Abstract

Extant strategic leadership literature has established the substantial and nuanced implications of narcissism in chief executive officers (CEOs) for firm outcomes, and psychological research on narcissism in groups highlights the importance of narcissism for interpersonal dynamics. However, there is little research on strategic leaders’ narcissism and the CEO–top management team (TMT) interface, especially related to its configuration by way of TMT composition. In this article, we therefore study two issues. First, we examine how CEO narcissism directly affects two aspects of TMT composition—the narcissism of newly appointed TMT members and TMT turnover. Second, we consider the moderating effect of TMT narcissism on the relationship between CEO narcissism and TMT turnover. To be able to test our theory, we develop and extensively validate a novel measure based on LinkedIn profiles that allows us to capture the narcissism of non-CEO executives. We find substantial support for our predictions in a large sample of executives of S&P 1500 corporations across a 5-year time frame. We discuss the contributions and implications of our findings for the literatures on executive narcissism, TMT composition, and the CEO–TMT interface.

One of the most vibrant conversations in strategic leadership research is the one on chief executive officers’ (CEOs’) narcissism—specifically, their tendency to possess “a grandiose yet fragile sense of self and entitlement as well as a preoccupation with success and demands for admiration” (Ames, Rose, & Anderson, 2006: 440-441). Ever since Chatterjee and Hambrick’s (2007) seminal study provided evidence that CEO narcissism is positively related to strategic dynamism, the number and size of acquisitions, as well as extreme organizational performance, researchers on CEO narcissism have identified a variety of additional important consequences of CEO narcissism (Cragun, Olsen, & Wright, 2020). For instance, scholars demonstrated that CEO narcissism is related to greater firm performance (Kraft, 2022; Olsen, Dworkis, & Young, 2014; Reina, Zhang, & Peterson, 2014), more and new product innovation and radical innovations in product portfolios (Kashmiri, Nicol, & Arora, 2017), as well as less innovation ambidexterity (You, Li, Jia, & Cai, 2023).

As of yet, there is hardly any scholarship on the implications of CEO narcissism—or any top management team (TMT) member’s narcissism, for that matter—at the CEO–TMT interface (Bromiley & Rau, 2016; Georgakakis, Heyden, Oehmichen, & Ekanayake, 2022; Simsek, Heavey, & Fox, 2018; van Doorn, Heyden, Reimer, Buyl, & Volberda, 2022). This interface is where the CEO and the rest of the TMT—namely, the dominant coalition responsible for strategic decision making (Finkelstein, Hambrick, & Cannella, 2009; Menz, 2012)—meet and interact to shape firm outcomes.

In particular, we know very little about how CEO narcissism affects the composition of the TMT and thus the configuration of the CEO–TMT interface. This is surprising given that CEOs have considerable discretion over the composition of their TMT and that narcissism is a profoundly social trait (Morf & Rhodewalt, 2001; Rhodewalt & Morf, 1995). In other words, evidence from social psychology would suggest that narcissism may have a substantial influence on how CEOs staff their organizations’ key positions, especially in terms of new TMT members’ narcissism. In fact, prior theoretical work proposing an effect of CEO narcissism on the hiring of new TMT members (Chatterjee & Pollock, 2017) and extant empirical research demonstrating the importance of CEO narcissism for the selection of new directors (Zhu & Chen, 2015b) strongly indicate that there is promise in empirical research into the issue of hiring new TMT members. Prior leadership research has highlighted the intricate social dynamics in leader–follower relationships with narcissistic individuals over time (Ong, Roberts, Arthur, Woodman, & Akehurst, 2016; Rosenthal & Pittinsky, 2006), raising the intriguing possibility of a potentially important but unexplored role of CEO narcissism in TMT turnover: the change of TMT composition through the dismissal or voluntary exit of TMT members.

Relatedly, there is a surprising lack of knowledge on the effects of other TMT members’ narcissism (hereafter, “TMT narcissism”) in general and on TMT turnover in particular. This is especially the case for a potential joint effect with CEO narcissism, which may emerge at the CEO–TMT interface. Initial work has studied the direct effects of chief financial officer (CFO) narcissism for financial reporting quality (Ham, Lang, Seybert, & Wang, 2017) and audit fees (Xiang & Song, 2021). Yet, with the notable exception of Bachrach, Kim, Patel, and Harms (2023), who explored how CEO narcissism is linked to TMT narcissism and how that relates to sales growth, research has rarely considered the narcissism of other top executives, let alone entire TMTs. Critically, no prior research has investigated any potential interactive effects of other top executives’ narcissism with CEO narcissism.

The dearth of pertinent empirical research on how executive narcissism affects the composition of the TMT is concerning in several ways. For one, we know that the composition of the TMT is highly consequential for the organization, making it imperative to understand how TMTs are configured. Not only have Hambrick (2007: 334) and others (Liu, Fisher, & Chen, 2018) made theoretical arguments to suggest that the “leadership of a complex organization is a shared activity, and the collective cognitions, capabilities, and interactions of the entire TMT enter into strategic behaviors,” but empirical research has clearly demonstrated that the entire TMT matters for firm outcomes. For instance, researchers recently found that TMT experiential variety (Fox, Simsek, & Heavey, 2022), CEO–TMT socialization similarity (Georgakakis, Greve, & Ruigrok, 2017), and TMT joint problem solving (Mistry, Kirkman, Hitt, & Barrick, 2023) are linked to firm performance. Not understanding the origins of the characteristics of the entire TMT is thus likely to deprive us of important insights about antecedents of important firm outcomes (Carpenter, Geletkancz, & Sanders, 2004). For another, recent literature has highlighted that the interpersonal dynamics at the CEO–TMT interface in particular (Chen, Simsek, Liao, & Kwan, 2022; Georgakakis et al., 2017, 2022; Simsek et al., 2018; van Doorn et al., 2022) are highly consequential for firm decision making and that we must expect them to be strongly shaped by the personality of the acting individuals, especially by socially relevant personality traits such as narcissism (Morf & Rhodewalt, 2001; Rhodewalt & Morf, 1995). Consequently, it is imperative to understand any interactive effects between CEO narcissism and TMT narcissism (Cragun et al., 2020) to obtain a “comprehensive social-interactionism CEO-TMT perspective” (Georgakakis et al., 2022: 6) and thus a complete picture of how executives’ personality affects the processes unfolding at the CEO–TMT interface, as well as their consequences.

Importantly, a key obstacle that has prevented research on these critical issues is the lack of appropriate measurement methods. Prior researchers measured the narcissism of CEOs (Chatterjee & Hambrick, 2007; Petrenko, Aime, Ridge, & Hill, 2016) and CFOs (Ham et al., 2017; Ham, Seybert, & Wang, 2018) leveraging company publications or using videometric techniques, but there is no established method to assess the narcissism of other TMT members. Even resorting to other unobtrusive methods, such as historiometric approaches (Wowak, Mannor, Arrfelt, & McNamara, 2016), is typically not feasible for TMT members beyond CEO and CFO.

In this article, we therefore first develop and extensively validate an unobtrusive measure of executive narcissism based on social media profiles on the platform LinkedIn. Then, we shed light on a key issue at the nexus of executive narcissism and TMT research—namely, the consequences of CEO and TMT narcissism for the composition of the TMT. Specifically, we propose that CEO narcissism is positively associated with the narcissism of newly hired TMT members, as well as TMT turnover. Importantly, we further discuss the interactive effect of CEO narcissism and TMT narcissism on TMT turnover, suggesting that TMT narcissism plays an amplifying role. We test our theory on a data set comprising 12,791 executives of 1,582 US corporations. We account for endogeneity (Hill, Johnson, Greco, O’Boyle, & Walter, 2021) and find substantial, albeit not complete, support for our theorizing.

Our research makes three contributions. First, we contribute to the strategic leadership literature on TMT composition (Andrus, Withers, Courtright, & Boivie, 2019; Bilgili, Calderon, Allen, & Kedia, 2017; Finkelstein et al., 2009) that studies which individuals constitute the CEO–TMT interface. In particular, we introduce CEO narcissism as a novel antecedent of executive appointment and departure, which both have important implications for firm outcomes (Messersmith, Lee, Guthrie, & Ji, 2014). Second, we contribute by even more deeply integrating the literature on executive narcissism with the CEO–TMT interface literature (Bromiley & Rau, 2016; Georgakakis et al., 2022; Simsek et al., 2018; van Doorn et al., 2022) by showing how the narcissism of CEO and TMT can interactively affect outcomes. Specifically, we show how TMT narcissism moderates the effect of CEO narcissism on TMT turnover. Finally, we make a key methodological contribution by developing and validating a novel unobtrusive measure for executive narcissism. Prior unobtrusive measures of narcissism had to rely on official company publications or media coverage (Chatterjee & Hambrick, 2007, 2011; Petrenko et al., 2016; Rijsenbilt & Commandeur, 2013), which are typically available for only the CEO or the CFO of large companies. In contrast, our measure builds on data that are frequently available for a broad group of TMT and board members, thus enabling potentially fruitful further research into the narcissistic tendencies of individual strategic leaders and entire TMTs, even of smaller firms.

Theory and Hypotheses

Construct of Narcissism

Narcissism research has come a long way since Freud’s seminal treatise on the subject written in 1914 (Freud, 1957). It was in this work that Freud for the first time made the distinction between the mental illness of narcissism and nonclinical narcissism that is maintained to this day. Psychiatrists tend to study the clinical condition referred to as narcissistic personality disorder and follow the definition set forth in the Diagnostic and Statistical Manual of Mental Disorders (fifth edition), which provides criteria to diagnose it. These criteria include a “grandiose sense of self-importance”; the belief that one is “special” and more important than others; “fantasies of unlimited success, power, [or] brilliance”; sensitivity to criticism; a “sense of entitlement”; interpersonal exploitativeness; a “lack of empathy”; and a need for “excessive admiration” (American Psychiatric Association, 2013: 669-671).

Researchers in nonclinical psychology and fields such as management consider these criteria as well but conceive of narcissism typically as a personality trait that every individual possesses to a certain extent. The development of the Narcissistic Personality Inventory (NPI), a highly influential and frequently used scale to assess nonclinical narcissism, captures four dimensions of narcissism that are clearly and closely related to the criteria previously laid out (Emmons, 1984, 1987; Raskin & Hall, 1979, 1981): authority/leadership, superiority/arrogance, self-absorption/self-admiration, and exploitativeness/entitlement.

Newer research has built on this conceptualization but focused more on the interpersonal dynamics of narcissism (Miller, Back, Lynam, & Wright, 2021), especially taking into account the social feedback that narcissists are seeking. For instance, Morf and Rhodewalt (2001) proposed the dynamic self-regulatory model of narcissism, integrating cognitive, affective, and protective processes to suggest that narcissists are striving for positive self-affirmation, even at the cost of interpersonal relationships. Back, Küfner, and Leckelt (2018) take a dual-pathway approach to social consequences of narcissism and find that it leads to agentic and antagonistic behaviors toward others, which typically elicit positive and negative social impressions, respectively. Rosenthal and Pittinsky (2006) highlight the relational aspects of narcissism when they focus on a leadership context and separate narcissistic personality and behaviors toward others.

Narcissism Among Leaders and Top Executives

Leadership researchers picked up on the idea of narcissism in leaders decades ago and suggested that it may be a quite common characteristic of leaders in general (Kets de Vries & Miller, 1985). To satisfy their narcissistic needs, narcissists constantly seek to gain success, control, and power (Kernberg, 1975; Raskin, Novacek, & Hogan, 1991). Leading positions provide individuals with great amounts of power and social standing and are thus particularly desirable for narcissists (Campbell, Hoffman, Campbell, & Marchisio, 2011; Kets de Vries & Miller, 1985).

Several empirical studies support the thesis that narcissistic individuals are more likely than others to emerge as leaders (e.g., Braun, 2017; Brunell, Gentry, Campbell, Hoffman, Kuhnert, & Demarree, 2008; Campbell et al., 2011; Grijalva, Harms, Newman, Gaddis, & Fraley, 2015; Nevicka, De Hoogh, Van Vianen, Beersma, & McIlwain, 2011). The reason for this is twofold: narcissists feel intrinsically called to lead others (Kets de Vries & Miller, 1985), and most people regard typical traits of narcissists, such as extraversion and confidence, as important characteristics of leaders, selecting narcissists into leadership roles (Grijalva, Harms, et al., 2015).

There is a range of consequences of leader narcissism, for instance, in terms of leadership perception and evaluation. Scholars have, for example, demonstrated that narcissistic leaders are often perceived as dominant (Leising, Borkenau, Zimmermann, Roski, Leonhardt, & Schütz, 2013) and charismatic (Galvin, Waldman, & Balthazard, 2010). At the same time, leader narcissism exhibits associations with poor supervisor ratings of interpersonal performance and integrity (Blair, Hoffman, & Helland, 2008) and perceived manipulativeness (Nevicka, De Hoogh, Van Vianen, & Ten Velden, 2013). Furthermore, in a study of US presidents, aspects of leader narcissism were positively associated with a variety of outcomes, including public persuasiveness, crisis management, winning the popular vote, as well as unethical behavior (Watts et al., 2013).

Leader narcissism significantly influences the behavior and performance of followers. Followers led by more narcissistic leaders are, for instance, more likely to experience malicious envy and engage in counterproductive tendencies (Braun, Aydin, Frey, & Peus, 2018). At the same time, there is a positive relationship between leader narcissism and follower career success, manifested through salary increments and promotions (Volmer, Koch, & Göritz, 2016).

The empirical literature on narcissism in top executives specifically is somewhat younger. Noteworthy in this regard is the research stream triggered by the work of Chatterjee and Hambrick (2007). They not only piqued strategic leadership researchers’ interest in the phenomenon but also developed a highly influential nonobtrusive measure of CEO narcissism that has been frequently employed in subsequent research.

This stream of research has produced a wealth of insights into narcissistic CEOs. For instance, scholars found that narcissistic CEOs are more likely to engage in extreme and risky corporate strategies and deliver fluctuating and extreme performance (Chatterjee & Hambrick, 2007, 2011). Researchers found CEO narcissism to be positively related to the adoption of discontinuous technologies (Gerstner, König, Enders, & Hambrick, 2013), research and development spending (Chatterjee & Hambrick, 2011; Ingersoll, Glass, Cook, & Olsen, 2019), firm innovation performance (Kraft, 2022; Zhang, Ou, Tsui, & Wang, 2017), and new and radical product innovations (Kashmiri et al., 2017). CEO narcissism has been linked to reduced innovation ambidexterity (You et al., 2023), increased likelihood of product harm crises (Kashmiri et al., 2017), and a reduced speed of recovery after crises (Buyl, Boone, & Wade, 2019). Scholars provided evidence that CEO narcissism is related to aggressive mergers and acquisitions (Ingersoll et al., 2019), manipulating policies to achieve desired results (Buyl et al., 2019; Olsen et al., 2014), bullying (Regnaud, 2014), managerial fraud (Rijsenbilt & Commandeur, 2013), reduced corporate misconduct (Donker, Nofsinger, & Shank, 2023), and executive compensation (O’Reilly, Doerr, Caldwell, & Chatman, 2014). Furthermore, CEO narcissism has been linked to firms’ aggressive tax avoidance (Olsen & Stekelberg, 2016), vulnerability to lawsuits (O’Reilly, Doerr, & Chatman, 2018), corporate social responsibility efforts (Petrenko et al., 2016; Tang, Mack, & Chen, 2018), reduced imitation of peer firms (Gupta & Misangyi, 2018), the management of a firm’s brand portfolio (Cao & Xu, 2022), as well as firms’ entrepreneurial orientation (Wales, Patel, & Lumpkin, 2013). Finally, researchers have shown that narcissistic business unit heads impede knowledge transfer between business units (Liu, Zhang, Gupta, Zheng, & Wu, 2022).

In related research, scholars in neighboring disciplines, such as accounting and finance, have begun to explore the role of other executives, such as the CFO. They identified, for instance, a link between CFO narcissism and more earnings management, less timely loss recognition, weaker internal control quality, and a higher probability of restatements (Ham et al., 2017) as well as a preference for more prestigious auditing firms, leading to higher audit fees (Xiang & Song, 2021).

Narcissism at the CEO–TMT Interface

What has largely been neglected, however, is the role of narcissism at the CEO–TMT interface. The CEO–TMT interface is where CEO and other TMT members come into contact and interact (Georgakakis et al., 2022; Simsek et al., 2018; van Doorn et al., 2022). To grasp the consequences of any strategic leader interface, one needs to understand the nature of the contact established there (Simsek et al., 2018: 288), and this appears particularly relevant in relation to a personality characteristic such as narcissism, which is so profoundly social (Morf & Rhodewalt, 2001; Rhodewalt & Morf, 1995).

In the context of the CEO–TMT interface and the personality trait of narcissism, two questions appear particularly pressing, both being related to TMT composition (Andrus et al., 2019; Bilgili et al., 2017; Finkelstein et al., 2009). First, what are the characteristics of those who meet at the interface in the first place? In particular, this includes the issue of how a CEO’s narcissism may affect the composition of the TMT in terms of the narcissism of its members. Second, what happens at the interface once it is established? Bromiley and Rau (2016: 185) summarize the literature and highlight the importance of “interactions . . . between the TMT and the CEO [for] organizational outcomes.” For instance, one might wonder about the processes unfolding over time, potentially leading to a reconfiguration of the CEO–TMT interface through TMT turnover. Furthermore, more recent research on the CEO–TMT interface emphasizes the interpersonal dynamics at the apex of the firm that drive firm decision making (Chen et al., 2022; Georgakakis et al., 2017; Georgakakis et al., 2022; Simsek et al., 2018; van Doorn et al., 2022). This research not only suggests a role of CEO narcissism but also hints at potential important interactive effects of CEO narcissism and TMT narcissism (Cragun et al., 2020).

Recent research on executive narcissism has begun to move toward a consideration of the TMT, but these efforts stop short of providing evidence about what exactly is unfolding at the CEO–TMT interface. Grijalva, Maynes, Badura, and Whiting (2020), for instance, found that basketball teams with higher team levels of narcissism and key players with higher levels of narcissism exhibited poorer organizational performance. Although the authors did not study CEOs and TMTs and did not account for interactive effects, their research clearly hints at a role of the narcissism of other group members beyond the leader. Bachrach et al. (2023) recently performed the first study in management to explore how CEO narcissism is linked to TMT narcissism and how that ultimately relates to sales growth. They found that CEO narcissism is positively related to TMT narcissism, but their study had to rely on a cross-sectional single-wave sample, limiting causal identification. Furthermore, while their work indicated an important role of the TMT, it did not examine any potential interplay between CEO narcissism and TMT narcissism. It is against this backdrop that we develop our theory on the individual and joint effects of CEO and TMT narcissism.

Effect of CEO Narcissism on New TMT Member Narcissism

The composition of the TMT and thus the configuration of the CEO–TMT interface (Simsek et al., 2018; van Doorn et al., 2022) are the outcome of a matching process between candidates for a TMT position and the firm (Schneider, Goldstein, & Smith, 1995). On one hand, a TMT candidate must be attracted to the position; that is, he or she needs to want to work under the leadership of a given CEO. On the other, although the CEO does not directly make TMT appointments, he or she can substantially influence the selection process by recommending or opposing candidates vis-à-vis the hiring committee (Shen & Cannella, 2002; Stern & Westphal, 2010; Westphal & Shani, 2016). Consequently, the CEO needs to choose the candidate for an executive appointment to happen.

Social psychology has long held that similarity between individuals leads to mutual attraction (Wetzel & Insko, 1982). This similarity–attraction paradigm has been extensively tested in numerous contexts—including, for example, regarding one’s personality in job-seeking contexts (van Hoye & Turban, 2015)—and has received overwhelmingly strong and consistent support.

Based on this broad tendency, it seems likely that TMT candidates and CEOs with similar narcissism levels would be attracted to each other. While this is somewhat intuitive for executives low in narcissism, who might appreciate each other’s modesty and empathy, it is notably likely to be the case for more narcissistic executives. Although there is potential for conflict between narcissistic executives over time, since they have a strong tendency to dominate others (Emmons, 1987; Raskin & Terry, 1988), there are various reasons to believe that this does not come to bear at the time of hiring. For instance, narcissists typically make a good first impression on others—for example, during job interviews or presentations—as they are superficially charming (Campbell et al., 2011), are skillful orators that stir enthusiasm (Maccoby, 2004), and are perceived as strong and competent individuals (Kets de Vries & Miller, 1985; Lubit, 2002). These tendencies are likely to instill mutual attraction in the new TMT candidate and the CEO during interactions throughout the hiring process. Furthermore, narcissistic tolerance theory holds that narcissists themselves are generally favorably disposed toward other narcissists (Burton, Adams, Hart, Grant, Richardson, & Tortoriello, 2017; Hart & Adams, 2014). Specifically, psychological research has generally established that similarity leads to interpersonal liking. Since narcissists are often aware of their own narcissistic tendencies and they recognize these tendencies in others, this makes them evaluate other narcissists favorably. In fact, this relationship is particularly pronounced for those who like themselves, as narcissists do. Consequently, even the potentially problematic tendencies of narcissists are initially not a concern for other narcissists, further suggesting that narcissistic CEOs and TMT candidates are likely to want to work together.

Conversely, narcissists and nonnarcissists tend to disagree about how to make a good impression (Hart, Adams, & Alex Burton, 2016). In case of a substantial narcissism differential between the CEO and a TMT candidate, there is thus a great chance that the candidate behaves in a way that will not be evaluated favorably by the CEO (and vice versa), decreasing the chance of an executive appointment.

Going beyond mutual attraction from sheer similarity, there is further reason to expect more narcissistic CEOs and TMT candidates to prefer narcissistic counterparts. Prior researchers have argued that narcissistic CEOs wish to surround themselves with people who display signals of excellence because this can reflect positively on themselves (Chatterjee & Pollock, 2017). Given narcissists’ general tendency to show off (Emmons, 1984, 1987) and their propensity for exhibitionism (Buss & Chiodo, 1991), more narcissistic TMT candidates must be expected to be more likely to display such signals of excellence, favoring them in the eye of the CEO. At the same time, it appears reasonable to expect this effect to hold in the other direction, with more narcissistic TMT candidates preferring to associate with CEOs of demonstrated excellence. Considering these arguments jointly, we thus posit:

Hypothesis 1 (H1): CEO narcissism is positively associated with the degree of narcissism of newly appointed TMT members.

Effect of CEO Narcissism on TMT Turnover

Narcissistic CEOs’ need for admiration and constant reaffirmation of their dominance and power (Raskin & Terry, 1988; Rosenthal & Pittinsky, 2006) can lead to friction at the CEO–TMT interface and changes in TMT composition by way of turnover for at least two reasons. First, as established previously, CEOs have substantial discretion with regard to who should serve on their TMTs. This encompasses not only hiring decisions but also dismissals. Such dismissals of TMT members constitute an opportunity for the CEO to assert dominance, which narcissistic individuals value (Groysberg, Polzer, & Elfenbein, 2011). Importantly, dismissing executives is a highly effective way of signaling dominance toward internal and external audiences. For internal audiences such as other TMT members, a colleague’s dismissal is extremely proximate, likely making the assertiveness and agency of the CEO and the fragility of the TMT members’ positions in the firm highly salient (Brockner, 1992). But dismissing a TMT member is also likely to attract the attention of outside audiences, such as the business press, signaling the CEO’s dominance more widely. Due to their relatively low empathy (Rosenthal & Pittinsky, 2006), it stands to reason that narcissistic CEOs can be particularly ruthless in dismissal decisions (Chatterjee & Pollock, 2017). This suggests that, occasionally, TMT member dismissals may even occur largely as a means of demonstrating dominance, requiring little to no fault on the part of the dismissed executives.

Second, beyond the CEO dismissing an executive, turnover may occur by TMT members leaving of their own volition. Research on narcissism in teams has shown that narcissists tend to emerge as leaders in teams not only because they want to lead but also because other team members ascribe leadership qualities to them (Brunell et al., 2008; Campbell et al., 2011; Grijalva, Harms, et al., 2015). However, this initial phase of infatuation tends to not last long (Leckelt, Küfner, Nestler, & Back, 2015). Over time, in fact quite quickly, team members recognize the downsides of having a narcissistic leader—such as a leader’s constant striving for self-enhancement and dominance—and “the appeal and attractiveness of the narcissistic leader rapidly wane” (Ong et al., 2016: 237). Consequently, it is reasonable to expect that top executives might simply leave narcissistic bosses and their organizations.

These two effects in tandem lead us to hypothesize that more narcissistic CEOs experience greater turnover in their TMTs:

Hypothesis 2 (H2): CEO narcissism is positively associated with TMT turnover.

Moderating Effect of TMT Narcissism on TMT Turnover

In addition, we expect the narcissism of the other TMT members to affect the CEO–TMT interface (Simsek et al., 2018) and therefore TMT turnover. Under conditions of low TMT narcissism, we simply expect the direct effect of CEO narcissism on turnover in the TMT to hold. If TMT members’ narcissism is low, the TMT is unlikely to affect the impact of the CEO’s narcissism much. In such a case, TMT members do not have a high need for narcissistic admiration and dominance themselves; as such, their own tendencies may generally not attenuate or amplify the consequences of the CEO’s narcissistic whims and needs. Accordingly, under low TMT narcissism, greater CEO narcissism is likely simply associated with greater TMT turnover, as laid out previously.

In contrast, in TMTs with higher narcissism, we expect this effect to be substantially more pronounced through a mechanism related to the CEO’s and the TMT members’ satisfaction of their own narcissistic needs. For one, although initially favorable toward them, narcissistic CEOs might over time feel particularly threatened by narcissistic TMT members. Narcissistic TMT members will have a strong sense of superiority and authority (Emmons, 1987) and may thus engage in hidden or open disagreements with the CEO (Chatterjee & Pollock, 2017). Narcissistic CEOs may perceive this as undermining their authority and withholding the narcissistic supply that they desire. Additionally, narcissists tend to strive for dominance (Emmons, 1987; Raskin & Terry, 1988), but when such highly dominant individuals are put into a subordinate position, they tend to act even more dominantly (Schmid Mast & Hall, 2003); this means that more narcissistic TMT members will be more likely to engage in aggressive conflict with the CEO, which is likely to displease a narcissistic CEO. Relatedly, dominant people prefer working with less dominant others (Dryer & Horowitz, 1997) and experience anger when forced to work with dominant others (Shechtman & Horowitz, 2006). When these notions are combined (Grijalva & Harms, 2014), they suggest that a narcissistic CEO might be particularly dissatisfied with and thus ultimately likely to dismiss a narcissistic TMT member.

For another, narcissistic TMT members themselves may be particularly inclined to leave when they work for a narcissistic CEO because they might be dissatisfied with the leader–follower relationship (Grijalva & Harms, 2014). Although narcissistic TMT members may initially be attracted to a narcissistic leader (Zhu & Chen, 2015b), they may very soon find out that their own narcissistic needs cannot be met under a narcissistic CEO. This is particularly the case with regard to their need to be in the limelight, which a narcissistic CEO will likely not allow (Kets de Vries, 2004; Lubit, 2002; Rosenthal & Pittinsky, 2006). Highly narcissistic CEOs and TMT members thus mutually prevent the satisfaction of needs directly emerging from their narcissistic personalities, leading to greater turnover.

Both notions may work together and exacerbate the effect via an additional performance mechanism. Narcissists perform strongly only when they perceive opportunities for self-enhancement (i.e., a chance to “shine”; Wallace & Baumeister, 2002). Of course, when narcissistic TMT members work under a narcissistic CEO, these opportunities may be exceedingly rare since the CEO may be unwilling to share the limelight, demotivating the narcissistic TMT members. Complementarily, Chatterjee and Pollock (2017: 712) propose that narcissistic CEOs “are often extremely demanding, and their lack of empathy and regard for others means they will not hesitate to get rid of someone who does not perform to their satisfaction.” Consequently, narcissistic TMT members may be more likely to genuinely underperform and be subsequently dismissed when they work for a narcissistic CEO.

Notably, these processes unfolding at the CEO–TMT interface in a highly narcissistic TMT will adversely affect its less narcissistic members. For one, their performance may suffer in a highly narcissistic TMT because their colleagues’ need for admiration, desire for self-enhancement, and exploitativeness may stifle mutual cooperation; lead to “hypercompetitiveness” (Luchner, Houston, Walker, & Alex Houston, 2011: 781); and render the TMT dysfunctional, making it harder for low-narcissism TMT members to perform well in their jobs. Less narcissistic TMT members may also be less likely than their more narcissistic colleagues to flaunt their achievements (Han, Liao, Kim, & Han, 2020), leading to a potentially further reduced perception of their performance by a narcissistic CEO. The ensuing lackluster performance, real or perceived, may then ultimately lead to their dismissal.

For another, less narcissistic TMT members may again simply decide that a highly narcissistic environment rife with open conflict and “narcissistic rivalry” among their fellow TMT members (Greenbaum, Gray, Hill, Lima, Royce, & Smales, 2022) is not where they want to be, and they may leave by themselves. Consequently, higher mean TMT narcissism under the leadership of a narcissistic CEO may lead to greater turnover of not only highly narcissistic TMT members but also less narcissistic ones.

Considering all these arguments jointly, we thus hypothesize:

Hypothesis 3 (H3): TMT narcissism moderates the positive relationship between CEO narcissism and TMT turnover such that the relationship becomes increasingly stronger with higher levels of TMT narcissism.

Method

Sample

We tested our hypotheses on a sample of S&P 1500 firms between 2015 and 2019. We included all firms that were part of the index at the end of each year. To ensure comparability of financial variables, we follow prior literature and exclude financial services firms (Standard Industrial Classification [SIC] major industry groups 60-67; e.g., Graf-Vlachy, Bundy, & Hambrick, 2020; Hambrick & Quigley, 2014). Our sampling frame ends in 2019 to avoid any potentially distorting effects of the COVID-19 pandemic, which began in early 2020. For H1, in which we test whether more narcissistic CEOs hire more narcissistic new TMT members, our sample comprises all appointments of TMT members in our sampling frame as observations. For H2 and H3, in which we test the influence of CEO narcissism and TMT narcissism on TMT turnover, we use firm-years as observations. More information can be found in the Analytical Procedures section.

Developing a Measure for Executive Narcissism Based on LinkedIn Data

Since using traditional survey-based measures for psychological constructs is notoriously challenging in research on the upper echelons (Cycyota & Harrison, 2006), researchers have frequently relied on unobtrusive measures. This is particularly true in the case of narcissism, for which validated psychometric self-report measures exist (e.g., NPI; Raskin & Hall, 1979, 1981), although it may not be a personality trait that top executives would want to admit scoring high in. Consequently, many upper echelons researchers interested in the narcissism of strategic leaders resorted to unobtrusive measures to capture narcissism (Cragun et al., 2020). Pioneering this approach, Chatterjee and Hambrick (2007, 2011) were the first to use publicly available documents, such as annual reports and press releases, to measure CEO narcissism by way of combining several indicators. Since then, their CEO narcissism index has become the most frequently used method in CEO narcissism research (Cragun et al., 2020).

Unfortunately, the index of Chatterjee and Hambrick (2007, 2011) relies on data such as the size of an executive’s picture in the annual report or the frequency with which an executive’s name appears in a company’s press releases, which are frequently available for only the CEO or can be sensibly interpreted for only the CEO. This singular focus on the CEO severely limits its utility. In particular, we were unable to use this measure (or derivatives; e.g., Buyl et al., 2019; Zhu & Chen, 2015a) to capture the narcissism of all TMT members. Similarly, unobtrusive narcissism measures based on signature sizes in company filings (Ham et al., 2017; Ham et al., 2018) or videometric approaches (Gupta & Misangyi, 2018; Petrenko et al., 2016) cannot be used for all TMT members. Even looking further—for instance, to historiometric methods that were used to capture other CEO characteristics, such as charisma (Wowak et al., 2016)—is not helpful because limited data availability prevents their application to all TMT members.

To solve this problem, we took inspiration from prior research to construct a novel measure of executive narcissism based on social media data. As narcissists aim to represent their superiority to a broader audience (Gerstner et al., 2013), previous studies used companies’ press releases (Chatterjee & Hambrick, 2007, 2011), letters to shareholders (Ham et al., 2018), or newspapers and business publications (Rijsenbilt & Commandeur, 2013) to capture this notion of self-presentation in their measures. We transfer this line of thought to individuals’ digital presence on social media. Specifically, we propose that an executive’s narcissistic tendencies will be reflected in their social media use. In fact, numerous studies provide support for the general notion that activity on social media platforms can be used to measure narcissism (e.g., Buffardi & Campbell, 2008; Grijalva et al., 2020; McKinney, Kelly, & Duran, 2012; Moon, Lee, Lee, Choi, & Sung, 2016; Panek, Nardis, & Konrath, 2013).

Since our population of interest comprises professionals, we used the social media platform LinkedIn to measure the narcissistic tendencies of TMT members. LinkedIn is currently the leading social media platform for professionals and lists >850 million users. In contrast to platforms such as Twitter, LinkedIn profiles comprise multiple elements that can be used to capture narcissism. Specifically, top executives can present themselves through a variety of activities and by displaying a range of personal information and achievements. In fact, prior researchers have already used the richness of these data to measure other personality traits, such as the Big Five (Van de Ven et al., 2017).

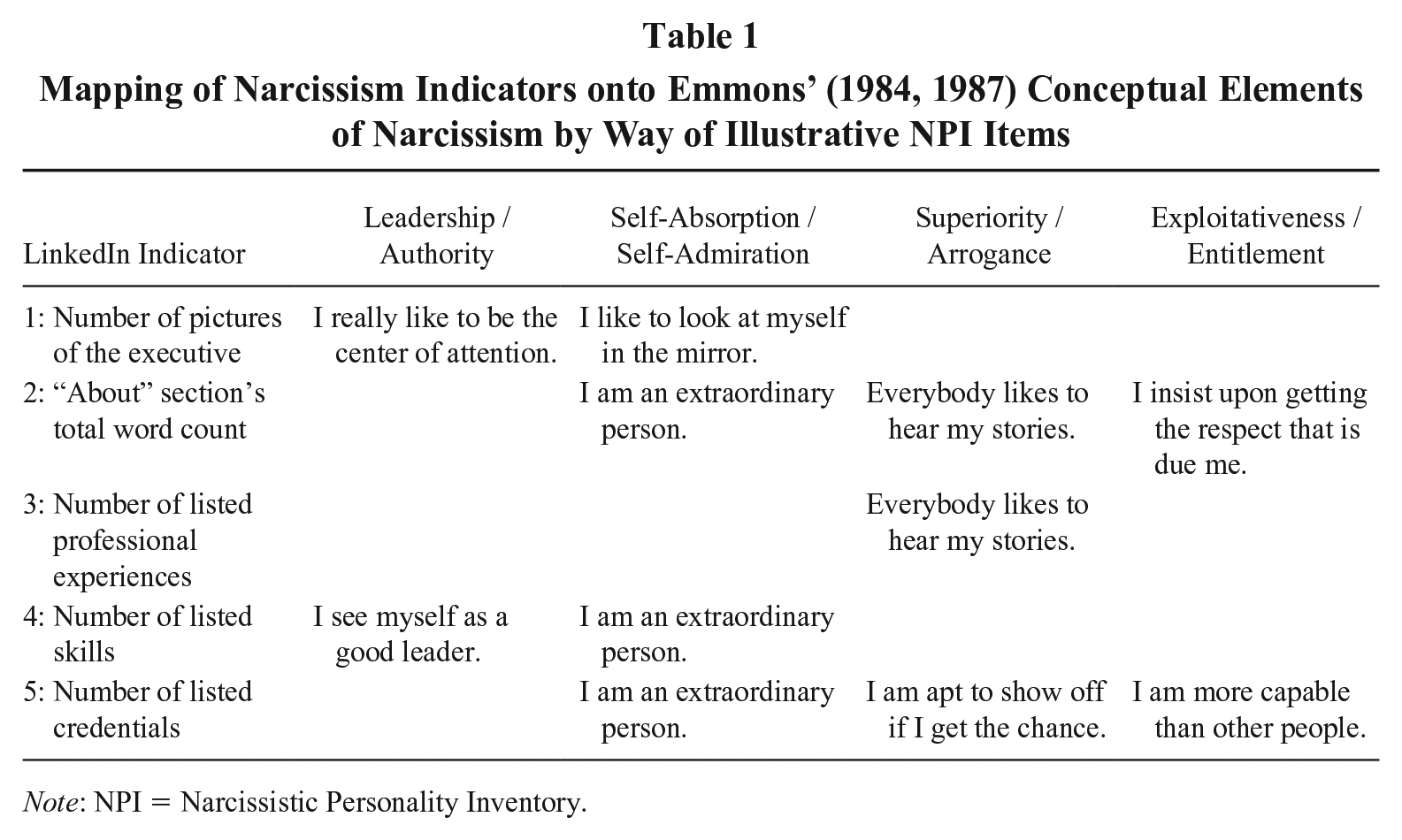

Our proposed narcissism measure is an index calculated from five indicators: the number of pictures of the executive, the “About” section’s total word count, the number of listed professional experiences, the number of listed skills, and the number of listed credentials (comprising the number of publications, patents, awards, and certificates). In selecting these face-valid indicators, we paid particular attention to theoretical criteria (Rijsenbilt & Commandeur, 2013). Specifically, to identify indicators that adequately capture aspects of narcissism, we related our proxy measures to Emmons’s (1984, 1987) four core components of narcissism: authority/leadership, superiority/arrogance, self-absorption/self-admiration, and exploitativeness/entitlement. We followed the logic outlined by Chatterjee and Hambrick (2007, 2011) and identified NPI items that aligned with the content of our indicators, which we then mapped to the component of narcissism that was captured by the specific NPI item (Emmons, 1987). In line with the notion that narcissism is a multilayered construct without completely clear distinctions (Chatterjee & Hambrick, 2011; Edwards, 2001), indicators could frequently be mapped onto more than one component. Table 1 provides an overview of our indicators and their mapping onto Emmons’s (1984, 1987) components.

Mapping of Narcissism Indicators onto Emmons’ (1984, 1987) Conceptual Elements of Narcissism by Way of Illustrative NPI Items

Note: NPI = Narcissistic Personality Inventory.

Number of pictures of the executive

A LinkedIn user can freely choose a profile picture and a background picture. In our sample, the profile picture was usually a portrait of the executive. The background picture, however, showed great variance. A few executives chose their company’s logo, a selection of products, or a landscape shot, or they did not have a second picture. Others used the background picture to show yet another facet of themselves. For example, they used photos of their public appearances or speeches, or they included a banner advertisement for their books, which in turn included their portraits on the covers. In some cases, individuals used a collage of themselves as a background image, showing themselves in multiple situations and actions. Given the extensive prior evidence showing that narcissists are more inclined to use pictures of themselves because they experience positive feelings when presenting themselves (McCain & Campbell, 2018), many studies on CEO narcissism (e.g., Buyl et al., 2019; Chatterjee & Hambrick, 2007, 2011; Rijsenbilt & Commandeur, 2013) take the prominence of the CEO’s photograph in the company’s annual report as an indicator for CEO narcissism. Similarly, studies measuring narcissism on social media have also used the profile picture as part of the measure (Grijalva et al., 2020). In line with this work, we thus used the number of times that executives appeared in the profile and background pictures of their LinkedIn profiles as our first indicator.

“About” section’s total word count

People can verbally describe themselves on their LinkedIn profiles using the “About” section. Top executives often use this section to provide an overview of their current positions, as well as professional and personal passions and achievements. Some top executives in our sample gave a broad but concise overview of their expertise, such as “Proven Leader With Expertise in Operations, Finance, and Transformation,” while others used this section to expound on personal details. Some listed awards and honors, such as “Director of the Year for Corporate Governance by Corporate Directors (2018),” yet others gave insights into personal preferences and hobbies: “loves playing guitar, cooking and spending time with his family.” Prior studies argue that narcissists feel the urge to describe themselves in extensive ways (Han et al., 2020; Rijsenbilt & Commandeur, 2013). This suggests that more narcissistic individuals are likely to list more facets (expertise, awards, personal preferences) and provide more details on themselves, which increases the number of words that they will write. In fact, researchers have used the number of words in executives’ Marquis Who’s Who biographies—the content of which can essentially be determined by the focal executive—as an indicator of narcissism (Buyl et al., 2019; Rijsenbilt & Commandeur, 2013). In line with this, we therefore used the “About” section’s total word count as our second indicator.

Number of listed professional experiences

The number of listed experiences varied widely across top executives’ profiles. While some top managers listed only their latest position, despite having spent decades at the firm, others listed their career path step by step, with an entry for every new position, whether at the same or different organizations. Some executives additionally listed their board memberships at various companies in detail, while others did not.

As mentioned previously, research shows that narcissists feel the need to present themselves in great detail (Han et al., 2020; Rijsenbilt & Commandeur, 2013). It is therefore likely that such people describe their career progression in as much detail as possible. Additionally, prior research has linked narcissism with a greater tendency to experience boredom (e.g., Kohut, 1977; Masterson, 1990; Miller, 1981; Winnicott, 1965), leading to a strong need for challenge and excitement (Wink & Donahue, 1997). Therefore, it appears likely that narcissists change their positions and their employers more frequently. Both lines of reasoning suggest that executives high in narcissism may list more positions on the LinkedIn profiles than individuals low in narcissism. We therefore used the number of listed experiences as our third indicator.

Number of listed skills

One important part of a LinkedIn profile is the “Skills & Endorsements” section. In this section, LinkedIn users can list hard and soft skills, and other users can endorse these skills. For most users, this section can facilitate job search efforts by providing a validated overview of a user’s capabilities. Top executives typically possess formidable expertise and have gained a multitude of skills in prior positions, which they could list. As top executives high in narcissism consider themselves to be special, possess a tendency to show off when given the opportunity (Han et al., 2020), and are prone to exaggeration (Hogan & Hogan, 2001), it appears likely that they would list as many skills as reasonably possible to draw attention to themselves. Our fourth indicator is therefore the total number of listed skills.

Number of listed credentials

The last indicator comprises information from the profile sections on honors and awards, patents, publications, and obtained certificates. Research shows that proudly and explicitly highlighting one’s accomplishments, strengths, and talents is a form of self-promotion that aims to enhance one’s status and attractiveness (Den Hartog, De Hoogh, & Belschak, 2020; Rudman, 1998). As highly narcissistic individuals constantly seek to satisfy their need for attention and acclaim (Rijsenbilt & Commandeur, 2013), they will engage in such self-promotional behaviors when given the opportunity to demonstrate their grandiose selves (Howes, Kausel, Jackson, & Reb, 2020). In fact, Item 20 of the established NPI narcissism scale captures whether respondents agree with the statement “I am apt to show off if I get the chance.”

We thus assume that narcissistic top executives will use the mentioned profile sections as a chance to show off their achievements—even those unrelated to their professional position. One executive, for instance, listed “Multiple world records in skydiving” in the section for honors and awards. We therefore used the number of all listed honors or awards, approved patents, publications, and obtained certificates as our fifth indicator of narcissism.

Calculating and Validating the Measure for Executive Narcissism

To calculate our measure of executive narcissism, we first identified all TMT members of a firm in each year according to ExecuComp. In total, we found 14,115 executives who worked in our sampled firms. Second, we manually searched for executives’ LinkedIn profiles via LinkedIn and Google. The search on Google was necessary because some executives did not use their birth name or full name (e.g., “Rick” instead of “Richard”) or had very common names. A Google search for the last name in combination with the firm’s name often revealed an executive’s LinkedIn profile. In total, we found 11,705 relevant LinkedIn profiles and manually extracted all relevant information.

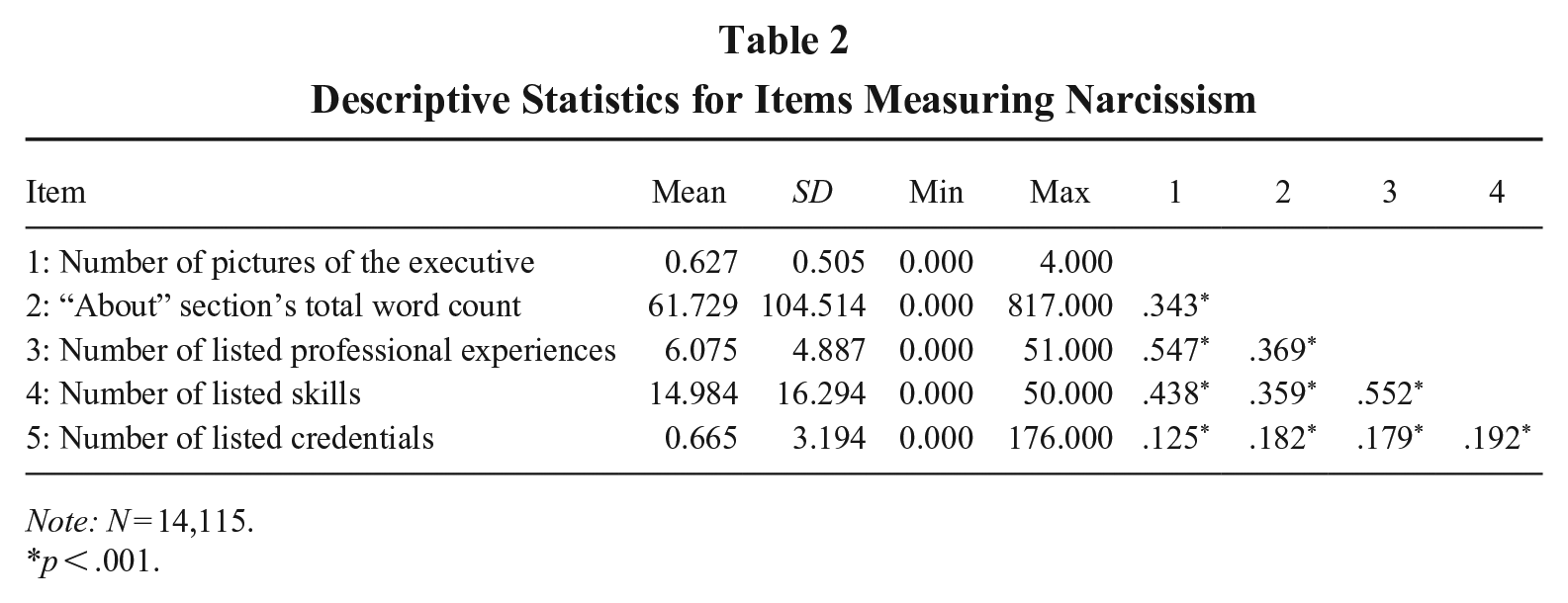

Table 2 shows the descriptive statistics and correlations of our five narcissism indicators. Note that all values were set to zero for executives without a LinkedIn profile, as we took this as an indication of low narcissism. For the calculation of our narcissism index, we used the standardized natural logarithm of our five indicators (after shifting them by one to avoid creating missing values) to account for different scales and distributions. However, to provide a more direct view of our data, Table 2 shows the untransformed values. The indicators are all correlated positively (r = .125-.552) and significantly (p < .001). When the standardized natural logarithm of our five indicators was used, the correlations increased (r = .221-.670) and remained significant (p < .001), similar to results found in prior work (e.g., Chatterjee & Hambrick, 2011) and demonstrating the coherence of our measure.

Descriptive Statistics for Items Measuring Narcissism

Note: N = 14,115.

p < .001.

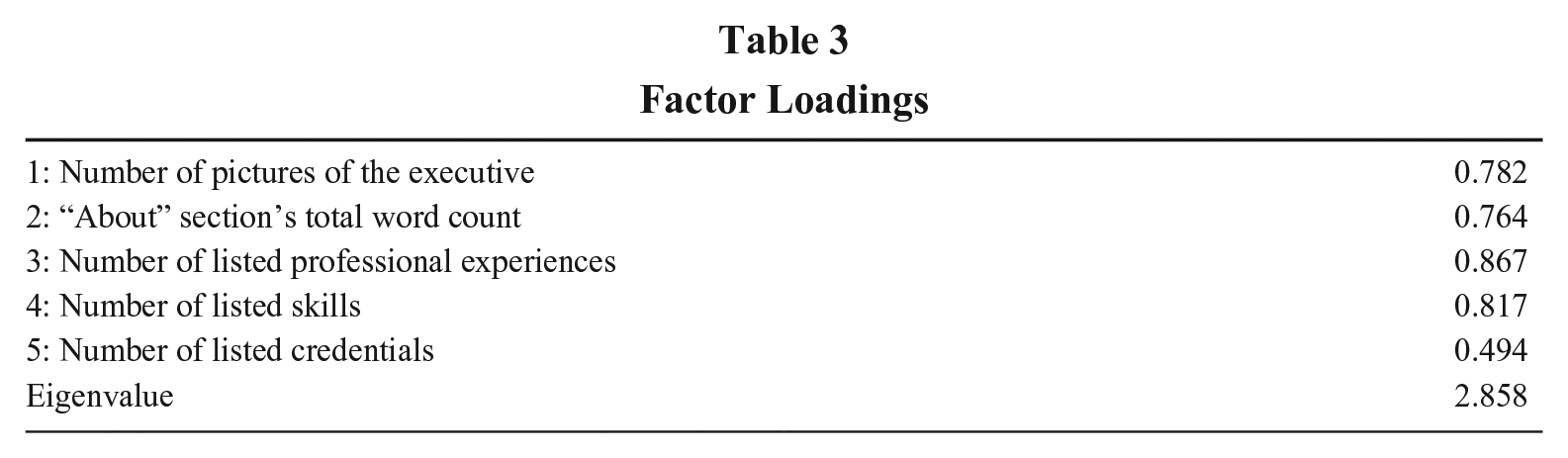

In addition, we followed work by executive narcissism researchers (Chatterjee & Hambrick, 2011; Zhu & Chen, 2015b) and performed a factor analysis to further establish the coherence of our measure. A factor test revealed the suitability of our data for a factor model (Bartlett test of sphericity, p < .001; Kaiser-Meyer-Olkin measure of sampling adequacy = .802). A principal component factor analysis revealed that all five indicators loaded onto a single factor that had an eigenvalue of 2.858 and explained 57.15% of the variance. All factor loadings were above the recommended .35 threshold (Emmons, 1987). Table 3 shows the factor loadings of our five indicators. Cronbach’s alpha (α = .803) is above the commonly accepted threshold value for forming a new index (Chatterjee & Hambrick, 2011; Nunnally, 1978). In line with prior work (e.g., Chatterjee & Hambrick, 2007, 2011), we calculated our overall narcissism measure as the simple mean of the five indicators.

Factor Loadings

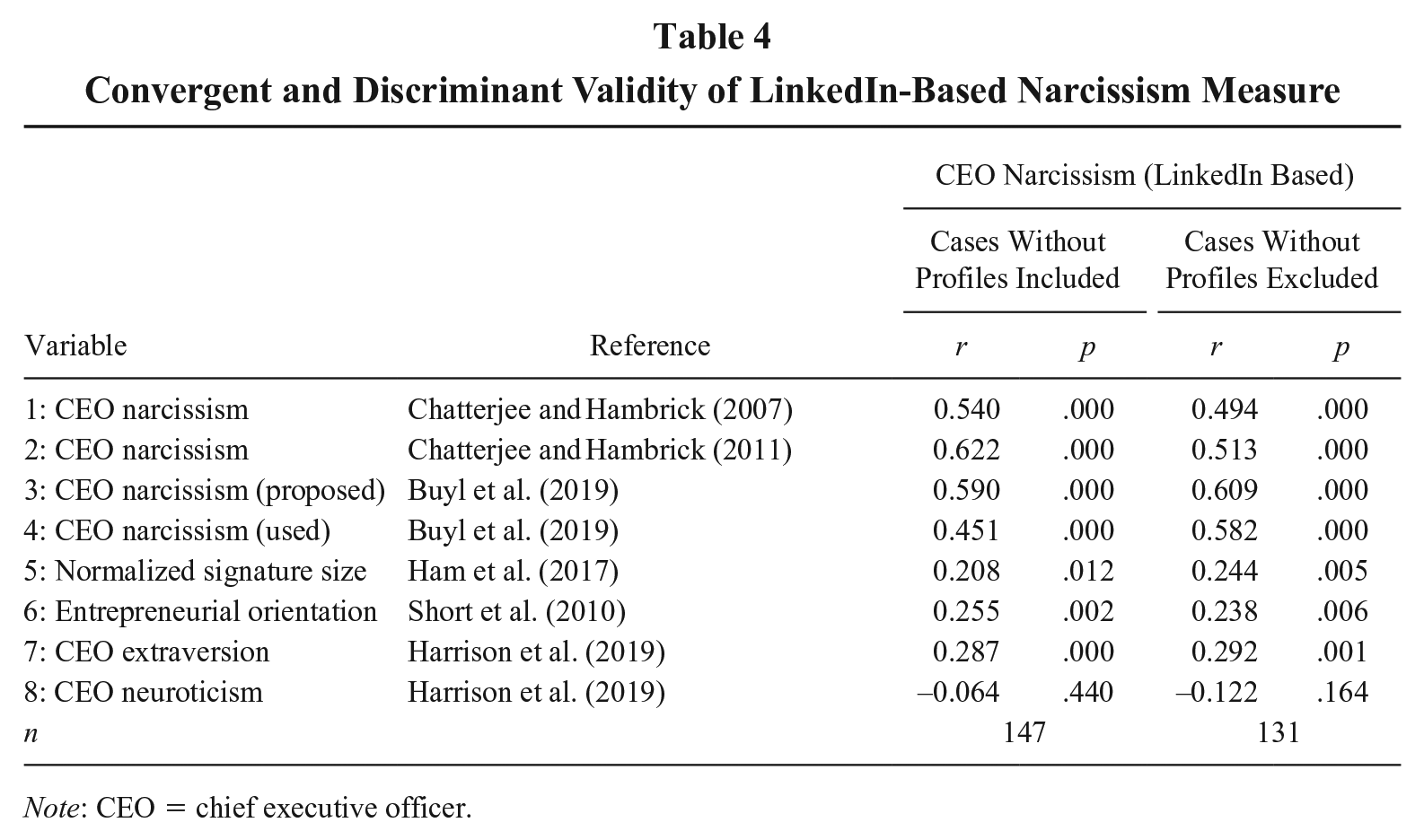

We sought to ensure that our measure genuinely captures executives’ narcissism. To this end, we performed analyses assessing the measure’s convergent and discriminant validity (Short, Broberg, Cogliser, & Brigham, 2010). In terms of convergent validity, we assessed whether our measure correlates with established measures of narcissism. We thus gathered the data needed to compute Chatterjee and Hambrick’s (2007, 2011) widely used measures of CEO narcissism: the prominence of the CEO’s photograph in the annual report (4-point scale capturing photo size and whether it shows the CEO alone or with other executives), the CEO’s prominence in the company’s press releases (number of CEO name mentions per thousand words in press releases), the CEO’s relative cash compensation (CEO cash compensation divided by that of the second-highest-paid executive in the firm), the CEO’s relative noncash compensation (CEO noncash compensation divided by that of the second-highest-paid executive), and the CEO’s relative use of first-person singular pronouns over first-person plural pronouns in the letter to shareholders. We randomly selected 150 CEOs from our sample and obtained complete data for 147 for all our validation checks. Our measure shows a positive and significant correlation (r = .540, p < .001) with the initially proposed narcissism measure of Chatterjee and Hambrick (2007). Using the updated version (Chatterjee & Hambrick, 2011), we found an even higher positive and significant correlation (r = .622, p < .001). Both correlations are large (Cohen, 2016), clearly suggesting the validity of our measure.

Given that one might challenge our decision to treat executives without a LinkedIn profile as not narcissistic, we also tested a version of our measure that excludes such cases. This reduces our validation sample to 131 CEOs. While the correlations with the measures of Chatterjee and Hambrick (2007, 2011) are still substantial and significant (r = .494, p < .001; r = .513, p < .001), they are clearly weaker than the chosen alternative. This gives us confidence to treat the absence of a LinkedIn profile as valid information about an executive’s low narcissism.

Furthermore, we tested our measure against prior narcissism measures. For one, we employed the measures proposed and ultimately used by Buyl et al. (2019). They took inspiration from prior work (Chatterjee & Hambrick, 2007; Rijsenbilt & Commandeur, 2013) and proposed an index comprising the prominence of a CEO’s picture in the annual report, the relative use of first-person singular pronouns versus first-person plural pronouns in the letter to shareholders, the number of signatures under the letter to shareholders (reversed), the number of words in the CEO’s biography in Marquis Who’s Who, as well as the CEO’s relative cash compensation and total compensation. Of these proposed six items, the authors used only four, excluding the compensation items after finding unexpected patterns in their data (Buyl et al., 2019). In our validation sample of CEOs, we found positive and significant correlations between our measure and Buyl and colleagues’ proposed measure (r = .590, p < .001) as well as the one that they ultimately used (r = .451, p < .001). For another, we followed prior literature that has experimentally demonstrated that the normalized size of an executive’s signature is a valid measure of narcissism (Ham et al., 2017; Ham et al., 2018). We collected annual reports for the same sample of CEOs that we used in our prior validation efforts and measured the size of the rectangular area enclosing the CEO’s handwritten signature, coding the absence of a handwritten signature as zero. We then normalized this size by the number of letters in the CEO’s name. The corresponding value correlated significantly with our narcissism measure (r = .208, p = 0.012), again corroborating its validity.

In addition, we tested if our measure would correlate positively with other constructs that must be expected to covary with narcissism. We followed prior CEO narcissism research (Buyl et al., 2019) and assessed our measure’s correlation with an established “letter to shareholder”–based measure of entrepreneurial orientation (Short et al., 2010), which is a construct that is positively related to CEO narcissism (e.g., Buyl et al., 2019; Wales et al., 2013). Again, we found a significant correlation with our narcissism measure (r = .255, p = .002), similar to the one that Buyl et al. (2019) found (r = .33).

Furthermore, we chose another personality trait to establish convergent validity. Out of the five factor model personality traits (McCrae & John, 1992), extraversion appears to be the most closely related to narcissism, as it shares some of the exhibitionist qualities with narcissism (Marshall, Lefringhausen, & Ferenczi, 2015). To test convergent validity, we collected CEO speech from conference call transcripts and analyzed them with a pretrained machine learning tool (Harrison, Thurgood, Boivie, & Pfarrer, 2019, 2020) to measure the CEOs’ extraversion. We found a positive and significant relationship (r = .287, p < .001) between extraversion and our narcissism measure. This result is in line with prior work (Marshall et al., 2015). In sum, we take these numerous tests as strong evidence for the convergent validity of our measure.

To assess discriminant validity, we correlated our measure with a variable that should show little or no correlation with narcissism. Neuroticism should be an adequate personality trait to support discriminant validity since it is not obviously theoretically related to narcissism. Other researchers’ empirical results support this by demonstrating a mildly negative insignificant correlation between the constructs (Marshall et al., 2015). We capture CEO neuroticism with the same tool and data set that we used to measure extraversion (Harrison et al., 2019, 2020). In line with the prior empirical results, we find a negative and nonsignificant relationship (r = −.064, p = .440) between neuroticism and our CEO narcissism measure. Table 4 shows the results of the convergent and discriminant validity tests.

Convergent and Discriminant Validity of LinkedIn-Based Narcissism Measure

Note: CEO = chief executive officer.

Finally, one might wonder if our measure might be deficient because executives’ LinkedIn profiles might be maintained by firms’ public relations (PR) departments or by executive assistants and not by the focal executives themselves. We believe that there are three reasons why this is unlikely to be an issue that would taint our measure. First and foremost, there is broad consensus in prior research that documents bearing the CEO’s name are indicative of CEO characteristics even if they might be at least partially prepared by PR departments or other parties. For instance, firms’ letters to shareholders are widely regarded as a reflection of CEO characteristics (e.g., Gamache, McNamara, Mannor, & Johnson, 2015; Junge, Luger, & Mammen, 2023), although they might not be written by the CEO alone. The reason is that the CEO’s name is directly associated with the document; thus, even if the PR department or an assistant is involved, each is expected to draft the document in a way that the CEO would approve of, and the CEO certainly needs to provide final approval. This is the case for letters to shareholders that reflect the CEO as the head of a company and likely even more for LinkedIn profiles that are explicitly designed to depict the CEO as a person.

Second, when we consider the absence and presence of various data in our particular sample, a deep involvement of the PR department seems unlikely. For instance, one would assume that the PR department would choose a profile and background picture that reflect a firm’s corporate identity. We randomly selected 50 profiles and coded whether the profile or background picture shows the corporate identity or any sign of the employer. While 78% of the profiles contained a professional profile picture (e.g., a headshot of the executive wearing a suit and tie), none of these images were in any way directly linked to the company. Furthermore, we found several background pictures with lakes, mountains, or pictures of what we must assume to be the executives’ families. Only four pictures contained the company name, slogan, or a product. Furthermore, one would assume that the PR department would be inclined to mention the firm’s name in the “About” section. We searched the “About” section of the executives for their firm names. We found that less than one fifth of the available profiles mentioned the firm name at all. In contrast to this relative absence of data suggesting no material involvement of a PR department, we find data that do not appear to be directly compatible with the motivations of a PR department. For instance, it is not obvious why a PR department would list all the experiences of a CEO, including those gained at competitors. It further seems unlikely that a PR department would attempt to list an executive’s individual skills.

Third, we conducted empirical tests to check whether the profiles of executives from the same firm share commonalities, which would suggest a role of a PR department. Given that we collected our data in 2022, we can assess this issue only with regard to the companies for which the executives were working in that year. We thus obtained information about executives’ employers in 2022 from ExecuComp and could match 3,646 executives to firms. We then performed two analyses. For one, we adjusted our five indicators by subtracting the firm mean from each data point and again computed pairwise correlations (Junge et al., 2023). The results remain essentially unchanged when compared with our initially obtained correlations (Table 2), suggesting that most variation is within the TMTs, which would not be expected if all profiles of a firm were managed by a PR team that implements a “house style.” Correlating the adjusted and unadjusted indicators reveals that they are highly positively and significantly correlated (r = .792, .797, .805, .823, .842; p < .001). For another, we assessed the degree of variance within firms for each of our five indicators. More precisely, we calculated the coefficient of variation (e.g., Zajac & Westphal, 1996) within each firm and computed the mean across firms. This mean ranges from .767 (number of listed professional experiences) to 1.454 (number of words in the “About” section). These results indicate that the different indicators vary substantially within firms and hence suggest that LinkedIn profiles are not uniformly managed by PR departments.

In sum, our extensive validation efforts demonstrate convergent and discriminant validity and support the notion that potentially PR department–managed LinkedIn profiles are not likely to distort our measure. We are therefore confident that our measure validly captures executive narcissism.

Independent and Dependent Variables

Our independent variables in all models relate to the narcissism of executives. CEO narcissism is the value of our narcissism index for a particular CEO, and TMT narcissism is the mean narcissism value of all TMT members of a firm, excluding the CEO, in a given year. We follow prior literature in strategic leadership research (e.g., Aime, Hill, & Ridge, 2020) and define the TMT as all the named executive officers as provided in firms’ Securities and Exchange Commission filings and thus listed in ExecuComp.

Our dependent variables differ by hypothesis tested. For H1, we operationalized the narcissism of a focal newly appointed TMT member, new TMT member narcissism, as the degree of narcissism of said executive according to our index. For H2 and H3, we operationalized TMT turnover as the number of executives leaving the firm’s TMT. We captured this by counting the executives who are no longer listed as TMT members in the year after the focal year. Notably, this implies that we needed to omit firms’ last years in our sample in case they cease to be publicly listed during our sampling frame (e.g., due to being acquired or taken private) because, in such cases, the TMT composition of the following year is not known.

Control Variables

We included control variables at the CEO, TMT, and firm levels. At the CEO level, we account for CEO structural power by including CEO duality and CEO share ownership (e.g., Buyl et al., 2019; Chatterjee & Hambrick, 2007, 2011). CEO duality is a dummy variable that equals 1 if the CEO is also chairman of the board and 0 otherwise (e.g., Buyl et al., 2019; Zhu & Chen, 2015b). CEO share ownership is the percentage of shares outstanding that are owned by the CEO (e.g., Chatterjee & Hambrick, 2007). Furthermore, we control for CEO tenure using the number of years that the CEO has been in office (e.g., Chatterjee & Hambrick, 2007, 2011; Zhu & Chen, 2015a) because CEOs with greater tenure exhibit a tendency of engaging in grandiose strategies (e.g., Chatterjee & Hambrick, 2007). We also control for CEO gender, which is a dummy variable that equals 1 if the CEO is male and 0 otherwise, as there are substantial gender differences in narcissism and its expression (Grijalva, Newman, et al., 2015; Ingersoll et al., 2019). Data were primarily obtained from ExecuComp and CapitalIQ.

At the TMT level, we controlled for TMT mean tenure, which is the arithmetic mean of all TMT members’ tenure (excluding the CEO; Lyngsie & Foss, 2017), to capture executives’ familiarity with and commitment to the organization and the effect that longer-tenured executives become more likely to leave an organization in any case. We further included the TMT’s gender ratio, which is the share of male executives in the TMT (excluding the CEO), because it may affect the social dynamics within the TMT (Dezsö & Ross, 2012). We also controlled for TMT size (Post, Lokshin, & Boone, 2022), which is the number of executives in the TMT (including the CEO), as larger teams are generally more likely to experience turnover events. For our test of H1, all variables were calculated excluding the focal newly appointed executive. Last, we controlled for the presence of a chief operating officer to account for whether the CEO delegates more operational matters (e.g., Chatterjee & Hambrick, 2007, 2011).

At the firm level, we controlled for firm size (natural logarithm of number of employees) and firm leverage (total debt over total equity) to control for resource availability and financial pressure (e.g., Chatterjee & Hambrick, 2007, 2011; Zhu & Chen, 2015a). To account for performance feedback and consequences, we included recent performance (ROAt-1; e.g., Chatterjee & Hambrick, 2007). ROA was calculated as the ratio of net income to total assets. Data were obtained from Compustat and CapitalIQ.

In addition, we included year dummies to account for year-specific macroeconomic conditions and contemporaneity (Certo & Semadeni, 2006), as well as dummies for all SIC major industry groups (2-digit) to capture industry effects (e.g., Chatterjee & Hambrick, 2007).

Analytical Procedures

To test H1, which predicts that more narcissistic CEOs will hire more narcissistic TMT members, we structure our data by new TMT member appointments. In our sample, 4,504 non-CEO executives were added to TMTs between 2015 and 2019, and we had complete data for 4,396. Each such appointment constitutes an observation in our regression analysis. Since one CEO can hire multiple new executives within this time frame, we performed our analysis with robust standard errors clustered at the CEO. To account for the likely endogenous nature of our independent variable (Hill et al., 2021), for example, because firms in particular situations may attract particular CEOs and TMT members, we perform an instrumental variable regression using Stata’s ivreg2 command.

To test H2 and H3, where our dependent variable is a count measure, we opted for a panel Poisson regression using Stata’s xtpoisson command. Our sample comprises 6,699 firm-years, covering 12,791 executives of 1,582 companies. Again, we must expect endogeneity because CEO narcissism may influence which kinds of prospective TMT members are attracted to an open position and which executives are ultimately hired (as we explicitly hypothesize in H1). These possibilities lead to substantial concerns about nonrandom selection (Shaver, 1998). As there is no instrumental variable version of xtpoisson, we use a control function approach to account for endogeneity (Petrin & Train, 2010). Specifically, we run a first-stage regression for each endogenous variable, in which the endogenous variable is predicted by using all control variables and an instrument. We retain the residuals of these first-stage regressions and include them in addition to the endogenous variables in our ultimate regression of interest (Wooldridge, 2015). We use bootstrapping to obtain accurate standard errors.

Since we expect the endogeneity of two variables, we need two corresponding credible—exogenous and strong—instruments. Specifically, we apply an approach that has been taken frequently in business research and relies on industry means (Germann, Ebbes, & Grewal, 2015; Krause, Wu, Bruton, & Carter, 2019). We thus instrument CEO narcissism with the industry mean of CEO narcissism (exclusive of the focal CEO), as this variable is likely to be strongly correlated with CEO narcissism, but there is no apparent causal path to our dependent variables that does not flow through CEO narcissism itself. It is, after all, unclear why the narcissism of other firms’ CEOs should have a direct impact on the narcissism of newly hired executives or TMT turnover. Consequently, we assume that this instrument is exogenous. For the analysis in H1, we compute the industry mean across all years, and for our panel-based tests of H2, we compute the industry mean separately for each year. Similar to the procedure for CEO narcissism, we instrument TMT narcissism with the annual industry mean TMT narcissism, exclusive of the focal firm’s TMT narcissism, in our analyses for H3. In the control function approach that we use for H2 and H3, interaction terms need not be instrumented separately. We report evidence of the instruments’ strength in our Results section.

We used robust standard errors clustered at the CEO in all models to address the possibility of heteroskedasticity (Cerrato, Alessandri, & Depperu, 2016). We examined variance inflation factors (VIFs) in all regressions without the year and industry dummies (Allison, 2012). All VIF scores are <1.5, and the mean VIF score is, depending on the model, between 1.07 and 1.13, well below the commonly accepted threshold of 10 (Hair, Black, Babin, & Anderson, 2019). This suggests that our estimations are unlikely to be tainted by multicollinearity.

Results

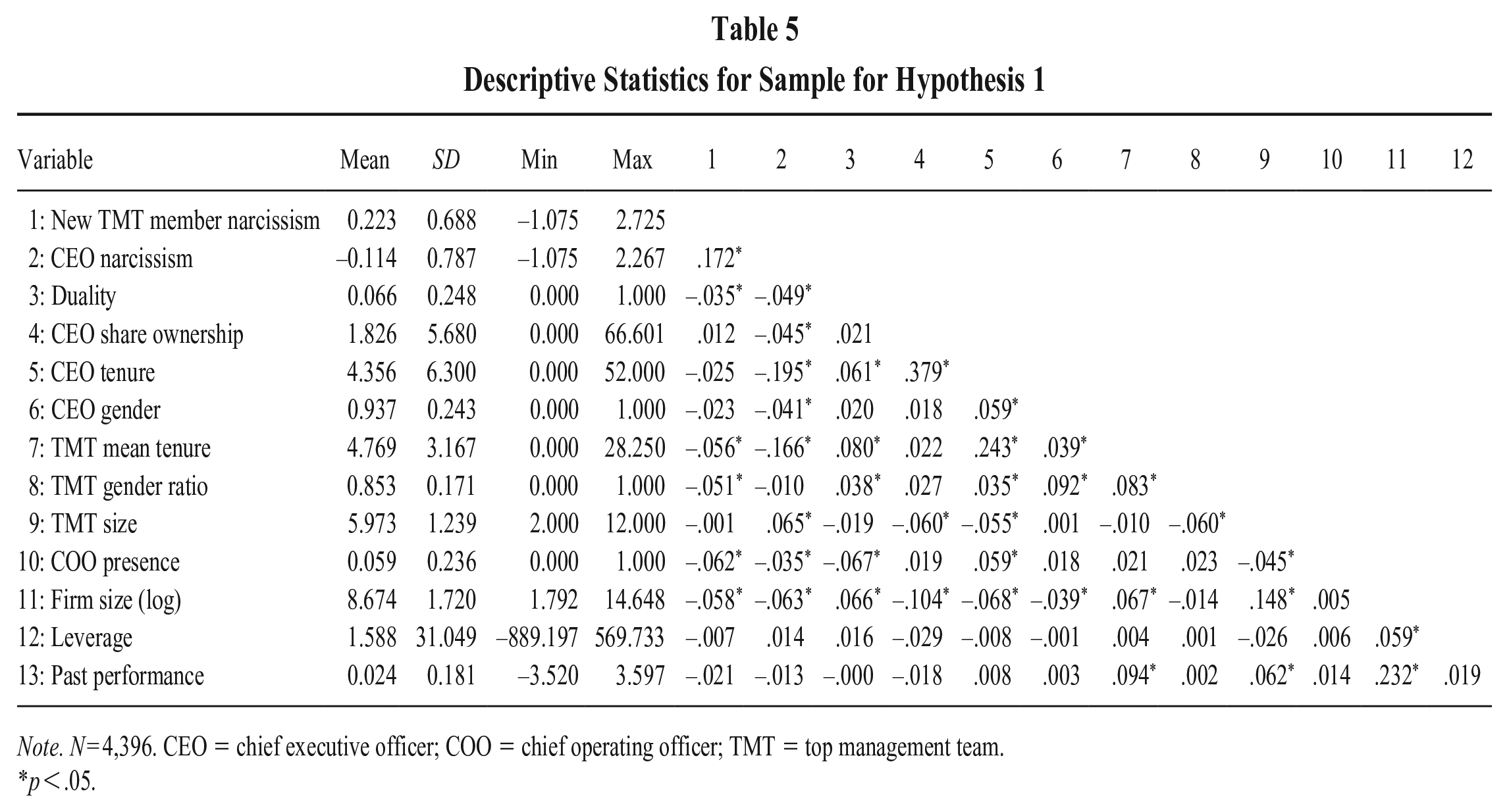

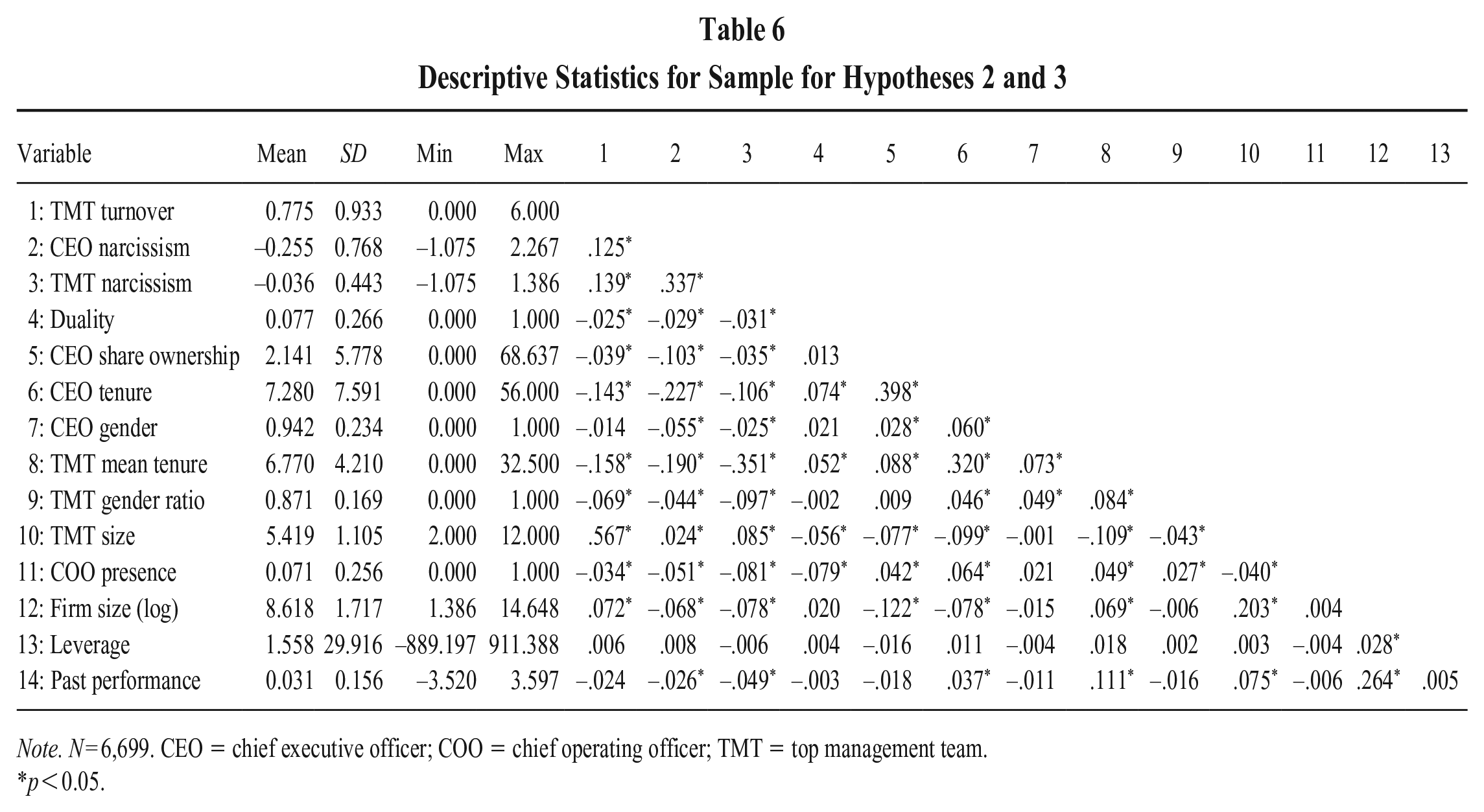

Table 5 provides means, standard deviations, minimum/maximum values, and pairwise correlations for the variables in the sample used to test H1. Table 6 provides the same information for the panel data set used to test H2 and H3.

Descriptive Statistics for Sample for Hypothesis 1

Note. N = 4,396. CEO = chief executive officer; COO = chief operating officer; TMT = top management team.

p < .05.

Descriptive Statistics for Sample for Hypotheses 2 and 3

Note. N = 6,699. CEO = chief executive officer; COO = chief operating officer; TMT = top management team.

p < 0.05.

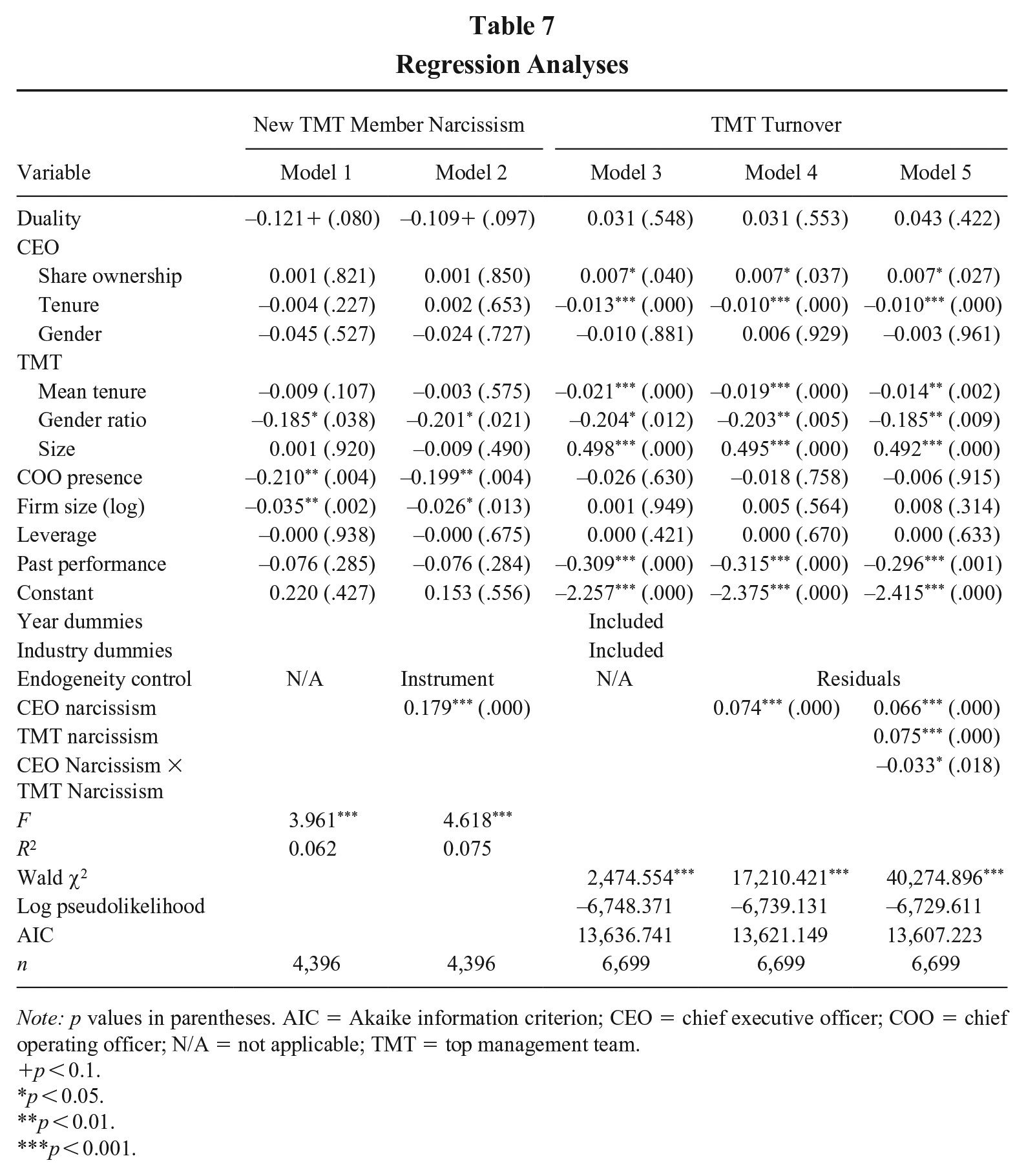

Table 7 shows the results of our regressions testing all hypotheses with two-tailed tests. Model 1 is the control model for H1. Model 2 tests H1, which predicts that higher CEO narcissism is positively associated with TMT narcissism. The first-stage F statistic is 1,636.090, which dramatically exceeds the commonly applied threshold of 10 (Angrist & Pischke, 2009) and suggests that the instrument is very strong and thus valid. The estimated relationship between CEO narcissism and the narcissism of a newly hired executive is positive and significant (b = .179, p < .001), supporting H1. For ease of interpretation, we standardized our independent and dependent variables in these models. Consequently, an increase of CEO narcissism by one standard deviation is associated with an increase of 18% of a standard deviation in narcissism of a newly hired executive.

Regression Analyses

Note: p values in parentheses. AIC = Akaike information criterion; CEO = chief executive officer; COO = chief operating officer; N/A = not applicable; TMT = top management team.

p < 0.1.

p < 0.05.

p < 0.01.

p < 0.001.

We reran Model 2 with synthetic instruments based on the heteroskedasticity of the error terms (Lewbel, 2012). Specifically, we ran this model once with synthetic instruments and once with our instrument and synthetic instruments. In both cases, nonsignificant Hansen J statistics (p = .097 and p = .127) suggest that the instruments may be valid, and the results are consistent with our main analysis. The latter analysis provided a nonsignificant C statistic (p = .663), which is suggestive evidence that our instrument for our main analysis is valid. We also ran Models 1 and 2 with the additional control variable mean TMT narcissism, calculated as mean TMT narcissism excluding the focal newly appointed executive. Our results again remain fully consistent.

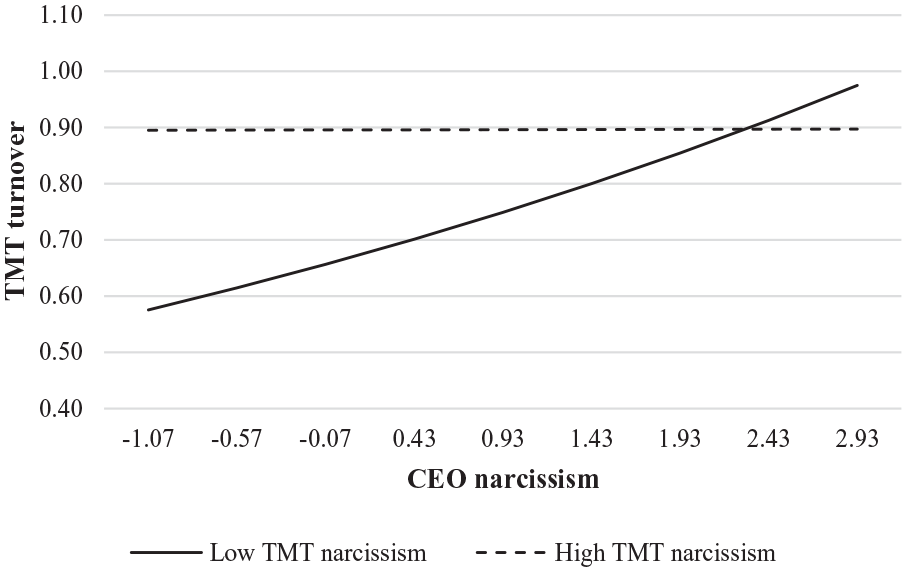

Models 3 through 5 test H2 and H3, which predict TMT turnover. Model 3 is the control model. Since we employed a control function approach to test H2 and H3 in Models 4 and 5, we cannot compute joint first-stage F statistics. Instead, we ran regressions predicting the endogenous variables with the instruments and all controls. For CEO narcissism and TMT narcissism, the instruments were significantly positively correlated with the endogenous variables and—more important—significantly predicted the endogenous variable conditional on all covariates (b = −.522, p < .001; b = −.728, p < .001, respectively). We take this as evidence of instrument strength, suggesting overall valid instruments. Model 4 tests H2, which predicts a positive association between CEO narcissism and TMT turnover. We find a positive and significant coefficient (b = .074, p < .001), supporting H2. In Model 5, we add TMT narcissism and the interactive effect of CEO narcissism and TMT narcissism. We find that CEO narcissism is still positively and significantly related to TMT turnover (b = .066, p < .001). Similarly, we find TMT narcissism to be positively and significantly associated with TMT turnover (b = .075, p < .001), while the interaction term has a negative and significant coefficient (b = –.033, p = .018). To ease interpretation, we visualize the marginal effects in Figure 1. As we standardized both independent variables but not the dependent variable, the ordinate indicates the number of executives leaving the TMT. When a CEO leads a low-narcissism TMT, the CEO’s effect is dominant, meaning that higher CEO narcissism is associated with greater TMT turnover. In contrast, when the CEO operates in a highly narcissistic TMT, we observe no such effect, meaning that higher CEO narcissism is not associated with TMT turnover. Hence, while the empirical relationship between CEO narcissism and TMT turnover is as expected under conditions of low TMT narcissism, we unexpectedly observe no relationship under conditions of high TMT narcissism. Notably, however, the effect of CEO narcissism on TMT turnover under these conditions is consistently high. Overall, we thus find an interactive effect but no support for H3 specifically.

Effect of CEO and TMT Narcissism on TMT Turnover

Supplementary Analyses of Leaving Executives’ Narcissism and Firm Performance Extremeness

We performed a supplementary analysis related to TMT turnover to study the question of whether the narcissism of the executives leaving a TMT (relative to that of remaining members) may be explained by CEO and TMT narcissism. Finding such effects would indicate that certain constellations of CEO and TMT narcissism might cause a particular kind of executive to leave or be forced out. To this end, we used the sample employed to test H2 and H3 and retained only the firm-years in which there was a turnover event in the TMT and not the whole TMT turned over (n = 3,478). We then ran instrumental variable random-effects regressions predicting the difference in narcissism between the leaving TMT members and the remaining TMT members via Stata’s xtivreg command with the firm as the panel unit. In contrast to the control function approach used to test H2 and H3, we now accounted for the endogenous interaction term of CEO and TMT narcissism by including a third instrument that is constructed as the product of the two instruments for CEO and TMT narcissism. Neither the coefficient for CEO narcissism (b = −.014, p = .884) nor that for the interaction between CEO narcissism and TMT narcissism (b = .402, p = .209) was significant. We repeated the analysis while controlling for the number of leaving TMT members and obtained nearly identical results. These results imply that there is no clear link between CEO and TMT narcissism and the narcissism of leaving executives. Specifically, this suggests that not only the particularly narcissistic or nonnarcissistic executives are leaving a TMT characterized by specific constellations of CEO and TMT narcissism. It is thus likely that all proposed theoretical mechanisms are at play—those affecting more narcissistic executives as well as less narcissistic ones.

Thus far, we have considered the implications of CEO and TMT narcissism only for matters related to the composition of the TMT to maintain a coherent focus. However, if our narcissism measure is valid and the narcissism of the entire TMT is broadly consequential, this might be reflected in other outcomes affected by the CEO–TMT interface, for instance, at the firm level as well. To demonstrate these broader consequences, we performed a second supplementary analysis to illuminate the effects of CEO and TMT narcissism for a different dependent variable that has been previously studied in the narcissism literature: firm performance extremeness (Chatterjee & Hambrick, 2007).

In their seminal work on CEO narcissism, Chatterjee and Hambrick (2007) theorized and found a direct effect of CEO narcissism on firm performance extremeness. Finding evidence of this effect would corroborate not only their results but also the validity of our narcissism measure.

Additionally, there might be an interactive effect with TMT narcissism because CEOs’ likelihood of executing extreme strategies is at least partially dependent on interactions at the CEO–TMT interface (Menguc & Auh, 2005; Simsek et al., 2018). As long as TMT members’ narcissism is low, their low need for admiration and dominance may lead them to just accept the CEO’s narcissistic tendencies as reflected in the firm strategies proposed by the CEO. Consequently, under conditions of low TMT narcissism, the direct effect likely holds, and greater CEO narcissism is positively associated with firm performance extremeness (Chatterjee & Hambrick, 2007). When TMT members are more narcissistic, however, they might not simply defer to the CEO, as their personal sense of superiority and self-admiration (Emmons, 1987) get in the way. Instead, they might develop their own distinct ambitious strategies. They may then either subtly pursue (Chatterjee & Pollock, 2017; Schill, Boutalikakis, Hawighorst, Graf-Vlachy, & Konig, 2022) these strategies or, satisfying their need for authority (Emmons, 1987), clash with the CEO during strategy making or implementation.

The ensuing multiplicity of competing strategies within the firm makes the emergence of a coherent overall strategy unlikely, reducing performance extremeness. If there is no one clear guiding policy, different parts of the firm are likely to pursue different directions (Rumelt, 2011), leading to a poorly coordinated organization with mediocre performance at best. Extreme positive performance is unlikely because no superior strategy can be implemented in a coherent fashion. Extreme negative performance is also not likely because the firm will be unable to take large concentrated risks (which may not pan out) due to its lack of internal alignment. Prior empirical work supports this notion, demonstrating that firms in which the CEOs are challenged on their strategy proposals by other executives exhibit reduced performance extremeness (Tang, Crossan, & Rowe, 2011).

Importantly, the more narcissistic the CEO is, the more pronounced these tendencies will be. Whereas a nonnarcissistic CEO may be able to effectively manage a narcissistic TMT because he or she can make relatively ego-free decisions, letting his or her TMT members have their “narcissistic supply” (Kernberg, 1975) but ultimately still “rallying the troops” and implementing a coherent strategy, a more narcissistic CEO will not want to let others shine besides her or him. Consequently, a more narcissistic CEO likely actively seeks open contests with narcissistic TMT members, further reducing the likelihood of productive alignment between CEO and TMT on strategic decisions. Greater CEO narcissism in the case of a highly narcissistic TMT may thus lead to less extreme performance outcomes.