Abstract

Recent scholarship has sought to develop a “scientific method” for startups. In this paper we contrast two approaches: lean startup and the theory-based view of startups. The lean startup movement has served an important function in calling for a normative and scientific approach to startups and venture creation. The theory-based view shares this agenda. But there are differences in the underlying theoretical mechanisms and practical prescriptions suggested by each approach. We highlight these differences and their implications for both research and practice. For example, we contrast lean startup’s emphasis on bounded rationality and entrepreneur–customer information asymmetry with the theory-based view’s emphasis on generative rationality and belief asymmetry. The theory-based view focuses on contrarian beliefs, associated problem formulation, and the development of a startup-specific causal logic for experimentation, resource acquisition, and problem solving. The right mix of entrepreneurial actions is contingent and startup-specific—guided by a startup’s unique theory. After pointing out differences between the lean and theory-based view of startups, we discuss opportunities for partial reconciliation, as well as opportunities for empirically comparing perspectives. Overall, we emphasize that a scientific method for startups needs to recognize the importance of contingent, discriminating alignment between entrepreneurial theories and the actions they prescribe (including different types of experimentation and validation, search, and forms of organization).

Introduction: Entrepreneurs as Scientists

Lean startup—as developed by Blank (2013), Blank and Dorf (2012), Ries (2011), and Osterwalder and Pigneur (2010)—has had a significant influence on how entrepreneurs approach startups and new ventures. Lean startup has also begun to shape how academics study and teach entrepreneurship (e.g., Leatherbee & Katila, 2020; Shepherd & Gruber, 2021), offering a framework and practical tool that also captures some of the insights of longer-standing academic literatures—including the literatures on technology evolution, organizational learning, product development, and strategic management (Contigiani & Levinthal, 2019).

We strongly endorse the normative message of lean startup, namely, that entrepreneurs can optimize their odds of success when they adopt a “scientific approach to the creation of startups” (Ries, 2011). The idea that entrepreneurs should act like scientists—and utilize the scientific method—is the central premise of the theory-based view (Felin & Zenger, 2009, 2016, 2017; Felin, Gambardella, & Zenger, 2021; Zellweger & Zenger, 2023). This approach has been formally modeled (Ehrig & Schmidt, 2022; Camuffo, Gambardella, & Pignataro, 2023a) and empirically tested through randomized control trials (e.g., Agarwal et al., 2023; Camuffo, Cordova, Gambardella, & Spina, 2020; Novelli & Spina, 2024). The theory-based view of startups concurs with lean startup’s emphasis on the scientific method and its focus on practical action and hypothesis-driven experimentation. Both lean startup and the theory-based view can be seen as part of an important normative movement within strategy and entrepreneurship that seeks to identify practical “interventions,” treatments and forms of training that might enable startups and companies to be more scientific and evidence-based about their decision making (e.g., Chatterji, Delecourt, Hasan, & Koning, 2019; Heshmati & Csaszar, 2023; Kotha, Vissa, Lin, & Corboz, 2023). But we argue that these interventions need to be theory-guided, both at the level of their scientific investigation and at the level of startups and firms themselves.

In this article, we take Blank and Eckhardt’s (2023) recent contribution as a reference point and offer contrasts between the theory-based view of startups and lean startup. We do so particularly in terms of the central mechanisms and the prescriptive “method” suggested by each approach. While some of these differences have briefly been discussed before (Felin, Gambardella, Stern, & Zenger, 2020), we go well beyond this work by addressing the central and novel points raised by Blank and Eckhardt (2023) in their target article. We recognize that lean startup has been further developed since its original conception—adding new frameworks and tools (e.g., Shepherd & Gruber, 2021), empirical tests (e.g., Burnell, Stevenson, & Fisher, 2023; Leatherbee & Katila, 2020), and links to adjacent disciplines (e.g., Ramoglou, Zyglidopoulos, & Papadopoulou, 2023). Some of these extensions suggest that the gap between the lean and theory-based approach to startups might be narrowing. However, the need to point to differences is made evident by Blank and Eckhardt’s (2023: 4) suggestion that the theory-based view is “consistent” with lean startup—a conclusion we do not fully endorse. While both approaches can broadly be “viewed as an application of the scientific method to entrepreneurship” (Blank & Eckhardt, 2023: 2), the specific mechanisms, assumptions, interventions, and practical prescriptions for startups and entrepreneurs are substantially different. We carefully point out these differences and offer possible complementary future directions that could further the development of a “scientific method” for startups. Some of the differences between the theory-based and lean view of startups can be reconciled by a “contingent” approach to entrepreneurship—an approach that recognizes the contextual and situational factors that shape which method or practice should be utilized (when and why), depending on the startup-specific theories held by an entrepreneur. We conclude by pointing out the need for those architecting startups to pursue a discriminating alignment between the type of theory entrepreneurs seek to explore and the downstream actions or choices related to different forms of experimentation and organization.

Lean Versus Theory-Based Startup

Blank and Eckhardt (2023) offer an extensive summary of lean startup, including a discussion of key concepts and tools such as Business Model Canvas and Market Opportunity Navigator (cf. Gruber & Tal, 2017, 2024; Osterwalder & Pigneur, 2010). Their paper provides a highly useful articulation of the current state of the lean startup approach, including links to recent developments (building on Shepherd & Gruber, 2021; cf. McGrath & Macmillan, 2000). Blank and Eckhardt’s paper also points to links between lean startup and adjacent theories and approaches, such as effectuation, bricolage, and discovery-creation. To their credit, their paper is inclusive and far-ranging. However, given space considerations, in this paper we focus largely on contrasting lean startup’s core assumptions and arguments with those of the theory-based view of startups.

Lean Startup: Foundations and Model Assumptions

As argued by Blank and Eckhardt (2023), the “core” premise of lean startup is that entrepreneurs and startups need to forego excessive planning and quickly engage with customers, for example by developing a minimum viable product. While attention is given to other stakeholders through tools like Business Model Canvas, Blank and Eckhardt specifically emphasize the need to “[reduce] information asymmetries between entrepreneurs and customers” (2023: 5, italics added). The assumption behind this information asymmetry is that customers have vital information or knowledge that a startup needs to somehow elicit, access, or incorporate into their nascent product, service, or value offering. The sooner the entrepreneur engages with the customer, the quicker this information asymmetry can be reduced. In short, lean startup’s primary emphasis is on “early and frequent customer feedback”—“quick rounds of experimentation and feedback”—to enable startups to “continually learn from customers” (Blank, 2013: 5-7). Notice that, according to lean startup, this asymmetry of information is one-sided, where the key information and knowledge is held by the customer and needs to be accessed by the startup.

Consistent with the concept of information asymmetry, lean startup builds on the idea of bounded rationality. As discussed by Blank and Eckhardt, entrepreneurs “are imperfect decision makers who suffer from biases in decision-making” (2023: 6). The argument is that bounded rationality is reduced or lessened if startups use the lean method—again, by garnering information and knowledge through various forms of customer interaction and validation. Lean startup recognizes that entrepreneurs cannot somehow access “all” customers, but they need to satisfice by securing frequent, “good enough data” from them (Blank, 2013). Customer interaction and feedback is meant to offer much-needed, ongoing scientific validation and evidence to ensure the venture is moving in the right direction—rather than wasting resources.

Several questions emerge from the emphasis that lean startup puts on information asymmetry between customers (or even other stakeholders) and the startup, as well as the strong emphasis placed on bounded rationality as an underlying assumption. For example, is customer interaction indeed the best way to validate a startup’s product idea, value offering, or strategy, relative to many other alternatives? Can customer interaction reliably offer a signal about what a startup should do? Is the emphasis on bounded rationality the right way to think about entrepreneurial cognition and startup learning? We discuss these questions in turn.

While customer feedback undoubtedly can be useful in some situations, there are several problems with focusing on customer feedback as the central mechanism for learning and validation. The immediate, practical problem with customer feedback is that it is likely to be extremely heterogeneous. One customer might like a particular product feature while another might not. Feedback might be highly idiosyncratic depending on the customers the startup happens to sample and interact with, and efforts to avoid the problem of idiosyncratic feedback—for example by sampling an even larger set of customers—only compound the problem. Customers might offer indefinite thoughts on how a particular product should evolve and what features ought to be added, improved, or completely removed. Lean startup offers no coherent mechanism for arbitrating between all this information, to recognize which bits of information might actually validate an idea or product and which might lead a startup astray. Interestingly, this problem was recognized in early work related to business models. As noted by Osterwalder and Pigneur, “another challenge lies in knowing which customers to heed and which customers to ignore” (2010: 129). To foreshadow our argument, we think theories are fundamental to the process of knowing who to listen to (or which customers or stakeholders to even solicit feedback from). In short, with heterogeneous customer feedback, it is hard to separate the signal from the noise. 1

Of course, in principle, there is nothing wrong with sampling and interacting with customers. As we discuss below, in some situations, the right form of customer interaction and experimentation can be useful; however, our central point here is that customer interaction is not a panacea for validation, and there is no clear reason to make information asymmetry between customers and startups—and the bounded rationality of the latter—the central problem that needs to be solved.

Customer feedback is but one of many tools and forms of experimentation and intermediate validation that a startup can use to guide its actions. When it comes to startup activity, there are no one-size-fits-all tools. Of course, whether customers buy a product is the ultimate market test and (eventual) source of validation. But it is not clear why customers might have better information than startup founders themselves when developing the startup’s product or value offering that is offered to customers. Customers might not even have a proper awareness of their own needs. Thus, much-needed validation might come from problem solving, experimentation, and exploration that do not initially involve customers at all. This could involve searching for a critical technology, exploring key assumptions, or conversing with potential resource providers. Validation might also come through efforts to elicit the engagement and buy-in of co-founders, early employees, and investors—actors who have far more riding on the possible success of the startup than customers. In fact, in some cases, founders and early employees are essentially customers themselves. They can be seen as lead users whose opinions and tastes shape how a product offering or technology evolves (as historically has been the case with Apple). These employees create the products they would like to see exist, rather than asking customers what they think is needed.

Importantly, customer feedback is of less value in situations where startups seek to develop radically discontinuous, novel product offerings and new sources of value. Customers might offer useful, incremental improvements on products that they are already habitually aware of and familiar with, but novel product offerings often demand more than casual responses to a mocked-up product. As we will discuss, the most valuable product and business ideas emanate from theories involving “what-if” forms of causal logic, that is, what if the following assumptions are true or the following problems can be solved? Obtaining quick customer feedback on such forms of novelty requires customers to imagine and embrace the underlying causal logic, which may be extraordinarily difficult to achieve without first demonstrating the accuracy of assumptions or the solvability of subproblems. This is aptly captured by Henry Ford’s famous quip: “If I had asked customers what they wanted, they would have said a faster horse.” It is also not clear that Henry Ford would have generated highly useful feedback from a rapidly developed crude prototype of the Model T.

Bounded rationality—an idea closely linked to information asymmetry—forms a second central assumption of lean startup, as discussed by Blank and Eckhardt (2023: 6). Boundedly rational models of search and decision-making essentially build on the idea of an information asymmetry between the searching actor and the environment (Simon, 1956). Searching actors cannot process or compute information omnisciently, and they therefore need to selectively sample and satisfice. In the context of lean startup, this sampling and information gathering is done by interacting with customers and by soliciting feedback on minimum viable products.

Lean startup’s focus on bounded rationality is aptly captured by Leatherbee and Katila in their work. They emphasize how “bounded rationality—finite information, finite minds, and finite time—makes young firms imperfect decision-makers” (2020: 571). Essentially, startups need to access information, advice, and feedback from customers to “mitigate” against bounded rationality. The logic of mitigating against bounded rationality—by seeking external advice and feedback (or “opening the aperture”)—has been discussed more broadly in entrepreneurship, in contexts such as incubators and entrepreneurial strategy (e.g., Cohen, Bingham, & Hallen, 2019; Miller, O’Mahony, & Cohen, 2024). Bounded rationality is also the underlying assumption of the literature in entrepreneurship that highlights the role of heuristics and information processing in uncertain environments (e.g., Artinger, Petersen, Gigerenzer, & Weibler, 2015). Bounded rationality of course is a central concept not just in entrepreneurship but also in organization economics, management, and strategy more broadly (e.g., Puranam, Stieglitz, Osman, & Pillutla, 2015).

When applied to startups and entrepreneurs, however, the concept of bounded rationality—particularly when operationalized as the one-sided information asymmetry between startups and customers—comes with some unhelpful baggage, in terms of what is assumed about human cognitive capacities and the organism-environment relationship. The focus on information processing—and associated bounded rationality—places emphasis on the cognitive task of seeing or “reading” the environment correctly (Chater et al., 2018). This makes entrepreneurial judgment and decision-making into a computational or representational task where the relevant data is “out there”—in the environment (for example, information held by customers)—and needs to somehow be appropriately mirrored, sampled, or processed. Applied to lean startup, the idea here is that entrepreneurs should focus on quickly learning from their environments—customers and other stakeholders—and apply these lessons to their products and strategy.

However, from a theory-based perspective, entrepreneurs do not want to accurately mirror their environments in the sense suggested by the idea of information processing. Entrepreneurial decision-making necessarily aspires to be generative. Startups are essentially trying to render something true that currently is untrue. Startups are seeking to create and essentially present sources of value rather than represent their environments. This creates a mismatch with the focus on bounded rationality and information processing. The idea of bounded rationality is focused on a representation of environments (in whole or in part; Chater et al., 2018), and it is usually applied to tasks with an objective answer, as is illustrated by popular experiments where subjects are asked to identify which of two cities has a larger population (Gigerenzer & Goldstein, 1996; for a review, see Felin & Koenderink, 2022). Search tasks like this, however, hardly capture the essence of entrepreneurial decision-making, which is focused on forward-looking beliefs and novelty. In entrepreneurial decision-making—unlike situations where bounded rationality is the relevant constraint—there is no “lookup table” for the right answer. Yet, lean startup essentially treats customer feedback as a form of lookup table for validated truth. In the uncertain environments which characterize most startup activity, however, there is no such table—and even if there were, the lookup table would only match current realities rather than the future ones that entrepreneurs are attempting to create.

Another problem with anchoring on bounded rationality in entrepreneurial decision-making—specifically in terms of the focus on human bias and error—is readily evident in a particular comment made by Blank and Eckhardt. They argue that “with appropriate training and discipline, agents can at best become boundedly rational decision agents” (Blank & Eckhardt, 2023, emphasis added). Lean startup essentially positions itself as a method for mitigating against human mistakes and errors by the entrepreneur (cf. Kahneman, 2011). Error-avoidance in decision-making is, of course, important, but by focusing on error-avoidance and bounded rationality—which provides the central logic for why lean startups should quickly validate ideas, products, and value offerings with customers—one is likely to only consider conservative options (including ones that can be more immediately validated), rather than options that go beyond the incremental. The very mechanism of pushing for early interaction with customers reinforces this conservatism. As a new lean startup tool to combat this tendency, the Market Opportunity Navigator invites a “more distant or global search for where to play” (Shepherd & Gruber, 2021: 971).

The emphasis of the theory-based view of startups is different from lean startup. This is not to say that lean startup is completely wrong, but simply to point out that there are substantive differences in what is prescribed to entrepreneurs. As we discuss below, the theory-based view argues that the most valuable forms of entrepreneurship emerge from contrarian beliefs and theories involving what-if forms of causal logic—logic that requires entrepreneurs and those evaluating what they propose, to essentially imagine an unseen state of the world, one in which a currently unsolved problem is solved. In many cases, rapid customer feedback is not the optimal place to start developing or testing such a theory. With such novel forms of entrepreneurship, the adage that “you cannot observe the counterfactual” has particular meaning. With these most valuable forms of entrepreneurship, you simply cannot observe the relevant facts or evidence, or even elicit them from customers or other stakeholders.

Theory-Based Startup: Different Foundations and Model Assumptions

The theory-based view of startups begins with different foundations and underlying assumptions from those of lean startup. The theory-based view of startups sees information, knowledge, and rationality through a very different lens. It sees humans—including economic actors like entrepreneurs—as generative agents rather than boundedly rational information processors, a critical distinction (Felin, Koenderink, & Krueger, 2017; also see Chater et al., 2018). Generative rationality means that rationality is not about asymmetric information processing—that is, the processing of data from customers, other stakeholders, or the environment—rather, rationality is highly proactive, shaped, and directed by the economic actor itself. The overly abstract notion of an environment, as traditionally understood in management, is not a meaningful construct within the theory-based view, nor is the idea of information asymmetry, as traditionally understood. Rather, the theory-based view emphasizes the role that beliefs, hypotheses, and theories play in directing awareness and attention toward highly specific, possible things in one’s surroundings (again, rather than the computation of information somehow received from the outside).

The central premise of the theory-based view is that humans do not strictly (or directly) learn from the environment. Rather, observation and learning are necessarily theory-laden. It is only when armed with a theory that something in the environment becomes salient and meaningful. Humans learn as their theories and hypotheses direct their perception, attention, and awareness toward specific things. Humans are endowed with a natural capacity for theorizing and hypothesizing about their surroundings, and it is this activity that is behind the emergence of novelty. Thus, entrepreneurs with different theories learn different things from the same environment (or customers, for that matter). Environments and environmental learning are therefore theory-specific. This mirrors the process of learning and knowledge acquisition in human development (Gopnik, Meltzoff, & Kuhl, 1999; Spelke, Breinlinger, Macomber, & Jacobson, 1992), evolutionary biology (Felin & Kauffman, 2023), as well as science (Popper, 1969). Environments “teem” with possible things that an agent might focus on and become aware of. But much of this remains latent, outside awareness (Felin & Koenderink, 2022). Things—any type of data or information—only become salient or visible in light of the hypotheses and theories that agents possess. This logic is aptly captured by Einstein who argued that “whether you can observe a thing or not depends on the theory which you use. It is the theory which decides what can be observed” (Polanyi, 1974: 64). This is the central starting point of the theory-based view.

This emphasis on theory might at first glance be seen as broadly consistent with lean startup. In fact, in the target article Blank and Eckhardt (2023) emphasize the importance of theory. Citing some of our recent work (specifically Felin, Gambardella, Stern, & Zenger, 2020), Blank and Eckhardt argue that “an element that scholars often overlook is that the lean startup is theory-driven and customer tested, as the theory of a potential business is developed before customer testing occurs” (2023: 7).

The emphasis on first developing a theory is welcomed by us. 2 However, while the emphasis on theory is welcome, we suggest there is work that remains in composing this integration. While perhaps an accidental oversight, the word “theory” or “hypothesis”—or any derivation of either word—is not even mentioned by Blank and Eckhardt in their table, which lists 24 different “key concepts and constructs” for lean startup (2023: 9-10). The authors certainly do discuss theories and theorizing in other parts of their article, but we think this omission from the summary of lean startup may simply highlight how hard it is to reconcile the idea of proactive theorizing with Blank and Eckhardt’s heavy emphasis on bounded rationality and a one-way information asymmetry between entrepreneurs and customers (and the need for the former to learn from the latter). If information asymmetry between entrepreneurs and customers is indeed the central problem—as they argue—then lean startup is logically consistent in placing its primary emphasis on reducing that asymmetry by “[favoring] rapid information gathering” (Blank & Eckhardt, 2023: 2).

The theory-based view does not make information asymmetry between entrepreneurs and customers (or other stakeholders)—or even the cognitive boundedness of entrepreneurs—its centerpiece. This is because relevant information is not necessarily held by customers (although it can be). Rather, the theories that entrepreneurs develop can be seen as having informational content themselves—thus, if anything, the asymmetry might in fact run in the other direction where startups need to educate customers rather than the other way around. Importantly, however, information and associated insights are theory-dependent. Put differently, theories encapsulate knowledge. Theories guide entrepreneurs to look for and observe specific things. The central assumption behind this approach is that all humans—including scientists and economic actors like entrepreneurs—engage in a quasi- or proto-scientific activity of hypothesizing and theorizing when engaging with their surroundings. Granted, just like in science, this process is not without its errors (Zellweger & Zenger, 2023). Critically, however, entrepreneurial theories might in fact go against existing data, information and even scientific (or customer) opinion and lead to—as pointed out by the Einstein quote above—the identification of novel data and information. Lean startup’s emphasis on “rapid information gathering” from customers (Blank & Eckhardt, 2023: 2) might lead to the premature invalidation of the most valuable theories.

To further contrast lean and the theory-based view of startups, while lean startup focuses on the asymmetry between entrepreneurs and customers in terms of information, the theory-based view focuses instead on heterogeneity and asymmetry in beliefs. Contrarian, discrepant or unique beliefs are the raw material of hypotheses and theories (Felin et al., 2021). Startups can be seen as a unique point of view, conjecture, or hypothesis about the future. Contrarian beliefs enable startups to see the world differently and to “hack” seemingly efficient, strategic factor markets (cf. Barney, 1986; Felin, Kauffman, & Zenger, 2023). Contrarian or divergent beliefs represent a point of view that by definition is not widely shared—which is the source of their value—and precisely because of their uniqueness, those holding such beliefs may find it hard to secure funding or other forms of intermediate validation (from customers or other stakeholders; Benner & Zenger, 2016).

One way that this idea of a startup-specific “point of view” manifests itself specifically is in how it sees the process of search. To offer a contrast, the aforementioned Market Opportunity Navigator—a tool that is part of lean startup—is a framework that enables startups to engage in “distant or global search.” The goal of distant or global search is to find and “identify a portfolio of market opportunities,” assess their “relative attractiveness” and to “choose the most promising option” (Shepherd & Gruber, 2021: 971-973; building on the work of McGrath & Macmillan, 2000). This form of general or global search—delineating options, comparing them, and choosing the best one—is certainly valuable and offers a plausible tool for startups to identify valuable opportunities. However, the theory-based approach to search is quite different. Search within the theory-based view is seen as a highly targeted process, where contrarian beliefs and theories provide startups with a “search image” that enables the recognition of value that is not evident to others (Felin et al., 2023). This might sound like a mere semantic distinction, but the distinction is in fact quite fundamental. Namely, with distant or global search there is a focus on information processing, that is, a focus on listing and amassing promising options or opportunities, comparing them, and choosing the best one (Shepherd & Gruber, 2021). The theory-based view, on the other hand, emphasizes that the salience or recognition of a valuable option is theory-dependent in the first place. Thus, the theory-based view does not focus on traditional forms of search (for example, on landscapes or other types of environments) but sees the process as a far more targeted one—a process of searching-for rather than searching-through. The distinction between global (or local-distant) versus theory-specific search has not only been discussed in the context of value creation (Felin et al., 2023), but it also has foundations in the cognitive sciences and research in the field of perception (see Chater et al., 2018).

Another reason that asymmetric, heterogeneous beliefs are emphasized by the theory-based view—over one-sided information asymmetry and bounded rationality—is because valuable beliefs may initially appear delusional to others—not just to customers, but also to other market actors or potential stakeholders, like investors. Beliefs that may turn out to be true (eventually), may go against existing data, evidence, and understandings, as is readily evident in the history of science. In fact, the more breakthrough or revolutionary the theory, the more likely it is to go against existing data and therefore lack access to immediate validation. To illustrate, Galileo had a contrarian and (at the time) unorthodox belief that the Earth orbited around the sun. The data, observations, and scientific consensus at the time were all against Galileo’s theory (Wootton, 2010). Existing scientific observations, data, and facts invalidated him. Therefore, he resorted to alternative sources of validation and evidence for his contrarian belief—new sources of data and experimentation illuminated by the theory. Eventually Galileo was proven correct. Startups similarly may possess contrarian beliefs and be in pursuit of realities that presently lack validation, data, and evidence. Startups of course are not providing validation or evidence for the laws of nature, but, rather, for the possible value of future products, strategies, and sources of value. This requires startups and firms to develop their own, underlying causal logic for “intervening” in the world and uniquely creating value (Felin & Zenger, 2017; cf. Heckman & Pinto, 2023; Pearl & Mackenzie, 2018).

If—as we suggest—customers (or even existing data) are not a reliable source of validation for a startup, then what is? The theory-based view recognizes any number of different mechanisms and intermediate sources of experimentation and validation for the realization of value. Notice that the mechanisms of validation advocated by lean startup—various forms of customer interaction and feedback—are but one of many ways for a startup to be more evidence-based and scientific. The choice of mechanism and scientific method depends on what a startup seeks to do and the type of theory the startup hopes to realize (Wuebker, Zenger, & Felin, 2023). The method of validation is theory-dependent. The theory-based view sees the realization of a contrarian belief about value as a process of problem formulation and problem solving. Intermediate “validation” (of a sort)—and the eventual realization of a value offering—here comes from searching for and finding a solution to a problem (Hsieh, Nickerson, & Zenger, 2007) or solutions to a structured set of subproblems (Felin et al., 2021) that, if collectively solved, solve the larger problem. That is, a startup’s contrarian or discrepant belief provides the impetus for carefully thinking about and formulating the set of assumptions that must be true, or the set of subproblems that must be solved in order to make a belief true. Once formulated, startups can then search for feasible solutions to these subproblems, or seek out evidence to validate assumptions. Failure to validate an assumption or solve a subproblem prompt early pivots—pivots that, when possible, preserve the remainder of the theory (Ehrig & Schmidt, 2022). Importantly, these early pivots can occur long before customer feedback on a complete solution is possible.

To offer a practical example of this process, consider Steve Jobs’s contrarian belief of the mid to late 1970s that computers would be a mass-market product—a belief that led Steve Jobs and Apple to engage in a process of problem formulation and problem solving. The contrarian belief was central for initiating the process of value creation. At this point in time, it was by no means obvious that personal computers would become a mass-market product, as existing applications of computing were focused on industrial and research settings or large-scale, specialized office applications. Even the first microcomputer, the Altair 8800, sold less than 10,000 units globally, which certainly did not suggest a basis for widespread consumer demand. The data at the time seemed to suggest that Jobs’s belief in the possibility of personal computers was wrong, if not delusional. Undeterred, Jobs’s contrarian belief led to the formulation of a theory and the articulation of central subproblems that stood in the way of solving the broader problem of rendering personal computers a mass consumer product. These subproblems included that computer use at the time required highly specialized skills, that computers were prohibitively expensive, that computer interfaces were hard if not impossible for lay people to interact with, that computers lacked aesthetic appeal and that the extant applications had no resonance with the average consumer. Once formulated, such problems enabled Jobs and Apple to search in a very direct way, to be guided toward and recognize subproblem solutions that enabled the development of a persuasive final product—the personal computer. 3 We suspect that an early effort to quickly roll out a clunky minimum viable product would merely have frustrated consumers and producers, rather than provide productive feedback.

We recognize that Blank and Eckhardt discuss various opportunities to advance and strengthen the lean startup approach—from its original conceptualizations—and specifically highlight the need to include “improvements to theorizing” (2023: 15-16). They argue that Osterwalder and Pigneur’s Business Model Canvas (BMC) “provides a way of building a complete, falsifiable theory of a business that helps the entrepreneur avoid omitting an activity essential to new business formation” (Blank & Eckhardt, 2023: 16). We concur that the BMC indeed features many important issues that a startup should consider: key partners, activities, resources, cost structure, value propositions, customer relationships, channels, revenue streams, and customer segments. As we discuss next, however, we see hypotheses and theories as something that originates from contrarian beliefs about how to solve problems, rather than an exercise in mapping business models across categories like key partners or cost structure. In our minds, the elements featured in BMC represent important downstream questions to consider once a contrarian view and theory of value has been articulated. Specifically, a theory enables the formulation of a problem and subproblems and guides the subsequent search for solutions to these problems. Many of the formulated problems can then in fact be addressed by considering BMC-related elements like key partners or resources—but it is the overall theory that enables the startup to recognize and see any of these possibilities (for example, in terms of how/which key partners might help or what particular resources might be needed).

Beyond theory, Blank and Eckhardt also recognize the importance of the construct of a problem and, particularly, what they call “problem testing.” However, problem testing, according to Blank and Eckhardt, “starts with ethnographic interviews” of customers and others that might have insights into various aspects of the BMC (2023: 7, emphasis added). From the perspective of the theory-based view, problems are not “tested” per se (although certainly some aspects might be). Rather, startups should first formulate a problem and relevant subproblems, compose a theory, and then engage in a process of solving subproblems by acquiring relevant resources, finding relevant technologies, or partnering with particular stakeholder or actors. We discuss the logic behind this argument next, and link it to the practical tool—called Value Lab—that originates from the theory-based view.

Practical Framework and Examples: Lean Versus Theory-Based Approach

Since both the theory-based view and lean startup are normative, it is important to delineate the “steps” and advice that each approach respectively offers for startups and entrepreneurs. In many ways, lean startup’s great virtue is that it has offered a set of practical tools for startups (Shepherd & Gruber, 2021). This research is in line with extant work that has sought to specify different types of “interventions,” treatments, and normative prescriptions that might enable startups and companies to be more effective in their decision-making (e.g., Chatterji et al., 2019; Heshmati & Csaszar, 2023; Kotha et al., 2023; Morris, Carlos, Kistruck, Lount, & Thomas, 2023). This work is in stark contrast to much academic research in entrepreneurship, which focuses on empirical description or theoretical abstraction, and therefore tends to be less accessible and useful to practitioners. The theory-based approach shares the desire to offer a normative framework for intervening in the world—even a pragmatic tool to help entrepreneurs be more effective (Felin et al., 2021). The theory-based view asks startups to envision how they might counterfactually “intervene” in the world—emphasizing causal analysis and causal inference (Frisch, 2013; Heckman & Pinto, 2023; Pearl & Mackenzie, 2018) 4 —and further asks startups to develop their own, unique, forward-looking “causal logic” for how to create value. The more general premise of the theory-based view is that theories inherently are (or should be) practical or pragmatic. Any intervention made by startups should be theory-guided. Thus, we strongly concur with Lewin who argued that “there is nothing so practical as a good theory” (1943: 118).

Value Lab as Practical Tool: Causal Logic for Theory Building and Testing

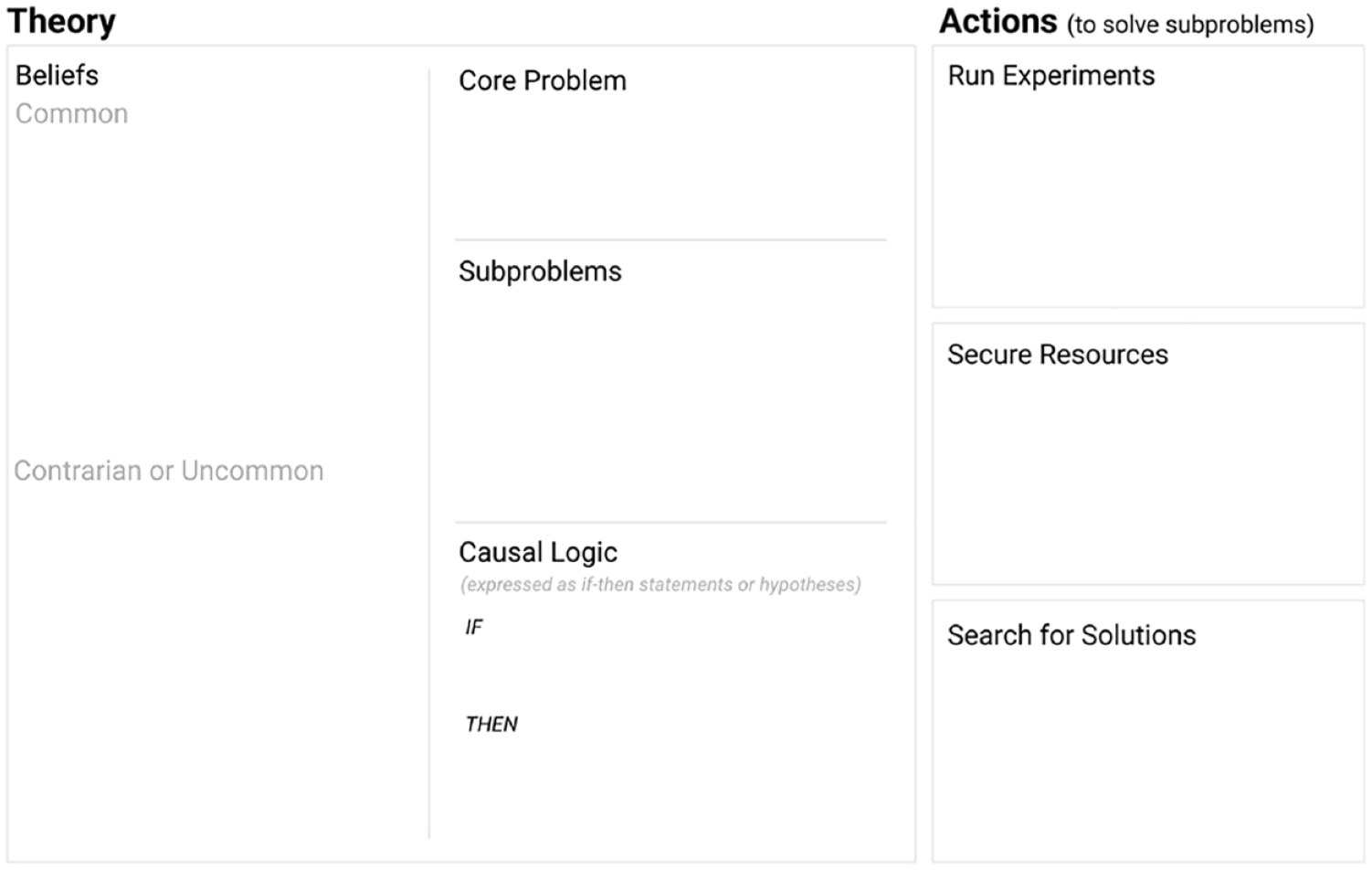

Blank and Eckhardt (2023) discuss and highlight some of the key practical frameworks of lean startup in their article, such as the Market Opportunity Navigator and Business Model Canvas. To offer a contrast to these frameworks, we discuss below a practical framework based on the theory-based view, called the Value Lab (see Figure 1, building on Felin et al., 2021). Contrasting the prescriptions of lean startup and the theory-based view is useful as it highlights what is practically emphasized and normatively suggested to entrepreneurs.

Value Lab

At a high level, Value Lab invites entrepreneurs and their collaborators to engage in three conversations to develop their theories and underlying causal logic for value creation. The first is a conversation about beliefs. Here entrepreneurs are pushed to articulate what they believe—specifically, what they believe that is in some form distinct, different, or contrarian from what others believe in relation to a space they seek to enter or a problem they seek to solve. Beliefs are the essential “raw material” of hypotheses and theories. The reason valuable beliefs need to be distinct, contrarian, or discrepant is because this enables startups to attend to potential sources of value that are not evident to others. Beliefs that are contrarian—somehow unique and different—enable entrepreneurs to “hack” competitive factor markets and create value (Barney, 1986; Felin et al., 2023). After all, value creation happens in a competitive context where obvious sources of value are likely to be competed away, thus placing a premium on unique and different ways of seeing the world.

As highlighted by Value Lab (see the first column), one way to elicit contrarian or heterogeneous beliefs is to first articulate the common beliefs or “orthodoxies” that others hold. These are deeply held beliefs or unquestioned assumptions about such things as customer taste or behavior, technology, or any number of other domains: supply chains or structure, governance, the evolution of markets, or future societal trends. Articulating the commonly held beliefs within an industry or market space can help entrepreneurs consider and sharpen what is truly unique or different about what they believe. To offer some brief examples, Steve Jobs famously held the unique belief that personal computers could become a mass market product; Howard Schultz believed coffee could be sold at a substantial premium; and, in the 1970s, the management of Luxottica—now the world’s largest eyewear conglomerate—believed eyewear could be transformed into a fashion item.

Of course, contrarian beliefs are just “talk” unless they lead to some form of practical problem solving and action. Therefore, the second conversation (see the second column of Figure 1) invites entrepreneurs to transform their unique beliefs into well framed problems that need to be solved (cf. Baer, Dirks, & Nickerson, 2013). Put differently, problems can be seen as the obstacles that stand in the way of realizing the contrarian or heterogeneous belief of the startup. Value creation in the theory-based view is fundamentally about finding, formulating, and solving problems (Nickerson & Zenger, 2004)—a process that is initiated by contrarian or heterogeneous beliefs (Felin et al., 2021). This enables the firm to develop a unique causal logic for how to create value. This involves formulating and solving problems unseen by others or solving widely recognized problems in new and novel ways. Again, this conversation involves more than restating a contrarian belief as a problem, but rather demands articulating the central obstacles that stand in the way of making a contrarian belief true.

An alternative framing asks, what must be true—or made to be true—for the entrepreneur to solve the central problem at hand. Often the factors that must be made true are a set of subproblems that need to be solved. To illustrate, Airbnb’s initial contrarian belief was that vacant rooms or apartments could be utilized as “hotel” accommodations—a belief that initially was seen as ludicrous (Felin & Zenger, 2017). The core problem for Airbnb was to broker safe, easy, and reliable access to the idle capacity found in privately owned housing. To solve this problem, the founders needed to address several key subproblems: develop an efficient and accessible matching mechanism (matching those seeking accommodation with those willing to offer it), facilitate secure payment, develop trust between complete strangers, and develop an efficient and effective vehicle for onboarding and listing properties that accurately signal the level of quality.

Notice that the process of assembling value is, more often than not, multistage, where different aspects of the theory are tested through different means. Put differently, composing value demands that different actions are used to solve different subproblems which collectively solve some larger problem. Thus, there is no one-size-fits-all approach to how a startup might solve problems or validate a particular solution. Rather, what the startup needs to do is theory-dependent (Wuebker et al., 2023). For example, Airbnb founders—as suggested by lean startup—in fact created what some might term a minimum viable product by renting out their own apartment (Gallagher, 2017). 5 Other aspects of their theory were addressed through different means, for example, by searching for subproblem solutions—like how to promote trust among strangers—which they solved by incorporating an eBay-like rating system. Thus, the eventual test of a theory, and the resulting product or service offering, emerges from different experiments, tests, and solutions linked to individual subproblems with the overall causal logic providing the glue that integrates across subproblems and assembles the actions and resulting value. To offer other examples: for Jobs and Apple, the core problem of generating a mass market personal computer required solving problems related to elegance, ease of use, and reliability; for Luxottica, launching eyeglasses as fashion items required developing a competence in fashion design, composing an ability to market eyeglasses in different countries, and developing a capacity to access and control their retail distribution (Camuffo, 2003). In all, in Column 2 of Value Lab (Figure 1), the aim is to structure the larger problem by articulating the set of subproblems that the entrepreneur believes must be solved to solve the larger problem. The problem and constellation of subproblems—and their overall causal structure—then becomes both the scaffolding around which a theory is built, and the guidance for actions to test various components of the theory.

The third conversation invites entrepreneurs to transform this articulation of an overarching problem with subsidiary subproblems into an expression of the firm’s theory of value. This expression seeks to capture the overall causal reasoning and structure of how value will be created—representing an exercise in causal logic (Pearl, 2009; Pearl & MacKenzie, 2018; also see Heckman & Pinto, 2023). The startup essentially is asked to think about how they might practically “intervene” in the world to create the conditions that enable the creation of the contrarian value that they foresee. Value Lab pushes the startup to create a logical causal diagram that goes from startup-specific beliefs to associated problems (and subproblems) and associated actions (including various forms of experimentation). As highlighted at the bottom of Column 2 in Figure 1, the overall logic of the theory can be summarized as a causal if-then statement that captures the overarching problem and subproblems. To illustrate, this might take the following form in the context of a company like Airbnb: “Airbnb believes that it can broker safe, reliable access to private hotel capacity, if it can generate trust between strangers renting and offering private hotel space, offer secure payment, and provide an effective vehicle for onboarding new properties while accurately signaling the quality of properties.” Clearly this expression is not necessarily a version crafted for public consumption, but it lays out what Airbnb believes it needs to make true to solve the problems it seeks to resolve, and thereby compose novel value.

The first two columns of Value Lab—focused on contrarian beliefs and problem solving (and establishing an underlying causal logic of the theory—offer the central foundations of the theory-based view and thus provide a useful contrast with lean startup. Economic value from the theory-based perspective originates from contrarian beliefs—and their pursuit along with associated problem framing and solving—while lean startup primarily emphasizes the rapid feedback from customers. In the third column of Value Lab, entrepreneurs are invited to consider alternative actions to take—actions that test, experiment, and explore solutions to the set of subproblems that must be resolved to solve the larger problem and generate the value that the entrepreneur foresees. This may involve conversations with customers, but also conversations with potential suppliers, resource providers, or other stakeholders (Wuebker et al., 2023). This process also involves identifying resources or technologies that need to be acquired for the hypothesized value to be created, where the theory guides startups to see and recognize solutions to the problems that have been formulated. As we discuss below, part of what the theory-based view of startups reveals is a way to accelerate learning about a theory even before obtaining customer feedback, by effectively matching entrepreneurial actions—including experiments—to the theories entrepreneurs propose. In all, the unique, startup-specific mix of actions (see Column 3 of Figure 1)—types of experiments, identification and securing of resources, and search for solutions—is guided by the cognitive work and theorizing that is done by addressing the previous two columns.

Discriminating Alignment Versus One-Size-Fits-All

The theory-based view of startups is a form of “meta”-theory that does not prescribe or emphasize any one way of validation, experimentation, team building, or governance. Rather, the theory-based view—and a tool like Value Lab—provides entrepreneurs with the scaffolding to come up with their own theory and startup-specific causal logic, and then to align or “match” the right activities and practices to validate and compose value with that theory (Wuebker et al., 2023). The theory-based view thus takes a page from transaction cost economics (Williamson, 1998) 6 and argues that entrepreneurial actions (including experiments) should be contingent on the type of theory and value that an entrepreneur envisions and explores. Our focus on contingency is broadly echoed by Zahra who argues that entrepreneurship research has “overlooked the importance of the contextual variables that stimulate, shape, and define the entrepreneurial act” (2008: 243). In our case, these contextual variables have to do with the heterogeneous beliefs and theories of startups and how different forms of experimentation, testing, and acting enable their realization and the creation of value.

By way of contrast, lean startup tends to push toward one-size-fits-all solutions, at the expense of a more contingent perspective. Lean startup’s strong emphasis on customer validation—due to information asymmetry between startup and customer—and the associated prescription of MVPs provides but one example (Blank & Eckhardt, 2023). Other examples can be highlighted. For example, lean startup argues that the idea that startups should engage in “stealth mode” has been made obsolete by the power of quick and transparent customer interaction. As put by Blank, “the lean startup methodology makes [stealth mode] obsolete because it holds that in most industries customer feedback matters more than secrecy and that constant feedback yields better results than cadenced unveilings” (2013: 6). We disagree. From a theory-based perspective, whether a startup should engage in secrecy or not—or any other practice (including the development of an MVP)—is dependent on the nature of the product or value offering that the startup is envisioning. Stealth and secrecy, in some situations, can be vitally important to the ultimate success of a startup, and therefore critical to maintain as a theory is explored and realized (Wuebker et al., 2023; also see Bryan, Ryall, & Schipper, 2022).

The prescriptions of the theory-based view—which experiments to conduct, or which actions to take—are contingent. To illustrate the contingent actions prescribed by the theory-based view, we might return to Value Lab (Figure 1). Specifically, the third column points toward various types of actions that a firm might take to validate, experiment with, execute, and realize various aspects of their theory of value. In other words, once a contrarian or discrepant belief has been developed (see Column 1) a problem (with subproblems) identified, and a theory composed, then startups can engage in a structured process of experimentation, resource identification, or acquisition, focused on solving the problem and subproblems. For example, a multitude of validation methods might be utilized in the realization of a given theory of value. The fashion eye glass firm Luxottica engaged in various forms of preliminary experimentation and actions—before interacting with customers—by observing the success of specific market players (essentially vicariously learning) and acquiring them (Camuffo et al., 2023a). The learning and activities of Luxottica were driven by the firm’s overall theory about “fashionable” glasses and the downstream problems—many of them related to vertical integration and different forms of licensing arrangements—which they needed to solve to create value from that theory.

The difference between a lean versus theory-based approach to startups is that the latter does not prescribe a primary method of validation, experimentation, or entrepreneurial action. This contrasts with lean startup. Lean startup argues that “while other methods of experimentation are not explicitly excluded, the primary methods of testing business theory in the lean startup” are focused on three ways of interacting with customers, namely: the “use of interviews with potential customers and experts, product testing with an MVP, and customer surveys (Blank & Eckhardt, 2023: 18, emphasis added). The primary methods for testing a theory from a theory-based perspective are more far-ranging and depend on the nature of the theory itself, specifically the subproblems that need to be solved, or the premises that need to be made true. From a theory-based perspective there is no primary method of experimentation, but rather a multitude of methods, including talking with potential suppliers, analyzing relevant technology, thought experimentation, persuading various stakeholders, searching for subproblem solutions (perhaps in other industries), and of course eventually obtaining customer feedback. From a theory-based perspective, the method of experimentation that is utilized depends on what the startup hopes to accomplish and the nature of the subproblems the startup needs to solve.

The problem is that rapidly developed customer-oriented MVPs only cover—and provide seeming validation for—a small and (often) incremental set of products that startups could feasibly create. In terms of creating significant value, startup products and value offerings are more likely to reflect theories involving multiplicative or combinatorial “packages” or bundles of features and unresolved subproblems that cannot meaningfully be validated by customers all at once upfront. The imagined end product often results from a “multi-step” process and overall causal structure that involves formulating problems and subproblems, then searching for solutions, engaging in experimentation, and acquiring the relevant solutions and resources. Some technology solutions might be readily incorporated off-the-shelf, while others require further development and integration. Some aspects of the product or value offering might be validated by a sequence of experiments, for example through A/B testing (aspects that lend themselves to comparing more desirable features: like what color a product should be) or some other form of interaction with customers or other stakeholders.

An entrepreneur’s theory guides the orchestration of an overall process of value creation, including the mix of activities and types of experiments that the startup should engage in. Thus, with many startup products and value offerings—particularly ones that are truly disruptive and not merely incremental—there is no immediate MVP or prototype that can be created to enable quick feedback or easy customer validation. In some cases, this might be possible—particularly for a specific aspect of a startup’s overall theory—but, in many cases, customers may in fact provide misleading signals rather than useful validation, particularly for products that they simply cannot (yet) imagine using.

All that said, lean startup’s emphasis on the need for startups to “learn” is certainly echoed from a theory-based perspective. However, the mechanisms of learning from a theory-based view include a larger menu of options. Rather than jumping by default to quickly develop and test an MVP (or a sequence of MVPs) and thereafter calibrating product market fit, here the learning exercise—as pointed to in the last column of Value Lab—typically involves testing assumptions, searching for subproblem solutions, and evaluating relevant technology or resources that might enable solving critical subproblems. In this sense initial experimentation, search, and learning is not about product market fit, but about determining whether a path to substantiating the contrarian belief—and a path to solving the corresponding problems—is feasible. Again, some aspects of the startup’s value offering might be tested with an MVP, amongst a host of other forms of experimentation, solution search, and resource acquisition.

The central point here is that startups need to appropriately “match” their actions with the type of theory they are pursuing, rather than relying on one-size-fits-all solutions. Here we might think of the entrepreneur as a Coasean (Coase, 1937) “entrepreneur-co-ordinator” who judges what activities to pursue and how and with whom to pursue them. The theory-based view similarly argues that these various activities and practices—whether to engage in them or not, and how—depend on the type of theory the entrepreneur is pursuing. In some instances, targeted feedback from (some) customers might indeed offer a valuable informational signal about a particular aspect of a prospective product or value offering. In other instances, however, customers might merely lead a startup astray. This type of discriminant nuance is essential. In all, the real power of generating a well formulated theory through a tool like Value Lab lies in accelerating the pace at which an entrepreneur learns about a theory’s value. A theory provides the roadmap for actions that accelerate learning. In this effort, the theory-based view is not wedded to any particular action or form of experimentation—like the need to focus on immediate customer validation. Of course, these approaches are not ruled out, but their use depends on the nature of the theory a startup is pursuing.

Pivots, Structured Theories, and Revised Beliefs

As emphasized by Blank and Eckhardt (2023), lean startup highlights not just learning from customers but also the need for startups to pivot. A pivot is broadly defined as a change in the direction, strategy, product or value offering of a startup or firm (also see Kirtley & O’Mahony, 2023, Burnell et al., 2023, and Leatherbee & Katila, 2020). Lean startup argues that if early and frequent interactions with customers do not offer validation for a particular product or strategy, then startups need to learn and change, that is, pivot toward something else. The central idea is that faster failure leads to faster pivots—a quicker shift to a more productive path. As put by Blank, startups “that ultimately succeed go quickly from failure to failure, all while adapting, iterating on, and improving their initial ideas as they continually learn from customers” (2013: 5, emphasis added).

From a theory-based perspective, learning, changing, and pivoting are also important; however, the central question for lean startup is, how should a startup decide what to pivot toward (or what aspect of the value offering to change, and how)? What does a startup learn from the process of interacting with customers? Might a startup have learned the wrong things from a particular customer interaction? Or, what should happen if a startup’s MVP does not receive validation from customers? When responding with a pivot, should the focus be on changes in the customer segment targeted, in the product attributes or mix, in the pricing, distribution, or perhaps the entire business model? Without a theory, a startup is left to the whims of customer feedback or aimless trial and error. From a theory-based perspective, any feedback is informed by a startup-specific theory, thereby providing greater precision for when and what to pivot toward. 7

A virtue of the theory-based view of startups is that it provides greater precision around what motivates (or should motivate) an entrepreneur’s decision to pivot, including an early pivot before a minimum viable product can even be composed. In the theory-based view, early pivots are motivated by an observation that a subproblem is unsolvable or a critical assumption is false. By contrast, lean startup focuses on pivots stemming from failure to achieve product market fit. While the theory-based view acknowledges this important source of pivots, the need to change a theory may become salient long before obtaining product market feedback, because, for example, the entrepreneur realizes that some of the subproblems are unsolvable or some of the assumptions are unsupported. In an important sense, a well composed theory permits even faster pivoting—pivoting in advance of obtaining market feedback on a product offering or a full MVP. Well-developed theories also enable more informed pivots—or, put differently, more informed revisions to beliefs. By exploring specific assumptions or seeking out solutions to critical subproblems, entrepreneurs examine the causal links or assumptions of their theories (Ehrig & Schmidt, 2022). This form of testing may occur in different ways for different aspects of a product or value offering. For example, Steve Jobs explored possible solutions to the subproblem of ease-of-use and eventually encountered the graphical user interface. Airbnb founders sought out solutions to elevating trust between strangers or arranging for secure payments, and found a useful approach in how eBay and other companies had dealt with similar problems. Luxottica explored different solutions for getting control of the retail network. The identification of these solutions—that is, what made these solutions salient to the entrepreneurs—was only possible given the initial contrarian belief and the formulation of a core problem which motivated the search for these solutions.

In a valuable extension of the theory-based view, Ehrig and Schmidt (2022) argue that entrepreneurs should order their assumptions—those things that must be true or must be made true— based on strength, and then test the weakest premise. When premises or assumptions are unsupported, entrepreneurs must revise their beliefs, ideally by replacing the unsupported assumption with an alternative that preserves the remainder of the causal theory. Only when an alternative cannot be found does the entrepreneur abandon a theory and take up a major pivot.

Within the framework of Value Lab, we view premises and assumptions as frequently taking the form of subproblems to be solved, and thereby made true. For instance, Airbnb’s theory is only as strong as its weakest premise—that is, its ability to solve its most intractable subproblem. In other words, the theory falls apart if Airbnb cannot find a mechanism to build trust among strangers who seek to offer or rent private hotel space. Airbnb’s theory hypothesizes a path to solving this subproblem. But if the hypothesized approach fails, Airbnb must either find an alternative way to resolve it (a sub-pivot of sorts) and thereby make this assumption true, or Airbnb must revise the theory, finding a new premise or set of premises that will support the overarching conjecture (Ehrig & Schmidt, 2022). As outlined in Value Lab, experiments, data gathering, and resource search all focus on solving subproblems, in support of validating a theory, or facilitating its revision.

Camuffo et al. (2023a) and Camuffo, Gambardella, and Pignataro (2023b) provide a closely related framing. They argue that entrepreneurship necessarily involves making “low-frequency high-impact” decisions—decisions that, because they are rare, cannot rely on past data to guide choice. They argue that theory formation begins with problem framing that includes defining relevant attributes and the relationships that connect them. For example, Luxottica realized that it could move into fashion eyewear from its standard business of eyewear solutions for vision correction. The theory of the standard business was to focus on lowering costs, which lowered prices, raised demand, and generated economies of scale—thereby generating a virtuous cycle of low costs, low prices, and high demand. Since the product was standard, relations with customers could be delegated to carefully managed retail stores. However, the idea of transforming eyewear into a fashion item reflected a new theory. From a potentially wide array of alternative framings about how to create this transformation, Luxottica focused on initiating alliances with fashion brand companies. The theory was that Luxottica could leverage the competence and brand of these companies rather than compose their own capability. The theory was that these fashion brands could apply their craft to a new domain—eyewear—and create truly original styles. In turn, this implied that Luxottica had to develop direct relations with customers, and this would thus demand integrating forward into retail. Luxottica tested this theory by monitoring small companies in the fashion glass business and by striking an early alliance with Armani. These experiments corroborated that there was a potential demand and mass appeal for higher-end eyewear that was fashionable, and that by building on the style and market of Armani, it could generate demand for Luxottica’s new products.

Overall, the theory-based view provides a distinctly different approach to learning—one less reliant on customer feedback and simple product market fit. The theory-based view is informed by experiments that test assumptions and search for subproblem solutions. Through this process, startups revise their beliefs as they learn—guided in the varied actions they take to facilitate learning by a startup-specific theory that points toward testing assumptions, searching for solutions to problems that have been formulated, or discovering critical resources.

Corroborating Evidence and Empirical Research Opportunities

The real validation for any normative theory is whether it works. Specifically, does a particular “treatment”—the advice or set of steps suggested by the theory or approach—actually enable startups to create more value, to engage in better pivots, and lead to better performance outcomes? Thus, next we briefly report on the current and ongoing empirical findings related to the theory-based view of startups, including one study that also directly compares lean startup with the theory-based view.

In a randomized control trial (RCT), Camuffo et al. (2020) randomly allocated 116 Italian startups to a treatment and a control group. Both groups underwent business-related training (eight sessions, every other week). The treatment group was trained to think scientifically by asking entrepreneurs to formulate theories and test them. (Note that this study followed the broad contours suggested by Value Lab, although the study was done prior to the full articulation of the framework.) By contrast, the control group was introduced to standard entrepreneurial tools and logic, such as external market analysis. This same design—with the same treatment and control groups—was replicated with additional RCTs totaling 759 randomly allocated startups (Camuffo, Gambardella, Messinese, Novelli, Paolucci, & Spina, 2024).

These initial RCTs produced three main findings. First, treated startups were more likely to terminate the pursuit of their entrepreneurial idea and were more likely to terminate them earlier. This termination result is intriguing. Treated entrepreneurs recognized earlier, and to a greater extent, that their ideas were in fact not valuable. This saves entrepreneurs—as well as investors and other stakeholders—precious resources and time. Anecdotal evidence from the startups in the training program corroborates this conjecture. Treated entrepreneurs recognized, based on good logical reasoning, why their ideas were not worth pursuing, and they recognized it earlier. Second, treated entrepreneurs pivoted once or twice, whereas entrepreneurs in the control condition did not pivot at all or pivoted many times. This pivoting result is consistent with the idea that when entrepreneurs see that their idea does not work, they know where to pivot, in line with the idea that theory-based entrepreneurs make more informed revisions to their beliefs. Conversely, entrepreneurs in the control group were more inclined not to change their idea, or to pivot rather “indefinitely,” in an aimless search for an alternative path to creating value. Without an underlying logic—or theory—that explains why their idea is not successful, they do not see how to remedy it by pivoting to a revised, better theory. Third, and finally, treated entrepreneurs obtained larger revenues and performed better, conditional on remaining active. This is consistent with the idea that a tighter theoretical focus can support a superior ability to discard false positives, and that more informed pivots improve performance results.

Further corroboration has come from the work of Novelli and Spina (2022). Their study included both new firms as well as more established, small organizations (with less than 10 employees) in a randomized control trial. Firms in the treatment group were encouraged to develop a theory with hypotheses that solved a problem. The control group, on the other hand, was simply exposed to generic strategy frameworks and testing techniques. Treated firms grew more quickly (in terms of revenue) than the control group, but the effect was more pronounced for more established small firms relative to newer startups. Qualitative evidence suggested that the treated group better understood when some of their beliefs were unsupported or that some of the problems (or subproblems) could not be solved, and therefore necessitated a pivot. While not a direct comparison of normative guidance from the theory-based view versus lean startup, the findings are nonetheless consistent with the importance of firm-specific theories when exploring and realizing new and contrarian ideas.

Finally, Agarwal et al. (2023) adopt a more elaborate research design that aims to explore the impact of a theory-guided approach versus a purely evidence-based approach, more consistent with lean startup. They studied 150 Tanzanian entrepreneurs randomly allocated to two training programs (six sessions, every other week). In one training program entrepreneurs were trained to formulate theories about their business based on causal links (identifying causes and effects) and test them via hypothesis development. In the other training program entrepreneurs were trained to find evidence for hypotheses, focusing on creating a minimum viable product and receiving feedback from customers. This study thus offers a relatively direct test—though preliminary—of the theory-based approach versus lean startup. The entrepreneurial firms treated with the theory-based approach attained significantly higher performance metrics, including higher revenues and higher profits, compared to the firms in the control condition which received the lean startup treatment (which was included in the control condition). The RCT also found that when the theory-guided entrepreneurs choose to pivot, they change more elements at the same time. That is, they adopt a more holistic approach to the business reflecting a broader, theory-informed perspective of what they need to do and test, and what they should aim at (and pivot toward). Entrepreneurs in the purely evidence-based training only changed single elements.

Most of the empirical work within the domain of “entrepreneur as scientist” is relatively recent. Some of the above RCTs offer early evidence that teaching entrepreneurs to be theory- and science-based improves performance outcomes (above and beyond basic business training) and leads to better performance as well as more informed experimentation and more focused pivots (Camuffo et al., 2021). However, Lean startup has of course also received empirical support from RCTs (Kotha et al., 2023). Our hope is that the varied approaches that focus on introducing the scientific method to startups can be studied comparatively, side-by-side, to understand the respective virtues and limitations of each approach.

Various entrepreneurial frameworks—such as the theory-based view, lean startup, effectuation, and discovery-creation—can each offer and put forward their respective treatments and methods for comparison. Various RCTs and empirical studies have suggested different types of treatments for startups, highlighting how interventions such as formal advice from peers (e.g., Chatterji et al., 2019) and specific types of business training (Kotha et al., 2023; also see Santamaria, Abolfathi, & Mahmood, 2023) can improve decision making and startup performance. While different forms of intervention are feasible, we argue that a theory-based approach to these interventions—that is, training startups to develop their own theory of value—will yield the best results. This of course is an empirical question, and thus further work is needed to corroborate this claim. More generally, we hope that future work can design and run explicit “horse races” between the varied proposed treatments and methods—like the theory-based view and lean startup (among others)—to discover their relative virtues and comparative implications for startup performance and value creation. Since intervention-oriented work (like RCTs) are a relatively new method within the domain of entrepreneurship and strategy, these types of comparisons have yet to be performed, although this certainly offers an important direction for future work.

In comparing different theories of startups and entrepreneurship, it is important to recognize the issue of contingency. That is, it might be that the value of different prescriptions and normative interventions is a function of the types of settings, types of outcomes, and types of startups that a given theory is focused on. Lean startup’s focus on customers certainly lends itself to value creation in settings where rapid learning from customers makes sense; but, in other situations—for example, where products are more complex or require substantial investment—customer feedback might not be as effective as other forms of validation. Thus, we see a need to develop contingent arguments that outline different theory types or forms of value creation, in order to explore which are best matched with varied types of validation, experimentation, and forms of governance (Wuebker et al., 2023). Importantly, comparative work like this can begin to establish the respective boundaries and contingencies of various approaches to entrepreneurship, delineating when and why certain approaches work. This type of research would offer extremely valuable insights and inform what is taught at universities, various training programs, accelerators, and incubators across the world. Furthermore, it would enable scholars to establish the boundary conditions of each approach, and enable the development of a more nuanced, contingent approach to entrepreneurship.

Before concluding, we offer some conciliatory, integrative thoughts. While we have highlighted a number of differences between lean startup and the theory-based view, there is certainly room for a heterogeneity of approaches when it comes to understanding something as complex as startups, strategy, and value creation. After all, a theory, by definition, cannot explain everything. Like maps, theories and models aim to provide focused representations of complex phenomena, rather than fully mirroring reality. Each theory provides a map of what it sees as important—simplifying and distilling key patterns rather than incorporating every detail. Different camps and schools of thought—within the domain of entrepreneurship and strategy—make different things salient, each offering a unique “lens” that focuses awareness and attention on certain phenomena. This is why we think there is power in moving toward a “contingent” approach with regard to a more scientific approach to startups, where contingencies and boundaries of different tools and approaches are recognized and appropriately utilized.

Conclusion

In this paper, we contrast the theory-based view with lean startup, in an effort to point toward a “scientific method” for entrepreneurship. We laud lean startup for its normative engagement with entrepreneurial practice and its call for a more scientific approach to startup activity. The theory-based view shares this agenda. However, while both approaches argue for a scientific approach to venture creation, they diverge in their underlying mechanisms and practical guidelines. In this paper we question the strong emphasis that lean startup—as outlined by Blank and Eckhardt (2023)—places on the information asymmetry between entrepreneurs and customers, bounded rationality, and the associated emphasis on customer validation (through MVPs and rapid, frequent feedback from customers). While customer feedback can be important in some situations, we highlight how it is far from a panacea. By way of contrast, the theory-based view emphasizes the role that contrarian or heterogeneous beliefs and theories play in shaping startup-specific experimentation, resource acquisition, and problem solving. We emphasize the need for discriminating alignment when it comes to entrepreneurial action, where one-size-fits-all tools yield to a recognition of the importance of contingently matching different activities, forms of experimentation, and practices with what entrepreneurs seek to accomplish. Our hope is that further theoretical and empirical work on the respective similarities and differences across different approaches to entrepreneurship will enable scholars to develop normative models that help startups improve their decision-making and performance outcomes.

Footnotes

Acknowledgements

Alfonso Gambardella acknowledges financial support from the Italian Ministry for Education, project: “Entrepreneurs As Scientists: When and How Start-ups Benefit from A Scientific Approach to Decision Making,” call PRIN 2017, Prot. 2017PM7R52, CUP J44I20000220001. Teppo Felin and Elena Novelli acknowledge financial support from the UK Department of Business Energy and Industrial Strategy - Innovate UK, project: 104754, “A Scientific Approach to SMEs Productivity”.