Abstract

Netflix and other transnational online video streaming services are disrupting long-established arrangements in national television systems around the world. In this paper we analyse how public service media (PSM) organisations (key purveyors of societal goals in broadcasting) are responding to the fast-growing popularity of these new services. Drawing on Philip Napoli’s framework for analysing strategic responses by established media to threats of competitive displacement by new media, we find that the three PSM organisations in our study exhibit commonalities. Their responses have tended to follow a particular evolution starting with different levels of complacency and resistance before settling into more coherent strategies revolving around efforts to differentiate PSM offerings, while also diversifying into activities, primarily across new platforms, that mimic SVoD approaches and probe production collaborations. Beyond these similarities, however, we also find that a range of contextual factors (including path-dependency, the role and status of PSM in each country, the degree of additional government support, cultural factors and market size) help explain nuances in strategic responses between our three cases.

Keywords

Introduction

The arrival of Netflix and other transnational subscriber-funded video-on-demand services (SVoDs) is profoundly impacting national television industries. Rapid uptake of SVoD is changing patterns of viewing, altering industry norms for programme funding and distribution, intensifying the globalisation of TV content, introducing new business models, and challenging national policy regimes (Doyle, 2016; Harvey, 2019; Lobato, 2019; Lotz, 2017; Steemers, 2016; Zboralska and Davis, 2017). Public service media (PSM) organisations like the BBC in the UK, RAI in Italy and VRT in Flanders are among the ‘legacy’ TV players (entities that existed before the internet) that are majorly affected by these developments (Raats and Jensen, 2020). PSM organisations still occupy a central yet challenged position in domestic media landscapes where they still represent the chief mechanism through which national policy-makers pursue important non-economic goals including universal access to high-quality media, range and diversity of content, and the promotion of national culture (Martin and Lowe, 2014).

This national importance also raises questions about how PSM organisations are responding strategically to the popularity of SVoD, particularly as academic analysis has tended to focus on disruptions caused by SVoDs, rather than responses to this disruption. Given these PSM organisations’ distinctive funding regimes, national roots and public service obligations, we would expect their responses to differ from other legacy players, notably commercial broadcasters, pay-TV companies and production companies. In her analysis of multi-platform strategies of PSM, Donders (2019) already described how PSM have increasingly moved towards online distribution, however mainly by providing new outlets for existing content. Much rarer is a clear strategic shift in which online platforms of PSM become the focal point and base for commissioning, producing and distributing content. In the same study, Donders also showed how public media have increasingly legitimized their activities and need to sustain existing levels of public funding because of growing competition with international SVoDs.

Drawing on Philip Napoli’s (1998) framework for analysing strategic responses by established media to threats of competitive displacement by new media, we ask: What strategies have PSM adopted in response to SVoD services across a range of policy, business and creative options, including collaboration with SVoDs? We adopt a comparative approach, focusing on the UK (BBC), Italy (RAI) and a smaller market, Flanders (VRT). We explore how organisational (e.g. level and type of funding) and contextual factors (market size, language, cultural proximity, national policy regimes, viewing habits, industry formations) shape strategic responses in these three cases. The time-frame is 9 years: from mid-2011 (when Netflix announced plans for European expansion – first in the UK and Ireland in January 2012 to mid-2020. 1

In placing the analytical focus on SVoD, we are mindful that SVoD represents only ‘one line of development within a wider ecology’ (Lobato, 2019: 10) of ‘internet-distributed television’ (Lotz, 2017), encompassing wide-ranging services, from video sharing platforms (YouTube), to transactional services (Apple’s iTunes, Google Play); from illegal streaming and download sites to live streaming services. SVoD services, however, represent the largest and most direct threat to established TV (including PSM), because they are proving to be the most popular form of watching ‘TV-like’ content online (Begum and Moyser, 2018). This is driven by ‘a strongly curated and programmed TV-like experience’ (Wang and Lobato, 2019: 4), where programmes are ‘produced in accord with professionalized, industrial practices of the television industry’ (Lotz et al., 2018: 36) and with heavy investment in ‘original’ programming (Westcott, 2019). The growing role these US platforms are playing as investors in North American and European productions places them in direct competition for rights and on- and off-screen talent with traditional broadcasters and commissioners.

The core of SVoD disruption can be expected on those ‘types of television markedly improved by the non-linear affordance of Internet distribution’ (Lotz, 2017: 17), such as scripted TV series. Data supplied by Media & Technology Digest shows that despite recently moving into unscripted series Netflix (currently the leading SVoD player globally, except in some markets, notably China) still places a major emphasis on TV fiction (Westcott, 2019), with 44% of its original hours in 2018 attributed to this genre. As will be discussed below, drama is also a core component of BBC, RAI and VRT output accounting for a significant proportion of their investment in original programming, as part of their public service remit to support domestic screen industries and promote national culture.

The paper is organised as follows. Part 2 conceptualises Netflix and SVoD as disruptive forces before moving on to introduce Philip Napoli’s framework for analysing organisational responses to disruptive media shifts. Part 3 justifies the choice of PSM case-studies. Organised around Napoli’s analytical categories, Part 4 presents the case-study analysis. In conclusion, we offer a comparative analysis of the impact of contextual factors on PSM responses to SVoD in our three case studies.

Analytical framework

At first sight Netflix represents the biggest threat to legacy television as a pioneering disruptor, innovator, and transnational challenger to long-established institutional, market and regulatory arrangements. Thus, the first step in building an analytical framework is to consider what makes Netflix (and SVoD more generally) distinctive and disruptive vis-a-vis legacy television services.

Amanda Lotz (2017: 4, 2018) identifies the following distinctive features of Netflix and other SVoD services that have emerged in its wake as ‘studio portals’: (1) ‘Non-linearity’, or the delivery of on-demand, ‘personally-selected content from an industrially curated library’; (2) Pure subscriber funding; (3) The adoption of targeting strategies based around ‘taste communities’, made possible by collecting viewing behaviour data generated by algorithmic filtering and recommendation; (4) Vertical integration involving exclusive control of a content library where Netflix operates as content producer and distributor through direct-to-consumer streaming.

Lotz is at pains to stress that none of these features on their own are unique. Vertical integration has long been a prominent strategy in the media business (Evens and Donders, 2018); there are also historical precedents of television purely funded through subscription; niche targeting is not new either, though what is new is the depth and granularity of consumer data available to SVoD companies (Jenkins, 2016); finally, ancillary technologies for viewing (VCRs, DVD players, DVRs) as well as pay-per-view services on pay-TV have long made non-linear viewing possible, although these viewing forms remained peripheral before the Internet (Johnson, 2019). It is the combination of these features into a single business proposition that makes Netflix (and SVoD more generally) a new and disruptive phenomenon. The seeming strong transnational character of Netflix (and, to a lesser extent, of other multi-territory SVoDs) and the availability of significant amounts of investment capital (Evens and Donders, 2018), can be added to the mix of ingredients that make SVoD a powerful business proposition (Lobato, 2019).

While not competing for revenue, SVoDs compete directly with PSM for viewers’ attention with claims about quality, eating particularly into PSM’s young audiences (Ofcom, 2019a). Another threat from SVoD is that their push into high-end, big-budget original programming has led to significant cost inflation for TV drama. Although this represents a problem for PSM operating with much smaller (and often shrinking) budgets, it also offers opportunities. If they own the rights, PSMs can license their content to Netflix and other SVoDs, creating new revenue streams in secondary windows (Steemers, 2016). Co-producing with SVoDs is also an opportunity to the extent that it allows PSM to scale up production budgets. These potential benefits, however, must be weighed against potential risks, including: cannibalisation of PSM’s own channels and services; ‘brand dilution’, whereby PSM’s financial and creative contribution to a show is concealed by Netflix branding it as a ‘Netflix Original’ (Wayne, 2018); the risk of PSM organisations (as minority partners) having to concede control over key creative decisions, and commercial pressures inherent in co-productions that prioritise globally appealing TV series, which contradict PSM remits to serve national communities. Finally, some public broadcasters are losing out on licensing deals for imported drama because distributors are privileging lucrative worldwide deals with large players like Netflix over deals secured on a territory-by-territory basis.

Having set out what is new and disruptive about Netflix and SVoD services, the next step is to consider what strategic responses are theoretically available to PSM as they adjust to new scenarios. For this purpose, Philip Napoli’s (1998) typology is especially useful as a framework grounded in economic and historical perspectives, situated within broader theories of media evolution (Lehman-Wilzig and Cohen-Avigdor, 2004). Napoli identifies four recurring organizational responses by legacy players to competitive threats from new media technologies. These responses are not mutually exclusive and can occur at different stages. They include:

(1) Complacency: Obliviousness to competitive threats posed by new technologies, especially in the early stages.

(2) Resistance: Efforts by legacy players to preserve the status quo, including legal (lobbying efforts, lawsuits), rhetorical (advertising campaigns) and economic (denying new challengers access to resources such as content rights) means.

(3) Differentiation: Efforts by established media to alter their content in ways that distinguish them from rivals including reallocating resources towards content not reflected in the drama-skewed offerings of SVoD services. This may extend to efforts at a discursive/rhetorical level to positively differentiate PSM from new media players through persuasive ‘political case-making’ (Picard, 2012).

(4) Diversification/Mimicry: Diversification refers to efforts by established media organizations to expand their activities across new platforms. To these four response patterns, Napoli adds a fifth identified by other media evolution scholars as ‘mimicry’ (Lehman-Wilzig and Cohen-Avigdor, 2004). As mimicry is closely related to diversification, that is expanding into new activities, we deal with both responses together, although mimicry can also be seen as ‘the flip side to differentiation’ because it involves attempts by incumbents ‘to adopt or simulate one or more of the key [technical] characteristics of the new, threatening medium’ (Mierzejewska et al., 2017: 21).

Expanding Napoli’s analytical framework, we also argue that ‘strategic collaborations’ as part of a ‘partnership agenda’ (Raats, 2019) with SVoDs provide a further strategic, but potentially risky response, particularly in relation to original drama, which underpins most SVoD marketing.

Case selection

Previous research on the impact of online streaming services tends to adopt either a general or US-centric perspective (Evens and Donders, 2018; Jenner, 2018; Lobato, 2019) or a single case-study approach, with the BBC by far the most studied case (Johnson, 2019). Yet, comparative research on audiovisual markets shows how different context-specific factors shape different responses in national markets (Raats et al., 2016). This suggests that contextual factors do have an impact on how different PSM reposition themselves towards video streaming. These factors include: historically-rooted national differences in the relative importance of different forms of distribution (e.g. cable vs free-to-air terrestrial television); levels of political support for PSM, whether or not they are adequately funded, and how much they rely on commercial revenues; differences in the extent of government support for national production; cultural factors (most importantly, language); and, last but not least, differences in market size. Market size and language also impact the production value and potential export capabilities of audiovisual content, thus also affecting positioning strategies of public broadcasters with regard to scripted television.

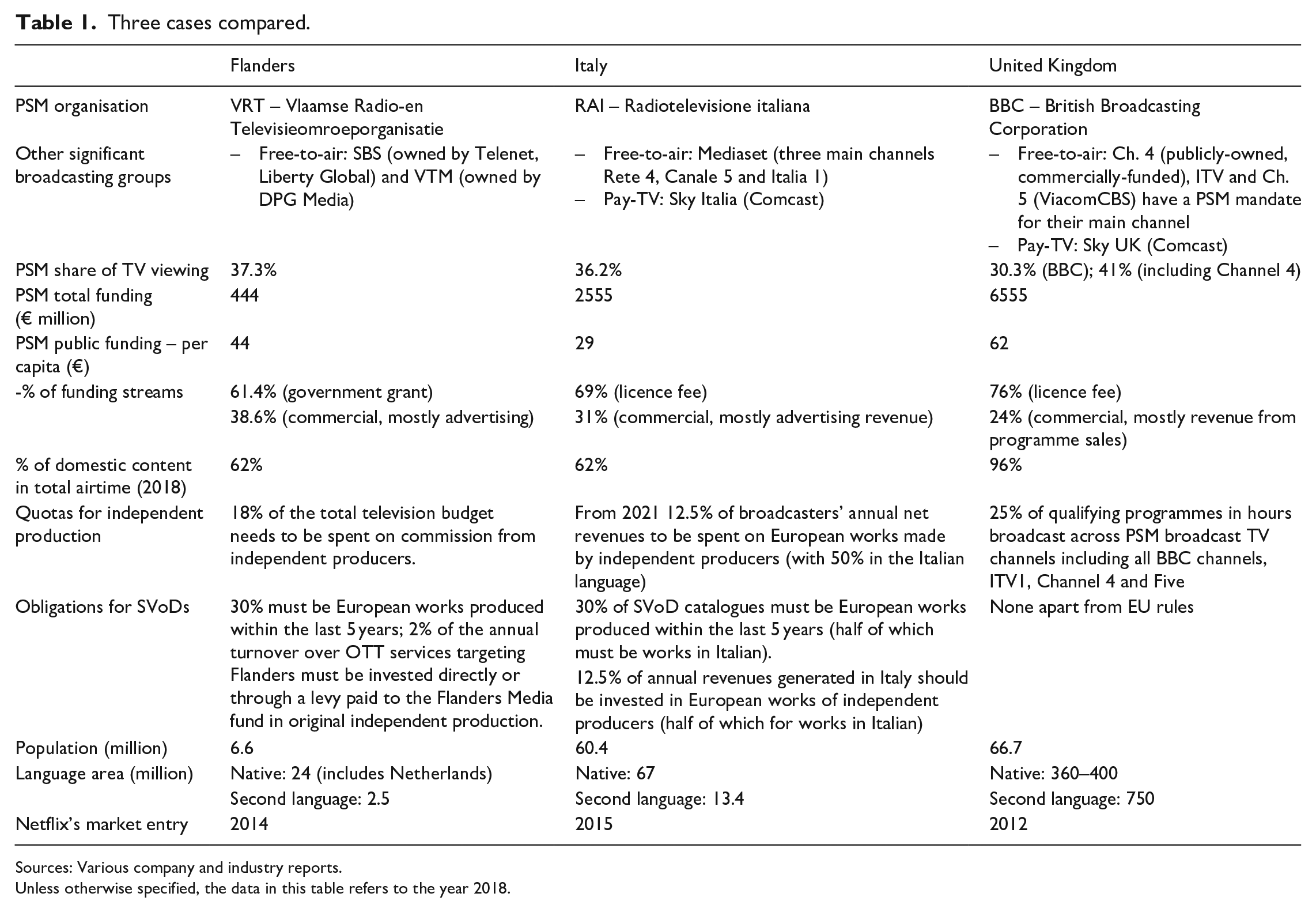

We have therefore selected three cases for this study – Italy (RAI), UK (BBC) and Flanders (VRT) 2 – that display clear differences on each of the aforementioned factors (see Table 1). VRT serves a relatively small domestic market, and only theoretically a larger language market, as content is mainly produced for a Flemish audience, and only few programmes are picked up in the Netherlands. Not only does the BBC serve the largest language area; the cultural proximity with the USA and English being the ‘language of advantage’ also allow it to distribute its content on a wider scale. RAI operates in a high-volume market and mainly produces content for domestic audiences although an increasing number of series are being picked up or produced solely for global SVoDs. However, there are also commonalities that are important to take into account when comparing PSM strategies: first, all three still account for a considerable national viewing share (over 30%); second, they all operate online streaming platforms; finally, all three play a key role in sustaining national drama production.

Three cases compared.

Sources: Various company and industry reports.

Unless otherwise specified, the data in this table refers to the year 2018.

Analysis

Complacency

Applying Napoli’s framework to PSM’s strategic responses to SVoD needs to account for the different scale and timing of responses. In the UK the BBC and Channel 4 cannot be accused of initial complacency as the launch of the BBC’s iPlayer (July 2007) and Channel 4’s 4oD player (November 2006) predate Netflix’s launch. Indeed, Netflix Chief Content Officer, Ted Sarandos, acknowledged its debt to the BBC for demonstrating video-on-demand’s viability well ahead of Netflix’ own launch (Kanter, 2016). In Italy, RAI launched online video portal, Rai.TV, operated by RAI Net in 2007, but online streaming was not seen as a strategic priority until after Netflix’s Italian launch in 2015. In 2016 Rai.TV was relaunched as RaiPlay. The platform was redesigned in 2019, and now features some original content, either produced specifically for RaiPlay or acquired for exclusive distribution (Visalli, 2019). In Flanders, VRT postponed launching online platform VRT NU until a new management contract was agreed with the government in 2016; since 2008 politicians and commercial broadcasters had pushed (unsuccessfully) for a joint venture instead. In both Italy and Flanders, the resilience of linear viewing, especially among older audiences, disincentivized PSMs for a long time from regarding online distribution as a prime way of reaching viewers. As recently as 2017, linear viewing was estimated to account for 92% of TV viewing in Italy – the highest proportion among the five largest European markets (Begum and Moyser, 2018).

Even in the UK where online streaming began early, complacency may be evident in the BBC’s failure to engage sufficiently with young and minority audiences (Ofcom, 2019a). Complacency can also be detected most strikingly in earlier regulatory interventions constraining broadcaster strategies, notably the Competition Commission’s 2009 decision to block commercial SVoD Service, Kangaroo, a joint initiative between BBC commercial subsidiary, BBC Worldwide, ITV and Channel 4, on the grounds that this posed a competitive threat to Pay TV operators, rather than recognising the future strength of transnational SVoDs. For the BBC this approach to a ‘hypothetical’ (BBC, 2019) competitive threat continues with regulators and policy-makers taking too ‘narrow’ a view of the UK market (BBC, 2019: 2; Channel 4, 2019: 2) that focuses on PSM impact on UK commercial players like Sky, rather than global SVoDs who ‘threaten the discoverability and viability of PSM content’, thereby inhibiting PSM’s ability to ‘keep pace with the market’ (BBC, 2019: 14). Similarly, in Flanders, regulatory short-sightedness is as much in evidence as strategic obliviousness by PSMs. After 2010 the policy debate rhetorically paved the way for a ‘partnership agenda’ with global SVoD while simultaneously presenting SVoD as common adversaries, yet none of this rhetoric resulted in fundamental long-term solutions.

Resistance

The PSM in this study have not sought to counter SVoD by denying Netflix and other SVoD services access to content produced or commissioned by PSM – resistance by economic means in Napoli’s conceptual parlance (more on which below). Instead PSM resistance strategies are more evident in policy lobbying. In the UK, prominence, competition rules, advertising, taxation, content regulation, PSM terms of trade with independent production companies, and production quotas are all issues on which the BBC and other PSMs are mounting resistance (Clementi, 2019). However, although UK PSMs point to the lack of regulatory restrictions on SVoDs and video sharing platforms, they and a 2019 report by the House of Lords Select Committee on Communications have not called for financial levies on overseas SVoDs (House of Lords, 2019: 42–43). Resistance is, however, visible in calls to extend regulation on PSM prominence from access to the 5 public service broadcasting (PSB) channels (BBC1, 2; ITV1; Channel 4; Five) on Electronic Programme Guides for linear TV to prominent access on on-demand services through user interfaces including those activated by voice-search (BBC, 2019: 19–20; Channel 4, 2019: 22). This is motivated by concerns that global companies and manufacturers who control devices and interfaces could undermine future PSM discoverability and availability by prioritizing their own services or those which have paid for prominence (Channel 4, 2019: 17). For the BBC resistance has traditionally occurred through robust defence of the licence fee, regarded as ‘risk capital for the British creative sector’ (BBC, 2019: 18). At the time of writing, this was set against several obstacles including a battle with the Conservative government about the BBC’s decision to remove free licence fees for the over-75s, a Government consultation in 2020 about decriminalising licence fee payments, a mid-term review of BBC governance in 2022, and growing hostility to the licence fee in favour of subscription within government circles. The BBC’s resistance is also evident in its request to Ofcom to increase the time programming rights are made available on the BBC iPlayer from 30 days to 1 year, seen as ‘absolutely vital’ (BBC, 2019: 2–3) if it is to have the ‘space to adapt and innovate to meet new global challenges’ (BBC, 2019: 4). This was greenlit by Ofcom in August 2019, followed by an agreement with producers’ association, Pact, in May 2020, which reduced the BBC’s backend revenue share on programmes produced by independent producers.

In Italy, in recent years, broadcasters, including RAI, have directed their lobbying against the introduction of stricter European/domestic content rules for broadcasters, a measure adopted by the former centre-left government in 2016 and reversed by the next (more nationalistic-oriented) right-leaning government. To the extent that European content quotas for legacy players have been lowered, while increasing the quotas for national content and tightening quotas and ‘prominence’ obligations for on-demand providers, the broadcasters’ lobbying efforts can be said to have been at least partly effective.

In Flanders, VRT, broadcasters and producers have mounted resistance by demanding an extension of production investment obligations to on-demand players based outside of Flanders (Econopolis/SMIT, 2017). Building on the European Union’s new Audiovisual Media Services Directive which allows member states to impose additional measures, since 2019 Netflix and other SVoDs are now obliged to contribute 2% of their Flemish turnover to local content production (Donders et al., 2018).

Differentiation

At a discursive/rhetorical level PSM seek to differentiate themselves from online streaming services by emphasizing their distinctive features as national public service providers. The key differentiator for PSM is universality and free access. Differentiation, however, also depends on how much support and flexibility PSM are afforded within national regulatory and policy environments, which not only maintain adequate funding and independence, but extend to other measures such as updating regulation on digital distribution as screen media become less linear.

Distinctiveness is supposed to be reflected in PSM services which US SVoDs, apart from landmark drama, do not currently provide. In our three cases, these include provision of accurate and impartial news, coverage of national issues and events, and commissioning practices that reflect issues in different communities and the diverse people that live in them (BBC 2019: 6; Channel 4, 2019: 6–7; House of Lords, 2019: 3).

Defence through differentiation is grounded on the principles of regulated plurality, universality and discoverability (Channel 4, 2019: 2), but extends increasingly to location, with the BBC promising to spend half its origination budget and base half its staff outside London (BBC, 2019: 3) and C4 moving its headquarters to Leeds in northern England (Channel 4, 2019: 13). However, it is more difficult to differentiate PSM if SVoDs and Pay TV operators also claim public service credentials through their quality content, investment and training initiatives (Netflix, 2019; Sky, 2019: 19), particularly in the realm of drama.

A commitment to investing in domestic drama is supposed to be a key differentiator for the PSMs in this case study, with drama strongly associated with local content, cultural identity and diversity, which in turn underpins the legitimacy of public funding from licence fees (UK, Italy), government grants (Flanders), and indirect production support from subsidies (e.g. the Flanders Audiovisual Fund’s Media Fund) and tax credits. In spite of PSM public statements about being dwarfed financially by US SVoD players like Netflix, BBC, RAI and VRT remain by far the largest investors in domestic fiction in their respective markets. VRT is the biggest producer and commissioner of scripted TV in Flanders, participating in eight out of 13 scripted series (including soaps and web series) aired in 2018. In 2019, VRT channels broadcast 12 out of 23 scripted television series (based on second author’s own data).

Similarly, in Italy, RAI is by far the largest originator of TV drama. Its output in the 2018/19 season, both in terms of hours and titles, accounted for over 75% of Italy’s total TV fiction in that season (APA, 2019). In its 2016 annual report, RAI claimed that its financial contribution to drama production amounted to more than 70% of total investment (RAI, 2017: 6). The ten most-watched titles in the 2018/19 season were all aired on RAI1, RAI’s flagship channel (APA, 2019). RAI’s strategy of investing in productions that tell stories about Italian contemporary reality or draw on Italian history and cultural heritage (in contrast with overseas content on streaming platforms) is strongly emphasized in RAI’s official pronouncements when it stresses its role in narrating ‘contemporary and historical Italy, in fostering Italian talent and industry, and in supporting innovation and the circulation of Italian productions in other countries’ (RAI, 2019: 73).

The UK presents a similar picture. As part of a strategy of differentiation, UK PSM can point to spend on first-run originations (BBC £1.19 billion in 2019) (Ofcom, 2020a: 47), which are spent largely on content for domestic audiences. Although SVoDs do invest substantial amounts in UK content they contribute only a small proportion of total hours. In 2019 only 299 hours in the UK Netflix catalogue were UK made (Ofcom, 2020a: 81) compared to over 31,500 first-run UK originated hours by UK public service broadcasters (PSBs), BBC, ITV, C4, and Five (Ofcom, 2020a: 49), although these are likely to be high-spend productions. In 2019 Netflix and Amazon Prime added 152 and 12 hours respectively of UK originated content to their UK catalogues (Ofcom, 2020a: 82). According to UK PSMs, the impact of SVoDs therefore needs to be viewed and understood ‘in the round [. . .] not just through the prism of landmark TV dramas’ (BBC, 2019: 23).

Mimicry

In three respects PSM strategies suggest mimicry. Firstly, while PSM online platforms predate Netflix’s entry, PSMs have updated the design and functions of these platforms, introducing features first adopted by Netflix such as personalised recommendations, ‘box-sets’ for binge-viewing, horizontal scrolling lists, and ‘micro-generic’ labels (‘great writers’, ‘women’s tales’). In Italy, the relaunch of RAI.net as RaiPlay in 2016 (and a further revamp in 2019) saw the adoption of graphical interface features typical of Netflix and other streaming services, and the implementation of mandatory registration as part of a new data strategy (Visalli, 2019). In the UK, too, mimicry is evident in attempts by the BBC to upgrade the iPlayer from a catch-up service to a destination with online accounts that allow personalised recommendations (BBC, 2019: 4, 13). In Flanders, VRT has altered the online interface and user modalities on VRT Nu to allow continued viewing where the user stopped last time, thematic and genre-based ways of finding content, and customized personal profiles which keep track of earlier viewing (see vrt.be/vrtnu). In the UK BBC attempts to extend windows on iPlayer from 30 days to 1 year resulted in tensions with independent producers, the underlying rights owners who want fair remuneration, a conflict which was only resolved with producers association Pact in May 2020.

A second feature of mimicry occurs through collaborations between national players to establish online subscription services or ‘local Netflixes’. In Flanders private broadcaster DPG Media promoted the idea of a ‘Flemish Netflix’ as part of a common adversary rhetoric to ensure that the Flemish government continued to maintain production support mechanisms (Raats et al., 2019). In advocating for a Flemish Netflix, similar to ventures in the UK (Britbox), France (Salto) and the Netherlands (NLZiet), little account is taken of the Flemish market’s small size and the difficulty of recouping investment. While VRT’s former CEO Paul Lembrechts was initially enthusiastic about what he called a ‘necessary’ collaboration (Bonneure, 2018), VRT eventually shied away from those plans in 2019 because the return-on-investment was too low and a subscriber-funded platform would have contradicted VRT’s obligations to make its content universally accessible on all platforms at no additional cost (De Tijd, 2019).

In the UK, the BBC overcame any qualms about universal access by working through its commercial subsidiary, BBC Studios. In 2017 together with commercial broadcaster ITV, BBC Studios established a North American subscription-based SVoD, Britbox. A UK version of the service was launched in late 2019. According to some commentators, these distribution-led strategies may not be sufficient to attract and retain audiences that are more used to Netflix, and there may be issues in securing rights as PSMs do not necessarily own them (McVay, cit. in Westminster Media Forum, 2019: 47). Current collaborations also include a deal between the BBC and Discovery to launch a global natural history SVoD outside of the UK (BBC, 2019: 16), representing a continuation of earlier collaborations with Discovery (Steemers, 2004).

In Italy, unlike in Flanders and in the UK, the idea that RAI should join forces with other ‘legacy’ players in the domestic market to run a streaming platform drawing on their respective libraries and funded through subscription has been floated but never seriously considered. A possible explanation is the historic rivalry between RAI and Mediaset, the private TV broadcaster controlled by the Berlusconi family. Also, Mediaset was an early mover into the SVoD space, launching its own subscription-based streaming service, focused on movies in 2013 (Infinity).

PSM strategic focus on high-budget drama with global appeal could be understood as a third form of mimicry. At VRT, a decision to only focus on exportable ‘Netflix-worthy’ drama has not occurred because most of VRT’s midweek dramas, soaps and children’s fiction appeal to Flemish audiences only. Yet producers and broadcasters do acknowledge that Netflix has raised viewers’ expectations about domestic content, with calls for ‘bolder’ and ‘more edgy’ themes and storytelling. Producers who pitch scripted projects to VRT also take more account of potential international appeal (Econopolis/SMIT, 2017; Raats and Jensen, 2020).

In the larger Italian market, RAI has sought collaborations with major US players, as part of a recent strategy to build its international reputation for high-end, high-budget TV drama ‘revolving around the symbolic force of Italian culture, history and literature’ (RAI, 2018: 30). Perhaps the most prominent example of such efforts has been My Brilliant Friend [2018], a co-production with HBO (HBO’s first ever non-English language series) (Edwards, 2020). In 2018, RAI was estimated to have invested roughly one-third of its €200 million annual drama budget in high-end TV series (Vivarelli, 2019). As part of this strategy, in 2017 RAI also entered an alliance (The Alliance) with European PSM France Télévisions and Germany’s ZDF to co-produce a range of English-language ‘high-end programmes’ with international appeal, an initiative explicitly framed as an anti-Netflix move (Vivarelli, 2018). At time of writing, the partnership had five projects in various stages of development (Vivarelli, 2020). While RAI’s high-end TV drama strategy marks a significant break with the past, RAI continues to be mainly a volume producer of lower-budget, more conventional fare targeting primarily domestic audiences. It is also the case that in Italy, pay-TV operator Sky Italia has been the real game changer, investing in bolder, ‘cinematic’-style original series from 2008, long before Netflix’s arrival (Edwards, 2020). Sky Italy’s original programming includes crime drama Gomorrah [2014], the most successful Italian TV series overseas. RAI’s move into high-end TV drama production can thus be seen as a response to Sky’s earlier ground-breaking strategy.

With increasing pressure on funding, all UK PSBs, but particularly the BBC, have sought out strategic collaborations that help production, including with US Pay TV operator HBO which co-produced the Philip Pullman adaptation, His Dark Materials in 2019 with the BBC. Co-productions have long been a common form of collaboration between UK PSBs and overseas partners in the form of pre-buys on a territory basis that leaves domestic rights free. UK players have rarely collaborated with European partners, and most partnerships have historically been concentrated in the US, mostly dating back to the 1970s, initially with PBS (Public Broadcasting Service) and later with commercial partners such as HBO, AMC and Starz (Steemers, 2004). These partnerships have continued and include The Night Manager [2016], a coproduction between the BBC, AMC and the Ink Factory, and Victoria [2016-] an ITV commission from Mammoth Screen, showcased on PBS’ Masterpiece strand, like many UK historical dramas before it.

Collaboration

As the section above has shown, our case studies all have a history of international co-production before the arrival of Netflix, however limited in the case of Flanders. PSM collaborations with SVoD adversaries, Netflix and Amazon, are undertaken for similar reasons. Collaborations enable PSMs to build scale and increase production budgets. However, as our three cases show, they also create tensions with PSM remits. And in countries like the UK, where the politics of ‘distinctiveness’ has been used by PSB opponents as a weapon to curtail the scope of PSM (see D’Arma, 2018; Goddard, 2017), collaborations with SVoDs, which seemingly run against ‘distinctiveness’, could be used instrumentally to undermine the political case for PSM.

Notwithstanding these potential tensions and risks, two main forms of collaboration are evident. The first involves distribution where PSMs, if they have the underlying rights, sell licenses to Netflix and others. The second occurs at the level of production, where PSMs function as co-production partners and participate in co-financing.

In the case of RAI, both forms of collaboration are in evidence, although at time of writing there has only been one (though prominent) co-production for what was Netflix’s first Italian-language original series, crime drama Suburra: Blood on Rome [2017], focusing on corruption and politics in present-day Rome. Netflix was the major partner in the co-production, keeping first-run rights to the series in Italy. The series was aired on RAI’s second channel 2 years after first airing on Netflix with disappointing ratings, raising questions about what value RAI was getting from the deal (IlPost, 2019). As for the second form of collaboration (licensing), RAI has licensed drama series and other content to both subscription and transactional online services, including Netflix. The most significant deal in recent years was with Amazon in 2018 to which RAI licensed the local second-run rights for a large catalogue of programming, including some of its more popular drama series.

Following the sale of VRT/Skyline’s critically acclaimed 2012 crime drama Salamander to BBC Four in 2013, a steady number of Flemish thrillers and crime dramas commissioned by VRT have been sold internationally, including crime drama Professor T [2015-18] which was remade in France and Germany. Since then, Netflix has licensed VRT content either directly through VRT’s own distribution arm or indirectly through independent producers, for which VRT receives some recoupment. Notable sales of VRT commissions to Netflix include: De Mensen’s Tytgat Chocolat [2017], a drama about people with Down’s Syndrome; De Mensen’s Hotel Beau Sejour [2017], a supernatural crime drama, which aired on Netflix in March 2017; Caviar’s psychological thriller Tabula Rasa [2017]; and Sylvester’s Sense of Tumor [2018], which aired on Netflix in April 2019. Some series are – depending on the number of territories sold to – presented as ‘Netflix originals’, despite the fact that Netflix only acquired them after production.

Like RAI, so far VRT has only co-produced one series with Netflix, the 2018 high concept thriller Undercover, together with the commercial subsidiary of German PSM, ZDF Enterprises, the Belgian telco Proximus, and Dutch producer Dutch Filmworks. Collaboration with Netflix was initiated by independent production company De Mensen, although the series was commissioned by VRT. In recent years, VRT has actively pursued co-financing and co-production opportunities, in order to generate a return on its drama investments. This more ‘proactive’ role has increased tensions with the Flemish Independent Film & Television Producers Association (VOFTP), demanding that VRT ‘backs down’ from initiating international sales and co-production deals which they believe should be the preserve of producers (Raats et al., 2019: 95). For independent producers as well as broadcasters, co-financing and co-production are seen as key to sustaining Flemish drama and recouping some investment, following years of producing 100% domestically (Raats and Jensen, 2020).

UK distributors, including BBC Worldwide (now BBC Studios) saw the benefits of selling to SVoDs early on as a boost to international sales, while also recognising tensions with the national orientations of UK broadcasting, and the risks arising from shifting sales in multiple territories to a smaller number of global platform buyers (Steemers, 2016: 734). By 2015, half of UK distributors were earning at least 10 percent of revenues from digital rights, including sales to Netflix and Amazon, with BBC Worldwide (26%) accounting for more (Broadcast, 2015: 14). However, a recurring problem for drama is that UK PSMs, the motor of drama commissioning in terms of both spend and hours, are commissioning less, with PSB hours for first-run UK drama originations almost halving from 627 hours in 2008 to 382 hours in 2019 (Ofcom, 2020b). Drama funding has almost halved from £524m to £291m in 2019 (Ofcom, 2020b). As a test of collaboration third-party drama spend on PSB drama commissions had risen to £311 million by 2018, when last figures were available (Ofcom, 2019b: 55), plugging the funding gap through deficit funding by producers, co-productions and tax credits.

As a co-producer, Netflix highlights its role in the UK as an investor who is ‘fundamentally collaborative and additive’ (Netflix, 2019: 2) working with the BBC in high profile independent drama commissions Dracula [2019] and Giri/Haj [2019]. Mostly these collaborations are producer-led. Yet this system poses a risk if global SVoDs seek to take all global rights in a property in a cost-plus system which closes down additional forms of rights exploitation (Doyle, 2016; Steemers, 2016). Longer term there is also a risk that PSMs with diminished funding will be cut out of some future commissions entirely if they are no longer deemed necessary partners by SVoDs, who want to fully fund productions, or by producers, who are happy to relinquish income from future sales (BBC, 2019: 12, 16; House of Lords, 2019: 39). The BBC sees a risk from a decline in collaborations, if it is not provided with the financial support from the licence fee ‘to invest in the UK talent pipeline and in the production and distribution of high-quality UK public service content to deliver the public purposes’ (BBC, 2019: 16). Although UK drama costs had risen to £1.5-£2 million an hour in 2018, PSMs’ share has barely increased since 2016 at £771,000 (Ofcom, 2019b: 58). Data compiled by the BFI shows that PSM co-productions with Netflix declined from 6 in 2017 to 1 in 2018, before rising to 4 in 2019 (Keen, 2019: 17). Amazon had co-produced 4 in 2018. Just like in Flanders and Italy, collaboration also raises issues of attribution (BBC, 2019: 16; Channel 4, 2019: 16), where SVoDs fail to fully attribute partners, by branding broadcaster coproduction or acquisition deals as Netflix originals outside the UK (Channel 4, 2019: 17).

Discussion and conclusion

This study has shown that all PSMs in this sample exhibit commonalities in their responses, which accord with Napoli’s framework. However, there are also clear differences which provide scope for comparison. Different strategies are contingent on national contexts and PSM repositioning is shaped as much by policy and regulatory priorities at the time, as by the arrival of Netflix. What is also clear is that most responses have tended to follow a particular evolution starting with different levels of complacency and resistance before settling into more coherent strategies revolving around efforts to differentiate PSM offerings, while also diversifying into new activities, primarily across new platforms, that mimic SVoD approaches and probe production collaborations, particularly in drama. PSM responses do not always occur in a linear way and different strategies can co-exist at the same time, often in contradictory ways. So, although all PSM in this sample exhibit some degree of resistance, usually through lobbying to protect their market position (e.g. on prominence, rights, quotas) they all simultaneously seek international sales and production collaborations with SVoD rivals.

From this analysis, however, we have identified path-dependency, the role and status of PSM in each country, the degree of additional government support or regulatory measures, cultural factors and market size as the key factors in explaining nuances in strategic responses between these three cases.

Path-dependency rooted in historical tradition plays out in policy and decision-making, determining levels of complacency or more active responses. For example, historical preferences for a particular technological carrier such as cable (Belgium), or free-to-air distribution (Italy) has impacted online access to PSM content and later strategic choices. This was the case in Italy where RAI was slow to develop its on-demand services, because free-to-air reception has been so dominant. It was also evident in Flanders, whose hesitancy was in part shaped by cable providers who redistribute VRT’s Flemish content. The BBC was an outlier in developing online streaming services comparatively early, but lobbying by commercial rivals and producers concerned about rights remuneration, meant it has been slower to capitalize on an early start.

The role and position of PSM in each country has also played a part in shaping responses. The degree to which PSM can demonstrate ‘distinctiveness’ which reinforces their role and position in national markets depends on the extent of political support, adequate funding, and the degree to which PSM depends on commercial revenues, including advertising (e.g. RAI) and programme sales (e.g. BBC). Typically, comparatively well-funded organizations with lower levels of commercial revenue, for example NRK in Norway, have been more resistant to partnerships with market players (Enli et al., 2019). Others, for example the BBC with a large commercial subsidiary BBC Studios (formerly BBC Worldwide), charged with increasing commercial revenues, have historically been more open to commercial collaborations and investment (Donders and Van den Bulck, 2016), as evidenced by the BBC’s collaborations with SVoDs, building on earlier production collaborations. Distinctiveness is also determined increasingly by whether and how much public broadcasters are required to commission productions externally, and the extent to which they can participate in rights exploitation. One might expect different strategic considerations for an in-house production, marketed by a PSM sales team than for a PSM external commission. In Flanders, for instance, most fiction is commissioned from independent producers who are mostly in charge of negotiating deals with the streaming services.

The ability to differentiate or diversify content and services may also depend on additional government support or regulatory measures designed to support domestic production. For example in Italy and Flanders, resistance by PSM and other legacy broadcasters has resulted in local investment obligations for overseas-based streaming players, but this has not happened in the UK, where production tax credits have been the preferred policy tool for enticing SVoD production to the UK. Indirectly PSM may be encouraged to differentiate through terms of trade frameworks, which underpin rights retention by independent producers. These allow producers to use a PSM commission as a mark of quality to garner interest from SVoDs either as a presale or co-production. This has been evident in the UK.

From this analysis cultural factors have also been key in determining responses, particularly around production collaborations with SVoDs. Cultural proximity (Straubhaar, 1991), particularly in relation to language, is an important factor in the cross-border circulation of content, affecting the potential to co-produce or export (Jensen et al., 2016). For example, the UK has benefited from English, the ‘language of advantage’ (Collins, 1989) in its off-screen and on-screen collaborations with the US, both historically in the broadcast and cable market (Steemers, 2004), and more recently with streaming services (Navarro and Prado, 2019). This has been less evident in Flanders and Italy, where producers, sometimes through PSM sales subsidiaries have managed to sell drama to SVoDs, but have only had limited experience of SVoD co-production.

Most significantly market size has been a key factor in shaping responses, because size influences the financial risks broadcasters are willing to take on. Smaller markets, such as Flanders, typically have limited potential to generate return-on-investment through advertising or subscription revenues. Consequently, they have smaller budgets for local drama (Lowe and Nissen, 2011), which in turn impacts their ability to secure the interest of SVoDs who demand ‘high-end’ productions. Even if Netflix occasionally buys a Flemish drama, it is less attracted to Flanders as a co-production partner because of the lack of scale and language, whatever tax benefits may be available. These obstacles can be partly overcome in small markets by PSM strategies built on developing scale, as was the case with drama from Denmark (Raats and Jensen, 2020), combined with government support measures (e.g. tax credits that attract investors), but in the absence of these initiatives, the possibilities of collaboration are more limited.

Many of the PSM responses outlined here can be characterized as pragmatism to unfolding developments, ranging from short-term ‘resistance’ (e.g., Flemish and Italian demands for investment obligations on Netflix) to involvement in co-productions, which are rare but increasing in Italy and Flanders. This type of collaboration, as we have indicated, poses risks to the future viability of PSM, if they become the minority partner and are marginalised out of high quality drama which sustains PSM distinctiveness as contributors to national culture. Longer term responses relate to continuing efforts to differentiate PSM from its rivals (crucial for public legitimacy and public funding) and the mimicry involved in slowly turning around a broadcast model to more personalised on-demand forms of engagement, although the policy, funding, audiences and discovery mechanisms to sustain these remain unanswered in all three case studies.