Abstract

Strategy research usually assumes that displays of weakness are disadvantageous for firms. In this study, we challenge this assumption. We propose that deliberate displays of weakness can help firms preserve stakeholder approval when taking controversial decisions. To test this proposition, we examine the use and effectiveness of organizational supplication in the context of workforce downsizing. Building on impression management theory, we predict that firms portray themselves as weak through downward earnings management before workforce downsizing announcements, and that this supplication tactic helps attenuate investors’ negative reactions. Moreover, we posit that supplication paired with an efficiency-focused verbal justification for the downsizing is particularly effective at attenuating negative investor reactions to downsizing announcements, as an additional verbal justification lends authenticity to the downsizing firm’s supplication attempt. Yet, we also theorize that organizational supplication through downward earnings management is less effective if positive firm evaluations by security analysts and the business media make it appear inauthentic. The empirical analysis of nearly 600 workforce downsizing announcements by the largest listed U.S. firms between 2001 and 2020 supports our theoretical predictions.

Introduction

The academic discourse in strategy research traditionally revolves around showcasing and leveraging organizational strengths (e.g., Ansoff, 1987; Learned, Christensen, Andrews, & Guth, 1969). It largely builds on the premise that appearing weak is detrimental to firms and thus should be avoided. In this study, we propose that the deliberate display of weakness can also be beneficial for firms, specifically when taking controversial decisions or actions. In our theorizing, we build on theory and research on organizational impression management (IM), which has generated valuable insights into how firms can influence stakeholder perceptions in a desirable way by strategically presenting or limiting available information (for reviews, see Bolino, Kacmar, Turnley, & Gilstrap, 2008; Bolino, Long, & Turnley, 2016). Yet, extant work on organizational IM has focused mostly on firms’ attempts to convey positive images to protect against negative stakeholder reactions, for example, through apologies, denials, or excuses (e.g., Elsbach, 1994, 2003; Elsbach, Sutton, & Principe, 1998; Lamin & Zaheer, 2012), the dissemination of positive news (Graffin, Haleblian, & Kiley, 2016; Short & Pfarrer, in press), or other IM tactics that emphasize positive firm attributes and behavior (e.g., Bass, Pfarrer, Milosevic, & Titus, 2023; McDonnell & King, 2013; Westphal & Graebner, 2010; Zavyalova, Pfarrer, Reger, & Shapiro, 2012).

In contrast, negative IM by which firms deliberately try to look bad to attenuate negative audience reactions has rarely been considered (Bolino et al., 2016). The few prior studies on negative organizational IM have focused on the strategic release of negative press releases before CEO stock option grants to reduce the options’ strike price (Quigley, Hubbard, Ward, & Graffin, 2020), the issuance of press releases, conference calls, and earnings guidance to lower analyst forecasts after a firm reported earnings above or below expectations (Washburn & Bromiley, 2014), and the concurrent release of additional negative news to amplify the impact of a negative event (so-called “big bath” or “amplification” tactics; e.g., Elliott & Shaw, 1988; Short & Pfarrer, in press; Walsh, Craig, & Clarke, 1991). While these studies have produced valuable insights into when and how firms deliberately induce or even amplify negative impressions among stakeholders, our scholarly understanding of whether firms also engage in negative IM tactics to attenuate the impact of controversial events is limited. This lack of knowledge is surprising, given that IM theory suggests that the deliberate display of weakness via supplication can be an effective means for firms to preserve stakeholder support (Bolino et al., 2008; Jones & Pittman, 1982; Leary, 1995).

Supplication relates to any attempts intended to elicit support, sympathy, and leniency by “portraying [oneself] as weak” (Bolino et al., 2008: 1082) or “helpless (handicapped, unfortunate)” (Jones & Pittman, 1982: 249). Proactively showcasing weakness via supplication thus constitutes a so far unexplored form of anticipatory IM, that is, “activities that are undertaken in anticipation of, or contemporaneously with, [a negative event]” (Graffin et al., 2016: 234) to influence audience reactions to the event (Elsbach et al., 1998; Graffin, Boivie, & Carpenter, 2011).

The study of supplication is theoretically relevant, in that it addresses the “need for research that broadens our understanding of [negative IM] tactics that are less well understood” (Bolino et al., 2008, 2016: 382). Moreover, knowledge on whether and under which conditions the use of negative IM tactics to convey a weak image reduces negative audience reactions to controversial firm decisions is an important complement to the rich body of literature on the effectiveness of positive organizational IM tactics.

To further our understanding of the use and effectiveness of negative IM tactics, we examine organizational supplication in the context of workforce downsizing. We use workforce downsizing, defined as an “intentional reduction in the number of people of an organization” (Brauer & Laamanen, 2014: 1313), as an empirical context because it elicits negative reactions by a firm’s key stakeholders, most notably investors (Cascio, Chatrath, & Christie-David, 2021; Datta & Basuil, 2015; Datta, Guthrie, Basuil, & Pandey, 2010). A review of prior literature shows that 35 of 39 empirical studies found that investors react negatively to downsizing announcements (see Appendix A). Workforce downsizing thus lends itself to the study of anticipatory, organizational IM attempts. The study of supplication in the context of downsizing is also of considerable practical interest. Downsizing has become a highly prevalent managerial practice in recent years. U.S. technology firms alone laid off more than 257,000 workers in 2023 and 124,000 in the first half of 2024 (Biron et al., 2023; Sayegh, 2024). The total number of job cuts in the United States surged to over 720,000 in 2023, an increase of 98% compared to 2022 and, apart from Covid-19-induced layoffs in 2020, the highest annual total since 2009 (Challenger, Gray, & Christmas, 2024). By examining the use and effectiveness of supplication in the context of workforce downsizing, we thus combine what McNamara and Schleicher (2024) labeled in a recent Journal of Management editorial the “theoretical insights path” and the “phenomenon-driven path” to build a substantive contribution.

Building on IM theory (Goffman, 1959; Leary, 1995; Schlenker, 1980), we posit that firms anticipate negative investor reactions to workforce downsizing and thus engage in supplication by intentionally lowering their performance through downward earnings management before a downsizing announcement. We further predict that supplication by means of downward earnings management is effective at attenuating investors’ negative reaction to downsizing announcements for two reasons: First, supplication makes a downsizing announcement less surprising for investors, as they will anticipate that the firm will announce restructuring measures to address the earnings shortfall. Second, supplication recasts downsizing as a “necessary evil” that a firm is forced to undertake to remedy the earnings shortfall. The decision to downsize thus appears logically compelling to investors, dampening their negative reaction.

As prior IM research “has examined [IM] tactics in isolation when, in fact, it is likely that IM tactics interact in meaningful ways” (Bolino et al., 2008: 1090), we further theorize that supplication is more effective if paired with a verbal justification. In IM literature, justifications are viewed as a form of positive IM, as actors provide explanations for a negative event or decision to escape disapproval (Bolino et al., 2008: 1082). Specifically, we reason that an efficiency-focused verbal justification lends authenticity to the downsizing firm’s supplication attempt and thus further helps attenuate investors’ negative reaction because investors view the downsizing as an appropriate and logically compelling decision to enhance efficiency.

In addition, our work extends established theoretical models of IM (i.e., Gardner & Martinko, 1988; Liden & Mitchell, 1988) by departing from the dyadic perspective on the IM process in prior IM literature and advocating a triadic perspective. Next to actor and audience, we theorize that infomediaries exert an important influence on the audience’s reaction to IM attempts. Specifically, we propose that evaluations of relevant infomediaries which are inconsistent with the impressions conveyed by the firm can lead the audience to deem firms’ IM attempts inauthentic. Hence, we reason that supplication is less effective if security analysts and the business media—key infomediaries for investors—provide positive firm evaluations which disconfirm the weak image conveyed by a downsizing firm. Our empirical findings, based on 598 downsizing announcements by the largest listed U.S. firms between 2001 and 2020, fully support our theoretical predictions.

Our study contributes to IM theory and literature in several respects. Our study’s unique focus on supplication, an unexplored negative organizational IM tactic (Bolino et al., 2008, 2016), allows us to generate novel insights into firms’ use of supplication and its effectiveness in the context of controversial decisions. Counter to the conventional emphasis in strategy research on displays of strength or power, our study reveals that deliberate displays of weakness can also be beneficial for firms. Our study thus uncovers a novel mechanism of how firms can positively bias audience reactions through IM tactics. Our work further extends IM theory and differs from past IM studies by going beyond the prevalent focus on single IM tactics. Our findings imply that the congruent use of negative, anticipatory IM (supplication) and positive, reactive IM (verbal justification) can be a particularly effective strategy for attenuating negative audience reactions.

In addition, our work extends existing theoretical frameworks of IM by considering the influence of infomediaries on the effectiveness of IM. While past IM research has conceptualized IM as a dyadic interaction between actor and audience, we advocate a triadic view which integrates infomediaries into the IM process. Our theorizing and empirical results suggest that the effectiveness of IM attempts hinges on the extent to which evaluations of relevant infomediaries confirm or disconfirm the desired image outcome.

Finally, our work advances workforce downsizing research. While investors’ negative reactions to downsizing are well documented, we innovate by highlighting how firms can effectively inhibit negative investor reactions to a downsizing announcement through supplication. We thereby extend the scarce research on downsizing firms’ IM attempts, which has so far exclusively studied positive IM tactics (e.g., Brauer & Vandepoele, 2024; Nègre, Verdier, Cho, & Patten, 2017; Zdaniuk & Chhinzer, 2019), and further our understanding of the sparsely explored contextual factors affecting investor reactions to downsizing (Datta et al., 2010; Datta, Basuil, & Radeva, 2012).

Background

Investors’ Reaction to Workforce Downsizing Announcements

Over the past 40 years, empirical research has consistently shown that, on average, workforce downsizing elicits negative investor reactions (see Datta & Basuil, 2015; Datta et al., 2010, 2012 for reviews; see Capelle-Blancard & Couderc, 2007; Eshghi & Astvansh, 2024 for meta-analyses). Out of 39 empirical studies (see Appendix A), 35 found negative short-term stock returns around downsizing announcements (e.g., Brauer & Zimmermann, 2019; Hillier, Marshall, McColgan, & Werema, 2007; Lee, 1997; Nixon, Hitt, Lee, & Jeong, 2004; Worrell, Davidson, & Sharma, 1991). 1 A primary explanation for investors’ negative reaction is that workforce downsizing incurs substantial direct and indirect costs (e.g., Brauer & Zimmermann, 2019; Capelle-Blancard & Couderc, 2007; Datta et al., 2010, 2012; Eshghi & Astvansh, 2024). Direct costs include severance payments, outplacement service costs, or expenses for early retirement plans (Cascio, 1993; Cascio et al., 2021; Nixon et al., 2004). Due to these substantial one-off costs, it often takes significant time before the expected cost savings materialize. In fact, the more extensive the downsizing the longer it generally takes for any positive impact to be reflected in the firm’s reported earnings. Investors have thus been found to react particularly negatively to large-scale downsizing (e.g., Brauer & Zimmermann, 2019; Lee, 1997).

Importantly, research has further argued and found that the indirect costs of workforce downsizing can be even more substantial (Cascio, 2010; De Meuse & Dai, 2012; Gerhart & Trevor, 1996). Indirect costs arise from knowledge losses as well as the disruption of organizational routines (Brauer & Laamanen, 2014; Nixon et al., 2004; Shah, 2000) and, most of all, negative psychological effects on those employees “surviving” the downsizing (Armstrong-Stassen, 1994; Brockner, Spreitzer, Mishra, Hochwarter, Pepper, & Weinberg, 2004; Cascio, 2010; De Meuse, Bergmann, Vanderheiden, & Roraff, 2004). “Survivors” often deal with a range of negative feelings, including guilt, fear, uncertainty, and demotivation, which have been found to lead to decreased job satisfaction, higher employee turnover and absenteeism, and lower job performance (e.g., Amabile & Conti, 1999; Brockner et al., 2004; De Meuse et al., 2004; Kets de Vries & Balazs, 1997; Trevor & Nyberg, 2008).

Due to these significant direct and indirect costs, downsizing is generally a measure of “last resort” (Cascio, 2005: 48) that investors perceive less negatively only in rare cases. Prior research suggests that negative investor reaction is less pronounced if workforce downsizing appears inevitable and well “thought through,” such as if the firm downsizes to stop a downward spiral (e.g., Eshghi & Astvansh, 2024: 798; Datta et al., 2012; Franz, Crawford, & Dwyer, 1998). Further, select studies reveal that investors tend to react less negatively in case a downsizing is temporary (Lee, 1997), forms part of a wider reorganization or restructuring strategy (Lee, 1997; Nixon et al., 2004), or when the downsizing firm provides a verbal excuse (Zdaniuk & Chhinzer, 2019). In total, prior research indicates that downsizing announcements elicit negative investor reactions, although their intensity may vary slightly. This suggests that firms will anticipate investors’ negative reactions and are motivated to use IM tactics to attenuate investors’ negative reactions.

Theory and Hypotheses

Supplication as a Negative, Anticipatory Impression Management Tactic

IM theory suggests that firms use supplication to advertise “weakness or shortcomings” to elicit audience leniency and support (Becker & Martin, 1995; Bolino & Turnley, 1999: 190; Bolino et al., 2008; Leary, 1995; Schlenker, 1980). Yet, empirical research on the use and effectiveness of supplication is scarce, and the few studies on the effect of individuals’ supplication in the workplace context have generated equivocal results. 2 While select studies suggest that supplication elicits supportive behavior by co-workers and helps to avoid undesirable tasks (Berkowitz & Daniels, 1964; Bolino et al., 2016), the majority of studies have found that supplication is associated with negative supervisor performance ratings and co-worker evaluations (e.g., Chawla et al., 2021; Harris, Kacmar, Zivnuska, & Shaw, 2007; Kacmar, Carlson, & Harris, 2013; Turnley & Bolino, 2001). A possible explanation for the predominantly negative findings on supplication is that “employees’ intentionally looking bad in a work setting is very uncommon” (Becker & Martin, 1995: 175; Bolino & Turnley, 1999, 2003), as employees typically want to appear powerful and competent at work. As a result, Turnley and Bolino (2001: 355) conclude that “[supplication’s] ‘desired’ image outcomes are of questionable value . . . in the context of work groups.”

Social psychology research offers further explanation for the ambiguous findings in individual-level IM literature on the effectiveness of supplication in the workplace context. Experimental findings suggest that displays of weakness are most effective if used in the context of failure or crisis (e.g., Crant & Bateman, 1993; Gibson & Sachau, 2000; Kowalski & Leary, 1990; Leary, 1995; Schouten & Handelsman, 1987). For instance, Gibson and Sachau’s (2000) study suggests that individuals who strategically feign inability prior to failure in a test successfully lower observers’ performance expectations, resulting in more lenient performance evaluations.

To summarize, although IM theory and select individual-level social psychology studies indicate that displays of weakness can be advantageous in specific contexts, the prevalence and effectiveness of intentional displays of weakness by firms remain largely unexplored and ill-understood. To address this void and advance IM theory, we argue in the following that firms frequently present themselves as weak prior to workforce downsizing announcements, thereby effectively mitigating negative investor reactions.

Organizational Supplication in the Context of Workforce Downsizing

Leary and Kowalski’s (1990) seminal process model of IM suggests that IM involves two main components: Impression motivation describes the extent to which actors intend to control how an audience perceives them. Impression construction refers to the specific images that actors aim to project. A firm’s decision to reduce its workforce serves as an appropriate context for this two-component process model. Due to investors’ predominantly negative reactions to workforce downsizing announcements, firms are strongly motivated to utilize IM tactics to avoid significant share price declines (Gardner & Martinko, 1988; Leary & Kowalski, 1990). Supplication appears an effective IM tactic to do so. As noted above, investors respond less negatively to downsizing when it appears necessary or inevitable (e.g., Datta et al., 2012; Eshghi & Astvansh, 2024; Franz et al., 1998; Iqbal & Shetty, 1995). A low-cost way for firms to convey this image is through supplication in the form of downward earnings management.

Earnings management refers to discretionary, lawful choices firms make in their financial reporting with the intent to “mislead . . . stakeholders about the underlying economic performance of the company” (Healy & Wahlen, 1999: 368; Chen, Luo, Tang, & Tong, 2015; Davidson, Jiraporn, Kim, & Nemec, 2004). Earnings management is a viable supplication tactic for several reasons: First, “[quarterly] earnings announcements are a dominant source of information in the equity market” (Basu, Duong, Markov, & Tan, 2013: 223). Survey research suggests that for chief financial officers the “two most important earnings benchmarks are quarterly earnings . . . and the analyst consensus estimate” (Graham, Harvey, & Rajgopal, 2005: 5). Abnormal stock volatility and abnormal returns around quarterly earnings announcements further evidence their importance to investors and other capital markets constituents (e.g., Basu et al., 2013; Dunham & Grandstaff, 2022; Nichols & Wahlen, 2004). Second, firms have high discretion over reported earnings and can usually alter them covertly, as it is difficult for investors and other stakeholders to detect earnings management (Graham et al., 2005; Healy & Wahlen, 1999). This makes earnings management a subtle and effective IM tactic.

Although past strategy work has mostly focused on upward earnings management by firms (e.g., Bascle & Jung, 2023; Chen et al., 2015; Davidson et al., 2004), selected studies in accounting and finance have shed light on when and why firms manage earnings downward. We organize this literature in Appendix B. Extant literature suggests that firms use downward earnings management around corporate events to reduce corporate expenses or take a “big bath” (e.g., Francis, Hasan, & Li, 2016; Gong, Louis, & Sun, 2008; Walsh et al., 1991). Building on these empirical insights, we argue that firms also deflate their earnings before downsizings for the purpose of supplication. Supplication is not intended to reduce expenses associated with a corporate event—such as the price of stock repurchases or stock options (Francis et al., 2016; Gong et al., 2008)—but, rather, to attenuate negative stakeholder reactions to the event. Supplication through downward earnings management is also fundamentally different from “big bath” accounting. While “big bath” accounting involves “a purported cleansing of the financial statements” (Elliott & Shaw, 1988: 92) or the release of “many negative announcements concurrently in an effort to clear out all of the firm’s bad news in one big splash” (Graffin et al., 2011: 766), supplication through downward earnings management occurs before a focal negative event and is not intended to “overstate the negativity of the event” (Graffin et al., 2016: 235, emphasis added) but to reduce its negative impact.

In summary, we predict, based on the two-component process model of IM by Leary and Kowalski (1990), that downsizing firms are motivated to utilize supplication through unusually high extents of downward earnings management to present themselves as weak, thereby construing the impression that the downsizing is necessary and inevitable. We thus state:

Hypothesis 1: Prior to workforce downsizing announcements, firms engage in supplication by means of a higher extent of downward earnings management than is predicted by their baseline extent of downward earnings management.

Organizational Supplication and Investor Reactions to Downsizing Announcements

Drawing on IM theory and social psychology research (Fiske & Taylor, 2017; Gardner & Martinko, 1988; Goffman, 1959; Leary, 1995), we theorize next that supplication through downward earnings management attenuates investors’ negative reactions to workforce downsizing announcements because it makes a firm’s decision to downsize less surprising and more logically compelling to investors. Supplication through downward earnings management reduces the negative surprise for investors by serving as an “early warning signal.” Lower-than-expected performance leads investors to anticipate that a firm will take efficiency-enhancing actions, such as workforce downsizing, in the near term. Investors—like all humans—value predictability (Fiske & Taylor, 2017; Miceli & Castelfranchi, 2015), particularly in respect to a firm’s actions and performance (e.g., Brown, 2001; Pan, McNamara, Lee, Haleblian, & Devers, 2018; Skinner & Sloan, 2002). Hence, we predict workforce downsizing announcements preceded by supplication to be received less negatively by investors because they are taken less by surprise.

The second reason why supplication attenuates investors’ negative reaction is that it makes the decision to downsize appear more logically compelling. Given the considerable direct and indirect costs associated with workforce downsizing (e.g., Capelle-Blancard & Couderc, 2007; Cascio et al., 2021; Datta et al., 2010; Nixon et al., 2004), firms need to persuade investors that such a severe restructuring measure is necessary. Supplication in the form of downward earnings management induces the impression among investors that downsizing is necessary to address the earnings shortfall and enhance operational efficiency. As firms usually downsize “with the goal of improving firm [operating] performance” (Budros, 1997; Datta et al., 2010: 282; Guthrie & Datta, 2008), the decision to downsize appears consonant with the wide-spread cognitive schema that downsizing is “a natural, acceptable strategy” to remedy performance shortfalls (McKinley, Zhao, & Rust, 2000: 235). Hence, investors are more likely to perceive the focal workforce downsizing as an appropriate managerial response. Given that greater adequacy and understandability of firm decisions and actions have been argued and shown to result in more favorable audience evaluations (Ashforth & Gibbs, 1990; Elsbach, 1994; Elsbach & Elofson, 2000; Suchman, 1995; Westphal & Graebner, 2010), we expect investors to evaluate workforce downsizing announcements less negatively when firms have engaged in supplication beforehand. Taken together, our theoretical arguments lead to the following hypothesis:

Hypothesis 2: Supplication through downward earnings management is associated with a less negative investor reaction to a workforce downsizing announcement.

Boundary Condition: The Authenticity of Organizational Supplication Attempts

IM theory suggests that authenticity is a key prerequisite for IM attempts to be successful (Gardner & Martinko, 1988; Goffman, 1959; Leary, 1995). Prior IM research has argued that IM attempts are deemed authentic if they are consistent with the actor’s characteristics and reputation, for example, if an applicant with a reputation for competence engages in self-promotion in a job interview (Bolino et al., 2016; Leary, 1995; Roulin, Bangerter, & Levashina, 2015). Similarly, authenticity research has argued that “authenticity is a cross-level mechanism through which organizations and their individual members orchestrate a coherent impression” (Lamertz, 2022: 3). However, while the importance of authenticity for IM’s effectiveness has been conceptually recognized, prior empirical work has omitted to systematically examine whether the authenticity of an actor’s IM attempts constitutes a critical boundary condition (Bolino et al., 2016). To address this gap in IM literature, we theorize next that the extent to which supplication attenuates investors’ negative reaction to downsizing announcements depends on its perceived authenticity. We contend that supplication appears more authentic when a firm’s verbal justification for downsizing aligns with its display of financial weakness. Conversely, we argue that it is perceived as inauthentic if positive evaluations from security analysts and the business media disconfirm its display of weakness.

The interplay of verbal justification and supplication

Justification is a positive, reactive IM tactic aimed to “minimize the perceived negativity of an event” (Bolino et al., 2008; Elsbach, 2003: 307). Prior studies have shown that firms frequently justify workforce downsizing decisions, for example, by stressing the need to cut costs to improve efficiency (e.g., Hillier et al., 2007; Nègre et al., 2017; Zdaniuk & Chhinzer, 2019). Next to the practical relevance of justifications in the context of workforce downsizing, we see theoretical value in considering how a firm’s justification influences the effectiveness of its supplication attempts. Examining the interplay of supplication and verbal justification is theoretically valuable, as prior reviews of IM literature lament that we lack knowledge of “how the use of [IM] tactics in combination influences observer reactions” (Bolino et al., 2008, 2016: 391). In particular, the combination of negative IM tactics (i.e., supplication) and positive IM tactics (i.e., justification) remains unexplored.

We posit that supplication and efficiency-focused verbal justifications can reinforce each other in the context of workforce downsizing. Efficiency considerations and poor financial performance are the most prevalent determinants of workforce downsizing (Cascio et al., 2021; Datta et al., 2010). If a firm acknowledges that it struggles with cost issues and needs to improve efficiency, this reinforces its previous display of weakness and underscores that downsizing constitutes a “necessary evil” to address its earnings shortfall. When paired with an efficiency-focused verbal justification for the downsizing decision, supplication through downward earnings management appears authentic, thereby enhancing its effectiveness in convincing investors of the logical soundness and appropriateness of the firm’s decision to downsize. Hence, we hypothesize:

Hypothesis 3: An efficiency-focused verbal justification by a firm for its workforce downsizing strengthens the attenuating effect of supplication on investor reaction to a workforce downsizing announcement.

The interplay of security analyst and business media evaluations and supplication

Security analysts constantly gather, process, and evaluate information on firms to issue earnings forecasts and recommendations on whether to buy, hold, or sell a firm’s stock. Because of their high perceived expertise, independence, and the fact that their status and career success depend on the accuracy of their assessments, security analysts serve as knowledgeable and trusted experts on a firm for investors (Bascle & Jung, 2023; Brauer & Wiersema, 2018; König, Mammen, Luger, Fehn, & Enders, 2018; Wiersema & Zhang, 2011). Likewise, the business media acts as a key infomediary group for investors by reducing information asymmetry and evaluating firms and their behaviors (e.g., Bednar, 2012; Graf-Vlachy, Oliver, Banfield, König, & Bundy, 2020; König et al., 2018; Oliver, Campbell, Graffin, & Bundy, 2023). Media coverage not only mirrors public opinion but also actively directs stakeholders’ attention to issues, and influences public perceptions of a firm through positive or negative coverage (Bednar, 2012; Graf-Vlachy et al., 2020).

If security analysts evaluate a firm favorably, as evidenced by positive revisions of their stock recommendations, investors assess the firm’s performance to be improving (Barber, Lehavy, & Trueman, 2010; Stickel, 1992; Womack, 1996). Likewise, empirical research suggests that positive media evaluations, as evidenced by the tone of media reports about a firm, indicate sustainable competitive advantages and improving performance (Deephouse, 2000; Graf-Vlachy et al., 2020; Pfarrer, Pollock, & Rindova, 2010; Oliver et al., 2023). In the light of positive security analyst recommendations or positively toned media articles, a firm’s attempt to convey an image of financial weakness through downward earnings management appears inauthentic. As a result, we predict that supplication is less effective in reducing negative investor reactions to downsizing when security analyst recommendations or business media articles on a firm have been positive.

In contrast, we posit that security analysts and the business media can unintentionally offer indirect IM support if their evaluations of the downsizing firm are unfavorable. Negative revisions of analyst recommendations indicate to investors that the firm’s earnings prospects are worsening (Barber et al., 2010; Stickel, 1992; Wiersema & Zhang, 2011; Womack, 1996). Similarly, negative media coverage indicates performance problems and “serve[s] as a powerful signal that current strategies and policies are inadequate and that change is needed” (Bednar, Boivie, & Prince, 2013: 914). Negative security analyst and business media evaluations thus lend greater authenticity to a firm’s deliberate display of weakness through downward earnings management. Therefore, we expect supplication to be more effective at attenuating negative investor reactions to downsizing if security analyst or business media evaluations of a firm have been negative. In sum, we predict:

Hypothesis 4: The more favorable security analysts’ evaluations of a firm prior to its workforce downsizing announcement, the weaker is the attenuating effect of supplication on investor reaction to a workforce downsizing announcement.

Hypothesis 5: The more favorable business media evaluations of a firm prior to its workforce downsizing announcement, the weaker is the attenuating effect of supplication on investor reaction to a workforce downsizing announcement.

Methods

Sample and Data Collection

To test our theoretical predictions, we sampled all downsizing announcements by the 250 largest U.S. firms as identified by Fortune between January 2001 and December 2020. We use the Fortune 250, which is a subset of the Fortune 500 and includes the Fortune 100, for two reasons. First, our study requires that the firms in our sample are publicly listed and extensively monitored by capital markets and the media. These conditions are typically fulfilled by large and visible firms which have stocks that are widely traded, such as the Fortune 250. Second, we chose to base our study on the Fortune 250 to ensure comparability with prior downsizing studies, which have typically utilized Fortune 100, 250, or 500 samples (e.g., Brauer & Zimmermann, 2019; Budros, 1997, 2002, 2004; Chalos & Chen, 2002; Farber & Hallock, 2009; Love & Kraatz, 2009; Wayhan & Werner, 2000). Admittedly, a caveat of this sample scope is that it does not reflect the full variability in firm size among U.S. firms. We sampled the Fortune 250 as of 2001, since that was the first year after the Dotcom crisis and the passing of the Regulation Fair Disclosure Act in 2000—two influential events that altered the composition of the Fortune 250 and the rules for disclosing workforce reductions. We excluded 17 private firms included in the Fortune 250, as stock market data were missing to assess investor reactions. This left us with 233 sample firms.

To identify all the workforce downsizing announcements of our sample firms, we used the “layoffs/redundancies” news category of the Factiva database to collect all news articles on each firm published in the Wall Street Journal, Reuters Newswire, or Dow Jones Newswire. Following past research (e.g., Farber & Hallock, 2009; Schulz & Himme, 2022), we then manually screened the articles’ headlines and abstracts to verify that an article provides actual information on a workforce downsizing event by the sample firm. We only focused on initial downsizing announcements, that is, the first announcement with the earliest date by a firm on a downsizing. We then analyzed these initial downsizing announcements. Specifically, we gathered information on the number and percentage of downsized workers, and how a firm justified its downsizing.

In total, we were able to identify 1,616 initial downsizing announcements by our sample firms. To identify confounding events, we adopted the approach by Graffin et al. (2011, 2016) and McWilliams and Siegel (1997). We screened all press releases by sample firms during the event window using a pre-specified guideline with 23 confounding event types. In line with past IM research (Graffin et al., 2011, 2016), we distinguish between confounding events beyond a firm’s control (i.e., allegations of misconduct, lawsuits) and those under a firm’s control (e.g., dividend, acquisition, or earnings announcements). While we exclude the former, we control for the latter, recognizing they might reflect deliberate IM attempts (Graffin et al., 2011; Jin, Li, & Hoskisson, 2022). As a result of this approach, we dropped 14 observations that were confounded by other downsizings by the same firm and 85 observations that were confounded by events beyond the focal firm’s control (i.e., allegations of misconduct, bankruptcy, class action and other lawsuits). Moreover, we had to exclude 63 downsizings due to missing data on the number of downsized workers and 773 downsizings due to missing data on quarterly financial items (e.g., accounts receivable or property, plant, and equipment), which we needed to calculate the earnings management measure and other control variables. 3 Finally, we excluded 83 downsizings due to missing data on stock returns, security analyst recommendations, or business media coverage. Our final sample thus consists of 598 downsizing announcements by 103 firms. The share of retained observations (37%) compares favorably with similar studies (ca. 30%) that use quarterly financial data to measure earnings management (Chen et al., 2015). The number of downsizings in our sample also still exceeds the average sample size of prior studies (N = 437) on investor reactions to downsizing (see Appendix A). On average, the firms in our final sample downsized about six times during the sample period and dismissed about 2,730 employees per downsizing.

We used Refinitiv Eikon and Compustat to collect quarterly financial data on our sample firms, such as their size, profitability, debt-to-equity ratio, level of diversification, and all balance sheet items needed to calculate our earnings management measure. For data on industry-level workforce reductions, we relied on the U.S. Bureau of Labor Statistics. To obtain press releases around each downsizing, we drew on PR Newswire and Business Wire, the two dominant press release distributors (Graffin et al., 2016; Zavyalova et al., 2012). In line with prior works (e.g., König et al., 2018; Lamin & Zaheer, 2012), we used Factiva and LexisNexis to collect all media reports on our sample firms in the New York Times and Wall Street Journal. We chose to focus on these two general media outlets, as they fit our study’s focus on investors as a general rather than an expert audience (see Hubbard, Pollock, Pfarrer, & Rindova, 2018), and as they are the two top-circulating newspapers in the United States (Wolfe, 2012). Focusing on these leading outlets also helps to avoid the bias from mimetic “pack journalism” (König et al., 2018). In addition, we gathered data on security analysts’ recommendations from Refinitiv I/B/E/S and data on stock prices and market values of our sample firms from the Center of Research in Security Prices (CRSP).

Key Outcome and Predictor Variables

Investor reaction to workforce downsizing announcements

Following prior research on workforce downsizing (Farber & Hallock, 2009; Nixon et al., 2004; Worrell et al., 1991), we conducted an event study to examine the short-term investor reaction to workforce downsizing and computed abnormal returns on our sample firms’ stock during an event window surrounding the initial announcement day of a workforce downsizing (McWilliams & Siegel, 1997). Abnormal returns constitute the difference between the actual return on a firm’s stock and the estimated return calculated via an economic model for the same stock. To derive cumulative abnormal returns (CAR), we then summed up the daily abnormal returns within the event window. Collectively, we assessed the CAR for each of our sample firms by applying the following formula:

where

Supplication

To assess firms’ supplication attempts, we utilize the most prevalent measure to capture firms’ earnings management: discretionary accruals (Dechow, Sloan, & Sweeney, 1995; Healy & Wahlen, 1999; Jones, 1991; Ronen & Yaari, 2008). Accruals (including nondiscretionary and discretionary components) represent differences in reported earnings and balance sheet items that result because the time at which income or expense is recorded and the time at which cash is received or paid for a transaction often diverge (e.g., Chen et al., 2015; Healy & Wahlen, 1999; Ronen & Yaari, 2008). While nondiscretionary accruals are mandatory expenses or assets that have yet to be realized, firms have extensive control over the discretionary accruals that influence reported earnings. Thus, earnings management scholars usually decompose accruals into a nondiscretionary and discretionary component using an estimation model to infer the extent a firm manipulates its earnings (Dechow et al., 1995; Healy & Wahlen, 1999; Jones, 1991). Like prior studies (e.g., Bascle & Jung, 2023; Chen et al., 2015; Davidson et al., 2004; Dechow et al., 1995; Ronen & Yaari, 2008), we calculate discretionary accruals using the modified Jones model. Under the modified Jones model, a firm’s total accruals are calculated as the difference between reported earnings and cash flow. The nondiscretionary part of total accruals increases with sales growth, assets growth, and depreciation expenses, which depend on the value of a firm’s property, plant, and equipment. The difference between total accruals and its nondiscretionary component reflects the discretionary accruals. Following Chen et al. (2015), we estimate the modified Jones model by industry quarter (see Appendix C). As we examine downward earnings management, we only focus on the level of negative discretionary accruals. Accordingly, if discretionary accruals are positive, our key predictor variable supplication is zero. To facilitate interpretation, we use the absolute value of negative discretionary accruals in our analyses. A higher value therefore indicates a higher extent of downward earnings management in the quarter before a downsizing announcement (i.e., Quarter −1; Chen et al., 2015; Gong et al., 2008). 4

Efficiency-focused justification

We measured efficiency-focused (verbal) justification as a dummy variable, which equals one if a firm states in its downsizing announcement that the need to “cut costs,” “improve efficiency,” or “enhance financial performance” motivate the downsizing, and zero otherwise. This measurement follows prior downsizing studies (e.g., Farber & Hallock, 2009; Hillier et al., 2007; Palmon, Sun, & Tang, 1997; Schulz & Himme, 2022) as well as prior research on justifications as a reactive IM tactic (e.g., Lamin & Zaheer, 2012; Marcus & Goodman, 1991; Nègre et al., 2017). To conduct our coding, we followed prior research (e.g., Farber & Hallock, 2009; Lamin & Zaheer, 2012) and first developed a coding guideline in which we defined five types of justifications: enhance efficiency, decline in demand, mergers and acquisitions (M&A), other, and missing. Using this coding guideline, the second author and a trained research assistant read all announcements and carried out the coding, equally dividing the work. The research assistant was provided with the coding guideline, anchoring examples, as well as counterexamples beforehand, and was trained using a random sample of 50 downsizing announcements (about 8% of our final sample). We evaluated interrater reliability using Krippendorff’s alpha, which was equal to 0.93, indicating high agreement between both coders (Hayes & Krippendorff, 2007).

Favorability of security analyst evaluations

To gauge the favorability of security analyst evaluations before downsizing announcements, we use analysts’ stock recommendations (Fanelli, Misangyi, & Tosi, 2009; Wiersema & Zhang, 2011). Consistent with our operationalization of supplication, and consistent with the time intervals in which analysts revise their recommendations, we measure the change of analyst recommendations between the quarter prior to a downsizing announcement (i.e., Day −90 to −1) and the quarter before that (i.e., Day −180 to −91). Following prior research (e.g., Fanelli et al., 2009; König et al., 2018; Wiersema & Zhang, 2011), we relied on the code system provided by Refinitiv I/B/E/S to derive the favorability of security analyst recommendations and classified analyst recommendations as positive (I/B/E/S Codes 1 and 2, i.e., “strong buy” or “buy”), negative (I/B/E/S Codes 4 and 5, i.e., “sell” or “strong sell”), or neutral (I/B/E/S Code 3, i.e., “hold”). To aggregate individual analyst recommendations to an overall measure of the favorability of security analysts’ recommendations, we computed the Janis-Fadner coefficient of imbalance (e.g., Janis & Fadner, 1943; König et al., 2018). In doing so, we calculated the ratio of positive recommendations to negative recommendations in the quarter before a downsizing announcement, while accounting for the total number of analyst recommendations in the same period. From the resulting favorability of analyst evaluations measure, we subtracted a baseline value of the (expected) favorability of analyst evaluations in the 3 months prior to the quarter preceding each downsizing announcement of our sample firms (i.e., Day −180 to −91) to capture the (abnormal) favorability of analysts’ evaluations (König et al., 2018).

Favorability of business media evaluations

In line with prior research (e.g., Deephouse, 2000; König et al., 2018; Pollock & Rindova, 2003), we conducted a content analysis of all articles in the New York Times and Wall Street Journal on each of our sample firms (ca. 60,000 articles) to assess the favorability of business media evaluations before a downsizing announcement. Consistent with our measure for the favorability of security analyst evaluations, we examined all articles in the quarter before a downsizing announcement (i.e., Day −90 to Day −1) and the quarter prior to that (i.e., Day −180 to −91). Following prior media works (Bednar, 2012; Pfarrer et al., 2010; Pollock & Rindova, 2003; Zavyalova et al., 2012), we used the textual analysis software Linguistic Inquiry and Word Count (LIWC), which contains pre-defined and pre-validated dictionaries of words measuring positive and negative tone in a text (Pennebaker, Boyd, Jordan, & Blackburn, 2015), to determine the rate at which positive and negative affective language were reflected in a media article. We coded an article as positive if its affective content was at least 66% positive, and as negative if its affective content was at least 66% negative. We then calculated the Janis-Fadner coefficient to assess the favorability of media evaluations in the quarter prior to a downsizing (Deephouse, 2000; Janis & Fadner, 1943) and derived the (abnormal) favorability of media evaluations in this quarter by deducting the (expected) favorability of media evaluations in a baseline period 3 months before the quarter preceding a downsizing (i.e., Day −180 to −91).

Control Variables

Our first set of control variables relates to the content of firms’ downsizing announcements. Research suggests that as the magnitude of workforce downsizing increases, investor reactions tend to become more negative (e.g., Lee, 1997; Nixon et al., 2004; Worrell et al., 1991). Hence, we control for downsizing magnitude measured as the percentage of downsized employees relative to total employees. Moreover, we account for a firm’s justification for its downsizing, as it has been shown to affect investors’ reaction (e.g., Farber & Hallock, 2009; Nègre et al., 2017; Zdaniuk & Chhinzer, 2019). Following prior research (Farber & Hallock, 2009; Hillier et al., 2007; Palmon et al., 1997), we thus include four binary control variables in all models based on the manual coding of our sample firms’ downsizing announcements reported above: efficiency-focused, demand-focused, M&A-related, and other justification. Each of these binary variables equals one if a firm made use of the respective type of justification and zero otherwise.

Furthermore, we control for the timing of a downsizing announcement and downsizing firms’ press releases and upward earnings management. As investors typically attend less to news that is published on a Friday, firms could use this tendency to avoid a negative investor reaction by announcing their downsizing on a Friday (DellaVigna & Pollet, 2009). Hence, we include a dummy variable that takes on the value of one when a Friday announcement was present, and zero otherwise. Prior research further suggests that investor reaction is influenced by the prevalence of downsizing in an industry (Brauer & Zimmermann, 2019; Lee, 1997). To account for this effect, we follow the approach by Brauer and Zimmermann (2019) to identify industry downsizing waves and include an industry downsizing wave dummy variable in all analyses. The variable equals one if a downsizing is announced within an industry downsizing wave, and zero otherwise. As firms may deliberately disseminate confounding press releases around negative events to influence investor perceptions (so-called strategic noise), we account for the number of press releases, i.e., all positive, neutral, and negative news releases, issued by a firm in the 3-day event window (Graffin et al., 2011; Jin et al., 2022). We also control for the extent of upward earnings management. Consistent with our operationalization of supplication, we measure this variable as the absolute value of positive discretionary accruals in the quarter prior to a downsizing.

Additionally, we consider several firm characteristics which may influence investor reaction to downsizing announcements. As more extensive analyst and media coverage are likely to lead to greater investor scrutiny, we control for security analyst coverage of a firm, measured as the number of security analysts who provide recommendations for the firm in the 90 days before a downsizing announcement, and for business media coverage, measured as the number of media articles published in the quarter prior to each downsizing (Fanelli et al., 2009; König et al., 2018; Wiersema & Zhang, 2011). We also account for firm size measured as the natural logarithm of a firm’s total assets (König et al., 2018; Nixon et al., 2004). We further control for firm performance and firm leverage measured as the quarterly change in a firm’s industry-adjusted return on assets and in its debt-to-equity ratio (Elayan, Swales, Maris, & Scott, 1998; Hillier et al., 2007). Moreover, we account for firm diversification measured as the Herfindahl-Hirschman index of concentration of a firm’s sales (Hou & Robinson, 2006). We measure all firm controls in the quarter prior to a downsizing announcement. Lastly, we include industry and year fixed effects in all our analyses.

Data Analysis

To test Hypothesis 1, we adopt the methodological approach of prior anticipatory IM works (Graffin et al., 2011, 2016) and compare a firm’s extent of downward earnings management in the quarter immediately preceding a downsizing announcement with the baseline extent of downward earnings management in the previous four quarters (i.e., Quarter −5 to −2) using a paired t test.

For our tests of Hypotheses 2 to 5, we use ordinary least squares (OLS) regression analysis with cluster-robust standard errors. As we have pooled cross-sectional data and observe firms only when they downsize, this approach is most suitable (Wooldridge, 2010). Nonetheless, when we re-run our analyses using a random-effects and fixed-effects approach, we obtain fully consistent results. We include robust standard errors clustered by firms to account for heteroskedasticity and multiple downsizings by the same firm. In all interaction tests, we mean-centered the component variables. We examined multicollinearity by deriving variance inflation factors (VIF) for all analyses. The maximum VIF of our key predictor variables is 1.29, and the average VIF in our models is 2.29, suggesting that multicollinearity is not an issue in our models (Chatterjee & Hadi, 2012). Finally, we conducted supplementary analyses to account for endogeneity. Results of a two-stage least squares (2SLS) regression analysis and a Heckman two-stage model fully support the findings of our OLS models and are reported below.

Results

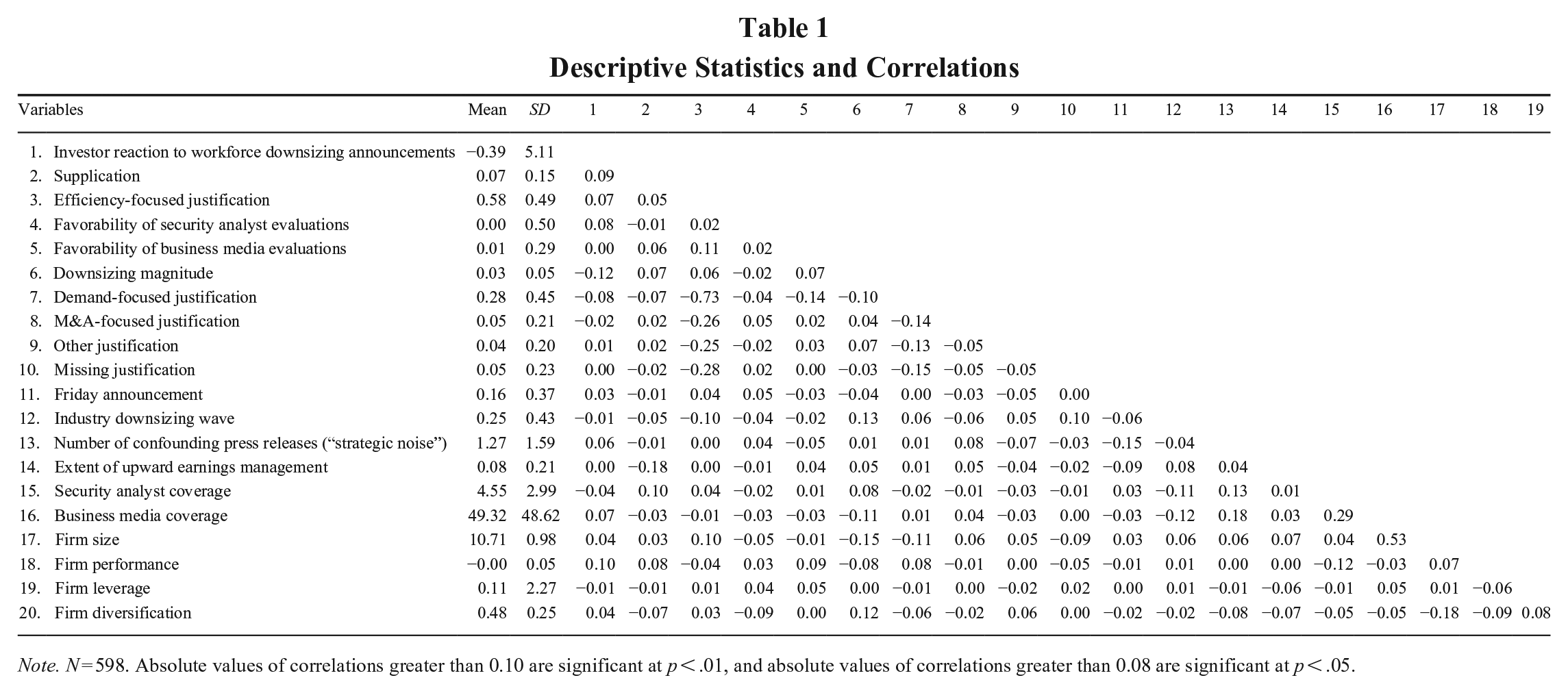

Table 1 presents descriptive statistics and correlations of all variables in our analyses. Consistent with prior research on workforce downsizing (e.g., Datta & Basuil, 2015; Datta et al., 2010, 2012; Eshghi & Astvansh, 2024; Hillier et al., 2007; Nixon et al., 2004; Worrell et al., 1991), we find that the average CAR over the 3-day event window is −0.39%. In line with prior downsizing studies, a t test shows that this negative investor reaction to workforce downsizing announcements is statistically significant (t = 1.85, p = .032). Equally, in line with prior downsizing research (e.g., Brauer & Zimmermann, 2019; Hillier et al., 2007; Lee, 1997; Nixon et al., 2004), we observe that downsizing magnitude is negatively correlated with investor reaction (r = −.12). In contrast, our key predictor variable supplication is positively correlated with CAR around workforce downsizing announcements (r = .09), providing initial support for Hypothesis 2.

Descriptive Statistics and Correlations

Note. N = 598. Absolute values of correlations greater than 0.10 are significant at p < .01, and absolute values of correlations greater than 0.08 are significant at p < .05.

In Hypothesis 1, we argued that firms engage in supplication by means of a higher extent of downward earnings management prior to downsizing announcements compared to the baseline period. We observe that, during the four-quarter baseline period until one quarter prior to the downsizing announcement (i.e., Quarter −5 to −2), the extent of downward earnings management is equal to 0.045. In contrast, in the quarter before a downsizing announcement, the extent of downward earnings management used by our sample firms increases substantially to 0.066, with 291 out of 598 workforce downsizings or 48.7% of all events in our final sample, showing a downward manipulation of a downsizing firm’s reported earnings. Hence, firms engage in about 45% more downward earnings management prior to a downsizing. This difference in the extent of earnings management prior to a workforce downsizing announcement compared to the baseline period is highly significant (t = 3.00, p = .001). Hypothesis 1 is thus strongly supported.

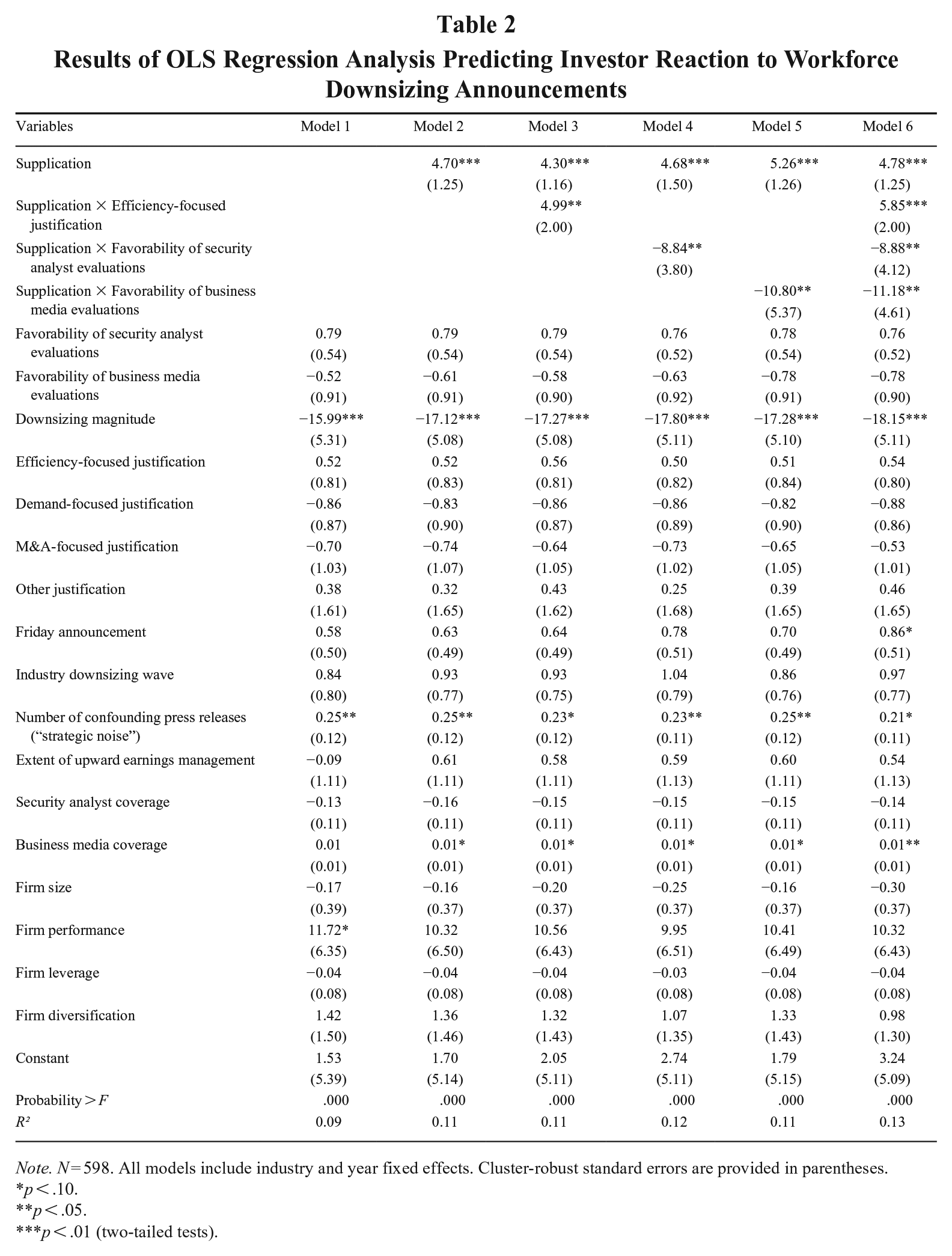

Table 2 presents the results of our OLS regression analyses. As indicated by the F values, all models have adequate fit. We predicted in Hypothesis 2 that supplication by means of downward earnings measurement is associated with a more favorable investor reaction to workforce downsizing announcements. As Model 2 of Table 2 shows, this prediction finds support. Supplication is significantly positively associated with investor reaction (β = 4.70, p < .001). Specifically, results indicate that extensive supplication (i.e., one standard deviation above the mean) is associated with an investor reaction that is 0.28% less negative. This positive “uplift” is economically significant. It corresponds to an increase in market value of $229 million when using the average total market value of $80.7 billion of our sample firms.

Results of OLS Regression Analysis Predicting Investor Reaction to Workforce Downsizing Announcements

Note. N = 598. All models include industry and year fixed effects. Cluster-robust standard errors are provided in parentheses.

p < .10.

p < .05.

p < .01 (two-tailed tests).

As a robustness check, we also tested Hypothesis 2 using 2SLS regression analysis. In the first stage of our 2SLS analysis, we instrumented downward earnings management with the absolute value of average income-decreasing nondiscretionary accruals of industry peers and the log-transformed absolute value of average total accruals of industry peers. Each of these factors might influence the extent to which firms engage in downward earnings management: A higher extent of industry peers’ income-decreasing nondiscretionary accruals enables a firm to use more downward earnings management, because it reduces the firm’s risk of being caught manipulating its earnings (Dechow et al., 1995). In contrast, higher total accruals by peers indicate that earnings management is prevalent within a firm’s industry (Healy & Wahlen, 1999), making it more likely that a focal firm engages in earnings management. Both instruments are strong predictors of firms’ downward earnings management (βDownwardNDA = 0.16, p = .007; βTotalAccruals = 0.06, p = .012) and do not correlate with our dependent variable investor reaction (rDownwardNDA = .03; rTotalAccruals = .03). In the second stage of our 2SLS analysis, we re-ran our test of Hypothesis 2, including the residuals from the first-stage regression. Consistent with our OLS results, we find that supplication is positively related to investor reaction to workforce downsizing announcements (β = 6.48, p = .001). Finally, we performed the Durbin-Wu-Hausman (DWH) test to check if the estimates obtained by the second-stage regression are consistent with our previous results and the residuals are not significantly associated with our dependent variable investor reaction (Semadeni, Withers, & Certo, 2014). We do not find evidence for endogeneity (DWH = 0.88, p = .350), suggesting that the coefficients of our initial models are unbiased and consistent.

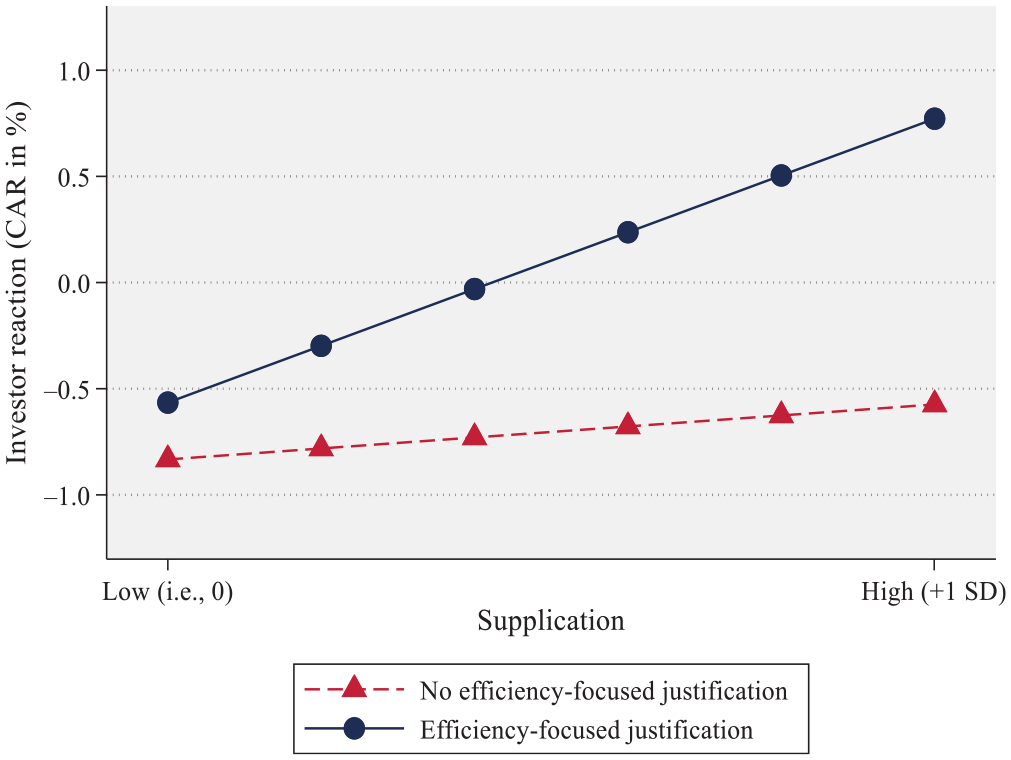

Hypothesis 3 argued that an efficiency-focused justification for a downsizing amplifies supplication’s positive effect on investor reaction to a workforce downsizing announcement. As shown in Model 3 of Table 2, the coefficient of the interaction term is positive and statistically significant (β = 4.99, p = .014), thereby supporting Hypothesis 3. We confirm these effects using a simple slopes analysis. The slope for the effect of supplication is positive and highly significant (p < .001) when the firm offers an efficiency-focused justification, but positive and non-significant (p = .365) in its absence. Figure 1 provides a graphical illustration of the moderating effect.

Moderating Effect of Efficiency-Focused Justifications on the Relationship Between Supplication and Investor Reaction to Workforce Downsizing Announcements

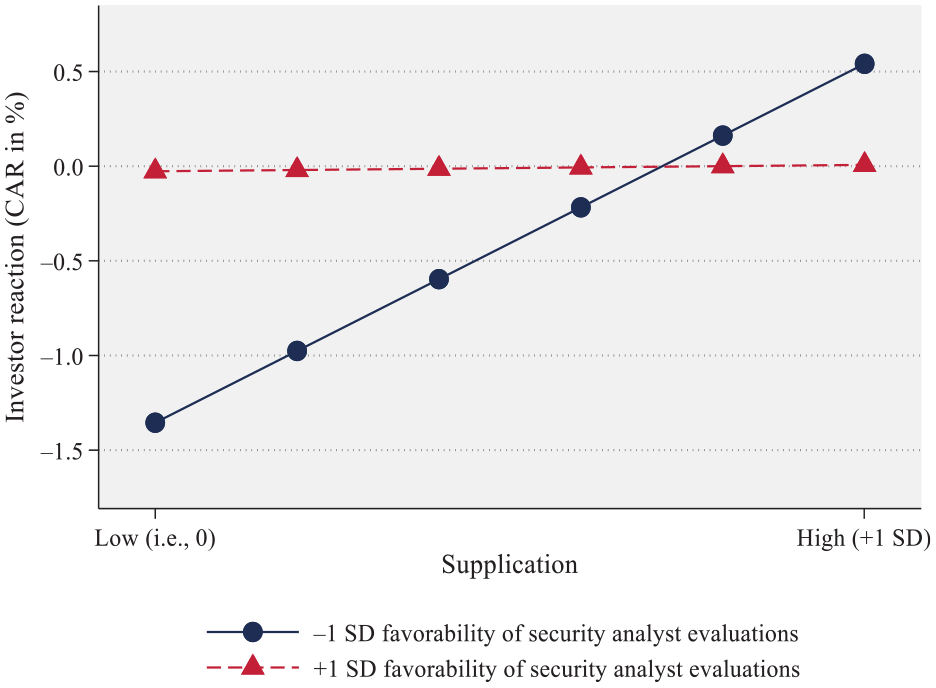

Hypothesis 4 posited that favorable security analyst evaluations attenuate the positive effect of supplication on investor reaction to a workforce downsizing announcement. Model 4 of Table 2 supports this hypothesis, as the coefficient of the interaction term is negative and statistically significant (β = −8.84, p = .022). A simple slope analysis again confirms this finding. Supplication’s effect is positive and non-significant (p = .871) when the favorability of security analyst evaluations is positive (i.e., mean plus one standard deviation), but positive and significant (p = .002) when the favorability of security analyst evaluations is negative (i.e., mean minus one standard deviation). Figure 2 graphically depicts the moderating effect.

Moderating Effect of Favorability of Security Analyst Evaluations on the Relationship Between Supplication and Investor Reaction to Workforce Downsizing Announcements

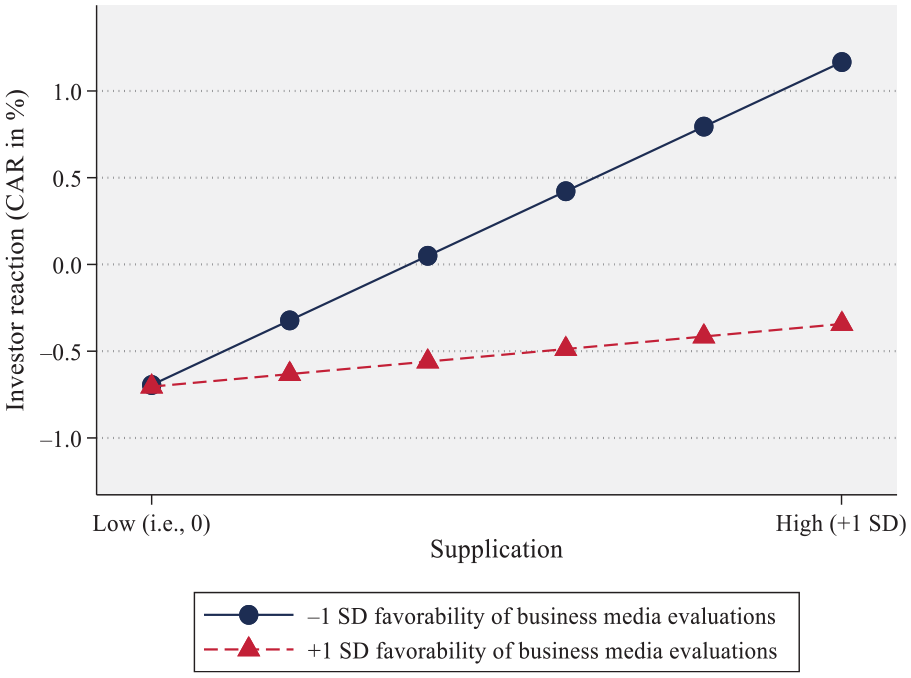

Hypothesis 5 predicted that favorable business media evaluations attenuate the positive association of supplication and investor reaction to a workforce downsizing announcement. As displayed in Model 5 of Table 2, the coefficient of the interaction term is negative and significant (β = −10.80, p = .047). Hence, Hypothesis 5 is also supported. In line with our prediction, the slope for the effect of supplication is positive yet non-significant (p = .166) when the favorability of business media evaluations is positive (i.e., mean plus one standard deviation) and positive and significant (p = .001) when the favorability of business media evaluations is negative (i.e., mean minus one standard deviation). Figure 3 visualizes the effect. Finally, Model 6 of Table 2 reports the full model. The coefficient estimates for all hypothesized relationships remain consistent.

Moderating Effect of Favorability of Business Media Evaluations on the Relationship Between Supplication and Investor Reaction to Workforce Downsizing Announcements

Supplementary Analyses

Next to the 2SLS analysis reported above, we performed several other supplementary analyses to test the robustness of our empirical results. First, we completed additional analyses to corroborate our finding that firms use an unusually high extent of downward earnings management before downsizing announcements, as predicted by Hypothesis 1. Specifically, we tested whether downsizing firms’ downward earnings management is higher than that of non-downsizing firms. We find that the extent of downward earnings management by downsizing firms is substantially higher than the average extent of downward earnings management by non-downsizing firms in the same quarter (t = 6.23, p = .000) and in the previous four quarters (t = 1.78, p = .038). Moreover, we observe that downsizing firms’ downward earnings management in the quarter prior to a downsizing announcement is also significantly higher than their downward earnings management in the previous two or three quarters (t3Q = 1.95, p = .026; t2Q = 1.31, p = .096). In addition, we re-ran our test of Hypothesis 1 using a fixed-effects model. Results show a positive association between the extent of downward earnings management and the likelihood of a downsizing announcement in the next quarter (β = 0.31, p = .044). We also find that a firm’s abnormal extent of downward earnings management, measured as the difference between its extent of downward earnings management and its baseline extent of downward earnings management in the four prior quarters, is a particularly strong predictor of a subsequent downsizing announcement (β = 0.48, p = .015). Collectively, these results provide strong support for Hypothesis 1.

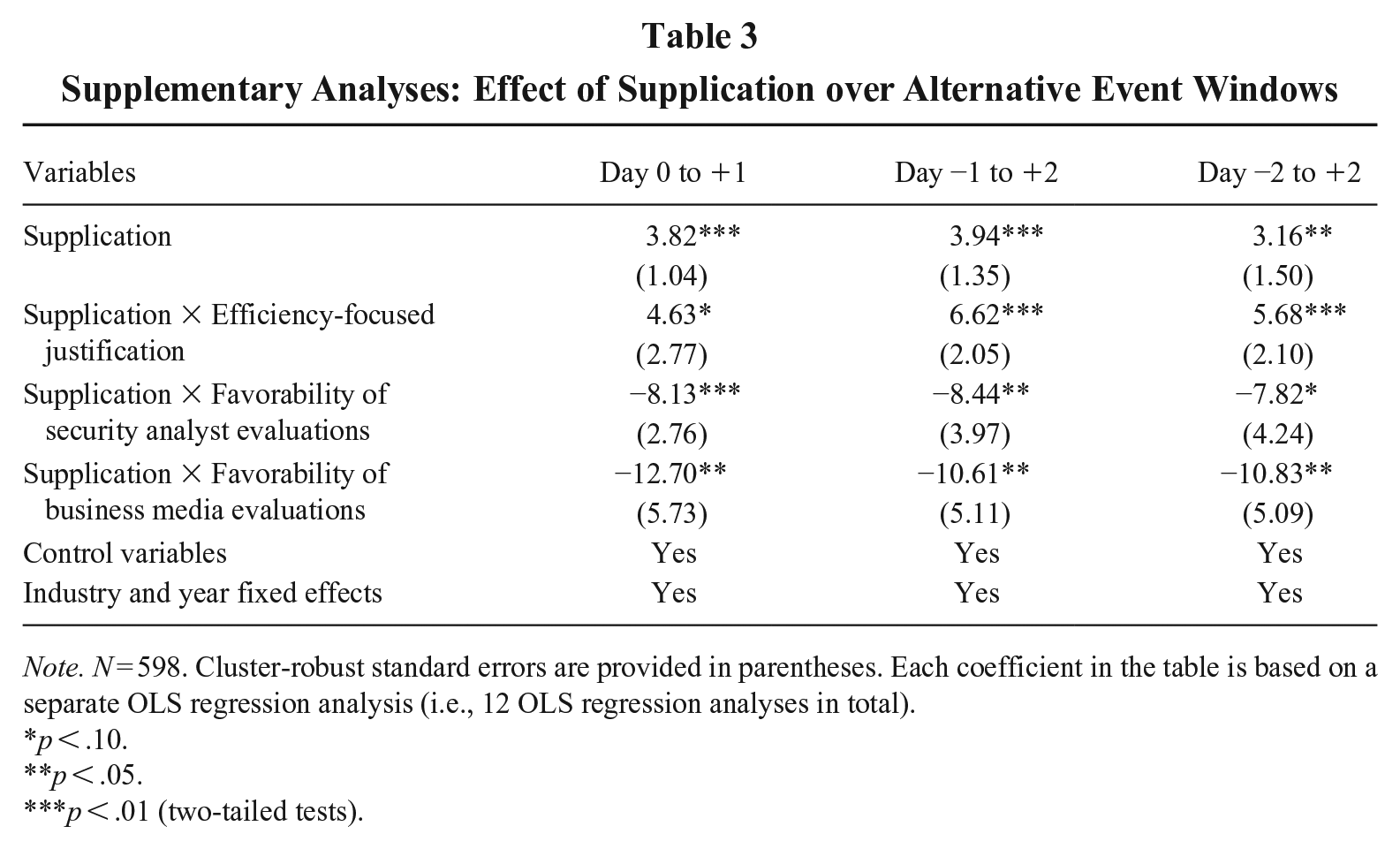

Second, we conducted further analyses to test the robustness of our results for Hypotheses 2 to 5. Specifically, we checked whether our results hold for different event windows (i.e., Day 0 to +1, Day −1 to +2, and Day −2 to +2). Our results are substantively unchanged for these event windows (see Table 3). We also tested whether the choice of the market model for our event study influences our results. We find that our results for all hypotheses remain consistent when we use alternative market models, such as the Fama-French three-factor model (Fama & French, 1993).

Supplementary Analyses: Effect of Supplication over Alternative Event Windows

Note. N = 598. Cluster-robust standard errors are provided in parentheses. Each coefficient in the table is based on a separate OLS regression analysis (i.e., 12 OLS regression analyses in total).

p < .10.

p < .05.

p < .01 (two-tailed tests).

Additionally, we examined the sensitivity of our results to different operationalizations of our key predictor variable. Specifically, we re-ran our test of Hypothesis 2 using the extent to which a firm manages its earnings upward or downward, that is, the level of discretionary accruals, as our key predictor variable. For this analysis, we created a continuous measure where positive values represent cases of upward earnings management and negative values represent cases of downward earnings management. In support of our findings on the effectiveness of supplication, we find that a higher extent of earnings management is negatively associated with investor reaction to downsizing announcements (β = −0.39, p = .026). Additionally, our findings on the effectiveness of supplication remain robust when excluding workforce downsizing announcements preceded by instances of upward earnings management (β = 3.79, p = .004).

Further, we checked if our results hold when we remove our extensive set of control variables. When we re-run our test of Hypothesis 2 without control variables, we continue to observe a positive and significant effect of supplication (β = 2.10, p = .023).

Third, we completed further empirical analyses to rule out alternative explanations for our results. An alternative explanation for our findings may be that variations in investor ownership across downsizing firms lead to differing reactions to workforce downsizing. To explore this possibility, we applied Bushee’s (1998, 2001) established investor classifications, which are widely used in strategy research, to categorize investors as either short-term oriented (“transient”) or long-term oriented (“dedicated”; e.g., Bushee & Miller, 2012; Callahan, Song, Shi, Veenstra, & McNamara, in press; Ekholm, 2006). We then examined whether investors’ reaction significantly differs for downsizing firms predominantly owned by short-term or long-term investors (i.e., mean plus one standard deviation). However, t tests indicate no such difference (tSTvsRest = 0.44, p = .329; tLTvsRest = 0.80, p = .211; tLTvsST = 0.59, p = .278). Our main results also remain unchanged when we control for the ownership share of transient, dedicated, or institutional investors as reported in firms’ 13-F filings. Interestingly, though, we find that supplication is less effective for downsizing firms with a higher share of institutional ownership (β = −19.90, p = .035). Given that institutional investors typically have greater financial literacy and more resources at their disposal compared to retail investors (e.g., Aghion, Van Reenen, & Zingales, 2013; Hansen & Hill, 1991), they are in a better position to accurately assess the authenticity of firms’ supplication attempts.

Furthermore, we explored alternative theoretical explanations for our interaction effects (Hypotheses 3 to 5). An alternative explanation for our interaction results may be that positive firm evaluations by security analysts or the business media, which disconfirm the firm’s display of weakness, create uncertainty among investors, thereby reducing the effectiveness of supplication. To test this possibility, we examined the combined influence of supplication and strategic noise on investors’ reaction. If increased uncertainty were to explain the diminished effectiveness of supplication, then we would expect strategic noise, which increases uncertainty through the deliberate release of confounding news, to reduce the effectiveness of supplication. Yet, we find that strategic noise in fact amplifies the positive effect of supplication (β = 2.50, p = .011). Thus, an uncertainty-based explanation does not seem to account for our empirical findings.

Moreover, one could argue that our set of interaction results can be explained by the fact that a firm’s justification for its downsizing and the evaluations of security analysts or the business media are stronger signals than supplication, thereby amplifying or nullifying supplication’s effect. Yet, empirical results do not support this explanation: neither the firm’s efficiency-focused justification (β = 0.52, p = .527) nor the favorability of analyst or media evaluations have a statistically significant, direct effect on investor reaction (βAnalyst = 0.79, p = .152; βMedia = −0.52, p = .567). In contrast, supplication shows a positive and significant association with investor reaction (β = 4.70, p < .001). Next to this empirical evidence, several theoretical reasons speak against the application of signaling theory, given our research focus on supplication. First, supplication does not qualify as a signal, as it is not costly, which is a key requirement for signals according to signaling theory (Connelly, Certo, Ireland, & Reutzel, 2011). 5 Second, downward earnings management does not meet the requirement of differential accessibility as any firm can use it. Third, the purpose of signals in classic signaling theory (Spence, 1973) is typically to convey positive attributes of the sender to the receiver. In contrast, our study suggests that downsizing firms intentionally display weakness in the form of lower-than-expected financial performance to elicit support and leniency.

Another alternative explanation for our moderating results might be that less favorable evaluations by analysts and the media lead investors to judge the downsizing firm and its leaders as less competent. Yet, this explanation is again at odds with the fact that we do not observe a significant direct effect of the favorability of analyst or media evaluations. To further rule out this alternative explanation, we conducted additional analyses and tested whether a firm’s reputation, as assessed by its inclusion and its rank in the Fortune Most Admired Companies (e.g., Love & Kraatz, 2009; Pfarrer et al., 2010), and its leaders’ competence in creating shareholder value, as measured by total shareholder return in the prior year, affect investors’ reaction to downsizing and supplication. If investors’ competence judgements are the underlying mechanism at play, we would expect firm reputation and prior total shareholder return to be positively associated with investor reaction. Yet, we again do not find evidence for a significant direct effect (βInclusionMAC = 0.21, p = .776; βRankMAC = −0.00, p = .831; βTSR = 1.10, p = .483). Moreover, we find that neither a firm’s reputation (βInclusionMAC = −2.40, p = .563; βRankMAC = 0.07, p = .582), nor its prior total shareholder return (β = −0.78, p = .937) influence supplication’s effectiveness. Collectively, these results suggest that investors’ competence judgments do not explain our interaction findings.

Fourth, besides our 2SLS analysis reported above, we conducted further analyses to address endogeneity concerns. Specifically, we used a Heckman two-stage estimation procedure (Certo, Busenbark, Woo, & Semadeni, 2016) to correct for sample selection bias. In the first stage of the Heckman procedure, we run a probit model predicting the likelihood that a firm engaged in downsizing using total shareholder return, measured as the sum of the percentage change in each firm’s share price and the dividend rate on the same firm’s stock over the previous four quarters, as exclusion restriction. We use total shareholder return as our exclusion restriction, as prior studies suggest that past poor stock performance and declining shareholder value pressurize firms to cut their workforce (Budros, 1997; Datta et al., 2010, 2012). In line with our prediction, total shareholder return is negatively associated with the likelihood of workforce downsizing (β = −0.52, p < .001). It is also not strongly correlated with our dependent variable (r = .01) and the error term in the second stage (r = −.01), thus fulfilling the key conditions for exclusion restrictions (Certo et al., 2016). The weak correlation between the computed inverse Mills ratio and our key predictor variable supplication in the second-stage model (r = .02) further suggests that our exclusion restriction has acceptable strength (Certo et al., 2016). However, we find that supplication is not a statistically significant predictor in the first stage (β = 0.23, p = .141). According to Certo et al. (2016: 2655), this suggests that “sample-induced endogeneity will not create bias.” Nevertheless, when we re-run our analyses including the inverse Mills ratio in our second stage models, we find that our results for all our hypotheses remain fully consistent.

Moreover, we assessed the potential of our results being confounded by an omitted variable by calculating the unconditional impact threshold for a confounding variable (ITCV) (Busenbark, Lange, & Certo, 2017; Busenbark, Yoon, Gamache, & Withers, 2022; Frank, 2000; Lonati & Wulff, 2024). Results from this analysis suggest that, for an omitted variable to invalidate our findings, it would have to exceed an unconditional ITCV of 0.091 (α = .10). As suggested by Lonati and Wulff (2024), we compare this ITCV to the zero-order impacts of two suitable benchmarks: the control variables firm performance and efficiency-focused justification. These variables represent suitable benchmarks as, theoretically, firm performance and efficiency-focused justifications can positively influence investor reaction to downsizing (e.g., Datta et al., 2010, 2012; Palmon et al., 1997), while firms that perform well and utilize justification as an IM attempt might be more inclined to use supplication. Indeed, they also show the highest positive correlation with investor reaction and supplication. Yet, we find that the zero-order impacts of firm performance (0.008) and efficiency-focused justification (0.004) are substantially lower than the unconditional ITCV (0.091). As recommended by Lonati and Wulff (2024), we also compared the ITCV to the combined explanatory power of the three variables with the highest positive correlations with both investor reaction and supplication (i.e., firm performance, efficiency-focused justification, firm size). We again find that their combined impact (0.013) is orders of magnitude smaller than the unconditional ITCV of 0.091. In sum, these comparisons suggest that omitted variable bias can be regarded as a minor concern in our study (see, e.g., Gamache & McNamara, 2019; Lonati & Wulff, 2024).

Fifth, we conducted further analyses to assess aggregate investor reaction, operationalized as the sum of investor reaction to a downsizing announcement and the preceding earnings release. We completed this analysis to rule out that the effect of supplication might be unfavorable on aggregate. Consistent with our main results, we observe that the aggregate investor reaction is less negative for firms that used supplication (−0.27%) than for firms that did not (−0.41%). More generally, we find that investors’ reaction to prior earnings releases and investor reaction to downsizing are not strongly correlated (r = 0.04). This suggests that investors’ less negative reaction to downsizing does not seem to be significantly influenced by investors’ reaction to previously issued downward-adjusted earnings. Finally, when re-running our test of Hypothesis 2 using investors’ aggregate reaction as a dependent variable, we continue to find a positive and significant relationship between supplication and aggregate investor reaction (β = 4.17, p = .009). Together, our main results and these supplementary analyses consistently show that supplication effectively attenuates investors’ negative reaction to downsizing announcements.

Discussion and Implications

Prior research on the effectiveness of anticipatory IM around controversial events has so far almost exclusively focused on tactics that involve the conveyance of positive images, for example, by releasing additional positive information simultaneously to a negative event (Gamache, McNamara, Graffin, Kiley, Haleblian, & Devers, 2019; Graffin et al., 2016; Short & Pfarrer, in press) or withholding negatively perceived information (Carlos & Lewis, 2018; Short & Pfarrer, in press; see Busenbark et al., 2017 for the only exception). Our work departs from this focus of prior IM literature and uncovers a previously unexamined mechanism for how firms can positively bias investor reactions. Specifically, our study reveals that firms can significantly attenuate negative investor reactions to controversial decisions not only by conveying positive images, but also by deliberately displaying weakness. In contrast to the few works on anticipatory, negative IM, which show how firms can use “big bath” tactics to amplify negative investor reactions (e.g., Short & Pfarrer, in press; Titus, Parker, & Bass, 2018), we illuminate that anticipatory, negative IM in the form of supplication can be effectively used to attenuate negative investor reactions. Despite being one of the most mentioned tactics in individual-level IM literature (Bolino et al., 2008, 2016; Leary, 1995; Jones & Pittman, 1982), supplication has received little empirical research attention (Bolino et al., 2008: 1090) and has not been studied on the organizational level. Applying insights from individual-level IM studies to the organizational level, our work provides unique empirical evidence that the repertoire of anticipatory IM tactics used by firms to cushion negative stakeholder reactions includes negative IM tactics and makes the intriguing counterpoint that stakeholder acceptance and support may also be gained by showing weakness rather than strength.

Another particularly novel feature of our study is that we examine the so far unexplored combination of negative, anticipatory IM with positive, reactive IM (Bolino et al., 2008, 2016). Although past studies have provided valuable insights into the influence of individual IM tactics (e.g., Graffin et al., 2016; König et al., 2018; Lamin & Zaheer, 2012; Pan et al., 2018), they did not examine whether combinations of IM tactics are considerably more effective than the use of a single tactic. Our empirical findings suggest that combining supplication with efficiency-focused verbal justifications is more effective than using either tactic alone. Extending the recent insights by Short and Pfarrer (2023) into the combination of positive IM tactics, our study demonstrates that the combination of negative, anticipatory and positive, reactive IM can be highly effective at attenuating negative audience reactions.

Furthermore, our study extends established theoretical frameworks of IM (i.e., Gardner & Martinko, 1988; Liden & Mitchell, 1988) by moving beyond the traditional dyadic perspective on the IM process and advocating a triadic perspective. Next to actor and audience, our study draws attention to the influence of infomediaries on an audience’s reaction to IM attempts. By highlighting the important role of security analysts and the business media as infomediaries in the IM process, our study hints at a novel explanation for why IM tactics succeed or fail. In particular, our empirical findings suggest that IM attempts are more successful if evaluations of relevant infomediaries support the actor’s IM and thereby lend indirect IM support. Unlike prior anticipatory IM studies which have assumed that investors are unable to see through firms’ IM attempts, our study reveals that information that disconfirms the impression a firm seeks to convey reduces the effectiveness of its IM attempts. Thereby, our empirical findings identify authenticity as an important boundary condition for the effectiveness of IM attempts. While prior conceptual research reasoned that IM must be authentic to be effective (e.g., Gardner & Martinko, 1988; Liden & Mitchell, 1988), this theoretical proposition has remained largely untested.