Abstract

Research on organizational misconduct has mostly evolved independently from the literature on corporate governance. Yet, our survey of research on the role of directors in organizational misconduct contexts yielded more than 110 articles in the last 17 years across the management, accounting, marketing, operations, public relations, and finance literatures, showing that research on the role of corporate governance in organizational misconduct has increasingly become a distinct domain of inquiry. With its own scholarly audience, including scholars working in strategy, ethics, decision-making, and leadership, this research has employed diverse theories and investigated different antecedents, reactions, and outcomes. It has also focused on how directors both influence and are affected by organizational misconduct. Consequently, this literature is currently fragmented in several respects. Our aim in this review is to generate conceptual integration that brings coherence to this growing body of research and to facilitate future research in this important domain. The review offers a cohesive view of the effects of corporate governance on misconduct and of misconduct on corporate governance and provides frameworks for integrating the disparate macrolevel theories that currently characterize this work.

Organizational misconduct can have devasting consequences for organizations and their stakeholders, including consumers (e.g., defective products), employees (e.g., discrimination or harassment), and shareholders (e.g., fraud). Some incidents of misconduct have even further-reaching effects—ones that destabilize financial markets and undermine public confidence in institutions (McDonnell & Nurmohamed, 2021). For example, the corruption scandal uncovered in 2015 at Petrobras, Brazil’s state-owned oil company, led to political upheaval, economic recession, and rising unemployment (Segal, 2015). Misconduct incidents can also pave the way for sweeping regulatory changes (e.g., Sarbanes-Oxley following the Enron and WorldCom scandals) or social movements (e.g., #MeToo; McDonnell & Nurmohamed, 2021). Given the consequential nature of these events, it is not surprising that scholarly research on organizational misconduct has expanded considerably over the past two decades. This work has sought to examine multiple facets of misconduct: its antecedents (Greve, Palmer, & Pozner, 2010), its consequences for stakeholders, the penalties levied on individuals and organizations as a result (McDonnell & Nurmohamed, 2021), and what corrective actions organizations engage in to mitigate the reputational and financial fallout of these events (Hersel, Helmuth, Zorn, Shropshire, & Ridge, 2019).

The role of directors and boards is critical in all these contexts. Directors are the highest legal authority of public companies (Finkelstein, Hambrick, & Cannella, 2009) and help ensure that organizations pursue their goals in ways that are consistent with legal and regulatory policies, obligations to stakeholder groups, and broader societal norms. As such, they have the potential, and responsibility, to be a critical safeguard against misconduct, which includes “illegal, unethical, or socially irresponsible behavior enacted by an organization that directly harms stakeholders” (Hersel et al., 2019: 549). Research on the antecedents of misconduct, therefore, often considers what characteristics of boards or directors are associated with the occurrence of misconduct (Neville, Byron, Post, & Ward, 2019; Zaman, Atawnah, Baghdadi, & Liu, 2021; Zorn, Shropshire, Martin, Combs, & Ketchen, 2017). Other streams of research also examine the consequences directors and boards experience in the wake of misconduct (Marcel & Cowen, 2014; Pozner, 2007; Srinivasan, 2005) and what actions they pursue to ameliorate reputational or financial damage to the firm or the board (Cowen & Marcel, 2011; Naumovska, Wernicke, & Zajac, 2020).

Regarding the broad literature on corporate misconduct, while directors may appear frequently in research studies, the literature lacks an integrated perspective on when and how they influence organizational misconduct and the events that follow the misconduct. Despite the significance of their role, it remains in the periphery or only tangentially addressed in the prior literature reviews on misconduct. This is, in part, due to broader fragmentation in the misconduct literature—this research has developed across fields including accounting, finance, strategic management, operations, marketing, and public relations. As other reviews have noted, work in these fields is often not in dialogue with each other, creating barriers to conceptual integration (Hersel et al., 2019). However, barriers to integration are compounded by the fact that existing studies tend to focus only on a single facet of misconduct. This is even evident in the structure of literature reviews in the domain of misconduct. For example, the review by Greve et al. (2010) focuses primarily on the antecedents of misconduct, Hersel et al. (2019) review the work on corrective actions, and McDonnell and Nurmohamed (2021) are exclusively concerned with organizational punishment. The consequence is that the literature lacks a broader, integrated perspective on how directors shape—and are impacted by—misconduct events. Such theoretical integration has the potential to resolve (or identify) contradictions in the literature, bring clarity to when and how director- or board-level interventions will affect misconduct or its consequences and, going forward, to amplify the impact of work on the mutual influences of governance and misconduct by identifying opportunities for theoretical integration and more robust exploration of multilevel dynamics. This perspective is also essential if the goal is for misconduct research to translate into practical applications concerning how governance and governance leaders can better avert misconduct or constructively respond when misconduct occurs.

Our review adopts a fundamentally different approach by synthesizing work specifically on directors and boards across different fields of study and streams of misconduct research. Our review of the 112 articles published in management, marketing, operations management, supply chain, public relations, accounting, and finance on the topic (using criteria specified in the appendix) revealed a range of different theories, concepts, and mechanisms (see Table 1) as well as different effects and outcomes for individuals, committees, boards, and firms. In reviewing this literature, we aim to develop a comprehensive and integrated framework that can highlight what is currently known from the work to date, identify gaps that deserve further attention, and provide a road map for future research. We do this in two steps. First, to organize our review, we classify studies focusing on the influences of governance on misconduct (i.e., the board and director antecedents of misconduct) to be studies of governance failures. In contrast, we consider studies on the influences of misconduct on governance to be studies of governance under failure. We separately review each of these two primary streams of misconduct research to identify common themes that characterize the research to date. We then offer an organically developed organizing framework that offers a more cohesive view of the literature and briefly discuss individual studies that are illustrative of key relationships in the framework (see Figures 1 and 2). To arrive at our framework, we identified categories of factors and relationships that exist in this prior research and included a category in the framework even if only one study exists in that category of factors or relationships. This framework then facilitates the identification of future research opportunities in each stream. Second, we take a holistic view of the literature that encompasses the streams of misconduct research to generate an integrative, broader view and identify opportunities for further integration across different streams of literature.

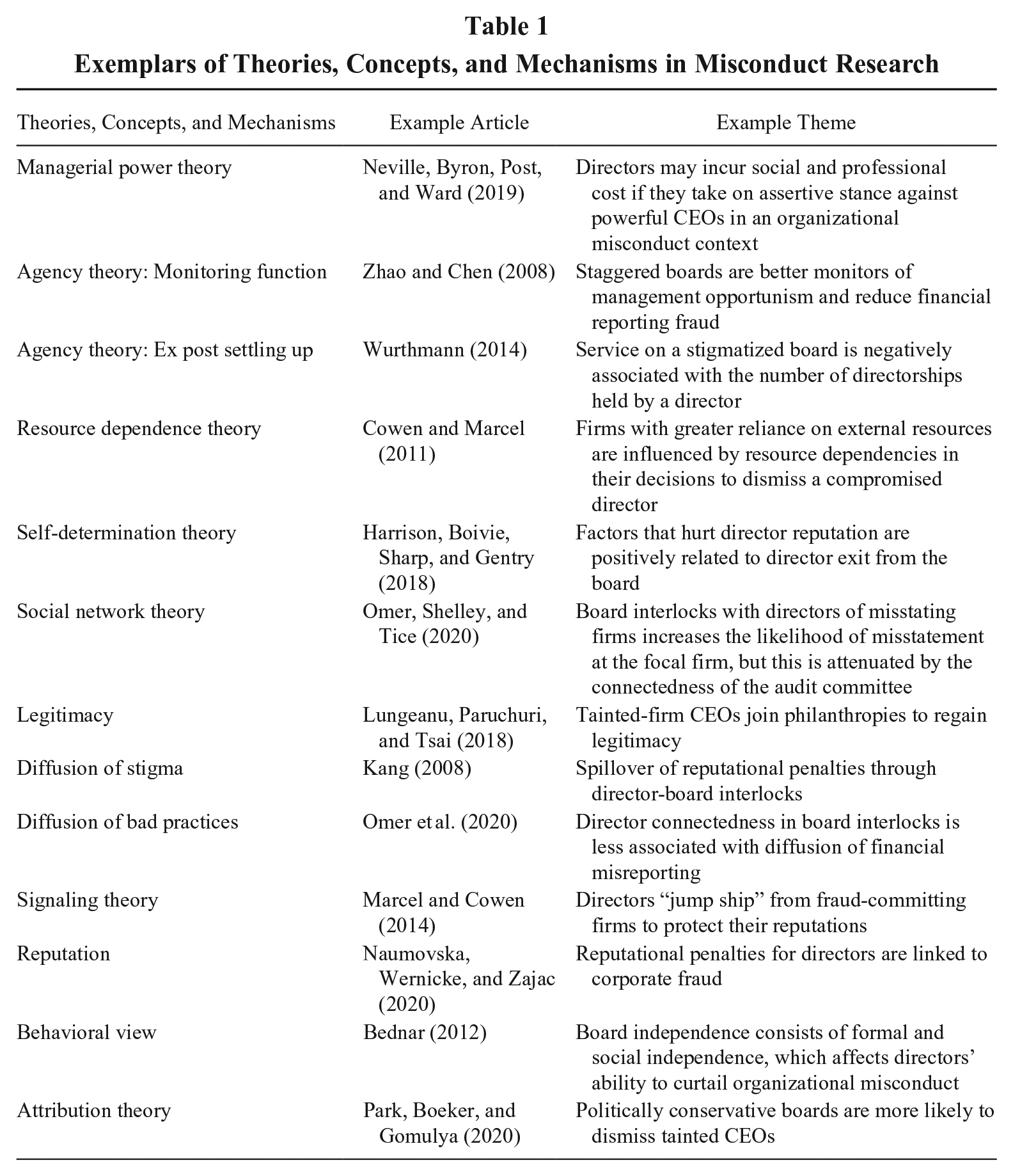

Exemplars of Theories, Concepts, and Mechanisms in Misconduct Research

Governance Failure: Director and Board Characteristics as Antecedents of Organizational Misconduct

Governance Under Failure: Board and Director Responses to Misconduct and the Consequences Endured

In sum, our review reveals that the literature at the intersection of directors and misconduct is rich, diverse, and fast growing. As such, we believe this review could act as a beacon for scholars who are interested in doing research in this domain by presenting a comprehensive landscape of the current state of knowledge, addressing aspects of fragmentation in the literature, and suggesting potential directions for future research.

Governance Failures: Director and Board Characteristics as Antecedents of Organizational Misconduct

Integrative Themes

We identified all articles where misconduct characteristics (e.g., presence or absence, severity of misconduct) were outcomes as this research concerns governance failures that culminate in misconduct. We coded these articles in terms of theories, mechanisms employed, empirical contexts studied, and relationships studied. Five themes emerged from reviewing these articles. The first theme derives from the theories employed in the area. Much of the research is focused on testing the prescriptions of agency theory (Fama, 1980; Fama & Jensen, 1983; Jensen & Meckling, 1976). In regard to the board attributes that might influence a firm’s engagement in misconduct, existing studies often consider factors prominent in agency theory, such as CEO duality (Efendi, Srivastava, & Swanson, 2007; O’Connor, Priem, & Coombs, 2006), director independence (Neville et al., 2019; Zorn et al., 2017), and board monitoring (J. Chen, Cumming, Hou, & Lee, 2016; Sáenz González & García-Meca, 2014). From the misconduct perspective, agency theory proposes that factors such as separating the CEO from the board chair, greater independence of the board, and more intense monitoring should reduce the incidence of misconduct. Thus, scholars often pursue the question of whether these assumptions hold and, if so, what boundary conditions constrain these relationships. Interestingly, as we describe in detail later, the results are mixed. For example, whereas independence may reduce misconduct (Neville et al., 2019), extreme independence may increase its incidence (Zorn et al., 2017).

A second observation is that, although scholars have conceptualized several categories of misconduct (e.g., fraud, product safety issues, employee mistreatment, and environmental violations), the majority of empirical work focuses on a limited range of deceptive behaviors. To elaborate, Hersel et al. (2019) summarize four different types of misconduct—fraud, product safety issues, employee mistreatment, and environmental violations—while other research has focused on intentional versus unintentional misconduct, integrity versus competence failures, frauds versus accidents, and focused versus endemic misconduct (Connelly, Ketchen, Gangloff, & Shook, 2016). However, much of the research has emphasized restatements of financial disclosures, stock option backdating, or earnings management (Mohliver, 2019; O’Connor et al., 2006; Zhao & Chen, 2008), which together represent only one category of misconduct (e.g., fraud or integrity failures).

A closely related pattern emerging within this theme is that different fields focus on different aspects, behaviors, or revelations as misconduct. Management and marketing literature has typically focused on revealed and/or transpired misconduct (e.g., product recalls or financial restatements), while others have also examined behaviors that are perceived to lead to misconduct (e.g., aggressive earnings management). To explain, the accounting literature on misconduct has focused on aggressive earnings management, a practice wherein managers manipulate financial reporting to essentially manage impressions about the firm’s performance (Caskey & Laux, 2016; Chan, Chen, Chen, & Yu, 2015; Klein, 2002; Zhao & Chen, 2008). It could be argued that earnings management does not rise to the level of misconduct typically focused on in management research (Greve et al., 2010; Hersel et al., 2019), as it is not illegal and may or may not be unethical. While it could still be considered an antecedent to misconduct (e.g., restatement; Chiu, Teoh, & Tian, 2013), the current management research has paid scant attention to earnings management as misconduct.

The third theme is the focus of existing work on how misconduct practices spread from organization to organization via social networks. Specifically, research has considered the social nature of organizations, examining social contagion of misconduct practices (Chiu et al., 2013; Omer, Shelley, & Tice, 2020; Surroca, Tribo, & Zahra, 2014). The idea that nefarious practices spread through board interlocks is indeed interesting, considering the capacity of such interlocks to serve as conduits of information between firms (Borgatti & Foster, 2003; Borgatti & Halgin, 2011; Howard, Withers, & Tihanyi, 2017). Thus, research has examined how and when such practices may spread from firm to firm through different information channels, such as board interlocks.

A fourth theme is the limited conceptual engagement with the multiple levels of analysis that characterize the relationship between governance and misconduct. The existing studies examining the effects of individual director characteristics often treat individual attributes as board characteristics. For example, studies often examine how the presence of a lawyer (Krishnan, Wen, & Zhao, 2011) or a woman (Cumming, Leung, & Rui, 2015) on the board influences the incidence of misconduct. Thus, it is a characteristic of the board, rather than the behavior or perspective of the individual director, that is examined. As will be discussed subsequently, the true multilevel nature of the misconduct phenomenon remains unexplored.

The final theme pertains to the focus of existing work on empirical quantitative testing using primarily U.S.-based samples. Exceptions to empirical studies include the quad model (Hambrick, Misangyi, & Park, 2015), a theoretical model for understanding the link between director characteristics and the likelihood of organizational misconduct. According to this model, the preferred director (for the purpose of monitoring executive behavior) is one who is independent, has the requisite expertise and bandwidth for the role, and is motivated to execute monitoring duties (Hambrick et al., 2015). With respect to the antecedents of misconduct, testing the prescriptions of such theories as the quad model or agency theory encourages the use of deductive research methods. The prescriptions from these theories all derive from governance relationships in the U.S. context. Less is currently known about these relationships external to the United States. Exceptions to the U.S. context include studies by Bajo, Bigelli, Hillier, and Petracci (2009); Hass, Tarsalewska, and Zhan (2015); and Sáenz González and García-Meca (2014), which we will describe further later.

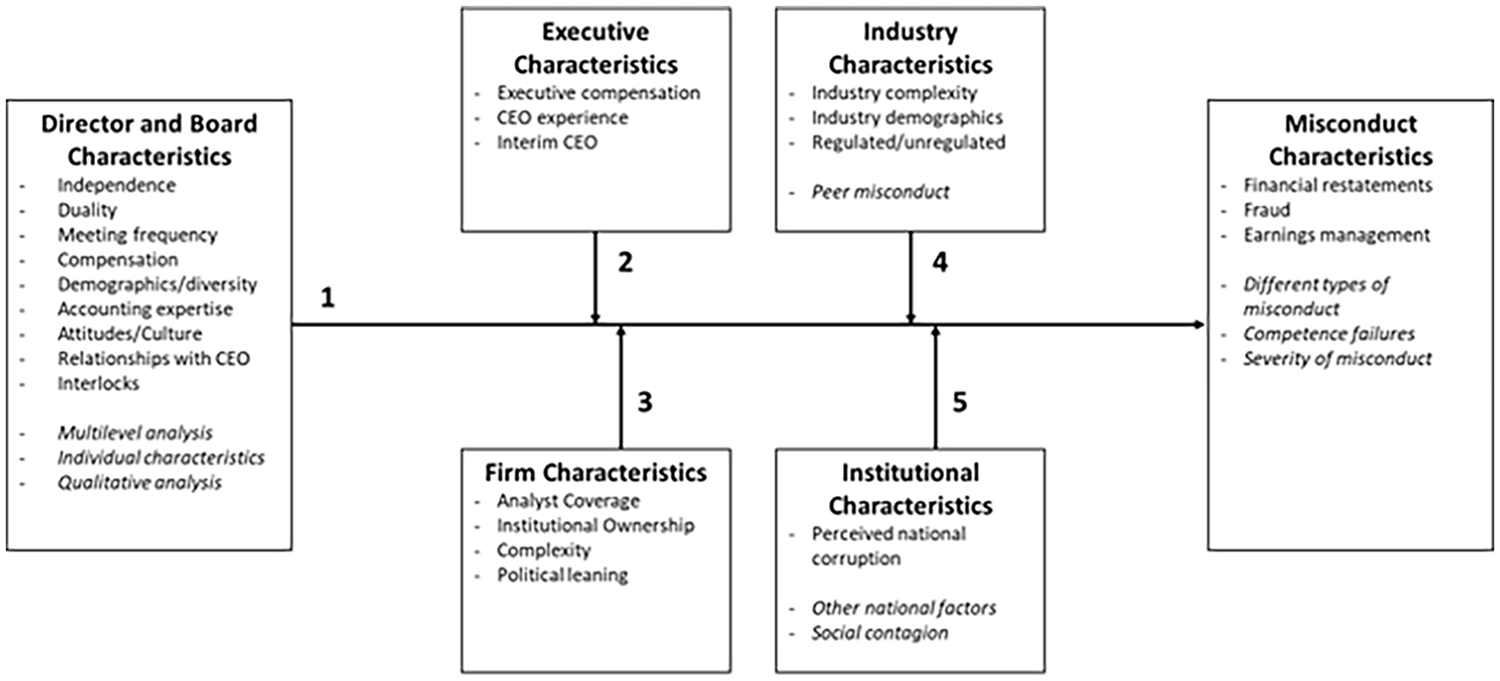

Organizing Framework

To describe the research landscape, we organized the studies regarding the director and board antecedents of organizational misconduct into the theoretical model depicted in Figure 1. Relationship 1 shows the associations between board and director characteristics and misconduct and the associated characteristics, including whether a firm engages in misconduct and the type and severity of misconduct. Research has further examined the joint influences of director and/or board characteristics with executive characteristics (relationship 2), firm characteristics (relationship 3), industry characteristics (relationship 4), and institutional environment characteristics (relationship 5). Next, we will review studies on each of these relationships.

Main Effects

The research investigating relationship 1 focuses on the misconduct characteristics, such as presence or absence of misconduct, intentional or nonintentional, and severity of misconduct. While some studies have focused on board actions, most of the research in this area has employed board attributes as predictors of misconduct.

Board actions as antecedents

Research employing board actions has investigated, for example, the effects of the adoption of clawbacks and frequency of board meetings on organizational misconduct likelihood, frequency, and intensity. Chan et al. (2015) found that clawbacks, a measure by which firms can recover executive compensation in the event of misstated financial reporting (thereby reducing restatements), were related to greater subsequent earnings management in firms with stronger growth opportunities or more transient institutional investors. In a rare non-U.S. study, Sáenz González and García-Meca (2014) found in the Latin American context that greater frequency of board meetings was associated with reduced earnings management.

Board attributes as antecedents

Because boards are collectives of multiple individuals, some research employing board attributes as predictors used “global unit properties” (e.g., board size; Kozlowski & Klein, 2000), while others employed “compositional” aggregation of individual director attributes as board attributes (e.g., percentage of independent directors, presence of women or accounting experts on the board). For example, Zhao and Chen (2008) found that staggered boards are related to a lower likelihood of financial fraud and reduced earnings management. Reviewing studies on board size as an additional example of the sparse research that uses global unit properties of boards, we found that larger boards are generally considered to provide better monitoring (e.g., Hass et al., 2015). But an exception to this general finding was documented by Sáenz González and García-Meca (2014), who found that larger board size is associated with greater engagement in earnings management. Another global unit properties attribute that we observed was a board-level phenomenon: accounting conservatism. Caskey and Laux (2016) predicted that accounting conservatism would be an important antecedent of good governance. They define accounting conservatism as “imposing stricter verifiability standards for reporting good news than for reporting bad news” (Caskey & Laux, 2016: 424). However, the authors concluded that accounting conservatism was actually associated with increased accounting manipulation.

The vast majority of research investigating board attributes as predictors of misconduct focused on “compositional” measures of boards. While Neville et al. (2019) in their meta-analysis found, consistent with agency theory, that board independence, board–audit committee independence, and CEO–board chair separation are negatively related to misconduct, Zorn et al. (2017) considered a situation in which firms adhere to an extreme form of agency theory prescriptions to minimize managerial abuses: the lone insider board, in which the CEO is the only insider executive on the board. Counterintuitively, they found that lone insider boards are related to greater likelihood of financial misconduct.

Studies have also focused on expertise, demographics, and attitudes to create compositional measures. For example, Cumming et al. (2015) focused on board gender diversity and found that the presence of women on the board tended to result in a lower likelihood of securities fraud, especially when in a male-dominated industry. Focusing on expertise, Krishnan et al. (2011) predicted that the presence of audit committee members with legal or accounting backgrounds would improve financial reporting quality, especially when directors with both attributes are present on the board. Additionally, Ege (2015) developed a composite measure of internal audit function quality, while also considering board competence and objectivity, and found that greater board quality and competence reduced the likelihood of misconduct. Focusing on attitudes, Bereskin, Campbell, and Kedia (2020) examined how prosocial motivations of employees and the board of directors (collectively) influence the likelihood of whistleblowing for misconduct. In the context of family-controlled firms in China, Guo, Luo, and Li (2022) introduced an alternative mechanism in preventing securities fraud: hierarchical inconsistency, which is when the formal organizational hierarchy does not align with the social hierarchy with respect to the board chair. They theorize and find that when directors are superior to the board chair in the social hierarchy, they are more likely to effectively monitor and prevent misconduct.

In an interesting twist, research has also focused on compositional measures based on the relationships between the CEO and individual board members. These studies focus on variances in independence of individual directors given prior relationships and their loyalty to the executives (Bednar, 2012). For example, Rose, Rose, Norman, and Mazza (2014) considered how friendship ties between directors and the CEO are related to earnings management and found that directors who were friends of the CEO were more likely to support earnings management behaviors that benefit the CEO. Similarly, Khanna, Kim, and Lu (2015) found that connections through appointment decisions between the CEO and these relevant directors resulted in a higher likelihood of fraud and greater costs associated with the fraud, but prior connections through education, employment, or social groups had no significant effect.

Board interlocks as antecedents

An even more interesting compositional board attribute is created from the composition of board directors who sit on boards of other firms—board interlocks—that faced misconduct. For instance, Chiu et al. (2013) examined the contagion of financial restatements through director interlocks among firms, finding evidence for such contagion and that this effect is stronger when the director common to the two firms is a part of the audit committee at either firm. Similarly, Omer et al. (2020) found evidence of contagion in financial reporting quality, such that firms with board interlocks to restatement firms were also more likely to have a restatement, but the presence of audit committee members who were better connected tended to attenuate this relationship as it was linked to a reduction in the adoption of low-quality reporting practices. Further, Surroca et al. (2014) considered the spread of corporate socially irresponsible practices from a firm to its subsidiaries, finding that it is higher when the subsidiary is connected to the parent through a board interlock.

Null effects

Interestingly, several corporate governance studies did not find a significant association between corporate governance factors and organizational misconduct. For example, in a study of the effects of corporate governance on the incidence of restatements, Larcker, Richardson, and Tuna (2007) determined that board characteristics, such as board size, affiliated directors, busy directors, and old directors, do not have a strong influence on misconduct. González, Schmid, and Yermack (2019) found that corporate governance factors, such as internal selection of CEO successors and director replacement, were not significant predictors of price fixing by cartel firms, and Bajo et al. (2009) found no evidence for the effect of CEO duality or board independence with respect to compliance with regulations regarding insider trading in Italy. Similarly, Mohliver (2019) found that CEO duality was not a significant predictor of backdating behavior. In the Chinese context, Hass et al. (2015) did not find a significant association between supervisory board equity compensation and corporate fraud.

Joint Effects

The research illustrated in Figure 1 has also focused on other factors that alter the effects of board and director characteristics on misconduct. These studies consider the interaction of board characteristics with executive characteristics (relationship 2), firm characteristics (relationship 3), industry characteristics (relationship 4), and institutional environment characteristics (relationship 5).

Moderating effects of executive characteristics

For exemplar studies of relationship 2, we focus on studies that have explored the joint effects of executive compensation configurations and board characteristics on misconduct (Efendi et al., 2007; O’Connor et al., 2006). For example, O’Connor et al. (2006) examined the CEO stock option compensation as an executive characteristic and CEO duality and board stock option compensation as board characteristics. Although agency theory suggests that stock options align managerial and shareholder interests and reduce misconduct, they found that this relationship was contingent on the specific combination of CEO duality and whether board members received stock option compensation. Interestingly, the authors found that when CEOs received a high proportion of their compensation from stock options, restatements were less likely under conditions of no duality and no board stock option compensation, but when the board received stock option compensation and the CEO was not also the board chair, this resulted in the highest likelihood of restatement (O’Connor et al., 2006). Efendi et al. (2007) extended this line of study by examining how executive compensation and CEO duality influence misconduct, finding that restatements associated with executive compensation were more likely when the CEO was also the board chair.

Several studies also focused on CEO attributes, such as expertise. For instance, Koch-Bayram and Wernicke (2018) found that CEOs with military experience were less likely to be involved in misconduct and that this effect was strengthened by stronger board oversight in the form of splitting the CEO and chair positions and greater board independence. G. Chen, Luo, Tang, and Tong (2015) found that firms with interim CEOs were more likely to engage in earnings management to improve the prospects of the interim CEO in achieving promotion to the permanent position but that this relationship was attenuated by board attributes that represent stronger monitoring, such as higher independence, greater board ownership, presence of financial or accounting expertise, and less busy directors.

Moderating effects of board characteristics

Regarding firm characteristics interacting with director or board characteristics (relationship 3), in their study of lone insider boards, Zorn et al. (2017) considered how the positive relationship between lone insider boards and firm misconduct is attenuated by analyst coverage and institutional ownership of firms but did not find support. Ndofor, Wesley, and Priem (2015) examined how the effects of executive compensation and board monitoring, measured by the number of audit committee meetings per year, on the incidence of restatement were moderated by firm characteristics. They found that under conditions of high firm-level complexity, greater audit committee meetings per year reduced the likelihood of restatement.

Moderating effects of industry characteristics

In terms of reviewing relationship 4, about how industry characteristics alter the relationship between board characteristics and misconduct, Ndofor et al. (2015) also investigated the moderating effects of industry complexity on the relationship between aggressive audit committee monitoring and misconduct, finding a nonsignificant interaction effect when considering industry complexity. However, as described earlier, Cumming et al. (2015) considered how the industry’s male-dominated nature could influence the relationship between board gender diversity and securities fraud. Considering joint effects, He and Yang (2014) found that the positive relationship between audit committee independence and earnings management found in unregulated industries was weakened in regulated industries. They also found that audit committee members’ average number of directorships was positively related to earnings management in regulated industries but negatively related in unregulated industries.

Moderating effects of institutional environments

One could consider how factors from the broader institutional environment, such as national legal systems, norms, and cultures, also act as moderators (relationship 5), such as critical cultural aspects, including power distance, masculinity versus femininity, and so on. As we noted earlier, research has begun to consider the antecedents of misconduct in contexts outside of the United States (Hass et al., 2015; Sáenz González & García-Meca, 2014). However, little research has examined the contingencies of national institutional characteristics. One exception is the meta-analysis by Neville et al. (2019), who found that the strength of the relationships between independence and CEO–board chair separation and misconduct are contingent upon the level of corruption characterizing the country from which the data come, with the relationship weakened in countries with greater corruption.

Future Research Opportunities

Our synthesis of the literature on director and board antecedents of misconduct reveals three key opportunities that should frame the future research agenda on the governance antecedents of misconduct. The first is the need for a finer-grained approach to the misconduct construct, which could help to resolve inconsistent findings. For example, as mentioned earlier, while some studies have shown a negative influence of board independence on organizational misconduct, other studies have shown positive associations. The second is the need for multilevel theorizing about the individual- and organization-level processes and factors that culminate in misconduct. Last, the literature would benefit from greater use of qualitative methodologies.

Misconduct Construct

To start, our review suggests that, especially across fields, many different types of events are being studied as “misconduct.” While these events may align with existing definitions of the construct, it is not clear that they all have the same relationship to governance. For example, although governance affects a range of organizational outcomes, the tools available to a board for averting fraudulent reporting or earnings management may differ in important respects from those that impact product failures or employee mistreatment. Thus, it is perhaps not surprising to encounter inconsistent findings regarding how director or board attributes relate to the incidence of misconduct. Indeed, the findings of existing research, in aggregate, do not show uniform support for the relationships illustrated in Figure 1. It is worth noting that the studies we reviewed focused on fraud or integrity failures, and we did not find any studies of board antecedents for the other categories of misconduct. It is critical that future research continues to unpack the ways that different governance practices, attributes, or director characteristics influence different types of misconduct, rather than treating misconduct as a monolithic phenomenon. In that sense, it is important to understand if processes that lead to one type of misconduct also give rise to other types of misconduct or if the processes are distinct for each kind of misconduct. For example, it is yet to be examined whether the governance factors that predict fraud also influence other types of misconduct in the same way, such as a competence failure like a product recall (Paruchuri, Pollock, & Kumar, 2019). Also, different practices or director attributes may differentially predict involvement or vulnerability to director deception by executives. A rigorous theoretical treatment that develops the key dimensions of the construct and how they are linked to governance practices would also likely reconcile some of these inconsistent results and identify other critical contingencies upon which relationships are bound.

Multilevel Theorizing

Beyond the need for clarity regarding the organizational misconduct construct itself, as an organizational phenomenon, it is important to remember that misconduct emerges from organizational processes (Allison & Zelikow, 1999; March & Simon, 1958). As such, the blame for misconduct can rarely be placed on a single individual—thus the need for multilevel theorizing. Coleman’s (1990) “boat model” provides a good starting point for multilevel analyses because its situational and transformational mechanisms connect macro- and micro- or meso-level work. Situational mechanisms involve the contextualization of micro or meso dynamics, while transformational mechanisms explore how dynamics at the individual (i.e., director) or group (i.e., committee, board) level aggregate to explain collective outcomes (e.g., board composition). This model suggests that the board actions leading to the occurrence and type of misconduct comprise a multilevel phenomenon. The situational mechanisms suggest that board attributes or actions would lead to, for example, cognitive understandings among firm executives and employees about the norms and culture in the organization. The action-formation mechanism suggests that these cognitive understandings of firm executives and employees cause them to behave in specific ways. Finally, the transformational mechanism suggests that these individual behaviors aggregate to become organizational misconduct. Yet, the current research has not delved very deeply into these mechanisms, and shedding light on these mechanisms not only would enrich our theoretical understanding of the pathways of board influence on misconduct but also would generate insightful practical implications for averting misconduct.

Empirical Approach

The empirical measurement approach in the existing literature has also rarely received multilevel consideration. The extant literature tends to treat individual characteristics or measures created from the composition of members as board attributes and has neglected the richness of measuring board attributes based on multilevel notions, such as “global” measures and “composite” measures. Some studies, such as those on interlocks, have considered the board’s global measure, but current research has not yet examined the joint effects.

Building on these ideas, another significant aspect regards board versus individual director influences. For example, studies have considered the presence of a director with accounting expertise (Krishnan et al., 2011) as a board characteristic rather than how a specific individual with different attributes impacts board processes. Directors, as individuals, vary across many important characteristics, including demographics, experience, personality, and attitudes, among others. We expect that these individual attributes could shape organizational misconduct in pathways that go beyond their effect on board dynamics. Investigating such pathways would show the effects that individual directors could have through boards and through other mechanisms and could reveal avenues for research on understanding the independent and joint effects of all pathways.

Turning to research methodologies, the studies presented in this review are primarily quantitative analyses. While testing the prescriptions of agency theory using quantitative empirical analysis may be adequate, other methodologies, such as inductive approaches or qualitative comparative analysis (QCA), could aid in the development of new insights into the relationships between director and board characteristics and misconduct characteristics. Specifically, future research can gain important insights into the processes and procedures that occur within the black box of corporate governance. Qualitative analysis can investigate the meetings, relationships, and attitudes of boards and individual directors to consider the behaviors that precipitate misconduct. Such analyses may result in novel theory regarding organizational misconduct and the role and impact of the board in this context. Similarly, studies using QCA can investigate how the combination of different attributes—firm attributes, board attributes, or individual attributes—is associated with outcomes that are not visible when studying these attributes in isolation. Future studies can continue to unpack how different combinations of attributes or practices can exacerbate or mitigate the occurrence of organizational misconduct. This is important to producing actionable insights that can support better governance outcomes.

Other Themes

In addition to these major themes, there are other opportunities for future research. With regard to empirical settings, research could also expand the empirical investigation into different contexts. As noted earlier, few studies have considered how institutional context, such as the firm’s national origin, or corporate culture (Hutton, Jiang & Kumar, 2015), such as political ideology, may serve as contingent factors in the relationship between director and board characteristics and misconduct. Legal systems, contract enforcements, and social dynamics are almost certain to vary across countries, so these relationships warrant examination across different national contexts. Future studies can test existing theoretical prescriptions in alternate contexts and build new theory in corporate governance contingent on the nation in which the study takes place. For example, directors’ assumptions about their roles on the board of directors may vary by national context, but current research has not explored that potential. Such differences in perspective may manifest as different attitudes and processes to safeguard against misconduct. Further, there may be specific misconduct behaviors that are unique to specific national contexts. Considering the importance of social arbiters’ judgment of the behavior to cross the line between right and wrong (Greve et al., 2010), scholars in this area must consider the potential that behavior in one context that is considered misconduct may not be condemned so harshly in another. Thus, the board of directors in one context may be more concerned with one type of behavior compared with others, with theoretical implications regarding the role of the board with respect to preventing misconduct.

Last, we note the research opportunities with regard to spillovers (Paruchuri & Misangyi, 2015). Studies have considered how misconduct behavior spreads from organization to organization, often considering the network effects of board interlocks as a mechanism through which misconduct diffuses (Omer et al., 2020; Surroca et al., 2014). Future research could also investigate how this contagion is affected by the relationships presented in Figure 1. For example, one could investigate if the misconduct occurred internally or through contagion as an outcome and investigate which relationships in Figure 1 predict this outcome. Additionally, researchers can consider what types of misconduct spread through social contagion or the types of misconduct that diffuse through different types of relationships. An understanding of social dynamics and how governance factors play into the contagion of negative behaviors is important for research and practice regarding the role of the board in preventing organizational misconduct.

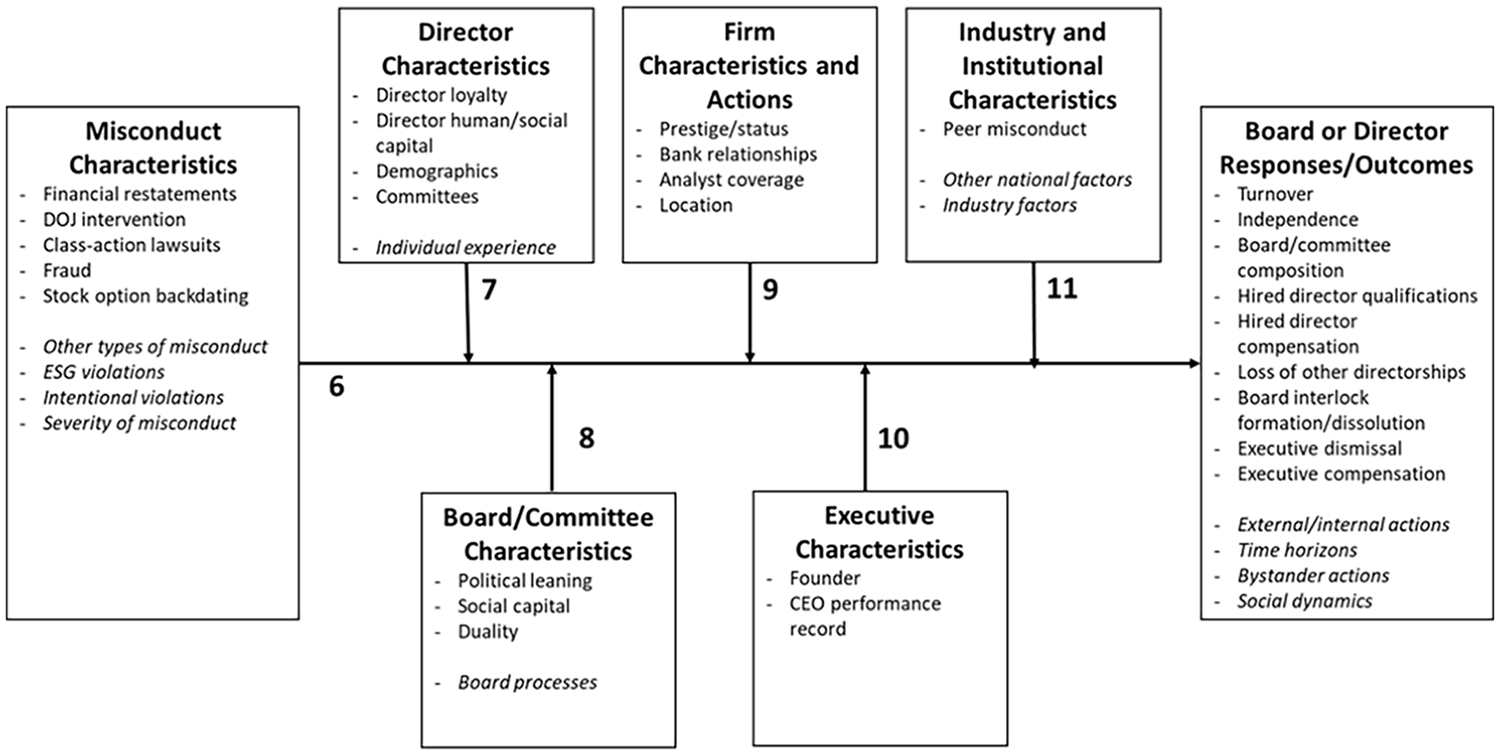

Governance Under Failure: Board and Director Actions and Outcomes in Response to Organizational Misconduct

Integrative Themes

A substantial body of research has explored actions taken by and consequences to boards of directors or individual directors in the context of organizational misconduct revelations. We review these studies under the rubric of governance under failure.

Several themes emerged in our review of studies focused on governance under failure. The first theme emerged in terms of the limited yet disjointed theories and mechanisms applied to explain the actions and consequences. Research on board and director responses has primarily drawn upon agency theory, resource dependence theory, and social network theory (Withers, Howard, & Tihanyi, 2020), even though other theories such as identity theory (Hillman, Nicholson, & Shropshire, 2008; Withers, Corley, & Hillman, 2012) and self-determination theory (Boivie, Graffin, & Pollock, 2012) are also occasionally used. The mechanisms employed to explain the actions generally include settling up (Naumovska et al., 2020; Wowak, Hambrick, & Henderson, 2011), threat management (Park, Boeker, & Gomulya, 2020), and stigma by association or negative spillovers (Marcel & Cowen, 2014). Occasionally, studies have also weighed the costs of replacing versus retaining (Beneish, Marshall, & Yang, 2017) and personal integrity signaling (Cline, Walkling, & Yore, 2018) as explanations. Some of the studies using reputational penalties and settling up are focused on penalties to executives and in executive labor markets (Arthaud-Day, Certo, Dalton, & Dalton, 2006). However, aside from Wiesenfeld, Wurthmann, and Hambrick (2008), the studies we reviewed seldom delved deeply into how the settling-up process might function.

A second theme emerged in terms of the narrow set of actions or outcomes considered. This research has predominantly focused on executive, CEO, or director turnover (Arthaud-Day et al., 2006; Boivie et al., 2012; Cowen & Marcel, 2011; Desai, Hogan, & Wilkins, 2006; Leone & Liu, 2010; Wiersema & Zhang, 2013; Withers et al., 2012). However, several scholars have also started to branch out and examine executive and director compensation changes (Cline et al., 2018; Ghannam, Bugeja, & Matolcsy, 2019), board adoption of creditor-friendly policies (Ferreira, Ferreira, & Mariano, 2018), and changes to board interlocks (Kang, 2008; Withers et al., 2020). Research has also started to examine not only such implications to directors at the focal firm (e.g., turnover, compensation) but also effects concerning their [potential] director roles in other firms (e.g., gaining or losing directorships at other firms). Most of the actions studied have occurred in a time frame of 1 to 3 years after the misconduct revelation.

To the extent that dependent variables in studies are about aspects not related to directors, such as CEO turnover or executive compensation, we consider them as reflective of board responses. But, when dependent variables are related to aspects of directors, such as director turnover or director pay, these studies could be considered as studying both board responses and outcomes to the individual director. We do so because information is not available to tease out board responses from individual outcomes in these cases. For example, because information about voluntary versus involuntary turnover of directors is not available, it is hard to tease apart if the director turnover is a response by the board to misconduct (involuntary turnover, making it a consequence faced by an individual director of board action) or a response by individual directors (voluntarily distancing themselves from the misconduct firm, making it their own individual response). The study by Marcel and Cowen (2014) is an exception, where they developed an approach to cleverly make this distinction through considering director resource provision.

Another theme emerged with respect to the limited types of misconduct studied. As with the literature on antecedents, the research on board and director reactions and outcomes has also tended to focus on a narrow range of organizational financial misconduct, such as option backdating and reporting irregularities (restatements). However, several authors have begun to expand the horizons by examining misconduct other than financial misconduct, such as the personal indiscretions of CEOs (Cline et al., 2018).

In terms of research methodologies, like the research on antecedents, most of the research on board and director responses and outcomes has taken the approach of deductive theorizing and quantitative empirical investigation. While an occasional theoretical paper was noted, none used qualitative approaches to induce theories, and none used other approaches, such as QCA.

Last, because boards consist of a group of individual directors, the study of board responses to misconduct is inherently a multilevel phenomenon, but it has not been examined as such. Yet, we note that many board- and committee-level characteristics were derived from director personal characteristics. Further, personal characteristics are combined across individuals to yield board- and committee-level “composite” constructs. However, studies focused on “global unit level” characteristics of boards are sparse (Caskey & Laux, 2016).

Organizing Framework

To build the landscape of our review, we organized individual studies in this domain into a framework shown in Figure 2. The fundamental question is whether misconduct firms’ directors or boards take actions or face consequences that are distinct from those of other firms’ directors or boards (relationship 6). However, much of the research in this area goes beyond this fundamental question by examining how the association of organizational misconduct characteristics with director or board reactions or outcomes is altered (moderated) by different categories of constructs. Figure 2 illustrates moderators such as director characteristics (relationship 7), board or committee characteristics (relationship 8), firm characteristics (relationship 9), executive characteristics (relationship 10), and industry and broader institutional characteristics (relationship 11).

Main Effects

We note that the direct association between misconduct characteristics and responses of or outcomes for boards and directors (relationship 6) is by far the most studied relationship in Figure 2. Much support has been found for the argument that firms enduring governance under failure take board-level actions and experience board-level outcomes that are distinct from those of nonmisconduct firms.

Outcomes for turnover

Regarding actions such as dismissals and/or turnover of directors, Arthaud-Day et al. (2006) showed higher turnover among the corporate directors and audit committee members in misconduct firms compared with other firms (i.e., presence vs. absence of misconduct). Similarly, Desai et al. (2006) found, in a matched sample of restating and nonrestating firms, that restating firms not only had higher CEO dismissal rates but also increased the number of outside directors on the board after restatements. In a different type of misconduct context (Department of Justice interventions), Heese, Krishnan, and Ramasubramanian (2021) found that such interventions resulted in higher board turnover and increased board independence. Additionally, Fich and Shivdasani (2007) observed no abnormal increase in director turnover linked to filing of class-action lawsuits alleging financial misrepresentation but found strong evidence of some costs borne in that they observed a reduction of 50% in future directorships held, and 96% of the directors who served on at least one other board lost at least one directorship within 3 years of the lawsuit. Importantly, the losses were worse for more serious cases of alleged fraud.

Outcomes for hiring and compensation

In complementing this understanding of dismissals and turnovers among corporate elites, other research has focused on hiring and compensation. Misconduct revelations often provoke calls to tighten oversight through changes in board and/or committee characteristics. For example, Caskey and Laux (2016) investigated how misconduct revelations led to boards and audit committees with higher proportions of outside directors and directors with financial expertise. Additionally, Ghannam et al. (2019) found that boards of firms enduring governance under failure hired directors with certain qualifications (accounting or legal experts) and experience (prior board experience) and provided these directors higher compensation compared with other firms. Similarly, Ferreira et al. (2018) found that firms were likely to appoint directors with links to creditors after debt covenant violations.

Outcomes for network changes

Extending these studies further, research has examined how governance under failure alters the network structure formed by directors serving on multiple boards. For example, Withers et al. (2020) examined how financial restatements influenced subsequent board interlock formation among Fortune 500 firms. They found that restatements frequently disrupt network ties, but the effects are reduced by social status. Additionally, Lungeanu, Paruchuri, and Tsai (2018) found that the CEOs extend their network ties by joining philanthropic boards after misconduct in order to repair their reputation and legitimacy.

Outcomes for executives

Several studies have also examined the responses of boards but do so in terms of consequences to other actors, such as executives. For example, Conyon and He (2016) studied corporate fraud in China and showed that boards penalize CEOs who commit fraud with lower pay and higher likelihood of turnover, depending on the severity of the fraud. Arthaud-Day et al. (2006) also found that C-suite executives, such as CEOs and CFOs, had a higher turnover in the 2-year postmisconduct period for perpetrator firms compared with other firms. They specifically found that CEOs and CFOs of restating firms, respectively, were 135% and 105% more likely to experience turnover than their counterparts in control firms.

Joint Effects

Research has also examined how the actions of and outcomes to boards and directors are shaped by director characteristics, board characteristics, firm characteristics, and executive characteristics. We summarize research on each moderator next.

Moderating effect of director characteristics

Illustrating how the director characteristics influence board reactions and outcomes of misconduct (relationship 7), Gomulya and Boeker (2014) found that CEO dismissal after financial restatements is shaped by director characteristics. Specifically, they found that directors who are more loyal—indicated by being inside directors or having been appointed by the CEO—tended to shape CEO replacement in the context of restatements. Marcel and Cowen (2014) found that directors with low human and relational capital tended to be replaced after an organizational fraud was revealed. They specifically found that directors with lower relational capital or lower human capital, in terms of business expertise and professional specialization, had higher turnover likelihood after organizational misconduct revelations. Using this distinction of high versus low resource provision, the authors theorize whether the turnover was voluntary. Similarly, Naumovska et al. (2020) argued that while directors suffer reputational damage in the context of organizational misconduct, some directors suffer more than others. The legitimacy resources provided by female and/or minority directors are somewhat protected by their rarity. Further, firms confront socioeconomic pressures to remedy the long-standing discrimination faced by female and minority directors, also reducing the extent of “settling up” (Fama, 1980) that they endure when their organizations are involved in misconduct. The authors term this effect “reputational immunity.” Indeed, they found that female or ethnic-minority directors experienced different levels of turnover, compared with male or nonminority directors, following organizational misconduct. Additionally, Ertimur, Ferri, and Maber (2012) considered whether directors were held accountable in the options backdating scandal of 2006 to 2007. They concluded that directors who served on compensation committees of backdating firms had more director election votes withheld and more turnover, especially in more severe cases of option backdating. The evidence, however, was not strong enough to conclude that the reputational penalties affected the behavior of the directors. Last, Beneish et al. (2017) found that the likelihood of board response (e.g., CEO dismissal) following a misconduct event was higher if there was a readily available potential replacement serving on the board of directors (based on director characteristics).

As a theoretical example of this relationship, Wiesenfeld et al. (2008) note the widespread theoretical explanation for how misconduct leads to a settling-up process but also note the exceptional heterogeneity in the reputational penalties paid by directors associated with the misconduct. The authors focus on organizational “failures,” but their approach to that construct encompasses most mainstream definitions of misconduct. They develop a dynamic model of the stigmatization process to explain the heterogeneity in penalties paid by executives and directors. In their approach, the settling-up process is driven by social arbiters who engage in “constituent-minded sensemaking” to determine the executive’s or director’s culpability for the failure. This is a rare theoretical article, and hence the empirical testing of these ideas is left to others.

Moderating effects of board characteristics

Research has also examined how board characteristics affect the board’s reaction to misconduct (relationship 8). For example, Park et al. (2020) found that the values and beliefs of the board shaped whether it took action against the CEO for the organizational misconduct. Focusing on board-level political ideology among S&P 1500 firms with restatements, they found that politically conservative boards are more likely to hold their CEOs accountable and fire them compared with politically liberal boards. Nguyen, Hagendorff, and Eshraghi (2016) found that the relationship between organizational misconduct and CEO dismissal was influenced by board monitoring. In considering director turnover, several studies have sought to examine why some directors are more likely than others to experience turnover (Cowen & Marcel, 2011; Naumovska et al., 2020; Wurthmann, 2014). For example, Cowen and Marcel (2011) showed that dismissal varied with the board’s social capital—boards with moderate levels of capital were most likely to part ways with a colleague because the legitimacy of such boards was more likely to be affected by affiliation decisions than that of very high- or low-capital boards. Last, Conyon and He (2016) showed that the misconduct firms’ boards imposed penalties on CEOs who committed fraud, in terms of lower pay and higher turnover, without CEO duality but not in cases of CEO duality.

Moderating effects of firm characteristics and actions

In examining how firm characteristics and actions shape board reactions to misconduct (relationship 9), Boivie et al. (2012) enriched their finding that firms experienced director turnover in the wake of events that tarnish the organization’s image, such as organizational misconduct, by examining the moderating effects of firm-level prestige. They found that director departure from boards after misconduct increased for prestigious firms but not for nonprestigious firms. Additionally, Ferreira et al. (2018) found that firms that have stronger lending relationships with their creditors appointed more directors after covenant violations than firms without such relationships. Cowen and Marcel (2011) found that firms with greater dependence on external monitors (e.g., security analysts) were more likely to dismiss directors that had been associated with misconduct at other firms. Further, using a sample of Chinese firms, Conyon and He (2016) showed that the penalties imposed by misconduct firms’ boards on CEOs who committed fraud, in terms of lower pay and higher turnover likelihoods, depended on the firm being located in a developed region. In a recent study, Burke (2022) theorized that negative media coverage about a firm’s environmental, social, and governance issues influences boards’ decisions to dismiss the CEO, finding that among firms in the top quintile of board independence or where the CEO is also the chair, there was a significant effect of media coverage on CEO dismissal. The author also found direct effects, noting that larger boards were more likely to dismiss the CEO, especially when the CEO was also the board chair.

Similarly, Withers et al. (2020) examined board interlock formation after organizational misconduct (defined as financial restatements). Specifically, they examined interlock formation among the Fortune 500 after misconduct. They show that misconduct firms tend to seek out ties with higher-status firms and leverage shared ties with third-party firms and preexisting relationships to do so. In effect, the firms’ characteristics shape how they formed interlocks with other firms following organizational misconduct.

In an interesting study of consequences to directors in other boards that they serve, we note that implicit in the theoretical treatment of the separation of ownership and control is the effectiveness of the executive and director labor markets. If such markets are efficient, then dismissal from one firm will sharply lower the executive’s or director’s value in other firms. Dou (2017) investigated whether leaving just prior to the announcement of misconduct protects directors in the subsequent labor market—the phenomenon that Jiang, Cannella, Xia, and Semadeni (2017) refer to as “jumping ship.” The Dou study used class-action lawsuits, earnings restatements, sharp dividend reductions, and debt covenant violations as indicators of misconduct. Their evidence supported the assertion that directors who jumped ship tended to lose more of their other directorships and were more often removed from their committee assignments on other boards where they stayed. The penalties were significantly higher than those endured by directors who stayed through the crisis.

Moderating effects of executive characteristics

Research has also started to examine the characteristics of the executives who may be fired or hired by boards in the wake of organizational misconduct (relationship 10). For instance, Leone and Liu (2010) studied board responses to accounting irregularities when the CEO is a founder. Consistent with expectations, they concluded that while accounting irregularities do increase the likelihood that founder CEOs will be replaced (by 29%), the increase is much larger for nonfounder CEOs (49%). Also, in support of scapegoating theory (Boeker, 1992) the study concluded that CFOs tend to bear a greater share of the blame when the CEO is a founder. The study bolsters the idea that directors respond differently to misconduct allegations when a founder is in charge than when a nonfounder is the CEO. Similarly, Beneish et al. (2017) found that CEO turnover was lower following a misconduct event if the CEO was a founder. They also showed that CEO turnover following a misconduct event was 17% more likely if the CEO’s performance track record was poor relative to peers.

Moderating effect of institutional factors

Wiersema and Zhang (2013) is a great example of how institutional factors can shape board reactions to misconduct (relationship 11). They examined how boards responded to misconduct in terms of executive dismissal and found that the institutional context of the firm, captured by the pervasiveness of the misconduct (stock option backdating) and media coverage of it, shaped the board’s response.

Future Research Opportunities

Our review has revealed several research opportunities to further understanding of the reactions of boards or directors to organizational misconduct and consequences to them thereof. As before, we classify them as the need for theoretical development regarding misconduct and governance practices, more multilevel theorizing and empirical testing, and the use of qualitative research methodologies.

Theoretical Development

Once again, some key research opportunities emerge from studying different misconduct phenomena, different actions or outcomes, different time horizons, and different contexts. We called earlier for a deeper theoretical treatment of the organizational misconduct phenomenon, and that call is echoed here. In addition to notions of misconduct specified in the earlier section, prior research has classified organizational misconduct into different categories: intentional versus unintentional, integrity failure versus competence failure, fraud versus accident, and focused versus endemic. Taking these distinctions about the level of intentionality involved as well as whether the misconduct was due to integrity failures versus competence failures is important (see, e.g., Schepker & Barker, 2018). Interestingly, we note the existence of contexts that involve clear-cut misconduct but with potential benefits for investors. For example, earnings management may be beneficial to investors and rarely rises to a level that threatens a response from the Securities and Exchange Commission (SEC) or even the major exchanges. An even more interesting context would involve price collusion with rival firms. This action is clearly illegal and unethical, but it is also has the potential to benefit investors (González et al., 2019). A similar story could be told for institutional investors who seek to invest in a set of rival firms in order to dampen the rivalry among them (Westphal & Zhu, 2019), to the benefit of managers and investors (though likely at significant cost to customers). Deeper theorizing about the organizational misconduct phenomenon may lead to the conclusion that there are many different types of misconduct and at least an equal number of theoretical explanations.

In terms of different actions and outcomes, future research could extend the investigation to examine boards’ externally oriented actions, such as media releases or press conferences, or internally focused behavior, such as changes in the extent of monitoring and/or advisory functions. Regarding time frames, it seems important to consider board actions and outcomes in different time frames (e.g., immediate, short term, and long term following the misconduct). An example of a study that focuses on long-term response is Arthaud-Day et al. (2006), who focus on turnover in the 24 months after the misconduct is revealed. Such turnover may not be initiated by firms in the first week or so. In that sense, the nature or types of responses undertaken, their effectiveness, and associated outcomes may differ with the time frame considered. While not stated, much of the existing research seems to assume (even if weakly so) that reactions will not vary over time. Lacking such research, we also do not know if and how the reactions to organizational misconduct might change over time or how these reactions impact the organization over time. By considering a dynamic time frame for the effects of misconduct on governance, future research can reveal new research questions that consider the efficacy of board decisions over time.

Some of the joint relationships shown in Figure 2 have attracted more research attention than others. For instance, relationship 11, about the joint influences of institutional environmental attributes (e.g., national cultures, institutional norms, industry complexity; see Ndofor et al., 2015), industry gender diversity (Cumming et al., 2015), and misconduct characteristics on board reactions, is apparently the least explored relationship and thus would appear to provide opportunities to shed light on their joint influences. Future studies in alternative institutional contexts can help to test the boundaries of existing theories and/or help build new theory in corporate governance contingent on the nation in which the study takes place.

Multilevel Theorizing and Modeling

In terms of the second major theme, the application of multilevel theorizing is likely to broaden the set of causal factors beyond the board, which at present dominates in the literature. For example, it is possible (and perhaps likely) that some directors may take actions individually, either for the organization or for their own well-being. For example, Gow, Wahid, and Yu (2018) examined how directors can manage the reputational consequences of misconduct through their disclosures. Directors of publicly traded firms must disclose their other business relationships (other outside directorships, for example) on proxy statements when they stand for election by shareholders. The authors show that when a director of one firm also serves on the board of a firm that experienced an adverse event (bankruptcy, SEC litigation, restatement), that director was less likely to report the relationship on other proxy statements, thus helping to limit the reputational damage.

In the aforementioned case, the actions taken by individual directors were entirely self-serving. A parallel story involves Warren Buffet, who joined the board of directors for the investment bank Salomon Brothers in 1987 (along with a sizable investment in the firm) and became board chair and CEO after the departure of John Gutfreund in 1991. Also in 1991, a huge scandal broke where it became clear that Salomon Brothers had engaged in bid rigging for the sale of U.S. treasuries (although the bid rigging did not occur during Buffet’s tenure as chair). Congress could have elected to ban Salomon from future financial dealings (effectively a death sentence) and seemed ready to do so, but Buffet persuaded Congress otherwise. His testimony, before a House subcommittee, began with an apology and then a promise of future action. His promise to Salomon employees included the following: “Lose money for the firm and I will be understanding; lose a shred of reputation for the firm and I will be ruthless” (Udland, 2019). In this example, a single director acted alone and likely saved the company from dissolution.

Future studies should continue to untangle individual director actions from those of the board at large. Doing so will help to develop a stronger understanding of director motivations and board processes and shed light on distinct pathways for individual responses and effectiveness of those corrective actions.

Last, studies of joint influences described in relationships 7 through 11 naturally lend themselves to multilevel theorizing, and a multilevel approach seems essential for developing a more complete understanding of the differential impacts that organizational misconduct has on the board and, subsequently, the firm and its stakeholders.

Empirical Approach

Finally, with respect to analytical technique—the third major theme—like the research on antecedents, the body of existing research in the governance under failure area lacks qualitative or other approaches such as QCA, and most of the research has focused on quantitative empirical analysis. Given the different strengths and weaknesses of different research methodologies, there is a need to investigate the organizational misconduct domain with different research methodologies. For example, the deliberations of boards of directors are nearly always opaque (Boivie, Withers, Graffin, & Corley, 2021), so outside observers have difficulty assigning culpability to individual directors. At the same time, however, the assignment of culpability for outcomes tends to swiftly occur, regardless of the actual role of the accused in the misconduct (Lungeanu et al., 2018). The inability to validly assign culpability to directors surely weakens the governance-correction capacity of factors like settling up and director labor markets. Application of qualitative methods could help to shed light on the hidden organizational processes and linkages among factors that shape boards’ actions in the wake of misconduct.

Other Themes

In addition to the preceding three major themes, two interesting idiosyncratic opportunities were also evident. A promising avenue for research involves other roles of directors. Upper-echelons theory (Hambrick & Mason, 1984) predicts that individual characteristics of organizational leaders will importantly affect choices made by those leaders. The theory could be extended to better understand board and director outcomes following misconduct as well. The literature we reviewed consistently assumed director roles only. That is, no prior research has considered if the outside director of a misconduct firm currently served in an executive role at another firm. Many independent directors are also executives at other firms (Stern & Westphal, 2010). It is well established that executives with external directorships fare better in their executive careers (often with improved job opportunities) than executives who do not serve as outside directors (Boivie, Graffin, Oliver, & Withers, 2016). Moreover, prior research has found that relationships among executives would influence the firm’s engagement in misconduct (Kuang, Liu, Paruchuri, & Qin, 2022). However, the implications of organizational misconduct have not yet been established for the substantial body of directors with ongoing executive roles in other firms. While we acknowledge that the trend is toward reduced external directorships for executives, it is still a significant and prevalent phenomenon, and novel insights could be generated by investigating these aspects.

Another idiosyncratic opportunity is to consider the need to investigate outcomes beyond director and executive turnover. For example, Lungeanu et al. (2018) examined how firms tried to rebuild their reputations after a misconduct event (financial restatements) by the CEOs’ joining boards of not-for-profit organizations (independent foundations). They also show that existing corporate philanthropy and stronger corporate reputations reduce the likelihood of adding board ties to foundations. As described earlier, the social nature of organizations is not excluded from the occurrence of organizational misconduct and the effects associated with it. When a firm is involved in misconduct, its relationships with other firms will also be affected (Jensen, 2006; Withers et al., 2020). Exploring how boards use relationships to rebuild damaged reputations, at the individual or board level, can also expand our understanding of the more distal consequences of misconduct, demonstrating how misconduct at one firm may influence outcomes for others. Furthermore, such analyses can also examine how these actions are influenced by the type of misconduct behavior, including the efficacy of such social actions.

Insights and Implications From Integration of Both Areas

Our review provides a more comprehensive and cohesive view of governance failure and governance under failure. While we have earlier noted the themes and future research opportunities in each of these aspects separately, some themes are common across both domains. For instance, most of the research across these domains has employed deductive theorizing, used empirical testing in U.S. contexts, and has focused on integrity violations.

However, beyond these common themes, there are also opportunities for integration across these domains. First, as we have noted several times before, this research needs multilevel theorizing. For instance, our review found patterns of situational mechanisms by which organizational misconduct alters individual directors’ motives, their reputations, the cost-benefit analysis of serving on boards, and how it shapes these directors’ and other audiences’ differential emphasis on monitoring and resource-provisioning duties (Boivie et al., 2012; Cowen & Marcel, 2011; Naumovska et al., 2020; Park et al., 2020). Our review also found patterns of transformational mechanisms regarding how characteristics or actions taken by individual directors serving on different committees in misconduct firms lead to differential outcomes for their boards but also for interconnected boards (Kang, 2008; Omer et al., 2020). Connecting this multilevel modeling of governance under failure with the multilevel modeling of governance failure will be a fruitful area to increase understanding of how aspects of governance failure can shape multilevel aspects of governance under failure.

Such theoretical integration between the two domains and across levels has the potential to resolve (or identify) contradictions in the literature, bring clarity to when and how director- or board-level interventions will affect misconduct and, going forward, to permit more robust exploration of multilevel dynamics. For instance, research on spillovers of stigma has shown that directors affiliated with tainted directors or misconduct firms also tend to be stigmatized (Kang, 2008). Yet, Lungeanu et al. (2018) found that CEOs of misconduct firms join the boards of philanthropies to regain lost legitimacy. This pattern of findings raises questions about the flow of stigma across levels: Does it flow easily from firms to individuals but less so from individuals to firms? Future research using multilevel approaches will help to clarify such contradictions.

Second, our review also provides a context for integrating the disparate macrolevel theories that currently characterize the work we reviewed, including agency theory, institutional theory, and resource dependence theory. Work in the domain exploring mutual influences of governance and misconduct has started to integrate these diverse perspectives. For example, while agency theory (Fama & Jensen, 1983) and resource dependence theory (Pfeffer & Salancik, 1978) have traditionally been used to explain functions related to directors more generally, research in the misconduct domain has started to integrate them with reputation theories, by emphasizing ex post settling up in labor markets for tainted directors (Pozner, 2008), and with self-determination theory, to explain the intrinsic and extrinsic motivation of directors to engage with high-demand jobs as directors in misconduct firms (Boivie et al., 2012; Harrison, Boivie, Sharp, & Gentry, 2018). Similar forms of theoretical integration have proven fruitful in other areas of governance research and impactful on the trajectory of future work. There are opportunities for much more of this kind of theoretical integration in the misconduct domain. Such integration of theories and theorization could arise when considering different aspects together. For example, theorizing about antecedents typically draws upon agency theory, while theorizing about board reactions often relies upon resource dependence theory or social identification theory. In integrating antecedents and reactions to organizational misconduct, future research will need to integrate theories across divergent domains.

Third, considering the categories of governance failure and governance under failure highlights the need for integrated thinking for empirical testing as well as theoretical modeling. With regard to empirical testing, for instance, research on antecedents shows that certain board or director characteristics predict the occurrence of organizational misconduct, and research on the consequences of misconduct investigates the effects for boards or directors, among others. Integrating these two lines of thought shows that the samples used in studying consequences may be biased, as systematic differences exist between boards that are involved and not involved in organizational misconduct. With respect to theoretical modeling, there is a need to integrate, for instance, how consequences to boards may vary based on the characteristics or actions of existing boards that may have lent themselves to being involved in organizational misconduct. These could take the form of mediation, moderated-mediation, or mediated-moderation hypothesizing.

Fourth, research on misconduct, albeit limited, has also distinguished between misconduct and publicization of misconduct, that is, scandal (Adut, 2005). Because publicization varies by misconduct type, perpetrator, or context, it would be fruitful to explore the role played by boards of directors (their characteristics, compositions, or actions) that would amplify or dampen publicization of misconduct. Further, research could investigate how such publicization of misconduct affects boards (in shaping their actions) and/or consequences to individual directors.

Last, the vast majority of the research we reviewed does not investigate the relative timing of misconduct, actions, and consequences. Taking into consideration this temporal aspect may sharply enrich our understanding of this topic. For instance, typical theorizing about the monitoring function of directors leads to the conclusion that directors of firms at or after the time misconduct is revealed will be penalized. However, changing the relative sequence of these aspects, Dou (2017) found that those directors who departed firms before misconduct was revealed were also penalized. Future research could further theorize about how different sequences of these aspects could involve different processes, dynamics, and outcomes.

Integration With External Corporate Governance

The focus of this review has been on the role of boards and directors in organizational misconduct contexts. That is, our review has focused primarily on corporate governance mechanisms relevant to the board, including factors such as board independence, CEO duality, and director incentive structure. Despite this focus on internal governance mechanisms, the implications for future research that have been drawn in summarizing this work could also be extended to research focusing on external governance factors.

Extant literature acknowledges external governance factors play a complementary and/or a substitutive role in governance. External corporate governance encompasses the mechanisms for monitoring and influencing executive behavior that are outside of the boundaries of the firm, including factors such as the legal system, the market for corporate control, external auditing, rating organizations, shareholder activists, or the media (Aguilera, Desender, Bednar, & Lee, 2015; Bednar, 2012; Daily, Dalton, & Cannella, 2003). These mechanisms theoretically serve as substitutes or complements to ensure that executives act in ways that benefit shareholder interests.

Prior research has begun to examine how external corporate governance factors influence misconduct, similar to relationship 1 in Figure 1. For example, research has examined how financial auditing by external entities may influence the incidence of fraud (Lennox & Pittman, 2010) and how media coverage may influence the board’s decision to dismiss executives following misconduct (Burke, 2022). Interestingly, Shi, Connelly, and Hoskisson (2017) found that external governance mechanisms that may negatively impact executives’ sense of autonomy and intrinsic motivation may actually increase the likelihood of financial fraud.