Abstract

Prior research suggests that firm-specific human capital is important in enabling board chairs to effectively lead their boards in their oversight duties. Despite this, some boards appoint newcomer directors to the chair position. This paper seeks to explain why. Building on power circulation and faultline theories, we posit that boards characterized by strongly divided subgroups with none dominant over the board may have difficulty in agreeing on promoting a director from among their ranks to the chair position, and instead select a board newcomer as a compromise solution. We further argue that this will be moderated by factors that affect either the power dynamics or the degree of contestation on the board. Analyses on a sample of 2,199 board chair appointments at S&P 1500 firms between the years 2001 and 2017 support our hypotheses.

Keywords

A board chair’s responsibility is to lead the board in providing guidance to and oversight of management, while also managing directors and the overall functioning of the board (Banerjee, Nordqvist, & Hellerstedt, 2020). The selection of a chair is thus an important consideration for a board, which must select an individual who has the requisite human and social capital to carry out these duties (Krause, Semadeni, & Withers, 2016b). A key element of such capital is knowledge about the inner workings of the firm. Indeed, firm-specific human and social capital enable a chair to better monitor management and to ensure that directors serve in their roles effectively (Bezemer, Nicholson, & Pugliese, 2018; Langan, Krause, & Menz, 2023). As such, individuals appointed as chair typically have considerable knowledge and experience within the firm; according to Spencer Stuart (2024), independent chairs of S&P 500 firms have on average 7.3 years board tenure prior to being promoted to the chair position.

Some boards, however, elect recently appointed, newcomer directors to serve as chair. Indeed, Spencer Stuart (2024) noted that 13% of independent board chairs in S&P 500 firms are board newcomers. Given the importance of firm-specific human and social capital in executing the role of chair, it is unclear why some boards appoint a newcomer to serve as their chair. Such an individual may know little about the firm’s operations and routines, making it more difficult to discern good management decisions from bad ones. A newcomer chair may also know very little about how the board functions and what the strengths and weaknesses of the directors are, making it more difficult to lead them effectively. In short, why a board would select a newcomer director over an incumbent director to serve as chair is not immediately clear.

The answer may lie in examining the power dynamics within the board. According to power circulation theory (Ocasio, 1994; Ocasio & Kim, 1999), board subgroups continually vie for power over the firm, with the most powerful subgroup at a given time holding the most influence and thus the leadership positions. This would suggest that at any given time, if a board chair is to be appointed, the dominant subgroup will control the appointment and, likely, appoint one of their existing members. However, a crucial assumption of this theory is that there is a dominant subgroup; the theory does not consider the case in which no subgroup dominates. In the absence of a dominant subgroup, board subgroups would need to come to an agreement regarding whom among them to promote to the chair position, and thus which subgroup to elevate through leadership. Yet, the literature on board faultlines finds that, when differences between subgroups are stronger, they have more difficulty in finding consensus and ultimately agreeing on decisions (Shin & You, 2023; Tuggle, Schnatterly, & Johnson, 2010). Hence, when no subgroup is dominant and differences between board subgroups are stronger, selecting a chair from one of the existing subgroups may prove highly difficult.

We argue that it is in these instances that a newcomer chair is likely to be appointed, as a newcomer will hold fewer loyalties to any existing subgroup, making them a viable compromise solution that avoids tipping the scales in any subgroup’s favor. Following this logic, we further suggest that other sources of power and contestation on a board will moderate this effect. We argue that CEO power may do so, as a powerful CEO may be able to break the impasse and influence decisions toward their own ends. We also argue that firm performance may strengthen contestation, because strong performance provides the opportunity for contests of boardroom power to dominate directors’ decision-making, while weak performance may deter subgroups from wanting to take power for fears of being blamed and scapegoated. Analyzing a sample of 2,199 board chair appointments at S&P 1500 firms between 2001 and 2017, we find support for these predictions.

Our study makes several contributions. First, our study provides some answers as to why a board would appoint an individual with little firm-specific knowledge and experience to the chair position. While ample research highlights the importance of firm-specific human and social capital in leading the board in its duties (e.g., Baysinger & Hoskisson, 1990; Langan et al., 2023; Zorn, Shropshire, Martin, Combs, & Ketchen, 2017), there are other considerations that can drive chair selection. Our study finds that power dynamics play an important role, underlining the challenges boards face in ensuring healthy functioning and the compromises they may be willing to make for such a purpose. Second, our research fills an existing theoretical gap regarding power circulation on a board. While existing theory suggests that the leadership of the firm will be held by the dominant subgroup (Ocasio, 1994; Ocasio & Kim, 1999; Zhang & Greve, 2019), it remains underdeveloped regarding cases when contestation is strong but no subgroup is dominant. Our study addresses this theoretical gap by demonstrating that, in such a case, the leadership of the firm may reflect a compromise solution among the subgroups. Finally, our study contributes to research on the choice and suitability of the individual who holds the board chair position (Garg, Li, & Shaw, 2018, 2019; Krause et al., 2016b). We explain how the chair’s origin can be an important selection criterion. In doing so, our study also distinguishes more finely the various types of non-CEO board chairs (Krause, 2017; Langan et al., 2023), offering a clearer picture of what drives variance in corporate governance practices across firms.

Theory and Hypotheses

Power Circulation Theory and Board Leadership

Research has shown that board chairs play a highly influential and complex role, which involves guiding the firm’s strategy, representing the firm to stakeholders, and managing director interactions (Banerjee et al., 2020). The board chair has structural power among directors (Finkelstein, 1992) and often works closely with the CEO in setting firm strategy (Krause, 2017; Langan et al., 2023). The chair also interacts with the firm’s stakeholders, influencing how the board and the firm as a whole are represented externally (Lorsch & Zelleke, 2005). As leader of the board, the chair determines committee memberships and sets agenda items, thereby influencing director participation and overall board priorities (Bezemer et al., 2018; Hoppmann, Naegele, & Girod, 2019; Krause, Withers, & Waller, 2024; Veltrop, Bezemer, Nicholson, & Pugliese, 2021). Accordingly, the board chair has strong influence over firm outcomes and performance (Withers & Fitza, 2017). Such influence may be desirable to any director or coalition of directors seeking to influence a firm’s direction, resulting in a competition for the position.

Power circulation theory posits that board subgroups regularly vie for power over the firm (Ocasio, 1994; Ocasio & Kim, 1999). The subgroup with the most power will hold the most influence over the board and assert its preferences on important firm decisions, such as who will hold the CEO position (Ocasio, 1994; Shen & Cannella, 2002b; You, Shin, & Chung, 2023), which firm(s) to acquire (Zhang & Greve, 2019), or how to change firm strategy (Levinthal & Pham, 2024). According to this theory, as the dominant subgroup’s power weakens, contestation from competing subgroups will eventually overthrow it and a new subgroup will assert its authority (Levinthal & Pham, 2024; Ocasio, 1994; Ocasio & Kim, 1999).

Ocasio and Kim (1999: 533-534) write: “At any one point, one individual and function will gain control over the firm’s political coalition. . . . Which individuals and groups are in positions of authority over the dominant coalition over the long run is inherently unstable.” An assumption of their model is that at any given time, there is always a dominant subgroup. However, there may be times when no subgroup is sufficiently dominant to unilaterally wield authority over the board. Rather, as is the case in many other political environments, there may be several competing subgroups of comparable power that must compromise on certain issues in order to come to a decision. However, such compromise can be difficult to achieve when subgroups are more strongly opposed.

According to faultline theory (Lau & Murnighan, 1998), the degree to which competing subgroups differ will determine how difficult it is for them to find consensus or agreement on decisions. These differences between subgroups are referred to as faultlines and are most often captured over demographic attributes, which are often the basis of similarity attraction and perceived shared values (Lau & Murnighan, 2005; Thatcher & Patel, 2012). At the board level, research has found that stronger demographic faultlines on boards can be related to lower board effectiveness as perceived by board members and represented in financial performance (Veltrop, Hermes, Postma, & de Haan, 2015). Strong demographic faultlines can negatively impact innovation strategy decisions (Zhang & Ma, 2022), as well as board advice and guidance activities (Crucke & Knockaert, 2016). They can also result in weaker CEO turnover-performance sensitivity (Shin & You, 2023; Vandebeek, Voordeckers, Huybrechts, & Lambrechts, 2021).

In short, directors on a board may split into subgroups with strong differences between them. At times, no subgroup may be sufficiently powerful to dominate the board. In such a case, a board may find it particularly difficult to find consensus and ultimately reach decisions. We argue that this may be the case when the board selects a new chair.

Opposing Demographic Subgroups and Board Chair Selection

Given the significance of the role, selecting a chair is an important consideration for a board. Most boards elect their chairs from among the ranks of established members, directors with several years of service on the board who have accumulated extensive firm-specific human and social capital (Krause et al., 2016b; Spencer Stuart, 2024). While there are substantial benefits to human and social capital of this kind (Baysinger & Hoskisson, 1990; Becker, 1962; Harris & Helfat, 1997; Zhang, 2008; Zorn et al., 2017), appointing an established board member to the chair position on a heavily divided board likely involves choosing a representative from one subgroup over another (Ocasio, 1994; Ocasio & Kim, 1999). Such a board will likely have difficulty arriving at consensus about which subgroup’s membership should be represented in the chair role (Lau & Murnighan, 2005; Westphal & Milton, 2000).

In such a case, a board newcomer may become a more acceptable option. A newcomer would hold fewer loyalties to any existing board subgroup. While a newcomer may have similar attributes to directors of one of the existing subgroups, the issue is not the demographic characteristics themselves, but rather the pre-existing subgroups that have built up over time based on these differences. Indeed, time is required for faultlines to become salient and for members to become entrenched in their subgroups (Lau & Murnighan, 1998). A newcomer to the board does not come from any of the existing subgroups, regardless of that individual’s specific demographic attributes.

Recent high-profile board chair appointments suggest that such compromises may be a common solution to board divisions. For instance, when Elon Musk was ordered to step down as board chair of Tesla in 2018, some argued that Tesla should recruit a new director to serve as chair, given that the board of Tesla was divided and selecting an individual from one of the existing subgroups might prove controversial. A newcomer, they argued, would come with “no baggage” and act as a truly independent third party (Stoll, 2018). Of course, Elon Musk retained strong control over a dominant coalition on the board, and the board chose an incumbent director and Musk loyalist for the chair position (Trentmann & Minaya, 2018).

The Tesla example highlights an important caveat on the prediction that divided boards will seek out a newcomer as a compromise chair candidate. This is only likely to occur if the subgroups divided by demographic faultlines on the board are relatively equal in their power. When faultlines between demographic subgroups are strong and no subgroup is particularly powerful, no group will be able to assert its wishes, and subgroups will instead need to find a compromise solution (Krause, Withers, & Semadeni, 2017). In such a case, the appointment of a newcomer director to serve as chair should be more likely.

Whereas power circulation theory generally holds that one coalition will hold power at a time and direct decision-making until toppled (Ocasio, 1994; Ocasio & Kim, 1999), we argue that equally matched subgroups can maintain an impasse, and this impasse will be reflected in compromise board decisions. In contrast, when faultlines between demographic subgroups are strong but one subgroup holds comparatively more power to dominate board decision-making, the dominant subgroup is likely to elevate an established board member from its side of the divide to the board chair position. In short, we posit that a newcomer board chair appointment should be more likely when divisions between demographic subgroups are stronger and no subgroup dominates the board.

Hypothesis 1: The more a board of directors is characterized by strong demographic faultlines and subgroup non-dominance, the more likely it is to appoint a board newcomer as chair.

Following this logic, factors that may affect the power dynamics or the degree of contestation on a board may moderate this hypothesized relationship. First, in considering the power dynamics on the board, if there is another powerful party with their own set of interests, they may be able to influence the board’s choice of chair, and thus the likelihood of a newcomer chair being appointed. As described by power circulation theory, the greater the power of the CEO, the greater their ability to influence outcomes of board subgroup contestations (Shen & Cannella, 2002a). We thus expect that the likelihood of a newcomer chair appointment should be moderated by the degree of power the CEO holds (Combs, Ketchen, Perryman, & Donahue, 2007).

Second, in considering the degree of contestation, power circulation theory posits that firm performance plays a key role in how contestation between board subgroups plays out (Ocasio, 1994). According to faultline theory (Lau & Murnighan, 1998), for the differences between subgroups to be of consequence, they need to be salient to directors and of relevance to their interactions and ultimate objectives. Firm performance is particularly salient to directors, given their responsibility to steward shareholders’ interests (Fama & Jensen, 1983). We thus expect that the likelihood of a newcomer chair appointment should be moderated by firm performance. Below we discuss each of these two factors and how they may affect the likelihood of a strongly divided board with no dominant subgroup to appoint a newcomer as chair.

A Powerful CEO as Another Dominant Force

While board dynamics and decision-making may be largely influenced by the interactions between board subgroups, the CEO also plays an important role (Combs et al., 2007). A CEO typically serves as a director but is often the only executive to do so (Spencer Stuart, 2024). As such, and given that they report to the board and influence the information the board receives (Boivie, Bednar, Aguilera, & Andrus, 2016), the CEO’s role on the board is fundamentally different from that of non-executive directors. This means that a CEO holds a unique type of influence over board dynamics that can affect decisions and outcomes. Key to this influence is the degree of individual power the CEO holds.

Research demonstrates that when a CEO holds little power, they have less influence over the board and its decisions (Krause et al., 2017). The result is lower discretion over strategic decisions (Quigley & Hambrick, 2012), less protection from challenges from other executives within the firm (Shen & Cannella, 2002a; Zhang, 2006), and an overall greater likelihood of dismissal (Fredrickson, Hambrick, & Baumrin, 1988). Powerful CEOs, on the other hand, can have strong influence over board decisions (Ozgen, Mooney, & Zhou, 2025). They can influence who is appointed to the board (Westphal & Zajac, 1995), how the board processes information (e.g., Boivie et al., 2016; Coles, Daniel, & Naveen, 2014), and even how the board evaluates the CEO’s future with the organization (Goyal & Park, 2002; Ocasio, 1994; You et al., 2023).

In the context of chair selection, CEO power should play an important role. A CEO with relatively low power should be less able to sway a decision in any direction, with the result that a divided board with no dominant subgroup may be more likely to remain at an impasse and resort to appointing a newcomer chair as a compromise solution. A powerful CEO, on the other hand, contending with a divided board with no dominant subgroup, should be in a strong position to drive decision-making themselves (Cannella & Shen, 2001; Combs et al., 2007), which could be the deciding factor when strongly opposed demographic subgroups find themselves unable to reach consensus regarding who should become chair.

Hence, a powerful CEO may be able to exert their influence over the board and tip the scales toward their preference. Such preferences are more likely to be for either the CEO themselves to take the chair position or for one of their allies to do so (Westphal & Zajac, 1995; You et al., 2023). Recruiting a board newcomer, with whom the CEO has less association, to become chair would be the riskier choice of the three, as the degree of commitment and partiality the newcomer holds toward the CEO would be comparatively lower (Quigley, Hambrick, Misangyi, & Rizzi, 2019; Zorn, DeGhetto, Ketchen, & Combs, 2020). In sum, CEO power should reduce the likelihood that a board newcomer is selected to serve as chair.

Hypothesis 2: The combined effect of board demographic faultline strength and subgroup non-dominance on newcomer board chair appointment is weaker when the CEO is more powerful.

Firm Performance and Subgroup Contestation

Firm performance is highly salient to a board of directors because a board’s main responsibility is to protect the financial health of the firm (Fama & Jensen, 1983). Power circulation theory posits that poor firm performance often precipitates contestation and thus the circulation of power, as it indicates that the dominant subgroup has become obsolete, weakening its hold over the board and firm (Ocasio, 1994). However, in the absence of a dominant subgroup ruling the board, poor firm performance is unlikely to increase contestation for power among evenly matched subgroups, as no specific subgroup can be blamed for the firm’s performance shortcomings. Unlike when the dominant subgroup is overthrown and scapegoated for the firm’s poor performance (Gamson & Scotch, 1964; Shen & Cho, 2005), evenly matched subgroups may prefer to avoid taking the reins of the board during poor performance for fears that they are blamed and subsequently ousted. Indeed, prior research demonstrates that directors prefer to depart a board when the firm is struggling rather than seek a leadership position on it (Boivie, Graffin, & Pollock, 2012). Hence, when performance is poor and no subgroup dominates the board, contestation between subgroups for the chair position may be comparatively lower, reducing the need to elect a newcomer chair as a compromise solution.

When firm performance is positive, on the other hand, there may be increased interest in competing for board dominance, given the success and prestige that can be enjoyed from leading a high-performing firm (e.g., Acharya & Pollock, 2013; Masulis & Mobbs, 2014). Unlike poor performance, positive firm performance also provides firm leaders with the capital to invest in strategic innovations and opportunities (Bourgeois, 1981), increasing the attractiveness of reigning over the firm. Taking over a well-performing firm may also allow the subgroup to entrench itself as the dominant one (Ocasio, 1994; Ocasio & Kim, 1999). Positive firm performance may thus offer fertile ground for subgroups with strong demographic differences to compete for power over the board and firm, increasing the salience of their differences. As competition increases among subgroups of comparable power, consensus over whom to appoint as chair should be more difficult to achieve, and a compromise solution of appointing a board newcomer as chair may increasingly become the only acceptable consensus option.

Hypothesis 3: The combined effect of board demographic faultline strength and subgroup non-dominance on newcomer board chair appointment is stronger when firm performance is higher.

Methods

We test our hypotheses on a sample of board chair appointments at firms that appeared in the S&P 1500 in any year between 2001 and 2017, inclusive. Data pertaining to boards and executives were collected from the BoardEx and Execucomp databases. Firm-level data were obtained from the Compustat database. After excluding observations with missing data, our initial sample consisted of 16,944 firm-year observations. This sample was used in our first-stage selection analysis described in more detail below. Since the tests of all hypotheses were of board chair appointments, we limited our final sample on which we test our hypotheses to board chair appointments only. This final sample of board chair appointments used in our second-stage analysis consisted of 2,199 observations.

Dependent Variable

Our dependent variable—newcomer chair appointment—is a binary variable that took a value of “1” if the chair appointment was of an independent director who had spent less than 1 year on the board prior to becoming chair. The variable took a value of “0” for all other possible types of board chair appointments; that is, if the appointment was of an independent director with 1 or more years of board tenure prior to becoming chair, or if the appointment was of a non-independent chair (e.g., former or current executive of the firm).

Independent Variables

Demographic faultline strength

To develop our measure of demographic faultline strength, we followed recent board faultline research (Barroso-Castro, Pérez-Calero, Vecino-Gravel, & del Mar Villegas-Periñán, 2020; Shin & You, 2023; Vandebeek et al., 2021; Zhang & Greve, 2019) and used the Average Silhouette Weight (ASW) measure developed by Meyer and Glenz (2013). While there are several ways of calculating faultlines, we chose the ASW for several reasons. The ASW has been demonstrated to be the most effective measure for determining faultlines when compared to other existing measures (Meyer & Glenz, 2013). In addition, and important to the context of boards, the ASW measure is the only one to accurately determine subgroup membership in the presence of more than two subgroups. This is particularly important when examining boards. In our sample, the mean number of non-executive directors on a board was 9.5, suggesting that boards with more than two subgroups are likely.

Meyer and Glenz’s (2013) calculation takes a set of attributes about individuals and uses agglomerative clustering algorithms to cluster members of a group into subgroups to achieve maximum homogeneity within each subgroup and maximum heterogeneity between subgroups. It then develops a maximum ASW per subgroup by quantifying how well each individual fits in their assigned subgroup, making incremental changes until the best configuration is achieved (for a detailed explanation of the calculation, see Meyer & Glenz, 2013).

We considered three attributes of non-executive directors to calculate demographic faultlines. First, gender represents one of the most important social attributes in general, and plays a strong role in the decisions directors make (Johnson, Schnatterly, & Hill, 2013). It is also a common attribute specifically in board faultline research (e.g., Crucke & Knockaert, 2016; Shin & You, 2023; Veltrop et al., 2015). Gender was measured as a categorical variable taking the value of “1” if the director was female and “0” if the director was male.

Second, age is considered highly salient from a demographic perspective. Directors of similar ages will have shared experiences and perspectives, which serve as strong factors in similarity attraction (Forbes & Milliken, 1999). Age is also the most common attribute in faultline research (Thatcher & Patel, 2012), and features prominently in board demographic faultline research (e.g., Shin & You, 2023; Vandebeek et al., 2021). Age was measured as years since birth.

Third, a director’s nationality plays an important role in how they self-identify and behave. Similar to race, it is a highly salient and recognizable attribute over which people categorize themselves and others. Nationality reflects culture and language differences among directors which have the ability to cause friction and create subgroupings (e.g., Hambrick, Li, Xin, & Tsui, 2001; Hinds, Neeley, & Cramton, 2014). As such, nationality has also been used extensively in faultline research (e.g., Elshandidy, Bamber, & Omara, 2024; Hinds et al., 2014; Li & Hambrick, 2005; Polzer, Crisp, Jarvenpaa, & Kim, 2006; Wu, Triana, Richard, & Yu, 2021). Moreover, prior research demonstrates that director nationality influences board functioning and firm outcomes (Estélyi & Nisar, 2016; Harjoto, Laksmana, & Yang, 2019; Kaczmarek & Nyuur, 2022). Given our United States—based sample, nationality was measured as a categorical variable taking the value of “1” if a director was American, and “0” if not, as reported in the BoardEx database. 1

With these attributes, we calculated the ASW measure using the asw.cluster package in R developed by Meyer and Glenz (2013). The resulting faultline strength measure, captured in the year prior to the chair succession, has a possible range from 0 to 1, with a larger value indicating a stronger faultline.

Demographic subgroup non-dominance

To capture whether a subgroup dominated the board, we followed recent work by You et al. (2023) in developing a measure that captured the power of each subgroup. This was done through the following steps: (1) determine the subgroup membership of each non-executive board director using the ASW measure; (2) sum each of the following three variables individually by subgroup: director title (a categorical variable capturing if a director was the board chair or a committee chair), the number of external directorships, and director ownership (the number of outstanding shares); (3) weight each of these summed variables individually based on the proportion of a board’s members that are in the subgroup; (4) standardize each of these weighted variables; and (5) add them together to give an overall value of the amount of power each subgroup held.

Based on this measure of subgroup power, we then took the most powerful subgroup on the board and divided its power by the sum of the power of all subgroups on the board, creating a measure that captures the power of the most powerful subgroup relative to the board—in other words, the degree of a single subgroup’s dominance over the board. We then took the inverse of this to represent demographic subgroup non-dominance. Thus, the final measure of demographic subgroup non-dominance takes a lower value when a single subgroup holds a larger proportion of power, and a higher value as this proportion lessens.

Moderator Variables

CEO power

Following recent studies, CEO power was measured as an index of multiple measures, capturing the construct’s multidimensional nature (Cannella & Shen, 2001; Krause, Filatotchev, & Bruton, 2016a; Krause, Priem, & Love, 2015; Langan et al., 2023). We measured CEO power as the sum of the standardized values of CEO tenure, CEO salary, and CEO stock ownership. A CEO’s influence over the firm and board may increase with their tenure in office, measured in years since assuming the role (e.g., Cannella & Shen, 2001; Hill & Phan, 1991; Van Essen, Otten, & Carberry, 2015). CEO salary has regularly been considered indicative of CEO power (Daily & Johnson, 1997; Finkelstein, 1992; Krause et al., 2015; Langan et al., 2023). CEO stock ownership, measured as the proportion of the firm’s outstanding shares owned by the CEO, is related to the CEO’s ability to influence board decisions (Cannella & Shen, 2001; Finkelstein, 1992; Krause et al., 2015).

Firm performance

We followed prior work examining the relationship between performance and board succession decisions, and measured pre-succession firm performance as a firm’s total shareholder return (TSR; e.g., Krause & Semadeni, 2013; Krause et al., 2017; Quigley & Hambrick, 2012). A firm’s TSR is highly salient to directors and shareholders, as it reflects whether the board is fulfilling its role of increasing shareholder value. TSR was calculated as the end of year share price minus the start of year share price, plus dividends, all divided by the start of year share price.

Control Variables

We controlled for several factors that may affect the type of board chair appointment; all were measured in the year prior to the chair succession unless otherwise specified. To account for the potential effect of the number of demographic subgroups, we included a variable, measured as the total number of demographic subgroups on the board. To capture the variance within a firm of each of the three variables used in the demographic faultlines calculation, we included variables for director gender ratio, calculated as the proportion of female directors on the board; director nationality ratio, calculated as the proportion of American directors on the board; and director age heterogeneity, calculated as the standard deviation of the ages of directors on the board (Shin & You, 2023). The appointment of a newcomer to serve as chair may be related to the proportion of new directors joining the board. We therefore included the proportion of new directors, measured as the proportion of directors who joined the board in the last year, as a control. Board members who are busier (i.e., sit on other boards contemporaneously) may be less likely to seek or be elected to the board chair role. In order to account for this, we controlled for the proportion of busy directors, measured as the proportion of directors on the board with three or more external directorships in listed firms (Fich & Shivdasani, 2006). Boards with a larger number of directors may also have more options for whom to appoint as board chair. We therefore included a control for the number of directors.

Recent research has found that board informational faultlines can have opposing effects to board demographic faultlines on some firm outcomes (e.g., Shin & You, 2023). As such, we followed this research and included a measure of board informational faultlines as a control. This measure was created using the ASW methodology and includes three non-executive director attributes: a director’s independence, primary job title, and board tenure (for a more detailed explanation of this measure, see Shin & You, 2023: 1355-1356). In keeping with our demographic faultline variables, we also included measures of informational subgroup non-dominance and the number of informational subgroups.

We included a control for whether the firm has an outsider CEO with a dummy variable taking the value of “1” if the incumbent CEO had had less than 2 years tenure within the firm prior to becoming CEO, and “0” otherwise (e.g., Kunisch, Menz, & Cannella, 2019; Quigley et al., 2019). Given that CEO-chairs may have the ability to influence a chair succession (e.g., Krause & Semadeni, 2013), we also included a variable capturing CEO duality taking the value of “1” if the incumbent CEO was the board chair in the year prior to the chair succession, and “0” otherwise. To account for any effects related to a CEO succession, we included a categorical variable taking the value of “1” if the chair succession occurred in the same year as a CEO succession and “0” otherwise.

To account for the possibility that firm size plays a role in chair selection, we included it as a control, measured as the natural log of employees. The degree of strategic persistence (or change) a firm is undergoing can also affect whether an insider or outsider is appointed. As such we included Finkelstein and Hambrick’s (1990) measure of strategic persistence as a control. To account for the potential that firms in some industries may be more likely to appoint newcomer chairs than those in others, we included a variable capturing the industry newcomer chair frequency, calculated at the two-digit SIC level. Finally, to account for industry and year unobservable effects, we included industry dummies and year dummies in our analyses (Certo & Semadeni, 2006).

Analyses

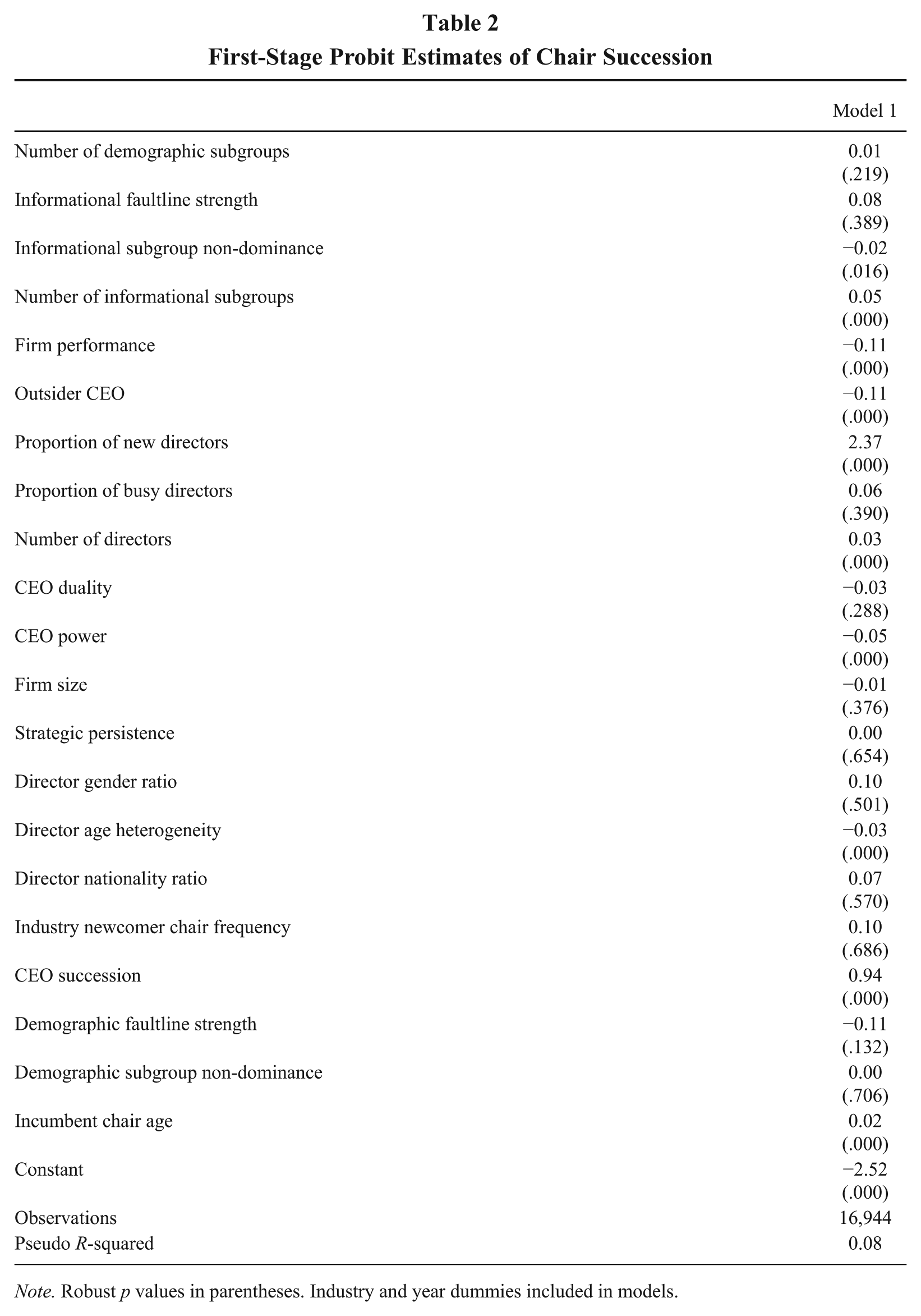

Because our sample consists only of board chair appointments, we needed to address the potential for sample selection-induced endogeneity. We therefore ran a two-stage Heckman selection model (Heckman, 1979), in which the first stage is a probit regression predicting the likelihood of inclusion in the final sample, and the second stage is a probit regression testing our hypotheses on the final sample (Shaver, 1998). The dependent variable of the first-stage probit regression took the value of “1” if the observation was of board chair succession, and “0” otherwise.

This analysis requires a valid exclusion restriction for the first stage. To meet the exclusion restriction, a variable must be included in the first stage that is positively related to the probability of a board chair succession, but does not directly predict the theoretical outcome of the second stage—in this case, a board’s decision to choose a newcomer to serve as chair. We used the variable incumbent chair age as the exclusion restriction in the first stage with the rationale that older board chairs should be more likely to step down from the chair position, triggering a succession. However, the incumbent chair’s age should not be a predictor of the board’s decision to choose a newcomer for the role.

From the results of the first-stage probit analysis, we obtained the predicted probabilities to calculate the inverse Mills ratio, which is included as a control in all second-stage models when its p value is less than .05 (Certo, Busenbark, Woo, & Semadeni, 2016). 2 The second-stage models are probit regression estimates with robust standard errors, testing our hypotheses on the final sample of board chair appointments. To check for the potential of multicollinearity, we examined the variance inflation factors (VIF) of our models. The average VIF was 1.36, and no VIF was above 2.19, suggesting that multicollinearity is not a concern.

In evaluating whether an exclusion restriction is sufficiently strong, Certo et al. (2016) suggest that two good indicators are the size of the pseudo R-squared from the first-stage model and the correlation between the inverse Mills ratio and the independent variable of interest in the second-stage model. They suggest that stronger exclusion restrictions are achieved as the pseudo R-squared from the first-stage model increases and as the correlation between the inverse Mills ratio and the independent variable of interest decreases. The pseudo R-squared from our first-stage model was 0.08. The correlation between the inverse Mills ratio and demographic faultline strength was −0.04 and the correlation between the inverse Mills ratio and demographic subgroup non-dominance was 0.02. Together, these indicators suggest that the strength of our exclusion restriction is sufficient to control for any selection bias (Certo et al., 2016).

Results

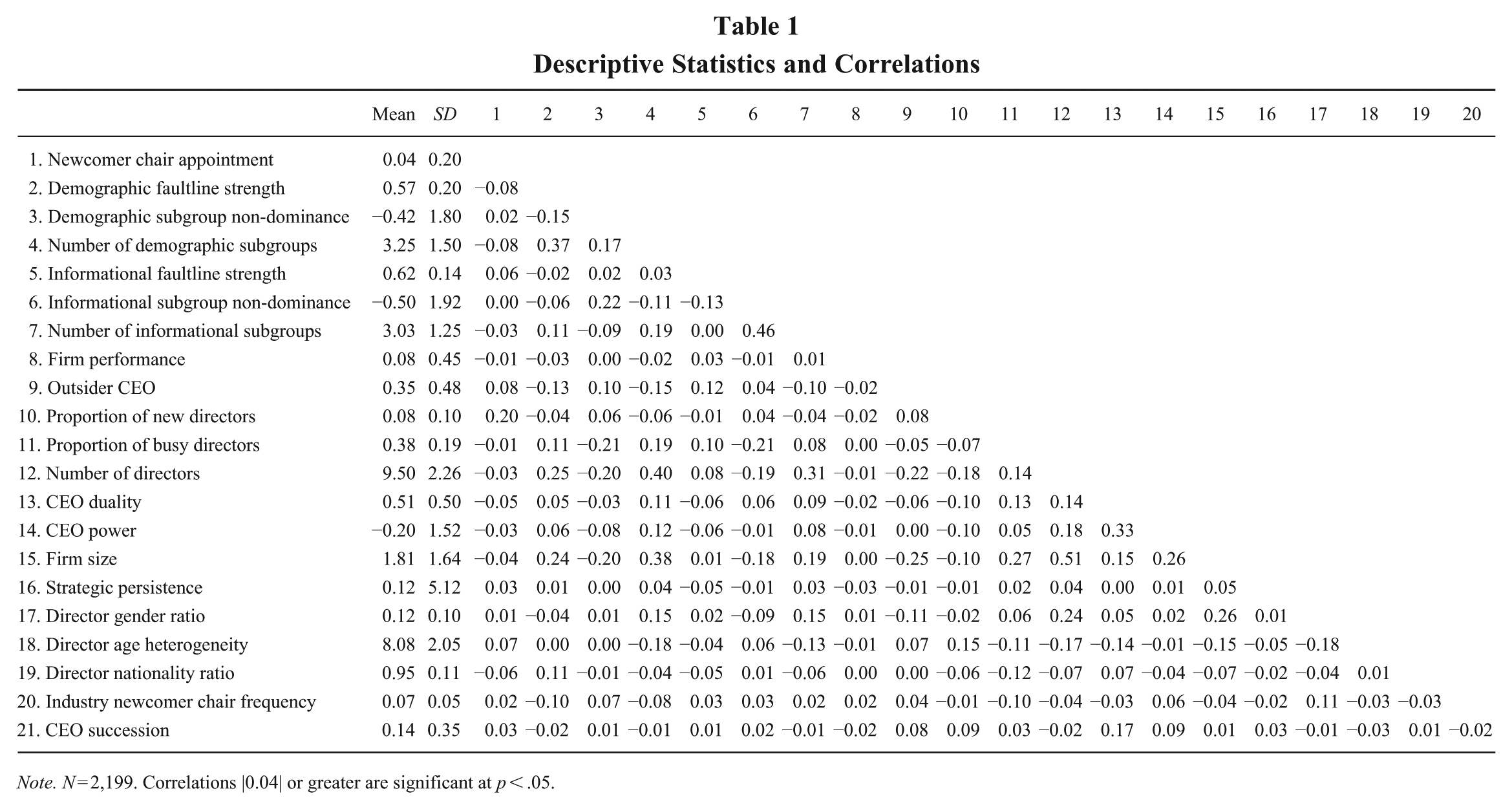

Table 1 provides means, standard deviations, and correlations from our final sample on which we test our hypotheses. Ninety-five chair successions involved a board newcomer being appointed as chair. As mentioned earlier, a chair was considered to be a newcomer chair if they had spent less than 1 year as a director on the board prior to becoming chair. Of those designated newcomer chairs, tenure on the board prior to becoming chair ranged from 0 to 10 months, and the average was just under 5 months. The average ratio of female directors on a board was 12% and ranged from 0% to 60%. The average age of directors was 61 years old, with an average standard deviation among boards of 8 years. We also found that boards varied in the degree of their internationalization ranging from 0% to 87% of directors being foreigners.

Descriptive Statistics and Correlations

Note. N = 2,199. Correlations |0.04| or greater are significant at p < .05.

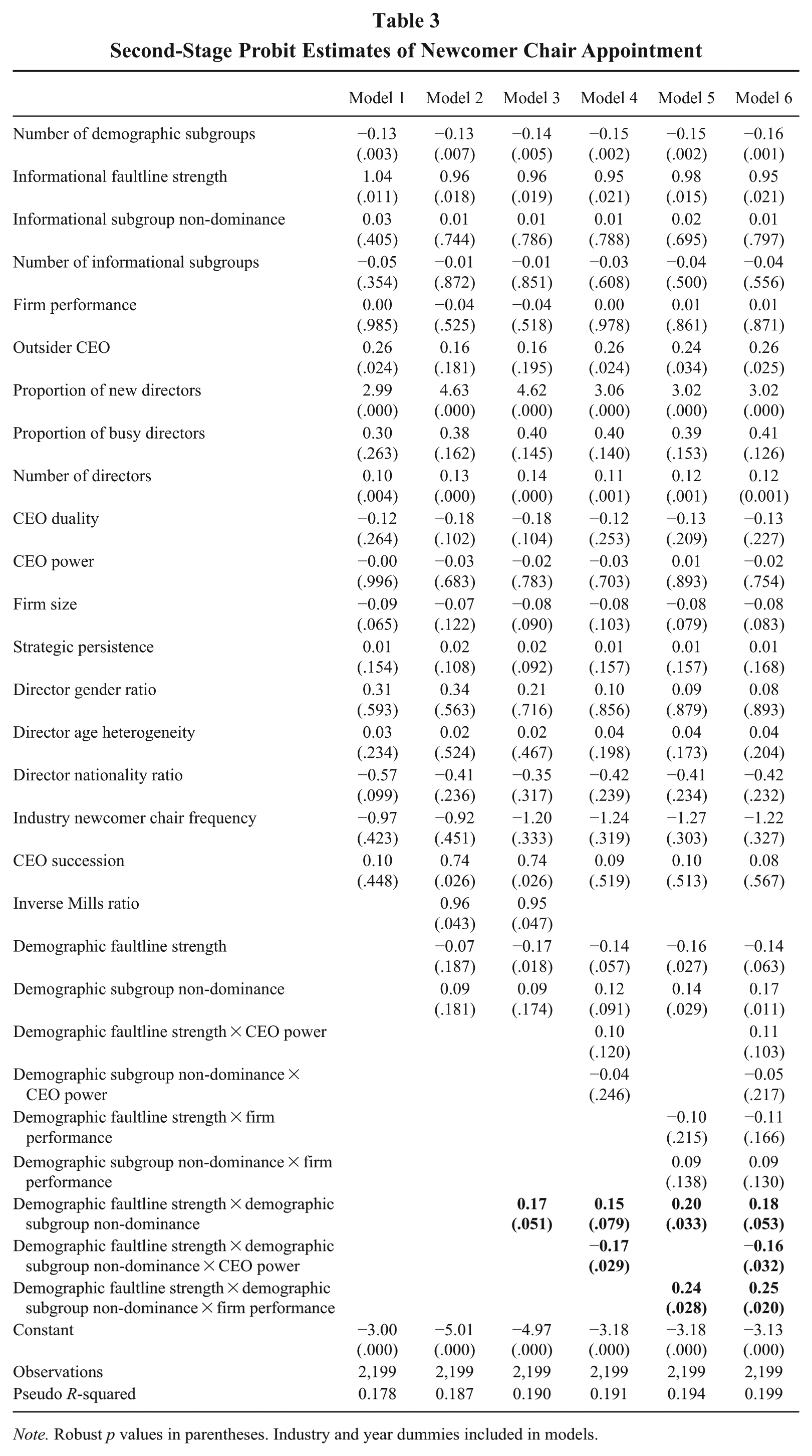

Table 2 reports the results from the first-stage probit estimate. As expected, the incumbent chair’s age is positively related to a board chair succession, and thus an observation’s inclusion in the final sample (p = .000). We also note that our independent variables of interest—demographic faultline strength and demographic subgroup non-dominance—are not significant predictors (p = .132; p = .706, respectively). Table 3 presents the results of our hypothesis tests. Model 1 includes the control variables only. In Model 2, we introduce the independent variables of interest—demographic faultline strength and demographic subgroup non-dominance. In Model 3 we introduce the interaction term of the two, which tests Hypothesis 1. In Models 4 and 5, we introduce three-way interactions with CEO power and firm performance respectively, which test Hypotheses 2 and 3. Model 6 includes all variables and interaction terms. For ease of interpretation, all variables included in the interaction terms are standardized. In reporting our findings, we cite the full models, which are the most appropriately specified given the interactions are significant and the moderator variables are mean-centered (Aguinis, Edwards, & Bradley, 2017; Busenbark, Graffin, Campbell, & Lee, 2021).

First-Stage Probit Estimates of Chair Succession

Note. Robust p values in parentheses. Industry and year dummies included in models.

Second-Stage Probit Estimates of Newcomer Chair Appointment

Note. Robust p values in parentheses. Industry and year dummies included in models.

Model 6 in Table 3 shows that the interaction of demographic faultline strength and demographic subgroup non-dominance is positively associated with a newcomer chair appointment, thus supporting Hypothesis 1 (p = .053). In terms of effect size, we find that when demographic faultline strength and demographic subgroup non-dominance are both at their means, the predicted probability of a newcomer chair appointment is 4%. When both are two standard deviations above their means, the predicted probability is 20%.

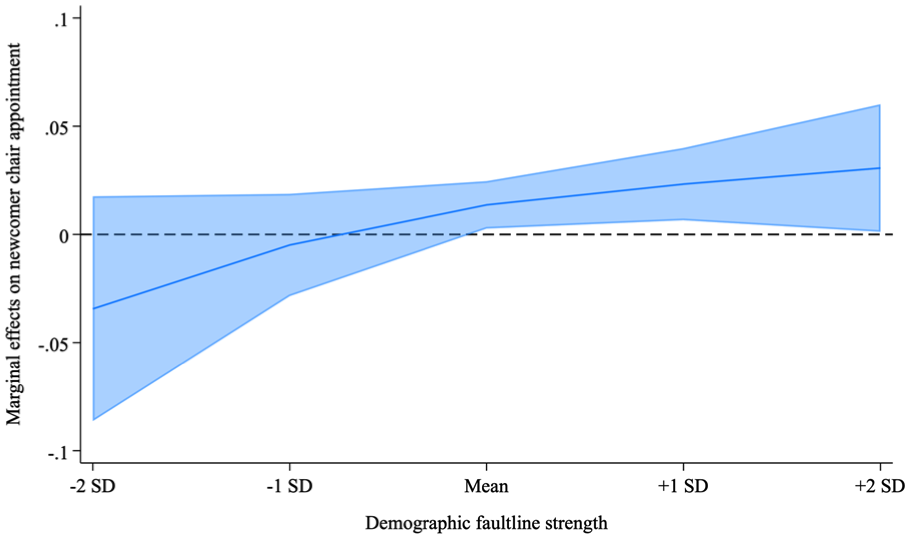

To visualize the effect of the interaction supporting Hypothesis 1, we followed recommendations by Busenbark et al. (2021) and plotted the average marginal effects of this interaction, which are reported in Figure 1. This figure displays the average marginal effect of a one standard deviation increase in demographic subgroup non-dominance on the likelihood of a newcomer chair appointment over the distribution of demographic faultline strength. As evident in the figure, when demographic faultlines are weaker, there is no effect on the likelihood of appointing a newcomer to serve as chair. However, when demographic faultlines are strong, the marginal effect of subgroup power non-dominance on the likelihood of newcomer chair appointment becomes positive and significant, consistent with Hypothesis 1.

Average Marginal Effects of Demographic Subgroup Non-Dominance Over the Distribution of Demographic Faultline Strength

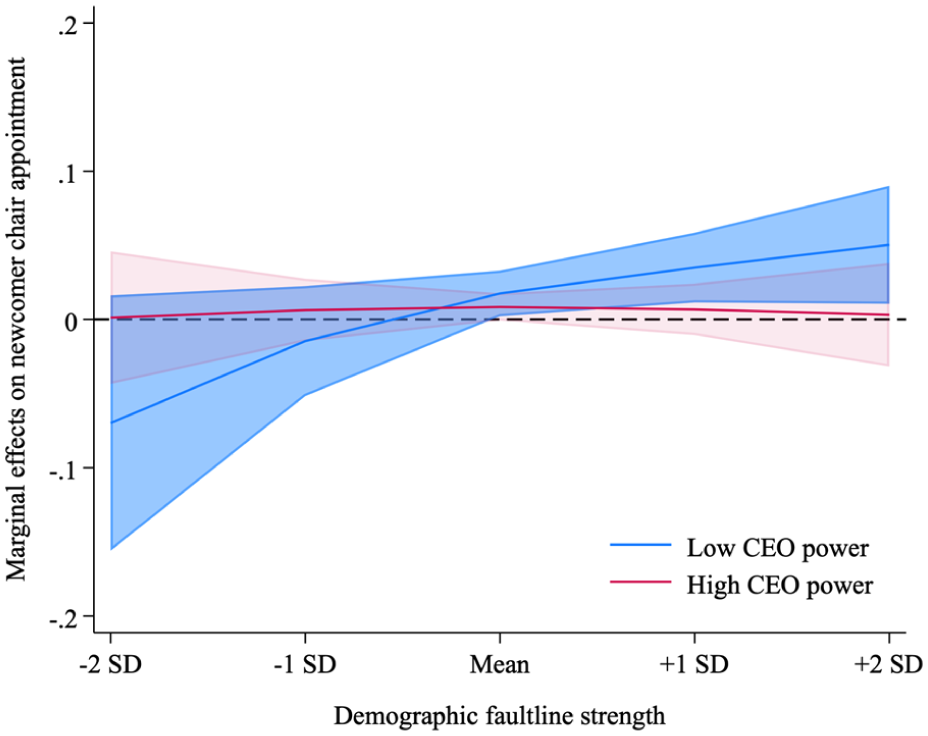

Model 6 also finds that the combined effect of demographic faultline strength and demographic subgroup non-dominance on a newcomer board chair appointment is weaker when the CEO is more powerful, thus supporting Hypothesis 2 (p = .032). To facilitate interpreting this three-way interaction we present, in Figure 2, the average marginal effects of this interaction. As evident, when CEO power is low and faultlines are strong, the marginal effect of demographic subgroup non-dominance on newcomer chair appointment is positive and significant. However, when CEO power is high, there is no statistically significant effect of demographic subgroup non-dominance on newcomer chair appointment at any level of faultline strength, consistent with Hypothesis 2.

Average Marginal Effects of Demographic Subgroup Non-Dominance at Low and High Levels of CEO Power, Over the Distribution of Demographic Faultline Strength

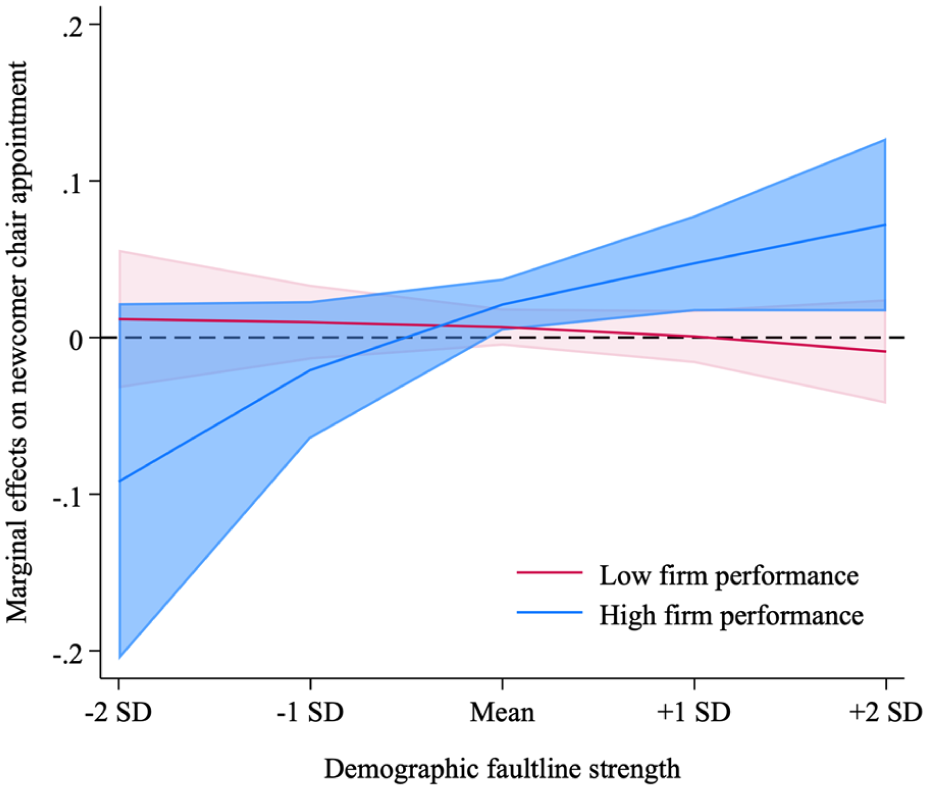

Finally, Model 6 finds that the combined effect of demographic faultline strength and demographic subgroup non-dominance on newcomer board chair appointment is stronger at high-performing firms, thus supporting Hypothesis 3 (p = .020). Figure 3 displays a plot of the average marginal effects of this interaction. As evident, when firm performance is low, there is no statistically significant effect of demographic subgroup non-dominance at any level of faultline strength. However, when firm performance is high and faultlines are strong, demographic subgroup non-dominance exhibits a positive and significant marginal effect on newcomer chair appointment, consistent with Hypothesis 3.

Average Marginal Effects of Demographic Subgroup Non-Dominance at Low and High Levels of Firm Performance, Over the Distribution of Demographic Faultline Strength

Robustness Tests

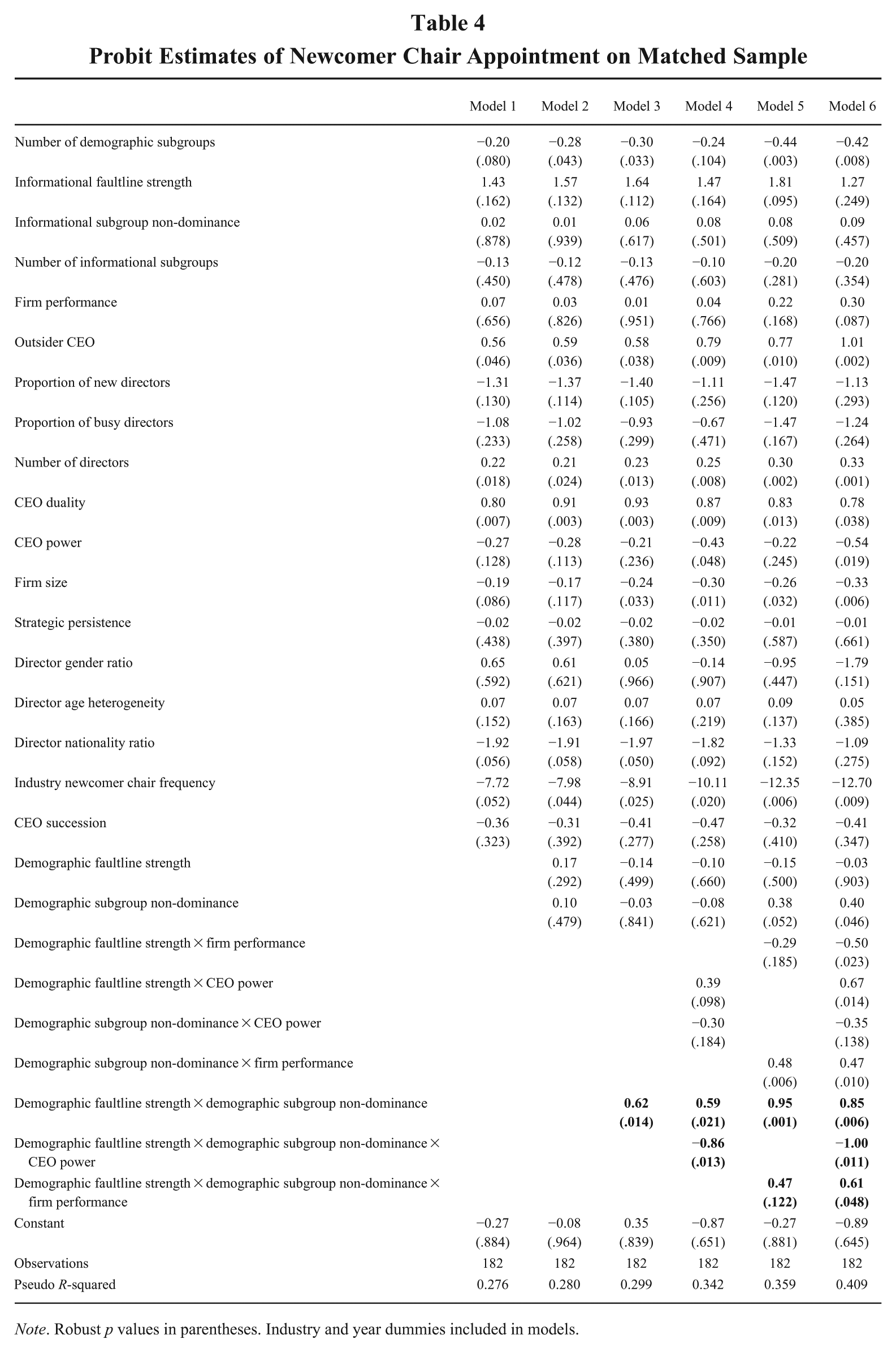

We carried out additional analyses to examine the robustness of our findings. To rule out the potential that firms that appoint a newcomer chair may be different than those that do not, we reran our analyses on a matched sample of chair appointments, matching appointments of newcomer chairs with appointments of non-newcomer chairs (Quigley et al., 2019). To generate the matched sample, we employed propensity score matching to determine the closest match of a newcomer chair appointment (treated) with a non-newcomer chair appointment (untreated; Narita, Tena, & Detotto, 2023). The matching strategy focused on key variables related to a chair appointment, including firm performance, whether the incumbent CEO also held the chair position (CEO duality), the proportion of new directors on the board, the proportion of busy directors, the number of directors, and the year of the chair appointment. The matching required common support and did not allow for replacement (i.e., ensured that multiple treated chair appointments were not matched to the same untreated chair appointment; Quigley et al., 2019). Results from analyses on this matched sample are reported in Table 4. As evident, the results are consistent with our main results.

Probit Estimates of Newcomer Chair Appointment on Matched Sample

Note. Robust p values in parentheses. Industry and year dummies included in models.

We tested our results using a 2-year measure of TSR instead of one, calculated as the average TSR in the 2 years prior to the chair succession. Results were materially unchanged. We also re-ran our analyses using return on assets (ROA), measured as firm net income divided by the book value of its assets in the year prior to the chair succession. Results using 1-year and 2-year measures were materially unchanged. We also included a measure capturing the institutional ownership of the firm (Jung, 2014), collected from the Thomson Reuters Institutional Ownership Database, and reran our analyses. Owing to missing values, our sample was reduced from consisting of 95 newcomer chair appointments to 75. Results remained materially unchanged with one exception: the three-way interaction including firm performance reported a similar coefficient but with a p value above traditional statistical significance thresholds (p = .159). However, when using a 2-year measure of TSR, results remained materially unchanged from those of the main analyses.

To consider the effect that the race of directors may have, we reran our analyses including three variables measuring the proportion of Black, Latino, and Asian directors, collected from the Institutional Shareholder Services database. Owing to missing values, our sample was reduced by about half, resulting in the number of outside chairs falling to 44. However, results were materially unchanged. We also combined these three variables into one variable measuring the proportion of non-White directors and re-ran the analyses. Results remained materially unchanged. Finally, noting the relatively high correlation between the number of directors and firm size (0.51), we removed firm size and re-ran the analyses. Results were materially unchanged.

Discussion

Given that a board chair’s responsibility is to lead the board in its oversight of management, and thus the need for firm-specific knowledge and experience, why a board would appoint a newcomer director to the position is not immediately clear. In this paper, we argue that a newcomer chair appointment may be a compromise solution for a divided board that cannot find consensus. We posit that CEO power moderates this relationship, as a powerful CEO can fill the vacuum of a stalemated board and sway the ultimate decision. We also posit that firm performance moderates this relationship, with good performance increasing competition to rule a successful firm while poor performance may dissuade subgroups from wanting to take the reins. Results supported our contentions. This paper offers scholars and practitioners further theoretical insights into how boards select their chairs and how they manage the sociopolitical dynamics that are at the heart of board functioning.

Contributions to Theory

Our paper contributes to theory on corporate governance in several ways. First, we offer an explanation as to why a board would appoint a newcomer to the position of chair. A large body of research highlights the importance of firm-specific human capital in leading the board in its responsibilities (e.g., Baysinger & Hoskisson, 1990; Langan et al., 2023; Zorn et al., 2017). Accordingly, why a board would not select an existing director who has such knowledge and experience to serve as chair is not immediately clear. Indeed, board chairs typically have considerable experience with the firm; according to Spencer Stuart (2024), independent chairs in S&P 500 firms have on average 7.3 years of tenure. That said, they also acknowledge that 13% of independent chairs are newcomers, also highlighting this curious phenomenon. This paper thus contributes by highlighting that, while firm-specific human capital may be important for the role, boards have other considerations in mind that drive their choices. The result is that, at times, boards are willing to appoint someone with less firm-specific knowledge and experience for the sake of impartiality. We believe that this finding may open new opportunities for research on the topic.

Second, we contribute to theory regarding the sociopolitical dynamics of boards. Power circulation theory suggests that, at any given time, there is a dominant subgroup of the board (Ocasio, 1994; Ocasio & Kim, 1999; Zhang & Greve, 2019). We demonstrate that this may not always be the case, and that, instead, the leadership of the board may, at times, reflect a case in which opposing subgroups agree on a compromise solution to their leadership. Our paper therefore extends existing theory by explaining the leadership implications when no subgroup dominates the board. We believe that this opens future opportunities to examine how other decisions are made when there is no dominant subgroup on the board. Indeed, given the influence the board has over firm decisions and outcomes, there are many other decisions made that may in fact be compromises among subgroups.

Finally, our paper also contributes to recent theoretical work on the choice and suitability of the individual who holds the board chair position. Recent research has highlighted the importance of considering how well directors—and pertinent to this study, the board chair—are qualified, noting that board chairs bring resources with them that aid in their suitability for the role (Garg et al., 2018, 2019; Krause et al., 2016b). We contribute to this work by suggesting that the board chair’s origin is also an important characteristic that can offer benefits. While much work has considered the importance of CEO origin (Berns & Klarner, 2017), there has been little work on board chair origin. As such, we also extend work on this subject and offer new paths forward to investigating how a board chair’s origin may play an important role in a variety of firm outcomes.

Managerial Implications

This study has important implications for practitioners. First, we answer the question of why a board would select a newcomer to lead it. Such a choice may not be immediately clear. Moreover, boards are unlikely to admit if they are stricken by competition and contestation. This paper thus offers some explanation to observers and practitioners as to why a newcomer with seemingly insufficient experience on the board is selected to become chair. Second, and related, we provide insights into ways that boards seek compromise solutions to issues around leadership. Our theory suggests that appointing a newcomer director to serve as board chair may be perceived by boards as a way to achieve impartial leadership when differences between evenly matched subgroups are strong. Our focus on demographic subgroups is also especially relevant to firms as they continue to strive for greater diversity. Indeed, faultline theory suggests that with diversity comes the potential for subgroup formation that can be detrimental for group effectiveness (e.g. Lau & Murnighan, 1998; Thatcher & Patel, 2012), and ultimately for firm performance (Crucke & Knockaert, 2016; Kaczmarek, Kimino, & Pye, 2012; Tuggle et al., 2010; Van Peteghem, Bruynseels, & Gaeremynck, 2018; Veltrop et al., 2015). Our finding that boards characterized by strong differences between demographic subgroups—with none powerful enough to dominate decision-making—are more likely to appoint a newcomer director to serve as chair, offers some insights that come directly from practice. As such, this paper serves as a good example of when academic research can learn from what firms are doing so that it can then inform scholars and practitioners alike.

Limitations and Extensions

This paper is subject to some limitations which offer opportunities for future research. We argue that whether an individual is an incumbent board member is a key selection attribute for boards who seek an impartial board chair as a compromise solution. We acknowledge that it is possible that a newcomer’s attributes might fit within an existing subgroup on the board. However, a key tenet of our argument is that a newcomer is viewed by the board as more impartial precisely because they are not an established board member, and thus are not an established member of a subgroup. We assume that the degree to which they may be similar to other directors or fit within an existing subgroup is less salient to a board than the fact that they are a newcomer to the board and firm. Our findings support this reasoning. However, future research could examine the specific demographic attributes of new directors appointed to boards divided into subgroups with none powerful enough to dominate. We focus on whether an individual is a newcomer; the question of other attributes of the appointed board chair is thus outside the scope of this paper. We acknowledge, however, that the literature might benefit from a greater understanding of what other attributes are considered and how different they may be from the attributes of the incumbent board members (Zhu, Shen, & Hillman, 2014), and encourage scholars to further examine this, going forward.

Relatedly, an assumption in our study is that a newcomer is not a member of an existing subgroup within the board. While it is possible that a newcomer may have had some prior relationship with one or several board members prior to joining, it should still be less significant than the relationships of an established board member, who will have had interactions and developed relationships with all board members over a longer period of time, and participated in board meetings and decisions. With the recent increased focus on qualitative studies examining boards of directors (Bezemer et al., 2018; Boivie, Withers, Graffin, & Corley, 2021; Veltrop et al., 2021), future research might investigate this question to understand how the influence of a newcomer director appointed as board chair affects board functioning, and how their socialization might occur over time.

In capturing subgroups on the board, we include a measure of director nationality. Given that our sample is of public U.S. firms, we follow prior research in measuring it as a binary variable capturing whether a director is an American or not (Estélyi & Nisar, 2016; Harjoto et al., 2019; Kaczmarek & Nyuur, 2022). However, there may be heterogeneity within the non-American category that might not be fully captured, limiting the degree to which we capture the complex dynamics from the various nationalities represented. As boards continue to internationalize, research might benefit from more fine-grained measures that capture the unique cultural and linguistic differences between directors and how they affect board outcomes. For instance, scholars could consider categorizing nationality based on the primary language of the country of origin, or by measuring cultural distance of the country of origin from the United States. Such operationalizations might offer further insights into how directors on a board align.

Finally, in this paper we argue that boards divided into demographic subgroups with none dominating the board will perceive a newcomer director as someone who may serve as a compromise leadership solution. We do not argue that disagreement between subgroups is actually reduced or that a newcomer chair is actually effective in mitigating difficulties between demographic subgroups. The focus of this paper is entirely on how boards respond from a composition and leadership perspective. We only argue that a board may perceive a newcomer director as a way to avoid any one subgroup assuming the board chair position. This is an important distinction. A natural extension of this paper would be to examine whether newcomer chairs actually do mitigate conflict and contestation between subgroups. In addition, given that, to the best of our knowledge, this is the first paper to examine the construct of the newcomer board chair, we believe there are many opportunities to further examine its antecedents and consequences, and we urge governance scholars to explore it further.

Conclusion

This study investigates how boards address the difficulties that may arise when they are characterized by strong differences between demographic subgroups with none powerful enough to dominate decision-making. We argue and find that, in such a case, a board is more likely to choose a newcomer director to serve as chair. We further find that this likelihood is moderated by CEO power and firm performance. This study therefore contributes to extant corporate governance theory and spurs new opportunities for future research on how boards manage sociopolitical conflict, as well as on the antecedents of board chair appointments.

Footnotes

Acknowledgements

We thank Associate Editor Cuili Qian and the anonymous reviewers for their contributions toward the development of this paper. We also thank research seminar participants at Copenhagen Business School, University of Cincinnati, Indiana University, Tilburg University, the University of Groningen, Simon Fraser University, the 2022 Academy of Management Annual Meeting, the 11th EIASM Workshop on Top Management Teams, the 2021 Strategic Management Society Annual Conference, and the 2021 ICGS Annual Conference for their helpful comments on earlier versions of this work. We gratefully acknowledge project funding from the Swiss National Science Foundation (Grant Number 185173).