sensational, conspiratorial, extreme, or graphic content (McKelvey and Hunt, 2019: 4).

In sum, limited control over or insight into algorithmic content curation in combination with lack of data access put cultural producers in a fundamentally weak position vis-à-vis tech companies. This is particularly problematic as they also largely depend on these companies for the monetization of their content. While cultural producers never had full control over visibility or access to data in the legacy screen industry, they generally had recourse to third party data measurement and to performance-based remuneration – both of which are no longer standard in the online screen industry.

Furthermore, algorithmic curation generates strong inequalities between producers, especially in the case of platforms, where already successful producers are rewarded with more visibility. With very large volumes of content being produced and distributed through both platforms and streaming TV services, there are of course always going to be winners and losers in the visibility game. However, it is possible to envision forms of curation which are fairer, providing cultural producers with a more equal chance for visibility. For instance, niche streaming services like MUBI or BFI Player still employ “non-personalized recommendation styles that emphasize ‘human expertise’ and ‘human curation,’ discovery and diversity” (Frey, 2021: 7).

Contractual relations

The weak negotiating position of cultural producers stemming from a lack of data access and a lack of control over curation really comes to light when examining the contractual relations that tie these producers to tech companies. These relations refer to the contracts and terms governing what can and cannot be produced and distributed on the leading streaming services and platforms. To analyze contractual relations, we must distinguish between the hosting versus commissioning model, which impacts the dependence of producers in terms of IP rights or platform terms.

A major difference between contractual arrangements in the legacy and online screen industries is that exclusivity is a cornerstone of streaming TV, meaning that cultural producers are generally left with limited IP rights and residuals (Idiz et al., 2021: 436). Historically, IP ownership was split between various stakeholders (including production partners) and residuals were paid based on performance (Cunningham and Craig, 2019: 100). However, today’s streaming TV services often employ a “work-for-hire model” (Lacourt et al., 2023: 19), which conceives of producers as employees. The crux of the issue is that “once a work is considered one made for hire, the authorship and copyright ownership belong to the employer or the person or entity who commissioned the work” (Lacourt et al., 2023: 20).

As previously discussed, different types of cultural producers have different relations to distributors. In terms of contractual relations, it is worth looking specifically at TV writers, as they have seen a significant shift in their work practices with the arrival of streaming TV services. In the traditional US network model, a low volume of shows was coming out yearly, there were long seasons, and writing was concurrent with production, allowing for training and growth on the job (Vox, 2023). All of this amounted to relative career stability and longevity. Conversely, in the streaming model, there is a much higher volume of shows being made, shorter seasons, and the writing generally happens ahead of production (Vox, 2023). This results in far more precarity for writers, who now need to find multiple projects per year. Where writers in a network model could rely on residual cheques between projects, writers for streamers no longer have this reliable source of continuous income.

To illustrate the precarity of such contractual arrangements, the story of Alex O’Keefe provides a telling example. O’Keefe worked as a writer on Hulu’s massive hit The Bear (2022). Yet, he lived below the poverty line while working on the series (the first season being only 8 episodes long) and received no additional pay once it was released (Thaler, 2023), despite the show’s immense popularity. This is a vital case as The Bear was created by FX (a subsidiary of Disney), but “because it’s streamed on Hulu and Disney+ rather than on a TV network, behind-the-scenes workers like O’Keefe don’t receive any additional paychecks once the show is out” (Thaler, 2023). Thus, even when writers work for legacy media companies, if content is distributed through a streaming TV service, they are contractually impacted. In this model, streaming TV services can also make derivative works without involving or compensating the original creative team. On top of these challenges, producers have to negotiate blindly, as discussed, because they have little insight into content performance, exacerbating the power imbalance between producers and streaming TV services (Cunningham and Craig, 2019: 50; Idiz et al., 2021: 437; Lacourt et al., 2023). Thus, contractual dependence is directly connected to limited data access and lack of control over algorithmic curation.

Contractual relations are significantly different in the case of platforms, which primarily host content and generally do not retain related IP rights (Cunningham and Craig, 2019: 264). Producers’ ownership of IP is evidenced by their ability to upload and monetize videos on different platforms and sell merchandise. Instead, content is governed by terms of service or developer terms set by platforms. These terms engender new forms of economic dependence. In an ad-sharing revenue model like YouTube, platforms unilaterally determine what percentage they share with creators. Although platform companies generate revenue from content in a variety of ways, the creator does not necessarily receive fair compensation. For instance, not all YouTube creators are eligible for the partner program and on Instagram only a “select group” (Instagram Help Center, n.d.) of producers can monetize ads, enhancing the inequality between producers (Caplan and Gillespie, 2020; Cunningham and Craig, 2019).

Platform moderation practices are also especially impactful, as producers are often not given insight into why their content is removed or demonetized. Crucially, such moderation practices tend to affect different types of producers unequally. From interviews with marginalized social media creators, Duffy and Meisner (2023) find that these creators perceive platform moderation as disproportionately punishing creators “outside of the mainstream” (p. 295) and rewarding those within it. Caplan and Gillespie (2020), in turn, maintain that YouTube’s Partner Program effectively constitutes “a system of tiered governance, hinged on rewarding audience size and celebrity, that is more akin to the contractual arrangements of traditional media” (Caplan and Gillespie, 2020: 9).

Thus, while there are notable differences between the hosting model of platforms and the commissioning model of streaming TV services, we observe that producers in both cases find themselves contractually in a weak position, precisely because they lack insight into how their content performs, is curated, and moderated. On platforms, producers can distribute their content through multiple outlets, however each platform brings its own moderation and monetization-related challenges. And on streaming TV services, producers are contractually tied to the streamer, yet they are required to depart from IP rights and residuals, which, in the legacy screen industry, were vital for economic survival.

Monetization

As we have observed in the previous sections, cultural producers across the online screen industry struggle in negotiations over the monetization of their content, as the leading tech companies control key instruments – data and visibility – in such negotiations. While it is clear that cultural producers tend to be in a dependent position, there are important differences in how this affects them economically, depending on the variation in monetization instruments. There is not only substantial variation between the commissioning model of streaming TV services and the hosting model of most online platforms, but the leading platforms in this industry also have different monetization schemes.

Since streaming TV services, like legacy broadcasters, function as gatekeepers, monetization through these services is only available to producers that are commissioned or whose content is acquired. Yet, as described in the previous section, global streaming TV services have departed from traditional remuneration models, preferring buy-out contracts and lump sum payments (Lacourt et al., 2023: 22), which do not compensate producers proportionately to the performance of their content. Evidenced by the writers’ strikes in the US and Denmark, fair remuneration is a central concern for cultural producers working for global streaming TV services (Pham, 2022; WGA, 2023a). Yet, the fact that they lack the fundamental tools to negotiate better economic terms is a marked break from their position in the legacy screen industry. Both The European Producers Club (n.d.) and European Audiovisual Observatory (Lacourt et al., 2023) have emphasized the fundamental importance of producers retaining IP and receiving fair remuneration for a sustainable screen industry.

Cultural producers have far more revenue options on platforms than on streaming TV services. These options include platform-native monetization (i.e. revenue generated via the platform), such as advertising, subscriptions, and gifts/donations. And platform independent options, such as direct donations, selling merchandise, sponsorships, and brand collaborations (Glatt, 2022: 3861; Kaye et al., 2021: 243). Within these broad categories, there are many variations based on different platforms and content types which differently affect creators. Yet, across the board, nearly every form of monetization is contingent on data and visibility. On YouTube, the ad-sharing partner program is only available to creators with a certain number of subscribers and views (YouTube Help, n.d.). On TikTok, creators can only earn revenue during live-streams via donations if they have enough followers (Kaye et al., 2021: 240–241). And on Twitch, creators are only invited to the affiliate subscription program if they meet particular requirements in terms of numbers of followers, hours streamed, and viewers (Twitch, n.d.). As visibility is highly competitive, allocated unevenly, and based on opaque and demonstrably biased curation and moderation systems, creators evidently do not have equal opportunities for success.

Here the link between contractual dependence and monetization is apparent, as success is determined by terms specific to a particular platform. Unlike producers for streaming TV services, platform creators own their IP and can generate income outside of platforms, for instance through brand collaborations (Glatt, 2022: 3861; Kaye et al., 2021: 243). Creators can also reduce their dependence on a platform and diversify their income streams through multi-platform presence (Duffy 2020; Glatt, 2022). To avoid “putting all [their] eggs in one basket” (Glatt, 2022: 3860), creators often release content and engage with their followers on multiple platforms. Though these revenue models theoretically emancipate creators from a specific platform, they are still contingent on visibility and data access, and therefore often only feasible for the most successful creators.

In sum, it is clear that platforms and streaming TV services intensify the winner-take-all market logic already characteristic of commercial broadcast TV. In the online screen industry, we observe stark inequality in terms of economic opportunities for cultural producers, which is intertwined with issues around access to viewing data, curation, and contractual arrangements – all controlled by tech companies. Hence, the inequalities already present in traditional commercial broadcasting appear to grow.

Conclusion

The starting point of this paper was the observation that the online screen industry is dominated by a small number of American and Chinese tech companies. As such, there is a critical shift from a legacy screen industry revolving around national broadcasters to one primarily dominated by global tech companies. This shift raises urgent questions about the dependence of cultural producers on big tech, which potentially has significant consequences for contemporary visual culture.

So far, media scholars have primarily explored these concerns through research on specific segments of the online screen industry, focusing on streaming TV services or particular platforms. Yet, as we have demonstrated in this paper, in dealing with global tech companies, cultural producers are confronted with similar challenges. Developing a cross-disciplinary conceptual framework, we argue that producers throughout the online screen industry are especially tied to tech companies through four key interrelated sources of dependence: (1) limited access to performance and viewing data, (2) little control over visibility, (3) contractual relations, and (4) economic ties.

Although digitization in principle increases opportunities for cultural producers, by making cultural production accessible to everyone, in practice it tends to generate new barriers and intensifies inequalities. In particular, we observe an unprecedented centralization and consolidation of control. In the online screen industry, we see the continuation and intensification of pre-existing concerns about commercial pressure on visual culture. As we have argued, the commercial interests and strategies of tech companies aggravate existing inequalities between producers and content distributors. From this perspective, it is vital to consider the online screen industry as a whole and from the perspective of producers, examining how cultural production occurs within a media landscape shaped by large tech companies.

In the research discussed in this paper, there has been a lot of emphasis on the continuities between streaming TV services and broadcast television, as well as on the differences between these services and digital platforms. While we recognize that the open hosting model of platforms and the closed commissioning model of streaming services lead to different economic relations with cultural producers, especially in terms of IP and monetization, we also observe that producers in both models face challenges around the four identified sources of dependence. This highlights the need to think about dependence from the perspective of producers, considering how they navigate the new online screen industry. By bringing together previously fragmented research, it becomes clear that across this industry limited access to data and a fundamental lack of control over content visibility result in a weak negotiating position of cultural producers vis-à-vis tech companies.

So far, this unequal power relation has especially been highlighted in the case of platforms, but it clearly applies in the case of streaming TV services as well – underscoring the need to employ the concept of dependence in research on streaming TV. Although the commissioning model of these services ensures that cultural producers are paid upfront, they also have to depart from the IP rights and residuals model of broadcast TV. Without the necessary data to gain insights into how their content is performing, they are also not in a strong position to (re-)negotiate their contracts or optimize their content. As such, the rise of global tech companies brings about a shift throughout the screen industry, which can only be observed by looking at the industry as a whole and shifting the analytical focus to producers.

At the same time, producers constantly try to contest, negotiate, and circumvent the economic, contractual, and infrastructural terms set by leading platforms and streaming TV services. There are, however, major differences in how producers are able to do so. On platforms, large and well-resourced producers tend to be more successful than individual creators in gaining access to data, generating visibility, and monetizing their content (Caplan and Gillespie, 2020; Poell et al., 2021). Individual creators certainly try to game platform algorithms and develop cross-platform strategies. Yet, they can’t get around precarious monetization options and unequal moderation practices, which, as research has demonstrated, they find difficult to challenge (Glatt, 2022; Petre et al., 2019). Conversely, TV producers working for streaming services have recourse to public funding and unionized collective action. However, their IP rights and residuals are also very limited, and they have little leverage to negotiate, as they lack access to performance and viewing data and insight into content visibility.

Evidently, these disparate power relations put further pressure on equality in an already highly competitive screen industry, but they also have implications for content diversity. While leading platforms and streaming services guided by their particular business models tend to cater to specific audiences and content niches, it is, simultaneously, in their business interest to reach large audiences and produce and reproduce hits. Furthermore, as platforms and streaming services are becoming more mainstream there is a tendency of cultural producers to avoid risky socio-cultural content to prevent demonetization. Such pressures will need to be considered by future research.

To conclude, we hope that our conceptual framework will encourage researchers to more systematically explore and compare how cultural producers in the online screen industry are coping with limited access to data and control over content curation, as they are trying to negotiate better contractual and economic terms vis-a-vis global tech companies. Our model can be meaningfully used in empirical studies by shifting the focus from specific platforms and services to producers. Taking the latter as the analytical starting point allows us to critically consider how commercial and technological dependence works across the online screen industry. Pursuing such research, we recommend systematically analyzing how the four sources of dependence work in relation to each other. Rather than focusing in isolation on the challenges cultural producers face in gaining visibility for their content, it is vital to study content visibility in relation to data access, contractual relations, and monetization. Pursuing such research should provide further insight into how the limited control of producers over content visibility is related to limited access to data, but especially also how it complicates negotiations over contracts and monetization. To understand how the rise of big tech is reshaping relations of power and dependence in the contemporary screen industry, comprehensive research along these lines is urgently needed.